Risk Rating and Credit Scoring for SMEsebrd.com/downloads/news/2_rr.pdf · Risk Rating and Credit...

21

Washington | London | Amman | Johannesburg | Mexico City | Ramallah | Islamabad Risk Rating and Credit Scoring for SMEs March 27, 2012

Transcript of Risk Rating and Credit Scoring for SMEsebrd.com/downloads/news/2_rr.pdf · Risk Rating and Credit...

Washington | London | Amman | Johannesburg | Mexico City | Ramallah | Islamabad

Risk Rating and Credit Scoring for SMEs

March 27, 2012

Introduction

DAI is a global development consulting agency, with 40 years of experience and offices in Washington D.C., London, Amman, Johannesburg, Mexico City, and Ramallah

With experience in 150 countries, DAI implements international development projects across the sectors of Corporate Services, Economic Growth, Environment and Energy, Governance, Health and Security

Introduction

DAI has extensive experience in management, economic and financial consultancy services to business and government clients throughout the world, focussing particularly on the area of MSME Lending and Leasing

These projects have included aspects of credit scoring and credit risk analysis, mutually reinforcing business strategies, structures, products, policies, and procedures and how to strengthen core functions, such as lending, risk management, marketing, internal control, and IT/MIS

DAI’s Experience in SME Credit Scoring

31 Financial Institutions

Key Benefits of Credit Scoring

Credit Scoring provides a consistent, quantitative estimate of borrower risk

Relative risk allows for differentiation in:

• the loan approval process• loan conditions and pricing• collection activities

Scoring leads to process automation (efficiency) and improved risk measurement (quantification) and management (consistency)

Working with Limited Data

Data availability affects how we weigh factors

Factor selection always involves expert judgment

Assuming we develop the best scorecard possible given our data and resources constraints, all scorecards are

again “equal” in that they must be monitored, periodically validated, and adjusted or re-developed

Scorecard Development

The greatest challenge is not statistical or technical ("accuracy") but rather human and organizational ("practicality")

How Scoring Works

Scoring models assume the future will be like the past– Based on historic data when available– Based on organizational experience in all cases

Scoring models should include the same set of key financial and non-financial risk factors that banks analyze subjectively

Assign points for the different risk characteristics – the point total for any given client is its “score”

How Scores Estimate Probability of Default

Group scores into some number risk classes

Evaluate borrower performance over time

Historic performance by risk class becomes the probability of default estimate for future periods

Example of Scoring Policy Table

Risk Class Decision Policy Interest Margin Historic PD

1 Branch Approval 1.25 0,00%

2 Branch Approval 1.75 0.08%

3 Branch Approval 2.25 1.9%

4 Branch Approval 3.00 3.6%

5 Central Review 5.00 6.8%

6 Exception Only 7.00 9.12%

7 Reject N/A 18.4%

Example SME Loan Process Without Scoring

Client Completes Application

Visit Client’s Place of Business

Check Credit Report / Minimum Criteria

Create Loan Memorandum

Present Loan to Credit Committee

30% 70%

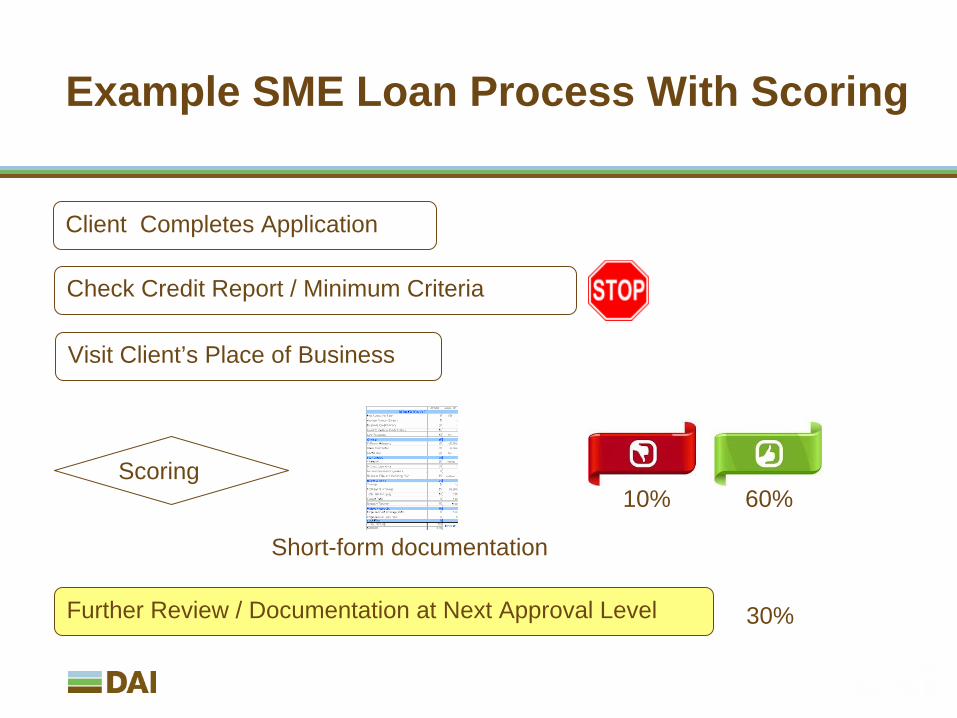

Example SME Loan Process With Scoring

Client Completes Application

Visit Client’s Place of Business

Check Credit Report / Minimum Criteria

Further Review / Documentation at Next Approval Level

10% 60%Scoring

30%

Short-form documentation

Example of Time and Money Savings

Reduce time documenting 70% of loans

Reduce time spent by Credit Committee reviewing 70% of loans

Systematically eliminate the riskiest 10% of applicants

Scorecard Deployment

A web-based online “single-entry, multiple use” application processing system is the most appropriate long-term model deployment solution.

SME Lending Scorecards Summary

1. No “right” set of factors

2. Factors should generally be those that the Bank considers the most important when subjectively deciding to issue or not issue a loan

3. If the factors make sense individually, then as a group of factors, the scorecard will be able rank risk

SME Lending Scorecard Example Factors

CAPACITYTotal SalesLoan Size as % of SalesTotal Debt/EquityCurrent RatioInventory TurnoverInterest CoverageDebt Coverage Ratio

CHARACTERYears with BankBusiness Credit HistoryOwner's Personal Credit HistoryYears Experience in BusinessType of Legal Entity

CAPITALClient Contribution to FinancingAverage Bank Account Turnover / Turnover from Income StatementAverage Bank Account Balance

COLLATERALLoan To Value RatioType of CollateralPresence of Additional Guarantees

CONDITIONSSector RiskKey Buyer/Supplier Dependencies

How Statistical Scoring Works

For each potential factor, count the number of good and the number of bad contracts for across each possible “category”

Look for meaningful patterns of increasing/decreasing risk

Assign point weights equal to the concentration of bad loans per category

Models Rank Applicants by Risk

Single Factor Cross Tabulation: Risk = “Bad Rate”

Example Variable “Requested Loan to Turnover”

Higher Ratio is Higher Risk

4,000 Loans, 200 are “Bad”

Loan Size to Turnover # Good #Bad Total Bad Rate

< 10% 1,000 0 1,000 0.0%11 - 25% 970 30 1,000 3.0%26 - 50% 930 70 1,000 7.0%>50% 900 100 1,000 10.0%

TOTAL 3,800 200 4,000 5.0%

Points037

10

Models Rank Applicants by Risk

Full Model Cross Tabulation: Risk = “Bad Rate”

More Points Indicate Higher Risk

4,000 Loans, 200 are “Bad

Score Range Goods Bads Total Bad Rate0 - 14 200 0 200 0.0%15 - 28 397 3 400 0.8%29 - 42 792 8 800 1.0%43 - 57 1,179 21 1,200 1.8%58 - 71 745 55 800 6.9%72 - 85 348 52 400 13.0%86 - 100 139 61 200 30.5%

TOTAL 3,800 200 4,000 5.0%

20

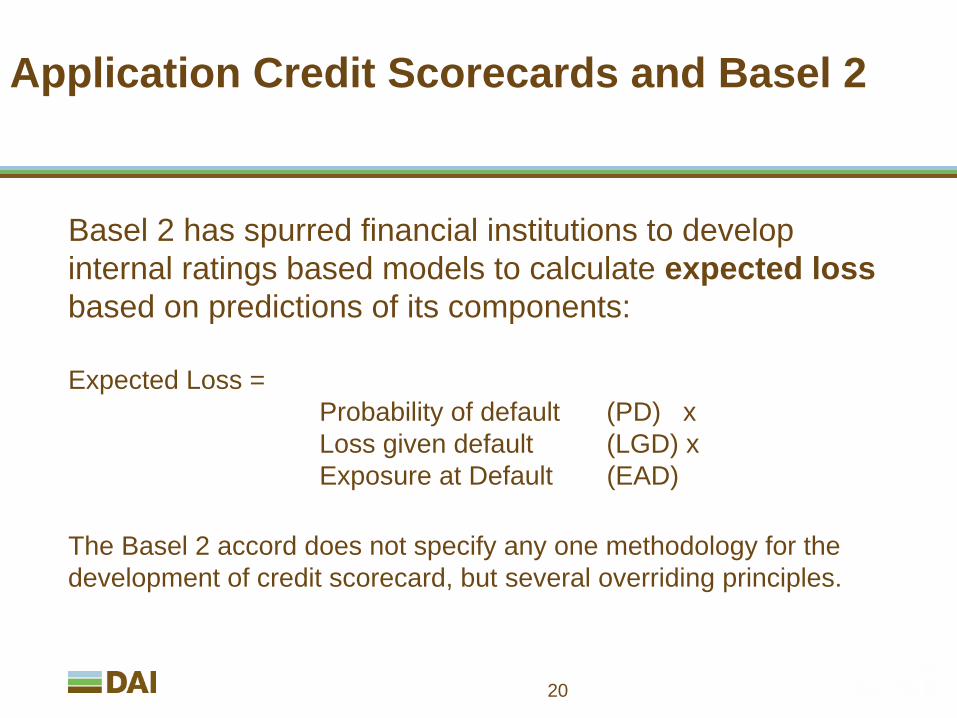

Application Credit Scorecards and Basel 2

Basel 2 has spurred financial institutions to develop internal ratings based models to calculate expected loss based on predictions of its components:

Expected Loss = Probability of default (PD) x Loss given default (LGD) x Exposure at Default (EAD)

The Basel 2 accord does not specify any one methodology for the development of credit scorecard, but several overriding principles.

Thank you

Questions?

![Validation of Internal Rating and Scoring Models ... of Internal Rating and Scoring ... [Basel II, §500] ... Basel I Advanced IRB Credit Risk AMA Operational Risk](https://static.fdocuments.us/doc/165x107/5ab075ad7f8b9a6b468b4b66/validation-of-internal-rating-and-scoring-models-of-internal-rating-and-scoring.jpg)