Rig market presentation -...

72

21 April 2016 Please refer to important disclosures on the last 6 pages of this document Andreas Stubsrud Direct: +47 24 13 21 16 Email: [email protected] Bård Rosef Direct: +47 24 13 21 56 Email: [email protected] Rig market presentation GCE NODE 2016

-

Upload

nguyentruc -

Category

Documents

-

view

215 -

download

0

Transcript of Rig market presentation -...

21 April 2016

Please refer to important disclosures on the last 6 pages of this document

Andreas Stubsrud

Direct: +47 24 13 21 16 Email: [email protected]

Bård Rosef

Direct: +47 24 13 21 56 Email: [email protected]

Rig market presentation

GCE NODE 2016

2 Source: Pareto Securities Equity Research

Oil market

Current OPEC-driven oil oversupply will evaporate in 2016 and 2017

Significant investments needed

Cost deflation and efficiency gains after pro-longed upcycle makes lower oil price sustainable in the long run

Rig market outlook

The worst demand down cycle in the history of offshore drilling

Supply will adjust due to cost of keeping rigs active and re-investment need building

Today’s topics

3

Table of contents

1. Oil market and E&P investments

2. Offshore drilling market

4

Oil market summary

Source: Pareto Securities Equity Research

Historic and Pareto Brent Crude Forecast

Oil demand grows 1-1.5mbd every year

Non-OPEC production from 2014 record growth to 2016 largest decline in 25 years

OPEC growth delays balancing: Iraq , Saudi record production - Iran nuclear sanctions lifted

Significant non-OPEC investments and oil prices ~USD 70/bbl needed to balance market long-term

Likelyhood of an «overshoot» increasing

5

2014: From deficit to surplus as OPEC changed strategy However, primarily the psychology of the market changing

Source: Pareto Securities Equity Research

2014 production growth/decline

0.8

-0.5

1.2

1.3

0.5

1.0

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

Productiondeficit 2013

US shale Non-OPECgrowth

OPEC growth Demandgrowth

Productionsurplus 2014

mbd

Very high non-OPEC production growth

The OPEC «surprise»

Demand somewhat soft

6

0.81.2

0.5

0.6

1.1

1.8

0.0

0.5

1.0

1.5

2.0

2.5

3.0

Productionsurplus 2014

US shale Non-OPECgrowth

OPEC growth Demandgrowth

Productionsurplus 2015

mbd

2015: OPEC continues to pump oil into the market «Lag» in production decline for non-OPEC production

Source: Pareto Securities Equity Research

2015 production growth/decline

Non-OPEC production growth halved

Iraq surprise + Saudi continuing to increase

Demand relatively strong

7

1.2

0.5

-0.7

0.2

0.81.0

0.0

0.5

1.0

1.5

2.0

Productionsurplus 2015

US shale Non-OPECgrowth

OPEC growth Demandgrowth

Productionsurplus 2016

mbd

2016: Momentum in production decline building High OPEC growth, with Iran sanctions lifted, delaying balancing

Source: Pareto Securities Equity Research

2016 production growth/decline

U.S. shale reponding rapidly to lower investments

Iran comeback

Assumed «low» demand growth Other non-OPEC

still growing

8

2017: Momentum in production decline building High OPEC growth, with Iran sanctions lifted, delays balancing

Source: Pareto Securities Equity Research

2017 production growth/decline excl. U.S. shale

0.5

-0.8

-0.4 0.4

1.0

-1.0

-0.5

0.0

0.5

1.0

Productionsurplus 2016

Non-OPECgrowth

OPEC growth Demand growth Productiondeficit YE'2017

mbd Significant increase in U.S. shale needed

Already «too late» for offshore production reversal

in 2017

Still «above normal» OPEC production growth

9

0%

5%

10%

15%

20%

25%

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015e

Spare capacity relative to world demand

OPEC production at record levels already

OPEC spare capacity

Structural decline in spare capacity

Non-OPEC production will have to grow also in the future, this in not 1986

Source: Pareto Securities Equity Research, IEA

0

1000

2000

3000

4000

5000

6000

7000

des. 62 des. 77 des. 92 des. 07

Iran production 1965-2016

Saudi production 1962-2016

0

2000

4000

6000

8000

10000

12000

des. 62 des. 82 des. 02

Iraq production 1965-2016

0.0

1.0

2.0

3.0

4.0

5.0

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Iraq crude production

mbd

10

Stronger than expected cost deflation offshore and onshore 30-40% cost deflation both onshore and offshore

Source: Company reports and data, Pareto Securities Equity Research

-30-35 % -30-35 %

-35-40 %

-20-45 %

-20-25 %

-15-20 %

-20-25 %

-15-35 %

-50 %

-45 %

-40 %

-35 %

-30 %

-25 %

-20 %

-15 %

-10 %

-5 %

0 %

Greenfielddeepwater

development

Greenfieldshallow waterdevelopment

"Full scale"subsea tie-back

Brownfieldprojects

Current prices Sustainable price reduction

-15-30 %

-10-20 %

-5-10 %

-20-40 %

-20-30 %-15-25%

-35 %

-30 %

-25 %

-20 %

-15 %

-10 %

-5 %

0 %

Drilling time per well Drilling & completioncost per lateral ft.

Well cost

2014 2015

Cost deflation U.S. shale Cost deflation offshore

11

US Lower 48 liquids production sensitive to oil price

Oil price > USD 50/bbl to re-ignite growth

Likely USD 70/bbl to balance market long-term

Source: Woodmackenzie, Pareto Securities Equity Research

US Lower 48 Liquids Production 2014-30e

0

2

4

6

8

10

12L48 Oil production (mill bbl/day)

USD 40 flat USD 50 flat USD 60 flat USD 70 flat Base case

-0.3

0.1

0.60.8

-0.4

-0.2

0.0

0.2

0.4

0.6

0.8

1.0

USD 40 flat USD 50 flat USD 60 flat USD 70 flat

mboed

Production growth p.a. 2017-2020

12

E&P spending falling significantly

Spending estimated down ~25% last year and another ~25% this year

Biggest declines for onshore U.S. which will rebound the most

*Source: Company data; Pareto

E&P spending growth and oil price

-30 %

-20 %

-10 %

0 %

10 %

20 %

30 %

0

20

40

60

80

100

120

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

y/y change

Nominal spending growth (rhs) Average Brent (lhs)

USD/bbl

13 1

3

Oil companies cutting spending because they “have to” do so

Oil companies need to cut their spending capex to bring their near to medum term budgets in balance

Needs ~USD 90/bbl to be able to spend as much as in 2014, which is unlikely but could lead to “overshoot” if required

*Statoil, Shell, Total, ENI, COP. Exxon, Chevron, Lukoil, PTTEP, Apache, OXY, BG , MROl, Husky, Murphy, Lundin, EnQuest

Source: Company data; Bloomberg; Pareto

E&P companies simplified cash flow overview*

46 46 50 52 58 49 51 52 53

155190

217242 232

176139 134 139

227

284 274

247 253

157146

0

50

100

150

200

250

300

350

2010 2011 2012 2013 2014 2015 2016e 2017e 2018e

Dividends Capex Operating cash flow

USDbn

USD 65/bbl

USD 55/bbl

USD 45/bbl

14

Project deferrals and cancellations remove > 3 mboepd by 2020

-16%

-37% -36%

-25%

-18%

-43%

-50%

-23%

-60%

-50%

-40%

-30%

-20%

-10%

0%

Majors USIndependents

US onshore Total

15 vs 14 16 vs 15

0

-0.6

-1.6

-2.4

-3.2

-4.6

-6 -7

-6

-5

-4

-3

-2

-1

0

2016 2017 2018 2019 2020 2021 2022

Capex budget reductions % – 2015/16e Annual oil production deferrals*– mill bbl/day

Source: Company Q4/15 reports,, Schlumberger, Pareto Securities Equity Research, * excluding tight oil

15

1.00.4

9.9

0

2

4

6

8

10

World annual demandgrowth

Chinese annual demandgrowth

Saudi Arabia crudeproduction

mbdmbd

15

Demand for new oil mainly driven by decline in existing production

Decline* in existing production is

equivalent to either

3-4x world demand growth

10x Chinese demand growth

1 Saudi Arabia every 3rd year

*Based on IHS Cera, IEA, Wood Mackenzie estimates and company guiding

Source: Pareto

Decline in existing production vs. demand growth and Saudi prod.

Annual decline in existing production: 3-4 mbd *

16 Source: Pareto Securities Equity Research, Petrobras

The impact of increased depletion is often overlooked

Oil growth/decline per year

Non-OPEC1.1 1 - 1.2

1 - 1.5

1

OPEC0.7

0.5

0

0.5

1

1.5

2

2% increase indepletion ex. Shale

U.S. shale & tight oilgrowth at "high" oil

prices

World demandgrowth

Current oversupply

mbd

Iran growth Q2'16-2017

OverprodutionQ2'16

17 1

7

In the short-term, 2010-14 investments limits production decline of long-lead offshore regions

Source: BP; Pareto

North Sea oil production

0

1

2

3

4

5

6

7

1970 1975 1980 1985 1990 1995 2000 2005 2010 2015e

New fields Historic/Base

mbd

18

0

2

4

6

8

10

12

14

16

2008 2009 2010 2011 2012 2013 2014 2015

USDbn

"Conventional" E&P spend down ~40%(2011 to 2015)

Source: Pareto Securities Equity Research, Rystad D-Cube

Estimated Petrobras post-salt capex down ~40% from peak

19 Source: Pareto Securities Equity Research, Petrobras

…which has seen post-salt production down 31% in the same period

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2008 2009 2010 2011 2012 2013 2014 2015

bpd (000)

Post-salt production

Post-salt production down 32%(January 2011 to July 2015)

20 Source: Pareto Securities Equity Research, Petrobras

…while total production is stable as pre-salt has grown

1,000

1,200

1,400

1,600

1,800

2,000

2,200

2,400

2008 2009 2010 2011 2012 2013 2014 2015

bpd (000)

Post-salt production Pre-salt production

21

Table of contents

1. Oil market and E&P investments

2. Offshore drilling market

22

E&P spending falling significantly

Spending estimated down ~25% last year and another ~25% this year

Biggest declines for onshore U.S. which will rebound the most

*Source: Company data; Pareto

E&P spending growth and oil price

-30 %

-20 %

-10 %

0 %

10 %

20 %

30 %

0

20

40

60

80

100

120

1997 1999 2001 2003 2005 2007 2009 2011 2013 2015

y/y change

Nominal spending growth (rhs) Average Brent (lhs)

USD/bbl

23

Current downturn (by far) the worst in the history of offshore drilling

Source: Pareto Securities Equity Research

Projected demand development vs. previous down cycles as % of pre-crisis high

New floater demand projections vs. August 2015 projection

50

60

70

80

90

100

110

120

-6 -5 -4 -3 -2 -1 0 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 33 34 35 36

1986 crash - Jackups 1986 crash - Floaters 1998-99 Asia crisis - Jackups

1998-99 Asia crisis - Floaters 2001-04 downcycle - Jackups 2001-04 downcycle - Floaters

2008-10 financial crisis - Jackups Current downturn - Floaters

Demand Peak Current stage in the cycle

Months vs. peak demand

24

Bigger cuts in brownfield drilling than originally projected

Source: Pareto Securities Equity Research

Demand by well type

New floater demand projections vs. August 2015 projection

85 91 104134

156 139107 ~95

2643

51

3833

29

17~15

10282

10090

85

75

60

~40

1 42

11

24

213 216

256266

276254

208

~150

0

50

100

150

200

250

300

apr.10 apr.11 apr.12 apr.13 apr.14 apr.15 des.15 TroughEst.

Development Appraisal Exploration Standby

# of floaters

25

Supply

Source: Pareto Securities Equity Research

Current floater fleet status

Currently Warm Cold Conf.

Contracted stacked stacked Total fleet Scrapped Marketed Total Inc. Scrap

2nd gen 18 7 9 34 19 72 % 53 % 34 %

3rd gen 20 10 9 39 21 67 % 51 % 33 %

4th gen 30 13 11 54 8 70 % 56 % 48 %

5th gen 17 7 17 41 4 71 % 41 % 38 %

6th gen 102 22 3 127 0 82 % 80 % 80 %

Total current fleet 187 59 49 295 52 76 % 63 % 54 %

Utilization

26

Supply expected to respond by delaying newbuilds

Source: Pareto Securities Equity Research

Expected delivery schedule IHS-orderbook vs. expected deliveries

Sete Brasil currenly expected to be moderated to seven rigs

Keppel CAN DO drillship and certain planned/on order semis in China not expected to be built

Newbuilds will continue to be dalayed and «timed to market» as it is better to stack at yard

Nevertheless remains an overhang as they will be bid agressively in tenders

21 20

29

7

11

9

6

4

3

3

70

43

0

10

20

30

40

50

60

70

80

Total orderbook Expected deliveries

Moored drillship

Benign semi

Harsh semi

Sete Brasil

Intl. drillship

0

10

20

30

40

50

60

70

jan

.16

apr.

16

jul.1

6

okt

.16

jan

.17

apr.

17

jul.1

7

okt

.17

jan

.18

apr.

18

jul.1

8

okt

.18

jan

.19

apr.

19

jul.1

9

okt

.19

jan

.20

apr.

20

jul.2

0

okt

.20

Intl. drillship Sete Brasil Harsh semi

Benign semi Moored drillship Original delivery schedule

Current delivery schedule

# of floaters delivered

27

Projected floater rig oversupply thorugh 2020

Source: Pareto Securities Equity Research

# of non-working rigs

-50

0

50

100

150

200

jan 2014 jan 2015 jan 2016 jan 2017 jan 2018 jan 2019 jan 2020

Scrapped Cold stacked Warm stacked/Idle Projected

# of floaters

28

Demand vs. total supply

Source: Pareto Securities Equity Research

Current floater fleet status

0

50

100

150

200

250

300

350

400

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011 2013 2015 2017 2019

Less than 10 years 10-20 years 20-30 years More than 30 years Total demand

# of rigs

29

Only 3 of 19 projected PDO’s submitted in 2013-14

Source: NPD; Companies; Pareto Securities Equity Research

Submitted field development plans in 2013-14 vs. NPD expectations

What happened to the «booming» NCS market?

19

3

2

9

5

Projected 2013-14PDO's in January 2013

PDO submitted in2013-14

PDO submitted in2015

Delayed Removed frompipeline

2x Barents

Sea

11x North Sea

7x Norwegian

Sea

Flyndre Oseberg Delta 2

Rimfaksdalen J. Sverdrup Maria

Downcycle on NCS primarily driven by reduced development drilling demand

This trend started long before the decline in the oil price

30

Norwegian Continental Shelf is not dead this time either

Source: Pareto Securities Equity Research

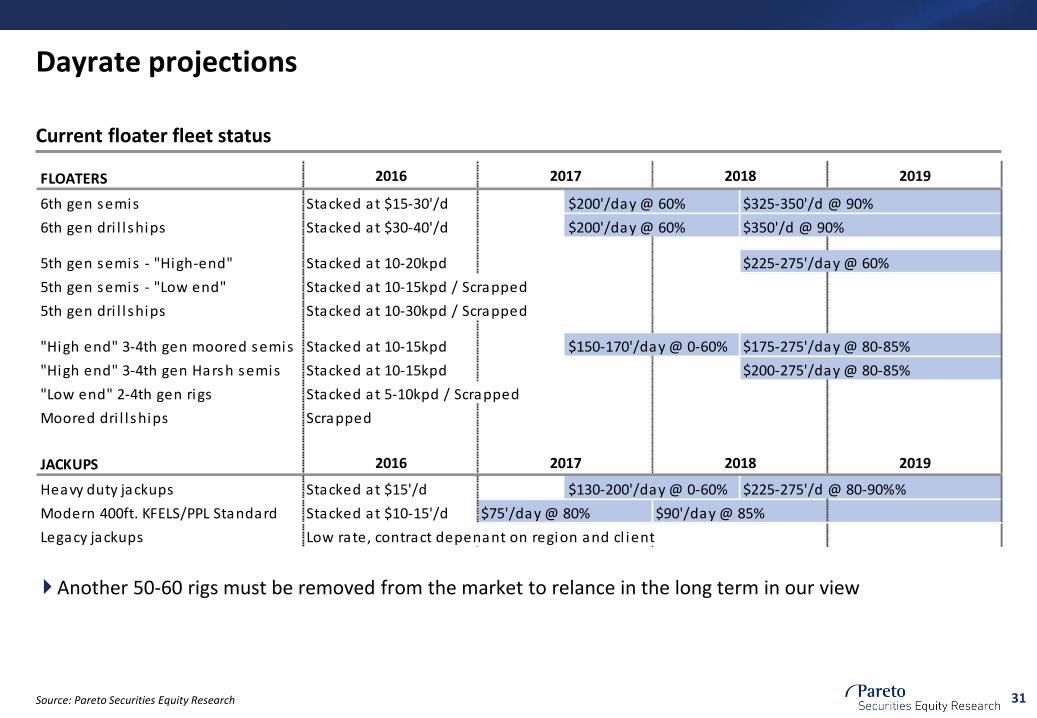

31

Dayrate projections

Source: Pareto Securities Equity Research

Current floater fleet status

Another 50-60 rigs must be removed from the market to relance in the long term in our view

FLOATERS

6th gen semis Stacked at $15-30'/d $200'/day @ 60% $325-350'/d @ 90%

6th gen dri l l ships Stacked at $30-40'/d $200'/day @ 60% $350'/d @ 90%

5th gen semis - "High-end" Stacked at 10-20kpd $225-275'/day @ 60%

5th gen semis - "Low end" Stacked at 10-15kpd / Scrapped

5th gen dri l l ships Stacked at 10-30kpd / Scrapped

"High end" 3-4th gen moored semis Stacked at 10-15kpd $150-170'/day @ 0-60% $175-275'/day @ 80-85%

"High end" 3-4th gen Harsh semis Stacked at 10-15kpd $200-275'/day @ 80-85%

"Low end" 2-4th gen rigs Stacked at 5-10kpd / Scrapped

Moored dri l l ships Scrapped

JACKUPS

Heavy duty jackups Stacked at $15'/d $130-200'/day @ 0-60% $225-275'/d @ 80-90%%

Modern 400ft. KFELS/PPL Standard Stacked at $10-15'/d $75'/day @ 80% $90'/day @ 85%

Legacy jackups Low rate, contract depenant on region and cl ient

2016 2017 2018 2019

2016 2017 2018 2019

32 Source: Pareto Securities Equity Research

Oil market

Current OPEC-driven oil oversupply will evaporate in 2016 and 2017

Significant investments needed

Cost deflation and efficiency gains after pro-longed upcycle makes lower oil price sustainable in the long run

Rig market outlook

The worst demand down cycle in the history of offshore drilling

Supply will adjust due to cost of keeping rigs active and re-investment need building

Today’s topics

33

APPENDIX

34

Demand recovery projected during 2018

Source: Pareto Securities Equity Research

Non-OPEC ex. Shale & FSU production growth vs E&P spending: 2000-18e Y-o-Y change in E&P spending, rig spending

Relative loss of market share to shale when the market recovers, with oil price lows reducing the «bear case» on sanctioning of long-cycled offshore greenfield projects

Activity revovery to ~80% of peak levels by YE’2018

Cumulative revenue of covered names down ~45% from the 2014 level reflecting new oil price reality

Initial recovery driven by tie-ins and recovery in brownfield drilling due to long lead times for large greenfield projects

Recovery driven by (1) accelerating depletion, (2) «more for less» prominent also offshore (3) 2018 the year when on-the-shelf projects looks likey to come back (based on Q1’16 oil price trough)

-25 % -25 %

No est. No est.

-14 %

-24 %

-14 %

29 %

-16 %

-23 %-20 %

1 %

-30 %

-20 %

-10 %

0 %

10 %

20 %

30 %

40 %

2015e 2016e 2017e 2018e

Total E&P spending Rig count Rig lease spending

0.5

0.1

0.4

-0.1

-0.3

-0.5

0.0

-0.3-0.1

0.5

0.8

-0.2

-0.8

0.3

1.2

0.8

0.1

-0.4

-0.8 -30%

-15%

0%

15%

30%

45%

-1.0

-0.5

0.0

0.5

1.0

1.5

2000 2002 2004 2006 2008 2010 2012 2014 2016e 2018e

Non-OPEC ex. US shale and FSU yoy Nominal spending growth yoy (rhs)

mbd spending

35

NCS floater market summary Bleak outlook on delayed development projects

Source: Pareto Securities Equity Research

Downturn driven by reduced development activity

Only 3 of 19 projected PDO’s submitted during 2013-14, with the downturn starting long before the oil price decline. Delayed tie-in projects in the Norwegian Sea the biggest disappointment

Exploration activity is expected to remain decent at current oil prices (although lower than in 2012-13) due to tax break, APA 2015 acreage and reduced drilling cost

Project economics to benefit materially for oilco’s on lower drilling cost with project pipeline primarily consisting of tie-back projects where well construction cost is a larger part of total capex than for new developments

Ample supply and limited contract opportunities in 2016

14 floaters available by YE’2016 and 21 of 28 available by YE’2017 with J. Sverdrup contract for Deepsea Atlantic the first long term contract award by Statoil since August 2013

Only 2 active tenders on-going with few other development drilling opportunities in the near-term pipeline other than some roll-overs in at Statoil’s North Sea brownfields

Exploration drilling, largely driven by smaller independents, expected to be short lead-time and short-duration contracts given well supplied market

Several rigs are very old and due for replacement

With very efficient high spec 6th gen semi Deepsea Atlantic getting USD 300’/day on long-term contract, short term work will be at lower rates. Idle time expected for rigs available in 2016

Legacy rigs is expected to largely be cold stacked with crew informed of lay offs for both coming off contracts in 2H’2015. Unlikely to come back unless demand picks up significantly, with more efficient rigs available

36

Significant open capacity following two years «without» contracts

Source: IHS-Petrodata; Pareto Securities Equity Research

NCS floater fleet overview

NCS fleet overview: 14 rigs available by YE’2016, 21 by YE’2017

J. Sverdrup award to Deepsea Atlantic the first contract awarded by Statoil since August 2013

6 rigs available in 2H’2015 including 4 high spec rigs

14 rigs available through YE’2016

21 of 28 contracted (incl. Newbuilds)rigs available through 2017

Rig Owner Built Type Operator Free

West Navigator NADL 2000 5G - jan.15 "Luke-warm"/Cold stacked

Trans. Spitsbergen Transocean 2010 6G - jun.15 Warm stacked

West Venture NADL 2000 5G Statoil jul.15

Trans. Searcher Transocean 1983 3G Edison aug.15

Bredford Dolphin Fred. Olsen 1980 3G AGR sep.15

Transocean Barents Transocean 2009 6G Shell sep.15

Island Innovator Maracc 2012 5G Lundin jan.16

Trans. Arctic Transocean 1986 4G RMN/OMV feb.16

Songa Trym Songa 1976 2G Statoil mar.16

Leiv Eiriksson Ocean Rig 2001 5G Rig share mar.16

Transocean Winner Transocean 1983 3G Det Norske jul.16

West Alpha NADL 1986 4G Exxon jul.16

COSLPioneer COSL 2010 5G Statoil aug.16

Songa Delta Songa 1980 3G Statoil sep.16

Songa Dee Songa 1984 3G Statoil okt.16

Bideford Dolphin Fred. Olsen 1975 3G Statoil jan.17

West Hercules Seadrill 2008 6G Statoil jan.17 Working in Canada Planned return

Stena Don Stena 2001 4G Statoil feb.17

Scarabeo 5 Saipem 1990 4G Statoil jun.17

Deepsea Bergen Odfjell 1983 3G Statoil jun.17

Scarabeo 8 Saipem 2012 6G Eni jul.17

Borgland Dolphin Fred. Olsen 1977 3G Rig share des.17

Deepsea Atlantic Odfjell 2009 6G Statoil mar.19

Transocean Leader Transocean 1987 4G EnQuest mai.19 Leaving to UK

COSLInnovator COSL 2011 5G Statoil sep.19

COSLPromoter COSL 2012 5G Statoil des.19

Songa Equinox Songa 2015 6G Statoil sep.23

Songa Endurance Songa 2015 6G Statoil nov.23

Songa Encourage Songa 2016 6G Statoil mar.24

Songa Enabler Songa 2016 6G Statoil jun.24

Q3

2015 2016 2017

Q1 Q2 Q3 Q4 Q1 Q2 Q4 Q1 Q2 Q3 Q4

37

Exploration drilling likely to be spot contracts

Source: IHS-Petrodata; Pareto Securities Equity Research

Currently active tenders on the NCS

Currently only two outstanding tenders with 2H’16 – 1H’17 start-up

Currently only three active tenders with start up in 2H’2016 to 1H’2017, of which at least one requires high spec rig

Status Operator Area Field Exp. Duration Exp. start-up Exp. award Comments

Actively

tenderingStatoil North Sea J. Sverdrup Ph. 1 3 years Mid-2016 2Q'2015 Targeting award before summer. Min 5,000 ton VDL

Actively

tenderingDetnor North Sea Alvheim Area 250 days 2H'2016 2H'2015

Tendering against the renewal of Transocean Winner

(contract expiry Jul-16). Current tender for 4 wells, but

could be longer term contract

Actively

tenderingWintershall

Norwegian

SeaMaria 580 days 2Q'2017 3Q'2015

4 proucers and 2 injectors from two subsea templates.

Delayed twice. Needs higher spec rig

Other potential demand

Status Operator Area Field Exp. Duration Exp. start-up Exp. award Comments

Likely

retendered.

Pot. jackup

Premier North Sea Vette (ex-Bream) 400 days 2017 2015-16

Expected to be retendered following delay in Jan-15.

Tender which closed in October 2014 saw 5 jackups and 5

semis offered. ~400ft. W.d.

Pre-tendering Repsol Misc. Exploration ~100-150 days mid-2016 N/ARepsol has issued RFI for 2-3 well exploration program in

2016. High spec rig required. Could be part of a rig share

Expects to use

West HerculesStatoil

Norwegian

SeaAasta Hansteen ~500 days 1H'2016 N/A

Plans to use West Hercules for the job. The rig is currently

drilling exploration wells in Canada and is contracted to

Jan 2017 (would likely need short extension to complete

campaign). Statoil also made disoveries of ~100-120m

bbls in 2015 exploration campaign, that will lead to follow

up work ("likely fast track") in Aasta Hansteen area

38

Given well-supplied market, we expect short lead-time/duration contracts

Source: NPD; Pareto Securities Equity Research

Historical # of exploration and appraisal wells by basin (start date)

Exploration activity expected to remain decent at 30-40 wells per year

~40 exploration and appraisal wells expected in 2015 which is down from very high 55-60 level in 2013-14

Statoil the company contributing most to reduction, down from 19 operated wells to 8-12 in 2015

Exploration activity expected to remain decent at ~30-40 wells p.a. going forward even at current oil price level

Modest investment to drill exploration wells on NCS due to tax refund introduced in 2005

46 more blocks incl. in APA 2015 round

In recent years’ tight market, other oilco’s have jointly chartered rigs with well slots to “offer” attractive duration, however going forward, the majority of the exploration contracts will likely be well based as on UK shelf

Exception of Statoil and Lundin which will use 1+ rig for E&A drilling each

0

10

20

30

40

50

60

70

North Sea Norwegian Sea Barents Sea

Exploration tax refund introduced

39

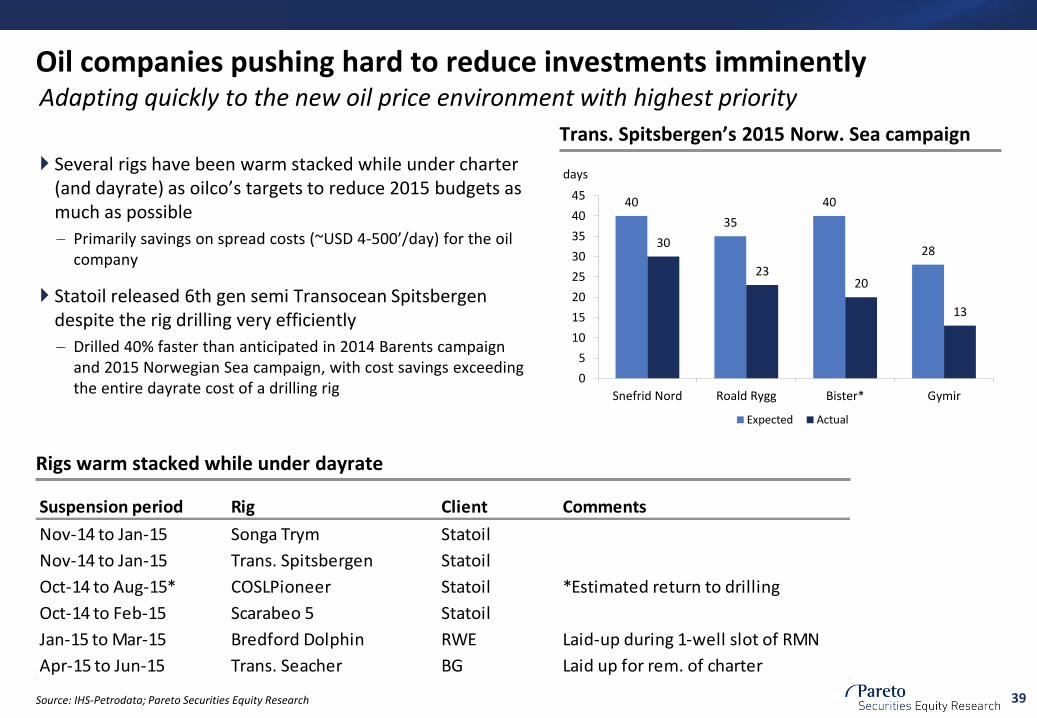

Adapting quickly to the new oil price environment with highest priority

Source: IHS-Petrodata; Pareto Securities Equity Research

Rigs warm stacked while under dayrate

Oil companies pushing hard to reduce investments imminently

Several rigs have been warm stacked while under charter (and dayrate) as oilco’s targets to reduce 2015 budgets as much as possible

Primarily savings on spread costs (~USD 4-500’/day) for the oil company

Statoil released 6th gen semi Transocean Spitsbergen despite the rig drilling very efficiently

Drilled 40% faster than anticipated in 2014 Barents campaign and 2015 Norwegian Sea campaign, with cost savings exceeding the entire dayrate cost of a drilling rig

Suspension period Rig Client Comments

Nov-14 to Jan-15 Songa Trym Statoil

Nov-14 to Jan-15 Trans. Spitsbergen Statoil

Oct-14 to Aug-15* COSLPioneer Statoil *Estimated return to drilling

Oct-14 to Feb-15 Scarabeo 5 Statoil

Jan-15 to Mar-15 Bredford Dolphin RWE Laid-up during 1-well slot of RMN

Apr-15 to Jun-15 Trans. Seacher BG Laid up for rem. of charter

40

35

40

2830

2320

13

0

5

10

15

20

25

30

35

40

45

Snefrid Nord Roald Rygg Bister* Gymir

Expected Actual

days

Trans. Spitsbergen’s 2015 Norw. Sea campaign

40

Decline in demand since 2013 primarily in the more mature basins

Source: IHS-Petrodata; Pareto Securities Equity Research

Floater market by basin NCS floater market by well type

23 floaters contracted following release of Spitbergen, down from 28 in 1H’2014

~6-7 rigs drilling E&A wells down from ~8-10 units

14 rigs drilling development wells down from 16 units

Operations suspended on 2 rigs (May)

North Sea accounting for ~60-70% of demand, Norwegian Sea ~20-30% and Barents Sea 5-15%

Activity has reduced significantly in the Norwegian Sea in 2014-15 vs. 2010-2013

The recent decline in demand has mainly been in the North Sea and Norwegian Sea while Barents have been steady at 1-3 rigs since 2013

0

5

10

15

20

25

30

jan

.09

mai

.09

sep

.09

jan

.10

mai

.10

sep

.10

jan

.11

mai

.11

sep

.11

jan

.12

mai

.12

sep

.12

jan

.13

mai

.13

sep

.13

jan

.14

mai

.14

sep

.14

jan

.15

mai

.15

Development Exploration & Appraisal Suspended* Yard/WoW/Mob etc.

# of contractedrigs

0

5

10

15

20

25

30

jan

.09

mai

.09

sep

.09

jan

.10

mai

.10

sep

.10

jan

.11

mai

.11

sep

.11

jan

.12

mai

.12

sep

.12

jan

.13

mai

.13

sep

.13

jan

.14

mai

.14

sep

.14

jan

.15

mai

.15

North Sea Norwegian Sea Barents Sea Suspended* Yard/WoW/Mob etc.

# of contracted rigs

41

Statoil mainly drilling development wells while other oilco’s are largely exploring

Source: IHS-Petrodata; Pareto Securities Equity Research

Other Oilco’s – Contracted floaters by well type Statoil – Contracted floaters by well type

Marority of Statoil’s demand is development drilling in mature Troll, Tampen and Oseberg areas

Other oilco’s have been steadily exploring

0

2

4

6

8

10

12

14

16

18

20

jan

.09

mai

.09

sep

.09

jan

.10

mai

.10

sep

.10

jan

.11

mai

.11

sep

.11

jan

.12

mai

.12

sep

.12

jan

.13

mai

.13

sep

.13

jan

.14

mai

.14

sep

.14

jan

.15

mai

.15

Development Exploration & Appraisal Suspended* Yard/WoW/Mob etc.

# of contracted rigs

0

2

4

6

8

10

12

14

jan

.09

mai

.09

sep

.09

jan

.10

mai

.10

sep

.10

jan

.11

mai

.11

sep

.11

jan

.12

mai

.12

sep

.12

jan

.13

mai

.13

sep

.13

jan

.14

mai

.14

sep

.14

jan

.15

mai

.15

Development Exploration & Appraisal Suspended* Yard/WoW/Mob etc.

# of contracted rigs

42 Source: Statoil; Pareto Securities Equity Research

Several tie-back prospects in the Norwegian Sea, however for now most have been delayed

Only Wintershall’s Maria project sanctioned from a healthy project list

Shell’s Linnorm & Hasselmus projects on hold

DEA/L1 Group’s Zidane project pushed further out

Statoil’s Trestakk, Mikkel Sør delayed. Limited updates on Asterix

Limited updates on Centrica’s Fogelberg

The Aasta Hansteen development and associated Polarled pipeline, where construction is currently underway, remains an important play opener for gas projects in the Norwegian Sea

Recent discoveries areas surrounding should also lead to additional work in Aasta Hansteen area and increase project robustness

Delayed tie-ins in the area the biggest «disappointment» the recent year

Polarled and certain potential tie-in projects

Norwegian Sea: Multiple modest-size development projects delayed

43 Source: Pareto Securities Equity Research

Pil & Bue discoveries the only “positive” news, with majority of other potential projects on hold

Several with relatively modest economics, however that will likely benefit significantly from reduced drilling cost with tie-in projects more rig intensive than new developments

Norwegian Sea: Current development project (requiring floating rig) pipeline

Project economics often challenging, but will benefit materially from lower drilling cost

Norwegian Sea: Multiple modest-size development projects delayed

Status Operator Area Field Exp. Duration Exp. start-up Exp. award Comments

Prospective

developmentVNG

Norwegian

SeaPil & Bue N/A N/A N/A

Among largest discoveries in Norway in 2014. Two new

exploration/appraisal wells drilled in 2015. Could be tied

back to Draugen or new Njord platform. Likely good

economics.

Development

on hold

RWE Dea /

L1 Group

Norwegian

SeaZidane ~400 days N/A N/A

Originally planned PUD in October 2014. Struggled with

tariff negotiations for tie-in, and need to make the

investment more robust. Also transition of ownership

Prospective

tie-inStatoil

Norwegian

SeaTrestakk N/A N/A N/A

Subsea tie-back to Åsgård A. Statoil originally planned

DG2 in March 2015 on the back of the oil price decline and

need to delay investments. NPD disputing the delay

Prospective

tie-inStatoil

Norwegian

SeaMikkel Sør N/A N/A N/A

Subsea templates tied back to Mikkel. Originally planned

PDO in 2013. PDO now expected in 2016

Prospective

tie-inCentrica

Norwegian

SeaFogelberg N/A N/A N/A Subsea tie-back to Heidrun or Asgard platform. HPHT field

Prospective

tie-inStatoil

Norwegian

SeaAsterix N/A N/A N/A Subsea tie-back

Potential

tie-inStatoil

Norwegian

SeaSnillehorn N/A N/A N/A

Could be developed as a fast-track subsea tieback to the

Hyme facilities.

Development

cancelledShell

Norwegian

SeaLinnorm ~300-500 days N/A N/A

Prev. plan was 4-5 HP/HT subsea wells tied back to

Draugen. Very challenging economics and unlikely to be

developed

Unkown status ShellNorwegian

SeaHasselmus N/A N/A N/A Tie in to Draugen

44 Source: Pareto Securities Equity Research

North Sea: Current development project (requiring floating rig) pipeline

Generally very robust economics due to good infrastructure

North Sea: A handful of fast-track projects will probably mature

Most potential future tie-in projects in the North Sea with very robust economics

Like in the Norwegian Sea, tie-in projects are more rig intensive than greenfield projects and benefit more from reduced drilling cost

Status Operator Area Field Exp. Duration Exp. start-up Exp. award Comments

Prospective

developmentWintershall North Sea Skarfjell N/A N/A N/A

Development options currently being evaluated. Could

be subsea tie-bck to Gjøa or independent

Prospective

tie-inStatoil North Sea Krafla N/A N/A N/A

Likely fast track candidate, with tie-back to Oseberg Sør.

Good economics and recent finds. Could use jackup

(~350ft. W.d)

Prospective

tie-inStatoil North Sea Grane D N/A N/A N/A Fast track cancidate. Tie-in to Grane. Good economics

Prospective

tie-inCentrica North Sea Frigg Gamma/Delta N/A N/A N/A Potential tie-back

Prospective

tie-inCentrica North Sea Fulla N/A N/A N/A ~350ft. W.d. Potentially jackup

Prospective

tie-in?Total North Sea Garantiana N/A N/A N/A

45

North Sea: Mature fields remain key for rig demand

Source: Statoil; Pareto Securities Equity Research

While J. Sverdrup takes the headlines, the mature fields in the Tampen and Oseberg area and the Troll field is the most important source of demand for floating rigs on the NCS

Statoil plans to continue drilling with four (DP) rigs at the Troll field alone to 2020

Equal to ~1/3 of its rigs under charter

Full exploitation of these areas is also one of the main objectives of the government being time-critical

Recent delay of a new Snorre C platform (Tampen)

Tampen-area, Troll and Oseberg area the biggest source of rig demand on NCS

# of rigs working at the Troll field

0

1

2

3

4

5

6

7

jan

.09

mai

.09

sep

.09

jan

.10

mai

.10

sep

.10

jan

.11

mai

.11

sep

.11

jan

.12

mai

.12

sep

.12

jan

.13

mai

.13

sep

.13

jan

.14

mai

.14

sep

.14

jan

.15

mai

.15

# of rigs

46 Source: Pareto Securities Equity Research

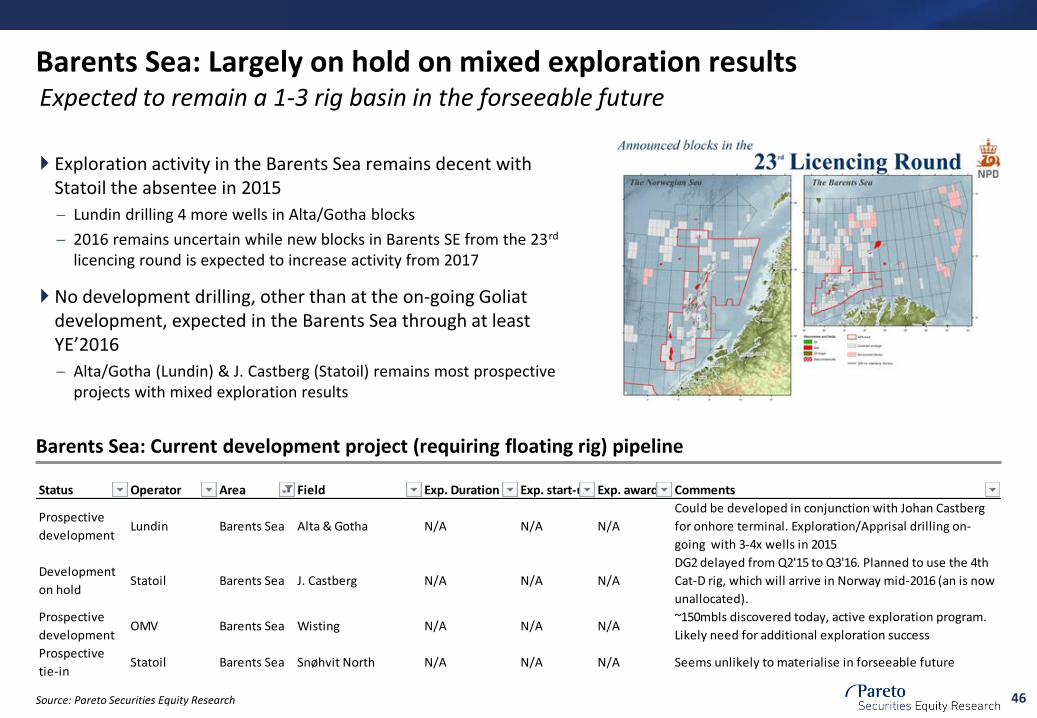

Barents Sea: Current development project (requiring floating rig) pipeline

Expected to remain a 1-3 rig basin in the forseeable future

Barents Sea: Largely on hold on mixed exploration results

Exploration activity in the Barents Sea remains decent with Statoil the absentee in 2015

Lundin drilling 4 more wells in Alta/Gotha blocks

2016 remains uncertain while new blocks in Barents SE from the 23rd licencing round is expected to increase activity from 2017

No development drilling, other than at the on-going Goliat development, expected in the Barents Sea through at least YE’2016

Alta/Gotha (Lundin) & J. Castberg (Statoil) remains most prospective projects with mixed exploration results

Status Operator Area Field Exp. Duration Exp. start-up Exp. award Comments

Prospective

developmentLundin Barents Sea Alta & Gotha N/A N/A N/A

Could be developed in conjunction with Johan Castberg

for onhore terminal. Exploration/Apprisal drilling on-

going with 3-4x wells in 2015

Development

on holdStatoil Barents Sea J. Castberg N/A N/A N/A

DG2 delayed from Q2'15 to Q3'16. Planned to use the 4th

Cat-D rig, which will arrive in Norway mid-2016 (an is now

unallocated).

Prospective

developmentOMV Barents Sea Wisting N/A N/A N/A

~150mbls discovered today, active exploration program.

Likely need for additional exploration success

Prospective

tie-inStatoil Barents Sea Snøhvit North N/A N/A N/A Seems unlikely to materialise in forseeable future

47

Government pressure mounting for continued investments

Source: Pareto Securities Equity Research

Norwegian authorities (Statoil’s main shareholder) pushing for continued exploitation

Last three Statoil «delays» in 2015 have all been disputed by Norwegian authorities

Veslefrikk

Trastakk

Snorre 2040

48

2825

21

26

21

11

2 1

4

0

5

10

15

20

25

30

YE'2013 Leaving C. stacked YE'2014 Leaving C. stacked Likely C.stacked

YE'2015 Likelyreturning

Newbuilds YE'2016

# of floaters

Cat-D deliveries offset by rigs leaving the shelf

Source: Pareto Securities Equity Research

Oversupply on the NCS is not driven by significant supply increase

W. Hercules to Faroe/Canada

Polar Pioneer to Shell Alaska/Singa

Ocean Vanguard (UK)

Trans. Leader to Premier UK

W. Navigator (NOR)

Bredford Dolphin Songa Cat-D’s

Trans. Searcher

W. Hercules from Canada

14x available incl. 8x 30-40 year old rigs

49

However, it will likely be painful to own legacy rigs

NCS fleet overview – by age

Supply side flexibility remains significant

Average age of ~20 years excl. Cat-D

Supply could decrease to 20 rigs by YE’2016 if all legacy rigs available by then is released

Source: IHS-Petrodats; Pareto Securities Equity Research

4039

38

35 35

32 32 3231

29 29

25

1514 14

76 6

5 54

3 3 3

0 0 0 00

5

10

15

20

25

30

35

40

45

Age (years)

12 legacy rigs8 off contract by YE'2016

50

Offshore project costs down ~30-40% on lower oil service costs ..but in the medium to long term costs will normalize

Source: Pareto Securities Equity Research

Cost deflation by project type Split of generic offshore development capex

Biggest savings for tie-ins and brownfield projects which are more drilling and subsea intensive

0 %

20 %

40 %

60 %

80 %

100 %

Greenfield deepwaterdevelopment

Greenfield shallowwater development

"Full scale" subseatie-back

Pipelines & misc. other Drilling - Other

Drilling - Rig lease Subsea - SURF

Subsea - Equipment Prod. facilities & processing equ.

-30-35 % -30-35 %

-35-40 %

-20-45 %

-20-25 %

-15-20 %

-20-25 %

-15-35 %

-50 %

-45 %

-40 %

-35 %

-30 %

-25 %

-20 %

-15 %

-10 %

-5 %

0 %

Greenfielddeepwater

development

Greenfieldshallow waterdevelopment

"Full scale"subsea tie-back

Brownfieldprojects

Current prices Sustainable price reduction

51

Significantly increased projects efficiency E.g. drilling efficiency improved ~20-40% from 2014

Source: Pareto Securities Equity Research

NCS drilling time/well Pre.salt Brazil well construction time

Total Dalia, Block 17, Angola Chevron USGoM deepwater drilling

0

100

200

300

400

Until 2010 2011 2012 2013 2014 2015eDrilling Completion (incl. WCT)

Days per well

0 %

20 %

40 %

60 %

80 %

100 %

2013 2014e 2015eDrilling time per well

Time per well

0

20

40

60

80

100

2012 2013 2014 2015Drilling time per well

Average days per 10'ft. drilled

-35 %

0 %

20 %

40 %

60 %

80 %

100 %

2014 average Improvedefficiencies

2015

Drilling time per well

Time per well

Significant built-in in-efficiencies after a decade long bull cycle

Improved drilling efficiency all else equal negative for demand, but also

Increases spending capacity of offshore focused E&P’s such as Petrobras

Increases offshore competitiveness

Promotes more subsea intensive developments

52

Onshore costs also continuing to come significantly down 30-40% cost deflation both onshore and offshore

Source: Company reports and data, Pareto Securities Equity Research

-15-30 %

-10-20 %

-5-10 %

-20-40 %

-20-30 %-15-25%

-35 %

-30 %

-25 %

-20 %

-15 %

-10 %

-5 %

0 %

Drilling time per well Drilling & completioncost per lateral ft.

Well cost

2014 2015

U.S. cost efficiencies

53 Source: Pareto Securities Equity Research

Average hurdle rate above current oil prices

Cost deflation accounting for majority of cost savings

65

38

11

16

18%

24%

42%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

0

10

20

30

40

50

60

70

Aggregateddevelopment

costs

Scope Cost deflation Aggregated MtMdevelopment

costs

Cost savings (%)Aggregated development costs (USDbn)

54

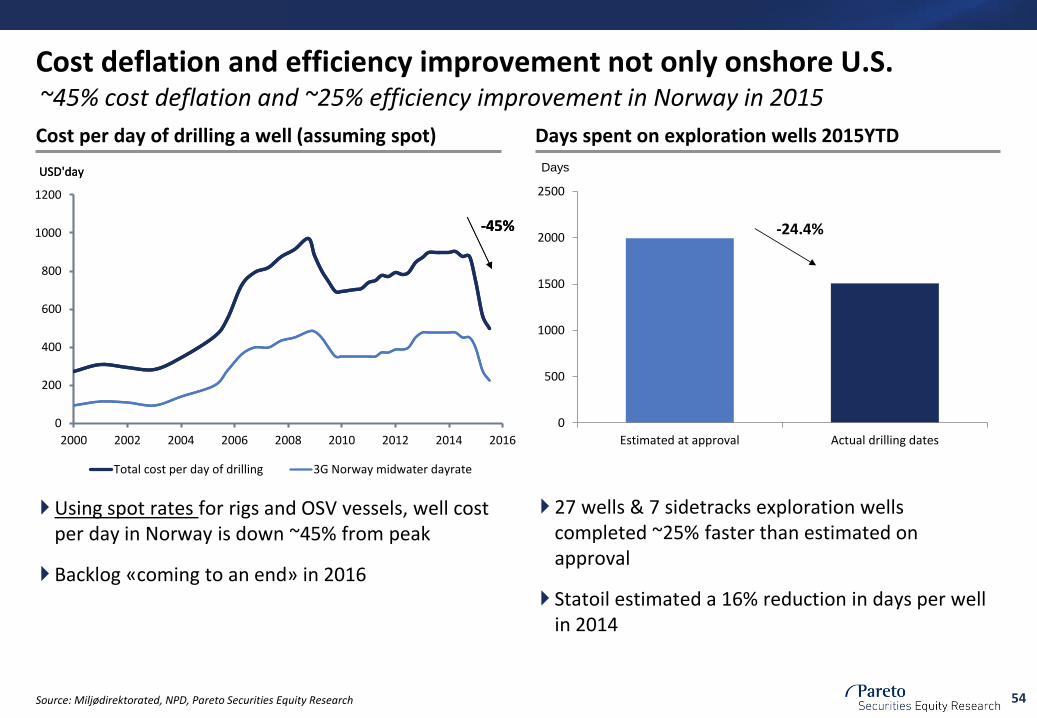

~45% cost deflation and ~25% efficiency improvement in Norway in 2015

Cost deflation and efficiency improvement not only onshore U.S.

Source: Miljødirektorated, NPD, Pareto Securities Equity Research

Days spent on exploration wells 2015YTD Cost per day of drilling a well (assuming spot)

Using spot rates for rigs and OSV vessels, well cost per day in Norway is down ~45% from peak

Backlog «coming to an end» in 2016

27 wells & 7 sidetracks exploration wells completed ~25% faster than estimated on approval

Statoil estimated a 16% reduction in days per well in 2014

0

500

1000

1500

2000

2500

Estimated at approval Actual drilling dates

Days

-24.4%

0

200

400

600

800

1000

1200

2000 2002 2004 2006 2008 2010 2012 2014 2016

Total cost per day of drilling 3G Norway midwater dayrate

USD'day

-45%

USD'day

-45%

55 Source: Pareto Securities Equity Research

Innovation

56

Wolfcamp (Permian) and Eagle Ford the lowest break-evens

Wolfcamp (Permian) and Eagle Ford the lowest average break-evens

Despite a wide variation within plays, production-weighted breakevens for key liquids plays span <USD15/bbl

Companies with concentrated positions in the Permian basin have the lowest break-evens

48 52

55 58 58 60

62 64

0

10

20

30

40

50

60

70

38 39

45 47 47 51

54 57 58

61

70 71

83 87

0

20

40

60

80

100

Liquids break-evens by key play – USD/bbl Liquids break-evens by company*– USD/bbl

Source: Woodmackenzie, Pareto Securities Equity Research, NPV discounted at 10% nominal, *weighted by 2016 production

57

Total OPEC capacity growth 2015-21e 0.8 mill bbl/day

Iran 2015-21e total capacity growth 340,000 bbl/day to 3.9 mill bbl/day

Iraq 2015-21e total capacity growth 270,000 bbl/day to 4.6 mill bbl/day

Saudi 2015-21e total capacity growth 70,000 bbl/day to 12.3 mill bbl/day

(Libya 2015-21e total capacity growth 190,000 bbl/day to 590,000 bbl/day)

Iran the largest addition increasing capacity 0.3 mill bbl/day to 3.9 mill bbl/day

Source: Pareto Securities Equity Research, IEA

35.64 35.72 35.89 36.02 36.17 36.34 36.44

27

28

29

30

31

32

33

34

35

36

37

2015 2017e 2019e 2021e

OPEC Crude Capacity 2015-21e; mill bbl/day

2015 2016e 2017e 2018e 2019e 2020e 2021e 2015-21e

Algeria 1,15 1,12 1,09 1,06 1,04 1,01 0,99 -0,16

Angola 1,81 1,81 1,77 1,81 1,78 1,76 1,8 -0,01

Ecuador 0,56 0,55 0,55 0,55 0,55 0,54 0,53 -0,03

Indonesia 0,69 0,71 0,71 0,69 0,67 0,65 0,63 -0,06

Iran 3,6 3,6 3,7 3,75 3,8 3,9 3,94 0,34

Iraq 4,35 4,35 4,36 4,4 4,45 4,53 4,62 0,27

Kuwait 2,83 2,87 2,91 2,93 2,94 2,9 2,88 0,05

Libya 0,4 0,4 0,43 0,46 0,49 0,53 0,59 0,19

Nigeria 1,91 1,9 1,84 1,75 1,78 1,85 1,85 -0,06

Qatar 0,68 0,67 0,66 0,66 0,66 0,66 0,66 -0,02

Saudi Arabia 12,26 12,31 12,43 12,45 12,44 12,39 12,33 0,07

UAE 2,93 2,97 3,02 3,07 3,12 3,17 3,2 0,27

Venezuela 2,48 2,46 2,44 2,43 2,45 2,44 2,42 -0,06

Total OPEC 35,65 35,72 35,91 36,01 36,17 36,33 36,44 0,79

OPEC Crude Capacity per Country 2015-21e; mill bbl/day

58

Pareto Oil Market Outlook - Summary

Strong oil demand growth 2015, slowing in 2016

Non-OPEC production from 2014 record growth to 2016 largest decline in 25 years

Strong OPEC growth delays balancing: Iraq , Saudi record production - Iran nuclear sanctions lifted

Market remains oversupplied > 1mill bbl/day - OPEC production freeze could balance market H2/16

11th Pareto E&P Independents Conference London March 31st 2016

Source: IEA, Pareto Securities Equity Research

Oil demand vs supply 2001-21e; mill bbl/day

28.5

29.5

30.5

31.5

32.5

33.5

34.5

Q1'10 Q1'11 Q1'12 Q1'13 Q1'14 Q1'15 Q1'16e Q1'17e

mbd

Call-on-OPEC OPEC production

OPEC production vs call-on-OPEC

75

80

85

90

95

100

105

2001 2003 2005 2007 2009 2011 2013 2015 2017e2019e2021e

Demand Supply

59

US oil rig count and oil production

Source: Baker Hughes, *EIA (Assumes 2016 Brent USD 34/bbl and 2017 USD 40/bbl,), Pareto Securities Equity Research

US Oil Rig Count 1987-2016 EIA: US Crude Production 2012-17e; mill bbl/day*

4.00

5.00

6.00

7.00

8.00

9.00

10.00

2012 2013 2014 2015 2016 2017

US Crude Production US Lower 48 Production (excl. GoM)0

200

400

600

800

1 000

1 200

1 400

1 600

1 800

7.17.1987 7.17.1992 7.17.1997 7.17.2002 7.17.2007 7.17.2012

60

2015 demand growth 5-year high, slowing in 2016

Demand growth 2015 1.8 mboepd highest in 5 years

Demand growth slowing to 1.2 mboepd yoy in 2016

Weaker economic growth in China and major oil producers (Brazil, Russia, Middle East, US)

Demand growth peaked in Q3/15 at 2.3 mill bbl/day

Demand slowed significantly in Q4/15 with warm start of winter removing 0.5 mill bbl/day demand

US demand has rebounded after declining Sep-Nov

Source: IEA; Pareto Securities Equity Research

0.8 0.6

1.6

3.1

1.4 1

1.5

-0.6 -1

3.1

0.9 1.1 1.2

0.9

1.8

1.2

-1.5

-1

-0.5

0

0.5

1

1.5

2

2.5

3

3.5

2001 2003 2005 2007 2009 2011 2013 2015

1.2

0.6 0.7

1.1

1.6

2.0

2.3

1.2 1.2 1.0 1.0

1.5

0

0.5

1

1.5

2

2.5

Q1/14 Q3/14 Q1/15 Q3/15 Q1/16e Q3/16e

Global oil demand growth 2001-2016e; mbd Oil demand growth Q1/14-Q4/16e; mill bbl/day

61

Less than 15% of US tight oil resources commercial at USD 40/bbl

50% is commercial at WTI USD 55/bbl – 95% of modelled resources commercial at WTI USD 80/bbl

New cumulative US tight oil liquids by break-even

Source: Woodmackenzie, Pareto Securities Equity Research,

62

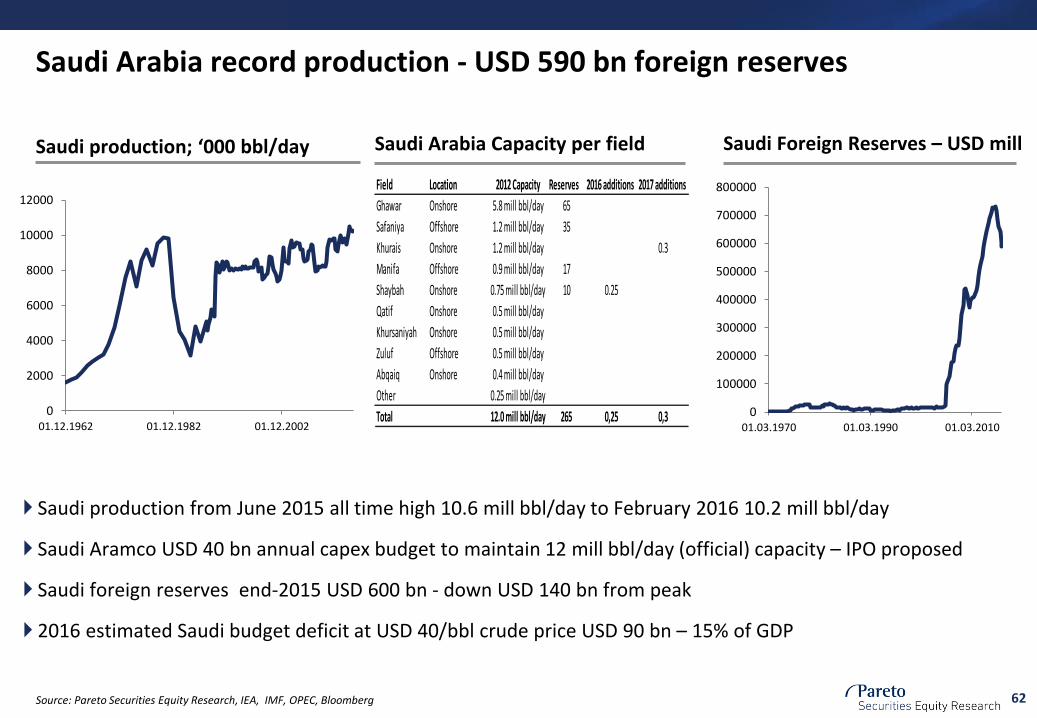

Saudi Arabia record production - USD 590 bn foreign reserves

Source: Pareto Securities Equity Research, IEA, IMF, OPEC, Bloomberg

Saudi Foreign Reserves – USD mill Saudi production; ‘000 bbl/day

Saudi production from June 2015 all time high 10.6 mill bbl/day to February 2016 10.2 mill bbl/day

Saudi Aramco USD 40 bn annual capex budget to maintain 12 mill bbl/day (official) capacity – IPO proposed

Saudi foreign reserves end-2015 USD 600 bn - down USD 140 bn from peak

2016 estimated Saudi budget deficit at USD 40/bbl crude price USD 90 bn – 15% of GDP

Field Location 2012 Capacity Reserves 2016 additions 2017 additions

Ghawar Onshore 5.8 mill bbl/day 65

Safaniya Offshore 1.2 mill bbl/day 35

Khurais Onshore 1.2 mill bbl/day 0.3

Manifa Offshore 0.9 mill bbl/day 17

Shaybah Onshore 0.75 mill bbl/day 10 0.25

Qatif Onshore 0.5 mill bbl/day

Khursaniyah Onshore 0.5 mill bbl/day

Zuluf Offshore 0.5 mill bbl/day

Abqaiq Onshore 0.4 mill bbl/day

Other 0.25 mill bbl/day

Total 12.0 mill bbl/day 265 0,25 0,3

Saudi Arabia Capacity per field

0

100000

200000

300000

400000

500000

600000

700000

800000

01.03.1970 01.03.1990 01.03.2010

0

2000

4000

6000

8000

10000

12000

01.12.1962 01.12.1982 01.12.2002

63

Iran – lifting of nuclear sanctions

Source: Pareto Securities Equity Research, Bloomberg, OPEC, IEA, Woodmackenzie

Iran crude production 1965-2016

Iran current production 3.0 mill bbl/day (IEA/Bloomberg) – 3.4 mill bbl/day (Iran own data OPEC report)

Lifting of nuclear sanctions – offering 70 upstream projects for foreign investments

Iran pre-sanction levels: 3.6 mill bbl/day in H2/2016 (IEA) – Woodmackenzie 3.7 mill bbl/day H2/2017

Iran 2020: IEA 3.9 mill bbl/day– Woodmackenzie: 4.0 mill bbl/day assuming USD 50 bn foreign investmenst

Projects for foreign investments

0

1000

2000

3000

4000

5000

6000

7000

01.12.1962 01.12.1977 01.12.1992 01.12.2007

Iran scenarios – 2010-2025e

64

Iraq record production, growth stalling from lack of investments

Source: IEA, Bloomberg, KRG MNR, Pareto Securities Equity Research

Iraq infrastructure and IS control Iraq crude production 1965-2016

Iraq record production in January 4.4 mill bbl/day (IEA) – 600,000 bbl/day KRG independent exports

Growth stalling both in Kurdistan and Basra region due to lack of new field and infrastructure investments

IS continues to control large, sunni-dominated areas and to threaten KRG and Iraq Federal Government

Iraq higher long term supply potential than Saudi Arabia > 15 mill bbl/day

0.0

1.0

2.0

3.0

4.0

5.0

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015

Iraq crude production

mbd

Iraq Scenarios & Targets

4.5

9.0

12.0

14.7

0

2

4

6

8

10

12

14

16

IEA 2020 Iraq 2020Target

Iraq 2020Old Target

Contractssignedw/IOCs

Basra region

65

Libya – IS Attacking Key Oil Infrastructure

Libya current oil production 370,000 bbl/day- IS controlling territory and attacking oil infrastructure

Libya oil production 1.6 mill bbl/day before the fall of Gaddafi in 2011

ISIS is conducting a sophisticated, multi-front campaign against Libya oil facilities

Source: The Maghreb and Orient Courier, Bloomberg, Pareto Securities Equity Research

0

500

1000

1500

2000

2500

3000

3500

01.12.1962 01.12.1977 01.12.1992 01.12.2007

ISIS Libya Campaign January – February 2016 Libya Crude Oil Production

66

Contact details

www.paretosec.com | Bloomberg: PASE (go) | Reuters: PARETO

Oslo (Norway) Pareto Securities AS Dronning Mauds gate 3 PO Box 1411 Vika N-0115 Oslo NORWAY Tel: +47 22 87 87 00

Stavanger (Norway) Pareto Securities AS Haakon VIIs gate 8 PO Box 163 N-4001 Stavanger NORWAY Tel: +47 51 83 63 00

Trondheim (Norway) Pareto Securities AS Nordre gate 11 PO Box 971 Sentrum N-7410 Trondheim NORWAY Tel: +47 21 50 74 60

Malmö (Sweden) Pareto Securities AB Stortorget 13 S-211 22 Malmö SWEDEN Tel: +46 40 750 20

Stockholm (Sweden) Pareto Securities AB Berzelii Park 9 PO Box 7415 S-103 91 Stockholm SWEDEN Tel: +46 8 402 50 00

Helsinki (Finland) Pareto Securities Oy Aleksanterinkatu 44, 6th floor FI-00100 Helsinki FINLAND Tel: +358 9 8866 6000

Copenhagen (Denmark) Pareto Securities AS Copenhagen Branch Bredgade 30 DK-1260 Copenhagen DENMARK Tel: +45 78 73 48 00

Perth (Australia) Pareto Securities Pty Ltd Level 24 77 St Georges Tce Perth, Western Australia AUSTRALIA, 6000 Tel: +61 8 6141 3366

Singapore Pareto Securities Pte Ltd 16 Collyer Quay #27-02 Income at Raffles Singapore 049318 SINGAPORE Tel: +65 6408 9800

London (UK) Pareto Securities Ltd 8 Angel Court London EC2R 7HJ UNITED KINGDOM Tel: +44 20 7786 4370

New York (US) Pareto Securities Inc 150 East 52nd Street, 29th floor New York NY 10022 USA Tel: +1 212 829-4200

Houston (US) Pareto Securities Inc 8 Greenway Plaza, Suite 818 Houston, TX 77046 USA Tel: +1 832 831-1895

Aberdeen (UK) Pareto Securities Ltd 46 Carden Place Aberdeen, AB10 1UP UNITED KINGDOM Tel: +44 1224 433466

Paris (France) Pareto Securities AS, Paris Branch 11 BD Jean Mermoz 92200 Neuilly Sur Seine FRANCE Tel: +33 141921234

67

Disclaimers and disclosures

Origin of the publication or report This publication or report originates from Pareto Securities AS (“Pareto Securities”), reg. no. 956 632 374 (Norway), Pareto Securities AB, reg. no. 556206-8956 (Sweden) or Pareto Securities Limited, reg. no. 3994976, (United Kingdom) (together the Group Companies or the “Pareto Securities Group”) acting through their common unit Pareto Securities Research. The Group Companies are supervised by the Financial Supervisory Authority of their respective home countries. Content of the publication or report This publication or report has been prepared solely by Pareto Securities Research. Opinions or suggestions from Pareto Securities Research may deviate from recommendations or opinions presented by other departments or companies in the Pareto Securities Group. The reason may typically be the result of differing time horizons, methodologies, contexts or other factors. Basis and methods for assessment Opinions and price targets are based on one or more methods of valuation, for instance cash flow analysis, use of multiples, behavioral technical analyses of underlying market movements in combination with considerations of the market situation and the time horizon. Key assumptions of forecasts, price targets and projections in research cited or reproduced appear in the research material from the named sources. The date of publication appears from the research material cited or reproduced. Opinions and estimates may be updated in subsequent versions of the publication or report, provided that the relevant company/issuer is treated anew in such later versions of the publication or report. Credit ratings are based on the same rating scale as international rating agencies and represent the opinion of Pareto Securities Research as to the relative creditworthiness of securities. A credit rating on a standalone basis should not be used as a basis for investment operations. Pareto Securities Research may also provide credit research with more specific price targets based on different valuation methods, including the analysis of key credit ratios and other factors describing the securities creditworthiness, peer group analysis of securities with similar creditworthiness and different DCF-valuations. All credit ratings mentioned in this publication or report are Pareto Securities Research’s own credit rating estimates unless otherwise mentioned. All descriptions of loan agreement structures and loan agreement features are obtained from sources which Pareto Securities Research believes to be reliable, but Pareto Securities Research does not represent or warrant their accuracy. Be aware that investors should go through the specific complete loan agreement before investing in any bonds and not base an investment decision based solely on information contained in this publication or report. Pareto Securities Research has no fixed schedule for updating publications or reports. Unless otherwise stated on the first page, the publication or report has not been reviewed by the issuer before dissemination. In instances where all or part of a report is presented to the issuer prior to publication, the purpose is to ensure that facts are correct. Validity of the publication or report All opinions and estimates in this publication or report are, regardless of source, given in good faith and may only be valid as of the stated date of this publication or report and are subject to change without notice. No individual investment or tax advice The publication or report is intended only to provide general and preliminary information to investors and shall not be construed as the basis for any investment decision. This publication or report has been prepared by Pareto Securities Research as general information for private use of investors to whom the publication or report has been distributed, but it is not intended as a personal recommendation of particular financial instruments or strategies and thus it does not provide individually tailored investment advice, and does not take into account the individual investor’s particular financial situation, existing holdings or liabilities, investment knowledge and experience, investment objective and horizon or risk profile and preferences. The investor must particularly ensure the suitability of an investment as regards his/her financial and fiscal situation and investment objectives. The investor bears the risk of losses in connection with an investment. Before acting on any information in this publication or report, we recommend consulting your financial advisor. The information contained in this publication or report does not constitute advice on the tax consequences of making any particular investment decision. Each investor shall make his/her own appraisal of the tax and other financial merits of his/her investment.

V. 04.2016

68

Disclaimers and disclosures

Sources This publication or report may be based on or contain information, such as opinions, recommendations, estimates, price targets and valuations which emanate from Pareto Securities Research’ analysts or representatives, publicly available information, information from other units or companies in the Group Companies, or other named sources. To the extent this publication or report is based on or contains information emanating from other sources (“Other Sources”) than Pareto Securities Research (“External Information”), Pareto Securities Research has deemed the Other Sources to be reliable but neither the companies in the Pareto Securities Group, others associated or affiliated with said companies nor any other person, guarantee the accuracy, adequacy or completeness of the External Information. Ratings Equity ratings: “Buy” Pareto Securities Research expects this financial instrument’s total return to exceed 10% over the next six months “Hold” Pareto Securities Research expects this financial instrument’s total return to be 0-10% over the next six months “Sell” Pareto Securities Research expects this financial instrument’s total return to be negative over the next six months Credit ratings: AAA Best Quality AA+ / AA / AA- Strong ability for timely payments A+ / A / A- Somewhat more exposed for negative changes BBB+ / BBB / BBB- Adequate ability to meet payments. Some elements of protection. BB+ / BB / BB- Speculative risk. Future not well secured B+ / B / B- Timely payments at the moment, but very exposed to any negative changes CCC+ /CCC/ CCC- Default a likely option Analysts Certification The research analyst(s) whose name(s) appear on research reports prepared by Pareto Securities Research certify that: (i) all of the views expressed in the research report accurately reflect their personal views about the subject security or issuer, and (ii) no part of the research analysts’ compensation was, is, or will be directly or indirectly related to the specific recommendations or views expressed by the research analysts in research reports that are prepared by Pareto Securities Research. The research analysts whose names appears on research reports prepared by Pareto Securities Research received compensation that is based upon various factors including Pareto Securities’ total revenues, a portion of which are generated by Pareto Securities’ investment banking activities. Limitation of liability Pareto Securities Group or other associated and affiliated companies assume no liability as regards to any investment, divestment or retention decision taken by the investor on the basis of this publication or report. In no event will entities of the Pareto Securities Group or other associated and affiliated companies be liable for direct, indirect or incidental, special or consequential damages resulting from the information in this publication or report. Neither the information nor any opinion which may be expressed herein constitutes a solicitation by Pareto Securities Research of purchase or sale of any securities nor does it constitute a solicitation to any person in any jurisdiction where solicitation would be unlawful. All information contained in this research report has been compiled from sources believed to be reliable. However, no representation or warranty, express or implied, is made with respect to the completeness or accuracy of its contents, and it is not to be relied upon as authoritative. Risk information The risk of investing in certain financial instruments, including those mentioned in this document, is generally high, as their market value is exposed to a lot of different factors such as the operational and financial conditions of the relevant company, growth prospects, change in interest rates, the economic and political environment, foreign exchange rates, shifts in market sentiments etc. Where an investment or security is denominated in a different currency to the investor’s currency of reference, changes in rates of exchange may have an adverse effect on the value, price or income of or from that investment to the investor. Past performance is not a guide to future performance. Estimates of future performance are based on assumptions that may not be realized. When investing in individual shares, the investor may lose all or part of the investments.

69

Disclaimers and disclosures

Conflicts of interest Companies in the Pareto Securities Group, affiliates or staff of companies in the Pareto Securities Group, may perform services for, solicit business from, make a market in, hold long or short positions in, or otherwise be interested in the investments (including derivatives) of any company mentioned in the publication or report. In addition Pareto Securities Group, or affiliates, may from time to time have a broking, advisory or other relationship with a company which is the subject of or referred to in the relevant Research, including acting as that company’s official or sponsoring broker and providing corporate finance or other financial services. It is the policy of Pareto to seek to act as corporate adviser or broker to some of the companies which are covered by Pareto Securities Research. Accordingly companies covered in any Research may be the subject of marketing initiatives by the Corporate Finance Department. To limit possible conflicts of interest and counter the abuse of inside knowledge, the analysts of Pareto Securities Research are subject to internal rules on sound ethical conduct, the management of inside information, handling of unpublished research material, contact with other units of the Group Companies and personal account dealing. The internal rules have been prepared in accordance with applicable legislation and relevant industry standards. The object of the internal rules is for example to ensure that no analyst will abuse or cause others to abuse confidential information. It is the policy of Pareto Securities Research that no link exists between revenues from capital markets activities and individual analyst remuneration. The Group Companies are members of national stockbrokers’ associations in each of the countries in which the Group Companies have their head offices. Internal rules have been developed in accordance with recommendations issued by the stockbrokers associations. This material has been prepared following the Pareto Securities Conflict of Interest Policy. The guidelines in the policy include rules and measures aimed at achieving a sufficient degree of independence between various departments, business areas and sub-business areas within the Pareto Securities Group in order to, as far as possible, avoid conflicts of interest from arising between such departments, business areas and sub-business areas as well as their customers. One purpose of such measures is to restrict the flow of information between certain business areas and sub-business areas within the Pareto Securities Group, where conflicts of interest may arise and to safeguard the impartialness of the employees. For example, the Corporate Finance departments and certain other departments included in the Pareto Securities Group are surrounded by arrangements, so-called Chinese Walls, to restrict the flows of sensitive information from such departments. The internal guidelines also include, without limitation, rules aimed at securing the impartialness of, e.g., analysts working in the Pareto Securities Research departments, restrictions with regard to the remuneration paid to such analysts, requirements with respect to the independence of analysts from other departments within the Pareto Securities Group rules concerning contacts with covered companies and rules concerning personal account trading carried out by analysts. Distribution restriction The securities referred to in this publication or report may not be eligible for sale in some jurisdictions and persons into whose possession this document comes should inform themselves about and observe any such restrictions. This publication or report is not intended for and must not be distributed to private customers in the US, or retail clients in the United Kingdom, as defined by the Financial Conduct Authority (FCA). This research report is only intended for and may only be distributed to institutional investors in the United States and U.S. entities seeking more information about any of the issuers or securities discussed in this report should contact Auerbach Grayson & Company at 25 West 45th Street New York, NY 10036 Tel. 1 212-453-3549 or Pareto Securities Inc. at 150 East 52nd Street, New York, NY 10022, Tel. 212 829 4200. Auerbach Grayson & Company is a broker-dealer registered with the U.S. Securities and Exchange Commission and is a member of the FINRA & SIPC. Investment products provided by or through Auerbach Grayson & Company or Pareto Securities Research are not FDIC insured may lose value and are not guaranteed by Auerbach Grayson & Company or Pareto Securities Research. Investing in non-U.S. securities may entail certain risks. This document does not constitute or form part of any offer for sale or subscription, nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. The securities of non-U.S. issuers may not be registered with or subject to SEC reporting and other requirements. The information available about non-U.S. companies may be limited, and non-U.S. companies are generally not subject to the same uniform auditing and reporting standards as U.S. companies. Fluctuations in the values of national currencies, as well as the potential for governmental restrictions on currency movements, can significantly erode principal and investment returns. Market rules, conventions and practices may differ from U.S. markets, adding to transaction costs or causing delays in the purchase or sale of securities. Securities of some non-U.S. companies may not be as liquid as securities of comparable U.S. companies. Auerbach Grayson & Company and/or Pareto Securities Research may have material conflicts of interest related to the production or distribution of this research report which, with regard to Pareto Securities Research, are disclosed herein. Pareto Securities Inc. is a broker-dealer registered with the U.S. Securities and Exchange Commission and is a member of FINRA & SIPC. U.S. To the extent required by applicable U.S. laws and regulations, Pareto Securities Inc. accepts responsibility for the contents of this publication. Investment products provided by or through Pareto Securities Inc. or Pareto Securities Research are not FDIC insured, may lose value and are not guaranteed by Pareto Securities Inc. or Pareto Securities Research. Investing in non-U.S. securities may entail certain risks. This document does not constitute or form part of any offer for sale or subscription, nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. The securities of non-U.S. issuers may not be registered with or subject to SEC reporting and other requirements. The information available about non-U.S. companies may be limited, and non-U.S. companies are generally not subject to the same uniform auditing and reporting standards as U.S. companies. Market rules, conventions and practices may differ from U.S. markets, adding to transaction costs or causing delays in the purchase or sale of securities. Securities of some non-U.S. companies may not be as liquid as securities of comparable U.S. companies.

70

Disclaimers and disclosures

Distribution in Singapore Pareto Securities Pte Ltd holds a Capital Markets Services License is an exempt financial advisor under Financial Advisers Act, Chapter 110 (“FAA”) of Singapore and a subsidiary of Pareto Securities AS. This report is directed solely to persons who qualify as "accredited investors", "expert investors" and "institutional investors" as defined in section 4A(1) Securities and Futures Act, Chapter 289 (“SFA”) of Singapore. This report is intended for general circulation amongst such investors and does not take into account the specific investment objectives, financial situation or particular needs of any particular person. You should seek advice from a financial adviser regarding the suitability of any product referred to in this report, taking into account your specific financial objectives, financial situation or particular needs before making a commitment to purchase any such product. Please contact Pareto Securities Pte Ltd, 16 Collyer Quay, # 27-02 Income at Raffles, Singapore 049318, at +65 6408 9800 in matters arising from, or in connection with this report. Additional provisions on Recommendations distributed in the Canada Canadian recipients of this research report are advised that this research report is not, and under no circumstances is it to be construed as, an offer to sell or a solicitation of or an offer to buy any securities that may be described herein. This research report is not, and under no circumstances is it to be construed as, a prospectus, offering memorandum, advertisement or a public offering in Canada of such securities. No securities commission or similar regulatory authority in Canada has reviewed or in any way passed upon this research report or the merits of any securities described or discussed herein and any representation to the contrary is an offence. Any securities described or discussed within this research report may only be distributed in Canada in accordance with applicable provincial and territorial securities laws. Any offer or sale in Canada of the securities described or discussed herein will be made only under an exemption from the requirements to file a prospectus with the relevant Canadian securities regulators and only by a dealer properly registered under applicable securities laws or, alternatively, pursuant to an exemption from the dealer registration requirement in the relevant province or territory of Canada in which such offer or sale is made. Under no circumstances is the information contained herein to be construed as investment advice in any province or territory of Canada nor should it be construed as being tailored to the needs of the recipient. Canadian recipients are advised that Pareto Securities AS, its affiliates and its authorized agents are not responsible for, nor do they accept, any liability whatsoever for any direct or consequential loss arising from any use of this research report or the information contained herein. Distribution in United Kingdom This publication is produced in accordance with COBS 12.3 as Non-Independent Research and approved under part IV article 19 of The Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the “FPO”) by Pareto Securities Limited for communication in the United Kingdom only to investment professionals as that term is defined in article 19(5) of the FPO. This publication is issued for the benefit of persons who qualify as eligible counterparties or professional clients and should be made available only to such persons and is exempt from the restriction on financial promotion in s21 of the Financial Services and Markets Act 2000 in reliance on provision in the FPO. Copyright This publication or report may not be mechanically duplicated, photocopied or otherwise reproduced, in full or in part, under applicable copyright laws. Any infringement of Pareto Securities Research´s copyright can be pursued legally whereby the infringer will be held liable for any and all losses and expenses incurred by the infringement.

71

Disclaimers and disclosures