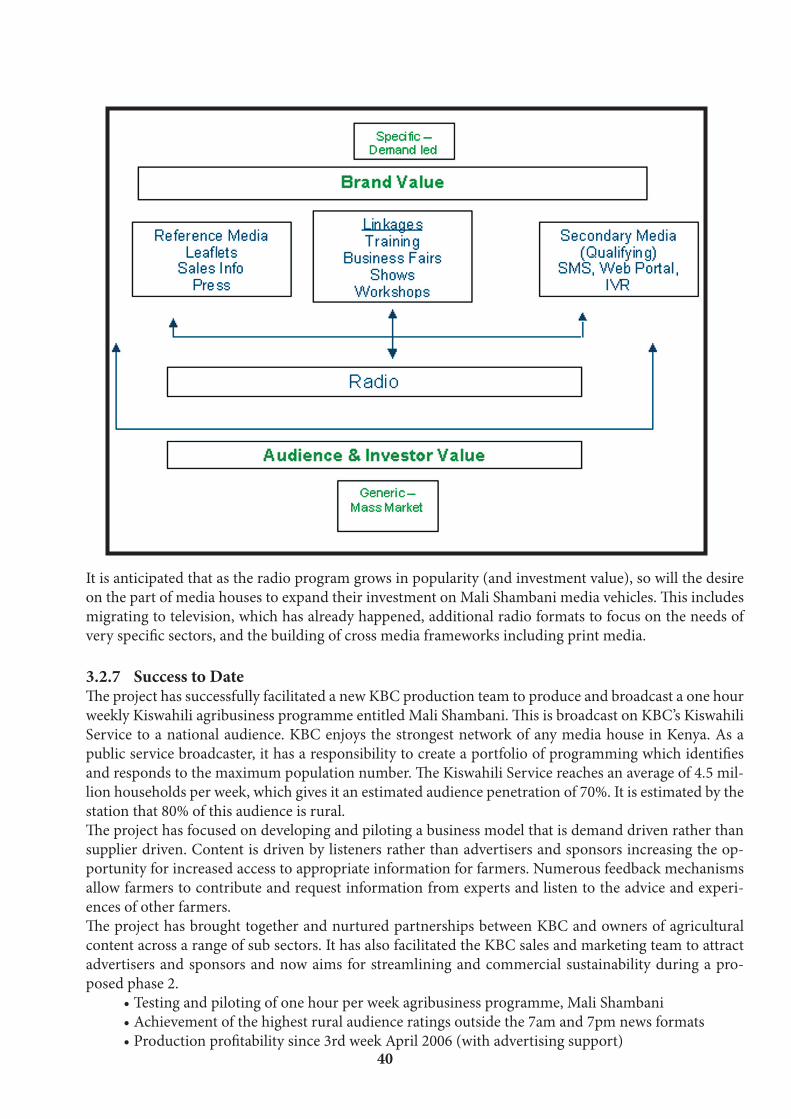

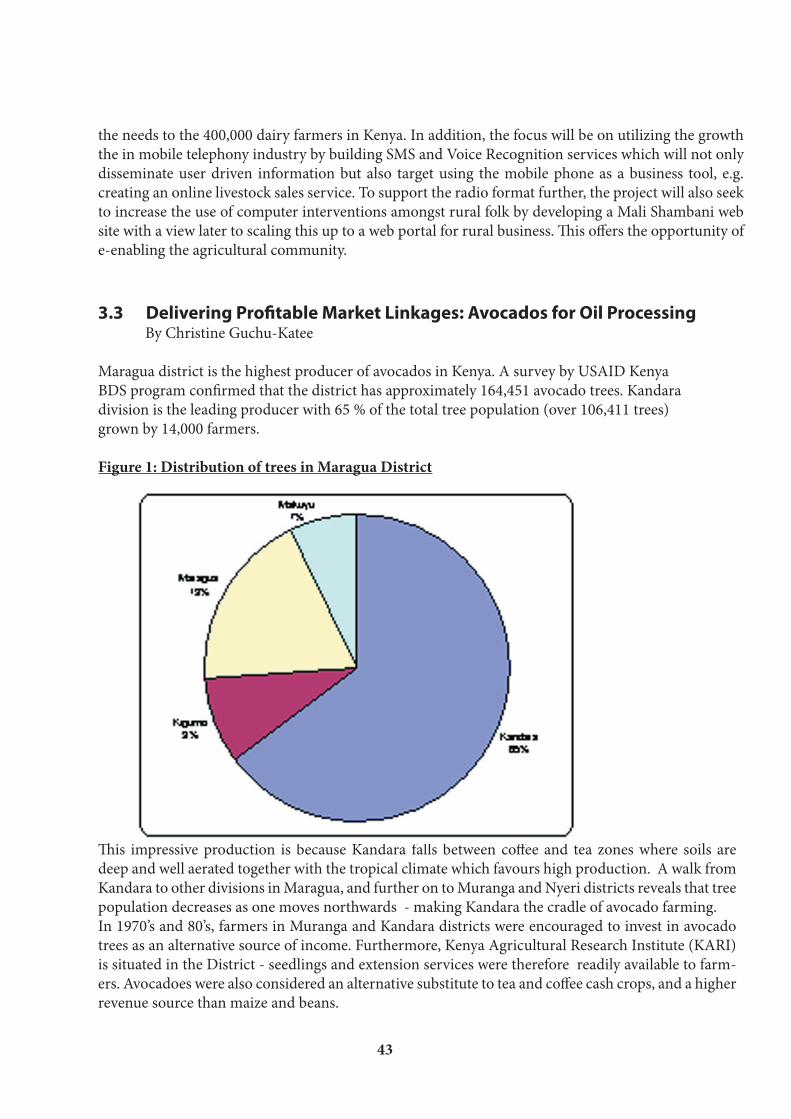

REPORT ON THE 2ND NATIONAL CONFERENCE OF … · REPORT ON THE 2ND NATIONAL CONFERENCE OF THE BDS...

83

REPORT ON THE 2ND NATIONAL CONFERENCE OF THE BDS DONOR COORDINATION GROUP HELD ON: 3RD – 4TH October 2006 VENUE: LAKE NAIVASHA SIMBA LODGE REPORT COMPILED BY: KENYA GATSBY TRUST P.O BOX 44817,00100 GPO NAIROBI. TEL: 020-2720711, 2720703,2720571 Email: [email protected]

Transcript of REPORT ON THE 2ND NATIONAL CONFERENCE OF … · REPORT ON THE 2ND NATIONAL CONFERENCE OF THE BDS...

REPORT ON THE 2ND NATIONAL CONFERENCE OF THE BDS

DONOR COORDINATION GROUP

HELD ON: 3RD – 4TH October 2006VENUE: LAKE NAIVASHA SIMBA LODGE

REPORT COMPILED BY:

KENYA GATSBY TRUSTP.O BOX 44817,00100 GPO

NAIROBI.TEL: 020-2720711, 2720703,2720571

Email: [email protected]

October 31, 2006

Dear Conference Participant:

Re: Second National Conference of the BDS Donor Coordination Group Technical Report

On behalf of the BDS Donor Coordination Group, I am happy to forward you the technical report for the Second National Conference of the BDS Donor Coordination Group, held this 3-4 October at Naivasha Simba Lodge.

This report offers a complete summary of the presentations and discussions which were held duringthe two-day event. In addition, we have included technical papers by each break-out panel presenterwhich provide a more in-depth account of their case study.

Once again, thank you for your active participation at this year’s event.

Sincerely,

David KnoppChair, BDS Donor Coordination Group

TABLE OF CONTENTS ABBREVIATION……………………………………………………………………………………...I CONFERENCE AGENDA....…………………………………………………………………………II PLENARY SESSION ONE: MAKING MARKETS WORK FOR THE POOR: WHAT IT IS AND HOW IT GUIDES PRIVATE SECTOR DEVELOPMENT PROGRAM.…………………….III1 BREAK-OUT SESSION ONE: VALUE CHAIN FINANCING...................................................... 11.0 INTRODUCTION..........................................................................................................................................11.1 COMMODITY CHAIN FINANCING: THE CASE OF HONEY IN KITUI DISTRICT.....................21.1.1 Introduction.....................................................................................................................................................21.1.2 Financial Sector in Kenya...............................................................................................................................21.1.3 The Honey Market Chain in Kitui District..................................................................................................31.1.4 KDA/ABD Response.......................................................................................................................................31.1.5 Actors and Financial Products.......................................................................................................................41.1.6 Conclusion........................................................................................................................................................41.2 USING VALUE CHAIN FINANCING TO MAKE MONEY GROW ON AVOCADO TREES..........51.2.1 Avocado Production in Kenya.......................................................................................................................51.2.2 Constraints to Avocado Production..............................................................................................................61.2.3 Response to these Constraints .......................................................................................................................61.2.4 Lessons Learnt..................................................................................................................................................71.2.5 Challenges Faced.............................................................................................................................................81.2..6 Key Innovations..............................................................................................................................................81.3 MAIZE WAREHOUSE RECEIPTING - AGRICULTURE PRODUCTIVITY AND POVERTY IN KENYA.........................................................................................................................81.3.1 Agriculture Productivity.................................................................................................................................81.3.2 Poverty Assessment in Kenya........................................................................................................................91.3.3 Key Challenges and Constraints to Growth................................................................................................91.3.4 What is Warehouse Receipting?..................................................................................................................111.3.5 Why is Maize Warehouse Receipting Important for Kenya?...................................................................131.3.6 Where is Maize Warehouse Receipting in Kenya?....................................................................................131.3.7 Current Situation...........................................................................................................................................171.3.8 Lessons Learned, Recommendations and the Way Forward...................................................................172 BREAK-OUT SESSION TWO: PRODUCER GROUP DYNAMICS............................................182.0 INTRODUCTION........................................................................................................................................182.1 THE VEGCARE PARTNERSHIP STORY – MATCH MADE IN HEAVEN OR IN A BED WITH THE ENEMY.......................................................................................................................192.1.1 Background....................................................................................................................................................192.1.2 The New Approach – Vegcare .....................................................................................................................212.1.3 Results after the 1st year...............................................................................................................................222.1.4 Farmer selection............................................................................................................................................222.1.5 EUREPGAP Protocols..................................................................................................................................23

2.1.6 Commercially sustainable marketing entity..............................................................................................232.1.7 Partnership.....................................................................................................................................................232.1.8 Conclusion.....................................................................................................................................................232.2 MAKING MONEY THROUGH AVOCADOES.....................................................................................242.2.1 Successes and Challenges of ‘Producer Group’ Linkages with a Lead Export Firm............................242.2.2 Innovative Market Approach.......................................................................................................................242.3 FRESHLINK VMO – BREAKING BARRIERS WITHIN THE HORTICULTURE INDUSTRY......262.3.1 Introduction...................................................................................................................................................262.3.2 Freshlink model............................................................................................................................................272.3.3 Achievements................................................................................................................................................282.3.4 Challenges......................................................................................................................................................282.3.5 Conclusions....................................................................................................................................................292.3.6 Future work....................................................................................................................................................293 BREAK-OUT SESSION THREE: EMERGING METHODS OF BUSINESS SERVICE DELIVERY.....................................................................................................................................303.0 INTRODUCTION........................................................................................................................................303.1 THE BUSINESS HUB APPROACH TO SERVICE DELIVERY.............................................................313.1.1 Introduction...................................................................................................................................................313.1.2 Chilling Plant Model.....................................................................................................................................323.1.3 Muki Dairy Case Analysis............................................................................................................................343.1.4 Replication......................................................................................................................................................343.1.5 Lessons............................................................................................................................................................343.1.6 Results.............................................................................................................................................................353.1.7 Risks in the model.........................................................................................................................................353.2 MALI SHAMBANI – BUSINESS SERVICE DELIVERY THROUGH INTERACTIVE RADIO......363.2.1 Project Background......................................................................................................................................363.2.2 The research phase........................................................................................................................................373.2.3 The Project Model.........................................................................................................................................373.2.4 Monitoring and Evaluation Framework.....................................................................................................383.2.5 Radio Format.................................................................................................................................................393.2.6 Information Integration...............................................................................................................................393.2.7 Success to Date..............................................................................................................................................403.2.8 Key Project Outputs.....................................................................................................................................413.2.9 Challenges/Lessons Learnt..........................................................................................................................423.2.10 The Next Stage...............................................................................................................................................423.3 DELIVERING PROFITABLE MARKET LINKAGES: AVOCADOS FOR OIL PROCESSING.......43

3.3.1 Constraining Factors at the Farmer Level..................................................................................................443.3.2 Marketing Constraints..................................................................................................................................443.3.3 Our Solution: A Profitable Market - Link Business..................................................................................453.3.4 Challenges and Lessons................................................................................................................................483.3.5 Conclusion.....................................................................................................................................................484 BREAK-OUT SESSION FOUR: SECTOR COORDINATION AND POLICY FORMULATION............................................................................................................494.0 INTRODUCTION........................................................................................................................................494.1 ROLE OF COFFEE APEX COMMITTEE IN INFLUENCING POLICY.............................................504.1.1 Background....................................................................................................................................................504.1.2 World Bank Value Chain Analysis..............................................................................................................514.1.3 Formation of the Coffee Apex Committee.................................................................................................514.2 AGRICULTURE POLICY FORMULATION............................................................................................534.2.1 Introduction...................................................................................................................................................534.2.2 Purpose for the Policy...................................................................................................................................534.2.3 Who should be involved...............................................................................................................................544.2.4 Process of policy formulation......................................................................................................................544.2.5 The Case for Coffee.......................................................................................................................................544.2.6 Future Policy Formulation Process.............................................................................................................554.3 KENYA FLOWER COUNCIL: SECTOR COORDINATION AND POLICY FORMULATION....554.3.1 Background Information..............................................................................................................................554.3.2 Main Objectives.............................................................................................................................................574.3.3 Key Activities.................................................................................................................................................574.3.4 Industry Promotions.....................................................................................................................................584.3.5 Capacity Building..........................................................................................................................................584.3.6 Lessons Learnt................................................................................................................................................594.3.7 Challenges.......................................................................................................................................................594.3.8 Conclusions....................................................................................................................................................595 PLENARY SESSION 2: CONFERENCE SYNTHESIS AND REMARKS FROM THE GLOBAL DONOR COMMITTEE........................................................................................606 ANNEXES......................................................................................................................................626.0 LIST OF PARTICIPANTS............................................................................................................................62

ABBREVIATIONS

ABL African Beekeepers LimitedABS African Breeders ServicesABD Agricultural Business Development ASAL Arid And Semi-Arid LandsAVOPP Avocado Oil Processing ProgramBDS Business Development ServicesBSMDP Business Service Marketing Development CBK Central Bank Of KenyaEBA Everything But ArmsESA Eastern And Southern AfricaEPA Economic Partnership AgreementEUREPGAP European Retailers Producer Good Agricultural PracticeGAP Good Agricultural PracticeGDP Gross Domestic ProduceGMO Group Management OfficersIFFP International Fair Flowers And PlantsIFAD International Federation Of Agricultural DevelopmentKEMCAP Kenya Micro Finance Capacity Building ProgrammeKFC Kenya Flower CouncilKMDP Kenya Maize Development ProgrammeKPLC Kenya Power And Lighting CompanyMFI Micro Finance InstitutionsMOU Memorandum Of UnderstandingR&D Research And DevelopmentREAP Rural Enterprise Agribusiness PromotionSACCO Savings &Credit Cooperative SocietySME Small And Micro EnterprisesWTO World Trade Organization

I

ABBREVIATIONS

ABL African Beekeepers LimitedABS African Breeders ServicesABD Agricultural Business Development ASAL Arid And Semi-Arid LandsAVOPP Avocado Oil Processing ProgramBDS Business Development ServicesBSMDP Business Service Marketing Development CBK Central Bank Of KenyaEBA Everything But ArmsESA Eastern And Southern AfricaEPA Economic Partnership AgreementEUREPGAP European Retailers Producer Good Agricultural PracticeGAP Good Agricultural PracticeGDP Gross Domestic ProduceGMO Group Management OfficersIFFP International Fair Flowers And PlantsIFAD International Federation Of Agricultural DevelopmentKEMCAP Kenya Micro Finance Capacity Building ProgrammeKFC Kenya Flower CouncilKMDP Kenya Maize Development ProgrammeKPLC Kenya Power And Lighting CompanyMFI Micro Finance InstitutionsMOU Memorandum Of UnderstandingR&D Research And DevelopmentREAP Rural Enterprise Agribusiness PromotionSACCO Savings &Credit Cooperative SocietySME Small And Micro EnterprisesWTO World Trade Organization

II

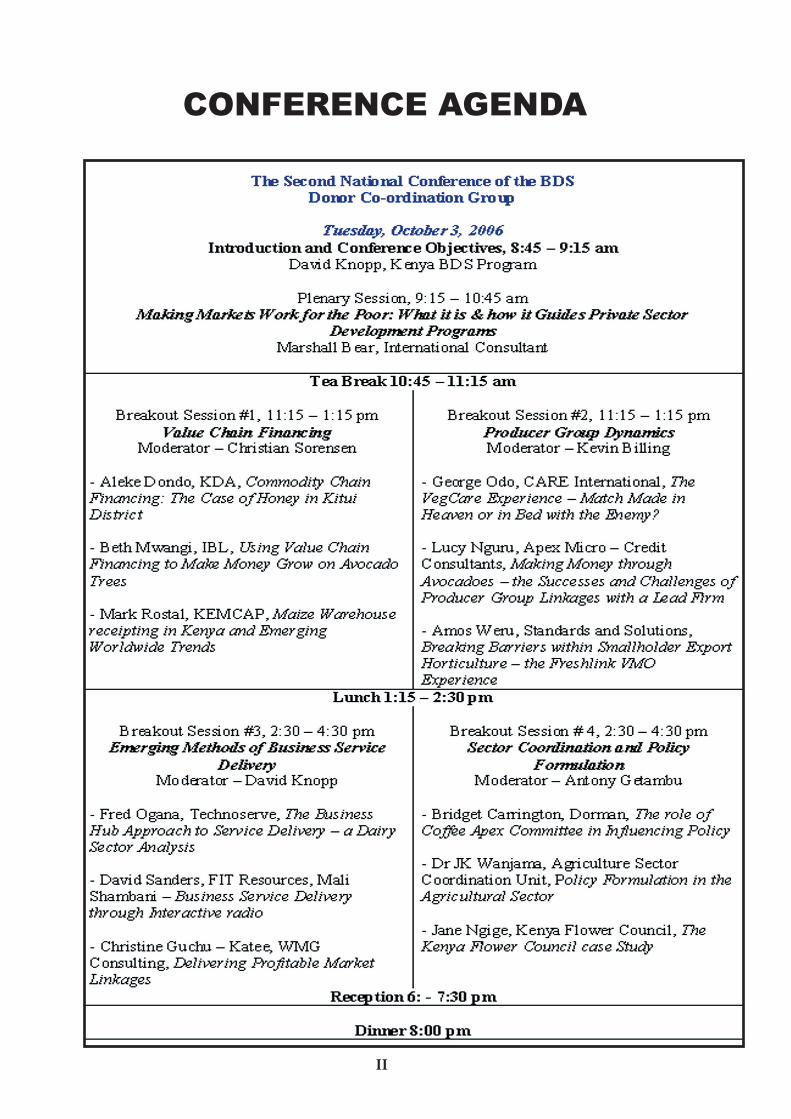

CONFERENCE AGENDA

PLENARY SESSION ONE

Making Markets Work for the Poor: What it is and how it guides Pri-vate Sector Develop-

ment Programs

By Marshall Bear

PLENARY SESSION ONEMaking Markets Work for the Poor: What it is and how it guides Private Sector Development ProgramsBy Marshall Bear, International Consultant

Introduction The purpose of this presentation was to explain to donor practitioners how MMW approach works andhow it can be used to guide project design and implementation. It also sought to understand how the ap-proach embraces sub-sector/value chains and other PSD approaches. More importantly, it focused on how to develop markets as opposed to why have the markets.It emerges that rural Small and Micro Enterprises (SMEs) are constrained by lack of information. There istherefore need to increase information accessibility for these rural SMEs on a sustainable basis. But while doing this, it is important to first understand the kind of information that is useful to rural SMEs. For in-stance, the mass media must ensure that the content that they deliver is relevant for the locals. The Essence of MMWMMW approach has an objective to provide more effective and inclusive market systems for the poor. It isgrounded in detailed understanding of market systems and shaped by an open, justified picture of sustain-ability. The approach has flexible, multi-faceted interventions aimed at leveraging more market activitythat are of a light touch, are indirect and facilitative.Objectives: the strategic rationaleAn effective private sector development generates growth and in doing so, builds capacity and createsopportunities. On the other hand, marketing systems functioning well creates the right and conducive environment for development of an effective and inclusive private sector. Development experiences showthat MMW intervention is necessary to bring about an inclusive and sustainable systematic change. Con-ventional interventions however often leave out the market system development and go straight to privatesector development from MMW interventions. What’s different about a MMW approachBoth the conventional and MMW interventions seeks to address problems that businesses face. A conven-tional approach asks how it can help to solve the problems. On the other hand, a MMW approach asks the market environment is not providing solutions to the problems. It also tries to identify why the market is not working for the poor.Defining pro-poor focusPro-poor potential refers to those high numbers of poor or disadvantaged groups that are close to markets, producers, workers and consumers and therefore they have a potential to change their situation. Pro-poor growth potential means ‘stepping up’ productivity/market share or ‘stepping out’’ new markets, jobs and opportunities. However, there are systematic constraints that hinder the pro-poor growth. Defining a realistic picture of sustainabilityThe following supporting functions presents a realistic picture of sustainability, for example for a commu-nity based tourism: • Maintenance and construction • Mediation • Finance • Infrastructure • Information • Negotiation • Booking • Marketing

III

The rules that can ensure sustainability and shift from communities’ interest in local tourism industryand also in the wider tourism industry include: Regulations, Standards, Informal rules and norms and Laws.

Developing a realistic picture of sustainability

FUNCTION WHO DOES? WHO PAYS? Business training/advice NGO/PS Donor / PS internship Advocacy NGO Donor/ members Finance NGO Donor Construction and maintenance PS Donor Joint venture mediation NGO/PS Donor Booking NGO Donor Marketing and branding NGO /PS Donor Information NGO Donor Standards NGO Donor Market research NGO /PS Donor Legal services PS Donor Conflict arbitration NGO Donor Regional planning NGO/ PS / Govt Donor/ Govt Advice to government NGO Donor

Market systems: A conclusion Market systems are more than mere transactions. They are both multi-functional and multi- player andmust involve the private and public. Market understanding is driven by what you need to know - pro-poor growth potential, systemic constraints and feasibility of donor practitioner intervention. Further, market systems are interconnected and interdependent - rules and supporting functions are often partsof other market systems. Finally, understanding of system constraints guides intervention decisions - may be indirect but explicitly links to pro-poor growth.

Sustainability: A conclusion - Conventional Vs. MMWConventional • Sustainability is not operationalised • General but ill-defined aspiration for the future MMW • Sustainability is placed at the centre of strategy and action • MMW builds a realistic, transparent picture of the future for the private and public sec-tors.

Intervention Design And Implementation – Conventional vs. MMWConventional There is general support for macro reform and;Direct delivery of support to target groups.

IV

MMWThere is specific support aimed at addressing market constraints through limited intervention; • Finite • Focussed • Facilitative

The method applies indirect intervention, relies on intelligence, influence and leverage.

A Facilitation Approach to ImplementationThere is need to stimulate market players to perform valid roles. Currently they’re not doing well in thatarea. This means ‘catalyzing, initiating, motivating and linking’ and getting them to do things. This strategyfor intervention is to determine a “pathway to crowding in” rather than “crowding out”.This strategy must recognize the importance of indigenous ownership and that interventions are time de-fined with finite resources. The strategy must also be one which establishes credible exit strategies fromoutset, against which progress can measured.

Guiding facilitation questions • Are intervention activities likely to be a market function in the future? Is what we are doing now likely to be required in the market in the future or is it purely temporal? • Should we be working through a market player? If action is a market function, identify market players with the incentives and capacity to play this role (or seek to ‘leave the door open’ for this to happen in the future) • Are our relationships with market players appropriate? Our interaction with market players should encourage them into roles and practices consistent with local system, building on local incentives and ownership. • Is our support right sized? Our actions must be consistent with local norms not development norms: otherwise we distort function, displace ownership, disorient players. • Is there potential for ‘crowding in’? keep asking “ should we be doing this?” always look for opportunities to crowd in market functions and players that better serve the poor.

Guidance for Panel DiscussionsThe following topics will be discussed; • Value chain financing, • Business service methods, • Producer group dynamics, • Sector coordination and policy.MMW guidanceThe MMW approach demands for markets and not models! It seeks to go beyond standard statistical mod-els and also to engage dynamic markets and new playersMMW model supports systems (not firm) solutions: • May be indirect but with explicit links to poor producers • May work with lead firms but to leverage wider change • Strengthen and align incentives of market players/functionsThe MMW model seeks to create and sustain market system capacity: • Benefits • Relationships • Learn and innovate

V

BREAK-OUT SESSION ONE: VALUE CHAIN FINANCING

PRESENTERS:

1. Aleke Dondo - Commodity Chain Financing: The Case of Honey in Kitui District.

2. Beth Mwangi –Using Value Chain Financing to Make Money Grow on Avocado Trees.

3. Mark Rostal – Maize Warehouse Receipting in Kenya.”

1 BREAK-OUT SESSION ONE: Value Chain Financing1.0 INTRODUCTIONBy Christian Sorensen, Senior Advisor ABDTwo worlds meet whenever the term value-chain financing is used, the BDS world and the microfinanceworld. Microfinance has been seen as a response to integrated approaches of development, where finan-cial and non-financial interventions are intertwined. But while micro-finance minimalism or purismis an important pillar in growth of the micro-finance sector, it is increasingly becoming clear that busi-nesses need much more than financial input to grow.On the other hand, BDS is treated as a non-financial service. As an answer to microfinance minimalism,possible business development services are identified to address all constraints along market chains. This,it emerges, has resulted into a bi-polar development world of projects, NGOs, specialists and consultants, who either focus on pure micro-finance or pure BDS, and who do not communicate with each other.During the seminar where one of the themes was the ‘interrelationship between micro-finance and BDS’it was concluded that those SMEs which receive loans have the capacity to do business up to a certain level before grounding to a halt. It also emerges that BDS is needed to improve their capacity – both tech-nically and in terms of e.g. business planning. This could also be interpreted to mean that those SMEswhich have received BDS need capital to expand and that SMEs require both microfinance and BDS.The Value Chain Approach and Sub-Sector Analysis describe the market chain and the transactions init from producer to final consumer. These approaches seek to identify and address constrains along thechain. The smoother functioning of the market chain is often the objective for developmental interven-tions. Most of these constrains are financial.

• Most producers e.g. farmers have problems with financing inputs and therefore sell their harvestimmediately at low prices due to lack of storage facilities and good marketing strategies. • Traders often complain of lack of short term finance to buy in bulk.• Volume suppliers – be they traders or organized farmers - have working capital constrains to cover the gaps from delivery to payment.• Processors have similar gaps from buying the raw material to selling the processed commodi-ties.• Asset financing is limited by lack of financial sources and appropriate finance products availablefor small farmers and processors in agriculture.

However, new financial products and initiatives especially for agriculture and SMEs are emerging. Theyinclude input financing, (e.g. by processors via contract farming in cotton), factoring, micro leasing, mi-cro insurance (e.g. livestock insurance) and warehouse receipt systemSome of the key questions for the theme of value chain financing are:

• How can the finance sector be convinced to think ‘commodity chain’ approach instead of withtheir conventional ‘catchments area’ approach? • Minimalism in Microfinance needs to be replaced by a more holistic approach – but how can thisdone without returning to ‘integrated approaches’ - and who coordinates between the two worlds of microfinance and BDS?• Where are we with the innovative finance approaches in Kenya?

The theme group tries to answer some of the questions based on experiences and ideas from Kenya.This session has three contributors namely;

• Aleke Dondo, Managing Director of K-REP Development Agency who discusses commodity chain financing from the perspective of the microfinance sector using the Case of Honey in KituiDistrict.

1

• Beth Mwangi, Director of Ideal Business Links describes the case of Using Value Chain Financing to Make Money Grow on Avocado Trees.• Mark Rostal, Chief of Party of AID assesses the experiences with Maize Warehouse Receipting in Kenya. This is one of the emerging finance service that target market constraints.

1.1 Commodity Chain Financing: The Case of Honey in Kitui District By Aleke Dondo

1.1.1 IntroductionValue chain approach is becoming increasingly popular as a development intervention and as a focus for research. Value chains describe the market sequence and activities between the source of a product to the time it is purchased by consumers. The aim of this approach is to identify and address constraints alongthe chain. Development practitioners are concerned about developing interventions which remove con-straints that hinder the smooth functioning of the market chain.Constraints that hinder smooth functioning of the market chain are of varied nature and therefore require different solutions that can be grouped into three categories:

• Those that require policy or strategic interventions;• Those which can be solved by Business Development Services (BDS); and,• Those which require financial services.

In market chain analysis, a tendency is to disregard constraints caused by lack of financial services orpoorly functioning financial markets. Some analyses wrongly assume that financial constraints will auto-matically be catered for by existing formal and informal financial service providers.This presentation addresses those constraints along a commodity chain that can be addressed throughprovision of financial services. It uses honey in Kitui district as a case study but first examines the financialsector in Kenya.

1.1.2 Financial Sector in KenyaCompared to most sub-Saharan countries, Kenya has a relatively well established banking and micro-finance sector. However, formal banks are not flexible enough to offer financial services to low-incomegroups. They are also not geared towards business expansion along commodity chains. On the otherhand, the microfinance sector has grown significantly in the last 20 years to offer financial services to thisneglected group. The sector however, has three major biases. Most MFIs operate in urban areas thereby ignoring ruralparts of ASAL districts such as Kitui. In addition, due to restrictions of the banking Act, many MFIs have developed as credit–led organizations. This has limited the extent to which they can mobilize deposits toensure their sustainability. Most MFIs provide credit for trading purposes only with their loan asset port-folios concentrated in short-term working capital loans. Finally, very few MFIs provide services for small-holder farming activities, yet it is a sector that engages more than 70% of Kenya’s labour force. Currently, most MFIs offer a single product to SMEs operators through a single methodology commonly called theGrameen model. Consequently, only a limited segment of the potential market is reached.Even with huge investment in the Kenyan microfinance sector, it is clear that existing products and meth-odologies restricts MFIs from meeting the demands of their services. For instance, the 1999 baseline sur-vey of Kenyan SMEs revealed that only 10.4% of enumerated enterprises had received financial servicesfrom any source, be it banks, NGOs, MFIs or money lenders. Not forgetting that in addition to loans, SME business people also need other financial services like mortgages and insurance.It is imperative, therefore, to develop financial products that will address the diverse financial needs of lowincome groups and in particular the smallholder farmers. It is also important that Kenyan financial sectorthink commodity value chain and develop appropriate financial products along the value chain.

2

Lastly, the financial constraints enumerated at the introduction of this section go along the entire valuechain of any commodity and requires appropriate financial products.

1.1.3 The Honey Market Chain in Kitui DistrictThousands of beekeepers produce honey using traditional log hives in Kitui district. According to 2004estimates, the district had 295,000 traditional log hives, compared to 2,793 langstroth hives and 1,020 top bar hives in Kenya. While the district has a potential to produce over 8,000 tonnes of honey per year, the annual output rarely exceeds 3,000 tonnes. The price of crude honey in the district ranges from KSh 40to KShs. 80 per kilogramme for traditional log hives’ honey and KSh 80 to KSh 100 for honey extracted from the langstroth hives. The farmers supply honey to traders who supply local and distant market proc-essors who package the product to be sold to supermarkets and retail shops mainly in Nairobi. While the largest formal market for Kitui honey is Nairobi, the market can be segmented into:

• Local markets within the district – mainly for honey from log hives and used mostly in making traditional liquor and herbal medicines;• Local or regional markets – purchased by local refinery channels in Kitui and Mwingi towns;• The Nairobi market passing through brokers; and,• Distance markets through formal processors such as African Beekeepers Limited (ABL) and Honey Care Africa.

In 2004, Danida through the Agricultural Business Development (ABD) programme began work with honey producers in Kitui District. Preparations to develop the honey market chain started with a work-shop involving honey producers, traders, honey processors and government officials. The workshop ex-plored constraints to the development of the sector and the market opportunities. Lack of appropriate financial services was cited as one of the major constraints along the entire honey value chain. ABD alsocommissioned a number of studies on the honey value chain in the district. The studies showed thatdeveloping the honey market system requires coordinated action by several market chain actors and sup-port institutions.Marketing of honey is constrained by the disorganized and weak marketing structures from the producer to the consumer. Shortage of bee forage especially during the dry months posses a serious threat to bee keeping practice in the district.

1.1.4 KDA/ABD ResponseKDA in collaboration with ABD project has identified a number of constraints that could be addressedby appropriate financial products. These include limited financial ability to acquire hives and honey har-vesting kits, and for working capital required by traders to purchase honey from producers. They alsolack capital to purchase centrifuge machines by bulk buyers. However, KDA plans to develop appropri-ate financing products for the entire honey value chain in Kitui. These will include loans to producers oflog hives, lease of centrifuge machines to bulk honey buyers. Other support activities like implementing standards for high value honey and capacity building for honey producers will be undertaken by partner organizations.To deliver these products, KDA will work through its network of eight Financial Services Associations (FSAs). They will also disseminate those financial products that prove to be effective to other microfi-nance organizations in Kitui District.Following is a brief breakdown of financial constraints faced by key actors.ProducersHigh cost of inputs especially that of langstroth beehives and honey harvesting kit is a major constraint faced by producers. To address this, KDA plans to introduce its tested financial lease product for beehivesand harvesting gear to three FSAs in Kitui District who will avail them to the honey producers. Producers will also get other benefits such as saving facilities from FSAs.TradersThere are two kinds of traders; those who buy in bulk and small scale traders. In Kitui, some individual

3

traders and honey processing companies buy honey in bulk. Individuals face two financial constraints;working capital to pay for honey delivered by producers and capital to purchase centrifuge machines for bulking and refining. In response, KDA will develop a factoring facility to pay off the honey producers ondelivery of honey to the traders. Organized groups of honey producers will also benefit from this initiative.For the small scale traders who lack capital to buy honey, KDA through the FSAs will develop a working capital loan for them. They will also have access to financial leases to acquire centrifuge machines.ProcessorsProcessors such as ABL and Honey Care Africa supply their processed and packaged honey to supermar-kets and retail shops. Supermarkets need 90 days before payment therefore imposing a cash flow problemto processors who have to pay cash to their suppliers. KDA will develop a factoring product for honey supplied by traders to processors.

1.1.5 Actors and Financial ProductsThe diagram below has three components. The top component shows the major actors along the honeychain in Kitui. The second (middle) component shows the financial products that will be developed andtested for the different actors. The third (bottom) component shows the institutions (FSAs and KDA) thatwill supply the proposed financial services.

1.1.6 ConclusionAll market chain analyses need to consider constraints caused by lack of financial services or poorly func-tioning financial markets. The Kenya financial sector is not geared towards looking at business expansionalong commodity chains. It is imperative that the sector begins to think systematically about commodity value chains and to develop appropriate financial products along the value chain if efforts geared at com-modity market chain development are to realize their full potential.

4

Diagram 1

1.2 Using Value Chain Financing To Make Money Grow On Avocado Trees By Beth Mwangi

1.2.1 Avocado Production in KenyaAvocado is an important export fruit crop in Kenya in terms of value of output and export earnings. Over 15000 tons of avocado valued at over Ksh 1 billion were exported in 2004. The fruit grows bestat altitudes of 1500-2100 meters above sea level, with well distributed rainfall of more than 1,000mm. The main varieties grown in Kenya are the Fuerte variety, which is grown for the fresh export market,the Hass variety promoted in the country during 1960-70s and the Pueblo variety. Central province ac-counts for 35% of total production with Eastern province accounting for 29% while Nyanza and Western provinces account for 14% and 11% respectively.Avocado has a high nutritional content and can be utilized in the following forms: Fresh fruit for human consumption locally or in the export markets, with the latter being the main outlet; and avocado oil for cosmetics and specialized cooking in small under- developed markets. The domestic market consumesover 80% of total production with the rest being exported as fresh fruits. France has been the largest buyer of fresh avocado from Kenya. Other main export markets include United Arab Emirates (UAE), Netherlands, UK and Germany.In the 1990s, diseases and insect pests invaded this fruit and nearly destroyed it completely. Diseases such as anthracnose, scab, cercospora and rootrot are common while prevalent insect pests are thrips, scales and fruitfly. Anthracnose lives on twigs, rotten fruits and on dead leaves. It hardly infects undam-aged fruits. It can be controlled by observing field hygiene such as removing dead twigs, application ofcopper based fungicide and first spray when flower buds appears. The second spray comes one monthlater at fruit set with the third coming a month after fruit set.Fruits are susceptible to scab only from flowering until about half size development. The fungus re-quires wet conditions. Fruit may escape if conditions at fruit set are dry and warm. The disease can becontrolled by growing tolerant cultivar like hass and observing field hygiene by use of copper basedfungicides.Cercospora requires humid and hot condition (above 20 degrees centigrade) to produce spores. Spores are dispersed by splash or wind. Infection takes place through lenticels and symptoms appears about 3 weeks after infection. Mature fruits are resistant to the disease. The disease can be controlled by sprayingcopper fungicides. The spray should cover much of the development period of the crop and it shouldreach the top of the tree.Thrips is a slender insect pest 1-2 mm long. It sucks sap from the plant causing silvering of infested part.The infected part turns brown and dries up causing flower drop. It can be controlled by natural enemieslike ladybird beetles, predatory thrips and mites. It can also be controlled by use of chemicals like del-tamethrin (Decis) and Achook (zadirachtin) at flowering stage.Symptoms of scale include discoloration, malformation, leaf, fruit drop and retarded growth. Damage is caused by toxic saliva. Control of scales includes pruning and opening up the tree to allow for air circu-lation, use of agro chemicals like DC– tron plus and insecticide plus mineral oil. Fruit fly lays eggs underthe fruit skin. The eggs hatch within 1-2 days causing fruit rot. Fruit fly can be controlled by collectingand destroying all fallen fruit, use of bait sprays consisting of an insecticide mixed with molasses and by use of commercial bait – GF 120 or acceptable chemicals like Deltamethrin.Lack of essential micro nutrients also affects the yields of avocado fruits. For instance, iron deficiencycauses laminae to turn yellow, veins retain green colour lending the tree unproductive. Magnesium defi-ciency causes pale patches on old leaves. A band beside the vein remains green with young leaves being affected first. Such deficiencies can be corrected by application of foliar feed containing required micronutrient whenever symptoms are detected.

5

1.2.2 Constraints to Avocado ProductionThe diseases on the avocado fruit led to low quality yields resulting into low grade avocado products. This,coupled with delayed shipments of deliveries thus resulting in spoilt fruits tarnished Kenya’s reputation in the export markets. This greatly reduced foreign export earnings from the avocado fruit. In addition, bro-kers started buying avocados at throw away prices. This discouraged many farmers from growing the crop.As a result, orchards were routinely neglected and unprunned trees let to grow to unmanageable heights. Even picking fruits for domestic consumption became unbearable. Eventually, farmers started perceiving the avocado tree as any other ordinary tree with some in main production areas of Maragua, Thika andKiambu opting to cut down the trees to pave way for other more productive crops. Most small scale producers of the avocado fruit lack the requisite skills and knowledge to undertake the control measures against diseases and insect pests’ attacks. The following are some of the problems facingthe farmers:

• Little knowledge on what to spray, when to spray, how to spray.• They lack knowledge and facilities for proper handling and storage of agrochemicals.• Failure to gain access to or afford high cost (upfront) of agro chemicals, spray equipment and la-bour.• Lack of inputs, skills and knowledge in crop husbandry resulting in diseased and under ripe fruits.• Lack of access or knowledge of business services market.

1.2.3 Response to these ConstraintsSince the inception of the Kenya BDS, A USAID funded initiative, in September 2002, the perception of the avocado tree has changed. Kenya BDS invited bids from business development services (BDS) providers to design an intervention to commercialize disease and pest control services. A proposal by IBL to commer-cialize agro chemical spraying services among small scale producers was accepted by Kenya BDS.Kenya BDS contracted IBL to identify and develop independent service providers; sensitize farmers on need for integrated pest management (IPM) and agrochemical spraying services; approach a financial serv-ice provider to extend credit facility to farmers’ groups for agrochemical services backed by strength of sup-ply contract with exporter; establish a check of system where the exporter pays farmers through the bank, which deducts scheduled loan payment before releasing net proceeds to the farmer.

1.2.3.1 IBL’s Role as a FacilitatorIBL held discussions with different financial service providers to identify potential partners to work with.A key criteria was capacity of the institution to reach out to the small holder farmers and their commit-ment and willingness to invest in development of a new financial product. Equity bank was selected as themost suitable partner. The bank agreed to develop an appropriate financial product to meet the needs of theavocado farmers. Since the loan amounts required by individual farmers are fairly small, it was agreed that the bank waive the traditional security requirements and loans be secured by the supply contract signed between farmer’s groups backed by chattels mortgage signed by individual farmer. IBL also developed a spraying scheme that meets market requirements and shared it with different export-ers who approved it. They further coordinated meetings between exporters and Equity bank to discussand agree on how they could work together to facilitate recovery of loans disbursed to farmers from sale proceed to be paid by the exporters. This led to signing of an MOU between the bank and different export-ers.Equity Bank agreed to:

• Develop an appropriate loan product to meet the needs of the avocado farmers. • Waive the traditional requirements for collateral.• Accept the supply contract signed between farmers’ groups and exporters as security for loans.

6

• However, individual farmers to sign chattels mortgage to enhance their commitment to repay loans• Establish a check of system where the exporter pays farmers through the bank, which deducts scheduled loan payment before releasing net proceeds to the farmer.• Send their credit officers to meeting organized by farmers’ groups to educate them on the loan ap-plication process.• Allow farmers to complete and sign the loan forms in their usual meeting places and submit them to the bank for processing.• Develop promotional materials for the new financial products.

1.2.3.2 Loan application processThose farmers’ groups who have signed a supply contract with an exporter can approach Equity Bank foran agro chemical loan facility. Individual group members will complete a loan application form and chat-tel agreement form (for the whole avocado season). These applications are consolidated at group level andsubmitted as one loan application for the consolidated amount. The bank approves the loan and issues aletter of offer to the group indicating the amount approved for the entire season. Group members whowish to pay cash for services can put their deposits into the groups’ savings account with the bank. Thebank is instructed to hold the cash received under ‘lien’ to ensure that it cannot be withdrawn for other purposes.To get agro chemical spraying services, farmers’ groups fill a requisition form for chemical spraying serv-ices from the service providers. Details in the requisition form includes; the number of trees to be sprayed, how many will be paid for in cash and to be paid through the loan facility from Equity bank. On the strength of information received, a SP delivers service and raises a services delivery note to be signed by individual farmers to acknowledge receipt of services. Delivery notes for services rendered to group mem-bers are consolidated and one invoice is raised for the farmers’ groups with the authorized signatories for the group endorsing an invoice for payment. The invoice is submitted to Equity Bank for settlement. Thebank debits the group’s loan account and credits the service providers.Loan plus interest accrued is recoverable from the sale proceeds of the avocado to the exporter. When farmers deliver their fruits to the exporters, the exporters remit payment to the bank (with details breaking down payment by group). The bank then pays farmers’ groups less 20% deduction for the loan repaymentuntil the loan is cleared. Since payments are made twice a month, it is assumed the whole loan should be fully repaid within three months.

1.2.3.3 Achievements The loan facility was well received with more than 95% of farmers in the groups throwing in their applica-tions. Only less than 5% pay cash for services. 3,500 farmers are accessing commercial spray services. 38 commercial SPs with access to modern tools and equipment for agro chemical spraying services are pro-viding services to farmers. As a result, more than 25,000 trees have been sprayed in the current avocado season. 3 cycles of spraying have already been done and more farmers’ groups are applying for the loan facility.

1.2.3.4 Expectations4,000 farmers are expected to benefit from the agrochemical loan facility in the first year. At least 40,000avocado trees will receive spray services. It is hoped that the services provided will increase Grade 1 yields from less than 25 pieces to over 300 pieces per tree during the first year. This model will eventually be rep-licated with mango and passion fruit smallholders.

1.2.4 Lessons Learnt• Awareness creation among farmers on opportunities available for them is critical for success.

7

• Services and products must be customized to meet the specific needs of different customers.• Financial education for farmers is very important.• Different stakeholders in the value chain must work together for the mutual benefit of all stake-holders.• The strength of the entire value chain depends on the performance of every single partner in thevalue chain. • The competitiveness of the final product corresponds to the capacities of the weakest link in thevalue chain.• Innovation holds the key to solving the problems facing small scale products. • Stakeholders must be willing to think and work outside the ‘box’.• Flexibility is important in designing financial products and services in order to give customers achoice.

1.2.5 Challenges Faced• Initial reluctance by farmers to sign the chattels mortgage forms due to skepticism about bank loans.• Farmer education is a time consuming process and during the pilot phase, only two cycles of spray-ing were done.• Internal wrangles in the farmers’ groups adversely affect the loan application process leading todelays.• Farmers with no trees applying for the avocado loan product. • SPs going to provide services only to find no trees.• Farmers indicating fewer trees on the loan application than they actually have. • Illiteracy – some farmers cannot sign the loan application form.

1.2.6 Key Innovations• Kenya Commercial Bank has agreed to reach out to small holder farmers.• Loan product tailored in a flexible manner to minimize interest payable by farmers.• Waiver of traditional security requirements.• Illiteracy is not a barrier to accessing loans as farmers can append their thumb prints.• Signing of MOU with stakeholders in the value chain to facilitate loan repayment• Small holder farmers who could not access financial services now have access. As a result, theyhave been able to increase their household incomes by increasing the competitiveness of their farm yields.

1.3 Maize Warehouse Receipting - Agriculture Productivity and Poverty in Kenya By Mark Rostal

1.3.1 Agriculture ProductivityWhile agriculture plays a significant role in Kenya’s economic development, the sector is dominated bysmall scale farmers. They consist of approximately 3.5 million people each with 20 hectares or less andan average of 2.5 hectares. They produce an estimated 60% of Kenya’s produce both for domestic and forexport markets. These farmers account for up to 75% of production in some commodities like coffee andtea. In the past 20 years, Kenya’s overall economic development has been erratic and highly correlated with growth in the agriculture sector. But since 2001, economic growth has been on a slow pace due to poor performance by key sectors such as tourism, horticulture, services and manufacturing. This has led to in-crease in poverty levels.But the worst hit sector is agriculture. Numerous statistical sources show that:

• Value-added agricultural GDP decreased from 19.7% in 2000 to 15.8% in 2003 with a slight in-crease to 16.4% in 2004;

8

• Agriculture’s contribution to GDP declined from 35% in 1964 to 24% in 2000;• Maize yields declined from 1.84 tons/hectare in the five years between 1985/86 to 1989/90, to 1.71tons/hectare between 1990/91 and 1994/95, to 1.58 tons/hectare in the eight years since the 1995/96 season.

1.3.2 Poverty Assessment in KenyaIt is estimated that 17 million Kenyans live below the poverty line. A survey of the Kenyan poverty situ-ation revealed the following:

• Absolute poverty is found throughout Kenya, with no geographic specific areas.• While many farming households produce and sell, they are often net buyers and are negativelyaffected by high food prices, with most subsistence farming households expending almost 72% oftheir incomes on food purchases. • Nonfood-poor households derive approximately 44% of their household incomes from off-farmactivities, while food-poor obtain the largest share of their income from crops (43%), and earn more income from off-farm than from livestock.• Food-poor incomes are one-sixth that of the nonfood-poor.• 60% of households that had no adult with primary education were chronically poor.

The Food Price Index (FPI) shows that the cost of food has been rising in Kenya for several years. FPIhas increased significantly in the past three years. Combined with decreasing incomes, it has resulted inhigher levels of food insecurity. As earlier mentioned, majority of farmers are net buyers, buying more than they sell. As such, they are always negatively and disproportionably affected by high food prices.

1.3.3 Key Challenges and Constraints to GrowthRural credit, in particular agricultural credit, is considered one of the major constraints to increasing smallholder agricultural production in Kenya and improving absolute poverty levels. Previously, the gov-ernments provided farmers with credit through state owned corporations such as the Agriculture Finance Corporation (AFC) that supplied credit, Kenya Farmers Association (KFA) that distributed agricultural inputs and the National Cereals and Produce Board (NCPB) that purchased agricultural produce. Thescheme worked reasonably well and reached many farmers but not necessarily the smallest. For instance, AFC’s mandate was to serve farmers with more than 5 acres but the average farm size reached was 20 acres, approximately 8 times more than the size of a small-scale farmer. In 1992, under budgetary and donor pressure, a program for economic liberalization began and govern-ment control over exchange rates, product pricing and marketing were lifted. Private sector traders be-came active and often farmers would side-sell their crops to better paying private traders rather than thegovernment operated boards. This new reality further eroded government’s ability to maintain the closedsystem and ensure loan repayment that was critical to the viability of the scheme. In addition, the system fostered a degree of rent seeking behaviors by those in power and eventually the structure collapsed, leav-ing farmers without institutions or services. Some have however been revived by the new government. Today, the development of Kenya’s agricultural sector is characterized by the following difficulties:

• An Uncertain Policy Environment.• Lack of Access to Financial Services.• High Interest Rates.• Excess Liquidity.• High Risk Agriculture.• Shortage of Financial Products.• Policy Environment.

1.3.3.1 Uncertain policy environmentLiberalization in Kenya proceeded at different paces and degrees in each of the various agricultural sectors. At the same time, the government tried to maintain influence in politically important sectors through fre-quent policy reversals which caused uncertainty, often leading to false and unrealized expectations by the

9

poor. Moreover, these misleading actions resulted in an uneven response from the private sector, which provided the opportunity for government to reassert itself and dominate in areas where services were not being provided, thus discouraging the private sector to enter and compete. Still, a scarcity of services exists in many crucial spheres, such as rural finance and market information,where neither the government nor the private sector is adequately engaged. Since liberalization, however, the microfinance sector has successfully flourished. But the sector has not helped much due to its con-centration on urban based SMEs while avoiding the agriculture sector just as commercial banks have so adeptly done.

1.3.3.2 Lack of access to rural financial servicesFinancial services are often wrongly interpreted to mean credit or loans. A strong and unmet demand forsavings services is widespread throughout all rural areas. Still, farmers cite lack of credit (or lack of access) as the primary obstacle preventing them from purchasing quality enhancing products such as fertilizers, improved seeds, agro-chemicals and irrigation facilities.

1.3.3.3 High interest ratesFarmers, business persons and consumers complain of high interest rates charged by banks and non-bank financial institutions. While rates have widely varied over the past several years, they are currently around18-20% at banks. MFI rates are substantially higher, reflecting greater operating costs and riskier clientele(including covariant risk). In general, high interest rates are caused by:

• Above average non-performing loan ratios, often caused by directed lending of shareholders;• Lack of reliable information on individual and business credit worthiness; • Underdeveloped risk assessment and credit evaluation techniques;• Over reliance on collateral, often times unrealizable collateral;• An ineffectual and expensive judicial system

Many banks in Kenya report increasing profitability year after year but have little to show in terms of ini-tiating agriculture-oriented financial services.

1.3.3.4 Excess LiquidityThe banking sector has been very liquid of late. With rates paid on Treasury Bills decreasing in recentyears, financial institutions have been forced to offer new loan products, aimed primarily at the urban-based formal wage sector as a means to match their previous risk-free earnings. Meanwhile, the rural sector has almost no access to credit or other financial services. This vastly undersubscribed market repre-sents a large, albeit riskier, opportunity for banks and other providers.

1.3.3.5 High-Risk AgricultureEven with Kenya classified as a deficit arid country, most agricultural activities depend on rain water.Majority of farmers are affected by the water deficit resulting in sizable, nation wide loan defaults for agri-culture. In addition, Kenyan agriculture is smallholder based, with little information available to financialinstitutions on the credit worthiness of potential clients. Only a fraction of farmers are reached by banks and MFIs.1.3.3.6 Shortage of Financial ProductsLittle investment has been undertaken to develop product-specific solutions for the agriculture sector. Most MFIs have focused on developing sustainable business models and products that maximize financialreturns, just as banks have successfully done.

10

1.3.4 What is Warehouse Receipting?1.3.4.1 History and DescriptionGrain warehouse receipting was first recorded in Mesopotamia around the year 2,400 B.C. Today, ware-house receipts are widely used for most commodities. In general, warehouse receipt financing has thepotential to improve the cash flow of farmers, traders, millers and governments through strategic grainreserves. For farmers, the benefits accrue through safe and secure storage. This helps to reduce spoilageby holding crops after harvest when prices are low and market supplies high to a future time when pricesare high and market supplies low. A warehouse receipt is a contractual agreement between a warehouse and a commodity owner, in most cases a farmer. Often, warehouse receipts serve as title to stored commodities. Since warehouse receiptsare considered negotiable instruments, the receipts can be traded, swapped, sold, used as collateral to finance loans, or used as a method of delivery against future contracts.Banks financing warehouse receipts do not buy the commodity outright; technically, financial institu-tions lend money against the collateral guarantee of a graded commodity in a known storage facility. Therefore, should the borrower (farmer) default, the bank fully recovers its loan if the correct precautionsand safeguards were properly instituted and acted upon. Warehouse receipt financing is still considered speculative. Banks must have a thorough understandingof individual commodities and market behavior. Borrowers must also understand the market and attend-ant risks, including the legal actions banks implement to realize their investments. In summary, warehouse receipting systems bring together:

• Producers and traders who deposit commodities in warehouses.• Warehouses that provide secure storage of commodities and issue receipts.• Lenders who accept the receipts as collateral for loans.• Collateral manager who inspect commodities and certify that warehouses meet basic standards.• Insurance providers that underwrite deposit risk against loss.

1.3.4.2 Mechanics (a schematic)Warehouse receipt systems introduce a number of participant and mechanisms not found in other ag-ricultural schemes. The collateral manager is critical to the overall success of the system. Producers andtraders deposit commodities to the warehouse. The warehouse provides secure and safe storage and is-sues a receipt to the producer, certifying that it is in possession of a specified quantity of a particular

11

Under the scenario above, the lender can dispose off the pledged goods only if the borrower defaults onthe loan or if the trigger price in the loan agreement is realized. Otherwise, title and any changes in the value of the deposited commodity belong to the depositor or borrower. A depositor can also transfer the receipt to a buyer, who in turn can take delivery of the commodity at the warehouse.

1.3.4.3 Optimal Warehouse Receipting Conditions • Legal and regulatory requirements, including laws that clarify the rights and responsibilities of system participants; title to warehoused goods; transferability of receipts, legal equivalence of the stored and documented commodities; and use of receipts as collateral.• Commonly used and accepted grades and measures.• A competent and trusted certification and inspection service.• Financial institutions willing to lend against receipts.• Commodity grades and standards.• Market information systems.• Legal and regulatory expertise tied to contracts, commercial codes, and financial regulations.

12

Diagram of a Warehouse Receipt System

1.3.4.4 Expertise Required• Warehouse management, certification and inspection.• Commodity grades and standards expertise.• Grain merchandising expertise.• Legal and regulatory expertise (title, collateral, negotiable receipts, warehouse inspection and certification services).• Insurance.• Receipts-backed lending experience or expertise.

1.3.4.5 Implementation Need-to-Knows• Not effective for capital investment.• Significant conditions required.• Viable storage facilities are difficult to locate because of government intervention in marketprices and other distortionary practices, high cost of financing and long payback periods, andfacilities are of low quality and are inadequately distributed.• Financiers and warehouses favor large producers

1.3.5 Why is Maize Warehouse Receipting Important for Kenya?1.3.5.1 The Constraints It Seeks to Address

• Warehouse receipt systems extend the sales season while providing small farmers access to lower losses due to spoilage, higher average prices, a reduction in seasonal price swings, and the economies of scale that derive from upgrading the marketing process with consistent standards and grades.• Receipts allow for a new source of collateral - secured commodity deposits.• Lenders reduce transaction and monitoring costs.• Traders leverage initial capital by purchasing more commodities with loans against each deposit made in a warehouse.• An effective system can allow for extensive outreach due to reduced transaction costs for finan-cial institutions.

1.3.5.2 The Benefits and Opportunities It Creates• Cost Effective Screening of willingness and ability to pay.• Expanded Collateral.• Appropriate Terms or Conditions.• Increased yields.• Lower Costs.• Higher Product Prices.• Standards and Efficient Sales.• Market Access. • Technical Services.

1.3.6 Where is Maize Warehouse Receipting in Kenya?1.3.6.1 BackgroundMaize warehouse receipting in Kenya is underdeveloped and still in its infancy. The private sector hasmade attempts to develop a functional system only to be blocked during various phases of implementa-tion. Recently, the United States Agency for International Development (USAID) began working to-wards bringing together private sector participants that are critical to the creation of a viable system. Leading this effort is USAID’s Kenya Maize Development Program acting as the focal point from which

13

1 Farmers trained to understand how warehouse receipting function, the benefits, the cost and risks • KMDP2 Farmers form groups to meet minimum tonnage requirements set by the bank(s) • Farmers • KMDP3 Groups appoint key leaders/decision makers/signatories • Farmers • KMDP4 Group leader (treasurer) trained to keep accurate records of each farmer’s contribution (number of bags deposited) • Farmers • KMDP5 Group arranges collection, inspection, grading and warehouse transportation • Farmers • KMDP6 Group ensures that a minimum warehouse receipt deposit of 100 million tons is obtained (smaller amounts can be deposited at the warehouse until 100 million tons is reached) • Farmers • KMDP7 Warehouse and collateral manager inspect and grade the quality and weigh the quantity • Warehouse • Collateral manager8 Warehouse dries and cleans the maize if needed (and applies the costs to the group and individual accounts) • Warehouse9 Group representative examines and records costs and later informs individual farmers • Farmers • KMDP10 Warehouse issues storage and handling contract • Warehouse11 Group leaders sign warehouse storage contract • Farmers • KMDP

all critical actions are directed. These efforts include but are not limited to:

• Providing extension services to increase yields.• Organizing farmers into viable groups.• Providing farmers with market information and training them on its use.• Sourcing viable vertical storage facilities and negotiating on behalf of the farmer’s interests.• Locating experienced collateral managers in the African context.• Training farmers on the merits of warehouse receipting as an alternative to current market behaviors and practices.

In addition, a leading Kenyan bank was provided with a US government guarantee, insuring against loan losses up to 50%, principle only. USAID-funded Kenya Microfinance Capacity Building Program (KEMCAP)was tasked with providing the bank with technical assistance and capacity building services. KEMCAP also coordinated actions between KMDP and the bank, monitoring progress against negotiated benchmarks.

1.3.6.2 Roles and responsibilities (timeline excluded)

Steps Activity Responsibility

14

15

12 Warehouse and/or collateral manager issues a “goods received” note for each ton of grain deposited • Warehouse • Collateral manager13 Group leaders receive a copy of the “goods received” and secure it in a safe location • Farmers • KMDP14 Banks inform the warehouse and collateral manager of the grain lending rate (limited to a certain time period) • Bank15 Bank or collateral manager (on bank’s behalf) provides the group leaders with a copy of the signed loan contract • Bank • Collateral manager16 Bank states the market value in the terminal market (Nairobi) and lends a percentage of the stated value against the warehouse receipt • Bank17 Group leaders sign the loan agreement with the bank • Farmers • KMDP18 Collateral manager forwards the loan agreement and the warehouse receipt to the bank • Collateral Manager19 Bank remits the loan to the nominated bank account • Bank20 Bank loan(s) issued to farmers by their chosen leaders • Farmers • KMDP21 Extension agent helps the farmers and warehouse market the grain to millers (with farmers dictating pricing) • Farmers • KMDP Warehouse22 Group leaders sign sales contracts with millers, traders and government • Farmers • KMDP • Buyers23 “Goods received” and note provided to buyers once payment has been made (buyers pay the bank) • Farmers • KMDP • Buyers24 Bank deducts loan principle, interest and other costs, afterward remitting the balance to the nominated farmer bank account and the warehouse for storage and handling • Bank25 Bank forwards the warehouse receipt (with copies for the warehouse and farmer group) to the collateral manager, providing notification that the bank no longer has a lien on the commodity • Bank26 Group leaders apportion funds based on each farmer’s deposits • Farmer • KMDP27 Warehouse releases grain to miller • Warehouse

1.3.6.3 The role of Kenya Maize Development Program and the FarmersKMDP educates and assists the farmers. Since the farmers have no experience with formal warehouse receipt financing and commercial grade storage, KMDP provides extensive hands-on and continuouseducation. Throughout the growing cycle, KMDP organizes farmers into groups, creates bank accounts,assists with the delivery of the maize to storage, enters into contracts and disburses funds if an agency agreement is required. KMDP also helps its farmers with marketing grain to millers, traders and other institutions while supervising contracts and payments.

1.3.6.4 USAID’s Kenya Microfinance Capacity Building Program’s RoleKEMCAP assists all participants in the scheme, especially the bank and KMDP. Throughout the proc-ess, they serve as facilitators while guaranteeing that critical benchmarks are achieved and necessary resources are brought to bear. In particular, KEMCAP provides assistance to the bank as requested. However, together with KMDP, KEMCAP develops pricing and cost models and also designing sensi-tivity analysis to demonstrate profit potential to all participants in the scheme.

1.3.6.5 The Bank’s RoleOnce a suitable warehouse with a collateral manager is appointed, internal bank systems must be de-signed, beta tested and activated, if not already present. The bank then assesses the market value ofmaize in the terminal market (Nairobi), afterwards lending a percentage of the assigned value againstthe warehouse receipt. In effect, the bank uses the commodity as collateral for each loan. Since the bankis in control of the commodity (through the assistance of the collateral manager) the bank does not need to have a long history or a long relationship with the farmers. Farmers deposit grain; the bank controls the farmer’s grain. If the farmer does not repay the bank loan or if the price hits a predetermined trigger price, the bank sells the grain to recoup potential or real losses.In general, the bank is ultimately responsible for numerous key actions: • Appraising warehouses. • Appointing collateral management. • Drafting loan agreements. • Creating warehouse receipts. • Building personnel capacities and capabilities. • Designing and implements policies and procedures, such as: A database price information and market trends Methodology for determining terminal, loan and trigger pricing Methodology for transmitting pricing information to farmers, the warehouse and the collateral manager Methodology for sales, assignment and release of asset commodities Risk assessment techniques, in particular, market and price exposure (i.e. daily com parison between and continuous trend analysis of terminal market and trigger prices) Loan manuals, contracts, warehouse receipts 1.3.6.6 The Warehouse’s RoleToday, Lesiolo Grain Handling (LHG) is the only credible private-sector vertical-storage facility able to implement warehouse receipt financing. However, a few other independent structures are entering themarketplace. LGH has the option of utilizing its limited space in Nakuru or rent other facilities in areas of the country. The other large scale warehouse facility is owned and operated by the National Cerealsand Produce Board, a government parastatal. It is yet to be privatized and it does not have a history of or willingness to work with the private sector (farmers notwithstanding).The warehouse’s role is relatively straightforward: it weighs, grades and stores the commodity at precise

16

temperatures while maintaining a pest and disease free environment. The warehouse also ensures that thecommodity is safe and insured against theft and other occurrences of loss (robbery, fire, etc.). It is respon-sible for issuing a goods received note to the farmer, complimenting the documentation provided by the agent for the bank or the collateral manager.

1.3.6.7 The Collateral Manager’s RoleThe collateral manager is ultimately responsible for overseeing the interests of the bank, ensuring the grainis graded and weighed correctly. In addition, the manager:

• Issues or endorses warehouse receipts.• Provides loan price and trigger price information to farmers.• Manages the loan contracting, receipting and commodity release process at the warehouse gate, while safeguarding and distributing documentation per established procedures.

1.3.7 Current SituationTwo years have been devoted to operationalize the scheme outlined above. Valuable lessons have been learned throughout the process and maize warehouse receipting is much closer to realization than expect-ed, even though in the third growing cycle since work began, maize warehouse receipting will not become a fixture of the financial services landscape yet. Much work remains to be done, but a large degree of theheavy lifting has been accomplished with new found excitement generated among many banks, additionalstorage capacity secured and a sense of optimistic momentum characterizing the future outlook.

1.3.8 Lessons Learned, Recommendations and the Way Forward1.3.8.1 Lessons Learned

• Time is a critical component and donor patience and perseverance is required (it takes time to improve yields and create historical information which is important to banker’s and other’s projec-tions).• Warehouse receipting is a complicated process with many moving parts, necessitating overarching coordination.• The process will fail without the full participation of an extension agent (KMDP); however, KMDPcannot be expected to “go it alone” since it has limited resources and field specific skills and thereforeoverarching coordination and complimentary technical assistance is absolutely required.• Storage space is not guaranteed; the private sector seeks the highest return at the lowest cost and risk.• Deal competition should be encouraged among banks and not all banks all equal; generally larger banks are more risk adverse and conservative while smaller banks are less risk adverse and oppor-tunistic.• Banks need to understand all the requirements upfront with their participation tracked and graded against the performance and compliance of others.• Guarantees are not necessary since the loan is fully collateralized.

1.3.8.2 Recommendations and the Way ForwardThe time for maize receipting continues to improve as knowledge and experience accrues. This informa-tion must be shared within the larger development finance and business community, including engageddonors, so that momentum is not lost as some funded programs come to end. Institutional know-how is easily lost as projects wind down and people move on. A process must be put into place so that this loss and leakage does not occur. That way, initiatives can be carried forward to ultimate success with the long-runoutcome of creating permanent fixtures to the financial services marketplace that will be leveraged manytimes with new and innovative products and solutions generated – for smallholder agriculture producers and other economically disadvantaged participants in the value chain.

17

BREAK-OUT SESSION TWO: PRODUCER GROUP DYNAMICS

PRESENTERS:

1. George Odo - The REAP to VegCare story: Match made in heaven? Or in bed with the enemy?

2. Lucy Nguru - Making Money with Avocadoes: The Successes and Challenges of Producer Group Linkages with a Lead Firm.

3. Amos Waweru - Breaking Barriers with Smallholder Export Horticulture: The Freshlink VMO Producer Groups Experience.

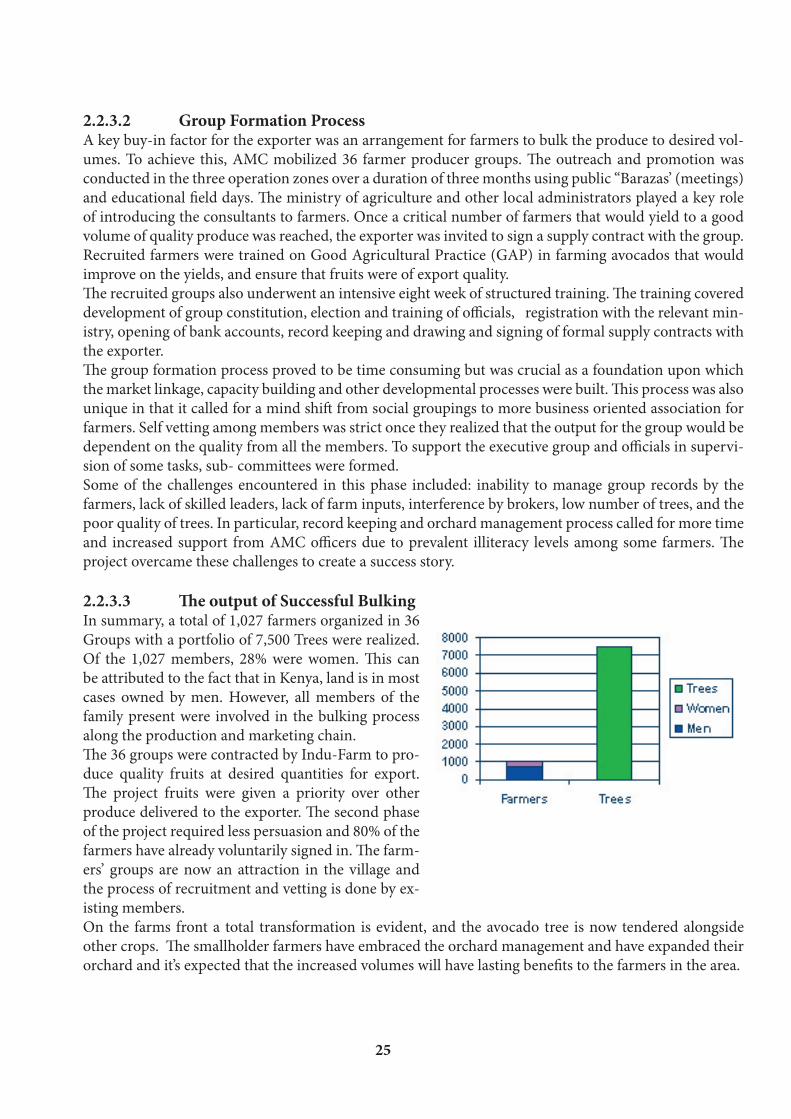

2 BREAK-OUT SESSION TWO: Producer Group Dynamics