REVIEW OF THE THEORETICAL LITERATURE - College of Europe

64

1 SUSTAINABLE GROWTH, EMPLOYMENT CREATION AND TECHNOLOGICAL INTEGRATION IN THE EUROPEAN KNOWLEDGE-BASED ECONOMY (SETI/SERD-2000-00126) REVIEW OF THE THEORETICAL LITERATURE by College of Europe (Bruges, Belgium), CeSPI (Rome, Italy), SPRU (University of Sussex, UK), Leverhulme (University of Nottingham, UK) January 2002

Transcript of REVIEW OF THE THEORETICAL LITERATURE - College of Europe

1

SUSTAINABLE GROWTH, EMPLOYMENT CREATION AND TECHNOLOGICAL

INTEGRATION IN THE EUROPEAN KNOWLEDGE-BASED ECONOMY

(SETI/SERD-2000-00126)

REVIEW OF THE THEORETICAL LITERATURE

by

College of Europe (Bruges, Belgium), CeSPI (Rome, Italy), SPRU (University

of Sussex, UK), Leverhulme (University of Nottingham, UK)

January 2002

2

Table of Contents

1. Introduction ............................................................................................................................................................................32. Technology and specialisation ............................................................................................................................................4

2.1 Technology and specialisation: theories and empirical evidence .....................................................................5The consideration of technology like a key determinant of country and sectorial trade performance has generatedan impressive development of theoretical and empirical proposals in the last years. Two themes in particularhave received special attention in recent years:....................................................................................................................5

2.1.1 The impact of technology on trade competitiveness and specialisation........................................................52.1.2 Trends in specialisation patterns ..........................................................................................................................7

2.2 The impact of specialisation on international competitiveness and economic growth ...............................9Table 2.1: The impact of specialisation on economic performance .................................................................10

Methodology .............................................................................................................................................................................10Dependent variable .............................................................................................................................................................10

Significant .................................................................................................................................................................................102.3 Specialisation and employment creation...............................................................................................................132.4 Open questions and directions for future research............................................................................................15

3. Services..................................................................................................................................................................................163.1 What are services?......................................................................................................................................................16

3.1.1 Services versus goods ..........................................................................................................................................163.1.2 The internationalisation of services ...................................................................................................................17

3.2 Trends in services ........................................................................................................................................................193.2.1 Trade in services....................................................................................................................................................19Table 3.1: World trade in goods and services .......................................................................................................20Table 3.2: Trade in services by EU country and broad sector for 1999 ........................................................20Table 3.3: Trade value by major economic region and selected industry (1990-1999) .............................22Table 3.4: Share in total services trade by major economic region and selected industry ...........................(1990-1999)......................................................................................................................................................................233.2.2 FDI in services.......................................................................................................................................................23Table 3.5: World foreign production in goods and services ..............................................................................24

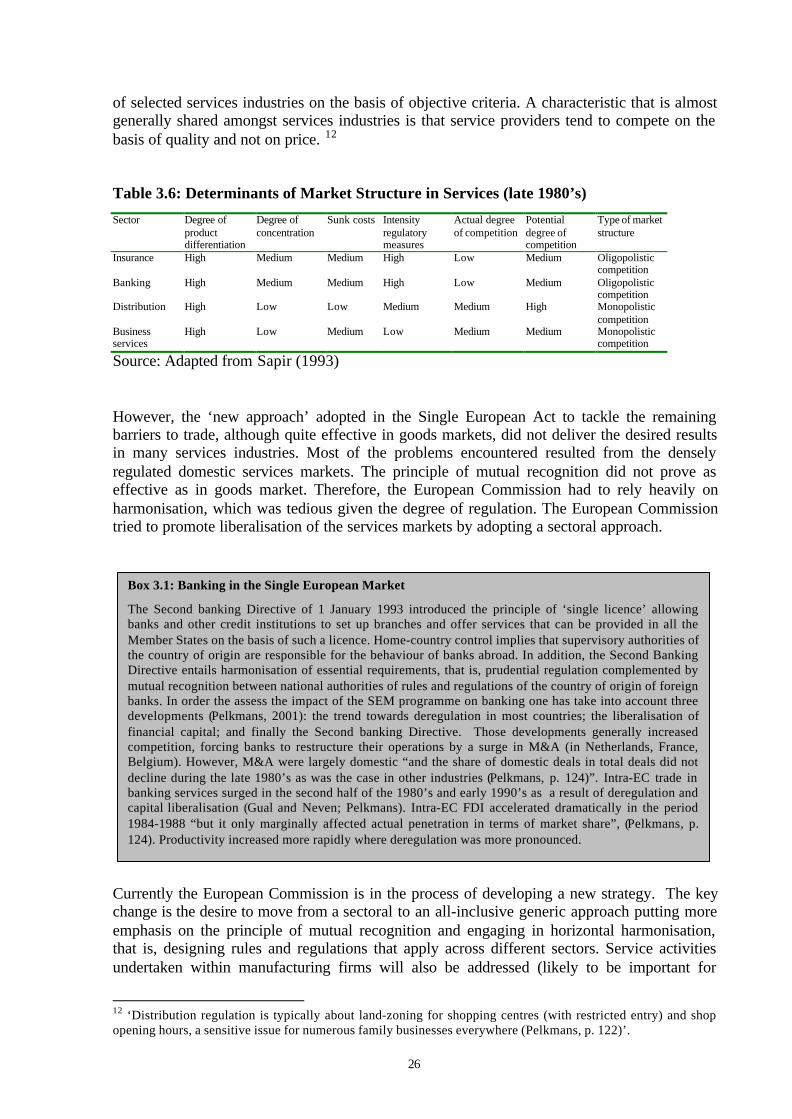

3.3 The regulatory environment ....................................................................................................................................253.3.1 The free movement of services within the EU .................................................................................................25Table 3.6: Determinants of Market Structure in Services (late 1980’s).........................................................263.3.2 The GATS and beyond ........................................................................................................................................27

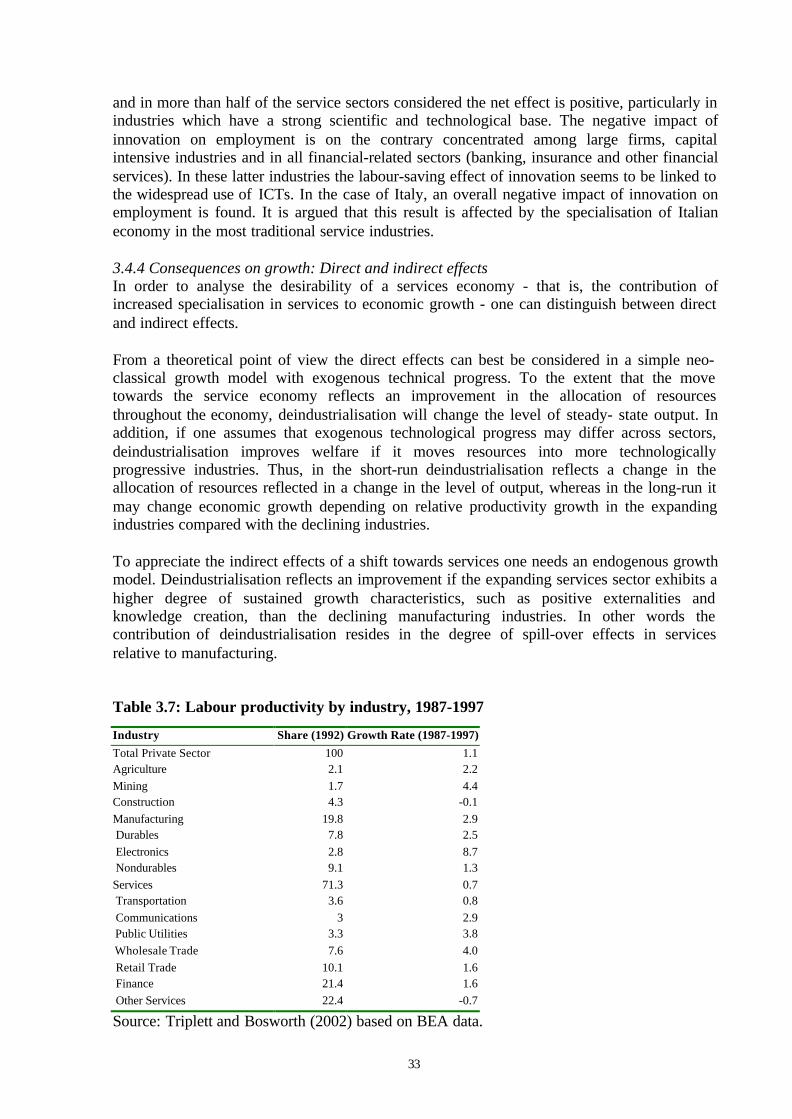

3.4 Services, employment and economic growth .......................................................................................................283.4.1 Explaining the service economy .........................................................................................................................293.4.2 Technological change in services.......................................................................................................................303.4.3 Consequences on employment....................................................................................................................313.4.4 Consequences on growth: Direct and indirect effects.....................................................................................33Table 3.7: Labour productivity by industry, 1987-1997 ....................................................................................333.4.5 The internationalisation of services and economic growth............................................................................35

3.5 Open issues and directions for future research...................................................................................................364. The Information and Communication Technology (ICT) revolution.........................................................................39

4.1 Theoretical frameworks ............................................................................................................................................404.1.1 ICT as a new techno-economic paradigm.........................................................................................................404.1.2 ICT as a GPT..........................................................................................................................................................40

4.2 ICT and growth in the US and in Europe: A short review..............................................................................414.2.1 An overview of the US debate on ICT and growth.........................................................................................414.2.2 International comparisons of ICT and growth in the OECD area.................................................................43

4.3 Open Issues and Directions for Future Research ...............................................................................................455. The internationalisation of technology ............................................................................................................................46

5.1 Theoretical framework ..............................................................................................................................................475.2 Recent empirical studies ............................................................................................................................................50

5.2.1 Studies based on R&D and patent data.............................................................................................................515.2.2 Studies based on surveys .....................................................................................................................................525.2.3 Studies based on patent citations analysis ........................................................................................................53

5.3 Open issues and directions for future research...................................................................................................546. A review of the methodology............................................................................................................................................54Bibliography .............................................................................................................................................................................59

3

1. Introduction

The aim of the SETI project is to investigate the impact of technological globalisation, thedevelopment and diffusion of Information and Communication Technologies (ICT) and therise of business services on national patterns of specialisation. Moreover, we are interested inassessing their impact on growth and employment potential in Europe. The interest for theseissues arises from a number of stylised facts. First, Europe is losing competitiveness in sectorswhere the rates of growth of innovation and demand have been faster. Second, the process ofinternationalisation of R&D appears to have been more marked in Europe with respect toJapan and the US and this raises the issue of the impact of this trend on European nationalsystems of innovation. Finally, the diffusion of ICT is producing an impact on the processesof internationalisation and the rise of business services. In this context we ask whether thepoor performance of Europe in the new technologies has contributed to the slowdown in thecatching-up process and the high rates of unemployment with respect to the US and what arethe future perspectives.

Different streams of literature are relevant for this project. First, there is a large literature onthe impact of technology on international specialisation. This literature is the starting point forthe development of the project. In this general framework we aim at assessing how the rise ofthe service sector, the internationalisation (globalisation) of technology, and the developmentand diffusion of ICT are shaping European specialisation patters. The phenomenon ofinternationalisation has been accompanied by the growth of particular activities within theservice sector and both trends have been favoured by the development of ICT.

Tertiarisation in a broad sense is not a new phenomenon, and the growth of the share ofemployment in the service sector follows a very long trend. Still the tertiarisation trendexperienced over the last two decades has some distinctive features, of which the mostmarked one is the unprecedented growth of business services over the last two decades. Thenew service sector mix very diverse types of activities, requiring different levels of skill. Thedevelopment of the highly qualified service activities in many new market niches is clearlylinked with the diffusion of ICT. This opens differentiated opportunities to different countries.The business services sector constitutes a new phenomenon, characteristic of a new set ofrelations between firms and this raises some new questions:

• How will different economies adjust to the broad organisational challenge with whichthey are confronted? And to what extent new organisational paradigms, linked to theincreasing role of services, will affect growth and employment performance at both theregional and national levels? Will, and to what extent, the process of internationalisationstrengthen the diffusion of new technology?

The role of manufacturing in overall growth of the developed countries has declined over thelast decades. Considering the increasing role of services as suppliers of high-quality inputsinto the manufacturing process one might be tempted to ask whether business services can bethe new engine of growth for the whole economy and how different economies will befavoured or hampered by this new phase of development. Because services are, by the strongpath-dependency of their development, very much country-specific, the emergence of a newgrowth regime is marked by national specificities, although one might have expected theopposite in times of increased internationalisation. In this context we want to investigatewhether there are interdependencies between national advantages in specific manufacturingsectors and the development of service activities. Anyway, the characters ofinternationalisation are different according to the types of sectors involved: this holds for

4

manufacturing and the service sector, as well as for the linkages between the two. Hence arelevant question is: • How the internationalisation and tertiarisation processes will differ across sectors? And

how existing specialisation patterns in Europe will affect future dynamics and constrainthe outcome?

In order to address these questions we will define a framework growth model where theeffects of specialisation, and innovation on growth and employment can be formally analysedand empirically tested along the lines already explored in Padoan (1998). Padoan (1998)presents an analytical description and an empirical estimation of a dynamic disequilibriummodel where equilibrium growth is made to depend upon the structure of specialisation aswell as on endogenous technological accumulation. A similar model can be developed inorder to analyse the relationship between innovation and employment creation at a sectorallevel. In this context it will be possible to formally analyse the relationship between growthand employment also within the service sector and the differences across countries.

The purpose of this review is to present the state of the art in different theoretical fields thatwill be integrated within the project. These are: the relationship between technology andspecialisation (Section 2); the process of tertiarisation (Section 3); the development anddiffusion of ICT (Section 4) and the internationalisation of technology (Section 5). Particularattention will also be devoted to the consequences of these new trends on growth andemployment opportunities. The review of the literature also aims at highlighting open issuesthat will be addressed in the development of the project. Finally, in the last section we reviewthe methodology that we intend to use in the quantitative part of the project. Figure 1.1summarises the various fields of literature relevant to the project and their interdependencies.

Figure 1.1 A summary of the streams of literature relevant to the SETI project

2. Technology and specialisation

This section focuses on technology-based theories of trade and specialisation. Section 2.1reviews the main theories and empirical evidence; Section 2.2 looks at the impact ofspecialisation on growth and international competitiveness; Section 2.3 examines the

Literature on the ICTrevolution (Section 4)

Literature ontechnology &specialisation(Section 2)

Literature on the rise ofbusiness services and theinternationalisation ofservices (Section 3)

Literature on theinternationalisation oftechnology (section 5)

Impact on growth and employment creation (all Sections)

5

relationship between specialisation and employment creation; finally, Section 2.4 emphasisesthe open questions and the directions for future research.

2.1 Technology and specialisation: theories and empirical evidence

The consideration of technology like a key determinant of country and sectorial tradeperformance has generated an impressive development of theoretical and empirical proposalsin the last years. Two themes in particular have received special attention in recent years:

• The first relates to the way in which technology enters as an explanation of the direction ofcountries’ trade specialisation.

• The second concerns to the characteristic traits of trade and technological specialisationpatterns of advanced countries: degree of stability, degree of concentration and trends toconvergence versus divergence over time.

Next, we present a brief description of the theoretical and the empirical literature around thesethemes. It is important to emphasise that almost all empirical research is confined to themanufacturing sector. This is a serious limitation if we agree with Laursen (2000, p. 12) that"private service sector makes up the same proposition of the economy as does manufacturingin many developed countries" and that "service sector is not only a growing sector indevelopment economies but also a more innovative sector in recent years".

2.1.1 The impact of technology on trade competitiveness and specialisation

Under the label of ‘technology gap theory’ Posner (1961) introduced the idea that temporarymonopoly profits can be appropriated, based on a technological lead, in an international tradecontext. Given the assumption that technology is not a free and universally available good,Posner argued that while technology might be important for trade in some sectors, and not inothers, innovations made in one country (in technology intensive sectors) would benefit thatcountry as long as the lead could be kept. That is, a country will have ample first-moveradvantages in a given sector, until other countries have imitated the innovation. Hence, in theoriginal formulation of Posner, once imitation has taken place, more traditional factors ofadjustment and specialisation would take over and determine trade flows. However, as arguedby Dosi and Soete (1988), there is not necessarily anything impermanent about theimportance of technology in determining trade flows, since static and dynamic scaleeconomies flowing from the initial break-through act to prolong the lead. Coupled with newproduct innovations, these scale economies might well secure a continuous trade flow. Aformalised neoclassical treatment of aspects of the idea is found in Krugman (1985). Metcalfeand Soete (1984) also observe that trade can be due to the difference between national rates ofdiffusion of demand and capacity growth and to time lags in technology transfer with respectboth to demand and production. While this type of trade should be transitory, it is possiblethat different diffusion patterns may result in different patterns of development within atechnology, thus affecting countries’ long-run comparative advantages. Overall studies usingthe technology-gap approach to trade emphasise inter-country differences in technical changeas the basis of international trade flows. In this framework it is variation across countries ininnovation capabilities within each sector, rather than inter-industry differences inendowments, which matters in explaining the direction of trade.

From an empirical point of view, the technology gap theory has gained support among othersfrom Soete (1981) and Dosi et al. (1990). Based on cross-country regression analysis, for asingle year, these two studies showed that among 40 sectors in about half of them

6

international competitiveness was influenced by technological advantages (measured as USpatents) in the same sector. From a panel data perspective, in a dynamic setting - and in anaggregate country perspective - Amendola et al. (1993) found convincing support for thehypothesis as well. Also applying panel data - and from a sectoral as well as a country-wiseperspective - Amable and Verspagen (1995) showed that competitiveness in trade wassignificantly influenced by technological capabilities (US patenting) in eleven out of theeighteen sectors in question, when using a dynamic specification of the model.

Given that the principal sources of technological change (inducement mechanisms) differbetween firms according to principal sector of activity, different explanations for trade shouldnot be expected to be of equal importance across industrial sectors. Thus, if tradespecialisation is determined to a large extent by technology, we should not expect theimportance of ‘technology’ to appear along the same dimensions. Some studies have used thePavitt taxonomy (1984) to identify the determinants of trade and specialisation distinguishingacross groups of sectors.

Using the Pavitt taxonomy and including as explanatory variables for market sharesinvestment, patents and unit labour costs, Amable and Verspagen (1995) find that there are anumber of cases where the results seem to support the taxonomy. However there are also anumber of cases where this is not true. Laursen and Meliciani (2000) also include somemeasures of forward and backward linkages and find support for the taxonomy. In particularthey find that, unit labour costs appear to play the largest role in supplier dominatedindustries, while ‘own sector’ technology (proxied by patents) plays the largest role in sciencebased industries. Upstream and downstream linkages are particularly important in determiningmarket shares in those industries which have important linkages with the others (scale

Box 2.1: The Pavitt taxonomyPavitt (1984) identifies differences in the importance of different sources of innovation according to whichbroad sector the individual firm belongs. The taxonomy of firms, according to principal activity, emergedout of a statistical analysis of more than 2000 post-war innovations in Britain and was explained by thesources of technology; the nature of users needs; and means of appropriation. Four types of firms wereidentified accordingly, namely supplier dominated firms, scale-intensive firms, specialised suppliers andscience-based firms. Supplier dominated firms are typically small and found in manufacturing and non-manufacturing sectors. Most technology comes from suppliers of equipment and material. Scale intensivefirms are found in bulk materials and assembly. Their internal sources of technology are productionengineering and R&D departments. External sources of technology include mainly interactive learning withspecialised suppliers, but also inputs from science-based firms are of some importance. Specialisedsuppliers are small firms, which are producers of production equipment and control instrumentation. Theirmain internal sources are primarily design and development. External sources are users (science-based andscale-intensive firms). Science based firms are found in the chemical and electronic sectors. Their maininternal sources of technology are internal R&D and production engineering. Important external sources oftechnology include universities, but also specialised suppliers. Even though the taxonomy was devised atthe level of the firm, it has implications at the level of the industry, as we would expect the broad sectoralregularities of firms to be reflected in the aggregate behaviour of the sector. Thus, given the abovedescription of the taxonomy, one would expect ‘own’ sector technology to be most important for gainingmarket shares in science based sectors, while downstream linkages should be expected to be moreimportant in the case of specialised suppliers. For scale intensive sectors inter-sectoral linkages - but also tosome extent R&D - should be of importance, while supplier dominated sectors should to some extent beexpected to be determined by upstream linkages and by low unit labour costs. The Pavitt taxonomy hasbeen criticised on a number of points, including a set of criticisms relating to the fact that the sectoralboundaries are not always straightforward. That is, firms (and sectors) cannot always easily be uniquelydefined as one of the four Pavitt type firms. Some firms (and sectors) may have such attributes, so that theycan be said to be affiliated to more than one of the Pavitt-type sectors.

7

intensive for upstream linkages and specialised suppliers for downstream linkages,respectively). Padoan (1998) also uses the Pavitt taxonomy to explain export and importshares in a dynamic model where knowledge accumulation affects trade performance andcompetitiveness but also trade enhance knowledge accumulation through imports. He findsthat the results are consistent with theoretical expectations about the importance of price andnon price determinants of trade performance in the four Pavitt’s macrosectors.

The technology-gap approach, in the most recent literature, has been used more often toexplain market shares rather than specialisation. Also the Pavitt taxonomy has been used inthis context with the aim of pointing out that different “factors of competitiveness” mightmatter more or less in different industries.

2.1.2 Trends in specialisation patterns

Taking into account the importance of technology like a key determinant of trade performanceand its principal microeconomic features, the empirical literature has also addressed thefollowing questions:

a) What is the degree of concentration of trade and technological specialisation patterns? Dothe countries tend to be more or less specialised over time?

b) What is the degree of similarity among specialisation patterns of advanced economies? Docountries converge or diverge in terms of specialisation patterns over time?

c) Are trade and technological specialisation patterns stable across countries and sectors?

Empirical studies do not show convincing conclusions in relation to the issue of the degree ofconcentration of each national pattern of specialisation. The findings of Amendola et al.(1992, 1998) show that in each country trade specialisation appears to be more concentratedthan technological specialisation, while the reverse is true in the work of Barcenilla (1999).Nevertheless, in the studies of Soete (1987), Archibugi and Pianta (1992a, 1992b), Amendolaet al. (1992, 1998) and Barcenilla (1999) there is a general consensus in the following result:smaller countries display a level of specialisation higher than big countries like Germany orFrance. This result reflects the fact that smaller countries need to reach a minimal dimensionin R&D and production to specialise in specific sectors. It is possible to notice a trend to de-specialisation in time that is evident in the trade field (Barcenilla, 1999; Laursen , 2000) andmore controversial in the technological field. Cantwell (1991) and Archibugi and Pianta(1992b) found an increase in technological specialisation. This is in contrast with the resultsof Barcenilla (1999) and Laursen (2000).

The issue of convergence is a major theme in economic research. General findings on thisissue show a clear economic or global convergence between advanced nations. The role oftechnology in this process is crucial, with innovations and product and process imitationleading to rapid diffusion of technical progress. Nevertheless, empirical studies ontechnological and trade specialisation have not reached clear conclusions.

The papers of Beelen and Verspagen (1994), Soete and Verspagen (1994), Barcenilla (1999)and Laursen (2000) show a tendency of trade specialisation patterns to converge, in contrastwith the findings of Wolff (1997) who recognises convergence in terms of factor endowmentsbut not in terms of patterns of specialisation. The results of Barcenilla (1999) show that theprocess of convergence is more evident in the technological than in the trade field. The

8

opposite is true in the findings of Archibugi and Pianta (1998) or Amendola et al. (1998) whoemphasise the existence of a paradox: a process of aggregate convergence is taking place withincreasing specialisation in selected technological niches by industrialised countries.

Finally, the hypothesis that national specialisation patterns evolve gradually and cumulativelyhas found great support in the empirical literature. It is especially true in the trade field. Theresults of Amendola et al. (1998), Barcenilla (1999) and Laursen (2000) confirm, in line withevolutionary theorising, that national export specialisation patterns are quite complex. Thestability of technological specialisation in the short and medium term is also recognised byPavitt (1988) and Cantwell (1989). However, the results of Barcenilla (1999) do not supportthe evolutionary hypothesis with respect to the technological field. Also Laursen (2000)specify that, in comparison, trade specialisation patterns are more stable than technologicalones. On this matter, Amendola et al. (1992) find that over long periods, the persistence oftechnological specialisation tends to fade away because of the emergence of newtechnological paradigms and new industries.

Recently, a study by Midelfart-Knarvik et al. (2000) has focussed on similar questionsadopting a different theoretical framework that draws both from factor-endowment and new-geography theories of specialisation. One of the merits of this study is that it considers alsosome service industries. The idea is that closer European integration is likely to bring with itmajor changes in industrial location. Industries will move to exploit differences in countries'comparative advantages. Moreover integration may change the attractiveness of central areasrelative to peripheral ones and may facilitate the clustering of activities that benefit fromlinkages with each other. The objectives of the study are to describe the changes in industriallocation that have occurred in Europe in recent decades; to establish whether these areassociated with countries’ economic structures becoming more or less similar, and industriesbecoming more or less spatially concentrated; to compare industrial location patterns inEurope and the US; and to identify the underlying forces that determine industrial locationand assess the extent to which these have changed in recent years. The authors find that:

a) Most European countries showed significant convergence of their industrial structureduring the 1970s, but this trend was reversed in the early 1980s. There has beensubstantial divergence from the early 1980s onwards, as countries have becomeincreasingly different from the average of the rest of the EU and, in bilateralcomparisons, from most of their EU partners.

b) The most dramatic changes in industry structure have been the expansion of relativelyhigh technology and high skill industries in Ireland and in Finland. However, thespecialisation process has occurred more generally, with nearly all countries showingincreasing difference from the early 1980s onwards.

c) Many, although not all, industries have experienced significant changes in theirlocation. In particular a number of industries that were initially spatially dispersed havebecome more concentrated. These are mainly slow growing and unskilled labourintensive industries whose relative contraction has been accompanied by spatialconcentration, usually in peripheral low wage economies. Amongst industries that wereinitially spatially concentrated, around half stayed concentrated. Significant dispersionhas occurred in a number of medium and high technology industries and in relativelyhigh growth sectors, with activity typically spreading out from the central Europeancountries.

9

d) Services are in general more dispersed than manufacturing. Two trends – the generalshift from manufacturing to services, and catch up by poorer countries with smallinitial services sectors – have reinforced this spatial dispersion of services.

e) While the industrial structures of EU countries are diverging, those of US states areconverging. However, in so far as it is possible to make any comparison of levels ofindustrial concentration between the EU and the US, they find that EU industries arestill less concentrated than are those in the US.

2.2 The impact of specialisation on international competitiveness and economic growth

Recently there has been a growing empirical literature on the relationship betweenspecialisation and trade and growth performance. This literature is very heterogeneous both inthe theoretical framework adopted and in the methodology. Moreover it mostly aims at testingsome ideas of various theoretical frameworks but it is rarely directly linked to any specificmodel. In other words the estimated equations are not, in most of the cases, reduced forms ofany specific theoretical model.

One way of looking at the impact of the different composition of national activities acrosssectors on countries’ trade performance has been the use of constant market share analysis.This approach aims at detecting to what degree the changes in the market share of a country inthe world market can be explained by the initial commodity composition of each country’sexports. In order to do so, it decomposes the overall change in market share into a structuraland a competitiveness component; the first effect is the difference between the hypotheticalshare had the single commodity shares remained constant at the initial commodity shares,while the second effect is the difference between the actual share and the hypothetical share.Most recent studies using constant market share analysis include Guerrieri and Milana (1995),Fagerberg (1996) and Laursen (1999). Guerrieri and Milana find that structural effectscontributed much to the remarkable gains in export shares achieved by Japan and the EastAsian NICs over the period 1973-90: these countries were able to improve their comparativeadvantage in high-technology goods as a whole and in particular in the field of electronics.Fagerberg finds that, between 1965 and 1990, trade in commodities with high R&Dexpenditures grew faster than other trade, and these changes were more favourable for thelarge and medium-sized high-income countries of the OECD area. Laursen, applying constantmarket share analysis to technology (patent data), finds that the catching-up countries (withthe exception of Japan) have been able to acquire market and technology shares despite their“wrong” specialisation pattern.

Other studies, within different theoretical frameworks, have directly analysed the impact ofthe degree and the “quality” of specialisation (either technological or trade specialisation) oncountries’ growth and trade performance. Table 2.1 summarises the main results emergingfrom these studies.

In a study directed at investigating the technological specialisation of the most advancedcountries, with no explicit theoretical claim, Archibugi and Pianta (1992b) made an attempt tocapture the effects of specialisation on growth, estimating an equation where growth inindustrial production is explained by specialisation in fast-growing patent classes, and anequation where it is related to the degree of specialisation (measured by the value of the Chi-squared statistics, a measure of concentration). They found no evidence of a significantrelationship between specialisation in the fast-growing patent classes and growth in industrial

10

production, while they found a strong link with the overall degree of specialisation. Theirresults suggest that there is a general advantage in being specialised that goes beyond thechoice of the more dynamic sectors. In a similar study, but using only correlation analysis,Pianta and Meliciani (1996) found a significant correlation between the degree oftechnological specialisation (measured by the value of the Chi-squared statistics) andcountries’ rates of growth. They also found that technological specialisation in electronics wasnot significantly correlated with countries’ rates of growth.

Table 2.1: The impact of specialisation on economic performance

Study Methodology Dependent variable Specialisation SignificantArchibugi and Pianta(1992b)

Pianta and Meliciani(1996)

Laursen (1999)

Dalum, Laursen andVerspagen (1999)

Amable (1996)

Pianta (1997)

Meliciani and Simonetti(1998)

Padoan (1998)

Meliciani (2001)

Regressionanalysis

Correlationanalysis

Regressionanalysis

Regressionanalysis

Regressionanalysis

Regressionanalysis

RegressionAnalysis

Regressionanalysis andsimulation

Regressionanalysis

Rate of growth ofindustrial production

Rate of growth of GDP

Rate of growth of exports

Sectoral growth of valueadded

Rate of growth of GDP

Rate of growth ofsectoral technologyRate of growth ofsectoral productionRate of growth ofsectoral exports

Rate of growth of GDP

Rate of growth of GDP,export and import shares

Rate of growth of GDP,export and import shares

Specialisation in fast growingpatent classesDegree of technologicalspecialisation

Technological specialisation inelectronics

Structural technology effectTechnology adaptation effectStructural market effect

Specialisation for each of thesector product groups

Inter-industry trade specialisationindexTrade specialisation in electronics

Technological specialisation inthe same sectorProduction specialisation in thesame sectorTrade specialisation in the samesector

Specialisation in fast growingpatent classesSpecialisation in ICT

Sectoral approach

Specialisation in fast-growingpatent classes

No

Yes

No

NoYesYes

Yes

Yes

Yes

No

No

No

Yes

Yes

Yes

Yes

Laursen (1999) estimates a technology-gap model of international competitiveness wheretechnological opportunity is assumed to affect countries’ ability to compete in internationalmarkets: assuming that technology is an important determinant of export growth, it can beexpected that countries which have access to sectors (or activities) offering high (low) levelsof technological opportunity will benefit from higher (lower) international demand. Withinthis framework, changes in trade performance are explained in terms of changes in unit labour

11

costs, investment, catching-up, a structural market effect (the advantage coming from beinginitially specialised in the classes that grew more in terms of exports), a structural technologyeffect (the advantage coming from being initially specialised in the classes that grew more interms of patents) and a technology adaptation effect (the ability to move actively into thetechnological sectors with above-average rates of growth). The results give no support for thestructural technology effect to have an impact on market shares, while a significant effect isfound for the technology growth adaptation effect and the structural market effect. Laursencomments on the results by stating that ‘it appears to be more important for national systemsof innovation to actively move into sectors offering above average technological opportunity,rather than being “fortunately” specialised initially’ (Laursen, 1999, p. 18).

Dalum, Laursen and Verspagen (1999) explore the relationship between specialisation andgrowth, arguing that this can be justified on the grounds of both supply-side elements(specialisation leads to higher productivity growth in the form of learning, and to the extent towhich different sectors or activities are characterised by different learning opportunitiesdifferent specialisation patterns can offer different growth opportunities) and demand-sideelements (Engel’s law, or the idea that as income rises demand for some goods grow morerapidly than for other goods). The supply-side elements are discussed in both the new growththeory and the evolutionary approach, while the demand-side arguments are characteristic ofthe post-keynesian and the evolutionary approaches. Dalum, Laursen and Verspagen do notcommit to any of the specific modelling environments proposed by the theories; rather theirapproach is based on a combination of certain elements of all theoretical frameworksdiscussed above.

In order to test the hypothesis that the structure of an economy matters for economic growth,they run a regression with the sectoral growth of value added as the dependent variable, andseveral variables (the growth rate of employment, the investment-output ratio, the number ofpatents granted in the US per employee, and the ratio of value added per employee relative tothe maximum level for the sector, as a measure of the scope for catching-up) together with ameasure of specialisation, as explanatory variables for a sample of OECD countries over theperiod 1965-88. The specialisation variable is computed as the revealed comparativeadvantage (RCA) for each of the sectors’ product groups; however owing to the large numberof product groups within some sectors they include in the regression only up to three of theprincipal components. The results for the specialisation variable show that, for all sectors buttextiles and basic metals, there is at least one, but often more, principal component for eachtime period (the time periods are 1965-1973, 1973-1979 and 1979-1988) that is significant.Over time the number of sectors where specialisation is significant appears to decrease.Looking at which activities have had a positive impact on growth, they find some unexpectedresults (for example that specialisation in semiconductors turns out to have had a negativeimpact on the rate of growth of the electrical goods sector in spite of high growth of trade insemiconductors). They conclude that a complex set of interacting supply and demand sidefactors can lead to unpredictable results as to which activities offer better opportunities forgrowth. Finally they also find that specialisation in some product groups has different impactson growth over time (positive or negative), and therefore policies aimed at changing thespecialisation patterns of the economy are risky and difficult to implement. Overall this studygives support to the view that specialisation can have an impact on growth, but fails toidentify some characteristics within the different product groups that can be beneficial ordetrimental to the growth process (it gives an ex post account of which product groupscontributed positively to sectoral growth with no ex ante explanation).

12

Amable (1996) refers to the work of Grossman and Helpman (1991), Rivera Batiz and Romer(1991), Lucas (1988), Young (1991) and Matsuyama (1992) as theoretical models where tradeaffects economic growth. In the first two studies the exchange of technical information, thediffusion of knowledge, scale effects and the differentiation of innovations (the consequenceof preventing duplication in research) act to enhance technical change, productivity and/orconsumers’ utility. In these models therefore it is the opening up of trade with the resultingprocess of specialisation that can be beneficial for growth, independently from the sectors inwhich countries specialise. In the other studies not every effect of international trade isnecessarily beneficial to growth. If international specialisation diverts a country fromtechnology-intensive industries, the opening up of trade can have a negative effect oncountries’ rates of growth. Referring to these streams of literature, Amable estimates anequation where growth depends on catching-up, education, investment and some measures ofspecialisation, in a sample of OECD as well as some Asian and Latin American countriesover the period 1960-90 (panel data). He uses three different measures of trade specialisation:inter-industry specialisation, a trade dissimilarity indicator, and an indicator of comparativeadvantage in electronics. The inter-industry specialisation index (Michaely index) is high if acountry’s trade structure is characterised by the coexistence of clearly defined export andimport industries, irrespective of the aggregate trade surplus: the higher the index the moretrade balances are dissimilar between industries, i.e. the higher is specialisation. The tradedissimilarity indicator measures the dissimilarity between a country’s trade pattern andinternational demand patterns: it is higher when a country exports commodities in an industrywhere international demand is relatively low. Its effect on growth is therefore expected to benegative. Considering that electronics has enjoyed fast rates of technological progress and hashad pervasive effects throughout most industry and service activities, specialisation inelectronics is expected to have a positive effect on economic growth. He finds a positiveeffect of inter-industry specialisation and also of specialisation in electronics, concluding thatthe positive influence of inter-industry specialisation does not mean that all patterns ofspecialisation are equivalent. On the contrary, countries specialised in electronics appear tohave experienced above-average rates of growth, and this lends some support to the view thatelectronics is a ‘strategic’ branch of activity.

Pianta (1997) investigates whether growth in technology, production and exports is higher inthe sectors where countries show stronger specialisation (measured by comparativeadvantage). He finds for a pooled sample of the six largest OECD countries (US, Japan,Germany, France, UK, and Italy) and 19 sectors, between the 1980s and the 1990s, thatnational sectoral performances in either production, export or patenting are negatively relatedto existing specialisation patterns. He concludes by stating that a sort of ‘decreasing returns’to specialisation appear to emerge that are at odds with the view of increasing benefits fromcomparative advantage: the presence of relative strengths within some sectors do not lead tohigher rates of growth within the same sectors either in technology, or in production andexports.

Meliciani and Simonetti (1998) look at the impact of specialisation in fast-growing patentfields and in ICT on economic growth, also controlling for the investment activity and theoverall technological intensity of the countries. They find that specialisation in ICT has apositive and significant impact on GDP growth over the whole period (70-93), whilespecialisation is fast-growing patent fields becomes significant only from the 1980s. Theyexplain this result considering that in the ‘70s many fast growing technology fields were stilllinked to the old technological paradigm, while the ICT paradigm becomes dominant startingfrom the 1980s.

13

Padoan (1998) estimates a dynamic disequilibrium model focused on trade specialisation andknowledge accumulation. The sectoral breakdown follows Pavitt taxonomy by groupingmanufacturing goods into four macrosectors. The empirical estimation shows the importanceof both price and non-price determinants of trade. Moreover simulation exercises confirmsteady state results on the relevance of country differences in trade specialisation and indomestic knowledge accumulation in affecting growth and they also clarify the relationshipbetween growth and changes in the structure of trade specialisation.

Meliciani (2001; 2002) looks at the impact of specialisation in fast-growing patent field oneconomic growth through the balance of payments. She finds that countries specialised infast-growing fields experience above average growth in export shares and below averagegrowth in import shares, with an overall positive impact on GDP growth through the balanceof payments.

Overall the empirical evidence on the importance of specialisation for internationalcompetitiveness and growth is controversial. While most studies find a link betweenspecialisation and growth and trade performance, there is no clear evidence whetherspecialisation matters per se, due to increasing returns, or if there are activities that offerbetter opportunities for growth. The rising importance of ICT, particularly over the 1980s, hasto be taken into account in order to understand the performance of different countries intechnology, trade and production. This can be an explanation for the limitations ofspecialisation per se to offer high growth opportunities in the more recent period.

2.3 Specialisation and employment creation

The debate on the effect of technological change on unemployment focuses on the labour-saving impact of process innovations and on the capability of the system to compensate theinitial displacement. Whereas the labour-saving effects of process innovations are only partlycompensated elsewhere in the system, by most of the various compensation mechanisms, thejob creation effects of product innovations can be very substantial and have a powerfulcompensating impact. To the extent therefore that the profits from labour saving processinnovation are subsequently channelled, directly or indirectly, into the development of newproducts and services, this provides the best possibility to generate new employment. This hasbeen particularly evident both in the US and in East Asia, but clearly Europe has not benefitedso much from this mechanism (Vivarelli, 1995). The job-creating and job-replacing effects oftechnical change have to be investigated in order to understand whether the sectors wheremore technological accumulation is taking place are also the fields where production andemployment grow.

The debate over the microeconomic causes of unemployment (or of equilibriumunemployment) largely ignores product composition even though this could be quite relevantfor determining equilibrium unemployment and its evolution over time. This point can beclarified by considering labour demand and supply effects. To the extent that labour demandis determined by product demand, the sectorial product composition affects demand for laboursince different products or sectors display different rates of growth of demand. The referencescommonly found in the literature relate to the distinction between mature and new productsand between industrial and service products. The demand for labour should grow faster innew sectors and in services. The available evidence confirms that the larger growth-elasticityof employment is found in services (in Europe as well as in the US) even though in the lattercase the growth elasticity of employment is high even in the manufacturing sector. On theother hand, as shown in the literature on endogenous growth and on the service economy, a

14

well developed advanced service sector generates positive externalities for the industrialsector. In the second place, given that productivity growth in services is lower than inindustry, the employment content of growth is enhanced by a higher share of services inoutput. A service orientation of employment has been under way for some time in theindustrialised economies at approximately the same rate as that of the share of value added inindustry and services (Baumol, Blackman, Wolff, 1989).

Product composition matters in determining the position and the evolution over time of thedemand for labour; however, the technological intensity for a given sectorial composition isalso relevant. It is not obvious that sectors of high demand growth or high technologicalinnovation are also those with the greatest growth of employment. As shown in Padoan(2000) the employment trend is worse in the so-called traditional sectors, and some of thehigh technology sectors display the best employment performance. The sectorial employmentdynamic within the manufacturing sector is highly variable, while the sector's overall trend isnegative. The main implication is that the production specialisation of a country and itsevolution are relevant for structural unemployment. This is another element of diversificationamong European countries (and regions).

The above considerations make it difficult to evaluate the role of the so-called technologicalcomponent of unemployment, i.e., whether the introduction of technology intensive products -which, per se, diminishes employment per unit - offsets the greater absolute employmentcreated by larger output. Available empirical evidence seems to confirm that employmentgrowth tends to be positive, or at least more sustained, in high-tech sectors. Moreover, there isevidence of a positive relation between innovation effort - as measured in terms of R&Dexpenditure as well as patenting - and employment. Of course, employment growth inducedby technological innovation will be possible to the extent that an adequate, highly trained,labour force will be available i.e., to the extent that a recomposition of labour demand ismatched by a recomposition of supply.

The dynamics of world demand are frequently associated with traditional (or mature) sectorswith low growth rates of demand, and innovative segments (often those with a high valueadded) with high growth rates (European Commission, 1998). Nevertheless, several studiesoffer a more complex picture. In a longer time-horizon we can discard cyclical componentsand concentrate the growth of international trade volumes (exports and imports of the mainOECD countries) as reference. We note that some medium-to-high-added-value sectors haveshown percentage growth rates lower than the industrial average in 1980-94 (and in 1970-94);this is the case of the petrochemical and steel segments, construction materials and food &beverages. On the other hand, trade volume have grown at a sustained pace in "traditional"segments such as furniture, footwear and clothing, in addition - as is to be expected - tochemistry (including pharmaceutics), machinery (including computers, consumer electronicsand telecommunications) and vehicles. Thus, the equation "traditional equals static" is notalways valid. This can help explain the relative employment creation performance ofsegments such as furniture, but it runs up against tangibly negative employment data in othertraditional sectors (even in those with sustained trade growth).

Several studies allow to classify the industrial sectors on the basis of a few parameters such asmarket concentration, the share of the factors of production in value added, returns to scale,intensity of R&D, and the number of patents (Davies and Lyons, 1996; OECD, 1996). A firstgroup of sectors with high R&D and skilled-labour intensity is also associated with high ratesof growth of world demand (computers, telecommunications, other chemicals and somesegments of the transport equipment). Among the capital-intensive sectors, we must

15

distinguish between skilled labour intensive ones (food, motor vehicles) and those whichemploy mostly unskilled labour (textiles, steel, glass, rubber and plastics). Finally, we canidentify sectors, respectively of high skilled-labour intensity (machinery, professionalinstruments, electrical equipment) and unskilled-labour intensity (clothing, furniture, leather,some metal products). In the high-tech and high added-value sectors, Europe as a wholedisplays a low "quality" of production specialisation, i.e., ability of generating value addedand of rewarding factors of production with high returns. While, in fact, only the US andJapan are specialised, respectively, in computers and telecommunications equipment both arealso specialised in vehicles (together with Germany and Spain), some EU countries arespecialised in chemicals (including Germany, France, UK and Netherlands) and in industrialmachinery (Germany, France, Italy, UK, Sweden and the Netherlands). Europe's limitedpresence in the high-tech sectors should be ascribed to a generally modest intensity of R&D inmany European countries (excluding Scandinavia, as well as non-EU Switzerland), measuredboth by low input levels of R&D and low output levels of patents.

2.4 Open questions and directions for future research

The literature reviewed so far is almost entirely confined to the manufacturing sector (oneexception is the paper by Midelfart-Knarvik et al.). This is a serious limitation when we wantto examine the impact of specialisation on growth and employment creation, especially inindustrialised countries. In fact in the EU services as a whole account for approaching two-thirds of output and employment. Moreover the development of new technologies have madethe manufacturing and the service sector much more interdependent. In particular services(especially business services) are playing an increasing role as suppliers of high-quality inputsinto the manufacturing process. Similarly the presence of delivery services can impact on theproductivity of manufacturing to the extent that services supply intermediate inputs to themanufacturing process. Finally the close interaction between many service activities and otherparts of the economy makes them potentially important conduits for the spread of newtechnologies, the diffusion of new knowledge and the promotion of organisational change.

We can therefore ask the questions: how is the rise of services affecting countriesspecialisation patterns? And what are the links between advanced services and manufactures?The ability to develop or adopt the new technologies in one country - to the extent that itaffects the development of high-quality business services - has not only a direct impact onnational specialisation in the manufacturing sector. It also has an indirect effect through theinterdependencies between the manufacturing and the service sector. This set of issues will beemphasised in Section 3.

The literature on technology and specialisation has also mostly ignored the issue of theinternationalisation (globalisation) of technology. The lack of interest in the location oftechnological activity by Multinational Enterprises (MNEs) can be attributed to thewidespread belief that MNEs were concentrating innovation activity in their home country.While this could be the case until recently, in the past decade the significance of theinternationalisation of R&D activities of MNEs has been growing. Moreover European firms,especially from small countries, have shown historically a higher tendency, with respect toAmerican firms, to conduct both production and innovation activities abroad.

The impact of these trends on national performance and, in particular, whether technologicalglobalisation has weakened the links between a country’s knowledge base and its trade,growth and employment performance is a controversial issue. Section 5 will focus on theoriesand empirical evidence concerning the globalisation of technology.

16

The processes of transformation that we have emphasised (the rise of business services andthe globalisation of technology) are strongly affected by the development and diffusion ofICT. Technological developments in telecommunications and information technology haveboosted the potential of many producer services. Also the internationalisation of services hastaken a major leap in the last two decades due to the revolution in ICT industries. MoreoverICT have a direct impact on countries’ specialisation patterns and growth and employmentperformance. Section 4 will deal with the most relevant issues raised by the diffusion of ICT.

3. Services

In developed countries the services sector has become increasingly important over the lastcouple of decades. In the EU services as a whole account for approaching two-thirds of outputand employment; for market services the share of output is close to 50%. Initially the growingimportance of services was met with concern since the services sector exhibits relatively lowproductivity growth. The expansion of services could well attract labour away from relativelyhigh growth manufacturing sectors into low-growth services industries. As a result, this trendwould lead to a reduction in economic growth. By contrast, more recently many have come tothe believe that there is something very positive about the growing importance of services orat least some groups of services. They put great emphasis on the role of producer servicesgenerally and information and communications technology (ICT) in particular. However todate there has been relatively little research, especially on the empirical side, that analyses thedifferential impact of individual services on economic growth.

The aim of this section is to provide a review of the literature on the economics of services,and in particular the internationalisation of services, as a contribution to the wider literaturereview. Not only has the relative importance of services in domestic production increased, butalso it has become increasingly clear that services are not as non-tradable as had beengenerally assumed. Even though this may never have been a very appropriate assumption, theinternationalisation of services has taken a major leap in the last two decades due to therevolution in ICT industries and the trend towards deregulation in domestic markets.Throughout the section special attention is given where possible to three key servicesindustries: distribution, management consulting and financial services.

The section is structured as follows. In Section 3.1 some concepts and definitions related tothe nature of services as well as to the internationalisation of services will be discussed. InSection 3.2 the recent developments in the internationalisation of services will be analysed.Section 3.3 reviews the regulatory environment for services both in the context of the EU andin the WTO. Section 3.4 examines how specialisation in services and the internationalisationof services affect economic growth and employment. Finally Section 3.5 discusses some openissues and directions for future research.

3.1 What are services?This section discusses first a number of concepts and issues related to the nature of services.Secondly, concepts related to the internationalisation of services will be examined.

3.1.1 Services versus goodsServices have long been defined negatively as all economic activities whose output is neitheragricultural nor a manufactured product. In a now classic study Fuchs (1968) tried to pindown the nature of services. Fuchs defines services on the basis of three key features. Thefirst feature that distinguishes services from goods resides in the non-storable nature of

17

services. As a result services have to be produced and consumed in the same place and at thesame time (generally referred to as the ‘physical proximity requirement’). Bhagwati (1984)and others have noted that due to the technological developments in telecommunications andinformation technology services the physical proximity requirement in the delivery of servicesmay have been reduced.1 However, the scope of separating receivers and providersgeographically may be limited due to the intangible nature of services, the second featureemphasised by Fuchs. Factor services are not as in manufactures employed to producephysical outputs, but factors instead produce intangible assets. Consequently, problems ofasymmetric information may arise as it is impossible to assess the quality of the service priorto purchase. Building a reputation is crucial to the strategy of services providers. Creatingtrust requires establishing long-term relationships which are importantly shaped by personalcontacts. The intangibility of services explains therefore the path-dependence thatcharacterises many service industries. Third, not only are services generally produced wherethey are consumed but they are also produced with the participation of the consumer, that is,services tend to be customised. Both intangibility and customisation tend to reinforce the‘physical proximity requirement’.

Hill (1977, p. 317-318) proposes a truly general definition distinguishing services from goods.“A good may be defined as a physical object which is appropriable and therefore transferablebetween economic units. A service – on the contrary – may be defined as a change in thecondition of a person, or of a good belonging to some economic unit, which is brought aboutas a result of the activity of some other economic unit, with agreement of the former person oreconomic unit”. According to this definition services are no longer considered as immaterialgoods, but are different in essence by being a change (Siniscalco, 1988). 2

More recently researchers seem to have abandoned the goal of defining services generally,instead they tend to adopt a more pragmatic approach acknowledging that the services sectorcomprises an extremely diverse set of economic activities. More attention is now directedtowards developing sensible classifications that allow one to answer more specific questions.

3.1.2 The internationalisation of servicesSampson and Snape (1985) argue that a definition based on geography as is used for goods, isnot appropriate, because this would exclude, for example, tourism. Indeed, they defineinternational transactions of services as ‘a transaction between the resident of one country anda resident of another’ (p. 172). However, this definition excludes for example foreignstudents. University students often spend one or more years abroad for study purposes and assuch become residents of the country of study. A more appropriate definition should thereforebe based on nationality. 3 Sapir and Winter (1994) implicitly acknowledge this as they includemigration and consequently argue that migration policy can constitute a barrier to trade.

The most common typology of international transactions in services is based on the analysisof movement of users and providers respectively that occurs for the transaction to take place

1 Bhagwati (1984) call this the ‘disembodiment effect’.2 For the measurement of services output Hill’s definition implies that one should focus on the change in thereceiver, which corresponds more to value-added than gross services output (Siniscalco, 1988). Weiss argues inresponse to Siniscalco that the challenge is to construct sound price indices as the value of the change incondition to the receiver is reflected in its price.3 Sampson and Snape’s definition however corresponds well to the existing balance of payments (BOP) statisticsas BOP statistics register transactions between residents and non-residents. A definition based on nationality,that is one that distinguishes between ‘foreign’ and ‘national’ residents is theoretically more appropriate, butpractically impossible to work with. However, analysis of the impact of GATS for example requires such data.

18

(Sampson and Snape, 1985; Sapir and Winter, 1994). This typology also provides the four‘modes of supply’ employed in the GATS.

Type 1 Neither the user nor the provider moves, but both reside in different countries. This isthe case to which Bhagwati (1984) referred. Trade in services of this type is similarto trade in goods. For this reason it is also called commodity trade. This type of tradein services is likely to arise in financial services (and some professional services).

Type 2 The user moves to the provider to receive the service. This the case in for exampletourism and education, but is not likely to be important for the three industries ofinterest in this paper. This is also called commodity trade.

Type 3 The provider moves to the user in order to perform the service. This type is referred toas factor trade (Ruane, 1990). This could be important for both financial andconsulting services if physical interaction is required but not on a regular basis.

Type 4 The provider establishes a foreign branch in order to obtain physical proximity tousers abroad. This is probably the most common type of internationalisation ofservices. It is important for banking, consultancy and distribution.

The first three types of transactions are generally referred to as trade, whereas type 4 involvesthe permanent movement of capital and possibly also labour. Theoretical models of trade inproducer services are proposed by Markusen (1989), Melvin (1989), Francois (1990a and b)Jones and Ruane (1990), Van Marrewijk et el. (1997), De Vaal and Van de Berg (1999).Models of the latter type by Van Marrewijk et al. (1996), and Markusen, Rutherford, and Tarr(2000).

Type 4 leads to the establishment of multinational service networks. Whereas internationalfragmentation of production in manufacturing is most often motivated by cost considerationsand market access, for services the ‘physical proximity requirement’ seems to be thepredominant consideration. Therefore, one may label such services providers as deliveryservices. Intuitively, it seems that service providers are more likely to establish several foreignaffiliates within a single country than for manufacturers.

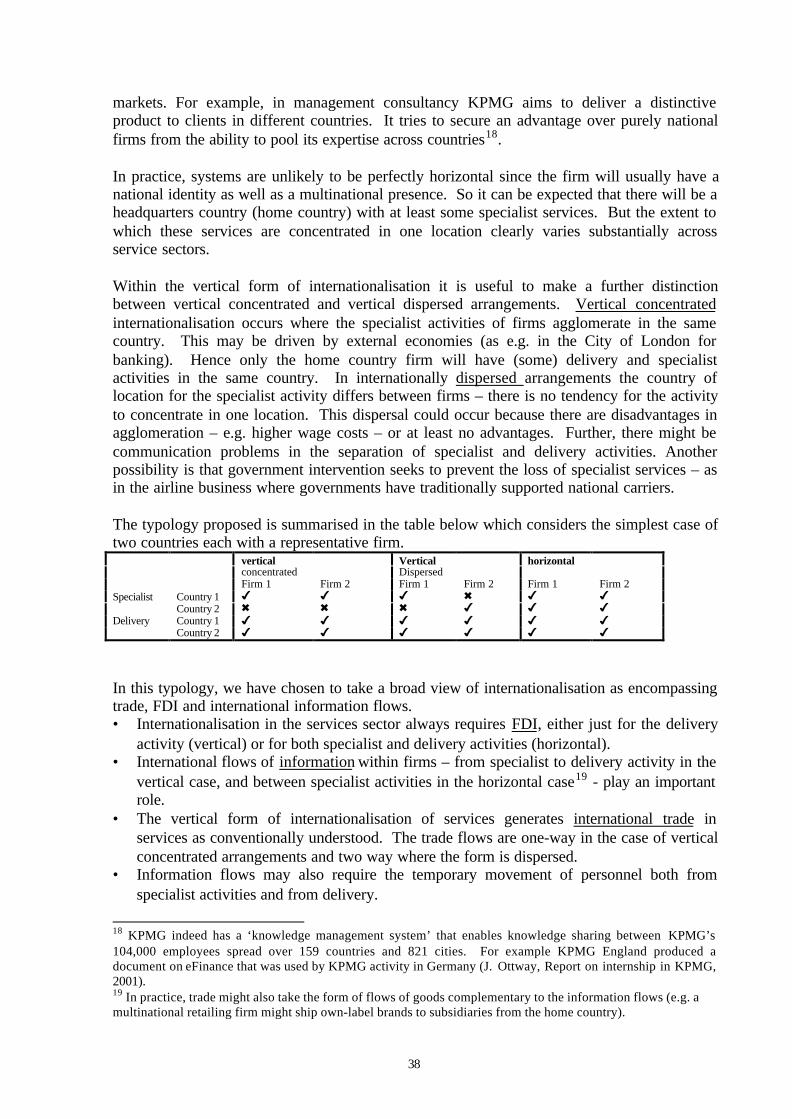

For some services activities, those where economies of scale are particularly important andphysical proximity may not be regularly required, it may be justified to concentrate them inone location. Such services could be called specialist or headquarter services. Specialistservice activities are like to include management, marketing and product development.

Given those two types of services the internationalisation of services may take two forms.First, vertical fragmentation refers to the international fragmentation of the integratedactivities according to their different functions, that is, delivery and specialist activities tend tobe separated geographically (Markusen, 1984). Second, horizontal fragmentation refers to thecase where delivery and specialist services are located within the same country. Therevolution in telecommunications especially is likely to promote the establishment ofvertically fragmented networks as the intra-firm flow of information tends to be the moreintensive in such networks. However, the extent of vertical fragmentation may be very limitedas a result of diverging regulatory environment. Harmonisation in the EU may have affectedthe form of internationalisation, encouraging a further concentration of specialist services(form the national to the European level).

Within the vertical form of international fragmentation it is possible to distinguish betweenvertically concentrated and vertically dispersed organisational structures. The former refers to

19

the case where specialist activities tend to be located within agglomerations and the latterwhere specialist activities are dispersed. Their location may be based on history.

Similarly it may be useful to analyse the impact of the presence of delivery services on theproductivity of manufacturing to the extent that services supply intermediate inputs to themanufacturing process. Further, do services follow manufacturers (Sapir, 1988) or aremanufacturers attracted by advanced services infrastructure?4

In addition to the commonly used typology based on international transactions, this sectionthus introduces a new functional typology which may help to analyse in more detail type 4 ofinternationalisation in services viz:

vertical fragmentation (concentrated)vertical fragmentation (dispersed)horizontal fragmentation

3.2 Trends in servicesIn this section the extent of the internationalisation of services is analysed. Ideally, one wouldconsider trade in services (types 1 to 3), foreign direct investment in services, and migrationrelated to the internationalisation of services (type 4). Data on migration with the aim ofsupplying or receiving a service is not available.5 Only recently have statistical offices startedcollecting FDI data that distinguish between services and manufacturing. Disaggregated FDIdata distinguishing different services sectors is available only for the United States. Thereview deals first with trade in services followed by FDI in services.

3.2.1 Trade in servicesTrade in services is measured according to the residential definition of internationaltransactions. As a result international trade between ‘foreign’ and ‘national’ residents of thesame country is omitted. Non-residents become residents if they reside in the country for oneyear or more. Trade in services in this section only approximates to types 1-3, thusunderestimating the extent of internationalisation in services.

Empirical research on trade in services is quite limited, not least because of the availabilityand quality of statistics of trade in services. Some have employed production and employmentdata in order to make inferences regarding the pattern of specialisation in a way to bypass datalimitations on trade. However, it seems that such measures differ importantly from trade-based indices.

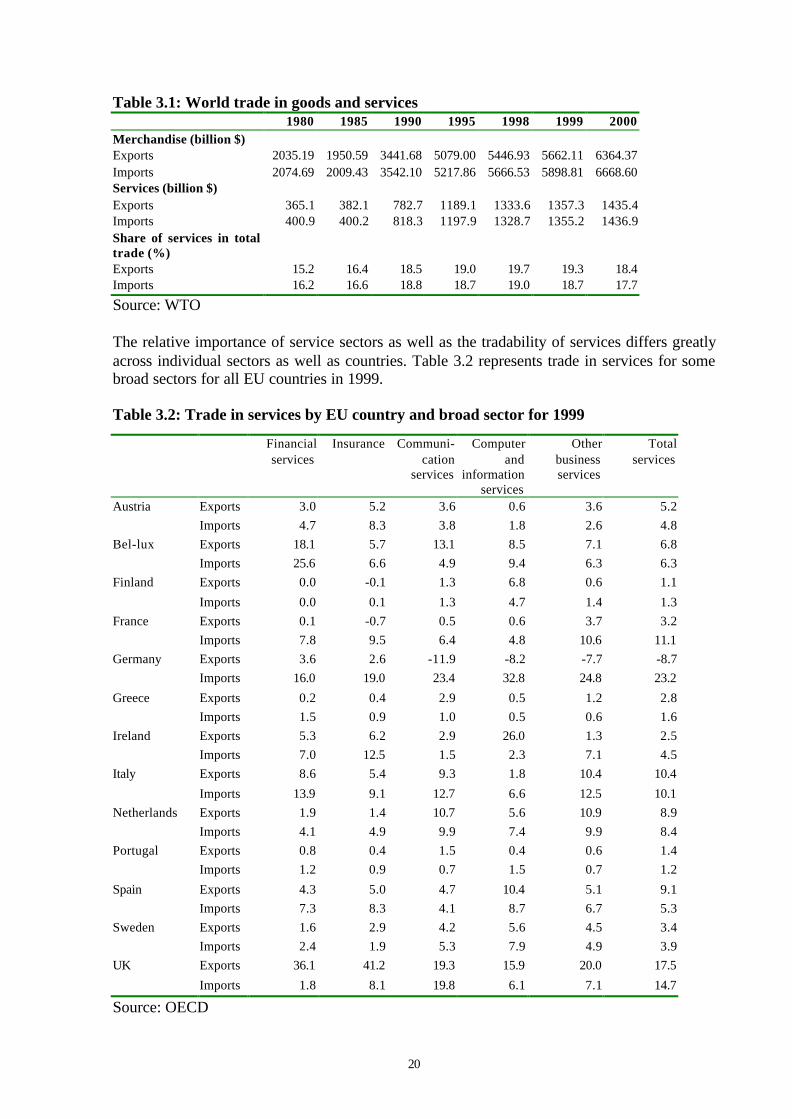

Table 3.1 compares trade in goods with trade in services. The first point to be noted is thattrade in services is much smaller than trade in goods. Nevertheless for a supposedly non-tradable sector the share of services in world trade is rather about 15% to 20%. Moreover, thetable shows that services have gained in relative importance from 15.2% of exports in 1980(16.2% of imports) to 18.4% of total exports in 2000 (17.7% of total imports). These sharestend be somewhat higher in developed countries and slightly lower in developing countries.

4 Gross, Raff, and Ryan (2001) find evidence for the former in the early years of Japanese FDI in Europe, butobserve that the picture is completely reversed in more recent years.5 Although not very satisfactory Chang et al. (1999) use BOP category ‘compensation for employees’ whichregisters “the earnings of all natural persons established abroad for less than one year (p. 112)”.

20

Table 3.1: World trade in goods and services1980 1985 1990 1995 1998 1999 2000

Merchandise (billion $)Exports 2035.19 1950.59 3441.68 5079.00 5446.93 5662.11 6364.37Imports 2074.69 2009.43 3542.10 5217.86 5666.53 5898.81 6668.60Services (billion $)Exports 365.1 382.1 782.7 1189.1 1333.6 1357.3 1435.4Imports 400.9 400.2 818.3 1197.9 1328.7 1355.2 1436.9Share of services in totaltrade (%)Exports 15.2 16.4 18.5 19.0 19.7 19.3 18.4Imports 16.2 16.6 18.8 18.7 19.0 18.7 17.7

Source: WTO

The relative importance of service sectors as well as the tradability of services differs greatlyacross individual sectors as well as countries. Table 3.2 represents trade in services for somebroad sectors for all EU countries in 1999.

Table 3.2: Trade in services by EU country and broad sector for 1999

Financialservices

Insurance Communi-cation

services

Computerand

informationservices

Otherbusinessservices

Totalservices

Austria Exports 3.0 5.2 3.6 0.6 3.6 5.2

Imports 4.7 8.3 3.8 1.8 2.6 4.8

Bel-lux Exports 18.1 5.7 13.1 8.5 7.1 6.8

Imports 25.6 6.6 4.9 9.4 6.3 6.3

Finland Exports 0.0 -0.1 1.3 6.8 0.6 1.1

Imports 0.0 0.1 1.3 4.7 1.4 1.3

France Exports 0.1 -0.7 0.5 0.6 3.7 3.2

Imports 7.8 9.5 6.4 4.8 10.6 11.1

Germany Exports 3.6 2.6 -11.9 -8.2 -7.7 -8.7

Imports 16.0 19.0 23.4 32.8 24.8 23.2

Greece Exports 0.2 0.4 2.9 0.5 1.2 2.8

Imports 1.5 0.9 1.0 0.5 0.6 1.6

Ireland Exports 5.3 6.2 2.9 26.0 1.3 2.5

Imports 7.0 12.5 1.5 2.3 7.1 4.5

Italy Exports 8.6 5.4 9.3 1.8 10.4 10.4

Imports 13.9 9.1 12.7 6.6 12.5 10.1

Netherlands Exports 1.9 1.4 10.7 5.6 10.9 8.9

Imports 4.1 4.9 9.9 7.4 9.9 8.4

Portugal Exports 0.8 0.4 1.5 0.4 0.6 1.4

Imports 1.2 0.9 0.7 1.5 0.7 1.2

Spain Exports 4.3 5.0 4.7 10.4 5.1 9.1

Imports 7.3 8.3 4.1 8.7 6.7 5.3

Sweden Exports 1.6 2.9 4.2 5.6 4.5 3.4

Imports 2.4 1.9 5.3 7.9 4.9 3.9

UK Exports 36.1 41.2 19.3 15.9 20.0 17.5

Imports 1.8 8.1 19.8 6.1 7.1 14.7

Source: OECD

21

Comparing imports and exports for the different countries, Germany and France have largetrade deficits in services revealing that their comparative advantage is still in manufacturing.By contrast, Spain, Greece and the UK run a trade surplus on services revealing a comparativeadvantage in services. However, for individual services sectors the picture differs importantly.Spain and Greece derive their comparative advantage in services from consumer services,especially tourism, whereas the United Kingdom’s comparative advantage is largely based onproducer services. Germany and France are large net importers of producer services.Elsewhere patterns of services activity are quite diverse.Financial services and insurance exhibit a similar pattern. The United Kingdom is the onlycountry with a strong trade surplus in these services sectors, while all others EU countries runa deficit. This may reflect the role of US and Japanese financial services firms within the EU. 6

Belgium-Luxembourg, Greece, Ireland, and Portugal are net exporters of communicationsservices, whereas France, Germany and Italy are net importers. This suggests an importantrole for country size in communications services. In computer services Ireland and the UnitedKingdom run notable trade surpluses. The category ‘other business services’ contains adiverse range of service activities. Broadly speaking, it consists of merchanting and traderelated services and miscellaneous business, professional and technical services. The lattergroup (consulting in a broad sense) represents more than 90% ‘of other business services’ inthe United Kingdom. Interestingly, Ireland appears to be a strong importer of other businessservices. Possibly, the dynamism of the Irish economy is reflected by the high demand forbusiness services. Alternatively, it could reflect the use of home service providers by foreignaffiliates in Ireland.

Disaggregated data for the world as whole are not available. Chang et al. (1999) estimatethem. Their results for 1996 reveal that transport and travel largely dominate global trade inservices, together accounting for 58% of total services trade. Financial and insurance servicesaccount for about a fifth of the remainder.7

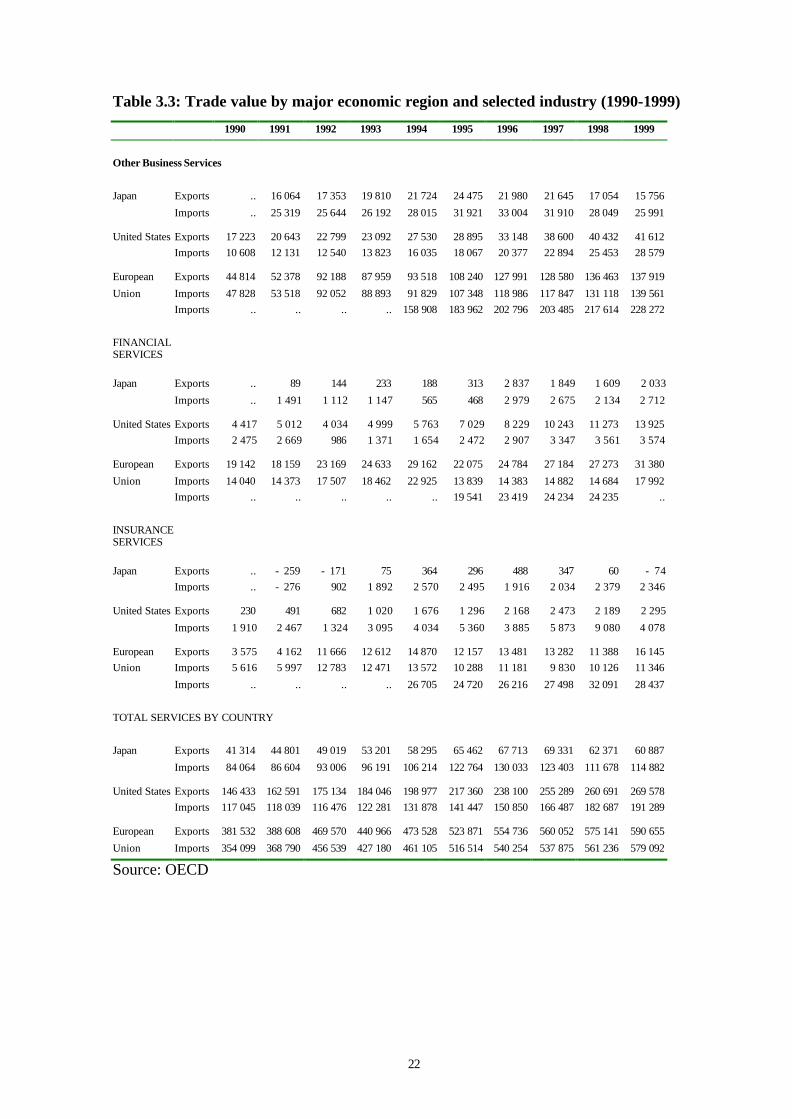

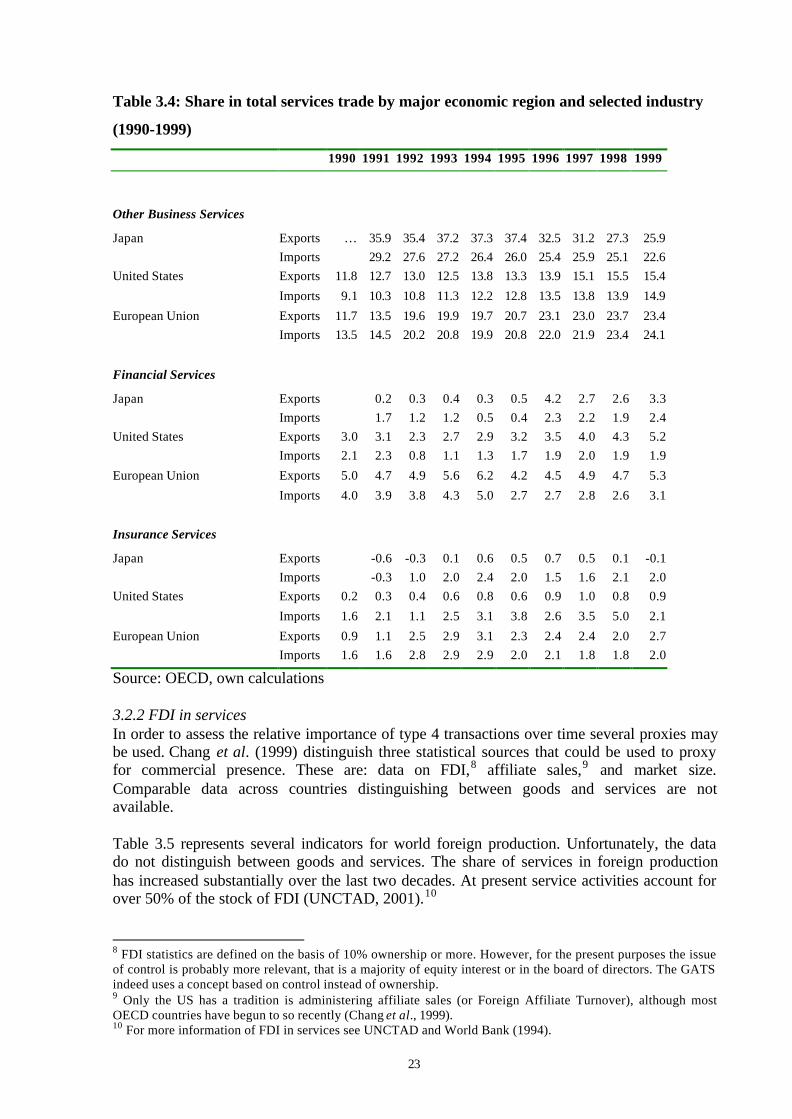

Table 3.3 represents the value and table 3.4 the share of trade in total services and someselected services for Japan, the US and the EU. For Japan trade in total services peakedaround 1996-1997 and fell back slightly afterwards. For both the US and the EU the value oftrade in total services increased significantly over the period 1990-1999 and at a fairlyconstant rate. Overall, the US is strong net exporter of services, the EU is also a net exporterbut by not nearly as much as the US, and Japan is a strong net importer. The only reversal inthe pattern of trade relates to the EU. The EU moved from a net importer in insurance andother business services in the early 1990’s to a net exporter in the late 1990’s. In the late1990’s the EU had become a net exporter of all three selected producer services.

6 For more information on the role of Japanese financial firms in the EU see Hawawini, G. and M. Schill (1994).7 The category ‘royalties and fees’ includes franchising, which under the GATS is a sub-sector of distributionservices.

22