Roberto Blanco - Financial policies, financialsystemsand productivity - Discussion

15

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH Session 3: Financial policies, financial systems and productivity Discussion Roberto Blanco Head of the Financial Analysis Division BIS-IMF-OECD Conference: Weak productivity: The role of financial factors and policies Paris, 10-11 January 2018 The views expressed in this presentation are those of the author and do not necessarily coincide with those of the Banco de España or the Eurosystem.

-

Upload

structuralpolicyanalysis -

Category

Economy & Finance

-

view

187 -

download

4

Transcript of Roberto Blanco - Financial policies, financialsystemsand productivity - Discussion

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Session 3: Financial policies, financial systems and productivity

Discussion

Roberto Blanco

Head of the Financial Analysis Division

BIS-IMF-OECD Conference: Weak productivity: The role of financial factors and policies

Paris, 10-11 January 2018

The views expressed in this presentation are those of the author and do not necessarily coincide with those of the Banco de España or the Eurosystem.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Discussion outline

3 papers:

1) Debt Overhang, Rollover Risk, and Corporate Investment: Evidence from the European

Crisis (S. Kalemli-Özcan, L. Laeven and D. Moreno) [KLM]

2) Distressed Banks, Distorted Decisions? (G. Anderson, R. Riley and G. Young) [ARY]

3) Monetary Policy, Factor Allocation and Growth (R. Banerjee, E. Kharroubi and F.

Zampolli) [BKZ]

• KLM and ARY: Real effects of credit constraints.

• BKZ: Factor allocation and productivity.

• Both topics are very relevant. Banco de España is also doing research in these two areas.

• First, I will discuss papers 1 and 2, and then paper 3.

2

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Real effects of credit constraints. What do papers do?

Topic of the papers: Both papers analyse real effects of the dependency of firms on weak

banks during the GFC.

Key identification assumption: Type of bank (weak vs strong) firms borrow from.

Real effects:

KLM focuses on the impact of credit constraints on investment.

ARY focuses on the impact of credit constraints on business failures (exit rates).

Sample of banks:

KLM: EMU banks.

ARY: British banks.

.

3

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Real effects of credit constraints. Main findings

1) KLM:

• The decline in investment during the crisis was stronger for firms with high leverage, high debt

service, and for those having a relationship with a weak bank.

• The negative effect of leverage is more pronounced when firms are linked to weak banks.

2) ARY:

• During the crisis, the probability of exit (firm failure) increased for firms borrowing from weak

banks relative to that of firms borrowing from strong banks. However, the effect is very small

(only 0.6 pp).

• The effect is more significant for firms with high leverage.

• There is also some evidence that this effect is more significant for relatively more productive

firms. This is the most interesting result of the paper. However, this result does not seem to be

robust (it is only found for certain horizons and datasets).

4

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Coefficients for2005-2007

Coefficients for2008-2013

Coefficients for2014-2015

Coefficients for05-08Q1

Coefficients for08Q2-13Q3

Coefficients for 13Q4-16Q2

Profitabilityit-1 __ 0.030*** -0.006__ ¡0.024***'_ Previous NPLs -0.021 0,003 -0,042***

Debt burdenit-1 _ '-0.009*** -0.012*** -0.009***_' Indebtedness -0,036*** -0,078*** -0,102***

Indebtednessit-1 _''-0.038*** -0.065*** -0.058***''' Debt burden 0,000 -0,002*** -0,003***

Sales growthit-1 __'0.041*** .0.032*** 0.032***'

No. of previous

relationships with banks

0,006*** 0,014*** 0,015***

Total factor

productivityit-1__-0.035*** . 0.010*** 0.041*** Total assets -0.001 0,009*** 0,005**

Age 0,004 0,018*** 0,003

Impact on the probability of a firm obtaining credit from any bank

Impact on the probability of positive net investment

Real effects of credit constraints. BE’sresearch

Some of these results are in line with the results of BE’ research [Herranz and Martínez-

Carrascal (2017), Blanco and Jiménez (forthcoming)]. We find that:

1) Indebtedness and debt burden are two key determinants for both investment decisions

and access to credit.

2) The sensitivity to these variables increased during the crisis.

5

Source: BE Annual Report, 2016, Chapter 2

Source: Blanco and Jiménez (forthcoming)

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Real effects of credit constraints. Drivers of results

What seems to be driving these results are the two following hypotheses:

H1: During the crisis, weak banks tightened credit supply conditions relative to strong banks.

H2: The ability of firms to switch from weak banks to strong banks was limited due to

asymmetric information problems.

However, the authors do not analyse that.

Suggestions:

Test for H1 in the sample used in the papers.

Analyse the role of the degree of dependency in weak banks:

KLM could analyse the role of the second main bank and the extent to which the results are

stronger for firms borrowing from a single bank.

ARY could analyse what happened to firms borrowing from both weak and strong banks.

6

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Real effects of credit constraints. Definition of weak banks (1)

Definition of weak banks:

KLM: Bank exposure to sovereign debt.

ARY: Banks receiving state funding between 2008 and 2009 or requiring a takeover to survive.

Is bank exposure to sovereign debt a good proxy for the strength of bank balance sheets?

Sovereign exposures do not seem to have been the main source of losses for EMU banks, except

for Greek banks. The role of delinquent loans to the private sector was more important.

7

0

5

10

15

20

25

30

35

40

07 08 09 10 11 12 13 14 15 16 17PRIVATE NON-FINANCIAL SECTORCONSTRUCTION AND REAL ESTATE SERVICES

%

NPL RATIO. SPANISH BANKS. DOMESTIC EXPOSURES

Source: Banco de España's Statistical Bulletin.

Loan losses calculated accumulating quarterly net impairment losses on loans in Spanish banksP&L accounts, since end-2007, for businesses in Spain. Sovereign debt securities lossesestimated accumulating quarterly theoretical losses on banks' holdings of Central Governmentbonds, for the same period. Theoretical quarterly losses are estimated by multiplying previousquarter banks' holdings of Central Government bonds by the quarterly change in SpanishCentral Government Bond Price Return Index (Table 22.17 of Banco de España's StatisticalBulletin).

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

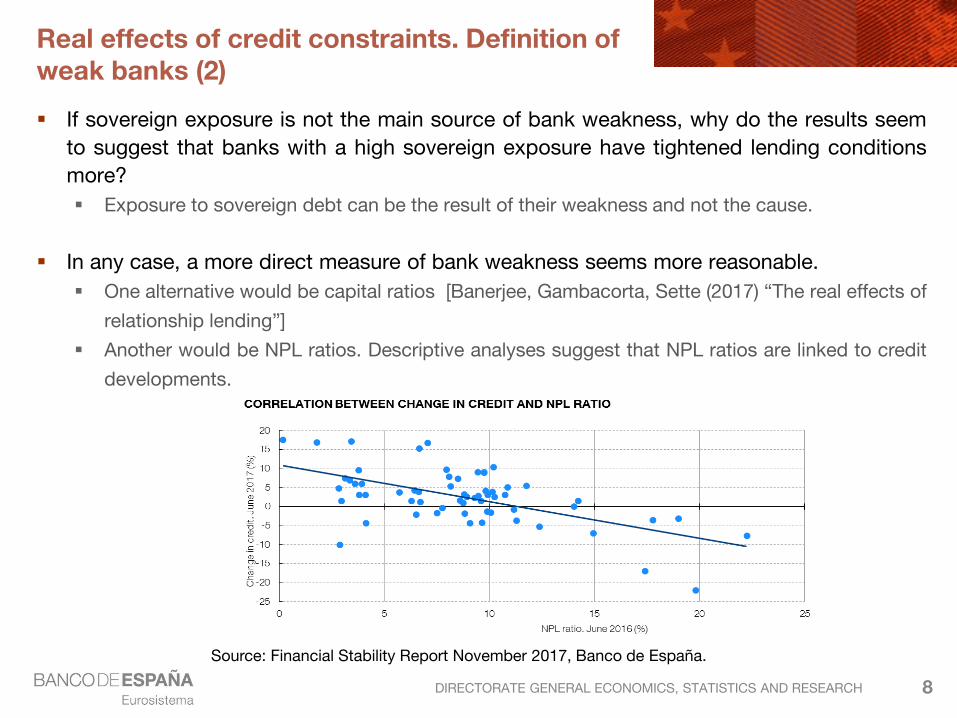

Real effects of credit constraints. Definition of weak banks (2)

If sovereign exposure is not the main source of bank weakness, why do the results seem

to suggest that banks with a high sovereign exposure have tightened lending conditions

more?

Exposure to sovereign debt can be the result of their weakness and not the cause.

In any case, a more direct measure of bank weakness seems more reasonable.

One alternative would be capital ratios [Banerjee, Gambacorta, Sette (2017) “The real effects of

relationship lending”]

Another would be NPL ratios. Descriptive analyses suggest that NPL ratios are linked to credit

developments.

8

Source: Financial Stability Report November 2017, Banco de España.

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Real effects of credit constraints. Definition of weak banks (3)

However, if the aim of the KLM paper is the analysis of the role of bank sovereign

exposure on investment, the following has to be taken into account:

Timing: sovereign risk was not priced in until 2010-11

Heterogeneity: not all countries have been affected in the same way.

9

These facts could have been considered in the specification (for example, by limiting the crisis period to years 2010-2012 or by allowing for differentiated time effects).

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Real effects of credit constraints. Definition of weak banks (4)

ARY definition of weak banks makes sense and is in line with the literature [Bentolila et al

(2013)].

However, the fact that banks receiving state funding between 2008 and 2009 were

encouraged not to cut lending could weaken the results and main explain why the

reported effects are so small.

To address this issue and to check the robustness of results, I suggest using alternative

measures of weak banks such as capital ratios [Banerjee, Gambacorta, Sette (2017)].

10

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Real effects of credit constraints. Othercomments

KLM:

Panel regression: If exposure to sovereign debt measures the effect of weak sovereigns on

banks only periphery sovereign debt should be considered (as in Table 7), but also including

that part held by non-domestic banks.

ARY:

Sample:

Possibly biased: only firms with collateralised loans are considered. What is the role of this

in the results?

Too small when productivity measures are considered (only 9,000 firms). This might explain

the lack of robust results in the relationship with productivity.

Results: It is far from clear why credit constraints faced by firms borrowing from weak banks

are stronger for more productive firms.

A possible explanation is the higher leverage of more productive firms.

The explanation based on forbearance seems inconsistent with the existence of credit

constraints .

11

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Factor allocation and productivity.Methodology to estimate misallocation

• The paper focuses on misallocation across sectors, but there is ample evidence pointing

to within-industry misallocation across firms as the main driver of aggregate productivity

developments [García- Sentana et al. (2016, BE WP), Gopinath et al. (2017, QJE)].

• The measure of misallocation across sectors is based on the covariance between growth

rates of market shares and productivity and resembles the cross-term in the

decomposition by Foster et al. (2006, RES). What is the conceptual difference between

both approaches?

• The measure is estimated using a one-step approach instead of the two-step approach in

Borio et al. (2016). Why is this approach more efficient?

• In the main specification used in equation 10 country-sector plus sector-time fixed effects

are considered. Therefore, only the variation over time is exploited. Are the main findings

robust to the inclusion of other fixed effects (time effects instead of sector-time fixed

effects)?

12

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Factor allocation and productivity. The role of monetary policy, main findings

Main finding: factor reallocation is linked to surprises in the slope of the yield curve.

Shocks that flatten the slope tend to have a negative effect on the contribution of reallocation

to aggregate productivity growth and vice versa.

The authors argue that this result implies that QE policies (which flatten the slope of the

yield curve) may have a detrimental impact to productivity growth, whereas conventional

monetary policies (which steepens the slope of the yield curve) have a positive effect.

13

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Factor allocation and productivity. The role of monetary policy, my comments (1)

Little variability of the interest rate variables (11 out of 15 countries are EMU countries and

share the same or similar interest rates).

The coefficient of interest could potentially capture other effects.

What is the theoretical justification for the relationship between unexpected changes in

the slope of the yield curve and factor allocation?

Why only unexpected changes do matter?

Expected changes in monetary policy do not have any effect on factor allocation whereas

expected changes do have an impact.

The results are interpreted in terms of the implications for the impact of monetary policy,

but changes in the slope of the yield curve may reflect a variety of shocks other than

monetary policy shocks such as changes in the economic outlook, sovereign risk during

the crisis.

14

DIRECTORATE GENERAL ECONOMICS, STATISTICS AND RESEARCH

Factor allocation and productivity. The role of monetary policy, my comments (2)

The authors suggest that during the crisis monetary policy has mainly been implemented

using non-conventional policies such as QE whose effect is the flattening of the yield

curve.

However, this is not true, specially for euro area countries. In the euro area, QE was introduced

in 2015. Policies targeting short term interest rates have played an important role until early

2016.

15