Risk and Returns: part 1 Economics 71a: Spring 2007 Mayo chapter 8 Malkiel, Chap 9-10 Lecture notes...

27

Risk and Returns: part 1 Economics 71a: Spring 2007 Mayo chapter 8 Malkiel, Chap 9-10 Lecture notes 3.2a

-

date post

21-Dec-2015 -

Category

Documents

-

view

216 -

download

1

Transcript of Risk and Returns: part 1 Economics 71a: Spring 2007 Mayo chapter 8 Malkiel, Chap 9-10 Lecture notes...

Risk and Returns: part 1

Economics 71a: Spring 2007

Mayo chapter 8Malkiel, Chap 9-10Lecture notes 3.2a

Goals

Return reminderWhat is risk?Types of riskStatistics backgroundRisk return tradeoff

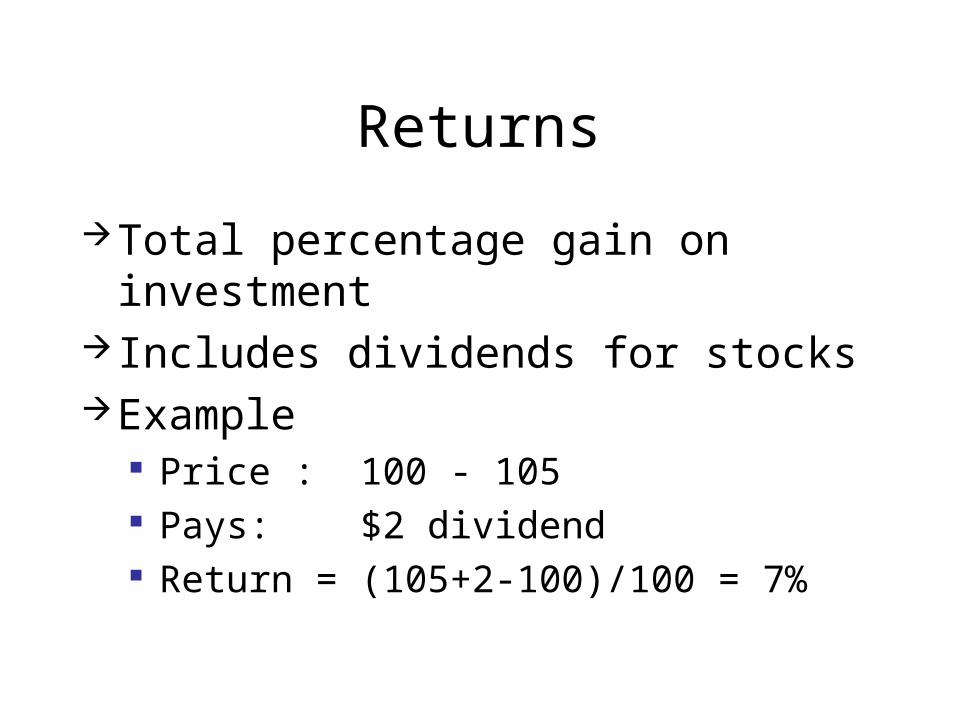

Returns

Total percentage gain on investment Includes dividends for stocksExample

Price : 100 - 105 Pays: $2 dividend Return = (105+2-100)/100 = 7%

What is Risk?

Hard questionNo good answerStatistical Features

Variance/Standard deviation Histograms (probability distributions)

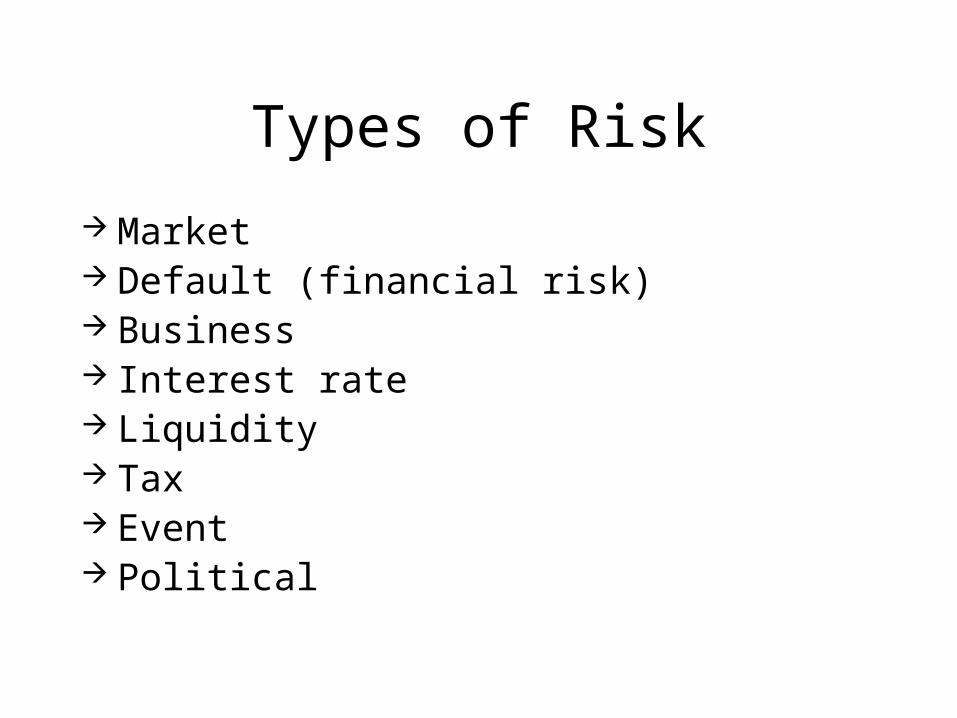

Types of Risk

Market Default (financial risk) Business Interest rate Liquidity Tax Event Political

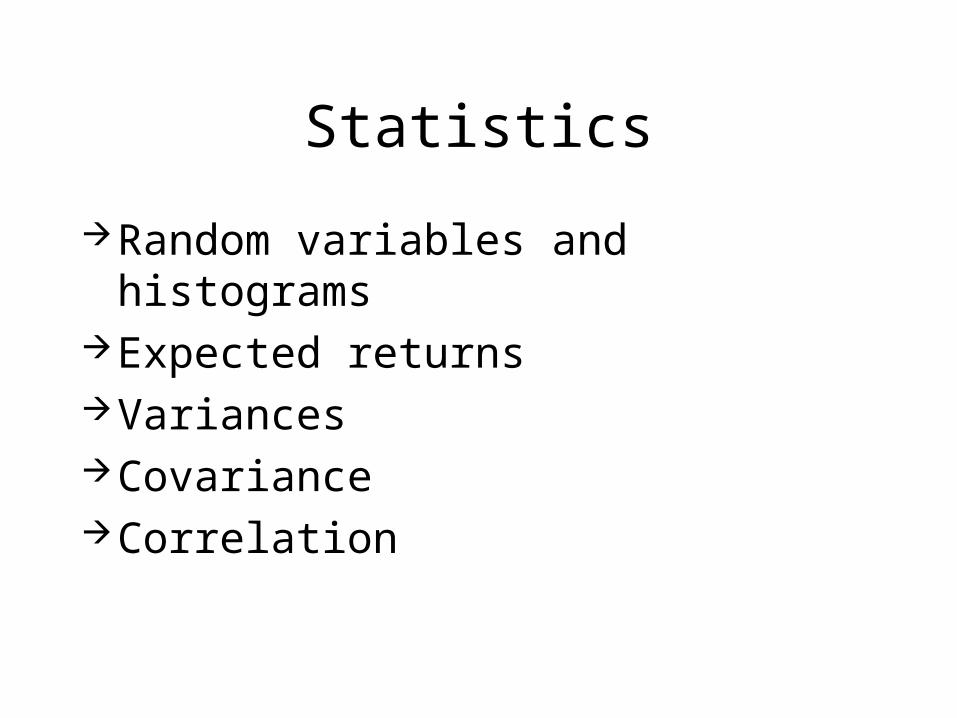

Statistics

Random variables and histograms Expected returnsVariancesCovarianceCorrelation

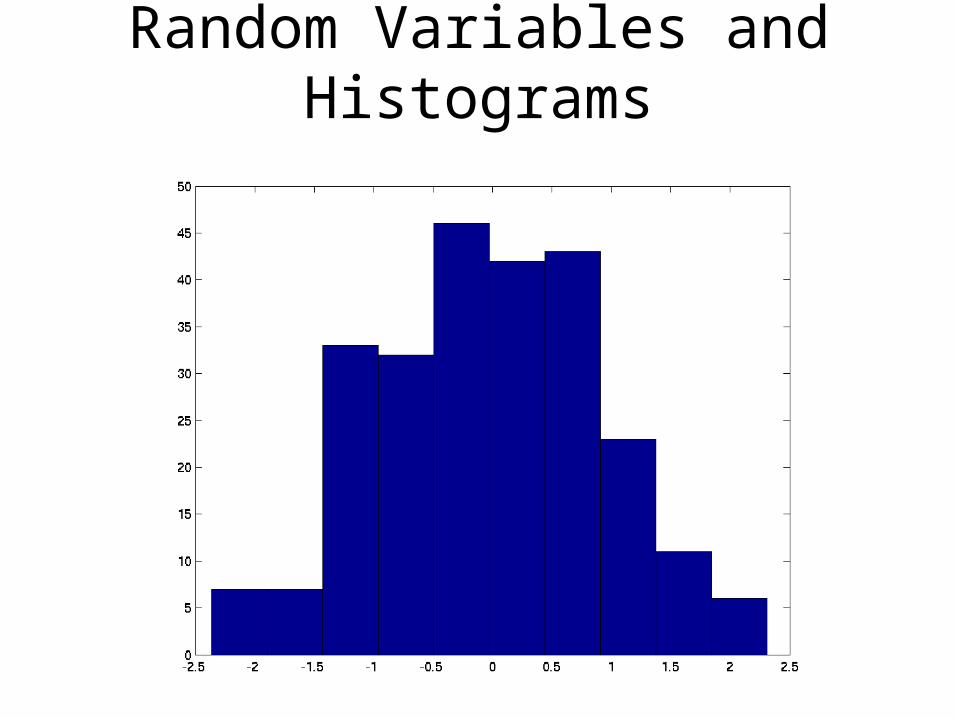

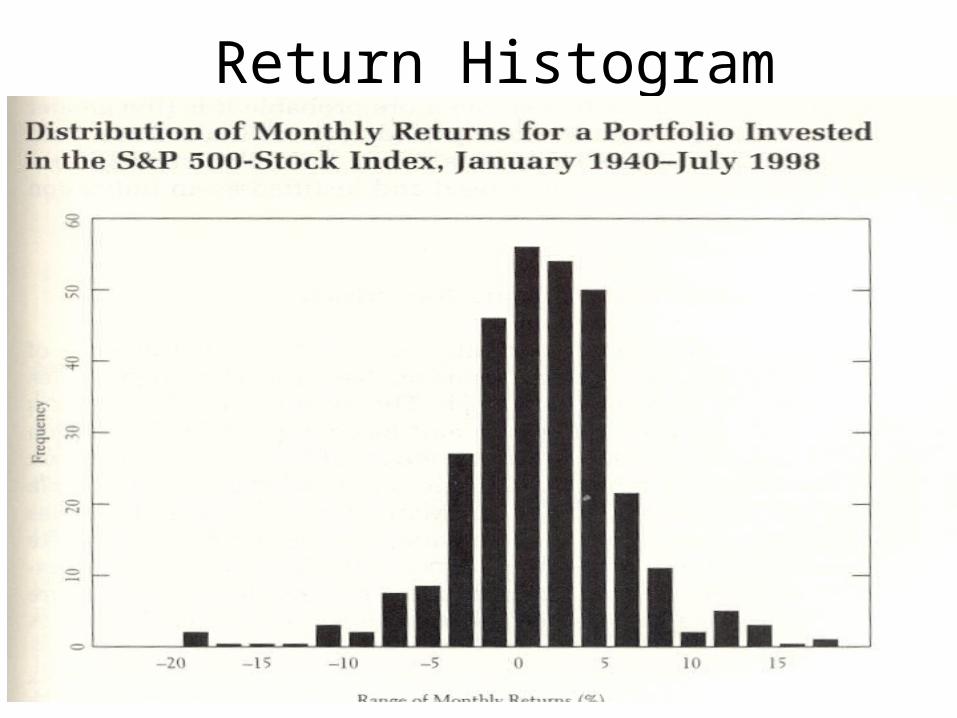

Histogram

Frequency with which random variable takes value

Gives a pictorial indication of riskMany possible shapesMost famous is the Normal Distribution

Random Variables and Histograms

Return Histogram

Expected Return, E(R)

N states of the world, 1, 2, ..,N

pi = probability of state i Ri = return in state i Also called “Expected value”

€

E(R) = piRi

i=1

N

∑

Mean

€

Mean(R) = R =1N

Ri

i=1

N

∑

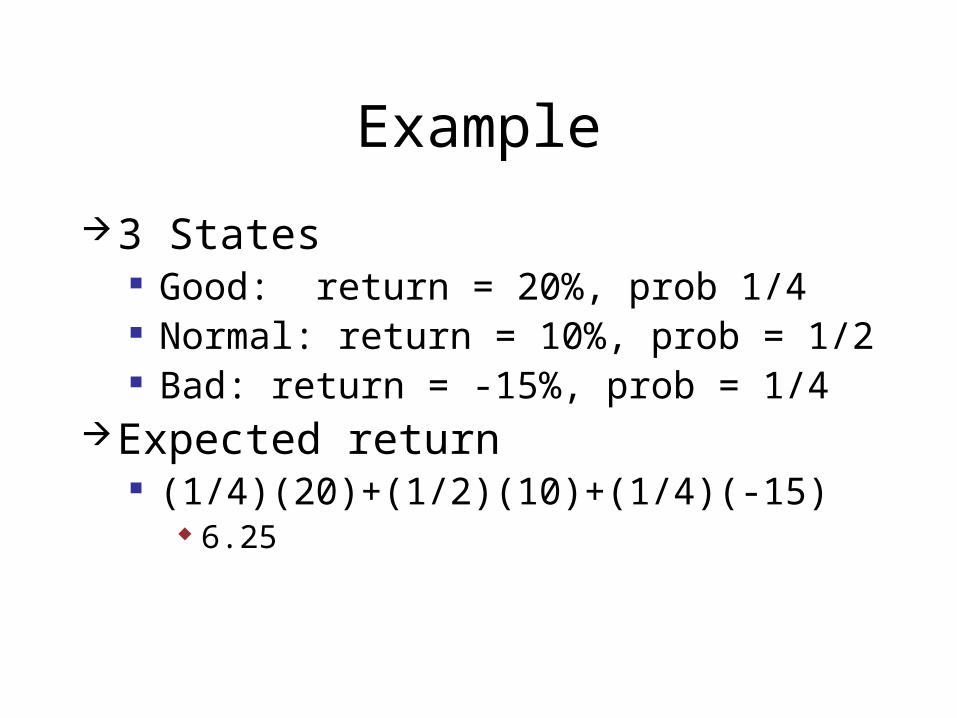

Example

3 States Good: return = 20%, prob 1/4 Normal: return = 10%, prob = 1/2 Bad: return = -15%, prob = 1/4

Expected return (1/4)(20)+(1/2)(10)+(1/4)(-15)

6.25

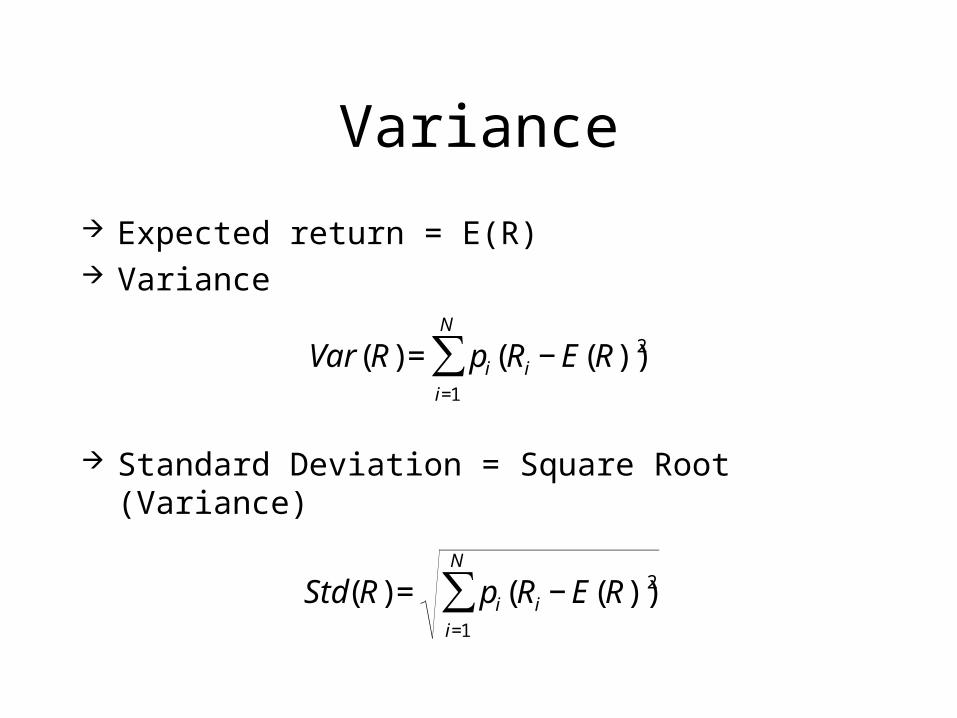

Variance

Expected return = E(R) Variance

Standard Deviation = Square Root (Variance)

€

Var (R) = pi (Ri − E(R))2

i=1

N

∑

€

Std(R) = pi (Ri − E(R))2

i=1

N

∑

Variance

€

var(R) =1

N −1(Ri − R )

i=1

N

∑2

R = mean(R)

std(R) = var(R)

Example

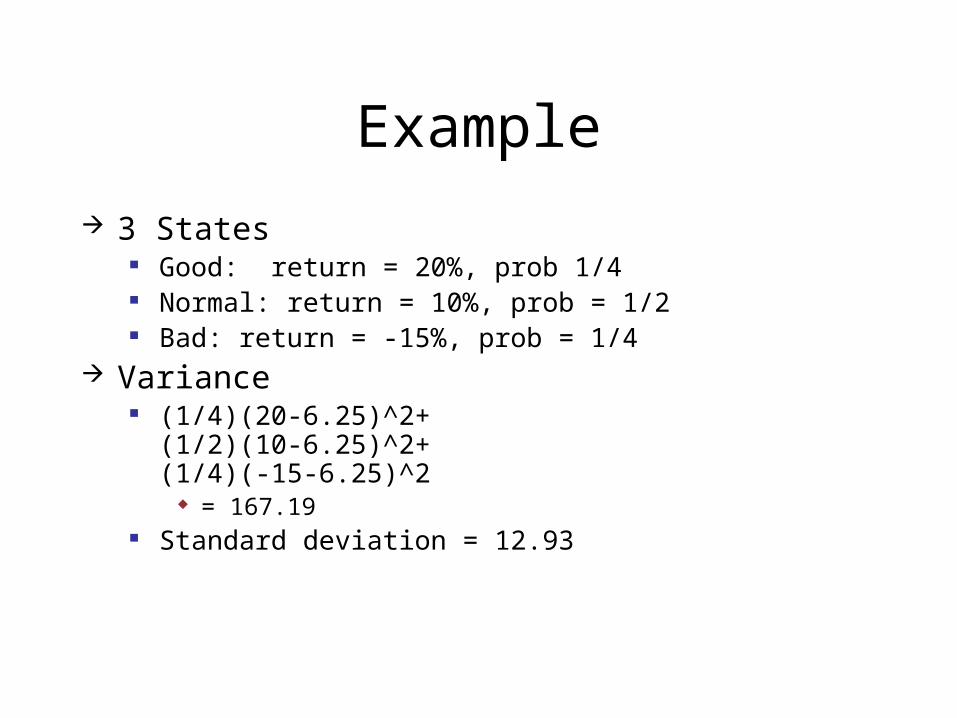

3 States Good: return = 20%, prob 1/4 Normal: return = 10%, prob = 1/2 Bad: return = -15%, prob = 1/4

Variance (1/4)(20-6.25)^2+

(1/2)(10-6.25)^2+(1/4)(-15-6.25)^2

= 167.19 Standard deviation = 12.93

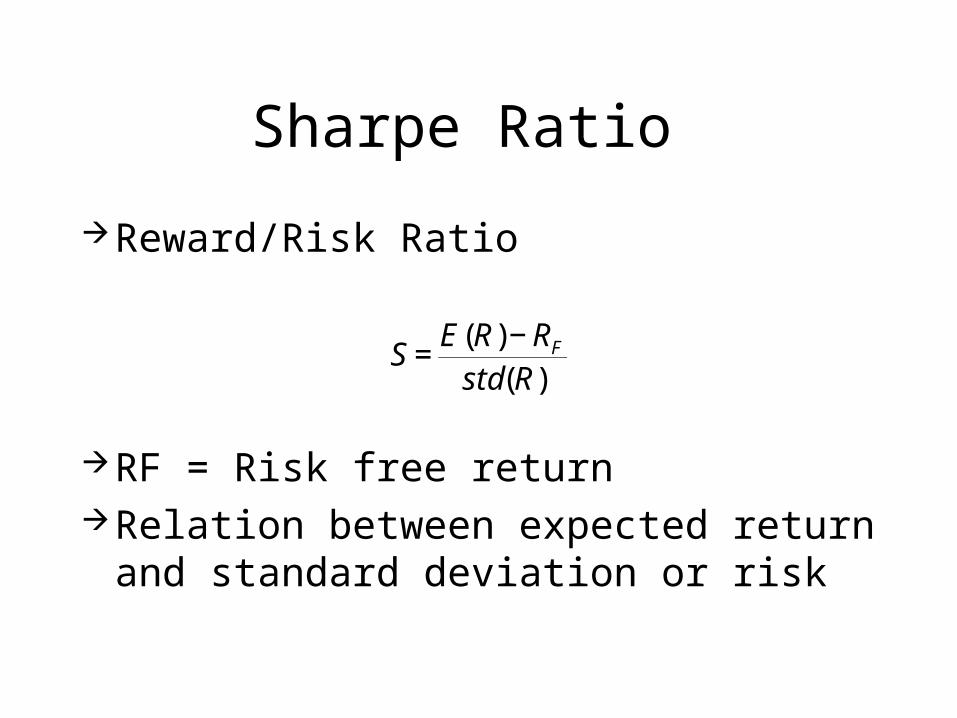

Sharpe Ratio

Reward/Risk Ratio

RF = Risk free returnRelation between expected return and

standard deviation or risk

€

S =E(R) − RF

std(R)

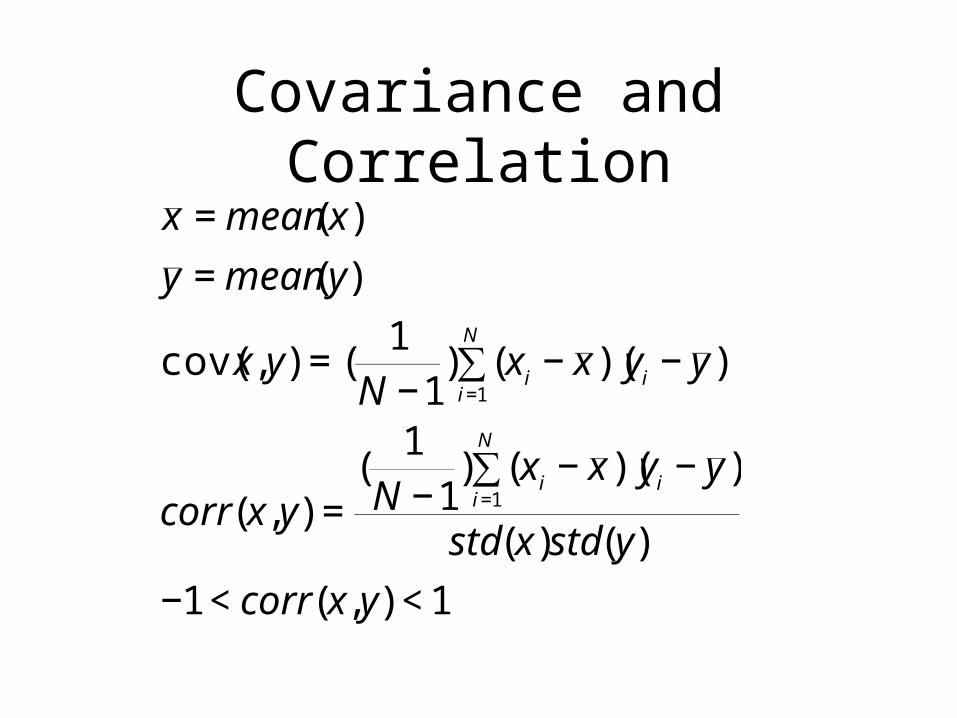

Covariance and Correlation

€

x = mean(x)

y = mean(y)

cov(x,y) = (1

N −1) (xi − x )(yi − y )

i=1

N

∑

corr(x,y) =(

1N −1

) (xi − x )(yi − y )i=1

N

∑

std(x)std(y)

−1 < corr(x,y) < 1

Expectations of Linear Functions

€

x = random variable

y = random variable

E(ax) = aE(x)

E(ax + c) = aE(x) + c

E(ax + by + c) = aE(x) + bE(y) + c

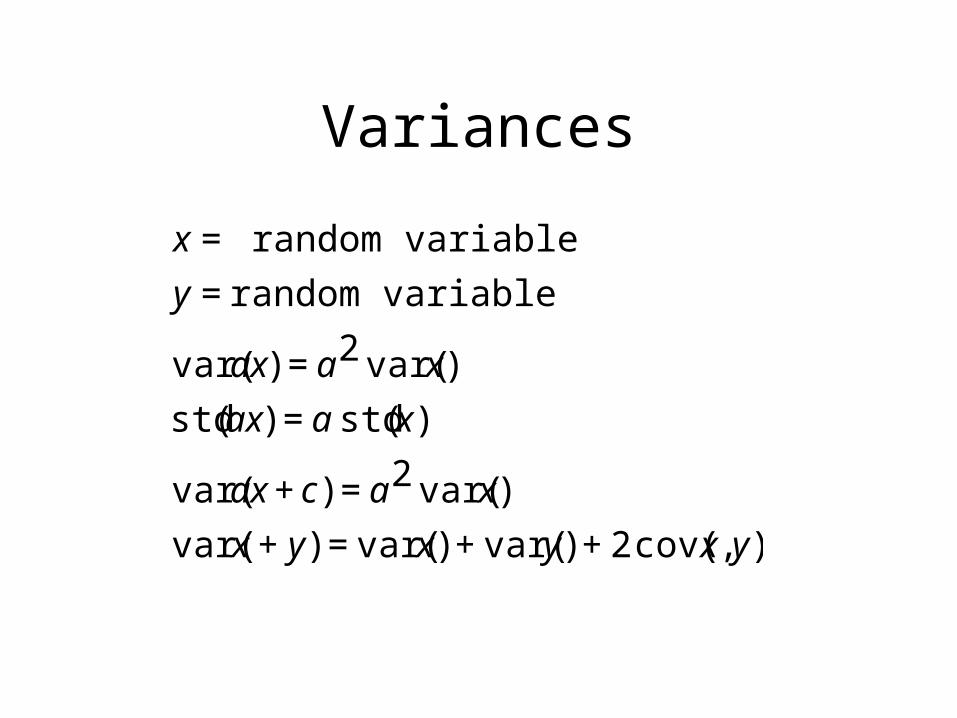

Variances

€

x = random variable

y = random variable

var(ax) = a2 var(x)

std(ax) = a std(x)

var(ax + c) = a2 var(x)

var(x + y) = var(x) + var(y) + 2 cov(x, y)

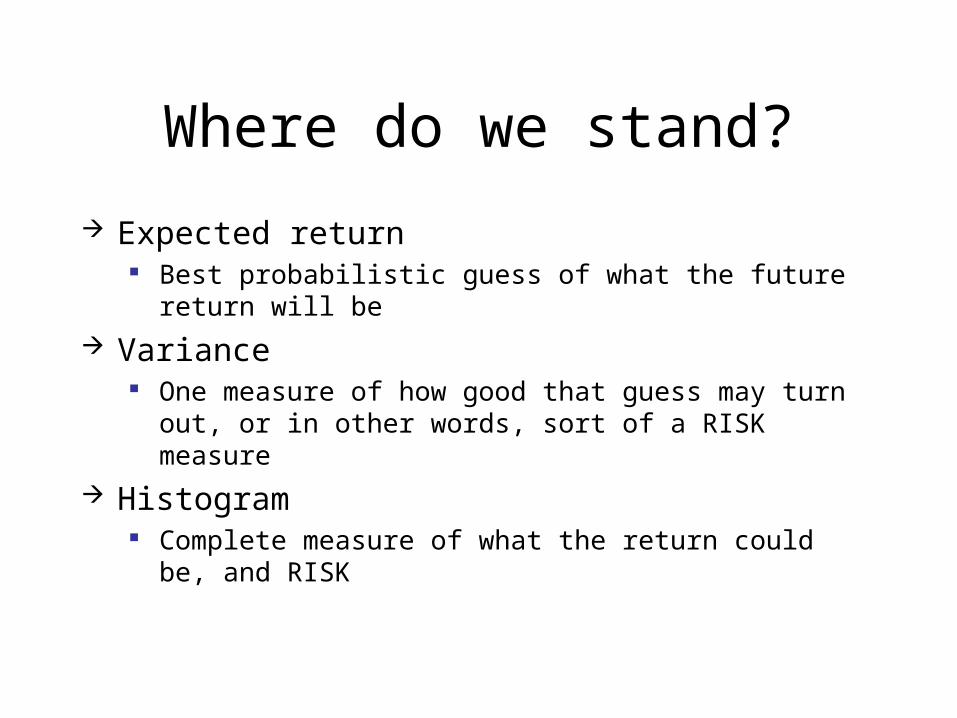

Where do we stand?

Expected return Best probabilistic guess of what the future return will be

Variance One measure of how good that guess may turn out, or in

other words, sort of a RISK measure

Histogram Complete measure of what the return could be, and RISK

Risk Versus Return

Efficient market world Return is fair payout for bearing risk Higher Risk -> Higher Return “No free lunch”

Not so efficient market world Opportunities might exist for low risk and high

return Need to search these out

Idealized Risk versus Return

Risk

Return

Returns

Realized returns Actually returns on your investments from

the pastExpected returns

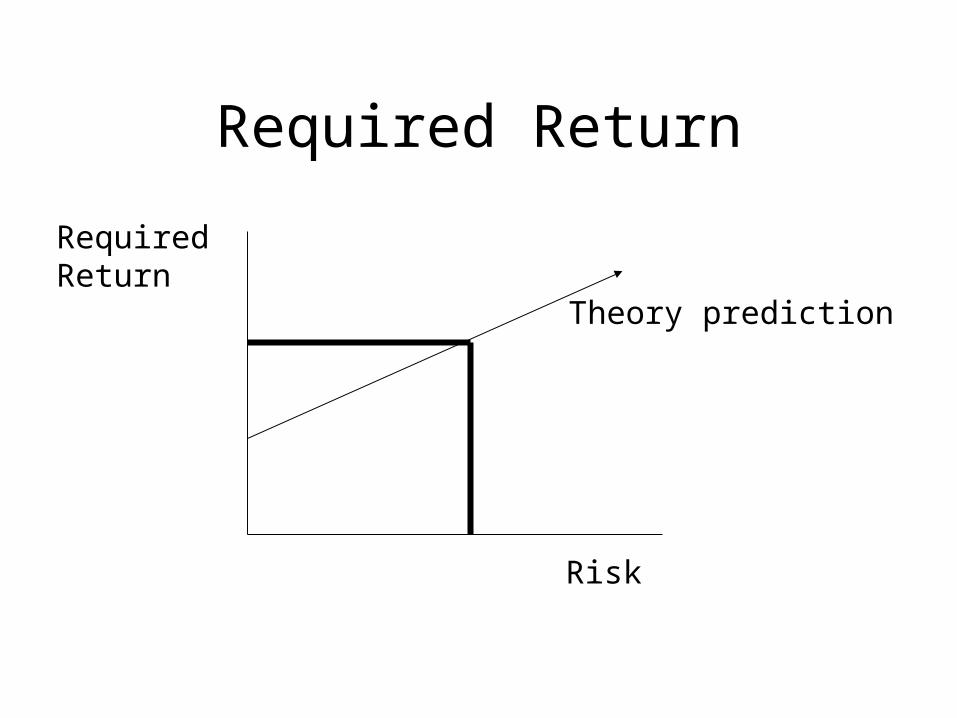

Mathematical forecast of future returnsRequired returns

Theoretically predicted return for a security given its risk level

Required Return

Risk

Required Return

Theory prediction

Risk versus ReturnEfficient Market View: Investment Opportunities

Risk

Return

*

* **

*

*

*

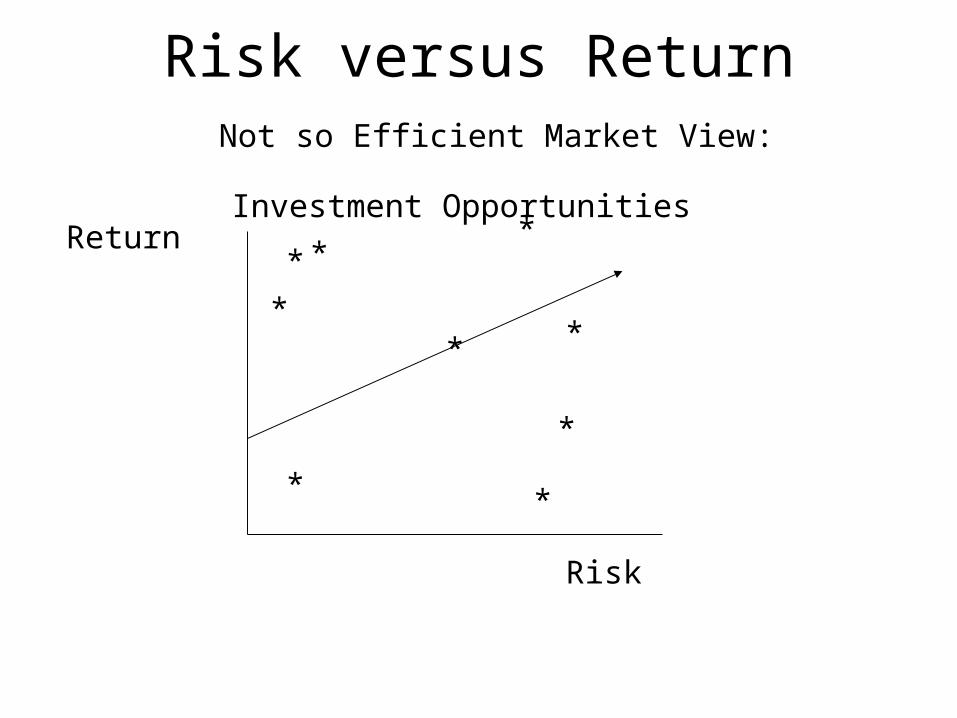

Risk versus Return Not so Efficient Market View: Investment Opportunities

Risk

Return*

**

*

*

**

*

*

Key Questions on Risk

What is the “right” measure of risk?How much risk do you want to bear

yourself?

![The Nutcracker (suite) [Op.71a] - Free-scores.com · Title: The Nutcracker (suite) [Op.71a] Author: Tchaikovsky, Piotr Ilitch - Arranger: Eduard Langer (1835 1905) - Publisher: New](https://static.fdocuments.us/doc/165x107/5b39d55c7f8b9a5a178ed2c7/the-nutcracker-suite-op71a-free-title-the-nutcracker-suite-op71a.jpg)