Rizwan Sultan Qazi

13

Rizwan Sultan Qazi

-

Upload

rizwan-s-qazi -

Category

Documents

-

view

123 -

download

1

Transcript of Rizwan Sultan Qazi

Rizwan Sultan Qazi

What has changed?

What’s the same?

The Product Life Cycle (PLC)

Building Your Loyalty Program ROI

Effective Customer Engagement Risk Management

Conclusion

Economy is not the only thing that has changed globally – Regulations have also..

Debit card is fast becoming payment instrument of choice Displacing cash and check For small ticket purchases

New generation of users more comfortable with debit &

appreciate “green” initiatives

Consumers taking more control of their money Increasingly aware of the cost of credit Have been focused on debt reduction

Card offers are becoming somewhat conservative Annual fees Interest rates Credit lines

Issuers are reducing credit limits and assigning lower limits at

point of approval

Penalty pricing is becoming harder to execute

Tougher risk management – no more border line approvals

Credit card remains highly profitable product within financial institutions

Issuers are attracting new clients with aggressive and different offers

Multi product clients tend to perform better across all

products – requires segmentation and smart offering

Loyalty programs and rewards schemes are becoming increasingly attractive and competitive

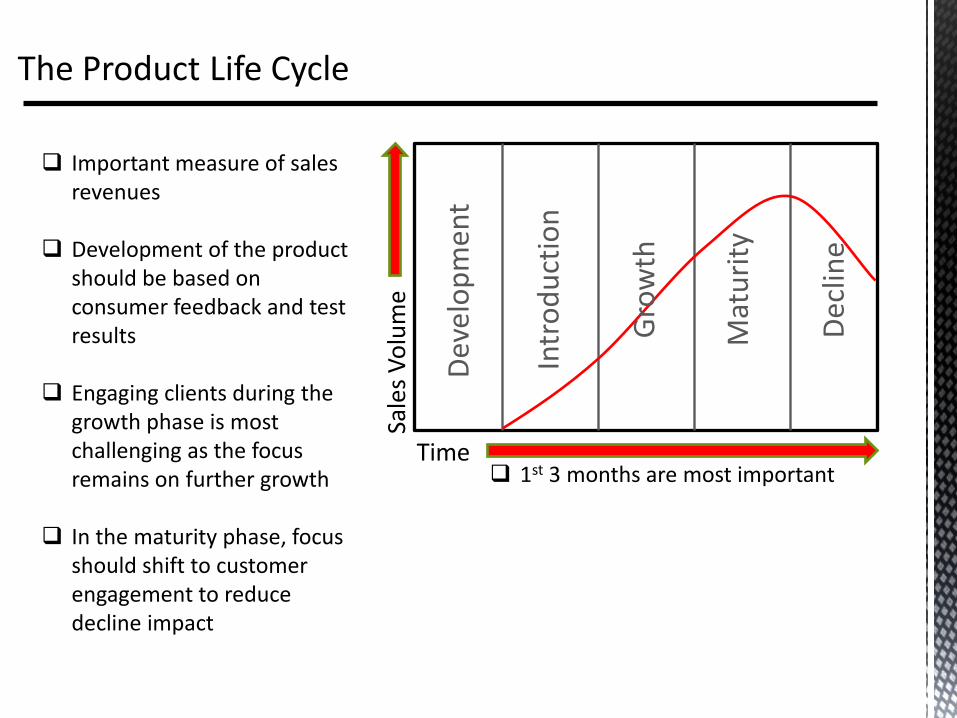

Important measure of sales revenues

Development of the product should be based on consumer feedback and test results

Engaging clients during the growth phase is most challenging as the focus remains on further growth

In the maturity phase, focus should shift to customer engagement to reduce decline impact

Dev

elo

pm

ent

Intr

od

uct

ion

Gro

wth

Mat

uri

ty

Dec

line

Time

Sale

s V

olu

me

1st 3 months are most important

Investment can be in: PEOPLE Technology and systems Marketing and advertising Product development and distribution channels

How to improve ROI:

Focus on PEOPLE – employees and customers fairly and equally Communicate often and with transparency and clarity Analyze date and create valuable information Do more segmentation and differentiate messaging using the insights

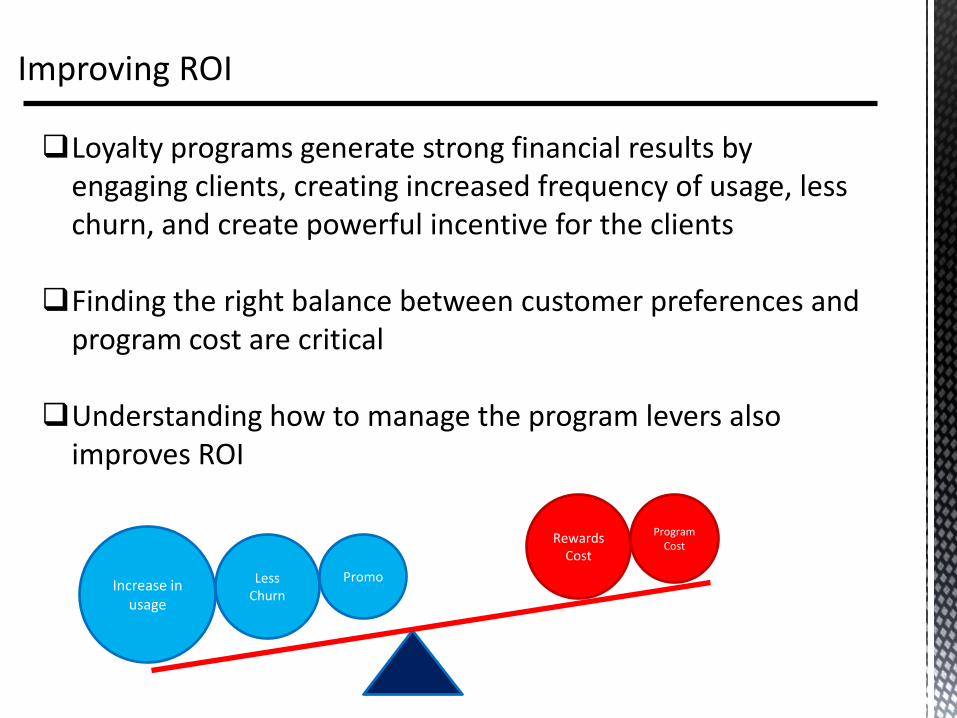

Loyalty programs generate strong financial results by engaging clients, creating increased frequency of usage, less churn, and create powerful incentive for the clients

Finding the right balance between customer preferences and

program cost are critical

Understanding how to manage the program levers also improves ROI

Increase in usage

Less Churn

Promo

Rewards Cost

Program Cost

From planning to launching a loyalty program and to manage it over time, it is important to know how the intersection of costs and revenues impact your bottom line

More flexible the program, more sustainable it is…

This allows more room to do more frequent promotions to

keep clients engaged

Communicate new features and updates in a timely fashion

Gather feedback on existing features

Upgrade and cross sell other products and services

Decrease churn or focus on retention

Better Risk Management is important to reduce impact to bottom line

Improve your Net Promoter Score

Does loyalty cannibalize usage?

How can we prevent cannibalization?

What is an acceptable ROI?

Better targeting, use of proxy information

Life cycle management to improve authorization approval rates, reduce fraud

Improve line management strategy to incentivize incremental usage

Manage delinquencies

“Your most unhappy customers are your greatest source of learning” – Bill Gates, Microsoft

“In business you get what you want by giving people what they want” – Alice MacDougal

“Customers don’t expect you to be perfect. They do expect you to fix things when they go wrong” – Donald Porter, BA

Manage delinquencies