Risk Management

84

Risk Management OFFICE PROJECT MANAGEMENT GROUP 3: Duran, Espiña, Gatela, Hernani, Ibañez I BS Architecture 4a MARCH 2015

-

Upload

francescleo-duran -

Category

Documents

-

view

213 -

download

0

description

risk management for architectural practice in an architectural firm

Transcript of Risk Management

Risk Management

OFFICE PROJECT MANAGEMENT

GROUP 3: Duran, Espiña, Gatela, Hernani, Ibañez I BS Architecture 4aMARCH 2015

Contents:

Introduction

Managing project risks and opportunities

Project disputes

Firm insurance

Introduction

RISK

“the possibility that something bad or unpleasant will happen”

“someone or something that may cause something bad or unpleasant to happen”

“to put (something) in a situation in which it could be lost, damaged, etc”

The word “risk” derives from the archaic Italian word “riscare”, which means “run into danger” or to imperil, endanger, or jeopardize.

Introduction

MANAGEMENT

“the act or skill of controlling and making decisions about a business, department, sports team, etc”

“act or art of managing: conducting or supervising of something”

Introduction

Risk Management

”is the identification, assessment, and prioritization of risks followed by coordinated and economical application of resources to minimize, monitor, and control the probability and/or impact of unfortunate events or to maximize the realization of opportunities”

Managing Project Risks

And Opportunities

Risks can come from different ways

There are two types of events:

positive events

negative events risks

opportunities

Opportunities can lead to rewards

One would want to take maximum advantage of this

Riskscan lead to losses

One would like to avoid and minimize this

Difference of issue and risk

Risk An uncertain future event or condition which if happens affect mission objectivesAssociated with future events which has not happened yet

Issue A risk which has already occurredGenerally regarded as a problemThis is what risk management is aiming to avoid

Risk Appetite and Tolerances

Risk AppetiteAmount and type of risk an organization is prepared to seek, accept or tolerateThe willingness to take risks

Risk ToleranceOrganization’s readiness to bear risk

Why take risk?

“There is a balance between risk and reward”

“Generally, more risks lead to more rewards.

But this is not always true”

One would want more rewards with less risk

Why take risk?

“There is a balance between risk and reward”

“Generally, more risks lead to more rewards.

But this is not always true”

One would want more rewards with less risk

Why take risk?

“There is a balance between risk and reward”

“Generally, more risks lead to more rewards.

But this is not always true”

One would want more rewards with less risk

Four Classic Strategies Used by Firms to Manage Risks

How the Architect Manage Risks

Identifying sources of risks

sources of risks

No. 4 : Negotiation and Contracts

Deal Makers and Deal BreakersWorking without an agreementHeightened standard of careIndemnitiesConstruction means and methodsGuarantees and CertificationsProper ScopeAdministration of the contract for constructionLimitation of liability

Making better

agreementsEstablish standard in-house practicesGetting

professional

supportUse standard

agreement form

sources of risks

No. 3 : Client Selection

Know the firm’s expertise – know the marketKnow the clientCondominium ProjectsRepeat Clients are like GoldGet the Right BuilderImpact of the Project Delivery Method

sources of risks

No. 2 : Project Team Capabilities

Use of TechnologyStaff Continuity on ProjectsOffice standards

sources of risks

No. 1 : Communication

Peer Reviews: Quality Assurance/Quality Control Know the ContractConduct Proper MeetingsDocument ControlWarning Signs of a ClaimSee It FirstHow to Preserve the Client Relationship

sources of risks

No. 1 : Communication

Risk Management Principles

Create Value Be an integral part of organizational processes Be part of decision-making processes Be systematic and structured Be transparent Be responsive to change Be capable of continual improvement and enhancement Be continually or periodically re-assessed

Benefits of Risk Management:

“Better decision-making through a good understanding of risks and their

likely impact.”

FEWERSURPRISES

EFFECTIVE USE OF RESOURCES

REASSURING STAKEHOLDERS

Plan riskmanagement

Identify risks

Analyse risks

Plan risk response

Monitor and control risks

STEPS IN RISK MANAGEMENT

Specifies management intent, systems and procedures required for managing risksWill provide the definitions of various risk related terms, roles and responsibilities related to risk, and tools and templatesSpecifies how the next four steps are executed

Plan Risk Management

STEPS IN RISK MANAGEMENT

Plan Risk Management

How to do this…

Risk identification

Risk analysis

Risk response

Risk monitoring

STEPS IN RISK MANAGEMENT

Identify Risks

STEPS IN RISK MANAGEMENT

First key step in the actual management of risksProcess of identifying potential risks, their cause, and consequencesSystematic process

Identify Risks

STEPS IN RISK MANAGEMENT

“Best done in a group environment”

Together with....

Management-Architect/designer

Staff/employees

Owner/client

Other stakeholder

Risk register – list of all the risks identified

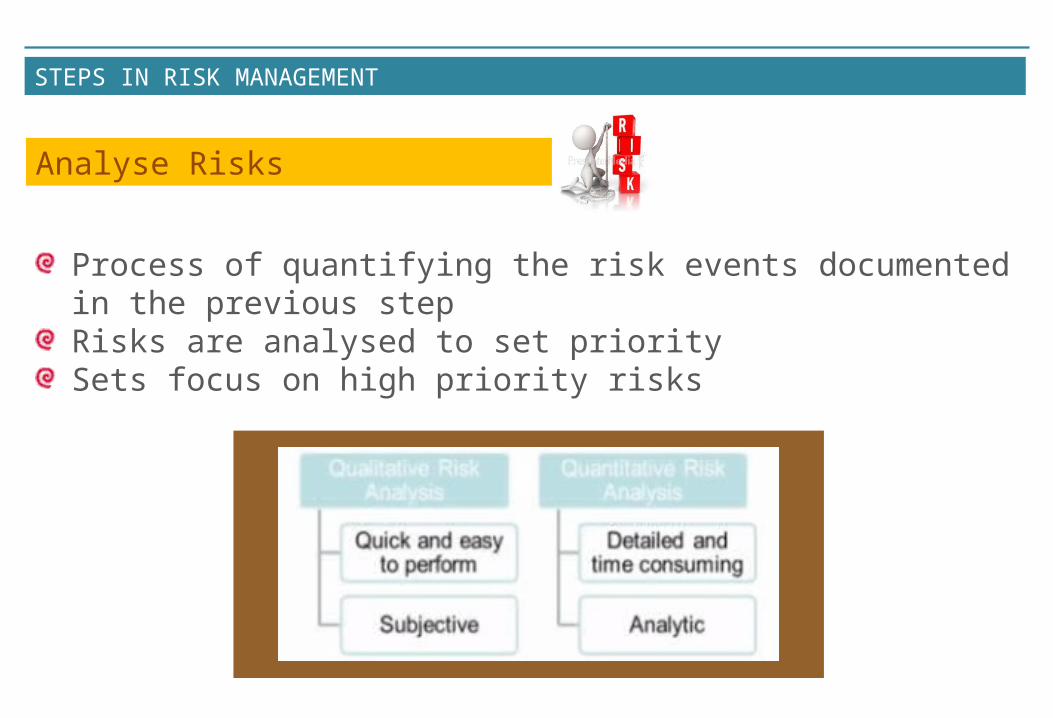

Analyse Risks

STEPS IN RISK MANAGEMENT

Process of quantifying the risk events documented in the previous stepRisks are analysed to set prioritySets focus on high priority risks

Plan Risk Response

STEPS IN RISK MANAGEMENT

How to decrease the possibility of negative risksHow to increase the possibility of positive risks

Monitor and Control Risk

STEPS IN RISK MANAGEMENT

Regularly review identified risks and ensure that these are still relevant

- identify new risks- eliminate risks no longer relevant

Unexpected risks

“risks that occur which were not

identified in the earlier steps”

Project Disputes

“PREVENT DISPUTES BEFORE THEY START”

“The best way to resolve a dispute is to prevent the dispute from ever beginning, or at least to prevent it from

gaining any serious momentum.”

The three most powerful tools in doing so are the successive steps of:

client selection; client education; and contract documentation

DISPUTE RESOLUTION METHODS:

MEDIATIONARBITRATIONLITIGATION

Note: “There are also countless variations to each path, and even some which blend them in some ways. However, understanding the basic process, advantages, and disadvantages of each is really the first stepping stone in the successful and

strategic use of the options. “

“a process in which a neutral person or persons facilitate communications

between the disputants to assist them in reaching a mutually acceptable

agreement”

MEDIATION

MEDIATION

Favoured by the AIA that it is the default first step in the dispute resolution process

Proved to be so useful in efficiently and cost-effectively resolving design professional claims that many professional liability carriers provide significant financial incentives to architects and engineers who can resolve their claims by this means

One rule that generally apply to all mediations is that it is a confidential and privileged process such that any statements made in mediation cannot be cited, quoted, or otherwise used against a party in any subsequent proceeding or elsewhere

MEDIATION

Four factors that can be most influential toward the potential for success in mediation:

Party Participation and AuthoritySelection of Mediator

important considerations for the selection of a mediator:

Adequate Advance Exchange of Information and PositionsTiming

Expertise Energy Empathy Perspective and Persuasion

Settlement The goal of mediation is a “settlement” resolving the dispute. Whether as a result of mediation or direct negotiation, it is critically important that this settlement agreement be reduced to a written agreement as soon as possible, to avoid differing recollections and “buyer’s remorse.”

ARBITRATION

“The process whereby the parties voluntarily submit their disputes for resolution by one or more impartial third persons instead of by a judicial

court process.”

ARBITRATION

4 characteristics of Arbitration resolution mechanism:

1. A private/third-party decision maker chosen by the parties or by a service provider chosen by the parties

2. A mechanism for ensuring neutrality in the rendering of the decision

3. An opportunity for both parties to be heard4. A binding decision or result

ARBITRATION

Parties can be included in and bound by arbitration only if they have agreed to do so.

Most design and construction disputes are not isolated to a single party, but may also include multiple other parties such as other design professionals, contractors, subcontractors, and supplier/manufacturers.

Although there may be very isolated strategic exceptions, it is generally critical for efficiency and fairness that all such parties and disputes be resolved in a single arbitration.

ARBITRATION

“Arbitration has many fans. It is included in many public works agreements and private developer

agreements.”

Most common perceived advantages to arbitration are:

Private—the dispute is not confidential, but arbitration awards are not published. Limitations on this privacy may exist on public projects.

Greater control over selection of decision maker, and better-qualified and experienced decision makers.

Faster due to avoidance of court congestion and timing and more limited prehearing procedures and discovery.

less costly, due to little or no discovery and shorter path to hearing. However, the arbitrator(s) themselves must be compensated.

Avoidance of lay juries

LITIGATION

“The public court system provided by local, state, and federal governments and it is

subject to the rules and procedures adopted by those

governments.”

LITIGATION

Is the default resolution venue

Absent an agreement, this is where nearly all disputes involving architects end up.

Can be slow (years), expensive, distracting, time-consuming, and public.

Generally the out-of-pocket costs to access the courts can sometimes be less than arbitration, and the procedures are time tested and well known.

EARLY NON-FACILITATED RESOLUTIONS

Mediation, arbitration, and litigation contemplates the involvement of third parties to assist in or resolve

the dispute. However, others may rightly suggest that what may be needed is merely for

the participants to just talk to each other and to listen…

EARLY NON-FACILITATED RESOLUTIONS

Ideally such a process is a rapid, phased, and escalating process with limited rounds.

Often, such processes will resolve issues before they escalate into a genuine dispute.

If that is the happy result of such a process, it is important that the resolution be memorialized in writing and signed by both “sides.”

THIS PROCESS would start with a mandatory meeting between the

project managers within five business days. If they cannot

resolve the issues, it would then “escalate” to the principal level for

a second discussion within five business days based on written

summaries provided by the project managers to both principals.

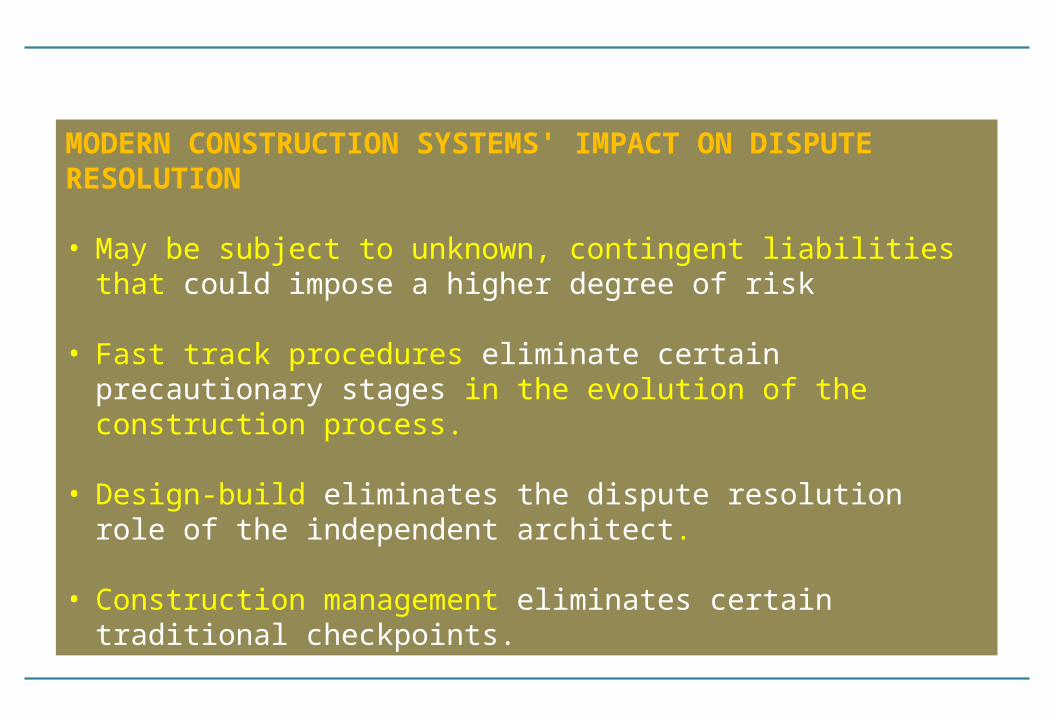

EFFECTS OF CONSTRUCTION METHODS IN DISPUTE RESOLUTION

“The advent of the new approaches to construction brings more uncertainty into the construction process, since many specifics are not determined at the time the contracts are signed. These uncertainties inevitably lead to

more disagreements, which in turn increase the

need for some satisfactory means of resolution.”

TRADITIONAL CONSTRUCTION ARBITRATION

Traditional ConstructionVoluntary, Binding Arbitration

NEW CONSTRUCTION METHODS

Fast TrackingDesign-Build

The Construction Manager

MODERN CONSTRUCTION SYSTEMS' IMPACT ON DISPUTE RESOLUTION

• May be subject to unknown, contingent liabilities that could impose a higher degree of risk

• Fast track procedures eliminate certain precautionary stages in the evolution of the construction process.

• Design-build eliminates the dispute resolution role of the independent architect.

• Construction management eliminates certain traditional checkpoints.

FIRM INSURANCE

I N S U R A N C E

“The equitable transfer of the risk of a loss, from

one entity to another in exchange for payment.”

“A form of risk management primarily used to hedge against the risk of a contingent, uncertain

loss.” IS LIKE A LIFE SAVER…..

Insurer or Insurance Carrier •Is a company selling the insurance

The insured or policyholder•Is the person or entity buying the insurance policy.

Premium•The amount of money to be charged for a certain amount of insurance coverage

I N S U R A N C E

RISKS FOR ARCHITECTS

must protect their firms against:litigation alleging negligence;

theft or destruction of property; personal risks ranging from health and disability to life and

retirement

Should share similar concerns regarding their own employees.

Newer, lesser-known virulent risks:

unproven sustainable products and designchanging standard of carehidden electronic “metadata” contracts that imply fiduciary duty

ARCHITECTS

2 Types of Insurance Applicable to Architectural Firms

Professional Liability Insurance

Commercial General Liability Insurance

“A professional liability insurance policy agrees to defend and pay on behalf of the

architect for claims alleging an error or negligence in the performance of

professional duties, in exchange for the premiums paid to the insurance

company.”

PROFESSIONAL LIABILITY INSURANCE

PROFESSIONAL LIABILITY INSURANCE

“Some firms decide not to purchase professional liability insurance, a business decision usually based on the cost of

the coverage that could ultimately put the firm and its

architects in jeopardy.”

NOTE : Even with professional liability coverage, a firm continues to retain some risk.

PROFESSIONAL LIABILITY INSURANCE

Reasons why an architect should consider the purchase of professional liability insurance:

Business survival

Continuing operations

Contract requirementsSocial responsibilit

y

PROFESSIONAL LIABILITY INSURANCE

Basic considerations for selecting professional liability insurance for a firm:

The coverage limitsDeductiblesCost of the insuranceEndorsement optionsExclusionsCore policies themselves

PROFESSIONAL LIABILITY INSURANCE

“The stability of the insurance carrier is paramount”

it is good practice to evaluate all the potential insurance carriers available

PROFESSIONAL LIABILITY INSURANCE

Broker

help firm owners evaluate the basic policy forms and endorsements and how suitable they are to their practice

architects rely heavily on their insurance broker in the selection of a professional liability insurer. Therefore, a critical step in choosing the best insurer for professional liability exposure is in the selection of the broker to access the marketplace.

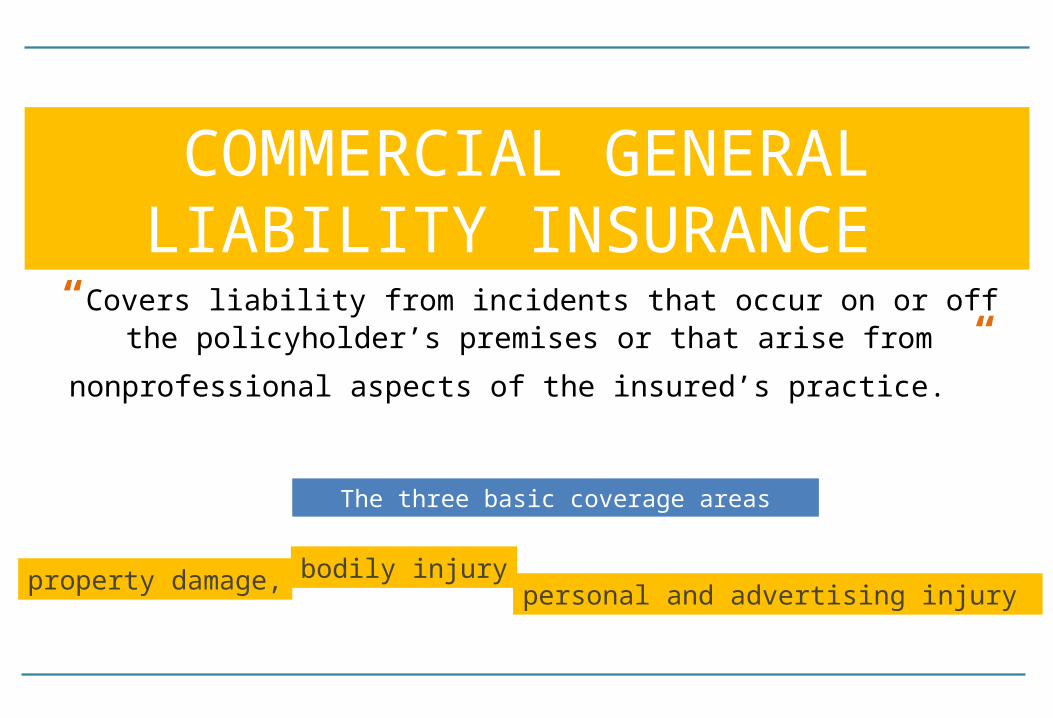

COMMERCIAL GENERAL LIABILITY INSURANCE

“Covers liability from incidents that occur on or off the policyholder’s premises or that arise from nonprofessional aspects

of the insured’s practice.”

The three basic coverage areas

property damage, bodily injurypersonal and advertising injury

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

Immediately protects the firm from injury and property damage claims that could seriously and detrimentally impact the business

Protects a business from lawsuits

General liability policies set limits on the amounts an insurance company is obligated to pay for each type of claim

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

helps to protect against claims brought by employees, such as:

Discriminationsexual harassment wrongful terminationEtc.

Coverage pay damages and defense costs.

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

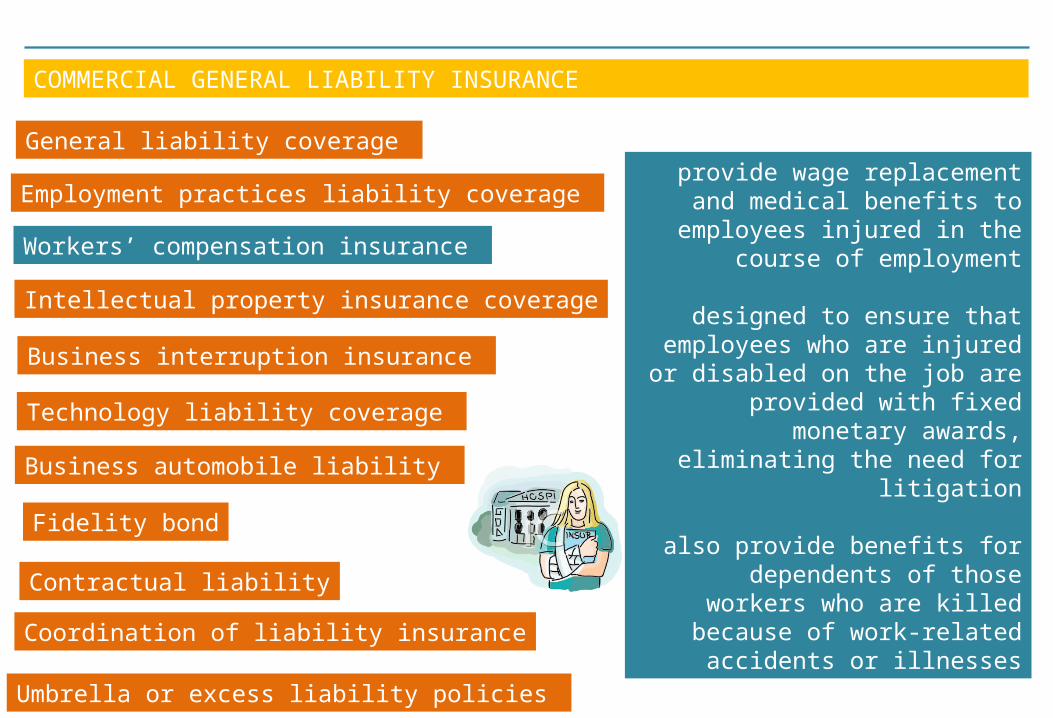

provide wage replacement and medical benefits to employees

injured in the course of employment

designed to ensure that employees who are injured or

disabled on the job are provided with fixed monetary awards, eliminating the need

for litigation

also provide benefits for dependents of those workers

who are killed because of work-related accidents or illnesses

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

Protects companies for copyright, trademark, or patent infringement claims arising out of the company’s operation

Generally, this insurance will pay defense costs and any judgment up to the policy limits

Protects the firm from suit by a competitor for infringing on an idea belonging to someone else.

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

reimburses the architect for ongoing expenses and loss of profits in the event of a fire or other casualty that interrupts normal business operations

can be written to cover fire, windstorm, extended coverage perils, computer crashes, and other hazards

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

this policy agrees to defend and pay claims on behalf of the architect for claims arising out of an alleged negligent act in managing the security of a computer system

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

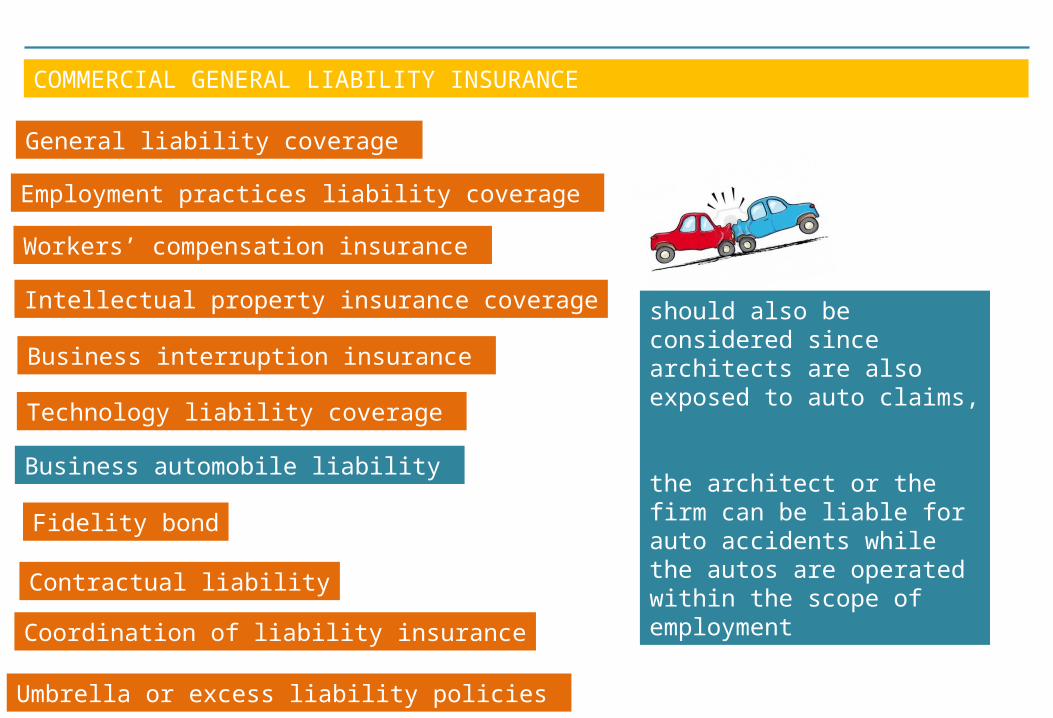

should also be considered since architects are also exposed to auto claims,

the architect or the firm can be liable for auto accidents while the autos are operated within the scope of employment

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

covers losses due to a bonded employee's theft of business property and money

is appropriate for all persons involved with the custody or disbursement of funds, management of firm finances, authorization of payments, purchasing,and other activities requiring the use of funds

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

Insurance that covers liability of the insured assumed in a contract

It is important tolearn to understand contracts and their importance toinsurance and risk management

Business contracts may contain a hold-harmless provision that will contractually transfer another’s legal liability to the architect

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

Professional, general, automobile, and other liability policies are interrelated

It is important to verify insurance coverage and amounts to avoid gaps in protection or duplication of coverage, as well as to correlate insurance limits

COMMERCIAL GENERAL LIABILITY INSURANCE

General liability coverage

Employment practices liability coverage

Workers’ compensation insurance

Intellectual property insurance coverage

Business interruption insurance

Technology liability coverage

Business automobile liability

Coordination of liability insurance

Umbrella or excess liability policies

Fidelity bond

Contractual liability

provide higher limits in conjunction with underlying general liability, automobile,and employer’s liability policies

COMMERCIAL GENERAL LIABILITY INSURANCE

Builder's Risk Insurance

Ordinance or Law Insurance

Tenant's Insurance

Crime Insurance

Product Liability Insurance

Health Insurance

COMMERCIAL GENERAL LIABILITY INSURANCE

Builder's Risk Insurance

Ordinance or Law Insurance

Tenant's Insurance

Crime Insurance

Product Liability Insurance

Health Insurance

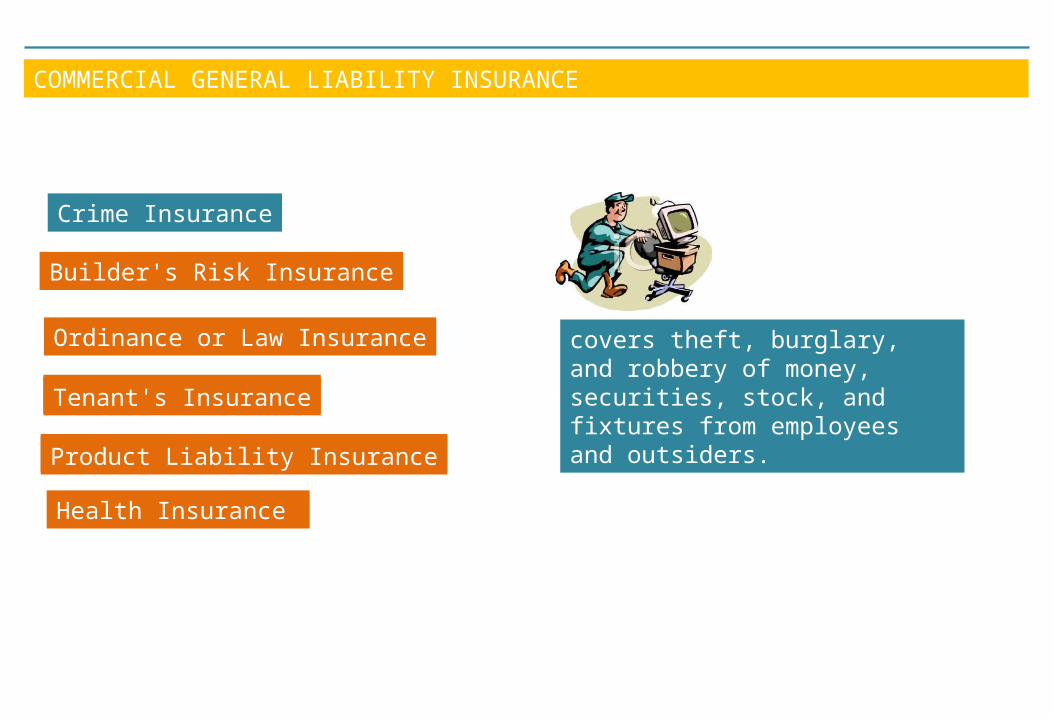

covers theft, burglary, and robbery of money, securities, stock, and fixtures from employees and outsiders.

Tenant's Insurance

Product Liability Insurance

COMMERCIAL GENERAL LIABILITY INSURANCE

Builder's Risk Insurance

Ordinance or Law Insurance

Tenant's Insurance

Crime Insurance

Product Liability Insurance

Health Insurance

Builder's risk insurance covers buildings while they are being constructed.

COMMERCIAL GENERAL LIABILITY INSURANCE

Builder's Risk Insurance

Ordinance or Law Insurance

Tenant's Insurance

Crime Insurance

Product Liability Insurance

Health Insurance

covers the costs associated with having to demolish and rebuild to code when your building has been partially destroyed

COMMERCIAL GENERAL LIABILITY INSURANCE

Builder's Risk Insurance

Ordinance or Law Insurance

Tenant's Insurance

Crime Insurance

Product Liability Insurance

Health Insurance

Commercial leases often require tenants to carry a certain amount of insurance.

A renter's commercial policy covers damages to improvements you make to your rental space and damages to the building caused by the negligence of your employees.

COMMERCIAL GENERAL LIABILITY INSURANCE

Builder's Risk Insurance

Ordinance or Law Insurance

Tenant's Insurance

Crime Insurance

Product Liability Insurance

Health Insurance

covers claims that arise from defective products that cause injury or harm

coverage vary with the type of product that is made

COMMERCIAL GENERAL LIABILITY INSURANCE

Builder's Risk Insurance

Ordinance or Law Insurance

Tenant's Insurance

Crime Insurance

Product Liability Insurance

Health Insurance

most businesses need to offer their workers health insurance

this insurance offers a health coverage benefit to the employees

NOW….

CAN YOU MANAGE RISKS???

References:

• The Architect’s Handbook of Professional Practice, American Institute of Architects

• Dispute Management Under Modern Construction Systems, Robert Coulson

• Introduction to Risk Management, QualityGurus.com

• Wikipedia

• Merriam-Webster Dictionary

• smallbusiness.findlaw.com

• businessinsurance.org

.E.N.D.Thank you!!!