Retirement Preparation - QSuper

72

Retirement Preparation

Transcript of Retirement Preparation - QSuper

Retirement Preparation

2

This material and any advice is provided by QInvest Limited (ABN 35 063 511 580, AFSL 238274) (QInvest). The person(s) speaking on behalf of QInvest are representative(s) of QInvest. For more information, refer to the Financial Services Guide, available at QInvest.com.au or QSuper.qld.gov.au.This material is current at the time of seminar. Any advice is general only, so it does not take into account your personal objectives, financial situation, or needs. Before you make any decision about whether to acquire any financial product, you should obtain and read the relevant product disclosure statement (PDS). Where necessary, consider seeking professional advice tailored to your individual circumstances.QSuper products are issued by Australian Retirement

Trust Pty Ltd (ABN 88 010 720 840, AFSL 228975) as trustee for Australian Retirement Trust (ABN 60 905 115 063). Any reference to QSuper is a reference to the Government Division of Australian Retirement Trust. PDSs and target market determinations (TMDs) for QSuper products are available at qsuper.qld.gov.au/calculators-and-forms/publications.

New PDSs and TMDs are expected to be available from 28 February 2022 at australianretirementtrust.com.au.You may use this material for personal, non-commercial purposes only. You may not otherwise use or distribute this information for another purpose without first obtaining our written consent.

Important informationAbout today’s presentation

Set yourself up1

4

What will your retirement look like?

5

Income needsWays to work out your income in retirement

Retirementbudget

ASFA retirement standard

2/3 rule

Association of Superannuation Funds of Australia (ASFA). To find out more, https://www.superannuation.asn.au/resources/retirement-standard

6

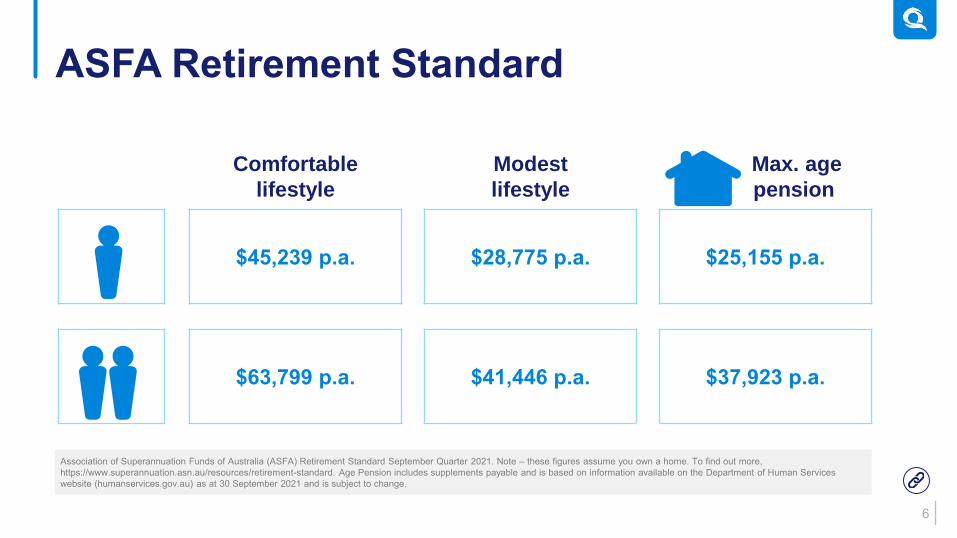

ASFA Retirement Standard

Comfortable

lifestyle

Modest

lifestyle

Max. age

pension

$45,239 p.a. $28,775 p.a. $25,155 p.a.

$63,799 p.a. $41,446 p.a. $37,923 p.a.

Association of Superannuation Funds of Australia (ASFA) Retirement Standard September Quarter 2021. Note – these figures assume you own a home. To find out more, https://www.superannuation.asn.au/resources/retirement-standard. Age Pension includes supplements payable and is based on information available on the Department of Human Services website (humanservices.gov.au) as at 30 September 2021 and is subject to change.

7

Life expectancyAt birth for a person born in that year

55

8187

58

8589

50

60

70

80

90

100

1905 1920 1935 1950 1965 1980 1995 2010 2025 2040 2055

Age

Male life expectancy Female life expectancy

2021

2021 Intergenerational Report. To find out more see The Australian Government Treasury site, treasury.gov.au/publication/2021-intergenerational-report

8

How are you tracking?Super Projection Calculator

This calculation is an estimate only and may vary significantly over time with changes in returns, inflation and fees. Full details of assumptions are available when using the calculator. Past performance is not an indication of future returns.

Ways to grow your super

2

10

Ways to grow your super

Defined benefit catch-up

Find any lost super

Consolidate your other super accounts

Maximise your employer contribution

Work longer

11

Ways to grow your super

Make extra contributions

Co-contribution from the Government

Start salary sacrificing

Contribute non-super assets

Transition to retirement strategy

12

Reasons to start a TTR strategy

Boost your super

• Be tax smart and keep the same pay

• Save more now so you have more in retirement

Boost your income

• Switch to part-time work or to a job that fits your life

• Source of additional income

13

How does a TTR strategy work?

Work full timeMaximise salary

sacrifice contributions

Take home pay Super

TTR income stream

Income stream payments

14

Rules applying to TTR account

You must receive a payment at least once each financial year

Minimum payment amount is 4% p.a. of the opening balance and/or 1 July balance (under age 651)

Maximum payment amount is 10% p.a.

No lump sum withdrawals2

1 Minimum rates reduced by 50% have been extended for the 2021-22 income year as a temporary measure put in place due to the coronavirus pandemic. For more details, see the QSuper site qsuper.qld.gov.au/learn/coronavirus-and-super. 2 This option is generally only available before retirement if you have an unrestricted non-preserved (cashable) amount in your super account. You must otherwise satisfy specific early access criteria, such as TPD, financial hardship or other grounds, to make lump sum withdrawals from your super or income stream. Go to qsuper.qld.gov.au/super/early-access for more details.

15

Is a TTR strategy right for you?Be clear about the outcome that you want to achieve

• Does this strategy suit your situation?

• Will you have enough to retire?

• If aged under 60 – tax benefits may be minimal

• Consider how important Defined Benefit account certainty is to you

• The danger with these types of strategies are that they require discipline so as to not spend the funds elsewhere

• Be aware of your contribution limits1

1 There is a limit on the total amount of superannuation you can transfer to a Retirement Income account without paying additional tax. This is known as the transfer balance cap. For the 2021-22 financial year, the transfer balance cap is set at $1.7 million. If you have a number of income streams or pension accounts (not including Transition to Retirement Income accounts), either at QSuper or across multiple super funds, you need to be aware that your combined account balances will all count towards this limit. Special rules apply for Defined Benefit lifetime pensions. Go to the Australian Taxation Office's website for more about the transfer balance cap.

16

Contribution limitsAs at 1 July 2021

1 Limit is current for the 2021-22 financial year. Additional catch-up contributions available from 2019-20. 2 Subject to having a balance below $1.7 million as at 30 June 2021. 3 Eligibility extended for one year following the financial year work test was met, up to age 74. Note: Once only lifetime exemption.

Age Before tax After tax

Under 67 $27,500 p.a.1 $110,000 p.a.2($330,000 bring forward rule)1

67 – 74 $27,500 p.a. with work test3 $110,000 p.a. with work test3

75+ Superannuation GuaranteeContributions only

N/A

Work test: You must have worked at least 40 hours within 30 consecutive days in a financial year

17

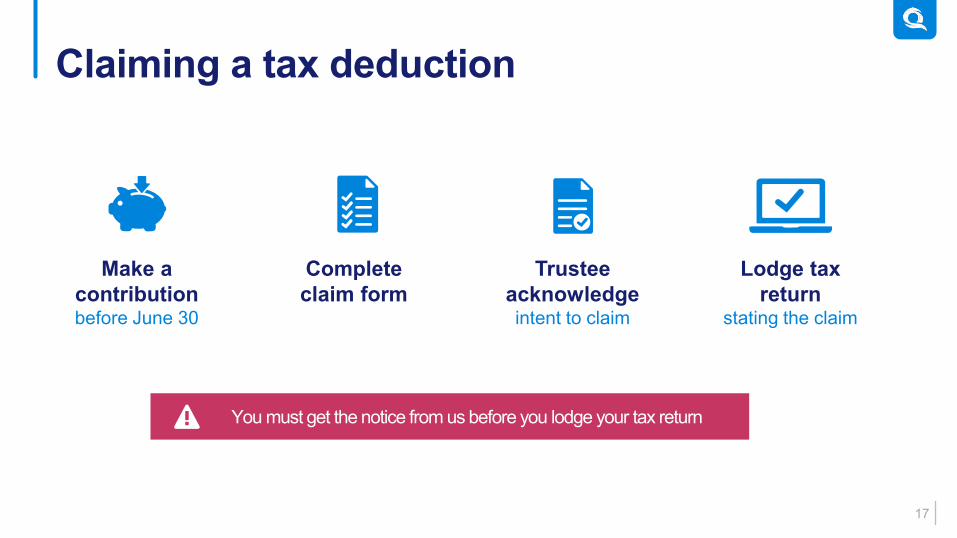

Claiming a tax deduction

Make a contributionbefore June 30

Complete claim form

Trustee acknowledgeintent to claim

Lodge tax return

stating the claim

You must get the notice from us before you lodge your tax return

18

Contribute to super – SusanCase study example

1 Medicare Levy of 2% is included for the 2021-22 financial year. This case study is provided for illustrative purposes only, and shouldn’t be relied on as personal, legal or taxation advice and doesn’t take the place of this type of advice either.

Age: 50Retire at: 62Current salary: $75,000 (has a marginal tax rate of 34.5%1).Current super balance: $150,000

ObjectivesGrow her super by making either:

• after-tax contributions, or• before-tax (salary sacrifice) contributions

19

Salary sacrifice exampleSalary of $75,000 and contribution of 5%

This diagram is provided for illustrative purposes only. We’ve rounded our figures in this calculation. Based on tax rates for the 2021-22 financial year and includes the Medicare levy of 2%. Note: Contributions to super are preserved until you meet a condition of release. Our example is generic only and doesn’t replace getting personal financial or tax advice. It’s based on a specific set of circumstances so your actual results may differ.

After-tax Before-tax(Salary Sacrifice)

NetBenefit$731

Contribution $3,750 $3,750

Income tax $15,262 $13,968

Take home pay $55,988 $57,282

Super balance $3,750 $3,188

20

Salary sacrifice exampleSalary of $75,000 and contribution of 5% + tax savings

This diagram is provided for illustrative purposes only. We’ve rounded our figures in this calculation. Based on tax rates for the 2021-22 financial year and includes the Medicare levy of 2%. Note: Contributions to super are preserved until you meet a condition of release. Our example is generic only and doesn’t replace getting personal financial or tax advice. It’s based on a specific set of circumstances so your actual results may differ.

After-tax Before-tax(Salary Sacrifice)

NetBenefit$1,116

Contribution $3,750 $5,725

Income tax $15,262 $13,287

Take home pay $55,988 $55,988

Super balance $3,750 $4,866

=

21

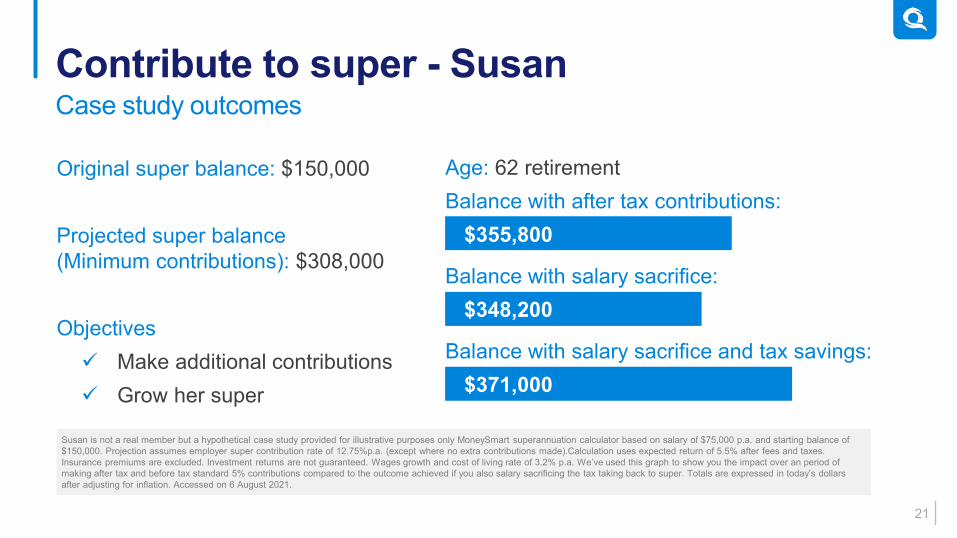

Contribute to super - SusanCase study outcomes

Age: 62 retirementBalance with after tax contributions:

$355,800

Balance with salary sacrifice: $348,200

Balance with salary sacrifice and tax savings: $371,000

Original super balance: $150,000

Projected super balance (Minimum contributions): $308,000

Objectives✓ Make additional contributions✓ Grow her super

Susan is not a real member but a hypothetical case study provided for illustrative purposes only MoneySmart superannuation calculator based on salary of $75,000 p.a. and starting balance of $150,000. Projection assumes employer super contribution rate of 12.75%p.a. (except where no extra contributions made).Calculation uses expected return of 5.5% after fees and taxes. Insurance premiums are excluded. Investment returns are not guaranteed. Wages growth and cost of living rate of 3.2% p.a. We’ve used this graph to show you the impact over an period of making after tax and before tax standard 5% contributions compared to the outcome achieved if you also salary sacrificing the tax taking back to super. Totals are expressed in today’s dollars after adjusting for inflation. Accessed on 6 August 2021.

Funding your retirement

3

23

The income layering approach

Lifetime

Pension

Age

Pension

Regular income paid for life

Income to pay for the things you cannot live without, such as:

Retirement

Income account

Other income

sources

Flexible payments and accessible funds

Income to pay for the things that improve your standard of living such as:

24

When can you access your super?

• Once you reach your access age and retire

• Once you stop working for an employer at or after age 60

• Once you turn age 65.

Date of birth Access ageBefore 1 July 1960 55

1 July 1960 – 30 June 1961 56

1 July 1961 – 30 June 1962 57

1 July 1962 – 30 June 1963 58

1 July 1963 – 30 June 1964 59

From 1 July 1964 60

25

Account types

Accumulation• Investment based• Money in and money out• Investment choice• Member bears

investment risk

Defined Benefit• Formula based• Multiple of salary• Closed option• Employer bears

investment risk

26

Options for your superannuationWhen you have retired

Flexible incomeRetirement Income

account

Income for lifeLifetime Pension

Park your fundsAccumulation

account

Or any combination of these

27

Park your moneyAccumulation account

• Gives you time to make your plans• Take lump sums as needed • Make additional contributions if eligible• Not assessed by Centrelink, until you reach Age Pension age

• Investment earnings are taxed at up to 15%• Consider if you are paying for insurance cover that you may

not need

Potential benefits

What else to consider

28

Flexible incomeHow the income account works

• Must have reached preservation age

• QSuper Income account: minimum $30,000 to open

• Control how much and how often you are paid

• You have full access to your funds

• May pay tax if you are under age 60

• Tax-free from age 60

Eligibility and conditions apply. If it is a Transition to Retirement Income account you will have a maximum income drawdown amount of 10% of your balance per year and no access to lump sum withdrawals. Also, your investment earnings are taxed in the same way as an Accumulation account. These limits will be removed once you tell us that you meet a condition of release or turn age 65.

29

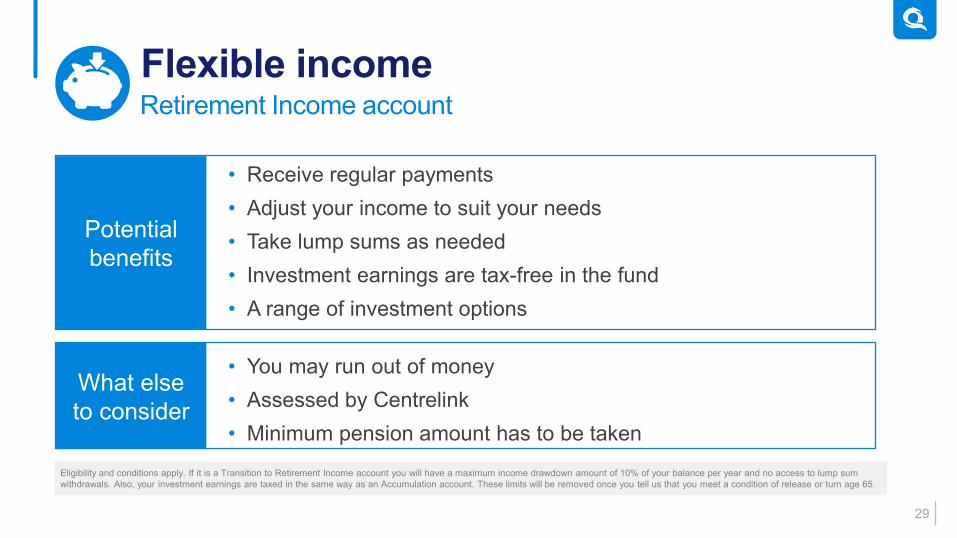

Flexible incomeRetirement Income account

• You may run out of money • Assessed by Centrelink• Minimum pension amount has to be taken

Eligibility and conditions apply. If it is a Transition to Retirement Income account you will have a maximum income drawdown amount of 10% of your balance per year and no access to lump sum withdrawals. Also, your investment earnings are taxed in the same way as an Accumulation account. These limits will be removed once you tell us that you meet a condition of release or turn age 65.

Potential benefits

What else to consider

• Receive regular payments• Adjust your income to suit your needs• Take lump sums as needed • Investment earnings are tax-free in the fund• A range of investment options

30

Income accountPayment rules

The minimum amount will be adjusted on 1 July each year.

Age range Minimum amount

55-64 4%

65-74 5%

75-79 6%

80-84 7%

85-89 9%

90-94 11%

95+ 14%

• Age-based minimum annual payment amount

• Calculated on commencement and 1 July balance each year

• At least one payment annually

• Flexible payments above the minimum amount

31

6-month cooling-off periodProviding time to decide if it’s right for you

Money-back protectionReceive at least your money back as income or the remainder as a death benefit2

Optional spouse protectionPayments continue if you pass away

Potential Age Pension benefitsDiscounted assets test

Higher incomeMarket linked with an annual adjustment1

1 Income can go up or down depending on pool performance. 2 Subject to a legislated maximum in limited circumstances

Income for life Fortnightly payments for the rest of your life

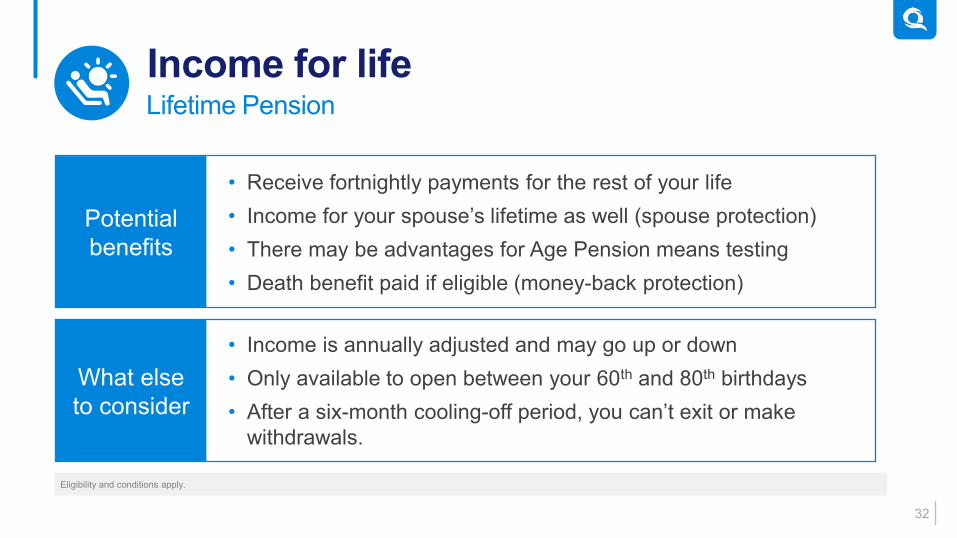

Lifetime PensionIncome for life

32

Income for lifeLifetime Pension

• Receive fortnightly payments for the rest of your life • Income for your spouse’s lifetime as well (spouse protection)• There may be advantages for Age Pension means testing• Death benefit paid if eligible (money-back protection)

• Income is annually adjusted and may go up or down • Only available to open between your 60th and 80th birthdays• After a six-month cooling-off period, you can’t exit or make

withdrawals.

Eligibility and conditions apply.

Potential benefits

What else to consider

33

Retirement bonusMore to look forward to in retirement

$40.9mpaid

21,800members

$1,876average bonus amount

Since June 2016. QSuper data, as at 30 June 2021.

34

Retire easily with usProcess to start receiving income

Illustrative purposes only.

Decide how much to allocate

Retirement Income account

Plan your payment

Set an investment

strategy

Lifetime Pension

Spouse protection option

Nominate a beneficiary

Nominate a beneficiary

or and

Single option

35

Mary’s storyCase study example

Age: 67Current super balance: $500,000

Objectives• Certainty of payments for rest of her life• Flexibility to withdraw extra money when needed

This case study is provided for illustrative purposes only, and shouldn’t be relied on as personal, legal or taxation advice anddoesn’t take the place of this type of advice either.

36

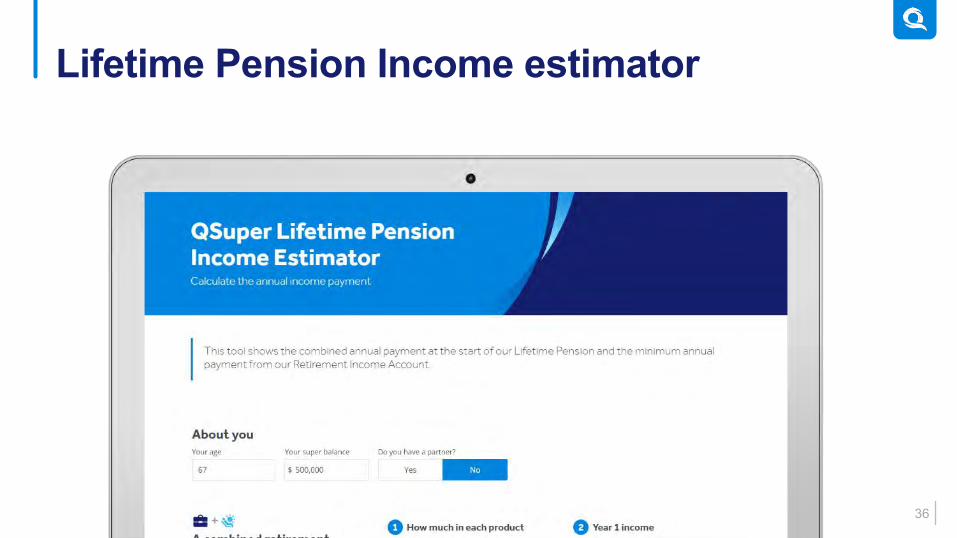

Lifetime Pension Income estimator

37

Mary’s storyCase study outcomes

Lifetime

Pension

$250,000

Age

Pension

Regular income paid for life

• Housing• Utilities• Clothing

• Transportation• Food• Medical expenses

Retirement Income account

$250,000

Flexible payments and accessible funds

• Meals out• Leisure

activities• Weekends

away

• Trip to France• New car• Replace fridge• Minor renovations

Mary is not a real member but a hypothetical case study provided for illustrative purposes only. Additionally, figures may be rounded for ease of understanding. Members should seek advice from a qualified licensed professional, regarding their own circumstances.

38

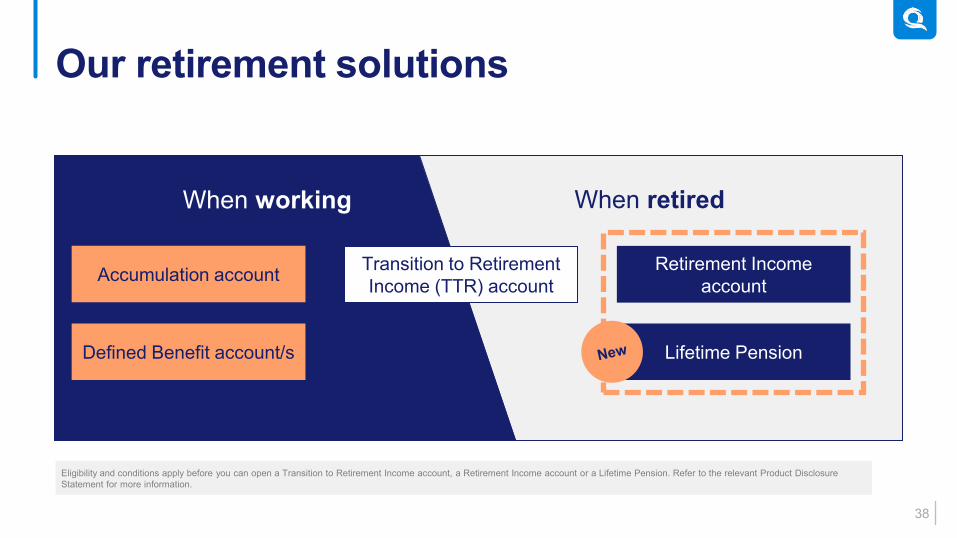

Our retirement solutions

Eligibility and conditions apply before you can open a Transition to Retirement Income account, a Retirement Income account or a Lifetime Pension. Refer to the relevant Product Disclosure Statement for more information.

Accumulation account

Defined Benefit account/s

Transition to Retirement Income (TTR) account

Retirement Income account

Lifetime Pension

When working When retired

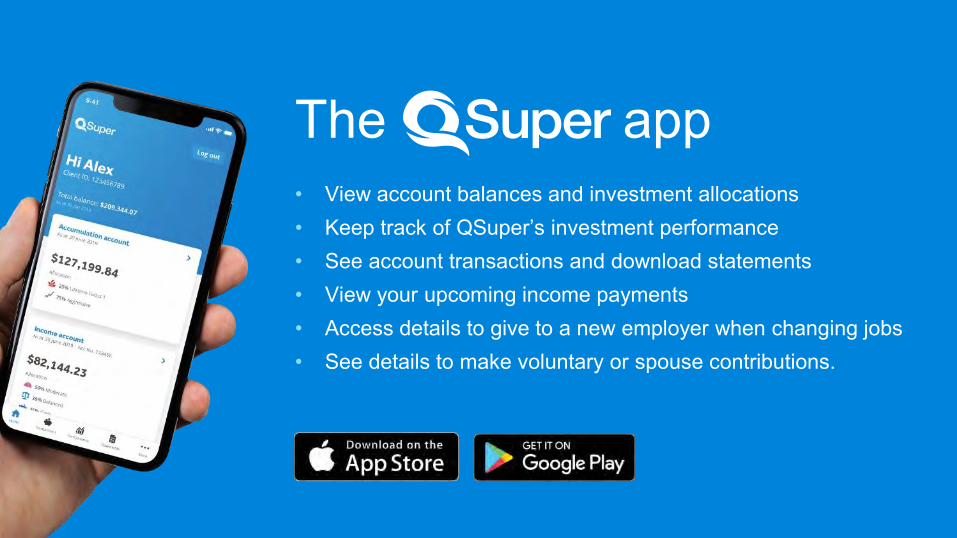

The app• View account balances and investment allocations• Keep track of QSuper’s investment performance• See account transactions and download statements• View your upcoming income payments• Access details to give to a new employer when changing jobs• See details to make voluntary or spouse contributions.

What tax applies?

4

41

Tax components of super

No tax when goes into super

Subject to 15% contributions

tax into super1

Tax freeAfter-tax

contributions

TaxableBefore-tax

contributions

No tax payable on withdrawal

May be taxable on withdrawal, depending on

age and withdrawal amount

1 Contributions limits apply. If your income plus concessional contributions are more than $250,000 per year, different tax rules apply. You will pay an extra 15% tax on your concessional contributions over this threshold.

42

Taxation – Lump sum withdrawalsAccumulation and Income account

55-59 60+

Tax free portion Tax free

100% tax freeTaxable component First $225,000 is tax free (low rate cap), and

balance taxed at 17%1

1 Including Medicare Levy of 2% for 2021-22 financial year.

43

Taxation – Lump sum withdrawalsExample – age under 60

$400,000 withdrawal $40,000 withdrawal

Tax free ¼ $100,000 $10,000$0 tax payable $0 tax payable

Taxable ¾ $300,000 $30,000

-$225,000 Low Rate Cap $225,000 Low Rate Cap

$75,000 x17%1 $195,000 Low Rate Cap remaining

$12,750 tax payable $0 tax payable

1 Includes 2% Medicare Levy

44

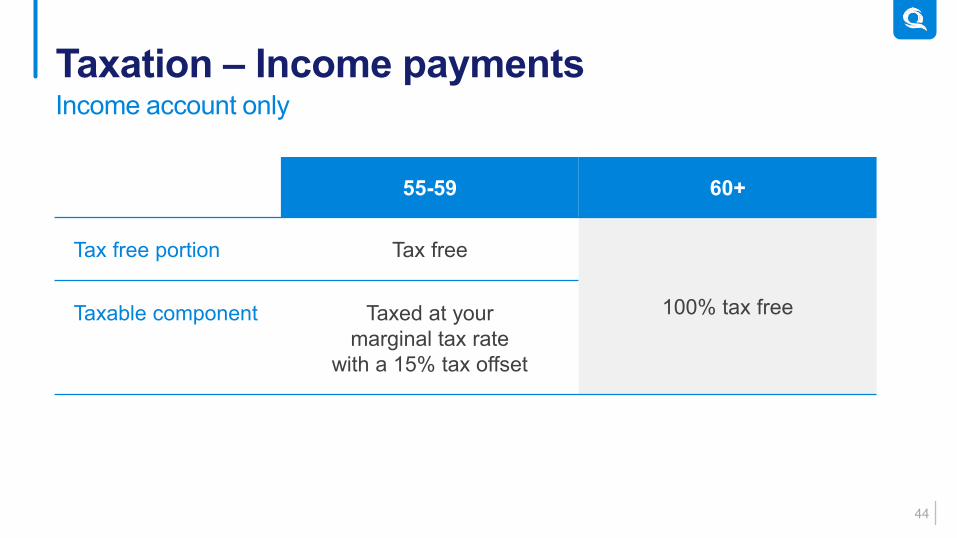

Taxation – Income paymentsIncome account only

55-59 60+

Tax free portion Tax free

100% tax freeTaxable component Taxed at yourmarginal tax rate

with a 15% tax offset

45

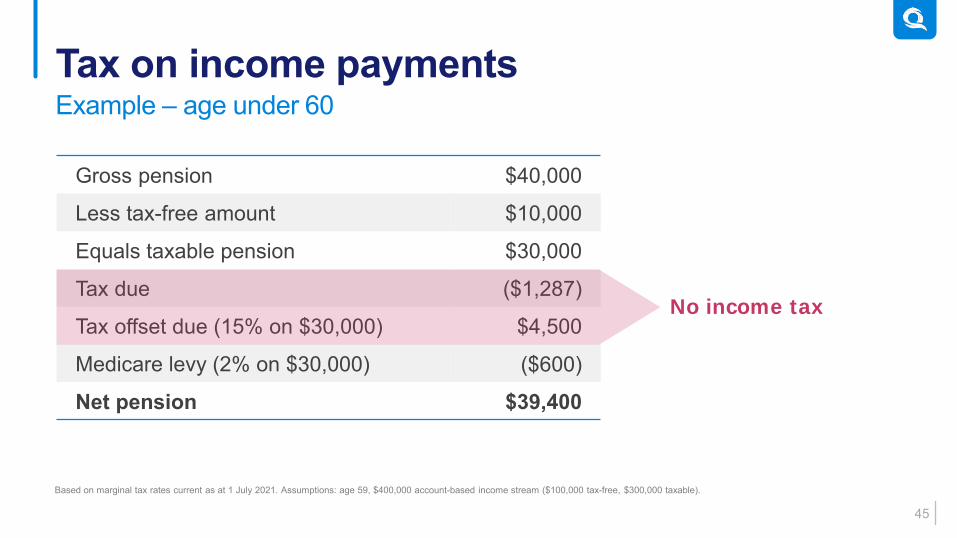

Tax on income paymentsExample – age under 60

Gross pension $40,000

Less tax-free amount $10,000

Equals taxable pension $30,000

Tax due ($1,287)

Tax offset due (15% on $30,000) $4,500

Medicare levy (2% on $30,000) ($600)

Net pension $39,400

Based on marginal tax rates current as at 1 July 2021. Assumptions: age 59, $400,000 account-based income stream ($100,000 tax-free, $300,000 taxable).

No income tax

46

How are super death benefits treated?

47

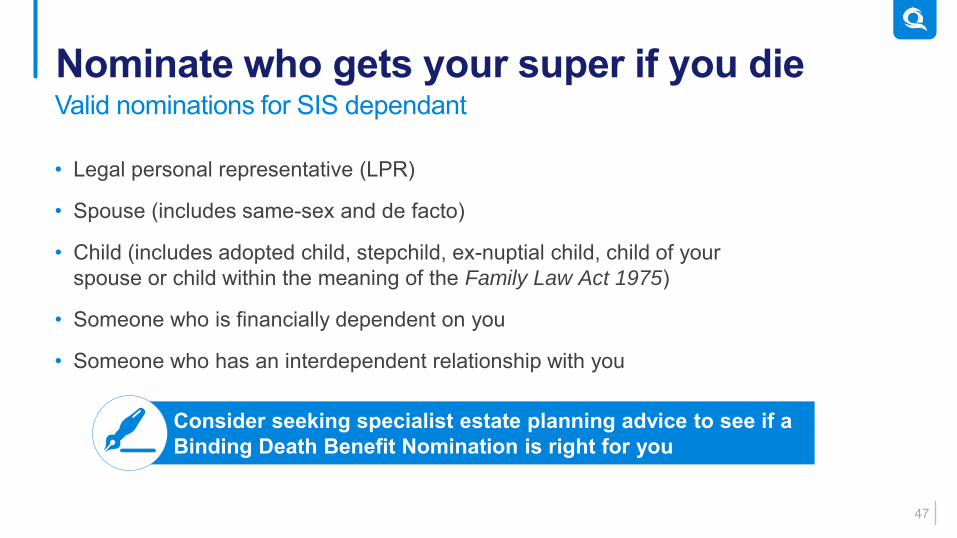

Nominate who gets your super if you dieValid nominations for SIS dependant

• Legal personal representative (LPR)

• Spouse (includes same-sex and de facto)

• Child (includes adopted child, stepchild, ex-nuptial child, child of your spouse or child within the meaning of the Family Law Act 1975)

• Someone who is financially dependent on you

• Someone who has an interdependent relationship with you

Consider seeking specialist estate planning advice to see if a Binding Death Benefit Nomination is right for you

48

Nomination options

Accumulationaccount

Defined benefit

Incomeaccount/s Lifetime Pension

No nomination

Binding death nomination available

Reversionary beneficiary available

Child pension only

Spouse protection option only

49

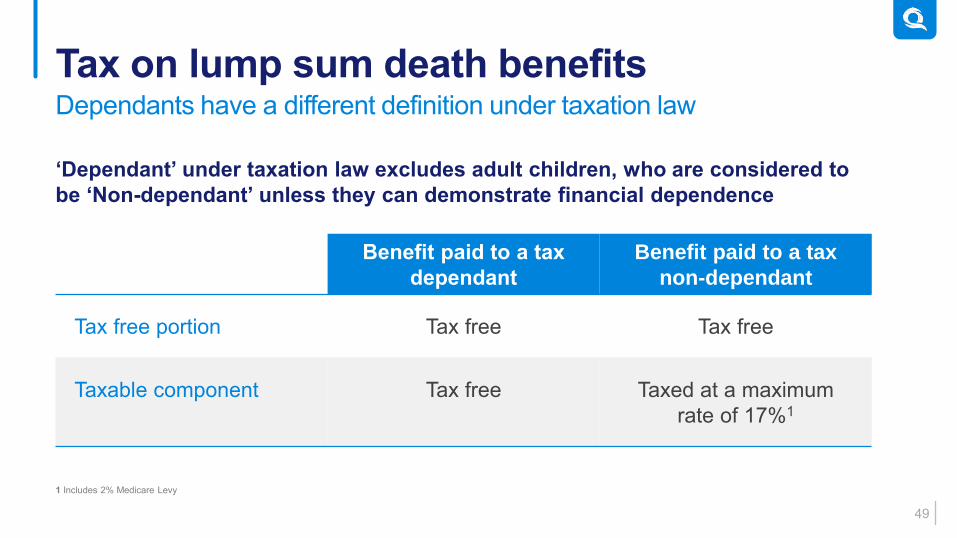

Tax on lump sum death benefitsDependants have a different definition under taxation law

‘Dependant’ under taxation law excludes adult children, who are considered to be ‘Non-dependant’ unless they can demonstrate financial dependence

Benefit paid to a tax dependant

Benefit paid to a tax

non-dependant

Tax free portion Tax free Tax free

Taxable component Tax free Taxed at a maximum rate of 17%1

1 Includes 2% Medicare Levy

50

Tax on reversionary incomeBeneficiary must be a dependant under SIS Act and taxation law

Tax treatment depends on the age of the deceased and the age of the beneficiary

Age of deceased OR

beneficiary is 60+ years

Age of deceased AND

beneficiary is under 60 years

Tax free portion Tax free Tax free

Taxable component

Tax free Taxed at your marginal tax rate with a 15% tax offset

Investing for retirement

5

52

Investment portfolioInvested in a wide range of asset classes around the globe

Asia$0.0

$2.5

$5.0

$7.5

$10.0

$12.5

$15.0

Australia

Inve

stm

ent $

in b

illio

ns

Equities Fixed Income Cash Real Estate Infrastructure Alternatives

United Kingdom EU total United States SouthAmerica

QSuper data as at 30 June 2021. This chart shows QSuper’s top investment holdings across the whole fund by geographic breakdown and asset class. Note that QSuper has other investment holdings in other countries such as Israel, Mexico, Canada and New Zealand that are not significant enough to show at this scale. Information for periods prior to 28 February 2022 are prior to QSuper's merger with Sunsuper to form Australian Retirement Trust.

53

Investment options12 investment options within 4 categories

LifetimeLet us manage it

• Lifetime

DiversifiedTake some control

• Moderate

• Socially responsible

• Balanced

• Aggressive

Single SectorMix your own investment

• Cash

• International shares

• Diversified bonds

• Australian shares

Self InvestMake all the decisions

• Australian shares

• Exchange traded funds

• Term deposits

54

Lifetime groupsInvestment options that adapt and grow with you

1 For Accumulation accounts only. All objectives are after fees and tax, measured over rolling 10-year periods. Past performance is not a reliable indicator of future performance. Risk and returns illustrated are not guaranteed and illustrate the possible risk/return expected over the long term.

Lifetime group1 Your age Lifetime balance Objective Risk

Outlook <40 Any balance CPI +4.5% p.a.

Aspire 1 40-49 <$50,000 CPI +4.5% p.a.

Aspire 2 40-49 $50,000+ CPI +4.0% p.a.

Focus 1 50-57 <$100,000 CPI +4.0% p.a.

Focus 2 50-57 $100,000 - $250,000 CPI +3.75% p.a.

Focus 3 50-57 $250,000+ CPI +3.5% p.a.

Sustain 1 58 or over <$300,000 CPI +2.5% p.a.

Sustain 2 58 or over $300,000+ CPI +2.0% p.a.

55

• Rebalancing

• Expertise

• Fee

• Emotion

• Diversification

• Inflation

• Risk

• Discipline

• Asset class features

• Expected return

• Timeframe

• Tax

InvestingConsiderations

56

Investor emotions

Optimism

Excitement

Thrill

Anxiety

Denial

Fear

Desperation

Panic

Capitulation

Despondency Depression

Hope

Relief

Optimism

Euphoria

57

Choosing your investment optionsRisk vs return

Ret

urn

Past performance is not a reliable indicator of future performance. Risk and returns illustrated are not guaranteed and illustrate the possible risk/return expected over the long term

Risk

Cash

Self Invest: Term Deposits

Moderate

Diversified Bonds

Balanced Socially Responsible

Aggressive

Australian Shares, International Shares

Self Invest: Australian Share & ETFs

58

How risk / return profile translateRange of annual returns over past 10 years

10.0018.13 24.59 21.19

3.7410.80

45.1960.85

-0.44 -1.87 -8.91 -2.72 -0.09 -0.09

-20.64 -19.08-30-20-10

010203040506070

Perc

enta

ge re

turn

Moderate Balanced Socially responsible Aggressive

Cash Diversified bonds Australian shares International shares

QSuper Accumulation Account minimum and maximum financial year returns for the period 30 June 2011 to 30 June 2021. Past performance is not a reliable indicator of future performance.Returns for periods prior to 28 February 2022 are based on the relevant product's returns prior to QSuper's merger with Sunsuper to form Australian Retirement Trust.

59

Diversified investment optionsManaged by a team of experts

All objectives are after fees and tax, measured over rolling timeframes as indicated in the table except for the Balanced option which is measured over a rolling 10-year period. Past performance is not a reliable indicator of future performance. Risk and returns illustrated are not guaranteed and illustrate the possible risk/return expected over the long term.

Investment options Timeframe Objective Risk

Moderate 3+ year CPI +2.5%

Balanced 5+ years CPI +3.5% measured over rolling 10-year period.

Socially Responsible 5+ years CPI +3.5%

Aggressive 10+ years CPI +4.5%

60

Single sector investment optionsAllows you to align your portfolio to your goals

The objective of each option is to match the return of the relevant indicies after fees and taxes. 1 The Bloomberg AusBond Bank Bill Index is constructed as a benchmark to represent the performance of a passively managed short-term money market portfolio. It comprises a series of bank bills of equal face value, each with a maturity seven days apart. 2 This option is managed externally through QIC Limited and is generally fully invested in a single asset class, however to accommodate market changes and transaction timings, it may be appropriate to hold up to 10% in cash. 3 Lifetime is only available in the Accumulation account. 4 Self Invest is not available in the Transition to Retirement Income account All objectives are after fees and tax, measured over rolling 10-year periods. Past performance is not a reliable indicator of future performance. Risk and returns illustrated are not guaranteed and illustrate the possible risk/return expected over the long term.

Investment options Timeframe Objective Risk

Cash <1 year Bloomberg AusBond Bank Bill Index1

Diversified bonds2 3+ years 40% Australian and 60% international diversified bonds index (hedged in AUD)

International share 10+ yearsMSCI World Developed Markets ex-Australia net dividends reinvested accumulation index3 (hedged in AUD)

Australian Shares 10+ years S&P/ASX 200 Accumulation Index4

61

Accumulation account investment returnsAs at 28 February 2022

Investment option10-year

compound average (%)

5-year compound average (%)

1 year

as at 28 Feb 2022 (%)

Balanced 8.34 6.89 6.61

Moderate 5.08 3.87 2.99

Socially Responsible 7.00 5.56 0.08

Aggressive 9.66 7.60 6.94

Cash 1.49 0.85 -0.14

Diversified Bonds 3.66 2.22 -2.62

International Shares 11.39 10.28 6.96

Australian Shares 9.49 8.01 7.77Past performance is not a reliable indicator of future performance. The figures shown reflect the returns of the QSuper Fund, not the returns of your investment in that option as they do not take into account the timing of contributions, investment switches or withdrawals. Returns are shown net of fees and tax, and may be rounded down to one decimal place. Each of our investment options has a different objective, risk profile, and asset allocation. Visit qsuper.qld.gov.au for more information. Returns for periods prior to 28 February 2022 are based on the relevant product's returns prior to QSuper's merger with Sunsuper to form Australian Retirement Trust.

62

Income account investment returnsAs at 28 February 2022

Investment option 10-year compound average (%)

5-year compound average (%)

1 year as at 28 Feb 2022 (%)

Balanced 9.35 7.90 8.32

Moderate 5.70 4.38 3.54

Socially Responsible 7.89 6.16 -0.12

Aggressive 10.80 8.81 9.21

Cash 1.75 1.00 -0.16

Diversified Bonds 4.25 2.58 -3.12

International Shares 12.37 11.22 7.15

Australian Shares 10.66 9.15 8.62Past performance is not a reliable indicator of future performance. The figures shown reflect the returns of the QSuper Fund, not the returns of your investment in that option as they do not take into account the timing of contributions, investment switches or withdrawals. Returns are shown net of fees and tax, and may be rounded down to one decimal place. Each of our investment options has a different objective, risk profile, and asset allocation. Visit qsuper.qld.gov.au for more information. Returns for periods prior to 28 February 2022 are based on the relevant product's returns prior to QSuper's merger with Sunsuper to form Australian Retirement Trust.

QSuper's Income account won SuperRatings Pension of the Year 2019, 2020, 2021 and 2022. These awards were received before QSuper merged with Sunsuper to become Australian Retirement Trust on 28 February 2022. This QSuper product has kept the same relevant features post merger. Past performance is not a reliable indicator of future performance. Ratings and awards are subject to change, and are only one factor to consider when deciding how to invest your super.

Visit qsuper.qld.gov.au/awards for details.

64

Our investment difference

1 To see how QSuper’s investment options have performed, visit qsuper.qld.gov.au/performance

Experienced investment team• A focus on delivering strong

long-term returns1

• Diversification to provide stability and balance risk

• Managing investments to suit your phase of life

• Sustainable investment and consideration of ESG risks

65

Questions to considerAbout investment risk

What’s your attitude to

investment risk?

How comfortable would you be with the possibility

of losing money?

What are the timeframes for

your goals?

The value of financial advice

6

67

What’s your plan to fund retirement?

Super balance Non-super assets Age PensionCentrelink1

Potential source of tax free income in

retirement

Taxable income in retirement

Additional income to boost the longevity of

your funds

1 Age Pension and other Centrelink benefits are subject to eligibility. For more information, see Department of Social Services, dss.gov.au/seniors/benefits-payments/age-pension.

68

Retirement accountsDesigned to be used together

Product features Retirement Income

account1 Lifetime Pension Together

Payments for life

Money-back protection

Revert to a spouse (can run out)

Access to withdrawals

Change regular payments

Change investments

1 There are some other conditions under which you can open a Retirement Income account even if you are under preservation age. Find out more at qsuper.qld.gov.au/our-products/superannuation/income-account

69

Advisers are experts on how to…

• Keep up with legislative changes

• Maximise your government and superannuation entitlements

• Calculate how much you need, and how much to save for retirement

• Guidance on spending decisions so money lasts in retirement

• Invest smarter

• Protect your family assets and income

• Make sure the plans that you have in place are on track.

Deciding what is best for you will depend on your personal circumstances and you may want to seek personal financial advice to get the most from your superannuation. You can find out more about financial advice options at qsuper.qld.gov.au/advice

70

Build your retirement planHelp you make smarter choices

Professional financial advice about your QSuper account• Transition to retirement

• Plan your QSuper retirement

• Manage your retirement income

• Retirement review

Deciding what is best for you will depend on your personal circumstances and you may want to seek personal financial advice to get the most from your superannuation. You can find out more about financial advice options at qsuper.qld.gov.au/advice.

&A

We can help youCall us on1300 360 750

Visit onlineqsuper.qld.gov.au

Book an appointmentqsuper.qld.gov.au/advice