Responses to the Incidental Parameter Problem · Andrew Adrian Yu Pua. Responses to the Incidental...

162

UvA-DARE is a service provided by the library of the University of Amsterdam (http://dare.uva.nl) UvA-DARE (Digital Academic Repository) Responses to the incidental parameter problem Pua, A.A.Y. Link to publication Citation for published version (APA): Pua, A. A. Y. (2016). Responses to the incidental parameter problem General rights It is not permitted to download or to forward/distribute the text or part of it without the consent of the author(s) and/or copyright holder(s), other than for strictly personal, individual use, unless the work is under an open content license (like Creative Commons). Disclaimer/Complaints regulations If you believe that digital publication of certain material infringes any of your rights or (privacy) interests, please let the Library know, stating your reasons. In case of a legitimate complaint, the Library will make the material inaccessible and/or remove it from the website. Please Ask the Library: http://uba.uva.nl/en/contact, or a letter to: Library of the University of Amsterdam, Secretariat, Singel 425, 1012 WP Amsterdam, The Netherlands. You will be contacted as soon as possible. Download date: 31 Jul 2018

Transcript of Responses to the Incidental Parameter Problem · Andrew Adrian Yu Pua. Responses to the Incidental...

UvA-DARE is a service provided by the library of the University of Amsterdam (http://dare.uva.nl)

UvA-DARE (Digital Academic Repository)

Responses to the incidental parameter problem

Pua, A.A.Y.

Link to publication

Citation for published version (APA):Pua, A. A. Y. (2016). Responses to the incidental parameter problem

General rightsIt is not permitted to download or to forward/distribute the text or part of it without the consent of the author(s) and/or copyright holder(s),other than for strictly personal, individual use, unless the work is under an open content license (like Creative Commons).

Disclaimer/Complaints regulationsIf you believe that digital publication of certain material infringes any of your rights or (privacy) interests, please let the Library know, statingyour reasons. In case of a legitimate complaint, the Library will make the material inaccessible and/or remove it from the website. Please Askthe Library: http://uba.uva.nl/en/contact, or a letter to: Library of the University of Amsterdam, Secretariat, Singel 425, 1012 WP Amsterdam,The Netherlands. You will be contacted as soon as possible.

Download date: 31 Jul 2018

In recent years, we have seen an explosion of data collected fromindividuals, firms, or countries across short or long periods oftime. This type of data gives us an opportunity to study thedynamics of change while controlling for time-invariantunobserved heterogeneity. Unfortunately, this type ofheterogeneity, which is usually in the form of individual-specificfixed effects, creates problems for identification, estimation, andinference, especially if we continue to use default procedureswithout modification or without critical exploration. Thisdissertation revolves around a common theme – what practicesand methods can be considered appropriate responses to theincidental parameter problem in panel data models. Myapproach to research is firmly rooted in the examination ofempirical and theoretical practices so that we can come to anunderstanding of what we can and cannot do.

Andrew Adrian Yu Pua (1984) is no stranger to double degrees.He received a BA in Economics and a BSc in Accountancy fromDe La Salle University – Manila (DLSU). He also received amaster’s degree in mathematics from the same institution. Afteraround three years as a faculty member of DLSU, he traveled toEurope to commence postgraduate studies. With the support ofthe European Commission through the Erasmus Mundus scheme,he obtained an MSc Wirtschaftsmathematik from UniversitätBielefeld and a Master Mathématiques Appliquées à l’Economieet à la Finance from the Université Paris 1 Panthéon-Sorbonne.Now, with the support of the same commission, he is about toreceive his PhD in Economics from both the University ofAmsterdam and the Université Catholique de Louvain.

Res

pon

ses

toth

eIn

cide

nta

lPar

amet

erPr

oble

m

Responses to theIncidental Parameter

Problem

Andrew Adrian Yu Pua

Responses to the Incidental Parameter Problem

Dit proefschrift is tot stand gekomen in het kader van EDE-EM (European Doctorate inEconomics – Erasmus Mundus), met als doel het behalen van een gezamenlijk doctoraat. Hetproefschrift is voorbereid aan de Faculteit Economie en Bedrijfskunde van de Universiteit vanAmsterdam en aan de Center for Operations Research and Econometrics van de UniversitéCatholique de Louvain.

La thèse a été préparée dans le cadre du programme doctoral européen EDE-EM (EuropeanDoctorate in Economics – Erasmus Mundus). Cette thèse a été préparée conjointment auFaculteit Economie en Bedrijfskunde, Universiteit van Amsterdam et au Center for OperationsResearch and Econometrics, Université Catholique de Louvain.

This thesis has been written within the framework of the EDE-EM (European Doctorate inEconomics – Erasmus Mundus), with the purpose of obtaining a joint doctorate degree. Thethesis was prepared in the Faculty of Economics and Business at the University of Amsterdamand in the Center for Operations Research and Econometrics at the Université Catholique deLouvain.

Layout and cover design by Andrew Adrian Yu Pua

ISBN 978-94-91030-84-0NUR 916

c© Andrew Adrian Yu Pua, 2016

All rights reserved. Without limiting the rights under copyright reserved above, no part ofthis book may be reproduced, stored in, or introduced into a retrieval system, or transmitted,in any form or by any means (electronic, mechnical, photocopying, recording, or otherwise)without the written permission of both the copyright owner and author of the book.

RESPONSES TO THE INCIDENTAL PARAMETER PROBLEM

ACADEMISCH PROEFSCHRIFT

ter verkrijging van de graad van doctor

aan de Universiteit van Amsterdam

op gezag van de Rector Magnificus

prof. dr. D. C. van den Boom

ten overstaan van een door het College voor Promoties ingestelde

commissie, in het openbaar te verdedigen in de Agnietenkapel

op donderdag 10 maart 2016, te 14:00 uur

door

Andrew Adrian Yu Pua

geboren te Manilla, Filipijnen

Promotiecommissie:

Promotor: Prof. dr. H. P. Boswijk Universiteit van AmsterdamProf. dr. S. van Bellegem Université Catholique de Louvain

Copromotor: Dr. M. J. G. Bun Universiteit van AmsterdamOverige leden: Prof. dr. G. Dhaene Katholieke Universiteit Leuven

Dr. K. J. van Garderen Universiteit van AmsterdamDr. N. P. A. van Giersbergen Universiteit van AmsterdamProf. dr. C. M. Hafner Université Catholique de LouvainProf. dr. S. Khan Duke UniversityProf. dr. F. R. Kleibergen Universiteit van Amsterdam

Faculteit: Economie en Bedrijfskunde

Acknowledgements

I acknowledge the funding and support of the Education, Audiovisual and Cul-ture Executive Agency (EACEA) of the European Union during my stay in Europefrom September 2009 to August 2014. The agency financed both my scholarshipfor the Erasmus Mundus Master Course QEM and my fellowship for the ErasmusMundus Joint Doctorate EDEEM. I also thank my promotor Peter Boswijk for offer-ing a teaching gig that allowed me to stay at the University of Amsterdam until 1February 2016.

I would like to thank six sets of people: my family, my friends, my colleagues,the participants at talks, the support staff, and the nameless future reader.

First, I spent most of my time with colleagues at the University of Amsterdam(UvA) and at the Center for Operations Research and Econometrics (CORE). I thankmy promotors, Peter Boswijk and Sébastien van Bellegem, for all the talks, discus-sions, and the candidness. I also thank Maurice Bun for his patience in going throughthe manuscript. They have decided to trust me and I hope I was able to deliver. Ialso thank my doctoral committee for taking the time to read my manuscript. Theircomments have been useful in rethinking about the approaches I considered in thethesis. Let me also single out members of my doctoral committee – Geert Dhaene,Shakeeb Khan, and Frank Kleibergen, for their support in my job search.

Second, I thank all the people who have attended my talks or listened to my ideas(either forced or of their own volition). Let me single out people who have offeredsome perspective through their comments – Luc Bauwens, Stéphane Bonhomme, Si-mon Broda, Martin Carree, Pavel Cížek, Geert Dhaene, Firmin Doko Tchatoka, Jian-qing Fan, Kees Jan van Garderen, Noud van Giersbergen, Refet Gürkaynak, ChristianHafner, Harry Haupt, Arturas Juodis, Shakeeb Khan, Jan Kiviet, Frank Kleibergen,Thierry Magnac, Michael Massmann, Salvador Navarro, Serena Ng, Cavit Pakel, DalePoirier, Renata Rabovic, Douglas Steigerwald, Martin Weidner, Frank Windmeijer,and Jeffrey Wooldridge. I also thank Roy van der Weide for sharing the data used inChapter 5.

Third, I thank all my friends for their support, even if I am usually not around.Most of my friends are back home in the Philippines and I thank them for makingmy return home so much fun. I also thank the EDEEM cohort for their help in ad-ministrative matters.

Fourth, the support staff at UvA and CORE have made smooth transitions possi-ble. Arnold van Meteren was one of my earliest contacts at UvA. He was responsiblefor facilitating my long-stay visa application in the Netherlands. José Kiss was veryhelpful in facilitating accommodation in Amsterdam and registration at the UvA.Kees Nieuwland made office life smoother by being there for computer-related is-sues. Jolanda Vroons also took his place as IT liaison and was very quick to respond.Evelien Brink, Ana Colic, Wilma de Kruijf, and Robert Helmink are always there to

v

help whenever I would need assistance. Marc van Steekelenburg has been helpfulin dealing with renewing my residence permit. Catherine Germain is possibly one ofthe best multi-taskers I have ever seen in action. She helped in smoothing out mymove to Belgium, dealing with French-speaking authorities, and expediting the finalactivities of the dissertation defense phase. Marie-Hélène Chassagne has also beenvery helpful with these final activities as well. Raphaël Tursis was one of the nicer ITguys I have met. I also thank Caroline Dutry, the only support staff at the coordinat-ing institution of the doctoral programme, for dealing with both administrative andfinance-related issues. The support staff is really the heart of any institution!

Fifth, I thank the reader of this thesis. I hope you enjoy reading this work just asI have enjoyed (though not without heartbreak) working on it. In case you did notnotice, the last few pages of the dissertation are blanks meant for notes.

Finally, I thank my mother for understanding the nature of what I have beendoing for the past years, despite her initial hesitations. I thank my brother and sisterfor being there with my mother in my absence. Although infuriating at times, I wouldlike to thank the cats and our lone dog back in our house, as they have stabilized thehousehold. I thank my better half Stephanie for being one of the constants in mylife.

vi

Contents

1 Introduction 11.1 The promise of panel data . . . . . . . . . . . . . . . . . . . . . . . . . . . . 11.2 Sketching some of the arguments . . . . . . . . . . . . . . . . . . . . . . . 41.3 How should we respond? . . . . . . . . . . . . . . . . . . . . . . . . . . . . 18

2 On IV estimation of a dynamic linear probability model with fixed effects 212.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 212.2 A situation where the LPM is a good idea . . . . . . . . . . . . . . . . . . 232.3 Main results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 25

2.3.1 The case of three time periods . . . . . . . . . . . . . . . . . . . . . 252.3.2 Large-T case . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 28

2.4 Practical implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 302.5 Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 342.6 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 34

3 Simultaneous equations models for discrete outcomes: Coherence andcompleteness using panel data 393.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 393.2 A stylized example . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 41

3.2.1 Coherence and completeness . . . . . . . . . . . . . . . . . . . . . 413.2.2 Why a cross section is not enough . . . . . . . . . . . . . . . . . . 453.2.3 Why panel data may be useful . . . . . . . . . . . . . . . . . . . . 47

3.3 The model . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 483.3.1 Background . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 483.3.2 Identification . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 503.3.3 Estimation and inference . . . . . . . . . . . . . . . . . . . . . . . . 54

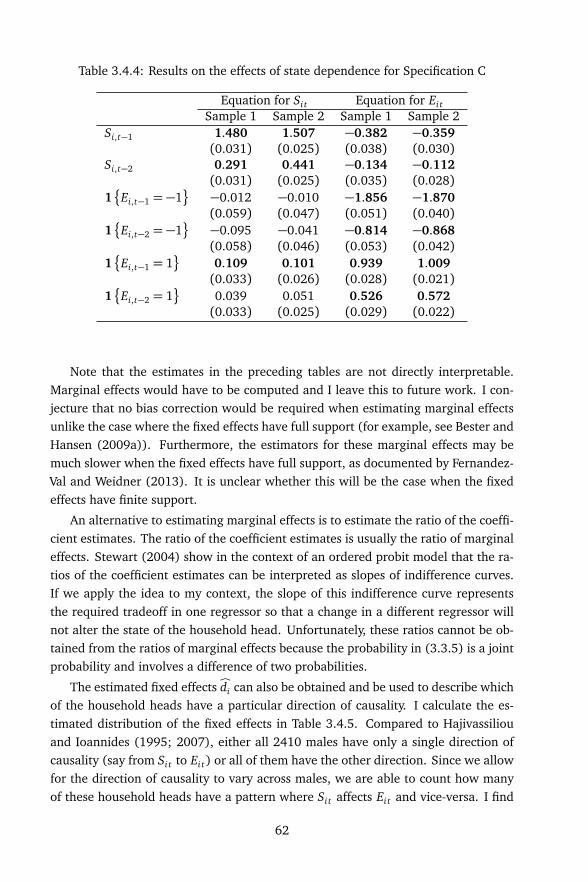

3.4 Revisiting the results of HI (1995; 2007) . . . . . . . . . . . . . . . . . . 573.4.1 Similarities and differences . . . . . . . . . . . . . . . . . . . . . . 573.4.2 Results . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 58

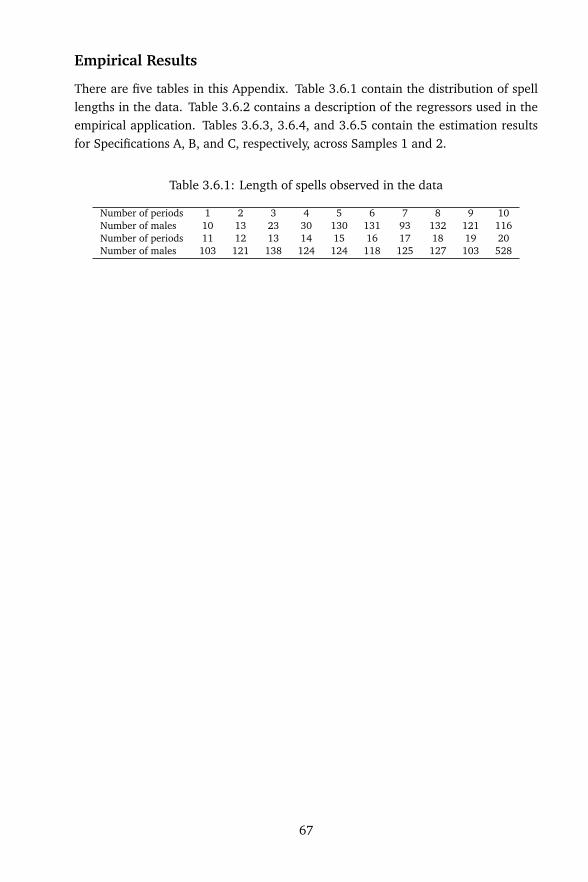

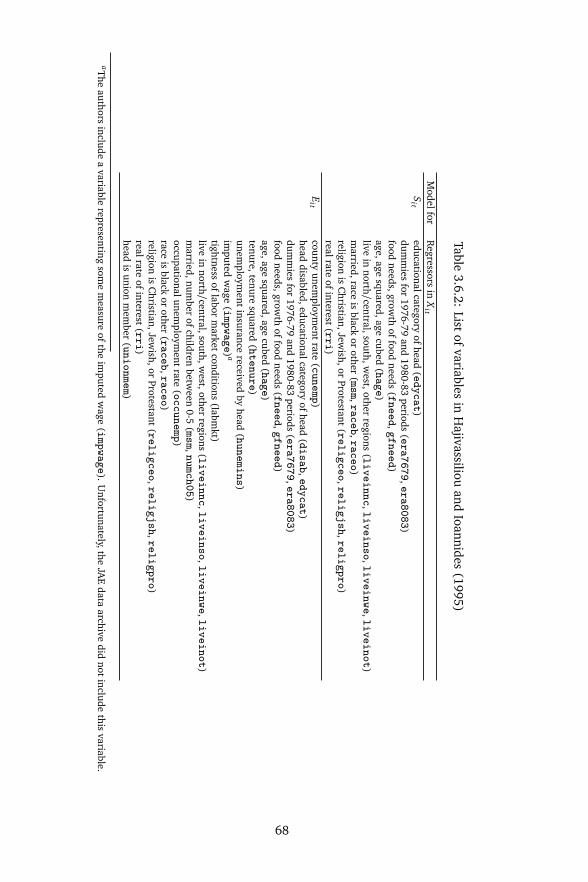

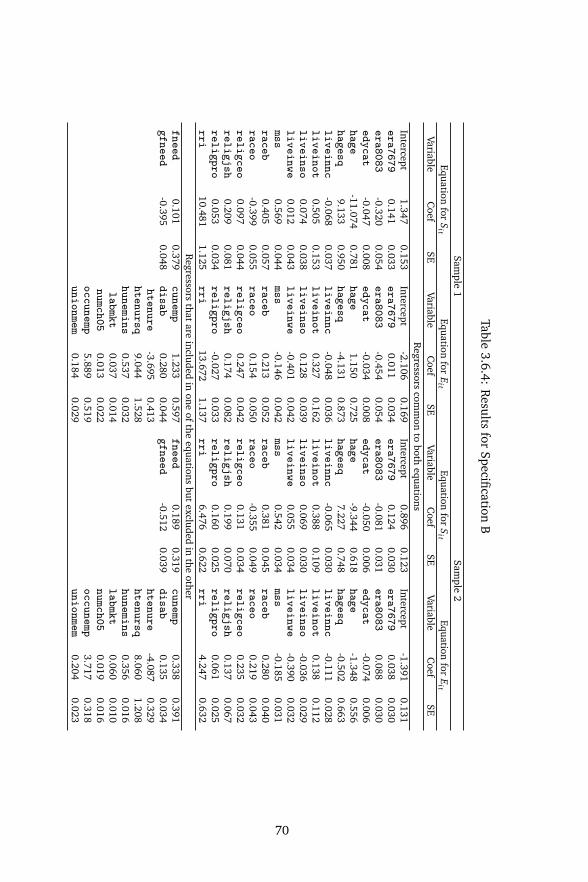

3.5 Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 633.6 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 64

vii

4 Estimation and inference in dynamic nonlinear fixed effects panel datamodels by projection 734.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 734.2 The projection approach . . . . . . . . . . . . . . . . . . . . . . . . . . . . 76

4.2.1 Concept . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 764.2.2 Implications . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 784.2.3 Computation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 804.2.4 Examples . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 83

4.3 Simulations . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 874.4 Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 924.5 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 93

5 The role of sparsity in panel data models 1095.1 Introduction . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1095.2 Panel lasso for the linear model . . . . . . . . . . . . . . . . . . . . . . . . 111

5.2.1 Setup and notation . . . . . . . . . . . . . . . . . . . . . . . . . . . 1115.2.2 Estimation and inference . . . . . . . . . . . . . . . . . . . . . . . . 1145.2.3 Choice of regularization parameter . . . . . . . . . . . . . . . . . . 120

5.3 Monte Carlo . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1225.4 Inequality and income growth . . . . . . . . . . . . . . . . . . . . . . . . . 1255.5 Concluding remarks . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 1275.6 Appendix . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 129

6 Summary 135

Bibliography 137

Nederlandse Samenvatting (Summary in Dutch) 147

viii

Chapter 1

Introduction

1.1 The promise of panel data

In this chapter, I show through a series of examples that panel data offer researchersthree broad but sometimes competing advantages – estimating structural or commonparameters more precisely, allowing for dynamics and feedback, and control of time-invariant unobserved heterogeneity. I am working within usual panel data contextwhere the cross-sectional units i are independently sampled.

Let y ti = (yi1, . . . , yi t) and x t

i = (x i1, . . . , x i t) for i = 1, . . . , n and t = 1, . . . , T . Thevariable yi t is the outcome of interest and x i t is a vector of regressors – both of whichare observable. We are interested in the conditional distribution of the observablesy T

i given x Ti , which is indexed by a finite-dimensional parameter θ . Unfortunately,

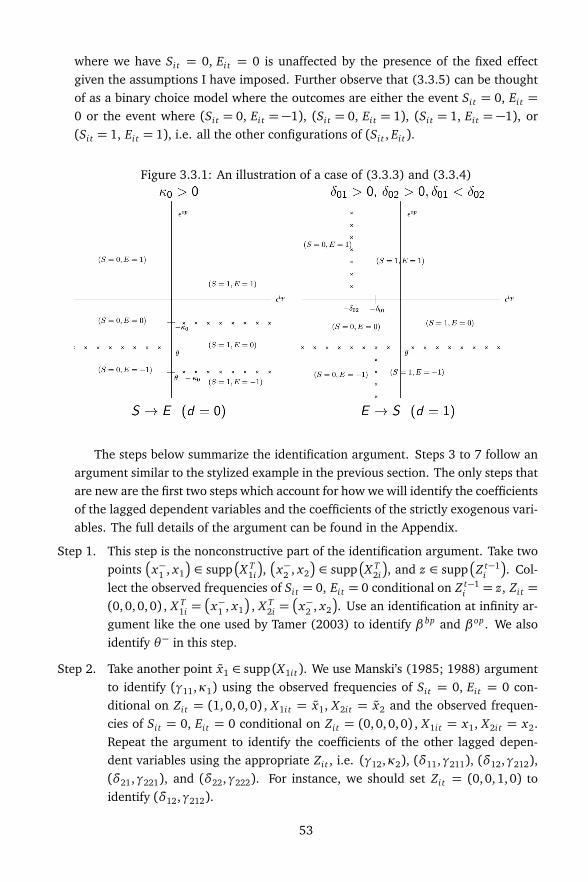

the presence of the unobservable αi , which is an individual-specific effect capturingtime-invariant unobserved heterogeneity potentially correlated with the regressors,obscures our ability to estimate and make inferences about θ . To see this, considera prototypical panel data model where the previously mentioned elements can befound in the following integral equation, i.e.,

f y|x

y Ti |x

Ti ;θ

=ˆ

f y|x ,α

y Ti |x

Ti ,αi;θ

fα|x

αi |x Ti

dαi ,

where f y|x ,α

y Ti |x

Ti ,αi;θ

is a conditional model and fα|x

αi |x Ti

is the distributionof time-invariant unobserved heterogeneity.

The integral equation can be modified can allow for x to be strictly exogenousand for y to have dynamics (where yi1 plays the role of the initial condition), i.e.,

f

yiT , . . . , yi2|yi1, x Ti ;θ

=ˆ

f1

yiT , . . . , yi2|yi1, x Ti ,αi;θ

f2

αi |yi1, x Ti

dαi ,

1

where the integrand is given by

f1

·|yi1, x Ti ,αi;θ

= gT

yiT |x Ti , y T−1

i ,αi

× . . .× g2

yi2|x Ti , yi1,αi

.

The integral equation can also be modified to allow for x to have feedback, i.e.,

f (yiT , . . . , yi2, x iT , . . . , x i2|yi1, x i1;θ )

=ˆ

f1 (yiT , . . . , yi2, x iT , . . . , x i2|yi1, x i1,αi;θ ) f2 (αi |yi1, x i1) dαi ,

where the integrand is given by

f1 (·|yi1, x i1,αi;θ ) = gT

yiT |x Ti , y T−1

i ,αi

hT

x iT |y T−1i , x T−1

i ,αi

× . . .

×g2

yi2|x2i , yi1,αi

h2 (x i2|yi1, x i1,αi) .

It is certainly possible for each of the terms of the above expression to be indexed bysome finite-dimensional parameter θ . Furthermore, it is also possible to have a multi-dimensional fixed effect αi . Note that having the time series dimension providesmore degrees of freedom for which to estimate θ but these degrees of freedom mayget consumed by considering more and more complex models, even if we retain fullyparametric specifications.

A large part of research in panel data econometrics adopts a fully parametricspecification for f y|x ,α while leaving fα|x unspecified (see the surveys by Chamber-lain (1984), Arellano and Honoré (2001), and Arellano and Bonhomme (2011)).Leaving fα|x unspecified is at the core of the fixed-effects approach because one hasto account for sources of heterogeneity not always observed by the econometrician.Since there is scarce guidance from economic theory as to the nature of heterogeneityobserved units should possess, we start with a widely used notion of heterogeneity– that any differences among observed units are relatively stable over time but areallowed to be correlated with the included regressors. Unfortunately, the presenceof individual-specific effects complicates the estimation of common parameters indynamic nonlinear fixed effects panel data models, as we shall see in the exam-ples in the next section. Alternatively, correlated random effects approaches, wheresome aspects of the distribution fα|x are specified, can be beneficial as discussed inExample 1.2.6. In practice, either we impose assumptions on the first and secondmoments of fα|x for linear models or we impose fully parametric assumptions on fα|xfor nonlinear models.

The conditional model with f y|x ,α fully specified can also be used as a startingpoint while treating the αi ’s as parameters to be estimated. In this case, Neymanand Scott (1948) call θ the structural parameter and αi the incidental parameter.The distinguishing feature of parametric statistical models with incidental parame-ters is the presence of a parameter αi that appears in only a finite number of proba-

2

bility distributions (in particular, that of ith cross-sectional unit). Neyman and Scott(1948) have shown that the maximum likelihood estimator (MLE) of θ may not beconsistent in this case.1 This unfortunate consequence of using ML have henceforthbeen referred to as the incidental parameter problem (see Lancaster (2000), Arel-lano and Honoré (2001), and Arellano and Bonhomme (2011) for surveys of somerecent developments).2

More formally, this incidental parameter problem arises because the MLE bθ hasthe following property for fixed T :

bθ = argmaxθ

1n

n∑

i=1

log f y|x ,α

y Ti |x

Ti ,Òαi (θ ) ;θ

(1.1.1)

p→ argmax

θ

limn→∞

1n

n∑

i=1

E

log f y|x ,α

y Ti |x

Ti ,Òαi (θ ) ;θ

6= argmaxθ

limn→∞

1n

n∑

i=1

E

log f y|x ,α

y Ti |x

Ti ,αi

(1.1.2)

Note that in (1.1.1), we have substituted an estimator of αi . Hence, the right handside of (1.1.1) is called the profile or concentrated likelihood. Plugging in an es-timator for a finite-dimensional nuisance parameter usually has an asymptoticallynegligible effect on the estimator for the parameter of interest. In contrast, when wesubstitute an estimator Òαi (θ ) for αi in (1.1.1), there is an asymptotically nonnegli-gible effect. The inconsistency of bθ can be traced to four interrelated reasons: (a)the parameter space grows with n, (b) the finite sample bias of bθ that does not dis-appear in the limit as seen in (1.1.2), (c) the profile or concentrated likelihood doesnot correspond to a joint density of the observables, and (d) the profile score, whichis the derivative of the profile log-likelihood with respect to θ , is not necessarily anunbiased estimating equation. Since these reasons are interrelated, general purposesolutions (some of which are surveyed from an econometrics perspective by Arellanoand Hahn (2007) along with its references and from the statistics perspective by Reid

1They also show using the example of estimating a normal mean with variances as incidental parame-ters that sometimes the MLE can be consistent but is no longer asymptotically efficient. They also proposea bias-adjustment method in the spirit of a profile score adjustment. Finally, they sketch the efficiencylosses resulting from the incidental parameter problem.

2It would seem that treating αi ’s as random variables (or random effects) and treating αi ’s as parame-ters are not different from each other. The former subsumes the usual random effects specification wherefα|x = fα. Leaving fα|x unspecified is sometimes called the fixed-effects approach. These two modelsgenerate estimators that actually have different distribution theories. Sims (2000) argues that “there is arandom effects distribution theory for the fixed effects estimator and vice versa.” The measurement errorliterature has been much more explicit about this distinction with respect to its treatment of the latentvariable representing the true value of the measurement. The two models are called structural and func-tional, respectively. See Moran (1971) for more details. Semiparametric estimation and efficiency theoryhas also been explicit with respect to the distinction. See Moran (1971), Bickel and Klaassen (1986),Bhanja and Ghosh (1992a; 1992b; 1992c), Bickel, Klaassen, et al. (1993), and Pfanzagl (1993) for moredetails.

3

(2013), which contain some of the different likelihoods available in the literature)will tend to focus on directly addressing one of these four reasons.

Because the incidental parameter problem is difficult to handle for many non-linear panel models, some approaches that weaken the fixed-effects approach havebeen proposed. Typically, the search for consistent estimators of common parametersdepends on a set of auxiliary assumptions. Assumptions include, but are not limitedto, correlated random effects strategies where the αi ’s are drawn from a known fα|x(a particular approach involving sparsity is explored in Chapter 5), fixed-T or large-T bias corrections that exploit full specification of f y|x ,α (some of which are exploredfurther in Chapter 4), and approaches invoking discrete support for fα|x (exploredfurther in a simultaneous equations context in Chapter 3). The next four chapters ofthis dissertation provide specific theoretical or empirical situations for which theseauxiliary assumptions may be appropriate (or inappropriate as will be seen in Chap-ter 2). Before discussing the rest of the thesis, I first discuss the incidental parameterproblem in more detail using seven examples.

1.2 Sketching some of the arguments

In this section, I consider some examples that demonstrate the theoretical and prac-tical relevance of the incidental parameter problem along with some proposed solu-tions. Example 1.2.1 is the many normal means problem posed in Neyman and Scott(1948) where the parameter of interest is the common variance of the observations.The MLE in this example is inconsistent and model-specific solutions are proposedto remedy this inconsistency.

Example 1.2.2 reconsiders the solutions in Example 1.2.1 when both n, T →∞.Next, Example 1.2.3 is an illustration of the more general case where the O

T−1

incidental parameter bias is characterized so that we can pursue a general purposesolution. The model-specific nature of fixed-T solutions is further explored in Exam-ples 1.2.4 and 1.2.5. Sometimes these structural parameters are not of main interestand we want to determine how to recover average marginal effects. Example 1.2.6contains a discussion of how this can be accomplished in fixed-T and large-T sit-uations. Finally, I consider situations where fα|x has discrete support in Example1.2.7.

Example 1.2.1. (Neyman and Scott (1948), Waterman (1993), and Hahn and Newey(2004)) Let yi t be iid draws from a N

αi0,σ20

distribution for i = 1, . . . , n andt = 1, . . . , T . The parameter of interest in this classic example is the variance param-eter σ2

0. The model allows for one individual-specific effect and does not contain anytime-varying regressors. The log-likelihood for one observation is given by

log f

yi t ;αi ,σ2

= −12

log 2π−12

log σ2 −(yi t −αi)

2

2σ2.

4

The MLE satisfies the following first order conditions obtained by taking the deriva-tive of the log-likelihood with respect to σ2 and αi:

∑

i

∑

t

−1

2σ2+(yi t −αi)

2

2σ4

= 0, (1.2.1)

∑

t

yi t −αi

σ2

= 0.

Profiling out the αi ’s using the second equation above gives

Òαi

σ2

=1T

∑

t

yi t = yi . (1.2.2)

Note that (1.2.2) is written as a function of σ2 even though σ2 does not explicitlyappear in the expression for this simple setup. In general, however, the profiled αi

is going to depend on the structural parameter. Substituting this into (1.2.1) andsolving for σ2 gives

cσ2 =1

nT

∑

i

∑

t

(yi t − yi)2 . (1.2.3)

Note that (1.2.2) does not depend on σ20 and both (1.2.2) and (1.2.3) are available

in closed form. The normality and independence assumptions imply that

Òαi

σ2

= yi ∼ N

αi0,σ20/T

.

Results from normal theory (applied to time series observations for the ith crosssectional unit) allow us to conclude that

∑

t (yi t − yi)2 ∼ σ2

0χ2T−1 for every i. Since

we have independence across i, we can write

∑

i

∑

t

(yi t − yi)2 ∼ σ2

0χ2n(T−1).

Furthermore, taking the expectation of cσ2 gives

Ecσ2 =1

nTE

σ20χ

2n(T−1)

= σ20

1−1T

. (1.2.4)

As a consequence, cσ2 is not an unbiased estimator of σ20 in finite samples.

If we want to determine if this finite sample bias disappears in large samples, wehave to think of the dimensions in which sample sizes could grow, i.e., the consistencyof cσ2 will depend on the asymptotic embedding. When T →∞ and n is fixed, cσ2

is consistent for σ20. When n →∞ and T is fixed, however, cσ2 is inconsistent for

σ20 because of (1.2.4). As a result, the finite sample bias does not disappear even if

n →∞. We can correct the finite-sample bias directly by using the bias-corrected

5

estimator cσ2c =

TT−1

cσ2. The degrees of freedom correction produces an unbiasedand consistent estimator in this case.

The previous example is practically relevant because it is a restricted version of astatic linear panel data model with strictly exogenous covariates. In particular, set-

ting β0 = 0 in the model where yi t |x Ti

iid∼ N

αi0 + β0 x i t ,σ20

produces the previousexample.

Note that the bias in (1.2.4) arises from the finite T setting. One can argue thatwe can view this bias as finite sample bias in the time series dimension broughtabout by our inability to consistently estimate αi . Letting T →∞ while fixing n is asolution for panel data typically encountered in financial (and sometimes macroeco-nomic) situations. In contrast, many existing datasets derived from surveys have alarge-n dimension with a relatively small T . Therefore, a slight change in the asymp-totic scheme may be fruitful.

Example 1.2.2. (Continuation of Example 1.2.1) Let us return to the earlier exam-ple. When both n, T →∞ at some unspecified rate, cσ2 will be consistent for σ2

0.Unfortunately, the limiting distribution of cσ2 may be incorrectly centered. Considerthe limiting distribution of

pnT

cσ2 −σ20

. We have

pnT

cσ2 −σ20

=p

nT

1nT

∑

i

∑

t

(yi t − yi)2 −σ2

0

=p

nT

1nT

∑

i

∑

t

(yi t −αi0 +αi0 − yi)2 −σ2

0

=p

nT

1nT

∑

i

∑

t

(yi t −αi0)2 −σ2

0

︸ ︷︷ ︸

Z1

−p

nT

1n

∑

i

( yi −αi0)2

︸ ︷︷ ︸

Z2

where Z1d→ N

0, 2σ40

as n, T →∞ and

Z2 =s

nTσ2

0

1n

∑

i

yi −αi0

σ0/p

T

2

=s

nTσ2

0

1n

∑

i

χ21

p→ κσ2

0

as n, T →∞ while n/T → κ2 for some finite constant κ > 0.3 As a consequence,we have p

nT

cσ2 −σ20

d→ N

−κσ20, 2σ4

0

3The result depends on sequential asymptotics. Here, we have T →∞ first then n→∞.

6

This example shows that the relative growth rates of the two dimensions influencethe magnitude of the nonzero center −κσ2

0. This nonzero center disappears whenn/T → 0. Otherwise, we can remove the nonzero center as follows:

pnT

cσ2 −σ20

+ Z2 =p

nT

cσ2 −σ20 +

σ20

T

d→ N

0, 2σ40

.

By plugging in a consistent estimator for σ20/T under this asymptotic scheme, we are

able to bias-correct cσ2. The bias-corrected estimator cσ2c = cσ2+cσ2/T will have a lim-

iting distribution that is centered at zero. Interestingly, the asymptotic variance of cσ2c

coincides with the asymptotic variance of cσ2. Finally, note thatEcσ2c = σ

20

1− 1/T 2

.As a result, this corrected estimator is different from the degrees of freedom correc-tion considered in Example 1.2.1 because this corrected estimator is biased for fixedT but it no longer has the O

T−1

bias.

The discussion in Examples 1.2.1 and 1.2.2 provides ways in which we can achieveeither consistency for fixed T or a correctly centered asymptotic distribution whenboth n, T →∞ at rate n/T → κ2. First, we have a closed form solution (1.2.3) forthe MLE of the structural parameter and a complete specification of the density ofthe data. Thus, we can derive the finite-sample distribution of (1.2.3). Second, thebias of the MLE in (1.2.3) also has a closed form and does not depend on αi (see(1.2.4)). In general, these conditions rarely arise so a general characterization of thenonzero center is needed, as seen in the next example.

Example 1.2.3. (Hahn and Newey (2004), Arellano and Hahn (2007), and Hahnand Kuersteiner (2011)) In the previous example, we have seen an indication thatthe bias in the estimator for the parameter of interest in a model with inciden-tal parameters is of order O

T−1

. We can think of this bias as time series finitesample bias and consider again the asymptotic setting where both n, T →∞ andn/T → κ2. This asymptotic setting will allow us to more generally approximatethe asymptotic bias in the estimator and then reduce its impact. Assume that bθis a consistent estimator under this asymptotic setting, i.e. lim

T→∞θT = θ0, where

θT is the large-n, fixed-T limit of some extremum estimator. Further assume thatp

nT

bθ − θT

d→ N (0,Ω). Under these assumptions along with a stochastic expan-

sion of θT , i.e., θT = θ0 + B/T +O

T−2

, we can write

pnT

bθ − θ0

=p

nT

bθ − θT

+p

nT (θT − θ0)

=p

nT

bθ − θT

+p

nTBT+p

nTO

T−2

=p

nT

bθ − θT

+s

nT

B +Os

nT 3

d→ N (Bκ,Ω) . (1.2.5)

7

Note that (1.2.5) is not centered at 0. In the previous example, we were able to derivethat B = −σ2

0. To remove the nonzero center in (1.2.5), we need to characterizeB and its components of this term because a characterization is essential for thepractical purpose of bias reduction and for the theoretical purpose of understandingthe sources of incidental parameter bias.

Hahn and Newey (2004) study the case of static panel data models with strictlyexogenous regressors. In this example, I highlight the general setting consideredby Hahn and Kuersteiner (2011). They show that in panel data models with fully-specified dynamics, the bias term is given by

B = −I −1

limn→∞

1n

n∑

i=1

f V Uαi

E

Vαii t

−12

limn→∞

1n

n∑

i=1

E

Uαiαii t

f V Vi

E

Vαii t

2

!

,

where the components of B involve (a) the information matrix I −1, (b) the cross-covariances of the αi-score Vi t and the αi-derivative of the θ -score Ui t :

4

f V Uαi =

∞∑

l=−∞

Cov

Vi t , Uαii,t−l

,

(c) the autocovariances of the αi-score

f V Vi =

∞∑

l=−∞

Cov

Vi t , Vi,t−l

,

and (d) the expectation of the second αi-derivative matrix of the θ -score, denoted byE

Uαiαii t

.5 The other remaining component of B is the αi-derivative of the αi-scoreVi t , denoted by Vαi

i t .The characterization of the nonzero center allows us to develop a bias correction

under large-n, large-T asymptotics. Observe that a feasible version of the correctionrequires us to specify a trimming parameter (called bandwidth) for the infinite sumsthat form B.

Unfortunately, there are negative results with respect to the point identificationof common parameters in fixed-T settings (see Chamberlain (2010)). Honoré andTamer (2006) show that the common parameters of panel data dynamic discretechoice models are only partially identified. Furthermore, bias correction may failto provide improvements in fixed-T settings. Given that the MLE is heavily biasedwithout bias correction (as documented by numerous Monte Carlo experiments inthe literature), it seems advisable to apply these corrections. In general, it is likelythat bias-corrected estimators of the common parameters will be found inside the

4In the linear model with strictly exogenous regressors, this cross-covariance is zero. Once dynamicsare allowed, this cross-covariance is not necessarily zero.

5In the linear model, this expectation is zero regardless of whether the regressors are strictly exogenousor not.

8

identified set. Although no proof of the previous claim exists, we obtain point iden-tification anyway once T becomes very large.

Observe that the examples so far apply to panel data models with strictly ex-ogenous regressors and variables with fully-specified feedback mechanisms. On theother hand, GMM based estimation of linear dynamic panel data methods in the spiritof Arellano and Bond (1991) can in principle allow for regressors whose dynamicsare not fully modeled. Unfortunately, these GMM estimators also have an asymptoticdistribution with a nonzero center under large-n, large-T asymptotics (see Alvarezand Arellano (2003)). Furthermore, these GMM estimators have been documentedto have poor finite sample performance and are susceptible to weak instruments (seeBun and Sarafidis (2015) and its references).

It should not be surprising that there is no uniformly good solution to the inci-dental parameter problem that would apply to every theoretical or empirical situa-tion. As a result, it helps to look for solutions on a case-by-case basis. One possibleapproach is to exploit the properties of the chosen parametric family to develop abias-correction. For instance, in Example 1.2.1, consider transforming the data yi t

into yi t − yi . The transformation allows us to eliminate the αi ’s because the distribu-tion of the transformed data only depends on σ2

0. As a result, the likelihood functionformed from the transformed data can be used to conduct estimation and inferencefor σ2

0. The resulting likelihood is called a marginal likelihood in the statistical lit-erature.6 Yet, it may be very difficult to find transformations or even subsets of thedata that will allow us to construct a marginal likelihood. Despite this, there are suc-cessful applications of this idea even outside the likelihood setting as the followingexample illustrates.

Example 1.2.4. (Honoré, 1992) Consider a linear panel data regression model wherey∗i t = αi + β x i t + εi t for i = 1, . . . , n and t = 1, 2. For simplicity, assume that x i t isscalar. Assume that

y∗i1, x i1, y∗i2, x i2

: i = 1, . . . , n

form a random sample but weonly get to observe data on both y and x when y∗i1 > 0 and y∗i2 > 0. Further assumethat εi1 and εi2 are independent, identically and continuously distributed conditionalon (x i1, x i2,αi) for all i.

Honoré (1992) develops a semiparametric approach in the spirit of a marginallikelihood calculation. The idea is to look for a subset of

y∗i1, y∗i2

: y∗i1 ∈ R, y∗i2 ∈ R

6Some authors call the likelihoods obtained after integrating out the nuisance parameters as marginallikelihoods. See Chamberlain (1980) for an example. To avoid confusion, I will call them integratedlikelihoods instead. In contrast, we obtain profile likelihoods by maximizing out the nuisance parameters.These two likelihoods represent different ways of eliminating nuisance parameters (see Basu (1977) andBerger, Liseo, and Wolpert (1999) for more details). The meaning of marginal likelihood I use fits withthe notion of marginal inference. See Kalbfleisch and Sprott (1970) and Christensen and Kiefer (2000) formore details. A more recent discussion on the types of likelihood functions can be found in Reid (2013).

9

that is unaffected by truncation. Observe that such a subset allows us to eliminateαi by differencing. In other words, we have y∗i1 = yi1 , y∗i2 = yi2 and both timeseries observations obey yi t = αi+β x i t+εi t . Notice that this differencing strategy isexactly the same strategy applied to a linear panel data model (as in Example 1.2.1).

Define ∆yi = yi1 − yi2, ∆x i = x i1 − x i2, and ∆εi = εi1 − εi2. Assume thatβ∆x i > 0. Consider the following sets

A =

y∗i1, y∗i2

: y∗i1 > β∆x i , y∗i2 > y∗i1 − β∆x i

,

B =

y∗i1, y∗i2

: y∗i1 > β∆x i , 0< y∗i2 < y∗i1 − β∆x i

.

Notice that whenever y∗i1 > β∆x i , we must have y∗i2 > 0. Observe that

Pr

y∗i1, y∗i2

∈ A|x i1, x i2,αi

= Pr

y∗i2 − y∗i1 > −β∆x i , y∗i2 + y∗i1 > β∆x i |x i1, x i2,αi

= Pr (εi2 − εi1 > 0,εi2 + εi1 > −2αi − 2β x i2|x i1, x i2,αi)

= Pr

∆εi < 0|x i1, x i2,αi ,εi2 + εi1 > −2αi − 2β x i2︸ ︷︷ ︸

Di

×Pr (Di |x i1, x i2,αi) .

Similarly, we can write

Pr

y∗i1, y∗i2

∈ B|x i1, x i2,αi

= Pr

y∗i2 − y∗i1 < −β∆x i , y∗i2 + y∗i1 > β∆x i |x i1, x i2,αi

= Pr (εi2 − εi1 < 0,εi2 + εi1 > −2αi − 2β x i2|x i1, x i2,αi)

= Pr (∆εi > 0|x i1, x i2,αi , Di)Pr (Di |x i1, x i2,αi)

Under the assumption that the distribution of ∆εi conditional on εi1 + εi2 and on(x i1, x i2,αi) is symmetric and unimodal around zero,7 we can then conclude that

Pr

y∗i1, y∗i2

∈ A|x i1, x i2,αi

= Pr

y∗i1, y∗i2

∈ B|x i1, x i2,αi

.

Furthermore, these two sets are unaffected by truncation and will be observable(since these sets satisfy y∗i1 > β∆x i > 0 and y∗i2 > 0). As a result,

Pr ((yi1, yi2) ∈ A|x i1, x i2) = Pr ((yi1, yi2) ∈ B|x i1, x i2) .

Therefore, the union of these two sets

A∪ B = (yi1, yi2) : yi1 > β∆x i , yi2 > 0

7See Honoré (1992) for a sufficient condition.

10

is the basis for constructing a moment condition that only involves the observablesbut not the fixed effect αi . Observe further that

E [1 (yi1, yi2) ∈ A∆εi |x i1, x i2,αi]

=ˆ

1(yi1,yi2)∈Auf∆ε|x1,x2,α,D (u) du

=

ˆ 0

−∞uf∆ε|x1,x2,α,D (u) du

F∆ε|x1,x2,α,D (0)Pr (Di |x i1, x i2,αi)

=

ˆ 0

−∞uf∆ε|x1,x2,α (−u) du

1− F∆ε|x1,x2,α,D (0)

Pr (Di |x i1, x i2,αi)

=−ˆ ∞

0v f∆ε|x1,x2,α (v) dv

1− F∆ε|x1,x2,α,D (0)

Pr (Di |x i1, x i2,αi)

= −E [1 (yi1, yi2) ∈ B∆εi |x i1, x i2,αi] . (1.2.6)

The previous derivation involves the expectation of a truncated random variable andthe i.i.d. assumption on the errors. We use the symmetry assumption to obtain thethird equality. Using (1.2.6), we are able to show that the moment condition

E [1 (yi1, yi2) ∈ A∪ B (∆yi − β∆x i)∆x i]

= E [1 (yi1, yi2) ∈ A∆εi∆x i] +E [1 (yi1, yi2) ∈ B∆εi∆x i]

= E [E [1 (yi1, yi2) ∈ A∆εi∆x i |x i1, x i2,αi]]

+E [E [1 (yi1, yi2) ∈ B∆εi∆x i |x i1, x i2,αi]] (1.2.7)

= 0

is satisfied, where 1 (· ) is the indicator function. The case where β∆x i ≤ 0 is analo-gous and will be part of the criterion function for estimating β . Notice that withoutthe indicator function in (1.2.7), we have the moment condition for β in the staticlinear panel data model with strictly exogenous covariates. A least squares objectivefunction can be formed where the resulting first-order condition is exactly the sampleanalog of (1.2.7).8

Searching for a suitable subset of the data is what makes marginal likelihoodapproaches (or any other approach in the same spirit) highly model-specific. Fur-thermore, assumptions have to be changed in very specific ways to accommodateslight changes in the model. Extensions of the previous example to allow for laggeddependent variables can be found in Honoré (1993) but require a modification of the

8See Honoré (1992) for more details.

11

argument along with the assumptions in the previous example. Abrevaya (1999) pro-poses an estimator for fixed effects models with an unknown transformation of thedependent variable that also has the flavor of a marginal likelihood approach. Strictlyspeaking, the estimators discussed here are semiparametric in nature but the com-mon feature is the search for subsets of the data from which to construct momentconditions or likelihoods that do not depend on αi , but are informative about thestructural parameters. Bonhomme (2012) provides a theory that allows any user ofa likelihood-based panel data model with strictly exogenous regressors to constructmoment conditions that are free of the fixed effects. One can think of the theory as ageneral treatment of the marginal likelihood approach. Unfortunately, it is possiblethat certain panel models will not possess moment conditions that are informative ofthe structural parameters. Aspects of this theory will be discussed further in Example1.2.7.

Yet another approach is to find appropriate conditioning sets so that a conditionallikelihood that does not depend on αi can be constructed. As a result, the score of theconditional likelihood is itself a moment condition that is free of αi . The followingexample illustrates this approach in a dynamic logit model.

Example 1.2.5. (Chamberlain, 1985; Maddala, 1987; Honoré and Kyriazidou, 2000)Consider a dynamic panel logit model with one strictly exogenous regressor. In par-ticular, we have for i = 1, . . . , n and t = 1, . . . , T :

Pr

yi t = 1|x i1, . . . , x iT , yi0, . . . , yi,T−1,αi

=exp

β x i t + γyi,t−1 +αi

1+ exp

β x i t + γyi,t−1 +αi

. (1.2.8)

This means that

Pr

yi t = 0|x i1, . . . , x iT , yi0, . . . , yi,T−1,αi

=1

1+ exp

β x i t + γyi,t−1 +αi

.

Assume that yi0 is observed and T = 3. Hence, we have a total of four observations.Define the sets

A = yi1 = 0, yi2 = 1, yi3 = d3 ,

B = yi1 = 1, yi2 = 0, yi3 = d3 ,

where d3 ∈ 0, 1. Let xi = (x i1, x i2, x i3) and d0 ∈ 0, 1. We can calculate thefollowing conditional probabilities:

Pr (A|xi , yi0 = d0,αi)

= Pr (yi3 = d3|xi , yi0 = d0, yi1 = 0, yi2 = 1)

×Pr (yi2 = 1|xi , yi0 = d0, yi1 = 0)× Pr (yi1 = 0|xi , yi0 = d0)

12

=exp (d3 (β x i3 + γ+αi))1+ exp (β x i3 + γ+αi)

×exp (β x i2 +αi)

1+ exp (β x i2 +αi)

×1

1+ exp (β x i1 + γd0 +αi),

Pr (B|xi , yi0 = d0,αi)

= Pr (yi3 = d3|xi , yi0 = d0, yi1 = 1, yi2 = 0)

×Pr (yi2 = 0|xi , yi0 = d0, yi1 = 1)× Pr (yi1 = 1|xi , yi0 = d0)

=exp (d3 (β x i3 +αi))1+ exp (β x i3 +αi)

×1

1+ exp (β x i2 + γ+αi)

×exp (β x i1 + γd0 +αi)

1+ exp (β x i1 + γd0 +αi).

Choosing A∪ B as a conditioning set and noting that A and B are disjoint sets, thedefinition of conditional probability allows us to write

Pr (A|yi0 = d0, A∪ B,αi)

=Pr (A|xi , yi0 = d0,αi)

Pr (A∪ B|xi , yi0 = d0,αi)

=Pr (A|xi , yi0 = d0,αi)

Pr (A|xi , yi0 = d0,αi) + Pr (B|xi , yi0 = d0,αi), (1.2.9)

Pr (B|yi0 = d0, A∪ B,αi)

= 1− Pr (A|xi , yi0 = d0, A∪ B,αi) . (1.2.10)

Both probabilities in (1.2.9) and (1.2.10) still depend on αi .

Consider first the case where β = 0. Observe that

Pr (A∪ B|xi , yi0 = d0,αi)

=exp (d3 (γ+αi))1+ exp (γ+αi)

×exp (αi)

1+ exp (αi)×

11+ exp (γd0 +αi)

+exp (d3αi)

1+ exp (αi)×

11+ exp (γ+αi)

×exp (γd0 +αi)

1+ exp (γd0 +αi)

=exp (d3αi)exp (αi) [exp (d3γ) + exp (γd0)]

[1+ exp (αi)] [1+ exp (γ+αi)] [1+ exp (γd0 +αi)].

Therefore, we can write (1.2.9) as

Pr (A|yi0 = d0, A∪ B,αi)

=

exp (d3 (γ+αi))1+ exp (γ+αi)

×exp (αi)

1+ exp (αi)×

11+ exp (γd0 +αi)

exp (d3αi)exp (αi) [exp (d3γ) + exp (d0γ)][1+ exp (αi)] [1+ exp (γ+αi)] [1+ exp (γd0 +αi)]

13

=exp (d3γ)

exp (d3γ) + exp (d0γ).

Similarly, (1.2.10) can be written as

Pr (B|yi0 = d0, A∪ B,αi) =exp (d0γ)

exp (d3γ) + exp (d0γ).

Both these conditional probabilities do not depend on αi and can be used to form aconditional likelihood depending only on γ.

Now, consider the case where β 6= 0. Honoré and Kyriazidou (2000) show that byfurther conditioning on the event x i2 = x i3, assumed to have positive probability,we can eliminate the dependence of (1.2.9) and (1.2.10) on αi . In particular, wehave

Pr (A|xi , yi0 = d0, A∪ B, x i2 = x i3,αi) =1

1+ exp (β (x i1 − x i2) + γ (d0 − d3)),

Pr (B|xi , yi0 = d0, A∪ B, x i2 = x i3,αi) =exp (β (x i1 − x i2) + γ (d0 − d3))

1+ exp (β (x i1 − x i2) + γ (d0 − d3))

and a conditional likelihood will be formed from observations where x i2 = x i3 andyi1 + yi2 = 1, i.e., a conditional MLE can be computed from the following optimiza-tion problem:

maxβ ,γ

N∑

i=1

1 yi1 + yi2 = 11 x i2 = x i3 log

[exp (β (x i1 − x i2) + γ (d0 − d3))]yi1

1+ exp (β (x i1 − x i2) + γ (d0 − d3))

.

The condition x i2 = x i3 is unlikely to be satisfied, so a kernel function replaces theindicator function above. Because we introduce a kernel function, the estimatorsfor the structural parameters converge at a rate slower than the usual parametricrate. We also cannot allow for time dummies because they never satisfy x i2 = x i3 bydefinition. Extensions to a semiparametric specification of the probability function(1.2.8) in the spirit of Manski (1987b), the multinomial logit case, and more thanfour observations for every i are available in Honoré and Kyriazidou (2000).

Even though the approaches in Examples 1.2.4 and 1.2.5 are both appealing andinsightful, the search for appropriate transformations of the data or appropriate con-ditioning sets will become cumbersome when T is a bit larger or when we makeslight changes to the model.

Some authors like Wooldridge (2005b) and Arellano and Bonhomme (2011) ar-gue that the structural parameters may not be of primary interest especially for policy.Policy parameters are usually of the form E

m

x Ti ,αi

, where m is some functionof the regressors and unobserved heterogeneity. These policy parameters have beencalled many names depending on the form of m, such as the average structural func-

14

tion (Blundell and Powell, 2004), quantile structural function (Chernozhukov et al.,2013), average index function (Lewbel, Dong, and Yang, 2012), average marginaleffect (Wooldridge, 2005b), and local average response (Altonji and Matzkin, 2005).These policy parameters represent summary measures that describe outcomes of cer-tain thought experiments. One such thought experiment involves a prediction ofwhat m will be when we set x T

i at some fixed value x while holding unobservedheterogeneity constant. Another thought experiment would involve predictions asto how m changes when we change the value x while holding unobserved hetero-geneity constant. Unfortunately, these policy parameters are hard to identify andrequire understanding the tradeoffs among competing assumptions as seen in thenext example.

Example 1.2.6. (Hoderlein and White (2012)) Consider the following nonseparablemodel where Yi t = g (X i t ,αi ,εi t) for i = 1, . . . , n and t = 1,2. An object of interest forpolicy is how E (Yi t |X i1 = x1, X i2 = x2) changes with x1 or x2, holding the source ofunobserved heterogeneity constant. In other words, the policy parameters of interestor average marginal effects at x1 and x2, are given by

M E1 (x1, x2) =ˆ ˆ

∂ g (x1, a, e)∂ x1

fαi ,εi1|X i(a, e|x1, x2) da de,

M E2 (x1, x2) =ˆ ˆ

∂ g (x2, a, e)∂ x2

fαi ,εi2|X i(a, e|x1, x2) da de.

Had we known what fαi ,εi t |X iis, then everything becomes straightforward and calcu-

lating M E1 (x) and M E2 (x) can be done directly. This situation is really the ideabehind the calculation of average marginal effects from fully parametric modelswith correlated random effects proposed by Chamberlain (1984) and Wooldridge(2005b). If we do not know fαi ,εi t |X i

, we have to indirectly recover M E1 (x) andM E2 (x) somehow. In particular, we have the following

E (Yi1|X i1 = x1, X i2 = x2) =ˆ ˆ

g (x1, a, e) fαi ,εi1|X i(a, e|x) da de,

E (Yi2|X i1 = x1, X i2 = x2) =ˆ ˆ

g (x2, a, e) fαi ,εi2|X i(a, e|x) da de,

with four derivatives given by

∂E (Yi1|X i1 = x1, X i2 = x2)∂ x1

= M E1 (x1, x2)

+ˆ ˆ

g (x1, a, e)∂ fαi ,εi1|X i

(a, e|x)∂ x1

da de

∂E (Yi1|X i1 = x1, X i2 = x2)∂ x2

=ˆ ˆ

g (x1,α,ε)∂ fαi ,εi1|X i

(a, e|x)∂ x2

da de

15

∂E (Yi2|X i1 = x1, X i2 = x2)∂ x1

=ˆ ˆ

g (x2, a, e)∂ fαi ,εi2|X i

(a, e|x)∂ x1

da de

∂E (Yi2|X i1 = x1, X i2 = x2)∂ x2

= M E2 (x1, x2)

+ˆ ˆ

g (x2, a, e)∂ fαi ,εi2|X i

(a, e|x)∂ x2

da de

The left hand side of the above derivatives are observable from the data. In con-trast, the right hand side involves objects that are unknown to the econometrician,specifically the distribution of the errors fαi ,εi t |X i

and their associated derivatives∂ fαi ,εi t |X i

/∂ x . To recover M E1 (x1, x2) and M E2 (x1, x2) from the four precedingequations, we have to make further assumptions since there are more unknownsthan the number of equations. It is not enough that we assume a form of time homo-geneity (which ensures that a repeated measurement will be beneficial with respectto controlling for αi), i.e.

fαi ,εi1|X i= fαi ,εi2|X i

because we are still unable to completely remove the distortion caused by the effect ofchanging x1 or x2 on the distribution of the errors. In addition, we have to conditionon the set where X i1 = X i2 = x to completely remove this distortion. As a result, weare able to identify the marginal effects by conditioning on an appropriate set underno assumptions about the nonseparable model and the distribution of the errors(aside from time homogeneity):9

M E1 (x) =∂E (Yi1|X i1 = X i2 = x)

∂ x1−∂E (Yi2|X i1 = X i2 = x)

∂ x1,

M E2 (x) =∂E (Yi2|X i1 = X i2 = x)

∂ x2−∂E (Yi1|X i1 = X i2 = x)

∂ x2.

Without conditioning on X i1 = X i2 = x , there are multiple avenues to recover the av-erage marginal effect. In general, we can only partially identify the average marginaleffect when there are bounds on g (X i t ,αi ,εi t) (see Chernozhukov et al. (2013)).

To avoid conditioning on X i1 = X i2 = x , we may consider correlated randomeffects strategies that use exchangeability (see Altonji and Matzkin (2005) for more)and dimension reduction to construct "instruments" that allow us to nullify the dis-tortions brought about by the effect of changing x on the distribution of the errors.Bester and Hansen (2009b) show that if there exists a sufficient statistic that could re-duce the dimension of the conditioning set X i1 = x1, X i2 = x2, . . . , X iT = xT , thenit is possible to recover the average marginal effect if T ≥ 3. Bester and Hansen(2009b) are actually able to weaken the assumption of time homogeneity in this

9Imposing further restrictions may help in trading off some assumptions for others. The gains will haveto be explored on a case-by-case basis.

16

case. Testing some of these assumptions is the subject of Ghanem (2015).Note that the discussion so far focuses on strictly exogenous regressors. Extend-

ing the ideas to dynamic models are not very straightforward under the conditionsmaintained in the earlier discussion. Bounds for the dynamic model are also avail-able in Chernozhukov et al. (2013). Parametric approaches that fully specify thedistribution of the errors are available in Wooldridge (2005b). Large-T bias correc-tions of marginal effects obtained from parametric fixed-effects models can be foundin Hahn and Newey (2004), Bester and Hansen (2009a), and Fernandez-Val (2009).

In the final example, I show that reducing the support of the distribution of thefixed effects may be helpful in identification of structural parameters. The lack ofpoint identification of structural parameters in nonlinear panel data models has beendocumented by Honoré and Tamer (2006) and Chamberlain (2010) if we leave thedistribution of the fixed effects unspecified. This lack of point identification can alsobe illustrated in the next example.

Example 1.2.7. (Bajari et al. (2011) and Bonhomme (2012)) Consider the followingpanel binary choice model with strictly exogenous regressors x i t :

Pr (yi t = 1|x i ,αi) = H (αi + β x i t) , i = 1, . . . , n; t = 1, . . . , T (1.2.11)

where the distribution of the individual-specific fixed effectαi given x i = (x i1, . . . , x iT )has finite and discrete support, i.e.

Pr (αi = αk|x i = x) = πx ,k, k = 1, . . . , K .

A fixed-effects setup means that we leave the πx ,k ’s unspecified and possibly depen-dent on x . Assume further that the inverse link function H is specified in advance.Since the αi ’s are unobservable, we have to look at the full conditional distributionof yi = (yi1, . . . , yiT ) given x i = x alone. As a consequence of the law of total prob-ability, this full conditional distribution can be written as

Pr (yi = y|x i = x) =K∑

k=1

Pr (yi = y|x i = x ,αi = αk;β)Pr (αi = αk|x i = x) (1.2.12)

for some binary sequence y . The left hand side of (1.2.12) can be recovered fromthe data on frequencies of each of the 2T possible binary sequences. We can collectevery (1.2.12) for each possible binary sequence so that we have a matrix equation

Py|x = Px (β)πx ,

where πx =

πx ,1, . . . ,πx ,K

Tis a K×1 vector, Px (β) is a 2T ×K matrix based on the

17

specification (1.2.11), and Py|x is a 2T×1 vector of conditional probabilities observedfrom the data.

Instead of differencing out every αi which is not generalizable outside linearmodels, we difference out πx by annihilating the matrix Px (β), i.e.

I − Px (β) Px (β)− Py|x =

I − Px (β) Px (β)− Px (β)πx = 0. (1.2.13)

Note that Px (β)− is the Moore-Penrose inverse of Px (β). The main message behind

(1.2.13) is not that it is possible to construct moment conditions that do not dependon αi but that the rank of the matrix Px (β) matters. If we know that K ≥ 2T , then(1.2.13) is not informative of β at all. On the other hand, considering models for thefixed effects for which K < 2T may be useful. We can interpret K < 2T as the supportof the fixed effects being less rich than the support of outcomes. In general, we willnot know whether K < 2T or otherwise. There are empirical situations, such as thegame-theoretic model estimated by Hahn and Moon (2010) and the one discussedin Chapter 3, where we would know the value of K .

In Hahn and Moon (2010), the reduced support of the fixed effects arises becausethe fixed effects represent which of the two pure strategy equilibria is selected byplayers and maintained over time. Further work that allow for time-varying fixedeffects with limited support has been studied by Bonhomme and Manresa (2015).The latter paper and Hahn and Moon (2010) have shown that bias correction in alarge-n, large-T context like we have seen in Example 1.2.3 is not needed at all.

1.3 How should we respond?

The discussion in the previous section comes from a perspective which emphasizeseither the elimination of nuisance parameters or the robustification of estimationand inference methods in the presence of nuisance parameters. Furthermore, thedistribution of the fixed effects is left unspecified as seen in Examples 1.2.1 to 1.2.5.As models become more complicated, this emphasis may become increasingly un-tenable, especially when there is meaning to be attached to nuisance parameters orwhen interest centers on functions of interest and nuisance parameters as seen in Ex-amples 1.2.6 and 1.2.7. Empirically relevant models also have to allow for dynamicsand predetermined regressors. Therefore, we need to search for methods that workin slightly complicated settings at the cost of making assumptions that may never-theless be motivated theoretically or empirically. I now describe the ideas pursuedin the succeeding chapters.

Many empirical situations (see Chapter 2 for examples) call for the estimationof a dynamic binary choice model with fixed effects. In Chapter 2, I demonstratethat it is inappropriate to estimate such a model by applying IV to a dynamic linearprobability model. Motivations behind the use of a dynamic linear probability model

18

include the ability to directly recover average marginal effects and the availabilityof software without additional programming. IV or GMM based estimators of thedynamic linear probability model can also allow for predetermined regressors. Wesaw the difficulties in recovering average marginal effects and allowing for dynamicsin Example 1.2.6. The main results of the chapter actually suggest that IV estimatorsof the linear probability model converge to an average marginal effect with incorrectweighting. Furthermore, this large-n limit might not even be found inside the large-n limit of the bounds proposed by Chernozhukov et al. (2013). In addition, these IVestimators do not converge to the true average marginal effect even as T →∞. As aresult, this chapter gives an example for which dealing with the incidental parameterproblem using IV may not be a good response.

Another empirical situation of interest involves the estimation of simultaneouslydetermined discrete outcomes. Allowing for fixed effects in these models has notbeen explored fully, since most research has focused on either cross-sectional models,continuous outcomes, or random effects (see for example, the research by Cornwell,Schmidt, and Wyhowski (1992), Leon-Gonzalez (2003), Matzkin (2008), Matzkin(2012), and Masten (2015)). Parameter identification in these models is furthercomplicated by the nonexistence of a unique reduced form. One way of partiallyresolving the identification problem is to introduce coherency conditions. Unfortu-nately, the coherency condition needs to be imposed a priori. In Chapter 3, I proposeusing panel data to estimate such models by allowing the data to determine how thecoherency condition will hold. The manner in which the coherency condition holdscan be represented as an incidental parameter that has finite support, in the spirit ofwhat we have seen in Example 1.2.7.

The discussion in Example 1.2.3 is an estimator-based bias correction. One willobserve that papers proposing an analytical correction of the estimator typically mo-tivate the correction using the score. In Chapter 4, I develop a score-based correc-tion involving projections. This approach is a useful and intuitive alternative whenconstructing estimating equations for the structural parameters that are relativelyinsensitive to inconsistent plug-ins. I show that the method can produce familiarestimators in special cases. I also show that projection exploits correct specificationto reap the gains from bias reduction especially when T is very small.

Although the notion of time-invariant heterogeneity is hardly unique, a large gapexists between specifications where we allow for full heterogeneity (i.e., acknowl-edging that all units are different from each other) and full homogeneity (i.e., ac-knowledging that all units are the same). This gap enables us to explore differentnotions of partial pooling. Researchers acknowledge that units might be differentfrom one another yet they may believe that some units are more alike than others.Despite this, they might be unwilling to specify which units are different from eachother and which units are similar to one another. I formalize the preceding intuitionby allowing some incidental parameters to take on the same value, namely zero.

19

In Chapter 5, I demonstrate that some notion of sparsity of the incidental parame-ters may be useful in constructing fixed-T consistent estimators that converge at theroot-n rate. In particular, I tune the lasso (see Tibshirani (1996; 2011) and Chapter5 for more) so that it will be able to detect the non-zero incidental parameters. Asubsample for which the incidental parameters are set to zero can then be used forestimation and inference. This is in contrast to the machine learning and big dataliterature where the main developments have concentrated on uncovering non-zeroeffects in a sea of zero effects.

The four essays included in this thesis demonstrate several different ways to copewith the incidental parameter problem. None of these essays offer a general solution.Instead, these essays provide situations for which the incidental parameter problemmay not be a serious impediment to theoretical and empirical work. However, Irestrict myself to parametric situations and leave the nonparametric situations tofuture research.

20

Chapter 2

On IV estimation of a dynamiclinear probability model withfixed effects

2.1 Introduction

Many researchers still use the dynamic linear probability model (LPM) with fixed ef-fects when analyzing a panel of binary choices. Several applications of the dynamicLPM with fixed effects can be found in papers published in top journals. Applicationsinclude assessing the magnitude of state dependence in female labor force participa-tion (Hyslop, 1999), examining the factors that affect exporting decisions (Bernardand Jensen, 2004), determining the effect of income on transitions in and out ofdemocracy (Acemoglu et al., 2009), and determining how overnight rates affect abank’s decision to provide loans (Jiménez et al., 2014). A more suitable approach,however, is to use limited dependent variable (LDV) models when analyzing discretechoice. Unfortunately, the inclusion of fixed effects creates an incidental parameterproblem that complicates the estimation of average marginal effects, especially whenthe time dimension is small (see the survey by Arellano and Bonhomme (2011)).Resorting to a random effects or correlated random effects approach may requirespecifying the full distribution of the fixed effects and initial conditions1 – some-thing that researchers may be unwilling to do because of the lack of specific subject

1Typically, only the first two moments of the full distribution are required in the case of linear models.In contrast, nonlinear models would typically require the full distribution because we use this distributionto integrate the fixed effects out of the distribution. There are some approaches that can be thought of asbeing in the middle of correlated random effects approaches and fixed-effects approaches. A prominentexample is using a special regressor to consistently estimate common parameters without imposing aparametric assumption on the distribution of the fixed effects and initial conditions, as proposed by Honoréand Lewbel (2002).

21

matter knowledge to construct such a distribution. Linear dynamic panel data meth-ods present an alternative that allows for fixed effects, dynamics, predeterminedregressors, fewer functional form restrictions, and even allow for heteroscedasticity.Therefore, using methods intended for linear dynamic panel data models seems tobe an attractive alternative in this setting.

In contrast, my results provide arguments against a commonly held sentimentamong researchers expressed quite forcefully in Angrist and Pischke (2009, p.107):

The upshot of this discussion is that while a nonlinear model may fit the CEF for LDVsmore closely than a linear model, when it comes to marginal effects, this probably mattersa little. This optimistic conclusion is not a theorem, but, as in the empirical example here,it seems to be fairly robustly true.

Why, then, should we bother with nonlinear models and marginal effects? One answeris that the marginal effects are easy enough to compute now that they are automated inpackages like Stata. But there are a number of decisions to make along the way (e.g.,the weighting scheme, derivatives versus finite differences), while OLS is standardized.Nonlinear life also gets considerably more complicated when we work with instrumentalvariables and panel data. Finally, extra complexity comes into the inference step as well,since we need standard errors for marginal effects.

In this paper, I explain why usual dynamic panel data methods, specifically instru-mental variable (IV) estimation, are inappropriate for estimating average marginaleffects if the conditional expectation function (CEF) is truly nonlinear. In particular,I show the large-n limit of the Anderson-Hsiao (1981; 1982) IV estimator (hence-forth AH) is an average marginal effect but subject to incorrect weighting. Giventhat the AH estimator is a special case of GMM, estimators in the spirit of Arellanoand Bond (1991) may be subject to the same problem. I also show that the effectof this incorrect weighting does not disappear even when T is large. Furthermore,I give examples to show that there are certain parameter configurations and fixedeffect distributions for which the large-n limit of the AH estimator is outside thenonparametric bounds derived by Chernozhukov et al. (2013).

Much research has been done on whether using the LPM is suitable. A particularlyeye-catching example was provided by Lewbel, Dong, and Yang (2012). They show,in a toy example, that OLS applied to the LPM cannot even get the correct sign of thetreatment effect even in the situation where there is just a binary exogenous regressorand a high signal-to-noise ratio. Horrace and Oaxaca (2006) show that the linearpredictor for the probability of success should be in [0,1] for all observations forthe OLS estimator to be consistent for the regression coefficients because the zeroconditional mean assumption does not hold when there are observations (whether inthe sample or in the population) that produce success probabilities outside [0, 1]. Onthe other hand, Wooldridge (2010) argues that "the case for the LPM is even strongerif most the regressors are discrete and take on only a few values". Problem 15.1 ofhis book asks the reader to show that we need not worry about success probabilitiesbeing outside [0, 1] in a saturated model. If we specialize the results in Wooldridge

22

(2005a) and Murtazashvili and Wooldridge (2008) to the LPM, then they show thatfixed-effects estimation applied to the LPM with strictly exogenous regressors canbe used to consistently estimate average marginal effects under a specific correlatedrandom coefficients condition.

I organize the rest of the chapter as follows. In Section 2.2, I present an exampleto show that it is possible to use the LPM to recover an average treatment effect undervery special assumptions that researchers are unwilling to make. In Section 2.3, Iderive analytically the consequences of not meeting these special assumptions wheninterest centers on the average marginal effect of state dependence for the cases ofT = 3 and T →∞. Next, I examine the practical implications of these results using anumerical example and an empirical application on female labor force participationand fertility in Section 2.4. The last section contains concluding remarks followedby a technical appendix.

2.2 A situation where the LPM is a good idea

Suppose we have a two-period panel binary choice model with a strictly exogenousbinary regressor:

Pr (yi t = 1|x i ,αi) = Pr (yi t = 1|x i t ,αi) = H (αi + β x i t) , (2.2.1)

where H : [0,1]→ R is some inverse link function that is increasing, yi t ∈ 0, 1 andx i = (x i1, x i2) = (0,1) for all i = 1, . . . , n and t = 1, 2. Assume that for all i, we haveyi1⊥yi2|x i ,αi .

The regressor x is a strictly exogenous treatment indicator such that all individ-uals are treated in the second period but not in the first period. In other words,specification (2.2.1) is basically a before-and-after analysis. In this setting, αi is anindividual-specific fixed effect drawn from some unspecified density g (α).

Suppose one ignores the binary nature of the outcome variable yi t and one startswith an LPM with fixed effects, i.e., yi t = αi+β x i t+εi t instead. The within estimatorfor β , which is equivalent to the first-difference estimator for T = 2, is then given by

bβ =

1n

n∑

i=1

(yi2 − yi1) (x i2 − x i1)

1n

n∑

i=1

(x i2 − x i1)2

=1n

n∑

i=1

(yi2 − yi1)1 (yi1 + yi2 = 1) =1n(n01 − n10) ,

where 1 (·) is the indicator function. The second equality follows from the defini-tion of x and the implication that yi2 − yi1 = 0 for all i such that yi1 = yi2. Thethird equality follows from defining nab =

∑ni=1 1 (yi1 = a, yi2 = b) as the number

23

of observations for which we observe the sequence ab. Thus, only those i for whichyi1 6= yi2 enter into the calculation of bβ .

When we calculate the large-n limit of the within estimator, we have

bβp→ˆ

Pr (yi2 = 1|x i ,α)Pr (yi1 = 0|x i ,α) g (α) dα

−ˆ

Pr (yi2 = 0|x i ,α)Pr (yi1 = 1|x i ,α) g (α) dα

=ˆ[(1−H (α))H (α+ β)−H (α) (1−H (α+ β))] g (α) dα

=ˆ[H (α+ β)−H (α)] g (α) dα

In the situation I have described, the average marginal effect∆= E [yi2 − yi1|x i = (0, 1)]can be written as:

∆ = E [E (yi2|x i = (0,1) ,α)−E (yi1|x i = (0, 1) ,α)]

= E [E (yi2|x i2 = 1,α)−E (yi1|x i1 = 0,α)] (2.2.2)

= E [H (α+ β)−H (α)] (2.2.3)

Despite the inability of the within estimator to consistently estimate β ,2 the withinestimator does coincide with ∆ even if the true model is nonlinear. In addition, thesample analog of ∆ is exactly the within estimator.

Notice that the result arises because of a lucky coincidence of factors – (a) thestrict exogeneity of x (allowing us to obtain (2.2.2)), (b) the independence of αi

and x i (allowing us to obtain (2.2.3)), and (c) the time homogeneity assumptionbecause H does not depend on time (which follows from (2.2.1)). Despite startingfrom a fixed effects treatment of αi , one has no choice but to assume independenceof αi and x i in order to obtain (2.2.3). This already violates the need to allow forarbitrary correlation between αi and x i . It is as if an omniscient Nature did not usethe knowledge of αi to assign a corresponding treatment vector x i to every unit.

Hahn’s (2001) discussion of Angrist (2001) has already pointed out the specialconditions under which the within estimator is able to estimate an average treatmenteffect. In addition, he emphasizes that the simple strategies suggested by Angrist(2001) require knowledge of the "structure of treatment assignment and careful re-expression of the new target parameter". Chernozhukov et al. (2013) also make thesame point and further show that the within estimator converges to some weightedaverage of individual difference of means for a specific subset of the data. They alsoshow that this weighted average is not the average marginal effect of interest.

2Incidentally, Chamberlain (2010) shows that β is not even point identified in this example unless His logistic. The result of Manski (1987a) does not apply here. He shows that β is identified up to scalewhen one of the strictly exogenous regressors has unbounded support.

24

Despite all these concerns, researchers still insist on estimating LPMs with fixedeffects. One may argue that the example above does not really arise in empiricalapplications but the example already gives an indication that complicated binarychoice models estimated through an LPM are unlikely to produce intended results.In particular, the lucky coincidence of factors mentioned earlier does not hold at allfor the dynamic LPM which I discuss next.

2.3 Main results

2.3.1 The case of three time periods

Consider the following specification of a dynamic discrete choice model with fixedeffects and no additional regressors:

Pr

yi t = 1|y t−1i ,αi

= Pr

yi t = 1|yi,t−1,αi , yi0

= H

αi +ρ yi,t−1

, i = 1, . . . , n, t = 1, 2,3, (2.3.1)

where y t−1i is the past history of y , αi is an individual-specific fixed effect, yi0 is an

observable initial condition, and H : R→ [0, 1] is some inverse link function. Assumethat (yi0, yi1, yi2, yi3,αi) are independently drawn from their joint distribution forall i. I leave the joint density of (αi , yi0), denoted by f , unspecified. This datagenerating process satisfies Assumptions 1, 3, 5, and 6 of Chernozhukov et al. (2013).

If H is the logistic function, thenρ can be estimated consistently using conditionallogit (Chamberlain, 1985). If H happens to be the standard normal cdf, then ρ isnot even point-identified (Honoré and Tamer, 2006).3 In both these cases, we alsocannot point-identify the average marginal effect ∆:

∆=ˆ

Pr

yi t = 1|yi,t−1 = 1,α, y0

− Pr

yi t = 1|yi,t−1 = 0,α, y0

f (α, y0) dαd y0

(2.3.2)even if we know H but leave the density of (yi0,αi) unspecified. This averagemarginal effect is of practical interest because it measures the effect of state de-pendence in the presence of individual-specific unobserved heterogeneity.

Despite these negative results, researchers still insist on using a dynamic LPMon the grounds that linearity still provides a good approximation even if the trueH is nonlinear.4 I use this as a starting point and determine the large-n limit of IVestimators for the dynamic LPM. The linear model researchers have in mind can beexpressed as:

yi t = αi +ρ yi,t−1 + εi t , i = 1, . . . , n, t = 1, 2,3,

3Honoré and Tamer (2006) actually show that the sign of ρ is identified for any strictly increasing cdfH and unrestricted distribution of (yi0,αi).

4The dynamic LPM is really a special case of (2.3.1), where H is the identity function.

25

where εi t = yi t − E

yi t |y t−1i ,αi

. We now take first-differences to eliminate αi:

∆yi t = ρ∆yi,t−1 +∆εi t , i = 1, . . . , n, t = 2,3.

Because the differenced regressor ∆yi,t−1 is correlated with the differenced error∆εi t , IV or GMM estimators have been used to estimate ρ. Using lagged differencesas instruments, the AH estimator can be written as

bρAHd =

∑ni=1∆yi1∆yi3

∑ni=1∆yi1∆yi2

.

Because of the binary nature of the sequences (yi0, yi1, yi2, yi3) : i = 1, . . . , n, it iscertainly possible for some of the first differences to be equal to zero. Therefore,there are only certain types of sequences that enter into the expression above. If weenumerate all these 16 possible sequences, we can rewrite the estimator as

bρAHd =n0110 + n1001 − n1010 − n0101

n0100 + n1010 + n0101 + n1011,

where nabcd =∑n

i=1 1 (yi0 = a, yi1 = b, yi2 = c, yi3 = d) denotes the number of ob-servations in the data for which we observe the sequence abcd.5

It can be shown6 that the large-n limit of bρAHd is

bρAHdp→

ˆH (α) (1−H (α+ρ)) (H (α+ρ)−H (α)) g (α) dα

ˆH (α) (1−H (α+ρ)) g (α) dα

(2.3.3)

=ˆ

wd (α,ρ) (H (α+ρ)−H (α)) dα

=ˆ ˆ

wd (α,ρ)

Pr

yi t = 1|yi,t−1 = 1,α, y0

− Pr

yi t = 1|yi,t−1 = 0,α, y0

dα d y0

where

wd (α,ρ) =H (α) (1−H (α+ρ)) g (α)ˆH (α) (1−H (α+ρ)) g (α) dα

.

Note that the weighting function wd (α,ρ) depends on the true value of ρ and the

5Note that we cannot just drop those sequences for which yi1+ yi2 6= 1, like in conditional logit. If wedo this, the resulting AH estimator becomes

eρAHd =−n1010 − n0101

n0100 + n1010 + n0101 + n1011,