Retail Development Draft Market Study

94

BRAILSFORD & DUNLAVEY Retail Development Draft Market Study March, 2008 © Brailsford & Dunlavey, Inc. 2008

Transcript of Retail Development Draft Market Study

BRAILSFORD & DUNLAVEY

Retail Development

Draft Market Study March, 2008

© Brailsford & Dunlavey, Inc. 2008

TABLE OF CONTENTS

Florida International University Retail Demand Study 1

SECTION

1 Executive Summary 2 Existing Conditions / Supply Analysis 3 Demand Analysis - University Village/Main Street

4 Demand Analysis - 8th Street Project

EXHIBITS A Best Practices B Stakeholder / Focus Group Interviews C Quantitative Demographic and Economic Data D Management Options

Section 1

EXECUTIVE SUMMARY

Florida International University Retail Demand Study 1

Introduction In January 2008, Brailsford & Dunlavey (B&D) was engaged by Florida International University (FIU) to study the retail potential of two distinct projects on the University Park campus. Current Situation FIU is Miami-Dade County’s first public, four-year university and is one of the largest universities in the nation. Since its founding in 1965 and its opening class in 1972, the school has grown to over 38,000 students on two campuses. The University Park campus has seen significant growth over the last 30 years, and it has recently been awarded the country’s 127th medical school. As such, the campus is planning to build significant research, academic, and health facilities on the northeast portion of the campus. To serve this growing campus, FIU will need additional food and retail options. The Work Plan B&D conducted six distinct analyses to determine the market demand for new retail spaces on the FIU campus, including:

• A series of student and faculty/staff focus groups and random intercept interviews to gain qualitative information regarding retail activities, spending and possible facility enhancements;

• Case studies of seven other institutions to understand best practices across the country;

• An on- and off-campus supply analysis to determine the locations of retail, and dining

amenities in and around the University Park campus;

• A preliminary demand analysis of potential retail opportunities on the University Park campus;

• A preliminary financial analysis of potential ground lease revenue for a retail

development on the northern portion of the campus; and

• Preliminary management options that the University should consider if it moves forward with the projects.

EXECUTIVE SUMMARY

Florida International University 2 Retail Demand Study

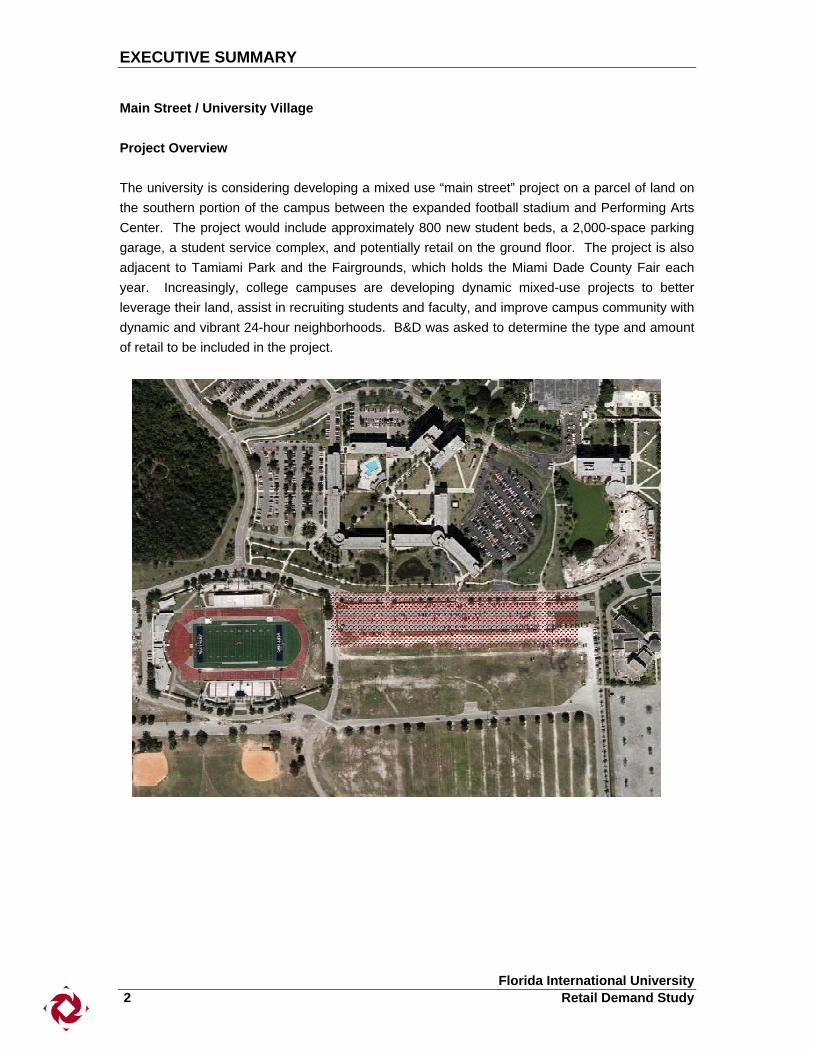

Main Street / University Village Project Overview The university is considering developing a mixed use “main street” project on a parcel of land on the southern portion of the campus between the expanded football stadium and Performing Arts Center. The project would include approximately 800 new student beds, a 2,000-space parking garage, a student service complex, and potentially retail on the ground floor. The project is also adjacent to Tamiami Park and the Fairgrounds, which holds the Miami Dade County Fair each year. Increasingly, college campuses are developing dynamic mixed-use projects to better leverage their land, assist in recruiting students and faculty, and improve campus community with dynamic and vibrant 24-hour neighborhoods. B&D was asked to determine the type and amount of retail to be included in the project.

EXECUTIVE SUMMARY

Florida International University Retail Demand Study 3

Project Drivers & Intended Outcomes B&D worked with a committee made up of FIU stakeholders, and the following drivers and outcomes were identified for the Main Street / University Village project: Drivers

Meet the growing retail and dining needs in the southern part of campus. Develop a dynamic mixed use neighborhood that will give FIU a competitive on-campus

amenity. Have long-term viability and be self-sustaining.

Outcomes

Generate additional revenues for campus. Encourage the Miami community to discover the campus. Capitalize on the synergies between the football stadium, PAC, new student support

center, and Frost Museum of the Art. Provide long-term parking and housing solutions.

Market Segment B&D has identified the following primary, secondary, and tertiary markets for the project:

Market Segment Primary Market Secondary Market Tertiary Market

Students On-campus students Off-campus students N/A

EmployeesFIU employees

within .25 miles of site

All other faculty / staff N/A

Residents N/A N/A 5-mile radius

Visitors Football Stadium, Museum, PAC Park visitors Fairgrounds visitors

EXECUTIVE SUMMARY

Florida International University 4 Retail Demand Study

Findings & Recommendations Based on the limited community access and visibility, it is clear that this project will need to be primarily internally focused to the FIU campus population. While the expanded football stadium and PAC will attract the community, the core traffic and revenue generation to the project will come from the existing campus population. The primary market will be FIU’s growing on-campus population. With currently over 2,000 beds in that portion of campus plus an additional 800 planned beds, the project will have an active 24-hour population from which to draw. While the project will certainly be attractive to on-campus students particularly in the evening, the key to the overall success of the project will be to develop anchors that will help drive commuters, faculty/staff, and other visitors to the project during the key daytime hours. Based on the current campus configuration, this will be no small feat. To do that, B&D recommends that the project include two anchors to support its overall success. The most ideal anchors for the project will be large lecture halls/classrooms to help pull students during the day, and new dining venues, which will provide attractive alternatives to the overcrowded food concepts at the Graham Center and generate additional revenue from game-day traffic. Other potential retail ideas on main street include a convenience store, coffeehouse/performance venue, satellite bookstore, Fedex/Kinkos, greek store, diner, and a relocated rathskeller. In addition to retail, other concepts to help generate traffic (but not revenue) would be more student organization space, meeting rooms, and a parking/transportation hub. Overall, the main street project on this site can be successful and self-sustaining if it focuses on a town center concept with mostly neighborhood-oriented retail, 800 beds of student housing, parking, and two strong anchors as discussed above. Based on our preliminary demand analysis, the campus should plan for approximately 30,000-40,000 square feet of retail in the Main Street / University Village location. There was some discussion at the conclusion of the study of the possibility of the parking being relocated to a different location. Clearly, this will have an impact on the vibrancy of main street as the original intent was to have pedestrians move through main street after parking their car. The residential student retail demand would not be as affected by the parking relocation; however, proximity to parking will be critical to their interest in living in the main street housing.

EXECUTIVE SUMMARY

Florida International University Retail Demand Study 5

8th Street Project Project Overview The campus was recently approved as the first public medical school in south Florida and the 127th in the country. As part of that initiative, the campus is developing the northeast portion of the campus for its academic health science campus. Part of the plan is to include a new Miami Dade Health Center, an ambulatory care center, and other academic and support facilities. Currently, Perkins+Will is developing a Master Plan for the northeast portion of the campus, and B&D was asked to determine the type and amount of retail for that portion of the campus.

EXECUTIVE SUMMARY

Florida International University 6 Retail Demand Study

Project Drivers & Intended Outcomes Similar to the Main Street project, B&D worked with a committee comprised of FIU stakeholders, and the following drivers and outcomes were identified for the 8th Street project: Drivers

Support the growing retail and dining needs of the new Academic Health Sciences Center population on the northeast side of campus.

Generate additional revenues for the campus. Outcomes

Create a competitive advantage for FIU. Encourage the Miami community to discover the campus. Capitalize on the growing community retail and dining needs of the University area. Increase the number of retail dining options for the rest of the campus.

B&D has identified the following primary, secondary, and tertiary markets for the 8th Street project:

Market Segment Primary Market Secondary Market Tertiary Market

Students Students within .25 miles of site All ofther students

Employees New AHSC employees

All other faculty / staff

Residents 10-minute drive 20-minute drive 30-minute drive

Visitors Clinic Visitors Campus Visitors

EXECUTIVE SUMMARY

Florida International University Retail Demand Study 7

Findings & Recommendations It is clear that there will be additional demand for retail and food on the northeast portion of campus after the development of the new academic health sciences facilities. To estimate demand, B&D developed a model for the internal demand (campus) and external demand (community) assuming that the project would have visibility and access off of 8th Street. Internal (Campus) Market With the growth of the new employees and students on that portion of campus, it is estimated that there will be over 2,800 employees and students in that precinct over campus in the next five years. Based on typical spending patterns, the estimated retail campus need in 2017 is approximately 32,000 gross square feet. At full campus build out, assuming all projects are completed, the resultant retail demand could be closer to 60,000-80,000 gross square feet.

Total On-Campus Retail Demand

2012 2017Total Annual Spending Per Person $3,350 $3,884

AHSC Faculty / Staff 687 864Miami-Date County Public Health Employees 700 811Ambulatory Care Clinic 300 348Medical Students 160 480Faculty / Staff within .25 miles 327 379

Total Population 2,174 2,882

Retail Sales / SF $350 $350Resultant Retail Space Demand 21,000 32,000

EXECUTIVE SUMMARY

Florida International University 8 Retail Demand Study

External (Community) Market With its large and diverse population, Miami has a strong and active retail market. While the retail market is starting to scale back due to a general slowdown in the economy and consumer spending, the long-term prognosis for the retail market in Miami remains strong. The primary community target market for the 8th Street retail project is a 10-minute drive time, or 5 miles away from the campus. Overall, there is significant income and population growth to support additional retail in the market. Based on population growth over the next five years, it is estimated that an additional 323,000 square feet of retail is needed within the target market. Assuming a 20%-30% penetration rate for this project, the resultant retail demand is approximately 80,000-110,000 gross square feet. Should the campus proceed with a large-scale retail project to attract the community, it may want to consider combining the retail project with the new proposed campus hotel, new graduate student housing, sit-down restaurants, a natural foods grocery store, and possibly an expanded campus bookstore with a large medical component. Many similar projects have included campus bookstores since they often make a strong anchor for the development. The ability for the campus to “sweeten the pot” by increasing the density of the project will improve the overall value to developers, and subsequently the overall ground lease revenue to the campus. The challenge for this project for FIU is to balance the needs of the growing University with the ability to provide attractive, visible, and accessible retail from the street. Developers will require surface parking, easy access, and potentially different design standards than the campus. The most valuable campus real estate from a retail perspective is the corner of 8th Street and 107th St, which would significantly alter the current Perkins+Will Master Plan. It is our recommendation that the University focus this project on the internal campus demand and reorient the retail inward to best serve that population. With the limited campus acreage available, the value of any annual ground lease revenue is probably not worth the tradeoffs required by the campus to make the retail viable. For a larger retail development, the campus may want to consider partnering with the town of Sweetwater to enhance their campus town project across of 8th Street.

EXECUTIVE SUMMARY

Florida International University Retail Demand Study 9

Additional Options B&D was asked to review whether other options are more appropriate. A total of three options were identified: Option A: Proposed location on 8th Street adjacent to proposed parking garage. Option B: A corner location on 8th Street and 107th St. Option C: Internal to AHSC Neighborhood The following matrix summarizes each of the potential options:

Scenarios Retail Demand (SF) Comments

Options Location Target Market AnchorsUniversity Operated

Special Purpose

EntityThird Party Developer

Risk(High, Moderate,

Low)

Return (High,Moderate,

Low)

A8th Street Adjacent

to New Parking

5 mile radius - Sweetwater,

Doral, Kendall

Sit down restaurants and Medical Supply Store (Bookstore branch) ü High Moderate 84,000 - 113,000

Limited Visibility and access are chief concerns

BCorner

8th St. & 107

5 mile radius - Sweetwater,

Doral, Kendall

Sit down restaurants and Medical Supply Store (Bookstore branch) ü Moderate Highest 84,000 - 113,000 Most ideal site from a retail perspective

C 32,000 Most ideal location for new AHSC populationInternal to AHSC

Neighborhood Internal ü Low

Academic Health Science Complex

Management OptionsSite FinancialMarketing Strategy

Next Steps The following next steps should occur:

Refine recommendations based on findings from the Aramark study and B&D’s student housing market study.

Refine the concepts and demand figures based on a quantitative survey of the FIU population.

Coordinate with Perkins+Will to ensure that adequate retail space is included in their master plan.

Develop a detailed financial analysis of the proposed project.

Section 2

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University Retail Demand Study 1

Objectives The objective of the Market Supply portion of the Market Analysis was to define the overall nature and competitiveness of the retail market on FIU’s campus as well as the market proximate to the University as it exists presently and as it may exist in the future. This information is necessary to provide context when gauging the viability of new retail development at FIU. The analysis specifically addressed the character of available retail, the location and quantities of specific product types, and typical lease rates. Incorporation of each of these factors into the analysis was instrumental in predicting the likely requirements, marketability, and competitiveness of the proposed project. Methodology B&D conducted an analysis of both the on and off-campus retail markets to evaluate the retails options in the target market area. The on-campus (internal) retail research included a review of on-campus retail sales number, tour of retail options, and conversations with Aramark and university administrators. Components of the off-campus (external) research included interviews with leasing agents, tours of facilities, and Internet research. Representatives from FIU, as well as professionals in the local property management community, assisted the project team in the development of a comparable retailers / properties list. A total of 14 ‘comparable’ rental properties were researched within the target market area. The properties were evaluated and categorized based on their market segment type. Definitions for the different property types are listed below. Internal Supply FIU has a significant retail operation on its University Park campus. Primarily concentrated within the Graham Center, the retail options generally serve the campus population. Sales figures for all retail and dining establishments totaled nearly $28 million in 2006-2007 or $312 per square foot. The sales per square foot at FIU is generally higher than the average for universities similar to FIU. Non-Food Retail FIU has a robust retail and dining operation on campus. Mostly located at the Graham Center, retail options include the campus bookstore, a dry cleaners, a salon, a copy shop, a flower shop and a travel agency. The campus bookstore is the main retail anchor at the Graham Center, driving approximately $15,942,725 in sales for 2006-2007. The average sales at the bookstore are a respectable $332 per square foot. Non-bookstore retail on campus is strong averaging $440 per square foot with total sales at $2,366,725.

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University 2 Retail Demand Study

Non Food Retail Sales

Square Feet

Sales 2006-2007

Sales / SF

Bookstore 48,026 $15,942,725 $332Afrodita's 468 $71,466 $153Copy Center 991 N/A N/ACredit Union 1,408 N/A N/ASanti's 1,063 $662,603 $623Travel 468 $1,443,339 $3,084Waves 987 $189,317 $192

Total 53,411 $18,309,450 $343

FIGURE: 2.1: Total non food retail sales for 2006-2007. As the campus grows and retail demand increases, it is expected that the additional retail space will be placed all across the campus to meet the demand of the immediate populations. Food Services Food service options on campus are also mostly centered around the Graham Center. Managed by Aramark, current options include Fresh Foods; fast food such as Subway, Burger King, Pollo Tropical and Einstein Bagels; and various coffee and convenience vendors such as Starbucks, Bustelo Coffee, Java City and the Breezeway convenience store. The food service sales were also strong for 2006-2007 with total sales at $8,457,027 or $238 per square foot.

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University Retail Demand Study 3

Food Services Sales

Square Feet

Sales 2006-2007 Sales / SF

Fresh Foods 17,670 $1,020,342 $58Subway 1,238 $841,542 $680Burger King 400 $277,558 $694Pollo Tropical 1,129 $615,993 $546Gracie's Grill 5,072 $182,322 $36Faculty Club 4,142 $119,180 $29Catering 0 $636,449 $0Einstein Bagels 605 $328,491 $543Camille's 1,100 $155,463 $141Bene Pizza 119 $147,009 $1,235Sushi 337 $216,693 $643Bustelo 360 $156,530 $435Java City GC/Vending 360 $0 $0Java City Library 100 $449,426 $4,494Starbucks - Library 1,446 $35,535 $25Breezeway-Convenience 1,440 $567,484 $394Remotes - West Side 50 $0 $0Meal Plans 0 $2,707,009 $0

Total 35,568 $8,457,027 $238

FIGURE 2.2: Total food service sales for 2006-2007. The average sales per square foot at FIU are significantly higher when compared to universities of similar size and demographics. FIU’s sales for food service including meal plans are $267 per square foot when the national average is in the $180-$200 per square foot range. This indicates that some of the existing food services facilities are over-subscribed.

Total Food Service Sales Per Square Foot

Average Sales / SF

Total Food Service Square Feet 35,568Total Food Service Sales $6,784,906 $191Total Sales w/Meal Plan $9,491,915 $267

National Range $180 - $200

FIGURE 2.3: Total food service sales per square foot for 2006-2007.

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University 4 Retail Demand Study

Another significant source of revenue on campus is vending machine sales. For 2006-2007, the campus had 180 machines that generated $1,034,888 in sales. This is exceptionally high and indicates that there is additional demand for more retail outlets on campus.

Retail and Food Services Sales

Square Feet Sales Sales / SFBookstore 48,026 $15,942,725 $332Food Services 35,568 $8,457,027 $238Other Retail 5,385 $2,366,725 $440Vending - $1,034,888 -

Total 88,979 $27,801,365 $312

FIGURE 2.4: Total retail and food service sales for 2006-2007. Market Area Overview According to the Urban Land Institute, there are five types of shopping center types, each distinctive in its own function. In all cases, a shopping center’s type and function are determined by its major tenant or tenants and the size of its trade area; they are never based solely on the area of the site or the square footage of the structure. All five categories of shopping centers exist within the market area, many in close proximity to FIU. The five types of retail developments are outlined in the chart below:

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University Retail Demand Study 5

Shopping Center Definitions

Size (SF) Typical Tenants

Convenience 0 - 29,000 Convenience StoreDry CleanersFast FoodCoffee Shop

Neighborhood 30,000 - 99,000 Super MarketPharmacyFast FoodSit-Down Restaurant

Community 100,00 - 249,000 Super MarketBig Box RetailersRestaurants

Regional 250,000 - 749,000 Big Box RetailersDiscount RetailersRestaurantsEntertainment

Super - Regional 750,000 + Traditional Mall

FIGURE 2.5: Shopping Center Definitions. Convenience Centers A convenience center provides for the sale of personal services and convenience goods similar to those of a neighborhood center. It contains a minimum of three stores, with a total gross leasable area of up to 30,000 square feet. Convenience centers are typically anchored by some type of personal or convenience services such as a mini-market. There are numerous examples of convenience centers within the target market, but they are insignificant for the purposes of this study.

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University 6 Retail Demand Study

Neighborhood Centers A neighborhood center provides for the sale of convenience goods (foods, drugs, and sundries) and personal services (laundry and dry cleaning, barbering, shoe repair, etc.) for the day-to-day living needs of the immediate neighborhood. It is built around a supermarket as the principal tenant and typically contains a gross leasable area of about 60,000 square feet but may range from 30,000 to 100,000 square feet. There are numerous neighborhood centers within the target market area. B&D evaluated the three closest to the FIU campus, as they will have the greatest impact on the proposed development at FIU.

Neighborhood Centers

Gross Leasable

AreaRent

$/SF/YearAnchor / Major

TenantDistance from FIU

Biltmore Plaza 38,000 $21 None 3

Florida International Plaza 55,983 $20 - $25 Office Depot 0.1

University Center N/P $20 - $25 Publix 0.1

Biltmore Plaza

University Center

FIUFlorida

International Plaza

Biltmore Plaza

University Center

FIUFlorida

International Plaza

Biltmore Plaza

University Center

FIUFlorida

International Plaza

Biltmore PlazaBiltmore Plaza

University Center

University Center

FIUFlorida

International Plaza

Florida International

Plaza

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University Retail Demand Study 7

Community Retail Centers A community retail center provides a wider range of soft lines (apparel for men, women, and children) and hard lines (hardware and appliances). The community center makes merchandise available in a greater variety of sizes, styles, colors, and prices. Many centers are built around a junior department store, variety store, super drugstore, or discount department store as the major tenant, in addition to a supermarket. Although a community center does not have a full-line department store, it may have a strong specialty store or stores. The typical size of a community center is about 150,000 square feet of gross leasable area but may range as small as 100,000 to as large as 249,000 square feet. There are currently three community retail centers in the target market.

Community Retail Centers

Gross Leasable

AreaRent

$/SF/YearAnchor / Major

TenantDistance from FIU

Bird Bowl Shopping Center 125,438 N/P Bird Bowl 4

Festival Plaza 152,000 $20 Starbucks 3

Laroc Center 115,000 $30 Sedano's Supermarket 3.3

Festival Plaza

Bird Bowl

Laroc Center

FIU

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University 8 Retail Demand Study

Regional Retail Centers A regional retail center provides general merchandise, apparel, furniture, and home furnishings in depth and variety, as well as a range of services and recreational facilities. It is built around one or two full-line department stores of generally not less than 50,000 square feet. Its typical size is about 500,000 square feet of gross leasable area but may range from 250,000 to more than 749,000 square feet. The regional center provides services typical of a business district yet not as extensive as those of the super regional center. There are currently three regional retail centers in the target market.

Mall of the Americas

Flagler Park Plaza

Concord Shopping Plaza

FIU

Regional Retail Centers

Gross Leasable

AreaRent

$/SF/YearAnchor / Major

TenantDistance from FIU

Concord Shopping Plaza 325,000 N/P Home Depot 1.8

Flagler Park Plaza 452,681 N/P Publix 2.9

Mall of the Americas 650,151 N/P Home Depot 3.4

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University Retail Demand Study 9

Super Regional Centers A super regional center offers extensive variety in general merchandise, apparel, furniture, and home furnishings, as well as a variety of services and recreational facilities. It is built around one or two full-line department stores generally of not less than 75,000 square feet each. The typical size of a super regional center is about 1,000,000 square feet of gross leasable area but can range from 750,000 to more than 1,500,000 square feet. There are currently two super regional centers within the target market.

Super Regional Retail Centers

Gross Leasable

AreaRent

$/SF/YearAnchor / Major

TenantDistance from FIU

Dolphin Mall 1,313,000 N/P Burlington Coat Factory 1.9

International Mall 1,072,370 N/P Macy's 1.9

Dolphin Mall International Mall

FIU

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University 10 Retail Demand Study

New Retail Centers in Target Market There are a number of new retail centers within the target market that have recently opened or will be coming on line in early 2008. The types range from small neighborhood centers (San Miguel Shopping Plaza) to large mixed-use projects (Park Square at Doral). Dolphin plaza is a small, high-end retail and dining concept that is utilizing its location near two major super-regional centers to capture its customers.

New Retail Centers

Gross Leasable

AreaRent

$/SF/YearAnchor / Major

TenantDistance from FIU

San Miguel Shopping Plaza 60,000 $25 - $55 None 2.8

Park Square at Doral N/P $55 TBD 6

Dolphin Plaza 31,000 $30 None 1.9

San Miguel

Park Square

Dolphin Plaza

FIU

EXISTING CONDITIONS / SUPPLY ANALYSIS

Florida International University Retail Demand Study 11

Miami-Dade County Retail Trends Although the housing market was extremely soft in 2007, the retail market remained relatively healthy in Miami-Dade County. According to fourth quarter 2007 data provided by CB Richard Ellis, the market is showing signs of weakness in early 2008 due to the current housing crisis. Although the market is softening, the long-term prognosis for retail in Miami-Dade is very good. Some key retail aspects include:

Miami-Dade County is still under-retailed. Strong spending by Latin Americans and Europeans with second homes in the area. Miami is a strong entry market for European retail concepts. 585,120 (sq. ft.) of retail space was delivered in 2007. Stricter underwriting standards for new projects. Vacancy rate increased from 2.9% to 3.3% Development will be tenant-driven with a focus on infill and mixed-use.

Section 3

DEMAND ANALYSIS: MAIN STREET

Florida International University Retail Demand Study 3

Objectives and Methodology FIU is a large university that has nearly reached its capacity at the University Park campus. With enrollment projected to remain flat for the coming years the retail demand analysis for this study is based upon a comparison of current spending patterns with national on-campus spending data. An analysis of the demographics of FIU, total food service and non-food retail sales numbers was conducted to gain an understanding of the current spending characteristics of the campus population. FIU Campus Demographic Determinants Currently FIU’s University Park campus has a total population of 31,064 students and 3,191 faculty and staff. Approximately 2,428 of those students are living on campus. Campus growth is projected to be relatively minimal for the coming years as undergraduate enrollment is not projected to grow. However, any growth that occurs will result from the development of the Academic Health Sciences Center, the Miami-Dade County Public Health Center and the ambulatory care clinic. Current estimates project an additional 1,500 new people on campus by 2012. Main Street Visitors Main Street will be clearly anchored by the on-campus residents on the southern edge of campus. There are currently 2,400 beds with plans for an additional 800 to be built on Main Street. In addition to the on-campus community, a number of new projects have come on line or are in the implementation stages on or near the proposed site for Main Street. These new developments have the potential to draw a significant number of visitors to the southern edge of campus.

Main Street Visitors

Student Service Center1 12,215Financial Aid Office1 21,516Fooball Attendees2 175,000Performing Arts Center3 10,000Frost Museum3 10,000Other3 20,000

Total Visitors 248,731

Notes:1. Data provided by FIU2. CH Johnson study3. B&D estimate

FIGURE 3.1: Estimated Main Street visitors.

DEMAND ANALYSIS: MAIN STREET

Florida International University 4 Retail Demand Study

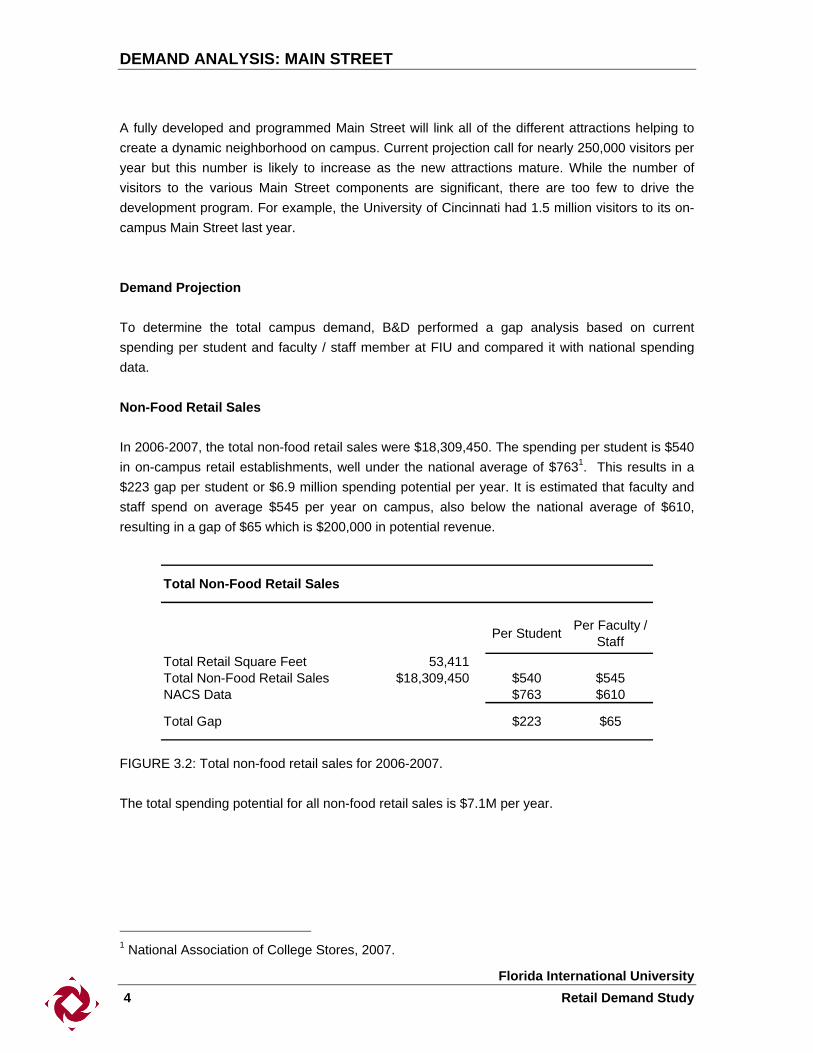

A fully developed and programmed Main Street will link all of the different attractions helping to create a dynamic neighborhood on campus. Current projection call for nearly 250,000 visitors per year but this number is likely to increase as the new attractions mature. While the number of visitors to the various Main Street components are significant, there are too few to drive the development program. For example, the University of Cincinnati had 1.5 million visitors to its on-campus Main Street last year. Demand Projection To determine the total campus demand, B&D performed a gap analysis based on current spending per student and faculty / staff member at FIU and compared it with national spending data. Non-Food Retail Sales In 2006-2007, the total non-food retail sales were $18,309,450. The spending per student is $540 in on-campus retail establishments, well under the national average of $7631. This results in a $223 gap per student or $6.9 million spending potential per year. It is estimated that faculty and staff spend on average $545 per year on campus, also below the national average of $610, resulting in a gap of $65 which is $200,000 in potential revenue.

Total Non-Food Retail Sales

Per Student Per Faculty / Staff

Total Retail Square Feet 53,411Total Non-Food Retail Sales $18,309,450 $540 $545NACS Data $763 $610

Total Gap $223 $65

FIGURE 3.2: Total non-food retail sales for 2006-2007. The total spending potential for all non-food retail sales is $7.1M per year.

1 National Association of College Stores, 2007.

DEMAND ANALYSIS: MAIN STREET

Florida International University Retail Demand Study 5

Food Service Sales For food service sales, B&D performed a similar gap analysis using national data from Envision Strategies. Total FIU food service expenditures including meal plans were $9,491,915 or $309 per person, well below the national average of $493 per student for a similar sized state institution in a metropolitan area. This gap of $184 per person translates into $5.6 million in lost revenue.

Total Food Service Sales

Per PersonTotal Food Service Sales $6,784,906 $221Total Sales w/Meal Plan $9,491,915 $309National Sales Data $493

Total Gap $184

FIGURE 3.3: Total food service sales including meal plans for 2006-2007. Based on current campus population and spending data, B&D estimates the total potential new revenue to be $12.6 million. The potential new spending translates to 40,000 square feet of retail based on the current average sales per square foot of $312. A conservative estimate of new retail sales is roughly $9.4 million, translating to an additional 30,000 square feet of retail as shown in figure 3.6.

Total Campus Demand

Conservative BaseTotal Potential New Campus Spending $9,375,000 $12,600,000Average Sales Per Square Feet $312 $312

Total Potential New Square Feet 30,000 40,000

FIGURE 3.4: Total campus retail demand.

Section 4

DEMAND ANALYSIS: 8TH STREET

Florida International University Retail Demand Study 1

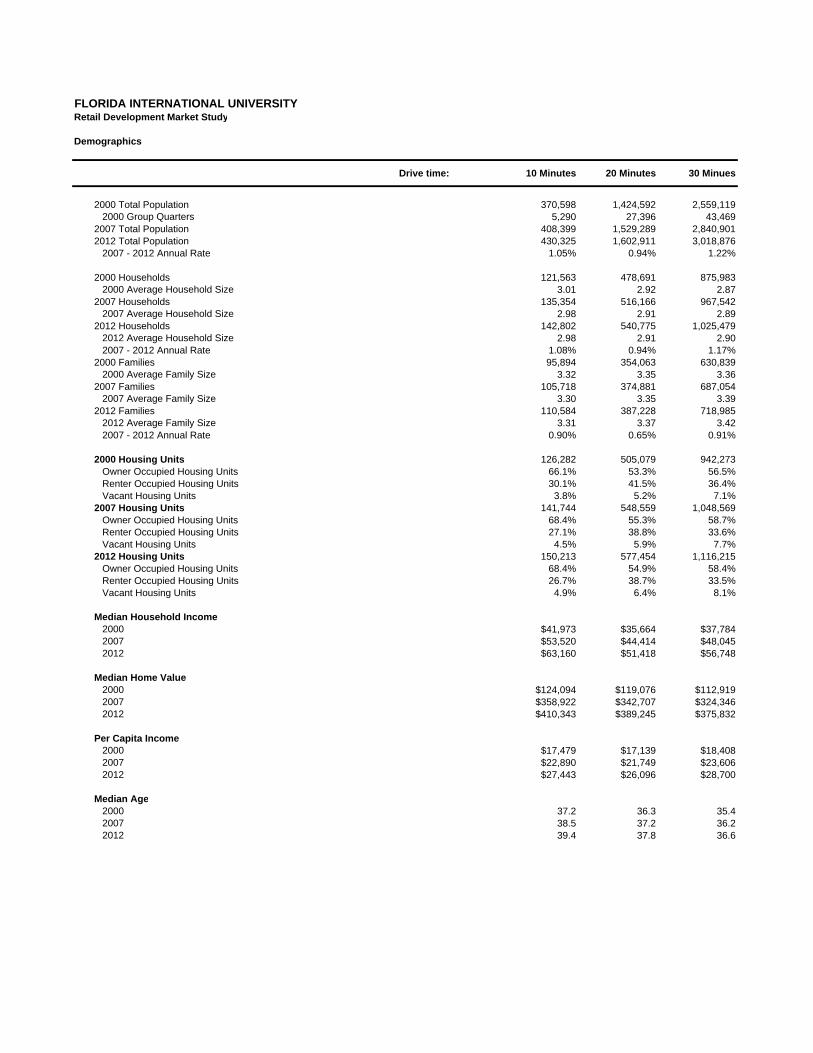

Objectives and Methodology - Demographic Review An analysis of the demographics of Miami, Florida was undertaken to gain an understanding of the characteristics of the market’s current and projected populations. The objective of the demographic analysis was to determine the impact any changes in population demographics may have on the retail market. B&D’s demographic data was obtained from the Market Profile Report published by Environmental Systems Research Institute, Inc (ESRI). The demographic report includes U.S. Census data from 2000 and ESRI estimates for 2007 and projections to 2012. The complete demographic data can be found in Exhibit C: Quantitative Demographic and Economic Data. Definition of Market Area Miami and Miami-Dade County are part of the Miami-Fort Lauderdale-Pompano Beach, FL Metropolitan Statistical Area. Defined by the United States’ Office of Management and Budget, a ‘metropolitan’ area has at least one core urban area of 50,000 or more residents and includes the county our counties containing the core urban area. This standardized geographic definition of markets is the basis by which common economic and demographic data is collected by federal agencies, including the U.S. Census Bureau. While most market analyses rely on the federal market area definitions, the definition of the Miami-Fort Lauderdale-Pompano Beach Metropolitan area does not represent the market for the product types being considered in this study. Rather, a better definition of the true market area is measured by driving times to and from FIU. Considering that 62% of the Miami-Fort Lauderdale-Pompano Beach Metropolitan area residents commute between 10 and 34 minutes to work, demographic and economic data was collected based upon drive time radii of 10, 20, and 30 minutes from FIU. For the purpose of this study, the 10-minute drive time radius defines the market area and the other radii are used to identify any unique characteristics that might be otherwise overlooked.

DEMAND ANALYSIS: 8TH STREET

Florida International University 2 Retail Demand Study

FIGURE 4.1: Map of the 10-, 20-, and 30-minute drive time market areas. Population Characteristics Based upon 2007 population estimates, the defined market includes nearly 2,800,000 people. Approximately 15% of the market is located within a 10-minute drive of FIU and another 25% of the market is located within 10 additional driving minutes. As might be predicted, the population densities increase between the 10-minute drive time area and the 20- to 30-minute drive time area.

10-Minute Drive 20-Minute Drive 30-Minute Drive

2000 Total Population 370,598 1,424,592 2,559,119

2007 Total Population 408,399 1,529,289 2,840,901Growth Rate 1.96% 1.43% 2.11%

2012 Total Population 430,325 1,602,911 3,018,876Growth Rate 1.05% 0.94% 1.22%

FIGURE 4.2: Market area population and growth data.

DEMAND ANALYSIS: 8TH STREET

Florida International University Retail Demand Study 3

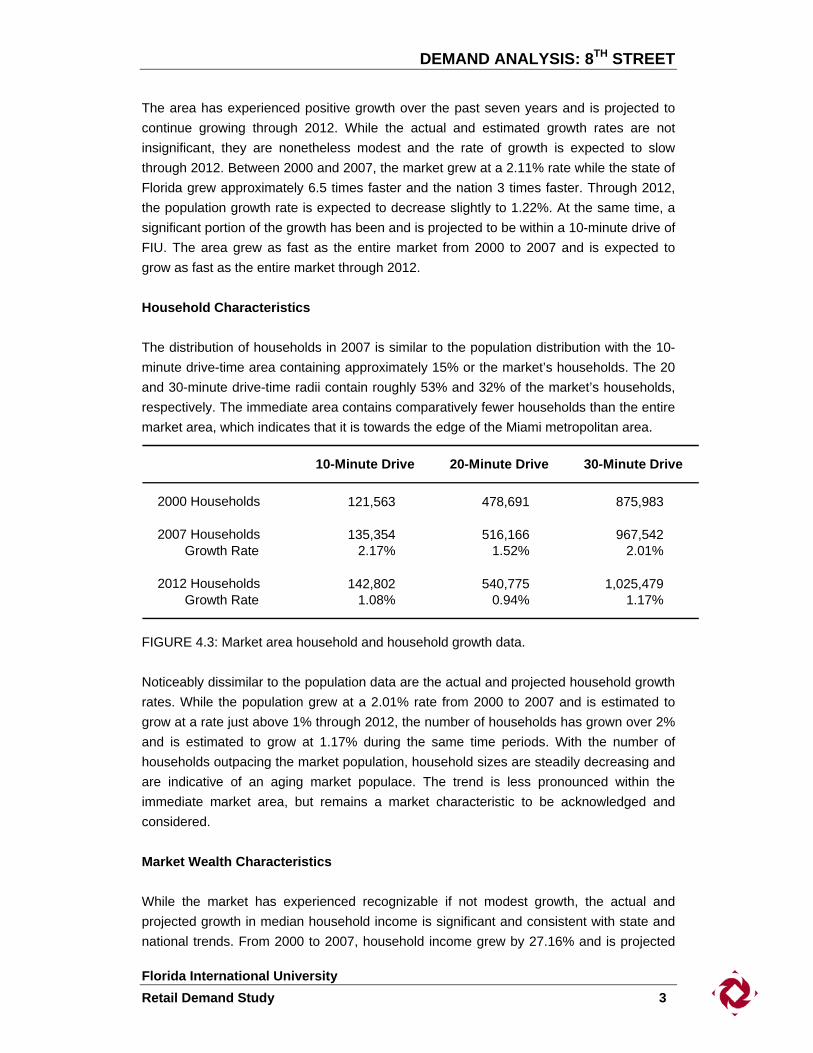

The area has experienced positive growth over the past seven years and is projected to continue growing through 2012. While the actual and estimated growth rates are not insignificant, they are nonetheless modest and the rate of growth is expected to slow through 2012. Between 2000 and 2007, the market grew at a 2.11% rate while the state of Florida grew approximately 6.5 times faster and the nation 3 times faster. Through 2012, the population growth rate is expected to decrease slightly to 1.22%. At the same time, a significant portion of the growth has been and is projected to be within a 10-minute drive of FIU. The area grew as fast as the entire market from 2000 to 2007 and is expected to grow as fast as the entire market through 2012. Household Characteristics The distribution of households in 2007 is similar to the population distribution with the 10-minute drive-time area containing approximately 15% or the market’s households. The 20 and 30-minute drive-time radii contain roughly 53% and 32% of the market’s households, respectively. The immediate area contains comparatively fewer households than the entire market area, which indicates that it is towards the edge of the Miami metropolitan area.

10-Minute Drive 20-Minute Drive 30-Minute Drive

2000 Households 121,563 478,691 875,983

2007 Households 135,354 516,166 967,542Growth Rate 2.17% 1.52% 2.01%

2012 Households 142,802 540,775 1,025,479Growth Rate 1.08% 0.94% 1.17%

FIGURE 4.3: Market area household and household growth data. Noticeably dissimilar to the population data are the actual and projected household growth rates. While the population grew at a 2.01% rate from 2000 to 2007 and is estimated to grow at a rate just above 1% through 2012, the number of households has grown over 2% and is estimated to grow at 1.17% during the same time periods. With the number of households outpacing the market population, household sizes are steadily decreasing and are indicative of an aging market populace. The trend is less pronounced within the immediate market area, but remains a market characteristic to be acknowledged and considered. Market Wealth Characteristics While the market has experienced recognizable if not modest growth, the actual and projected growth in median household income is significant and consistent with state and national trends. From 2000 to 2007, household income grew by 27.16% and is projected

DEMAND ANALYSIS: 8TH STREET

Florida International University 4 Retail Demand Study

to grow another 18.11% by 2012. Also, the increase in wealth is generally evenly distributed within the market areas with only a 4% variance in 2000, 2007, and 2012 median household income figures.

10-Minute Drive 20-Minute Drive 30-Minute Drive

2000 Median HH Income $41,973 $35,664 $37,784

2007 HH Income $53,520 $44,414 $48,045Growth Rate 27.51% 24.53% 27.16%

2012 HH Income $63,160 $51,418 $56,748Growth Rate 18.01% 15.77% 18.11%

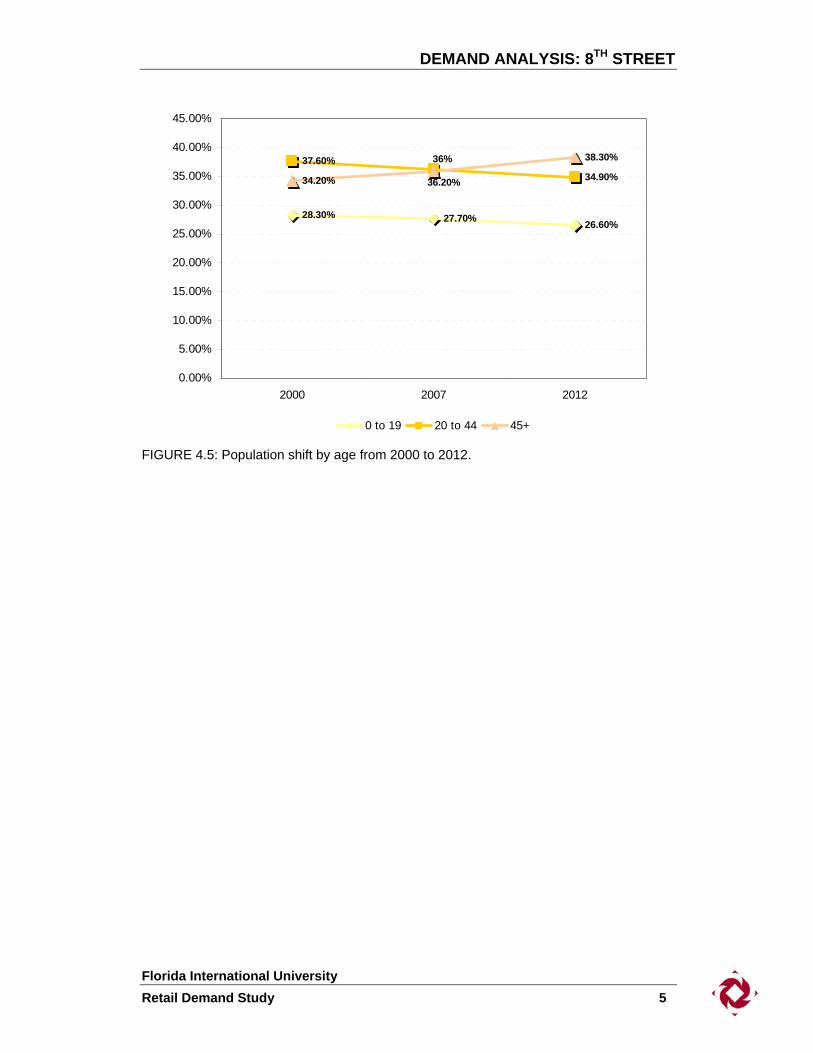

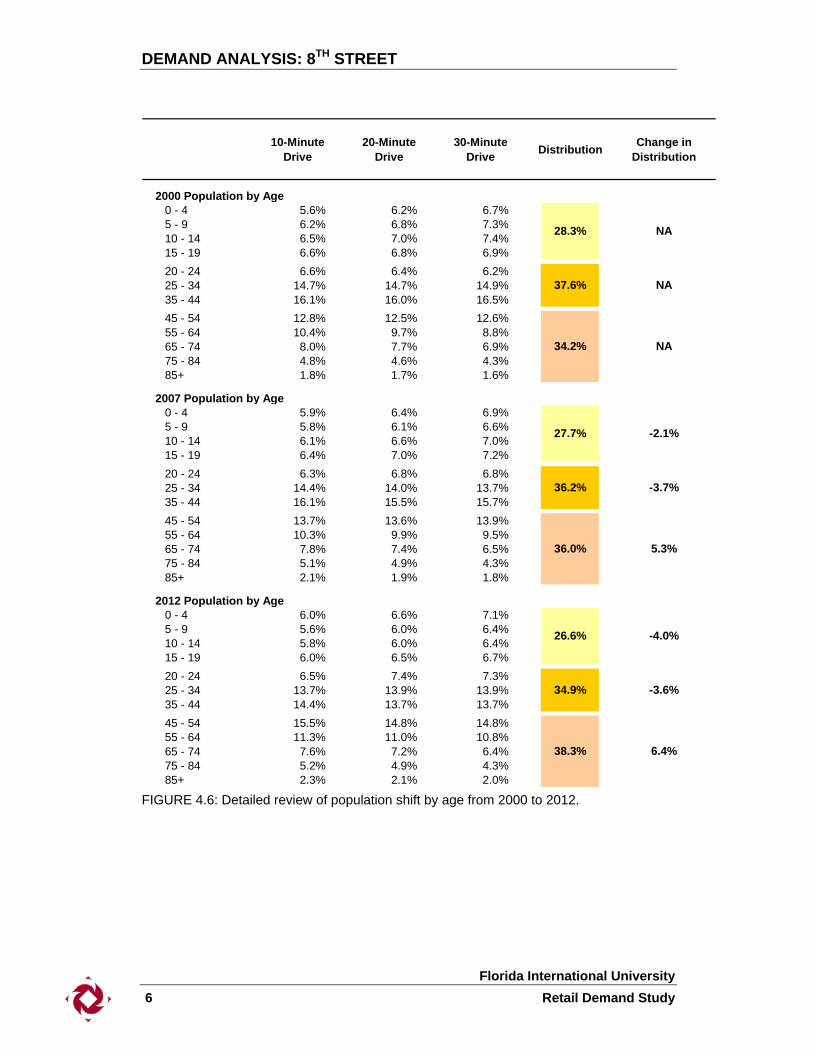

FIGURE 4.4: Market area median household income and growth data. Market Population Age Characteristics As indicated by the population and household data, the age of the market population has been increasing and will continue to increase. An analysis of the population according to 12 age categories indicates that the percentage of persons aged between 0 and 19 years has fallen 2.1% from 28.3% in 2000 to 27.7% in 2007. By 2012, the same category is estimated to fall another 4% from 27.7% of the population to 26.6% of the population. Young professionals and adults aged between 20 and 44 years have fallen similarly from 37.6% of the population in 2000 to 36.2% of the population in 2007. The fall is projected to continue with the percentage dropping another 3.6% to 34.9% by 2012. The decline in percentage of the younger population is offset by a significant increase in the portion of the population over the age of 45. Between 2000 and 2007, the older population segment rose from 34.2% of the market population to over 36%. The growth in the older population is expected to continue, albeit at a slower rate, with nearly 36.3% of the market population over the age of 45 projected by 2012.

DEMAND ANALYSIS: 8TH STREET

Florida International University Retail Demand Study 5

28.30% 27.70% 26.60%

37.60%34.90%34.20%

38.30%

36.20%

36%

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

35.00%

40.00%

45.00%

2000 2007 2012

0 to 19 20 to 44 45+

FIGURE 4.5: Population shift by age from 2000 to 2012.

DEMAND ANALYSIS: 8TH STREET

Florida International University 6 Retail Demand Study

10-Minute Drive

20-Minute Drive

30-Minute Drive Distribution Change in

Distribution

2000 Population by Age 0 - 4 5.6% 6.2% 6.7% 5 - 9 6.2% 6.8% 7.3% 10 - 14 6.5% 7.0% 7.4% 15 - 19 6.6% 6.8% 6.9% 20 - 24 6.6% 6.4% 6.2% 25 - 34 14.7% 14.7% 14.9% 35 - 44 16.1% 16.0% 16.5% 45 - 54 12.8% 12.5% 12.6% 55 - 64 10.4% 9.7% 8.8% 65 - 74 8.0% 7.7% 6.9% 75 - 84 4.8% 4.6% 4.3% 85+ 1.8% 1.7% 1.6%

2007 Population by Age 0 - 4 5.9% 6.4% 6.9% 5 - 9 5.8% 6.1% 6.6% 10 - 14 6.1% 6.6% 7.0% 15 - 19 6.4% 7.0% 7.2% 20 - 24 6.3% 6.8% 6.8% 25 - 34 14.4% 14.0% 13.7% 35 - 44 16.1% 15.5% 15.7% 45 - 54 13.7% 13.6% 13.9% 55 - 64 10.3% 9.9% 9.5% 65 - 74 7.8% 7.4% 6.5% 75 - 84 5.1% 4.9% 4.3% 85+ 2.1% 1.9% 1.8%

2012 Population by Age 0 - 4 6.0% 6.6% 7.1% 5 - 9 5.6% 6.0% 6.4% 10 - 14 5.8% 6.0% 6.4% 15 - 19 6.0% 6.5% 6.7% 20 - 24 6.5% 7.4% 7.3% 25 - 34 13.7% 13.9% 13.9% 35 - 44 14.4% 13.7% 13.7% 45 - 54 15.5% 14.8% 14.8% 55 - 64 11.3% 11.0% 10.8% 65 - 74 7.6% 7.2% 6.4% 75 - 84 5.2% 4.9% 4.3% 85+ 2.3% 2.1% 2.0%

34.9%

38.3%

-2.1%

-3.7%

5.3%

-4.0%

-3.6%

6.4%

27.7%

36.2%

36.0%

26.6%

28.3%

37.6%

34.2%

NA

NA

NA

FIGURE 4.6: Detailed review of population shift by age from 2000 to 2012.

DEMAND ANALYSIS: 8TH STREET

Florida International University Retail Demand Study 7

Market Race / Ethnicity Characteristics Based on 2007 population estimations, the target market area is predominately of Hispanic Origin. The number of Hispanics in the market area increased 1.34% to 85.6% in the period from 2000 to 2007. The Hispanic population is expected to increase another .71% to 88.7% by 2012. The rest of the population in the target market is evenly distributed between the different ethnicities. The demographics for the market area are slightly higher than Miami-Dade County, where 61% of the population is of Hispanic origin.

10-Minute Drive

20-Minute Drive

30-Minute Drive

Growth Rate

2000 Population by Race/EthnicityTotal 370,600 1,424,592 2,559,117 White Alone 88.5% 77.1% 69.2% Black Alone 2.3% 12.8% 20.5% American Indian Alone 0.1% 0.2% 0.2% Asian or Pacific Islander Alone 1.5% 1.3% 1.7% Some Other Race Alone 4.4% 4.8% 4.5% Two or More Races 3.2% 3.7% 3.8%Hispanic Origin 80.1% 68.9% 53.2%

2007 Population by Race/EthnicityTotal 408,399 1,529,289 2,840,902 White Alone 88.3% 77.5% 69.2% -0.05% Black Alone 2.3% 11.9% 19.6% 0.00% American Indian Alone 0.1% 0.2% 0.2% 0.00% Asian or Pacific Islander Alone 1.5% 1.4% 1.9% 0.00% Some Other Race Alone 4.5% 5.2% 5.1% 0.45% Two or More Races 3.2% 3.8% 4.0% 0.00%Hispanic Origin 85.6% 75.2% 59.8% 1.34%

2012 Population by Race/EthnicityTotal 430,324 1,602,911 3,018,876 White Alone 88.5% 77.9% 69.4% 0.05% Black Alone 2.2% 11.3% 18.8% -0.89% American Indian Alone 0.1% 0.2% 0.2% 0.00% Asian or Pacific Islander Alone 1.4% 1.4% 2.0% -1.37% Some Other Race Alone 4.6% 5.4% 5.5% 0.44% Two or More Races 3.2% 3.9% 4.1% 0.00%Hispanic Origin 88.7% 78.7% 64.1% 0.71%

FIGURE 4.7: Market area population by race/ethnicity.

DEMAND ANALYSIS: 8TH STREET

Florida International University 8 Retail Demand Study

Retail Demand Projection – 8th Street The retail improvements being considered by the University are not unique to FIU. In fact, many universities are looking at ways to develop excess on-campus land to generate additional revenues for these universities. Our analysis looked at internal (campus) demand and external (community) demand. Internal (Campus) Demand FIU has seen unprecedented growth in both undergraduate and graduate programs in the past decade. A significant number of new buildings have been built to meet the demand. The next phase in the University’s evolution is the development of the Academic Health Sciences Center (AHSC). Granted the 127th medical school in the United States, FIU has embarked on the planning and development of a medical campus in the northeast quadrant of campus. The campus will include the College of Nursing and Health Sciences, the College of Medicine, the Miami-Dade Department of Public Health, numerous research buildings, a medical office space and retail to support the population of the AHSC campus. The build-out of the AHSC campus is projected to last for 20 years, with the first buildings coming on line by 2012. It is important to note that the demand numbers are based on the development projects that are expected to come on line in the next five years. B&D chose to focus on the first five years because there are too many unknown variables that could impact the build out of the AHSC campus.

5-Year AHSC Development Program

College of Nursing & Health Sciences 101,000 SFMiami-Dade Dept of Health Building 106,500 SFFUI School of Public Health 33,600 SFHLS-3:Science Classroom Complex 1 138,800 SFGraduate Classroom Building 59120 SFParking Garage 5 / Public Safety 1400 spaces / 12,000 SFAmbulatory Care Clinic 120,000 SFPhase 1-Satellite Chiller Plant 15,000 SF

FIGURE 4.8: The projected 5-year development program for the AHSC campus. The University market and, more specifically, the faculty, staff and employees of the Academic Health Science Center campus represent an additional potential market with significant spending power. With a projected 2012 population of nearly 2,174 AHSC faculty and staff, medical students, and Miami-Dade County public Health Center employees—

DEMAND ANALYSIS: 8TH STREET

Florida International University Retail Demand Study 9

and with each group spending an average of $3,3501—the AHSC population will spend nearly $7.3 million per year. The community demand, in comparison, is projected to create $110M in spending over a 5-year period, or $22M per year. The $7.3M in AHSC spending would support nearly 21,000 square feet of retail space. As the AHSC campus grows in population, the retail demand will increase significantly. After full campus build out, it is likely that the internal demand alone for the AHSC could be closer to 60,000-80,000 gross square feet.

AHSC / University Market Retail Demand - 2012

Total Annual Spending Per Person $3,350

AHSC Faculty / Staff 687Miami-Date County Public Health Employees 700Ambulatory Care Clinic 300Medical Students 160Faculty / Staff within .25 miles 327

Total AHSC Population 2,174

Retail Sales / SF $350Resultant Retail Space Demand 21,000

FIGURE 4.9: AHSC and University market retail demand analysis. The demand for retail square footage on the part of the AHSC and University is a constant demand and reflects the amount of space that would support spending each year. Unless employment projections or enrollment increases, the 21,000 square feet of retail space—once put in place—will support spending in the future. The demands of the AHSC and University are applicable only because traditional campus retail spaces, such as the bookstore, could potentially be moved to a location in the NE quadrant of campus as part of the master planning effort. The community market demand number, on the other hand, represents the amount of retail space that could be absorbed each year as the population continues to grow. Community Demand The analysis of the retail market for the community relied upon the projected population change and expected sales activity within the study area to define square footage demands. Between 2007 and 2012, the population is projected to grow by 21,926 persons, or 7,448 households, and each new person will create demand for retail space. On average, each person within the market will spend approximately $19,299, including 1 ICSC Office Worker Retail Spending Patterns, 2006.

DEMAND ANALYSIS: 8TH STREET

Florida International University 10 Retail Demand Study

investments, vehicles, mortgages, food, recreation, etc. Because certain establishments are not appropriate for the study area and because certain services are already provided, the average per-person spending figure was reduced to $5,031. A home improvement store or car dealership, for example, are considered inappropriate uses for the study area, and so those spending categories were not included. The $5,031 figure generally includes food, personal care products, video equipment, and limited household supplies. The 21,926 persons will generate nearly $110M in new spending appropriate to the study area. Assuming average sales of $350 per square foot for sustainable retail businesses, the new spending will create a demand for over 315,000 square feet of retail space. On an annual basis, the spending should support an absorption of 63,000 square feet of retail space each year.

Community Market Retail Demand

Total Annual Spending Per Person $5,031Population Change, 2007-2012 21,926Retail Sales / SF $350Resultant Retail Space Demand 315,000Annual Retail Space Absorption 63,000

FIGURE 4.10: Community market retail demand analysis. Assuming a 20-30% penetration for the community retail market, the combined community and AHSC / University retail demand ranges from 81,000 square feet to 113,000 square feet.

Total Retail Demand

20% Market Penetration

30% Market Penetration

Community Retail Demand 63,000 95,000AHSC / University Demand 21,000 21,000

Resultant Retail Demand 84,000 - 113,000

FIGURE 4.11: Combined community market and AHSC / University retail demand.

Exhibit A

BEST PRACTICES

Florida International University Retail Demand Study 1

OBJECTIVES The objective of the Best Practices study was three-fold: to identify instances where universities developed Main Streets to enhance on-campus student life, to define proven options which are potentially relevant to the challenges facing FIU, and finally to inform the final recommendations in terms of how these options might be applied to the FIU Main Street and 8th Street projects. METHODOLOGY The research in this section was completed via various telephone and in-person interviews as well as Internet research of selected case studies relevant to this study. Main Street Case Studies The following university campus-related best practice case studies were selected:

• Rochester Institute of Technology • University of California, San Diego • University of Cincinnati • University of Central Florida

University Campus Edge Retail Case Studies The following campus edge retail best practice case studies were selected according to the criteria noted above:

• Florida Atlantic University • George Washington University • Ohio State University

The following matrix describes the issue each university faced and the actions that were taken to solve the problem.

BEST PRACTICES

Florida International University 2 Retail Demand Study

CASE STUDY ISSUE SOLUTION / PROJECT SUMMARY

Rochester Institute of Technology

• No real gateway to campus. • Little campus life. • Student recruitment and

retention issues.

The development of Park Point at RIT, an $85 million mixed-use development that includes housing, retail and dining options.

University of California, San Diego

• No collegetown atmosphere. • No central hub of student activity

on campus. • Recruitment and retention

issues.

The development of a campus downtown to create a hub of student activity. The project includes a student services center, student union building, dinging, retail, classrooms and a lecture hall / movie theater.

University of Cincinnati

• Little campus life. • Recruitment and retention

issues.

The creation of an internal campus main street. The $234 million mixed-use project includes a student services center, student life center, recreation center and campus housing.

University of Central Florida

• No central hub of student activity on campus.

• Little campus life. • Recruitment and retention

issues.

The development of Knight’s Plaza, a mixed-use development centered around the athletic village. The project includes a new area, housing and retail.

Florida Atlantic University

• Develop excess university land. • Generate money for the

university.

The development of University Commons, a 174,000 sf lifestyle center.

George Washington University

• Redevelopment of former university hospital.

• Generate money for the university.

• Enhance neighborhood retail options.

The development of Square 54 and the I Street retail corridor. The Square 54 mixed-use development will include 450,000 sf of office space, 330,000 sf of apartments and 88,000 sf of retail.

Ohio State University

• Revitalization of the University District.

• Enhance the housing and retail options in the neighborhood.

• Create a sense of place to foster the collegetown atmosphere.

The development of Square 54 and the I Street retail corridor. The Square 54 mixed-use development will include 450,000 sf of office space, 330,000 sf of apartments and 88,000 sf of retail.

BEST PRACTICES

Florida International University Retail Demand Study 3

ROCHESTER INSTITUTE OF TECHNOLOGY – ROCHESTER, NEW YORK Background Rochester Institute of Technology is a large private university located in the southwest section of Rochester. RIT’s suburban location with limited nearby transportation and entertainment options provided little in the way of a collegetown atmosphere. Recognizing the increasing importance of the student experience outside the classroom, RIT administrators commenced the planning and development of a collegetown-type development to create a competitive position for the University and to help with student retention. The Intervention With excess land in the northeast corner of campus, the University selected a developer to privately develop 64 acres of land to create a dynamic student community that will serve as the University’s new commercial gateway into campus. Park Point at RIT is an $85 million mixed-use project that includes 80,000 square feet of retail and 300 student apartments (900 beds). Anchored by a two-story, 40,000 square foot Barnes & Noble Academic Superstore, other retail uses include clothing stores, dining and entertainment establishments and a salon. Construction began in 2007 with a projected completion date of August 2008. As of March 2008, nearly 95% of the retail space has been leased. Deposits for the housing are going well but not as expected. In order to ensure high occupancy, the housing has been opened to the general community, much to the dismay of many RIT students. Park Point at RIT is being developed by the Wilmorite Company, a national retail and student housing developer. The University and Wilmorite entered into a ground lease agreement where the developer pays RIT a fixed amount annually for a specified period of time. Wilmorite also manages the retail leasing while United Reality Management manages the operations of the housing. Retail Concepts

• RIT Bookstore (Barnes & Noble) • Salon and Spa • Fitness Center

BEST PRACTICES

Florida International University 4 Retail Demand Study

• Cellular phone store • Clothing • Sports Bar • Multiple dining establishments

Program Outcomes RIT benefits include:

• 80,000 SF of Retail ($28 sf/year) • 300 student apartments (900 beds) • The establishment of a campus entrance • A vibrant mixed-use community • Additional revenues for the University

Lessons Learned

• The market can only support so much retail—demand for retail was not as great as the University had expected.

• Affordability is key—the cost of housing is higher than most on- and off-campus options and has had an impact on their ability to lease the apartments.

• Patience is essential—the site had significant wetland issues which provided for a long and challenging permitting process.

BEST PRACTICES

Florida International University Retail Demand Study 5

UNIVERSITY OF CALIFORNIA, SAN DIEGO – SAN DIEGO, CALIFORNIA Background The sprawling campus of the University of California, San Diego is located in the upscale coastal community of La Jolla. Completely surrounded by a residential neighborhood and far removed from the commercial center of La Jolla, UCSD lacks a traditional collegetown atmosphere or central location for campus life. The Intervention Faced with strong competition for students with other University of California schools located in more vibrant areas, UCSD was at a competitive disadvantage when it came to the traditional collegetown atmosphere. Located in the upscale La Jolla neighborhood of San Diego there was little student-focused off-campus entertainment, retail and student housing. The quiet environment was good for studying but campus life left much to be desired. In the late 1980’s the University embarked on planning and developing a central location on campus that would serve as the hub for student life. The first phase was the replacement of the small and outdated Student Center with the Price Center, the University’s student union building. The Price Center includes the dining hall, foot court, student activity space, classrooms and retail. It is anchored by the University Bookstore and a large multi-purpose lecture hall that houses classes during the day and is a movie theater in the evening. Opened in the early 1990s, the Price Center was successful from the start and was quickly at capacity. With the Price Center now an emerging hub for campus life, the University developed plans to create a “downtown” for the campus. The new downtown includes a new student services center and an expanded price center designed around expansive outdoor areas to create an “outdoor room” and to take advantage of the year-round hospitable climate. The new Student Services center is a one-stop shop for all administrative functions of the University including, admissions, financial aid and the registrar. While most functions of student service centers are now done on-line, UCSD’s Student Services center will be the first stop for all prospective students and their

BEST PRACTICES

Florida International University 6 Retail Demand Study

parents. In addition to administrative functions the center also has a number of restaurants, student activity space and meeting rooms. In addition to the Student Services center and an expanded Price Center, initial plans called for student housing in the downtown. Thus far none has been developed primarily because of a lack of developable land. Retail Concepts

• UCSD bookstore • Grocery store • Copy center • Post office • Bike shop • The Loft, a campus pub, restaurant and performance space • Various ethnic restaurants

Program Outcomes

• A vibrant mixed-use hub of activity for the campus. • Campus amenities that aid in recruitment and retention of students. • A place that students can identify with as the heart of the campus.

Lessons Learned

• Marketing and programming are essential to attracting students to the downtown in the evening.

• The Student Services Center has not drawn as many visitors as expected, primarily because most transactions are now done on-line.

• An active hub of campus life is a valuable recruitment tool for potential students. • Including student housing in the downtown would help to keep the area active well into

the evening.

BEST PRACTICES

Florida International University Retail Demand Study 7

UNIVERSITY OF CINCINNATI – CINCINNATI, OHIO Background The University of Cincinnati is a large public research institution located near downtown Cincinnati. Primarily a commuter campus with little options for student life, the University recognized the need to develop a central place on campus for students to congregate. The Intervention In an effort to create a sense of place and keep students on campus longer, the University commenced the planning and development of an on-campus main street concept that located a number of high traffic facilities along a central corridor. The University strategically located the student services center, student life center, recreation center and student residence halls in close proximity to the athletic village to create a critical mass of activity on the campus. The facilities all front onto a fully landscaped and programmed corridor creating a main street atmosphere. To further create a sense of place and brand the area, the University continued its tradition of building facilities designed by famous architects that are cutting edge in design and technology. The anchors for the $234 million main street are the 350,000 square feet recreation center, the 114,000 square feet student life center and the University of Cincinnati bookstore. Dining and retail options along Main Street are diverse ranging from a traditional dining hall to a full-service sit down restaurant. Managed by Aramark, the dining establishments are a mix of local and regional restaurants and large national chains. Retail options include a computer store, cellular phone store, a convenience store and the bookstore. A unique asset to the main street is its proximity to the athletic facilities. During athletic events, Main Street is a hub of pre- and post-game activity. Businesses along Main Street have capitalized on this by fostering a street fair atmosphere on game day. With the high number of visitors, auxiliary services recognized the area’s potential for corporate sponsorships as another way to generate revenue for the University. Retail Concepts

• UC Bookstore • Business of Main (Computers) • Main Street Express Mart (Convenience) • Cellular Phone Store

BEST PRACTICES

Florida International University 8 Retail Demand Study

Recreation Center

Athletic Facilities

Student Services Center

Student Life CenterMain Street

Recreation Center

Athletic Facilities

Student Services Center

Student Life CenterMain Street

Recreation Center

Athletic Facilities

Recreation Center

Athletic Facilities

Student Services Center

Student Life CenterMain Street

Student Services Center

Student Services Center

Student Life CenterMain Street

Student Life CenterMain Street

• Stadium View Café • Catskeller • Market on Main

Program Outcomes

• 180,000 sf Student Services Center

• 114,000 sf Student Life Center

• 350,000 sf Recreation Center

• 811 on-campus beds • Students are spending more

time on campus. • A central hub of student life on campus. • A vibrant mixed-use neighborhood. • An increase in the number of visitors to UC. • Additional revenues to the University.

Lessons Learned

• Anchors are essential—the bookstore, dining options and recreation center are the main drivers of traffic for Main Street.

• Programming is critical—Main Street needs to have daily programming to continue to attract visitors and to foster the area’s sense of place.

• Build flexibility into the retail space—the retail spaces were too large for many of the retailers that wanted to be along Main Street. Dividable spaces would have allowed for more retail options.

BEST PRACTICES

Florida International University Retail Demand Study 9

UNIVERSITY OF CENTRAL FLORIDA – ORLANDO, FLORIDA Background The University of Central Florida is a largest public institution in the state of Florida and the sixth largest in the nation. Located in Orlando, UCF has traditionally been a commuter campus with many non-traditional students. In an effort to transition to a more traditional campus atmosphere, the University has begun to develop the facilities and ammentites on more traditional campuses. Over the past decade the University has been active in building more on-campus housing, enhancing campus ammenities and improving the athletics department. The Intervention A major component of their efforts to enhance a number of aspects of the UCF campus, the University embarked on a multifaceted approach to create a hub of activity on campus, recruit and retail students and to enhance the competitiveness of the athletics department. The development of the $300 million Knights’ Plaza is an attempt to address many of the issues in one major project. Knights’ Plaza consists of a new 10,000-seat arena / convocation center, a new 45,000-seat football stadium, 89,000 square feet of retail, a 24,000 square foot dining facility, 2,000 on-campus beds and two 700-space parking garages. While still in the early stages the project has been a success and shows potential for the future. Retail Concepts

• Ron Jon Surf Shop • UCF Bookstore (Barnes & Noble) • Red Brick Pizza • Knight and Firkins English Pub • University Pharmacy • Convenience Store • Salon / Spa

BEST PRACTICES

Florida International University 10 Retail Demand Study

Program Outcomes

• Enhanced concerts and sporting events at the convocation center. • A nighttime hub of activity on the campus. • Expanded on-campus retail options. • A recruitment and retention tool for both the university and the athletics department.

Lessons Learned

• The campus bookstore, dining facility and event traffic from the convocation center drive the retail sales at Knights Plaza.

• The phased construction process has been difficult for retailers as there is not yet a critical mass of retailers and visitors are not sure that businesses are open.

• The metered parking needs to be studied and implemented in a way that is fair to both visitors and retailers.

• Many students feel that it is too far removed from the center of campus.

BEST PRACTICES

Florida International University Retail Demand Study 11

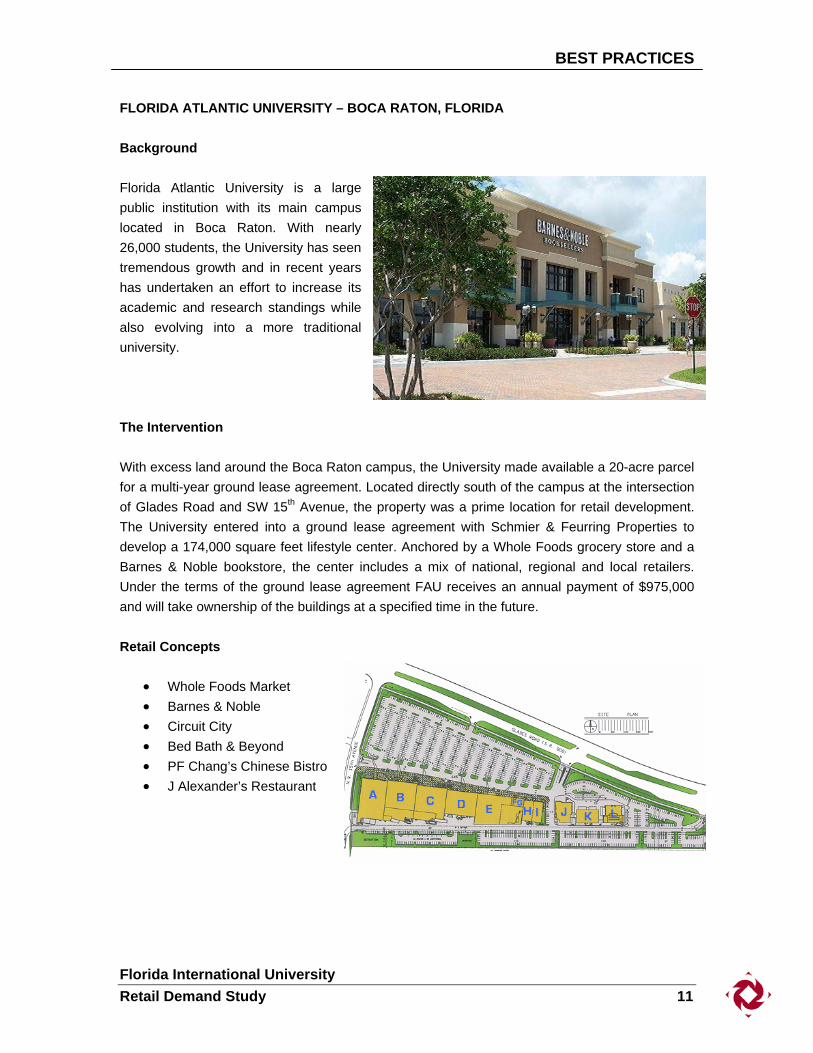

FLORIDA ATLANTIC UNIVERSITY – BOCA RATON, FLORIDA Background Florida Atlantic University is a large public institution with its main campus located in Boca Raton. With nearly 26,000 students, the University has seen tremendous growth and in recent years has undertaken an effort to increase its academic and research standings while also evolving into a more traditional university. The Intervention With excess land around the Boca Raton campus, the University made available a 20-acre parcel for a multi-year ground lease agreement. Located directly south of the campus at the intersection of Glades Road and SW 15th Avenue, the property was a prime location for retail development. The University entered into a ground lease agreement with Schmier & Feurring Properties to develop a 174,000 square feet lifestyle center. Anchored by a Whole Foods grocery store and a Barnes & Noble bookstore, the center includes a mix of national, regional and local retailers. Under the terms of the ground lease agreement FAU receives an annual payment of $975,000 and will take ownership of the buildings at a specified time in the future. Retail Concepts

• Whole Foods Market • Barnes & Noble • Circuit City • Bed Bath & Beyond • PF Chang’s Chinese Bistro • J Alexander’s Restaurant

BEST PRACTICES

Florida International University 12 Retail Demand Study

BEST PRACTICES

Florida International University Retail Demand Study 13

GEORGE WASHINGTON UNIVERSITY – WASHINGTON, D.C. Background George Washington University is a large private institution located in the Foggy Bottom neighborhood of Washington, D.C. Faced with growing student enrollment, the need to expand to meet the University’s population and mission, and a very contentious town-gown relationship, GW seeks to redevelop the only vacant parcel of land on its campus. The Intervention Square 54 is a vacant 2.5-acre parcel of land that was once the site of the old George Washington Hospital. Located on Washington Circle, the property is owned by the University and is available for development under a 60-year ground lease agreement. The development team chosen to develop Square 54 is a joint venture of Boston Properties and Kettler. GW and the development team are currently in the planning and approvals process for the Square 54 mixed-use project. Plans call for a mixed-use project that includes 450,000 square feet of Class-A office space, 330,000 square feet of market-rate apartments, 88,000 square feet of retail space and an underground parking garage. Designed by Pelli Clarke Architects, it will be a signature address along Pennsylvania Avenue. As part of the approval process, GW was forced to create more neighborhood- and student-focused retail options in Foggy Bottom. To do so, the planning team has created a 3-block long retail corridor from Square 54 and the Foggy Bottom Metro station to the 2000 Pennsylvania retail center. Plans call for the creation of retail spaces in the ground floors of existing academic and office buildings, outdoor seating, street furniture and enhanced streetscaping. The intent is to create a Main Street on the campus and within the neighborhood that will be a center of activity for both the students and the local residents. Build-out will occur over a 15-year period as properties redevelop and space becomes available. Proposed Retail Concepts

• Neighborhood grocery store. • High-end restaurant. • Upscale retail. • Neighborhood- and student-focused retail along I Street.

BEST PRACTICES

Florida International University 14 Retail Demand Study

Lessons Learned

• Neighborhood buy-in critical—with a contentious relationship with the Foggy Bottom neighborhood, it was essential that GW was inclusive during the planning process.

• Office space and housing are lucrative—the majority of income from the ground lease comes from the office and housing components of the project.

• The neighborhood’s needs are also the university’s needs—Foggy Bottom is underserved with retail and GW doesn’t have a central hub of activity on campus. The development of the I Street retail corridor meets everyone’s needs.

BEST PRACTICES

Florida International University Retail Demand Study 15

OHIO STATE UNIVERSITY: CAMPUS PARTNERS – COLUMBUS, OHIO Background Ohio State University is one of the largest public institutions in the United States with an enrollment of more than 50,000 students. After decades of disinvestment, the University District, an area located on the edge of OSU’s Columbus campus, had become a crime-ridden strip of rundown buildings and campus bars. The Intervention In 1995, Ohio State University and the City of Columbus created Campus Partners for Community Urban Redevelopment to improve the quality of life in University District. Campus Partners, a 501(c)(3) organization with its primary funding from Ohio State, spearheaded a community-based planning process to develop a comprehensive revitalization plan for the area. The major initiatives of the plan were to create a collegetown atmosphere around the campus; improve the retail and rental housing markets; and improve the quality of life in the neighborhood. A major initiative of the revitalization plan was to redevelop a 7.5-acre parcel of land on the southern edge of campus into a vibrant mixed-use community. In 1999 it commenced another community-based planning process for the site and proposed a $153 million mixed-use project featuring restaurants, an eight-screen cineplex, locally and nationally owned retailers, 184 market-rate apartments for faculty and staff, office space, and a 1,200-space parking garage. Financing for the project came from the University, city, state and a mix of New Market Tax Credits and Tax Increment Financing. Campus Partners assumed the role of developer with the help of Jones Lang LaSalle and began construction in 2003. The project opened in the fall of 2005 with much fanfare from the University, city and neighborhood. The project has created a southern gateway to the campus and has begun to spur other private development on adjacent parcels of land. Retail Concepts

• OSU Campus Bookstore (Operated by Barnes & Noble) • Salon & Spa • Potbelly Sandwich Works • Sunflower Market • Caribou Coffee • Panera Bread • McFadden’s Restaurant & Saloon

BEST PRACTICES

Florida International University 16 Retail Demand Study

Program Outcomes

• 184 market-rate apartments for faculty, staff and mature students. • 88,000 square feet of office space. • 249,000 square feet of retail space. • 1,200 space parking garage. • Increased private sector development.

Lessons Learned

• Getting neighborhood buy-in was critical to the projects success. • Patience and perseverance are essential—the planning, financing and development

process was very complex and needed committed leadership that could withstand a long rigorous process.

• The development model was critical to the projects success—Campus Partners realized early on that they did not have the capacity to develop a mixed-use project alone. Bringing in a large national real estate advisory firm to help guide the project was essential to Campus Gateway’s realization.

BEST PRACTICES

Florida International University Retail Demand Study 17

LESSONS LEARNED The following lessons garnered from the above case studies are especially noteworthy for the purposes of this study. In moving forward the University will have to utilize a number of these lessons learned because there is no single solution to the problem.

• Open, continued, and pro-active communication and education between stakeholder groups is critical to effective town-gown cooperation.

• The mixed-use development approach is a powerful urban revitalization trend nationally

and internationally, and can amplify positive results for Main Street Development.

• Programming is critical — the physical design of Main Street is not enough to attract visitors. Daily programming with events such as festivals, farmers markets and concerts are necessary to amplify the success of Main Street.

• Flexibility is essential — mixed-use, Main Street development continuously evolves as

projects mature and retail trends change. Finding the right mix of uses may take some time; it is critical that the spaces are designed in a way that they can be changed if necessary.

For further details on how the above may be translated into potential solutions, refer to Section 1: Executive Summary.

Exhibit B

FOCUS GROUP REPORT

Florida International University Retail Demand Study 1

FOCUS GROUP REPORT Objectives The purpose of the focus group and intercept interviews was to engage a variety of individuals in dynamic conversation about retail issues at Florida International University. B&D was trying to develop a better understanding of ways that retail options can be improved to positively impact FIU student life. The focus groups are intended to yield qualitative data for the researchers, while identifying sensitivities and previously unconsidered issues surrounding retail options at FIU. Methodology B&D organized focus groups to obtain a diverse mix of feedback from a wide range of FIU students, faculty, and staff. Over 65 individuals participated in nine focus groups on January 14th and 15th, 2008, on the FIU campus. In addition, B&D conducted random intercept interviews with students across different areas of campus. A moderator from B&D led each of the focus group sessions. The moderator guided the conversation to address retail issues. The moderator presented a series of open-ended questions and encouraged individuals to discuss tangential issues and engage in dynamic conversation. While the moderator was predisposed to obtaining answers to the questions asked, he or she also paid close attention to participant-generated issues raised during the interviews. Focus Groups Composition Group A: Commuter Students 10 participants (5 female, 5 male) Group B: On-Campus Students 4 participants (2 female, 2 male) Group C: Commuter Students 14 participants (10 female, 4 male) Group D: On-Campus and Commuter Students 14 participants (10 female, 4 male) Group E: Faculty and Staff 12 participants (7 female, 5 male) Group F: On-Campus Students 14 participants (10 female, 4 male) Group G: Faculty and Staff 14 participants (7 female, 7 male)

FOCUS GROUP REPORT

Florida International University 2 Retail Demand Study

Summary of Findings Why did you choose to attend or work at FIU? Many students chose to attend FIU because it is close to home and affordable. Several students indicated that they chose FIU because they like the diversity on campus and that it is a welcoming environment for international students. Faculty chose FIU because it provides many opportunities for growth and career enhancement. A number of faculty members commented that they enjoy the mix of backgrounds among faculty and staff and the sense of community on campus. Students, faculty and staff agreed that it is exciting to be on a rapidly growing campus. More specific points included: On-Campus Residents

• A number of students were attracted to FIU because of its diversity and programs for international students.

• Five students chose FIU because they were recruited to play sports. • One student responded that he chose FIU because of the growing campus and its