Results Presentation Q1 2014 - Talanx/media/Files/T/Talanx/reports-and-presentations/... · German...

42

Herbert K. Haas, CEO Dr. Immo Querner, CFO Results Presentation Q1 2014 15 May 2014

-

Upload

duongthuan -

Category

Documents

-

view

215 -

download

0

Transcript of Results Presentation Q1 2014 - Talanx/media/Files/T/Talanx/reports-and-presentations/... · German...

Herbert K. Haas, CEO Dr. Immo Querner, CFO

Results Presentation Q1 2014 15 May 2014

Results Presentation Q1 2014, 15 May 20142

Agenda

Group HighlightsI

Investments / CapitalIII

SegmentsII

Essentials Risk Management Reports 2013IV

OutlookV

Appendix

Mid-term Target Matrix

Q1 2014 Additional Information

Risk Management Reports 2013

Results Presentation Q1 2014, 15 May 20143

Q1 2014 – On track to reach FY2014 targets I

Talanx had a good start into FY2014. When adjusting for the SwissLife effect of €22m (after tax) in Q1 2013, the Net Income of €192m even exceeds last year’s level

GWP marginally lower (-0.5% vs. Q1 2013) mainly due to currency effects (+1.6% currency-adj.), the decline in traditional German life business and more selective Reinsurance underwriting

Moderate large loss burden does not boost Q1 2014 results - treatment of unused large loss budget in Primary Insurance in correspondence with established Reinsurance practice

End of March 2014, shareholders’ equity stood at €7,538m (FY2013: €7,214m), or €29.82 per share. Solvency I ratio at 220% (FY2013: 210%)

Talanx confirms its FY2014 target to achieve Net Income of at least €700m

Results Presentation Q1 2014, 15 May 20144

Summary of Q1 2014

Good results, even when compared to the strong Q1 2 013 figures

€m, IFRS Q1 2014 Q1 2013 ChangeGross written premium 8,414 8,458 (1) %Net premium earned 5,599 5,715 (2) %

Net underwriting result (415) (249) n/m

Net investment income 1,010 875 +15 %Operating result (EBIT) 509 530 (4) %Net income after minorities 192 208 (7) %

Key ratios Q1 2014 Q1 2013 ChangeCombined ratio non-lifeinsurance and reinsurance

95.8% 95.0% 0.8%pts

Return on investment 4.3% 3.7% 0.6%pts

Balance sheet Q1 2014 FY 2013 ChangeInvestments underown management

88,069 86,310 +2 %

Goodwill 1,103 1,105 (0) %

Total assets 136,760 132,863 +3 %

Technical provisions 95,127 91,697 +4 %

Total shareholders' equity 11,741 11,211 +5 %

Shareholders' equity 7,538 7,214 +4 %

I

Comments

� Slight decline in gross written premium, mainly due to currency effects (currency-adj. GWP: +1.6%), the decline in traditional German life business and more selective Reinsurance underwriting

� Combined ratio rises by only 0.8%pts to 95.8%, predominantly due to a lower run-off result in Retail Germany

� Realisation of capital gains, in Retail Germany to finance Zinszusatzreserve (ZZR). ~40% of the anticipated ZZR charge for FY2014 (€~272m in German local GAAP, HGB) already digested in Q1 2014

� Q1 2014 net income (€192m) even exceeds the strong Q1 2013 level, when adjusting for the base effect of €22m from last year’s partial disposal of Talanx’s SwissLife stake

� Shareholders’ equity up to €7,538m, or €29.82 per share. Solvency I ratio up to 220% (FY2013: 210%)2013 numbers in this presentation adjusted on the basis of IAS8

Q1 2014 results – Key financials

Results Presentation Q1 2014, 15 May 2014

13.413.40.0

5

I

� Large loss burden of €41m in Q1 2014 higher than in Q1 2013 (€13m), but still at a moderate level

� Net burden of man-made large losses of €10m in Primary and €31m in Reinsurance

� No large losses from Nat Cat

� Treatment of unused large loss budget in Primary Insurance in correspondence with established Reinsurance practice

Large losses1 in Q1 2014

1 definition „large loss“: in excess of €10m gross

(€m) Primary insurance Reinsurance Talanx Group

Total Nat Cat 0.0 0.0 0.0

Aviation 1.9 30.6 32.5

Total man-made large losses

10.2 30.6 40.8

Property 8.3 0.0 8.3

Total large losses 10.2 30.6 40.8

Impact on Combined Ratio (incurred) 0.8%pts 1.9%pts 1.4%pts

Total large losses (Q1 2013)

Results Presentation Q1 2014, 15 May 20146

Combined ratios

Development of net combined ratio 1 Combined ratio by segment/selected carrier

Q1 2014 combined ratios remain well below 100% in m ost lines and units

I

Q1 2014 Q1 2013 FY2013

Industrial Lines 98.6% 99.4% 101.3%

Retail Germany 100.2% 95.0% 102.4%

Retail International 95.1% 94.1% 95.8%

HDI Seguros S.A., Brazil 97.5% 95.7% 96.7%

HDI Seguros S.A., Mexico4 90.2% 80.1% 90.6%

TUiR Warta S.A., Poland2 95.1% 93.7% 94.3%

TU Europa S.A., Poland3 79.0% 68.8% 87.0%

HDI Sigorta A.Ş., Turkey 104.4% 106.5% 105.9%

HDI Assicurazioni S.p.A., Italy 94.5% 99.4% 98.8%

Non-Life Reinsurance 94.5% 94.0% 94.9%Expense ratio Loss ratio

1 incl. net interest income on funds withheld and contract deposits2 Warta acquisition closed on 1 July 2012; numbers incl. HDI Asekuracia TU S.A. (legal merger on 28 Dec 2012)3 TU Europa acquisition closed on 1 June 20124 numbers incl. Metropolitana

Q1 Q2 Q3 Q4 Q1

2013 2014

95.0

68.8

26.3

97.0

70.5

26.6

100.6

75.0

25.7

95.1

68.4

26.8

95.8

69.2

26.7

Results Presentation Q1 2014, 15 May 20147

GWP trend

GWP development (€bn)

� Seasonal pattern remains intact

� In Q1 2014, GWP virtually flat vs. Q1 2013

� Negative currency effects (GWP currency-adj:+1.6%), the decline in traditional German life business and a more selective Reinsurance underwriting curb GWP growth

Q1 2014 top-line virtually flat vs. previous year

I

Industrial Lines

Non-Life Reinsurance

Retail Germany

Life/Health Reinsurance

Retail International

Corporate Functions and Consolidation

2012 2013

8.5

Q1 Q2 Q3 Q4 Q1

2013 2014

6.5 6.46.8

8.4

1.6

1.6 1.51.6

1.5

2.2

1.9 1.91.9

2.1

1.1

1.1 1.01.1

1.2

2.1

1.5 1.6 1.8

2.0

1.70.7 0.7 0.7

1.8

(0.2) (0.2) (0.2) (0.2) (0.2)

Results Presentation Q1 2014, 15 May 20148

Agenda

Group HighlightsI

Investments / CapitalIII

SegmentsII

Essentials Risk Management Reports 2013IV

OutlookV

Appendix

Mid-term Target Matrix

Q1 2014 Additional Information

Risk Management Reports 2013

Results Presentation Q1 2014, 15 May 2014

83% 98% 59% 80%80%

9

P&L for Industrial Lines Comments

II

High level of residual large loss budget – EBIT benef its from higher investment result

� GWP grew 1.6% in Q1 2014 (currency-adj.:+2.2%), increase mainly from international business

� On track to reach self-retention level of ~50% in FY2014. Q1 2014 retention level affected by transfer of business to Talanx Re and typical quarterly time shift in reinsurance accounting

� Slight improvement in Q1 2014 combined ratio although unused large loss budget has not improved the technical result

� Increase in investment income and positive forexcontribution lead to higher EBIT result

� Higher tax rate of 40.5% (Q1 2013: 34.7%) resulting from tax surcharge on large corporatesin France

Segments – Industrial Lines

€m, IFRS Q1 2014 Q1 2013 Change

Gross written premium 1,763 1,735 +2%

Net premium earned 407 439 (7%)

Net underwriting result 6 2 +205%

Net investment income 72 55 +30%

Operating result (EBIT) 60 33 +84%

Group net income 35 19 +81%

Return on investment (annualised) 4.2% 3.2% +1.0%pts

Combined ratio*

Expense ratio Loss ratio

FY2013: 101%

99% 103%116%

85%99%

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 201419% 20% 18% 26% 19%

*incl. net interest income on funds withheld and contract deposits

Results Presentation Q1 2014, 15 May 2014

36% 35% 29% 41% 34%

59% 69% 76% 64% 67%

FY2013: 102%

10

II

CommentsP&L for Retail Germany

Q1 2014 compares to strong Q1 2013 with positive bas e effect from one-time reserve releases

� GWP decline by 4% due to reduction in traditional German life business and focus on profitability in motor. Premiums in liability and property lines increased

� Increase in combined ratio from lower (one-time) run-off results than in Q1 2013. On adjusted level, Q1 2014 EBIT would improve by €4m vs. Q1 2013

� Realisation of capital gains to finance ZZR (€126m) leads to ROI of 4.7% (Q1 2013: 3.8%); neutral on EBIT level

� ~40% of anticipated 2014 ZZR allocation already digested (forecast of ~€272m for FY2014; FY 2013: €313m; both according to HGB). Total ZZR stock expected to rise close to €1bn until year-end 2014

� Higher tax rate (Q1 2014: 38.6% vs. Q1 2013: 29.7%) due to loss making start-up of Talanx Re’s Retail Germany-related cell

Segments – Retail Germany

€m, IFRS Q1 2014 Q1 2013 ChangeGross written premium 2,027 2,113 (4%)

Of which Life 1,219 1,277 (5%)Of which Non-Life 808 835 (3%)

Net premium earned 1,287 1,323 (3%)Net underwriting result (430) (296) n/m

Of which Life (430) (313) n/mOf which Non-Life (0) 18 (100%)

Net investment income 501 387 +29%Operating result (EBIT) 54 66 (18%)Group net income 29 43 (32%)

Return on investment (annualised) 4.7% 3.8% +0.9%pts

Combined ratio*

Expense ratio Loss ratio*incl. net interest income on funds withheld and contract deposits

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014

95%104% 105% 105% 100%

Results Presentation Q1 2014, 15 May 2014

29% 30% 32% 30%

67% 67% 67% 64% 65%

27%

11

II

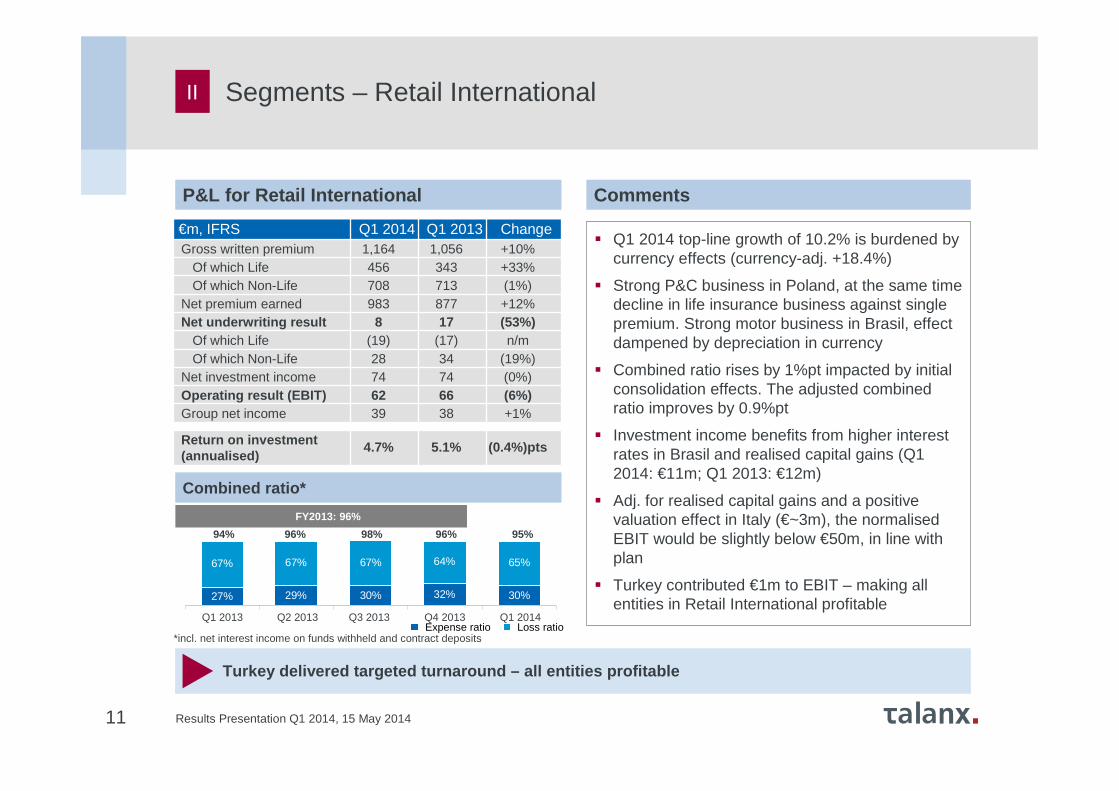

P&L for Retail International Comments

Turkey delivered targeted turnaround – all entities profitable

� Q1 2014 top-line growth of 10.2% is burdened by currency effects (currency-adj. +18.4%)

� Strong P&C business in Poland, at the same time decline in life insurance business against single premium. Strong motor business in Brasil, effect dampened by depreciation in currency

� Combined ratio rises by 1%pt impacted by initial consolidation effects. The adjusted combined ratio improves by 0.9%pt

� Investment income benefits from higher interest rates in Brasil and realised capital gains (Q1 2014: €11m; Q1 2013: €12m)

� Adj. for realised capital gains and a positive valuation effect in Italy (€~3m), the normalisedEBIT would be slightly below €50m, in line with plan

� Turkey contributed €1m to EBIT – making all entities in Retail International profitable

Segments – Retail International

Combined ratio*

€m, IFRS Q1 2014 Q1 2013 ChangeGross written premium 1,164 1,056 +10%

Of which Life 456 343 +33%Of which Non-Life 708 713 (1%)

Net premium earned 983 877 +12%Net underwriting result 8 17 (53%)

Of which Life (19) (17) n/mOf which Non-Life 28 34 (19%)

Net investment income 74 74 (0%)Operating result (EBIT) 62 66 (6%)Group net income 39 38 +1%

Return on investment (annualised)

4.7% 5.1% (0.4%)pts

*incl. net interest income on funds withheld and contract depositsExpense ratio Loss ratio

FY2013: 96%

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014

94% 96% 98% 96% 95%

Results Presentation Q1 2014, 15 May 2014

26% 26% 25% 23% 26%

68% 68% 72% 72% 69%

FY2013: 95%

12

Segments – Non-Life Reinsurance

Underwriting and investment income contributed posi tively

II

P&L for Non-Life Reinsurance Comments

� Q1 2014 GWP down by 4.1% (currency-adj.: -1.7%) on the back of active cycle management in a competitive market, e.g. reduced premium income from Nat Cat business

� Only one major loss (€31m) - well below Q1 2014 budget of €156m

� Investment income benefits from increased level of realisations mainly in connection with bond redemption and the change of balance sheet currency of the Bermudian entities

� Limited impact from inflation swaps (Q1 2014: €-1m; Q1 2013: €-2m)

� EBIT margin2 of 17.5% (Q1 2013: 15.7%) is well above target

€m, IFRS Q1 2014 Q1 2013 Change

Gross written premium 2,108 2,198 (4%)

Net premium earned 1,632 1,692 (4%)

Net underwriting result 86 98 (12%)

Net investment income 211 195 +9%

Operating result (EBIT) 286 266 +8%

Group net income 96 79 +22%

Return on investment (annualised)

3.3% 3.0% +0.3%pts

Combined ratio 1

1 incl. net interest income on funds withheld and contract deposits 2 EBIT margins reflect a Talanx Group viewExpense ratio Loss ratio

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014

94% 94% 97% 95% 95%

Results Presentation Q1 2014, 15 May 201413

Segments – Life/Health Reinsurance

Heading for a normalised result in FY2014

II

P&L for Life/Health Reinsurance Comments

� GWP declined by 2.8% in Q1 2014 (currency-adjusted: +0.7%); growth was further driven by China and longevity business, offset by reduced premium income from two large financing treaties

� Technical result slightly below expectations

� Net investment income at expected level

� EBIT margin1 of 5.0% slightly below Q1 2013 (7.3%) as financial solutions and longevity business ahead of plan, compensated by weaker margin in mortality and morbidity business

� ModCo contribution to net investment income of €2m in Q1 2014 vs. €6m in Q1 2013EBIT (€m)

€m, IFRS Q1 2014 Q1 2013 Change

Gross written premium 1,517 1,560 (3%)

Net premium earned 1,281 1,389 (8%)

Net underwriting result (87) (68) n/m

Net investment income 152 162 (6%)

Operating result (EBIT) 64 101 (37%)

Group net income 21 37 (43%)

Return on investment (annualised)

4.1% 4.3% (0.2%)pts

1 EBIT margin reflects a Talanx Group view

101

2934

-25

64

Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014

Results Presentation Q1 2014, 15 May 201414

Agenda

Group HighlightsI

Investments / CapitalIII

SegmentsII

Essentials Risk Management Reports 2013IV

OutlookV

Appendix

Mid-term Target Matrix

Q1 2014 Additional Information

Risk Management Reports 2013

Results Presentation Q1 2014, 15 May 201415

Fixed-income-portfolio split Comments

� Investment portfolio remains strongly dominated by fixed-income securities (Q1 2014: 90% portfolio share)

� 80% (Q1 2013: 83%) of fixed-income portfolio invested in A or higher-rated bonds

� 16% of “investments under own management” are held in USD, 27% overall in non-euro currencies

� Moderate increase in GIIPS sovereign exposure to 1.7% of total assets (FY2013:1.2%)

� Investments under own management up by +1.7% y/yand +2.0% vs. 31 Dec. 2013

� Share of equity investments remains at around 1%

Asset allocation as of 31 March 2014

Investments – Breakdown of investment portfolioIII

Conservative investment style remains broadly uncha nged

Breakdown by rating

Breakdown by type

Total: €88.1bn Total: €79.5bn

90%

9%

Other

Equities

Fixed income securities

1%

Other

Covered bonds

Corporate bonds

Government bonds

2%

28%

31%

21%

20%

BBB and below

A

AA

AAA

29%

32%

37%

Results Presentation Q1 2014, 15 May 201416

III

Investment yield up to 4.3% (Q1 2013: 3.7%)

Net investment income Talanx Group Comments

� “Ordinary investment income” in line with Q1 2013 level

� On the back of the increase in asset base, the “current investment income from interest” has also slightly increased compared to Q1 2013

� Higher realised net gains on investments due to:

� Retail Germany’s ambition to finance a major part of this year’s assumed ZZR charge early in the year,

� the selective de-risking in Industrial Lines,

� the change of balance sheet currency of the Bermudian entities in Non-Life Re

� Contribution from unrealised results in reinsurance derivatives vs. Q1 2013: delta inModCo €-4m and inflation swaps €+1m

� Return on investment of 4.3% (Q1 2013: 3.7%)

Net investment income

€m, IFRS Q1 2014 Q1 2013 Change

Ordinary investment income 765 763 +0%

Thereof current investment income from interest 716 712 +1%

Thereof profit/loss from shares in associated companies 4 1 +471%

Realised net gains on investments 210 76 +177%

Write-ups/write-downs on investments (10) (13) (27%)

Unrealised net gains/losses on investments 16 1 +1298%

Investment expenses (55) (42) +30%

Income from investments under own management 926 784 (18%)

Income from investment contracts 0 2 (87%)

Interest income on funds withheld and contract deposits 84 88 (5%)

Total 1,010 875 +15%

Results Presentation Q1 2014, 15 May 201417

Optimized capital structure

� Shareholders’ equity is up by 2.4% vs. Q1 2013 and even 4.5% vs. FY2013. The recent increase q/q is mainly due to net earnings as well as OCI effects from rates and currencies of €131m

� Goodwill stands at €1,103m. When deducting non-controlling interests, the amount reduces to €1,095m

� Book value per share stands at €29.82, while NAV2 per share is €25.49 at the end of March 2014

� Both per share figures do not contain off-balance sheet reserves. After the recent decline in interest rates, these amount to €~3.5bn (see next page), or roughly €1.30 per share (shareholder share only)

� Subordinated liabilities decline following the call of the 2004 issued €750m Hannover Finance bond in February

III

1 adjusted due to IAS82 NAV calculated as shareholders‘ equity minus shareholder share in goodwill

Shareholders’ equity up by ~€320m vs. FY2013 helped by net income and positive OCI effects

Capital breakdown (€bn)

Shareholders‘ equity Minorities Subordinated liabilities

Equity and capitalization – Solid equity base

7.26.8 7.0

4.23.9 3.9

3.13.1

7.2

3.1 3.1

4.0

31 Mar 2013 30 June 13 30 Sep 13 31 Dec 13 31 Mar 13

3.1

4.2

7.4

14.4

3.1

3.9

6.8

13.8

3.1

3.9

7.0

14.0

3.1

4.0

7.2

14.3

2.4

4.2

7.5

14.1

31 Mar 13 30 June 13 30 Sep 13 31 Dec 13 31 Mar 14

Results Presentation Q1 2014, 15 May 201418

∆ market value vs. book value

III

Talanx’s off-balance sheet up to €3.5bn end of March 2014 (end Dec 2013: €2.9bn)

Unrealised gains and losses (off and on balance she et) as of 31 March 2014 (€m)

31 Dec 13 2,779 150139 49 (250) 2,867 1,619 321 1,940 4,808

Equity and capitalization – Unrealised gains

Total

3,464133 140 59 (298)

3,498

2,404345 2,749 6,247

Loans andreceivables

Held to maturity

Investmentproperty

Real estateown use

Subordinatedloans

Off balancesheet reserves

Availablefor sale

Other assets On balancesheet reserves

Total unreal-ised gains(losses)

Results Presentation Q1 2014, 15 May 201419

Agenda

Group HighlightsI

Investments / CapitalIII

SegmentsII

Essentials Risk Management Reports 2013IV

OutlookV

Appendix

Mid-term Target Matrix

Q1 2014 Additional Information

Risk Management Reports 2013

Results Presentation Q1 2014, 15 May 201420

TERM (Talanx Enterprise Risk Model) run 2013 overal l confirms reliability of the internal model. Capital Adequacy Ratio of 333% close to 2012 level of 351% for 99.5% confidence level

At the 99.97% confidence level – which reflects Tala nx’s own strategic targets -, the Capital Adequacy Ratio stands at 186% (2012: 196%)

Market risks at 37% remain well below the 50% thres hold. Non-life risks representing 38% of risk capital consumption making it the largest single ri sk category

Increase in MCEV to €3.5bn, with the MCEV roughly e qually split between Primary Insurance and Reinsurance. 2013 improvement in Primary Insurance largely driven by capital market development (incl. duration management) , in Reinsu rance positive new business contribution

Significant reduction in duration gap in Life and t he more favourable yield and spread environment trigger the material decline in yield s ensitivity of the MCEV

First-time presentation of separate MCEV values for the cumulated German and foreign entities of Primary Insurance

Essentials – Risk Management Reports 2013IV

Results Presentation Q1 2014, 15 May 201421

Agenda

Group HighlightsI

Investments / CapitalIII

SegmentsII

Essentials Risk Management Reports 2013IV

OutlookV

Appendix

Mid-term Target Matrix

Q1 2014 Additional Information

Risk Management Reports 2013

Results Presentation Q1 2014, 15 May 201422

Targets are subject to no large losses exceeding bu dget ( cat ), no turbulences on capital markets ( capital ), and no material currency fluctuations ( currency )

Gross written premium 2 +2-3%

Return on investment ≥ 3.4%

Group net income ≥ €700m

Return on equity ~ 10%

Dividend payout ratio 35 - 45% target range

V Outlook for Talanx Group 20141

1 The targets are based on an increased large loss budget of €185m (from €80m) in Primary Insurance and €670m (from €625m) in Reinsurance2 On divisional level, Talanx expects gross written premium growth of +3-5% in Industrial Lines, -(1-2)% in Retail Germany, +4-8% in Retail International and a flat to

low single-digit growth rate in Reinsurance

Results Presentation Q1 2014, 15 May 201423

Agenda

Group HighlightsI

Investments / CapitalIII

SegmentsII

Essentials Risk Management Reports 2013IV

OutlookV

Appendix

Mid-term Target Matrix

Q1 2014 Additional Information

Risk Management Reports 2013

Results Presentation Q1 2014, 15 May 2014

1 Risk-free rate is defined as the 5-year rolling average of the 10-year German government bond yield

2 Derived from actual asset duration. Currently ~ 6.5 years, therefore the minimum return is the 13-year average of 13-year German government bond yield. Annually rolling

Segments Key figures Strategic targets

GroupReturn on equity ≥ 750 bps above risk free1

Group net income growth ~ 10%

Dividend payout ratio 35 - 45%

Return on investment2 ≥ 3.5%

Industrial LinesGross premium growth3 3 - 5%

Combined ratio ≤ 96%

EBIT margin4 ≥ 10%

Retention rate 60 - 65%

Retail GermanyGross premium growth ≥ 0%

Combined ratio (non-life) ≤ 97%

New business margin (life) ≥ 2%

EBIT margin4 ≥ 4.5%

Retail InternationalGross premium growth3 ≥ 10%

Combined ratio (non-life) ≤ 96%

Value of New Business (VNB) growth 5 - 10%

EBIT margin4 ≥ 5%

Non-life reinsuranceGross premium growth 3 - 5%

Combined ratio ≤ 96%

EBIT margin4 ≥ 10%

Life & health reinsuranceGross premium growth3 5 - 7%

Value of New Business (VNB) growth ≥ 10%

EBIT margin4 financing and longevity business ≥ 2%

EBIT margin4 mortality and health business ≥ 6%

3 Organic growth only; currency neutral4 EBIT/net premium earned

Note: growth targets are on p.a. basis. They are based on 2012 results.

Mid-term Target MatrixA

24

Results Presentation Q1 2014, 15 May 201425

€m, IFRS Q1 2014 Q1 2013 Change

P&L

Gross written premium 1,763 1,735 +2%

Net premium earned 407 439 (7%)

Net underwriting result 6 2 +205%

Net investment income 72 55 +30%

Operating result (EBIT) 60 33 +84%

Net income after minorities 35 19 +81%

Key ratios

Combined ratio non-life insurance and reinsurance

98.6% 99.4% -0.8%pts

Return on investment 4.2% 3.2% 1.0%pts

Industrial Lines

Q1 2014 Q1 2013 Change

2,027 2,113 (4%)

1,287 1,323 (3%)

(430) (296) n/m

501 387 +29%

54 66 (18%)

29 43 (32%)

100.2% 95.0% 5.2%pts

4.7% 3.8% 0.9%pts

Q1 2014 Q1 2013 Change

1,164 1,056 +10%

983 877 +12%

8 17 (53%)

74 74 (0%)

62 66 (6%)

39 38 +1%

95.1% 94.1% 1.0%pts

4.7% 5.1% -0.4%pts

Retail Germany Retail International

Note: Differences due to rounding may occur.

Q1 2014 Additional Information - SegmentsA

Results Presentation Q1 2014, 15 May 201426

€m, IFRS Q1 2014 Q1 2013 Change

P&L

Gross written premium 2,108 2,198 (4%)

Net premium earned 1,632 1,692 (4%)

Net underwriting result 86 98 (12%)

Net investment income 211 195 +9%

Operating result (EBIT) 286 266 +8%

Net income after minorities 96 79 +22%

Key ratios

Combined ratio non-life insurance and reinsurance

94.5% 94.0% 0.5%pts

Return on investment 3.3% 3.0% 0.3%pts

Note: Differences due to rounding may occur.

Q1 2014 Q1 2013 Change

1,517 1,560 (3%)

1,281 1,389 (8%)

(87) (68) n/m

152 162 (6%)

64 101 (37%)

21 37 (43%)

--- --- ---

4.1% 4.3% -0.2%pts

Q1 2014 Q1 2013 Change

8,414 8,458 (1%)

5,599 5,715 (2%)

(415) (249) n/m

1,010 875 +15%

509 530 (4%)

193 208 (7%)

95.8% 95.0% 0.8%pts

4.3% 3.7% 0.6%pts

Non-Life Reinsurance Life and Health Reinsurance

Group

Q1 2014 Additional Information - Segments (continued)A

Results Presentation Q1 2014, 15 May 201427

Retail Germany Retail International

1 Entity results from Sept 2012 merger of HDI Direkt Versicherung AG and HDI-Gerling Firmen und Privat Versicherung AG

2 Talanx ownership 67.5%3 includes HDI Asekuracja TU S.A., Poland; Talanx ownership of 75.74%4 Talanx ownership 50% + 1 share; closed on 1 June 2012 5 includes Metropolitana6 includes HDI-Gerling Zycie, Poland; Talanx ownership of 75.74%

Numbers for main carriers represent data entry values, fully consolidated

GWP, €m, IFRS Q1 2014 Q1 2013 Change

Non-life Insurance 808 835 (3%)

HDI Versicherung AG1 772 799 (3%)

Life Insurance 1,219 1,277 (5%)

HDI Lebensversicherung AG 500 561 (11%)

neue leben Lebensversicherung AG2 243 249 (3%)

TARGO Lebensversicherung AG 251 245 +2%

PB Lebensversicherung AG 175 176 (0%)

Total 2,027 2,113 (4%)

GWP, €m, IFRS Q1 2014 Q1 2013 Change

Non-life Insurance 708 713 (1%)

HDI Seguros S.A., Brazil 189 212 (11%)

TUiR Warta S.A.3, Poland 229 222 +3%

TU Europa S.A.4, Poland 45 29 +54%

HDI Assicurazioni S. p. A., Italy (P&C) 81 84 (4%)

HDI Seguros S.A. De C.V., Mexico5 43 42 +2%

HDI Sigorta A.Ş., Turkey 50 51 (2%)

Life Insurance 456 343 +33%

TU Warta Zycie S.A., Poland6 39 57 (32%)

TU Europa Zycie4, Poland 55 97 (43%)

Open Life4 6 4 +47%

HDI Assicurazioni S. p. A., Italy (Life) 249 68 +267%

Total 1,164 1,056 +10%

Q1 2014 Additional Information – GWP of main risk carriersA

Results Presentation Q1 2014, 15 May 201428

Q1 2014 Additional Information – Details on GIIPS exposure

Total GIIPS exposure (31 March 2014)

� Total GIIPS exposure incl. private sector assets at ~4.2% of total assets

� GIIPS sovereign exposure at 1.7% of total assets (Q1 2013: 0.7%, FY2013: 1.2%) – Talanx may top up its sovereign exposure to selected GIIPS government issuers to up to 3% of total assets in the course of 2014

� Talanx over time has slightly raised its exposure to Italian and Spanish issuers very selectively, following the investment strategy already communicated to the capital markets

� Additional investments of ca. €1.2bn since 31 Dec. 2013 mainly in sovereign (€~0.8bn) and semi-sovereign (€~0.3bn) issue issuers

A

Comments

Slight increase in GIIPS investments – increase in u nrealised gains

Details on sovereign exposure in €m

Total: €2,149m (amortized cost), €2,291m (fair value)

Total unrealised gain: €142m

€m Government bonds Corporate bonds

GIIPS exposure SovereignSemi-

SovereignFinancial Corporate Covered Other Total

Greece 7 - - - - - 7

Ireland 228 - 10 50 130 237 656

Italy 1,347 - 410 482 848 19 3,106

Portugal 26 - 5 3 - - 35

Spain 682 574 131 233 367 - 1,987

Total 2,291 574 557 769 1,344 256 5,790

670

25

1,250

2013

682

26

1,347

228

7

Greece Ireland Italy Portugal Spain

Amortized cost Fair value

Results Presentation Q1 2014, 15 May 2014

MCEV 2013 - Overview

MCEV of €3.5bn reflects life business of primary i nsurance and reinsurance

� Split of primary insurance business into German domestic (Primary D) and international (Primary INT) business shown to acknowledge the increase of international business

� MCEV explicitly calculated for the major primary life insurance carriers in Germany, Italy, and Poland, namely HDI-, neue leben-, PB and TARGO Lebensversicherung AG, HDI Pensionskasse AG, HDI Assicurazioni S.p.A. Life and Towarzystwo Ubezpieczen na Zycie WARTA S.A., and for the active life and health reinsurance businesses of Hannover Re L&H

� Covered businesses contribute more than 93% of the total IFRS net premiums written by life insurance and life and health reinsurance businesses of the Group

29

A

29.72,727.13,538.31,534.51,807.61,192.61,730.7393.61,337.1MCEV after minorities

46.71,151.51,688.91,030.9986.5120.6702.475.8626.6Value in-force (VIF)

-54.334.915.9-39.4-38.074.353.9-12.866.7Look through and other adjustments

-46.2-85.2-124.6-51.6-67.2-33.7-57.4-5.4-51.9Cost of required capital (CoRC)

12.1-338.9-297.8-214.9-215.0-124.0-82.8-10.0-72.9Cost of residual non-hedgeable risks (CoRNHR)

60.8-713.7-279.4-7.9-2.0-705.7-277.5-13.8-263.7Financial options and guarantees (FOGs)

5.32,254.42,374.81,344.71,308.7909.71,066.1117.7948.3Present value of future profits (certainty equivalent)

17.41,575.61,849.4503.6821.11,072.11,028.3317.8710.5Net asset value (NAV)

%€ m€ m€ m€ m€ m€ m€ m€ m

Change20122013201220132012201320132013

TotalINTD

TalanxReinsurancePrimary insurance

Results Presentation Q1 2014, 15 May 2014

2727.1 36.4 2763.5

233.1164.1 12.4

423.0 807.8 33.0 3538.3

OpeningMCEV

Initialadjustments

Adjustedopening MCEV

New businessvalue

Roll forward Operatingassumptionsand variances(incl. modelchanges)

Economic andother non-operatingvariance

Total MCEVearnings

Closingadjustments

Closing MCEV

MCEV 2013 - Movement of Embedded Value

Movement of Embedded Value (€m)

Increase of MCEV for primary business mainly due to higher yields and lower credit spreads

30

A

2,727 36 2,763

233

423

164 12

807 33 3,538

Results Presentation Q1 2014, 15 May 2014

Primary insurance

� Increase of MCEV for domestic primary insurance mainly driven by economic variances, due to the more favourable economic environment compared to year end 2012

� Improved credit modelling positively affects MCEV, more than offsetting the negative effects of more conservative modelling of certain assets regarding credit risk

Reinsurance

� Excellent value of new business

� Reduced collateral costs for US mortality business

� Negative effects from change in interest rates and currency exchange rates

Comments

31

Apart from increase in primary insurance MCEV, rein surance business contributed an excellent new business value

A

VIF= value in force FS= free surplus RC= required capital

MCEV 2013 - Analysis of change

TalanxFS + RC= NAV

VIF TotalFS + RC= NAV

VIF Total Total

€ m € m € m € m € m € m€ m € m

Opening MCEV 1,072.1 120.6 1,192.6 503.6 1,030.9 1,534.5 2,727.1

Capital injection -33.9 -1.8 -35.7 155.2 - 155.2 119.4

Dividend payments -74.4 - -74.4 -12.6 - -12.6 -86.9

Other implications 3.3 4.7 8.0 30.8 -34.9 -4.1 3.9

Adjusted opening market consistent embedded value (MCEV) 967.1 123.4 1,090.5 676.9 996.1 1,673.0 2,763.5

New business value -2.2 85.6 83.4 -41.0 190.7 149.7 233.1

Expected existing business contribution (reference rate) 1.7 108.0 109.6 4.9 36.5 41.4 151.1

Expected existing business contribution (in excess of reference rate) 0.6 -3.2 -2.6 15.6 - 15.6 13.0

Transfers from VIF and required capital (RC) to free surplus (FS)

109.6 -109.6 - 107.6 -107.6 - -

Experience variances -0.7 -107.9 -108.6 -47.2 56.8 9.6 -99.0

Assumption changes - -61.7 -61.7 -23.8 -15.6 -39.4 -101.2

Other operating variances 4.1 191.9 196.1 12.0 -20.3 -8.3 187.8Operating MCEV earnings 113.1 103.0 216.1 28.0 140.6 168.6 384.8

Economic variances -9.8 458.5 448.7 76.5 -107.1 -30.6 418.1

Other non-operating variances - -0.1 -0.1 - 5.0 5.0 4.9

Total MCEV earnings 103.3 561.4 664.7 104.5 38.6 143.1 807.8Closing adjustments -42.1 17.5 -24.6 39.7 -48.1 -8.5 -33.0

Capital injection -1.9 17.9 16.0 131.9 - 131.9 147.8

Dividend payments -39.4 - -39.4 -63.2 - -63.2 -102.7

Change in currency exchange rates -0.8 -0.3 -1.1 -28.9 -48.1 -77.1 -78.2

Closing MCEV after minorities 1,028.3 702.4 1,730.7 821.1 986.5 1,807.6 3,538.3

ReinsurancePrimary insurance

Results Presentation Q1 2014, 15 May 2014

Increase of Talanx’s new business value by 6.3%

32

A

Primary segment� Increase in new business

value� Increase of profitability due to:� Decrease of FOGs for

domestic primary insurance due to lower guaranteed interest rates

� Decrease of CoRNHR due to lower necessary internal risk capital

Reinsurance segment� New business value on the

same excellent level as last year

� Lower contribution of treaties by the subsidiaries in Ireland, Bermuda and the US where the premiums are set equal to the fees leads to lower new business margin

*The values for 2012 exclude the NBV of WARTA because WARTA was included in the 2012 MCEV results only as a closing adjustment. **The values for 2013 exclude the new business written by HDI-Gerling Zycie since the merger of WARTA with HDI-Gerling Zycie is included in the 2013 MCEV only in the closing adjustments.

MCEV 2013 – New Business

-8.3%3.4%3.1%5.8%4.0%1.7%2.2%0.8%2.5%New businessmargin

6.3219.2233.1153.8149.765.483.45.478.0New business valueafter minorities

-71.0-4.7-8.0-3.7-5.2-1.0-2.8-1.4-1.3Look through and other adjustments

-15.7-7.7-8.9-5.5-7.7-2.2-1.2-1.1-0.1Cost of requiredcapital (CoRC)

3.4-30.5-29.5-18.8-22.7-11.7-6.8-1.8-5.0

Cost of residual non-hedgeable risks(CoRNHR)

90.8-18.1-1.7---18.1-1.7-4.32.6

Financial optionsand guarantees(FOGs)

-6.4346.6324.4246.0226.3100.798.116.281.8

Present value of future profits(certaintyequivalent)

34.9-66.4-43.2-64.1-41.0-2.2-2.2-2.20.0Profit/Loss on newbusiness

%€ m€ m€ m€ m€ m€ m€ m€ m

Change2012*2013**201220132012*2013**2013**2013

TotalINTD

TalanxReinsurancePrimary insurance Comments

Results Presentation Q1 2014, 15 May 2014

Reduced impact of changes in interest rates due to more favourable economic situationHigher diversification effect between German/intern ational Primary Insurance and Reinsurance

� Decrease of sensitivities with respect to economic data

� Asymmetrical and non-linear impact from embedded options and guarantees on shareholders’ cash flows

� Impact on MCEV thus lower in 2013 due to more favourable economic environment

� Increased asset duration for primary business also positively affects interest sensitivity

33

A MCEV 2013 - Sensitivity analysis

D INT

2013 2013 2013 2012 2013 2012 2013 2012

€ m € m € m € m € m € m € m € m

MCEV after minorities 1,337.1 393.6 1,730.7 1,192.6 1,80 7.6 1,534.5 3,538.3 2,727.1

% % % % % % % %

Mortality/Morbidity + 5% (non-annuity) -1.5 -2.2 -1.7 -3.5 -25.4 -33.4 -13.8 -20.3

Mortality/Morbidity -5% (non-annuity) 1.7 2.2 1.8 3.3 25.3 36.0 13.8 21.7

Mortality +5% (annuity) 1.8 0.0 1.4 3.1 4.5 3.6 2.9 3.4

Mortality -5% (annuity) -1.9 0.0 -1.5 -3.3 -4.8 -3.8 -3.1 -3.6

Lapse rate +10% -2.4 -0.9 -2.1 -1.3 -8.9 -12.3 -5.5 -7.5

Lapse rate -10% 2.8 1.0 2.4 1.4 5.7 8.3 4.1 5.3

Maintenance expenses +10% -5.1 -2.3 -4.4 -9.2 -2.7 -3.2 -3.5 -5.8

Maintenance expenses -10% 5.1 2.3 4.5 8.9 2.5 2.9 3.5 5.5

Yield curve +1% 7.9 -1.8 5.7 32.4 -8.8 -7.5 -1.7 10.0

Yield curve -1% -13.7 1.4 -10.3 -75.3 8.2 9.0 -0.8 -27.8

Swaption implied volatilities +25% -3.5 -1.1 -2.9 -16.5 -0.2 -0.3 -1.5 -7.4

Equity and property value +10% 2.6 2.1 2.5 4.9 0.1 0.1 1.2 2.2

Equity and property value -10% -2.8 -2.1 -2.6 -5.2 -0.1 -0.1 -1.3 -2.3

Equity option volatilities +25% -0.7 -0.1 -0.6 3.8 0.0 0.0 -0.3 1.6

Talanx

Total

Primary insurance Reinsurance

Results Presentation Q1 2014, 15 May 2014

MCEV 2013 -New Business Value sensitivity analysis

Diversification for economic sensitivities between domestic and international primary business

34

A

*The values for 2012 exclude the NBV of WARTA because WARTA was included in the 2012 MCEV results only as a closing adjustment. **The values for 2013 exclude the new business written by HDI-Gerling Zycie since the merger of WARTA with HDI-Gerling Zycie is included in the 2013 MCEV only in the closing adjustments.

D INT

2013 2013** 2013** 2012* 2013 2012 2013** 2012*

€ m € m € m € m € m € m € m € m

NBV after minorities 78.0 5.4 83.4 65.4 149.7 153.8 233.1 2 19.2

% % % % % % % %

Mortality/Morbidity + 5% (non-annuity) -1.5 -24.4 -3.0 -9.0 -19.9 -27.5 -13.9 -22.0

Mortality/Morbidity -5% (non-annuity) 4.1 24.4 5.4 6.5 19.2 26.7 14.3 20.7

Mortality +5% (annuity) 0.8 -0.1 0.7 2.5 12.3 1.1 8.2 1.5

Mortality -5% (annuity) -0.9 0.1 -0.8 -3.0 -13.0 -1.2 -8.6 -1.7

Lapse rate +10% -4.8 -10.2 -5.1 -6.7 -5.8 -7.4 -5.6 -7.2

Lapse rate -10% 8.2 13.2 8.5 5.0 5.6 6.0 6.6 5.7

Maintenance expenses +10% -3.2 -20.3 -4.3 -16.7 -5.1 -3.2 -4.8 -7.3

Maintenance expenses -10% 4.6 20.2 5.6 12.7 5.0 3.6 5.2 6.3

Yield curve +1% 0.4 -41.6 -2.3 43.1 -9.6 -9.2 -7.0 6.4

Yield curve -1% -0.1 39.7 2.5 -96.9 10.1 9.7 7.4 -20.0

Swaption implied volatilities +25% 0.2 -24.0 -1.4 -17.6 0.0 0.0 -0.5 -5.3

Equity and property value +10% 0.8 5.0 1.1 4.4 0.0 0.0 0.4 1.3

Equity and property value -10% -1.2 -5.9 -1.5 -5.2 0.0 0.0 -0.5 -1.6

Equity option volatilities +25% -0.9 -2.2 -0.9 4.1 0.0 0.0 -0.3 1.2

Talanx

Total

Primary insurance Reinsurance

Results Presentation Q1 2014, 15 May 2014

MCEV 2013 - Duration concepts

Duration of bond portfolio increased for life insur ance because of portfolio adjustments Active and significant reduction of asset-liability-missma tch in life insurance

Durations of technical reserves and bond portfolio, 2013 and 2012

35

13.1 13.1

5.95.1

9.9 9.610.4

11.7

5.95.1

8.3 8.5

6.87.2

3.94.0

9.210.0

Primary insurance(life) 2013

Primary insurance(life) 2012

Primary insurance(non-life) 2013

Primary insurance(non-life) 2012

Talanx Group 2013 Talanx Group 2012

Technical reserves (Macaulay) Technical reserves (effective) Bond portfolio (Macaulay incl. derivatives)

∆ < 1.0 ∆ =2.5

∆ =1.9∆ =1.2

∆ =1.1∆ =1.7

20122013 approx.for slightly lower modified duration

A

Results Presentation Q1 2014, 15 May 2014

SCR 2013 - Result History (Economic View)

CAR almost unchanged compared to 2012 which is refl ected by the simultaneous change of own funds and SCR

Comments

� Own funds (after minorities) increase significantly from €6.6bn (31 Dec 2012) to €7.8bn 31 Dec 2013

� Change in own funds from 2012 to 2013 largely due to

� the increase of the own funds for the primary life insurance companies, which is mainly driven by higher yields and lower credit spreads end 2013

� the increase of the own funds for the Hannover Re Group, which is mainly driven by the best estimate revaluation of the reserves, the discount effects on claim reserves due to an increase of interest rates

Own Funds (€bn)

5.6 5.6 6.6

2010 2011 2013year

Solvency Capital Required (€bn)

Capital Adequacy Ratio (CAR)

36

2012

7.8

1.7 2.0 1.9

2010 2011 2013year

2012

2.4

322%277%

351%

2010 2011 2013year

2012

333%

A

Results Presentation Q1 2014, 15 May 2014

(As of 31 December 2013, €bn)

Talanx Group features a well-diversified portfolio

1 Solvency capital requirement; determined according to 99.5% security level, economic view, after minorities

� Diversification effect of 25% among primary divisions

� The Group benefits from a diversification effect of 15% between primary insurance and reinsurance

� This corresponds to an absolute amount of €0.4bn

SCR1 by Division Comments

Diversifi-cation

betweenprimary

divisions and corporatefunctions

37

0.5

1.3

27%

48%

52%

2.4

1.4

(0.4)

(0.4)

(25%)

(15%)

0.5

30%

0.4

0.4

23%

CorporateOperations

PrimaryInsurance

Re-insurance

Diversifi-cation

betweenprimary

and reinsurance

Talanx Group

21%

RetailGermany

RetailInternational

IndustrialLines

SCR 2013 – Split by division

31 Dec 12

0.6 0.3 0.5 0.4 0.7 1.1 1.3 0.5 1.9

A

35% 18% 25% 22% 40% 45% 55% 22%

Results Presentation Q1 2014, 15 May 2014

(as of 31 December 2013, €bn)

Material rise in Own Funds in comparison to year-en d 2012

1 economic view, after minorities

Own funds 1 by Division

38

SCR 2013 - Own Funds by division

7.8

(1.9)

4.1

2.0

1.3

2.4

Retail Germany RetailInternational

Industrial Lines Reinsurance Corporate Functions

Talanx Group

31 Dec 12 1.8 1.1 1.9 3.7 (1.9) 6.6

A

39 Results Presentation Q1 2014, 15 May 2014

Solvency capital requirement split into components

High diversification between risk categories

Risk components of Talanx Group 1

(as of 31 December 2013, €m)

Mar

ket

risk

nonl

ife a

nd

rein

sura

nce

Mar

ket

risk

prim

ary

life

Pen

sion

ris

k

Div

ersi

ficat

ion

Tot

al

mar

ket

risk

Pre

miu

m

and

rese

rve

risk

(non

life)

Nat

Cat

(n

et)

Cou

nter

part

y de

faul

t ris

k

Div

ersi

ficat

ion

Non

life

risk

Fur

ther

ris

k (li

fe)

Ope

ratio

nal

risk

Oth

er r

isk

Tot

al r

isk

befo

re ta

x an

d be

fore

di

vers

ifica

tion

Tax

effe

ct

(non

life

and

smal

l en

titie

s)

Div

ersi

ficat

ion

Tot

al r

isk

1.81,632

33.6% 433

8.9% 390

8.0%

653

13.4%

1,802

37.1%

1,388

28.6%

1,409

29.0%

259

5.3%

1,200

24.7%1,856

38.2%

781

16.1% 389

8.0%

29

0.6%

4,857

100.0%

651

1,850

2,356

1 Figures show risk categorisation of the Talanx Group after minorities, tax effects and diversification effects as of 2013. Solvency capital requirement determined according to 99.5% security level, economic view, after minorities

A

Results Presentation Q1 2014, 15 May 2014

SCR 2013 - Sensitivity of Solvency Capital Ratios

Conservatism of Talanx´s economic view underlined by not including subordinated liabilitesinto Own Funds

Inclusion of subordinated liabilities

7.8

2.4333%

Own Funds SCR CAR

Own funds incl.subordinatedliabilities

9.7

2.4

412%

SCR CAR

Economic view Comments

� In the Economic View, subordinated liablitiesare not included in Own Funds

� Subordinated liabilities would lead to an increase in own funds of roughly €1.9bn

� Inclusion of subordinated liabilities leads to an increase in the capital adequacy ratio to 412%

� Consideration of subordinated liabilities has no influence on solvency capital requirements

40

A

Results Presentation Q1 2014, 15 May 2014

SCR 2013 - Sensitivity of Solvency Capital Ratios „Haircut Effect”

Talanx´s CAR would be at a comfortable level even af ter a haircut

1 Solvency capital requirement; determined according to 99.5% security level, Regulatory View (including subordinated liabilities 267%)

Effect of availability constraints on CAR

333%233%

CAR Economic View at

Talanx level

Capital Adequacy Ratio Comments

� Regulatory framework under Solvency II relates minorities to the availability of capital, respectively Own Funds. This places restrictions on regulatory Own Funds on Group level (e.g. minority interest)

� The amount, however, depends on the risk capital allocated to solo entities

� Capital allocation is determined by an appropriate allocation method

� The main impact on availability of Own Funds stems from minority interest in Hannover Re

41

Internal Model basedallocation after haircut at

HDI VaG level1

A

Results Presentation Q1 2014, 15 May 201442

This presentation contains forward-looking statements which are based on certain assumptions, expectations and opinions of the management of Talanx AG (the "Company") or cited from third-party sources. These statements are, therefore, subject to certain known or unknown risks and uncertainties. A variety of factors, many of which are beyond the Company’s control, affect the Company’s business activities, business strategy, results, performance and achievements. Should one or more of these factors or risks or uncertainties materialize, actual results, performance or achievements of the Company may vary materially from those expressed or implied as being expected, anticipated, intended, planned, believed, sought, estimated or projected.in the relevant forward-looking statement.

The Company does not guarantee that the assumptions underlying such forward-looking statements are free from errors nor does the Company accept any responsibility for the the actual occurrence of the forecasted developments. The Company neither intends, nor assumes any obligation, to update or revise these forward-looking statements in light of developments which differ from those anticipated.

Where any information and statistics are quoted from any external source, such information or statistics should not be interpreted as having been adopted or endorsed by the Company as being accurate.Presentations of the company usually contain supplemental financial measures (e.g., return on investment, return on equity, gross/net combined ratios, solvency ratios) which the Company believes to be useful performance measures but which are not recognised as measures under International Financial Reporting Standards, as adopted by the European Union ("IFRS"). Therefore, such measures should be viewed as supplemental to, but not as substitute for, balance sheet, statement of income or cash flow statement data determined in accordance with IFRS. Since not allcompanies define such measures in the same way, the respective measures may not be comparable to similarly-titled measures used by other companies. This presentation is dated as of 15 May 2014. Neither the delivery of this presentation nor any further discussions of the Company with any of the recipients shall, under any circumstances, create any implication that there has been no change in the affairs of the Company since such date. This material is being delivered in conjunction with an oral presentation by the Company and should not be taken out of context.

Disclaimer