Rod Cameron - Hicksons - Mortgage enforcement

45

This address represents a brief summary of the law relating to the issues raised and should not be relied on as a substitute for professional advice. Specific legal advice should always be sought in relation to any particular circumstances and no liability will be accepted for any losses incurred as a result of reliance on this address. © Hicksons 2014 Mortgage Enforcement 3 October 2014 Address by Rod Cameron

-

Upload

informa-australia -

Category

Business

-

view

778 -

download

4

Transcript of Rod Cameron - Hicksons - Mortgage enforcement

This address represents a brief summary of the law relating to the issues raised and should not be relied on as a substitute for professional

advice. Specific legal advice should always be sought in relation to any particular circumstances and no liability will be accepted for any

losses incurred as a result of reliance on this address. © Hicksons 2014

Mortgage Enforcement

3 October 2014

Address by Rod Cameron

© Hicksons 2014

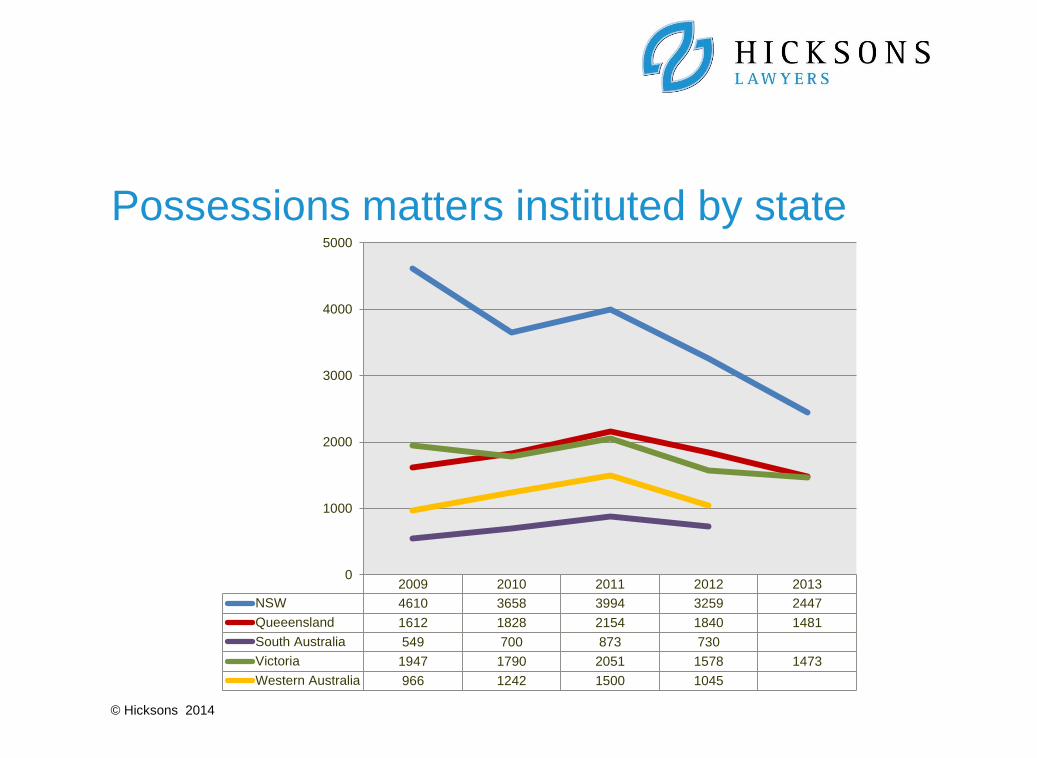

2009 2010 2011 2012 2013

NSW 4610 3658 3994 3259 2447

Queeensland 1612 1828 2154 1840 1481

South Australia 549 700 873 730

Victoria 1947 1790 2051 1578 1473

Western Australia 966 1242 1500 1045

0

1000

2000

3000

4000

5000

Possessions matters instituted by state

© Hicksons 2014 Slide 3

Overview

• Unjust contract defences

• Enforcement of securities

• Proportionate liability

© Hicksons 2014 Slide 4

Unjust contract defences• Contracts Review Act 1980 (NSW) s7

Where contract unjust at the time it was made, the Court may, if it considers it just:

• refuse to enforce any or all of the contract

• declare the contract void, in whole or in part

• vary the contract in whole or in part and/or vary or terminate a land instrument

• National Credit Code s76

Where credit contract unjust at the time it was entered into or changed, the Court

may reopen the credit contract and:

• reduce the amount payable by the borrower

• set aside or vary the credit contract

• order discharge of any mortgage

• make orders for the benefit of the parties

• make ancillary or consequential orders

© Hicksons 2014 Slide 5

Unjust contract claims (continued)

• Borrowers can seek to avoid or vary loan contracts and mortgages

alleging that the contract was unjust

• Frequently such cases involve allegations that the borrower has been

conned into the loan contract by a spouse, son, daughter, in-law or

close friend

© Hicksons 2014 Slide 6

First Mortgage Management v Pittman [2012] NSWSC 1332, Garling J, 1 November 2012

• Borrowers were 2 elderly brothers, uneducated, unsophisticated, living a

subsistence lifestyle

• Margot Locke was a neighbour and property developer – befriended the

borrowers – described by court as manipulative, greedy, exploiter of the

vulnerable and thoroughly discreditable

• Locke convinced borrowers to borrow money secured by mortgages

over their properties for her development projects

• Locke dealt with lender and arranged for her solicitor to provide

‘independent’ legal advice to borrowers to meet lending requirements

© Hicksons 2014 Slide 7

First Mortgage Management v Pittman (continued)

History of borrowers’ loans for Locke

• Early 1994 borrowed $172,000 from National Mutual – repaid March

1995 - no financial benefit to borrowers

• October 1994 borrowed $910,000 from Forrest Knoll – by 1997 amount

had increased to $1,650,000 – repaid November 1998

• November 1998 borrowed $660,000 from Flamanda – repaid from First

Mortgage loan

• March 2006 borrowed $500,000 from Morandon - repaid from First

Mortgage loan

• December 2006 borrowed $1,900,000 from First Mortgage

• February 2008 borrowed further $125,000 from First Mortgage

© Hicksons 2014 Slide 8

First Mortgage Management v Pittman (continued)

• Garling J concluded the First Mortgage loan contracts were unjust

for the following reasons:

• material inequality in bargaining power between lender and

borrowers

• no negotiation about terms – presented by Locke as ‘fait accompli’

• no reasonable opportunity for borrowers to negotiate or reject

terms, given documents sent to lawyers nominated by Locke

• neither borrower able to reasonably protect his own interests

• lender’s superior and dominant position not rectified by legal advice

because it was not of substance and was not independent of Locke

• borrowers’ legal advice did not meet and could not have met

lender’s requirements of independence

© Hicksons 2014 Slide 9

First Mortgage Management v Pittman (continued)

• borrowers’ legal advice did not explain the terms and their legal and

practical effect

• loan structure – LVR and interest rates meant all equity likely to be

quickly consumed by interest

• reliance on development proceeds problematic because no legal

obligation on Locke to make any repayment and lender made no

enquiries regarding its nature and extent

• lender failed to comply with lending manual

• borrowers received no direct financial benefit

• Garling J set aside the mortgage and dismissed the borrowers’ claim

against Locke as, with the mortgage set aside, the borrowers had

suffered no loss

© Hicksons 2014 Slide 10

First Mortgage Management v Pittman [2014] NSWCA 110, Beazley P, Gleeson JA, Sackville AJA, 7 April 2014

and 19 August 2014

• Relief must be for the purpose of avoiding an unjust consequence or

result – relief should not provide an unwarranted benefit

• From $2,030,000 advanced by First Mortgage $512,500 was applied to

discharge Moranon Mortgage and $660,000 was applied to discharge

Flamanda Mortgage

• Garling J mistakenly thought Flamanda Mortgage was the only loan

refinanced – he held that mortgage unjust but didn’t address:

• whether there was an unjust consequence or result from the

Flamanda Mortgage

• whether the Moranon Mortgage was unjust

© Hicksons 2014 Slide 11

First Mortgage Management v Pittman Appeal (continued)

• Court of Appeal held:

• borrowers failed to prove that they had not benefited by the

discharge of the Moranon Mortgage and the Flamanda Mortgage

• orders setting aside mortgages should be overturned

• amount due under mortgages set at amounts from loan used to

refinance the Moranon Mortgage and the Flamanda Mortgage

• As a result of appeal lender’s position improved by $1,172,500

• Borrowers granted late leave to cross appeal against Locke and matter

remitted to Garling J to determine claim against her

© Hicksons 2014 Slide 12

RHG v Baira, RHG v Ianni[2014] NSWSC 849, Davies J, 1 July 2014

• 1992 Baira gave a guarantee supported by a mortgage over her home

to support business borrowings of daughter and son-in-law

• 2000 Iannis gave a guarantee supported by a mortgage over their home

to support investment borrowings of son and daughter-in-law

• 2005 Iannis borrowed $910,000 from RHG to refinance the Iannis

Guarantee loan and release equity – solely for benefit of son and

daughter-in-law

• 2006 Baira borrowed $650,000 from RHG to refinance the Baira

Guarantee loan – solely for benefit of daughter and son-in-law

© Hicksons 2014 Slide 13

RHG v Baira, RHG v Ianni (continued)

• Court determined guarantee and mortgage were unjust noting:

• even though Baira and the Iannis were unsatisfactory witnesses

they were never told they were changing from guarantors to

borrowers

• the transactions converted Baira and the Iannis from

guarantors/mortgagors with only contingent liability limited to the

value of their homes, to borrowers/mortgagors with no limit on

liability and without a right of recourse against the children or their

properties

© Hicksons 2014 Slide 14

RHG v Baira, RHG v Ianni (continued)

• Even though the broker was held to not be the agent of RHG:

• RHG had notice of aspects of the loan application indicating

unjustness or at least putting RHG on notice that it might be taking

advantage of the special disability and disadvantage of Baira and

the Iannis

• if RHG had followed its own guidelines and done other things that

might be expected of RHG then RHG would have ascertained the

unjustness

© Hicksons 2014

PTVL v Belcastro (No 2)[2013] NSWSC 1189, Adams J, 30 August 2013

• Husband and wife borrowed funds by low doc loan to support fencing

business they had bought into

• Repayments made from 2003 to 2008

• Borrower wife defended claim for possession alleging loan and

mortgage contract were unjust

© Hicksons 2014 Slide 16

PTVL v Belcastro (No 2) (continued)

• Court determined loan and mortgage were not unjust noting:

• public interest had to be taken into account – keeping people to

their bargains

• public interest also required protecting the vulnerable and

promoting suitable lending systems

• borrowers in this case knew the nature of the transaction

• borrowers in best position to assess viability of business

• no imbalance of power other than usual lender/borrower

• no indication necessity to resort to security was inevitable

• lender not bound to carry out detailed investigation of borrowers’

ability to carry through plan for repayment

© Hicksons 2014

ANZ v Londish[2014] NSWSC 202, Adamson J, 12 March 2014

• Mrs Londish was wealthy by inherintance and the sole owner of the

family home

• Mr Londish managed investment properties owned by companies,

owned by Mr and Mrs Londish

• Mrs Londish was well educated and articulate but did not have detailed

knowledge of or involvement in the management of the companies or

the property investments

• In 2003 Mr Londish sought to purchase three units in Walsh Bay – after

being unable to obtain finance, a loan to Mrs Londish was obtained from

Challenger using the home as security

© Hicksons 2014 Slide 18

ANZ v Londish (continued)

• In 2009 the Challenger Mortgage was refinanced by a loan from ANZ

which was again secured by mortgage over the home

• In 2011 the companies and property investments became unprofitable

and there was default in respect of the ANZ loan

• ANZ took action seeking possession of the home

• Mrs Londish contended that the Challenger Mortgage was unjust and

should to be set aside and that the ANZ Mortgage which refinanced the

Challenger Mortgage should also be set aside

© Hicksons 2014 Slide 19

ANZ v Londish (continued)

• The Court held that neither the Challenger Mortgage nor the ANZ

Mortgage was unjust and entered judgment for possession of the home

and for debt

• The Court particularly noted:

• consideration of public interest required consideration of community

standards and business morality:

• both transactions were commercially prudent

• Challenger required proof of financial and legal advice to Mrs

Londish

• ANZ had no reason to believe that the refinance was other

than commercially beneficial to Mrs Londish and her family

© Hicksons 2014 Slide 20

ANZ v Londish (continued)

• it would be antithetical to public interest for a party to a loan

and mortgage, made for sound commercial reasons, to be

relieved of its provisions when it transpired that the ultimate

enterprise funded by the contract was not viable, for reasons

extraneous to the loan

• there was no material inequality between Challenger and Mrs

Londish, particularly when Mr Londish negotiated on behalf of Mrs

Londish

• Mrs Londish was neither aged nor suffering from any physical or

mental incapacity

• Mrs Londish was articulate, intelligent, and well educated

• Mrs Londish was given legal advice about the Challenger Mortgage

© Hicksons 2014 Slide 21

ANZ v Londish (continued)

• Mrs Londish may not have been given financial advice about the

Challenger Mortgage however it was probable that Mr Londish

informed Mrs Londish of the relevant financial circumstances

• Mr Londish may have exerted pressure on Mrs Londish to grant the

Challenger Mortgage however any such pressure was not ‘undue’ –

Mrs Londish knew the risks and knew the family income was

substantial – her decision to grant the Challenger Mortgage was

the result of careful consideration of what could be gained in

commercial terms and the limited risks

© Hicksons 2014 Slide 22

ANZ v Londish (continued)

• the relative power between Mrs Londish and ANZ should be

measured by reference by the power of Mr Londish and the

companies

• there was negotiation between Mr Londish and ANZ at least in

respect of the interest rate

• it was appropriate that Mrs Londish be the sole borrower given that

she was the sole registered proprietor of the home which was the

security for the loan

© Hicksons 2014 Slide 23

ANZ v Londish (continued)

• even though Mrs Londish did not receive independent legal or

financial advice before executing the ANZ Mortgage she

understood the nature and meaning of a mortgage, financial advice

at the time would have indicated no significant financial problems

and Mrs Londish appreciated that the interest rate would be lower

and the additional funds would enable the investment properties to

be improved

• ANZ did not meet with Mrs Londish to make sure she understood

the transaction however she did understand the transaction and

was prepared to enter into it

• there was no evidence of any unfair tactics or pressure having

been applied by Mr Londish to Mrs Londish

© Hicksons 2014 Slide 24

Enforcement of securities• Legislative developments

• Recent cases

© Hicksons 2014 Slide 25

Personal Properties Securities Act (PPSA)

legislative developments• Transitional provisions had the effect that a pre PPSA security interest had

two years protection to enable registration – the transitional protection

period expired on 31 January 2014 – a pre 31 January 2012 security

interest can still be registered however it will now rank behind any prior

registered security interest or any administrator or liquidator appointment

• From 1 July 2014 the definition of ‘motor vehicle’ has been slightly narrowed

(previously capable of at least 10km/h or has motor(s) greater than 200

watts, now capable of speed of at least 10km/h and has motor(s) greater

than 200 watts) – intended to reduce PPSA costs for small to medium sized

hire businesses by reducing the number of equipment leases involving

PPSR serial number lease registrations

© Hicksons 2014 Slide 26

Personal Properties Securities Act (PPSA) legislative developments

(continued)

• Currently leases of serial numbered goods longer than 90 days are PPS

Leases and therefore must be individually registered to protect the lessor’s

interest in those goods

• If passed the Personal Properties Securities Amendment (Deregulatory

Measures) Bill 2014 will mean that leases of serial numbered goods for less

than 12 months (rather than 90 days) will not fall within the definition of a

PPS Lease

• The effect of the change will be that leases of serial numbered goods

between 90 days and 12 months will no longer have to be registered as

individual PPS Leases

© Hicksons 2014 Slide 27

Central Cleaning Supplies (Aust) v

Elkerton[2014] VSC 61, Ferguson J, 7 March 2014

• September 2009 Swan signed a Central Cleaning Credit Application

which included provision and supply of goods would be governed by

Central Cleaning’s Standard Terms and Conditions

• November 2012 to May 2013 Central Cleaning supplied goods and

issued invoices which included a retention of title clause

• Central Cleaning did not register the security interests created by the

retention of title clause

• May 2013 Swan went into administration and subsequently went into

liquidation

© Hicksons 2014 Slide 28

Central Cleaning Supplies (Aust) v Elkerton (continued)

• Central Cleaning claimed return of the goods supplied which had not

been paid for

• Central Cleaning claimed it had a transitional security interest under the

Credit Application

• Court held the retention of title was contained in each invoice and did

not form part of the Standard Terms and Condition and was therefore

not incorporated in the Credit Application

• Each invoice after 30 January 2012 was not a transitional security

agreement – therefore Central Cleaning’s interest under each of those

retention of title clauses was not temporarily perfected as a transitional

security interest

© Hicksons 2014 Slide 29

APR Energy & Forge Group Limited

recent news

• It has been reported that APR leased to Forge four gas turbines worth

about $50m

• It appears that APR did not register the assets on the PPSR

• Forge went into administration - KordaMentha were appointed receivers

• KordaMentha are asserting that the gas turbines vested in Forge and

that APR’s interest in the gas turbines has been lost because the PPS

Leases were not registered before the administration

• If this is correct, failure to register the APR’s PPS Lease interest

(registration fee $16) may result in APR loosing its interest in $50m

assets

© Hicksons 2014 Slide 30

Proportionate liability – lessons for

pleading recovery claims

• Proportionate liability is usually not relevant to a lender claim against a

borrower – such a claim is usually not an apportionable claim because it

is not a claim for loss arising from a failure to take reasonable care but

is rather a claim for debt

• Proportionate liability however is frequently relevant to a lender claim

against a third party such as a broker, valuer, solicitors or real estate

agent – such a claim will usually be a claim for loss arising from failure

to take reasonable care whether under contract or tort and therefore be

an apportionable claim

• In a lender claim against a third party the borrower could be a

concurrent wrongdoer if the borrower had liability to lender independent

of the debt – eg for misrepresentation – see Kayteal Pty Limited v

Dignan [2011] NSWSC 197

© Hicksons 2014 Slide 31

Proportionate liability risk for lenders

• If:

• there are multiple concurrent wrongdoers; and

• one or more of those multiple concurrent wrongdoers is

impecunious and uninsured; then

the ability of a lender to recover loss on a loan may be restricted

© Hicksons 2014 Slide 32

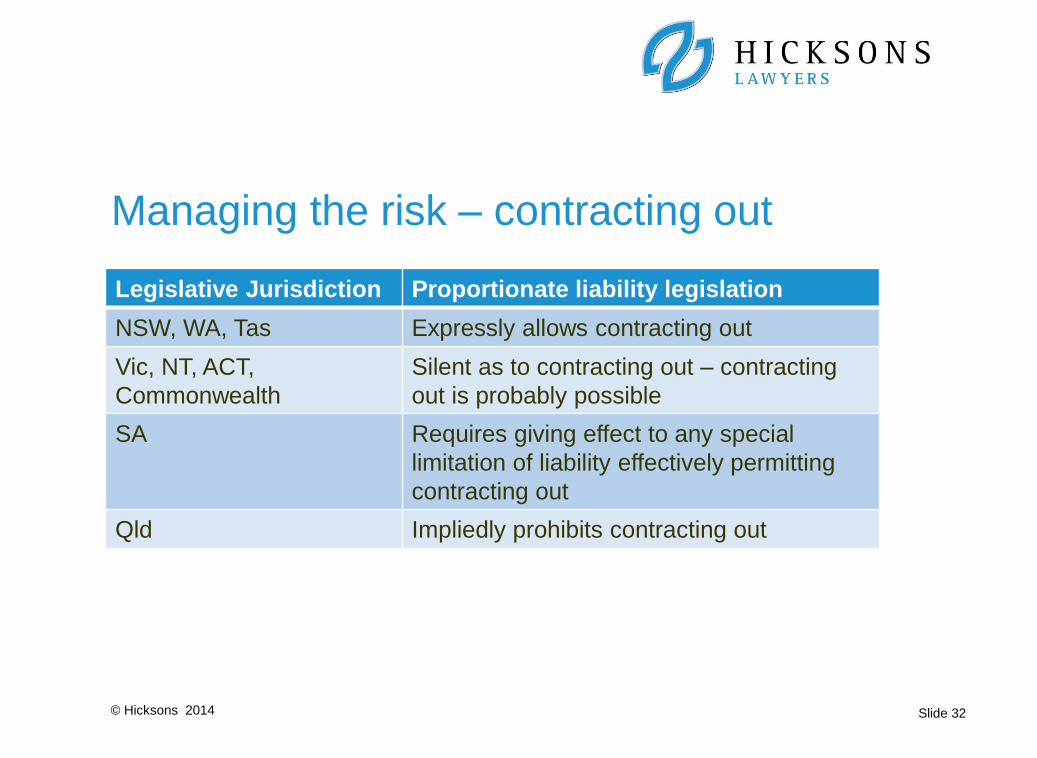

Managing the risk – contracting out

Legislative Jurisdiction Proportionate liability legislation

NSW, WA, Tas Expressly allows contracting out

Vic, NT, ACT,

Commonwealth

Silent as to contracting out – contracting

out is probably possible

SA Requires giving effect to any special

limitation of liability effectively permitting

contracting out

Qld Impliedly prohibits contracting out

© Hicksons 2014 Slide 33

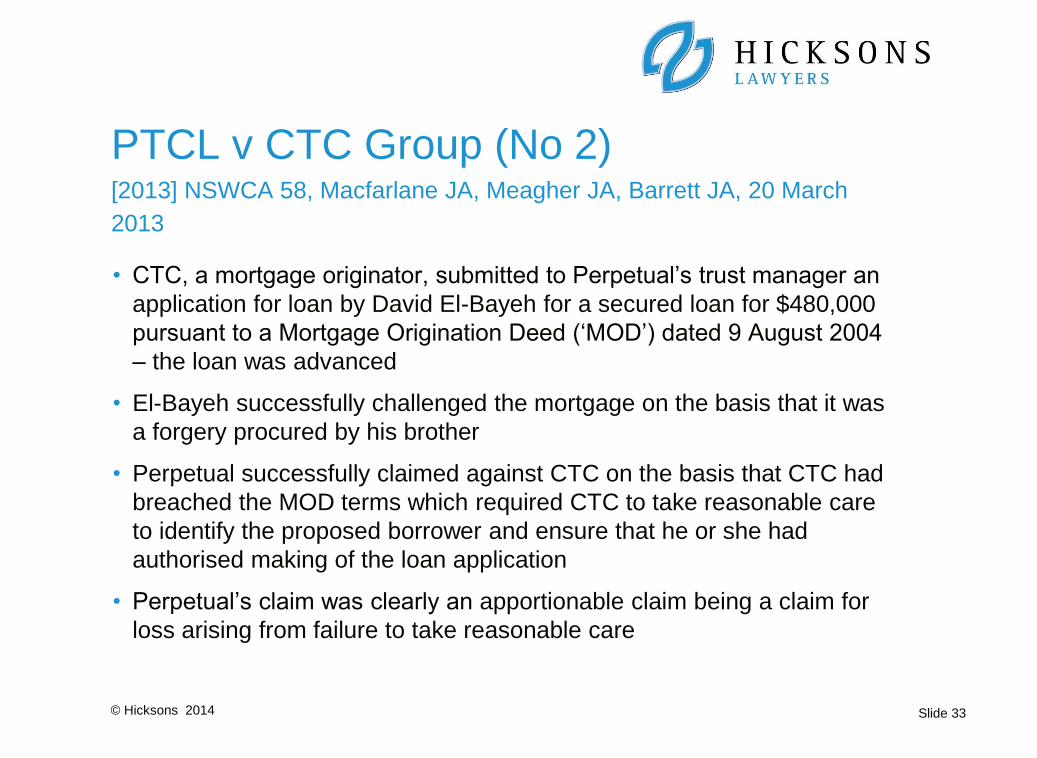

PTCL v CTC Group (No 2)[2013] NSWCA 58, Macfarlane JA, Meagher JA, Barrett JA, 20 March

2013

• CTC, a mortgage originator, submitted to Perpetual’s trust manager an

application for loan by David El-Bayeh for a secured loan for $480,000

pursuant to a Mortgage Origination Deed (‘MOD’) dated 9 August 2004

– the loan was advanced

• El-Bayeh successfully challenged the mortgage on the basis that it was

a forgery procured by his brother

• Perpetual successfully claimed against CTC on the basis that CTC had

breached the MOD terms which required CTC to take reasonable care

to identify the proposed borrower and ensure that he or she had

authorised making of the loan application

• Perpetual’s claim was clearly an apportionable claim being a claim for

loss arising from failure to take reasonable care

© Hicksons 2014 Slide 34

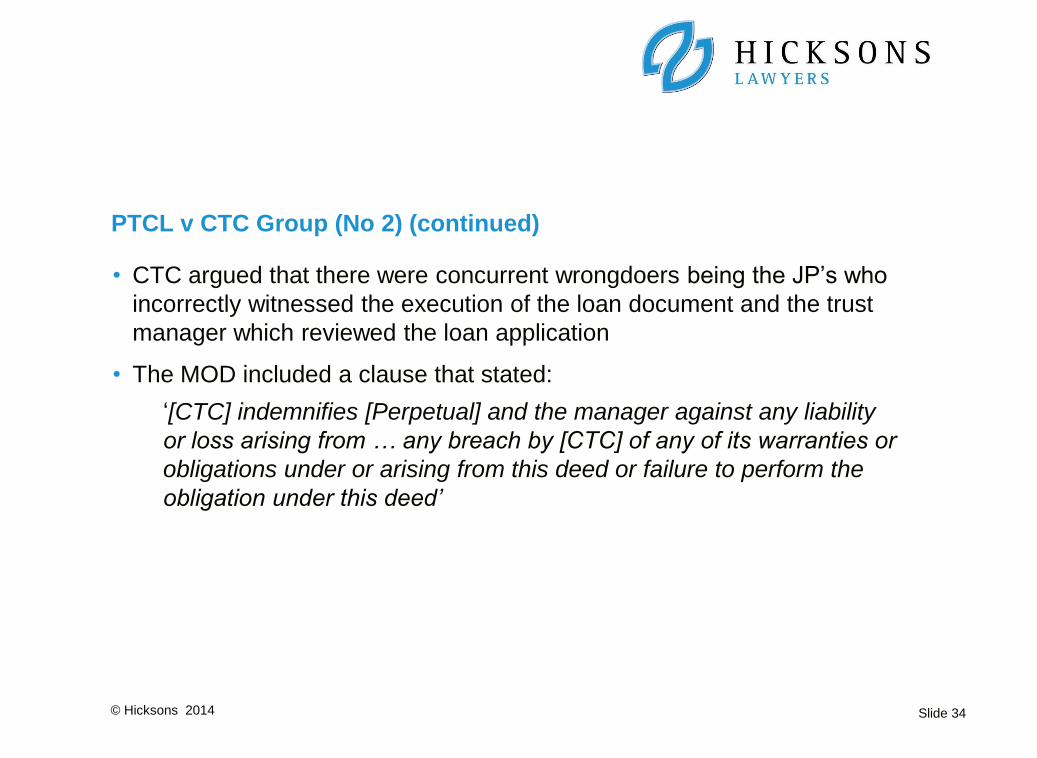

PTCL v CTC Group (No 2) (continued)

• CTC argued that there were concurrent wrongdoers being the JP’s who

incorrectly witnessed the execution of the loan document and the trust

manager which reviewed the loan application

• The MOD included a clause that stated:

‘[CTC] indemnifies [Perpetual] and the manager against any liability

or loss arising from … any breach by [CTC] of any of its warranties or

obligations under or arising from this deed or failure to perform the

obligation under this deed’

© Hicksons 2014 Slide 35

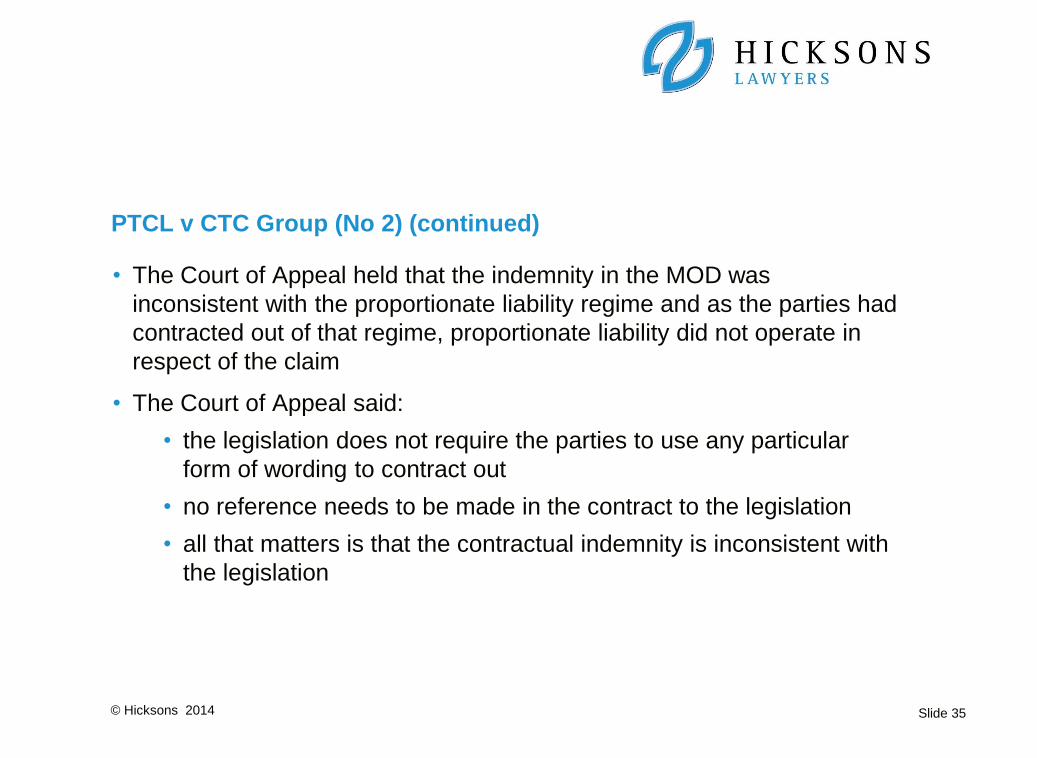

PTCL v CTC Group (No 2) (continued)

• The Court of Appeal held that the indemnity in the MOD was

inconsistent with the proportionate liability regime and as the parties had

contracted out of that regime, proportionate liability did not operate in

respect of the claim

• The Court of Appeal said:

• the legislation does not require the parties to use any particular

form of wording to contract out

• no reference needs to be made in the contract to the legislation

• all that matters is that the contractual indemnity is inconsistent with

the legislation

© Hicksons 2014 Slide 36

PTCL v CTC Group (No 3)[2014] NSWCA 290, MacFarlane J, Meagher JA, Barrett JA, 28 August

2014

• CTC sought special leave to appeal to the High Court

• The High Court dismissed the application for special leave

• CTC and Perpetual have been unable to agree the quantification of

damages which CTC should pay to Perpetual

• The Court of Appeal ordered that the proceedings be remitted to the

Common Law Division to determine the amount of damages and make

consequential orders as to costs

© Hicksons 2014 Slide 37

Multiple causes of action – apportionable

and non-apportionable

• Frequently a claimant will have multiple causes of action available to

recovery the claimant’s loss

• If one or more of the available causes of action is not an apportionable

claim the question arises whether the claimant can elect to recover

under the non-apportionable cause of action to avoid potential reduction

of damages by apportionment

© Hicksons 2014 Slide 38

Judicial disagreement regarding election

between causes of action

• In Reinhold v NSW Lotteries Corporation (No 2) [2008] NSWSC 187:

• Barrett J considered the nature of a ‘claim’ for the purposes of

proportionate liability – he held that ‘claim’ refers to a claim as

proved and established, not as made or advanced (pleaded)

© Hicksons 2014 Slide 39

Judicial disagreement regarding election between causes of action

(continued)

• In Perpetual Trustee Company Limited v CTC Group (No 2) [2013]

NSWCA 58:

• Macfarlane JA stated:

‘the application of [the relevant proportionate liability legislation]

turns not on the facts that happen to be found but on the

essential character of the plaintiff’s successful cause of action’

• Meagher JA stated that he preferred not to express a view on the

issue

© Hicksons 2014 Slide 40

Judicial disagreement regarding election between causes of action

(continued)

• Barrett JA stated:

‘it cannot be suggested … that the nature or quality of a ‘claim’

is, for relevant purposes, to be determined solely by looking at

the Court’s decision in relation to it. Nor is the nature or quality

of a claim to be determined solely by looking at the terms in

which it is framed. Rather, it is a combination of the terms in

which the claim is framed (or pleaded) and the relevant findings

of the Court’

© Hicksons 2014 Slide 41

Judicial disagreement regarding election between causes of action

(continued)

• In Perpetual Trustee Company Limited v Ishak [2012] NSWSC 697:

• Brereton J held that Perpetual was entitled to damages under the

Fair Trading Act, 1987 (NSW) section 42 (misleading and deceptive

conduct – an apportionable claim) and section 45 (false

representations regarding an interests in land – a non-

apportionable claim) – he then held that Perpetual was entitled to

its full damages without reduction for proportionate liability,

implicitly indicating that the plaintiff could rely upon the non-

approtionable cause of action, effectively avoiding the operation of

the proportionate liability regime

© Hicksons 2014 Slide 42

Judicial disagreement regarding election between causes of action

(continued)

• In Wealthsure v Selig [2014] FCAFC 64 (30 May 2014):

• Mansfield J and Besanko J held that the effect of the relevant

Commonwealth proportionate liability legislation was that the

proportionate liability provisions apply where different causes of

action cause the same loss or damage irrespective of whether one

of those causes of action was a non-apportionable claim – ie no

ability for claimant to elect

• White J dissented indicating that the damages for the non-

apportionable cause of action should be assessed without

reference to the proportionate liability regime

© Hicksons 2014 Slide 43

Judicial disagreement regarding election between causes of action

(continued)

• In ABN AMRO Bank v Bathurst Regional Council [2014] FCAFC 65 (6

June 2014):

• Jacobson J, Gilmore J and Gordon J disagreed with Mansfield J

and Besanko J and agreed with White J to the effect that where two

separate contraventions cause the same loss or damage the

claimant could elect the remedy which the claimant wished to

enforce and accordingly the claimant could enforce the non-

apportionable cause of action and thereby avoid reduction of

damages on the basis of proportionate liability

© Hicksons 2014 Slide 44

Judicial disagreement regarding election between causes of action

(continued)

• The decisions are not consistent however the trend appears to be

towards allowing a claimant to elect to rely on a non-apportionable

cause of action if one is available

• If there are multiple causes of action and one or more of the available

causes of action is a non-apprortionable claim, the claimant should

consider not pleading the apportionable causes of action and a lender

should avoid pleading facts relating to the borrower which could

constitute allegations of loss arising from the borrower’s failure to take

reasonable care

This address represents a brief summary of the law relating to the issues raised and should not be relied on as a substitute for professional

advice. Specific legal advice should always be sought in relation to any particular circumstances and no liability will be accepted for any

losses incurred as a result of reliance on this address. © Hicksons 2014

This address represents a brief summary of the law relating to the issues raised and should not be relied on as a substitute for professional

advice. Specific legal advice should always be sought in relation to any particular circumstances and no liability will be accepted for any

losses incurred as a result of reliance on this address/document/paper [etc] by those relying solely on this address/document/paper [etc]

Hicksons Lawyers, Level 32, 2 Park Street, Sydney NSW 2000 AustraliaDX 309 Sydney ABN 58 215 418 381t +61 2 9293 5311 f +61 2 9264 4790www.hicksons.com.au

Liability limited by a Scheme approved under Professional Standards Legislation

SYDNEY · NEWCASTLE · CANBERRA · MELBOURNE · BRISBANE

This was a presentation by Rod Cameron of Hicksons.

If you require any further information, please contact:

Rod Cameron, Partner

t +61 2 9293 5407

f +61 2 9264 4790