Revisiting the Drivers of US Consumer Price Inflation...Instead, core PCE has decelerated to 1.5%...

10

Investment Research Revisiting the Drivers of US Consumer Price Inflation Ronald Temple, CFA, Managing Director, Co-Head of Multi-Asset and Head of US Equity David Alcaly, Research Analyst In recent months, both headline and core measures of US consumer price inflation have decelerated. In part, this has reflected “transitory” effects unrepresentative of underlying pricing pressure—for example, waning positive contribu- tions from energy prices and new negative ones from competition in wireless services. However, the deceleration has been broader and inflation readings have continued to surprise to the downside, reinvigorating debate over their funda- mental drivers. We believe nascent “lowflation” fears are overdone, just as “reflation” enthusiasm was six months ago, and we anticipate that underlying pressure for higher prices will continue to build. Nonetheless, recent trends bear close watching, particularly since new transitory factors will continue to depress year-on-year measures into 2018. In this update to A Look under the Hood of US Consumer Price Inflation we briefly review recent trends in inflation, take a “bottom-up” look at sources of recent weakness, revisit the ambiguities surrounding inflation, and outline key sources of cyclical pressure. In the appendix, we update our dashboard of inflation measures.

Transcript of Revisiting the Drivers of US Consumer Price Inflation...Instead, core PCE has decelerated to 1.5%...

Investment Research

Revisiting the Drivers of US Consumer Price Inflation

Ronald Temple, CFA, Managing Director, Co-Head of Multi-Asset and Head of US Equity

David Alcaly, Research Analyst

In recent months, both headline and core measures of US consumer price inflation have decelerated. In part, this has reflected “transitory” effects unrepresentative of underlying pricing pressure—for example, waning positive contribu-tions from energy prices and new negative ones from competition in wireless services. However, the deceleration has been broader and inflation readings have continued to surprise to the downside, reinvigorating debate over their funda-mental drivers. We believe nascent “lowflation” fears are overdone, just as “reflation” enthusiasm was six months ago, and we anticipate that underlying pressure for higher prices will continue to build. Nonetheless, recent trends bear close watching, particularly since new transitory factors will continue to depress year-on-year measures into 2018.

In this update to A Look under the Hood of US Consumer Price Inflation we briefly review recent trends in inflation, take a “bottom-up” look at sources of recent weakness, revisit the ambiguities surrounding inflation, and outline key sources of cyclical pressure. In the appendix, we update our dashboard of inflation measures.

2

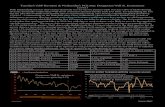

Recent Trends in InflationEntering 2017, the eighth year of the United States’ recovery from the financial crisis, inflation appeared to be on an upward trajectory. The year-on-year change in the Personal Consumption Expenditures Price Index excluding food and energy (core PCE) gradually rose from a low of 1.3% in July 2015 to 1.9% in January 2017. With the unemployment rate falling to levels last seen in 2001 and broader measures of labor market slack showing improvement, it was widely expected that core inflation would continue to rise gradually, even as headline inflation subsided due to stable energy prices.

Instead, core PCE has decelerated to 1.5% year-on-year as of June, with shorter-term trends slowing more dramatically (Exhibit 1). Furthermore, this recent deceleration has coincided with weaker measures of wage growth (Exhibit 2) and of market-implied future inflation, both of which had similarly shown gradual acceleration over the previous year.

Not Just “Transitory” FactorsThe recent slowing in inflation has once again raised questions about its medium-term trajectory, many of which have dogged the Federal Open Market Committee (FOMC) for much of the recovery. How can the FOMC continue to be so confident in its forecasts, given that the forecasts to date have proven to be overly optimistic (Exhibit 3), and given that the FOMC has undershot its 2% inflation target since April 2012?

By way of explanation, the FOMC has pointed to several “tran-sitory” factors—temporary effects outside of its control and unreflective of underlying inflationary pressure. Plunging energy prices and a rapidly appreciating US dollar were significant nega-tive drags on inflation from late 2014 through late 2015, and both have since contributed to improvements. While direct energy prices are excluded from core measures of inflation, they likely have an indirect impact, as they are an input for many of the other goods and services that are included. Perhaps this indirect effect has contributed to core inflation’s moderate acceleration and now its recent deceleration, both of which coincide with similar patterns in energy’s contribution to headline inflation (Exhibit 4). However, while the recent weakening of the US dollar (on a year-over-year basis) has fed through to now-rising import prices (Exhibit 5, top), other factors have clearly been more influential on core goods inflation, which has weakened since the beginning of 2017 (Exhibit 5, bottom). Nonetheless, import prices are likely to rise further, as the dollar has depreciated in recent weeks, and this increase may be transmitted to consumer prices with a lag.

Exhibit 1Core Measures of Inflation Have Decelerated since February 2017

(%)

-1

0

1

2

3

4

201720152013201120092007

Recession

Fed Target3-Month Change (Annualized)Y/Y Change

As of June 2017

Source: Bureau of Economic Analysis, Haver Analytics

Exhibit 2Wage Growth Also May Have Slowed

(%)

0

1

2

3

4

5

201720152013201120092007

Recession

Atlanta Fed Wage Growth Tracker3-Month Change (Annualized)Avg. Hourly Earnings (Y/Y Change)

As of July 2017. Atlanta Fed Wage Growth Tracker as of June 2017.

Source: Bureau of Labor Statistics, Federal Reserve Bank of Atlanta, Haver Analytics

Exhibit 3FOMC Projections Have Been Repeatedly Revised Down

(%)

1.0

1.4

1.8

2.2

201720162015201420132012

Actual Dec 2012Dec 2013

Dec 2014Dec 2015

Dec 2016Jun 2017

As of June 2017

Chart displays the actual year-on-year percent change in the core PCE price index versus the median projection by FOMC participants at December FOMC meetings. Projections from 2014 and earlier are the mid-point of the central tendency.

Source: Bureau of Labor Statistics, Federal Reserve Board, Haver Analytics

3

In her June 2017 press conference, FOMC Chair Janet Yellen highlighted a new set of transitory factors: “The recent lower read-ings on inflation have been driven significantly by what appear to be one-off reductions in certain categories of prices, such as wireless telephone services and prescription drugs. These price declines will, as a matter of arithmetic, restrain the 12-month inflation figures until the extraordinarily low March reading drops out of the calcu-lation.”1 Indeed, the rate of increase in prices for both cellphone services and prescription drugs has declined dramatically since the beginning of 2017 (Exhibit 6), and together they account for nearly half the fall in the rate of core inflation as measured by PCE.

However, some critics question whether these “one-off” headwinds to inflation should be seen as transitory, given that the consumer experience is improving in wireless communications. Are these effects genuinely idiosyncratic or are they a feature of how prices do not always move in unison? Is the FOMC in danger of serially making excuses and should it be less hawkish on inflation?

Regardless, the deceleration in core inflation has been broader than just cellphone services and prescription drugs, as a number of other component price indices have slowed—including housing and health care, which together account for nearly half of the compo-nents in core PCE by weight (Exhibit 7). Plausible explanations exist for why prices may be rising less rapidly for many components:

• Prices for apparel and similar goods may be reflecting height-ened competition in the retail sector;

• Housing inflation, already higher than its pre-crisis average, may be plateauing as new supply dampens rapid rental price increases;

• Auto sales have slowed and used car inventories are high; and

• Health care inflation is already low by historical standards, although it could rise with policy change

What Drives Inflation?While it is possible to explain deceleration in some component price indices, the aggregate picture is more puzzling and poses a serious dilemma for the FOMC. Eight years of growth, however tepid, tighter labor markets, and healthier consumer finances should theoretically result in higher demand for resources and, as a consequence, more rapidly rising prices.

Exhibit 4Energy Prices Are No Longer a Tailwind

PCE Price Index, Y/Y Change (%)

-1.5

0.0

1.5

3.0

20172016201520142013201220112010

Differenceex-EnergyHeadline

As of June 2017

Source: Bureau of Economic Analysis, Federal Reserve Board, Haver Analytics

Exhibit 6Cellphone Service and Prescription Drug Price Inflation Has Fallen…

PCE Price Index, Y/Y Change (%)

-16

-8

0

8

201720152013201120092007

Recession

Prescription DrugsCellphone ServicesCore PCE

As of June 2017

Source: Bureau of Economic Analysis, Haver Analytics

Exhibit 5Core Goods Inflation Has Not Reflected Rising Import Prices

Y/Y Change (%) Y/Y Change (%)

Trade Weighted USD [Inverted, RHS]Nonpetroleum Import Prices [LHS]

-6

-3

0

3

6

18

9

0

-9

-18

20172016201520142013201220112010

Y/Y Change (%) Y/Y Change (%)

Core Goods PCE [RHS]Consumer Goods Import Prices [LHS]

-2

0

2

4

-1

0

1

2

20172016201520142013201220112010

As of June 2017

Source: Bureau of Economic Analysis, Federal Reserve Board, Haver Analytics

4

Our view remains that they will. However, as discussed in A Look under the Hood of US Consumer Price Inflation, the experience since the mid-1990s has been moderate, stable inflation rising to the 2.0%–2.5% range for core PCE and 2.0%–3.0% range for core CPI (Exhibit 8), not the rapid, uncontrollable rise to undesirable levels implied by some of the more heated “reflation” sentiment earlier in 2017 or by arguments that the FOMC is “behind the curve.” Furthermore, this experience has not been unique to the United States. Rather, core inflation has converged and moder-ated across many developed markets (Exhibit 9), suggesting it is a feature of the modern economy.

If the moderate inflation of the past two decades is more representa-tive of today’s economy than the experience of the Great Inflation of the late 1960s through early 1980s, cyclical pressures may have a weaker relationship with inflation than theory suggests. For example, the year-on-year change in core PCE never rose above 2.0% in the late 1990s, even as the unemployment rate fell to 3.9%, a full percentage point below the level the Congressional Budget Office (CBO) considered “full employment” at the time (Exhibit 10). Similarly, while the relationship between wage growth and tight labor markets appears to have held up reasonably well in the late 1990s and early 2000s, moderate and relatively stable inflation has meant that the relationship between inflation and wage growth has been murkier (Exhibit 11).2 It also is remarkable how big an impact the transitory factors cited by the FOMC have had on infla-tion, relative to large changes in the unemployment rate.

Exhibit 7… But the Deceleration Has Been Broader

YTD Change in Approximate Contribution to Core PCE (bps)

-10 -5 0 5 10

Recreational durablesTobacco

Stationary & newsHousehold supplies

Social servicesTransportation

Personal care productsRecreational nondurables

LuggagePhones & faxes

Educational booksEducation services

Water supply & sanitationCars & parts

Personal care servicesAlcohol

Household durablesTherapuetic goods

Household maintenanceProfessional services

JewelryHealth care

Food & lodgingHousing

RecreationApparel

Core goodsPharmaceuticals

Communication services

As of June 2017

Source: Bureau of Economic Analysis, Haver Analytics

Exhibit 8Inflation Has Been Moderate since the 1990s

Y/Y Change (%)

0

5

10

15

20172009200119931985197719691961

Recession

2%–3%Core PCECore CPI

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Exhibit 9Inflation Converged and Moderated across Developed Economies

Core CPI of 20 Developed Economies, Y/Y Change (%)

-4

0

4

8

12

201720132009200520011997199319891985

10th–90th Percentile RangeMedian

As of July 2017

Sample includes: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Ireland, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Spain, Sweden, Switzerland, UK, US. Australia and New Zealand CPI are disaggregated quarterly data series.

Source: Haver Analytics, national sources

Exhibit 10How Strong Is the Relationship between Unemployment and Inflation?

(Percentage Points) Y/Y (%)

Core PCE [RHS]Unemployment Gap [LHS]

-2

0

2

4

6

0

1

2

3

4

20172014201120082005200219991996

Recession

As of June 2017

The unemployment gap is the difference between the actual unemployment rate and the CBO estimate of the natural rate of unemployment.

Source: Bureau of Labor Statistics, Congressional Budget Office, Haver Analytics

5

At a minimum, these observations suggest that inflation is well within the control of central banks and that growth and the quality of growth ought to be a greater concern for policymakers. More generally, it also calls into question how well the factors driving inflation are understood, as Chair Yellen herself pointed out in an October 2016 speech—in particular whether the “reduction in sensitivity was somehow caused by the recession or instead pre-dated it and was merely revealed under extreme conditions.”3

Fundamentals Are Still SupportiveAmbiguities about the drivers of inflation aside, the outlook for the US economy remains healthy and continued growth should contribute to cyclical pressures. Starting with the labor market, job growth has remained solid and the unemployment rate has fallen to its pre-crisis low. A variety of other labor market measures also suggest tightening (Exhibit 12). There may be some “hidden slack” in still-elevated levels of part-time workers and still-low levels of prime age (25–54) labor force participation. However, labor force participa-tion is difficult to interpret as it was declining prior to the crisis and both measures have improved since the beginning of the year.

Wage growth, while mildly weaker than cycle highs, is still far higher than post-crisis lows. Furthermore, recent slowing has been sharpest in high-wage industries, while low-wage industries have seen accelerating wage growth.4 Together with continued job growth, wage gains are contributing to higher household income. Household finances also have been supported by rising wealth, as aggregate net worth continues to hit new highs and aggregate equity in housing—particularly important to middle class house-holds—surpassed its pre-crisis peak in nominal terms in the first quarter of 2017. Rising household income and wealth should continue to support consumption and growth.

First quarter real GDP growth was lower than expected at 1.2%, but there have been questions about the accuracy of the Bureau of Economic Analysis’s first-quarter seasonal adjustments in recent years and second-quarter real GDP growth strengthened consider-ably to 2.6%. Furthermore, growth in real final sales to private domestic purchasers—a cleaner measure of domestic demand because it excludes the contributions of trade, government, and changes in inventories—was stronger than headline GDP growth, rising by 3.1% in the first quarter and 2.7% in the second quarter. Measures of household and business sentiment have moderated somewhat after a post-election burst, but still remain elevated.

The international environment also is more constructive as GDP growth in other major economies increasingly appears to be in sync with the steady recovery in the United States. Growth in the euro zone has become more robust, broadening to more countries on the back of strengthening domestic consumption and investment. China’s economic growth re-accelerated in 2016, driven by fiscal and credit stimulus. The Japanese economy has expanded for six consecutive quarters for the first time since 2001, and its unemploy-

Exhibit 12Most Labor Market Measures Suggest Tightening

Jul 2017 or Most Recent

Jan 2017

Post-2007 Worst

2006—2007 Best

Household Survey

Unemployment Rate (%) 4.3 4.8 10.0 4.4

U-6 Rate (%) 8.6 9.4 17.1 7.9

Long-Term Unemployment Rate, 27 Weeks + (%)

1.7 1.9 5.9 1.4

Employment to Population Ratio, Ages 25–54 (%)

78.7 78.2 74.8 80.3

Labor Force Participation Rate, Ages 25–54 (%)

81.8 81.5 80.6 83.4

Establishment Survey (Payrolls)

Private Nonfarm Payrolls, M/M Change (thousands, 3mma)

184 177 -774 284

Average Hourly Earnings, Y/Y Change (%)

2.4 2.4 1.3 4.2

Other Wage Measures

Employment Cost Index, Wages, and Salaries (%)

2.3 2.5 1.4 3.6

Atlanta Fed Wage Growth Tracker (%)

3.2 3.2 1.6 4.4

Job Openings and Labor Turnover Survey (JOLTS)

Job Openings Rate (%) 4.0 3.7 1.7 3.4

Quits Rate (%) 2.1 2.2 1.3 2.2

Hires Rate (%) 3.7 3.7 2.8 4.0

Unemployment Insurance Claims

Initial Claims, 4-Week Average (thousands)

241 252 659 287

Ongoing Claims, 4-Week Average (thousands)

1,965 2,085 6,553 2,378

As of July 2017. Other Wage Measures and Job Openings and Labor Turnover as of June 2017. Employment Cost Index as of March 2017. Initial unemployment claims as of 5 August 2017. Ongoing claims as of 29 July 2017.

Source: Bureau of Labor Statistics, Department of Labor, Federal Reserve Bank of Atlanta, Haver Analytics

Exhibit 11How Strong Is the Relationship between Wages and Inflation?

Core PCE, Y/Y Change (%)

Average Hourly Earnings, Y/Y Change (%)

R² = 0.0328

10864200

3

6

9

121965–19741975–19841985–19941995+Linear (1995+)

As of June 2017

Average hourly earnings are for production and nonsupervisory workers.

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

6

ment rate has reached a 23-year low. Among other things, global synchronized growth lowers the likelihood of a repeat of the rapid appreciation in the US dollar and its impact on import prices.

ConclusionWe expect underlying cyclical pressure to continue to build and for consumer price inflation to grind higher toward cycle highs in the 2%–3% range. Mechanically, the drag from wireless services and prescription drugs is likely to continue to depress inflation readings into the first quarter of 2018, especially relative to expectations earlier in the year. However, “reflation” sentiment almost certainly was overdone. The experience of the last few decades has been moderate inflation, controllable at ever-lower interest rates, and with a weaker relationship to labor market measures than in the 1970s and 1980s. Sharp reversals to high levels of inflation seem unlikely.

For similar reasons, we also think current pessimism is excessive and see very few reasons why inflation should weaken compared to earlier in the recovery. US labor market conditions are clearly tighter than when energy prices plunged in late 2014 and “lowflation” fears first emerged. The outlook for the US economy continues to be healthy and growth appears to be benefiting more households, even as the financial and psychological impacts of the crisis slowly fade. Energy prices, while still low, have stabilized and global growth has become more synchronized, providing a supportive international environment. While the Federal Reserve’s rhetoric has become progressively more hawkish, financial conditions remain relatively loose and the FOMC has identified weaker-than-expected inflation and wage growth as areas of concern.

In A Look under the Hood of US Consumer Price Inflation, we discussed structural risks to inflation from policy change in Washington, D.C. While tax cuts and significant new infrastruc-ture spending would add to cyclical pressures, they seem unlikely in the short term. Efforts to repeal and/or replace the Affordable Care Act could substantially alter the outlook for health care prices and spending, but now appear to be less likely.

Although “reflation” sentiment may have been partially driven by elevated expectations for domestic policy changes, a lack of legislative success in these arenas (coupled with escalating contro-versy) could still motivate the White House to deliver on its campaign promises on trade. Such a turn to protectionism could meaningfully increase inflation pressures. Moreover, President Donald Trump has announced one appointee for the FOMC, Randal Quarles, and could appoint as many as four additional voting members in the next 12 months if Janet Yellen and Stanley Fischer choose to retire when their terms end as FOMC Chair and Vice Chairmen respectively. While we have no particular insight in terms of whom Trump might choose, the complexion and direction of the FOMC could change meaningfully under new leadership with implications for inflation.

While near-term measures point to softness in inflation, we continue to believe the medium-term trajectory will be gradual increases in inflation with the tail risk that protectionism could substantially add to inflation. We continue to monitor the implica-tions of populism for policy and inflation as well as the underlying economic factors that can affect price pressures. Meanwhile, we believe it is important for investors to evaluate their positioning to ensure that they are protected from the risk of higher inflation while also earning a reasonable return on their assets.

7

Appendix: Inflation DashboardWe display four categories of the key indicators to understand past inflation trends and gain forward-looking insights.

Recent Trends5

Energy Price Impact Fading from Headline Inflation

Recession

Y/Y Change (%)

CPI-U All ItemsPCE Price Index

-2

0

2

4

6

2017201520132011200920072005

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Shorter-Term Trends Reflect Deceleration (Headline Indices)

RecessionCPI-U All ItemsPCE Price Index

Headline, 3-Month Change, Annualized (%)

-12

-6

0

6

12

2017201520132011200920072005

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Core Measures Decelerating As Well

Recession

Core, Y/Y Change (%)

CPI-UPCE Price Index

0

1

2

3

2017201520132011200920072005

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Shorter-Term Trends Reflect Deceleration (Core Indices)

Recession

Core, 3-Month Change, Annualized (%)

CPI-UPCE Price Index

-1

0

1

2

3

4

2017201520132011200920072005

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Expectations

Market Expectations Moderated (CPI)

(%)

-4

-2

0

2

4

2017201520132011200920072005

5-Year Breakeven Inflation10-Year Breakeven Inflation5-Year Forward Inflation Expectation

As of 8 August 2017

Source: Federal Reserve Board, Haver Analytics

Consumer Expectations Low but More Stable (CPI)

Recession

Expected Inflation Rate (%)

Next YearNext 5 Years

0

2

4

6

2017201520132011200920072005

As of July 2017

Source: Haver Analytics, University of Michigan

8

Major Components

Services Drive Inflation (CPI)

Recession

Y/Y Change (%)

-4

-2

0

2

4

2017201520132011200920072005

Core CPIGoods Less Food & EnergyServices Less Energy

As of June 2017

Source: Bureau of Labor Statistics, Haver Analytics

Housing Inflation Has Rebounded to Pre-Crisis Levels

Housing Share: CPI 33.7%; PCE 15.8%

Y/Y Change (%)

-2

0

2

4

6

2017201520132011200920072005

CPI Shelter2002–2007 Avg.PCE Housing

Recession

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Energy Prices Have Stabilized

Y/Y Change (%)

-40

-20

0

20

40

2017201520132011200920072005

CPI EnergyPCE Energy

Recession

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Services Drive Inflation (PCE)

Y/Y Change (%)

-2

0

2

4

2017201520132011200920072005

Core PCEGoods Less Food & Energy

Services Less Energy

Recession

As of 31 July 2017

Source: Bureau of Labor Statistics, Haver Analytics

Food Prices Accelerating

Y/Y Change (%)

-4

0

4

8

2017201520132011200920072005

CPI FoodPCE Food

Recession

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Health Care Services Price Growth down from Pre-Crisis Levels, Especially PCE

Health Care Share: CPI 6.7%; PCE 17.2%

Y/Y Change (%)

0

2

4

6

2017201520132011200920072005

CPI Medical Care ServicesPCE Health Care

Recession

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

9

Producer Prices

Domestic Producer Prices Are Rising

Core PPI, Y/Y Change (%)

-12

-6

0

6

12

2017201520132011200920072005

Finished GoodsIntermediate Goods

Recession

As of July 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Core Import Prices Are Rising…

Imports, Y/Y Change (%)

-24

-12

0

12

24

2017201520132011200920072005

All ImportsNonpetroleumCore Consumer Goods

Recession

As of June 2017

Source: Bureau of Labor Statistics, Haver Analytics

International Producer Prices Are Rising

(%)

-12

-6

0

6

12

2017201520132011200920072005

Euro Zone Japan China

As of June 2017

Euro Zone: Domestic PPI for Industry excluding Construction & Energy. Japan: Domestic CGPI excluding consumption tax & summer electric charges. China: PPI All Industry Products.

Source: Bank of Japan, China National Bureau of Statistics, Eurostat, Haver Analytics

… And the USD Has Weakened

Trade-Weighted USD, Y/Y Change (%)

-12

0

12

24

2017201520132011200920072005

RealNominal

Recession

As of July 2017

Source: Federal Reserve Board, Haver Analytics

Cyclical Pressures

Labor Market Is Tightening

(%)

3

8

13

18

2017201520132011200920072005

U3UnemploymentRate

U6 Unemployment +Marginally Attached +Part-Time for EconomicReasons Rate

CBO Estimateof the Natural Rateof Unemployment

Recession

As of June 2017

Source: Bureau of Economic Analysis, Bureau of Labor Statistics, Haver Analytics

Wage Growth Acceleration Has Slowed Recently

(%)

1.2

2.3

3.4

4.5

2017201520132011200920072005

Avg. Hourly Earnings, Y/Y Change Employment Cost Index, Y/Y ChangeAtlanta Fed Wage Growth Tracker

Recession

As of June 2017

Average hourly earnings is for production & nonsupervisory workers. Employment Cost Index is wages & salaries for all civilian workers and is a disaggregated quarterly series.

Source: Eurostat, Bank of Japan, China National Bureau of Statistics, Haver Analytics

10

This document reflects the views of Lazard Asset Management LLC or its affiliates (“Lazard”) based upon information believed to be reliable as of 29 August 2017. There is no guarantee that any forecast or opinion will be realized. This document is provided by Lazard Asset Management LLC or its affiliates (“Lazard”) for informational purposes only. Nothing herein constitutes investment advice or a recommendation relating to any security, commodity, derivative, investment management service or investment product. Investments in securities, derivatives and commodities involve risk, will fluctuate in price, and may result in losses. Certain assets held in Lazard’s investment portfolios, in particular alternative investment portfolios, can involve high degrees of risk and volatility when compared to other assets. Similarly, certain assets held in Lazard’s investment portfolios may trade in less liquid or efficient markets, which can affect investment performance. Past performance does not guarantee future results. The views expressed herein are subject to change, and may differ from the views of other Lazard investment professionals.

This document is intended only for persons residing in jurisdictions where its distribution or availability is consistent with local laws and Lazard’s local regulatory authorizations. Please visit www.lazardassetmanagement.com/globaldisclosure for the specific Lazard entities that have issued this document and the scope of their authorized activities.

LR28734

Notes1 Janet Yellen, “Transcript of Chair Yellen’s Press Conference,” Federal Reserve, 14 June 2017.

2 Nick Bunker, “Is the Fed being misguided by the Phillips Curve?,” Washington Center for Equitable Growth, 21 June 2017.

3 Janet Yellen, “Macroeconomic Research After the Crisis,” Federal Reserve, 14 October 2016.

4 Jan Hatzius et al., “US Daily: Wage Growth Trends by Income Level: Top Down, Bottom Up,” Goldman Sachs, 20 July 2017.

5 The Consumer Price Index (CPI) is the more widely cited measure of inflation and is used to calculate price changes for economic data like real wages, financial instruments like Treasury Inflation-Protected Securities (TIPS), cost of living adjustments in tax brackets, government programs like social security, and collectively bargained wages. The Personal Consumption Expenditures (PCE) price index is the deflator for consumption’s contribution to GDP in the National Income and Product Accounts and is the preferred measure of the Federal Reserve.

Important InformationPublished on 8 September 2017.

This content represents the views of the author(s), and its conclusions may vary from those held elsewhere within Lazard Asset Management. Lazard is committed to giving our investment professionals the autonomy to develop their own investment views, which are informed by a robust exchange of ideas throughout the firm.