REVIEWING THE PHARMACY LANDSCAPE · 10/16/2018 · HEALT H W EALT H CAREER REVIEWING THE PHARMACY...

15

HEALTH WEALTH CAREER REVIEWING THE PHARMACY LANDSCAPE OCTOBER 16, 2018 Virginia Rivas, Pharm.D. West Market Pharmacy Lead

Transcript of REVIEWING THE PHARMACY LANDSCAPE · 10/16/2018 · HEALT H W EALT H CAREER REVIEWING THE PHARMACY...

H E A LT H W E A LT H C A R E E R

R E V I E W I N G T H E

P H A R M A C Y L A N D S C A P E

OCTOBER 16, 2018

Virginia Rivas, Pharm.D.

West Market Pharmacy Lead

2 Copyright © 2018 Mercer (US) Inc. All rights reserved.

A G E N D A

1

2

3

UPWARD PRESSURES ON DRUG PRICES

PHARMACY MANAGEMENT CONSIDERATIONS

PBM MARKET AND INDUSTRY UPDATES

3 Copyright © 2018 Mercer (US) Inc. All rights reserved.

PBM MARKET AND

INDUSTRY UPDATES

4 Copyright © 2018 Mercer (US) Inc. All rights reserved.

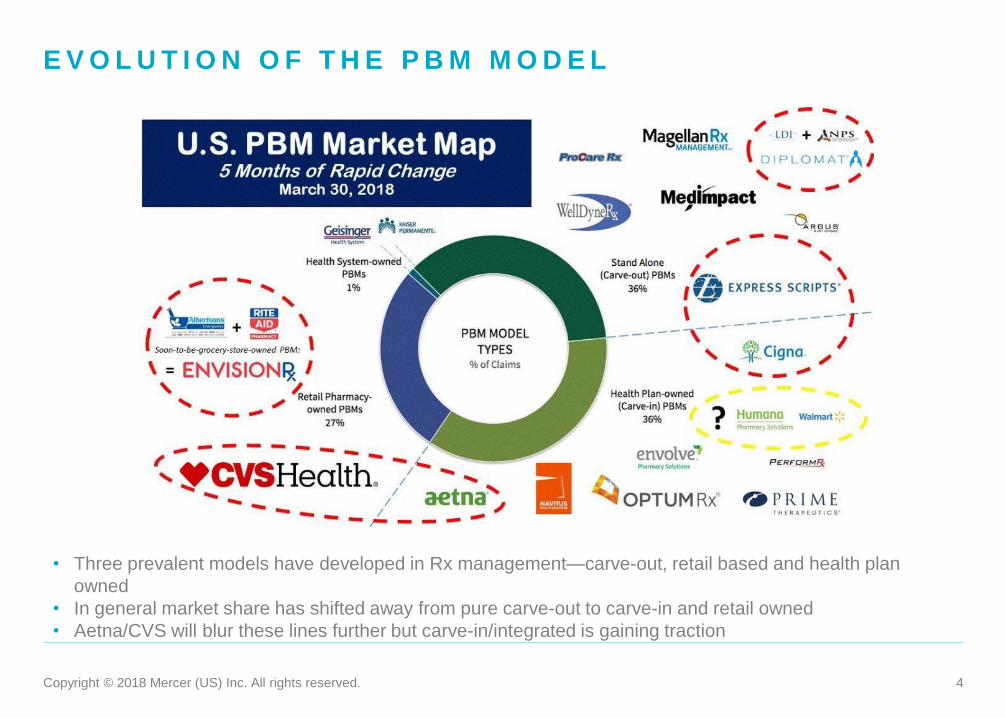

E V O L U T I O N O F T H E P B M M O D E L

• Three prevalent models have developed in Rx management—carve-out, retail based and health plan

owned

• In general market share has shifted away from pure carve-out to carve-in and retail owned

• Aetna/CVS will blur these lines further but carve-in/integrated is gaining traction

5 Copyright © 2018 Mercer (US) Inc. All rights reserved.

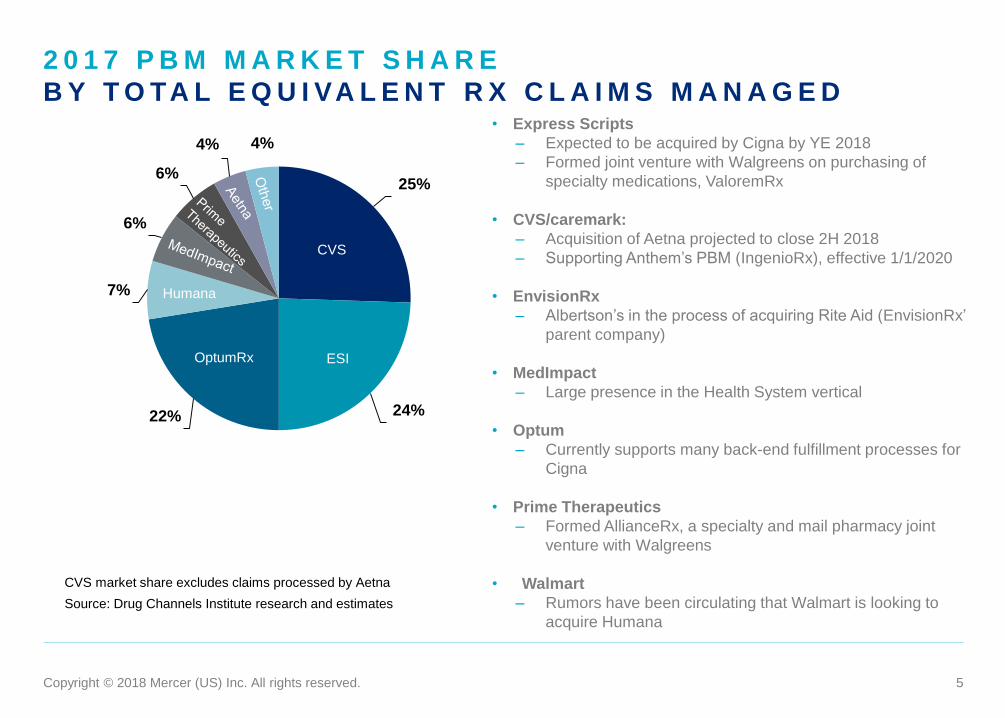

2 0 1 7 P B M M A R K E T S H A R E

B Y T O TA L E Q U I VA L E N T R X C L A I M S M A N A G E D • Express Scripts

– Expected to be acquired by Cigna by YE 2018

– Formed joint venture with Walgreens on purchasing of

specialty medications, ValoremRx

• CVS/caremark:

– Acquisition of Aetna projected to close 2H 2018

– Supporting Anthem’s PBM (IngenioRx), effective 1/1/2020

• EnvisionRx

– Albertson’s in the process of acquiring Rite Aid (EnvisionRx’

parent company)

• MedImpact

– Large presence in the Health System vertical

• Optum

– Currently supports many back-end fulfillment processes for

Cigna

• Prime Therapeutics

– Formed AllianceRx, a specialty and mail pharmacy joint

venture with Walgreens

• Walmart

– Rumors have been circulating that Walmart is looking to

acquire Humana

25%

24% 22%

7%

6%

6%

4% 4%

ESI

CVS

OptumRx

Humana

CVS market share excludes claims processed by Aetna

Source: Drug Channels Institute research and estimates

6 Copyright © 2018 Mercer (US) Inc. All rights reserved.

UPWARD PRESSURES ON

DRUG PRICES

7 Copyright © 2018 Mercer (US) Inc. All rights reserved.

6.3%

5.1% 5.2% 5.5% 5.4%

8.0% 7.4% 7.6% 7.8%*

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

2010 2011 2012 2013 2014 2015 2016 2017 2018* Projected

2017 growth in cost for specialty drugs: 15.4%

Avg. annual change in prescription drug benefit cost for large employers

Source: Mercer National Survey of Employer-Sponsored Health Plans

D R U G C O S T S I N E M P L O Y E R H E A LT H P L A N S

C O N T I N U E T O R I S E N E A R LY 8 % P E R Y E A R

8 Copyright © 2018 Mercer (US) Inc. All rights reserved.

H O T P H A R M A C Y T O P I C S I N T H E N E W S

M a y 11 , 2 0 1 8

“Drugs that can cost tens of thousands of dollars a month

mostly treat rare conditions.”

The 5 most expensive drugs in the United States

Ap r i l 2 5 , 2 0 1 8

“The price of just one of [her] drugs will be about $600,000

this year.”

Mother, wife, million-dollar patient

F e b r u a r y 2 , 2 0 1 8

“… [A] recently approved revolutionary gene therapy drug

aimed at treating a rare type of inherited retinal dystrophy

will come with an eye watering price tag.”

New million-dollar eye treatment

J u l y 2 7 , 2 0 1 8

“A growing chorus … is calling for a rethinking of after-the-

fact drug discounts (rebates) that some say contribute to

rising prices.”

Meet the rebate, the new villain of high drug prices

https://www.washingtonpost.com/graphics/2018/business/million-dollar-patient/?utm_term=.fd76685bc7c3

https://www.washingtonpost.com/graphics/2018/business/million-dollar-patient/?utm_term=.fd76685bc7c3

https://www.washingtonpost.com/graphics/2018/business/million-dollar-patient/?utm_term=.fd76685bc7c3

https://www.washingtonpost.com/graphics/2018/business/million-dollar-patient/?utm_term=.fd76685bc7c3

9 Copyright © 2018 Mercer (US) Inc. All rights reserved.

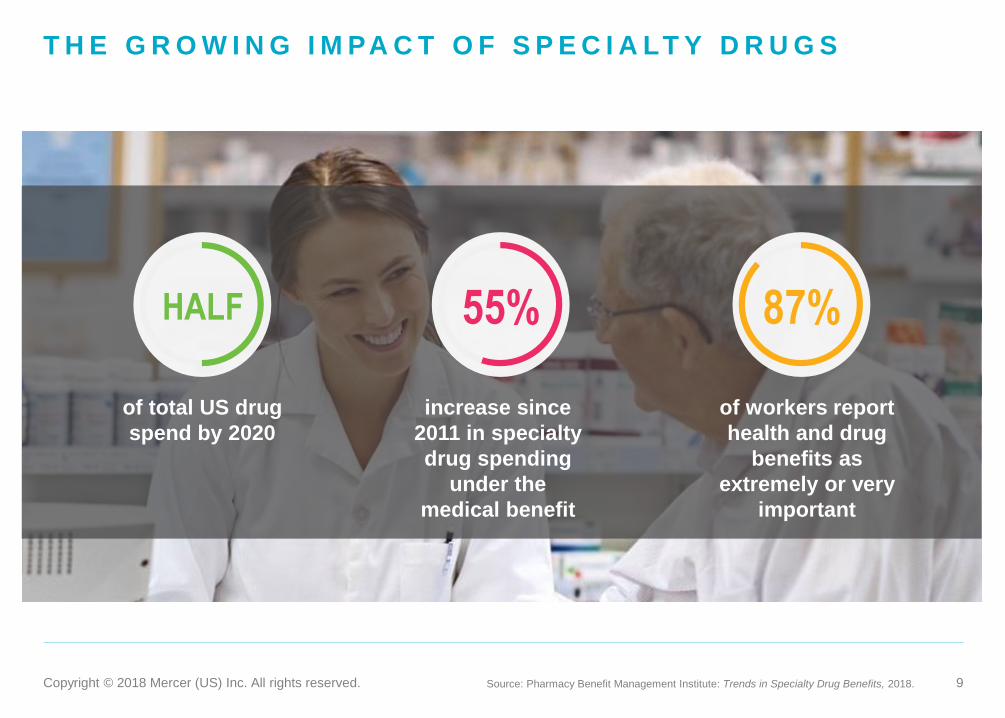

T H E G R O W I N G I M PA C T O F S P E C I A LT Y D R U G S

Source: Pharmacy Benefit Management Institute: Trends in Specialty Drug Benefits, 2018.

of total US drug

spend by 2020

HALF

increase since

2011 in specialty

drug spending

under the

medical benefit

55%

of workers report

health and drug

benefits as

extremely or very

important

87%

10 Copyright © 2018 Mercer (US) Inc. All rights reserved.

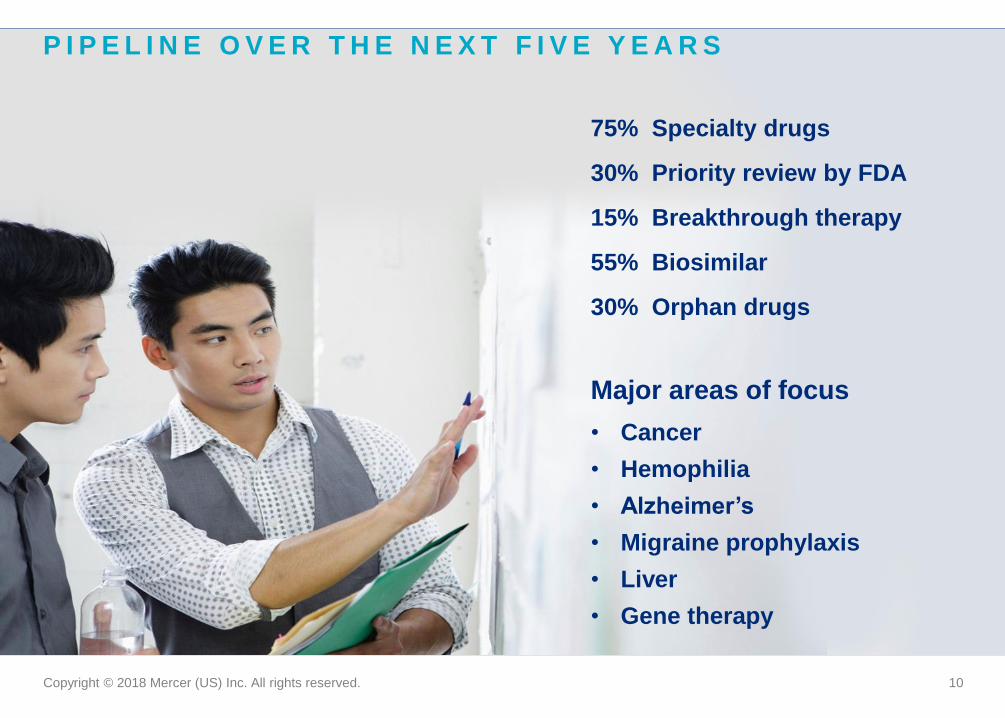

P I P E L I N E O V E R T H E N E X T F I V E Y E A R S

75% Specialty drugs

30% Priority review by FDA

15% Breakthrough therapy

55% Biosimilar

30% Orphan drugs

Major areas of focus

• Cancer

• Hemophilia

• Alzheimer’s

• Migraine prophylaxis

• Liver

• Gene therapy

11 Copyright © 2018 Mercer (US) Inc. All rights reserved.

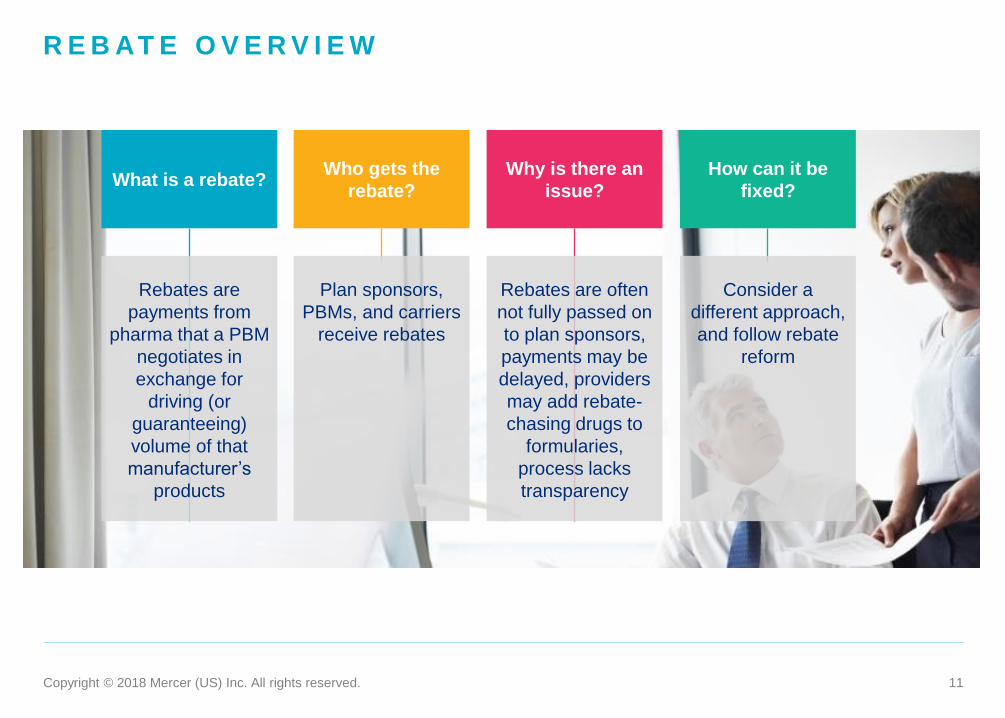

R E B AT E O V E R V I E W

Who gets the

rebate? What is a rebate?

Why is there an

issue?

How can it be

fixed?

Plan sponsors,

PBMs, and carriers

receive rebates

Rebates are

payments from

pharma that a PBM

negotiates in

exchange for

driving (or

guaranteeing)

volume of that

manufacturer’s

products

Rebates are often

not fully passed on

to plan sponsors,

payments may be

delayed, providers

may add rebate-

chasing drugs to

formularies,

process lacks

transparency

Consider a

different approach,

and follow rebate

reform

12 Copyright © 2018 Mercer (US) Inc. All rights reserved.

L E G A L R E C A P : W AT C H R E G U L AT O R Y A N D

L I T I G AT I O N D E V E L O P M E N T S , B U T F O C U S O N

C O N T R A C T I N G

• Few federal legal initiatives to address escalating drug costs in employer

sponsored plans:

– ERISA does not generally regulate what drugs are covered and not covered

– Efforts to hold PBMs accountable as fiduciaries through the courts have not

been successful

– No action so far on ERISA Advisory Council recommendation from 2014

– Trump administration focus has been on changes to the public programs

with the goal to drive changes across the entire system

• More activity at the state level, but legal barriers could impede progress, and many

laws won’t apply to self-insured ERISA plans

• For now, plan sponsors should continue to focus on contracting and plan terms

13 Copyright © 2018 Mercer (US) Inc. All rights reserved.

PHARMACY MANAGEMENT

CONSIDERATIONS

14 Copyright © 2018 Mercer (US) Inc. All rights reserved.

C O N S I D E R AT I O N S F O R P H A R M A C Y M A N A G E M E N T

Determine where your biggest opportunit ies are to manage

special ty t rend – Rx and medical

Gauge your dependence on rebates, and consider al ternat ives

Monitor federal and state legislat ive in i t iat ives and

regulatory changes

Revisi t current arrangements to address areas for improvement

15 Copyright © 2018 Mercer (US) Inc. All rights reserved.