Results 2016 and Outlook 2017 - Komax · 21 March 2017 / Results 2016 and Outlook 2017 / 7 THE WAY...

45

THE WAY TO MAKE IT Results 2016 and Outlook 2017 21 March 2017

Transcript of Results 2016 and Outlook 2017 - Komax · 21 March 2017 / Results 2016 and Outlook 2017 / 7 THE WAY...

THE WAY TO MAKE IT

Results 2016 and Outlook 201721 March 2017

21 March 2017 / Results 2016 and Outlook 2017 / 2

THE WAY TO MAKE IT

2016 in brief

Sale of Medtech business unit to GIMA

Four acquisitions• Thonauer Group• SLE Electronics USA• Ondal Tape Processing• Kabatec

Development of 2017–2021 strategy

Launch of various new products

Establishment of new site in Mexico

Restructuring in Porta Westfalica (exit from the module testing business)

Summary 2016 was an intensive year. We coped well with the various challenges and delivered a very pleasing result.

21 March 2017 / Results 2016 and Outlook 2017 / 3

THE WAY TO MAKE IT

Agenda

2016 financial year

Operational performance

Financial performance

Focus on core market (wire)

Focus and outlook 2017

Questions

21 March 2017 / Results 2016 and Outlook 2017 / 5

THE WAY TO MAKE IT

Significant rise in revenues

315.1

373.0

2015 2016

in CHF millionRevenue growth 18.4%, internal growth 8.8%• Europe CHF 190.1 million (2015: CHF 156.5 million) • North/South America CHF 77.9 million (2015: CHF 64.3 million)• Asia CHF 73.5 million (2015: CHF 61.8 million)

1

1 As a result of the sale of Komax Medtech, the 2015 figures have been restated in accordance to IFRS 5.

21 March 2017 / Results 2016 and Outlook 2017 / 6

THE WAY TO MAKE IT

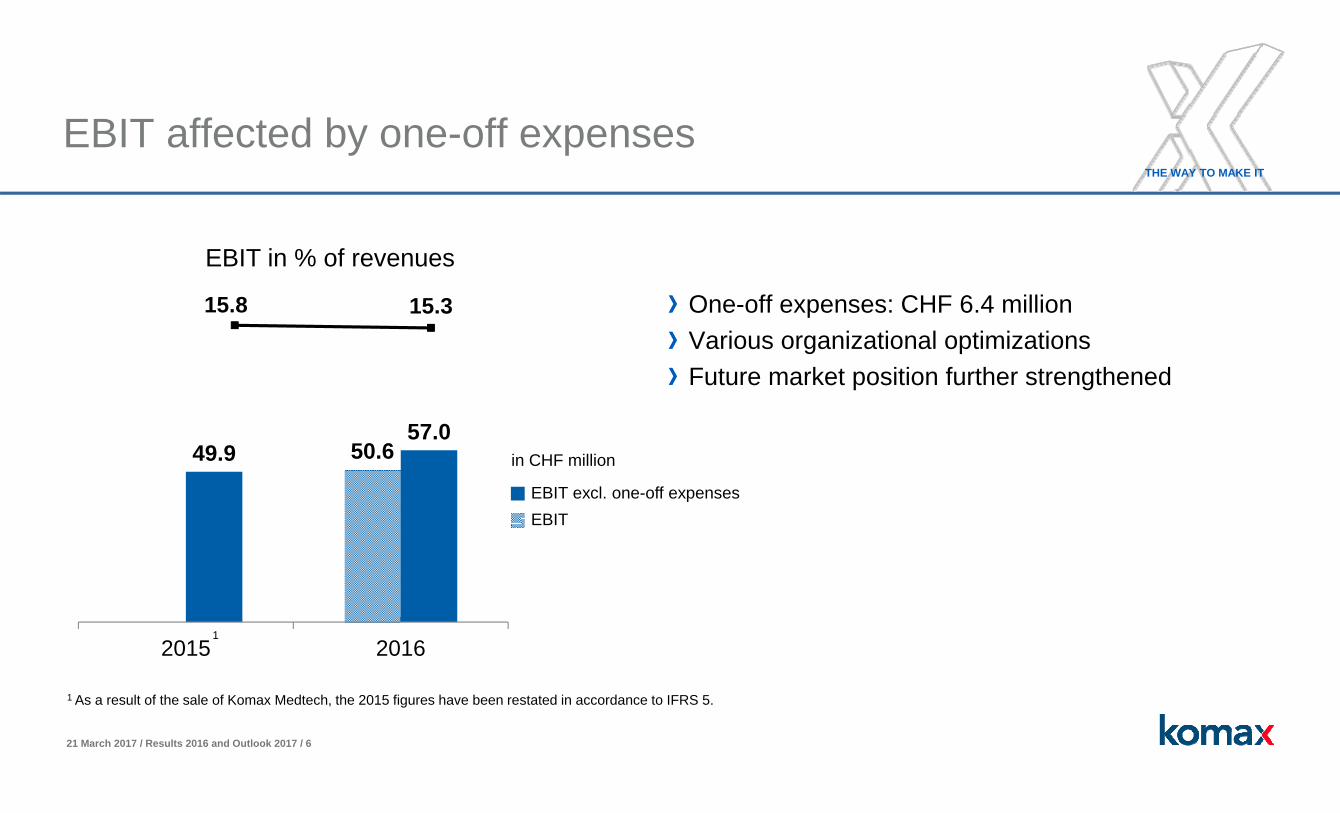

15.8 15.3

50.649.957.0

2015 2016

EBIT affected by one-off expenses

EBIT excl. one-off expensesEBIT

in CHF million

One-off expenses: CHF 6.4 millionVarious organizational optimizationsFuture market position further strengthened

1

1 As a result of the sale of Komax Medtech, the 2015 figures have been restated in accordance to IFRS 5.

EBIT in % of revenues

21 March 2017 / Results 2016 and Outlook 2017 / 7

THE WAY TO MAKE IT

Komax Medtech: Key figures of the sale

28.3

1.74.1 2.0

Signing(March 2016)

NWC/ND Adj.(Closing

April 2016)

Earn-Out(2017)

KSM 24%(2018)

in CHF million

1

1 Komax Systems Malaysia

Strategic buyer: GIMA

Contingent consideration of CHF 6.1 million in total• Earn-out: CHF 4.1 million • Sale of residual stake (24%): CHF 2.0 million

Optimal timing for divestment of BU Medtechthanks to record-high order intake prior to the sale

75% of goodwill credited

Komax Medtech transaction value

21 March 2017 / Results 2016 and Outlook 2017 / 8

THE WAY TO MAKE IT

Agenda

2016 financial year

Operational performance

Financial performance

Focus on core market (wire)

Focus and outlook 2017

Questions

21 March 2017 / Results 2016 and Outlook 2017 / 9

THE WAY TO MAKE IT

Sales growth with broad-based regional spread

Net sales by region

Change from previous year

-10% 0% 10% 20% 30%

Revenues: CHF 373.0 million

Revenue growth: 18.4%

Internal growth: 8.8%

SwitzerlandEuropeAfricaNorth/South AmericaAsia

As a result of the sale of Komax Medtech, the 2015 figures have been restated in accordance to IFRS 5.

49%Europe

8%Africa

21%North/

South America

20%Asia 2%

Switzerland

21 March 2017 / Results 2016 and Outlook 2017 / 10

THE WAY TO MAKE IT

32.5

–19.7–5.7

-6.4

EBIT 2015 Material/revenues Personnel Operating expenses EBIT 2016 excl.one-off expenses

One-off expenses EBIT 2016

Positive EBIT development

in CHF million

49.9

Gross profit margin2016: 63.9% • Product mix• Volume effect

Gross profit margin2015: 65.4%

~ 57 50.6

Personnel expensesin % of revenues2016: 33.8%

Personnel expensesin % of revenues2015: 33.7%

• Higher volumes • Higher variable

costs• Influenced by

acquisitions

• Porta Westfalicarestructuring

• Mexico set-up• Turkey

21 March 2017 / Results 2016 and Outlook 2017 / 11

THE WAY TO MAKE IT

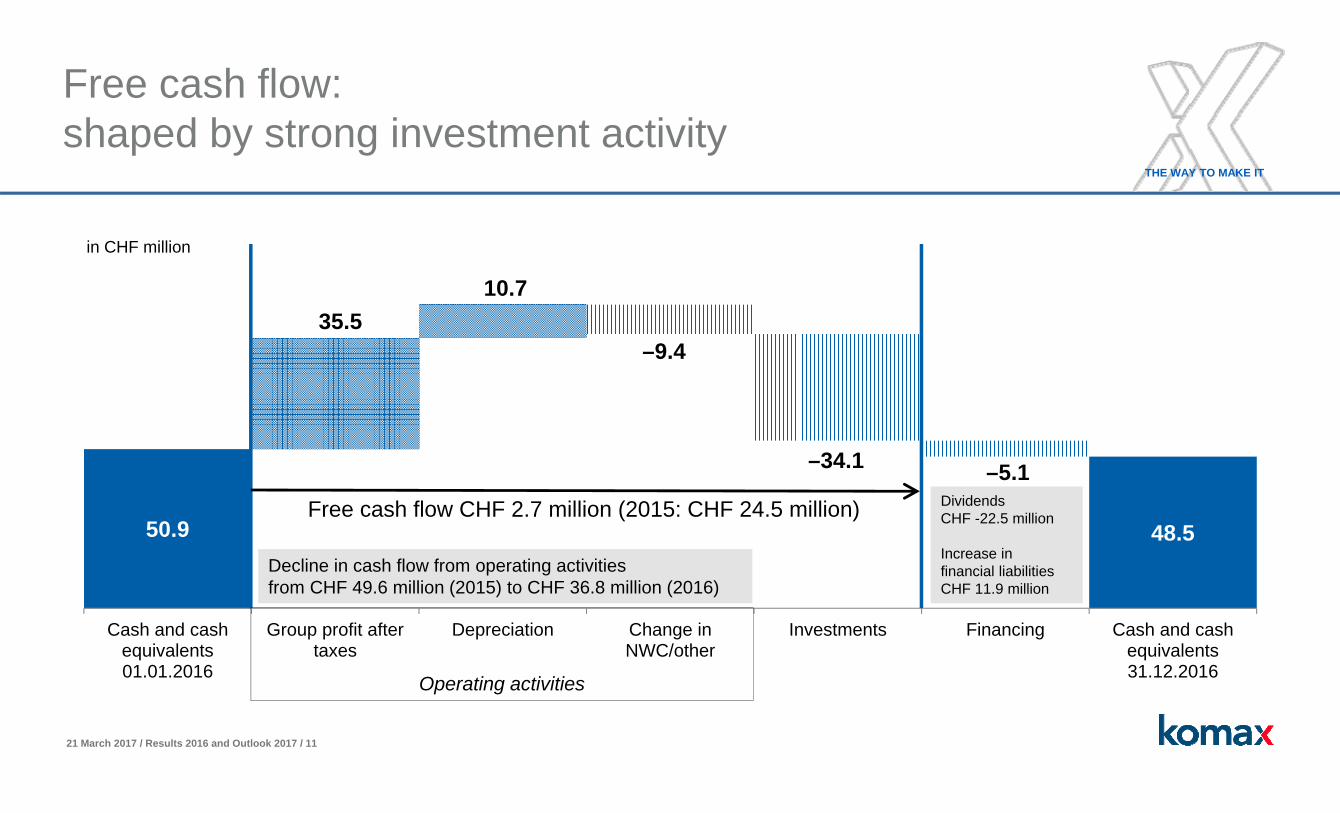

Free cash flow: shaped by strong investment activity

50.9 48.5

35.510.7

–9.4

–34.1 –5.1

Cash and cashequivalents01.01.2016

Group profit aftertaxes

Depreciation Change inNWC/other

Investments Financing Cash and cashequivalents31.12.2016

Free cash flow CHF 2.7 million (2015: CHF 24.5 million)

in CHF million

Operating activities

Decline in cash flow from operating activities from CHF 49.6 million (2015) to CHF 36.8 million (2016)

DividendsCHF -22.5 million

Increase in financial liabilitiesCHF 11.9 million

21 March 2017 / Results 2016 and Outlook 2017 / 12

THE WAY TO MAKE IT

High investment volume in 2016

Net investment (excl. acquisition and sale of companies)

45%Land, buildings

24%IT software,

hardware

31%Tangible assets

Net investment (excl. acquisition and sale of companies): CHF 21.4 million(2015: CHF 25.1 million)• Property, plant and equipment (CHF 17.1 million)• Intangible assets (CHF 4.7 million)

Investment volume over the next five years: CHF 16–20 million p.a. on average

Investment sum in 2016 for acquisitions:CHF 36.2 million (2015: CHF 0).

Cash outflow from divestment of Komax Medtech: CHF 23.6 million

21 March 2017 / Results 2016 and Outlook 2017 / 13

THE WAY TO MAKE IT

Positive currency effect

14%CHF

18%USD

45%EUR

11%Others

12%CNY

60

70

80

90

100

110

120

Dec

13

Feb

14

Apr

14

Jun

14

Aug

14

Oct

14

Dec

14

Feb

15

Apr

15

Jun

15

Aug

15

Oct

15

Dec

15

Feb

17

EUR (Basis: 1.21) USD (Basis: 1.00) BRL (Basis: .3763) CNY (Basis: .1610)

Change in currency breakdown due to acquisitions and divestments• Significant rise in other currencies

(from 5% to 11%)

Net sales by currency

Currency impact• Net sales +0.8%• Gross profit margin +0.6 percentage points• EBIT margin +0.2 percentage points

21 March 2017 / Results 2016 and Outlook 2017 / 14

THE WAY TO MAKE IT

–6.1

–2.2

2015 2016

29.235.5

2015 2016

17.6 18.3

Tax rate in % of EBT

Group profit after taxes (EAT) rises by 21.5%

in CHF million

Financial result

Absolute increase in EAT of CHF 6.3 million Improvement in financial result by CHF 3.9 million to CHF –2.2 million; prior year influenced by abandonment of minimum EUR/CHF exchange rate (2015: CHF –6.1 million)

Expected medium-term tax rate approx. 21%

1

1 As a result of the sale of Komax Medtech, the 2015 figures have been restated in accordance to IFRS 5.

EAT

in CHF million

21 March 2017 / Results 2016 and Outlook 2017 / 15

THE WAY TO MAKE IT

Financial base remains strong

71.072.6

Equity ratio in % of total assetsEquity ratio 72.6%

Net cash of CHF 17.4 million (31.12.2015: CHF 34.4 million)

Intangible assets CHF 69.9 million (31.12.2015: CHF 49.5 million), of which goodwillCHF 45.9 Mio. (31.12.2015: CHF 29.2 million)

Technology assets of CHF 9.7 million(31.12.2015: CHF 8.2 million)

399.0429.6

283.1311.9

31.12.2015 31.12.2016

Total assetsShareholders' equity

in CHF million

21 March 2017 / Results 2016 and Outlook 2017 / 16

THE WAY TO MAKE IT

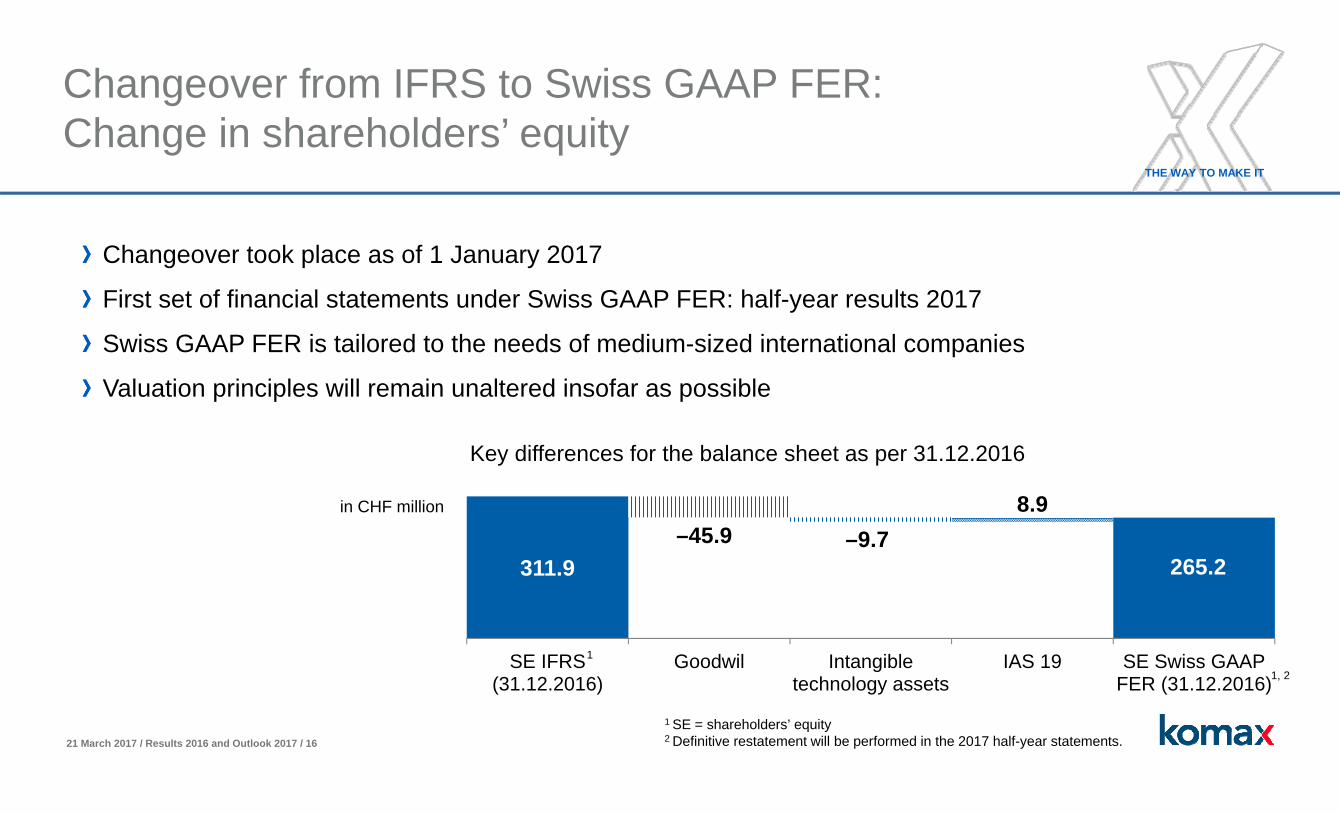

Changeover from IFRS to Swiss GAAP FER:Change in shareholders’ equity

Changeover took place as of 1 January 2017

First set of financial statements under Swiss GAAP FER: half-year results 2017

Swiss GAAP FER is tailored to the needs of medium-sized international companies

Valuation principles will remain unaltered insofar as possible

311.9–45.9 –9.7

8.9

SE IFRS(31.12.2016)

Goodwil Intangibletechnology assets

IAS 19 SE Swiss GAAPFER (31.12.2016)

in CHF million

265.2

Key differences for the balance sheet as per 31.12.2016

1, 2

1 SE = shareholders’ equity2 Definitive restatement will be performed in the 2017 half-year statements.

1

21 March 2017 / Results 2016 and Outlook 2017 / 17

THE WAY TO MAKE IT

120.0100.0

26.2

40.0

27.6

2015 2016

New syndicated loan

0.81 0.91

Average interest rate in %New syndicated loan of CHF 100 million with an option of an additional CHF 40 million

Duration: until January 2022

Average rate of interest on financial loans: 0.91% (2015: 0.81%) Credit line

thereof utilized

in CHF million

Credit option

without external basket

21 March 2017 / Results 2016 and Outlook 2017 / 18

THE WAY TO MAKE IT

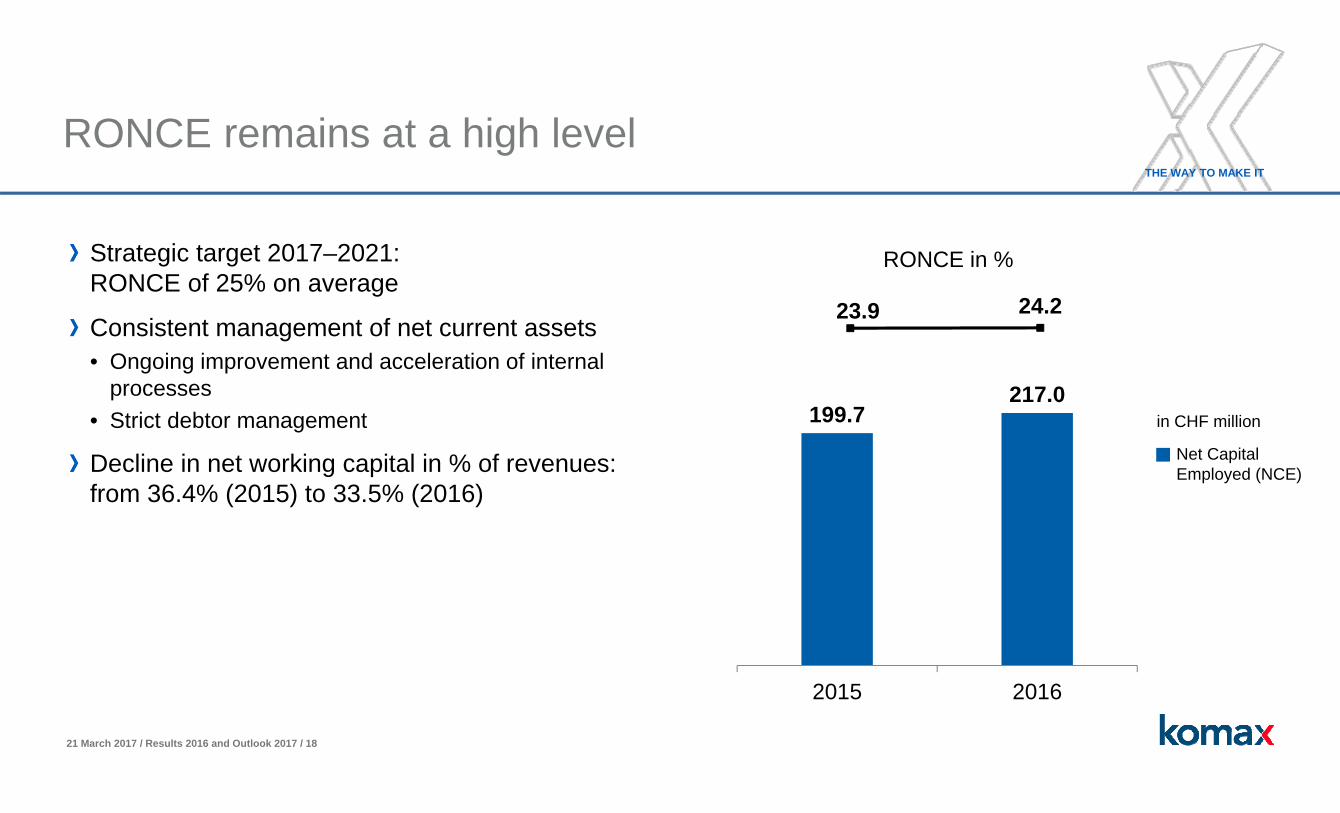

RONCE remains at a high level

Strategic target 2017–2021: RONCE of 25% on average

Consistent management of net current assets• Ongoing improvement and acceleration of internal

processes• Strict debtor management

Decline in net working capital in % of revenues: from 36.4% (2015) to 33.5% (2016)

RONCE in %

23.9 24.2

199.7217.0

2015 2016

Net Capital Employed (NCE)

in CHF million

21 March 2017 / Results 2016 and Outlook 2017 / 19

THE WAY TO MAKE IT

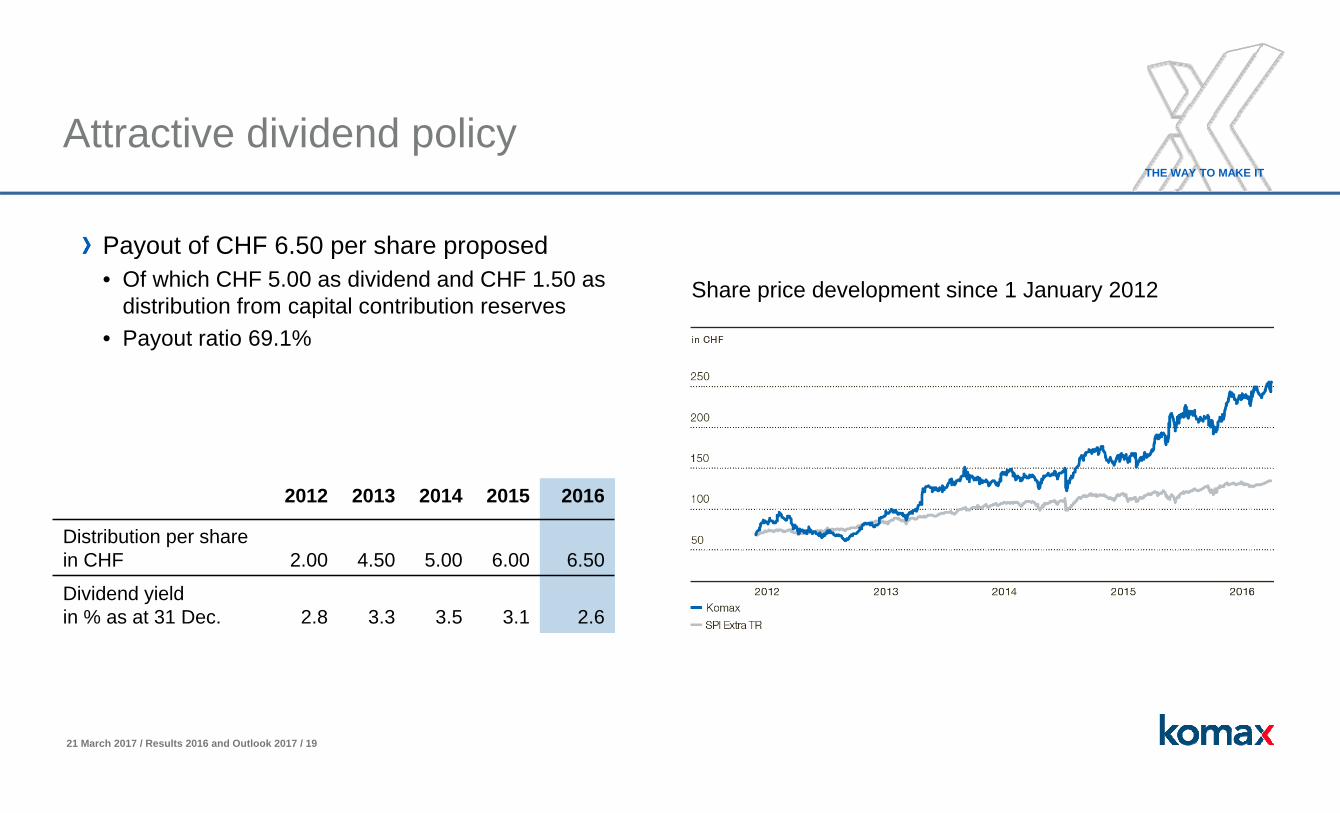

Attractive dividend policy

Payout of CHF 6.50 per share proposed• Of which CHF 5.00 as dividend and CHF 1.50 as

distribution from capital contribution reserves • Payout ratio 69.1%

Share price development since 1 January 2012

2012 2013 2014 2015 2016

Distribution per sharein CHF 2.00 4.50 5.00 6.00 6.50

Dividend yieldin % as at 31 Dec. 2.8 3.3 3.5 3.1 2.6

21 March 2017 / Results 2016 and Outlook 2017 / 20

THE WAY TO MAKE IT

Agenda

2016 financial year

Operational performance

Financial performance

Focus on core market (wire)

Focus and outlook 2017

Questions

21 March 2017 / Results 2016 and Outlook 2017 / 21

THE WAY TO MAKE IT

Impressive facts about vehicle wiring systems

Compact Full-size

Wires approx. 1300(approx. 25% twisted)

approx. 1800(approx. 30% twisted)

Crimp contacts approx. 2300 approx. 3200Plug housings approx. 250 approx. 300Wire length (total) approx. 2000 m approx. 4000 mWire length (maximum) approx. 7 m approx. 8 mWeight of wire harness approx. 30 kg approx. 38 kgCost of wire harness CHF 350 – 500 CHF 600 – 800

The wires have a cross-section of between 0.13 mm2 and 70 mm2 and are made of copper and aluminium.

21 March 2017 / Results 2016 and Outlook 2017 / 22

THE WAY TO MAKE IT

Megatrends

The benefits for Komax

SafetyFrom accident protection to accident avoidance thanks to additional sensors

Affordable vehiclesIncrease in cost efficiency through platform strategies and automation

Continuous growth number of vehicles produced and sold“Electrification” marked increase in amount of cabling per vehicleIncreasing complexity of vehicle power supply systems processing increasingly automatedGreater quality and efficiency demands can only be met by automated solutionsNew types of wire innovations offer opportunity for USPs

Environmental awareness / climate changeElectro-mobility: emission-free vehicles as objective

Integrated automobileComplex integrated information systems form the basis for autonomous driving; comprehensive infotainment systems

21 March 2017 / Results 2016 and Outlook 2017 / 23

THE WAY TO MAKE IT

Strong growth in wires requiring processing

Source: IHS 2015, Light Vehicle Production Forecast, Komax Market Research

2015 2016 2017 2018 2019 2020 2021

Rising number of vehicles producedCAGR 2015 – 2021: approx. 3%

In addition:2 – 3% CAGR over 5 years

Two additional factors are doubling the volume growth that comes from the increase in vehicle production:• Rise in number of wires in vehicles• Pressure for automation

21 March 2017 / Results 2016 and Outlook 2017 / 24

THE WAY TO MAKE IT

Key strategic priorities

Innovative production concepts

Solutions along the value chain

Increase in global reach

Development of non-automotive markets

21 March 2017 / Results 2016 and Outlook 2017 / 25

THE WAY TO MAKE IT

Global market leader in the taping area

Gap in value chain closed through acquisitions (Ondal and Kabatec)

Global leader in the taping area

21 March 2017 / Results 2016 and Outlook 2017 / 26

THE WAY TO MAKE IT

Key strategic priorities

Innovative production concepts

Solutions along the value chain

Increase in global reach

Development of non-automotive markets

21 March 2017 / Results 2016 and Outlook 2017 / 27

THE WAY TO MAKE IT

Special circuit solutions

Antennae Infotainment

Data transmission / sensors / airbags

E-mobility

21 March 2017 / Results 2016 and Outlook 2017 / 28

THE WAY TO MAKE IT

Key strategic priorities

Innovative production concepts

Solutions along the value chain

Increase in global reach

Development of non-automotive markets

21 March 2017 / Results 2016 and Outlook 2017 / 29

THE WAY TO MAKE IT

Global production: vehicles and harnesses

Vehicle production

Harnessproduction

21 March 2017 / Results 2016 and Outlook 2017 / 30

THE WAY TO MAKE IT

Geographic markets

~ 20 Crimp to crimp machines~ 20 Other machines

21 March 2017 / Results 2016 and Outlook 2017 / 31

THE WAY TO MAKE IT

Acquisitions: Thonauer Group, Practical Solution

Development and production site in SingaporeDistribution centre in ShanghaiSales channel in Central and Eastern Europe

21 March 2017 / Results 2016 and Outlook 2017 / 32

THE WAY TO MAKE IT

Key strategic priorities

Innovative production concepts

Solutions along the value chain

Increase in global reach

Development of non-automotive markets

21 March 2017 / Results 2016 and Outlook 2017 / 33

THE WAY TO MAKE IT

Development of non-automotive markets

MultimediaConnected carsAutonomous driving

SafetyLightweight constructionReduction of emissions

Small batchesE-mobilityIntegrated production / industry 4.0

Aerospace Telecom/Datacom Industrial

Selective and complementary build-up of competencies in non-automotive areas supports success of core business

21 March 2017 / Results 2016 and Outlook 2017 / 35

THE WAY TO MAKE IT

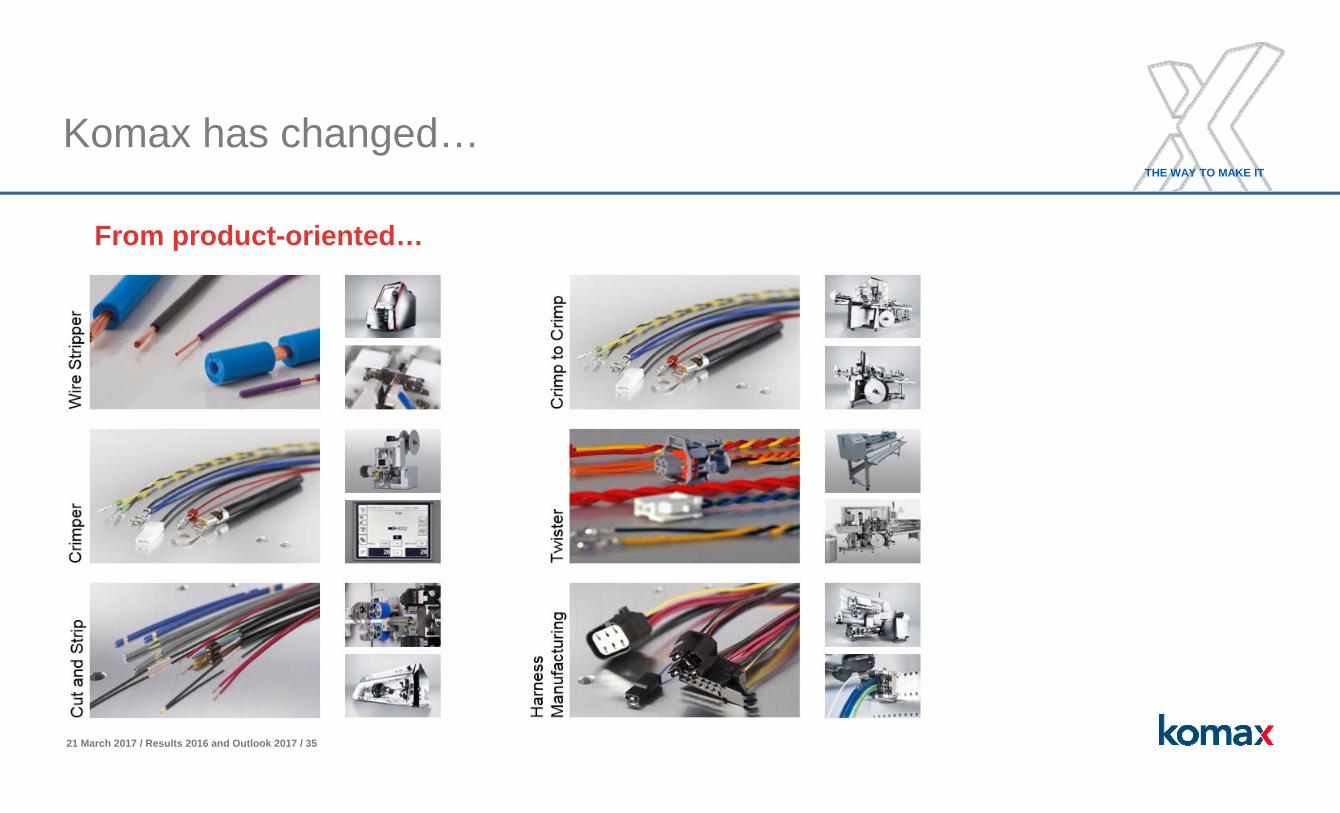

From product-oriented…

Komax has changed…

21 March 2017 / Results 2016 and Outlook 2017 / 36

THE WAY TO MAKE IT

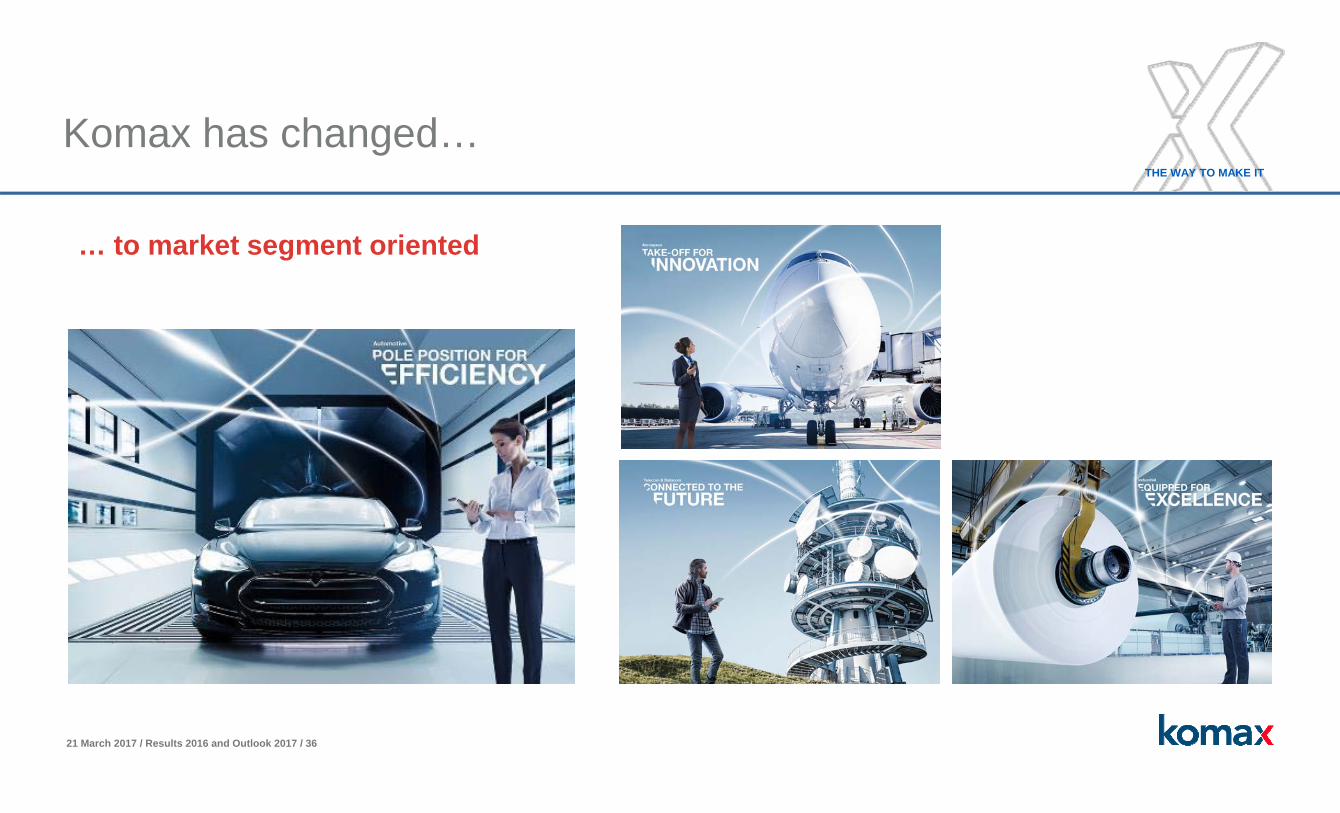

Komax has changed…

… to market segment oriented

21 March 2017 / Results 2016 and Outlook 2017 / 37

THE WAY TO MAKE IT

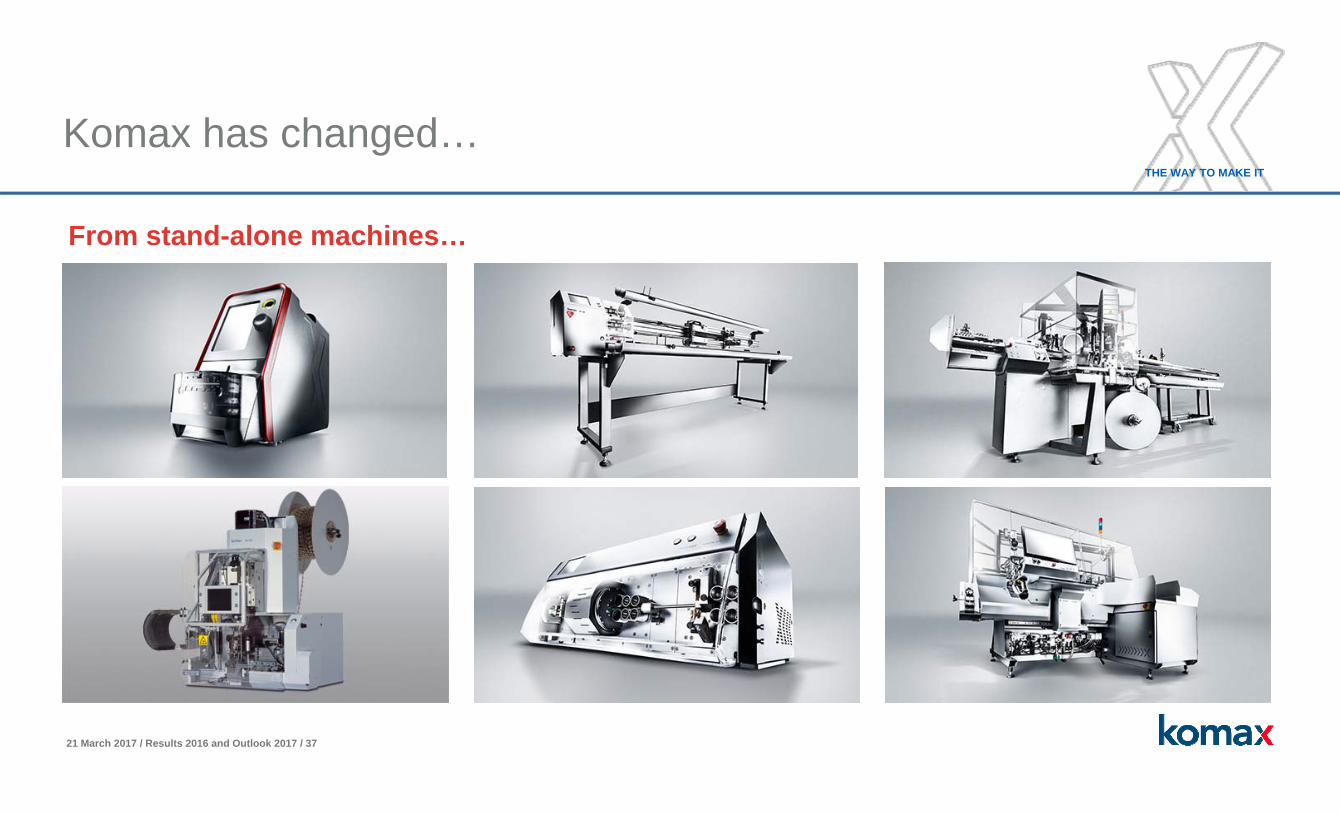

Komax has changed…

From stand-alone machines…

21 March 2017 / Results 2016 and Outlook 2017 / 38

THE WAY TO MAKE IT

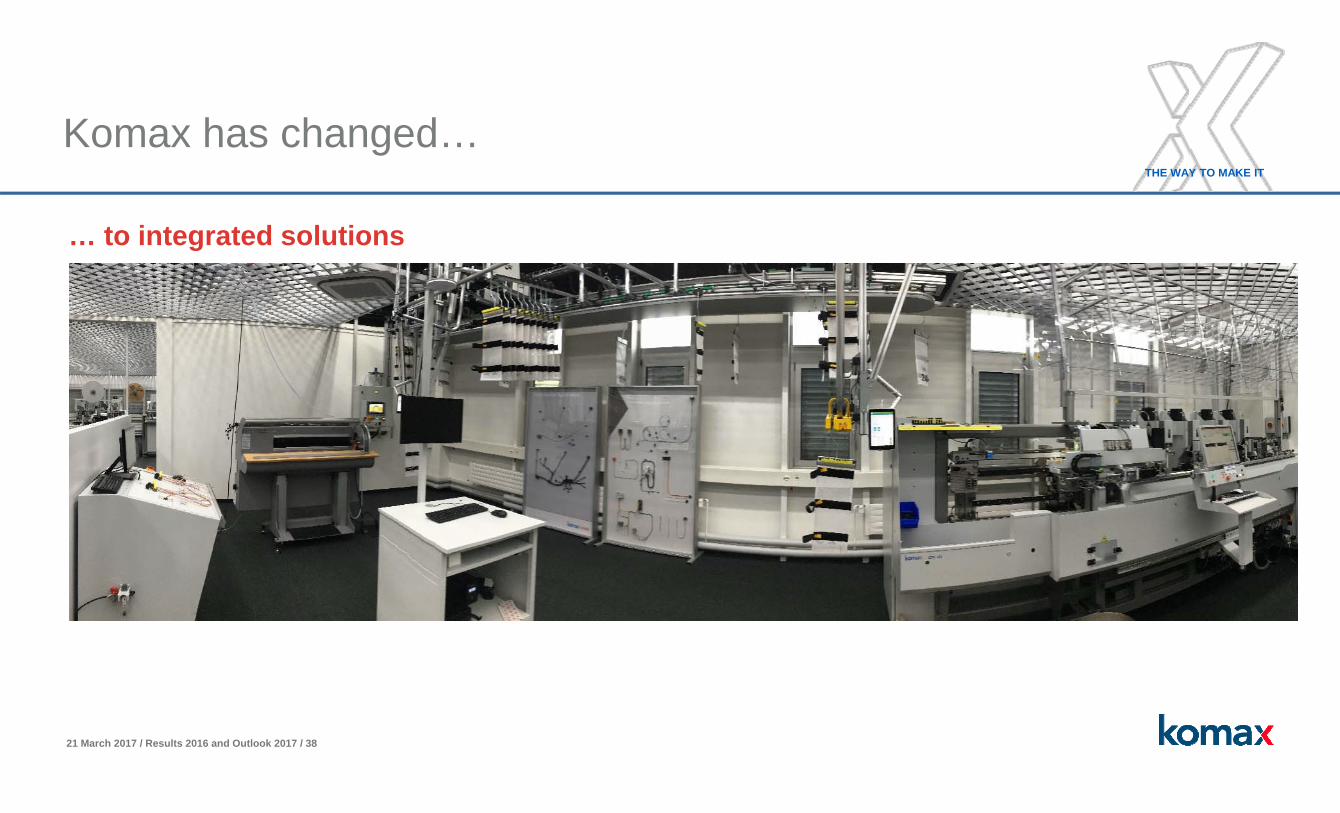

Komax has changed…

… to integrated solutions

21 March 2017 / Results 2016 and Outlook 2017 / 39

THE WAY TO MAKE IT

Komax has changed…

From capital goods…

21 March 2017 / Results 2016 and Outlook 2017 / 40

THE WAY TO MAKE IT

Komax has changed…

… to services

21 March 2017 / Results 2016 and Outlook 2017 / 41

THE WAY TO MAKE IT

Agenda

2016 financial year

Operational performance

Financial performance

Focus on core market (wire)

Focus and outlook 2017

Questions

21 March 2017 / Results 2016 and Outlook 2017 / 42

THE WAY TO MAKE IT

Focus 2017

Integration of acquired companies and exploitation of synergy potential

Innovation (launch of various new products)

Digital transformation • Introduction of global ERP system• Industry 4.0

Start of work on newbuild in Dierikon (scheduled for H2 2017)

Implementation of 2017–2021 strategy

21 March 2017 / Results 2016 and Outlook 2017 / 43

THE WAY TO MAKE IT

2017–2021:Ambitious targets, attractive dividend policy

CHF

500–600million

CHF

80–100million

Avg. 25% 50–60%of EAT

Revenues EBIT RONCE Payout

2021 2021 2017–2021 2017–2021

21 March 2017 / Results 2016 and Outlook 2017 / 44

THE WAY TO MAKE IT

Outlook Komax Group

The Komax Group is very well positioned, and is confident of achieving a result in the 2017 financial year that is in line with its strategic targets for 2017–2021.

After the first two months of 2017, we expect momentum in the automotive industry to remain strong, and anticipate that demand for automation solutions for wire processing will remain high. The above applies only if the political and global economic framework remains stable.

21 March 2017 / Results 2016 and Outlook 2017 / 45

THE WAY TO MAKE IT

Contact / Financial calendar

Financial calendarContact

Roger MüllerIndustriestrasse 66036 DierikonSwitzerlandPhone +41 41 455 06 [email protected]

www.komaxgroup.com

Annual General Meeting 12 May 2017Dividend payment 18 May 2017Half-year results 2017 24 August 2017First Information on the year 2017 23 January 2018Annual media andanalyst conference on the2017 financial results 20 March 2018Annual General Meeting 19 April 2018

21 March 2017 / Results 2016 and Outlook 2017 / 46

THE WAY TO MAKE IT

Disclaimer

This presentation contains forward-looking statements in relation to Komax which are based on current assumptions and expectations. Unforeseeable events and developments could cause actual results to differ materially from those anticipated. Examples include: changes in the economic and legal environment, the outcome of legal disputes, exchange rate fluctuations, unexpected market behaviour on the part of our competitors, negative publicity and the departure of members of management. The forward-looking statements are pure assumptions, made on the basis of information that is currently available.

THE WAY TO MAKE IT

Results 2016 and Outlook 201721 March 2017