RISK MITIGATION STRATEGIES AND PERFORMANCE OF INSURANCE …

85

RISK MITIGATION STRATEGIES AND PERFORMANCE OF INSURANCE INDUSTRY IN KENYA: A CASE OF MOTOR INSURANCE COMPANIES JANET MAKOKHA OKUMU D53/OL/CTY/24244/2014 A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF THE REQUIREMENTS THE DEGREE OF MASTER OF BUSINESS ADMINISTRATION (STRATEGIC MANAGEMENT OPTION) OF KENYATTA UNIVERSITY November, 2017

Transcript of RISK MITIGATION STRATEGIES AND PERFORMANCE OF INSURANCE …

RISK MITIGATION STRATEGIES AND PERFORMANCE OF INSURANCE

INDUSTRY IN KENYA: A CASE OF MOTOR INSURANCE COMPANIES

JANET MAKOKHA OKUMU

D53/OL/CTY/24244/2014

A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILLMENT OF

THE REQUIREMENTS THE DEGREE OF MASTER OF BUSINESS

ADMINISTRATION (STRATEGIC MANAGEMENT OPTION)

OF KENYATTA UNIVERSITY

November, 2017

ii

DECLARATION

This research project is my original work and to the best of my knowledge has not

been submitted for a degree in any other university. No part of this Project should be

reprinted without permission from the Kenya University.

Signature: ____________________________ Date___________________________

Student: Janet Makokha Okumu

Declaration by the Supervisor

This research Project has been submitted for examination with my approval as the

University Supervisor.

Dr Jane Wanjira

Lecturer, Department of Business Administrations

Signature: ___________________________________ Date______________

iii

DEDICATION

This Project is dedicated to my parents Mr & Mrs Okumu and to my siblings.

iv

ACKNOWLEDGEMENTS

I am grateful to God Almighty for seeing me through this Project. I acknowledge my

supervisor, Dr. Jane Wanjira who mentored me throughout this journey. I must

confess that through your input, I have managed to reach this far it is very true that it

is good to be mentored by experts. I would also like to thank my friends, relatives,

and classmates for their support throughout the project work. May God bless you.

v

TABLE OF CONTENTS

DECLARATION........................................................................................................... ii

DEDICATION.............................................................................................................. iii

ACKNOWLEDGEMENTS ........................................................................................ iv

TABLE OF CONTENTS .............................................................................................. v

LIST OF TABLES ....................................................................................................... ix

LIST OF FIGURES ...................................................................................................... x

ABBREVIATIONS AND ACRONYMS .................................................................... xi

OPERATIONAL DEFINITION OF TERM ............................................................ xii

ABSTRACT ................................................................................................................ xiii

CHAPTER ONE: INTRODUCTION ......................................................................... 1

1.1 Background of the Study .......................................................................................... 1

1.1.1 Risk Mitigation Strategies...................................................................................... 3

1.1.2 Organization Performance ..................................................................................... 3

1.1.3 Key Performance Indicators of Insurance Companies in Kenya ........................... 4

1.1.4 Insurance Companies in Kenya ............................................................................. 4

1.1.5 Motor Insurance ..................................................................................................... 5

1.2 Statement of the Problem .......................................................................................... 6

1.3 Research Objectives .................................................................................................. 7

1.3.1 General Objective .................................................................................................. 7

1.3.2 Specific Objectives ................................................................................................ 7

1.4 Research Questions ................................................................................................... 7

1.5 Research Hypotheses ................................................................................................ 8

1.6 Significance of the study ........................................................................................... 8

1.7 Scope of the Study .................................................................................................... 9

vi

1.8 Limitations of the Study............................................................................................ 9

1.9 Organization of the Study ....................................................................................... 10

CHAPTER TWO: LITERATURE REVIEW .......................................................... 11

2.1 Introduction ............................................................................................................. 11

2.2 Theoretical Framework ........................................................................................... 11

2.2.1 Agency Theory..................................................................................................... 11

2.2.2Contingency Planning Theory .............................................................................. 12

2.2.3 Arbitrage pricing theory ....................................................................................... 12

2.2.4 Resource Based Theory ....................................................................................... 13

2.3 Conceptual literature ............................................................................................... 13

2.3.1 Risk controlling Strategy ..................................................................................... 13

2.3.2 Risk Avoidance Strategy...................................................................................... 13

2.3.3 Risk based audit strategy ..................................................................................... 14

2.4 Empirical Review.................................................................................................... 15

2.4.1 Risk Control Strategy and Performance .............................................................. 15

2.4.2 Risk Avoidance Strategy and Performance ......................................................... 16

2.4.3 Risk based audit strategy and Performance ......................................................... 16

2.4.4 Product Mix Strategy and Performance ............................................................... 18

2.5 Summary of Research Gaps .................................................................................... 18

2.6 Conceptual Framework ........................................................................................... 23

CHAPTER THREE: RESEARCH METHODOLOGY ......................................... 25

3.1 Introduction ............................................................................................................. 25

3.2 The Research Design .............................................................................................. 25

3.3 Population of the study ........................................................................................... 25

3.4. Data sources and collection instruments ................................................................ 27

vii

3.5 Validity and reliability of Research instrument ...................................................... 27

3.5.1 Pilot Study…… ................................................................................................... 27

3.5.2 Validity………. ................................................................................................... 28

3.5.3Reliability……… .................................................................................................. 28

3.6 Data Collection Procedure ...................................................................................... 28

3.7 Data analysis and Presentation................................................................................ 28

3.8 Ethical considerations ............................................................................................. 29

CHAPTER FOUR: DATA ANALYSIS, INTERPRETATION AND

DISCUSSION OF THE FINDINGS.......................................................................... 31

4.1 Introduction ............................................................................................................. 31

4.2 Response Rate ......................................................................................................... 31

4.3 Reliability Test of the Instrument ........................................................................... 31

4.4 Demographic Characteristics of the Respondents .................................................. 32

4.4.1 Gender and Age of the respondents ..................................................................... 32

4.4.2 Period of Work and Department .......................................................................... 33

4.5 Descriptive Statistics ............................................................................................... 34

4.5.1 Risk Controlling Strategy .................................................................................... 34

4.5.2 Risk Avoidance Strategy...................................................................................... 36

4.5.3 Risk based audit strategy ..................................................................................... 40

4.5.4 Product Mix Strategy ........................................................................................... 41

4.5.5 Performance of Regulated Motor Insurance Companies ..................................... 44

4.6 Inferential Statistics ................................................................................................ 45

4.6.1 Correlation Analysis ............................................................................................ 45

4.6.1.1 Diagnostic test ................................................................................................... 47

4.6.1.2 Test for Multicollinearity .................................................................................. 47

viii

4.6.1.3 Test for Normality............................................................................................. 47

4.6.1.4 Heteroskedasticity test ...................................................................................... 48

4.7 Regression Analysis ................................................................................................ 49

CHAPTER FIVE: SUMMARY OF THE FINIDNGS, CONCLUSIONS AND

RECOMMENDATIONS ............................................................................................ 53

5.1 Introduction ............................................................................................................. 53

5.2 Summary of the findings ......................................................................................... 53

5.3 Conclusion .............................................................................................................. 54

5.4 Recommendations ................................................................................................... 55

5.4 Areas for Further Research ..................................................................................... 56

REFERENCES ............................................................................................................ 57

APPENDICES ............................................................................................................. 60

Appendix I: Questionnaire for Employees ................................................................... 60

Appendix II: List of Registered Insurance Companies ................................................ 69

Appendix III: Nacosti Permit Letter ............................................................................ 71

Appendix IV: Data Collection Authorization ............................................................. 72

ix

LIST OF TABLES

Table 2.1 Summary of Literature and Research gaps ................................................20

Table 3.1: Distribution of Target Population of the companies and Employees .........26

Table 3.2: Distribution of the sample size ...................................................................27

Table 4.1 Reliability of Risk Mitigation Strategies and Performance of Insurance

Industry ........................................................................................................................32

Table 4.2 Gender and Age of Respondents .................................................................32

Table 4.3 Period of Work and Department ..................................................................33

Table 4.4 Risk Controlling Policy ...............................................................................34

Table 4.5: Risk Controlling Strategy and Performance of Motor Insurance

Companies....................................................................................................................35

Table 4.6: Types of Risks ............................................................................................37

Table 4.7: Risk Avoidance Strategy and Performance of Motor Insurance

Companies....................................................................................................................38

Table 4.8: Risk-based Auditing Strategy and Performance of Motor Insurance

Companies....................................................................................................................40

Table 4.9: Effectiveness of Product Mix Strategies in Mitigating Risks ....................42

Table 4.10: Product Mix Strategy and Performance of Motor Insurance Companies ....43

Table 4.11 Performance of Regulated Motor Insurance Companies ...........................44

Table 4.12: Correlation Matrix ...................................................................................46

Table 4.13: Multicollinearity results using VIF ...........................................................47

Table 4.15: Model Fitness............................................................................................49

Table 4.16: Analysis of Variance.................................................................................50

Table 4.17: Regression Coefficients ............................................................................50

x

LIST OF FIGURES

Figure 2.1: Conceptual Framework ......................................................................................... 24

Figure 4.1: Test for Normality ................................................................................................. 48

xi

ABBREVIATIONS AND ACRONYMS

AKI: Association of Kenya Insurance

CEOs: Chief Executive Officers

MBO: Management by Objectives

GDP: Gross Domestic Product

MIP: Medical Insurance Providers

IRA: Individual Retirement Account

xii

OPERATIONAL DEFINITION OF TERM

Performance: The process of executing a task against a set standard.

Product mix strategy: Its determined by the size and growth of the market

products a company sells. Product mix entails the total

number of product lines that a firm offers to its clients.

Risk avoidance: It is the elimination of hazards, activities and exposures

that can negatively affect an organization.

Risk control strategy: Risk control is the method by which firms measure

potential losses and take action to reduce or eliminate

such threats.

Risk management: This is the human activity which integrates

identification of risk, risk assessment measurement,

monitoring, developing strategies to manage it, and of

those risks which can threaten firm achieving

Performance.

Risk mitigation strategy: It is a structured and coherent approach to identifying,

assessing, and managing project risk

Risk transfer strategy: An act of moving losses, damage to another

organisation or person.

xiii

ABSTRACT

Effective risk mitigation strategies are the key to achieve performance in the Motor

insurance industry. This involves knowing and analysing risks, making, and

reviewing risk handling techniques and checking the progress of these to avoid and/or

reduce the impact of risk on the performance of the firm. It is against this background

that this Project assessed risk mitigating strategies on performance of motor insurance

companies. The study’s general objective was to establish the effects of risk

mitigation strategies on performance of insurance industry in Kenya: a case of motor

insurance companies. Specifically, the Project focused on the Risk control, risk

avoidance, risk transfer and product mix strategies on performance of the insurance

industry. The study was anchored on Agency theory which is based on the outreach as

a way of mitigating risks. The research used descriptive survey research designs. The

target population of this study was the management and the other employees of all the

18 Motor insurance companies, the sample size of the study was54.The sampling

procedure was both simple random sampling and purposive sampling. Primary data

entailed using of questionnaires. Content validity was ensured by asking questions

that are relevant and captured the research objectives, reliability was measured with

the help of cronbach’s alpha (α). Descriptive statistics such as means, standard

deviation and frequency distribution tables were used to analyse the data. Qualitative

data was analyzed using content analysis to generate qualitative report which were

presented in a continuous prose. Inferential statistics such as regression and

correlation analysis were used to establish the effects of risk mitigation strategies on

performance of insurance industry in Kenya, a case of motor insurance companies.

Data presentation was done by the use of bar charts and graphs, percentages and

frequency tables for ease of understanding and interpretation. The study found out

that risk control strategy and performance of regulated motor insurance companies in

Kenya are positively and significantly related. The results further indicate that risk

avoidance strategy and the performance of regulated motor insurance companies were

positively and significantly related. It was further established that product mix

strategy and performance of regulated motor insurance companies were positively and

significantly related while risk based audit strategy and performance of regulated

motor insurance companies were also positively and significantly related. The study

concluded that risk controlling strategy, risk avoidance strategy, risk based audit

strategy and product mix Strategy have a positive and significant effect on

performance of Motor Insurance Companies. Based on the findings and conclusions

that risk controlling, risk avoidance Strategy, risk based audit strategy and product

mix strategy has a positive and significant effect on performance of Motor Insurance

Companies, the study recommends motor insurance companies should work toward

investing more on risk reduction strategies in order to improve their performance.

1

CHAPTER ONE

INTRODUCTION

1.1 Background of the Study

Today’s world presents serious challenges. Fundamental changes in natural,

economic, social, and political spheres, shifting stakeholder expectations and wide-

reaching technological innovations lead to a perpetually changing and demanding risk

environment. This calls for continuous adaptation from businesses around the globe.

(The Geneva Papers on Risk and Insurance, 2013).

External forces must be death within the insurance industry and continuation of

growth of the frontiers of risk mitigation. Law frameworks and procedures too must

adapt. It is important that the Law responses to the new challenges be made to support

the economy.

Insurers have expanded into new geographic markets and developing a greater range

of insurance product offerings and services to improve on their performance in that

some insurers and non-insurance are engaging in activities such as banking and asset

management services.

Affordability of insurance products is low in Africa due to poor standards of living in

that only upper and middle income earners can access the insurance products.

Nevertheless, the relatively unexplored insurance industry is expected to be resilient

thanks to consistent GDP growth, rapid urbanization and increases in the working

aged population across the continent.

South Africa, one of the region’s most advanced, is currently troubled, economies,

unsurprisingly accounted for almost 75 percent, or $51.6bn, of all insurance premiums

on the continent in 2013 according to global reinsurance firm Swiss Re. According to

South African Insurance Association report (2015), However South Africa’s

dominance is set to be challenged by a number of promising countries.

MsMaïdou also points to Kenya and Ethiopia as significant up-and-coming insurance

markets, “especially due to the size of their population and growing middle class”.

Although the penetration rate for insurance in Kenya stood at only 2.75 percent in

2013, the market has grown by just over 15 percent each year from 2010 to 2013.

2

Premiums reached $1. 5bn.The recent $350m investment partnership between

Prudential Financial and Leapfrog Investments, which targets high-growth insurance

markets in Africa, is a clear sign that global companies are keen to tap this potential.

In 2015 Group Jubilee Holdings Limited (JHL) achieved a turnover of Kshs 30.16

Billion hence increase in growth by 25 percent to Ksh. 1.72 Billion in 2015. In recent

years Jubilee Holdings, a strategy was implemented to expand investments to reduce

the risk of volatility from stock market movements. This strategy entailed increasing

investments in government bonds and diversifying into investments in the energy

sector, such as Tsavo power and Bujagali, and in other infrastructure projects such as

SEACOM, that are giving returns in dollar terms (Abuogi, 2014).

Kenya being developed has the best insurance markets although the competition is

tough. Currently, according to the Association of Kenyan Insurers (AKI), Kenya

represents 70% of the East African insurance market, which also includes Tanzania,

Uganda, Rwanda and Burundi. Insurance penetration and accessibility have been

improving steadily in Kenya. There is a potential for increase in demand for insurance

as middle class is growing, more Kenyans have disposable income. Increase in

urbanisation, giant infrastructure projects, new energy schemes and growing industry.

Huge infrastructure plans have made investment opportunities in insurance. Some of

the main ventures include the construction of the second runway and new terminal at

Jomo Kenyatta International Airport, the Lamu Transport Corridor project, and the

Standard Gauge Railway (SGR) project (Abuogi, 2014).

Life insurance penetration is 1.2% of GDP and general insurance about twice that,

bringing the total to 3.44% in 2013, according to AKI figures. This measure of

insurance penetration dropped to 2.93% in 2014 after GDP was rebased with a 25%

increase. Now 4% penetration by year-end looks possible; this compares favourably

to the majority of Africa’s markets, although it is slightly down from the 2010 target

of 5% by 2015. Worldwide insurance penetration is about 6.5% of GDP, so Kenyan

insurers say there is great room for growth. William Maara, managing director of

Barclays Life Assurance Kenya, told OBG that, “Given low penetration rates, the

Kenyan insurance sector has significant growth potential. This is particularly true

following the expansion of the branch network into previously untapped markets;

expansion was further supported by the introduction of new products to the market.”

3

1.1.1 Risk Mitigation Strategies

Risk mitigation strategy is the method of evaluating, knowing, and determining the

behaviour risks that arises during the course of the project lifecycle (Chacko and

Harris, 2006). It entails a series of steps to support better decision making through

good understanding of the risks inherent in a Project and their likely impact.

The risk management planning describes risk identification, risk analysis and risk

handling. The plan should illustrate the role of risk evaluation in design reviews,

technical outcome, observing and changing control processes. The strategies to

mitigate risks entail moving the risks to another party, avoiding the risks, minimising

the negative effect or probability of the risk, or even accepting some or all of the

potential or actual consequences of a particular threat, and the opposites for

opportunities.

Controlling asset quality is only guaranteed when the credit risk department has

strong policies and risk systems. The optimal control risk strategy is the one that is in

line with the business strategy. It is not the one that minimizes losses, but the one that

provides a good policy value in line with the insurance business objectives.

1.1.2 Organization Performance

Organizational performance constitutes of the actual output of an organization as

measured against its intended outputs (or goals and objectives). Performance can be

assessed through evaluating a firm’s profitability, solvency, and liquidity. The

performance of a company can be measured by monitoring the firm’s profitability

levels. The return on equity (ROE) and the return on assets (ROA) are the used as

measures of profitability. By monitoring a firm’s profitability levels, one can measure

its financial performance.

Organizational performance is therefore the ability of an organization to fulfil its

mission through sound management, strong governance, and a persistent rededication

to achieving results. Organization performance measurement is considered a

multifaceted concept that occurs at different of levels for industry, corporate and

business sectional unit.

4

1.1.3 Key Performance Indicators of Insurance Companies in Kenya

A Key Performance Indicator (KPI) is used by an organization to evaluate its success

in reaching its strategic objectives by measuring the performance of the critical

activities towards an objective examples are financial ratios and sales growth rates.

Key among the indicators in insurance company are: Net income ratio, policy sales

growth, percentage of sales growth, claims ratio, and quotas-to-production are all

commonly used key performance indicators, or KPIs, in the insurance industry.

Insurance premiums represents total sales in the insurance industry. The net income

ratio is calculated by dividing net income by the total of earned premiums for a given

period. It measures the effectiveness of the company at generating profits with each

dollar of earned premium. A net income ratio of 10 percent is worse than a net income

ratio of 20 percent. The latter is 10 percent more efficient at creating net income out

of earned insurance premiums and is considered more profitable.

The claims ratio is an insurance KPI that measures how well your sales are covering

the cost of claims. It is calculated by dividing total claims per period by the total

earned premium per period. It is often used as an auditing KPI -- a high metric could

be a sign of fraud. The average time to settle a claim can be used in conjunction with

the claims ratio. It is calculated by dividing the total number of days taken to settle a

claim by the total claim. A high time to settle and a high claims ratio is cause for

concern.

1.1.4 Insurance Companies in Kenya

The insurance sector in Kenya is divided into two broad sub sectors namely; General

and Life insurance. The general insurance sector is by far the larger of the two in

terms of size and market penetration. The main players in the Kenyan insurance

company are insurance companies, reinsurance companies, insurance brokers,

insurance agents and the risk managers. The statute regulating the companies is the

insurance Act; Laws of Kenya, Chapter 487. The office of the commissioner of

insurance was established under its provisions to strengthen the government

regulation under the Ministry of Finance. There is also self-regulation of insurance by

the Association of Kenya Insurers (AKI). The professional body of the industry is the

Insurance Institute of Kenya (IIK), which deals mainly with training and professional

5

education. There were 49 operating insurance companies as at the end of 2015. 25

companies wrote non-life insurance business only, 13 wrote life insurance business

only while 11were composite (both life and non-life). There were 198 licensed

insurance brokers, 29 medical insurance providers (MIPs) and 5,155 insurance agents.

Other licensed players included 133 investigators, 108 motor assessors, 25 loss

adjusters and 24insurance surveyors (Ernst & Young, 2012)

Kenyan insurance industry consist of insurance companies, reinsurance companies,

intermediaries such as insurance brokers and insurance agents, risk managers or loss

adjusters and other service providers (Insurance Regulatory Authority, 2010). The

statute regulating the industry is the insurance Act; Laws of Kenya, Chapter 487. The

office of the commissioner of insurance was established under its provisions to

strengthen the government regulation under the Ministry of Finance. There is also

self-regulation of insurance by the Association of Kenya Insurers (AKI) established in

1987 as a consultative and advisory body to insurance companies and registered under

the Society Act Cap 108 of Kenyan law (AKI, 2010).

In Kenya Insurance availability and affordability are both policy concerns, as

evidenced by government’s many regulations of the insurance market. Legislation of

any country creates an enabling environment and business opportunities for all

entrepreneurs. Insurance service providers were 21 loss adjusters, 2 claims settling

agents, 193 loss assessors/investigators, 26 insurance surveyors, and 8 risk managers

during the year. The gross written premium by the industry was Kshs76.9 billion

compared to Kshs65.0 billion in 2006 representing a growth of 18%. The gross

written premium from General insurance was Kshs49.76 billion while that from long

term business was Kshs23.1 (AKI, 2014).

1.1.5 Motor Insurance

Level of risk determines insurance premiums. Generally, insurance policy with

increase of risk in claims insurance leads to higher rates (Gollier, 2003). With much

information at hand, insurers can evaluate risk of insurance policies at much higher

accuracy. To this end, insurers collect a vast amount of information about

policyholders and insured objects.

6

Due to increase in completion and dynamic change, a firm ought to have effective risk

mitigation strategies such as risk avoidance, risk reduction, risk retention and risk

transfer for a firm to excel (Olsson, 2008).

1.2 Statement of the Problem

Insurance companies are the backbone for most small business development of any

country and as such several studies have been carried out in line with this. Several

empirical studies have been carried out in this area of organizational performance;

Tripp, M., and Bradley, H., (2004). Conducted study on How to Quantify Operational

Risk in General Insurance Companies. Belasco, E. (2008). Conducted a study on ‘The

Role of Price Risk Management in Mitigating Risks in profits of Motor Insurance’.

Faure, M. (2006). Did a study on the Economic Criteria for Compulsory

Insurance. The Geneva Papers on Risk and insurance: Issues and practice. However

none of these studies seem to address comprehensively the issue of Risk mitigating

strategies and performance in motor insurance therefore that is the concern for this

paper.

Locally, Essendi (2013) examined the effects of risk management on the performance

of insurance companies. Results showed that formulation of new motor policy is

based on the existing credit policy of the insurance companies. Wanja (2013)

investigated the effects of credit policy used by commercial banks on their

performance.

These studies failed to indicate the extent to which risk mitigation strategies such as

risk control, risk limitation, risk auditing strategy influence performance in motor

vehicle insurance companies. Despite the significant role played by risk mitigation

strategies on performance in insurance companies, this has not attracted attention of

many authors. This study therefore sought to fill the existing knowledge gap by

determining the effects of risk mitigation strategies on performance of motor

insurance companies in Kenya

7

1.3 Research Objectives

1.3.1 General Objective

The general objective of this study was to establish the effects of risk mitigation

strategies on performance of Insurance Industry, a case of Motor Insurance

Companies

1.3.2 Specific Objectives

The specific objectives of this study were;

i. To determine the effects of risk controlling strategy on performance of Motor

Insurance Companies.

ii. To establish the extent to which risk avoidance influences performance of

Motor Insurance Companies.

iii. To establish influence of risk based audit strategy on performance of Motor

Insurance Companies.

iv. To determine influence of product mix strategy on performance of Motor

Insurance Companies.

1.4 Research Questions

This study sought to answer the following research questions:

i. How does risk controlling affect performance of Motor Insurance Companies?

ii. To what extent does risk acceptance strategy influences performance of Motor

Insurance Companies?

iii. To what extent does risk transfer strategy affects performance of Motor

Insurance Companies?

iv. How does product mix strategy affect performance of Motor Insurance

Companies?

8

1.5 Research Hypotheses

i) H0: Risk controlling does not affect performance of Motor Insurance

Companies.

ii) H0: Risk acceptance strategy does not affect performance of Motor Insurance

Companies.

iii) H0: Risk transfer strategy does not affect performance of Motor Insurance

Companies.

iv) H0: Product mix strategy does not affect performance of Motor Insurance

Companies.

1.6 Significance of the study

This study is significant to insurance companies, general public, students and the

insurance regulators as it offers valuable contributions from both a theoretical and

practical perspective.

Theoretically, the study shows to the general understanding of risk management

practices and their effect on financial performance. The study shall enable Insurance

companies in Kenya to improve their risk management process and to adopt efficient

strategies to improve firm financial performance through the risk management

processes.

This shall enable the insurance companies to perform better and to grow their

businesses and maintain a competitive advantage. Apart from benefiting the insurance

companies, the general public will also benefit from the study through improved

insurance services and better management of risks. This will result to affordable rates

of insurance premiums and reduction in levels of non-payment and fraud.

The study will be helpful to the government in setting regulations on insurance

practices in Kenya through the IRA and safeguarding the resources of the country. It

will also be helpful to the government in the developing policy papers, policy making

regarding risk mitigation strategy and other regulatory requirements of insurance

companies in Kenya may also benefit from the findings of this study. The policy

makers may gain insight on how well to incorporate the sector effectively to ensure

9

effective mitigation of risks for the insurance industry to achieve high company

performance.

The study shall also add value to the existing body of knowledge on risk management

to benefit academicians and aid further research on risk management in the insurance

sector and the financial sector. The findings of the study shall be relevant to scholars

and researchers as it may provide information regarding effects of risk mitigation

strategies on insurance company performance in Kenya.. This may aid further research

on risk management in the insurance sector and the financial sector.

1.7 Scope of the Study

The study sought to investigate the effects of risk mitigation strategies on

performance of insurance industry with special focus on Motor Insurance Companies

in Nairobi. The study focused on risk controlling strategy, risk avoidance, risk based

audit strategy and product mix strategy as independent variables. Legislation and

inflation as moderating variables and performances dependent variables. The study

covered all the branches in Nairobi. The study adopted descriptive research. The area

of the study was done in Nairobi as this is the location of the Motor Insurance

Companies are. The study considered a study period of 5 year from 2011 to 2015.

1.8 Limitations of the Study

There was a shortage of literature on the relationship between risk mitigation and

employee productivity. Majority of the studies within the risk mitigation sector have

focused on the relationship between risk and productivity and not performance. This

study focused on obtaining additional information from the respondents by

conducting informal discussions.

The study encountered unwillingness by respondents to reveal information, which

may be thought confidential. However, the researcher assured the respondents that the

information they offered held confidentially and might be used for academic purposes

only in seeking to establish the effects of risk mitigation strategies on performance of

Motor Insurance Companies

10

1.9 Organization of the Study

This document was organized into five chapters. Chapter one presented the

background of the study, the motor insurance companies in Kenya, statement of the

problem, objectives of the study, significance of the study, delimitations, and

limitations of the study.

Chapter two outlined theoretical review, empirical review, and conceptual framework.

Chapter three focused on methodology which included the research design, empirical

model, target population, sampling design and procedure, data collection instrument,

validity of the instrument, reliability of the instrument, data collection procedure and

data analysis. Chapter four presents the findings, interpretation, and discussion of the

data, while chapter five, made a conclusion and recommendations of the study.

11

CHAPTER TWO

LITERATURE REVIEW

2.1 Introduction

This chapter critically reviewed the available literature on risk management and

performance. It began by reviewing theories underpinning this study, then an

overview of the empirical studies and literature on the risk mitigation and

performance. It also presented the summary of knowledge gaps and conceptual

framework.

2.2 Theoretical Framework

The following theories guided it: Agency theory, contingency planning theory

arbitrage pricing theory and results based theory.

2.2.1 Agency Theory

Agency theory extends the analysis of the firm to include separation of ownership and

control, and managerial motivation. Theory also elaborates differences on interest

between shareholders, management, and debt holders due to variance in earning

distribution, which can result in the firm taking too much risk or not engaging in

positive net value projects (Mayers and Smith, 1987).

Stulz (1984) asserts that managers are presumed to be working on behalf of firm

owners and concern themselves with both expected profit and the distribution of firm

returns around their expected value. They have an obligation to avoid risk in so as to

minimize the variability of firm returns and hence achieve it

Agency theory provides strong support for risk management as a response to

mismatch between managerial incentives and shareholder interests. Shareholders and

managers have different interests to the firm and risk management objectives vary for

the different stakeholders. While shareholders may require high risk – high return

investments, management prefer low risk and return investments. The agency theory

emphasizes the need for risk controlling in the firm to align the interests of mangers

and shareholders and to contribute to the performance of the firm.

12

2.2.2 Contingency Planning Theory

Contingency planning (CP) also known as is an important element in risk

management since a risks cannt be fully eliminated despite organization efforts to

avoid, mitigate or prevent them.Entails making major plans for preparation of

distaters incidents and availing resources to be used in such events when they occur.

This theory support risk acceptance strategies as in Contigency planning the firm

indentify the risks and determine the response to specific risks. Due to change in the

external enviroment, firm would mitigate risk through acceptance strtaegies . The

study focused on determining the effect of risk acceptance strategy on performance of

the motor insurance companies.

2.2.3 Arbitrage pricing theory

The Arbitrage Pricing Theory (APT) was developed primarily by Ross (1976). It is a

one-period model that has the stochastic properties of returns of capital assets are

consistent with a factor structure. The Arbitrage Pricing Theory (APT) describes the

price where a mispriced asset is expected to be.

It is often viewed as an alternative to the capital asset pricing model (CAPM), since

the APT has more flexible assumption requirements. Whereas the CAPM formula

requires the market's expected return, APT uses the risky asset's expected return and

the risk premium of a number of macro-economic factors. Arbitrageurs use the

APT model to profit by taking advantage of mispriced securities. A mispriced security

has a price that differs from the theoretical price predicted by the model.

The theory states that price of a security is driven by factors which are divided into

two groups: macro factors, and company specific factors. Linear pricing relation is a

must for equilibrium in a market where agents maximize certain types of utility. It

derives that either from the assumption of the preclusion of arbitrage or the

equilibrium of utility-maximization.

Expected returns and the betas helps identification of the stochastic discount factor.

APT relates to the price of the security to the fundamental factors driving it. The

theory does not show the factors hence need to be determined empirically which may

include economic growth and interest rates.

13

2.2.4 Resource Based Theory

According to the Resource Based Theory all inputs that allow the firm to function and

to implement its strategies are firm resources.

There are input factors which are generic resources that can be acquired in the market

and logistics input factors which include raw skills loading skills, driving skills,

picking skills, computer operating skills factors forklift trucks, warehouse racking,

packaging materials, and inventory. When input factors are transformed they become

part of the firm’s assets, hence contributing to the outputs of the firm (Grant, 2002).

When resources enable a firm to implement product mix strategy that improves

performance and exploit market opportunities or neutralizes risks only then is when

they are considered valuable (Barney, 2001).

The theory stipulates clearly that through utilization of the organization resources,

insurance will be in a position to consider its assets and its financial capability to

evaluate and produce product based on the need in the market.

2.3 Conceptual literature

2.3.1 Risk controlling Strategy

The method by which firms evaluate potential losses and take action to reduce or

eliminate such threats is called Risk control .It is a technique that uses findings from

risk assessments and implements changes to reduce risk in these areas.

The expected amount of loss is inversely related to its corresponding likelihood that

risks that will cause a high damage to corporation like earthquakes or fire as

compared to risks that occur daily such as interest rate risks or foreign exchange risks

which often cause relatively minor losses only, (Fatemi and Glaum 2000).

2.3.2 Risk Avoidance Strategy

Risk Avoidance strategy involves taking some action hence limiting the firms

exposure. For example a company should have backups as a disk drive may fail. A

situation is often intensified by lack of clearly defined risk limits, deliberately

misleading reports, lack of intra-organizational communication concerning risk

vulnerability, poor knowledge of the business environment and lack of timely

decision making.

14

Some risk events can be dealt with by obtaining information, improving

communication, clarifying requirements, or acquiring expertise. Usage of a familiar

approach, reduction of scope, increase of resources may be examples of avoidance

(Meinhard, 2006).

2.3.3 Risk based audit strategy

Accountability in corporate has been raised in various developed nations hence the

need of an appropriate Risk Based Audit.

By issuance of qualified opinions to firms with unreliable financial statements could

improve the precision of financial statement information investor’s screen out such

firms by the help of auditors.

Life insurance companies and intermediaries understand the risks and are able to

exercise sound judgment on implementation of rick based strategy. This is done

through training, recruitment, taking professional advice and learning by doing, good

practice guidance is also valuable.

2.3.4 Product Mix Strategy

The rate of transparency of insurance products is low taking into account of a larger

risk orientation in product design and pricing as compared to the past might hence

resulting in more complexity.

Diversification of products within each product line, makes it hard for the company

to know the required effort and timing for experience monitoring a product level

hence making it a challenge to set a risk limit .

Different product mix results to rise of exposures to risk hence insurance companies

provide protection at price exposures. An insurance company may opt to drop one or

more product lines or product items resulting into increase in profits from fewer

products. Modification product of already established is more profitable than making

a new product.

15

2.4 Empirical Review

This section reviewed literature from past studies which were related to this study.

2.4.1 Risk Control Strategy and Performance

A study by Yusuwan, Adnan & Omar, (2008) carried out the level of awareness,

policies used when encountering risks and problems faced when implementing risk

management in a construction project

A conclusion was carried out that risk management affects project finances

production, outcome, and efficiency and that risk management is conducive for

project with specific characteristics such as new technology.

A research carried out by Manabet al., (2010) focused on the drivers: mandate from

board of directors globalization, shareholders pressure, technology, improved decision

making, competitive pressure, good business practice catastrophic event and good

business practices which contributes to the success of Enterprise Wide Risk

Management (EWRM) implementation with corporate governance compliance and

improvement in for profit companies in Malaysia. Only 85 participated in this study

two types of companies were chosen that is financial companies and non-financial

companies. The conclusion of the study corporate governance, mandate from board of

directors, shareholder value, improved decision making and good business practices

results to success of Enterprise Wide Risk Management (EWRM).

Strutt (1993) conducted a study on impact of risk management on financial

performance of banking industry in US. The study used panel-corrected covariance

matrix of the coefficient estimates and uses panel-corrected standard errors. The

program used in the study can show unbalanced panel data. The main of this research

was to investigate the relationship between prepayment risk and credit union

performance. Results show that credit was significantly related to return on loans

(RETLNS) for the Controlling of all credit unions thus borrowers can either refinance

or default on a loan and therefore incorporate the risk premium into the required rate

of return on loans. It was evident that the relationship between risk and return on

loans was consistent for all but one credit controlling.

16

2.4.2 Risk Avoidance Strategy and Performance

A study by Eisenmann (2002) found that the Managerial risk connects with

organizational risk and further showed that the risk taking and risk avoidance

behaviour was dependend on the ownership structure. They analysed whether to

diversify their assets or not under increasing perishable business environment. Bettis

and Mahajan (1985) found that diversification minimises risk and enhances

performance. Diversification is the best way for minimising risks to target level

among the securities and in firm assets.

Kor and Leblebici (2005) & Hamilton and Shergill (1993) finds that managing

resources will results to higher outcome under diversification. Minimisation of risks

and attainment of high firm size will lead towards achievement of goals

Ruefli, Collins & Lacugna (1999), illustrates that diversification of products and

systematic risks of pricing are related to the Monopolistic market power. Risk is

inappropriately measured if the focus is on the distribution of outcomes. Risk

measurement assumes losses that might occur throughout an investment period, hence

investor ought to use the methods best related to project of their investment,

(Kritzman and Rich, 2002).

Laurentis and Mattei (2004) conducted a research on Lessors’ recovery risk

management capability and found that the development of modern reliable systems of

risk management can enhance even more those management capabilities. This means

that credit firms should invest resources in projects aimed at correctly implementing

rating systems and risk models, and highlights once more the importance of these

tools well beyond the scope of regulatory compliance. The research method used is

that mixed research method.

2.4.3 Risk based audit strategy and Performance

Empirical studies on effect of risk assessment on financial performance are reviewed

in this section. According to McCord (2002), risk evaluation of material misstatement

at the financial statement level and also at the planning stage, shows the way on

17

performing a combined assessment of inherent and control risk, hence making room

for the auditors to evaluate other risk factors in an audit.

A study on the impact of risk-based audit on financial performance in Kenya’s

insurance companies conducted by Kasiva (2012) found out that risk-based auditing

through risk management should be enhanced to enable the organization concerned to

detect risks on time.

A survey was carried out of internal auditors’ risk management practices in the

Kenya’s banking sector, Kibaara (2007) concluded that, most banks in Kenya were in

the process of making the ERM process and strategies in line with risk assessment.

Implementing a risk-based strategy requires that life insurance companies and

intermediaries have a good understanding of the risks and are able to exercise sound

judgment. This requires the building of expertise within life insurance companies and

intermediaries, including for example, through training, recruitment, taking

professional advice and learning by doing.

According to Momo and Ukpong (2013), Equitable Life Assurance Society of United

Kingdom collapsed in the year 2000 due to mismanagement of funds by the directors

subsidize current annuity rate policies instead of the guaranteed annuity rate policies.

Skandia, Sweden's largest insurance company which leads in providing variable

annuities and other savings products also ruined its reputation in 2003 when three of

its top executives were investigated on misuse of firms assets.

The Kenyan insurance industry was mainly found to be vulnerable to economic risks

and legal risks. However, the industry was also affected by political risks,

technological risks, socio- cultural risks, geographical risks, management risks and

personnel risks to a moderate extent. These were mainly mitigated using, risk

avoidance, risk retention, risk transfer and risk reduction techniques. Towards

ensuring sustainability in the industry, there is an urgent need for the insurance firms

to frequently train their staff on risk mitigation, empower risk managers, identify and

train internal risk experts, and provide adequate budgetary allocations for risk

mitigation.

18

2.4.4 Product Mix Strategy and Performance

The indirect resource demand in addition to the effort involved in direct

implementation and maintenance with respect to product design and pricing processes

is considered to be rather significant. This product mix strategy concerns with finding

and communicating new uses of products. Lundholm, (2012) in their study using a

sample of 51,866 firms from 69 countries, found that credit facilities influence a

company’s profitability in that profitability negatively by leverage hence making

highly profitable firms to raise their capital through internal financing.

Memba (2015) evaluated the impact of risk management practices on financial

performance of life assurance firms in Kenya. The study found that adaptation of

premium valuation should be considered by the management on insurance firms to

enable financial performance of life assurance firms in Kenya.

Linbo & Sherril (2004) assessed the efficiency in relation to risk in large domestic

USA banks. They found that profit efficiency is related to credit risk and insolvency

risk but not to liquidity risk or to the mix of loan products..

2.5 Summary of Research Gaps

The empirical studies were reviewed in the preceding section focused on the different

credit institutions issues that affect the financial performance of credit unions. Much

has not been done on the financial performance of insurance firms in Kenya.

According to Boadi, et al. (2013), studies on profitability of Insurance industry have

not carried out especially in emerging and developing markets. Cagil and Karabay

(2010) assert that most of the studies on insurance industry have used Data

Envelopment Analysis to assess their financial performance with a few studies using

multivariate analysis. It is because of this reason that the present research used

multivariate analysis to study the influence of risk management practices on financial

performance of life assurance firms in Kenya with a concentration on adverse

selection problem. As a result, this study is designed to fill the aforementioned gaps

and provide concluding recommends having the main objective of analyzing.

However, these studies failed to whether there is a significant relationship between

risk mitigation strategies which as risk control strategy, risk limitation strategy,

19

product mix strategy has significant impact on performance of motor insurance

companies on the performance of motor insurance companies in Nairobi.

20

Table 2.1 Summary of Literature and Research gaps

Author Focus of the study Findings Research gaps Focus of the current study

Laurentis and

Mattei (2004

The study focused on Lessors’

recovery risk management

capability

The study found that

the development of

modern reliable

systems of

risk management can

enhance even more

those management

capabilities

The study failed to determine

influence of risk management

on performance specifically in

motor insurance companies

The current study focused on the effect of

risk mitigation strategies on performance

of motor insurance companies

Carey (2001) A survey of risk management

practices

The study found that

on average the lowest

percentage is on the

measuring, mitigating

and monitoring risk

that is 69% score as

compared to risk

management policies

and procedures that is

82.4%, and internal

control of banks that

is 76%.

The study failed to establish

whether risk management

practices impacted on

performance of the organization

The current study focused on the extent to

which risk mitigation strategies would

impact on organization performance

focusing on motor insurance companies

21

Liewellyn,

(1998

Effects of risk management

practices on Value Creation in

credit unions in Slovenia

The study found that

risk management

practice influence

Performance in

respect to ,efficiency

, productivity , capital

structure and liquidity

ratio

The study failed to establish

whether risk management

strategies had significant

influence on performance

The current study focused on the extent to

which risk mitigation strategies would

impact on organization performance

focusing on motor insurance companies

Kiragu (2014) The study focus on management

of change

The study found that

management of

change influence

growth in size and

profits and reduction

in the cost of

products

The study was limited to

establishing effects of change

management on performance of

insurance companies

The current study focused on the effects of

risk mitigation strategies on performance

of the motor insurance companies

Ndungu and

Gekara (2014

Impact of risk management

practices on performance of

insurance companies in Kenya

The study found that

risk avoidance,

transfer, control and

most importantly

accepting influence

performance

The study failed to establish

whether risk management

strategies impacted significantly

on performance

The current study filled the gap by

focusing on Risk control Strategy, Risk

limitation Strategy, Product Mix Strategy

and Risk Based Auditing Strategy.

22

Memba (2015 Assessment the influence of risk

management practices on

financial performance of life

assurance firms in Kenya

The study revealed

that underwriting

practices, claims

adjustment provisions

and premium

valuation methods

influence the

financial performance

of life assurance

firms in Kenya.

The study focus on underwriting

practices, claims adjustment

provisions and premium

valuation methods as risk

management practices

influencing performance in life

insurance firms

This study focused on risk mitigation

strategies, product mix, risk control, and

Risk limitation Strategy

Karabay (2010 The study focus on determining

influence of risk management

practices on financial

performance of life assurance

firms in Kenya with a

concentration on adverse

selection problem

The study found that

risk management

practices on financial

performance of life

assurance

This study sought the extent to

which risk management

practices on financial

performance of life assurance

firms in Kenya

However, this study found out that there

is a significant relationship between risk

mitigation strategies on the performance of

motor insurance companies in Nairobi

Source: (Author, 2017

23

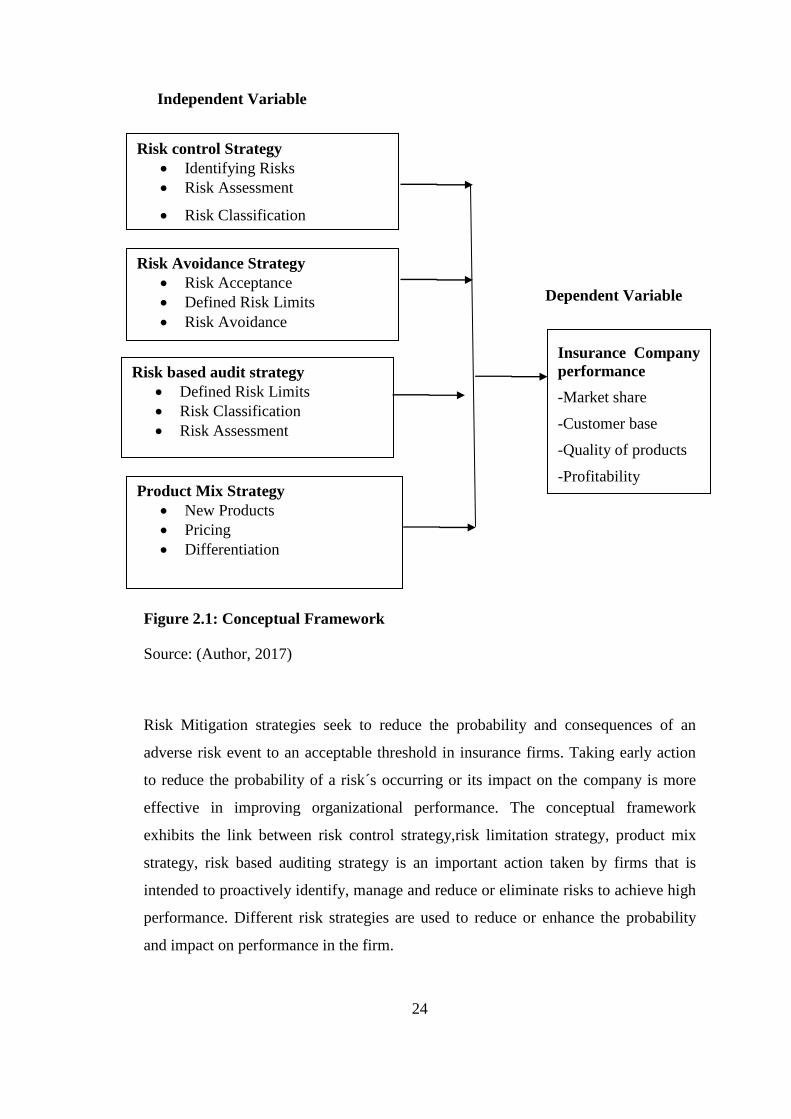

2.6 Conceptual Framework

Conceptual framework is a schematic presentation which shows variables that when

combined together explains the issue of concern. The conceptual framework is a set of

ideas used to show the relationship between the independent variables (factors) and

the dependent variables (outcome). Conceptual framework creates a link between the

research title, the objectives, the study methodology and the literature review

(Coulthard, 2004). Conceptual framework explaining the relationship between risks

mitigation strategies as the independent variable andperformance of insurance firms

as the dependent variable is presented in Figure 2.1.

24

Figure 2.1: Conceptual Framework

Source: (Author, 2017)

Risk Mitigation strategies seek to reduce the probability and consequences of an

adverse risk event to an acceptable threshold in insurance firms. Taking early action

to reduce the probability of a risk´s occurring or its impact on the company is more

effective in improving organizational performance. The conceptual framework

exhibits the link between risk control strategy,risk limitation strategy, product mix

strategy, risk based auditing strategy is an important action taken by firms that is

intended to proactively identify, manage and reduce or eliminate risks to achieve high

performance. Different risk strategies are used to reduce or enhance the probability

and impact on performance in the firm.

Risk Avoidance Strategy

Risk Acceptance

Defined Risk Limits

Risk Avoidance

Insurance Company

performance

-Market share

-Customer base

-Quality of products

-Profitability Product Mix Strategy

New Products

Pricing

Differentiation

Risk based audit strategy

Defined Risk Limits

Risk Classification

Risk Assessment

Risk control Strategy

Identifying Risks

Risk Assessment

Risk Classification

Dependent Variable

Independent Variable

25

CHAPTER THREE

RESEARCH METHODOLOGY

3.1 Introduction

The chapter presents the research design and methodology of the study. The chapter

therefore entails the way the study was designed, the data collection techniques and

the data analysis procedures.

3.2 The Research Design

The research used descriptive research design. This research design involves

collection of data that illustrates events and then organizes, tabulates, depicts, and

describes the data. (Onen & yuko, 2011). The descriptive survey research design

refers to a set of methods and procedures that describe variables. According to

Kothari (2004), a descriptive design involves execution of a plan, re-arranging,

collecting and analysis of data so as to provide information being sought.

This design is also used in collecting qualitative data to provide a great depth of

responses resulting in a better and elaborate understanding of the phenomenon under

study. Descriptive survey design portrays the variables by answering who, what, and

how questions. According to Mugenda and Mugenda (2003), descriptive design is a

procedure of acquiring quantitative and qualitative data so as to test hypotheses or to

answer the questions of the current status of the subject under study. Descriptive

research is used to illustrate the general characteristic of the study population and

show the relationship between the dependent and independent variables. The research

design was deemed fit to establish the effects risk mitigation strategies on

performance of motor insurance companies in Kenya.

3.3 Population of the study

According to Ngechu (2004), a population is a set of people, services, elements, and

events, group of things or households that are being investigated. This definition

ensures that population of interest is homogeneous. The study targeted all the 18

Motor insurance companies. The study population comprised of staff working in

motor insurance companies namely: the management, the staff at the corporate level

and the functional level who were credit officer, operation managers, finance officer,

26

chief auditors and chief IT officers and human resource directors making a total of

108 staff. Association of Kenya Insurers (2016).

Table 3.1: Distribution of Target Population of the companies and Employees

Population Category per Company Frequency

Operation Officers 18

Chief Auditors 18

Financial managers 18

Chief Accountants 18

Human resource directors 18

Chief IT officers 18

Total 108

Source: Association of Kenya Insurers (2016)

Cooper and Schinder (2003) defines sampling as a selection of a few items (a sample)

from a bigger group (population) to used on estimation on the relevance of an

unknown piece of information or outcome regarding the bigger group. A sample is a

representative part of the population that the researcher is interested in (Kumar, 2005).

Stratified sampling was used to select the sample of the study the method assures the

researcher that the sample was representative of the population in terms of certain

critical factors that had been used as a basis for stratification. Stratified samplings as

noted by Neuman (2003) is a procedure in which the population from which a sample

is to be drawn does not entail an identical group and hence requires comparisons

between various sub-groups. Kothari (2004) indicated that a minimum sample size of

20% or 30% of a large study population is sufficient for a study. Therefore the study

adopted a stratified random sampling and adopted a sample proportion of 50% as

indicated by Kothari (2004) to determine a sample size of 54 respondents.

27

Table 3.2: Distribution of the sample size

Strata Frequency Sample

Proportion

Sample

Size

Chairman of Audit Committee 18 0.5 9

Chief Auditors 18 0.5 9

Financial managers 18 0.5 9

Chief Accountants 18 0.5 9

Human Resource directors 18 0.5 9

Chief IT officers 18 0.5 9

Total 108 54

Source: Researcher 2016

3.4. Data sources and collection instruments

The main sources of data for this study were primary and secondary sources. This

data was collected using the questionnaires. Questionnaires ensured that details and

relevant information on the subject of study was collected. Questionnaires were used

in collecting data and consisted of a mixture of open ended and close ended questions.

According to Babbie, (1998), questions ought to be open ended and closed ended in a

questionnaire give room for intensity and richness of individual perceptions in

respondent responses.

The study used questionnaires because it is flexible and facilitates the capture of in-

depth knowledge of the respondents, promotes respondent cooperation and allows the

interviewer to probe further for clarification of issues. As a method of data collection

questionnaires are appropriate because of ease to analysis and is cost friendly

(Andersn, 2003).

3.5 Validity and reliability of Research instrument

3.5.1 Pilot Study

Piloting was carried out before the questionnaires are administered to the participants,

to certify that the questions are relevant, made sense and are clearly understandable.

The pilot study involved (10% of the sample size). The respondents were randomly be

selected to form the requisite sample size in the pilot study.

28

3.5.2 Validity

Creswell (2003) emphasizes that validity is the extent to which results are obtained

from data analysis of the data actually under study. There are two kinds of validity.

These include content validity and face validity. Face validity refers to the probability

that a question is misinterpreted or misunderstood. According to Cooper and

Schindler (2006) pre-testing is an efficient way to increase the chances of face

validity. Alternatively, content validity, also called logical validity, refers to the

degree to which a measure depicts all facets of a given social construct. This study

ensured both the face validity and the content validity.

3.5.3 Reliability

Reliability is the extent to which research instruments come up with consistent results.

The questionnaires reliability was statistically established by measuring the internal

consistency. In turn, internal consistency was measured by the use of Cronbach’s

Alpha (α). The alpha value ranges between 0 and 1 with reliability increasing

consistently with increase in value. Coefficient of 0.6-0.7 is a normally accepted rule

of thumb that designates acceptable reliability and 0.8 or higher indicates good

reliability (Greener, 2008). This study used cronbach’s Alpha test for the reliability of

the data collection tools, this was generated electronically with the help of SPSS.

3.6 Data Collection Procedure

The researcher sought a letter of introduction from Kenyatta University to be

presented to the motor insurance companies’ management. This may help the

researcher to gather information easily and the respondents involved in the study were

to be informed through writing. The researcher also obtained consent to collect data

through a letter to companies for the study and to be permitted to collect data and be

accorded assistance during collection of data. How the questionnaires were

distributed and how you ensured you collected appropriate data.

3.7 Data analysis and Presentation

The collected data was well examined and checked for completeness and

comprehensibility. Data was then summarized, coded and tabulated. Qualitative data

was analysed using content analysis to generate qualitative report which were

29

presented in a continuous prose. Quantitative data was analysed using descriptive

statistics such as means, standard deviation and frequency distribution were used to

analyse the data to establish the effects of risk mitigation strategies on performance of

insurance industry in Kenya: a case of motor insurance companies

Inferential statistics such as regression and correlation analysis was used to establish

the effects of risk mitigation strategies on performance of insurance industry in

Kenya: a case of motor insurance companies.The response on risk mitigation

strategies were measured by computing indices based on the responses derived from

the Likert-Scaled questions. The study adopted linear equation model as presented.

Y = α+ βX1 + β2X2 + β3X3 + β4X4+ є

Y= Performance

X1 = Risk Controlling Strategy

X2= Risk Avoidance Strategy

X3= Risk based audit strategy

X4= Product Mix Strategy

α = Constant

β= Coefficient factor

β1-4 = the regression coefficient or change included in Y by each χ,

є = error term

3.8 Ethical considerations

The ethical principle of confidentiality and respect are relevant and important in this

study. This is because slum upgrading project has encountered enough shares of

political witch hunt and envy. In this regard, informed consent of the respondents

were sought before recruitment into the study. Confidentiality and anonymity were

ascertained by using codes to represent the respondents instead of names and data was

collected in private and secure environment, only the people involved in collecting the

data had access to it.

30

Plagiarism which is an academic theft was avoided at all cost. With the help of

incitation and reference list, the researcher honestly acknowledged borrowed

resources from other previous scholars and authors. The study adopted APA 6th

edition to help evade plagiarism and any other form of academic dishonesty.

31

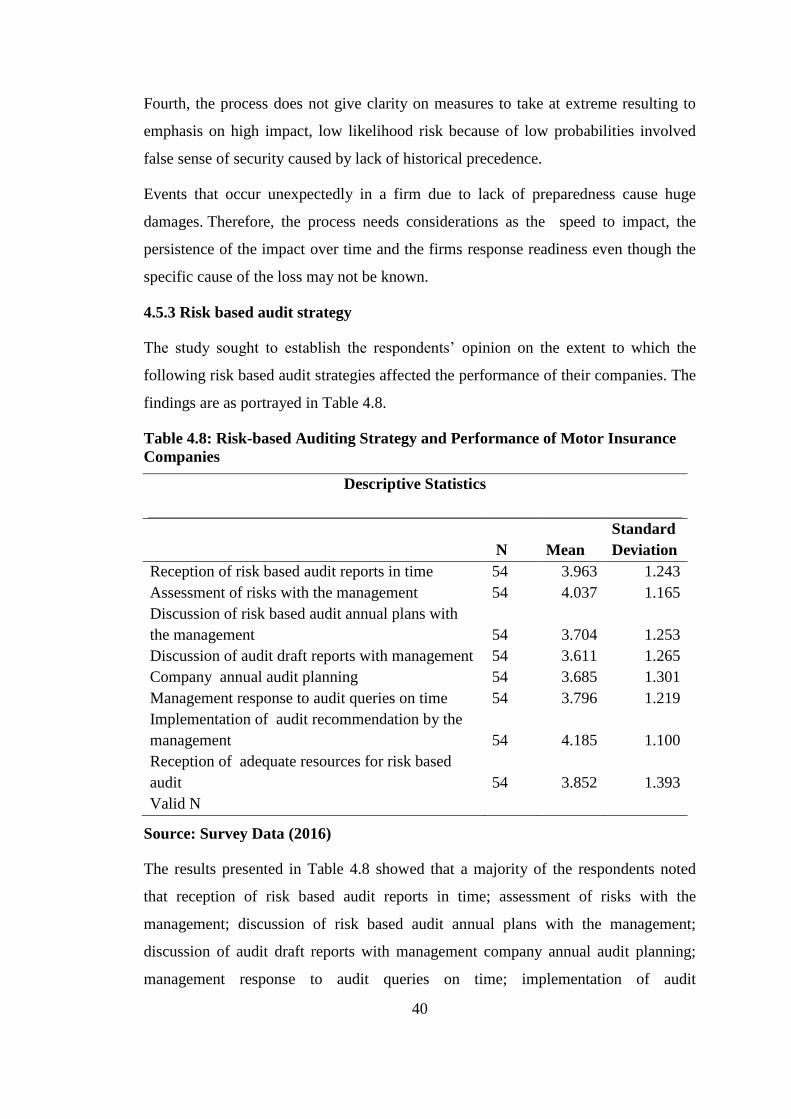

CHAPTER FOUR

DATA ANALYSIS, INTERPRETATION AND DISCUSSION OF THE

FINDINGS

4.1 Introduction

This section presents and discusses the findings on Risk mitigation strategies and

performance of insurance industry in Kenya. The findings are presented according to

the research objectives. The demographic characteristics were presented first,

followed by findings based on the objectives of the study.

4.2 Response Rate

The study targeted 54 respondents from the insurance sector and managed to get data

from all of them, this was a response rate of (100%), which was a sufficient response

rate for a valid scientific generalization. Onen and Yuko (2011) recommend a

response rate of above 80% as good enough for a scientific study.

4.3 Reliability Test of the Instrument

Five questionnaires were piloted by giving to individuals who were not included in

the final study sample. The 5 questionnaires were coded and responses input into

SPSS which was used to generate the reliability coefficient. The researcher used the

most common internal consistency measure known as Cronbach’s Alpha (α) which

will be generated by SPSS. It indicates the extent to which a set of test items can be

treated as measuring a single latent variable (Cronbach, 1951). The recommended

value of 0.7 was used as a cut–off of reliability for this study. All the variables were

found to be reliable since their Cronbach alpha was above 0.7 which was used as a

cut-off of reliability for the study. Table 4.1 shows the reliability results.

32

Table 4.1 Reliability of Risk Mitigation Strategies and Performance of Insurance

Industry

Variable No of Items Respondents α=Alpha Comment

Risk Control Strategy 8 5 0.723 Reliable

Risk Avoidance Strategy 6 5 0.758 Reliable

Risk-based audit Strategy 8 5 0.777 Reliable

Product Mix Strategy 7 5 0.764 Reliable

Performance 5 5 0.795 Reliable

Source: Survey Data (2016)

4.4 Demographic Characteristics of the Respondents

This section consists of information that describes the basic characteristics of the

respondents such as their gender, department of their work, the years of working in

the current company as well as their age brackets. These variables were carefully

selected as they were deemed to add more value to the findings and were in line with

the objectives.

4.4.1 Gender and Age of the respondents

The respondents were asked to indicate their age and gender. The findings are

presented in Table 4.2

Table 4.2 Gender and Age of Respondents

Count

Age

Total

Percent

(gender)

21-25 26-30 31-35 36-40 41-45 46-50

Gender

Male 0 2 8 14 5 4 33 61.1

Female 1 4 5 7 3 1 21 38.9

Total

1 6 13 21 8 5 54 100.0

Percent

(age) 1.90% 11.10% 24.1% 38.9% 14.8% 9.30% 100.0%