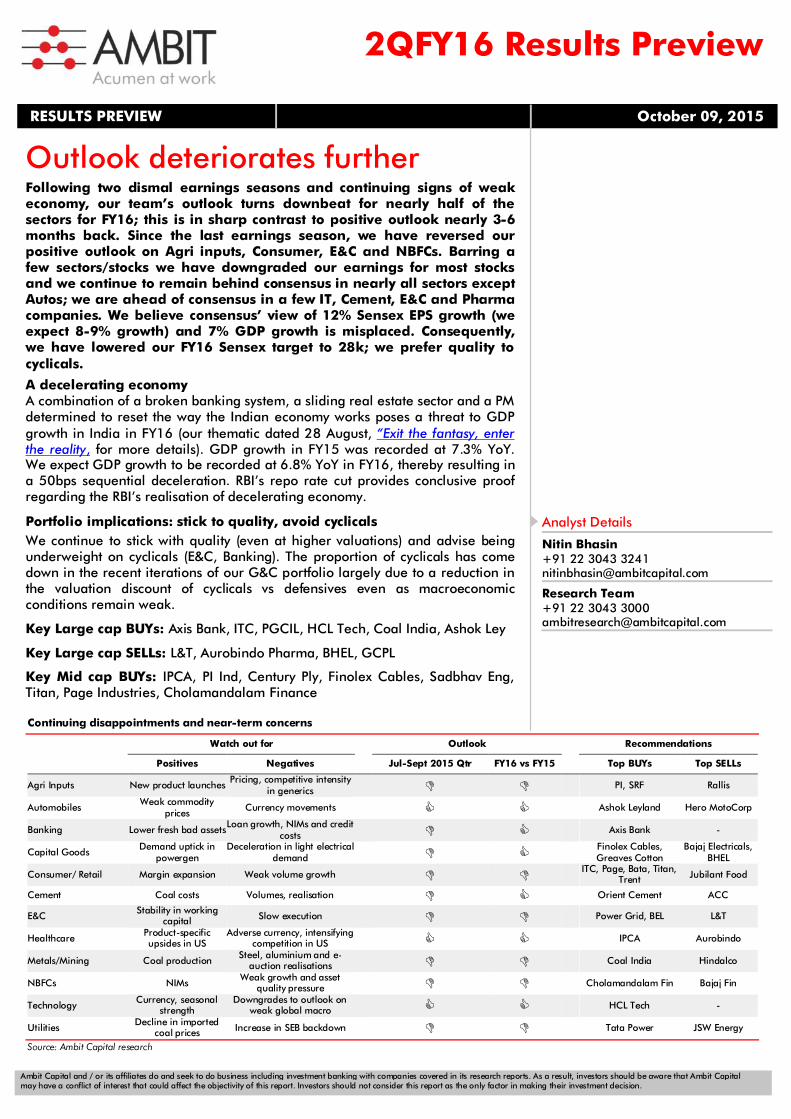

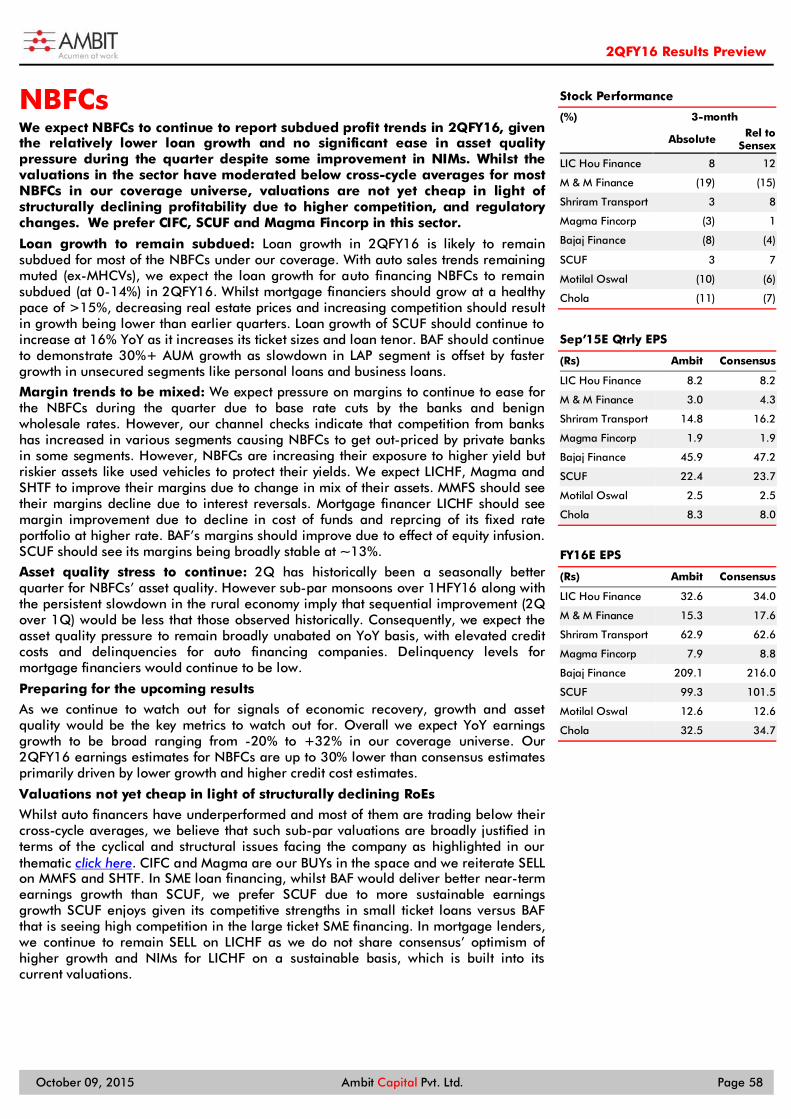

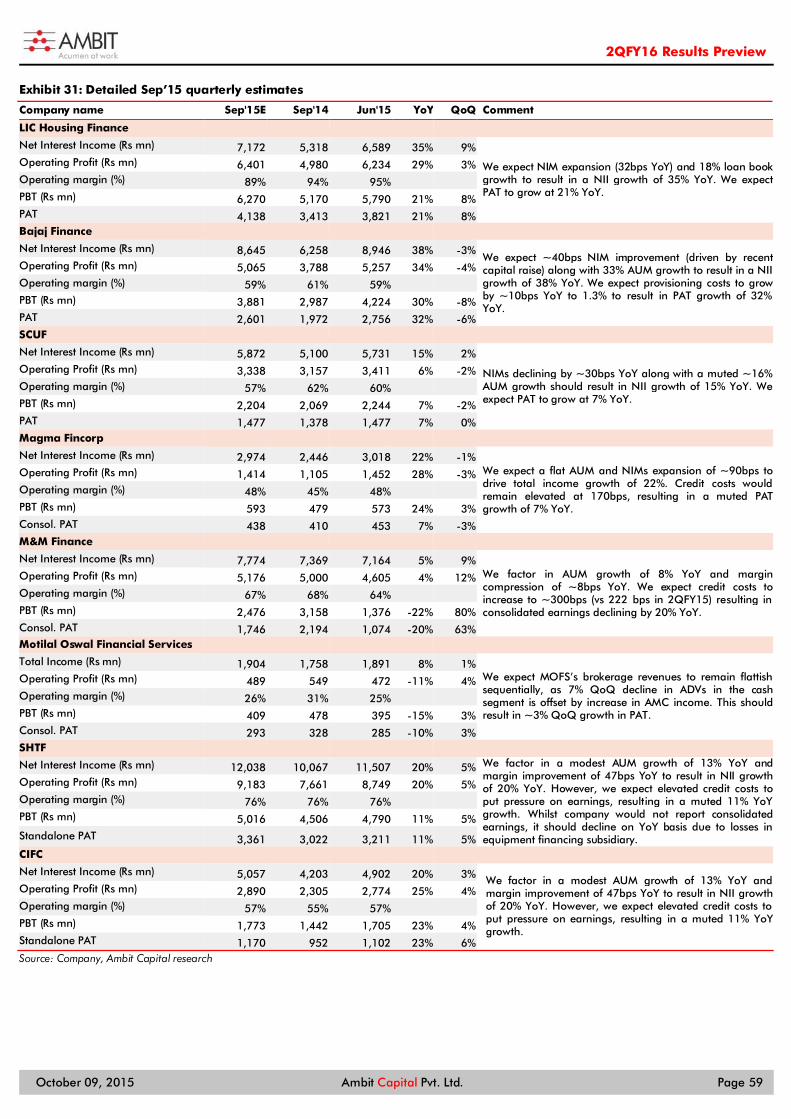

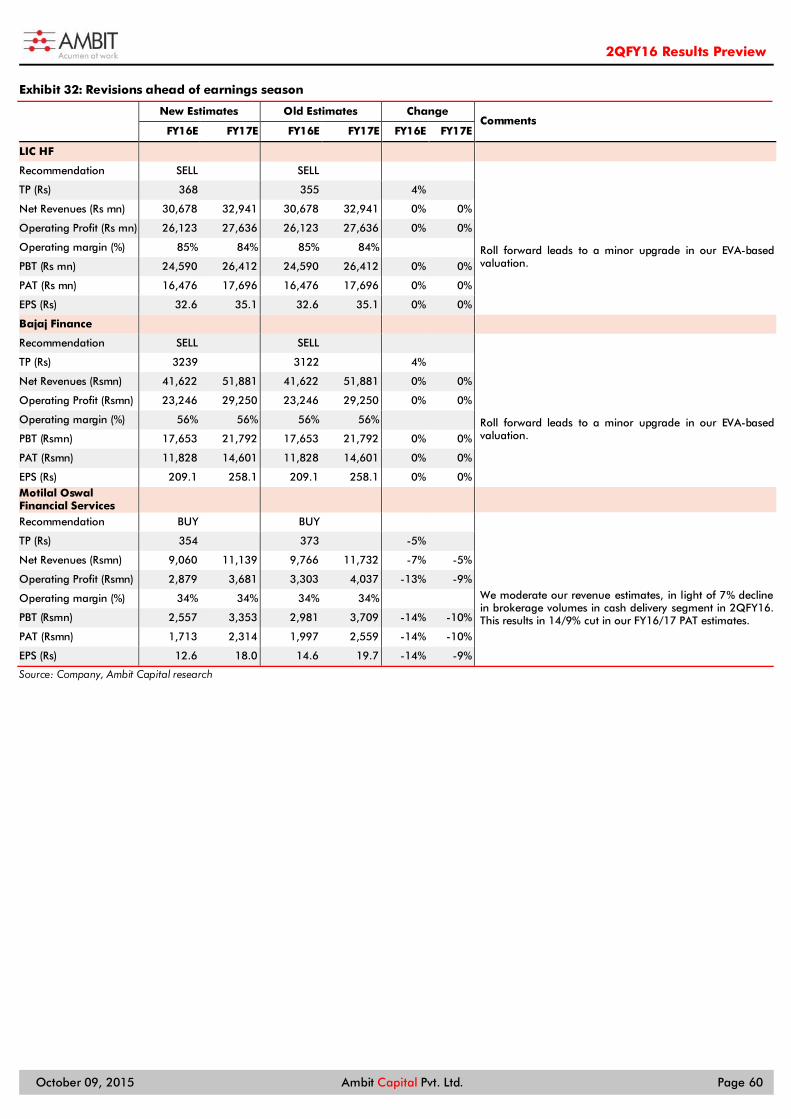

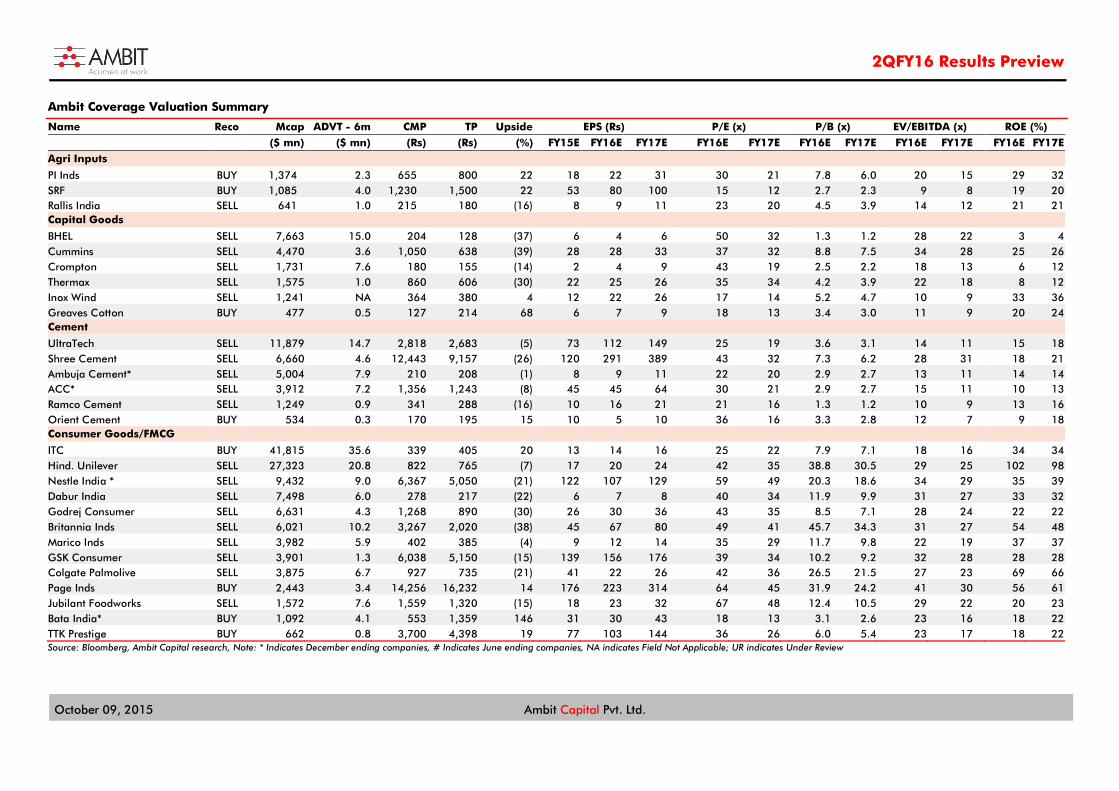

RESULTS PREVIEW October 09, 2015 Outlook...

75

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision. Outlook deteriorates further Following two dismal earnings seasons and continuing signs of weak economy, our team’s outlook turns downbeat for nearly half of the sectors for FY16; this is in sharp contrast to positive outlook nearly 3-6 months back. Since the last earnings season, we have reversed our positive outlook on Agri inputs, Consumer, E&C and NBFCs. Barring a few sectors/stocks we have downgraded our earnings for most stocks and we continue to remain behind consensus in nearly all sectors except Autos; we are ahead of consensus in a few IT, Cement, E&C and Pharma companies. We believe consensus’ view of 12% Sensex EPS growth (we expect 8-9% growth) and 7% GDP growth is misplaced. Consequently, we have lowered our FY16 Sensex target to 28k; we prefer quality to cyclicals. A decelerating economy A combination of a broken banking system, a sliding real estate sector and a PM determined to reset the way the Indian economy works poses a threat to GDP growth in India in FY16 (our thematic dated 28 August, “Exit the fantasy, enter the reality, for more details). GDP growth in FY15 was recorded at 7.3% YoY. We expect GDP growth to be recorded at 6.8% YoY in FY16, thereby resulting in a 50bps sequential deceleration. RBI’s repo rate cut provides conclusive proof regarding the RBI’s realisation of decelerating economy. Portfolio implications: stick to quality, avoid cyclicals We continue to stick with quality (even at higher valuations) and advise being underweight on cyclicals (E&C, Banking). The proportion of cyclicals has come down in the recent iterations of our G&C portfolio largely due to a reduction in the valuation discount of cyclicals vs defensives even as macroeconomic conditions remain weak. Key Large cap BUYs: Axis Bank, ITC, PGCIL, HCL Tech, Coal India, Ashok Ley Key Large cap SELLs: L&T, Aurobindo Pharma, BHEL, GCPL Key Mid cap BUYs: IPCA, PI Ind, Century Ply, Finolex Cables, Sadbhav Eng, Titan, Page Industries, Cholamandalam Finance 2QFY16 Results Preview RESULTS PREVIEW October 09, 2015 Continuing disappointments and near-term concerns Watch out for Outlook Recommendations Positives Negatives Jul-Sept 2015 Qtr FY16 vs FY15 Top BUYs Top SELLs Agri Inputs New product launches Pricing, competitive intensity in generics PI, SRF Rallis Automobiles Weak commodity prices Currency movements Ashok Leyland Hero MotoCorp Banking Lower fresh bad assets Loan growth, NIMs and credit costs Axis Bank - Capital Goods Demand uptick in powergen Deceleration in light electrical demand Finolex Cables, Greaves Cotton Bajaj Electricals, BHEL Consumer/ Retail Margin expansion Weak volume growth ITC, Page, Bata, Titan, Trent Jubilant Food Cement Coal costs Volumes, realisation Orient Cement ACC E&C Stability in working capital Slow execution Power Grid, BEL L&T Healthcare Product-specific upsides in US Adverse currency, intensifying competition in US IPCA Aurobindo Metals/Mining Coal production Steel, aluminium and e- auction realisations Coal India Hindalco NBFCs NIMs Weak growth and asset quality pressure Cholamandalam Fin Bajaj Fin Technology Currency, seasonal strength Downgrades to outlook on weak global macro HCL Tech - Utilities Decline in imported coal prices Increase in SEB backdown Tata Power JSW Energy Source: Ambit Capital research Analyst Details Nitin Bhasin +91 22 3043 3241 [email protected] Research Team +91 22 3043 3000 [email protected]

Transcript of RESULTS PREVIEW October 09, 2015 Outlook...

Ambit Capital and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, investors should be aware that Ambit Capital may have a conflict of interest that could affect the objectivity of this report. Investors should not consider this report as the only factor in making their investment decision.

Outlook deteriorates further Following two dismal earnings seasons and continuing signs of weak economy, our team’s outlook turns downbeat for nearly half of the sectors for FY16; this is in sharp contrast to positive outlook nearly 3-6 months back. Since the last earnings season, we have reversed our positive outlook on Agri inputs, Consumer, E&C and NBFCs. Barring a few sectors/stocks we have downgraded our earnings for most stocks and we continue to remain behind consensus in nearly all sectors except Autos; we are ahead of consensus in a few IT, Cement, E&C and Pharma companies. We believe consensus’ view of 12% Sensex EPS growth (we expect 8-9% growth) and 7% GDP growth is misplaced. Consequently, we have lowered our FY16 Sensex target to 28k; we prefer quality to cyclicals.

A decelerating economy A combination of a broken banking system, a sliding real estate sector and a PM determined to reset the way the Indian economy works poses a threat to GDP growth in India in FY16 (our thematic dated 28 August, “Exit the fantasy, enter the reality, for more details). GDP growth in FY15 was recorded at 7.3% YoY. We expect GDP growth to be recorded at 6.8% YoY in FY16, thereby resulting in a 50bps sequential deceleration. RBI’s repo rate cut provides conclusive proof regarding the RBI’s realisation of decelerating economy.

Portfolio implications: stick to quality, avoid cyclicals We continue to stick with quality (even at higher valuations) and advise being underweight on cyclicals (E&C, Banking). The proportion of cyclicals has come down in the recent iterations of our G&C portfolio largely due to a reduction in the valuation discount of cyclicals vs defensives even as macroeconomic conditions remain weak.

Key Large cap BUYs: Axis Bank, ITC, PGCIL, HCL Tech, Coal India, Ashok Ley

Key Large cap SELLs: L&T, Aurobindo Pharma, BHEL, GCPL

Key Mid cap BUYs: IPCA, PI Ind, Century Ply, Finolex Cables, Sadbhav Eng, Titan, Page Industries, Cholamandalam Finance

2QFY16 Results Preview

RESULTS PREVIEW October 09, 2015

Continuing disappointments and near-term concerns

Watch out for Outlook Recommendations

Positives Negatives Jul-Sept 2015 Qtr FY16 vs FY15 Top BUYs Top SELLs

Agri Inputs New product launches Pricing, competitive intensity

in generics PI, SRF Rallis

Automobiles Weak commodity

prices Currency movements

Ashok Leyland Hero MotoCorp

Banking Lower fresh bad assets Loan growth, NIMs and credit

costs Axis Bank -

Capital Goods Demand uptick in

powergen Deceleration in light electrical

demand Finolex Cables, Greaves Cotton

Bajaj Electricals, BHEL

Consumer/ Retail Margin expansion Weak volume growth ITC, Page, Bata, Titan,

Trent Jubilant Food

Cement Coal costs Volumes, realisation

Orient Cement ACC

E&C Stability in working

capital Slow execution Power Grid, BEL L&T

Healthcare Product-specific upsides in US

Adverse currency, intensifying competition in US IPCA Aurobindo

Metals/Mining Coal production Steel, aluminium and e-

auction realisations Coal India Hindalco

NBFCs NIMs Weak growth and asset

quality pressure Cholamandalam Fin Bajaj Fin

Technology Currency, seasonal

strength Downgrades to outlook on

weak global macro HCL Tech -

Utilities Decline in imported

coal prices Increase in SEB backdown Tata Power JSW Energy

Source: Ambit Capital research

Analyst Details

Nitin Bhasin +91 22 3043 3241 [email protected]

Research Team +91 22 3043 3000 [email protected]

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 2

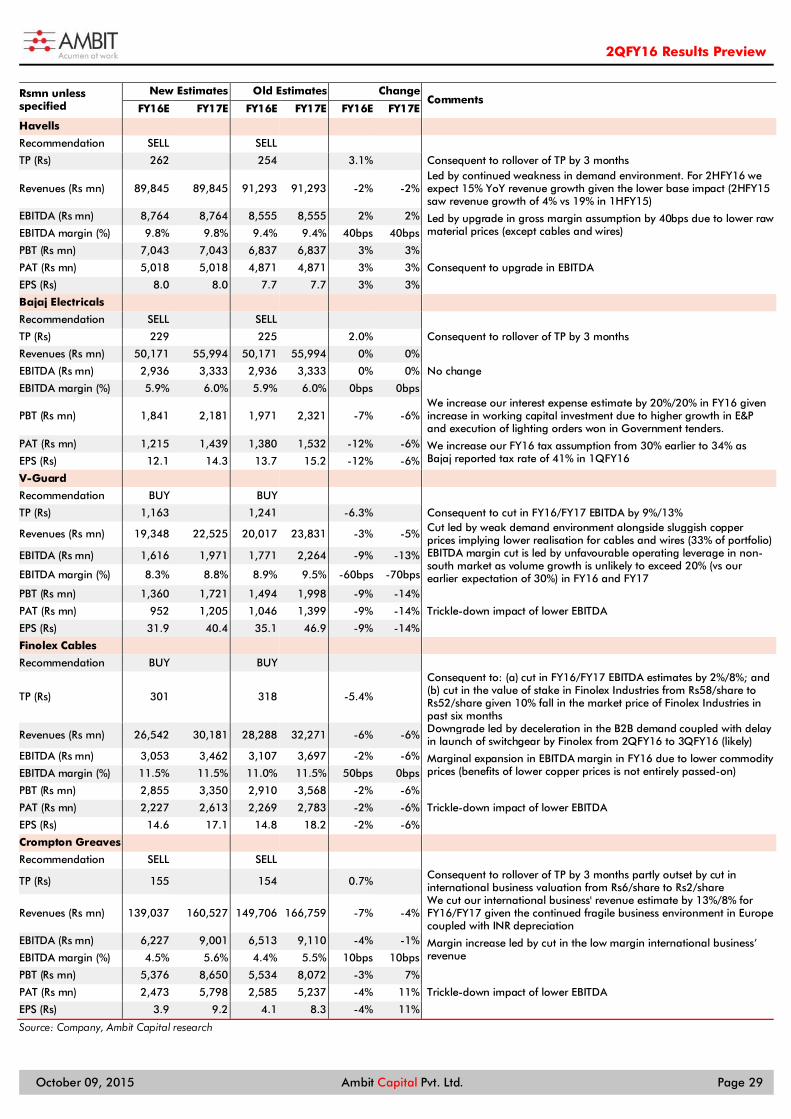

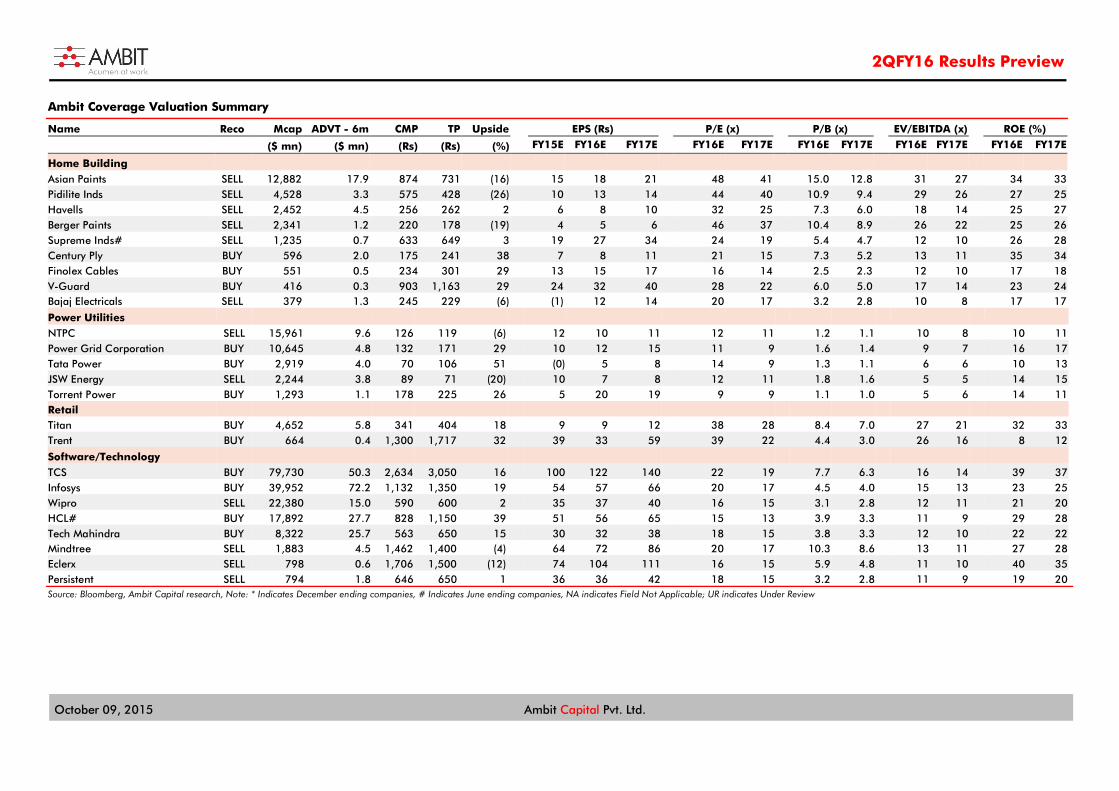

Exhibit 1: Material revisions to estimates and valuations ahead of earnings season (more than 5%)

Company New EPS estimate (%) Change in EPS estimates (%)

Valuation Stance

FY16E FY17E FY16E FY17E New Old Change (%) Ashok Leyland 4 5 10% 4% 105 99 7% BUY

BHEL 4 6 -37% -34% 128 116 9.8% SELL

Cummins 28 33 3% 2% 638 608 4.9% SELL

Bajaj Electrical 12 14 -12% -6% 229 225 2.0% SELL

V-Guard 32 40 -9% -14% 1,163 1,241 -6.3% BUY

Finolex Cables 15 17 -2% -6% 301 308 -5.4% BUY

Crompton 4 9 -4% 11% 155 154 0.7% SELL

AIA Engineering 42 50 -8% -10% 950 1,038 -8% SELL

Voltas 13 15 11.9 13.1 220 157 40% SELL

MOFS 13 18 -14% -9% 354 373 -5% BUY

Source: Ambit Capital research

Exhibit 2: Sectoral snapshot ahead of results

FY16 estimate revisions before results Compared to FY16 consensus Stance

Up Down Higher Lower BUY SELL

Agri Inputs - SRF, PI PI, SRF Rallis PI Rallis

Automobiles Ashok Leyland Maruti Suzuki

Ashok Leyland, Bajaj Auto,

Maruti Suzuki, Eicher Motors,

TVS Motor, Mahindra CIE,

Exide Industries,

Balkrishna Industries, Tata Motors, Hero

MotoCorp

Tata Motors, Maruti Suzuki, Ashok Leyland,

Mahindra CIE

Hero MotoCorp, Eicher Motors, Exide

Industries, Bajaj Auto, TVS Motor, Balkrishna

Industries

Banking - South Indian Bank

-

HDFC Bank, ICICI Bank, Axis Bank, SBI,

PNB, BOI, Karur Vysya Bank, Federal

Bank, City Union Bank

Axis Bank, IndusInd Bank, Bank of Baroda,

City Union Bank

ICICI Bank, Kotak Mahindra Bank,

HDFC Bank, SBI, PNB, Karur Vysya Bank

Capital Goods Cummins, Havells BHEL, Finolex, Bajaj, V-Guard, Crompton

Finolex Cables, Greaves Cotton

BHEL, Thermax, Cummins, Havells, V-

Guard, Bajaj Electricals, Crompton,

Inox

V-Guard, Greaves,

Finolex Cables

BHEL, Thermax, Cummins, Havells,

Bajaj, Crompton, Inox

Consumer

Asian Paints, Jubilant Foodworks, Berger

Bata, Page, Trent Pidilite, Jubilant

Foodworks, Asian Paints, Berger, Titan

Bata, TTK, Page, Titan, Trent

Jubilant, Asian Paints, Berger, Pidilite

Cement - -

UltraTech, Ambuja, Orient,

ACC Ramco, Shree orient

UltraTech, Ambuja, ACC, Ramco, Shree

E&C L&T, Power Grid, Voltas, Blue Star

AIA Engineering, Engineers India

Power Grid, Bharat

Electronics, Voltas, Engineers

India

L&T, AIA Engineering, VA Tech, Blue Star

Power Grid, Bharat Electronics

L&T, AIA Engineering, Voltas, Engineers

India, VA Tech, Blue Star

Healthcare NA NA Sun, IPCA,

Lupin, Torrent Pharma

Aurobindo, Dr. Reddy, Cadila

Lupin, Torrent, IPCA, Cadila

Aurobindo, Dr. Reddy, Cipla

Metals & Mining - - Nalco, Hindalco, Tata

Steel, SAIL, Coal India

Coal India Hindalco, Nalco, Tata

Steel, SAIL

NBFCs NA MOFS

NA SCUF, LICHF, MMFS, BAF, MGMA, CIFC

MGMA, SCUF, MOFS, CIFC

LICHF, MMFS, SHTF, BAF

Technology TCS, Infosys, Wipro,

TechM, eClerx, MindTree, Persistent

HCL Tech

HCLT, TechM, MindTree, eClerx

TCS, Infosys, Persistent

TCS, Infosys, HCLT, TechM

Wipro, MindTree, Persistent, eClerx

Utilities NTPC Tata Power,

Torrent Power JSWE, NTPC, Tata Power, Torrent

Power NTPC, JSWE

Source: Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 3

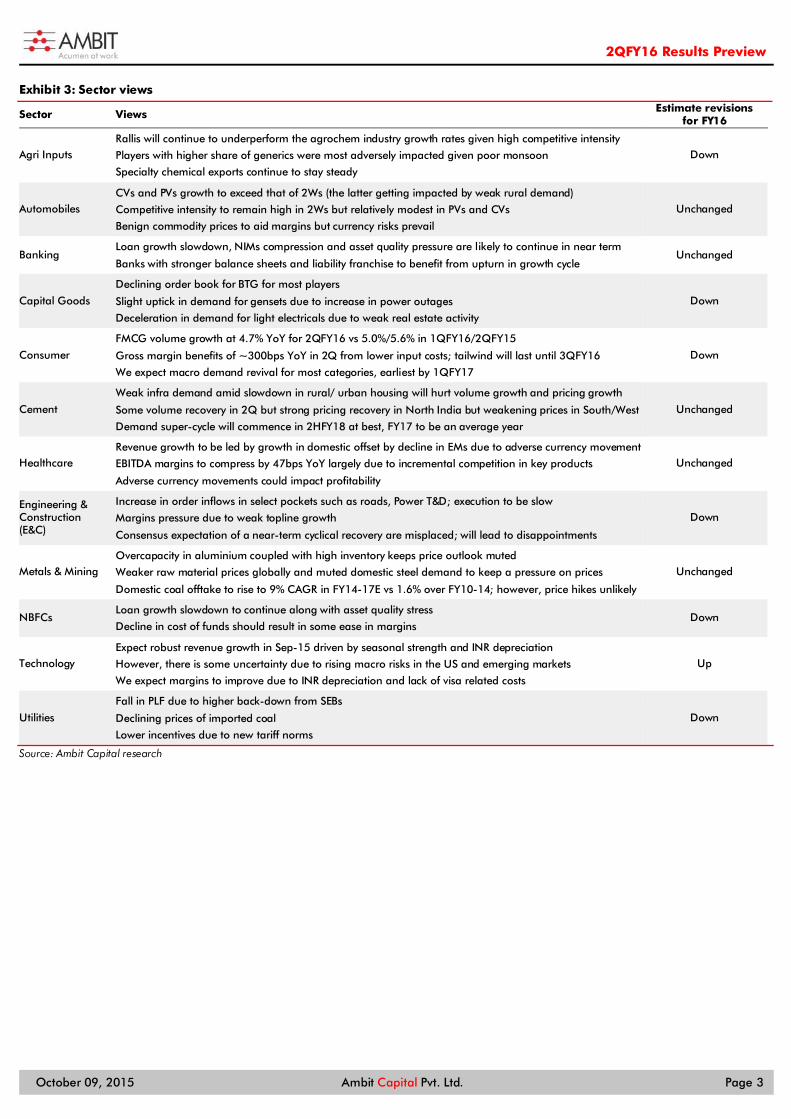

Exhibit 3: Sector views

Sector Views Estimate revisions for FY16

Agri Inputs Rallis will continue to underperform the agrochem industry growth rates given high competitive intensity

Players with higher share of generics were most adversely impacted given poor monsoon

Specialty chemical exports continue to stay steady

Down

Automobiles CVs and PVs growth to exceed that of 2Ws (the latter getting impacted by weak rural demand)

Competitive intensity to remain high in 2Ws but relatively modest in PVs and CVs

Benign commodity prices to aid margins but currency risks prevail

Unchanged

Banking Loan growth slowdown, NIMs compression and asset quality pressure are likely to continue in near term

Banks with stronger balance sheets and liability franchise to benefit from upturn in growth cycle Unchanged

Capital Goods

Declining order book for BTG for most players

Slight uptick in demand for gensets due to increase in power outages

Deceleration in demand for light electricals due to weak real estate activity

Down

Consumer

FMCG volume growth at 4.7% YoY for 2QFY16 vs 5.0%/5.6% in 1QFY16/2QFY15

Gross margin benefits of ~300bps YoY in 2Q from lower input costs; tailwind will last until 3QFY16

We expect macro demand revival for most categories, earliest by 1QFY17

Down

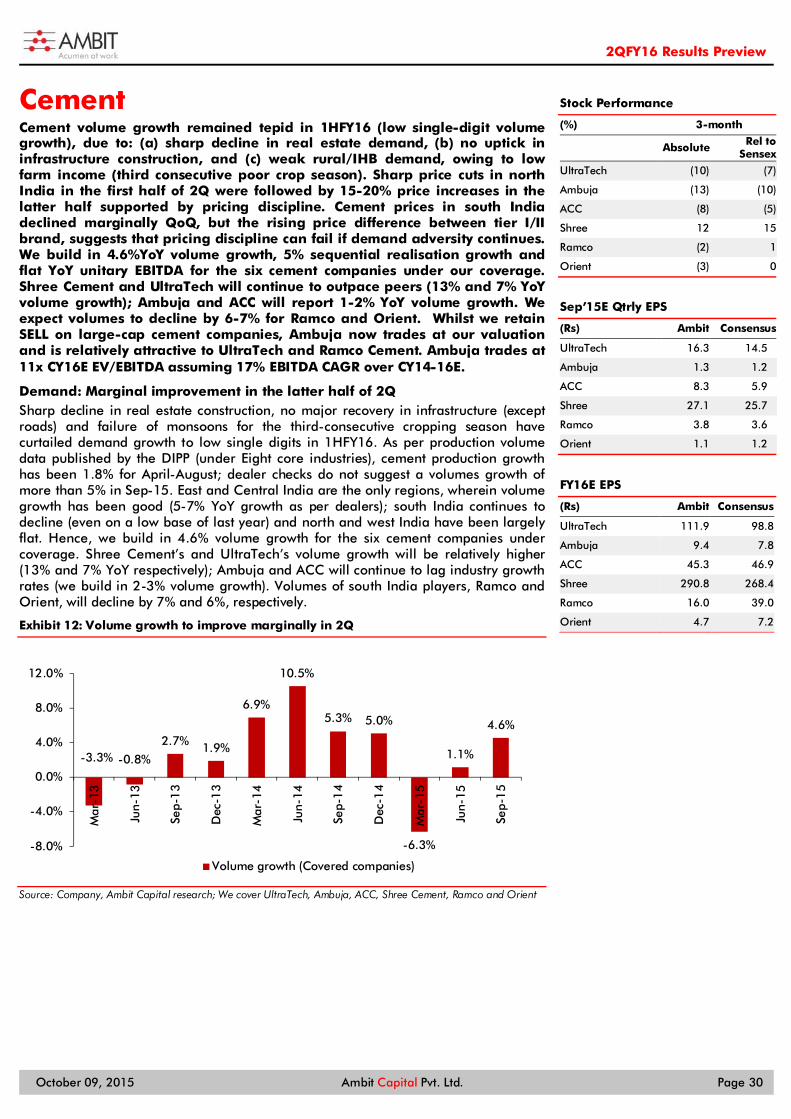

Cement

Weak infra demand amid slowdown in rural/ urban housing will hurt volume growth and pricing growth

Some volume recovery in 2Q but strong pricing recovery in North India but weakening prices in South/West

Demand super-cycle will commence in 2HFY18 at best, FY17 to be an average year

Unchanged

Healthcare Revenue growth to be led by growth in domestic offset by decline in EMs due to adverse currency movement

EBITDA margins to compress by 47bps YoY largely due to incremental competition in key products

Adverse currency movements could impact profitability

Unchanged

Engineering & Construction (E&C)

Increase in order inflows in select pockets such as roads, Power T&D; execution to be slow

Margins pressure due to weak topline growth

Consensus expectation of a near-term cyclical recovery are misplaced; will lead to disappointments

Down

Metals & Mining Overcapacity in aluminium coupled with high inventory keeps price outlook muted

Weaker raw material prices globally and muted domestic steel demand to keep a pressure on prices

Domestic coal offtake to rise to 9% CAGR in FY14-17E vs 1.6% over FY10-14; however, price hikes unlikely

Unchanged

NBFCs Loan growth slowdown to continue along with asset quality stress

Decline in cost of funds should result in some ease in margins Down

Technology Expect robust revenue growth in Sep-15 driven by seasonal strength and INR depreciation

However, there is some uncertainty due to rising macro risks in the US and emerging markets

We expect margins to improve due to INR depreciation and lack of visa related costs

Up

Utilities

Fall in PLF due to higher back-down from SEBs

Declining prices of imported coal

Lower incentives due to new tariff norms

Down

Source: Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 4

TOP BUY RECOMMENDATIONS Recommendation Upside (%) Rationale/catalysts

ITC

22

Expect flat cigarette volume growth YoY in 2HFY16 due to weak base (vs -15% YoY in 1HFY16)

Government’s hawkish stance against cigarette taxation is not sustainable

Upside from improvement in profitability of non-cigarette FMCG business

(ITC IN)

CMP: Rs332

TP: Rs405

Coal India

23

Offtake growth to revive to 9% CAGR in FY15-20E vs 1.6% CAGR recorded over FY10-14

Volume growth coupled with rising mix of contracted labour to derive operating leverage

CIL trades at FY17 P/E of 12.7x, in line with historical average

(COAL IN)

CMP: Rs 346

TP: Rs425

Axis Bank

40

The bank aggressively diversified and de-risked its balance sheet on the assets and liabilities side

Strong capital position, provision coverage and operating profitability offset asset quality risks

Trading at valuation of 11.7x FY17E EPS (a ~24% discount to new private sector banks’ average)

(AXSB IN)

CMP: Rs 492

TP: Rs690

HCL Tech

39

Better portfolio mix (higher exposure to cost-focused service-lines such as IMS)

Stable senior management team, efficient use of capital (RoE of 33% in FY15)

We expect that recent investments in the business will accelerate organic growth

(HCLT IN)

CMP: Rs838

TP: 1,150

Power Grid

29%

Capitalisation momentum ot sustain (Rs293bn in FY16) resulting in a 23% earnings CAGR (FY15-18)

Ability to raise capital at lower cost than peers makes it the front runner to win TBCB contracts

Inexpensive valuation of 1.4x FY16 P/B given its regulated business model and strong earnings visibility

(PWGR IN)

CMP: Rs 132

TP: Rs171

Titan Company

24

New Golden Harvest Scheme will begin contributing materially from FY17E (12% of jewellery revenues)

Low making charges, high debt:equity and restrictions on customer deposits will reduce competition

Stock trades at 27x FY17E earnings (FY17E EPS growth of 33%) at a discount to 5-year average of 32x

(TTAN IN)

CMP: Rs325

TP: Rs404

Bharat Electronics

16%

Moving up the value chain by increasing focus on system integration projects

Its project management skills, technical know-how and large manufacturing base are key advantages.

Well placed to leverage structural changes in defence procurement; 19x FY17 PE reasonable

(BHE IN)

CMP: Rs1,203

TP: Rs1,390

Ashok Leyland

15

MHCV demand continues to revive and AL continues to gain market share

Operating leverage, non-core asset sale and limited capex to improve profitability and balance sheet

Core CV business currently trades at 9.8x FY17E net earnings,10% higher than historical average

(AL IN)

CMP: Rs 92

TP: Rs105

Tata Power

50

Improving cash flows of Mumbai and Delhi distribution circle

Reducing losses at Mundra led by falling imported coal prices

Improving performance of Maithon led by sign up of long term PPAs

(TPW IN)

CMP: Rs70

TP: Rs106

Page Industries

19

Kidswear launch in 3QFY16, implementation of new IT platform, rapid expansion of EBOs

Competitive advantages include manufacturing prowess, brand and product development

Weak sales growth in 2QFY16E given distributor liquidity issues; ~100bps EBITDA margin gains

(PAG IN)

CMP: Rs 13,570

TP: Rs 15,764

Cholamandalam Finance

18

RoAs would improve to 2% by FY18E due to declining cost of funds and improving operating leverage

Growth in lucrative LCV financing and old CV financing should drive long term sustainable growth

Current valuations at 2.5x 1yr fwd P/B ignore the long-term growth prospects of the company

(CIFC IN)

CMP: Rs625

TP: Rs740

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 5

Recommendation Upside (%) Rationale/catalysts

IPCA

31

Earnings bottomed out; expect normalised revenue from HCQS and Insti business from 3QFY16

Import alert to be resolved by FY18E and see lumpy product approvals in FY19-20E

Strong positioning in the DNA and 5’R’ frameworks comforts us on the sustainability of earnings

(IPCA IN)

CMP: Rs 821

TP: Rs952

PI Industries

23

Credible play on the rising chemical exports opportunity plus the underpenetrated agri inputs sector

Industry-leading execution (27% revenue CAGR over FY09-15, 14-27% RoCEs over FY09-15)

Valuation implies 26x FY17 eps, we build 30% eps FY15-17 CAGR, high RoCEs, strong cash conversion

(PIIN)

CMP Rs652

TP Rs800

Sadhav Engineering

25

3.2x LTM book-to-bill and reducing leverage will drive 20%/37% EPC revenue/PAT CAGR over FY15-18

Improving traffic and debt refinancing to improve cash flows and generate growth capital

Inexpensive implied valuation of 11x for the construction basis the current market cap of SIPL

(SADE IN)

CMP: Rs 300

TP: Rs375

Trent Ltd

31

Improving sales density in Westside will result in doubling standalone EBITDA from FY15 to FY17E

Westside and Zara (49%JV) are plays on the largely unorganized 18bn womens wear market.

The stock trades at 15X FY17E EBITDA with EBITDA growth of 3x over FY15-17E.

(TRENT IN)

CMP: Rs1,315

TP: Rs1,717

Century Plyboards

38

Strengthening brand/distribution and raw material security aiding market share gains

Margin expansion (to 17.3%-17.7& in FY16-17 against 15.9% in FY15) led by benign commodity prices

30% + RoEs over FY16-18 and trading at a reasonable 16x FY17 EPS

(CPBI IN)

CMP: Rs 175

TP: Rs242

Finolex Cables

26

Expect Finolex to report the highest revenue growth in cables and wires led by pan India expansion

Ability to leverage brand is the highest given strong brand re-call (more than 50 year old brand)

Valuation at 13x FY17 P/E is attractive

(FNXC IN)

CMP: Rs 236

TP: Rs301

Greaves Cotton

67

Uptick in demand in FY16 led by recovery in 3W and 4Ws

Signing-up of at least one large OEM in FY16 in the 4W space in the 1.5-3.5 tonne

Doubling of market share in gensets over FY15-17E from 4% in FY15

(GRV IN)

CMP: Rs126

TP: Rs214

Source: Bloomberg, Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 6

TOP SELL RECOMMENDATIONS Recommendation Downside (%) Rationale/catalysts

L&T

7%

Due to rising proportion of civil projects, book-to-bill continues to increase; only 10% revenue growth in FY16

High proportion of capital employed (nearly half) in non-capex-recovery-oriented segments Our valuation for the standalone business implies 17x FY17 core P/E and see limited room for re-rating

(LT IN)

CMP: Rs1,534

TP: Rs1,420

BHEL

37 ~31% of BHEL’s order book is moving at slow pace and an additional 13% has actually been stalled. Enquiries from the private sector continue to be negligible Enquiries from NTPC may decelerate given its shift towards expanding through the acquisition route

BHEL IN

CMP: Rs 203

TP: Rs 128

Hero MotoCorp

2 Muted domestic motorcycle sales on the back of weak rural demand Rising competitive intensity and scooterisation to continue impacting Hero’s domestic market share The stock currently trades at 15.2x FY17 net earnings, marginally higher than historical average

HMCL IN

CMP: Rs 2,542

TP: Rs 2,500

Aurobindo Pharma

45 Aurobindo’s profits and future pipeline will be under threat as incumbents return in US over FY16-18 Lack of investments in long-term growth drivers; material governance issues with the promoter’s FY17E P/E is at 16.2x vs our implied multiple of 10.5x due to structural issues in its business

ARBP IN

CMP: Rs 755

TP: Rs 414

Godrej Consumer

30 Market share saturation in household insecticides; MNC competition in Hair Colour Macro/integration issues in its Africa business; Macro headwinds in Indonesia International business RoCE due above headwinds and management's inorganic growth ambitions.

(GCPL IN)

CMP: Rs1,265

TP: Rs890

Bajaj Finance

39 BAF’s asset quality risks due to slowdown in real-estate prices and increasing high-risk borrowers Increasing delinquencies in unsecured business loans pose additional risks Valuations of ~3.4x one-year forward P/B, do not factor in increased risks to asset quality and growth

(BAF IN)

CMP: Rs5,120

TP: Rs3,239

ACC

9 Weak demand and ongoing loss in market share leading to only marginal volume growth Poor cost efficiency leading to rising costs despite reduction in fuel prices Trading at a rich 10x one-year forward EBITDA, a 20% premium to its five-year average

(ACEM IN)

CMP: Rs1,357

TP: Rs1,241

Hindalco

5 Overcapacity in aluminium and high inventory keeps aluminium price outlook muted Deallocation of coal blocks has significantly impacted profitability of Mahan and Aditya smelters The stock is trading at FY17E EV/EBITDA of 6.6x, a premium to the historical average of 6.0x

(HNDL IN)

CMP: Rs81

TP: Rs78

JSW Energy

22 Decline in merchant realisation in FY16 and FY17 Limited decline in imported coal prices from hereon Limited organic growth expansion given leveraged balance sheet (FY16 net debt:equity of 1.8x).

(JSWE IN)

CMP: Rs89

TP: Rs71

Jubilant Foodworks

21 Over 40% price hikes cumulatively over the past two years amidst price elastic demand Pressure on SSG from high competitive intensity and store splits; >10% SSG at least 3 quarters away ~150bps EBITDA margin drag from Dunkin Donuts to continue for another three years

(JUBI IN)

CMP: Rs1,675

TP: Rs1,320

Rallis

21 Higher share of highly competitive generics facing price erosion in the domestic agro chemicals market Exports sales also muted as the major markets of Brazil and Australia are drought hit Muted margins in the fast growing seeds segments to drag the overall margin

RALI IN

CMP: Rs 217

TP: Rs 180

Bajaj Electricals

7 Loss of market share in consumer durables business due to roll out of theory of constraints (TOC) Minimal margin expansion in lightings given rising participation in Government tenders E&P business’s RoCE to remain capped at 6%

(BJE IN)

CMP: Rs 250

TP: Rs229

Source: Bloomberg, Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 7

Economy GDP growth to decelerate in FY16; expect 25bps rate cut in FY16 form hereon A combination of a broken banking system, a sliding real estate sector and a PM determined to reset the way the Indian economy works poses a threat to GDP growth in India in FY16 (see our thematic dated 28 August, “Exit the fantasy, enter the reality, for more details). GDP growth in FY15 was recorded at 7.3% YoY. We expect GDP growth to be recorded at 6.8% YoY in FY16, thereby resulting in a 50bps sequential deceleration. As regards inflation, we expect CPI inflation to bottom out by 2QFY16 and then rise to an average of 5% YoY in 4QFY16. As the CPI inflation remains well below the RBI’s comfort zone and as the downside risks to the GDP growth increases, we expect the RBI to cut the repo rate by another 25bps in FY16 (over and above the 125bps which the RBI has already administered in CY15).

In our note dated March 23, 2015, “Modi hits the ‘reset’ button,” we made the point that PM Modi is seeking to engineer three structural resets: (1) shift India’s savings landscape away from gold & land and towards the formal financial system, (2) disrupt the Indian model of crony capitalism model, and (3) redefine India’s subsidy mechanism. The new structure will take some time to become fully operational; hence, the three resets look likely to adversely impact GDP growth in FY16. The short-term pain in GDP growth will be driven by: (1) alterations in the subsidy regime, which will adversely affect rural/semi-urban consumption and construction activity; (2) crony capitalists’ refusal to begin capex activity, as they see reduced scope for supernormal profits under Modi; and (3) Modi’s attack on black money, leading to a crack in land & real estate prices, which will adversely impact lenders’ balance sheets.

Furthermore, in our note dated August 28 (click here for the note) we had highlighted the challenges faced by the macro environment both from rising domestic risks (PM Modi’s three resets, a major real estate slowdown, banking system breakdown and the NDA’s inability to expedite structural reforms) and global risks (a failing Chinese economy likely to lead to further yuan devaluation).

In view of the above-mentioned dynamics, we believe that the GDP growth rate in FY16 will be lower than FY15 (see Exhibit 1 on the right-hand side).

Inflation to average at 4.5% in Fy16

CPI inflation was recorded at an average of 6% YoY in FY15. We expect average inflation to be recorded at ~4.5% YoY in FY16 which implies that whilst CPI inflation is likely to abate in FY16. In terms of the trajectory, we expect CPI inflation to bottom out to an average of ~4% YoY in 2QFY16 and then rise to an average of ~5% YoY in 4QFY16.

Overall, we expect CPI inflation to be recorded at an average of 4.5% YoY in FY16 (see Exhibit 2 on the right-hand side).

Monetary policy implications

In its previous policy review on September 29, the RBI cut the repo rate by 50bps. Whilst we continue to expect the RBI to cut the repo rate by another 25bps over the remaining part of FY16, we do not expect the RBI to administer this rate cut at the next monetary policy review scheduled for December 1, 2015, given that we expect the Fed to administer a rate hike before the end of CY15 and given that the RBI has clearly said that in the immediate term it will focus on ensuring that banks pass on the RBI’s policy rate cuts.

We expect GDP growth in FY16 to be recorded at 6.8% YoY

Source: CEIC, Ambit Capital research

We expect CPI inflation to average at 4.5% YoY in FY16

Source: CEIC, Ambit Capital research

5.1%

6.9%7.3%

6.8%

4%

5%

6%

7%

8%

FY13 FY14 FY15 FY16(E)

Rea

l GD

P g

row

th(Y

oY

cha

ng

e, i

n %

)

2%

3%

4%

5%

6%

1Q

FY16

2Q

FY16

(E)

3Q

FY16

(E)

4Q

FY16

(E)

CPI in

fla

tion

(YoY

ch

an

ge,

in %

)

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 8

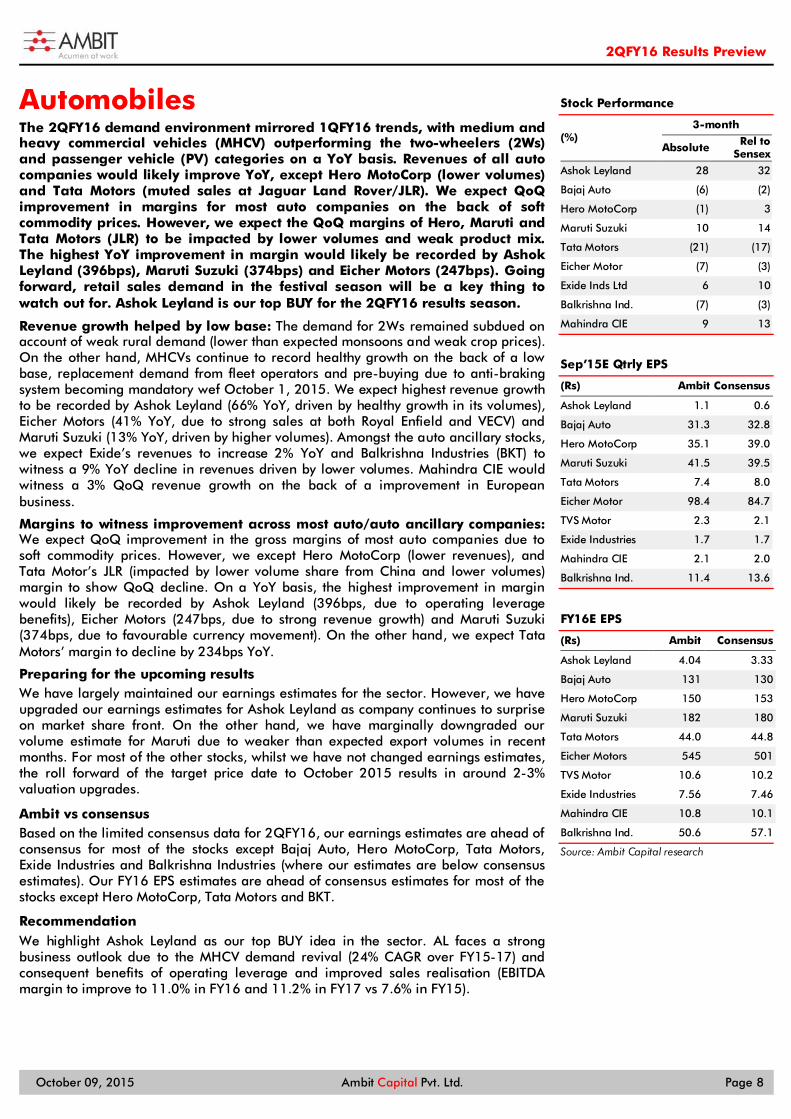

Automobiles The 2QFY16 demand environment mirrored 1QFY16 trends, with medium and heavy commercial vehicles (MHCV) outperforming the two-wheelers (2Ws) and passenger vehicle (PV) categories on a YoY basis. Revenues of all auto companies would likely improve YoY, except Hero MotoCorp (lower volumes) and Tata Motors (muted sales at Jaguar Land Rover/JLR). We expect QoQ improvement in margins for most auto companies on the back of soft commodity prices. However, we expect the QoQ margins of Hero, Maruti and Tata Motors (JLR) to be impacted by lower volumes and weak product mix. The highest YoY improvement in margin would likely be recorded by Ashok Leyland (396bps), Maruti Suzuki (374bps) and Eicher Motors (247bps). Going forward, retail sales demand in the festival season will be a key thing to watch out for. Ashok Leyland is our top BUY for the 2QFY16 results season.

Revenue growth helped by low base: The demand for 2Ws remained subdued on account of weak rural demand (lower than expected monsoons and weak crop prices). On the other hand, MHCVs continue to record healthy growth on the back of a low base, replacement demand from fleet operators and pre-buying due to anti-braking system becoming mandatory wef October 1, 2015. We expect highest revenue growth to be recorded by Ashok Leyland (66% YoY, driven by healthy growth in its volumes), Eicher Motors (41% YoY, due to strong sales at both Royal Enfield and VECV) and Maruti Suzuki (13% YoY, driven by higher volumes). Amongst the auto ancillary stocks, we expect Exide’s revenues to increase 2% YoY and Balkrishna Industries (BKT) to witness a 9% YoY decline in revenues driven by lower volumes. Mahindra CIE would witness a 3% QoQ revenue growth on the back of a improvement in European business.

Margins to witness improvement across most auto/auto ancillary companies: We expect QoQ improvement in the gross margins of most auto companies due to soft commodity prices. However, we except Hero MotoCorp (lower revenues), and Tata Motor’s JLR (impacted by lower volume share from China and lower volumes) margin to show QoQ decline. On a YoY basis, the highest improvement in margin would likely be recorded by Ashok Leyland (396bps, due to operating leverage benefits), Eicher Motors (247bps, due to strong revenue growth) and Maruti Suzuki (374bps, due to favourable currency movement). On the other hand, we expect Tata Motors’ margin to decline by 234bps YoY.

Preparing for the upcoming results We have largely maintained our earnings estimates for the sector. However, we have upgraded our earnings estimates for Ashok Leyland as company continues to surprise on market share front. On the other hand, we have marginally downgraded our volume estimate for Maruti due to weaker than expected export volumes in recent months. For most of the other stocks, whilst we have not changed earnings estimates, the roll forward of the target price date to October 2015 results in around 2-3% valuation upgrades.

Ambit vs consensus Based on the limited consensus data for 2QFY16, our earnings estimates are ahead of consensus for most of the stocks except Bajaj Auto, Hero MotoCorp, Tata Motors, Exide Industries and Balkrishna Industries (where our estimates are below consensus estimates). Our FY16 EPS estimates are ahead of consensus estimates for most of the stocks except Hero MotoCorp, Tata Motors and BKT.

Recommendation We highlight Ashok Leyland as our top BUY idea in the sector. AL faces a strong business outlook due to the MHCV demand revival (24% CAGR over FY15-17) and consequent benefits of operating leverage and improved sales realisation (EBITDA margin to improve to 11.0% in FY16 and 11.2% in FY17 vs 7.6% in FY15).

Stock Performance

(%) 3-month

Absolute Rel to Sensex

Ashok Leyland 28 32

Bajaj Auto (6) (2)

Hero MotoCorp (1) 3

Maruti Suzuki 10 14

Tata Motors (21) (17)

Eicher Motor (7) (3)

Exide Inds Ltd 6 10

Balkrishna Ind. (7) (3)

Mahindra CIE 9 13

Sep’15E Qtrly EPS

(Rs) Ambit Consensus

Ashok Leyland 1.1 0.6

Bajaj Auto 31.3 32.8

Hero MotoCorp 35.1 39.0

Maruti Suzuki 41.5 39.5

Tata Motors 7.4 8.0

Eicher Motor 98.4 84.7

TVS Motor 2.3 2.1

Exide Industries 1.7 1.7

Mahindra CIE 2.1 2.0

Balkrishna Ind. 11.4 13.6

FY16E EPS

(Rs) Ambit Consensus

Ashok Leyland 4.04 3.33

Bajaj Auto 131 130

Hero MotoCorp 150 153

Maruti Suzuki 182 180

Tata Motors 44.0 44.8

Eicher Motors 545 501

TVS Motor 10.6 10.2

Exide Industries 7.56 7.46

Mahindra CIE 10.8 10.1

Balkrishna Ind. 50.6 57.1

Source: Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 9

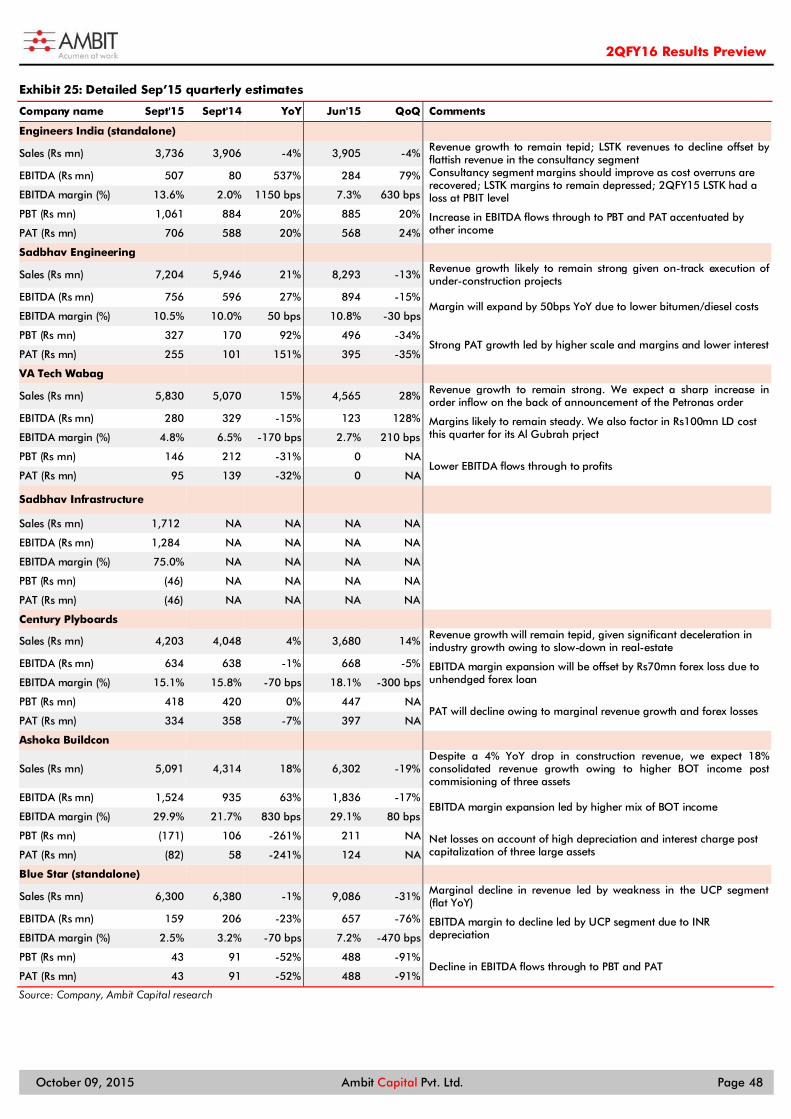

Exhibit 4: Detailed Sep'15E quarterly estimates

Company Sep'15E Sep'14 Jun‘15 YoY QoQ Comments

Ashok Leyland

Sales (Rs mn) 53,274 32,177 38,412 66% 39% Volumes (ex-Dost) have increased by 64% YoY and 39% QoQ (including Dost, volumes up 47% YoY and 32% QoQ). Price hikes to further help YoY revenue growth.

EBITDA (Rs mn) 5,990 2,344 3,887 156% 54% Operating leverage benefits from higher volumes and benign raw material prices to drive margin strong expansion. EBITDA margin (%) 11.2% 7.3% 10.1% 396bps 113bps

PBT (Rs mn) 4,480 563 2,349 696% 91% EBITDA margin improvement and moderating interest costs to significantly lift the bottom-line. PAT (Rs mn) 3,226 117 1,593 2653% 102%

Bajaj Auto

Sales (Rs mn) 59,734 59,933 56,559 0% 6% While volumes have been flat YoY, 4% volume growth to drive the QoQ revenue growth

EBITDA (Rs mn) 12,664 12,244 11,821 3% 7% Lower commodity prices and better export realisations (due to INR depreciation relative to US$) to drive margin improvement EBITDA margin (%) 21.2% 20.4% 20.9% 77bps 30bps

PBT (Rs mn) 12,938 12,391 14,980 4% -14% YoY EBITDA trend to reflect at the net earnings level. QoQ earnings impacted by higher other income base in 1QFY16. PAT (Rs mn) 9,057 8,530 10,148 6% -11%

Hero MotoCorp

Sales (Rs mn) 67,001 69,153 69,553 -3% -4% 7% YoY and 4% QoQ decline in volumes lead to de-growth in revenues

EBITDA (Rs mn) 9,764 9,348 10,479 4% -7% EBITDA margin to witness YoY improvement on the back of lower commodity prices EBITDA margin (%) 14.6% 13.5% 15.1% 105bps (49)bps

PBT (Rs mn) 9,729 10,484 10,463 -7% -7% YoY net earnings trend impacted by high ‘other income’ base of 3QFY15 PAT (Rs mn) 7,005 7,634 7,503 -8% -7%

Maruti Suzuki

Sales (Rs mn) 139,565 123,038 134,249 13% 4% Revenue growth led by 10% YoY and 4% QoQ increase in volumes.

EBITDA (Rs mn) 22,470 15,208 21,891 48% 3% Improvement in YoY margin largely driven by favourable currency movement (Yen depreciation vs INR) and operating leverage benefits from higher volumes EBITDA margin (%) 16.1% 12.4% 16.3% 374bps (21)bps

PBT (Rs mn) 17,404 10,805 16,705 61% 4% YoY EBITDA trend to reflect at the net earnings level

PAT (Rs mn) 12,531 8,625 11,929 45% 5%

Tata Motors

Sales (Rs mn) 593,401 605,642 610,195 -2% -3% Muted JLR volumes to impact YoY and QoQ revenue trends

EBITDA (Rs mn) 79,833 95,666 91,088 -17% -12% JLR's margin to witness YoY and QoQ decline on the back of unfavourable geographical mix (lower volume share from China) and weaker product mix EBITDA margin (%) 13.5% 15.8% 14.9% (234)bps (147)bps

PBT (Rs mn) 31,709 56,444 44,754 -44% -29% Net earnings to be further impacted by higher depreciation and tax rates PAT (Rs mn) 23,782 32,805 29,052 -28% -18%

Eicher Motor

Sales (Rs mn) 32,086 22,750 29,167 41% 10% We expect strong volume growth in Eicher’s commercial vehicle and Royal Enfield business to drive robust revenue growth.

EBITDA (Rs mn) 5,097 3,053 4,316 67% 18% Consolidated EBITDA margin uplift driven by strong YoY margin improvement (205bps) at Royal Enfield and commercial vehicle business (142bps). EBITDA margin (%) 15.9% 13.4% 14.8% 247bps 109bps

PBT (Rs mn) 4,394 2,672 3,573 64% 23% Net earnings performance to mirror the EBITDA level performance.

PAT (Rs mn) 2,667 1,650 2,218 62% 20%

TVS Motor

Sales (Rs mn) 27,972 26,831 26,212 4% 7% Despite flat YoY volumes, improvement in realisations (due to higher share of motorcycles/scooters) to drive revenue growth

EBITDA (Rs mn) 1,876 1,627 1,637 15% 15% Margins to improve due to higher volumes/capacity utilisation

EBITDA margin (%) 6.7% 6.1% 6.2% 64bps 46bps

PBT (Rs mn) 1,446 1,313 1,180 10% 23% Net earnings performance to mirror the EBITDA level performance.

PAT (Rs mn) 1,085 948 902 14% 20%

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 10

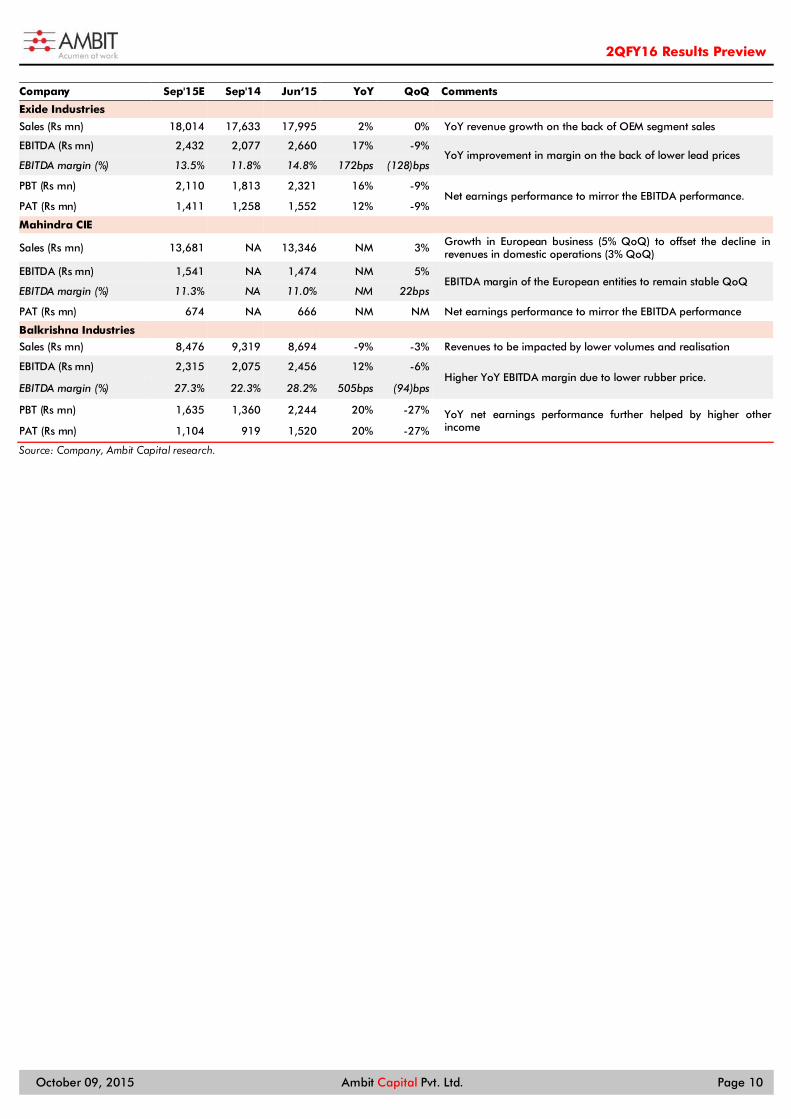

Company Sep'15E Sep'14 Jun‘15 YoY QoQ Comments

Exide Industries

Sales (Rs mn) 18,014 17,633 17,995 2% 0% YoY revenue growth on the back of OEM segment sales

EBITDA (Rs mn) 2,432 2,077 2,660 17% -9% YoY improvement in margin on the back of lower lead prices

EBITDA margin (%) 13.5% 11.8% 14.8% 172bps (128)bps

PBT (Rs mn) 2,110 1,813 2,321 16% -9% Net earnings performance to mirror the EBITDA performance.

PAT (Rs mn) 1,411 1,258 1,552 12% -9%

Mahindra CIE

Sales (Rs mn) 13,681 NA 13,346 NM 3% Growth in European business (5% QoQ) to offset the decline in revenues in domestic operations (3% QoQ)

EBITDA (Rs mn) 1,541 NA 1,474 NM 5% EBITDA margin of the European entities to remain stable QoQ

EBITDA margin (%) 11.3% NA 11.0% NM 22bps

PAT (Rs mn) 674 NA 666 NM NM Net earnings performance to mirror the EBITDA performance

Balkrishna Industries

Sales (Rs mn) 8,476 9,319 8,694 -9% -3% Revenues to be impacted by lower volumes and realisation

EBITDA (Rs mn) 2,315 2,075 2,456 12% -6% Higher YoY EBITDA margin due to lower rubber price.

EBITDA margin (%) 27.3% 22.3% 28.2% 505bps (94)bps

PBT (Rs mn) 1,635 1,360 2,244 20% -27% YoY net earnings performance further helped by higher other income PAT (Rs mn) 1,104 919 1,520 20% -27%

Source: Company, Ambit Capital research.

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 11

Exhibit 5: Revisions ahead of earnings season

New Estimates Old Estimates Change

Comments FY16E FY17E FY16E FY17E FY16E FY17E

Bajaj Auto

Recommendation SELL SELL

Whilst we maintain our earnings estimates, upgrades to valuation is driven by roll-forward of DCF target date to October 1, 2016 (vs July 2016 earlier)

TP (Rs) 2,410 2,350 3%

Revenues (Rs mn) 247,928 278,539 247,928 278,539 0% 0%

EBITDA (Rs mn) 52,051 58,478 52,051 58,478 0% 0%

EBITDA margin (%) 21.0% 21.0% 21.0% 21.0% - -

PBT (Rs mn) 54,000 61,279 54,000 61,279 0% 0%

PAT (Rs mn) 37,800 42,895 37,800 42,895 0% 0%

EPS (Rs) 131 148 131 148 0% 0%

Ashok Leyland

Recommendation BUY BUY

We have upgraded the volumes to account for better than expected volume trends in the recent months. This drives revenue, margin and valuation upgrades for Ashok Leyland.

TP (Rs) 105 99 7%

Revenues (Rs mn) 191,003 230,909 185,594 227,867 3% 1%

EBITDA (Rs mn) 20,953 25,943 19,593 25,178 7% 3%

EBITDA margin (%) 11.0% 11.2% 10.6% 11.0% 41 19

PBT (Rs mn) 15,339 20,698 11,608 16,954 32% 22%

PAT (Rs mn) 11,504 15,524 10,484 14,950 10% 4%

EPS (Rs) 4.04 5.45 3.68 5.25 10% 4%

Maruti Suzuki

Recommendation BUY BUY We have marginally downgraded the export volumes for Maruti based on recent monthly trends which has led to revenue and EBITDA downgrades. We have also marginally increased the tax rates. Despite the 3-4% downgrades to earnings estimates, TP remains unchanged due to roll-forward of DCF TP to October 1, 2016 and higher tax rates adequately built in our long term estimates (FY18 onwards).

TP (Rs) 4,750 4,750 0%

Revenues (Rs mn) 584,498 670,231 588,007 674,569 -1% -1%

EBITDA (Rs mn) 93,461 110,588 94,022 111,304 -1% -1%

EBITDA margin (%) 16.0% 16.5% 16.0% 16.5% 0 0

PBT (Rs mn) 74,188 93,028 74,796 93,902 -1% -1%

PAT (Rs mn) 54,899 68,841 56,845 71,365 -3% -4%

EPS (Rs) 182 228 188 236 -3% -4%

TVS Motor

Recommendation SELL SELL

Whilst we maintain our earnings estimates, upgrades to valuation is driven by roll-forward of DCF target date to October 1, 2016 (vs August 2016 earlier)

TP (Rs) 245 240 2%

Revenues (Rs mn) 115,682 135,527 115,682 135,527 0% 0%

EBITDA (Rs mn) 8,246 11,278 8,246 11,278 0% 0%

EBITDA margin (%) 7.1% 8.3% 7.1% 8.3% - -

PBT (Rs mn) 6,733 9,865 6,733 9,865 0% 0%

PAT (Rs mn) 5,050 7,399 5,050 7,399 0% 0%

EPS (Rs) 10.6 15.6 10.6 15.6 0% 0%

Hero MotoCorp

Recommendation SELL SELL

Whilst we maintain our earnings estimates, upgrades to valuation is driven by roll-forward of DCF target date to October 1, 2016 (vs July 2016 earlier)

TP (Rs) 2,500 2,425 3%

Revenues (Rs mn) 293,768 331,291 293,768 331,291 0% 0%

EBITDA (Rs mn) 41,123 46,376 41,123 46,376 0% 0%

EBITDA margin (%) 14.0% 14.0% 14.0% 14.0% - -

PBT (Rs mn) 41,677 46,744 41,677 46,744 0% 0%

PAT (Rs mn) 30,008 33,422 30,008 33,422 0% 0%

EPS (Rs) 150 167 150 167 0% 0%

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 12

New Estimates Old Estimates Change

Comments FY16E FY17E FY16E FY17E FY16E FY17E

Eicher Motors

Recommendation SELL SELL

Whilst we maintain our earnings estimates, upgrades to valuation is driven by roll-forward of DCF target date to October 1, 2016 (vs July 2016 earlier)

TP (Rs) 16,500 15,800 4%

Revenues (Rs mn) 167,034 175,827 167,034 175,827 0% 0%

EBITDA (Rs mn) 25,985 29,101 25,985 29,101 0% 0%

EBITDA margin (%) 15.6% 16.6% 15.6% 16.6% - -

PBT (Rs mn) 23,811 27,359 23,811 27,359 0% 0%

PAT (Rs mn) 14,827 16,696 14,827 16,696 0% 0%

EPS (Rs) 545 613 545 613 0% 0%

Source: Company, Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 13

Agri Inputs/Chemicals Agri input players are likely to have a muted quarter driven by weak demand in the domestic and exports markets. On the domestic side, weak monsoons (14% below normal) have put pressure on agrochemical offtake. Globally too, weak weather patterns and low commodity prices have impacted overall demand. We continue to expect PI and SRF to outperform their peers led by their competitive strengths in specialty chemicals exports. In domestic agrochem, we expect PI to perform well vs peers, delivering 12% revenue growth; Rallis will continue underperforming, with flat sales in the domestic and international business. We expect margin expansion for PI, SRF, and Rallis, driving earnings growth of 22%, 53% and 2% respectively. We will watch out for the growth outlook and balance sheet management amidst a weaker operating environment in the quarterly management commentary. North resilient but south and west India on a weak footing Our channel checks across India suggest a cocktail of problems: (a) poor rains and weaker profitability impacting farmer sentiments; (b) weak infestation of insects and other plant diseases due to an unfavourable climate (humidity and sporadic rains); (c) drop in pricing on some fast-selling technicals (Acephate, Cypermethrin, Chloropyriphos, Prophenophos, Imidacloropid, Fipronil, and Dichlorophos) due to drop in global demand/weakened crude prices, leading to MTM losses on inventory; and (d) heightened aggression amongst generic players amidst a weak monsoon. Players with a higher share of novelty products/branded products are able to combat such pressures to a certain extent. North has done better than south and west Our agri channel checks seem to suggest that north India has relatively performed better partly driven by good irrigation facilities; however, the upcoming Rabi season will face pressure from lower reservoir levels. North India in particular was infested with white flies which helped products such as Ulala (from UPL). Mancozeb (one of the big generic molecules for UPL) has seen a sharp jump in realisations, combating the trend seen in generics. Of late, the incidence of BPH (brown plant hopper) insects in rice has been high, leading to better agrochemical offtake (favourable for Osheen – an insecticide from PI). Weak demand in west India (Gujarat, Maharashtra), Madhya Pradesh and integrated Andhra Pradesh (Telangana and Seemandhra) was led by pressure on farmer profitability. Commodity pricing (soybean and cotton) was weak and farmer sentiments to invest were also poor given the lower rainfall. Players focused on generics have also faced the ire of falling technical prices. International business facing challenges from weak environment International business offtake for generic exporters, such as Rallis and Insecticides India, has been weak amidst a cocktail of weakening currencies, lower commodity prices and crash in technical prices. Agrochem demand for Maize and Soybean has declined given weaker maize/soybean demand, as lower crude prices have reduced ethanol requirements for blending. We see some impact from these issues on PI (CSM business) and SRF (Fluorospecialty chemicals). However, on an absolute basis, we still expect them to deliver 20-25% YoY revenue growth. Balance sheet issues likely to be crucial The third continued bad season (Kharif 2014, Rabi 2014-15 and Kharif 2015) is also likely to put pressure on companies with higher receivable days. Our channel checks suggest much lower secondary offtake than primary sales. As a result, we see pressure from both inventory and receivables. Sales growth needs to be seen in conjunction with WC deterioration for agrochem companies. Amongst prominent agrochem companies, Insecticides India and Dhanuka Agritech have the longest working capital cycles and they may be impacted the most. Rallis too had been relaxing its working capital norms, which needs to be watched out for.

Stock Performance

(%) 3-month

Absolute Rel to Sensex

PI Industries -3 1

Rallis India -13 -8

SRF Ltd -6 -1

Sep’15E Qtrly EPS

(Rs) Ambit Consensus

PI Industries 4.3 4.3

Rallis India 4.15 8.1

SRF Ltd 20.5 DNA

FY16E EPS

(Rs) Ambit Consensus

PI Industries 21.8 22.0

Rallis India 9.2 9.5

SRF Ltd 79.6 76.9

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 14

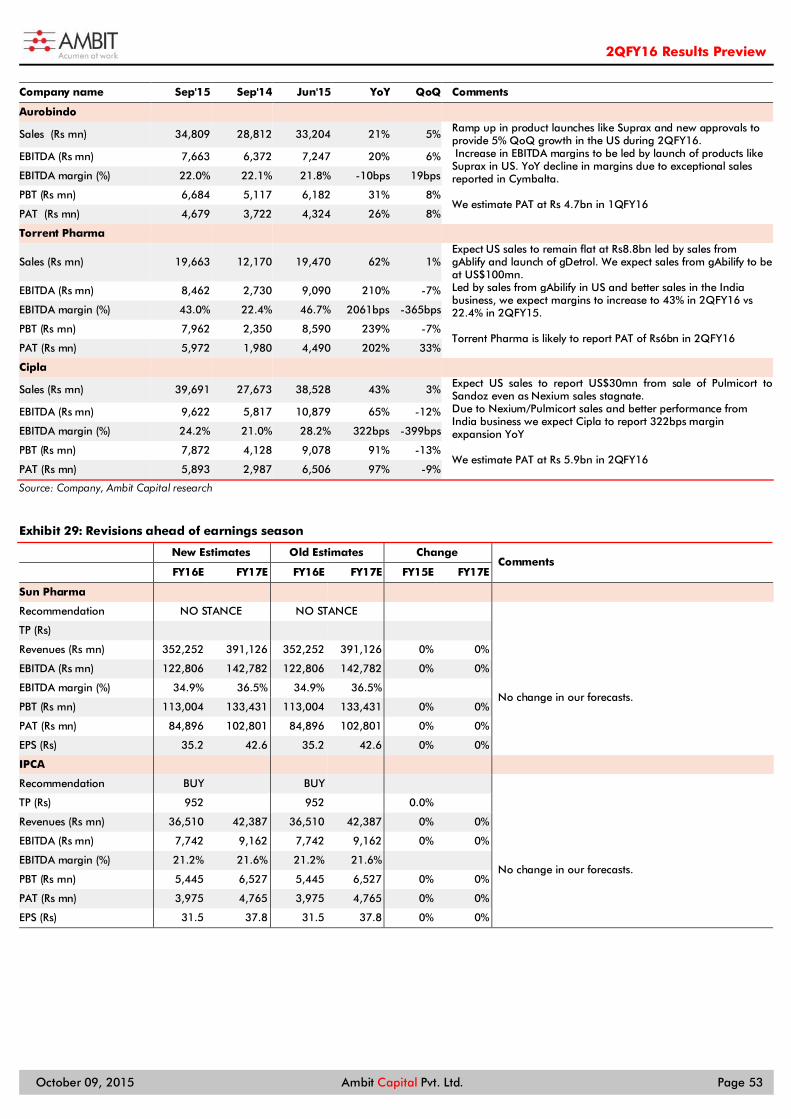

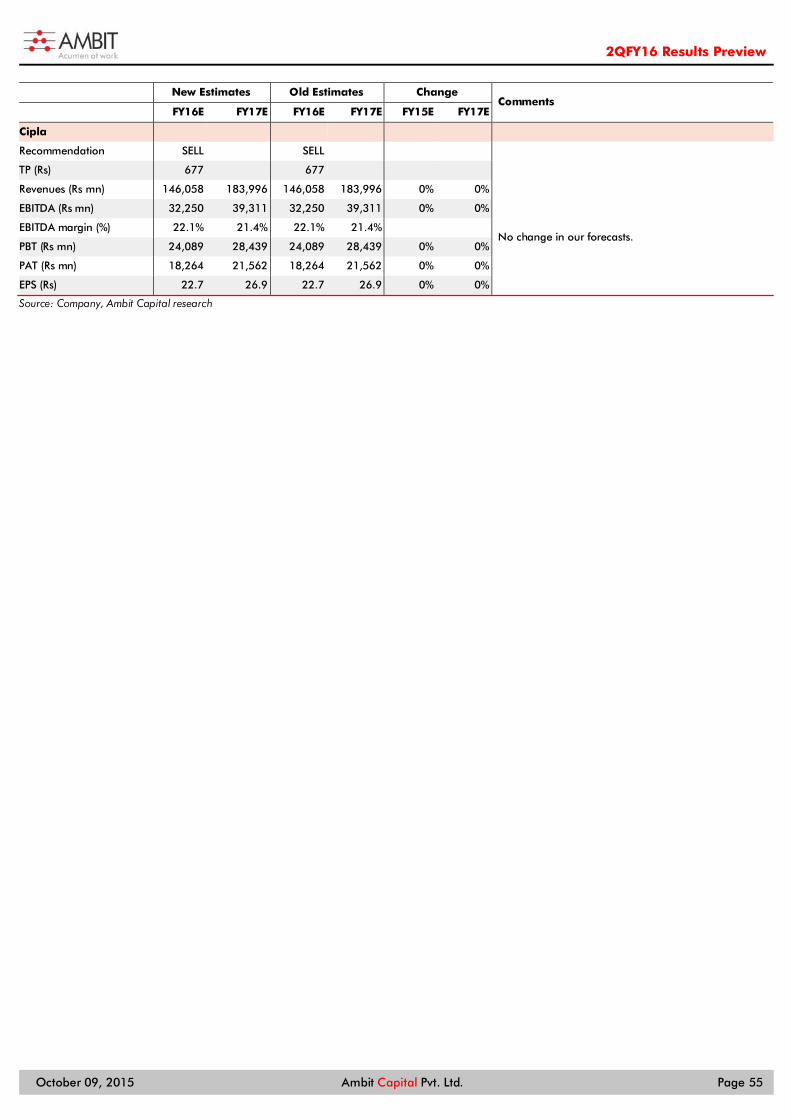

PI – CSM growth likely to sustain; domestic business to remain steady We expect PI to report robust growth of 17% led by 22% growth in the CSM business and 12% growth in the domestic business. CSM business growth would be led by continued execution of high order book of US$600mn (3.2x last 12 month revenues) and marginal benefit from a softer base in the corresponding quarter in the previous year. Domestic business growth is likely to be ~12% driven by good growth in Nominee Gold and good traction on Keefun. We expect a ~200bps expansion in EBITDA margins primarily led by: (a) higher share of CSM business and (b) operating leverage due to higher revenue base. PI’s management has historically maintained that it is able to pass on any impact of RM/forex fluctuations to clients. SRF – Chemicals and packaging to drive healthy earnings growth We expect SRF to deliver 17% topline growth primarily led by 25% growth in chemicals and 10% growth each in the technical textiles and packaging films business. We expect growth in chemicals to be led by higher exports in R134a, better realisations for R22, and 25% growth in the specialty chemicals business. We expect EBITDA margin expansion of 260bps led by: (a) positive mix impact from the higher-margin chemicals business and (b) improving profitability of technical textiles and packaging films business. Rallis – Expect a weak quarter We expect Rallis to report flat sales growth in both the domestic and exports agrochem business. Our channel checks continue to suggest negative impact on the generic segment through: (a) significant price erosion for most generic technical (b) aggressive trade margins and credit period by relatively unorganised players and topline focused players. Such players have been very aggressive with their product placements, sales incentives, dealer credits, product packaging etc., which could create pressure on sales of the erstwhile leaders such as Rallis. On exports, challenges in Europe and Latin America are pretty evident. The drought situation in Australia is also grave. On Metahelix we build in 25% growth for 2Q, leading to overall consolidated sales growth of ~2%. We believe 100bps of margin expansion (led by lower technical prices) which would drive EBITDA growth of 8%. Growth looks high primarily because of a softer base. We expect PAT growth of 2% due to higher depreciation charges and lower tax rates in base quarter. Other non-covered players Dhanuka would likely report flat sales growth along with some compression in overall margins due to weaker demand for soybean herbicides. Insecticides India would pressure on both domestic and exports due to lower technical prices and lower demand offtake. UPL will benefit from good performance of Ulala and realisation jump in Mancozeb. Monsanto India will continue to witness pressure from lower glyphosate demand and weaker demand for high-priced corn seed products. Kaveri will also see decline in sales due to poor outlook for cotton and corn. Margins for Kaveri will be impacted due to royalty issues. PI Industries – BUY; SRF – BUY; Rallis – SELL We continue to hold on to our conviction on PI to deliver 30% EPS CAGR over FY15-17E. Our belief of 26% FY15-17E CSM growth (vs the management’s conservative guidance of 20%) is premised on the following: (a) healthy order book growth of 38% YoY in 1QFY16 to US$600mn (3.2x last 12-month revenues), (b) on-track commissioning of two plants in Jambusar, for which capacities are tied up, and (c) improvement in farmer sentiments globally post a difficult CY14/CY15. In the domestic business, we are building in FY15-17E revenue CAGR of 15% (vs 21% CAGR over FY10-15) driven by the base portfolio and continued strength in new launches. We are also building in 150bps of margin expansion over FY15-FY17E, with mix improvement and operating efficiencies. We retain our BUY stance with a TP of Rs800, implying 26x FY17E multiples.

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 15

SRF is set to benefit from three positive catalysts—(a) Refrigerants business is witnessing better realisations in R22 (led by volume cuts as per Montreal protocol) and export-led volume uptick in R134a; (b)improving profitability in packaging/technical textiles due to improving realisations/efficiencies; and (c) incremental revenues from new plant additions in the specialty chemicals business. Change in estimates We cut our EPS estimates for PI by 4%/6% for FY16/17. Despite rolling forward, our TP reduces to Rs800 from Rs825, implying an earnings multiple of 26xFY17 EPS. We downgrade SRF revenue growth marginally by 1% for FY16 and FY17. Our TP of Rs1,500 does not change as we roll forward our earnings estimates, implying 15x FY17E earnings. We roll forward our earnings for Rallis and our new target price or Rs180 implies 17x FY17E EPS.

Key things to watch out for: (a) Commentary for domestic agrochemicals growth in FY16; (b) channel inventory and receivable levels; (c) export situation given slowdown in agri businesses.

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 16

Exhibit 6: Detailed Sept’15 quarterly estimates

Rs mn Sep'15 Sep'14 Jun''15 YoY QoQ Comments

Rallis India

Standalone (Rs mn) 5,784 5,784 2,440 0% 137% We expect standalone business growth to remain flat driven by similar growth rates in domestic and international business.

Metahelix (Rs mn) 720 576 2,209 25% -67% We expect Metahelix to continue doing well, with 25% YoY growth during the quarter

Sales (Rs mn) 6,563 6,419 4,683 2% 40% We expect overall sales growth of 2% primarily led by Metahelix.

EBITDA (Rs mn) 1,315 1,219 565 8% 133%

EBITDA Margin 20.0% 19.0% 12.1% 104bps 797bps

On margins, we expect some improvement driven by lower technical prices supporting standalone margins. We do not build in much improvement in Metahelix margins

PBT (Rs mn) 1,133 1,075 (28) 5% -4162%

PAT (Rs mn) 747 734 331 2% 126% PAT growth is muted at 2% due to poor sales growth

PI Industries

Domestic (Rs mn) 2,426 2,166 2,717 12% -11% We expect domestic business growth of 12%

CSM (Rs mn) 2,561 2,099 2,825 22% -9% On the CSM business, we believe strong growth rates to continue leading to 22% growth in CSM for FY16

Sales (Rs mn) 4,998 4,266 5,548 17% -10% We expect sales growth to be good led by strong performance in both domestic and exports business

EBITDA (Rs mn) 955 726 1,358 31% -30%

EBITDA Margin 19% 17% 24% 207 bps -538 bps We expect margins to improve driven by higher share of high-margin CSM business and operating leverage

PBT (Rs mn) 891 717 1,302 24% -32%

PAT (Rs mn) 597 490 873 22% -32% PAT growth of 22% driven by strong sales growth and steady margin expansion

SRF Ltd.

Technical Textiles Business 4,781 4,346 4,042 10% 18%

Chemicals & Polymers Business 3,995 3,196 3,798 25% 5% We expect the chemicals business to grow @25% due to a larger base effect.

Packaging Films 1,939 1,762 1,851 10% 5%

Sales (Rs mn) 10,714 9,169 9,522 17% 13%

EBITDA (Rs mn) 2,463 1,869 2,293 32% 7% We expect the overall EBITDA margin to improve as operating leverage kicks in and the packaging films improving realisations

EBITDA margin (%) 23.0% 20.4% 24.1% 261 bps -109 bps Increase in EBITDA margins due to improvement in realisations of Packaging films and operating leverage in the Chemicals segment.

PBT (Rs mn) 1,679 1,092 1,653 54% 2%

Adjusted PAT (Rs mn) 1,175 769 1,211 53% -3% We expect the PAT to grow around 53% on a YoY basis due to a low base effect

Source: Company, Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 17

Exhibit 7: Revisions ahead of earnings season

New Estimates Old Estimates Change

Comments FY16E FY17E FY16E FY17E FY16E FY17E

PI Industries Recommendation BUY BUY TP (Rs) 800 825 -3% We have brought down our domestic

business growth estimates from 18% earlier to 12%. Accordingly our margins are also adjusted by 40-80bps for FY16/FY17 driven by lower operating leverage. Our TP is revised to Rs 800 vs Rs 825 earlier due to ~5% cut in earnings

Revenues (Rs mn) 22,639 28,405 23,506 29,384 -4% -3%

EBITDA (Rs mn) 4,433 5,964 4,691 6,399 -6% -7%

EBITDA margin (%) 20% 21% 20% 22% -38 bps -78 bps

PBT (Rs mn) 4113 5629 4,291 5,981 -4% -6%

PAT (Rs mn) 2,961 4,165 3,090 4,426 -4% -6%

EPS (Rs) 22 31 23 33 -4% -6%

SRF Recommendation BUY BUY TP (Rs) 1,500 1,500 0%

We have brought down our specialty chemicals growth estimates from 30% to 25% for FY16. Our TP remains the same due to roll forward.

Revenues (Rs mn) 49,979 55,467 50,278 55,871 -1% -1%

EBITDA (Rs mn) 10,380 12,183 10,457 12,296 -1% -1%

EBITDA margin (%) 21% 22% 21% 22% -3 bps -4 bps

PBT (Rs mn) 6,350 8,081 6,428 8,194 -1% -1%

PAT (Rs mn) 4,572 5,737 4,628 5,817 -1% -1%

EPS (Rs) 80 100 81 101 -1% -1%

Rallis Recommendation SELL SELL TP (Rs) 180 170 6%

Our target price is upgraded by 6% due to earnings roll forward

Revenues (Rs mn) 20,352 22,981 20,374 23,007 0% 0%

EBITDA (Rs mn) 3,122 3,573 3,119 3,569 0% 0%

EBITDA margin (%) 15.3% 15.5% 15.3% 15.5% -3 bps -4 bps

PBT (Rs mn) 2,532 2,948 2,551 2,967 -1% -1%

PAT (Rs mn) 1,823 2,123 1,802 2,094 1% 1%

EPS (Rs) 9.2 10.7 9.3 10.8 -1% -1%

Source: Company, Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 18

Banking The 2QFY16 results for the banking sector are likely to remain muted, with slowing balance sheet growth, NIM pressure and elevated credit costs. Credit growth would stay muted (~9-10% for the entire banking system), as corporate loan demand has failed to improve. Low growth is resulting in intensifying competition on pricing amongst banks to sustain market share, which coupled with base rate cuts during the quarter would lead to NIM compression. Credit costs would remain higher, as slippages from restructured assets to NPAs plus fresh NPAs addtions remain elevated. Overall, we estimate net profit growth of 8% YoY (vs 2% decline in 1QFY16) for banks in our coverage universe during the quarter, with private sector banks growing profits at 14% YoY. Our top picks are Axis Bank and IndusInd Bank. We are negative on most PSU banks, as we believe elevated credit costs and weak operating performance would keep their financial performance subdued.

Credit growth stays muted: RBI data shows muted system-level loan growth of ~9.6% as at end-September 2015. Corporate credit growth has been muted due to weak demand, corporates opting for bond market, wherever possible, and asset quality stress faced by banks for such loans. PSU banks would grow slower than the system and new private sector banks on average should grow at ~18%. Overall, we expect loan growth of 9% during the quarter for banks under our coverage.

NIMs to come under pressure: Full impact of base rate cuts in 1QFY16, further base rate cuts in 2QFY16 and slow loan growth pressuring yields will lead to margin pressure for banks across the board, except for a few. Overall, for banks under our coverage, we do not expect any revival in income growth and we build in NII growth of ~7% YoY, slowing from 9-11% NII growth seen in the last three quarters.

Asset quality stress unlikely to ease: Credit costs would remain higher, as a combined impact of fresh formation of NPAs, restructured loans slipping to NPAs and incremental provisions on aging NPAs. PSU banks with large restructured books and low provision coverage are at a particular disadvantage.

Treasury gains to cushion the earnings: With bond yields easing by ~35bps during the quarter, banks are likely to partly utilise treasury gains in 2Q to offset profitability pressure, the way they did in FY15. With bond yields falling by ~90-120bps during FY15, treasury gains had contributed to 15% of banks’ PBT during FY15 (FY14: 5%).

Cost lever pushed to the hilt: Amidst a weak income growth environment, banks, particularly private sector banks, have tightly controlled their operating expenses. Whilst this is likely to continue, further improvement appears difficult and resumption in growth would increasingly become critical to support earnings growth. The cost-to-income ratio for new private sector banks, having improved from 46% in FY12 to 42% in FY15, is expected to be at 44% in 2QFY16 vs 45% in 2QFY15.

Preparing for the upcoming results We highlight trends in slippage from the pool of restructured loans to NPLs, NIMs and loan mix trends for various set of banks as key variables to monitor during the quarter.

Ambit vs consensus Whilst our earnings estimates for the quarter are ~5% lower than consensus estimates, our earnings estimates for FY16 and FY17 are ~5-10% below consensus. The divergence is predominantly driven by weaker loan book growth forecasts, NIM pressure and our higher slippage assumptions and weaker upgrades/recovery forecasts.

Stock Performance

(%) 3-month

Absolute Rel to Sensex

HDFC Bank 1 4

ICICI Bank (9) (6)

Axis Bank (15) (12)

Kotak Mahindra Bk. (8) (5)

IndusInd Bk. 6 9

State Bk. of India (9) (6)

Bank of Baroda 23 26

Punjab National Bk. (2) 1

Bank of India (19) (16)

Union Bk. of India 15 18

Federal Bank (14) (11)

Karur Vysya Bk. (8) (5)

City Union Bank (11) (8)

South Indian Bk. (7) (4)

FY16E EPS

(Rs) Ambit Consensus

HDFC Bank 48.2 50.1

ICICI Bank 20.6 21.7

Axis Bank 34.1 36.7

Kotak Mahindra Bk. 22.1 21.2

IndusInd Bk. 38.9 41.1

State Bk. of India 17.7 21.3

Bank of Baroda 21.4 20.3

Punjab National Bk. 20.1 20.6

Bank of India 16.8 25.7

Union Bk. of India 34.1 33.8

Federal Bank 5.5 6.1

Karur Vysya Bk. 42.4 45.0

City Union Bank 7.3 7.7

South Indian Bk. 3.2 3.0

Sept'15E Quarterly PAT

(Rs mn) Ambit Consensus

HDFC Bank 29,339 27,316

ICICI Bank 28,637 29,168

Axis Bank 19,381 19,438

Kotak Mahindra Bk. 6,159 5,844

IndusInd Bk. 5,350 5,127

State Bk. of India 31,331 34,087

Bank of Baroda 9,652 9,000

Punjab National Bk. 9,360 8,671

Bank of India 3,008 3,568

Union Bk. of India 5,688 4,959

Federal Bank 2,327 2,406

Karur Vysya Bk. 1,226 1,216

City Union Bank 1,035 1,056

South Indian Bk. 812 843

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 19

Recommendation

Consolidated net profit for banks in our coverage universe is likely to grow by 8% YoY, compared to a decline of 2% in 1QFY16. Consolidated RoAs are likely to be ~0.92% (down 4bps YoY, up 7bps QoQ). New private sector banks are likely to deliver an average RoA of 1.7% vs PSU banks’ ~0.5%. We are BUYers of Axis Bank (AXSB IN, US$18.0bn, TP `690, 40% upside) and IndusInd Bank (IIB IN, US$8.6bn, TP `1,075, 14% upside). We are SELLers on most PSU banks, as we believe the elevated credit costs and weak operating performance would keep financial performance subdued. We are SELLers on HDFC Bank (HDFCB IN, US$41.9bn, TP `1,045, 3% downside) and Kotak Mahindra Bank (KMB IN, US$18.4bn, TP `515, 21% downside) due to their expensive valuations and the market’s lofty earnings expectations, which these companies would find difficult to meet.

Exhibit 8: Detailed Sept'15E quarterly estimates

Sep'15 Sep'14 Jun'15 YoY QoQ Comment

HDFC Bank

Net Interest Income (Rs mn) 67,663 55,110 63,888 23% 6%

Growth in PAT is in line with growth in assets

Operating Profit (Rs mn) 51,101 40,602 48,499 26% 5%

Cost to income (%) 44.8% 46.3% 45.2% PBT (Rs mn) 44,386 36,043 41,219 23% 8%

PAT (Rs mn) 29,339 23,815 26,957 23% 9%

ICICI Bank

Net Interest Income (Rs mn) 52,801 46,566 51,151 13% 3%

Higher provisions to result in muted net profit growth

Operating Profit (Rs mn) 52,596 46,979 50,378 12% 4%

Cost to income (%) 36.2% 36.5% 37.8% PBT (Rs mn) 40,910 38,484 40,824 6% 0%

PAT (Rs mn) 28,637 27,090 29,762 6% -4%

Axis Bank

Net Interest Income (Rs mn) 42,179 35,249 40,562 20% 4%

We expect PAT growth of 20% in-line with loans growth. Credit costs to be broadly unchanged at 122bps.

Operating Profit (Rs mn) 37,928 31,623 40,921 20% -7%

Cost to income (%) 40.0% 42.2% 35.6% PBT (Rs mn) 29,144 24,373 29,703 20% -2%

PAT (Rs mn) 19,381 16,107 19,784 20% -2%

Kotak Mahindra Bank

Net Interest Income (Rs mn) 17,467 10,389 15,982 68% 9%

YoY earnings growth is entirely driven by kicker from acquisition of ING Vysya Bank. On a pro-forma basis (KMB+ING), earnings would be down 1% YoY due to pressure on fee income and credit cost.

Operating Profit (Rs mn) 11,146 7,336 5,970 52% 87%

Cost to income (%) 52.9% 51.3% 72.7% PBT (Rs mn) 9,332 6,800 2,917 37% 220%

PAT (Rs mn) - standalone 6,159 4,445 1,898 39% 225%

IndusInd Bank

Net Interest Income (Rs mn) 10,304 8,331 9,807 24% 5%

Stronger operating profit growth (30% YoY) to support PAT growth of 24% YoY.

Operating Profit (Rs mn) 9,434 7,247 9,227 30% 2%

Cost to income (%) 46.4% 47.9% 45.9% PBT (Rs mn) 8,046 6,515 7,994 24% 1%

PAT (Rs mn) 5,350 4,302 5,250 24% 2%

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 20

Sep'15 Sep'14 Jun'15 YoY QoQ Comment

State Bank of India

Net Interest Income (Rs mn) 136,614 132,746 137,320 3% -1%

Expect muted NIM and elevated credit cost.

Operating Profit (Rs mn) 89,942 84,219 92,021 7% -2%

Cost to income (%) 53.2% 52.8% 51.1% PBT (Rs mn) 44,758 41,469 52,024 8% -14%

PAT (Rs mn) 31,331 31,004 36,924 1% -15%

Bank of Baroda

Net Interest Income (Rs mn) 32,861 34,011 34,596 -3% -5%

Elevated credit cost to limit RoAs at 0.55%

Operating Profit (Rs mn) 21,302 24,029 22,020 -11% -3%

Cost to income (%) 50.9% 45.3% 50.3% PBT (Rs mn) 13,594 15,149 16,022 -10% -15%

PAT (Rs mn) 9,652 11,042 10,522 -13% -8%

Punjab National Bank

Net Interest Income (Rs mn) 40,272 42,542 41,765 -5% -4%

Muted loan growth (7% YoY), NIM compression and elevated credit costs to lead to RoAs of 0.6%.

Operating Profit (Rs mn) 29,591 28,760 31,321 3% -6%

Cost to income (%) 44.9% 49.6% 43.1% PBT (Rs mn) 14,076 11,081 13,207 27% 7%

PAT (Rs mn) 9,360 5,753 7,207 63% 30%

Bank of India

Net Interest Income (Rs mn) 29,167 30,307 29,127 -4% 0%

Muted loan growth (1% YoY) and elevated provision, including unamortised provisions sitting on balance sheet, to lead to RoAs of just 0.2 %.

Operating Profit (Rs mn) 17,759 21,355 17,042 -17% 4%

Cost to income (%) 53.9% 47.1% 54.6% PBT (Rs mn) 3,760 11,721 1,895 -68% 98%

PAT (Rs mn) 3,008 7,860 1,297 -62% 132%

Union Bank of India

Net Interest Income (Rs mn) 22,233 20,844 21,302 7% 4%

Muted loan growth (6% YoY), NIM compression and elevated credit costs to lead to RoAs of 0.6%.

Operating Profit (Rs mn) 15,728 13,339 14,882 18% 6%

Cost to income (%) 48.7% 53.9% 48.9% PBT (Rs mn) 8,553 5,485 8,458 56% 1%

PAT (Rs mn) 5,688 3,713 5,188 53% 10%

Federal Bank

Net Interest Income (Rs mn) 6,694 6,058 6,048 10% 11%

Expect muted operating profit (up 2% YoY) and eleavted credit costs .

Operating Profit (Rs mn) 4,321 4,098 3,672 5% 18%

Cost to income (%) 50.9% 48.9% 54.0% PBT (Rs mn) 3,526 3,641 2,141 -3% 65%

PAT (Rs mn) 2,327 2,403 1,414 -3% 65%

Karur Vysya Bank

Net Interest Income (Rs mn) 4,283 3,374 4,231 27% 1%

We expect some recovery in margins but muted loan growth and elevated credit costs to keep RoAs subdued at 0.9%.

Operating Profit (Rs mn) 2,979 2,071 2,957 44% 1%

Cost to income (%) 48.7% 56.2% 49.5% PBT (Rs mn) 1,844 1,140 1,781 62% 4%

PAT (Rs mn) 1,226 905 1,346 35% -9%

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 21

Sep'15 Sep'14 Jun'15 YoY QoQ Comment

City Union Bank

Net Interest Income (Rs mn) 2,294 2,062 2,236 11% 3%

Loan growth is likely to remain muted but superior margins to protect profitability at ~1.5%.

Operating Profit (Rs mn) 1,953 1,728 1,972 13% -1%

Cost to income (%) 39.8% 41.7% 40.0% PBT (Rs mn) 1,380 1,182 1,521 17% -9%

PAT (Rs mn) 1,035 937 1,116 10% -7%

South Indian Bank

Net Interest Income (Rs mn) 3,524 3,584 3,403 -2% 4%

Elevated cost to income ratio and provisions to lead to muted RoAs of 0.5%.

Operating Profit (Rs mn) 1,954 2,110 1,809 -7% 8%

Cost to income (%) 57.7% 53.3% 59.3% PBT (Rs mn) 1,194 1,152 1,014 4% 18%

PAT (Rs mn) 812 763 653 6% 24%

Source: Company, Ambit Capital research

Exhibit 9: Revisions ahead of earnings season

New Estimates Old Estimates Change

Comments FY16E FY17E FY16E FY17E FY16E FY17E

HDFC Bank Recommendation SELL SELL

TP (Rs) 1,045 990 Net interest income (Rs mn) 262,996 308,716 262,996 308,716 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 204,818 246,875 204,818 246,875 0% 0%

Cost to income (%) 44.0% 42.8% 44.0% 42.8% PBT (Rs mn) 181,664 217,873 181,664 217,873 0% 0%

PAT (Rs mn) 120,807 144,885 120,807 144,885 0% 0%

EPS (Rs) 48.2 57.8 48.2 57.8 0% 0%

ICICI Bank Recommendation SELL SELL TP (Rs) 290 280 Net interest income (Rs mn) 214,717 249,218 214,717 249,218 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 218,103 253,743 218,103 253,743 0% 0%

Cost to income (%) 37.2% 37.2% 37.2% 37.2% PBT (Rs mn) 169,886 192,505 169,886 192,505 0% 0%

PAT (Rs mn) 119,260 135,139 119,260 135,139 0% 0%

EPS (Rs) 20.6 23.3 20.6 23.3 0% 0%

Axis Bank Recommendation BUY BUY

TP (Rs) 690 665 Net interest income (Rs mn) 169,622 198,037 169,622 198,037 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 150,217 176,102 150,217 176,102 0% 0%

Cost to income (%) 41.6% 41.6% 41.6% 41.6% PBT (Rs mn) 119,757 147,963 119,757 147,963 0% 0%

PAT (Rs mn) 80,836 99,875 80,836 99,875 0% 0%

EPS (Rs) 34.1 42.1 34.1 42.1 0% 0%

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 22

New Estimates Old Estimates Change

Comments FY16E FY17E FY16E FY17E FY16E FY17E

Kotak Mahindra Bank Recommendation SELL SELL TP (Rs) 515 498 Net interest income (Rs mn) 73,581 85,385 73,581 85,385 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 48,416 56,678 48,416 56,678 0% 0%

Cost to income (%) 54.5% 54.4% 54.5% 54.4% PBT (Rs mn) 39,101 49,102 39,101 49,102 0% 0%

PAT (Rs mn) - standalone 26,589 33,389 26,589 33,389 0% 0%

PAT (Rs mn) - consolidated 44,530 52,635 43,602 51,600 2% 2%

EPS (Rs) - consolidated 48.9 57.8 47.9 56.6 2% 2%

IndusInd Bank Recommendation BUY BUY TP (Rs) 1075 1,030 Net interest income (Rs mn) 43,353 55,371 43,483 55,485 0% 0%

Incorporating the impact of the just completed QIP

Operating profit (Rs mn) 39,919 51,239 39,726 51,150 0% 0%

Cost to income (%) 45.7% 44.8% 46.0% 45.0% PBT (Rs mn) 34,183 44,522 34,062 44,527 0% 0%

PAT (Rs mn) 22,903 29,830 22,822 29,833 0% 0%

EPS (Rs) 38.9 50.6 38.7 50.6 0% 0%

State Bank of India Recommendation SELL SELL TP (Rs) 235 235 Net interest income (Rs mn) 576,591 640,601 576,591 640,601 0% 0%

Our 28 September note on SBI covered the change in estimate and valuation

Operating profit (Rs mn) 410,559 470,769 410,559 470,769 0% 0%

Cost to income (%) 50.2% 49.1% 50.2% 49.1% PBT (Rs mn) 194,383 238,128 194,383 238,128 0% 0%

PAT (Rs mn) 132,180 161,927 132,180 161,927 0% 0%

EPS (Rs) 17.7 21.7 17.7 21.7 0% 0%

Bank of Baroda Recommendation BUY BUY TP (Rs) 215 210 Net interest income (Rs mn) 148,956 167,326 148,026 168,204 1% -1%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 106,605 120,519 105,675 121,397 1% -1%

Cost to income (%) 44.9% 45.1% 45.1% 44.9% PBT (Rs mn) 64,991 76,810 64,060 77,068 1% 0%

PAT (Rs mn) 47,443 56,071 46,764 56,259 1% 0%

EPS (Rs) 21.4 25.3 21.1 25.4 1% 0%

Punjab National Bank Recommendation SELL SELL TP (Rs) 140 138 Net interest income (Rs mn) 188,224 216,719 185,759 215,118 1% 1%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 132,943 155,564 130,479 153,962 2% 1%

Cost to income (%) 44.7% 43.3% 45.2% 43.6% PBT (Rs mn) 53,896 68,304 51,432 66,702 5% 2%

PAT (Rs mn) 37,188 47,130 35,488 46,025 5% 2%

EPS (Rs) 20.1 25.4 19.1 24.8 5% 2%

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 23

New Estimates Old Estimates Change

Comments FY16E FY17E FY16E FY17E FY16E FY17E

Bank of India Recommendation SELL SELL TP (Rs) 150 145 Net interest income (Rs mn) 124,601 133,006 124,299 133,476 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 80,540 80,967 80,238 81,437 0% -1%

Cost to income (%) 51.6% 54.7% 51.7% 54.5% PBT (Rs mn) 13,530 25,966 13,228 26,436 2% -2%

PAT (Rs mn) 10,824 20,773 10,582 21,149 2% -2%

EPS (Rs) 16.8 31.2 16.5 31.8 2% -2%

Union Bank of India Recommendation SELL SELL TP (Rs) 150 147 Net interest income (Rs mn) 95,361 109,554 95,362 109,555 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 67,774 76,858 67,775 76,858 0% 0%

Cost to income (%) 49.0% 49.0% 49.0% 49.0% PBT (Rs mn) 32,289 41,109 32,290 41,110 0% 0%

PAT (Rs mn) 21,472 27,338 21,473 27,338 0% 0%

EPS (Rs) 34.1 43.0 34.1 43.0 0% 0%

Federal Bank Recommendation SELL SELL TP (Rs) 70 68 Net interest income (Rs mn) 26,819 31,473 26,819 31,473 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 17,734 20,967 17,734 20,967 0% 0%

Cost to income (%) 50.7% 49.7% 50.7% 49.7% PBT (Rs mn) 14,296 17,848 14,296 17,848 0% 0%

PAT (Rs mn) 9,436 11,780 9,436 11,780 0% 0%

EPS (Rs) 5.5 6.9 5.5 6.9 0% 0%

Karur Vysya Bank Recommendation SELL SELL TP (Rs) 430 415 Net interest income (Rs mn) 16,718 18,116 16,718 18,116 0% 0%

Roll forward leads to a minor upgrade in our target price.

Operating profit (Rs mn) 11,396 12,350 11,396 12,350 0% 0%

Cost to income (%) 51.2% 52.2% 51.2% 52.2% PBT (Rs mn) 6,876 7,856 6,876 7,856 0% 0%

PAT (Rs mn) 5,157 5,892 5,157 5,892 0% 0%

EPS (Rs) 42.4 48.4 42.4 48.4 0% 0%

City Union Bank Recommendation BUY BUY TP (Rs) 115 115 Net interest income (Rs mn) 9,186 10,660 9,186 10,660 0% 0%

No change in estimates and valuation.

Operating profit (Rs mn) 7,845 9,012 7,822 8,983 0% 0%

Cost to income (%) 42.8% 43.1% 42.9% 43.2% PBT (Rs mn) 5,598 6,696 5,575 6,667 0% 0%

PAT (Rs mn) 4,366 5,223 4,348 5,200 0% 0%

EPS (Rs) 7.3 8.8 7.3 8.7 0% 0%

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 24

New Estimates Old Estimates Change

Comments FY16E FY17E FY16E FY17E FY16E FY17E

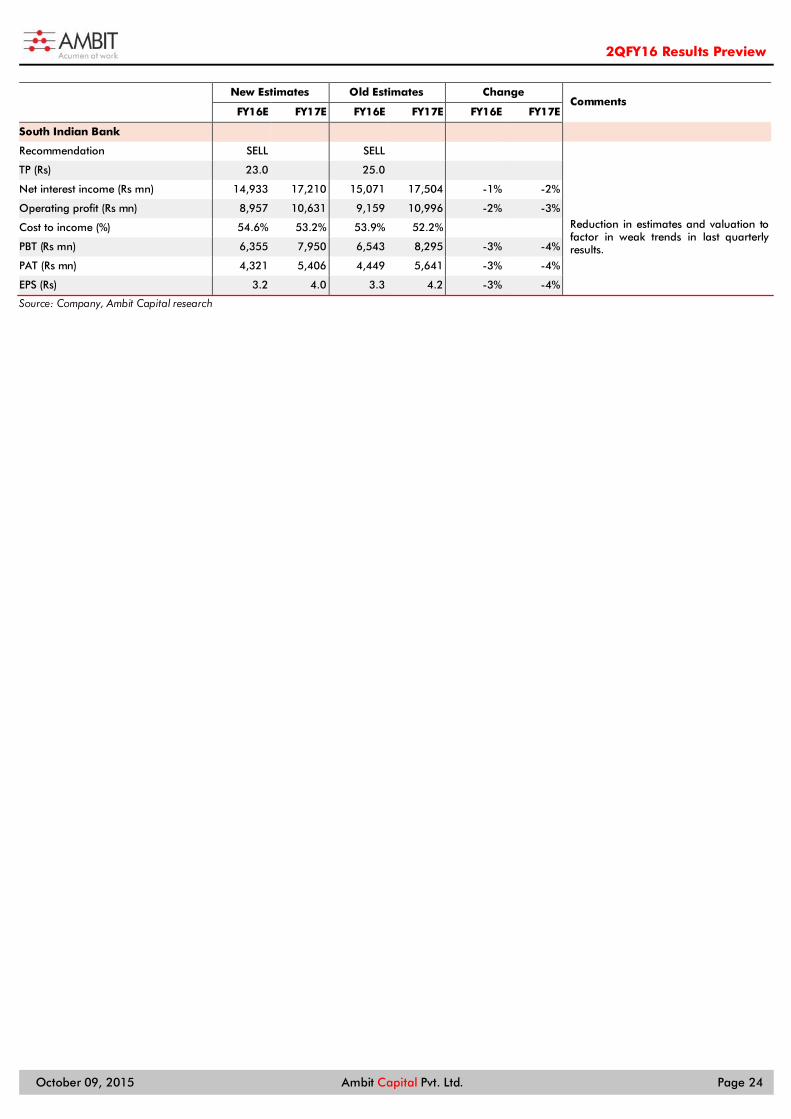

South Indian Bank Recommendation SELL SELL TP (Rs) 23.0 25.0 Net interest income (Rs mn) 14,933 17,210 15,071 17,504 -1% -2%

Reduction in estimates and valuation to factor in weak trends in last quarterly results.

Operating profit (Rs mn) 8,957 10,631 9,159 10,996 -2% -3%

Cost to income (%) 54.6% 53.2% 53.9% 52.2% PBT (Rs mn) 6,355 7,950 6,543 8,295 -3% -4%

PAT (Rs mn) 4,321 5,406 4,449 5,641 -3% -4%

EPS (Rs) 3.2 4.0 3.3 4.2 -3% -4%

Source: Company, Ambit Capital research

2QFY16 Results Preview

October 09, 2015 Ambit Capital Pvt. Ltd. Page 25

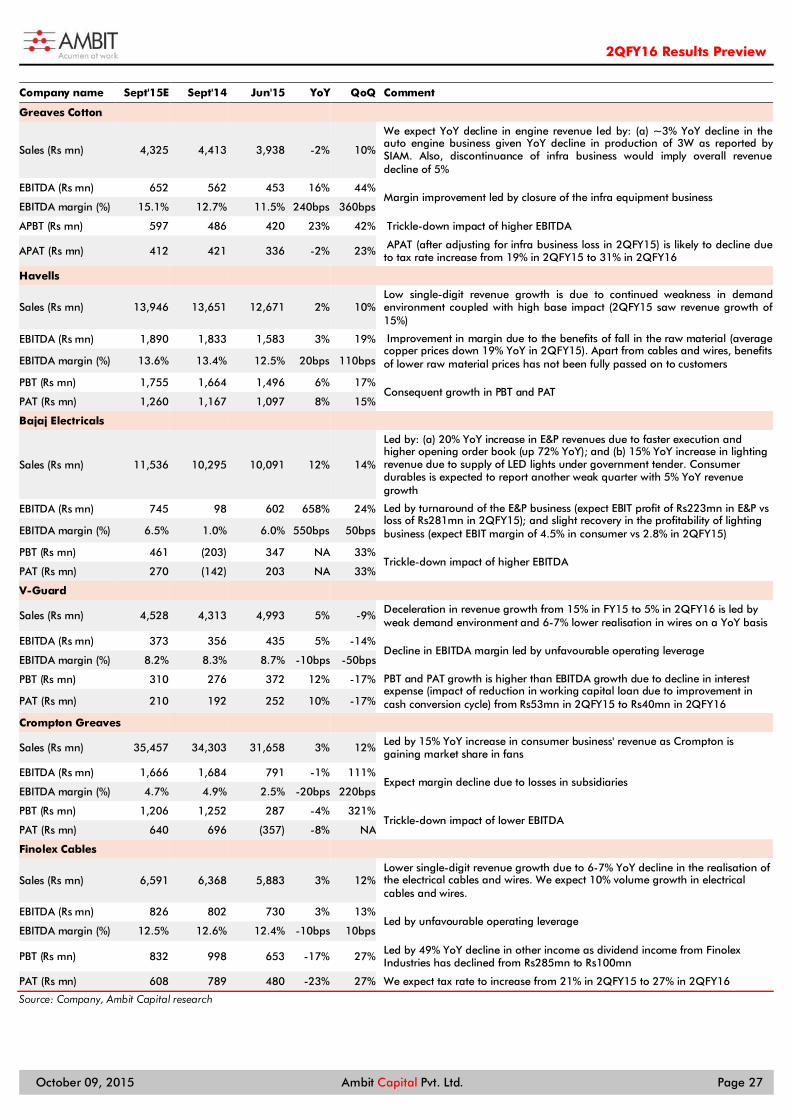

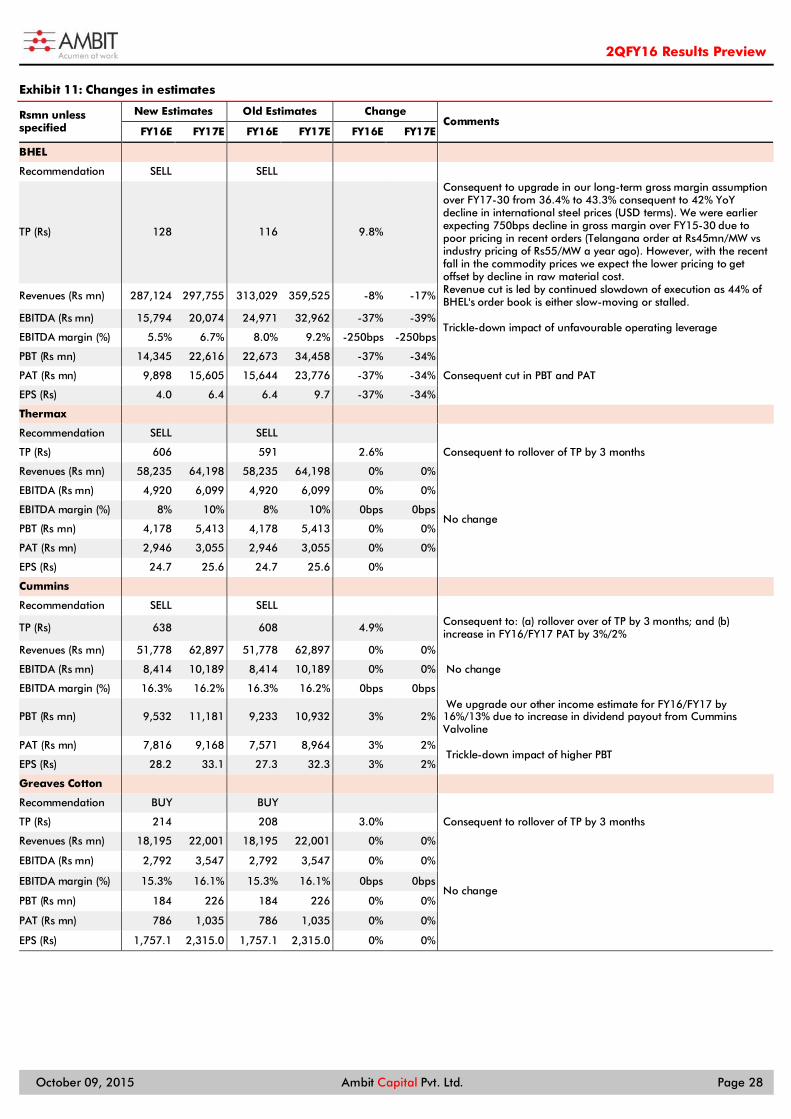

Capital Goods Demand across various sub-sectors in 2QFY16 is likely to be weak (except for Inox Wind) given industrial capex deceleration and weak order execution due to liquidity challenges. However, companies under our coverage would report higher profitability growth (vs their revenue growth) led by softening of raw material prices. BHEL and Inox Wind are likely to report the strongest PAT growth of 81% and 76% YoY. Cummins (KKC) is likely to report PAT growth of 5% YoY due to higher growth in exports, and Greaves (GRV) is likely to report a PAT decline of 2% YoY (despite 16% EBITDA growth) due to higher tax rate. We expect PAT growth of 8% and 10% for Havells and V-Guard respectively due to expansion in gross margins. We expect Bajaj Electricals (BJE) to turn into black led by the turnaround of the E&P business. Thermax, Finolex Cables (Finolex) and Crompton (CRG) may report YoY decline in profits. Our top BUYs are V-Guard and GRV and our top SELL is BJE.