Corporate Profits: Profits Before Tax, Profits Tax Liability, and ...

Responsible Partnerships Responsible Partnerships Between ForBetween For‐‐profits and profits and

NonprofitsNonprofits

23nd Annual Statewide Affordable 23nd Annual Statewide Affordable Housing Conference Housing Conference

Florida Housing CoalitionFlorida Housing CoalitionSeptember 21, 2010September 21, 2010

Tim MorganTim MorganDevelopment Partner, The NRP Group LLC, Development Partner, The NRP Group LLC, Cleveland , OhioCleveland , Ohio

David LeonDavid LeonAttorney & CPA, Partner, Broad & Cassel, Attorney & CPA, Partner, Broad & Cassel, OrlandoOrlando

Bob AnsleyBob Ansley, FAICP, FAICPPresident, Orlando Neighborhood Improvement President, Orlando Neighborhood Improvement CorporationCorporation

Types of Partnerships & Joint Types of Partnerships & Joint VenturesVentures

NonprofitNonprofit ForFor‐‐profitprofit

General PartnerGeneral Partner Limited PartnerLimited Partner

CoCo‐‐General PartnerGeneral Partner CoCo‐‐GP; Limited PartnerGP; Limited Partner

LLC Managing MemberLLC Managing Member LLC MemberLLC Member

LLC MemberLLC Member LLC Managing MemberLLC Managing Member

PrincipalPrincipal Contractor (e.g., fee developer)Contractor (e.g., fee developer)

The main issue is the inherent The main issue is the inherent conflict:conflict:

Nonprofit Nonprofit ––guided by charitable purpose with prohibition guided by charitable purpose with prohibition against private benefit against private benefit

ForFor‐‐profit profit ––operates exclusively for private benefit operates exclusively for private benefit (profit)(profit)

MAKING PARTNERSHIPS WORK

Presented By:Tim Morgan

Responsible Partnerships Between For-Profits and Non-Profits

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

NRP Overview

• Industry leading experience and development of over 200 affordable housing developments throughout the United States since 1994.

• NRP has an experienced staff of professionals skilled in planning, development, finance, construction and management.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

NRP Overview

• 65% of NRP developments completed in partnership with non-profit entities.

• Over 4,000 elderly units, 4,000 single family homes and 7,000 multifamily apartments units throughout the United States.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

NRP Overview

• Experienced in wide geographic range from Michigan to Florida and North Carolina to Texas.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Reasons to Joint Venture

• Non-profit set aside for housing tax credits.

• Non-profit knowledge of local politics, soft money availability and approval process.

• Financial strength of the non-profit may be insufficient and lenders/investors may require a financially strong partner to provide appropriate project guarantees.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Reasons to Joint Venture

• For either acquisitions or new development, for-profits may provide “risk capital”.

• Skills, experience and capacity.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Reasons to Joint Venture

• Non-profits may have access to soft money; i.e. City/County/State HOME Funds, PLP program, CRA loans, FHLB, AHP and tax abatement.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Reasons to Joint Venture

• Non-profit may not have in-house development experience.

• Non-profit better understands needs of the neighborhood and market.

• Experience with tenant population.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Selecting the Right Partner

• Honesty, integrity, reputation and chemistry.

• Development expertise.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Selecting the Right Partner

• Financial resources including relationships with lenders and syndicators.

• Housing experience.

• Long-term expectations; i.e. strategic plan.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Selecting the Right For-Profit

• Technical expertise in securing tax credit allocations.

• Reputation for “getting the job done” on time and on budget.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Selecting the Right For-Profit

• Development services capability.

• Financial resources – up front “risk capital”.

• Construction experience and cost control.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Issues Concerning Properly Structuring Relationship

• Fair financial relationship between non-profit and for-profit will ensure long-term success of relationship.

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

Issues Concerning Properly Structuring Relationship

• Developer AgreementFee sharingCash Flow sharingProject reporting/asset managementClearly identify roles and responsibilitiesRisk, guaranteesResidual split

Telephone: 216-475-8900 Fax: 216-584-2505 E-mail: [email protected]

SCENARIO #1

Nonprofit is a 70% General Partner in development.

Nonprofit receives 50% of developer fee.

Nonprofit provides 50% of all risk capital.

Nonprofit owns the project site.

Nonprofit provides 50% of all guarantees required under Limited Partnership Agreement including Operating Deficit Guarantee.

Nonprofit shares in cash flow from project on a 50% (FP) / 50% (NP) basis.

NRP is general contractor.

SCENARIO #1

SCENARIO #2

Nonprofit receives 30% of developer fee.

Nonprofit is a 51% General Partner in development.

Nonprofit provides 30% of all risk capital.

Nonprofit does not own the project site but has excellent relationship with municipality and is designated a CHDO.

Nonprofit provides 30% of all guarantees required under Limited Partnership Agreement including Operating Deficit Guarantee.

Nonprofit shares in cash flow from project on a 70% (FP) / 30% (NP) basis.

NRP is general contractor.

SCENARIO #2

SCENARIO #3

Nonprofit is a 20% General Partner in development.

Nonprofit receives 20% of developer fee.

Nonprofit provides 0% of all risk capital.

Nonprofit does not own the project site and is not a designated CHDO but has strong reputation with local municipality.

SCENARIO #3

Nonprofit provides 20% of all guarantees required under Limited Partnership Agreement including Operating Deficit Guarantee.

Nonprofit shares in cash flow from project on a 80% (FP) / 20% (NP) basis.

NRP is general contractor.

Basic Principles

Basic PrinciplesBasic PrinciplesA.A. Primacy of Charitable PurposePrimacy of Charitable Purpose

501(c)(3) entities must have a charitable purpose.501(c)(3) entities must have a charitable purpose.

Relieving the poor and distressed by providing safe, Relieving the poor and distressed by providing safe, decent affordable housing is a charitable purpose.decent affordable housing is a charitable purpose.

RevRev‐‐Proc 96Proc 96‐‐32 provides a safe harbor for charitable 32 provides a safe harbor for charitable entities to meet, (e.g. 20 % at 50% area median income entities to meet, (e.g. 20 % at 50% area median income (ami) or 40% at 60% ami and 75% at 80% ami overall).(ami) or 40% at 60% ami and 75% at 80% ami overall).

Need to make sure the charitable purpose is met as part Need to make sure the charitable purpose is met as part of the Partnership.of the Partnership.

B.B. Private Benefit and Private InurementPrivate Benefit and Private Inurement

BasicBasic PrinciplesPrinciples

BasicBasic PrinciplesPrinciples

Translation:Translation:

It is better to receive than to giveIt is better to receive than to give.

Basic PrinciplesBasic Principles

B.B. Private Benefit and Private InurementPrivate Benefit and Private InurementIt is better to receive than to give.It is better to receive than to give.

Inurement Inurement ‐‐ officers, directors, substantial officers, directors, substantial contributors.contributors.

Benefit Benefit ‐‐ third party partners, developers, etc. third party partners, developers, etc.

Need to make sure the Partnership does not Need to make sure the Partnership does not confer a Private Benefit on the other partners.confer a Private Benefit on the other partners.

Basic PrinciplesBasic PrinciplesC.C. Specific Directives: LowSpecific Directives: Low‐‐Income Housing Income Housing

Tax Credit (Tax Credit (““LIHTCLIHTC””))

Rules of nonRules of non‐‐profit setprofit set‐‐aside (IRC 42(h)(5))aside (IRC 42(h)(5))

Memorandum for Manager, EO Determinations Memorandum for Manager, EO Determinations ((ChoiChoi Memo)Memo)

Rev. Rul. 2004Rev. Rul. 2004‐‐51, 200451, 2004‐‐22 I.R.B.22 I.R.B.

Basic PrinciplesBasic Principles

C.C. Specific Directives: LIHTCSpecific Directives: LIHTC

Tax rules for nonprofit setTax rules for nonprofit set‐‐aside aside

Ownership (IRC 42(h)(5)(B))Ownership (IRC 42(h)(5)(B))

Material Participation (IRC 469(h) and IRS 8823 Material Participation (IRC 469(h) and IRS 8823 Guide, Chap. 22)Guide, Chap. 22)

Basic PrinciplesBasic Principles

C.C. Specific Directives: LIHTCSpecific Directives: LIHTC

Memorandum for Manager, EO DeterminationsMemorandum for Manager, EO Determinations

(Choi Memo)(Choi Memo)

Basic PrinciplesBasic PrinciplesC.C. Specific Directives: StateSpecific Directives: State

Florida Housing Finance Corporation (Florida Housing Finance Corporation (““FHFCFHFC””) recently ) recently instituted the instituted the ““Priority 1Priority 1”” concept which emphasizes Forconcept which emphasizes For‐‐Profit/NonProfit/Non‐‐Profit partnerships.Profit partnerships.

NonNon‐‐Profit has to own at least 51% of the General Partner Profit has to own at least 51% of the General Partner interest. interest.

NonNon‐‐Profit has to receive at least 25% of the developer fee.Profit has to receive at least 25% of the developer fee.

NonNon‐‐Profit articles must provide for fostering of affordable Profit articles must provide for fostering of affordable housing.housing.

Rev. Rul 2004Rev. Rul 2004‐‐51, 200451, 2004‐‐22 I.R.B.22 I.R.B.

True Sustainability: A New Model to Aid True Sustainability: A New Model to Aid Nonprofits in Developing SelfNonprofits in Developing Self‐‐Sustaining Sustaining Revenue Streams (Revenue Streams (GuideStarGuideStar))

BasicBasic PrinciplesPrinciples

C. Specific Directives C. Specific Directives –– Ad Valorem ExemptionAd Valorem Exemption

Florida Statute 196.1978 Florida Statute 196.1978 –– requires the nonrequires the non‐‐profit to be profit to be the sole general partner.the sole general partner.

Question: How much for how long?Question: How much for how long?

S.B. 360S.B. 360

The City of Weston, Florida, et al. vs. The Honorable Charlie The City of Weston, Florida, et al. vs. The Honorable Charlie Crist, et al. (Leon County Circuit Court)Crist, et al. (Leon County Circuit Court)

Plaintiffs, a coalition of local governments, seek declaratory Plaintiffs, a coalition of local governments, seek declaratory and injunctive relief, challenging Senate Bill 360 as containingand injunctive relief, challenging Senate Bill 360 as containingmore than one subject and constituting an unfunded more than one subject and constituting an unfunded mandatemandate on local governments.on local governments.

BasicBasic PrinciplesPrinciples

C. Specific Directives C. Specific Directives ‐‐ HOME fundingHOME funding

CHDO SetCHDO Set‐‐Aside for Home Funds requires CHDO to Aside for Home Funds requires CHDO to have have ““effective project controleffective project control”” (CFR 92.300(a)(1)).(CFR 92.300(a)(1)).

DecisionDecision‐‐making authority (e.g. Managing Member)making authority (e.g. Managing Member)

BasicBasic PrinciplesPrinciples

D. The Other Side D. The Other Side –– ForFor‐‐Profit partner Profit partner requirements.requirements.

Restrictions on withdrawing from the partnershipRestrictions on withdrawing from the partnership

Obligation for the nonObligation for the non‐‐profit to assist in finding a new profit to assist in finding a new substitute.substitute.

Ability to remove the nonAbility to remove the non‐‐profit partner if it loses its profit partner if it loses its (c)(3) status.(c)(3) status.

Consent rights on various issues which the nonConsent rights on various issues which the non‐‐profit profit otherwise has control over as the 51% general partner.otherwise has control over as the 51% general partner.

The Business Aspects of The Business Aspects of Partnering Partnering –– the Nonprofit Viewthe Nonprofit ViewHave competent legal representation Have competent legal representation all along the way.all along the way.

Memorialize your arrangement earlyMemorialize your arrangement early

•• Start with IRS requirementsStart with IRS requirements

•• Define the decisionDefine the decision‐‐making process making process including veto power, if any. including veto power, if any.

•• Describe the method of communication and Describe the method of communication and frequency of meetingsfrequency of meetings

•• Define the roles of each party. DonDefine the roles of each party. Don’’t forget t forget ““material participationmaterial participation””..

•• Allocate responsibility for costs/expenses.Allocate responsibility for costs/expenses.

•• Define the compensation split and the timing Define the compensation split and the timing of payment.of payment.

•• Include provisions whereby a partner can exit.Include provisions whereby a partner can exit.

When the partners decide to proceed on When the partners decide to proceed on a project, go to formal contract.a project, go to formal contract.

Have competent legal representation all Have competent legal representation all along the way.along the way.

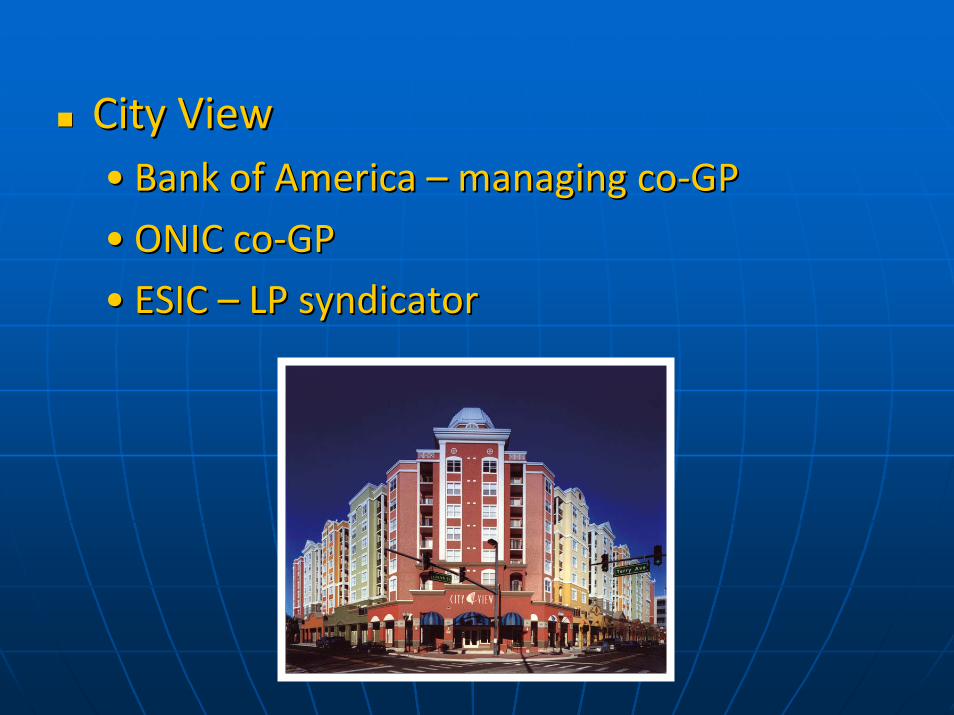

ExamplesExamples

Forest EdgeForest Edge•• ONIC ONIC –– GPGP•• Enterprise (ESIC) Enterprise (ESIC) –– LP syndicatorLP syndicator

City ViewCity View•• Bank of America Bank of America –– managing comanaging co‐‐GPGP•• ONIC coONIC co‐‐GPGP•• ESIC ESIC –– LP syndicatorLP syndicator

2010 Project2010 Project•• ONIC ONIC –– GPGP•• TBA TBA –– LP syndicatorLP syndicator•• NRP Group NRP Group –– Fee developer; general Fee developer; general contractorcontractor

ResourcesResourcesJoint Ventures with ForJoint Ventures with For‐‐Profit Developers. A Guide for Community Profit Developers. A Guide for Community Development Corporations (by LISC)Development Corporations (by LISC)www.lisc.org/content/publications/detail/4957/www.lisc.org/content/publications/detail/4957/

CHDO Survivor Kit, pp. 13CHDO Survivor Kit, pp. 13‐‐17, 5817, 58‐‐6060www.nacced.org/chdokit.pdfwww.nacced.org/chdokit.pdf

IRS Memo on LIHTC JVIRS Memo on LIHTC JV’’sswww.irs.gov/pub/irswww.irs.gov/pub/irs‐‐tege/lihtcp_choimemo_073007.pdftege/lihtcp_choimemo_073007.pdf

IRS Guide for Completing Form 8823, Chapter 22 on material IRS Guide for Completing Form 8823, Chapter 22 on material participation by nonprofitsparticipation by nonprofitswww.novoco.com/low_income_housing/resource_files/irs_regulationswww.novoco.com/low_income_housing/resource_files/irs_regulations_forms/8823_guide_forms/8823_guide

/22/22‐‐1%20Other%20Noncompliance1%20Other%20Noncompliance‐‐Nonprofits.pdfNonprofits.pdf

Info. on IRS Rev. Info. on IRS Rev. RulRul 20042004‐‐51 re Ancillary Joint Ventures51 re Ancillary Joint Ventureshttp://www2.guidestar.org/rxa/news/articles/2005/truehttp://www2.guidestar.org/rxa/news/articles/2005/true‐‐sustainabilitysustainability‐‐aa‐‐newnew‐‐modelmodel‐‐toto‐‐

aidaid‐‐nonprofitsnonprofits‐‐inin‐‐developingdeveloping‐‐selfself‐‐sustainingsustaining‐‐revenuerevenue‐‐streams.aspx?articleId=795streams.aspx?articleId=795