Risk Map Report 2016

33

RISKMAP REPORT 2016

-

Upload

red-fox-communications -

Category

Investor Relations

-

view

374 -

download

0

Transcript of Risk Map Report 2016

R I S K M A P R E P O R T

2016

Published by Control Risks, Cottons Centre, Cottons Lane, London SE1 2QG. Control Risks Group Limited (‘the Company’) endeavours to ensure the accuracy of all information supplied. Advice and opinions given represent the best judgement of the Company, but subject to Section 2 (1) Unfair Contract Terms Act 1977, where applicable, the Company shall in no case be liable for any claims, or special, incidental or consequential damages, whether caused by the Company’s negligence (or that of any member of its staff) or in any other way.

Copyright: Control Risks Group Limited 2015. All rights reserved. Reproduction in whole or in part prohibited without the prior consent of the Company.

All map data © OpenStreetMap contributors. Boundaries and names shown on maps follow globally accepted standards and do not imply any acceptance or endorsement whatsoever on the part of Control Risks.

Control Risks is a global risk consultancy. We help some of the most

influential organisations in the world to understand and manage the

risks and opportunities of operating across the globe, particularly in

complex and hostile markets.

Our unique combination of services, geographical reach and the trust

our clients place in us ensure we can help them to effectively solve their

problems and realise new opportunities in a dynamic and volatile world.

Working across five continents and with 36 offices worldwide, we

provide a broad range of services to help our clients to be successful.

R I S K M A P R E P O R T

2016Control Risks is delighted to launch RiskMap 2016, our global forecast of business risk. The year ahead is set to be a fascinating and testing one. As Control Risks CEO Richard Fenning writes in his introduction, insurgent forces in business and politics will challenge norms more than ever, requiring companies to be nimble and resilient as they navigate the contours of risk and opportunity.

RiskMap draws on our worldwide network of expertise to create the authoritative guide to the challenges and opportunities of the coming year. This year we have moved much of our RiskMap report online, where you will find an array of digital content to complement this book.

We will be hosting 26 RiskMap briefing events worldwide and numerous webinars. To find out more please go to riskmap.controlrisks.com

Hannah Kitt, Global Marketing Director

THE AGE OF INSURGENCY

01PENDULUM

SWING

05PLANNING FOR

‘6% CHINA’

09THE COMMODITIES

SUPERCYCLE: A PAUSE NOT AN END

13TINKER, TAILOR, (SOLDIER), SPY

17CYBER SECURITY

OUTLOOK

21ACTIVISM

IN 2016

25TERRORISM OUTLOOK

29MARITIME RISK

OUTLOOK

33MANAGING 21ST

CENTURY CRISES

37RISK RATING

FORECAST 2016

41

THE AGE OF INSURGENCY

RiskMap Report 2016

2

THE AGE OF INSURGENCY

RiskMap Report 2016

1

THE AGE

OF INSURGENCYRICHARD FENNING, CHIEF EXECUTIVE OFFICER

Welcome to RiskMap 2016, our annual preview of what the year ahead has in store.

In 2016, business and politics will be reshaped by a phenomenon common to both: insurgency. In both worlds, the established order is being challenged by disruptive forces that appear rapidly, upset the status quo and wrong-foot the powers that be.

GUERRILLA CAPITALISM

The business headlines are dominated by companies like Uber and Airbnb – usurpers in stodgy sectors unused to change and reeling from these new companies now fulfilling the promise and hype of the original dotcom boom. Harnessing extraordinary advances in computer processing power, they are running lean, outsourced operations able to move rapidly around the globe exploiting regulatory models designed for a different era. This new form of guerrilla capitalism, made possible by a step change in technological capability and a non-conformist

genius for innovation, will wreak havoc in other sectors as ill-prepared as the taxi and hotel businesses.

And not just in consumer sectors. In the oil business, fracking went from the margins of the industry to confronting the assumed economics of traditional producers in just a few years. The ability of the shale industry to adjust production, even as it took a clobbering from the collapse in prices, is typical of a new type of company: more mobile, more agile, and with the kind of flexibility that leaves the behemoths of the oil and gas industry struggling to reinvent themselves.

POLITICS OF INSURGENCY

This upheaval in business is mirrored in the world of politics. The new insurgent model – makeshift, audacious and willing to seek out unconventional funding – applies as much to Libyan militia gangs as it does to Palo Alto start-ups. And it goes beyond organisational theory right to the pinnacle of power. As I write this, the nomination process ahead of the US presidential election is being shaken up by an insurgent anti-politics that is propelling unlikely Republican candidates to the head of the pack. No doubt more mainstream candidates will eventually prevail, but this anti-establishment surge has rocked US politics to its core.

In China, where maintaining the external appearance of pervasive power is paramount, the wild

gyrations of the Shanghai stock exchange in 2015 reminded the political establishment that there are forces at work beyond its immediate control. This is occurring at a time when the task of adjusting the economy to an era of lower and different growth is reaching its critical phase – a process that has been likened to performing open heart surgery while the patient is running a marathon – making the leadership particularly nervous of triggering large-scale popular discontent at such a delicate moment.

Ironically, it is one of the Chinese government’s flagship initiatives – the anti-corruption drive – that could do just that. The purge of corrupt officials and businesspeople has tapped into a rich seam of pent-up public disgruntlement over persistent graft and incompetence. It now runs the risk of taking on a life of its own and turning on its creators, becoming one of those dynamic, disruptive forces fuelled by the frustrations that inevitably come from wholesale economic restructuring.

Similarly, Brazil is in the grip of zealous prosecutors pursuing allegations of corruption at state oil giant Petrobras that are extending into the highest echelons of society. The elite has seen any number of anti-corruption campaigns launched with great fanfare, only to see them fizzle out before they intrude on their cosseted lifestyle. But this one is now too close for comfort. It is one of those largely unplanned

phenomena, again propelled by grassroots agitation, that is reshaping the often sclerotic and cosy nature of Brazilian power.

DISRUPTERS CONFRONT REALITIES OF POWER

In India, arch-disrupter Narendra Modi must live up to his promise to change the way India is governed. Having swept to power with his own brand of Gujarati radicalism on a wave of iconoclastic popular support that shattered the Congress-dominated consensus, he now faces the same popular intolerance of inaction that he exploited so cleverly in opposition. And what applies to Modi in Delhi equally applies to President Joko ‘Jokowi’ Widodo in Jakarta. Beware the disrupter who is handed the reins of power.

Nobody should heed this maxim more than Russian President Vladimir Putin. Russian foreign policy has been built on a strategy of disruption – a skilful ability to unsettle the West in eastern Ukraine, Crimea and Syria with the aim of restoring Russia’s international prestige. Nobody should underestimate the ability of Putin and Foreign Minister Sergei Lavrov to continue to outmanoeuvre their opponents in this game of geopolitical chess, or the amount of genuine sentiment that underpins their domestic support. But the cold reality of the parlous state of Russia’s hydrocarbon economy cannot be ignored forever.

THE AGE OF INSURGENCY

RiskMap Report 2016

3

of bubonic plague. But current perception trumps historic relativity. The fact we have weathered these storms before means little if your boat is sinking before you reach the Greek coast, your company is left stranded by an unforeseen technical innovation or you have just discovered a 16-year-old hacker at large in your key database.

Nevertheless, it is important to challenge the idea that we face unprecedented calamity. Each year in RiskMap we are at pains to emphasise that, for all the apparent insecurity that surrounds us, the world remains full of promise for the well-prepared investor. Risk is a necessary precondition for opportunity, and 2016 will be no exception. To put our current anxieties into context, we have included in this year’s publication a RiskMap for 1975, the year Control Risks was founded. As you will see, there was plenty to be concerned about 40 years ago. But somehow the world survived, and four decades later we are immeasurably wealthier, healthier and in many ways safer than we were back then.

The search for a solution to the migrant crisis will dominate Europe in 2016. Mounting popular opposition to mass immigration – even in tolerant Germany, with its declining population – has all the hallmarks of single-issue insurgency outside mainstream politics that appeals to the visceral worries of Europeans fearful for their security in the wake of the attacks in Paris.

Elsewhere, unconventional forces continue to challenge the established order. In South Africa, the disrupter has become the disrupted. Robben Island alumnus President Jacob Zuma will continue to

face increasingly militant opposition from the attention-grabbing extra-parliamentary activities of Julius Malema’s Economic Freedom Fighters. More broadly, the ‘Born Frees’ – those born since the end of Apartheid without the same innate respect for the ANC as their parents – are losing faith in a parliamentary process dominated by a single party perceived not to be delivering on the promise of a better South Africa.

GLOBAL DISRUPTERS

Beyond the pale of politics and business sit malevolent disrupters. Islamic State (IS) fulfils all the criteria,

emerging from the embers of al-Qaida in Iraq to create an adaptive organisation that seems able to outwit the forces arraigned against it. Even if IS can be contained militarily in Iraq and Syria, it has demonstrated that it is able and willing to extend beyond the caliphate and strike cities in western Europe.

Less murderous but still pernicious are the cyber criminals who, on a daily basis, and often with few resources other than those available to tech-savvy teenagers, are able to penetrate the defences of the world’s biggest corporations. No wonder then that state-sponsored cyber teams are able to do such damage.

Behind all this disruption sits the biggest potential disrupter of all: the possibility of another financial crisis triggered by any combination of the end of cheap money, another eurozone crisis or a Chinese hard landing. The prospect of a repeat variation of 2008 may only be lurking in the shadows, but it is there. The prospect of Presidents Barack Obama, Xi Jinping and Putin coming together to avert financial peril seems sadly remote.

FORTY YEARS OF RISK

Every age thinks it is unique. And I am sure that our forebears would argue that there is nothing new in this notion of disruptive insurgency. No doubt they felt the same at the sudden onset of mechanised agriculture, Marxism or a new strain

PENDULUM SWING

RiskMap Report 2016

6

PENDULUM SWING

RiskMap Report 2016

5

PENDULUM SWING

JONATHAN WOOD, DIRECTOR

The post-Cold War order has fallen on hard times. The 2008-09 global financial crisis severely dented the legitimacy and attractiveness of free market capitalism, but accelerated the relative rise of major emerging markets – particularly China. Western retrenchment, a deliberate foreign policy reaction to a decade of disappointing foreign wars and severe fiscal challenges, left a global power vacuum prone to destabilising international competition.

The threadbare nature of world order was exposed by Russia’s annexation of parts of Ukraine, Islamic State (IS)’s conquests in Iraq and Syria, the Gulf states’ military campaign in Yemen, and China’s construction of naval and air bases in disputed parts of the South China Sea. As multilateral initiatives on trade, finance and climate change stumbled, geopolitical blocs such as the BRICS authored rival, parallel institutions. Rising powers and non-state actors – not the traditional Western custodians of global governance – started setting the global agenda.

But in 2016, the pendulum is likely to swing back towards traditional powers.

ECONOMIC STRENGTH

Emerging market growth is plunging, but in 2016 core economies – even the euro area – are likely to see their best annual performance since 2010. Growth is on track to significantly exceed the average of the last 15 years. Unemployment, the most visible and durable signature of the global financial crisis, is trending down: the strongest core economies – US and UK – are effectively at full employment, and even Greece and Spain, the weakest, are heading in the right direction.

Core countries are certainly not immune to the emerging market

slowdown, but as consumption-led economies they benefit from the resultant low commodity prices and cheaper manufactured imports. The persistent threat of deflation will convince Western central banks to maintain loose monetary policies, keeping any potential interest rate rises – most likely in the US and UK – small and gradual.

POLITICAL STABILITY

Western countries are hardly paragons of political efficiency, but at least they derive political legitimacy from democratic process rather than raw economic performance. The US presidential campaign is likely to temper both left- and right-wing impulses, damping the potential for disruptive policymaking in 2016. Meanwhile, stronger economic

growth should blunt the rise of fringe political movements in Europe, though this partly depends on whether the EU can craft a coherent response to the migration and refugee crisis.

By contrast, as we suggested in last year’s RiskMap, slow growth is a potentially serious threat to political stability in emerging markets and developing countries. Weak commodity prices impair patronage networks, welfare payments and financial stability. The slowdown confounds rising middle-class aspirations, accentuating calls for reform. Corruption scandals abound as opposition parties and electorates scrutinise government competence. Even if ultimately beneficial in terms of transparency,

EurozoneG7World EM

1

2

3

4

5

6

7

0

1980s 1990s 2000s 2010-15 2016

0

5

10

US

0

5

10

UK

0

10

20

30

0

10

20

30

Greece Spain

Average growth rates (%), 1980-2016: G7, Eurozone and emerging markets

Unemployment rates (%), Q1 2010 - Q2 2015, selected Western economies

PENDULUM SWING

RiskMap Report 2016

8

PENDULUM SWING

RiskMap Report 2016

7

Finally, threats from transnational Islamist extremism will continue. Al-Qaida remains intact – and in some venues enhanced – despite 15 years of aggressive counter-terrorism efforts; IS is very likely to prove equally resilient in 2016. A more interventionist policy in Syria will increase the intent of IS, its allies and sympathisers to conduct attacks in the West.

LAST GASP OR DEEP BREATH?

Its multi-decade growth acceleration over, China’s economy is entering a ‘new normal’ of single-digit expansion as it navigates the delicate transition to a consumption-led economy. Emerging markets in general face fundamental political transitions on the back of middle-class development. Barring a major new supply disruption, energy prices are likely to remain subdued for years as flexible US shale oil provides marginal ‘swing’ production. For all its bombast, Russia’s economy has suffered under the weight of low oil prices and Western sanctions, both of which will persist in 2016. Increased food and mineral production capacity, developed during the ‘commodities supercycle’, has alleviated scarcity concerns. Taken together, these trends could suggest a prolonged period of Western resurgence, beyond 2016.

We think this is unlikely. The conditions underpinning the post-Cold War world order – unrivalled US power and untrammelled global capitalism

– simply no longer apply. Emerging markets have arrived as economic and military powers, with the capacity to act as both essential partners and potential spoilers. States have forcibly inserted themselves into the global economy through the internationalisation of state-owned enterprises (SOEs), spread of sovereign wealth funds, massive accumulation of sovereign liabilities and creative manipulation of monetary policy. Global challenges, such as climate change or economic rebalancing, are essentially unsolvable without the participation of the key rising powers. Multipolarity is a fact, not a trend.

reform and legitimacy, these factors will make many emerging markets less predictable in 2016.

GEOPOLITICAL FLEXIBILITY

Just as financial and sovereign debt crises forced Western countries to turn inwards, dealing with domestic economic challenges and maintaining political stability will occupy emerging market attention in 2016. Counter-intuitively, this could provoke geopolitical instability as – deprived of growth – governments seek external sources of legitimacy, such as defending sectarian allies or promoting national greatness. Certainly, adventures by Russia, China and Iran in their near abroads – Ukraine, the South China Sea and Syria, respectively – have been very popular at home, if costly to maintain.

Stronger economic growth will confer strategic flexibility on Western powers. Energy security will not be a major concern, given the high likelihood of a persistent global oil supply surplus and accompanying low natural gas prices. Sovereign and financial risk, which is surging in emerging markets due to currency depreciation, is in abeyance in Europe and the US (thanks to the Greek bailout and US budget deal). Military expenditure is rising in many NATO member states for the first time since the global financial crisis, largely in response to the perceived threat from Russia. Financial and other sanctions remain – for now – powerful policy instruments.

An improved economic position will also support the political realisation that Western powers ignore global instability and insecurity at their peril. In a globalised world, the national security frontier is potentially everywhere. The US in particular is likely to adopt a more assertive international posture in the final year of President Barack Obama’s term, including escalating interventions in the Middle East, challenging China in East Asia, supporting counter-terrorism efforts in sub-Saharan Africa and beefing up NATO’s deterrence to Russia in Europe.

IMPLICATIONS FOR BUSINESS

A pendulum swing to traditional Western powers is likely to have a net stabilising influence during 2016. Expect more pragmatic and sustained diplomacy. The implementation of the Iran nuclear deal in 2016 will illustrate the effect of negotiation backed by credible leverage (such as sanctions). Western countries, often long on moralising but short on execution, are likely to be more selective and therefore more influential, even in intractable conflicts in the Middle East.

Greater economic transparency and predictability are also likely. Even as China drove the world economy, uncertainties about its economic policymaking, official statistics and domestic financial risks produced an aura of unpredictability around growth prospects. By contrast,

Western economies are better understood, produce more reliable data and have undertaken stabilising structural reforms since the crisis, especially in the financial sector. Firm commitment to continued liberalisation, illustrated by finalisation of the massive Trans-Pacific Partnership (TPP) trade agreement, means greater policy predictability – at least in 2016.

Finally, the perceived uncertainty of US strategic and security commitments – the central factor in the global power vacuum – will diminish as the US seeks to strengthen its global alliances and deflect military-industrial inroads by Russia, China and other defence suppliers.

But destabilising dynamics will persist. Western strength would validate the dominant strategic concern of China and Russia, namely that they are being ‘contained’ by the US and NATO, respectively. This will preserve high levels of domestic political support for confrontation and may encourage escalatory actions to maintain or regain initiative. Russia’s near abroad and the East and South China Seas will remain geopolitical hotspots in 2016.

The Syria conflict will persist: more concerted military assistance and direct action will not lead to any resolution. No side in the conflict is likely to achieve decisive strength in 2016, and increasingly open proxy warfare boosts the likelihood of security and diplomatic spillovers.

PLANNING FOR ‘6% CHINA’

RiskMap Report 2016

10

PLANNING FOR ‘6% CHINA’

RiskMap Report 2016

9

PLANNING FOR

‘6% CHINA’ANDREW GILHOLM, MANAGING DIRECTOR

LOUIS KUIJS, HEAD OF ASIA ECONOMICS, OXFORD ECONOMICS

In 2015, Chinese GDP expanded at its slowest annual rate since Deng Xiaoping launched his historic reforms in 1978 (excluding the sanctions years of 1989 and 1990). The 11-trillion-dollar question of China’s economy looks more pressing than ever: is it on the brink of crisis and a collapse in growth, or is it just experiencing turbulence as it transitions to another phase in its development?

The short answer is that China is not ‘on the brink’. However, growth will not rebound to old rates and rebalancing – though underway – will not be smooth. Oxford Economics sees growth likely to slow from 6.3% in 2016 to nearer

5% by 2020. Business leaders should forget ‘bulls versus bears’ debates predicting either continuity or collapse, and focus on figuring out how a more likely ‘middle’ scenario could affect them. This means understanding divergent trends in different parts of the economy and emerging government policy responses – some of which look increasingly ominous for multinationals.

HOLD THE OBITUARIES

2015 saw the biggest souring of sentiment on China since 2008. This spread belated recognition of the gravity of current challenges to growth, but was mainly triggered by the wrong issues. Panicky responses from international markets and media to China’s

summer stock market slump were out of all proportion to its significance for the real economy. Debate on the reliability of official data was another distraction: Beijing’s GDP numbers probably understate the slowdown, but divergent assessments of its severity reflect issues with statistics and disparate trends within the economy, not necessarily a big cover-up.

Property weakness and industrial overcapacity will continue to hit some sectors and regions very badly, but policy easing and reasonably resilient consumption will provide a cushion, especially for services and light industry. As many industries and indicators send monthly distress signals in 2016, it will be important not to lose perspective.

First, China has not suddenly gone from unstoppable growth engine to spent force. Even after three decades of breakneck growth, many measures show there is still much more room for rapid ‘catch-up growth’ – China’s economy still looks like 1960s Japan, not 1990s Japan. Meanwhile, the national savings ratio (around 50% of GDP), a still modest banking loan-to-deposit ratio (80%) and a structural current account surplus provide a significant – if shrinking – buffer against problems such as asset bubbles and rising debt.

Second, growth falling below a certain level is not a trigger for – or even a strong predictor of – social or political instability. This notion was bogus in the mid-2000s and during

12 FORECAST

10

8

4

6

2

0

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20 15010050 200

-6

-8

-10

-12

2

-4

4

-2

China, 2015

Japan, 1990

South Korea, 1997

Thailand, 1997

UK, 2007

US, 2007

Spain, 2007

Loan-to-deposit ratio, %

Cur

rent

acc

ount

, % G

DP

6

0

China: Real GDP growth (%), 2010-20 A systemic financial crisis is still unlikely

Source: Oxford Economics/Haver Analytics Source: Oxford Economics, Haver, CEIC Data

PLANNING FOR ‘6% CHINA’

RiskMap Report 2016

12

PLANNING FOR ‘6% CHINA’

RiskMap Report 2016

11

incremental change in the next few years. Whether such a cautious approach is enough to reverse some negative trends, and whether recent steps snowball or stagnate, depends on Xi. Official media paint him as a frustrated reformer blocked by vested interests, implying he may do more after consolidating control at the 2017 Communist Party congress. But Xi’s conservative political instincts suggest he only buys into market reform insofar as it preserves, not dilutes, the Party-state’s monopoly on power, with all the limitations and tensions that implies.

THE BIG SQUEEZE

Such existential economic dilemmas are still a relatively long-term issue, but one aspect of reform is likely to cause more immediate concerns: the emerging ‘Made in China’ strategy announced in 2015. In some respects this is typical of an emerging market government supporting industrial upgrading to escape the ‘middle income trap’. China is likely to be relatively successful in this regard compared with some other Asian economies, such as Thailand and Malaysia. However, ‘upgrading’ seems likely to involve aggressive industrial policy tools that will intensify a big, uncomfortable squeeze from slower growth; pressure on pricing, margin and market share; localisation demands; and tighter regulatory enforcement.

We discuss the Made in China agenda in more detail in one of our RiskMap podcasts, because for many multinationals the outlook is troubling: ‘6% China’ will be too big and fast-growing a market not to remain a major part of their global business, but it will be an even tougher place to do that business.

Another feature of 6% China may be further periodic policy and market volatility. Beijing needs the benefits of more open financial markets, but tools like capital and currency controls have been a pillar of stability in past crises. The desire to wield a veto over markets remains strong, and when it interferes with policymaking it can shake confidence.

Adding to policy tensions, a large chunk of the top leadership is due to retire at the 2017 congress and promotion manoeuvring has begun. A second term for Xi is not under threat, but elite politics is much more opaque than it seems from all the confident coverage and commentary. Anyone who doubts this should recall that in little over a year after taking power, Xi went from being seen as a relatively weak leader to being declared ‘the strongest since Mao Zedong’. 2016 will bring further tests not only of that still unproven strength, but of what Xi will do with it.

the global financial crisis, when the theory of ‘sub-8% growth equals unrest’ kept cropping up. It has resurfaced with a lower growth number, but the logic remains weak. The slowdown creates very real strains, but companies on the ground are mainly seeing localised operational and ‘micropolitical’ impacts such as labour strife, engaging official stakeholders during restructuring, or disputes with cash-strapped local governments. Macropolitical risk certainly demands scrutiny in 2016, but not for some economic ‘trigger point’.

So far, this sounds like the same bullish case made to debunk doomsaying amid cries of imminent ‘hard landing’ a decade ago, or in late 2008 as Chinese growth plunged during the global financial crisis. But to be clear, there are more clouds on

the horizon now and less room for complacency. Political indicators in 2015 raise questions about long-term growth and the short-term environment for foreign companies.

AGILE AUTHORITARIANS?

Beijing has proved sceptics wrong before by reforming its way out of trouble, and may well do so again. It has a track record of competent policymaking and of executing major reforms to adapt its economy when facing trouble. This is partly a systemic strength: Chinese leaders have more room than their democratic peers to accept short-term restructuring pain for long-term growth gains. But such bold gambits also relied on leadership, as with Deng’s reforms in 1978 and 1992, and former premier Zhu Rongji’s SOE and banking reforms, and WTO entry.

President Xi Jinping raised hopes of recapturing this agility after a gambit-free decade under his predecessor. A 2013 reform blueprint, though vague, stressed the ‘decisive role’ of the market. Moves to centralise decision-making were widely interpreted as giving Xi more power to drive through change. But evidence from key policy areas in 2015 offered little to support the image of Xi the strongman reformer.

Take SOE reform. The government knows another overhaul is essential to boost competition and a stifled private sector, and to rein in industrial overcapacity and debt. Restructuring has long faced resistance and Xi seemed armed to overcome it. New ‘leading groups’ sit above notorious bureaucratic ‘silos’ and an unrelenting anti-corruption crackdown has cowed powerful SOEs. Yet the SOE reform plans that emerged in 2015 smack more of tinkering than transformation. They look symptomatic of exactly the siloed, consensus-constrained approach that prevailed before Xi. Other important but thorny policy arenas, such as fiscal and healthcare reform, show a similar lack of thrust.

This is not to say that nothing is happening. An optimistic reading would be that it was never realistic to think Xi could enact sweeping reforms in his first term amid a serious slowdown, but that he has put in place important foundations for a cycle of self-reinforcing,

OTHER METALS STEEL

2009 201520142013201220112010200820072006

8

7

6

5

4

3

2

1

0

Harder budget constraints are urgently needed: profit margin (%)

Source: Oxford Economics, CEIC Data

THE COMMODITIES SUPERCYCLE: A PAUSE NOT AN END

RiskMap Report 2016

14

THE COMMODITIES SUPERCYCLE: A PAUSE NOT AN END

RiskMap Report 2016

13

THE COMMODITIES

SUPERCYCLE:

A PAUSE NOT

AN END

MICHAEL MORAN, MANAGING DIRECTOR

Is the commodities supercycle, the great transformative economic trend of the early 21st century, a thing of the past? Many analysts now say yes and have consigned the great explosion of commodity prices that began as the last century ended to history. We believe they are wrong, at least in part: the supercycle is not over, but merely in a swoon, laid low by anaemic global growth rates and some dubious purchasing practices.

The downturn in commodity prices that started in late 2012 has hit bottom, even though gluts persist in some vital markets – in oil and gas, thanks to fracking in the US and a global economic slowdown, and in steel, aluminium and copper, thanks to Chinese stockpiling during the boom. Oxford Economics, our joint-venture partner, already sees signs of a price revival for some metals and alloys, an indication that a gradual depletion of excess inventories is having an effect.

That’s the good news – at least if you are an exporter of raw material, or a

mining firm specialising in those alloys. The bad news is that the high value of the US dollar, in which most trade is settled, and the low growth rates of the world’s largest economies will mean the glut depressing prices of most commodities will take longer to work through the metabolism of the global economy.

The bottom line: prices for energy and most commodities will stay low in 2016, but will rise gradually as the decade continues. The supercycle – like globalisation itself – has not died, so much as been temporarily kicked into reverse. Unlike globalisation, which survives only as long as the global consensus about free trade and political stability, the laws of supply and demand suggest that commodity prices (oil excepted) will soon start to rise again.

HOW WE GOT HERE

Context is crucial. Starting in 2000, commodity prices boomed for a variety of reasons. They drew fuel from the voracious demand of China and other emerging market economies. Political risk also played a part as shocks such as the September 2001 attacks in the US, the Iraq war and the Arab spring threatened to disrupt global supply lines.

This boom in prices was not episodic and was not confined to just a few commodities. Individual commodity prices will rise and fall for reasons very specific to those markets. But from 2000 to 2012, dozens of commodities rose and fell (mostly rose) in lockstep – thus the supercycle – acting as a great transfer of wealth, capital and

influence from commodities importers to exporters, from the advanced to the emerging market economies.

China’s importance is easy to see. Soon after 2000, it became the world’s largest consumer of commodities, purchasing 40% of all natural resources traded internationally in 2000-12, according to the IMF. Demand rose in other emerging markets too, as their middle classes swelled and consumption boomed. But it was China’s buying spree in particular – both its scale and its propensity to buy much more than it needed and stockpile the surplus – that kept prices rising. The severing of the link between demand and acquisition by China’s purchasing managers probably made the current correction inevitable.

200

120

140

160

180

100

80

20082007200620052004200320022001 20152014201320122011201020092000

60

40

20

0

15

10

5

0

ENERGY MINERALS AGRICULTURE CHINA GDP

Commodity price indices (nominal USD) and Chinese GDP growth (%), 2000-15

Source: World Bank

THE COMMODITIES SUPERCYCLE: A PAUSE NOT AN END

RiskMap Report 2016

15

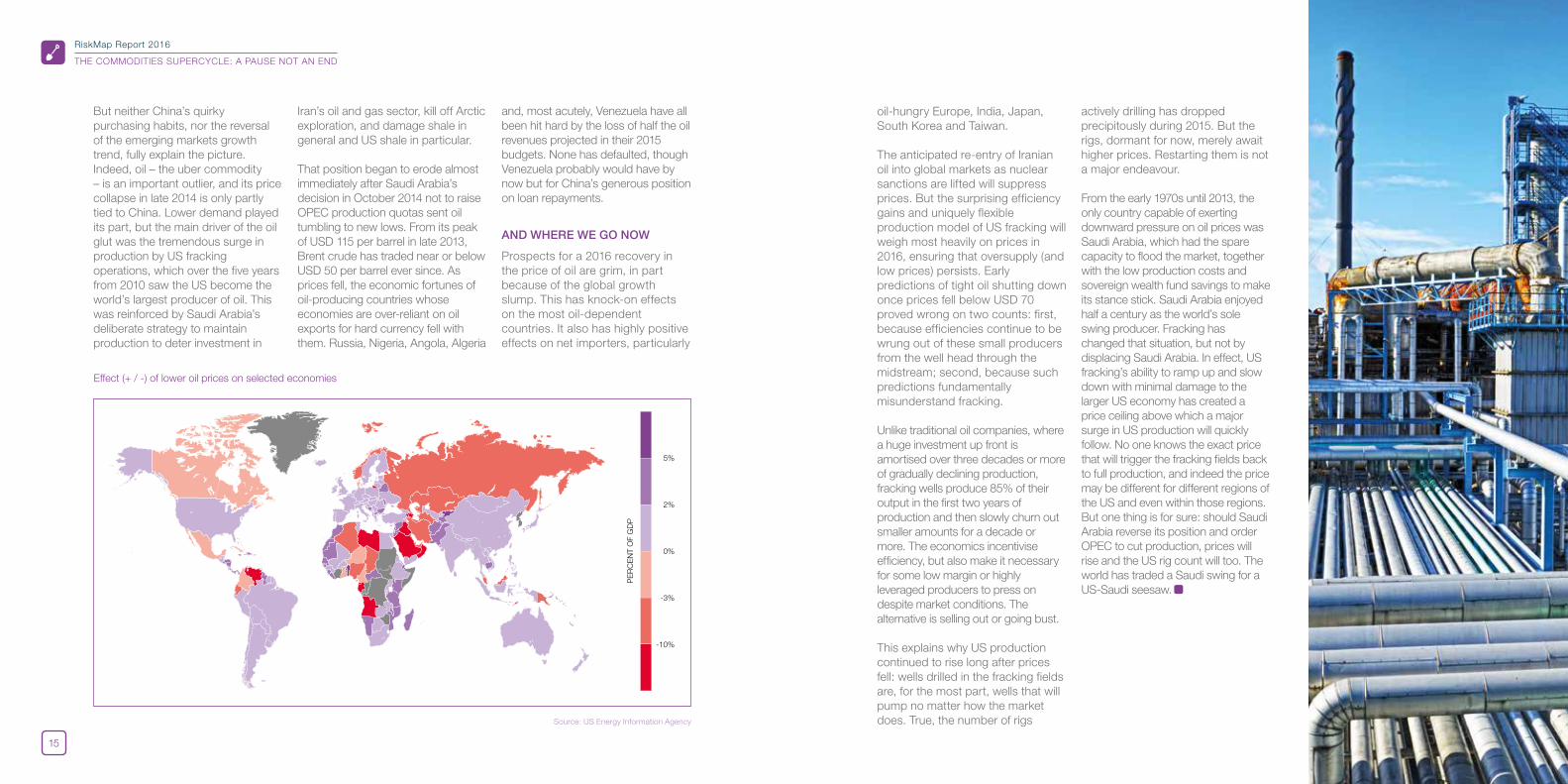

oil-hungry Europe, India, Japan, South Korea and Taiwan.

The anticipated re-entry of Iranian oil into global markets as nuclear sanctions are lifted will suppress prices. But the surprising efficiency gains and uniquely flexible production model of US fracking will weigh most heavily on prices in 2016, ensuring that oversupply (and low prices) persists. Early predictions of tight oil shutting down once prices fell below USD 70 proved wrong on two counts: first, because efficiencies continue to be wrung out of these small producers from the well head through the midstream; second, because such predictions fundamentally misunderstand fracking.

Unlike traditional oil companies, where a huge investment up front is amortised over three decades or more of gradually declining production, fracking wells produce 85% of their output in the first two years of production and then slowly churn out smaller amounts for a decade or more. The economics incentivise efficiency, but also make it necessary for some low margin or highly leveraged producers to press on despite market conditions. The alternative is selling out or going bust.

This explains why US production continued to rise long after prices fell: wells drilled in the fracking fields are, for the most part, wells that will pump no matter how the market does. True, the number of rigs

actively drilling has dropped precipitously during 2015. But the rigs, dormant for now, merely await higher prices. Restarting them is not a major endeavour.

From the early 1970s until 2013, the only country capable of exerting downward pressure on oil prices was Saudi Arabia, which had the spare capacity to flood the market, together with the low production costs and sovereign wealth fund savings to make its stance stick. Saudi Arabia enjoyed half a century as the world’s sole swing producer. Fracking has changed that situation, but not by displacing Saudi Arabia. In effect, US fracking’s ability to ramp up and slow down with minimal damage to the larger US economy has created a price ceiling above which a major surge in US production will quickly follow. No one knows the exact price that will trigger the fracking fields back to full production, and indeed the price may be different for different regions of the US and even within those regions. But one thing is for sure: should Saudi Arabia reverse its position and order OPEC to cut production, prices will rise and the US rig count will too. The world has traded a Saudi swing for a US-Saudi seesaw.

But neither China’s quirky purchasing habits, nor the reversal of the emerging markets growth trend, fully explain the picture. Indeed, oil – the uber commodity – is an important outlier, and its price collapse in late 2014 is only partly tied to China. Lower demand played its part, but the main driver of the oil glut was the tremendous surge in production by US fracking operations, which over the five years from 2010 saw the US become the world’s largest producer of oil. This was reinforced by Saudi Arabia’s deliberate strategy to maintain production to deter investment in

Iran’s oil and gas sector, kill off Arctic exploration, and damage shale in general and US shale in particular.

That position began to erode almost immediately after Saudi Arabia’s decision in October 2014 not to raise OPEC production quotas sent oil tumbling to new lows. From its peak of USD 115 per barrel in late 2013, Brent crude has traded near or below USD 50 per barrel ever since. As prices fell, the economic fortunes of oil-producing countries whose economies are over-reliant on oil exports for hard currency fell with them. Russia, Nigeria, Angola, Algeria

and, most acutely, Venezuela have all been hit hard by the loss of half the oil revenues projected in their 2015 budgets. None has defaulted, though Venezuela probably would have by now but for China’s generous position on loan repayments.

AND WHERE WE GO NOW

Prospects for a 2016 recovery in the price of oil are grim, in part because of the global growth slump. This has knock-on effects on the most oil-dependent countries. It also has highly positive effects on net importers, particularly

PE

RC

EN

T O

F G

DP

-10%

-3%

0%

2%

5%

Effect (+ / -) of lower oil prices on selected economies

Source: US Energy Information Agency

TINKER, TAILOR, (SOLDIER), SPY

RiskMap Report 2016

18

TINKER, TAILOR, (SOLDIER), SPY

RiskMap Report 2016

17

CHARLES HECKER, SENIOR MANAGING DIRECTOR

This is a book of forecasts, but for a moment, please cast your mind back. Do you remember the television images of Russian President Vladimir Putin eating dinner alone at the 2014 G20 summit in Brisbane, Australia? Russia had just annexed Crimea and Malaysian Airlines flight MH17 had just been shot from the sky. Ostracised by polite political society, Putin looked like an unpopular teenager shunned into the corner of the school cafeteria.

If anyone was at the nadir of his geopolitical fortunes, it was the lonely Russian president and his plate of tepid summitry.

Now cast your mind forward. The same Russian president has launched airborne attacks on rebel and Islamic State positions in Syria. He has altered the order of things in that conflict and, probably, beyond. The same people who froze out Putin in Brisbane are now chilled by the prospect of a resurgent Russia.

If geopolitical fortunes can rise and fall over the course of a meal, and if global events can whipsaw rapidly from one extreme to another, what are we meant to think about the nature of power? How firm is anyone’s grasp on the stewardship of global events?

In other words, who is in control?

The three most powerful leaders in the world are – in no particular order – US President Barack Obama (we’ll call him Tinker), China’s Xi Jinping (we’ll call him Tailor) and Vladimir Putin (you get the message). Each of them would eagerly shape the world in their own fashion. If only they could.

In 2016, a combination of international pressures and domestic restraints will prevent any one of these leaders from moulding global events to suit his agenda. This might be a good thing – unchecked power concentrated in anyone’s hands would seriously destabilise an interconnected world. But this fragile, competitive triumvirate will not ease any of the world’s most severe geopolitical crises.

THE WARY REALIST

Just as the time approaches to contemplate retirement – building a presidential library, working on that tricky tee shot – Obama has scored some significant political wins. The second half of his second term has seen hard-fought domestic

(economic recovery) and foreign (Iran, Cuba) policy victories. This is contrary to the impression that his presidency has achieved little on either front. His lack of success in the Middle East has not helped, but no one seems capable of doing anything in that region. Obama, the Tinker, has always had a pained, cerebral approach to politics foreign and domestic. In setting his foreign policy agenda, he resembles a man about to tread a path of smouldering coals.

Some say that Obama’s international posture betrays a president uninterested in foreign affairs. This is not the case. He is not, however, interested in the same brand of foreign affairs of interventionists like John McCain or George W Bush. Where some easily segment the world into extremes, Obama sees nuance. He knows how hard it is to genuinely ‘win’ at anything in modern geopolitics.

The US is now politically an inward-looking country, weary of foreign engagements. It has withdrawn from Iraq; it has almost withdrawn from Afghanistan. It has shied away from Syria and the Middle East more broadly. If the Republicans win the White House at the end of 2016, they would seek to dismantle the Iran deal faster than you can say ‘centrifuge’.

To be sure, the US and its global military footprint remain a significant guarantor of the status quo around the world. As a result, no one is

really in the mood to pick a fight. That said, it feels like the status quo is under attack everywhere. And the US is now reluctant to put boots on the ground in times of acute crisis. Conflict brews and boils over on almost every continent.

BACK AT THE TABLE

This is the perfect power vacuum for Putin to exploit. And the timing could not be better. A world with a deep sense of turmoil lacking resolute leadership presents an ideal opportunity for Putin to re-insert himself and his nation into global affairs on the grandest of scales. ‘Finally’, he must be thinking, ‘we’re back in the mix’.

Putin confounded – even embarrassed – the rest of the world with the annexation of Crimea in 2014. This won Russia international recognition, to be sure, but perhaps not the kind Putin yearned for. But then: Syria. Russia’s air intervention in Syria achieved Putin’s immediate goal of being taken instantly seriously as a decisive commander-in-chief at the helm of a country to be reckoned with. Many group dinners followed.

Putin has once again proven a master manipulator, forcing the international diplomatic community into tortured contemplation. Fifteen years since taking the helm of the world’s largest country, seasoned Russia experts everywhere still ponder Putin and the country he rules. Is Russia a lamentable

TINKER, TAILOR,

(SOLDIER), SPY

TINKER, TAILOR, (SOLDIER), SPY

RiskMap Report 2016

20

TINKER, TAILOR, (SOLDIER), SPY

RiskMap Report 2016

19

No one doubts that China’s role on the world stage is fixed. But for the moment, China is the sort of country that other countries – and companies – want to gain favour with. They’re afraid of China, but more afraid of what might happen if they anger China, rather than what the country might do unprovoked.

This lack of consistent global leadership and the insecurity it engenders come at a time when nations and the business community seem more than ever to crave stability and predictability. This is cause for concern in 2016. It is not, however, cause for alarm. We remain in the throes of the transition from a predictable, neatly ordered world to something new. Should we expect a soldier soon? Perhaps it will be ever thus.

has-been whose economy continues to shrink and whose currency continues to languish? Or is it a potentially lethal loose cannon governed by an unpredictable strongman? The narrative of hair-trigger hubris and fighter jets suggests that we must soon stop the prolonged puzzling.

In the end, the precise reasons for intervening in the Syrian conflict don’t really matter. Putin’s Syrian adventure is more a geopolitical antic than a well-considered Middle East strategy. But it happened. Now, the global order and, in the wake of the aviation disaster over

the Sinai, Russia too will have to reckon with the fallout. The crisis in Syria and the broader picture in the Middle East – particularly Russia’s relationship with Iran – will be some of the greater casualties of Putin’s adventurism on a global scale. (Short of full-scale war, Russia’s relationship with the US and the EU could hardly get much worse.)

TWIN CHALLENGES

No one seems to be in two minds about how important China is. But Xi must periodically feel like he is running two countries. On the international stage, China is an

object of obsessive attraction and fearful respect. Domestically, China is experiencing economic and social convulsions likely to severely test the Party’s formula for ‘resilient authoritarianism’. Promoting one while harnessing the other must not be easy. Until China is in sync domestically and internationally, it will never fully be the world’s superpower. For the time being, Xi is the Tailor – carefully weaving his country into the global political and economic fabric. The domestic problems? Hide them behind a silken lining.

Xi’s remarkable power consolidation has relied heavily on an unprecedented crackdown on corruption – the most sustained and far-reaching in modern Chinese history, taking down hundreds of officials, including many heavyweights. Like any leader with a loaded agenda of international and domestic priorities, Xi must be looking for where the tipping points lie. Ultimately, his challenge is one of stewardship: keeping a country in transition on course and convincing China’s international partners that a sure hand remains in control.

It is that narrow, but sharp sliver of doubt that most undermines China’s emerging role on the global stage. Many companies will spend 2016 assessing their exposure to China, wondering if the country can manage to brake without skidding.

CYBER SECURITY OUTLOOK

RiskMap Report 2016

22

CYBER SECURITY OUTLOOK

RiskMap Report 2016

21

OUR FORECAST FOR THE TOP FIVE MOST IMPACTFUL CYBER ATTACK TECHNIQUES OF 2016

Scores as at Oct 2015.

The threat score considers the actors involved, the tools used and the attack method’s severity, impact and likelihood of success.

Under 5 – low-level threat: awareness important but immediate action not required.

5-7 – medium-level threat: organisations should seriously consider implementing mitigation measures.

7-10 – high-level threat: organisations must immediately take measures against the threat.

HARDWARE COMPROMISE7.99

7.11

APT OPERATIONS7.07

7.07

DATA LEAK6.53

CRIMINAL TARGETED ATTACK

RANSOMWARE

CYBER SECURITY OUTLOOK

JOHN NUGENT, SENIOR CONSULTANT

CYBER SECURITY OUTLOOK

RiskMap Report 2016

24

CYBER SECURITY OUTLOOK

RiskMap Report 2016

23

All data is sourced from Control Risks’ Cyber Threat Intelligence reporting.

DEFINITIONS

Impact – Impact is based on the assessed magnitude of the effect of the attack on the confidentiality, integrity and availability of systems and information targeted, as well as the value of those assets.

APT campaigns – Advanced persistant threat campaigns: nation-state-led espionage operations.

Data leak – Public exposure of information with a commercial or reputational value.

Hardware compromise – Compromise of the integrity of physical systems.

Ransomware – Malicious software that prevents or limits users from accessing their system or files (often through encryption) to extort victims.

Criminal targeted attacks – Campaigns using advanced techniques to steal from specific pre-selected targets.

INCREASE IN AVERAGE IMPACT OF CYBER ATTACKS

18%INCREASE IN NUMBER OF POLITICALLY MOTIVATED CYBER ATTACKS

56%INCREASE IN NUMBER OF CRIMINAL TARGETED ATTACKS

100%

16% TELECOMMUNICATIONS

26% FINANCIAL

14% RETAIL

8% OIL AND GAS

36% GOVERNMENT

Sectors targeted (% total attacks)

THE NUMBER AND IMPACT OF CYBER ATTACKS INCREASED FROM OCTOBER 2014 TO OCTOBER 2015.

GOVERNMENT AND FINANCE WERE ESPECIALLY TARGETED.

50

40

30

20

10

0

2014 Q4 2015 Q1 2015 Q2 2015 Q3 2015 Q4 2016 Q22016 Q1

A GREATER NUMBER OF NATION STATES WILL CONDUCT ATTACKS, WITH A LARGER PROPORTION CAPABLE OF OPERATIONS WITH A SEVERE IMPACT.Number of distinct nation states engaging in cyber operations each quarter between October 2014 and October 2015�

Average threat score for cyber attacks targeting ICS

Impact of cyber attacks on integrity of systems and data (index, Jan 2015=100), Jan-Oct 2015

A BROADER RANGE OF THREAT ACTORS WILL TARGET INDUSTRIAL CONTROL SYSTEMS (ICS), WITH A GREATER IMPACT.

ATTACKERS WILL INCREASINGLY FOCUS ON MANIPULATING DATA, AFFECTING ITS INTEGRITY RATHER THAN ITS CONFIDENTIALITY OR AVAILABILITY.

We forecast that in 2016 there wi l l be at least

37% riset a r g e t i n g

By the end of 2016 we expect a

In 2016 we forecast a integrity of systems and data rise in the threat

posed to the

in the severity of cyber attacks

c o m p a r e d w i t h 2 0 1 5I C S

45 15% increase

<

act ively conduct ing cyber operations and a

in the impact of their attacksnation states

2016

(WORST CASEFORECAST)

9.22015

6.720144.0

350

300

250

200

150

100

50

0

40%

JAN FEB MAR APR MAY JUN JUL AUG SEP OCT NOV DEC JAN 2016

TREND

TREND

ACTIVISM IN 2016

RiskMap Report 2016

26

ACTIVISM IN 2016

RiskMap Report 2016

25

Activists will pose new challenges in 2016 as they continue to expand their range of targets and tactics. In particular, campaigns against businesses that are resistant to their methods are shifting the focus to suppliers, contractors, regulators and financers of the main target. As a result, some companies may find themselves unexpectedly in the firing line.

Secondary and tertiary targeting was pioneered by animal rights activists, but is becoming more widespread. The tactic gives activists a better chance of finding an accessible target and of gaining the element of surprise by putting pressure on companies that are unprepared for protests. Activists of all stripes will increasingly look to find weak links in target companies’ supply chains, hoping that businesses less inured to protests will lack the capability or resolution to combat sudden activist activity.

Banks, transport companies and even cultural bodies linked to targeted industries will increasingly find themselves the focus of activism. Environmental groups have begun to target banks and politicians linked to support for fracking. Law firms and investors supporting North American energy projects are also increasingly the subject of protests.

Activist groups seeking to target maritime operations are particularly likely to rely on secondary and tertiary targeting. Offshore oil and gas exploration and extraction take place in areas inaccessible to most activists. Campaigners will instead look to target supply and support vessels, which are far easier to reach in key commercial ports, as with Greenpeace’s blockade in mid-2015 of support vessels in Seattle (US) destined for Arctic operations.

NEW METHODS

New technologies will offer new opportunities. Cyber attacks can paralyse systems through distributed denial of service (DDoS) attacks and damage

ACTIVISM IN 2016

MOLLY MCPARLAND, ASSOCIATE ANALYST

ACTIVISM IN 2016

RiskMap Report 2016

28

ACTIVISM IN 2016

RiskMap Report 2016

27

such single-issue campaigns are unlikely to forge a sustainable, international movement.

Even local campaigns will benefit from wider alliances. Increased global recognition and mounting international commitments to combat climate change will provide opportunities for regional collaboration on environmental causes. Throughout the Americas, most notably in Canada and the US, environmental groups are increasingly finding allies in indigenous rights movements concerned with protection of native habitats and the environment. These co-operation efforts will combine heightened public exposure of the environmental movement and the legal protections afforded to indigenous communities to increase their chances of success.

Eternally innovative and adaptive, activism will remain one of the most colourful aspects of political engagement in 2016, and present new risks for an expanding range of businesses and individuals. Not only must businesses monitor their own activities, but awareness of the reputation of companies further along supply chains, and of activist activity in the relevant locale or sector, is also increasingly imperative.

reputations when sensitive information is accessed or leaked. These are both favoured tactics of the Anonymous ‘hacktivist’ movement, whose recorded attacks, typically with diffuse ‘civil liberties’ objectives, have affected almost 100 major businesses, governments and institutions in the last five years.

Meanwhile, the growing affordability of more hi-tech assets will promote further innovation. The use of drone flights to disrupt public events was famously showcased in a ‘drone attack’ on one of German Chancellor Angela Merkel’s campaign rallies in September 2013. Given the low cost of entry, it is surprising the use of drones has yet to become more

widespread. With a little engineering knowledge, it is possible for activists to retrofit drones to carry devices such as paintball guns – activists in Mexico use a drone for political graffiti – or even weapons. Such tactics are likely to be of particular interest to activist groups more prone to using violence to further their cause, such as radical or ‘black bloc’ anarchists, who often infiltrate larger, peaceful protests to cause destruction before disappearing into the crowd.

Anarchists – unlike other activists, whose actions primarily promote their agendas for change – often see destructive action as an end in itself, an attack on an unjust system. Their violence is typically characterised by

crude arson and small-scale IED attacks by individuals or small groups, frequently targeting government, security or telecoms infrastructure. Companies should be aware of the risks posed by such anarchist infiltration at larger protests. However, most activism in 2016 is likely to remain non-violent: larger movements usually eschew violence, viewing it as illegitimate, immoral and detrimental to attracting public sympathy to their cause.

REGIONALISATION

Local priorities and opportunities will chiefly determine actions and campaigns in 2016. The broad anti-capitalist movement has increasingly splintered since the height of the Occupy movement in 2012. Anti-austerity has taken prominence in Europe; anti-gentrification in the US. With austerity policies unlikely to ease in the next year and inequality rising, these issues are likely to remain the focus of 2016 Western socioeconomic campaigning. National and local economic developments will promote different priorities elsewhere, as with anti-corruption protests in Asia and South America.

Broader, less tangible issues such as anti-capitalism will seem secondary in importance. While transnational trade deals, such as the Trans-Pacific Partnership (TPP) and Transatlantic Trade and Investment Partnership (TTIP), are likely to generate protests involving tens of thousands of people globally,

50

30

35

40

45

25

20

JAN

201

4

FEB

201

4

MA

R 2

014

AP

R 2

014

MAY

201

4

JUN

201

4

JUL

2014

AU

G 2

014

SE

P 2

014

OC

T 20

14

NO

V 2

014

JAN

201

5

FEB

201

5

MA

R 2

015

AP

R 2

015

MAY

201

5

JUN

201

5

JUL

2015

AU

G 2

015

SE

P 2

015

OC

T 20

15

NO

V 2

015

DE

C 2

014

15

10

5

0

ANIMAL RIGHTS ENVIRONMENTAL ANTI-CAPITALIST

INDIGENOUS RIGHTS ANTI-FRACKING ANARCHIST

Monthly direct action incidents, Jan 2014 - Nov 2015, by perpetrator type

Source: Control Risks

TERRORISM OUTLOOK

RiskMap Report 2016

30

TERRORISM OUTLOOK

RiskMap Report 2016

29

The deadly attacks in Paris in November demonstrated Islamic State (IS)’s ability to plan operations away from its stronghold in Iraq and Syria. Yet attacking the West is a retaliatory tactic: IS’s primary purpose will remain to consolidate its position and build a caliphate in Syria and northern Iraq.

Domestic militants ranging from the ELN in Colombia to Naxalites in India and Niger delta militants in Nigeria will remain active in 2016. But the ripple effects of IS’s emergence and the rejuvenation of al-Qaida in Yemen and Syria mean it is these two movements that will primarily shape the global terrorist threat.

ISLAMIC STATE: GATHERING STRENGTH

IS gained notoriety in part for its brutal, filmed murders of hostages, but its main focus is entrenching and expanding territorial control in Iraq and Syria. The group’s ideology centres on establishing an Islamic caliphate and cleansing Muslim lands of the millions of Shia and other religious minorities whom IS views as ideological deviants. Escalating foreign interventions in Iraq and Syria feed this narrative by allowing it to portray itself as a defender of Islam from infidel forces.

The air campaign and resistance in certain areas – such as from the Kurds in north-eastern Syria – may push IS out of some locations, but the group is likely to retain control of significant amounts of territory, including the urban centres of Raqqa and Mosul, in 2016.

The Paris attacks were the first clear indication that the group has used its foothold in Iraq and Syria to plan operations in the West. Three trends will determine how the threat it poses abroad will develop.

First, IS has encouraged sympathisers in statements by spokesman Abu Mohammed al-Adnani to conduct attacks on their own initiative in their home countries. Attacks committed by such recruits are unlikely to reach the level of

TERRORISM OUTLOOK

GRAHAM GRIFFITHS, ANALYST

TERRORISM OUTLOOK

RiskMap Report 2016

32

TERRORISM OUTLOOK

RiskMap Report 2016

31

infrastructure targets. However, co-ordinated assaults using militant tactics – especially against ‘soft’ targets – remain difficult to defend against. Intelligence apparatuses are fallible and large-scale attacks will remain possible.

More effective counter-terrorism efforts can mitigate threats, but the volatile combination of state collapse, foreign military intervention, and extremist ideologies will continue to attract fighters from around the world and strengthen extremist groups. While these groups will continue to focus on conflict zones such as Syria and Libya in 2016, the establishment of new safe havens and radicalisation of a new generation of militants will ultimately lead to further attacks directed abroad.

sophistication of al-Qaida’s more ambitious plots, but ‘lone wolves’ can nevertheless be difficult to detect and stop. Adoption of IS’s penchant for spectacle – for example, beheadings – will deliver an outsized impact on public perception.

Second, IS will stage retaliatory attacks for foreign air strikes against the group. As in 2015, countries where IS has a strong operational presence, such as Turkey and Egypt, will be most at risk. Greater foreign intervention is likely to increase attempted retaliation as weakening of IS’s conventional capabilities will cause the group to shift resources toward more asymmetric tactics.

Finally, foreign fighters returning home will pose a security threat, though this has been overstated. IS has attracted thousands of fighters through the power of its message that recruits are joining a struggle to re-establish an Islamic caliphate: they have not travelled to Syria and Iraq just to return home. However, highly trained recruits with Western passports – supported by radicalised cells in Europe – give the group the strategic flexibility to plan retaliatory, mass-casualty attacks.

IS AFFILIATES: LOCAL FOCUS

Few significant new pledges of allegiance to IS are likely in 2016: most Islamist militant groups have made their stance clear. Any new affiliates will gravitate to the group’s

sectarian ideology, but are unlikely to develop significant operational ties with the core organisation, meaning their impact will be largely determined by local factors. Pakistan and Afghanistan have seen defections from the Taliban to IS and some adoption of the latter’s virulent anti-Shiism, but this is contributing to infighting and greater targeting of religious minorities rather than bolstering transnational terrorism.

IS’s magnetism was highlighted by the March 2015 pledge of allegiance from Nigerian extremist group Boko Haram. The group is under rising pressure, with Chad, Niger and Cameroon joining the battle against it, but it is likely to retain significant operational capacity in 2016. Increasingly effective counter-terrorism efforts will push the group to rely on hit-and-run tactics rather than attempting to control territory.

Newly founded IS affiliates in the Gulf also appear to be following the targeting imperatives of the main organisation. Saudi Arabia will continue to face attacks on security forces and the Shia minority in 2016, while smaller Gulf states will be at risk of intermittent attacks.

RE-ORIENTATION OF AL-QAIDA

IS continues to eclipse al-Qaida, but the re-orientation of al-Qaida’s affiliates over 2015 show that the latter can still pose a transnational threat. Al-Qaida in the Arabian Peninsula (AQAP) has long been

most focused on attempting spectacular attacks abroad. The group suffered setbacks in 2015, as drone strikes eliminated several top leaders, but has benefited from Yemen’s collapse into civil conflict by seizing territory.

Jabhat al-Nusra (JaN), al-Qaida’s Syrian affiliate, has also worked to consolidate its presence, increasing its ties to local communities and participation in local governance while entering military alliances with other hardline Islamist factions.

Despite the local focus of AQAP and JaN in 2015, al-Qaida maintains that the ‘crusader’ West constitutes its main target. Al-Qaida’s ability to operate freely in Afghanistan was key to its ability to launch large-scale attacks abroad, and its affiliates’ success in entrenching themselves in Yemen and Syria points to a likely increase in capability to plot transnational attacks in the coming years.

COUNTER-TERRORISM

IS’s dramatic rise has not been the only factor to affect the militant landscape. Increasingly sophisticated counter-terrorism operations have changed militant tactics. In Western countries and the Gulf states, greater vigilance has encouraged the ‘lone wolf’ phenomenon or pushed militant groups to adopt loose forms of organisation that preclude sophisticated attacks against well-defended industrial and

MARITIME RISK OUTLOOK

RiskMap Report 2016

34

MARITIME RISK OUTLOOK

RiskMap Report 2016

33

The year ahead will highlight the diverse nature of global piracy trends, with threats enhanced in some areas and reduced in others. Beyond piracy, geopolitical tensions and localised conflict will remain threats to the maritime sector in certain areas.

EAST AFRICA: ROLLING BACK SECURITY

Although Somali piracy remains in the headlines, in reality it has gone quiet. After several years as the primary maritime security issue, activity off the coast of Somalia by late 2015 had fallen to just 1% of its 2011 high point and the trend is positive. Governments and shipping companies face the challenge of responding to the diminished threat without unravelling the work that helped to curtail the problem.

The success of counter-piracy measures off the coast of East Africa will, paradoxically, lead to their gradual dismantling. The shipping industry’s ‘high risk area’ was reduced in 2015; the coming year will see a reduction in ship security measures and further redeployment of warships away from counter-piracy patrols. The mandates of the NATO and EU naval task forces are set for review in December 2016. Renewal – at least in the form of counter-piracy patrols – will be increasingly difficult to justify.

Somali pirate activity will remain minimal in 2016, even though pirate groups retain some ability to launch offshore operations. The absence of major hijacks since 2012 suggests a shift away from the piracy ‘business model’ by former and prospective pirate groups and their financiers. But although much reduced, attacks will remain a threat: the onshore factors – including political instability in Somalia – that fostered the hijack-for-ransom model still exist.

A return to the levels of activity seen between 2008 and 2011 is unlikely. Both the industry and the navies involved have learnt their lessons. Any

MARITIME RISK OUTLOOK

TIM HART, SENIOR ANALYST

MARITIME RISK OUTLOOK

RiskMap Report 2016

36

MARITIME RISK OUTLOOK

RiskMap Report 2016

35

Operators face risks of crew fatalities and destruction of cargo or vessels – whether intentional or not – when calling at contested ports. Detention by local forces, damaged facilities or reduced port capacity, and restrictions caused by naval blockades round out the list of additional hazards.

These are shifting risks, varying not just from country to country but from port to port. As in 2015, Libya and Yemen in particular will present significant, dynamic risks to ships continuing to make port calls in 2016, though international efforts will seek to limit the impact on the shipping lanes running nearby.

Geopolitical tensions will affect offshore oil and gas developments, but their impact on commercial shipping routes will remain limited. The South and East China Seas will garner most headlines, more because of the interaction between naval forces than the impact on trade. Threats will persist in other areas, either as a result of international arbitration or government actions. Developments in the boundary dispute between Kenya and Somalia, and tensions between Guyana and Venezuela over historic claims are just two examples that could affect offshore developments in the year ahead. Commercial shipping is likely to remain insulated, but fishing activities or oil and gas exploration in disputed zones could face localised harassment.

sign of a resurgence by individual pirate groups will bring an aggressive naval response and a swift reintroduction of ship security measures until activity again declines.

SOUTH-EAST ASIA: THEFT AND ROBBERY TO REMAIN THE MAIN THREAT

In 2016, levels of piracy will remain high in South-east Asia compared with activity over the previous year. 2015 saw a particularly sharp rise in piracy incidents. That spike, though, was a result of a rise in attacks involving vessels underway in the western Singapore Strait, rather than a region-wide increase.

In response to greater international attention, states bordering the Strait will increase their focus on policing shipping lanes and prosecuting

offenders. But even with the introduction of localised security initiatives, criminal activity will simply shift to other areas or more vulnerable targets.

In South-east Asia more broadly, small local product tankers will remain exposed to piracy attacks on their cargo, continuing a trend from the previous year. Theft and robbery will remain the main threat to commercial shipping in the region.

WEST AFRICA: PIVOTAL YEAR AHEAD

Reported activity in West Africa remained stable in 2015 after a decline in 2014. Levels of offshore kidnapping in the Niger delta declined, while few hijacks of product tankers were reported in the wider Gulf of Guinea.

Nonetheless, there are reasons for continued caution. First, historic regional trends show significant ebbs and flows in activity, so annual statistics do not necessarily reflect long-term trends. Secondly, 2016 will be a crucial year to determining the future stability of the Niger delta. A scheduled end to the militant amnesty programme, the fallout from controversial gubernatorial elections, and the low oil price could all exacerbate tensions between former militants and the federal government. A major militant campaign remains unlikely, but a rise in violent piracy off the Niger delta is a threat in 2016.

CONFLICTING VIEWS

In the coming year, conflict and domestic instability will continue to present one of the most significant risks to commercial shipping.

THEFT

ROBBERY

HIJACK

ATTEMPT / APPROACH / OTHER

KIDNAP

250

200

150

50

100

0

Ho

rn o

f A

fric

a

Gul

f o

f G

uine

a/W

est

Afr

ica

So

uth-

east

Asi

a

So

uth

Asi

a

Car

ibb

ean

Cen

tral

and

So

uth

Am

eric

a

Sub

-Sah

aran

Afr

ica

Mid

dle

Eas

t

Eas

t A

fric

a

Reported incidents of piracy, armed robbery and theft by region, 1 Jan - 31 Oct 2015

Source: Control Risks

MANAGING 21ST CENTURY CRISES: HIGH STAKES, MANY STAKEHOLDERS

RiskMap Report 2016

38

MANAGING 21ST CENTURY CRISES: HIGH STAKES, MANY STAKEHOLDERS

RiskMap Report 2016

37

An acute crisis challenges any business, but for today’s international, interdependent companies, the complexity of responding is greatly multiplied. Intricate supply chains cross national boundaries: a US company might design a product in Japan, manufacture it in India, and distribute it in Mexico, Nigeria and Pakistan. Doing business in each of these countries is difficult enough. Four of them are also kidnapping hotspots.

The effects of a crisis in one jurisdiction can be felt across a business. A natural disaster in Japan or Thailand derails the global release of the next must-have gadget. One man with a gun and a cause in a Sydney cafe triggers a crisis that consumes a European brand in Australia. The victims are from all over the world. While the loss of life is the greatest tragedy, the collateral damage will include a company’s morale, reputation, operations and finances.

For a multinational business experiencing an acute crisis such as a kidnap or hostage-taking, there is no option to seek resolution in isolation. A multilateral response is the only way out of these complex crises. There will still be significant hurdles. Some of those will come from the very parties being affected.

CONFLICT WITHIN A CRISIS

Just as the external business environment becomes more varied, so does a company’s internal landscape. As multinational businesses enter new territories, often via joint ventures, responsibility for risk mitigation and crisis response diffuses among multiple stakeholders. That said, ultimate responsibility and accountability for risk mitigation and crisis management remains with the parent organisation.

A US company dealing with the kidnap of a French employee in Libya must resolve an acute crisis within the rules and regulations of at least three

MANAGING 21ST CENTURY

CRISES: HIGH STAKES,

MANY STAKEHOLDERSNICOLA WHITE, SENIOR ANALYST

MANAGING 21ST CENTURY CRISES: HIGH STAKES, MANY STAKEHOLDERS

RiskMap Report 2016

40

MANAGING 21ST CENTURY CRISES: HIGH STAKES, MANY STAKEHOLDERS

RiskMap Report 2016

39

from a long-awaited freedom. Algerian forces resolved a much larger incident in January 2013 by taking unilateral action at the In Amenas siege, but with a significant number of hostage fatalities. The victims who lost their lives represented a range of nationalities from an array of employers, all with a vested interest in their safe and timely release.

A PROBLEM SHARED

The threats we face from kidnapping constantly evolve, but never recede. Kidnappers, driven to achieve ever greater ideological and financial success, relentlessly innovate. They learn to apply extreme pressure more efficiently, and to leverage social tools to disseminate their message to the world. External political or economic changes can quickly see dormant trends resurface. Within this maelstrom of change, one constant remains: the duty of care for an employee rests with the employer, without regard for governments and other stakeholders. These issues will only become more complex as we weave our international businesses more tightly together.

countries. Making this work requires an elusive level of international collaboration and a deep understanding of the laws, regulations, political landscape, business and national culture, and language of each jurisdiction.

Early frustrations and complex dilemmas will arise from conflicting policies and competing priorities. Multiple cultures and languages will create communication barriers. If a company and its joint-venture partner have differing policies on acceding to varied types of demands, the victim’s peril endures and increases until a compromise is

reached. Alternatively, commercial stakeholders may be in agreement, but disagree with the advice given by government entities. And what if the governments involved offer conflicting advice? Add this to the more traditional issues a kidnap provokes: a divided family, company conflicts between legal and HR functions, and consular advice that conflicts with the message from home.

Organisations behave differently in these high-pressure crises. Companies, for example, will often share information more openly among stakeholders. Governments,

which consider issues of national security to be paramount, often prohibit open dialogue in sensitive cases. Governments may act unilaterally in exercising their sovereign rights to protect their citizens at home or abroad.

The option of unilateral intervention is a notoriously difficult dilemma for governments and the results of this kind of action are mixed; many end in tragedy despite the best intentions. An attempt in Yemen in December 2014 ended in the death of a US kidnap victim and also of a South African national who may have been hours away

GovernmentC

GovernmentB

LawEnforcement

B

Lawenforcement

C

Familyof B

Familyof C

CompanyY

Localstakeholders

CompanyX

GovernmentA

Lawenforcement

A

Familyof A

Thekidnappers Media

Three victims kidnapped in country A:Nationality A, employed by company X

Nationalities B and C, employed by company Y

Potential stakeholders in a kidnap-for-ransom involving three victims of three nationalities employed by two different companies

Source: Control Risks

RISK RATING FORECAST 2016

RiskMap Report 2016

42

RISK RATING FORECAST 2016

RiskMap Report 2016

41

RISK RATING

FORECAST 2016

RISK RATING DEFINITIONS

POLITICAL RISK

Political risk evaluates the likelihood of state or non-state political actors negatively affecting business operations through regime instability or direct/indirect interference. It also evaluates the influence of societal and structural factors – such as corruption, infrastructure and bureaucracy – on business. Political risk may vary according to factors such as industry sector and investor nationality.

INSIGNIFICANT

The environment for business is benign. For example: political stability is assured, investor-friendly policies are entrenched, there is no threat of contract renegotiation or repudiation, and infrastructure for business is excellent.

LOW

Political and operating conditions are broadly positive. Occasional and/or low-level challenges do not significantly impede business. For example: government policies are investor-friendly with some exceptions, contracts are generally respected, non-state actors have little adverse influence over government decisions, infrastructure is generally robust or there is little risk of reputational damage.

MEDIUM