Roadshow Title In Here - Home - C&C Group · securities of C&C Group plc (the "Company"). The...

108

Investor Seminar Glasgow 10 th November 2010

-

Upload

duongnguyet -

Category

Documents

-

view

216 -

download

0

Transcript of Roadshow Title In Here - Home - C&C Group · securities of C&C Group plc (the "Company"). The...

Investor Seminar

Glasgow 10th November 2010

Stephen GlanceyChief Operating Officer

Glasgow 10th November 2010

Kenny NeisonStrategy and IR Director

• Investor Presentation

• Lunch

• Brewery visit and tour

• Trade Visits

• Dinner and Cider Tasting

Overview of Today

• Philosophy and Progress

• Our Brands

• Ireland

• C&C Investment Case

Introduction

Marketing Overview UK

• Paul Bartlett -

• Kirsty Hunter – Head of Consumer Marketing Magners GB

• Sandra Mitchell – Brand Director Tennent‟s

Republic of Ireland Overview

• Michael Merrins

• Stephen Kent

Introducing the Presenters

DISCLAIMER

This presentation does not constitute an invitation to underwrite, subscribe for, or otherwise acquire or dispose of any shares or othersecurities of C&C Group plc (the "Company").

The presentation contains forward-looking statements, including statements about the Company's intentions, beliefs and expectations.These statements are based on the Company's current plans, estimates and projections, as well as the Company's expectations ofexternal conditions and events. Forward-looking statements involve inherent risks and uncertainties and speak only as of the date theyare made. The Company undertakes no duty to and will not necessarily update any such statements in light of new information orfuture events, except to the extent required by any applicable law or regulation. Recipients of this presentation are therefore cautionedthat a number of important factors could cause actual results or outcomes to differ materially from those expressed in any forward-looking statements.

Past performance is no guide to future performance and persons needing advice should consult an independent financial adviser.

Any statement in this presentation which infers that the transactions may be earnings accretive does not constitute a profit forecastand should not be interpreted to mean that the Company’s earnings or net assets in the first full financial year following thetransactions, nor in any subsequent period, would necessarily match or be greater than those for the relevant preceding financial year.

Your attention is drawn to the risk factors set out in the Appendix to this presentation. They are not set out in any particular order ofpriority. The risks described in this document, however, are not exhaustive and consequently do not necessarily comprise all thoseassociated with the Company and/or the recently acquired businesses. There may be other risks which may have an adverse effect onthe business, financial condition, results or future prospects of the Company.

DISCLAIMER

C&C Group plc and its subsidiaries Wm.Magner Limited and Bulmers Limited of

Clonmel Ireland are not connected to H P Bulmer Limited of Hereford, UK.

Bulmers Original Cider produced by Bulmers Ltd of Clonmel is sold outside the

Republic of Ireland under the name Magners Original Irish Cider.

Stabilise

ConsolidateTransform

Two Years In…..

Consumers

Customers

EmployeesSuppliers

Shareholders

Stakeholder Approach

Long Term

View

• Decentralised business model

• Small Head Office - capital allocation

• Shareholder alignment

• Balanced investment in customer and consumer

Point Of Differentiation

We Zig while others Zag

• Successful integration of Tennent's and Gaymers

• Grow with the market in Great Britain

• Hold earnings in Ireland

• Lay the foundation for international development

• Capital structure

Our Objectives This Year

• Transitional services for 1 year

• Production volume triples

• Employee base moves from 450 to 1200

• Sales Force integration in all territories

• Revenue and cost delivery

• Three plants versus one

• Focus on business with minimal customer disruption

• Separation of Spirits Division

Integration….A huge task

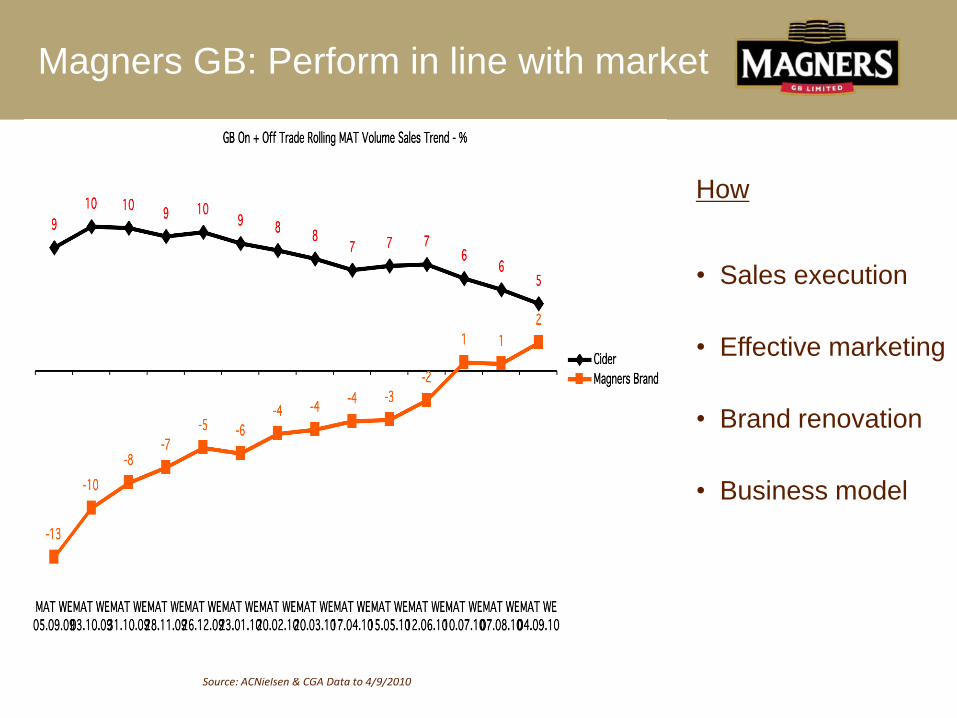

Magners GB: Perform in line with market

Source: ACNielsen & CGA Data to 4/9/2010

How

• Sales execution

• Effective marketing

• Brand renovation

• Business model

Ireland: Hold earnings

Source: ACNielsen Data to Sep 2010

Reality H1 2010/11:

• Bulmers volume (3.4%)

• Price (4.7%)

• Operating Margin (0.3ppt)

Focus:

• Cost

• Innovation

• Diversification

• Investment

• From FY09 Clonmel output per man from 6Khl to 9Khl

• From FY09 reduce cost per HL produced from €20 to €13

• October further reduction in Ireland operations €3m annualised benefit.

• Full year synergy guidance €18m

Operations….continued focus on cost reduction

• World cider market is growing

• C&C is No 2 in GB and in the

top 3 Cider brands in the world

• CAGR of 15% from FY06 to

FY11

• North America and Australia

have been the growth engines

• Plan to scale up resource in

USA

Magners International Volume Growth

9 13 15 1420 16

02

5 1111 7

20

30 20 23 21 18

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

F06 F07 F08 F09 F10 H1 F11

Magners Export Growth

North America

Iberia

Australia

Other Markets

+35%+9%

82Khl+15%(2%)+21%

68Khl+35%

89Khl +9%

71Khl(2%)

73Khl+39%

53Khl+21%

khl

Update on capital structure

Free Cash Flow• Half Year Cash Surplus

• C&C is well invested with strong

cash flow characteristics

• Capable of free cash flow

conversion at 70% - 80% EBITDA

• Current preference to retain

flexibility and liquidity

• Cash utilisation will be driven by

TSR philosophy

Paul BartlettMarketing Director

Glasgow 10th November 2010

Kirsty HunterHead of Consumer Marketing Magners GB

Sandra MitchellBrand Director Tennent’s

Magners GB Bulmers ROI

Locally relevant brand strategy and execution

Consumer + Customer needs by market

Marketing Goal: Strong Local Brands & Margin Optimisation

Magners ROWTennent‟s

Growing with

growing Cider

category

Revitalise

brand amongst

18-24yr olds

Extend share of

LADs

Sustainable

consumer-led

growth

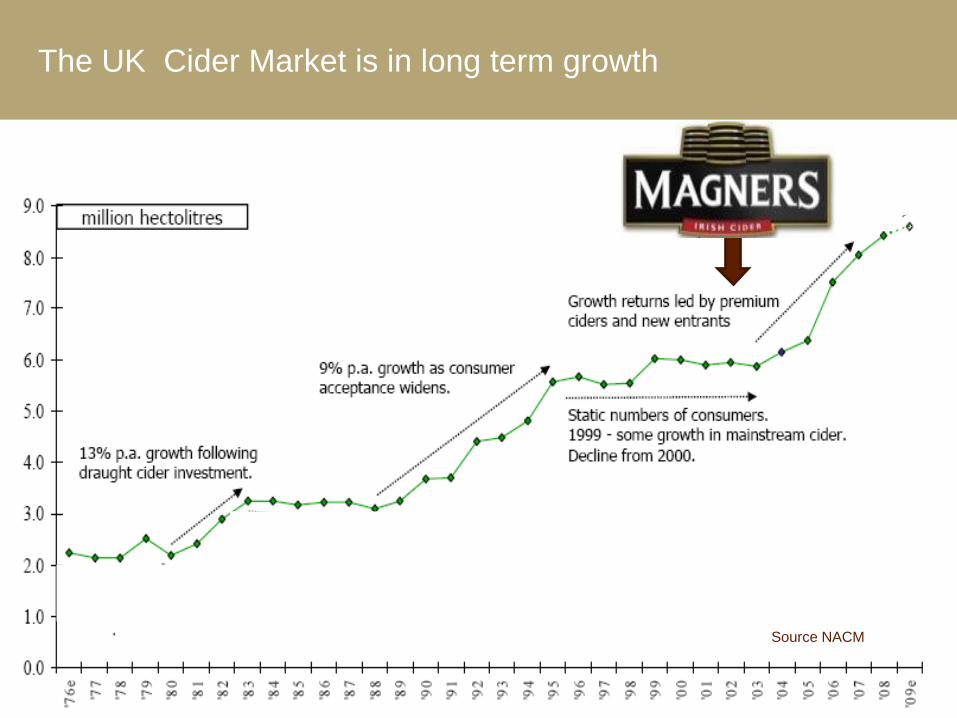

The UK Cider Market is in long term growth

Source NACM

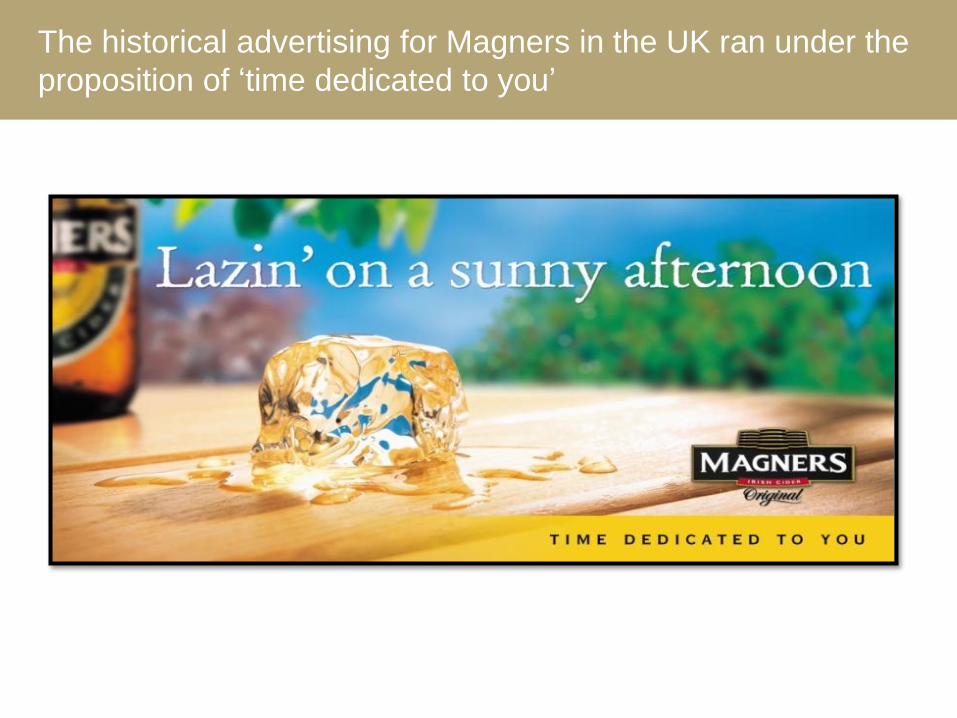

The historical advertising for Magners in the UK ran under the

proposition of „time dedicated to you‟

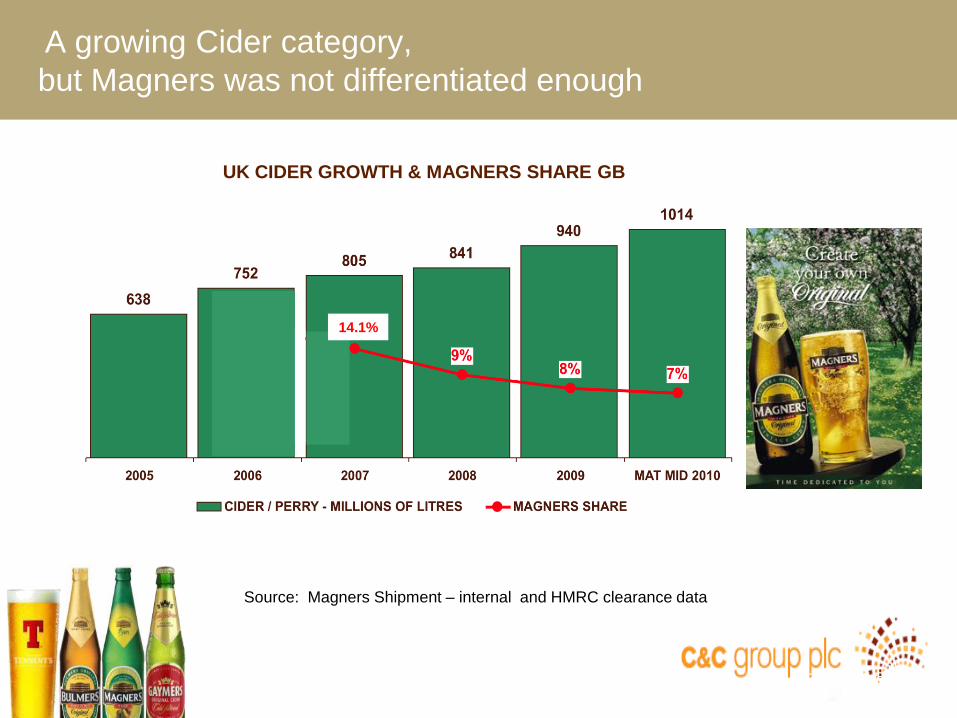

A growing Cider category,

but Magners was not differentiated enough

Source: Neilson

Source: Magners Shipment – internal and HMRC clearance data

12.4%

14.1%

UK CIDER GROWTH & MAGNERS SHARE GB

Whilst we worked on a new unique proposition for Magners in

GB we successfully launched Magners Pear

Volume (000s Ltr)

BRANDMAT TO WE 06.09.08

MAT TO WE 04.09.10

MAGNERS PEAR CIDER 0 4682

CRABBIES GINGER BEER 0 3424

BUDWEISER BREW NO 66 0 1616

GROLSCH BLONDE 0 1016

AMBER JACK 0 1001

JACK DANIELS & COLA 0 913

BULMERS SUMMER BLEND 0 656

WKD CORE 0 585

REKORDERLIG STRAWBERRY & LIME 0 574

MARSTONS CLASSIC 0 507

Source: Nielsen Off Trade MAT Sept 2010

• Magners Pear was the seventh Pear to launch to the market in GB

• Supported with heavyweight TV investment

• Value Share of Pear Cider Off Trade = 16.3%

• Value Share of Pear Cider On Trade = 18.6%

• Being late to market has made achieving potential hard.

Source: Nielsen Off Trade MAT Sept 2010

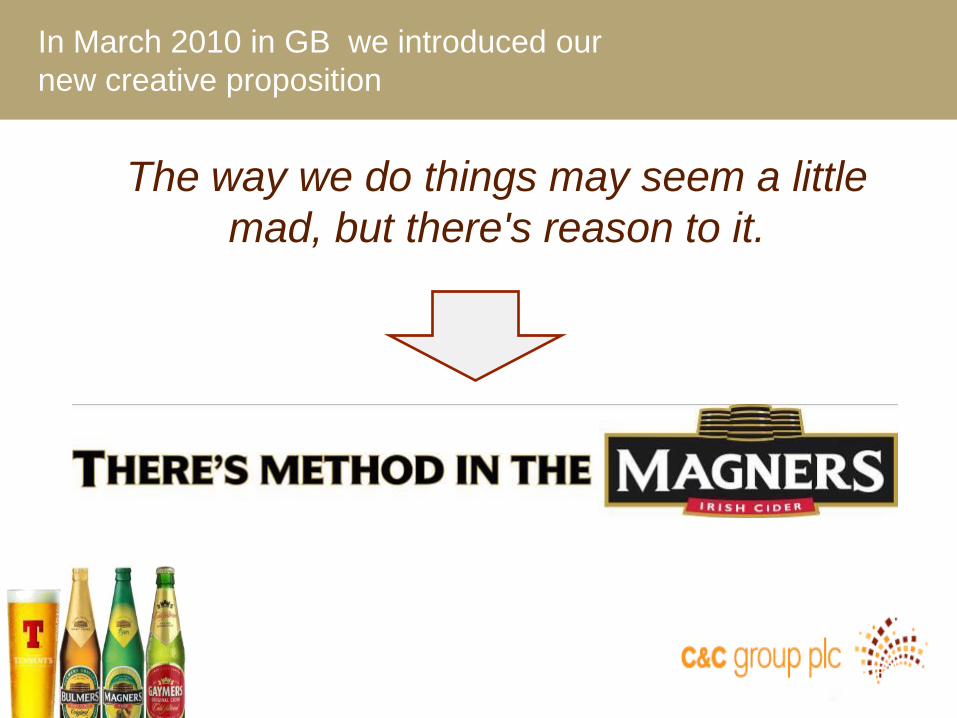

The way we do things may seem a little

mad, but there's reason to it.

In March 2010 in GB we introduced our

new creative proposition

Which we launched through two TV executions

„Catch‟ and „Straight‟

% Share of Voice01/03/10 - 31/8/10

Magners Cider

Carling Lager

Strongbow Cider

Fosters Lager

Carlsberg Lager

Budweiser Beer

Bulmers Cider

Guinness Draught

Heavy investment behind Magners within a well supported

category (4 of the top 11 brands are cider)

14.49%

11.95%

10.07%

9.97%

7.24%

6.23%

6%

5.51%

5.45%

4.66%

4.01%3.33%

2.01%

1.75%

1.68%

Source: NMR

Source: NMR

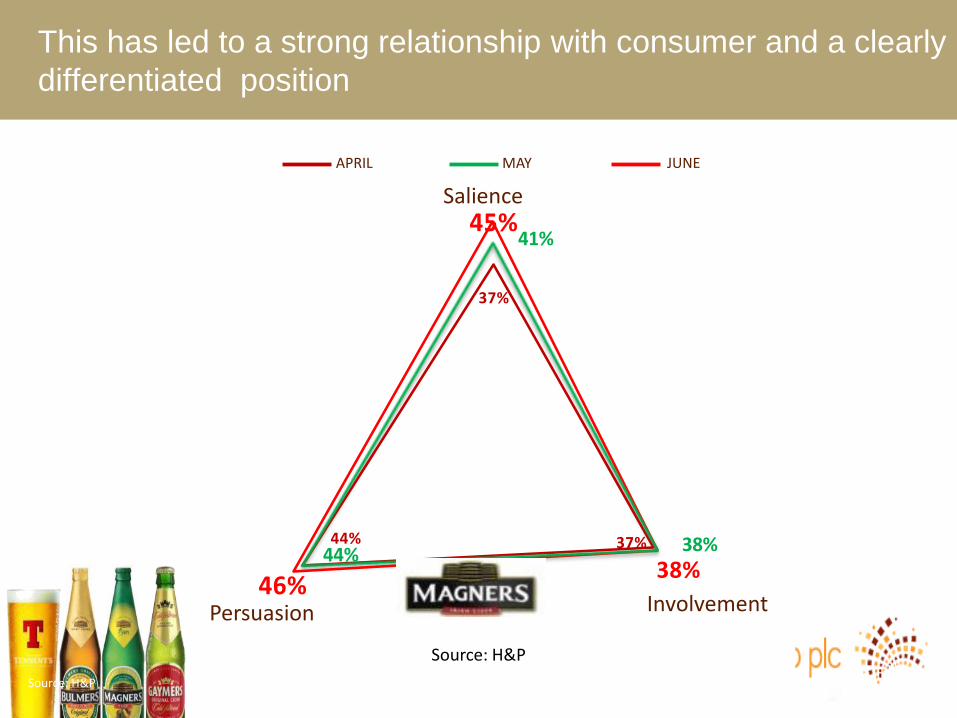

37%

37%44%

45%

38%46%

41%

38%44%

Salience

This has led to a strong relationship with consumer and a clearly

differentiated position

APRIL MAY JUNE

Source: H&P

InvolvementPersuasion

Source: H&P

Magners ahead of category leader on key measures

‘Excellent Quality’

‘Worth Paying More For’

Source: Hall and Partners, Aug 2010

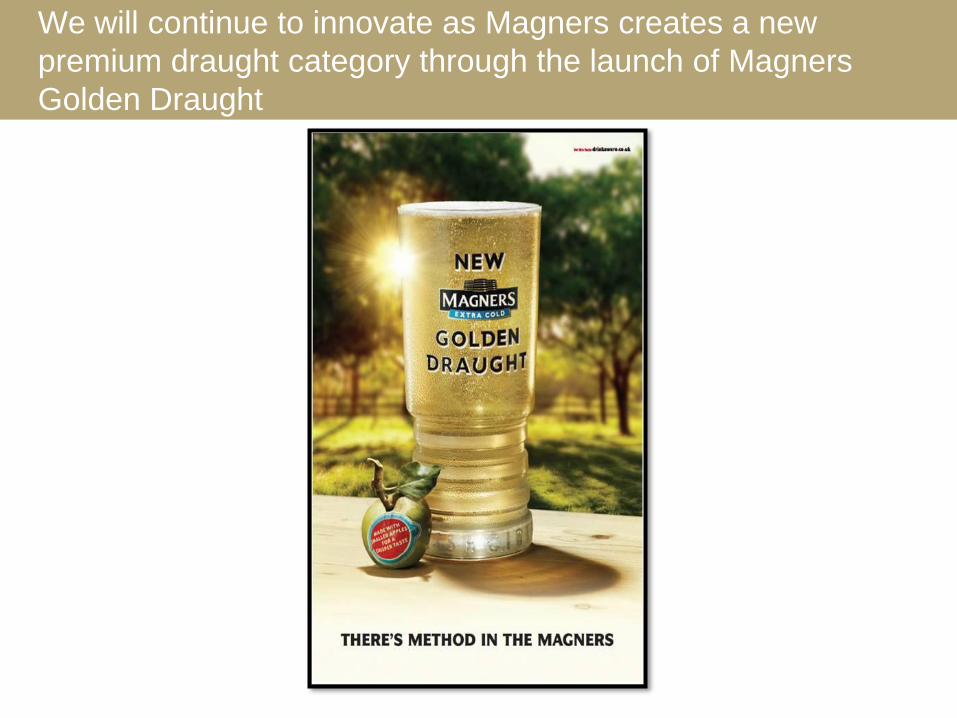

We will continue to innovate as Magners creates a new

premium draught category through the launch of Magners

Golden Draught

Source:Nielsen Ons

The purchase of the Gaymers business allows us to support our

Growth plan for the Magners Brand

Gaymers

• Gives us the opportunity to meet different consumer needs without stretching Magners too far

Blackthorn

• Strong in the SW of England, cider heartland and will support our distribution of Magners Golden Draught

Addlestones

• Super premium offering that supports Magners in the top end outlets

Own label

• Leverage Own-Label to support Magners growth plans

• Magners was a phenomenon which changed perception of Cider in GB

• Magners was not well differentiated from competition

• Nor were customers well managed

• New proposition and improved customer focus

• Magners has returned to growth

Summary

Tennent‟s Lager

• 1 in 3 pints of all beer consumed in Scottish pubs

• Stocked by 7 out of 10 pubs

• Highest rate of sale of any beer brand in the GB Off Trade

• A Scottish icon

• “it sits at the heart of what it means to be Scottish”

Scotland‟s No.1 Long Alcoholic Drink Brand

CGA Aug 2010; AC Nielsen; 2010; Brand GeneticCGA Aug 2010; AC Nielsen; 2010; Brand Genetic

£0

£200,000

£400,000

£600,000

£800,000

£1,000,000

£1,200,000S

tell

a A

rto

is

Car

lin

g

Fo

ster

s

Mag

ner

s

Bac

ard

i

Bu

lmer

s

Cap

tain

Mo

rgan

Ru

m

Sm

irn

off

Jack

Dan

iels

Str

on

gb

ow

Gro

lsch

Co

ors

Ten

nen

ts

Ru

ssia

n S

tan

dar

d

Ab

solu

t

San

Mig

uel

So

uth

ern

Co

mfo

rt

Tennent‟s had been suffering from underinvestment over the

past few years, leading to brand health decline

Nielsen Jan 2010. Scotland Media

2009 Scotland Media Spend

SOURCE MPG & Company Estimates

In 2010, we set out our new strategy to revitalise the brandIn 2010, we set out our new strategy

Build Brand Preference

amongst 18-24 year old ABC1

drinkers

Identify and exploit new

profit streams through

innovation

Improve brand presence in

Trade & build Off Trade Value

Revitalise the brand

Quality Football MusicAdvertising

In 2010, we’re back in business with a new brand advertising and PR campaign...

In June 2010, we launched a new advertising campaign, aimed

at our target 18-24 year old lager drinkers

*MPG data 2010

• In 2010, Tennent’s has now jumped to

No 5 media spender in Scotland this

year to date

• 83% of 18-24 year olds saw TV adat least 10 times

*MPG data 2010

Sources: H&P 2006; 2cv Football Research 2007 Celtic & Rangers own data 2009

We launched a new 3 year sponsorship agreement with Celtic

and Rangers

•

•Scotland’s national passion – 73% 18-24 yr old Scots claim an interest in football (1)

• Rangers and Celtic are supported by 70%+ of Scottish football fans

Scotland’s No.1 Alcohol Brand

• 100,000+ music fans over 3 days• 27 hours of BBC TV coverage• Sold out every year since 1996 despite nowbeing more than 4 times its original size

Official T in the Park website

In July, we celebrated the 17th year of the

T in the Park music festival

Official T in the Park website

This month, we opened the „Tennent‟s Training Academy‟

•Launch of the newly created Tennent’sTraining Academy in Wellpark Brewery• Capacity to train up to 15,000 bar staff eachyear from running a pub to serving a perfect pint.

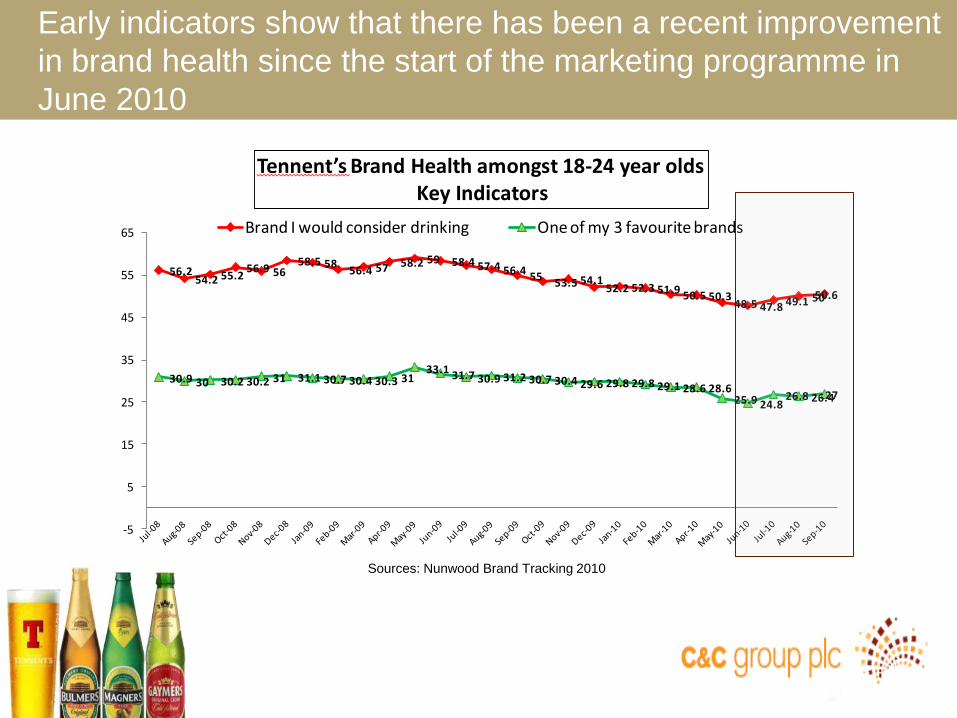

56.254.2 55.2

56.9 5658.5 58

56.4 57 58.2 59 58.4 57.4 56.4 5553.5 54.1

52.2 52.3 51.9 50.5 50.348.5 47.8 49.1 5050.6

30.9 30 30.2 30.2 31 31.1 30.7 30.4 30.3 3133.1 31.7 30.9 31.2 30.7 30.4 29.6 29.8 29.8 29.1 28.6 28.6

25.9 24.826.8 26.427

-5

5

15

25

35

45

55

65

Tennent’s Brand Health amongst 18-24 year oldsKey Indicators

Brand I would consider drinking One of my 3 favourite brands

Early indicators show that there has been a recent improvement

in brand health since the start of the marketing programme in

June 2010

Sources: Nunwood Brand Tracking 2010

• Tennent‟s revitalisation programme launched 2010

• TV and Poster advertising

• Sponsorship of Celtic and Rangers

• 17th year of T in the Park

• New Tennent‟s Training Academy

• Early signs of brand health recovery in 2010

• Positive platform for further growth

Summary

Michael MerrinsManaging Director Bulmers Ireland

Glasgow 10th November 2010

Stephen KentMarketing Director Bulmers Ireland

Republic of Ireland

1. Market Overview Michael Merrins

• Drinks Industry Trends

• Bulmers Performance against the market

• Key Challenges

2. Brand Growth Initiatives Stephen Kent

• Key Pillars

• Performance Impact

3. Priorities & Summary

Agenda

-

1,000,000

2,000,000

3,000,000

4,000,000

5,000,000

6,000,000

7,000,000

MAT SEP07 MAT SEP08 MAT SEP09 MAT SEP10

On & Off Trade LAD Volume (hectolitres)

In 2010, LAD volume continues to decline

Source: ACNielsen

-7% -9% -4%

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

4,000,000

MAT SEP07 MAT SEP08 MAT SEP09 MAT SEP10

On & Off Trade LAD Value (€ '000)

LAD market value continues to decline

Source: ACNielsen

-5% -7% -7%

4 2 2 4

4241

30 26

1010

8 7

8 11

12 16

35 3748 47

2002 2004

3+ times a week

1 / 2 times a week

Once a fortnight

Once every 3-4 weeks

Less often/never

20102008

% % % %

Consumers are changing behavior…..- Republic of Ireland Pub Drinking frequency has dropped since 2002

Source: B&A Dublin

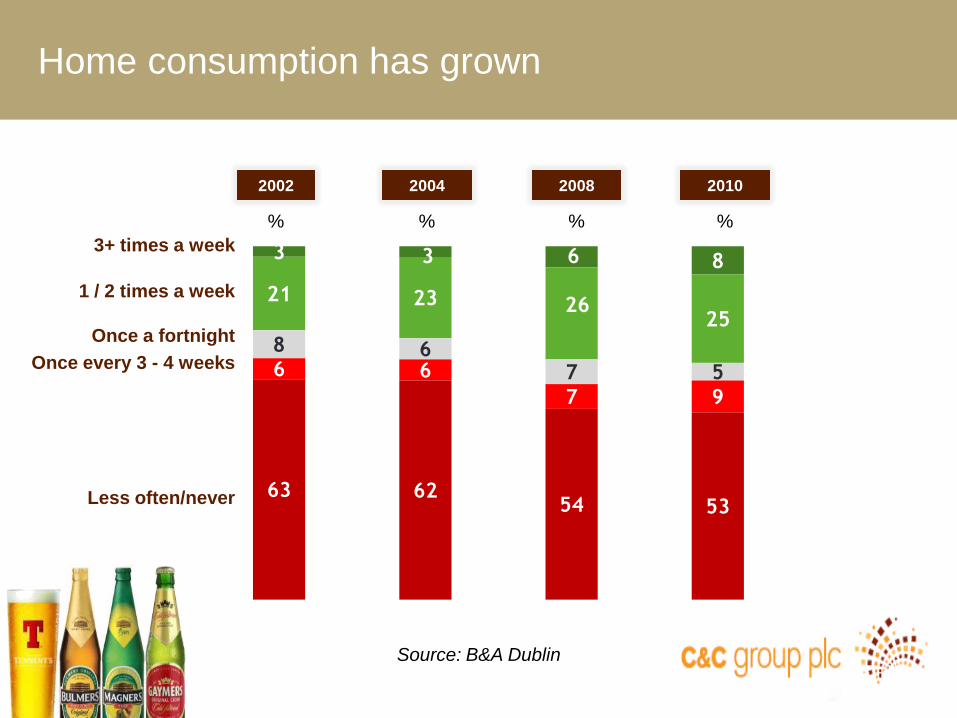

3 3 6 8

21 23 2625

8 67 56 6

7 9

63 6254 53

3+ times a week

1 / 2 times a week

Once a fortnight

Once every 3 - 4 weeks

Less often/never

2002 2004 20102008

% % % %

Home Consumption is on the rise……..- Republic of Ireland Home consumption has grown

Source: B&A Dublin

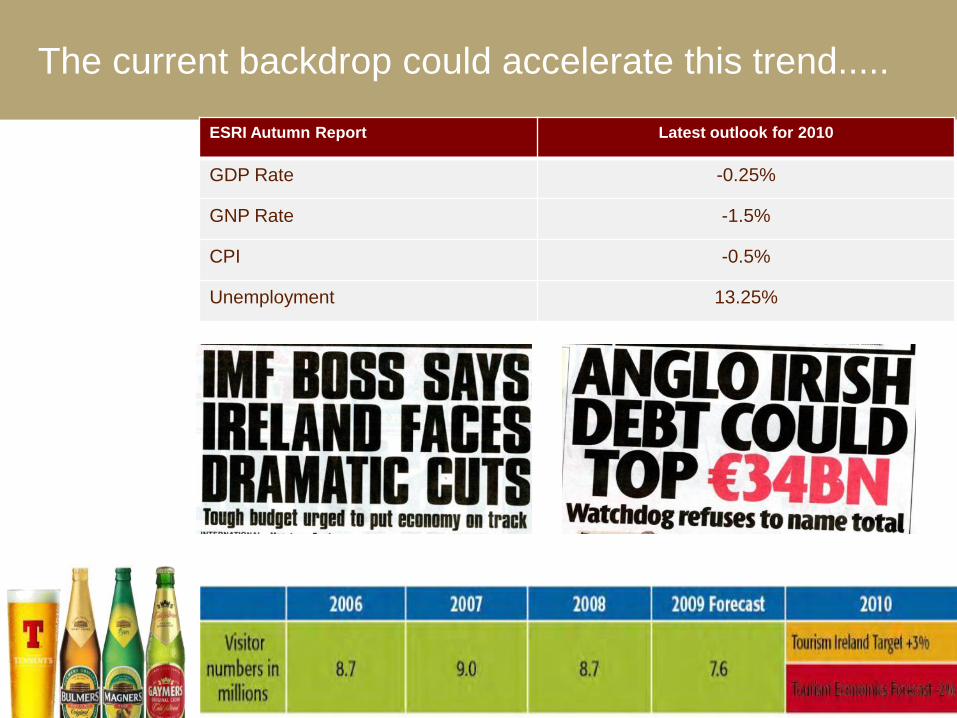

The current backdrop could accelerate this trend.....

ESRI Autumn Report Latest outlook for 2010

GDP Rate -0.25%

GNP Rate -1.5%

CPI -0.5%

Unemployment 13.25%

Cider gradually rebuilt its share of LAD

0

2

4

6

8

10

12

14 Market Share of Irish LAD Market

Bulmers

Other ciders

Incl. Other C&C brands

Cider Duty

Doubled

Smoking

Ban

%

Source:

Revenue Commissioners (Calendar Years)

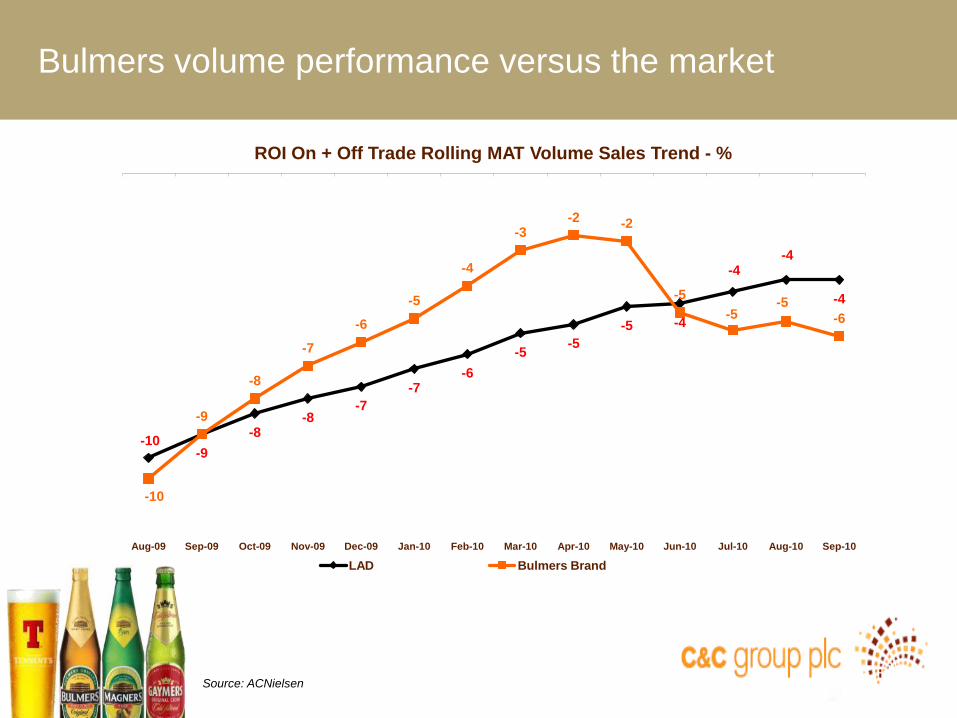

Bulmers volume performance versus the market

Source: ACNielsen

-10-9

-8-8

-7

-7-6

-5-5

-5 -4

-4-4

-4

-10

-9

-8

-7

-6

-5

-4

-3-2 -2

-5

-5-5

-6

Aug-09 Sep-09 Oct-09 Nov-09 Dec-09 Jan-10 Feb-10 Mar-10 Apr-10 May-10 Jun-10 Jul-10 Aug-10 Sep-10

ROI On + Off Trade Rolling MAT Volume Sales Trend - %

LAD Bulmers Brand

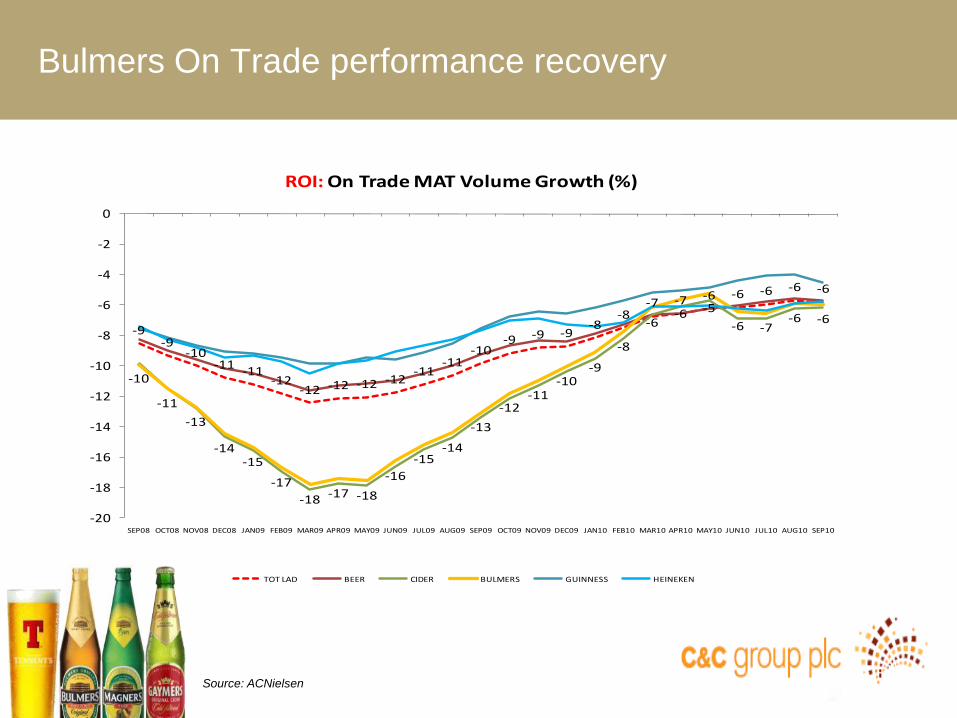

Bulmers On Trade performance recovery

Source: ACNielsen

-9-9

-10-11

-11-12

-12 -12 -12 -12-11

-11-10

-9 -9 -9-8

-8-7 -7 -6 -6 -6 -6 -6

-10

-11

-13

-14-15

-17

-18 -17 -18

-16

-15-14

-13

-12-11

-10-9

-8

-6-6 -5

-6 -7-6 -6

-20

-18

-16

-14

-12

-10

-8

-6

-4

-2

0

SEP08 OCT08 NOV08 DEC08 JAN09 FEB09 MAR09 APR09 MAY09 JUN09 JUL09 AUG09 SEP09 OCT09 NOV09 DEC09 JAN10 FEB10 MAR10 APR10 MAY10 JUN10 JUL10 AUG10 SEP10

ROI: On Trade MAT Volume Growth (%)

TOT LAD BEER CIDER BULMERS GUINNESS HEINEKEN

Volatility in Bulmers Off Trade volume performance

Source: ACNielsen

-7-6

-5

-4-3 -3

-3-2

-1-1

01 1

45

67

7 7 8 7

6

0

-2-3

-4

-8

-6

-4

-2

0

2

4

6

8

10

SEP09 OCT09 NOV09 DEC09 JAN10 FEB10 MAR10 APR10 MAY10 JUN10 JUL10 AUG10 SEP10

ROI: Off Trade MAT Volume Growth (%)

TOT LAD BULMERS

Brand Growth Initiatives

Glasgow 10th November 2010

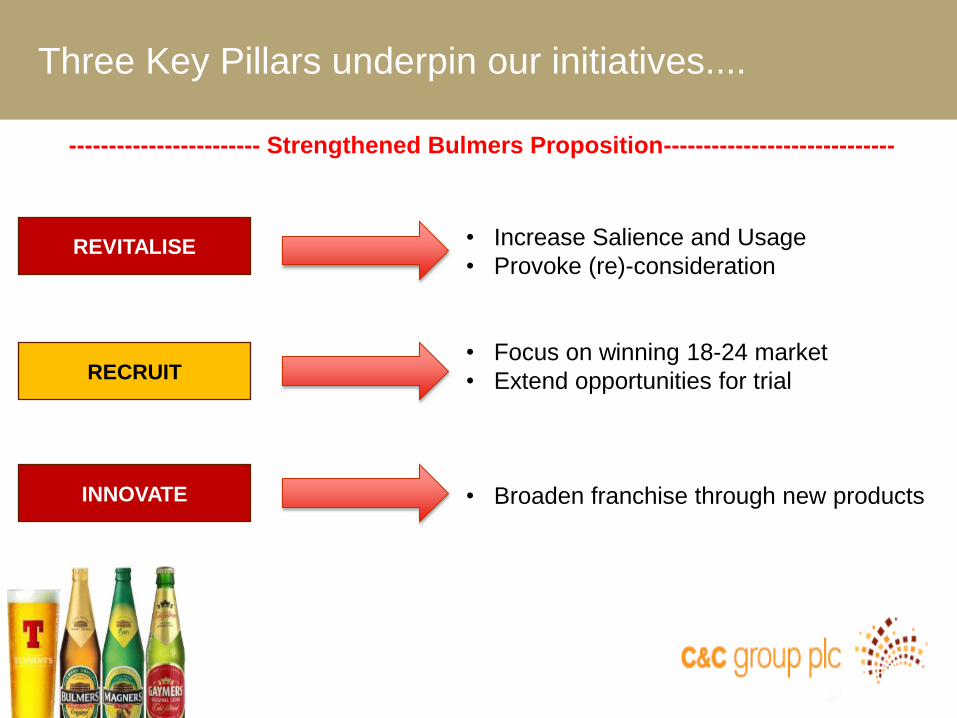

Three Key Pillars underpin our initiatives....

REVITALISE

RECRUIT

INNOVATE

------------------------ Strengthened Bulmers Proposition-----------------------------

• Increase Salience and Usage

• Provoke (re)-consideration

• Focus on winning 18-24 market

• Extend opportunities for trial

• Broaden franchise through new products

Our Calendar has been step-change....- Republic of Ireland

March 2009 Bulmers Pear Launched

June 2009 Pint Bottle Price Reduced

Summer 2009 New Off Trade Promotional Strategy

October 2009 New Beer Portfolio Integrated

March 2010 New Berry Launched

New

Creative

Campaign

May 2010

Becks Vier /Tennent's Distribution DriveMay 2010

Bulmers Draught Price Reduced

Our Calendar has been step-change....

Bulmers Berry

• Bulmers Berry launched to directly appeal

to 18-24s

• Creative and PR tailored to drive appeal with

‘An Undergrowth Movement’’

• Grocery data show 46% of Berry volume comes

from non-Bulmers brands.

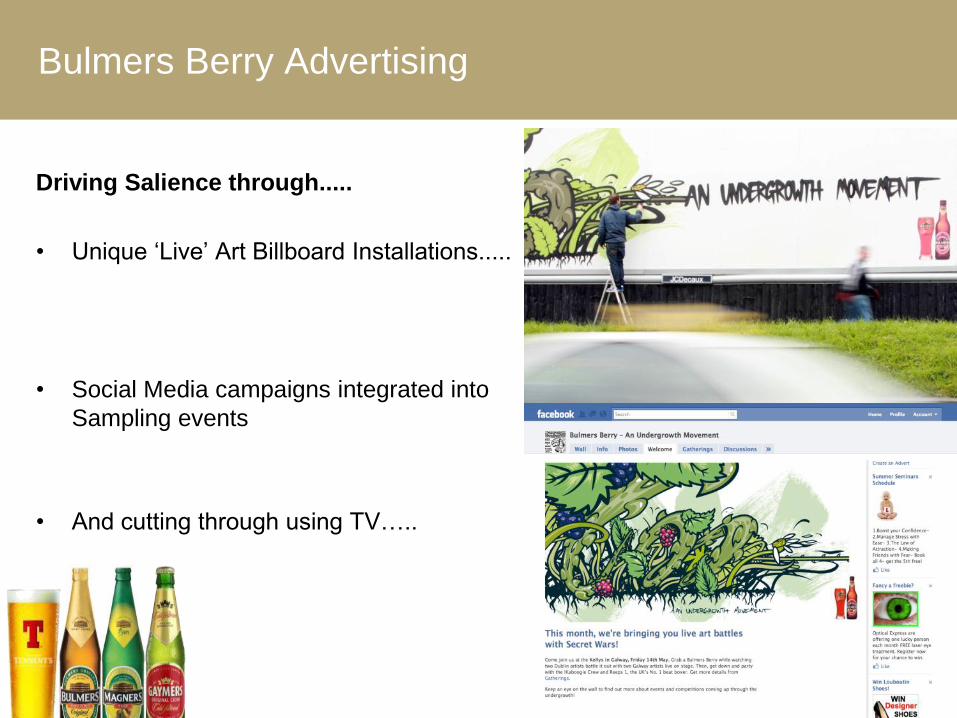

Bulmers Berry Advertising

Driving Salience through.....

• Unique „Live‟ Art Billboard Installations.....

• Social Media campaigns integrated into

Sampling events

• And cutting through using TV…..

Bulmers Berry TV Advertisement...

Our Bulmers Pint Bottle Price Reduction reversed a trend...

Source: ACNielsen

-7

-8

-10

-12

-14

-15

-17

-19 -19

-20-19

-18 -18-17

-16-15

-14

-13

-11

-9-8

-6 -7-6

-3

480

482

484

486

488

490

492

494

496

498

500

-25

-20

-15

-10

-5

0

AUG08SEP08OCT08NOV08DEC08JAN09FEB09MAR09APR09MAY09JUN09JUL09AUG09SEP09OCT09NOV09DEC09JAN10FEB10MAR10APR10MAY10JUN10JUL10AUG10

Cent

Hecto

litre

s

On Trade - Bulmers Original Pint Bottle, Volume Growth YOY (%) vs RSP/Pint, MAT

VOLUME GROWTH YOY % RSP PER PINT CENT

Bulmers Draught Support

• Reduced price to harmonise retail price with

premium lager

• Strong ROS support programmes

• New Livery and Glassware

• Dedicated Advertising Campaign

Bulmers Draught TV Advertisement....

Our Recruitment Strategy extended our reach....

Over 200,000

Consumers

Sampled

We united our Brand message....with a Brand TV Campaign

63

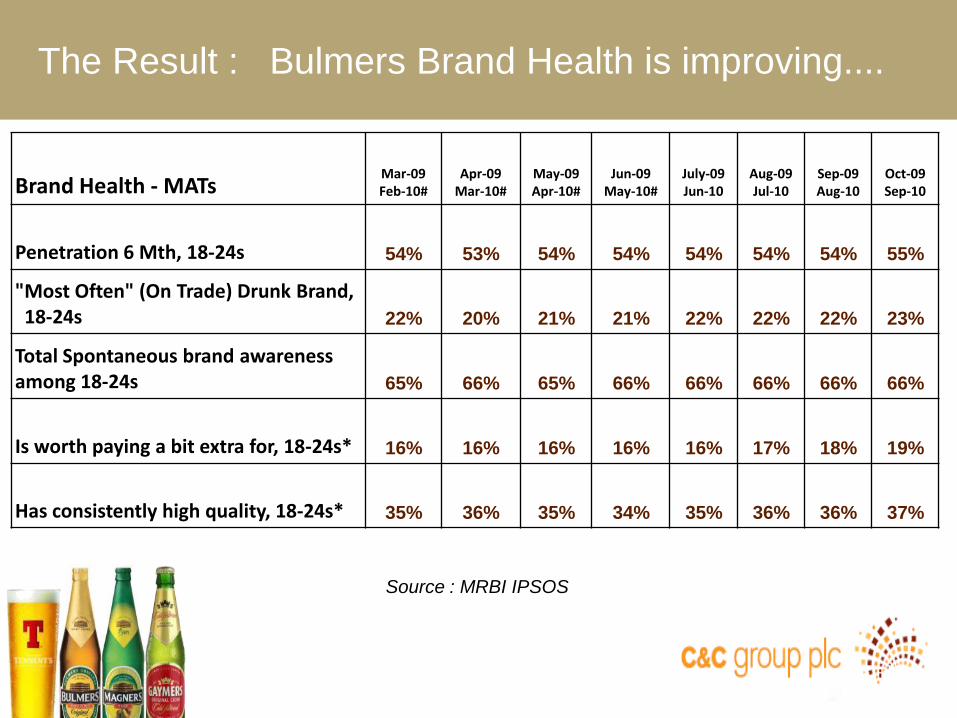

Brand Health - MATsMar-09Feb-10#

Apr-09Mar-10#

May-09Apr-10#

Jun-09May-10#

July-09Jun-10

Aug-09Jul-10

Sep-09Aug-10

Oct-09Sep-10

Penetration 6 Mth, 18-24s 54% 53% 54% 54% 54% 54% 54% 55%

"Most Often" (On Trade) Drunk Brand, 18-24s 22% 20% 21% 21% 22% 22% 22% 23%

Total Spontaneous brand awarenessamong 18-24s 65% 66% 65% 66% 66% 66% 66% 66%

Is worth paying a bit extra for, 18-24s* 16% 16% 16% 16% 16% 17% 18% 19%

Has consistently high quality, 18-24s* 35% 36% 35% 34% 35% 36% 36% 37%

The Result : Bulmers Brand Health is improving....

Source : MRBI IPSOS

Finally, these are early days with Beer....

Progress is slow but positive…

Regional Beer Advertising commenced....

Becks Vier in Cork

Tennent‟s in Northwest

Distribution Drive Successful.....

Summary

66

1. Hold and grow Bulmers share of LAD.

• Brand Health is at a two year high.

• Share of Cider has strengthened across On and Off Trade

• Our Brand campaigns are focused and effective.

2. Protect and optimize earnings in the ROI market.

• Continued investment in our brands to deliver volume

• Innovation to deliver growth especially through Off Trade

• Focus on Cost Reduction.

• Leverage our beer brands to deliver incremental profit.

John Dunsmore

Chief Executive Officer

Glasgow 10th November 2010

C&C Investment Case

1. Long term in perspective

2. Differentiation, not Scale, is the objective

3. Cider is a global growth category

4. C&C is a top 3 cider company in the world

5. Magners is the preferred cider brand in the biggest cider market in the world

6. Our cash position gives us choices

7. Team focus on sustainable value growth

8. Entrepreneurial

The basis for investment

Why companies fail

How the Mighty Fall, by Jim Collins

The hubris of success

„When the rhetoric of success (“we‟re successful

because we do these specific things”) replaces

penetrating understanding and insight (“we‟re

successful because we understand why we do

these specific things and under what conditions

they would no longer work”)‟

How is this relevant to C&C?

How the Mighty Fall, by Jim Collins

• Advertising strategy…..localised

• Route to market strategy…..have one

• Internal or external people?

• Relationship between group and divisions

• International management resource

How is this relevant to the future?

Flywheel not yet in place

How the Mighty Fall, by Jim Collins

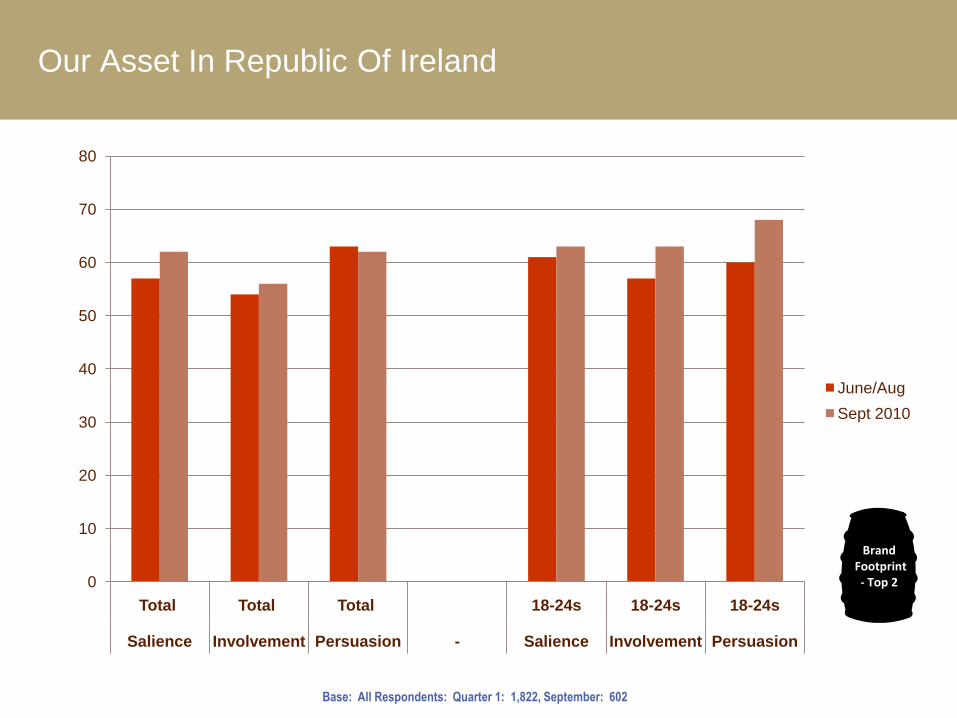

Our Asset In Republic Of Ireland

BrandFootprint- Top 2

Base: All Respondents: Quarter 1: 1,822, September: 602

0

10

20

30

40

50

60

70

80

Total Total Total 18-24s 18-24s 18-24s

Salience Involvement Persuasion - Salience Involvement Persuasion

June/Aug

Sept 2010

Our Asset In Northern Ireland

(Base: All Past 3 Month 18-64 yo Beer/Cider Drinkers)

94 97

36

19

11

6

7

63

33

21

14

13

Northern Ireland On Trade Consumer Funnel – July 2010

Our Asset In Scotland

37%

37%44%

45%

38%46%

41%

38%44%

Salience

This has led to a strong relationship with consumer and a clearly

differentiated position

APRIL MAY JUNE

Source: H&P

InvolvementPersuasion

Source: H&P

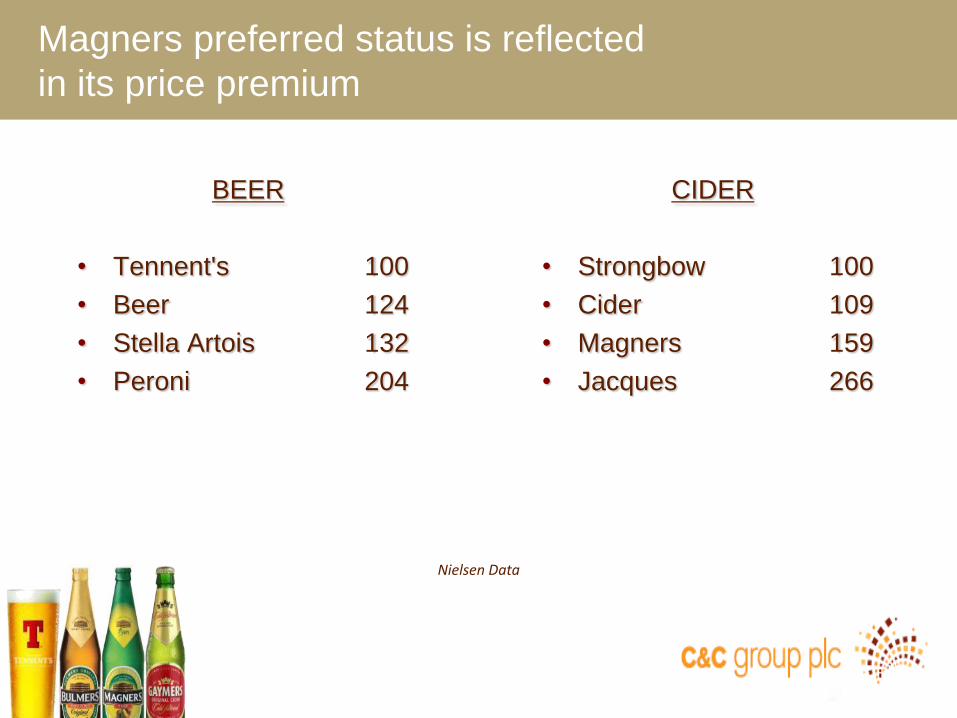

BEER

• Tennent's 100

• Beer 124

• Stella Artois 132

• Peroni 204

Magners preferred status is reflected

in its price premium

CIDER

• Strongbow 100

• Cider 109

• Magners 159

• Jacques 266

Nielsen Data

NET FAVOURABLE SCORES ADVANTAGE GROUP SURVEY 2010

Our UK Sales effectiveness is starting to help….

but a long way to go

2010

Carlsberg 64

AB Inbev 42

Magners 21

Molson-Coors 14

Gaymers 7

Miller Brands 7

Diageo -6

Heineken -8

Wells & Youngs -26

2009

Carlsberg 45

Heineken 34

AB Inbev 33

Molson-Coors 21

Wells & Youngs 21

Gaymers 7

Miller Brands -7

Magners -10

Diageo/Guinness -67

Category Development & Support

Our UK Sales effectiveness is starting to help….

but a long way to go

2010

Carlsberg 64

AB Inbev 42

Magners 21

Molson-Coors 14

Gaymers 7

Miller Brands 7

Diageo -6

Heineken -8

Wells & Youngs -26

2009

Carlsberg 45

Heineken 34

AB Inbev 33

Molson-Coors 21

Wells & Youngs 21

Gaymers 7

Miller Brands -7

Magners -10

Diageo/Guinness -67

Category Development & Support

22nd 19th

OVERALL POSITION

NET FAVOURABLE SCORES ADVANTAGE GROUP SURVEY 2010

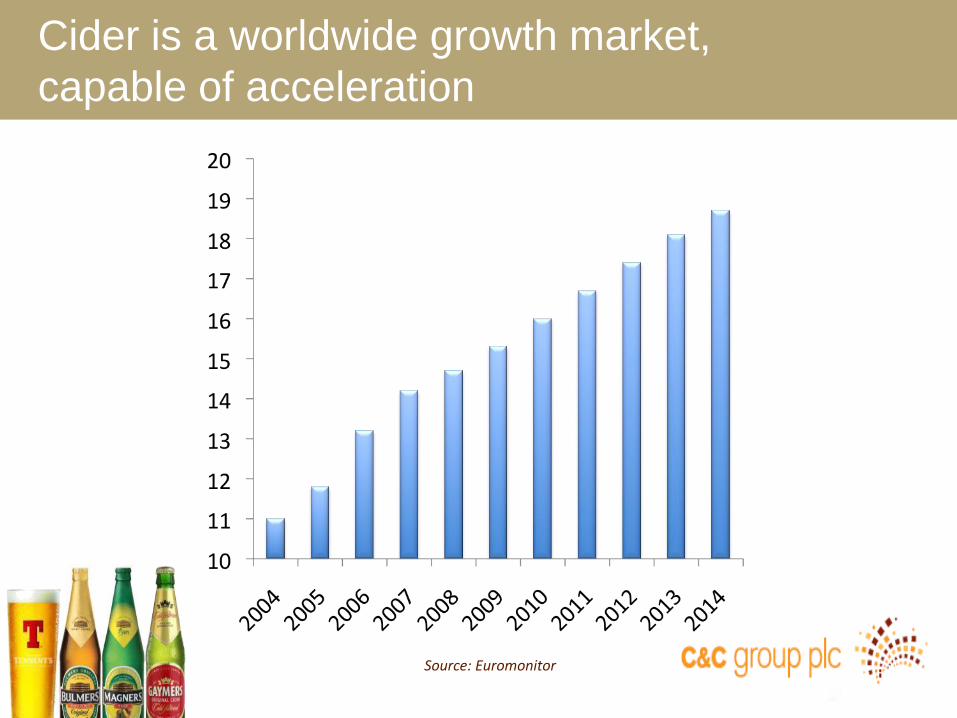

Cider is a worldwide growth market,

capable of acceleration

Source: Euromonitor

1. Heineken 19.5

2. C&C 12.7

3. Distell 12.1

4. Halewood 2.9

5. Aston Manor 2.8

6. Carlsberg 2.7

7. Saenz Briones 2.7

8. AGRIAL 2.5

9. Sidra La Victoria 2.2

10. Foster‟s 1.5

(VOLUME MARKET SHARE PERCENT)

C&C is one of the Top 3 Cider producers in the world

Source: Euromonitor

• Imagination

• Speed

• Flexibility (to local markets)

• Conservative entrepreneurialism

C&C‟s (potential) management USP

• Domestic markets provide cashflow for expansion

• International development benefits from a long term “Spirits”

type of approach

• We have to pioneer the category as well as our brands

• We will expand in line with management competency

• Operational improvement has been back-end driven so far

• There is more to do now than when we started

The opportunities for C&C are expanding all the time

Investor Seminar

Glasgow 10th November 2010

Mike Lees MD Scotland

Tom McCusker MD N Ireland

Tennent’s has been leading for a long time

and will continue to do so going forward

1556

Wellpark Brewery

established by the

monks of St Mungo

1885

Hugh Tennent launched

the UKs first commercial

scale lager – Tennent’s

Lager

1860

J&R Tennent becomes

the largest exporter of

bottle beers worldwide

1935

Tennent’s Lager

launched the first UK

lager in cans

1955

Tennent’s Lager launches

the first flat topped cans in

the UK

1967

Charrington United

Breweries merges

with Bass

2001

Bass acquired by

Interbrew

1963

Charrington United Breweries

acquires Tennent’s

Tennent’s launches the first

lager brand in draught

2008

Merger of InBev (ex-

Interbrew) and

Anheuser-Busch

2009

C&C acquires

Tennent’s

Tom McCusker MD N Ireland

Source: Canadean and NI DHSS

NI market place

• Part of UK - Legislation / duty / currency

• Devolved local government via NI assembly

• Land border with ROI - cross border trading

• Close links and affinity with Scotland

• TNI - evolved from integration of ABI NI and C&C NI

• TNI - a 120 year history in NI

• HPBulmers (Heineken) main competitor to Magners

NI Market Place

Brand Portfolio is vital – TNI strong in key areas

No. 1

CiderNo. 1

Packaged

LAD

No. 1

Premium

Packaged

Lager

No 1

On trade

Lager

Highest ROS

Draught

Lager

No 2

Packaged

LADs

No. 1 Non

Alcoholic

Beer

No 2

Total

LADs

Source AC Nielsen

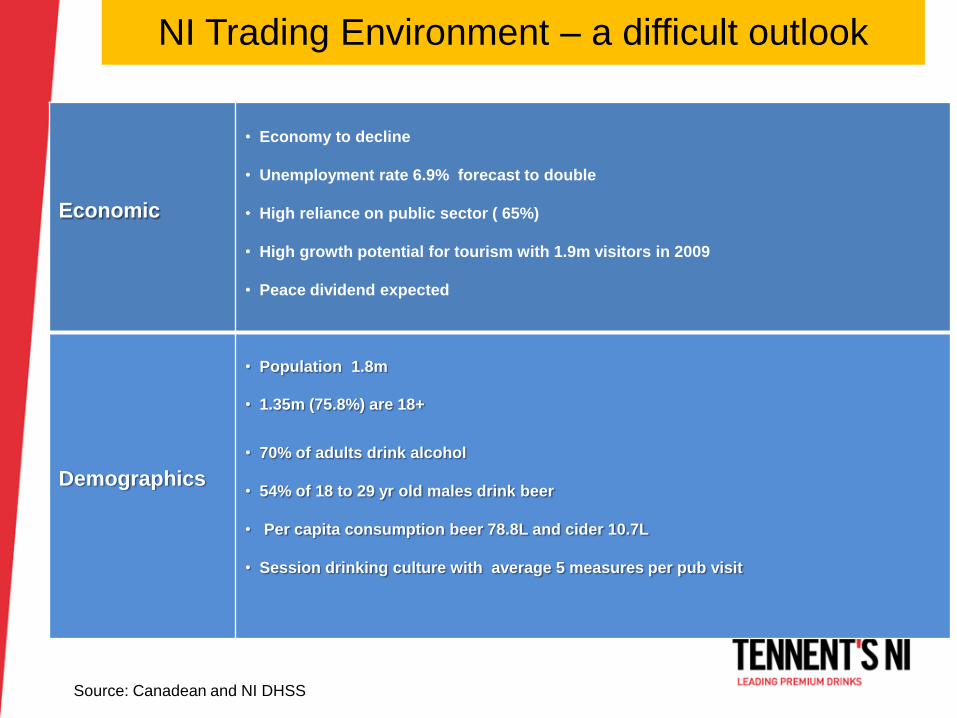

NI Trading Environment – a difficult outlook

Economic

• Economy to decline

• Unemployment rate 6.9% forecast to double

• High reliance on public sector ( 65%)

• High growth potential for tourism with 1.9m visitors in 2009

• Peace dividend expected

Demographics

• Population 1.8m

• 1.35m (75.8%) are 18+

• 70% of adults drink alcohol

• 54% of 18 to 29 yr old males drink beer

• Per capita consumption beer 78.8L and cider 10.7L

• Session drinking culture with average 5 measures per pub visit

Source: Canadean and NI DHSS

NI Beer and Cider Splits

• Total 1.5m HL

• Overall Beer & Cider shrinking @ -3%, driven by On Trade

• Cider still enjoying growth in the off trade but slowing in recent months

Beer On37%

Beer Off50%

Cider On4%

Cider Off9%

Source AC Nielsen

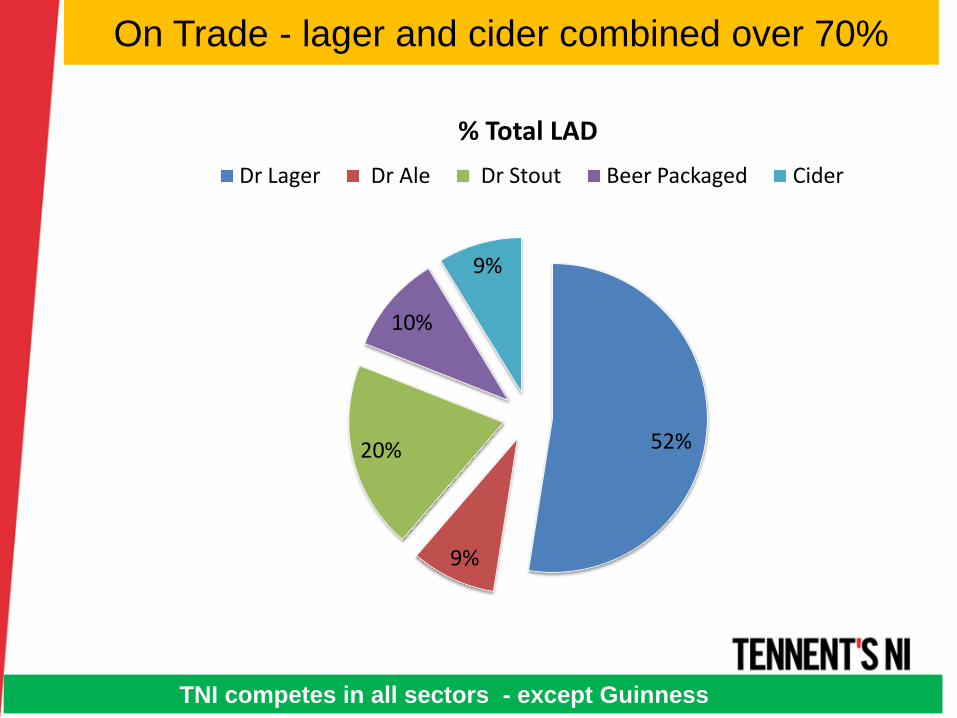

On Trade - lager and cider combined over 70%

52%

9%

20%

10%

9%

% Total LAD

Dr Lager Dr Ale Dr Stout Beer Packaged Cider

TNI competes in all sectors - except Guinness

Tied by Loan – a big part of On Trade mix

Ties usually continue for 10 yrs for draught lager, ale and cider

Diageo31%

Free49%

TNI20%

% of On Trade Outlets

Diageo45%

Free33%

TNI22%

% of Total LAD Volume

Dr Guinnessvia Diageo 2%

Free35%

TNI63%

% of Total TNI Volume

Company estimates

Manufacturers’ shares of On Trade beer and cider

All others 5%

Diageo 61% includes

Guinness @ 32%

Molson Coors 5%

TNI 29%

Source AC Nielsen

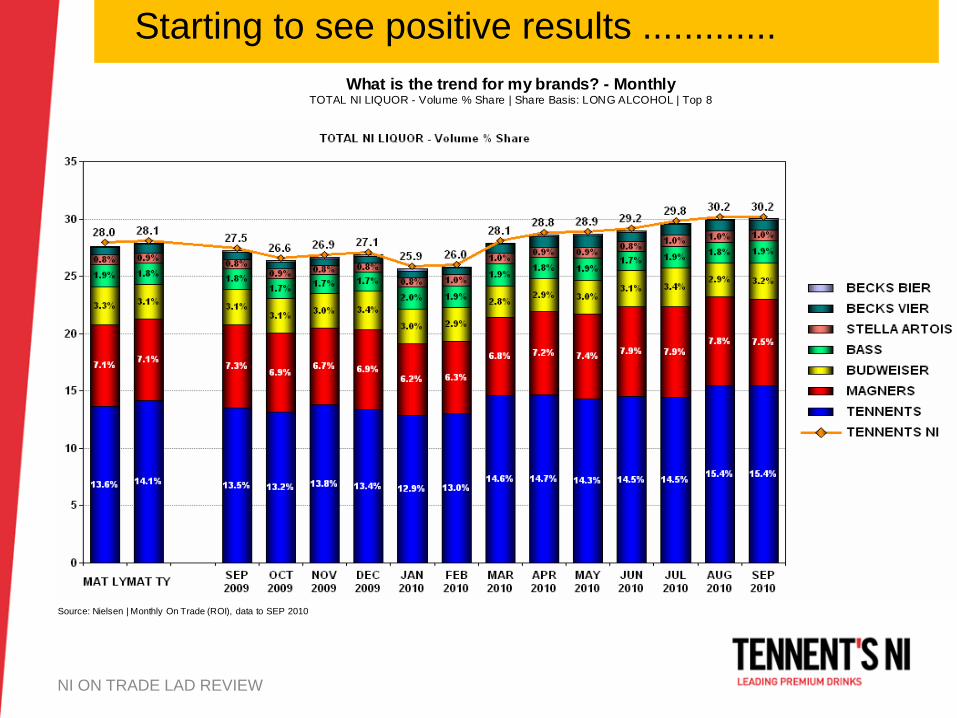

NI ON TRADE LAD REVIEW

What is the trend for my brands? - MonthlyTOTAL NI LIQUOR - Volume % Share | Share Basis: LONG ALCOHOL | Top 8

Source: Nielsen | Monthly On Trade (ROI), data to SEP 2010

Starting to see positive results .............

Magners performing well – maintaining share

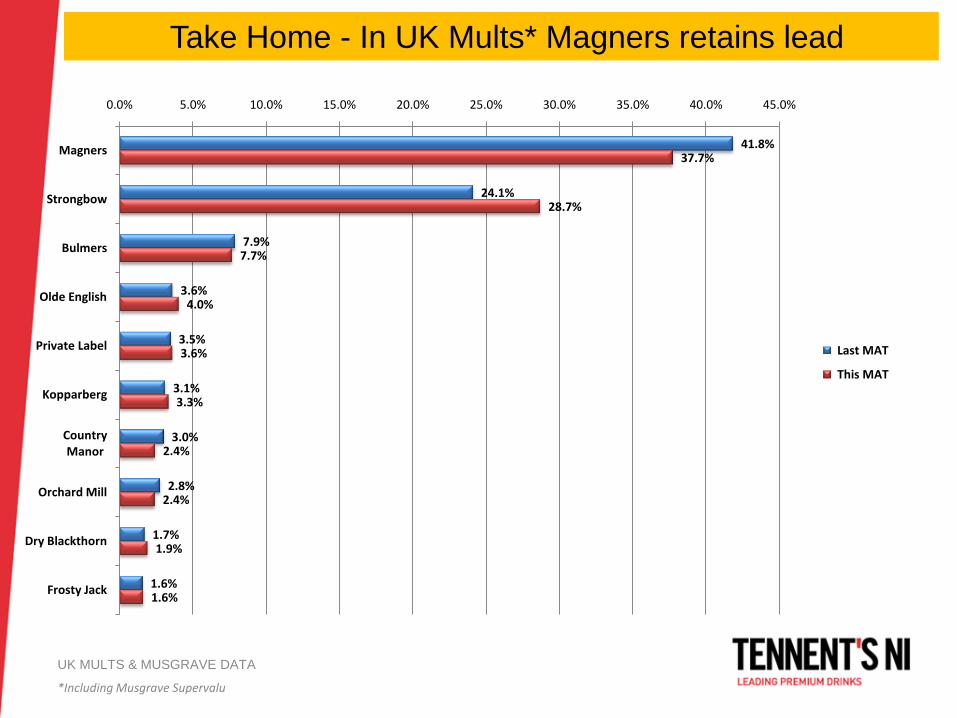

UK MULTS & MUSGRAVE DATA

UK MULTS & MUSGRAVE DATA

*Including Musgrave Supervalu

41.8%

24.1%

7.9%

3.6%

3.5%

3.1%

3.0%

2.8%

1.7%

1.6%

37.7%

28.7%

7.7%

4.0%

3.6%

3.3%

2.4%

2.4%

1.9%

1.6%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0% 30.0% 35.0% 40.0% 45.0%

Magners

Strongbow

Bulmers

Olde English

Private Label

Kopparberg

Country Manor

Orchard Mill

Dry Blackthorn

Frosty Jack

Last MAT

This MAT

Take Home - In UK Mults* Magners retains lead

UK MULTS & MUSGRAVE DATA

Including Musgrave Supervalu

20.8%

9.3%

14.0%

7.2%

5.1%

3.7%

5.3%

4.9%

2.9%

3.0%

22.7%

14.2%

11.6%

5.8%

4.5%

4.4%

4.2%

4.0%

3.5%

3.1%

0.0% 5.0% 10.0% 15.0% 20.0% 25.0%

Carlsberg

Budweiser

Tennents

Stella Artois

Magners

Coors Light

Harp

Miller

Strongbow

Carling

Last MAT

This MAT

Take Home -TNI has 4 of top ten LADs via UK Mults*

Summary

• Difficult market – making solid progress

• Great brand portfolio – fit for purpose

• Sustained brand support

• Loan investment and good loan book

• Excellent RTM – direct coverage of on trade

• Experienced and knowledgeable team

• Building momentum

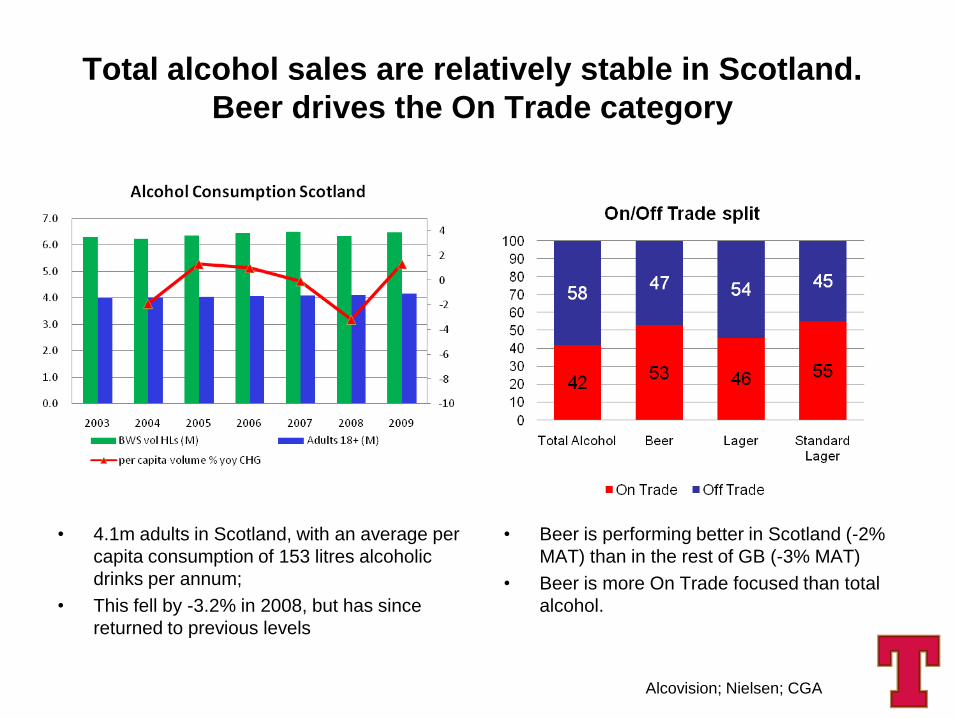

Total alcohol sales are relatively stable in Scotland.

Beer drives the On Trade category

• 4.1m adults in Scotland, with an average per

capita consumption of 153 litres alcoholic

drinks per annum;

• This fell by -3.2% in 2008, but has since

returned to previous levels

• Beer is performing better in Scotland (-2%

MAT) than in the rest of GB (-3% MAT)

• Beer is more On Trade focused than total

alcohol.

Alcovision; Nielsen; CGA

In the Off Trade, we have seen our share decline, as

we start to rebuild Tennent’s value

Nielsen Off Trade MAT 2.10.10

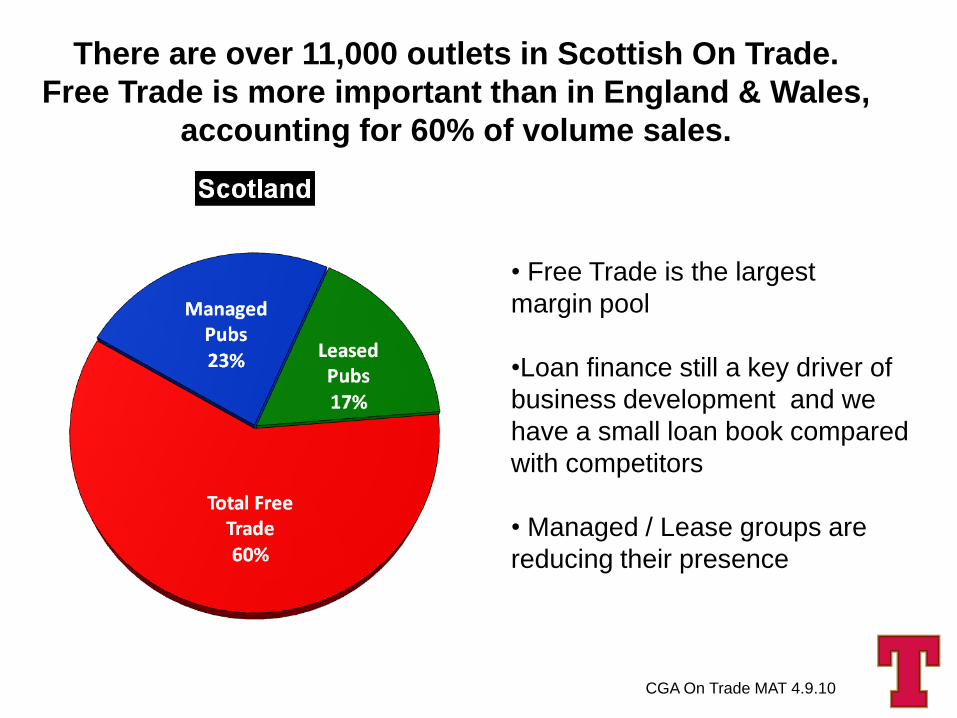

There are over 11,000 outlets in Scottish On Trade.

Free Trade is more important than in England & Wales,

accounting for 60% of volume sales.

CGA On Trade MAT 4.9.10

• Free Trade is the largest

margin pool

•Loan finance still a key driver of

business development and we

have a small loan book compared

with competitors

• Managed / Lease groups are

reducing their presence

Draught Standard

Lager47%

Draught Premium

Lager11%

Pkgd Lager

7%

Draught Ale25%

DraughtStout

9%

Pkgd Ale & Stout

1%

Scotland OnsBeer Volume Segmentation

Draught Standard Lager is the biggest segment in

the Scottish On Trade. Tennent’s is the leading

brand.

CGA On Trade MAT 4.9.10

Tennent’s is a local business

• Experienced direct sales force with market knowledge

• Long-standing trading history with wholesalers

• Links with independent outlets strengthened by a quality

loan book

• New Contact Centre

• New Credit Control / Finance Team

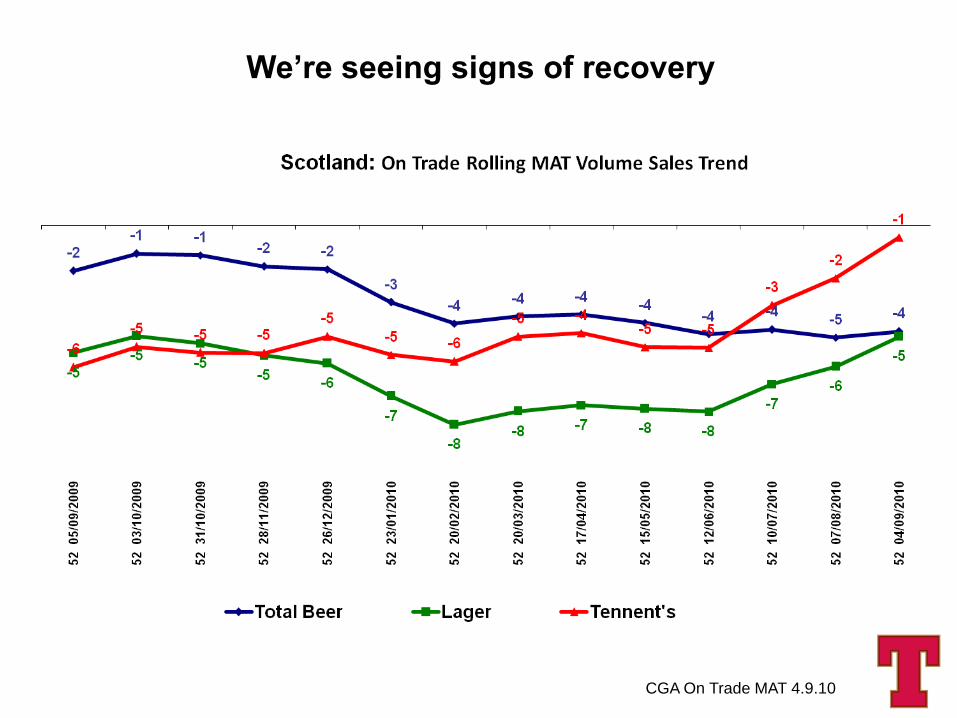

We’re seeing signs of recovery

CGA On Trade MAT 4.9.10

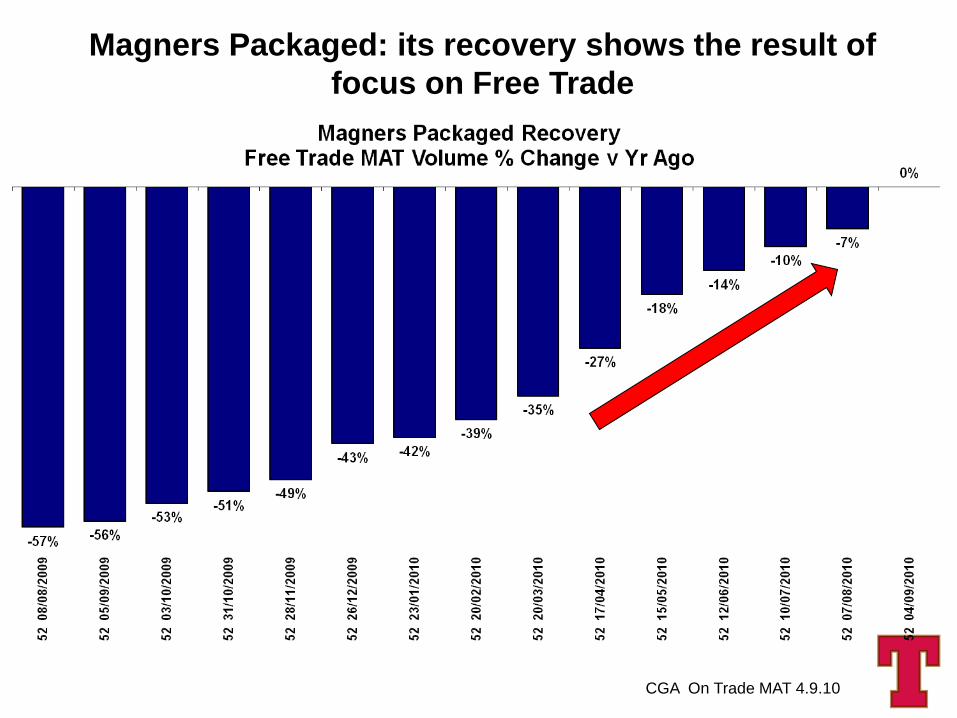

Magners Packaged: its recovery shows the result of

focus on Free Trade

CGA On Trade MAT 4.9.10

Mike Lees MD Scotland

Tom McCusker MD N Ireland