Risk: BUY (-) HIGH - Sanochemia€¦ · Risk: Close Brothers ... PT Graha (Indonesia, Malaysia),...

36

Internet: www.sanochemia. Sector: Biotechnology WKN: 919963 ISIN: AT0000776307 Reuters: SCPH.DE Bloomberg: sac GY Short company profile Share data: Share price (last closing price, EUR): Shares outstanding (m): Market capitalisation (EURm): Enterprise value (EURm): Ø daily trading volume (3 m., no. of shares): Performance data: High 52 weeks (EUR): Low 52 weeks (EUR): Absolute performance (12 months) Relative performance: (vs. TecDAX) 1 month 3 months 6 months 12 months Shareholders: Sanochemia Ltd. Free float Financial calendar: 2010/11 results Author Igor Kim (Analyst) Close Brothers Seydler Research AG Phone: +49 (0) 69-977 84 56 0 Email: [email protected] -27.3% -11.4% 4.4% 4.72 EPS - 0.06 11,055 1.68 0.24 www.cbseydlerresearch.ag -7.9% -17.0% 60.2% 39.8% 26 January 2012 22.29 30.45 0.29 - SANOCHEMIA Pharmazeutika AG is a fully-fledged specialty pharmaceutical company spanning the entire length of the value added chain. 1.93 11.56 - - 4.1 EBIT - 1.6 - 3.4 Revenue - 33.2 - 39.0 - 43.4 new old new old new old Change 2010/11E 2011/12E 2012/13E Share price (dark) vs. TecDAX Source: CBS Research AG, Bloomberg SANOCHEMIA Pharmazeutika AG Recommendation: BUY (-) Risk: HIGH (-) Price Target: EUR 3.20 (-) Heading for emerging markets ▪ SANOCHEMIA Pharmazeutika AG is a fully-fledged specialty pharmaceutical company spanning the entire length of the value added chain. SANOCHEMIA‟s activity is subdivided by four business segments: 1) HUMAN PHARMACEUTCIALS segment which involves Radiology and Therapeutics and generates the bulk of the company‟s sales 2) PRODUCTION segment comprising Synthesis and Pharmaceutical production. 3) RESEARCH AND DEVELOPMENT segment represents SANOCHEMIA‟s R&D activities and 4) New segment Veterinary Pharmaceuticals arose from acquisition of Alvetra & Werfft GmbH. Alvetra annual sales total EUR ~7m and have a positive operating income. ▪ Following an intensive internationalisation of its radiological business in the so-called pharmerging markets either by direct sales or distribution partnerships SANOCHEMIA signed a number of contracts with Iberoinvesa (Spain, Portugal, Latin America), Gammamed Farm (Russia), Kish N.B.S. (Iran). PT Graha (Indonesia, Malaysia), Sankem Pharma and Halley (Italy). The company already generates 40% of its radiological revenues from exports. We assume that aggressive expansion into emerging markets should be the main driver of segment growth. We forecast the export of radiology products to continue its growth at rapid pace reaching above 50% of Human Pharmaceuticals segment in the mid-term. We estimate CAGR of 27% and 15% of sales growth for the period over 2010/11E-13/14E for radiology export and Human Pharmaceuticals respectively. ▪ While we expect Human Pharmaceuticals to be driven by the expansion of radiology export share, we anticipate the development of Production segment to remain relatively flat with estimated CAGR of ~4% over 2010/11E-13/14E. Also the recently established Veterinary Pharmaceuticals segment should demonstrate a robust growth in the medium term with forecasted CAGR of ~17% over 2010/11E-13/14E. For 2011/12E we expect EBIT margin in tune of 9%, which should gradually increase to at least 13% in the long term (in best case scenario we expect long-term operating margin to grow up to 15%). ▪ On the basis of our DCF valuation model, we derived the fair value of EUR 3.27/share, and set the price target at EUR 3.20 with BUY recommendation. 17 November 2011 Source: SANOCHEMIA Pharmazeutika AG, CBS Research AG Please notice the information on the preparation of this document, the disclaimer, the advice regarding possible conflicts of interests, and the mandatory information required by § 34b WpHG (Securities Trading Law) at the end of this document. This financial analysis in accordance with § 34b WpHG is exclusively intended for distribution to individuals that buy or sell financial instruments at their own account or at the account of others in connection with their trading activities, occupation, or employment. Expanding export of radiology business drives top-line Y/E 30.09., EUR m 2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E Revenue 29.5 29.5 27.1 33.2 39.0 43.4 Operating result -1.2 -4.6 -1.3 1.6 3.4 4.1 EBT -4.0 -10.8 -2.0 0.8 3.1 3.7 Net result -3.7 -10.8 -1.4 0.7 2.8 3.5 EPS -0.34 -1.04 -0.12 0.06 0.24 0.29 CPS 0.83 -0.50 -0.31 0.29 0.42 0.60 EBIT margin n/m n/m n/m 4.9% 8.8% 9.5% EBT margin n/m n/m n/m 2.4% 7.8% 8.5% Net margin n/m n/m n/m 2.2% 7.3% 7.9%

-

Upload

doankhuong -

Category

Documents

-

view

214 -

download

0

Transcript of Risk: BUY (-) HIGH - Sanochemia€¦ · Risk: Close Brothers ... PT Graha (Indonesia, Malaysia),...

Internet: www.sanochemia.atSector: Biotechnology

WKN: 919963 ISIN: AT0000776307

Reuters: SCPH.DE Bloomberg: sac GY

Short company profile

Share data:

Share price (last closing price, EUR):

Shares outstanding (m):

Market capitalisation (EURm):

Enterprise value (EURm):

Ø daily trading volume (3 m., no. of shares):

Performance data:

High 52 weeks (EUR):

Low 52 weeks (EUR):

Absolute performance (12 months):

Relative performance: (vs. TecDAX)

1 month

3 months

6 months

12 months

Shareholders:

Sanochemia Ltd.

Free float

Financial calendar:

2010/11 results

Author Igor Kim (Analyst)

Close Brothers Seydler Research AG

Phone: +49 (0) 69-977 84 56 0

Email: [email protected]

-27.3%

-11.4%

4.4%

4.72

EPS - 0.06

11,055

1.68

0.24

www.cbseydlerresearch.ag

-7.9%

-17.0%

60.2%

39.8%

26 January 2012

22.29

30.45

0.29-

SANOCHEMIA Pharmazeutika AG is a fully-fledged

specialty pharmaceutical company spanning the entire

length of the value added chain.

1.93

11.56

-

- 4.1EBIT - 1.6 - 3.4

Revenue - 33.2 - 39.0 - 43.4

new old new old new old

Change 2010/11E 2011/12E 2012/13E

Share price (dark) vs. TecDAX

Source: CBS Research AG, Bloomberg

SANOCHEMIA Pharmazeutika AG

Recommendation:

BUY (-) Risk:

HIGH (-) Price Target:

EUR 3.20 (-)

Heading for emerging markets

▪ SANOCHEMIA Pharmazeutika AG is a fully-fledged specialty

pharmaceutical company spanning the entire length of the value added

chain. SANOCHEMIA‟s activity is subdivided by four business segments: 1)

HUMAN PHARMACEUTCIALS segment which involves Radiology and

Therapeutics and generates the bulk of the company‟s sales 2)

PRODUCTION segment comprising Synthesis and Pharmaceutical

production. 3) RESEARCH AND DEVELOPMENT segment represents

SANOCHEMIA‟s R&D activities and 4) New segment Veterinary

Pharmaceuticals arose from acquisition of Alvetra & Werfft GmbH. Alvetra

annual sales total EUR ~7m and have a positive operating income.

▪ Following an intensive internationalisation of its radiological business in the

so-called pharmerging markets either by direct sales or distribution

partnerships SANOCHEMIA signed a number of contracts with Iberoinvesa

(Spain, Portugal, Latin America), Gammamed Farm (Russia), Kish N.B.S.

(Iran). PT Graha (Indonesia, Malaysia), Sankem Pharma and Halley (Italy).

The company already generates 40% of its radiological revenues from

exports. We assume that aggressive expansion into emerging markets

should be the main driver of segment growth. We forecast the export of

radiology products to continue its growth at rapid pace reaching above 50%

of Human Pharmaceuticals segment in the mid-term. We estimate CAGR of

27% and 15% of sales growth for the period over 2010/11E-13/14E for

radiology export and Human Pharmaceuticals respectively.

▪ While we expect Human Pharmaceuticals to be driven by the expansion of

radiology export share, we anticipate the development of Production

segment to remain relatively flat with estimated CAGR of ~4% over

2010/11E-13/14E. Also the recently established Veterinary Pharmaceuticals

segment should demonstrate a robust growth in the medium term with

forecasted CAGR of ~17% over 2010/11E-13/14E. For 2011/12E we expect

EBIT margin in tune of 9%, which should gradually increase to at least 13%

in the long term (in best case scenario we expect long-term operating

margin to grow up to 15%).

▪ On the basis of our DCF valuation model, we derived the fair value of EUR

3.27/share, and set the price target at EUR 3.20 with BUY recommendation.

▪

▪

17 November 2011

Source: SANOCHEMIA Pharmazeutika AG, CBS Research AG

Please notice the information on the preparation of this document, the disclaimer, the advice regarding possible conflicts of interests, and the mandatory information required by § 34b WpHG (Securities Trading Law) at the end of this document. This financial analysis in accordance with § 34b WpHG is exclusively intended for distribution to individuals that buy or sell financial instruments at their own account or at the account of others in connection with their trading activities, occupation, or employment.

Expanding export of radiology business drives top-line

Y/E 30.09., EUR m 2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E

Revenue 29.5 29.5 27.1 33.2 39.0 43.4

Operating result -1.2 -4.6 -1.3 1.6 3.4 4.1

EBT -4.0 -10.8 -2.0 0.8 3.1 3.7

Net result -3.7 -10.8 -1.4 0.7 2.8 3.5

EPS -0.34 -1.04 -0.12 0.06 0.24 0.29

CPS 0.83 -0.50 -0.31 0.29 0.42 0.60

EBIT margin n/m n/m n/m 4.9% 8.8% 9.5%

EBT margin n/m n/m n/m 2.4% 7.8% 8.5%

Net margin n/m n/m n/m 2.2% 7.3% 7.9%

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 2

Table of content:

Investment thesis ...................................................... 3

SWOT analysis ........................................................... 5

Valuation ................................................................... 7

Discounted Cash Flow ............................................................................... 7

Further upside potential not captured in valuation ..................................... 8

Company .................................................................... 9

Short profile ................................................................................................ 9

Company structure ..................................................................................... 9

Shareholder structure ............................................................................... 10

Management board .................................................................................. 10

Supervisory Board.................................................................................... 10

Business model ....................................................... 11

SANOCHEMIA market access ................................................................. 11

Segment overview ................................................... 12

PRODUCTION segment ............................................................................. 12

HUMAN PHARMACEUTICALS segment .................................................... 13

Radiology – Diagnostics ........................................................................... 13

Therapeutics: tolperisone ......................................................................... 13

VETERINARY PHARMACEUTICALS segment .......................................... 14

RESEARCH & DEVELOPMENT segment .................................................. 14

Strategy ................................................................... 16

Internationalisation of radiology business ................................................ 16

Partnerships ............................................................ 18

Partnerships: Radiology ........................................................................... 18

Partnerships: tolperisone ......................................................................... 19

Market environment ................................................ 21

Imaging agents– Contrast Media ................................................................ 21

Market drivers .......................................................................................... 22

Competition .............................................................................................. 22

Alzheimer‟s disease (Galantamine) ............................................................ 22

Financials ................................................................ 24

9M/2010/11 figures. ................................................................................. 24

Financial forecast ........................................................................................ 25

Export of radiology products should be the main growth driver ................ 25

Sales projection: segment breakdown ..................................................... 26

Earnings projection .................................................................................. 27

Appendix .................................................................. 29

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 3

Investment thesis

Founded in 1990 and located in Vienna (Austria), SANOCHEMIA Pharmazeutika

AG (SANOCHEMIA) is a fully-fledged specialty pharmaceutical company spanning

the entire length of the value added chain. SANOCHEMIA‟s business model is

based on three pillars: 1) Development and production of innovative specialty

pharmaceuticals, which covers such indications as CNS/ Neurodegeneration, Pain,

Oncology as well as diagnostics based on imaging agents and veterinary. The

company is particularly well positioned in the diagnostics segment 2) APIs (Active

Pharmaceutical Ingredients) synthesis for pharmaceutical products. APIs syntheses

comprises both APIs synthesis for SANOCHEMIA products and contract

manufacturing for third parties 3) Manufacture and global distribution of imaging

agents (contrast media – used in all imaging-based medical investigations) and

diagnostics.

SANOCHEMIA‟s activity is subdivided by four business segments: 1) HUMAN

PHAMRACEUTCIALS segment involves Radiology and Therapeutics and

generates the bulk of the company‟s sales 2) PRODUCTION segment comprises

Synthesis and Pharmaceutical production 3) RESEARCH AND DEVELOPMENT

segment represents SANOCHEMIA‟s R&D activities. 4) New segment Veterinary

Pharmaceuticals arose from acquisition of Alvetra & Werfft GmbH. Alvetra annual

sales total ~EUR 7m and have a positive operating income.

The main component of SANOCHEMIA‟s strategy is an intensive

internationalisation of its radiological business in the so-called pharmerging

markets. In terms of geographical focus, the company targets growth markets in

Latin America, Middle East as well as selected markets of Africa and Asia. Also

Russia and US are likewise important markets for SANOCHEMIA. The entrance

into these markets will be executed either by direct sales or distribution

partnerships.

The rapid expansion into the above mentioned regions should relieve the

company‟s dependence on European markets, which are characterised by a

complicated regulatory environment, particularly in Germany.

SANOCHEMIA already generates 40% of its radiological revenues from exports.

The aim is to boost the current level of exports, currently at ~EUR 4.5m, by more

than 50%. This estimate is based on existing marketing authorisations, a steadily

growing product range and the continuous expansion of a network of strong, local

sales partnerships.

The signing of contracts with Iberoinvesa (Spain, Portugal, Latin America),

Gammamed Farm (Russia), Kish N.B.S. (Iran) and Halley (Italy) represents a major

step for the Company in these large, growing markets which should yield top and

bottom-line growth in the short- and mid-term.

A further boost to sales revenues could come in the form of the launch of Scanlux

(iopamidol) in the US. Following the approval of the FDA for production in Neufeld,

SANOCHEMIA plans to launch this product in business year 2012/13. Efforts are

also continuing to expand further in South American and Middle East markets.

Through the submission of a so-called GCC-DR (Gulf Cooperation Council – Drug

Registration) covering multiple Arabian markets, SANOCHEMIA aims to make rapid

progress in the Gulf States.

Four business

segments

The export share

should significantly

increase in the mid

term

US provides an

additional significant

potential in the mid-

and long-term

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 4

In Germany and Switzerland, SANOCHEMIA's tolperisone formulation has already

been launched and is being successfully marketed, under the trademarks Viveo®

(Germany) and Tolcare® (Switzerland) by Orion Pharma. In Turkey, tolperisone

(Agileo®) is already at an advanced regulatory stage, and the approval is expected

in 2012, after which SANOCHEMIA‟s partner, EIP Eczacibasi Ilac Pazarlama will

launch the sale of the product. Furthermore, the company has recently sealed the

deal with Remedica, which will be responsible for the distribution of tolperisone

(Agileo®) in Egypt and so-called MENA countries (For further detail see section

“Partnerships”).

For 2010/11 we expect that the company will further increase its export share of

radiology products, which should boost sales in HUMAN PHARMACEUTICALS

segment. We anticipate the export share of this segment to increase by 53% to

EUR 6.9m (PY: EUR 4.5m), which will represent ~38% of the segment (PY: 29%).

Furthermore, we forecast the export of radiology products to continue its growth at

rapid pace reaching above 50% of HUMAN PHARMACEUTICALS segment in the

mid-term. We estimate CAGR of 27% and 15% of sales growth for the period over

2010/11E-13/14E for radiology export and HUMAN PHARMACEUTICALS

respectively.

While we expect HUMAN PHARMACEUTICALS to be driven by the expansion of

radiology export share, we anticipate the development of Production segment to

remain relatively flat with estimated CAGR of ~4% over 2010/11E-13/14E. The

recently established Veterinary Pharmaceuticals segment should demonstrate a

robust growth in the medium term with forecasted CAGR of ~17% over 2010/11E-

13/14E (It should be noted that in 2010/11E the sales in this segment are not

consolidated for the entire year).

Considering that price pressure in European countries particularly in Germany

significantly affect company margins, we believe that rapid expansion into

pharmerging will notably contribute to margin growth. For 2011/12E we expect

EBIT margin in tune of 9%, which should gradually increase to at least 13% in the

long term (in best case scenario we expect long-term operating margin to grow up

to 15%).

On the basis of our DCF valuation model we derived the fair value of EUR 3.27/

share, and set the price target at EUR 3.20 with BUY recommendation.

Tolperisone: Rapid

access to target

markets

Export business is the

main growth driver

Expansion into

international markets

should improve

margins

BUY recommendation

PT: EUR 3.20

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 5

SWOT analysis

Strengths

SANOCHEMIA‟s business model covers all key steps in the value-added

chain in house: development, production, marketing and sales

Diversified business model

SANOCHEMIA already has a footprint in attractive fast growing markets and

well positioned in its core segments radiology and oncology diagnostics

Experienced management

The discontinuation of low-margin products as well as restructuring

measures optimised operating expenses and improved margins

Given its long and proven track record in the area of API research,

SANOCHEMIA was among the first to recognise the potential of

galantamine.

Weaknesses

Over the last three years the company has generated negative losses

In some European markets, particularly Germany, the regulatory

intervention of healthcare authorities significantly affects the prices of

SANOCHEMIA‟s products and company‟s margins

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 6

Opportunities

The continual demand for new patient tailored therapeutic options and

especially improved diagnostics underpins long-term growth prospects

The development of own synthesis processes for the necessary

(radiological) APIs should reduce company‟s dependence on suppliers

and boost margins in the API synthesis business

R&D pipeline offers a mid- and long term upside potential

The development of a new process for the manufacture of highly pure

forms of synthetic galantamine and its derivatives should provide the basis

for the extension of SANOCHEMIA‟s worldwide synthesis patent from

2014 until 2027. This new, high-purity form of the product could potentially

become the industry standard for this substance.

Turnaround is expected in 2010/11

While US and EU are the largest markets, emerging markets offer notably

higher growth rates

Ageing populations are a strong demand driver for imaging agents, as

they are implemented in the diagnosis of such age-related diseases

including cancer, cardiovascular disease, and neurological disease.

The increasing installation of CT and MRT equipment all over the world

should support the contrast media market.

The need for non-invasive approaches in early diagnostic procedure

particularly in oncology is becoming important.

Threats

Risks related to the failure of clinical trials

Development of market entrance might be slower than expected due to

prolonged approval processes and other regulatory affairs

Internationalisation strategy implies a greater exposure to country risk

associated with emerging markets

Further capital increases might dilute EPS and decrease the share price

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 7

Valuation

Discounted Cash Flow

Our Discounted Cash Flow (DCF) model is based on the following assumptions:

Weighted average cost of capital (WACC): We set the risk-free rate at 3.5%

which is rather conservative in view of the current long-term yields of German

federal bonds. We assumed an equity risk premium of 6.0% and a debt risk

premium of 2.6%. We set the beta factor at 1.5. We assumed a long-term target

equity ratio at market values of 70%. These premises lead to a WACC of 10.14%.

Phase 1 (2010/11E-13E): We estimated the free cash flows (FCF) of phase 1

according to our detailed financial forecasts for this period described in the

financials section of this document.

Phase 2 (2013/14-20E): For Phase 2, we made more general assumptions,

considering company‟s strategy to increase its presence in international markets.

Overall, we allowed annual revenue growth to decrease successively to 3.5%,

resulting in a CAGR 2013/14WE-19/20E of ~5.4%. We assume that the company

can achieve in the long-run an EBIT margin of ~13.8%.

Terminal value: For the calculation of the terminal value, we applied a long-term

FCF growth rate of 2.0%, which should be a rather conservative assumption in

regards to the long-term inflation rate to be expected. Based on these assumptions,

we calculated a fair value of equity of EUR 37.8m, corresponding to a fair value per

share of EUR 3.27. We set the price target of EUR 3.20.

Source: CBS Research

Discounted Cash Flow Model

PHASE 1 PHASE 2 PHASE 3

EUR m 2010/11E 2011/12E 2012/13E 2013/14E 2014/15E 2015/16E 2016/17E 2017/18E 2018/19E 2019/20E

8

Sales 33.2 39.0 43.4 47.3 50.9 54.4 58.0 60.7 63.2 65.4Sales grow th 22.7% 17.4% 11.3% 9.0% 7.6% 7.0% 6.5% 4.7% 4.1% 3.5%

EBIT 1.6 3.4 4.1 4.8 5.5 6.1 6.9 7.6 8.2 9.0

EBIT margin 4.9% 8.8% 9.5% 10.1% 10.8% 11.2% 11.9% 12.6% 12.9% 13.8%

Income tax on EBIT -0.1 -0.2 -0.3 -0.5 -0.8 -1.4 -1.6 -1.7 -1.8 -2.0

Depreciation and amortisation 3.8 4.5 4.7 4.8 4.9 5.0 5.1 5.2 5.6 5.7

Change in net working capital -0.3 -0.2 -2.6 -1.1 -1.6 -1.3 -0.8 -0.5 -0.4 -0.3

Net capital expenditure -3.6 -3.4 -3.9 -4.2 -4.9 -5.0 -5.1 -5.2 -5.6 -5.7

Free cash flow 1.4 4.1 1.9 3.8 3.0 3.3 4.4 5.4 6.0 6.7

Present values 1.4 3.6 1.6 2.7 2.0 2.0 2.4 2.6 2.6 2.4 30.1

Present value Phase 1 6.6 Risk free rate 3.5% Target equity ratio 70.0%

Present value Phase 2 16.8 Equity risk premium 6.0% Beta (fundamental) 1.50

Present value Phase 3 30.1 Debt risk premium 2.6% WACC 10.14%

Total present value 53.5 Tax shield 23.0% Terminal growth 2.0%

Excess cash 1.4

Financial debt -17.1

1.0% 1.5% 2.0% 2.5% 3.0%

9.1% 3.92 4.14 4.39 4.68 5.02

Fair value of equity 37.8 9.6% 3.55 3.74 3.95 4.19 4.47

10.1% 3.23 3.39 3.27 3.77 4.01

Number of shares (m) 11.6 10.6% 2.94 3.08 3.23 3.41 3.60

11.1% 2.68 2.80 2.93 3.08 3.25

Fair value per share (EUR) 3.27

Sensitivity analysis

Terminal growth (Phase 3)

WACC

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 8

Further upside potential not captured in valuation

Estimating the fair value of SANOCHEMIA, we have confined ourselves by the DCF

model valuation and have not taken into consideration, the further upside from

SANOCHEMIA‟s programs, which are presently in clinical trial stage.

We also see a significant upside potential from the possible approval of Secrelux as

well as Tolperison in US market. However, adhering to a conservative approach we

did not take into consideration the potential in US market neither in our valuation

nor in our estimates, leaving it for further upside.

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 9

Company

Short profile

Founded in 1990 and located in Vienna (Austria), SANOCHEMIA Pharmazeutika

AG (SANOCHEMIA) is a fully-fledged specialty pharmaceutical company spanning

the entire length of the value added chain. The Company focuses on the

development and manufacture of novel drugs and diagnostics in selected indication

areas including; neurodegeneration, pain and oncology, as well as in vivo

diagnostics contrast media. SANOCHEMIA and its subsidiaries are engaged in the

production and sale of pharmaceuticals and diagnostics for human medicine and

the synthetic production of active pharmaceutical ingredient (API) such as

galantamine, which is used in a drug to treat Alzheimer‟s disease. Having acquired

Alvetra u. Werfft GmbH, SANOCHEMIA entered into a new operating segment

“Veterinary Pharmaceuticals”.

Strategic positioning: In contrast to Classical Pharma and Biotech

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

Company structure

SANOCHEMIA has subsidiaries across Europe that manufacture and distribute

radiological products in selected markets. Currently, sales offices operate in

Germany, Switzerland, the UK and the US. The following chart illustrates

SANOCHEMIA Pharmazeutika AG‟s structure.

Company structure

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

R&D

Pharmaceuticals

PreclinicClinic/

RegistrationProduction

Sales & Marketing

Biotech

Specialty Pharmaceuticals

SANOCHEMIA

Sanochemia

Pharmazeutika AG

Board of Management:

CEO Dr. Werner Frantsits

CTO Anton Dallos

CMO Maria Popova

Sanochemia

Diagnostics UK Ltd.100%

Sanochemia

Diagnostics

International Ltd.

100%

Sanochemia

Corporation U.S.A

Sanochemia

Diagnostics

Deutschland GmbH

100% 100% 100%

Alvetra Werf f t

Sanochemia

Beijing Representative

Off ice

Specialty

pharmaceutical

company spanning the

entire length of the

value added chain

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 10

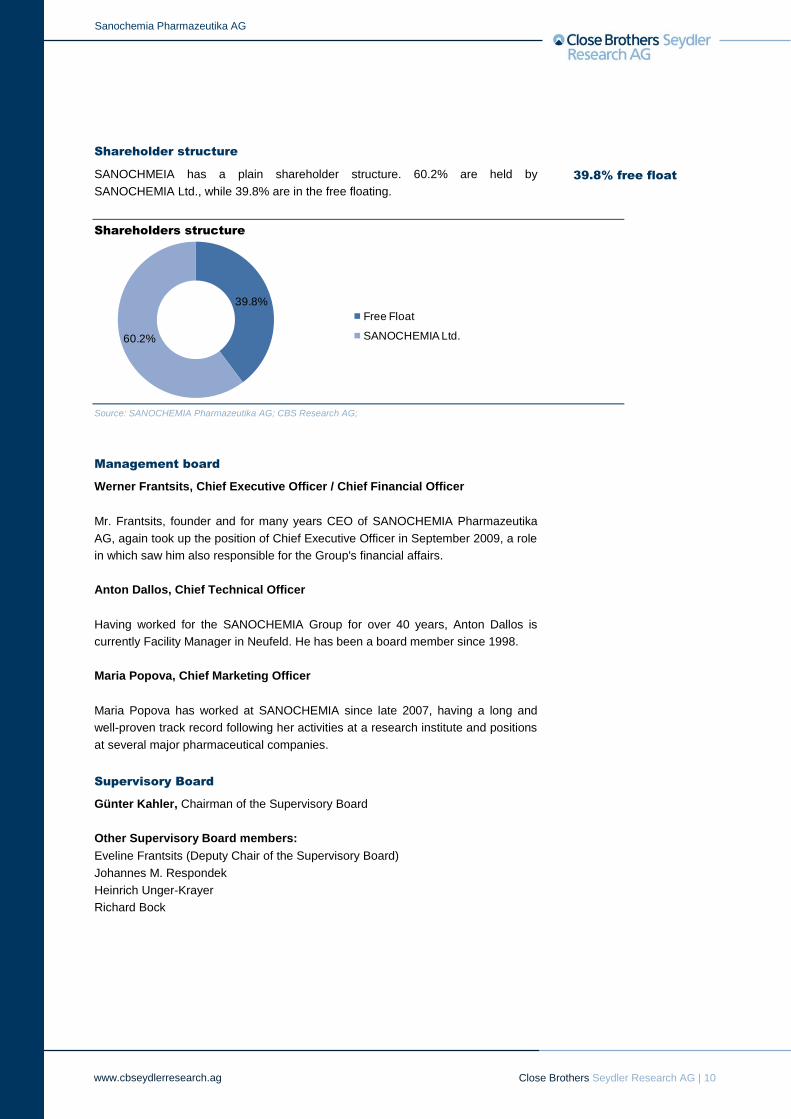

Shareholder structure

SANOCHMEIA has a plain shareholder structure. 60.2% are held by

SANOCHEMIA Ltd., while 39.8% are in the free floating.

Shareholders structure

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

Management board

Werner Frantsits, Chief Executive Officer / Chief Financial Officer

Mr. Frantsits, founder and for many years CEO of SANOCHEMIA Pharmazeutika

AG, again took up the position of Chief Executive Officer in September 2009, a role

in which saw him also responsible for the Group's financial affairs.

Anton Dallos, Chief Technical Officer

Having worked for the SANOCHEMIA Group for over 40 years, Anton Dallos is

currently Facility Manager in Neufeld. He has been a board member since 1998.

Maria Popova, Chief Marketing Officer

Maria Popova has worked at SANOCHEMIA since late 2007, having a long and

well-proven track record following her activities at a research institute and positions

at several major pharmaceutical companies.

Supervisory Board

Günter Kahler, Chairman of the Supervisory Board

Other Supervisory Board members:

Eveline Frantsits (Deputy Chair of the Supervisory Board)

Johannes M. Respondek

Heinrich Unger-Krayer

Richard Bock

39.8%

60.2%

Free Float

SANOCHEMIA Ltd.

39.8% free float

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 11

Business model

The striking difference between SANOCHEMIA and other conventional

biotechnology companies is that the bulk of sales are generated by current product

sales and contract manufacturing.

SANOCHEMIA‟s business model is based on three pillars: 1) Development and

production of innovative specialty pharmaceuticals, which covers such indications

as CNS/ Neurodegeneration; Pain and Oncology as well as diagnostics based on

imaging agents. The company is particularly well positioned in the diagnostics

segment; 2) APIs (Active Pharmaceutical Ingredients) synthesis for pharmaceutical

products. APIs syntheses comprises both APIs synthesis for SANOCHEMIA

products and contract manufacturing for third parties; 3) Manufacture and global

distribution of imaging agents (contrast media – used in all imaging-based medical

investigations) and diagnostics.

As a full-service provider of specialty pharmaceuticals SANOCHEMIA covers the

entire value chain including development, production, marketing and sales of

specialty pharmaceuticals. The company performs all stages of product

manufacture at its Neufeld plant. The existing product portfolio is backed by the

R&D pipeline which provides next generation products to broaden the portfolio.

Thus, the company‟s value potential comprises not only of currently ongoing

business, but also the mid- and long-term potential, provided by the company‟s

R&D pipeline.

SANOCHEMIA‟s activity is subdivided by four business segments: 1) HUMAN

PHAMRACEUTCIALS segment involves Radiology and Therapeutics and

generates the bulk of the company‟s sales 2) PRODUCTION segment comprises

Synthesis and Pharmaceutical production. 3) RESEARCH AND DEVELOPMENT

segment represents SANOCHEMIA‟s R&D activities. 4) New segment

VETERINARY PHARMACEUTICALS arose from acquisition of Alvetra & Werfft

GmbH. Alvetra annual sales total ~EUR 7m and have a positive operating income.

SANOCHEMIA market access

SANOCHEMIA has its own sales teams that deal with direct sales to hospitals and

doctors in Germany, UK and Austria. The Company also cooperates with

specialised distributors targeting radiologists, urologists, cardiologists and hospital

markets. At the same time, it also takes part in international tenders.

SANOCHEMIA‟s Austrian facilities function as a CMO (contract manufacturer) and

sell products to subsidiaries based on transfer prices.

Distribution channels

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

Sanochemia AG - CMO

*Company subsidiaries – SDD (Germany), SUK (UK), SDI (Switzerland), SanoCorp (USA)

Doctors, Hospitals

SDD, SUK, SDI,

SanoCorp USA*

Doctors, Hospitals.

International TenderDistributor

Diversified business

model

Full service provider of

specialty

pharmaceuticals

Four business

segments

Diversified distribution

channels provides

rapid market

penetration

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 12

Segment overview

Business segments

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

PRODUCTION segment

The PRODUCTION Division is engaged in the synthesis of active pharmaceutical

substances (APIs), drug formulation and pharmaceutical production. These

activities are performed either on behalf of the HUMAN PHARMACEUTICALS

Division or on a contract manufacturing basis for third parties. The range of

services provided by this division spans the chemical synthesis of innovative APIs

to the manufacture of drugs and clinical diagnostics. This division also includes

research and development expenditure and income relevant to production.

Synthesis: Operations related to API Synthesis (synthetic galantamine, contract,

synthesis, internal requirements) involve the development and production of APIs

ranging from establishing laboratory processes through up-scaling to industrial-

scale production.

Galantamine

The synthetic galantamine manufactured by SANOCHEMIA is used in a drug

marketed by Janssen and Shire as Reminyl® and Razadyne® in the treatment of

mild to moderate Alzheimer‟ disease. SANOCHEMIA holds exclusive production

contract with Janssen extending for the duration of the patent protection of API

synthesis process until 2014. galantamine generates the bulk of sales in

PRODUCTION segment.

The development of a new process for the manufacture of highly pure forms of

synthetic galantamine and its derivatives should provide the basis for the extension

of SANOCHEMIA‟s worldwide synthesis patent from 2014 until 2027. This new,

high-purity form of the product could potentially become the industry standard for

this substance. With this status the company would significantly strengthen its

competitive position, as it would require that any competitors would have to

demonstrate the same qualitative standards as those of SANOCHEMIA‟s high-

purity form. The awaited global patent protection on this process will make it difficult

for third parties to attain the new standard of quality.

The potential of galantamine as an API is, far greater than originally assumed. As a

result, this substance is being investigated around the world in a range of other

therapeutic options. Given its long and proven track record in the area of API

HUMAN PHARMACEUTICALS

Manufacture and global sales

of:

-Diagnostics

Radiology: Imaging agents,

-Therapeutics

Viveo® (Tolperison)

PRODUCTION

Manufacture of premium quality APIs and ready formulations:

-Synthesis

Production of premium APIs e.g. Galantamin

-Pharmaceutical production

-Contract manufacturing

VETERINARY PHARMACEUTICALS

Manufacture and global sales

of:

-Therapeutics

Alvegesic ®

Carofertin®Menbuton (Injectable

solution)

RESEARCH & DEVELOPMENT

-Pharmaceuticals

Tolperisone

PVP Hypericin

-DiagnosticsMR Lux/ MagnetoluxCyclo-Lux

SecreluxPVP Hypericin

PRODUCTION spans

the chemical synthesis

of innovative APIs to

the manufacture of

drugs and clinical

diagnostics

galantamine is the

main sales driver in

PRODUCTION segment

The awaited synthesis

patent extension for

galantamine should

extend the protection

until 2027

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 13

research, SANOCHEMIA was among the first to recognise the potential of

galantamine.

Pharmaceutical production: Production division also involves the

manufacture of sterile and semi-sterile injectables, suspensions and solutions.

Contract manufacturing

SANOCHEMIA has a long track record established through the manufacture of

around 200 products with the main focus on:

• Parenterals (injection and infusion solutions)

• Liquids (oral and rectal)

• A wide range of OTC products (gargles, ointments, creams and gels)

• Sterile eye ointments

• Topical ointments for human and veterinary medicine

HUMAN PHARMACEUTICALS segment

The manufacture and sale of HUMAN PHARMACEUTICALS has long been the

company‟s core business. The HUMAN PHARMACEUTICALS division is primarily

responsible for the Group's diagnostic activities. SANOCHEMIA‟s most important

radiological products include a range of x-ray/CT imaging agents and the MRT

imaging agent. The extension of SANOCHEMIA's product portfolio through the

inclusion of the therapeutic, tolperisone, has added to this segment's revenue-

generating potential. These products are marketed partly through subsidiaries

(SANOCHEMIA Diagnostics) and through agreements with selected marketing

partners.

Radiology – Diagnostics

The extensive portfolio of imaging agents for CT (Computer tomography) and MR

(Magnetic Resonance) includes ionic imaging agents, non-ionic imaging agents,

barium sulphates, MR imaging agents.

Range of radiological products

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

Therapeutics: tolperisone

Tolperisone is a centrally-acting muscle relaxant with an excellent efficacy and

safety profile. It mediates muscle relaxation without concomitant sedation.

Preparation/ Application X-ray CT MRT

Entire

body

Head

spine

Gastro-

intestinal

Kidney, heart,

vessels

Kidney,

urinary Pancreas

Barilux ® (barium sulphate) x x x

Colognost® (radio opaque

market) x x

Gastrolux ® (inonic contrast

medium) x x x

MR-Lux ® (paramagnetic contrast

medium) x x x x x x x

Secrelux ®(pancreas function

diagnostic) x x

Scanlux ®/Unilux ® (non-ionic

contrast medium) x x x x x x

Urolux Retro ® (ionic contrast

medium) x x

HUMAN

PHARMACEUTICALS -

core business

Broad range of

radiology products

Tolperisone adds to

the revenue-generating

potential of HUMAN

PHARMACEUTICALS

segment

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 14

According to company, tolperisone neither causes impairment of coordination,

weakness, mental confusion or withdrawal phenomena in contrast to other muscle

relaxants. Primary indications for tolperisone the treatment of muscle spasms

associated with neurological conditions such as stroke and multiple sclerosis.

VETERINARY PHARMACEUTICALS segment

This division encompasses all veterinary pharmaceuticals with main markets being

in Austria, Central and Eastern Europe, Middle East, and South Eastern Asia.

The main products of the veterinary pharmaceutical range of Alvetra are

Alvegesic®, a special painkiller for use after operations, and Carofertin®, a

biological product used to increase fertility in cattle and pigs. Both products are

approved in numerous markets.

RESEARCH & DEVELOPMENT segment

RESEARCH & DEVELOPMENT (R&D) Division focuses on identifying and

advancing substances for the treatment of CNS disorders and on the innovative

further development of tried-and tested substances. SANOCHEMIA‟s competitive

advantage lies in a combination of assessing the clinical potential of drug

candidates and in the speedy performance of pre-clinical and clinical trials.

This segment is mostly responsible for the company‟s own R&D activities. Only

minor externally-generated revenues have as yet been obtained through contract

R&D activities.

R&D pipeline

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG

Vidon (PVP Hypericin): (bladder cancer diagnostic): The efficient and early

diagnosis of bladder cancer is an important factor in the treatment of these

malignant tumours.

SANOCHEMIA has successfully completed a Phase IIa clinical trial with PVP

Hypericin in bladder cancer diagnostics. The final report confirmed the excellent

staining properties and the significantly improved parameters of Vidon® compared

RegistrationPhase IIIIndication Phase IIPhase IPre-clinic

Neurological indication

Neurological indication

+ acute muscle spasms

Phototherapy Bladder cancer

StatusProduct/

Project

Tolperisone

PVP hypericine

Pharmaceuticals

MR-Lux/ Magnetolux

Cyclo-Lux

Secrelux

PVP hypericine

MRT contrast medium

MRT contrast medium

Pancreas

Bladder cancer

Diagnostics

Registered & marketed in DE & CH, TR licensed

High purity quality- active substance & pill- indication

expansion

Development as a therapeutic

Marketed in DE & CH, EU DCP Phase completed in 15 countries

Galenic Development of macrocyclic MRT contrast agent

Line extension MRCP Indication:

S-MRCP study planned (start 2011)

Successful Phase IIa, Phase IIbstarted in 2011 .

New business

segment: Veterinary

Pharmaceuticals

R&D segment

represents long term

potential for the

company

PVP Hypericin in

bladder cancer

diagnostic

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 15

to the product already on the market. The study also did not reveal any side effects

worthy of mention.

The company recently launched a patient recruitment for a clinical Phase IIb trial for

the investigation of efficacy and safety profile of Vidon® (PVP-Hyperizin) for the

diagnostics of non-muscle invasive bladder carcinoma. Overall, 200 patient will be

enrolled in new centres in Austria and Germany. The trial endpoints is the

investigation of sensitivity and false positive rate of fluorescent supporting bladder

endoscopy with Vidon® in comparison to bladder endoscopy with white light. The

first patient was enrolled in the study at the end of October. The results are

expected to be published in spring 2013.

The recently started Phase IIb-Study and already completed monocentric clinical

trials provide the basis for further Phase III trial with VIdon. SANOCHEMIA intends

to launch the final market approval trial in 2013. With the advancing development in

Europe the company also plans to apply for market approval in US and other

markets.

Given that considerable demand exists for new and more efficient diagnostic

methods and taking into account that Vidon offers marked competitive advantages

over the product already on the market, a development success here would mean

enormous market potential for SANOCHEMIA in the mid-term. The progress made

to date is accelerating the search for licensing and marketing partners both in

Europe and the USA.

Secrelux: – already marketed in Germany and, as a result of its uniqueness,

available in many other countries on a named-patient basis – is currently the focus

of efforts to secure marketing authorisation in other important European markets,

including an extension to cover the area of magnetic resonance (SMRCP). The

rising demand for this product from radiologists and gastroenterologists is a clear

indication of the degree to which it is widely accepted and needed.

Cyclolux: Cyclolux is a galenic development project in the area of MRT contrast

media. With this program SANOCHEMIA is positioned in a particular area of

marcrocyclical MRT contrast media with low side effects. This novel product is a

good addition to SANOCHEMIA‟s product portfolio, given that currently in EU the

side effects profile of gadolinium-based MRT contrast media is of particular

significance for radiologist and cardiologist.

Phase IIb trial results

are expected in early

2013

Secrelux in pancreas

diagnostic: Searching

partner for further

development

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 16

Strategy

Internationalisation of radiology business

The main component of SANOCHEMIA‟s strategy is an intensive

internationalisation of its radiological business in the so-called pharmerging

markets. In terms of geographical focus the company targets growth markets in

Latin America, Middle East as well as selected markets of Africa and Asia. Also

Russia and US are likewise important markets for SANOCHEMIA. The entrance

into these markets will be executed either by direct sales or distribution

partnerships.

The rapid expansion into the above mentioned regions should relieve the

company‟s dependence on European markets, which are characterised by a

complicated regulatory environment, particularly Germany.

As mentioned above, distribution partnerships play an important role in

SANOCHEMIA‟s strategy. The company has already seen some success in

utilizing this strategy and established a number of partnerships that should drive the

Company‟s HUMAN PHARMACEUTICALS business (for more details see section

“Partnerships”).

SANOCHEMIA already generates 40% of its radiological revenues from exports.

The aim is to boost the current level of exports, currently at ~EUR 4.5m, by more

than 50%. This estimate is based on existing marketing authorisations, a steadily

growing product range and the continuous expansion of a network of strong, local

sales partnerships.

The signing of contracts with Iberoinvesa (Spain, Portugal, Latin America),

Gammamed Farm (Russia), Kish N.B.S. (Iran) and Halley (Italy) represents a major

step for the Company in these large, growing markets which will yield top and

bottom-line growth in the short- and mid-term. (For more details see section

“Partnerships”)

A further boost to sales revenues could come in the form of the launch of Scanlux

(iopamidol) in the US. Following the approval of the FDA for production in Neufeld,

SANOCHEMIA plans to launch this product in business year 2012/13 and generate

revenues of USD 3-5m in the first two years post-launch. Efforts are also continuing

to expand further in South American and Middle East markets. Through the

submission of a so-called GCC-DR (Gulf Cooperation Council – Drug Registration)

covering multiple Arabian markets, SANOCHEMIA aims to make rapid progress in

the Gulf States.

In addition to Scanlux, MR-lux represents another attractive product available for

global marketing. The next x-ray imaging agents, Gastrolux and Barilux, are also

set to follow.

MR-lux: SANOCHEMIA‟s imaging agent for MRT is also set to be marketed

globally. Following the successful conclusion of the regulatory procedure (DCP)

and the rapid preparation of European markets, other countries are already in the

pipeline – including important markets such as Iran, Latin America and, in the near

future, Russia.

SANOCHEMIA is also focusing on the development of follow-up products for the

diagnostics range. On the one hand, the company is specialising intensively in the

Internationalisation of

radiological business

is the key strategic

direction

The export share

should significantly

increase in the mid

term

US provides an

additional significant

potential in the mid-

and long-term

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 17

development of cancer diagnostics. With the products Secrelux and Vidon (PVP

Hypericin), SANOCHEMIA possessed two innovative product candidates with

enormous market potential. On the other, the company is working on an improved

MRT diagnostic – Cyclolux (For more details see section “R&D segment”).

Tolperisone marketing strategy: The company strategy with tolperisone implies

rapid access to target markets via national marketing authorisations. In Germany

and Switzerland, SANOCHEMIA's tolperisone formulation has already been

launched and is being successfully marketed, under the trademarks Viveo®

(Germany) and Tolcare® (Switzerland) by Orion Pharma.

In Turkey, tolperisone (Agileo®) is already at an advanced regulatory stage, and

the approval is expected in 2012, after which SANOCHEMIA‟s partner, EIP

Eczacibasi Ilac Pazarlama will launch the sale of the product.

Furthermore, the company has recently sealed the deal with Remedica, which will

be responsible for the distribution of tolperisone (Agileo®) in Egypt and so-called

MENA countries (For further detail see section “Partnerships”).

An additional focus lies on forging ahead with the US development with a strong

local partner. In the US market, tolperisone represents a so-called new chemical

entity (NCE) which would mean an enormous marketing advantage in a key sales

market. Furthermore, the company aims to expand its geographical footprint of this

product with an extensive network of partnerships outside EU (For further details

see section “Partnerships”).

Tolperisone: Rapid

access to target

markets

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 18

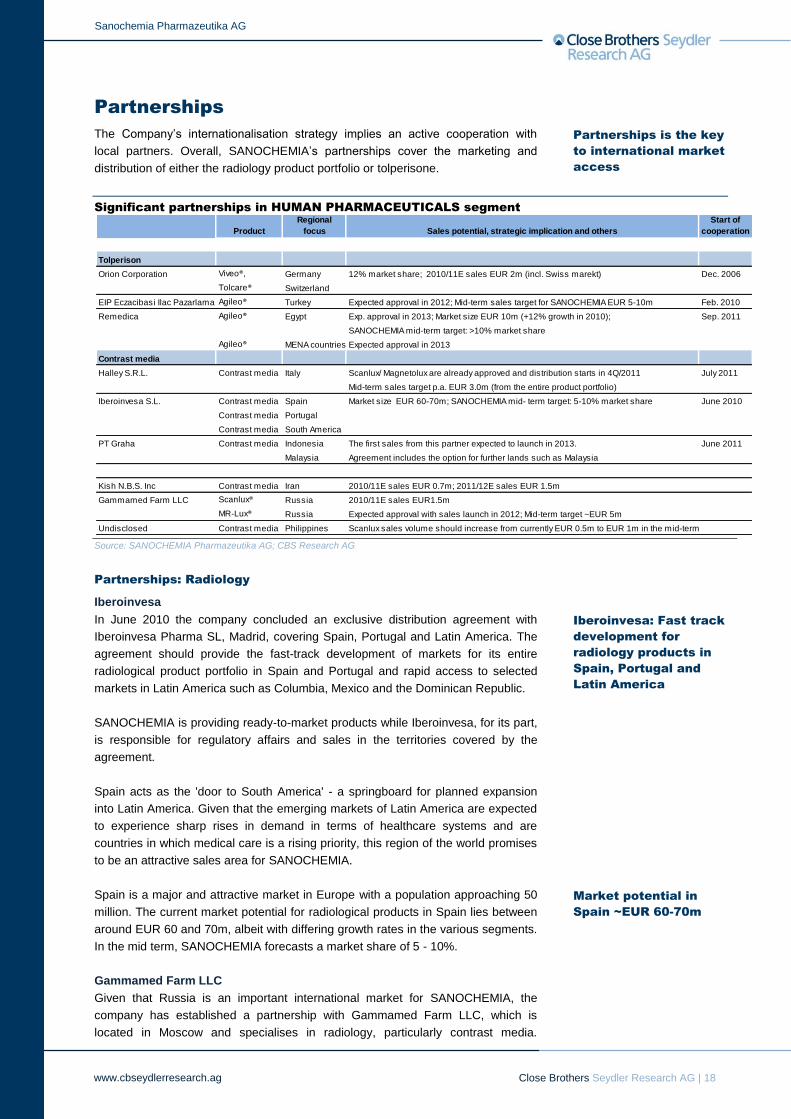

Partnerships

The Company‟s internationalisation strategy implies an active cooperation with

local partners. Overall, SANOCHEMIA‟s partnerships cover the marketing and

distribution of either the radiology product portfolio or tolperisone.

Significant partnerships in HUMAN PHARMACEUTICALS segment

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG Partnerships: Radiology

Iberoinvesa

In June 2010 the company concluded an exclusive distribution agreement with

Iberoinvesa Pharma SL, Madrid, covering Spain, Portugal and Latin America. The

agreement should provide the fast-track development of markets for its entire

radiological product portfolio in Spain and Portugal and rapid access to selected

markets in Latin America such as Columbia, Mexico and the Dominican Republic.

SANOCHEMIA is providing ready-to-market products while Iberoinvesa, for its part,

is responsible for regulatory affairs and sales in the territories covered by the

agreement.

Spain acts as the 'door to South America' - a springboard for planned expansion

into Latin America. Given that the emerging markets of Latin America are expected

to experience sharp rises in demand in terms of healthcare systems and are

countries in which medical care is a rising priority, this region of the world promises

to be an attractive sales area for SANOCHEMIA.

Spain is a major and attractive market in Europe with a population approaching 50

million. The current market potential for radiological products in Spain lies between

around EUR 60 and 70m, albeit with differing growth rates in the various segments.

In the mid term, SANOCHEMIA forecasts a market share of 5 - 10%.

Gammamed Farm LLC

Given that Russia is an important international market for SANOCHEMIA, the

company has established a partnership with Gammamed Farm LLC, which is

located in Moscow and specialises in radiology, particularly contrast media.

Product

Regional

focus Sales potential, strategic implication and others

Start of

cooperation

Tolperison

Orion Corporation , Tolcer in SwitzerlandViveo®, Germany 12% market share; 2010/11E sales EUR 2m (incl. Swiss marekt) Dec. 2006

Tolcare® Switzerland

EIP Eczacibasi Ilac Pazarlama Agileo® Turkey Expected approval in 2012; Mid-term sales target for SANOCHEMIA EUR 5-10m Feb. 2010

Remedica Agileo® Egypt Exp. approval in 2013; Market size EUR 10m (+12% growth in 2010); Sep. 2011

SANOCHEMIA mid-term target: >10% market share

Agileo® MENA countries Expected approval in 2013

Contrast media

Halley S.R.L. Contrast media Italy Scanlux/ Magnetolux are already approved and distribution starts in 4Q/2011 July 2011

Mid-term sales target p.a. EUR 3.0m (from the entire product portfolio)

Iberoinvesa S.L. Contrast media Spain Market size EUR 60-70m; SANOCHEMIA mid- term target: 5-10% market share June 2010

Contrast media Portugal

Contrast media South America

PT Graha Contrast media Indonesia The first sales from this partner expected to launch in 2013. June 2011

Malaysia Agreement includes the option for further lands such as Malaysia

Kish N.B.S. Inc Contrast media Iran 2010/11E sales EUR 0.7m; 2011/12E sales EUR 1.5m

Gammamed Farm LLC Scanlux® Russia 2010/11E sales EUR1.5m

MR-Lux® Russia Expected approval with sales launch in 2012; Mid-term target ~EUR 5m

Undisclosed Contrast media Philippines Scanlux sales volume should increase from currently EUR 0.5m to EUR 1m in the mid-term

Partnerships is the key

to international market

access

Iberoinvesa: Fast track

development for

radiology products in

Spain, Portugal and

Latin America

Market potential in

Spain ~EUR 60-70m

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 19

Recently SANOCHEMIA announced a large order from Russia to the amount of

EUR 3m for SANOCHEMIA‟s Scanlux of which EUR 1.5m will be generated in

2011. Furthermore, SANOCHEMIA expects the approval of its innovative contrast

media MR-lux®, with subsequent market launch in 2012. According to the

company, the mid-term sales target generated from this product is expected to

increase up to EUR 5m.

Halley S.R.L

In July 2011, SANOCHEMIA signed an agreement with an Italian company Halley

S.R.L. for distribution of SANOCHEMIA‟s portfolio for CT (computerised

tomography) and MRT (magnetic resonance). Moreover, SANOCHEMIA will also

distribute its Secrelux for diagnosis of pancreas lesions and tumours in the Italian

market.

SANOCHEMIA‟s leading contrast media Scanlux® and Magnetolux® are already

approved in Italy. The sales of these products will start in the near future, which will

be followed by the successive launches of further products from SANOCHEMIA‟s

radiology product portfolio. The company‟s mid-term sales target to be generated in

Italy is ~EUR 3m p.a.

Kish N.B.S.Inc,

SANOCHEMIA also has long-term contracts with its Iranian partner Kish N.B.S.Inc,

Tehran, which will market SANOCHEMIA‟s contrast medium in Iran. According to

SANOCHMEIA, a strong sales increase up to EUR 0.7m is expected for 2010/11

(PY: EUR 0.1m). For 2011/12, the company expects revenues from this partner to

total to EUR 1.5m.

PT Graha

In June 2011, SANOCHEMIA announced that it has signed an exclusive

distribution partnership with Indonesian PT Graha. The concluded cooperation,

which covers Indonesian and includes the option for further lands such as

Malaysia, represents an important step into one of the fastest growing markets in

Asia. The first sales from this partner expected to launch in 2013. The agreement

will include the approval and distribution of radiology products Scanlux, Magnetolux

and Secrelux.

Sankem Pharma

At the end of June 2011, the company announced a launch of contrast media sales

in Philippines. According to SANOCHEMIA, the sales volume for Scanlux in this

region should increase from currently EUR 0.5m to EUR 1m in the mid-term. The

company also asserts that the introduction of other products should further

contribute to the sales growth in this region.

Partnerships: tolperisone

Orion Corporation

In December 2006, SANOCHEMIA and Finnish pharmaceuticals company Orion

Corporation have concluded an exclusive agreement for the marketing and sale of

tolperisone in Germany and Switzerland. The agreement relates to a formulation of

tolperisone for use in the treatment of muscle spasm associated with neurological

conditions such as stroke and Multiple Sclerosis (MS).

Aside of the already received milestone payments SANOCHEMIA manufactures

and supplies Orion Corporation with the product for the duration of the agreement.

Halley: distribution

partner in Italy

Gammamed Farm:

Partner in Russian

market

Kish N.B.S.: First sales

from this partner are

expected in 2010/11

PT Graha: Distribution

partner in Indonesia

Sankem Pharma:

Partner in Philippines

Agreement with Orion:

First step in the

internationalisation of

Tolperisone

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 20

In Germany, tolperisone is marketed under the mark Viveo®, while in Switzerland

under the mark Tolcare®. The company expects to reach ~EUR 2m in both of

these markets in the ongoing year. Overall, SANOCHEMIA aims to achieve ~20%

of market share in EU countries where the product has marketing authorisation.

EIP Eczacibasi Ilac Pazarlama A.S.

SANOCHEMIA and the Turkish pharmaceuticals company EIP Eczacibasi Ilac

Pazarlama A.S. ("EIP") have signed an exclusive agreement relating to the

marketing and sale of Agileo® (tolperisone) in Turkey.

With a population about 73m inhabitants, Turkey is a so-called emerging market

with above-average growth. According to SANOCHEMIA, the sales potential in the

entire Turkish muscle relaxant market is ~EUR 90m (2008) and has increased by

more than 30% in recent years. The estimated sales volume for SANOCHEMIA‟s

dosage form can therefore be expected to range within EUR 5-10m in the mid-term.

Remedica

On 9 September 2011 SANOCHEMIA signed an exclusive agreement with

Remedica to market and distribute its drug Agileo® in Egypt and the countries in

the Middle East and North Africa (MENA). By 2013 Remedica expects to obtain

approval to offer Agileo in Egypt and MENA.

According to SANOCHEMIA, the Egyptian market for muscle relaxants amounts to

EUR 10m and in 2010 it grew by 12%. Given that the market is mostly dominated

by obsolete preparations while tolperisone represents a novel therapy,

SANOCHEMIA expects to rapidly gain market share of ~10% in the mid-term.

EPI Eczacibasi Ilac

Pazarlama: Partner for

distribution of

Tolperisone in Turkey

Remedica: Tolperisone

partner in Egypt and

MENA countries

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 21

Market environment

Imaging agents– Contrast Media

Contrast agents are used with many types of imaging examinations, including X-

ray/CT and MRT. They use different mechanisms depending on the underlying

imaging technique. Contrast agents implemented for CT based on X-ray allow the

creation of an artificial contrast between the organ or tissue under focus and

surrounding anatomic structures. Today, most of CT procedures require the use of

contrast agents.

The mode of action of MRT contrast media comprises of the electromagnetic

behaviour of tissues. Most MRT contrast agents are based on gadolinium.

While CT/ X-rays represents the standard procedure in modern diagnostics, MRT

contrast media represent modern technology, with a strong growth rate of >7% p.a.

Global contrast media market 2009:

In EUR bn in %

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

The worldwide market for contrast media in 2009 amounted to ~USD 6.5m. The

bulk of the market is attributable to CT agents (~70%), while MRT agents represent

~23%.

According to Global Industry Analysts (GIA) research, the world imaging agents

market is forecasted to exceed ~USD 14bn by 2015, mainly propelled by increasing

volume of diagnostic examinations and broadening applications.

In terms of geographical breakdown, the US represents the largest imaging agents

market worldwide followed by Japan and Europe. However, firms are increasingly

searching for opportunities in developing markets of Asia, Latin America, and

Eastern Europe that in distinction to EU and the US enjoy attractive budgets at the

disposal. (Source: Global Industry Analysts: “Imaging Agents: Global Strategic

Business Report”/ 2010).

Despite the substantial impact of recession on the imaging equipment market, the

impact on the imaging agents market has been less significant. This is due to the

widespread availability of existing equipment in key markets including EU and the

US and increasing focus on diagnostic examinations.

4.6

1.5

0.4

CT agents MRT agents Ultrasound

71%

23%

6%

CT agents MRI agents Ultrasound

Contrast media; Broad

application in imaging

examinations

CT contrast agents

account for 70% of

contrast media market

More opportunities in

developing markets

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 22

Market drivers

Ageing populations are a strong demand driver for imaging agents, as

they are implemented in the diagnosis of such age-related diseases

including cancer, cardiovascular disease, and neurological disease.

The increasing installation of CT and MRT equipment all over the world

should support the contrast media market.

The need for non-invasive approaches in early diagnostic procedure

particularly in oncology is becoming important.

Competition among hospitals will force them to expand their services

including diagonsitics based on CT and MRT contrast media.

Competition

The market leader for contrast media is Bayer Schering Pharma (Germany), which

was a pioneering developer of contrast agents. There are also a number of several

well-established players in different market segments. Given the broad spectrum of

contrast media and agents, there are different companies that take leading

positions in different categories. To mention some of the market players: AMAG

Pharmaceuticals, Inc. (USA), Bayer Schering Pharma AG (Germany), Bracco

Group (Italy), Covidien (USA), GE Healthcare (UK), Guerbet Group (France) and

Lantheus Medical Imaging (USA).

Alzheimer’s disease (Galantamine)

Alzheimer‟s disease (AD) is the fastest growing CNS segment. Presently only two

classes of drugs are approved for Alzheimer‟s disease: Acetylcholin esterase

inhibitors (AChE-I) (for mild to moderate AD) and NMDA receptor anatagonists

(NMDA-I) (for moderate to severe AD). In the table below, the approved AD drugs

in both classes are briefly summarised.

Market for Alzheimer’s disease drugs

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

Among AChE-I AD drugs, AriceptTM

(API: donepezil) produced by Pfizer/Eisai

enjoys a US market share of ~50%. Novartis produces ExelonTM

(API: rivastigmine)

with a market share of ~10%. Finally J&J, Janssen, Shire produces RazadyneTM

/

ReminylTM

(API: galantamine) for a market share of ~10%.

Drug Marketed by API US market share

Aricept Pfizer/Eisai Donepezil Approx. 50%

Exelon Novartis Rivastigmine Approx. 10%

Razadyne/Reminyl J&J, Janssen, Shire Galantamine Approx. 10%

Drug Marketed by API US market share

Namenda/Axura/ Ebixa Forest, Lundbeck, Merz memantine Approx. 30%

Acetylcholine esterase inhibitors

NMDA receptor antagonist (NMDA-I)

Alzheimer’s disease -

the fastest growing

CNS segment

Aricept (Pfizer/Eisai)

takes the dominant

position in AD market

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 23

The rest of AD market is dominated by NMDA-I antagonist Namenda/Ebixa (Forest,

Lundbeck) with ~30% market share in the US. The table above outlines the drugs,

active pharmaceutical content, manufacturers and market share.

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 24

Financials

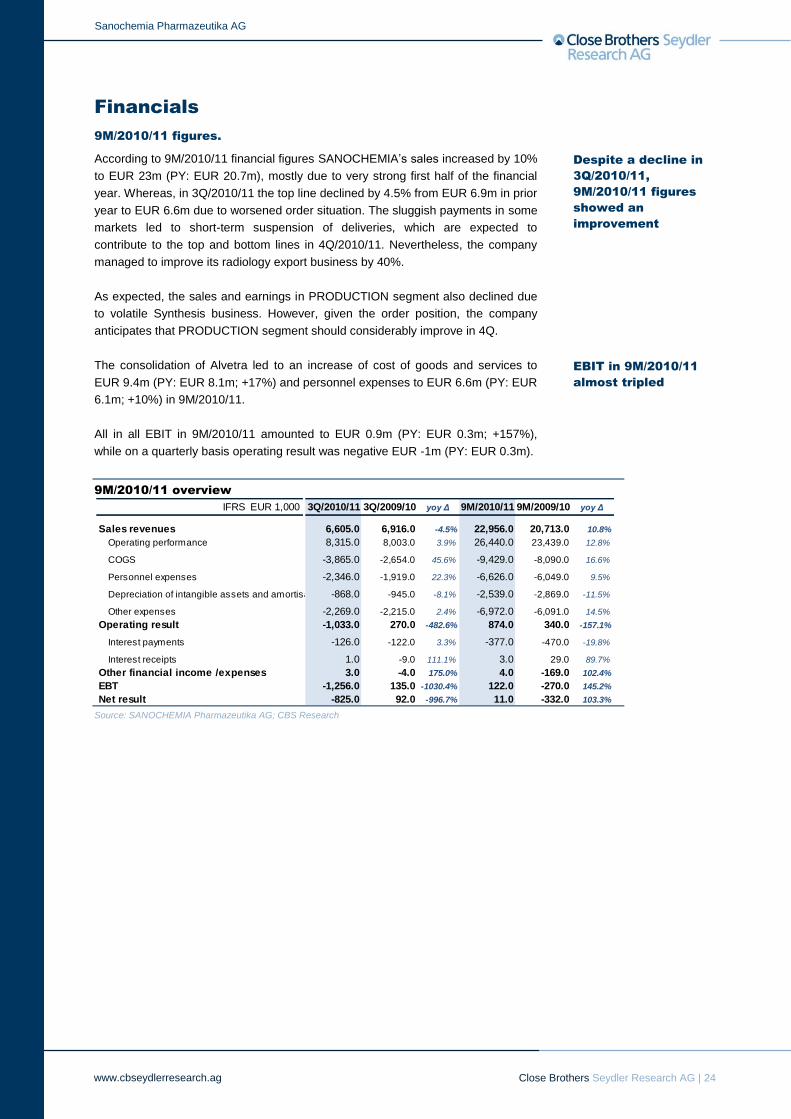

9M/2010/11 figures.

According to 9M/2010/11 financial figures SANOCHEMIA‟s sales increased by 10%

to EUR 23m (PY: EUR 20.7m), mostly due to very strong first half of the financial

year. Whereas, in 3Q/2010/11 the top line declined by 4.5% from EUR 6.9m in prior

year to EUR 6.6m due to worsened order situation. The sluggish payments in some

markets led to short-term suspension of deliveries, which are expected to

contribute to the top and bottom lines in 4Q/2010/11. Nevertheless, the company

managed to improve its radiology export business by 40%.

As expected, the sales and earnings in PRODUCTION segment also declined due

to volatile Synthesis business. However, given the order position, the company

anticipates that PRODUCTION segment should considerably improve in 4Q.

The consolidation of Alvetra led to an increase of cost of goods and services to

EUR 9.4m (PY: EUR 8.1m; +17%) and personnel expenses to EUR 6.6m (PY: EUR

6.1m; +10%) in 9M/2010/11.

All in all EBIT in 9M/2010/11 amounted to EUR 0.9m (PY: EUR 0.3m; +157%),

while on a quarterly basis operating result was negative EUR -1m (PY: EUR 0.3m).

9M/2010/11 overview

Source: SANOCHEMIA Pharmazeutika AG; CBS Research

IFRS EUR 1,000 3Q/2010/11 3Q/2009/10 yoy Δ 9M/2010/11 9M/2009/10 yoy Δ

Sales revenues 6,605.0 6,916.0 -4.5% 22,956.0 20,713.0 10.8%

Operating performance 8,315.0 8,003.0 3.9% 26,440.0 23,439.0 12.8%

COGS -3,865.0 -2,654.0 45.6% -9,429.0 -8,090.0 16.6%

Personnel expenses -2,346.0 -1,919.0 22.3% -6,626.0 -6,049.0 9.5%

Depreciation of intangible assets and amortisation of intangible assets-868.0 -945.0 -8.1% -2,539.0 -2,869.0 -11.5%

Other expenses -2,269.0 -2,215.0 2.4% -6,972.0 -6,091.0 14.5%

Operating result -1,033.0 270.0 -482.6% 874.0 340.0 -157.1%

Interest payments -126.0 -122.0 3.3% -377.0 -470.0 -19.8%

Interest receipts 1.0 -9.0 111.1% 3.0 29.0 89.7%

Other financial income /expenses 3.0 -4.0 175.0% 4.0 -169.0 102.4%

EBT -1,256.0 135.0 -1030.4% 122.0 -270.0 145.2%

Net result -825.0 92.0 -996.7% 11.0 -332.0 103.3%

Despite a decline in

3Q/2010/11,

9M/2010/11 figures

showed an

improvement

EBIT in 9M/2010/11

almost tripled

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 25

Financial forecast

Following the strategy to focus more on profitability rather than sales growth, the

SANOCHEMIA‟s sales in 2009/10 decreased by 8% to EUR 27.1m (PY: EUR

29.5m), while operating result improved by 73% from EUR -4.6m to EUR -1.3m.

While sales revenues in the entire HUMAN PHARMACEUTICALS segment

decreased by 12% to EUR 16.1m in 2009/10 (PY: EUR 18.3m), the export share

have considerably increased by 26% to EUR 4.5m (PY: EUR 3.6m), which

represented 28% of HUMAN PHARMACEUTICALS segment (PY: 20%). The

PRODUCTION segment in the mentioned period indicated a slight decline.

Export of radiology products should be the main growth driver

It is challenging to project SANOCHEMIA‟s sales, given that the development of

radiology export business largely depends on its partners. Despite concluded

agreements with numerous partners in international markets, there is a risk that

approval as well as sales launches in relevant markets might be delayed.

For 2010/11 we expect that the company will further increase its export share of

radiology products, which should boost sales in HUMAN PHARMACEUTICALS

segment. We anticipate the export share of this segment to increase by 53% to

EUR 6.6m (PY: EUR 4.5m), which will represent ~39% of the segment (PY: 29%).

Projected development of export sales in EUR m

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG; * Bulgaria, Greece, Italy, Malta, Slovakia,Slovenia, Spain and Cyprus; **

Oman, Syrien, United Arab Emirates, Iran; *** Georgia

0

3

6

9

12

15

2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E 2013/14E

US

Central and South AmericaWestern Asia***

Russia

Middle East**

Europe (CEE and South Europe)*Asia

Africa

Σ 2.7Σ 3.6

Σ 4.5

Σ 6.9

Σ 9.9

Σ 12.2

Σ 14.1

Radiology export projection

2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E 2013/14E CAGR 11E-14E

Africa 1.2 1.3 1.3 1.6 2.2 2.5 2.8 20%

as % of total export 44% 37% 30% 24% 22% 20% 20%

yoy change n.a. 9% 1% 23% 33% 15% 13%

Asia 0.0 0.0 0.1 0.1 0.5 0.8 1.1 130%

as % of total export 0% 0% 2% 1% 5% 7% 8%

yoy change n.a. 10% 549% 9% 456% 60% 38%

Europe (CEE and South Europe)* 1.2 1.6 1.8 2.8 3.8 4.7 5.4 25%

as % of total export 44% 44% 40% 41% 39% 38% 38%

yoy change n.a. 31% 14% 55% 36% 23% 16%

Middle East** 0.1 0.1 0.5 0.5 1.3 1.5 1.5 43%

as % of total export 2% 4% 10% 7% 13% 12% 10%

yoy change n.a. 144% 220% 9% 164% 10% 1%

Russia 0.0 0.1 0.1 1.0 1.0 1.3 1.6 18%

as % of total export 0% 4% 3% 14% 10% 10% 11%

yoy change n.a. n.a. 2% 565% 6% 28% 21%

Western Asia*** 0.1 0.2 0.0 0.1 0.2 0.2 0.2 22%

as % of total export 3% 5% 1% 2% 2% 2% 1%

yoy change n.a. 152% -74% 130% 79% 0% 1%

Central and South America 0.2 0.2 0.6 0.8 0.9 0.9 1.1 11%

as % of total export 6% 6% 14% 12% 9% 8% 8%

yoy change n.a. 18% 208% 27% 10% 5% 20%

US 0.0 0.0 0.0 0.0 0.0 0.4 0.5 n.a.

as % of total export 0% 0% 0% 0% 0% 3% 3%

yoy change n.a. n.a. n.a. n.a. n.a. n.a. 18%

Total Export 2.7 3.6 4.5 6.9 9.9 12.2 14.1 27%

Improved operating

result despite sales

decline in 2009/10

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 26

The signs for such an aggressive assumption of export growth were already visible

in 9M/2010/11 results. Particularly, sales in Russia, Europe (CEE and South

Europe) and Africa should considerably propel the export share of radiology

products.

Furthermore, aside of above mentioned regions, Middle East as well as Central and

South America are expected to significantly contribute to the SANOCHEMIA‟s

export business in the medium term. In terms of growth Asia and Middle East are

forecast to be the most intensive regions with estimated CAGR of 130% and 43%

over 2010/11E-13/14E respectively.

Thus, we assume that aggressive expansion into emerging markets should be the

main driver of segment growth. Furthermore, we forecast the export of radiology

products to continue its growth at rapid pace reaching above 50% of HUMAN

PHARMACEUTICALS segment in the mid-term. We estimate CAGR of 27% and

15% of sales growth for the period over 2010/11E-13/14E for export and HUMAN

PHARMACEUTICALS respectively.

Sales projection: segment breakdown

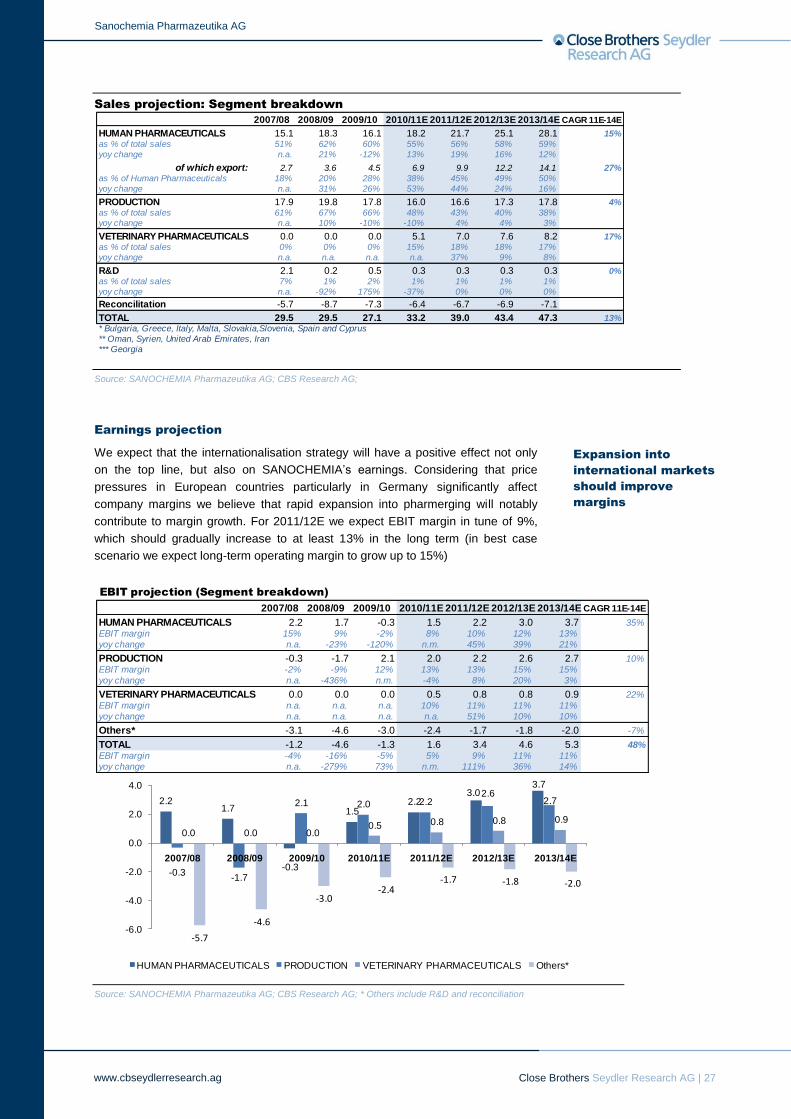

While we expect HUMAN PHARMACEUTICALS to be driven by the expansion of

radiology export share, we anticipate the development of Production segment to

remain relatively flat with estimated CAGR of ~4% over 2010/11E-13/14E. Also the

recently established Veterinary Pharmaceuticals segment should demonstrate a

robust growth in the medium term with forecasted CAGR of ~17% over 2010/11E-

13/14E (It should be noted that in 2010/11E the sales in this segment are not

consolidated for the entire year).

Sales projection: Segment breakdown

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

15.1 18.3 16.1 18.2 21.7 25.1 28.1

17.919.8

17.8 16.016.6

17.317.85.1

7.07.6

8.2

2.1

0.2

0.5

0.3

0.3

0.30.3

-5.7 -8.7 -7.3 -6.4 -6.7 -6.9 -7.1

-9

1

11

21

31

41

51

2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E 2013/14E

HUMAN PHARMACEUTICALS PRODUCTION VETERINARY PHARMACEUTICALS R&D Reconciliation

Σ 29.5Σ 29.5

Σ 27.1

Σ 33.2

Σ 39.0

Σ 43.4

Σ 47.3

Export of radiology

products should be the

main growth driver

Sanochemia Pharmazeutika AG

www.cbseydlerresearch.ag

Close Brothers Seydler Research AG | 27

Sales projection: Segment breakdown

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG;

Earnings projection

We expect that the internationalisation strategy will have a positive effect not only

on the top line, but also on SANOCHEMIA‟s earnings. Considering that price

pressures in European countries particularly in Germany significantly affect

company margins we believe that rapid expansion into pharmerging will notably

contribute to margin growth. For 2011/12E we expect EBIT margin in tune of 9%,

which should gradually increase to at least 13% in the long term (in best case

scenario we expect long-term operating margin to grow up to 15%)

Source: SANOCHEMIA Pharmazeutika AG; CBS Research AG; * Others include R&D and reconciliation

2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E 2013/14E CAGR 11E-14E

HUMAN PHARMACEUTICALS 15.1 18.3 16.1 18.2 21.7 25.1 28.1 15%

as % of total sales 51% 62% 60% 55% 56% 58% 59%

yoy change n.a. 21% -12% 13% 19% 16% 12%

of which export: 2.7 3.6 4.5 6.9 9.9 12.2 14.1 27%

as % of Human Pharmaceuticals 18% 20% 28% 38% 45% 49% 50%

yoy change n.a. 31% 26% 53% 44% 24% 16%

PRODUCTION 17.9 19.8 17.8 16.0 16.6 17.3 17.8 4%

as % of total sales 61% 67% 66% 48% 43% 40% 38%

yoy change n.a. 10% -10% -10% 4% 4% 3%

VETERINARY PHARMACEUTICALS 0.0 0.0 0.0 5.1 7.0 7.6 8.2 17%

as % of total sales 0% 0% 0% 15% 18% 18% 17%

yoy change n.a. n.a. n.a. n.a. 37% 9% 8%

R&D 2.1 0.2 0.5 0.3 0.3 0.3 0.3 0%

as % of total sales 7% 1% 2% 1% 1% 1% 1%

yoy change n.a. -92% 175% -37% 0% 0% 0%

Reconcilitation -5.7 -8.7 -7.3 -6.4 -6.7 -6.9 -7.1

TOTAL 29.5 29.5 27.1 33.2 39.0 43.4 47.3 13%

* Bulgaria, Greece, Italy, Malta, Slovakia,Slovenia, Spain and Cyprus

** Oman, Syrien, United Arab Emirates, Iran

*** Georgia

EBIT projection (Segment breakdown)

2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E 2013/14E CAGR 11E-14E

HUMAN PHARMACEUTICALS 2.2 1.7 -0.3 1.5 2.2 3.0 3.7 35%

EBIT margin 15% 9% -2% 8% 10% 12% 13%

yoy change n.a. -23% -120% n.m. 45% 39% 21%

PRODUCTION -0.3 -1.7 2.1 2.0 2.2 2.6 2.7 10%

EBIT margin -2% -9% 12% 13% 13% 15% 15%

yoy change n.a. -436% n.m. -4% 8% 20% 3%

VETERINARY PHARMACEUTICALS 0.0 0.0 0.0 0.5 0.8 0.8 0.9 22%

EBIT margin n.a. n.a. n.a. 10% 11% 11% 11%

yoy change n.a. n.a. n.a. n.a. 51% 10% 10%

Others* -3.1 -4.6 -3.0 -2.4 -1.7 -1.8 -2.0 -7%

TOTAL -1.2 -4.6 -1.3 1.6 3.4 4.6 5.3 48%

EBIT margin -4% -16% -5% 5% 9% 11% 11%

yoy change n.a. -279% 73% n.m. 111% 36% 14%

2.21.7

-0.3

1.52.2

3.03.7

-0.3-1.7

2.1 2.0 2.22.6

2.7

0.0 0.0 0.00.5 0.8 0.8 0.9

-5.7

-4.6

-3.0-2.4

-1.7 -1.8 -2.0

-6.0

-4.0

-2.0

0.0

2.0

4.0

2007/08 2008/09 2009/10 2010/11E 2011/12E 2012/13E 2013/14E

HUMAN PHARMACEUTICALS PRODUCTION VETERINARY PHARMACEUTICALS Others*

Expansion into

international markets

should improve