Retailing in China: Successfully Navigating China Customs ... · PDF fileRetailing in China:...

45

Retailing in China: Successfully Navigating China Customs & CIQ Requirements New York January 2013 www.pwccustoms.com

-

Upload

nguyendieu -

Category

Documents

-

view

223 -

download

0

Transcript of Retailing in China: Successfully Navigating China Customs ... · PDF fileRetailing in China:...

Retailing in China: Successfully Navigating China Customs & CIQ Requirements

New York January 2013

www.pwccustoms.com

PwC

Introductions and Contacts

China US

2

Hugo Hu Manager, China

Tel: 86 21 2323 8071

Damon Paling Partner, China

Tel: 86 21 2323 2877

Anthony Tennariello Partner, New York

Tel: 646 471 4087

Maytee Pereira Director, New York

Tel: 646 471 0810

PwC

Agenda

1. Warm up!

2. Business model trends

3. Regulatory outlook

4. Major Customs and CIQ regulatory risks and best-practice solutions

5. Managing your Customs Brokers

6. Benchmarking your cross-border supply chain efficiency

7. Managing return to overseas

8. Sourcing and First Sale

3

PwC

Warm up!

PwC

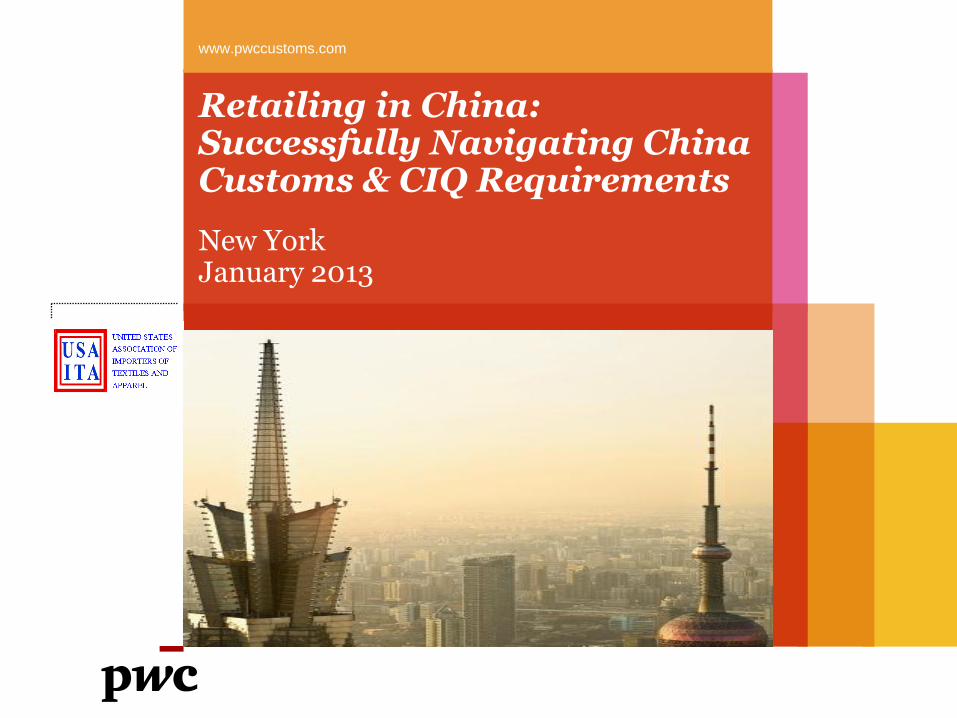

Warm-up! Macroeconomics

5

China is now the largest global exporter and the second-largest importer next to the US.

Since joining the WTO almost 11 years ago, the average duty rate fell from 15.8% to 9.8%.

Exports remain weak and the textile industry is plagued with slow demand from the US/EU. Did China meet their 2012 7.5% growth target?

The Yuan hit a 19 year high against the USD in October 2012, rising to the upper trading limit set by the Central Government.

New leadership, Xi Jinping, rumored to lead more measures to boost domestic demand.

China to be an “upper-middle income” economy by 2020 with GDP over $10,000.

PwC

Warm-up! Current environment & trends

6

Franchise businesses & China’s luxury market expanding rapidly.

FIEs are facing fierce competition in Tier 1 cities; now targeting sales in Tier 2 and 3 cities.

Gap Inc. has 45 retail stores in China by the end of year, and planned opening of 4 Outlet stores in China.

A multi channel retailing strategy is essential to success.

Consumers becoming sophisticated and brand loyal- ensure to adopt the right brand strategy for the market.

Retailers setting up their own logistics facilities to enhance sustainability.

PwC

Warm-up! Ecommerce

7

China to be the largest ecommerce market by 2015 at about 350 billion USD.

Tier 1 consumers are looking for brands not available in China; tier 2 & 3 city consumers are looking for brands not yet available in their city. Zara, who has already

opened 100 stores in Mainland since 2006, launches their online site in September 2012.

Internet reach to consumers quickly outpacing physical retail consolidation.

Online sales grew at 140% each year since 2004, making it a powerhouse driver of domestic consumption.

PwC

Business Model Trends

PwC

Business Model Trends - Overview • Transition away from 3rd party distributors to related party

distributors (involving license buy-back)

• Using an I/E Agent at start-up stage and gradually import under its own name (i.e. acting as Import-of-Record)

• Still tend to round-trip through Regional Distribution Centre (“RDC”) or Overseas Principal, but China-to-China start being more and more popular

• Use of FICE to clear goods through multiple gateway ports

• Register at Port of Entry; clear at destination Port

o Registration at Port of Entry (e.g. Pudong Airport)

o Clearance and pay duties at destination Port (e.g. Beijing and Shenzhen)

9

PwC

Business Model Trends – Import Model

• 31% of fashion retailers still use an I/E agent to act as their IoR.

• It is the industry trend for companies to act as their own IoR.

• Companies wish to tighter operational control (including forex remittance) and save service provider costs by moving certain functions in-house.

• The results of fashion retail industry is quite consistent with other industries.

10

Fashion Retail Industry

Other Industries

69%

31% Yes

No

77%

23%

Yes

No

PwC

Business Model Trends – Regional Distribution Centre • Based on a PwC survey in 2012, more

than 40% of the fashion retailers have not yet set up a RDC in Asia

• Nearly 60% of the retailers are now operating a DC in Hong Kong, Singapore or China.

• Fashion retail sector now considers that Asian market to be of strategic importance.

• Mainland China is a preferred destination for establishment of a RDC as operating costs (storage and labor) are typically lower than HK/Singapore.

11

26%

33%

41%

HK/Singapore

China

PwC

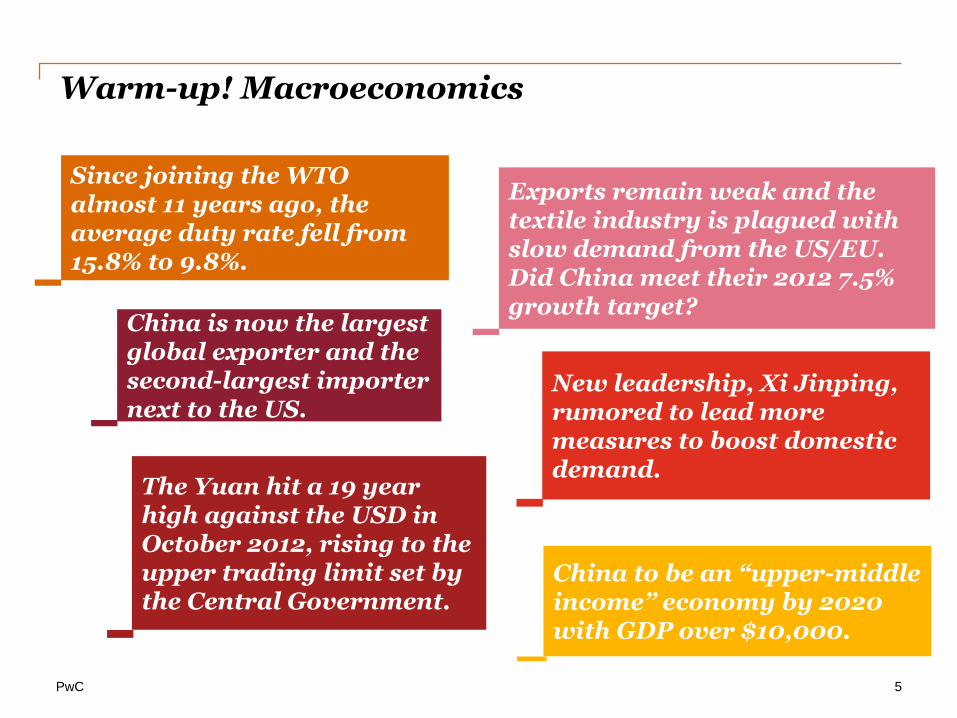

Business Model Trends – Regional Headquarter

12

Retail Stores China

FICE/WFOE Overseas

Headquarter in EU or the US

Regional Headquarter

(share service)

Retail Store (Brand A)

Retail Store

(Brand B)

Retail Store

(Brand C)

Retail Stores China

FICE/WFOE Overseas

Headquarter in EU or the US

Brand A

Retail Store

(Brand A)

Retail Store

(Brand A)

Brand B Retail Store

(Brand B)

PwC

Regulatory outlook

PwC

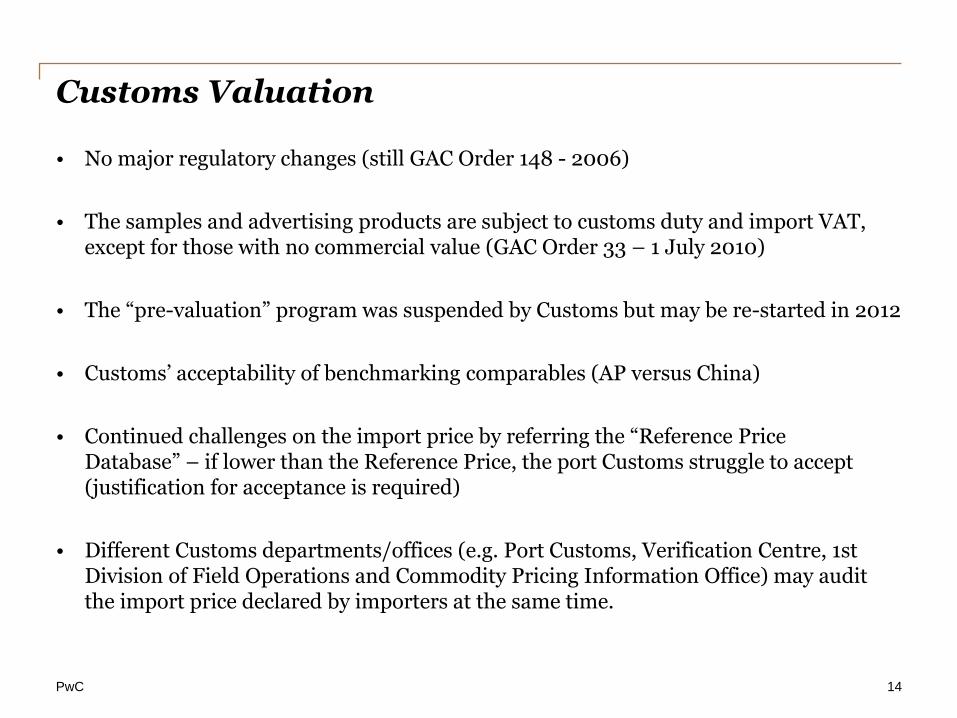

Customs Valuation

• No major regulatory changes (still GAC Order 148 - 2006)

• The samples and advertising products are subject to customs duty and import VAT, except for those with no commercial value (GAC Order 33 – 1 July 2010)

• The “pre-valuation” program was suspended by Customs but may be re-started in 2012

• Customs’ acceptability of benchmarking comparables (AP versus China)

• Continued challenges on the import price by referring the “Reference Price Database” – if lower than the Reference Price, the port Customs struggle to accept (justification for acceptance is required)

• Different Customs departments/offices (e.g. Port Customs, Verification Centre, 1st Division of Field Operations and Commodity Pricing Information Office) may audit the import price declared by importers at the same time.

14

PwC

Free Trade Agreement

• Strong FTA network within Asia-Pacific Region • China and the US still do not have a plan for negotiating a FTA

• China and EU still do not have a plan for negotiating a FTA

• China government and Swiss government are negotiating a bilateral FTA

• Operational issues

Shipping products through an RDC in China may cause them to lose

their eligibility for reduced duty rates when imported into the ultimate destination market.

3rd party invoicing through the Headquarter in the US

15

PwC

Tariff Classification

• Regulatory change on HS Classification in 2011 provided clearer explanation on the application of General Rule of Interpretation.

• HS 2012 was implemented in China on 1 January 2012. 14 changes relate to textile products

5 changes relate to accessories of base metal

• Customs not only conduct audit on the HS codes for imports, but also focus on the HS codes for exports as they relate to VAT refund and licensing requirements.

• Pre-classification ruling issued by Shanghai Customs is still not easy to obtain.

• Importers tend to engage the customs brokers approved by Customs (e.g. 20 brokers in Shanghai were authorized) for obtaining a tariff classification opinion.

16

PwC

Major Customs and CIQ regulatory risks and best-practice solutions

PwC

Major Customs and CIQ regulatory risks

Relatively high customs duties and consumption taxes!

• High tariff rates for apparel products (14% - 25%), accessories (6.5% - 35%).

• Due to the high tariff rates, the fashion retail industry is the main target for Customs.

• No Free Trade Agreement (“FTA”) opportunity for EU/US fashion.

• Main challenges are around tariff classification and customs valuation :

Tariff classification: not only relates to determine tariff rates, but also relevant to non-tariff measures

Customs valuation: Incoterms, arm’s length pricing and payments for intangibles

• Customs audit profile:

Periodical customs audit on import price

Multiple customs departments/offices may audit the importers at the same time

18

PwC

Customs best-practice solutions

• Customs Valuation

o Prepare defense documentation to show arm’s length pricing

o Check for any prescribed adjustments to the declared Transaction Price

o Voluntarily discuss with Customs valuation issues in order to manage risks, ensure compliance, and control the landed cost

• Tariff Classification

o Translate the existing HS Codes of the exporting country/area into the corresponding China HS Code per the PRC Tariff Book

o Watch out for translation issues and variations in nomenclature

o Seek a pre-classification decision with Customs for goods where the HS Code determination is complex

19

PwC

Major Customs and CIQ regulatory risks and best-practice solutions (Cont’d)

Lead time is crucial for fashion apparel industry!

• Customs brokers are engaged to facilitate the import/export -> periodical broker review and evaluation are essential to:

achieve trade compliance

enhance faster customs clearance by way of simplified procedures.

• Enterprise classification rating is an important criteria for achieving speedy clearance.

• Customs’ reform on paperless declaration which could significantly reduce the lead time for customs clearance.

• Whenever Customs inquiries technical issues such as tariff classification and valuation, “cash deposit mechanism” can be adopted to clear the goods timely and minimise the impact for daily import operation.

20

PwC

Major Customs and CIQ regulatory risks (Cont’d)

Non-tariff measures are complicated and costly!

• In theory, most of the License A apparel products (app. 301 apparel items under Chapters 61 and 62 – please see handout) are subject to 100% statutory inspection.

• Product quality as well as labelling are the two focuses for CIQ and other government bureaus – please see next slide for some extracts of industry news

• The quality criteria and testing procedures etc. are referred to relevant national standards (GB) which change in a regular basis.

• In practice, inspection of the same product that is routinely imported may take place.

• Clearance time of goods could be largely affected if sample testing is required for the products - normally takes up to app. 30 days.

• Complicated procedures for disposal of disqualified products.

• CITES application is time-consuming and involving different levels of government authorities.

21

PwC

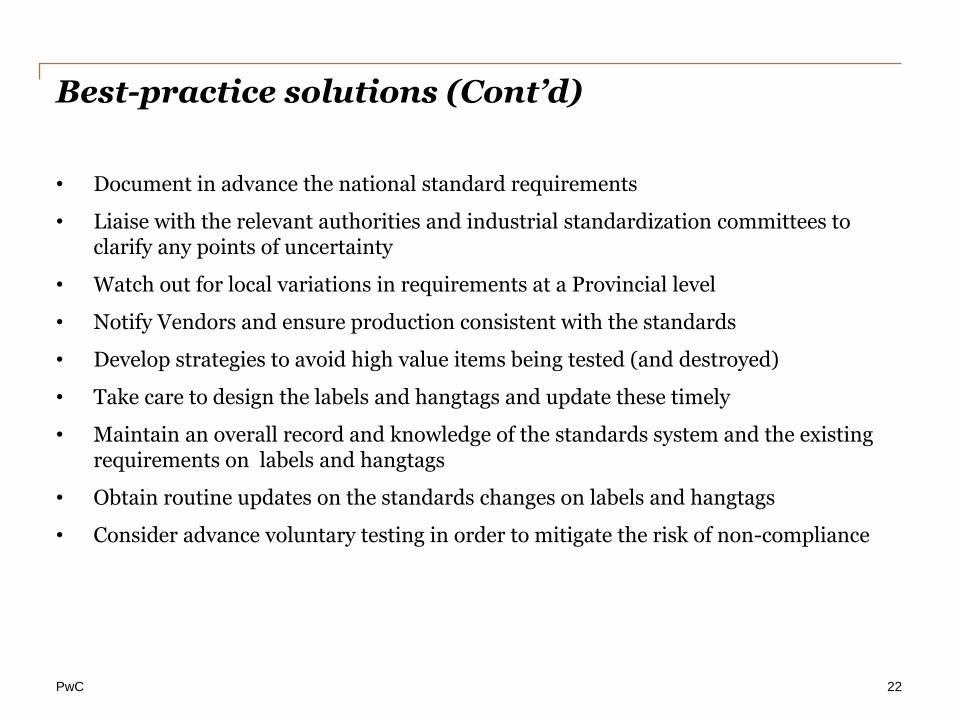

Best-practice solutions (Cont’d)

• Document in advance the national standard requirements

• Liaise with the relevant authorities and industrial standardization committees to clarify any points of uncertainty

• Watch out for local variations in requirements at a Provincial level

• Notify Vendors and ensure production consistent with the standards

• Develop strategies to avoid high value items being tested (and destroyed)

• Take care to design the labels and hangtags and update these timely

• Maintain an overall record and knowledge of the standards system and the existing requirements on labels and hangtags

• Obtain routine updates on the standards changes on labels and hangtags

• Consider advance voluntary testing in order to mitigate the risk of non-compliance

22

PwC

Latest Updates on Standards

23

Standard No. Standard Title Replaced Standard No.

Effective Date

SB/T 10782-2012 Service specification for sales of clocks and watches

N/A Dec 1, 2012

SB/T 10785-2012 Quality requirements for ironing suits and trousers

N/A Dec 1, 2012

SB/T 10787-2012 Acceptance testing specifications for textile products

N/A Dec 1, 2012

SB/T 10472-2012 Technical requirements for commodity checking of indoor decorative textiles

SB/T 10472-2008 Dec 1, 2012

SB/T 10473-2012 Technical requirements for commodity checking of baby clothes

SB/T 10473-2008 Dec 1, 2012

PwC

Stories of failure to meet labelling requirement

24

Incorrect safety category: should be Category A (infant

products), not Category B (direct

skin contact)

PwC

CIQ Pre-Testing Program 2012

• CIQ “pre-testing” program (2012) in Shanghai

Under the pilot program, goods are to be “pre-tested” at the Shanghai CIQ lab, and a “pre-testing certificate” is issued.

This program is supported by JinAn Government for speeding up goods inspection and clearance time.

• Current 10 participants:

Chanel Ermenegildo Zegna

Prada Richemont

Christine Dior Alfred Dunhill

Bally Givenchy

Nike Salvatore Ferragamo

Adidas Celine

Mango

25

PwC

Managing your Customs Brokers

PwC

Broker Management

27

• The Customs Broker’s principal role of assisting with the cross border clearance of goods as the agent of an importer/exporter means they provide a key link with Customs and other authorities.

• The IoR/EoR shall assume joint liability together with the Customs Broker for the short-payment and violations due to mis-declaration, even if the mistake was made by Customs Broker.

• Periodical broker review and evaluation should be conducted to ensure the customs compliance levels and improve the broker service quality.

• Rationalization of the number of Customs Brokers used in order to strengthen customs compliance levels, save costs, and increase overall operating efficiency.

PwC

Broker Management (Cont’d)

28

• The technical knowledge and competence levels of Customs Brokers varies greatly, ranging from highly trained specialists to unskilled clerical assistants

• The internal controls and standard operating procedures of Customs

• Brokers vary greatly, ranging from best-in-class to non-existent

• Key decisions may be taken by junior staff with insufficient knowledge, with their focus being on minimizing clearance times rather than compliance

• So-called “informal solutions” and “informal arrangements” may exist

Challenges Non-compliance Risks

• Seizure of goods

• Interruption to the supply chain and consequent production delays

• Additional assessment duty, interest and financial penalty

• Clearance under cash deposit

• Negative publicity

• Damage to company reputation

PwC

Broker Management (Cont’d)

29

• Certain key criteria should be considered to determine the broker qualification, for example, Clearance lead time Quality Cost premium Similar experience Flexibility Customs categories Customer service Supporting function Compliance level Local Customs relationship Data system and data management.

PwC

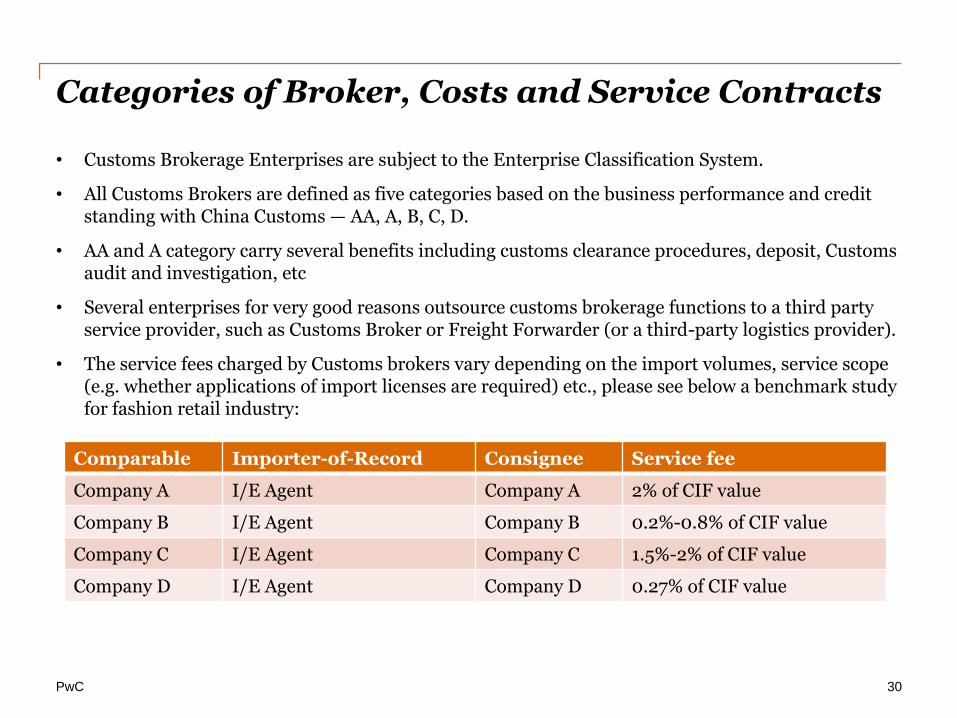

Categories of Broker, Costs and Service Contracts

30

• Customs Brokerage Enterprises are subject to the Enterprise Classification System.

• All Customs Brokers are defined as five categories based on the business performance and credit standing with China Customs — AA, A, B, C, D.

• AA and A category carry several benefits including customs clearance procedures, deposit, Customs audit and investigation, etc

• Several enterprises for very good reasons outsource customs brokerage functions to a third party service provider, such as Customs Broker or Freight Forwarder (or a third-party logistics provider).

• The service fees charged by Customs brokers vary depending on the import volumes, service scope (e.g. whether applications of import licenses are required) etc., please see below a benchmark study for fashion retail industry:

Comparable Importer-of-Record Consignee Service fee

Company A I/E Agent Company A 2% of CIF value

Company B I/E Agent Company B 0.2%-0.8% of CIF value

Company C I/E Agent Company C 1.5%-2% of CIF value

Company D I/E Agent Company D 0.27% of CIF value

PwC

Sample service fee charges of brokers

31

Item Broker A (RMB) Broker B (RMB)

Customs declaration 350 350

Customs declaration forms 200 for 20 HS codes 200 for 20 HS codes

Customs inspection Charge per outlay 200

Customs inspection service fee 240 (if any) 200 (if any)

CIQ process fee 200 50

CIQ inspection fee Charge per outlay n/a

CIQ inspection service fee 240 200

Delivery order switching At cost n/a

Carrier surcharge At cost At cost

CITES application cost 1.5% of CIF value 1.5% of CIF value

CITES collection card At cost 0

CITES application service fee 600/certificate 1,100/certificate

Master file management cost 1,600 per file 0

PwC

Innovation of brokerage system

32

1. Master File management

Pre-classification

Commodity Database

Declaration requirements

Licensing requirements

2. Document production

Automatic translation

Consolidation Automatic sequencing

Automatic separation of Certificate A and non-A

3. Paperless declaration

Data pre-entry Document uploading

Data processing

Document approval

4. KPI report and record

tracking

Customs clearance time

CIQ clearance time

CIQ Sample Testing (if

any)

Delivery to labelling

warehouse

PwC

Benchmarking your cross-border supply chain efficiency

PwC

Customs Enterprise Categories and Clearance Procedures

Category Clearance Procedures

AA • Eligible for convenient clearance procedures of a Category A enterprise, plus expedited procedures

• Proceed straight from electronic-document checks to clearance of goods without spot checks

• Designated special Customs staff to handle problems in the Customs clearance process

A • Eligible for convenient clearance procedures

• Designate official to implement prior investigation on the site of manufacturing or loading

• Enjoy priority of declaration, investigation, and clearance

• Enjoy priority of declaration procedure in non-working days and holidays

• Deposit empty-transfer or do not adopt deposit transfer policy

B Subject to normal clearance procedures

C Subject to stricter supervision during the clearance process

D Same as C, plus opening each container where necessary

34

• Customs Category

Note : Category AA or A enterprise may has a greater chance to negotiate on special treatments with Customs.

To upgrade from Category B to A, enterprise should submit application to registration Customs and obtain approval from Customs in Charge.

PwC

Typical Clearance Process and Time

35

Import Clearance Procedures and Timeline

Day 1 - 2 Day 2 - 3 Day 3 Day 4 Day 5

Cu

sto

ms/

CIQ

Imp

ort

erC

ust

om

s B

rok

er

Provide the Air Waybill Notice

Input declaration information

electronically for Customs purpose

Input information electronically for

commodity inspection

purpose

Duty and VAT payment via EDI

Obtain Import Declaration Form

for forex remittance

Day 1

Port Customs Declaration

Issuance of Import Declaration Form

CIQ verification of the documents

Translate the documents into

Chinese and prepare invoices

in Chinese

Receive the documents in

foreign lanuage

CIQ sample testing if required

PwC

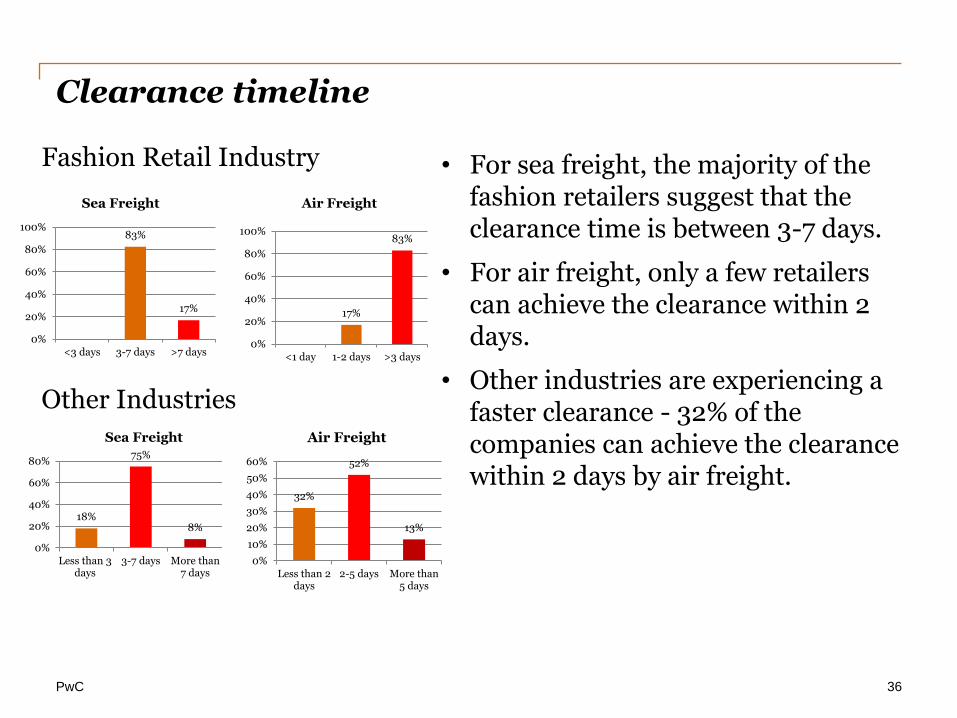

Clearance timeline

• For sea freight, the majority of the fashion retailers suggest that the clearance time is between 3-7 days.

• For air freight, only a few retailers can achieve the clearance within 2 days.

• Other industries are experiencing a faster clearance - 32% of the companies can achieve the clearance within 2 days by air freight.

36

Fashion Retail Industry

Other Industries

18%

75%

8%

0%

20%

40%

60%

80%

Less than 3days

3-7 days More than7 days

Sea Freight

32%

52%

13%

0%

10%

20%

30%

40%

50%

60%

Less than 2days

2-5 days More than5 days

Air Freight

83%

17%

0%

20%

40%

60%

80%

100%

<3 days 3-7 days >7 days

Sea Freight

17%

83%

0%

20%

40%

60%

80%

100%

<1 day 1-2 days >3 days

Air Freight

PwC

Paperless Declaration – New initiative for Shanghai Customs • Currently, the program is still in trial

as there are certain preconditions for paperless declarations:

37

IOR must be Category A company

The customs broker must be Category A or

AA

IOR must use E-port and EDI

system

No subject to any licensing requirement

Shipped through ocean freight

• Some of local Customs advised that they only accept export declaration, but others accept both import and export declarations

• The scheme may extend next year to include Category B companies.

• The implementation will be gradual rather than immediate and other China ports will start to move towards paperless filing also within the next 3 years.

PwC

Managing returns to overseas

PwC

Return of unsold inventory

39

Issues

• Customs treat the return as sales for export purpose.

• Procedures and documentation requirements for a normal export transaction should be followed.

• Which Trade Mode should be used? General Trade or Returned Goods (local Customs may have different interpretations)

• No customs duty refund scheme in China for this circumstance.

• VAT refund may be not allowed if the retailer acts as the EoR.

• For products under Chapters 61 and 62, License B may be difficult to obtain if these products are not made in China.

Solution

• Use an I/E agent for export

• I/E agent can export under General Trade

• Value of the exported goods may only be scrutinized for the purpose of ensuring the correct amount of VAT refund that the exporter (i.e. I/E agent) can obtain.

• Get HS code right - tariff classification determines the export customs supervision requirement i.e. non-tariff export trade barrier as well as the export VAT refund rates.

PwC

Sourcing and First Sale

PwC

Payments

Payments Invoice

Invoice

US/EU Importer

Asian Vendors Unrelated

Middleman/Principal

Suppliers related to the Middleman

Orders Placed

Delivery of Goods

First Sale Transaction Orders

Placed

United States

First Sale Structure Still a popular planning strategy

PwC

Opportunity

42

• Given your new found visibility to your downstream suppliers and supply chain, consider the availability of using an earlier sale for customs valuation purposes:

Achieve lower landed cost without impacting suppliers bottom line Gives suppliers competitive advantage for their client base Approach allows satisfaction arms length requirements while

maintaining supplier’s confidential financial information

PwC

Summary

PwC

What are the upcoming challenges?

44

Continued uncertain economic outlook; Analysts optimistic that 2013 will be better.

Labor costs have doubled and rent prices have increased over 30% in the last few years.

“Price wars” are not uncommon in China. Maintaining relationships with suppliers as margins narrow is critical.

Weak logistics infrastructure still a challenge for traditional “brick and mortar” establishment and distribution.

Continued emphasis on product quality, standards, safety from both the government and consumers.

Thank you!

This publication has been prepared for general guidance on matters of interest only, and does

not constitute professional advice. You should not act upon the information contained in this

publication without obtaining specific professional advice. No representation or warranty

(express or implied) is given as to the accuracy or completeness of the information contained

in this publication, and, to the extent permitted by law, PricewaterhouseCoopers Worldtrade

Management Services (Shanghai) Co., Ltd. its members, employees and agents do not accept

or assume any liability, responsibility or duty of care for any consequences of you or anyone

else acting, or refraining to act, in reliance on the information contained in this publication or for

any decision based on it.

© 2012 PricewaterhouseCoopers Worldtrade Management Services (Shanghai) Co., Ltd. All

rights reserved. In this document, “PwC” refers to PricewaterhouseCoopers Worldtrade

Management Services (Shanghai) Co., Ltd which is a member firm of

PricewaterhouseCoopers International Limited, each member firm of which is a separate legal

entity.