RIO ALTO MINING LIMITED (RIO) - Kallpa SAB · 2010-02-04 · RIO ALTO MINING LIMITED (RIO) 2 EQUITY...

14

RIO ALTO MINING LIMITED (RIO) 1 EQUITY RESEARCH Ricardo Carrión (627-5220) María Belén Vega (627-5220) [email protected] [email protected] The fair value of Rio Alto Mining Limited (RIO)’s equity, calculated over a discounted cash flow to equity model is USD$174.62 million. Fair value of RIO, taking into consideration the number of shares outstanding - post money is US$1.03 per share. We calculate the share’s fair value to be 194.51% higher than its current market price of USD$0.35 per share. It must be noted that this calculation was based on the total resources disclosed by the NI 43-101 and is focused mainly on the development and exploitation of the first stage of the La Arena Gold Oxide Project. RIO is a mining company dedicated to the development and exploitation of the gold and copper project La Arena, with shares trading in the TSX-V (TSXV: RIO), Frankfurt Stock Exchange (WKN: MS2) and the Bolsa de Valores de Lima (BVL: RIO). The corporate structure is depicted in the graphic below: RIO has the option to acquire from IAMGOLD (IMG) 100% of La Arena S.A. for USD$47.55 million. La Arena S.A. is the owner of 44 concessions with a total area of 21,000 hectares of which 1,720 hectares are the area of development of the oxide and sulphide deposits. November 19, 2009 RECOMENDATION: Overweight + Source: Bloomberg Elaborated by KALLPA SAB INITIAL COVERAGE Fair Value: USD 1.03 Va RIO ALTO MINING LIMITED (BVL: RIO) Fair Value of Equity (USD Million) 174.62 Fair Value of Share (USD) 1.03 Share Market Price (USD) 0.35 Shares Outstanding - Pre Money (Million) 75.50 Shares Outstanding - Post Money (Millon) 169.40 Market Capitalization (USD Million) 26.49 Trading BVL / TSXV / MS2 52 Week Range (USD) 0.06 / 0.41 Variation YTD 321.05% PER 2011 e 2.34 Option to buy 100% of La Arena S.A. from IAMGOLD Rio Alto Mining Ltd. La Arena S.A La Arena Proyect Other Prospects 21,000 ha. 1,720 ha. IAMGOLD

Transcript of RIO ALTO MINING LIMITED (RIO) - Kallpa SAB · 2010-02-04 · RIO ALTO MINING LIMITED (RIO) 2 EQUITY...

RIO ALTO MINING LIMITED (RIO)

1

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

The fair value of Rio Alto Mining Limited (RIO)’s equity,

calculated over a discounted cash flow to equity model is

USD$174.62 million. Fair value of RIO, taking into

consideration the number of shares outstanding - post money

is US$1.03 per share. We calculate the share’s fair value to be

194.51% higher than its current market price of USD$0.35

per share.

It must be noted that this calculation was based on the total

resources disclosed by the NI 43-101 and is focused mainly on

the development and exploitation of the first stage of the La

Arena Gold Oxide Project.

RIO is a mining company dedicated to the development and

exploitation of the gold and copper project La Arena, with

shares trading in the TSX-V (TSXV: RIO), Frankfurt Stock

Exchange (WKN: MS2) and the Bolsa de Valores de Lima

(BVL: RIO).

The corporate structure is depicted in the graphic below:

RIO has the option to acquire from IAMGOLD (IMG) 100%

of La Arena S.A. for USD$47.55 million. La Arena S.A. is the

owner of 44 concessions with a total area of 21,000 hectares

of which 1,720 hectares are the area of development of the

oxide and sulphide deposits.

November 19, 2009

RECOMENDATION:

Overweight +

Source: Bloomberg

Elaborated by KALLPA SAB

INITIAL COVERAGE

Fair Value: USD 1.03

Va RIO ALTO MINING LIMITED (BVL: RIO)

Fair Value of Equity (USD Mill ion) 174.62

Fair Value of Share (USD) 1.03

Share Market Price (USD) 0.35

Shares Outstanding - Pre Money (Mil lion) 75.50

Shares Outstanding - Post Money (Mil lon) 169.40

Market Capitalization (USD Mil lion) 26.49

Trading BVL / TSXV / MS2

52 Week Range (USD) 0.06 / 0.41

Variation YTD 321.05%

PER 2011e

2.34

Option to buy 100% of La

Arena S.A. from IAMGOLD

Rio Alto Mining Ltd.

La Arena S.A

La ArenaProyect

OtherProspects

21,000 ha.

1,720 ha.

IAMGOLD

RIO ALTO MINING LIMITED (RIO)

2

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

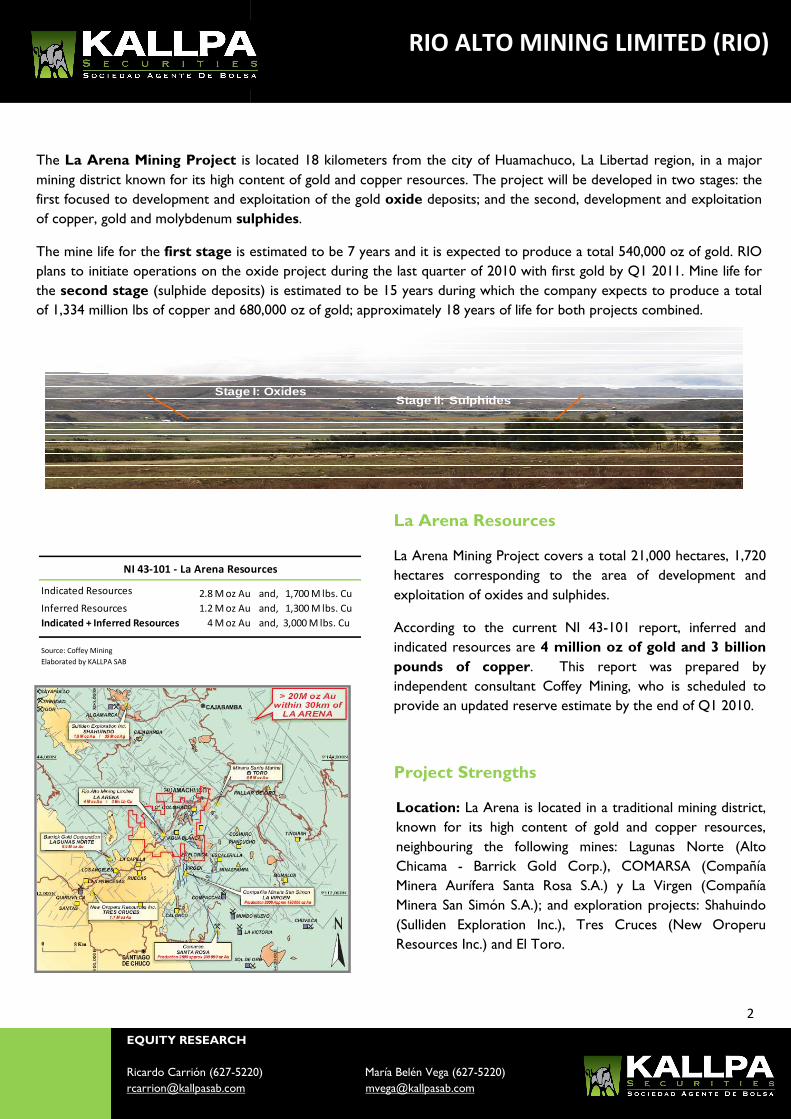

La Arena Resources

La Arena Mining Project covers a total 21,000 hectares, 1,720

hectares corresponding to the area of development and

exploitation of oxides and sulphides.

According to the current NI 43-101 report, inferred and

indicated resources are 4 million oz of gold and 3 billion

pounds of copper. This report was prepared by

independent consultant Coffey Mining, who is scheduled to

provide an updated reserve estimate by the end of Q1 2010.

Project Strengths

Location: La Arena is located in a traditional mining district,

known for its high content of gold and copper resources,

neighbouring the following mines: Lagunas Norte (Alto

Chicama - Barrick Gold Corp.), COMARSA (Compañía

Minera Aurífera Santa Rosa S.A.) y La Virgen (Compañía

Minera San Simón S.A.); and exploration projects: Shahuindo

(Sulliden Exploration Inc.), Tres Cruces (New Oroperu

Resources Inc.) and El Toro.

Source: Coffey Mining

Elaborated by KALLPA SAB

The La Arena Mining Project is located 18 kilometers from the city of Huamachuco, La Libertad region, in a major

mining district known for its high content of gold and copper resources. The project will be developed in two stages: the

first focused to development and exploitation of the gold oxide deposits; and the second, development and exploitation

of copper, gold and molybdenum sulphides.

The mine life for the first stage is estimated to be 7 years and it is expected to produce a total 540,000 oz of gold. RIO

plans to initiate operations on the oxide project during the last quarter of 2010 with first gold by Q1 2011. Mine life for

the second stage (sulphide deposits) is estimated to be 15 years during which the company expects to produce a total

of 1,334 million lbs of copper and 680,000 oz of gold; approximately 18 years of life for both projects combined.

Indicated Resources 2.8 M oz Au and, 1,700 M lbs. Cu

Inferred Resources 1.2 M oz Au and, 1,300 M lbs. Cu

Indicated + Inferred Resources 4 M oz Au and, 3,000 M lbs. Cu

NI 43-101 - La Arena Resources

Stage II: SulphidesStage I: Oxides

RIO ALTO MINING LIMITED (RIO)

3

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

La Arena’s proximity to major projects like Alto Chicama and

La Virgen not only are an indication of the exploration

potential of the area but also brings additional benefits to the

Project since many of the mining companies have invested in

the required infrastructure to initiate operations (e.g. power

lines). Proximity to the city of Huamachuco (12 km) reduces

expenses related to maintenance of a mining camp since the

majority of the workers live in that city.

Topography and Altitude: La Arena is located 3,400

meters above sea level, not a considerable altitude when

compared with many other mines in Peru. Also, the terrain

is relatively flat, an advantage that translates into cost savings

since it minimizes distances between mining areas and the

processing plant.

Existing infrastructure: Easy access to a paved road is a

great advantage as the Project is only 3.5 hours from the city

of Trujillo. With regards to power supply, an interconnected

high tension power line is located 15 kilometres from La

Arena. RIO is currently negotiating the installation of

infrastructure to connect to the power grid and include

these expenses in the cost per Kwh.

La Arena has access to underground water that will be

extracted by pneumatic pumping from a depth of

approximately 100 metres. Water will be reused once it has

been processed by mine operations.

Management and Board of Directors with mine

development and administration expertise: Directors

and Management of La Arena with proven experience in the

development and start up of mining projects. (Please read

Rio Alto Mining Limited’s Summary at

www.kallpasab.com/reporte-empresas.asp, Only available in

Spanish)

Good community relations: RIO has excellent relations

with local community members. Studies carried over La

Arena indicate a low probability of technical, environmental

or social difficulties that may impair the development of the

project. Another key advantage is the lack of systemic

agricultural activity in the area that could disturb mine

operations.

RIO ALTO MINING LIMITED (RIO)

4

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

Risk Factors and Mitigants

Prices of Gold and Copper: A decline in the price of

gold and copper would have a negative impact on the

financial results of La Arena. For the next five years market

consensus considers an average price higher than USD

1,000 per oz of gold and USD 2.5 per pound of copper.

With regards to the oxide project, our valuation has been

calculated on the base of an average price of USD 850 per

ounce of gold and an average operative cost per ounce

(cash cost) of USD 420. KALLPA SAB believes that during

the life of project, the price of gold won’t be lower than

USD 800 per ounce, thus easily exceeding the estimated

cash cost.

Financing Risk: Though mining operations require a

substantial investment of capital, start-up of La Arena

requires an initial investment of only USD 30 million; a

smaller investment than the start-up capital required by

most gold mines in Peru.

Political Risk: Operations could be hampered for

changes in regulation and development of political events;

i.e. elections. Nevertheless, it must be noted that during

the last two decades, Peru has become a very attractive

country for the development of mining operations which

is a reason why KALLPA SAB expects no fundamental

negative change to political risk.

Real reserves versus proven and probable reserves:

Like every mining company there is an amount of uncertainty

regarding possible differences between estimated and proven

reserves from studies and those actually extracted by

operations. Currently, Coffey Mining is updating existing

reserves for La Arena; this report should be finalized by the

end of Q1 2010.

Licenses, rights and permits: Usually among the risks

associated are those related to licenses, rights and permits. In

this particular case, RIO reached some very important

milestones when submitting its Environmental Impact Study

(EIA) to the Energy and Mines Ministry (MEM) in the month of

September of this year. It must be noted that the majority of

surface rights for the areas where the work for the oxide

project and subsequent sulphide project will be performed

have already been acquired. We must emphasize that RIO’s

operations will be carried out in a mining district and in

proximity to the city of Huamachuco where the community

understands mining activities.

RIO ALTO MINING LIMITED (RIO)

5

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

Valuation of the La Arena Mining Project

Calculation of the fair value of RIO’s equity was based on Coffey Mining’s NI 43 – 101 for the 1,720 hectares of the La

Arena project and focused on the first stage of the project corresponding to development and exploitation of the gold

oxide resources. KALLPA SAB believes that development of this first stage will generate significant value for the company

and make possible the funding of capital necessary to initiate operations on the second stage (sulphide project) and start

exploration on the other mining prospects located within the 21,000 hectares of La Arena. It is worth noting that, within

the 1,720 hectares of the project to be valued, oxide resources (720 hectares) represent only 1million oz of gold of the

total resources estimated by Coffey, hence, gold and copper reserves need to be valued in-situ in order to calculate the

actual fair value of RIO. As a consequence, the valuation of RIO’s La Arena Project includes the gold oxide project plus

value of gold and copper in-situ contained in the sulphide deposits.

I. Valuation of the Oxide Deposits

To calculate the value of the first stage gold oxide project, we used the Discounted Cashflow Valuation Method (DCF).

Thus, from the free cash flow to equity discounted at the shareholder’s cost of equity, which is 11.87%, we obtain a fair

value for RIO of USD 47.378 million.

Assumptions Used for the Valuation of Oxides

Price of gold Under a conservative approach, the price of gold used to

evaluate La Arena’s gold oxide project is USD 850 per

ounce. We must highlight that last month the price of gold

fluctuated between USD 1,028 and USD 1,142 per ounce.

Also, market consensus for the next four years is that the

price of the precious metal will continue to be above the

USD 1,000 mark as is shown in the table on the left.

Mineral reserves and production According to RIO´s management, total reserves for the

Oxide project reached 38.50 million tonnes with an average

ore grade for gold of 0.58 g/t and a recovery of 70%. Also,

the strip ratio is 1:1(one tonne of waste per tonne of ore).

These numbers are to be confirmed by Coffey Mining’s new

reserve estimate report due by end of Q1 2010.

The Company's production plan calls for extraction and

processing of 10,000 tonnes per day during the first year and

an increase to 24,000 tonnes per day starting in the second

year. Using the mentioned assumptions, development of the

gold oxide project would produce a total of 50,000 ounces

of gold in the first year and an average of 100,000 ounces for

each remaining year to complete 540,000 ounces of gold

during the estimated 7 years of life of the project.

Tonnes 38,500,000

Ore Grade (Au g/t) 0.58

Strip Ratio 1:1

First Stage - Oxide Deposit

Gold Price 2011 2012 2013 2014

Market Consensus (USD/oz) 1063 1082 1075 1198

KALLPA SAB (USD/oz) 850 850 850 850

Source: Bloomberg

Elaborated by KALLPA SAB

Source: Bloomberg

Elaborated by KALLPA SAB

Source: RIO

Elaborated by KALLPA SAB

500

600

700

800

900

1,000

1,100

1,200

En

eF

eb

Ma

rA

br

Ma

yJu

nJu

lA

go

Se

pO

ctN

ov

Dic

En

eF

eb

Ma

rA

br

Ma

yJu

nJu

lA

go

Se

pO

ctN

ov

Dic

En

eF

eb

Ma

rA

br

Ma

yJu

nJu

lA

go

Se

pO

ct

2007 2008 2009 . 2010 - 2017

US

D p

er

ou

nce

Evolution of Gold Price

Projection - USD 850 /ounce

RIO ALTO MINING LIMITED (RIO)

6

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

Estimated CAPEX

In order to initiate operations in Q4 2010, the gold oxide

project requires an initial investment of approximately USD

30 million. These funds will be used to acquire machinery and

equipment to build the plant and required infrastructure to

operate the project. It’s assumed that RIO will exercise the

option to purchase 100% of La Arena S.A. by 2012. The

exercise of this right will be reflected in a significant increase

of the CAPEX (USD 47.55 million) on that specific year. This

payment results in a significant increase of the CAPEX for La

Arena for that year as such payment corresponds to an

increase of the intangible assets of the project.

Estimated Operating Expense (OPEX)

Calculation of the operation expense (OPEX) for the oxide

project includes the mining, processing and treatment of ore

and effluents. According to management, mining cost totals

USD1.99 per tonne mined. Costs for processing and

treatment of ore and effluents were based on the preliminary

study prepared by the independent consultant Heap Leaching

Consulting S.A.C. in August 2009. This study detailed

processing, laboratory, maintenance and treatment of

effluents for the oxide project considering a production of

10,000 and 24,000 tons per day. The study determined that

the costs for the processing plant, chemical analysis lab and

its maintenance total approximately USD 1.69 and USD 1.44

per tonne for a rate of production ranging between 10,000

and 24,000 tonnes per day, respectively. Other fixed

expenses contemplated were waste treatment plants and

costs related to mining camp, salaries and insurance which

total USD 138 thousand and USD 346 thousand for a rate of

production of 10,000 and 24,000 tons per day, respectively.

Including all these items, the average operation cost (cash

cost) totals USD 420 per ounce produced.

It should be noted that Run of Mine (ROM) processing will

be through Dump Leaching, which has the advantage of not

requiring the additional cost of crushing.

Source: RIO

Elaborated by KALLPA SAB

Source: RIO

Elaborated by KALLPA SAB

-

20

40

60

80

100

120

2010 2011 2012 2013 2014 2015 2016 2017

US

D M

illi

on

Net Revenue vs OPEX and CAPEX

Net Revenue OPEX + CAPEX OPEX

OPEX

48 million

CAPEX

51 million

68%

22%

2%1%

7%

OPEX Distribution

Mining

Procesing Plant

Laboratory

Plant Maintance

Fixed Costs

RIO ALTO MINING LIMITED (RIO)

7

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

RIO ALTO MINING LIMITED

Income Statement (USD)

2011e

2012e

2013e

2014e

2015e

2016e

2017e

Total Revenues 42,768,110 107,044,370 76,138,553 71,451,596 85,850,143 46,991,936 29,004,415

Royalties -427,681 -1,540,887 -922,771 -829,032 -1,117,003 -469,919 -290,044

Net Revenue 42,340,429 105,503,482 75,215,782 70,622,564 84,733,140 46,522,017 28,714,371

Operating Expenses 1/

Cost of Sales

(Exc. depreciation y amortization) -23,321,722 -48,227,129 -49,666,217 -49,602,410 -49,034,927 -5,736,058 -1,272,000

Depreciation and Amortization 2/

-3,729,697 -3,926,063 -19,972,162 -19,992,888 -20,979,383 -2,875,533 -2,875,533

Selling, General and Admin. -500,000 -500,000 -500,000 -500,000 -500,000 -500,000 -500,000

Income From Operations 14,789,011 52,850,290 5,077,402 527,266 14,218,830 37,410,425 24,066,837

Other Income and Expenses - - -275 - - - -

Income Before Taxes and Worker Shares 14,789,011 52,850,290 5,077,127 527,266 14,218,830 37,410,425 24,066,837

Worker Shares -1,183,121 -4,228,023 -406,170 -42,181 -1,137,506 -2,992,834 -1,925,347

Income Tax -2,281,767 -14,586,680 -1,401,287 -145,525 -6,000,000 -10,325,277 -6,642,447

Net Income (Loss) 11,324,123 34,035,587 3,269,670 339,559 7,081,324 24,092,314 15,499,043

1/ Operating costs are kept relatively constant for the useful life of mine, except for the years 2016 and 2017. On those years, the operating cost related to mining is lower because the tonnes mined per day total

1.175 and 0 thousands, respectively, in comparison to the rate of production of 10,000 and 24,000 tons per day for previous years. Nevertheless the gold ounces recovered total 54 and 34 thousand, compared to the

annual production of 50 and 100 thousand. Therefore, ounces of gold recovered in the last two years would have lower operating costs since the tonnes leached would have been mined.

2/ The jump in the depreciation in the years 2013 - 2015 is due to the increase in the intangible assets of RIO after acquiring 100% of La Arena S.A. upon exercising the option with IMG. Intangible assets are

depreciated at an annual rate of 33.3%.

RIO ALTO MINING LIMITED (RIO)

8

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

Calculation of the Discount Rate

Calculation of the fair value of the first stage of the project

was based on the free cash flow to equity. The rate used to

discount the free cash flow to equity, corresponds to the

shareholder’s cost of equity (COK) as 100% of the

financing is equity based and corresponds to 11.87%.

To determine COK we used the Capital Asset Pricing Model

(CAPM) adjusted for emerging countries. The rate on risk

free assets equals 3.4% and results from the return of the 10

year American Treasury Bonds adjusted to Peruvian

premium risk debt. The latter adds a 2.20% premium to the

return of risk free assets.

COK

11.87%

Risk Free Rate(rf)

3.4%

Peruvian Premium Risk

2.20%

Levered Beta (b)

0.965

Market Premium (rm - rf)

6.50%

RIO ALTO MINING LIMITED

Free Cash Flow to Equity (USD)

2010e

2011e

2012e

2013e

2014e

2015e

2016e

2017e

Net Income - 11,324,123 34,035,587 3,269,670 339,559 7,081,324 24,092,314 15,499,043

Depreciation - 3,729,697 3,926,063 19,972,162 19,992,888 20,979,383 2,875,533 2,875,533

Cash Flow from Operating Activities - 15,053,820 37,961,650 23,241,832 20,332,447 28,060,707 26,967,847 18,374,576

Investing Activities

CAPEX 1/ 2/

-29,809,430 -1,788,420 -51,238,849 -3,966,795 -4,909,376 -5,314,008 1,147,601 -

Cash Flow Before Financing Activities -29,809,430 13,265,400 -13,277,199 19,275,038 15,423,071 22,746,698 28,115,448 18,374,576

Financing Activities

Rio Alto Mining Limited 30,000,000 - -

Issuing of Long Term Debt - - 11,799

Interest and Amortizations - - - -12,074 - - - -

Reserve Account 190,570 13,265,400 - - - - - -

Use of Reserve Account - - 13,265,400 - - - - -

Free Cash Flow to Equity - - - 19,262,964 15,423,071 22,746,698 28,115,448 18,374,576

1/ CAPEX for the year 2010 responds to the i nitia l investment required to s tart operati ons on the oxi de depos its .

2/ CAPEX for the year 2012 i ncl udes the payment of USD 47.55 mil l i on to IMG, after RIO exerci ses the option to acquire 100% of La Arena S.A.

RIO ALTO MINING LIMITED (RIO)

9

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

The employed beta was obtained from an average of mining

companies engaged in the exploration and development of

gold projects that are comparable to RIO, and are shown in

the table on the left. Thus the average unlevered beta for the

comparables is 0.9654 which is then applied to RIO’s

debt/equity structure. Since for the first stage, RIO will

finance its capital requirements through shareholder

contribution or issuance of new shares of the company, its

debt/capital structure is 1 and hence the unlevered and

levered betas are the same.

Finally, we assumed a market premium of 6.50%.

As mentioned before, La Arena resources, for both oxides

and sulphides, total 4 million ounces of gold and 3,000 million

lbs of copper. Of this amount, the oxide deposit has

approximately 1 million ounces of gold; while the sulphides 3

million ounces of gold and 3,000 million lbs of copper. This

evaluation assumes the development and exploitation of the

oxide project and leaves a balance of estimated resources of

3 million oz Au and 3,000 million lbs. Cu in-situ.

Canaccord Adams maintains a mining sector section that provides a weekly valuation of the price of ounce of gold and

pound of copper in-situ. This price is obtained from the weighted average of the market capitalization per ounce of gold

equivalent calculated for 40 junior companies trading in the TSX-V. The last report issued by Canaccord Adams, showed a

price of USD 40.56 per ounce of gold in-situ. KALLPA SAB used this price for valuation of gold in-situ. It must be

highlighted that among the list of comparable companies used by Canaccord Adams for this calculation we find six of the

companies we consider comparable to RIO. Furthermore, Canaccord Adams assumes an average price per pound of

copper in-situ of around USD 0.03. KALLPA SAB used USD 0.02 per pound of copper to determine the value of copper

in-situ.

Though La Arena will initiate operations soon, KALLPA SAB finds it prudent to apply a discount of 30% to the value of

average price of gold and copper in-situ. This discount will diminish with time as confidence and certainty grows from

development of the first stage resulting in the acquisition of capital necessary for the development and exploitation of the

second stage (sulphide project). Prices used to calculate value in-situ, after such discount are USD 28.41 and USD 0.014

per ounce of gold and pound of copper, respectively. Thus, the value corresponding to the resources for 3 million oz Au

and 3,000 million lbs. Cu is USD 85.24 and USD 42.00 million, respectively.

II. Valuation of Gold and Copper In-Situ

Assumptions for Valuation

Supuestos Empleados en la Valorización del Oro y Cobre In-situ

Source: RIO

Elaborated by KALLPA SAB

Gold (Au) Copper (Cu)

I. Oxides 1M oz Au -

II. Sulphides 3M oz Au 3,000M lbs. Cu

Total Oxides + Sulphides 4M oz Au 3,000M lbs. Cu

NI 43-101: Resources of La Arena Project

Source: RIO

Elaborated by KALLPA SAB

Company Country Unlevered Beta

Timmins Gold México 0.5707

Greystar Resources Colombia 1.5761

Guyana Goldfields Guyana 1.0081

Colossus Minerals Brazil 1.1284

Andina Minerals Inc Chile 0.8477

Luna Gold Corp Brazil 0.7910

Sulliden Exploration Inc Perú 1.4198

Pediment Gold Corp México 1.3620

Linear Gold Corp México 0.7697

Dorato Resources Perú 0.4685

International Tower Hill Alaska - EE.UU 0.6613

Rainly River Resources Canada 1.1274

Minera IRL Limited Perú 0.8188

Average 0.9654

Beta of Junior Comparable Mining Companies

RIO ALTO MINING LIMITED (RIO)

10

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

UPSIDE POTENCIALS

Price Vectors

In a conservative scenario, prices used to value gold and

copper amount to USD 850 per ounce and USD 2 per

pound, respectively. Given that market consensus expect

prices higher that USD 1,000 and USD 2.5 for ounce of

gold and pound of copper, respectively, this could be

translated later in an increase of the fair value calculated by

KALLPA SAB.

Sulphide Deposit

Although within the fair value of the company we have

assigned a value to mineral in-situ, the shareholder must

remember that such value has been assigned to a passive

situation where the mineral has not been extracted yet

and does not reflect real value if the company decides to

develop and exploit the project. In that sense, KALLPA

SAB believes it is convenient, and a good source of

reference, to establish the fair value of RIO in case the

sulphide project is developed. (See page 13) Also we must

note that valuation of the sulphide project does not

consider molybdenum production which may translate

into an additional source of revenue for RIO.

Potential for Further Exploration and

Development: Mining Prospects

Combined, the oxide and sulphide projects cover only an

area of 1,720 hectares of La Arena’s total of 21,000

hectares. Besides the mining project La Arena (oxide +

sulphide), RIO has other five prospects: María Angola, La

Florida, Cerro Colorado, Agua Blanca and El Alizar all with

a high potential for development of gold, copper and

molybdenum. Rio plans to start with preliminary

exploration of Agua Blanca as geological studies indicate a

high amount of copper and gold in La Florida due to its

proximity to La Virgen gold project.

Comparable Junior Mining Companies

We must point out that because RIO is a company relatively

new to the market and its project has not been extensively

marketed, its current market value is lower than those of

comparable companies at an earlier stage of development.

Dilution Effect

Valuation of the oxide deposit has been done using current

criteria as, for example, the total number of shares to be

issued by RIO to obtain capital for operations start-up. In this

regard, shareholders must remember that KALLPA SAB has

used the assumption of a USD 30 million CAPEX to be

financed via equity, taking into consideration the issuance of

shares at USD 0.35 per share. KALLPA SAB believes that if

the company decides to finance part of the project in the

future, it will be able to do it at higher levels than current

prices and therefore will require the issuance of a smaller

number of shares. (Lower dilution)

Company Country Market Cap. (USD)

Guyana Goldfields Guyana 401,638,602

Greystar Resources Colombia 390,014,377

International Tower Hill EE.UU 364,776,828

Colossus Minerals Brazil 363,066,717

Luna Gold Corp Brazil 162,884,044

Andina Minerals Inc Chile 154,250,329

Rainly River Resources Canadá 124,380,849

Timmins Gold México 107,077,899

Sulliden Exploration Inc Perú 91,426,659

MINERA IRL Limited Perú 71,048,060

Linear Gold Corp México 59,123,699

Pediment Gold Corp México 46,682,005

Dorato Resources Perú 40,052,772

Rio Alto Mining Limited Perú 27,950,000

Source: RIO

Elaborated by KALLPA SAB

RIO ALTO MINING LIMITED (RIO)

11

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

Potential for Additional Appreciation (UPSIDE): Development of Oxides + Sulphides

In addition to the previous valuation, focused in the development of the gold oxide deposit, we performed a valuation of the

resources stipulated in NI 43-101 contained in the project’s 1,720 hectares including not only the development and

exploitation of the oxide project but also the sulphides. That is to say this new valuation includes total development of the

resources: oxides + sulphides.

Therefore, from the free cash flow to equity resulting from the development and exploitation of the total resources, we

obtain a present value for the oxide + sulphide project of USD 219.62 million.

Additional Assumptions Used for Valuation of Oxides + Sulphides

To calculate the value of the oxide + sulphide project we

have used the assumptions detailed in the previous valuation

and other pertaining to the sulphide deposits which we

explain next.

Vector for Copper Prices

Using a conservative approach, the price of copper used to

calculate the value of sulphides is USD 2 per pound. We

must note that the market consensus is that the price will

fluctuate within USD 2.60 and USD 2.92 for the next four

years, as it is shown in the table on the left.

Mineral Reserves and Production

According to RIO´s management, total reserves for copper

and gold sulphide projects amount 184 million tonnes of ore

with an average ore grade of 0.4% and 0.3 g/t, respectively.

Likewise, recovery for copper and gold is estimated at 88%

and 40%, respectively. Strip ratio is calculated at 0.951:1.

These numbers are to be confirmed by Coffey Mining’s new

reserve estimate due by the end of 2010.

The production plan contemplates extraction and processing

of 36,000 tonnes of mineral per day during the life of project,

calculated to be 18 years. Using these assumptions the

development of the sulphide project would produce a total

of 1,334 million pounds of copper and 680,577 ounces

of gold.

Copper Price 2011 2012 2013 2014

Market Consensus (USD/pound.) 2.68 2.92 2.84 2.49

KALLPA SAB (USD/pound.) 2.00 2.00 2.00 2.00

Source: Bloomberg

Elaborated by KALLPA SAB

Source: Bloomberg

Elaborated by KALLPA SAB

Source: RIO

Elaborated by KALLPA SAB

1.00

1.50

2.00

2.50

3.00

3.50

4.00

4.50

En

eF

eb

Ma

rA

br

Ma

yJu

nJu

lA

go

Se

pO

ctN

ov

Dic

En

eF

eb

Ma

rA

br

Ma

yJu

nJu

lA

go

Se

pO

ctN

ov

Dic

En

eF

eb

Ma

rA

br

Ma

yJu

nJu

lA

go

Se

pO

ct

2007 2008 2009

US

D p

er

po

un

d

Evolution of Copper Price

Projection - USD 2 / pound

2010 - 2017

Tonnes 38,500,000

Ore Grade (Au g/t) 0.58

Strip Ratio 1:1

First Stage - Oxide Deposit

RIO ALTO MINING LIMITED (RIO)

12

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

Estimated Operation Costs (OPEX) The OPEX calculated for the sulphide project is USD 6.73 per tonne of mineral and USD 1.70 per tonne of waste. Within the USD 6.73, mining costs accounts for USD 1.99 per tonne of mineral and the other USD 4.74 include ore rehandling, processing, salaries and environmental & community costs. There are also costs related to the production of concentrates of copper and gold.

Estimated CAPEX

To initiate operations for the sulphide project, scheduled for

2015, the Company will require an initial capital investment of

approximately USD 300 million, to be used in the acquisition

of machinery and equipment also the construction of plant

and the necessary infrastructure to operate this project. We

assume that part of the initial CAPEX would be provided by

the cash flow from the first stage operation (oxides). It is

planned that the CAPEX not covered by the cash flow from

the oxide project will be financed as follows: 75% from the

issuance of shares of RIO and the remaining 25% from

issuance of a seven year debt.

Calculation of the Discount Rate

To calculate the value of the oxide + sulphide we worked

over the base of the free cash flow to the Company. The

rate used to discount free cash flow to the Company

corresponds to the weighted average cost of capital

(WACC), which is 10.95%. WACC combines shareholder’s

cost of capital and the cost of debt according to the debt /

capital structure of the company.

The cost of debt without taxes used is 4.90% the tax rate

used is 30%.

To determine COK we used the Capital Asset Pricing Model

(CAPM) adjusted for emerging countries. The rate of risk

free assets equals 3.4% and results from the return of 10 year

American Treasury Bonds adjusted to the Peruvian risk. The

latter adds a 2.20% premium to the return free of risk.

Source: RIO

Elaborated by KALLPA SAB

WACC

10.95%

D/(E+D)

25%

Cost of Debt* (1-T)

4.90%

E/(E+D)

75%

COK

12.97%

29%

13%

58%

CAPEX DistributionAccording to type of fixed assets

Intangibles

Buildings &

Roads

Plant &

Equipment

Source: RIO

Elaborated by KALLPA SAB

Tonnes 184,000,000

Ore Grade (Au g/t) 0.3 g/t

Ore Grade (Copper %) 0.4

Strip Ratio 0.951:1

Second Stage - Sulphides Deposit

RIO ALTO MINING LIMITED (RIO)

13

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

The employed beta was obtained from an average of junior

mining companies engaged in the exploration and

development of gold projects that we think are comparable

to RIO, and that are shown for the valuation of the oxides.

Thus the average unlevered beta for the comparables is of

0.9654 which is then leveraged to RIO’s debt/equity

structure which is of 75% equity and 25% debt. The levered

beta is 1.1343.

Lastly, we assumed a market premium of 6.50%.

Final Considerations

The following table shows a comparison of the total value of RIO taking into consideration the valuations contained in

this report.

In this table you can appreciate the substantial increase in the fair value of the equity caused by the development of the

sulphides instead of postponing the development or assigning the sulphides an in situ value.

I. Valuation of Oxides + Gold and Copper In Situ USD Million

Value of Oxides 47.38

Value of Gold In Situ 85.24

Value of Copper In Situ 42.00

Total Value of RIO 174.62

II. Valuation of Oxides + Sulphides USD Million

Total Value of RIO 219.62

Source: RIO

Elaborated by KALLPA SAB

COK

12.97%

Risk Free Rate (rf)

3.4%

Peruvian Premium Risk

2.20%

Levered Beta (b)

1.1343

Market Premium (rm - rf)

6.50%

RIO ALTO MINING LIMITED (RIO)

14

EQUITY RESEARCH

Ricardo Carrión (627-5220) María Belén Vega (627-5220)

[email protected] [email protected]

This document is for information purposes only. In no circumstances should be used or considered as an offer to sell or a solicitation of any offer to buy shares or other securities mentioned in this report. The information herein has been obtained from or it is based upon sources believed to be reliable, but KALLPA Securities Sociedad Agente de Bolsa does not guarantee the accuracy or certainty of such information, or future market values of stocks or other securities mentioned. The opinions expressed in this document constitute our opinion as of the date of this publication and are subject to change without notice. KALLPA Securities Sociedad Agente de Bolsa does not guarantee that updates could be carried out due to changes in market circumstances. Authors of this research report hereby certify that the view expressed herein accurately reflect his or her personal views and no part of the analysts´ compensation was, is or will be directly or indirectly linked to the specific recommendations or views expressed in this document. The securities mentioned herein may not be available for purchase in some countries. KALLPA Securities Sociedad Agente de Bolsa may have positions or be holding any of the investments or related investments mentioned in this document and effect transactions in any securities mentioned herein or may seek to do investment banking with them.

Management

Alberto Arispe CEO (+511) 6275225

Sales & Trading

Enrique Hernández Head Trader (+511) 6275221

Alberto Piaggio Trader (+511) 6275222

Corporate Finance & Capital Markets

Ricardo Carrión Managing Director (+511) 6275220

Equity Research

María Belén Vega Analyst (+511) 6275220

Miloban Paredes Analyst (+511) 6275220

Operations

Eduardo Macpherson Head of Operations (+511) 6275220

KALLPA SECURITIES SOCIEDAD AGENTE DE BOLSA