Revision - Classical and Keynesian.pptx

29

Keynes and the Classical Economists: The Early Debate on Policy Activism

-

Upload

mskhan0078 -

Category

Documents

-

view

218 -

download

3

Transcript of Revision - Classical and Keynesian.pptx

Keynes and the Classical Economists:

The Early Debate on Policy Activism

THE CLASSICAL MODEL

Say’s LawThe classical economists based their predictions about full employment on a principle known as Say’s Law, the creation of French economist J. B. Say (1776–1832). According to Say’s Law, “Supply creates its own demand.” In other words, in the process of producing output, businesses also create enough income to ensure that all the output will be sold. Because this theory occupies such an important place in classical economics.

THE CLASSICAL MODEL

Flexible Wages and Prices The classical economists believed that all prices—including wage rates (the price oflabor) and other input prices—were highly flexible. They believed that Say’s Law and the flexibility of interest rates would ensure that spending would be adequate to maintain full employment.

THE CLASSICAL MODEL

Full EmploymentAs a consequence of their faith in Say’s Law and the flexibility of wages and prices, the classical economists viewed full employment as the normal situation. They held this belief in spite of recurring periods of observed unemployment. By the mid 1800s, economists recognized that capitalist economies tend to expand over time but not at a steady rate. Instead, output and employment fluctuate up and down, growing rapidly in some periods and more slowly, or even declining, in others.

THE CLASSICAL MODEL

Laissez-FaireThe classical theorists’ belief in the economy’s ability to maintain full employment through its own internal mechanisms caused them to favor a policy of laissez-faire, or government by nonintervention. Society was advised to rely on the market mechanism to take care of the economy and to limit the role of government to the areas where it could make a positive contribution—maintaining law and order and providing for the national defense, for example.

THE KEYNESIAN CRITICISM

The role of demand sideKeynesian economics places central importance on demand, believing that on the macroeconomic level, the amount supplied is primarily determined by effective demand or aggregate demand. For example, without sufficient demand for the products of labor, the availability of jobs will be low; without enough jobs, working people will receive inadequate income, implying insufficient demand for products. Thus, an aggregate demand failure involves a vicious circle.

THE KEYNESIAN CRITICISM Wage/Price rigidityKeynes argued that the classical assumption of highly flexible wages and prices was not consistent with the real world. Ac-cording to Keynes, a variety of forces prevent prices and wages from adjusting quickly, particularly in a downward direction. First, markets are less competitive than the classical theory assumed. Keynes saw that many product markets were monopolistic or oligopolistic. When sellers in these markets noted that demand was declining, they often chose to reduce output rather than lower prices. And in labor markets, particularly those dominated by strong labor unions, workers tended to resist wage cuts. As a consequence, wages and prices did not adjust quickly; they tended to be rigid or “sticky.”

THE KEYNESIAN CRITICISM

Employment with unemploymentKeynes and the classical economists agreed that the economy would always tend toward equilibrium, but they disagreed about whether the level of output at which the economy stabilized would permit full employment. In the classical model the economy tends to stabilize at a full-employment equilibrium. In the Keynesian model the economy tends toward equilibrium but not necessarily at full employment. When the economy is in equilibrium at less than full employment, an unemployment equilibrium exists.

THE KEYNESIAN CRITICISM

Government interventionBecause Keynes did not believe that a market economy could be relied on to automatically preserve full employment and avoid inflation, he argued that the central government must manage the level of aggregate demand to achieve those objectives. How could this be accomplished? One approach was through fiscal policy, the manipulation of government spending and taxation in order to guide the economy’s performance. Another approach would be to use monetary policy: policy intended to alter the supply of money in order to influence the level of economic activity.

Consumption function

Consumption function

Consumption function shows the relationship between the level of consumption expenditure and the level of income.

C = f (Y) C = a + bY C = 100 + 0.75Y

Where “a” is autonomous and “bY” is income induced consumption.

THE KEYNESIAN

ECONOMICS

Autonomous consumption expenditure

Autonomous consumption expenditure occurs when income levels are zero. Such consumption does not vary with changes in income. If income levels are actually zero, this consumption is financed by borrowing or using up savings.

Induced consumption

Induced consumption describes consumption expenditure by households on goods and services which varies with income. Consumption is considered induced by income.

THE

KEYNESIAN ECONOMICS

Consumption function

Marginal Propensity to Consume

The marginal propensity to consume (MPC) is the extra amount that people consume when they receive an extra unit of income.

MPC = ΔC / ΔY

MPC is the slope (first derivative) of consumption function.Induced consumption can be described by formula: Induced consumption = MPC . Y

Y = C + S … MPC= ΔC/ ΔY … APC = C/Y MPS= ΔS/ ΔY … APS = S/Y

“Complete the table”

.

Y

C

0

Consumption function C = f(Y)

Savings

Consumption

45˚

Y1 Y 2

a

A

DB

C

The Consumption Function45˚ line: At any point on the 45˚line consumption exactly equals income and the households have zero saving. MPC is the slope of the consumption function, which measures the change in consumption per unit change in income.

“Determinants of Consumption”

Current disposable income: it is the central factor determining a nation's consumption.

Permanent income: it is the level of income that households would receive when temporary influences are removed.

Wealth: it is the net value of tangible and financial items owned by a nation or person at a point of time.

Other (interest rate, inflation, expectations).

SavingSaving is that part of income that is not consumed. Saving equals income minus consumption: S = Y – C

Income is the sum of consumption and savings: Y = C + S

then and

1Y

S

Y

C1

Y

S

Y

C

Marginal propensity to save

It is defined as the fraction of an extra unit of income that goes to extra saving.MPC + MPS = 1 because the part of each unit of income that is not consumed is necessarily saved.

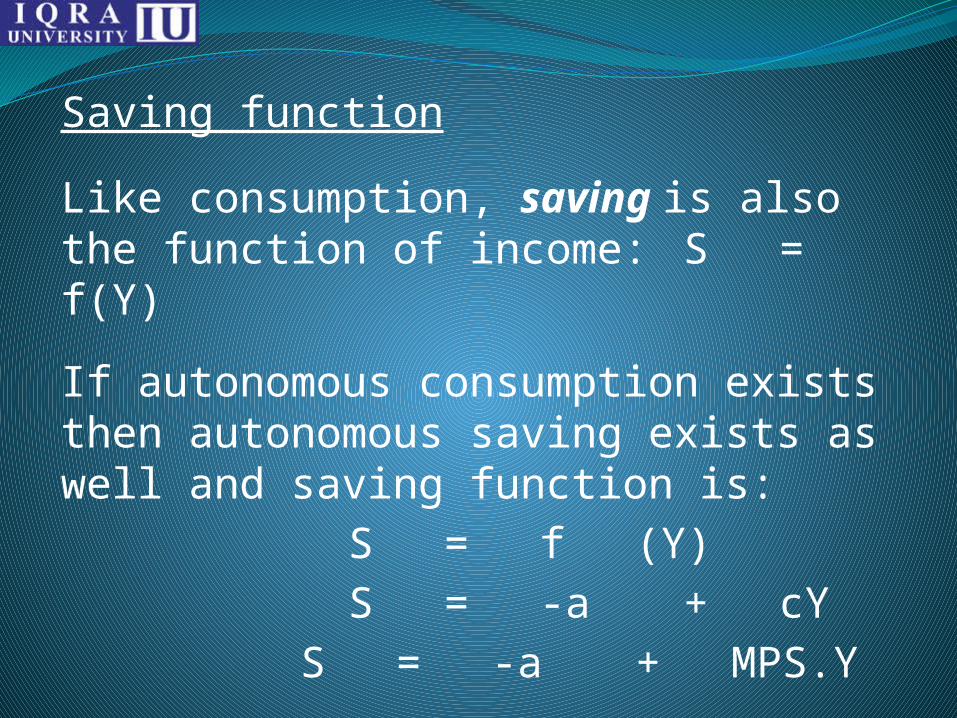

Saving function

Like consumption, saving is also the function of income: S = f(Y)

If autonomous consumption exists then autonomous saving exists as well and saving function is: S = f (Y) S = -a + cY S = -a + MPS.Y

.

The saving function is the mirror image of the consumption function. It shows the relationship between the level of saving and income.

0

C = f(Y)

45˚

Y E

CA

-CA

S = f(Y)

C, S

Y

InvestmentInvestment pays two roles in macroeconomics:It can have a major impact on AD (real output and employment)

It leads to capital accumulation (it increases the nation's potential output and promotes economic growth in the long run)

Determinants of InvestmentRevenues: an investment should bring the firm additional revenue.

Costs: interest rate influences the costs of the investment.

Consumer demand: the bigger the increase in consumer demand, the more investment will be needed.

Expectation: business expectation about future state of economy.

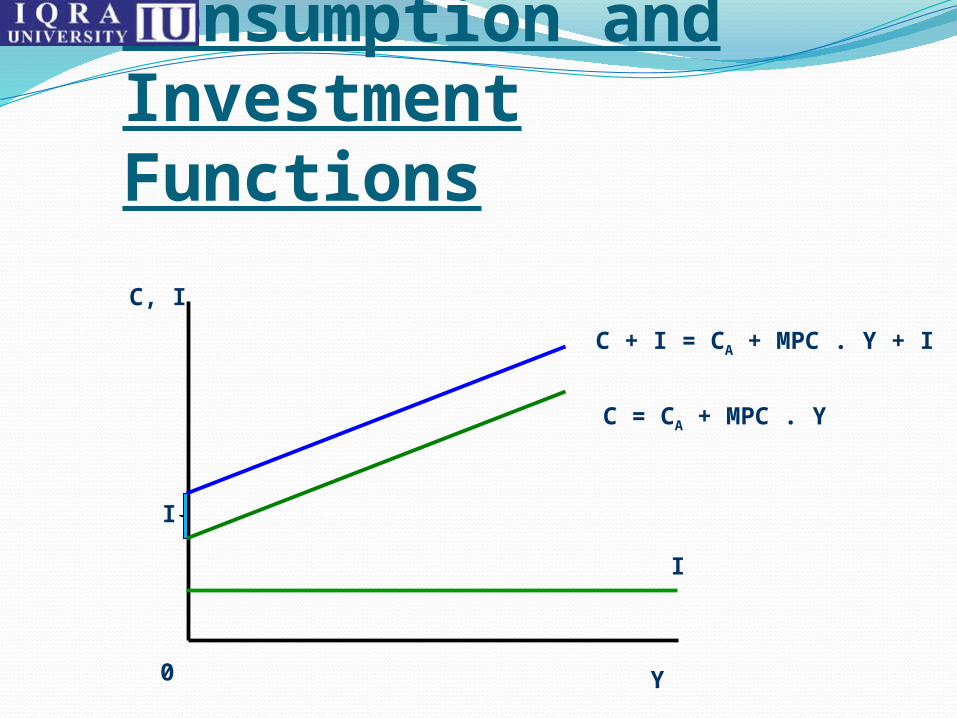

Consumption and Investment FunctionsThe spending curve shows the level of desired expenditure by consumers (CA + MPC.Y) and businesses (I) corresponding to each level of output.

Consumption and Investment Functions

Y

C, I

0

C = CA + MPC . Y

C + I = CA + MPC . Y + I

I

I

Consumption and Investment FunctionsThe spending curve shows the level of desired expenditure by consumers (CA + MPC.Y) and businesses (I) corresponding to each level of output.

Consumption and Investment Determine Output

If the level of output is e. g. Y1 at this level of output the C+I spending line is above 45˚line, so planned spending is greater than planned output.

This means that consumers would be buying more goods than the businesses were producing. Thus spending disequilibrium leads to a change in output.

Equilibrium National Income

Y

C, I

0

45˚

C + I = CA + MPC . Y + I

E

Y1 YE Y2

Consumption and investment determine output

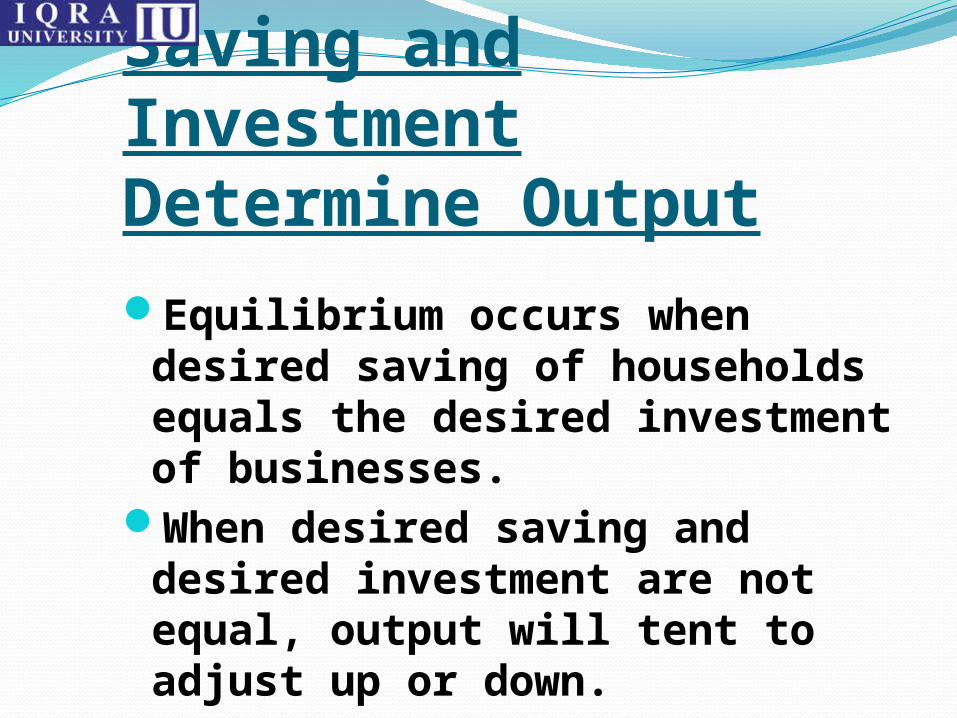

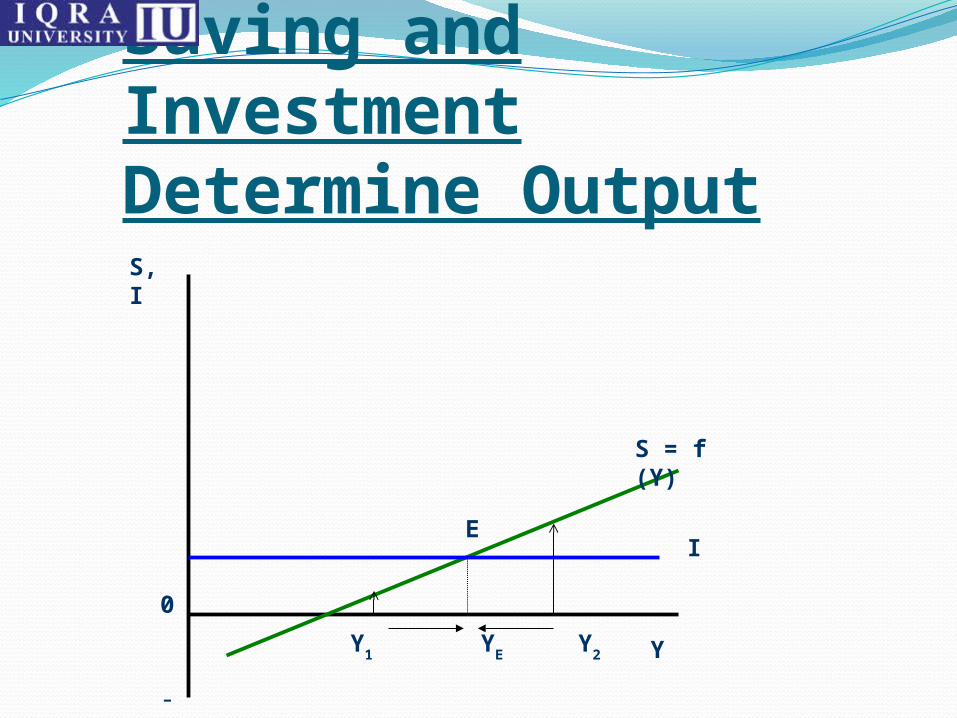

Saving and Investment Determine OutputEquilibrium occurs when desired saving of households equals the desired investment of businesses.

When desired saving and desired investment are not equal, output will tent to adjust up or down.

Saving and Investment Determine Output

Y

S, I

0

S = f (Y)

E

Y1 YE Y2

I

-

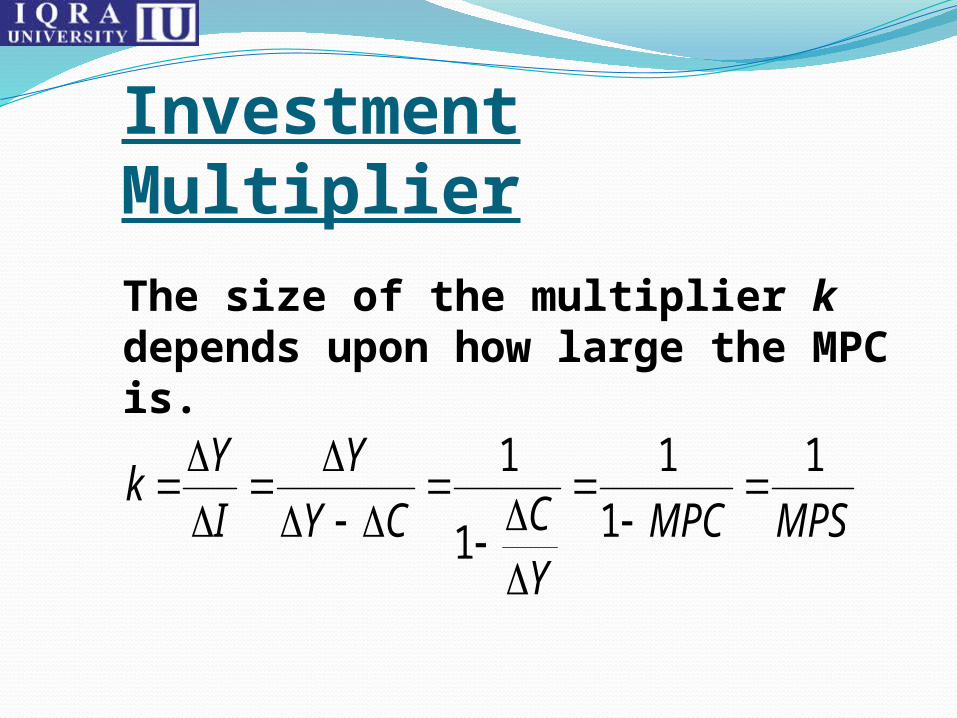

Investment MultiplierThe Keynesian investment multiplier

model shows that an increase in investment will increase output by a multiplied amount – by an amount greater than itself.

The multiplier is the number by which the change in investment must be multiplied in order to determine the resulting change in total output.

Investment MultiplierThe size of the multiplier k depends upon how large the MPC is.

MPSMPCYCCY

Y

I

Yk

1

1

1

1

1

![Knowledge and Games: Theory and Implementation · [19] Johan van Benthem. Dynamic logic for belief revision. Journal of Applied Non-Classical Logics, 17(2):129–155, 2007. Cited](https://static.fdocuments.us/doc/165x107/5f0b439e7e708231d42fa7e2/knowledge-and-games-theory-and-implementation-19-johan-van-benthem-dynamic-logic.jpg)