Risks Ahead: Global Corporate Real Estate Trends 2013

18

Risks Ahead Global Corporate Real Estate Trends 2013

-

Upload

jll -

Category

Real Estate

-

view

1.016 -

download

1

Transcript of Risks Ahead: Global Corporate Real Estate Trends 2013

Risks Ahead Global Corporate Real Estate Trends 2013

Jones Lang LaSalle 3

Tod Lickerman Global Director and CEOCorporate Solutions, Americas

John Forrest Global Director and CEOCorporate Solutions, Asia Pacific

Vincent Lottefier Global Director and CEOCorporate Solutions, Europe, Middle East and Africa

However, we believe that with increased risk comes even greater reward. If the right decisions are taken, those who effectively manage the risks will be rewarded with the opportunity to drive productivity enhancements and corporate competitiveness.

We sincerely thank those of you who shared your thoughts and perspectives. Your input has provided a clear picture of the pressures facing CRE teams across the world. While the picture is clear, it is also complex as some geographies and industry sectors show high degrees of variation. Accordingly, we will issue additional reports focusing on country and industry level results over the remainder of the year, as well as pieces that dive deeper into the specific themes and issues raised in this global report.

To view these reports when they are released, and to explore the trends in more detail, visit www.jll.com/globalCREtrends.

IntroductionWe are delighted to introduce Jones Lang LaSalle’s second biennial report on global corporate real estate (CRE) trends, which provides powerful insights into the current condition and future direction of CRE.

More than 600 CRE executives from 39 countries contributed to this report through surveys and interviews. Their responses show that amid continuing challenges in the economic and operating environment, there are more risks ahead. CRE teams have been tasked with a broader and more strategic agenda since our first report was released in 2011. Five global trends have emerged, each with its associated risks.

Post the global financial crisis (GFC), the elevation of CRE has created a new tipping point. CRE must keep pace with the increasing speed and demands of the broader business or risk a return to the undervalued positioning of the past. This will require change in the mandate, structure, positioning and method of CRE.

4 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 5

Leadership pressure demands action at both tactical and strategic levels. CRE teams are being challenged to impact and add value to a wider range of agenda items.

A trend that has intensified since our 2011 report, the rising expectations of senior leaders require CRE teams to make a step change. This is challenging given the minimal investment in in-house CRE talent over the past few years. There is a scarcity of the right strategic skills to deliver clear workplace productivity outcomes and address the rising focus on worker productivity. When combined with resource constraints, the ability to fully deliver to this agenda is unrealistic.

Risk: Perceived underperformance if step change is not realizedWhat you can do: Be clear about your priorities. Leverage and partner with your supply chain and create capacity so that you can focus on managing internal stakeholders.

Extended and complex demands on in-house CRE teams are driving rapid growth in CRE outsourcing across more geographies, functions and corporations.

Those with CRE outsourcing experience continue to seek innovative delivery models that harness greater strategic contributions and deliver best practice—a trend that has gained significant momentum since 2011. Today, they are joined by a growing number of new corporations taking varied and sometimes innovative paths toward strategic outsourcing. Some are starting out with tactical out-tasking, while others are progressing quickly by following the paths taken by pioneers. The majority view outsourcing as a partnership, and more and more, are involving procurement in CRE decision making.

Risk: Undervaluing external contributionsWhat you can do: Take control of your supply chain. Proactively partner with your organization’s procurement team so that it has a better understanding of CRE and its potential contribution to corporate strategy. This will reduce the risk of undervaluing relationships with service partners or constraining their ability to deliver over the long term.

Embracing new work styles and implementing supportive new workplaces has been a strategic vision, if not immediate intention, for years. This is changing rapidly.

Workplace transformation is taking on a new resonance in developed countries as senior business leaders respond to an improving economic environment. The emphasis is on cost control, efficiency gains and productivity improvements. In emerging countries where strong growth is moderating, workplace transformation is gaining relevance and momentum. Globally, if backed with the required investment capital, it has the potential to influence the strategic contribution, financial impact and positioning of the CRE function.

Risk: Not investing enough to fulfill strategic potential What you can do: Don’t shy away from the strategic contribution CRE already makes. Embrace big data, analytics and performance tracking to demonstrate value. Be clear on what has and can be achieved. But, be clearer still on the investment needed to maximize the strategic contribution CRE can make, particularly in relation to the workplace and worker productivity.

A greater focus on workplace transformation calls for a cultural shift within the CRE team. CRE teams need to become adept at working across the organization and positioning themselves as agents and managers of change across shared services.

Collaboration between CRE, information technology (IT), human resources (HR) and finance is already occurring with surprising intensity on an ad hoc, project basis. In the future, collaboration—possibly driven by changes in organizational structures—will be necessary if true workplace value is to be realized. Partnering with these shared services must become a CRE core competency. This leadership opportunity has the potential to garner more influence and standing for CRE within the organization.

Risk: Losing influence and standing as a specialistWhat you can do: Take the lead. Use real estate and the workplace as the common ground for greater collaboration with functional areas such as IT, HR and finance. Engage with your support service counterparts to identify the intersections with CRE and clearly articulate their value.

The CRE function remains tasked to deliver operational platforms in select growth markets. These markets will be central to driving corporate competitiveness.

Senior business leaders will have high demands for speed and quality of delivery in emerging markets that lack transparency and are operationally challenging. Time and costs can escalate rapidly, while compromises around the quality of the real estate solution are inevitable. Delivery is a significant and often underestimated drain on the finite resources and skills of the CRE function. This can put the reputation of CRE across the wider business at risk unless carefully managed.

Risk: Damaging reputation through delivery failure What you can do: Don’t let emerging markets become CRE’s greatest reputational risk. Manage expectations and educate the business about the challenges of delivering real estate solutions in less transparent markets. Ensure this is clearly communicated early in the process.

Executive Summary

Five global trends are shaping the future of CRE

CRE teams face increasing pressure. When combined with a lack of investment or injections of new talent into these teams over recent years, this points to significant risks ahead. However, the many risks produced by the current business climate also present incredible opportunities for CRE teams. Those that proactively lead their organizations to a more productive workplace will be the winners. CRE teams are now uniquely positioned to dramatically impact the culture, collaboration and performance of their companies. This position requires a fundamental rethink of the CRE contribution—one that will shape not only the future form and function of the CRE team, but also its opportunity to add strategic value and deliver competitive advantage.

Expectations and pressures build, heightening the risk of underperformance

1 Increased demand is leading to faster-paced evolution of CRE outsourcing

2 Workplace transformation is the key to unlocking worker productivity and optimizing portfolios

3 CRE must become a collaborative change agent 4 Failure to deliver in

emerging markets will become one of CRE’s greatest reputational risks

5

54123

Jones Lang LaSalle 7

Expectations and pressures build, heightening the risk of underperformance

Global Trend 1:

• Reporting primarily to the C-suite—senior company executives such as the CEO, COO and CFO—has enabled CRE teams to strengthen the alignment between business and CRE strategy. However, economic realities and capital expenditure constraints have maintained pressure on CRE teams to implement short-term tactics, often to the detriment of longer-term strategic moves. This focus has been aimed at bolstering corporate financial performance through cost savings and/or capital release.

• Most CRE teams are finding it challenging to continue achieving year-on-year cost savings targets through tactical means, as most of the easier opportunities within portfolios have already been realized.

• A more strategic set of demands is therefore gaining significance, such as driving improved workplace and worker productivity. These fresh demands apply further pressure to CRE teams and expose structural flaws that jeopardize their future contribution and position.

• Corporate resistance to capital expenditure, the sometimes small and fragmented structure of the CRE function, inadequate access to deep data and analytics to measure value and a fundamental skill and knowledge gap within CRE teams all present barriers to meeting this rising demand.

• The future qualities perceived as most required by CRE teams suggest that these capacity caps and skill gaps will become even greater obstacles to their contribution and ultimate success.

6 Global Corporate Real Estate Survey 2013

Only 28% regard themselves as “well

equipped” to meet the various tactical and strategic demands now being placed

upon them

68% view demand from the C-suite and

senior leadership as being strongest for improving

the productivity of the real estate portfolio

72% experience high expectations to deliver clear productivity enhancements for the workplace and 61%

for the workforce

75% of respondents experience increasing demand from senior business leaders

to reduce direct real estate costs

More than 70% cite increasing tactical

demands in areas such as enhancing workplace

utilization rates and reducing operating

costs

48% view financial constraints as the greatest limitation on bringing more

strategic value to their business through CRE, with34% citing lack of effective data and analytics as the

biggest constraint

8 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 9

Today

Three yearsfrom now

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Moderately alignedEntirely aligned

Not aligned Not aware of any corporate goals

Minimally aligned

1%1%C-Suite

58%

Managerial

26%

Executive Operational Other

14%

Close to 60% of global CRE heads report directly into the C-suite (Fig 1), a relationship that has continued to develop since the onset of the GFC. This has ensured that the alignment between corporate strategy and CRE strategy has become, and will continue to be, strong (Fig 2).

Fifty-two percent of CRE executives describe corporate and CRE strategies as being “entirely aligned” today. This will increase to 72% in the next three years. This alignment enables real estate issues or opportunities to be flagged early in strategy development. It also speaks to the continued rise in importance of the CRE function.

Senior leadership continues to demand swift and decisive action to identify and secure cost savings. Expectations around the size of cost savings from real estate have been high and sustained. CRE teams are responding with a range of tactical real estate plays to generate cost savings (Fig 3). However, the challenge of continuing to deliver sizeable cost savings year-on-year through tactical initiatives is enormous. Much of the easier cost-saving opportunities within portfolios have already been taken.

For CRE teams, this is problematic because the inherent inflexibility of real estate portfolios, together with wider market forces, creates inertia and forces longer-term thinking.

Figure 3: Increasing tactical demands being placed on CRE

Figure 2: Alignment of CRE strategy to corporate strategy, today and three years from now

Figure 1: Reporting lines for the global head of CRE

QUESTION: How are the demands of senior leadership/C-suite on the CRE team changing in the following areas?Base: 545 respondents (those who responded that demands are increasing)

Hard-line reporting into the C-suite strengthens strategic alignment

Uncertain economic conditions mean that demand for short-term cost savings through tactical real estate initiatives is still a priority

75%74%73%64%63%57%49%28%

Reducing direct real estate costs

Increasing utilization of existing buildings in portfolio

Reducing the operational costs of the real estate portfolio

Challenging the business about its presumed space needs

Limiting exposure to future real estate costs

Getting clear on portfolio size/opportunities via data collection

Reducing the size of the portfolio

Running own vs. lease assessments

QUESTION: To what level of the organization does the global head of CRE currently report?Base: 470 respondentsNote: C-suite refers to senior company executives such as the CEO, COO and CFO; managerial level includes presidents, vice presidents, managers; executive level includes officers, supervisory roles; operational level includes administrators, personal assistants and clerks.

QUESTION: To what extent is your CRE strategy aligned to your company’s broader business strategies/corporate goals?Base: 545 respondents

10 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 11

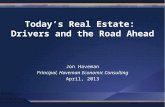

Global

Americas

Asia Pacific

Well equipped to meet all demands

28%37%21%25%

Can meet most demands

65%58%67%69%Europe, Middle East

and Africa

Ill equipped to meet the demands

7%5%12%6%

Figure 4: Increasing strategic demands being placed on CRE

Figure 5: Company expectations of productivity outcomes from CRE

Figure 6: CRE leaders’ ability to meet new demands

QUESTION: How well equipped do you feel to meet the demands listed in Figs 3 and 4?Base: 545 respondents

Greater engagement with the C-suite and more alignment between business and CRE strategy has led to an uncomfortably broad range of demands now being placed on CRE professionals. The result is that only just over a quarter of CRE executives believe that they are “well equipped” to address such demands (Fig 6). The maturity of CRE outsourcing in the Americas is reflected in the nearly 40% of CRE executives located here that feel “well equipped”, while in other parts of the world the perceived ability to rise to the challenge is limited.

Productivity improvement is the standout strategic priority and leads the demands being placed on CRE teams

A small proportion of CRE leaders feel “well equipped” to meet the varying demands being placed upon them

Reporting to the C-suite brings with it enormous scrutiny over the cost, structure and utilization of the real estate portfolio as senior leaders demand a more strategic approach from CRE teams (Fig 4). Their demands seek to provoke a transformation within portfolios, most notably to support enhanced levels of workplace and worker productivity. Expectations around delivering improvements in productivity are on the rise across the board (Fig 5). While workplace productivity improvement was featured in our 2011 report as an emerging trend for best-in-class workplace strategy, it is now a “high expectation”. It is also taking CRE beyond the workplace to encompass people, business and asset productivity.

QUESTION: What productivity outcomes is your company expecting the CRE function to deliver?Base: 545 respondents (those who responded that expectations to deliver in these areas are “high”)

QUESTION: How are the demands of senior leadership/C-suite on the CRE team changing in the following areas?Base: 545 respondents (those who responded that demands are increasing)

68%65%65%56%55%54%53%46%46%

Enhancing productivity of the real estate portfolio

Transforming the quality of the workplace

Presenting scenarios and solutions to the business

Bringing more flexibility to the portfolio

Enabling remote or mobile working

Driving the sustainability agenda

Aligning CRE with business drivers and functional areas

Delivering a platform for growth in select markets

Attracting and retaining talent

Workplaceproductivity

72%

Peopleproductivity

61%

Businessproductivity

57%

Assetproductivity

47%

12 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 13

Figure 7: Major constraints hindering CRE from enhancing its strategic position

Figure 8: The key requirements of CRE teams

QUESTION: In your opinion, what are the top two constraints that are hindering CRE from enhancing itself as a strategic value add to your organization?Base: 545 respondents

Structural and financial constraints present a significant risk to addressing leadership demands

While few position themselves as being “ill equipped” for the challenges ahead, it is clear that new skills and greater capacity will be required if CRE is to tackle such a broad and challenging agenda. The existing structure and skills of CRE teams will constrain CRE from enhancing its strategic position, as recognized by around a quarter of CRE executives (Fig 7).

However, the primary constraint identified is financial. This may be considered a refreshing change from the top constraint in our 2011 report, which was “uncertainty around the future shape and size of the business”. The focus has now shifted to more internal obstacles. The lack of budget ownership, which often sits with another function, market or business line, can be considered an aggravating factor.

Almost half of CRE executives recognize that broader strategic agendas cannot be fully met without some investment and one third feel restricted by the lack of effective data and analytics to measure value. By comparison, financial constraints are of little concern in Japan (4%), but having a fragmented team comes in as the top constraint (50%) reflecting the CRE organizational immaturity in that country.

The future required attributes of the CRE team are not well served by current structures and the risk of CRE underperformance is high

The qualities required by CRE teams (Fig 8) suggest that the capacity caps and skill gaps afflicting CRE teams will be even greater impediments to the contribution and ultimate success of CRE teams in the future. Of the nine attributes that are important to a CRE organization, only one represents a real estate specific skill set (“Presenting real estate options and scenarios”). The remaining key requirements are much more focused on broader business skills. This will need to be addressed through a combination of investment and fundamental rethinking of the form and function of the CRE team. Without both, the risk of CRE teams failing to meet senior leadership expectations remains high.

QUESTION: Rank the importance of the following CRE attributes to your organization.Base: 545 respondentsNote: In this table, responses include the top-ranked attribute only. Totals may not equal 100% due to rounding.

26%

48%

Financialconstraints

34%

Data and analytics

32%

C-suitecommitment

27%

Fragmentedteam

Skill and knowledge

22%20%17%12%8%8%5%4%3%

Forward thinking/Challenging status quo

Presenting real estate options and scenarios

Business acumen/Understanding of broader business

Providing data and insights

Focused on innovation

Efficient stakeholder management outside CRE

Improving the internal reputation of CRE

Improving CRE team communication/Relationship skills

Adding new skills (e.g. change management, financial acumen, etc.)

14 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 15

• Amplified by the emergence of a broader strategic CRE agenda, capacity caps and skill gaps within many in-house CRE teams have in turn fuelled growth in the CRE outsourcing market. Gaining momentum since 2011, this tendency will continue over the next three years, and is now moving at a much faster pace.

• CRE outsourcing is gaining traction across more geographies, industry sectors and corporations. Only 8% of companies have not outsourced any aspect of their CRE function, a big drop from 24% in 2011. This indicates that CRE outsourcing is quickly catching up to other outsourced functions—such as IT, HR and finance—that are seen to be further along the outsourcing curve.

• Most companies firmly view outsourcing as a long-term, strategic relationship seeking to add value rather than a price-driven, tactical transaction. This holds true regardless of whether or not they are currently heavily outsourcing CRE service delivery. These companies use outsourcing to draw upon expertise and skill sets not available within their own organizations and release internal capacity to focus on addressing strategic pressures.

• This strategic viewpoint is important, given the increasing role that procurement plays in the CRE buying decision. There is a perception that procurement teams lack understanding of the characteristics of CRE services, and a growing risk that these qualities will be overlooked in a price-driven procurement process.

• Procurement involvement may hinder the strategic influence of CRE teams. As such, there is an urgent need for the CRE community to educate and clearly articulate its value proposition.

Increased demand is leading to faster-paced evolution of CRE outsourcing

Global Trend 2:

Lease administration as well as energy and sustainability services are forecast to see the greatest reduction in

full in-house delivery, both decreasing by

11%

of those identifying active

procurement participation

believe that procurement

has limited knowledge of

what it takes to secure CRE

services

58%

of respondents view CRE

outsourcing as an entirely

strategic relationship,

while 6% see it as a

purely tactical transaction

30%

have retained project management, build-out and design in-house—the lowest

level of any service type—although just 18%

have fully outsourced these services

12%

increase in full outsourcing is expected for both portfolio and facilities management and lease administration services—the highest

predicted increase in full outsourcing over the next three years

A 9%

have retained portfolio

strategy work in-house and

only 3% have placed this

service in a fully outsourced

delivery model

52% have procurement teams actively involved in CRE decision making; 36% cite permanent involvement

69%

over the next three years

8%do not currently outsource

any CRE services. In Asia Pacific, this rises to

12%. In both cases, this is very low compared to 2011

at 24%

16 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 17

9% 21% 33%Outsourcing

represents a tactical transaction, mainly with the lowest-cost

supplier

6%

Outsourcing represents a strategic relationship, where I assess longer-term

value add with a partner

30%

15%22% 27% 15%21%14%18% 22% 23%23%

15%34% 18% 18%16%12%26% 20% 23%19%

19%28% 24% 11%17%13%17% 29% 18%23%

18%12% 30% 18%14%11% 26% 22%28%

22%

17%25% 25% 13%19%14%21% 22% 22%21%

22%52% 15% 3%8%19%44% 20% 5%11%

Energy and sustainability services

Lease administration12%42% 14% 19%13%

11%31% 12% 28%19%

Transaction services

Project management/Build-out/Design

Portfolio and facilities management

Portfolio strategy

Property management

Today

Three years from now

Fully outsourced43Fully-in-house 2

Ninety-two percent of companies are practicing some form of real estate outsourcing. The extent differs between regions, with a greater number of firms headquartered in the United States and Australia showing the most maturity. Globally, only 8% are delivering all real estate services fully in-house, a significant decrease from 24% in 2011.

The balance of services performed in-house or through outsourced models is changing (Fig 9). Specialist and resource-intensive services remain most likely to be outsourced, with project management overtaking transaction services as the most frequently outsourced function since 2011. The majority still prefer to retain sensitive elements such as portfolio strategy in-house. Over the next three years, there will be further advancement along the outsourcing continuum as CRE teams seek more support from the market in delivering tactical and strategic real estate activities.

Figure 9: Outsourcing activity by service line, today and three years from now

Figure 10: Current attitudes toward CRE outsourcing

A large majority of CRE executives maintain that outsourcing represents a strategic relationship where partnership value is assessed over the long term, as opposed to a minority who see it as a tactical transaction mainly with the lowest-cost supplier (Fig 10). A growing number of corporations are looking beyond tactical out-tasking and are seeking to capitalize on the greater value and synergy that comes from deeper, strategic partnerships. Only a minority of corporations do not use or want to use key performance indicators (KPIs). Many are starting to push some of the financial and operational risks to external partners and we are seeing an evolution toward risk-sharing contracts in some cases.

CRE outsourcing is developing rapidly across geographies, industries and a broader range of services. Solutions are being sought, creating new models, new interrelationships and new points of engagement

CRE executives see outsourcing as a strategic imperative with value derived from long-term partnership and the development of shared goals

QUESTION: How would you best describe the delivery of the following CRE services, today and three years from now?Base: 519 respondents (companies that practice outsourcing)Note: Totals may not equal 100% due to rounding.

Figure 11: The role of procurement in CRE

The active involvement of procurement in the CRE outsourcing decision creates risks of undervaluing partnerships and failure to deliver needed step change

Procurement is a business function with increasingly strong links to CRE. Thirty-six percent of CRE executives describe procurement as being actively involved in CRE “on a permanent basis” (Fig 11). This proportion becomes higher (47%) for the largest companies in our sample with global headcounts of more than 100,000. Even for the 33% who report involvement “on an ad hoc basis”, the trend toward greater integration of procurement and CRE is clear.

There is a lot that CRE executives can learn from procurement, not least in terms of processes and vendor management. However, there are signs that this can be an unhappy marriage in some cases. Fifty-eight percent report that procurement has a limited knowledge of real estate and the nature and complexity of the services being procured. There is a responsibility for CRE teams, and indeed service partners, to more effectively educate procurement and articulate the added value that effective CRE management can deliver. The risk of not doing so is that outsourced models will become price-oriented rather than value-driven, and desired capacity expansion and innovation delivery will not be realized.

QUESTION: Please rate your current attitudes toward outsourcing on a scale of 1–5. Base: 519 respondents (companies that practice outsourcing)Note: Totals may not equal 100% due to rounding.

QUESTION: Is your internal procurement team actively involved in CRE?Base: 545 respondents; 373 respondents with procurement involved

36% Involvement on a permanent basis

42% Knowledgeable about CRE

33% Involvement on an ad hoc basis

58% Limited knowledge of CRE

We hire external procurement consultants

3%

No involvement of procurement23%

3% No internal procurement team

Other2%

18 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 19

However, up to

point to no change in the quantity, quality, utilization or density of the workplace over the last three years

27%have already overseen a reduction in the size of their real estate portfolio over the last three years

31%maintain that the quality

of their workplace has

improved during the last

three years, with 68%

suggesting that space

utilization has also increased

67%

• CRE teams have, where market forces and tenure allow, already reduced the size of the occupied portfolio while simultaneously increasing the quality, occupation density and utilization rate of the space. While this is encouraging in the context of productivity, there is growing pressure from senior management for more to be done to unlock the productivity of workers.

• The standout limitation in driving workplace transformation and the creation of more productive spaces is a financial one. The lack of investment capital available to underpin transformation programs is a far more significant constraint than the cultural and managerial resistance seen as the top restraints in our 2011 report.

• This represents a tremendous risk to CRE teams. While team structures and outsourced relationships can be shaped to accommodate a strategic agenda, real progress will always be stifled without investment capital.

• Occupancy planning data, a cornerstone of workplace strategy and planning, is the most desired planning tool to enhance future CRE performance.

identify occupancy planning data as the most desired

technological tool needed to

enhance CRE performance

46%

Workplace transformation is the key to unlocking worker productivity and optimizing portfolios

Global Trend 3:

• We have seen how the new and extended CRE agenda shines the spotlight on organizational productivity. Workplace is a key driver of that agenda and represents a unique opportunity for the CRE function—if appropriately structured, resourced and focused—to make a strategic, business-wide contribution.

regard the lack of investment capital as the key constraint to workplace transformation,

followed by 15% who cite difficulty in changing management styles to

support workplace change as the biggest barrier

22%believe that space utilization will increase further over the next three years, with only 42% believing that the real estate portfolio will increase in size over this period

79%

20 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 21

There is no doubt that CRE portfolios have undergone a process of transformation over the past three years (Fig 12). Ongoing pressure on operating costs has led more than two thirds of CRE executives to increase the utilization rate of space on a global basis.

The quality of space has also been a focus, with two thirds of CRE executives pointing to improvements in the space occupied from either a design or environmental point of view. Occupational densities have increased as well, with 62% noting an increase in the ratio of headcount to unit of space.

The transformative pressures that have been felt by CRE will only intensify over the next three years (Fig 12). CRE teams will be faced with the challenge of further increasing densities and utilization rates without negatively impacting quality or worker experience. This suggests that demand will increasingly be for modern, flexible, densely occupied space of a high quality, which supports creative and collaborative work and enables talent attraction and retention.

Figure 12: The extent of workplace transformation over the last three years and envisaged over the next three years

Figure 14: Technological tools most desired to achieve future vision

Figure 13: Constraints in delivering workplace transformation

The standout limitation in driving workplace transformation and the creation of more productive spaces is recognized as a financial one (Fig 13). The lack of investment capital available to underpin workplace transformation is a far more significant constraint than the cultural and managerial resistance that has often been highlighted in accounts of workplace programs and also seen in our 2011 report.

This is not to underplay the impact of these softer, people issues. Rather, it is to note that presently, the constraint being placed on capital investment is most powerfully impacting the workplace transformation agenda. This leads to a tremendous risk because without investment capital, any real progress will always be stifled. CRE teams must make a stronger case for further investment if the productivity agenda is to be fulfilled.

Workplace productivity is being addressed through CRE, but there is recognition that more could and should be done

Numerous constraints have limited the scope of workplace transformation to date, but key among these has been the lack of investment capital and occupancy planning data

It is clear that some key technological tools need to be in place to support workplace planning. Forty-six percent of CRE executives need occupancy planning tools to help them deliver to a higher level in the future (Fig 14). Occupancy planning is core to the delivery of any workplace solution and also in measuring productivity gains. A lack of adequate technological tools has been identified and key industry players are working toward developing more comprehensive solutions.

46%33%33%31%26%

Occupancy planning data

Portfolio dashboards

Financial modeling

Rental benchmarking

Lease management

QUESTION: In your organization, what is the single most limiting factor in driving workplace transformation?Base: 545 respondentsNote: Table excludes “Others” (6%) and “None” (4%). Totals may not equal 100% due to rounding.

QUESTION: What technological tools would most enhance your performance as a CRE professional?Base: 536 respondentsNotes: In this table, responses include the top-ranked attribute only. Less desired tools are “retail network planning”, “electronic documents” and “other” choices.

QUESTION: To what extent has your global corporate workplace transformed over the last three years/will transform over the next three years in terms of quantity, quality, utilization and density?Base: 545 respondents

22%15%14%10%7%7%7%5%2%

Lack of investment capital

Difficulty in changing management styles

Employee resistance

Lack of management engagement

Lack of sustained C-suite sponsorship

Lack of opportunity through real estate tactics

Complexity arising from cultural diversity

Difficulty in building a compelling business case

Technology deficiencies

Incr

ease

dDe

crea

sed

The last three years Next three years

Quantity Quality Utilization Density

48%

31%

42%

36%

67%73% 68%

79%

62%72%

6% 4%12%

7%15%

9%

22 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 23

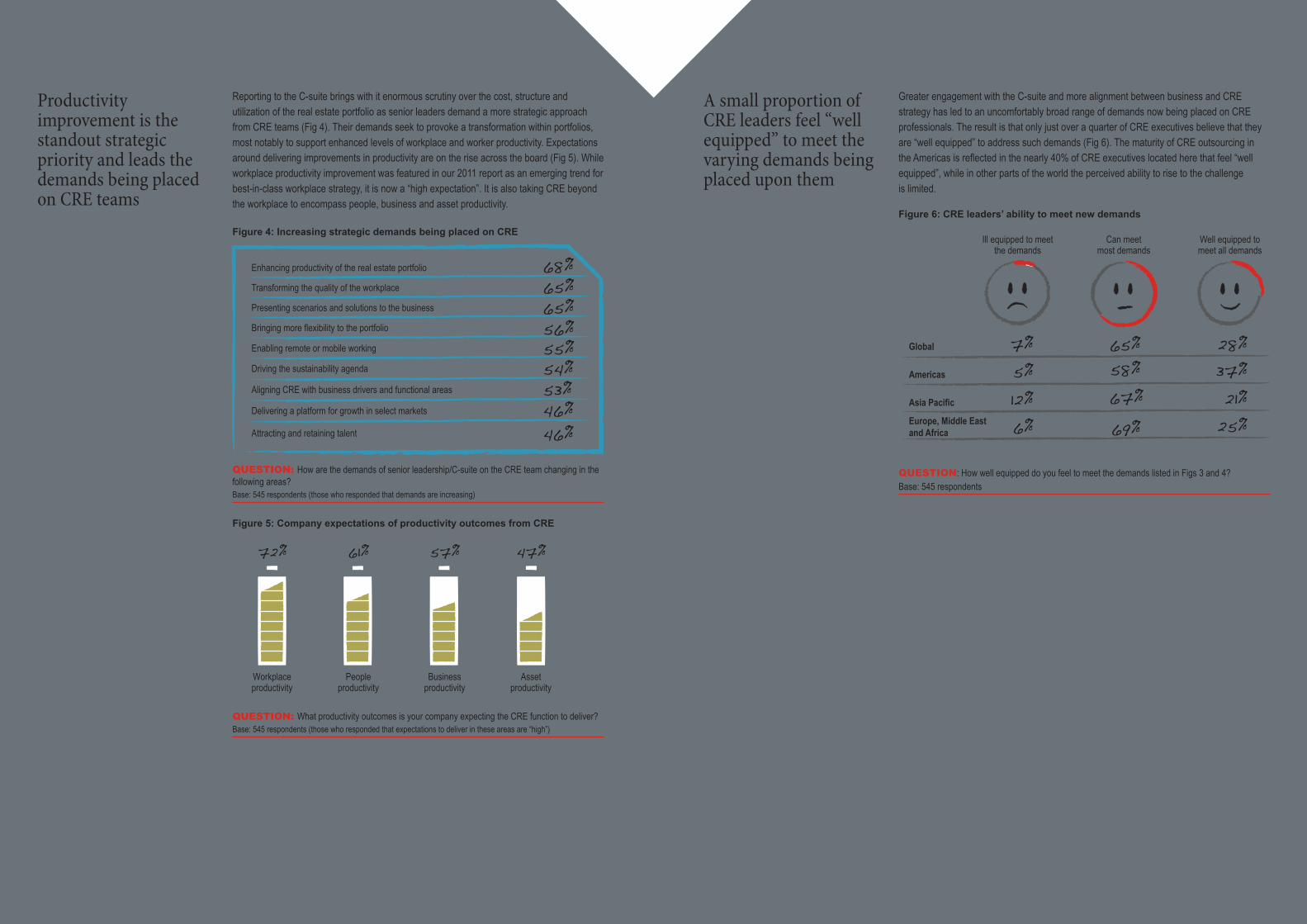

• Advancing a more challenging strategic agenda—one that focuses specifically on workplace and worker productivity—requires closer association with other corporate support functions.

• IT, HR, finance and CRE are already collaborating in the pursuit of current workplace strategies. For the majority, this remains an ad hoc, project-based activity. However, this collaboration is happening much faster than previous industry predictions.

• The formation of collaborative organizational structures, such as shared services, is likely to increase over the next three years. This presents a leadership opportunity for CRE teams to really drive the adoption of strategies that enhance workplace and worker productivity.

• CRE teams can take a strong leadership role in these structures and become company-wide change agents. This will extend the relevance and impact of CRE.

CRE must become a collaborative change agent Global Trend 4:

identify with the model of shared services integration between CRE and

finance; collaboration with HR, IT and finance functions is forecast to shift to

an integrated shared services model over the next three years

51%

45%are collaborating with the IT

function within their organization on an ad hoc or project basis, with almost one third pointing to more formalized collaboration or shared

services integration

14%

39%of respondents reside within a

dedicated CRE department

report that their organization has no global head of CRE,

pointing to decentralized and fragmented CRE

structures for some

8% have the CRE function contained within an administrative or

shared services group

24 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 25

The next wave of collaboration will be crucial to CRE success and is leading to structural change

Increased and potentially formally structured collaboration between support services could represent a new elevation opportunity for CRE

As the workplace productivity agenda takes hold over the next three years and programs of transformation are financed and pursued, more formal collaboration structures will be required. This could see CRE being absorbed into an administration or shared services structure (Fig 17). It will force alignment between functional teams and, in turn, lead to further alignment with broader business strategies and goals. This means a core skill for CRE executives going forward will be to actively collaborate with HR, IT and finance. This integration is expected to increase significantly across all three disciplines, with HR the frontrunner at a staggering 67% increase over the next three years.

It is natural for CRE professionals to be anxious about the development of shared services models over the medium term, but they do present opportunities. Rather than being perceived as a threat to influence or specialization, CRE teams should embrace these formal collaboration structures as vehicles for delivering positive change across their organization. We believe CRE teams should be taking a strong leadership role in these new configurations to establish creative and productive workplaces. Adopting the position of company-wide workplace change agent (rather than a tactical specialist) will extend the relevance of CRE and mitigate any risk of becoming marginalized.

Figure 17: Level of shared services integration, today and three years from now

QUESTION: How would you describe the collaboration of CRE with the following business functions today and in three years’ time?Base: 545 respondents

QUESTION: Within what department does the global head of CRE reside?Base: 545 respondentsNote: Table excludes “Others (7%). Totals may not equal 100% due to rounding.

Almost 40% of respondents globally have a dedicated CRE department in which a global head of CRE resides (Fig 15). This is more common as the size of the company increases. Forty-nine percent of the largest companies within our sample—those with a global headcount exceeding 100,000—have a dedicated CRE department.

As senior business leaders demand a more strategic CRE agenda, notably around the issues of workplace productivity, CRE teams are being required to exert influence over a broader range of corporate functions. The work that CRE teams will undertake going forward impacts everyone within the organization, all of the time. Collaboration with other support functions will become just as necessary as a strong relationship with leadership if transformation is to be achieved. This will be most required with those support functions that have a vested interest or contribution to make to the productivity agenda—notably HR, IT and finance.

For most, CRE represents a dedicated function within the organization Figure 15: Department within which the global head of CRE resides

Workplace transformation demands greater collaboration with other corporate functions

CRE has a track record of collaboration, but this is primarily ad hoc and project-focused

Collaboration between support functions is already in evidence in the pursuit of current CRE strategies (Fig 16), although for the majority, this remains an ad hoc, project-based and temporary relationship. CRE executives recognize that collaboration occurs regularly between the heads of these departments at a slightly more strategic level. On average, across the three support functions, 15% identify collaboration at the functional head level.

Figure 16: Level of ad hoc collaboration, today and three years from now

QUESTION: How would you describe the collaboration of CRE with the following business functions today and in three years’ time?Base: 545 respondentsNote: In this table, percentages combine top-ranked “ad hoc” and “project-based” collaboration responses.

39%15%10%8%2%2%1%1%14%

Dedicated CRE department

Corporate office/General management

Finance

Administration/Shared services

Procurement

Human resources

Supply chain and logistics

No global head of CRE

Information technology

Today Three years from now

HR

IT

Finance

41%30%

45%34%

31%26%

Today Three years from now

Change

HR 67%44%26%

IT 48%46%31%

Finance 18%60%51%

26 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 27

• The dual emphasis on building operational platforms in emerging growth markets and right-sizing portfolios in mature or developed markets, identified in our 2011 report, continues.

• Portfolio sizes in developed western economies will flat-line or reduce in volume, with more companies anticipating a decrease in portfolio size than those anticipating an increase.

• Portfolio growth will be strongest in the world’s emerging economies, which also tend to be the least transparent real estate markets. Operating in these opaque environments represents a potential reputational risk to CRE over the next three years.

Failure to deliver in emerging markets will become CRE’s greatest reputational risk

Global Trend 5:

• There is a real danger that the pursuit of growth and need for competitive advantage in emerging markets will lead to unrealistic demands being placed on CRE teams.

• The task of delivering new operational platforms in emerging markets has been underestimated by CRE leaders. Platform building in emerging markets can rapidly erode CRE team capacity and divert resources from meeting their broad and extended agenda. Managing expectations and educating senior leadership will be crucial.

Respondents are very bullish about expected

portfolio growth in Latin America;

of respondents see

delivering a platform for

growth in select markets

as an increasing strategic

demand imposed on CRE

teams by senior leaders

46%

Emerging countries continue to receive a lot of attention

with 44%

China

19%identify lack of transparency within real estate markets as the single greatest challenge

when expanding into emerging markets

state that they will dedicate no more than 50% of their time (or none at all) to emerging markets; 34% anticipate spending no more than one day per week on these markets

62%

see the lack of suitable real estate offer as their greatest challenge. This was greater among respondents in Asia

(14%)

10%

of respondents anticipating net portfolio growth in

31%Brazil

over the next three years, 38% in India, 20% in Russia,

12% in Turkey and 8% in South Africa

expect growth in

and 16% in Mexico, while net portfolio growth is back from decreasing to stable (1%) in the United States

The majority are anticipating portfolio reduction in most European markets,

in France-15%

and -12% in the United Kingdom, while the drop is more moderate in Germany (-5%) and in the Nordic countries (-14%)

28 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 29

2013-20162009-20129.27.6

2.5

2.72.0

0.8-0.3

3.3

0.70.10.1

8.37.2

2.9

4.23.5

2.71.7

4.8

1.41.40.8

China

India

Africa

Brazil

Global

Australia

United States

United Kingdom

Germany

Japan

France

Figure 18: Global GDP Growth Rates 2013-2016 vs. 2009-2012 (% growth per annum)

Companies’ intentions with respect to portfolio growth are polarized, with relatively strong growth anticipated in emerging markets and anemic growth in the developed world. These intentions are very much in line with GDP growth projections (Fig 18).

Source: IHS Global Insight, 2013

Subdued global economic growth rates are forcing corporations to address portfolio sizes in developed economies

While portfolio sizes are set to increase marginally in the United States, overall portfolio sizes in Western Europe will reduce over the next three years (Map 1). This will prolong the trend toward higher vacancy rates in developed real estate markets, which have edged upward as a result of space rationalization and consolidation. In line with the emphasis on productivity outlined in this report, corporations have reduced portfolio size in developed markets by improving utilization rates, increasing occupational densities and optimizing portfolios across markets.

There is significant opportunity in the current global economic climate to generate competitive advantage by creating new or enhanced operating platforms in emerging markets. Emerging economies continue to be in focus with the percentage of CRE executives anticipating portfolio growth in such markets being consistently high (Map 1), continuing the trend identified in our 2011 report. A key difference is the emergence of Africa as a focus for growth, with 8.5% predicting growth in South African portfolios, for example.

This trend aligns with our finding that 46% of CRE executives cite the delivery of operating platforms for growth in select markets as an increasing strategic demand from senior business leaders (refer back to Fig 4). It is also consistent with the fact that just under a third of CRE executives believe that their organization has become less risk averse over the last three years. This reduced risk aversion is particularly marked in the Americas and shapes attitudes toward emerging markets, specifically Mexico and Brazil.

But selective growth opportunities will continue to be actively pursued in emerging markets

Map 1: Net portfolio growth anticipated over the next three years

Map 2: Global real estate transparency 2012

Source: Global Real Estate Transparency Index, Jones Lang LaSalle, 2012

30% + Net Portfolio Growth

Negative Net Portfolio Growth (20%-10%)

Rest of region

Negative Net Portfolio Growth (10%-1%)

Stability (0% Net Growth)

1%-10% Net Portfolio Growth

11%-30% Net Portfolio Growth

Country

Not covered

Highly Transparent

Transparent

Semi-Transparent

Low Transparency

Opaque

QUESTION: Over the next three years, how will your portfolio evolve in each of the following regions?Note: Net portfolio growth percentages in this map are obtained by deducting responses anticipating portfolios to decrease from responses anticipating portfolios to increase. Other possible responses (“remain the same”, “do not know” and “not applicable”) were left out.

Jones Lang LaSalle 31

Figure 20: Time likely to be spent by CRE on emerging markets over the next three years

Delivering real estate solutions in emerging markets presents a significant reputational risk for CRE

The time and cost implications of delivering real estate solutions in many of these select growth markets are considerable. This is not typically the concern of senior leaders, but without effective management of stakeholder expectations, the status of the CRE team could be threatened. The possibility of not meeting the expectations of senior management is high and delivery failure can damage the reputation and standing of the team.

This risk is intensified by the fact that few CRE teams seem to be planning to dedicate much time to this strategic priority. Only 19% are likely to spend more than half of their time on delivering in emerging markets (Fig 20). There is a sense that the size of the task and its complexity may be underestimated and this may place even more pressure on current team capacity and skills, further undermining the ability of the CRE team to deliver on its broadening agenda.

QUESTION: How much of your time as a CRE professional is likely to be focused on developing/emerging markets over the next three years?Base: 545 respondents

19%34%28%14%5%

None

Minimal (up to 20%)

Moderate (20%-50%)

Majority (50%-80%)

Major (>80%)

Many of the target markets for growth will present substantial transparency and potential delivery challenges

While establishing operating platforms in new markets is a strategic imperative, delivery is also a tactical demand, which in this context is particularly challenging due to market opacity. The transparency issue is well recognized, with 19% specifically identifying real estate market transparency as the issue (Fig 19).

Figure 19: Perceived challenges of platform delivery in emerging markets

QUESTION: In your opinion, which of the following is the single greatest challenge when expanding into developing/emerging markets?Base: 545 respondents

19%18%17%10%7%7%8%14%

Real estate market transparency

Political transparency

Economic transparency

Lack of suitable real estate offer

Lack of unified real estate standards

Start-up costs

Others

None

It is revealing to compare Map 1 with Map 2 drawn from Jones Lang LaSalle’s 2012 Global Real Estate Transparency Index, which shows the levels of market transparency around the world. There is a clear correlation between markets that have high portfolio growth and markets that have low levels of transparency.

In practical terms, opaque markets equate to a slower speed to market, higher barriers to market entry and costs and complexity around the routes to market entry. It is echoed by the fact that some CRE executives point to the limited real estate offering or absence of standard market practices within emerging markets as challenges. CRE teams need to enable the pursuit of growth, but the wider business may be ill-informed about the practicalities of expanding within an opaque, emerging market.

32 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 33

This report summarizes the global aggregated findings of Jones Lang LaSalle’s second Global Corporate Real Estate Survey. The research collection phase was concluded in December 2012.

The response to the Survey was unprecedented. Through a combination of online and telephone fieldwork, we received 636 survey responses from CRE executives spread across 39 countries. This represents a 24% increase in respondents from our 2011 survey and illustrates both the growing maturity of CRE, as well as the importance placed upon the future of the industry.

The respondent pool also reflects a broad cross section of the corporate community. Our base sample, as used within this report, covers 545 companies, each employing more than 1,000 people worldwide.

As evident from the figures herein, our survey responses were well balanced and reflective of the views of CRE leaders drawn from a diverse range of sectors, domicile and operational locations, as well as companies of varied size.

Jones Lang LaSalle was supported by market survey experts Kadence International in collecting, compiling and segmenting the research data.

Responses by region where respondents are based (companies above 1,000 employees only)

Responses by industry sector

About the Survey

Asia Pacific 155 Europe, Middle East and Africa

216

Americas174

Responses by department respondents sit in

Responses by organization size (number of employees)

10%5,001-10,000

31%10,001-50,000

18%1,000-5,000

25%More than 100,000

16%50,001-100,000

government

other33%

8% consumer products

8%

energy8%

professional services

12%

banking and financial services24%

technology, media and telecommunications28% manufacturing

and industrial17%

55% dedicated CRE department

15% corporate or general management

10% finance

9% administration or shared services

1% IT

1% HR

1% supply chain and logistics

6% others

34 Global Corporate Real Estate Trends 2013 Jones Lang LaSalle 35

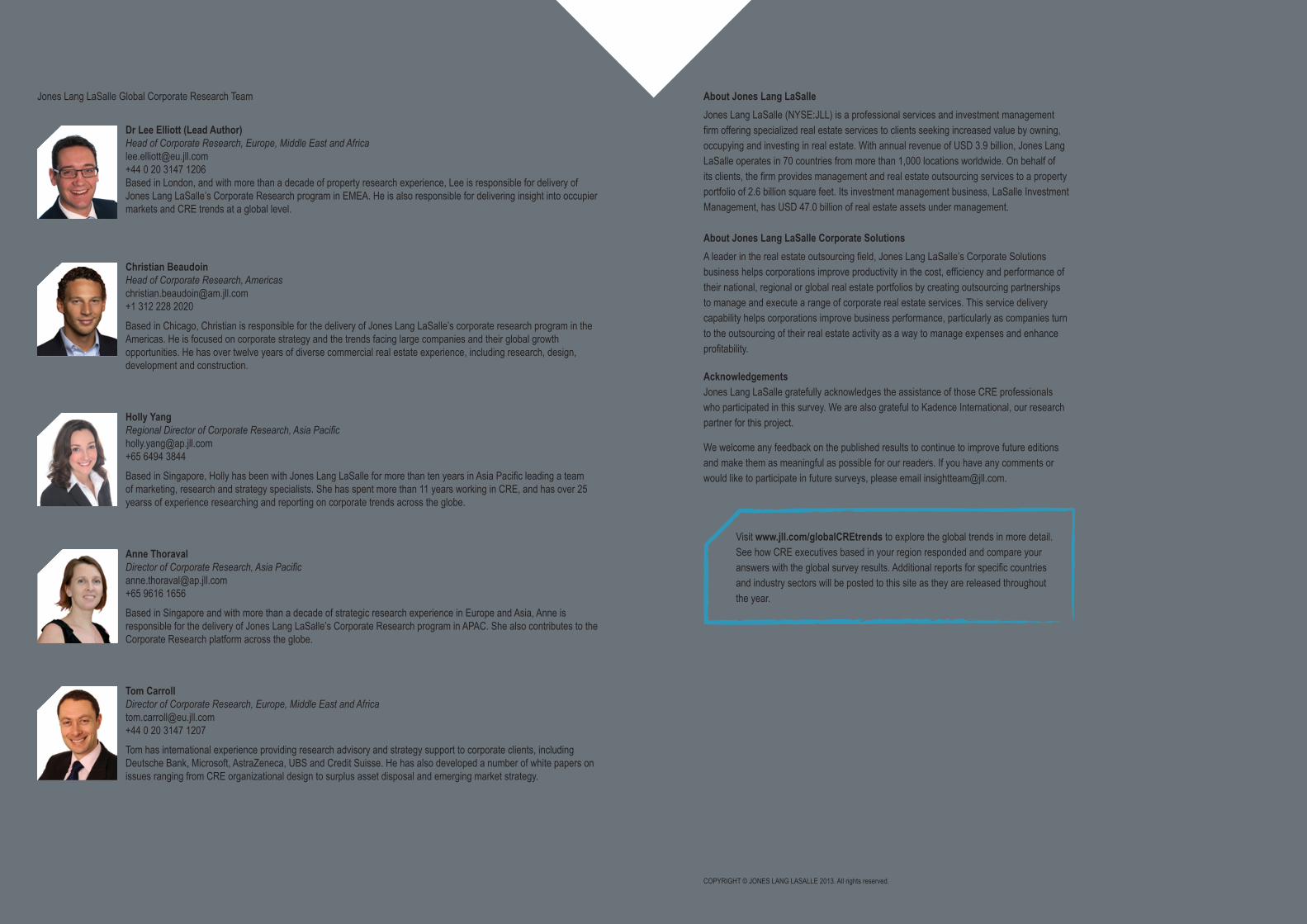

Jones Lang LaSalle Global Corporate Research Team

Dr Lee Elliott (Lead Author) Head of Corporate Research, Europe, Middle East and Africa [email protected] +44 0 20 3147 1206Based in London, and with more than a decade of property research experience, Lee is responsible for delivery of Jones Lang LaSalle’s Corporate Research program in EMEA. He is also responsible for delivering insight into occupier markets and CRE trends at a global level.

Christian Beaudoin Head of Corporate Research, [email protected] +1 312 228 2020

Based in Chicago, Christian is responsible for the delivery of Jones Lang LaSalle’s corporate research program in the Americas. He is focused on corporate strategy and the trends facing large companies and their global growth opportunities. He has over twelve years of diverse commercial real estate experience, including research, design, development and construction.

Tom Carroll Director of Corporate Research, Europe, Middle East and [email protected] +44 0 20 3147 1207

Tom has international experience providing research advisory and strategy support to corporate clients, including Deutsche Bank, Microsoft, AstraZeneca, UBS and Credit Suisse. He has also developed a number of white papers on issues ranging from CRE organizational design to surplus asset disposal and emerging market strategy.

Anne Thoraval Director of Corporate Research, Asia [email protected] +65 9616 1656

Based in Singapore and with more than a decade of strategic research experience in Europe and Asia, Anne is responsible for the delivery of Jones Lang LaSalle’s Corporate Research program in APAC. She also contributes to the Corporate Research platform across the globe.

Holly Yang Regional Director of Corporate Research, Asia [email protected] +65 6494 3844

Based in Singapore, Holly has been with Jones Lang LaSalle for more than ten years in Asia Pacific leading a team of marketing, research and strategy specialists. She has spent more than 11 years working in CRE, and has over 25 yearss of experience researching and reporting on corporate trends across the globe.

About Jones Lang LaSalleJones Lang LaSalle (NYSE:JLL) is a professional services and investment management firm offering specialized real estate services to clients seeking increased value by owning, occupying and investing in real estate. With annual revenue of USD 3.9 billion, Jones Lang LaSalle operates in 70 countries from more than 1,000 locations worldwide. On behalf of its clients, the firm provides management and real estate outsourcing services to a property portfolio of 2.6 billion square feet. Its investment management business, LaSalle Investment Management, has USD 47.0 billion of real estate assets under management.

About Jones Lang LaSalle Corporate SolutionsA leader in the real estate outsourcing field, Jones Lang LaSalle’s Corporate Solutions business helps corporations improve productivity in the cost, efficiency and performance of their national, regional or global real estate portfolios by creating outsourcing partnerships to manage and execute a range of corporate real estate services. This service delivery capability helps corporations improve business performance, particularly as companies turn to the outsourcing of their real estate activity as a way to manage expenses and enhance profitability.

Acknowledgements Jones Lang LaSalle gratefully acknowledges the assistance of those CRE professionals who participated in this survey. We are also grateful to Kadence International, our research partner for this project.

We welcome any feedback on the published results to continue to improve future editions and make them as meaningful as possible for our readers. If you have any comments or would like to participate in future surveys, please email [email protected].

Visit www.jll.com/globalCREtrends to explore the global trends in more detail. See how CRE executives based in your region responded and compare your answers with the global survey results. Additional reports for specific countries and industry sectors will be posted to this site as they are released throughout the year.

COPYRIGHT © JONES LANG LASALLE 2013. All rights reserved.