RETAILING PARKSON HOLDINGS - AmeSecurities Holdings 130321.… · Parkson Holdings 21 March 2013...

13

RETAILING PARKSON HOLDINGS (PKS MK, PKNS.KL) 21 March 2013 China a dampener in the near term Company report HOLD Tan Ee Zhio [email protected] +603 2036 2304 (Re-initiation) Rationale for report: Re-initiation Price RM4.64 Fair Value RM4.43 52-week High/Low RM5.50/RM4.30 Key Changes Fair value Re-initiation EPS Re-initiation YE to Jun FY12 FY13F FY14F FY15F Revenue (RMmil) 3,447.5 3,592.2 4,333.3 4,975.0 Core net profit (RMmil) 379.2 266.4 332.3 366.2 EPS (Sen) 34.8 24.5 30.5 33.7 EPS growth (%) 7.8 (4.2) 24.7 10.2 Consensus EPS (Sen) - 31.7 35.7 43.7 DPS (Sen) 16.0 12.0 15.0 16.0 PE (x) 13.3 19.0 15.2 13.8 EV/EBITDA (x) 4.7 5.0 3.9 3.3 Div yield (%) 3.4 2.6 3.2 3.4 ROE (%) 15.5 9.7 11.3 11.7 Net Gearing (%) Net cash Net cash Net cash Net cash Stock and Financial Data Shares Outstanding (million) 1,088.2 Market Cap (RMmil) 5,049.3 Book value (RM/share) 2.46 P/BV (x) 1.9 ROE (%) 15.5 Net Gearing (%) Net cash Major Shareholders Narajaya Sdn Bhd (27.7%) Tan Sri Cheng Heng Jem (20.2%) Free Float (%) 12.3 Avg Daily Value (RMmil) 5.4 Price performance 3mth 6mth 12mth Absolute (%) 2.7 (0.6) (17.3) Relative (%) 1.0 (0.1) (21.3) 601 896 1,190 1,485 1,779 2.00 3.50 5.00 6.50 8.00 M a r - 0 8 S e p - 0 8 M a r - 0 9 S e p - 0 9 M a r - 1 0 S e p - 1 0 M a r - 1 1 S e p - 1 1 M a r - 1 2 S e p - 1 2 M a r - 1 3 I n d e x P o i n t s ( R M ) Parkson FBMKLCI PP 12247/06/2013 (032380) Investment Highlights • We are re-initiating coverage on Parkson Holdings Bhd (PHB), with a HOLD at our fair value of RM4.43/share, based on a sum-of-parts valuation for FY14F. • Over the past year, PHB has rapidly expanded into China and Southeast Asia via its respective 52%-owned and 68%-owned listed-subsidiaries, Parkson Retail Group (PRG) and Parkson Retail Asia (PRA). PRA has further expanded into Southeast Asia’s least developed markets – Vietnam, Sri Lanka, Myanmar and Cambodia – following its foray into Indonesia in 2011. • On the revenue front, PHB is driven by China (66%), followed by Malaysia (26%) and Indonesia (4%). China and Vietnam have been adversely impacted by slower economic growth, resulting in weak consumer spend. • China’s SSSG has hit historical lows, with contractions of 1% and 2% in 1QFY13 and 1HFY13, respectively. There, we believe, were largely attributed to intensification of competition among China-based retailers (including Golden Eagle and Intime). There appears to be a footfall shift towards more appealing malls amid their proliferation in numbers. • Despite efforts to improve merchandising mix and establishment of an e- commerce portal to circumvent the slowdown in SSSG, the impact of these efforts is too early to gauge. Parkson undergoes facelifts once every 4-5 years in order to maintain footfall momentum. • All in, we opine management’s guidance of a mid-single digit SSSG in FY13 may not be achievable. We are mainly uncertain about China’s turnaround in SSSG, given that the key issue stems from a more competitive landscape. We believe China’s 3Q SSSG growth would remain flat at best, and any recovery will be gradual. Expansion will be at a slow pace, at 5 new stores per annum. • PRA will continue to expand its network in Indonesia based on a dual- branding strategy (Parkson and Centro). The recent acquisition of Ordel is deemed as a strategic platform for PRA to further expand into the larger Indian sub-continent. Underpinned by stable recurring income, PHB aims at a higher ratio of self-owned properties, moving forward. • For FY13F, we project a healthy SSSG at 5% for Malaysia and Indonesia, riding on stable consumer spending. This should cushion a muted outlook in China and Vietnam given the near-term cyclical SSSG that is in negative territory. • FY13F-FY15F growth will be driven by an enlarged network of outlets – China (FY13F: +8 and FY14F: +5) and Southeast Asia (FY13F: +7 and FY14F: +8), coupled with the foray into Myanmar and Cambodia. Our annual new store assumption is at two for each market. • On a more positive note, the stock is a great play in the Asian consumer sector. Balance sheet is healthy, with a strong cash pile of RM1.5bil as at end-1HFY13. • It is trading at 15x FY14F PE, on par with its 5-year historical mean and at a 33% discount to local peer AEON Co (M) Bhd’s (AEON Mk Equity, Non- rated) 20x.

Transcript of RETAILING PARKSON HOLDINGS - AmeSecurities Holdings 130321.… · Parkson Holdings 21 March 2013...

RETAILING

PARKSON HOLDINGS (PKS MK, PKNS.KL) 21 March 2013

China a dampener in the near term

Company report HOLDTan Ee Zhio

+603 2036 2304

(Re-initiation)

Rationale for report: Re-initiation

Price RM4.64

Fair Value RM4.43

52-week High/Low RM5.50/RM4.30

Key Changes

Fair value Re-initiation

EPS Re-initiation

YE to Jun FY12 FY13F FY14F FY15F

Revenue (RMmil) 3,447.5 3,592.2 4,333.3 4,975.0

Core net profit (RMmil) 379.2 266.4 332.3 366.2

EPS (Sen) 34.8 24.5 30.5 33.7

EPS growth (%) 7.8 (4.2) 24.7 10.2

Consensus EPS (Sen) - 31.7 35.7 43.7

DPS (Sen) 16.0 12.0 15.0 16.0

PE (x) 13.3 19.0 15.2 13.8

EV/EBITDA (x) 4.7 5.0 3.9 3.3

Div yield (%) 3.4 2.6 3.2 3.4

ROE (%) 15.5 9.7 11.3 11.7

Net Gearing (%) Net cash Net cash Net cash Net cash

Stock and Financial Data

Shares Outstanding (million) 1,088.2

Market Cap (RMmil) 5,049.3

Book value (RM/share) 2.46

P/BV (x) 1.9

ROE (%) 15.5

Net Gearing (%) Net cash

Major Shareholders Narajaya Sdn Bhd (27.7%)

Tan Sri Cheng Heng Jem (20.2%)

Free Float (%) 12.3

Avg Daily Value (RMmil) 5.4

Price performance 3mth 6mth 12mth

Absolute (%) 2.7 (0.6) (17.3)

Relative (%) 1.0 (0.1) (21.3)

601

896

1,190

1,485

1,779

2.00

3.50

5.00

6.50

8.00

Mar-08

Sep-08

Mar-09

Sep-09

Mar-10

Sep-10

Mar-11

Sep-11

Mar-12

Sep-12

Mar-13

Index Points

(RM)

Parkson FBM KLCI

PP 12247/06/2013 (032380)

Investment Highlights

• We are re-initiating coverage on Parkson Holdings Bhd (PHB), with a

HOLD at our fair value of RM4.43/share, based on a sum-of-parts

valuation for FY14F.

• Over the past year, PHB has rapidly expanded into China and Southeast

Asia via its respective 52%-owned and 68%-owned listed-subsidiaries,

Parkson Retail Group (PRG) and Parkson Retail Asia (PRA). PRA has

further expanded into Southeast Asia’s least developed markets –

Vietnam, Sri Lanka, Myanmar and Cambodia – following its foray into

Indonesia in 2011.

• On the revenue front, PHB is driven by China (66%), followed by Malaysia

(26%) and Indonesia (4%). China and Vietnam have been adversely

impacted by slower economic growth, resulting in weak consumer

spend.

• China’s SSSG has hit historical lows, with contractions of 1% and 2% in

1QFY13 and 1HFY13, respectively. There, we believe, were largely

attributed to intensification of competition among China-based retailers

(including Golden Eagle and Intime). There appears to be a footfall shift

towards more appealing malls amid their proliferation in numbers.

• Despite efforts to improve merchandising mix and establishment of an e-

commerce portal to circumvent the slowdown in SSSG, the impact of

these efforts is too early to gauge. Parkson undergoes facelifts once

every 4-5 years in order to maintain footfall momentum.

• All in, we opine management’s guidance of a mid-single digit SSSG in

FY13 may not be achievable. We are mainly uncertain about China’s

turnaround in SSSG, given that the key issue stems from a more

competitive landscape. We believe China’s 3Q SSSG growth would

remain flat at best, and any recovery will be gradual. Expansion will be at

a slow pace, at 5 new stores per annum.

• PRA will continue to expand its network in Indonesia based on a dual-

branding strategy (Parkson and Centro). The recent acquisition of Ordel

is deemed as a strategic platform for PRA to further expand into the

larger Indian sub-continent. Underpinned by stable recurring income,

PHB aims at a higher ratio of self-owned properties, moving forward.

• For FY13F, we project a healthy SSSG at 5% for Malaysia and Indonesia,

riding on stable consumer spending. This should cushion a muted

outlook in China and Vietnam given the near-term cyclical SSSG that is in

negative territory.

• FY13F-FY15F growth will be driven by an enlarged network of outlets –

China (FY13F: +8 and FY14F: +5) and Southeast Asia (FY13F: +7 and

FY14F: +8), coupled with the foray into Myanmar and Cambodia. Our

annual new store assumption is at two for each market.

• On a more positive note, the stock is a great play in the Asian consumer

sector. Balance sheet is healthy, with a strong cash pile of RM1.5bil as at

end-1HFY13.

• It is trading at 15x FY14F PE, on par with its 5-year historical mean and at

a 33% discount to local peer AEON Co (M) Bhd’s (AEON Mk Equity, Non-

rated) 20x.

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 2

RE-INITIATE WITH HOLD; FAIR VALUE:

RM4.43/SHARE

We are re-initiating coverage Parkson Holdings Bhd

(PHB), with a HOLD at our fair value of RM4.43/share

based on a sum-of-parts valuation for FY14F.

For FY13F, we project a healthy SSSG at 6% for Malaysia

and Indonesia, riding on stable consumer spending. This

should cushion a muted outlook in China and Vietnam,

given the near-term cyclical SSSG that is in negative

territory.

FY13F-FY15F growth will be driven by an enlarged

network of outlets – China (FY13F: +8 and FY14F: +5) and

Southeast Asia (FY13F: +7 and FY14F: +8), coupled with

the foray into Myanmar and Cambodia. Our annual new

store assumption is at two for each market.

It is trading at 15x PE FY14F, on par with to its 5-year

historical mean and at a 33% discount to local peer AEON

Co (M) Bhd’s (AEON Mk Equity, Non-rated) 20x.

PARKSON OCCUPIES 2.5MIL SQM OF GFA IN

CHINA AND SOUTH EAST ASIA

� Parkson is mushrooming everywhere!

Over the past one year, PHB has been expanding rapidly

in China and Southeast Asia, via its respective 52%-owned

and 68%-owned listed-subsidiaries, Parkson Retail Group

(PRG) and Parkson Retail Asia (PRA). See Table 2.

Since its foray into Indonesia (via Centro & Kem Chick) in

June 2011, PRA has continued with its expansion to the

region’s least developed markets – Vietnam, Sri Lanka (via

Ordel), Myanmar and Cambodia.

PRA had in July 2012 acquired a 47.5%-stake in Odel Plc,

a fashion retailer listed on the Colombo Stock Exchange in

Sri Lanka, and in August 2012 started a joint venture in

Parkson Myanmar with a 70%-stake.

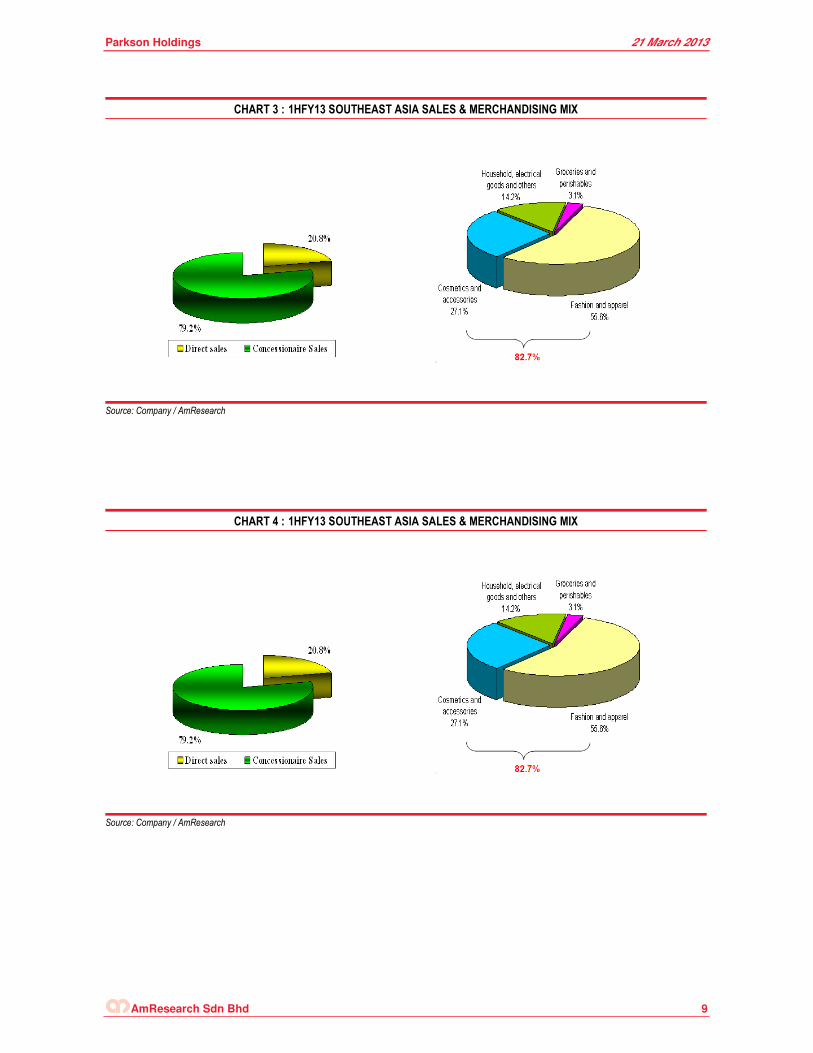

� An asset-light model

PRG and PRA lease premises from mall owners. Given

that the bulk of the group’s business is based on

concessionaire sales (refer to Chart 3 and 4), PHB has

minimal inventory risks. Parkson’s direct sales mainly

constitute cosmetics.

� Well-mapped expansion on track

Three stores in China, which were delayed for opening last

year, are now on track for opening in 2013. To-date, the

Parkson store at Hefei 3 has opened. PRG has another 7

stores in the pipeline for opening in 2013. This will

increase gross floor area (GFA) by 14.7% to 2mil sqm.

PRA’s two new stores – one each in Kuching, Malaysia

and Surakarta, Indonesia – had opened during 1HFY13 in

November 2012. Another five new stores are in the

pipeline by end-FY13F for Southeast Asia – 1 in Malaysia,

2 in Vietnam, 1 in Indonesia and 1 in Myanmar. Hence,

GFA is estimated to rise by 11.4% to 702,000 sq m.

DECELERATION IN CONSUMER SPEND FOR

PARKSON RETAIL GROUP (PRG)

� Weaker-than-expected same store sales growth (SSSG) affected by the weaker consumer spend

Historical lows in SSSG. PHB’s weaker-than-expected

1HFY13 results were affected by a deceleration in

consumer spend, particularly in China and Vietnam. China

and Vietnam have been adversely impacted by slow

economic growth, resulting in weak consumer spend.

Evidently, PRG’s SSSG for 1QFY13 and 1HFY13 slumped

to new historical lows, at 1% and 2% contractions,

respectively. It is worth noting that SSSG during the global

financial crisis in June 2009 was at 4.9%.

Over the past three years, SSSG had remained healthy,

averaging at low-to-mid teens.

� What affected the weakening of PRG’s performance?

Cutting down on corporate gifts. Corporate gifts

constitute c.15% of sales.

Intensification of competition in retail landscape. We

believe the SSSG contraction was also largely attributed to

intensification of competition among the China-based

retailers such as Golden Eagle and Intime. There appears

to be a footfall shift towards more appealing malls amid

their proliferation in numbers.

Parkson undergoes facelifts once every 4-5 years. Stores

in Shanghai and Beijing are currently under

refurbishments.

Start-up losses. Operating losses were incurred in new

stores. In 2012, 4 stores were opened, while 3 stores

delayed opening to this year. In addition, PRG closed 2

stores last year.

� Expansion continues with additional 14.7% and 7.9% of gross floor area for FY13F and FY14F, respectively

PRG has a pipeline of 13 new stores over FY13F-FY14F

(see Table 4).

The GFA is expected to rise by 14.7% on the back of 8

more stores. Five new stores with a total GFA of

164,520sqm (+7.9%) are expected to open in FY14F.

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 3

� Challenging FY13F – growth to be flat at best

Slower rate of expansion. Expansion will continue, but at

a slower pace, targeting five new stores p.a. (vs. 8-10

previously). Management has highlighted that store

expansion will be more selective in China, going forward.

Expansion will centre on cities (80%) in which it is already

present given the ‘know-how attained’, while the remaining

20% of the expansion will be in cities new to the group.

We are uncertain about China’s turnaround in SSSG,

given that the key issue stems from an increased

competitive landscape. We believe China’s 3Q SSSG

growth would remain flat, at best, and any recovery will be

gradual.

Hence, we have assumed a contraction of 2% in SSSG for

FY13F and a mild rebound to +1% for FY14F.

Product differentiation and merchandising mix. PRG is

focus on improving the merchandising mix based on

individual cities’ preferences to circumvent the slowdown in

SSSG.

Online shopping presence. PRG started e-commerce in

November 2012 for goods sold at Parkson, to mitigate the

rising popularity of online retailers. Response has been

rather slow as shoppers are unaware of this service.

Therefore, PRG will be actively promoting the e-commerce

site in the next 1-2 years.

Higher self-owned property ratio. Apart from just

expanding via new outlets, PRG aims at a higher ratio of

self-owned properties, underpinned by stable recurring

income. PHB targets to own 1 mall for every 4 malls

operated.

PRG will continue to be on a lookout for third-party stores

or properties for acquisition and greenfield malls.

The Qingdao acquisition last year for a site to build a

shopping mall will be ready in 2-3 years’ time.

PARKSON RETAIL ASIA’S (PRA) CONTINUOUS

EXPANSION IN SOUTHEAST ASIA

PRA’s expansion strategy in Southeast Asia is through

physical store openings, which are facilitated by

partnerships with property developers or the acquisition of

existing retail businesses.

Besides having 39 stores in Malaysia, PRA is present in

Vietnam, Indonesia (via Parkson/Centro) and Sri Lanka

(via Odel) with 8, 9 and 17 stores, respectively.

Since its foray into Indonesia in June 2011, PRA’s

expansion in Southeast Asia has take it to the region’s

least developed markets, such as Vietnam, Cambodia, Sri

Lanka and Myanmar.

Given the region’s fast-emerging middle-class, PRA is on a

constant lookout for opportunities to enter into other

Southeast Asia markets.

� Parkson Malaysia, the second largest revenue contributor, with market share of c.20%

The group’s biggest markets. Malaysia is the second

largest contributor to the group at c.26% of revenue,

followed by China. Parkson Malaysia is the second-largest

department store operator in the country commanding a

20% market share, after The Store Corp.

Sustaining a healthy SSSG growth. We have assumed

SSSG growth of 5% each for FY13F and FY14F, riding on

a buoyant consumer spending.

PRA’s pipeline for Malaysia is to open 2 stores each in

FY13F and FY14F (+>20,000sqm). So far, Plaza Merdeka,

Kuching had opened its doors in November 2012.

Introduction of e-commerce. In October 2012, similar to

Parkson China, Parkson Malaysia had introduced an e-

commerce portal.

� Indonesia’s growth to remain buoyant at favourable and stable SSSG

Via Centro department store. In June 2011, PRA made

its foray into Indonesia through the acquisition of Centro

Department Store from Indonesia’s Sentosa Group. PRA

owns 9 stores (8 Centro and 1 Kem Chick), spanning

across Indonesia.

Dual branding strategy to continue. The group intends

to continue its dual branding in Indonesia – Centro targets

at the low-middle income, while Parkson targets the upper-

middle.

Given Parkson's premium brand compared to Centro, the

former’s expansion will be concentrated in the first-tier

cities such as Jakarta, Medan and Surabaya.

There is no plan to convert the Centro brand to Parkson for

the time being. Nonetheless, the group could potentially

convert some Centro stores into Parkson in due course

should the population becomes even more affluent.

Stable SSSG. Backed by strong domestic consumption in

Indonesia coupled with a growing middle to upper class,

we have assumed a stable SSSG of 5% respectively for

FY13F and FY14F.

Centro at Surakarta opened in November 2012, and

another Centro is targeted to open in FY13F. Parkson’s

full-fledged store is earmarked to open in FY14 at St.

Moritz 2, Jakarta, and occupying 17,101 sq m. The

remaining two stores for FY14F are under Centro.

� Slower growth in Vietnam translates into continued weakness in SSSG

No sign of recovery in the short term. Vietnam recorded

a negative SSSG in 1HFY13. This was underpinned by an

overall negative growth in Vietnam owing to the policies

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 4

implemented by the government to manage inflation and

reduce the trade deficit.

As a result, this has led to a slower economic growth in the

country. The Vietnamese economy could see some

improvements in the next 1-2 years.

SSSG to possibly turn positive in FY14F. Vietnam

SSSG contracted by 6.3% and 7.4%, for 1QFY13 and

1HFY13, respectively. Note that 9% SSSG was achieved

in FY12.

Management expects a flat SSSG growth (or a possible

contraction) in FY13F amid a weakening Vietnamese

economy. Nonetheless, they foresee a potential recovery

in SSSG in FY14F.

As such, we forecast SSSG in Vietnam to contract by 5%

in FY13F and to register a zero SSSG growth in FY14F, in

view of a slight recovery in the economy.

But, nothing is stopping new store openings.

Underpinned by a potential recovery in the Vietnamese

economy in the next 1-2 years, the group has four

confirmed new stores over FY13F-FY14F (2 stores for

each FY) – three in Ho Chi Minh and one in Danang.

These would contribute an additional 75,484 sq m of GFA.

For now, PRA is focused on store refurbishments and

renovations, along with securing good locations at good

rental rates.

� Leveraging on experience in Vietnam to push into Myanmar market

First Parkson store in Myanmar earmarked for April.

The first store will be in Yangon (commercial city of

Myanmar) occupying a GFA of 4,000 sq m. This small

Parkson store is located in Yoma’s FMI Centre, a 12-storey

commercial building located in Yangon’s up-market

Pabedan Township.

JV with established local real estate players. PRA owns

a 70%-stake in Parkson Myanmar, with Yoma Strategic

Holdings Ltd (20%) and First Myanmar Investment

Company Ltd (10%) holding the balance. These partners

are well-established players in the local real estate

landscape.

Penetrating into untapped Myanmar with less risks.

The JV enables PRA to establish and expand its Parkson

network across Myanmar. Given the group’s first-mover

advantage in the rapidly-growing retail sector, the JV is a

positive. This is further underpinned by a largely under-

served middle- to upper-income segment.

Gradual expansion. Before venturing further in Myanmar

or eventually having a full-fledged Parkson store in 2-3

years, this first store will enable PRA to survey and gauge

the market’s retail preferences.

� Not lagging behind, Cambodia is next!

As growth in Southeast Asia is leaning towards the less

developed countries, PRA’s first Parkson in Cambodia’s

capital city of Phnom Penh will open in FY14F, with a total

GFA of 36,500 sq m.

� First foreign retailer to enter Sri Lanka, with Odel Plc buy (47.6%-owned)

Leveraging on Odel’s retail experience. PRA made a

maiden entry into Sri Lanka via the acquisition of 47.5% of

retailer Odel Plc last year. This will be a strategic platform

for the group to further expand into the larger Indian sub-

continent.

Odel has 17 stores with a total 150,000 sq f of floor space

and an online shopping website.

A good strategy to shorten learning curve. PRA intends

to eventually set up a Parkson departmental store upon

the understanding of the Sri Lankan market. Expansion

plans in Sri Lanka or in other India sub-continent markets

are likely to be rolled out in 1-2 years’ time through store

openings and development of its own floor space.

No change to business model for now. The group does

not intend to change Odel’s business model. Nonetheless,

similar to PRA’s strategy in Indonesia, we believe PRA has

the ability to propel Odel one level up by developing the

brand.

Potential upside to spur earnings. Given PRA’s track

record in managing Centro in Indonesia, we see a potential

upside in Odel’s earnings growth. As such, we have

assumed a 5% SSSG.

PARKSON HOLDINGS (PHB) AIMS TO OWN

MORE MALLS

� Complex management provides stable recurring income

Presently, KL Festival City (99% occupancy rate) is the

only mall in PHB’s portfolio. Meanwhile, the upcoming

second mall is located in Malacca. It is expected to be

ready within 2-3 years at a total cost of RM400mil.

Under PHB’s mall concept, Parkson department store will

remain as an anchor tenant and the remaining retail space

will be leased to third-party retailers.

PHB targets to have an enlarged number of shopping

malls, going forward. The group’s experience in running

departmental stores should provide an advantage to it

being a mall owner.

Despite a small contribution from the shopping mall

management arm (c.1% of group revenue) for now, it is

seen as a growing earnings stream.

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 5

� Targets to own 1 out of 4 malls PHB operates

The group is on a constant lookout for opportunities for

greenfield malls. Having said, PHB is open to acquiring

existing malls and refurbish them, if feasible.

More importantly, PHB targets to own 1 out 4 malls in

which it is operating.

� A possible REIT-ing of own malls?

Given PHB’s preference for an asset-light business model,

a possible REIT structure could take-off in the foreseeable

future. This is feasible upon PHB owning at least 5 malls

and the income stream becoming considerable large.

FINANCIALS

� Overall positive SSSG assumption

PHB’s earnings growth is underpinned by expansion in its

gross floor area (GFA) and healthy same store sales

growth:-

(1) Continued expansion in GFA of a minimum of 10%-

15% per annum, supported by a pipeline of new store

openings. The group has earmarked 15 and 13 new

stores for FY13F and FY14F, respectively.

(2) Enlarged network of outlets – China (FY13F: +8 and

FY14F: +5) and Southeast Asia (FY13F: +7 and

FY14F: +8) coupled with forays into Myanmar and

Cambodia. Our annual new store assumption is at 2

for each market.

(3) We assume healthy SSSG for Malaysia and

Indonesia, riding on a buoyant consumer spending.

This should cushion a muted outlook in China and

Vietnam, given the near-term cyclical SSSG that is

presently in negative territory.

(4) Stable margins from a lucrative concessionaire-based

business model. Concessionaire sales constitute the

bulk of the group’s revenue (PRG: 90%, PRA: 80%)

(5) Small but growing earnings stream from its shopping

complex management arm in KL Festival City.

Meanwhile, the total merchandise margin should remain

flattish at c.19%. Fashion & apparel and cosmetic &

accessories are expected to dominate the group’s revenue

at between 80%-90%.

� Strong balance sheet, huge cash pile

Balance sheet remains healthy with a strong cash pile of

RM1.5bil as at end-1HFY13.

� 1HFY13 disappointed, owing to decelerating consumer spend in China

1HFY13 revenue grew 3% YoY attributed to new stores

contributions and positive SSSG in Malaysia (4%) and

Indonesia (7%).

However, given the slow economic growth in Vietnam and

China, which resulted in weak consumer spend. As such,

SSSG for Vietnam and China were in negative territory of

7% and 2%, respectively.

Further to that, consumer spending was delayed in

2QFY13 due to late arrival of the Lunar New Year.

Compared to 2QFY12, the Lunar New Year spend was

mainly captured at that point.

One-off items such as acquisition and start-up costs

arising from the e-commerce venture had also contributed

to a weaker 1HFY13.

� No official dividend policy

PHB has no official dividend policy. Since FY11, the group

has maintained a payout of at least 40% of earnings.

In light with the historical payout ratio, we have assumed

the same for FY13F-FY15F. This translates into DPS 2.6

sen and 3.2 sen, respectively, for FY13F and FY14F.

� Key catalysts

Other key catalysts:-

(1) Recovery in consumer spend in China and

Vietnam;

(2) Faster-than-expected new store openings; and

(3) Better-than-expected cost management

initiatives.

KEY RISKS

Key risks include:-

(1) Significant slowdown in consumer spending in all

countries – China, Malaysia, Indonesia, Vietnam,

Cambodia and Sri Lanka;

(2) Delay in commencement of store openings; and

(3) Higher-than-expected costs for new stores, e-

commerce and JVs.

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 6

VALUATIONS

� Re-initiate with a HOLD; fair value: RM4.43/share

We are re-initiating coverage on Parkson Holdings Bhd

(PHB), with a HOLD at a fair value of RM4.43/share,

based on a sum-of-parts valuation for FY14F.

For FY13F, we project a healthy SSSG at 6% for Malaysia

and Indonesia, riding on stable consumer spending. This

should cushion a muted outlook in China and Vietnam,

given the near-term cyclical SSSG that is in negative

territory.

FY13F-FY15F growth will be driven by an enlarged

network of outlets – China (FY13F: +8 and FY14F: +5) and

Southeast Asia (FY13F: +7 and FY14F: +8), coupled with

the foray into Myanmar and Cambodia. Our annual new

store assumption is at two for each market.

It is trading at 15x PE FY14F, on par with to its 5-year

historical mean and at a 33% discount to local peer AEON

Co (M) Bhd’s (AEON Mk Equity, Non-rated) 20x.

TABLE 1 : SUM-OF-PARTS VALUATION BASED ON FY14F

Stake %

Valuation

multiple (x)

Value

(RMmil)

Parkson Retail Group 51.5 10.0 2,075.6

Parkson Retail Asia 67.6 11.0 985.2

Total 3,060.7

Net cash/(debt) 2,013.5

Total 5,074.2

Share capital (mil) 1,145.4

Discount factor 0.0

Fair value (RM/share) 4.43

Upside/(downside) to current share price (%) (4.5)

Source: Company / AmResearch

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 7

TABLE 2 : PHB STRUCTURE

Source: Company / AmResearch

TABLE 3 : GROSS FLOOR AREA AND OPERATING AREA

Source: Company / AmResearch

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 8

CHART 1 : 1HFY13 PHB REVENUE BREAKDOWN

Malaysia

26%

China66%

Vietnam

3%

Indonesia

4%

Property &

investment holding1%

Source: Company / AmResearch

CHART 2 : 1HFY13 PHB EBIT BREAKDOWN

Malaysia21%

China75%

Vietnam1%

Indonesia3%

Property & investment holding

0%

Source: Company / AmResearch

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 9

CHART 3 : 1HFY13 SOUTHEAST ASIA SALES & MERCHANDISING MIX

Source: Company / AmResearch

CHART 4 : 1HFY13 SOUTHEAST ASIA SALES & MERCHANDISING MIX

Source: Company / AmResearch

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 10

TABLE 4 : CHINA EXPANSION PLAN

Source: Company / AmResearch

TABLE 5 : SOUTHEAST ASIA EXPANSION PLAN

Source: Company / AmResearch

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 11

CHART 5 : B BAND CHART

0.0

1.0

2.0

3.0

4.0

5.0

Mar-08

Jun-08

Sep-08

Dec-08

Mar-09

Jun-09

Sep-09

Dec-09

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

(x)

CHART 6 : PE BAND CHART

1.0

2.2

3.4

4.6

5.8

7.0

8.2

9.4

10.6

11.8

13.0

14.2

15.4

16.6

17.8

19.0

20.2

21.4

22.6

Mar-10

Jun-10

Sep-10

Dec-10

Mar-11

Jun-11

Sep-11

Dec-11

Mar-12

Jun-12

Sep-12

Dec-12

Mar-13

(x)

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 12

TABLE 6 : FINANCIAL DATA

Income Statement (RMmil, YE 30 Jun) 2011 2012 2013F 2014F 2015F

Revenue 2,925.4 3,447.5 3,592.2 4,333.3 4,975.0

EBITDA 971.3 1,026.5 1,000.8 1,121.6 1,188.9

Depreciation (141.6) (190.9) (240.8) (250.3) (258.5)

Operating income (EBIT) 829.7 835.6 760.0 871 930.4

Other income & associates 0.1 0.2 1.5 1.5 1.5

Net interest (24.6) 51.9 14.5 28.9 56.3

Exceptional items 0.0 0.0 0.0 0.0 0.0

Pretax profit 805.3 887.7 776.0 901.7 988.2

Taxation (198.6) (219.0) (194.0) (225.4) (247.1)

Minorities/pref dividends (258.2) (289.5) (315.6) (344.0) (375.0)

Net profit 348.4 379.2 266.4 332.3 366.2

Core net profit 348.4 379.2 266.4 332.3 366.2

Balance Sheet (RMmil, YE 30 Jun) 2011 2012 2013F 2014F 2015F

Fixed assets 1,557.2 1,686.3 1,765.6 1,835.3 1,895.8

Intangible assets 1,235.1 1,309.5 1,375.0 1,375.0 1,376.0

Other long-term assets 517.9 905.2 699.6 699.6 536.5

Total non-current assets 3,310.2 3,901.0 3,840.1 3,909.8 3,808.3

Cash & equivalent 2,740.6 3,031.0 2,813.2 3,277.0 3,773.0

Stock 246.4 281.7 298.2 369.6 435.7

Trade debtors 362.6 573.4 482.2 581.7 667.9

Other current assets 604.4 0.0 9.8 9.8 9.8

Total current assets 3,954.1 3,886.1 3,603.4 4,238.1 4,886.4

Trade creditors 1,702.9 2,043.2 1,576.2 1,953.4 2,302.7

Short-term borrowings 1,189.0 0.2 0.2 0.2 0.2

Other current liabilities 46.8 45.1 46.9 46.9 46.9

Total current liabilities 2,938.7 2,088.5 1,623.2 2,000.5 2,349.8

Long-term borrowings 761.4 1,260.6 1,060.6 860.6 660.6

Other long-term liabilities 194.7 222.8 264.2 457.1 507.3

Total long-term liabilities 956.1 1,483.4 1,324.9 1,317.7 1,167.9

Shareholders’ funds 2,228.2 2,680.2 2,837.6 3,039.3 3,242.2

Minority interests 1,141.4 1,535.0 1,657.8 1,790.5 1,933.7

BV/share (RM) 2.07 2.46 2.61 2.79 2.98

Cash Flow (RMmil, YE 30 Jun) 2011 2012 2013F 2014F 2015F

Pretax profit 805.3 887.7 776.0 901.7 988.2

Depreciation 141.6 190.9 240.8 250.3 258.5

Net change in working capital 62.4 94.3 (392.4) 206.4 197.1

Others (252.1) (271.5) (195.5) (226.9) (248.6)

Cash flow from operations 757.1 901.4 428.9 1,131.4 1,195.3

Capital expenditure (196.6) (324.1) (320.0) (320.0) (319.0)

Net investments & sale of fixed assets 22.8 (30.0) (30.0) (30.0) (30.0)

Others (8.8) (211.3) 0.0 0.0 0.0

Cash flow from investing (182.6) (565.4) (350.0) (350.0) (349.0)

Debt raised/(repaid) (934.4) 499.2 (200.0) (200.0) (200.0)

Equity raised/(repaid) 0.0 0.0 0.0 0.0 0.0

Dividends paid (283.5) (362.1) (108.8) (130.6) (163.2)

Others 1,170.2 (350.9) 10.5 11.5 11.5

Cash flow from financing (47.7) (213.7) (298.3) (319.1) (351.7)

Net cash flow 526.8 122.3 (219.4) 462.3 494.5

Net cash/(debt) b/f 1,461.2 (377.0) (19.4) 662.3 694.5

Net cash/(debt) c/f 786.5 1,770.3 1,752.4 2,416.2 3,112.3

Key Ratios (YE 30 Jun) 2011 2012 2013F 2014F 2015F

Revenue growth (%) 7.5 17.8 4.2 20.6 14.8

EBITDA growth (%) 9.6 5.7 n/a 12.1 6.0

Pretax margins (%) 27.5 25.7 21.6 20.8 19.9

Net profit margins (%) 11.9 11.0 7.4 7.7 7.4

Interest cover (x) 33.7 n/a n/a n/a n/a

Effective tax rate (%) 24.7 24.7 25.0 25.0 25.0

Net dividend payout (%) 48.5 60.1 40.8 39.3 44.6

Debtors turnover (days) 45 50 54 45 46

Stock turnover (days) 29 28 29 28 30

Creditors turnover (days) 206 198 184 149 156

Source: Company, AmResearch estimates

Parkson Holdings 21 March 2013

AmResearch Sdn Bhd 13

Anchor point for disclaimer text box

Published by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

Printed by

AmResearch Sdn Bhd (335015-P) (A member of the AmInvestment Bank Group) 15 t h F l oo r B a ng un an A mB a n k Gr o u p 55 Jalan Raja Chulan 50200 Kuala Lumpur Tel: ( 03 ) 2 07 0- 2 4 4 4 ( r e sea rc h ) F a x: ( 03 ) 2 07 8- 3 1 6 2

The information and opinions in this report were prepared by AmResearch Sdn Bhd. The investments discussed or recommended in this report may not be suitable for all investors. This report has been prepared for information purposes only and is not an offer to sell or a solicitation to buy any securities. The directors and employees of AmResearch Sdn Bhd may from time to time have a position in or with the securities mentioned herein. Members of the AmInvestment Group and their affiliates may provide services to any company and affiliates of such companies whose securities are mentioned herein. The information herein was obtained or derived from sources that we believe are reliable, but while all reasonable care has been taken to ensure that stated facts are accurate and opinions fair and reasonable, we do not represent that it is accurate or complete and it should not be relied upon as such. No liability can be accepted for any loss that may arise from the use of this report. All opinions and estimates included in this report constitute our judgement as of this date and are subject to change without notice.

For AmResearch Sdn Bhd

Benny Chew Managing Director