Report on Public Issues by Insurance · PDF filePublic Issues by Insurance Companies ... to...

36

Page | 1 Report on Public Issues by Insurance Companies SEBI Committee on Disclosures and Accounting Standards (SCODA)

Transcript of Report on Public Issues by Insurance · PDF filePublic Issues by Insurance Companies ... to...

Page | 1

Report on

Public Issues by

Insurance Companies

SEBI Committee on Disclosures and Accounting

Standards (SCODA)

Page | 2

Table of contents

Section No Section Page

Number

1 Background 3

2 Constitution of the Sub-group 3

3 Scope of the Sub-group 4

4 Recommendations of Sub-group 4

5 Other issues raised by IRDA 10

List of Annexure

Annexure

Number

Details of Annexure Page

No.

Annexure I Industry specific risk factors for insurance sector 13

Annexure II Overview of Insurance Industry 21

Annexure III Comparison table on disclosures made in offer

documents of life insurance companies in other

jurisdictions

23

Annexure IV Glossary of terms used in Insurance Industry 29

Page | 3

Public Issues by Insurance Companies

1. Background:

1.1. There have recently been media reports that insurance companies in India are planning

to raise money from the capital market through initial public offers. Till now, no

company from the insurance sector has accessed the capital markets in India. Since the

nature of business and risks involved in insurance sector are of a different kind, it was

felt that there is a need to review whether the present disclosure requirements in offer

documents as well as those on a continuous basis are suitable and sufficient for the

insurance companies.

1.2. In this context, SEBI has been in receipt of suggestions/ observations from merchant

bankers and international consultants on additional insurance sector-specific

disclosures. SEBI has also received suggestions/comments from IRDA on the

disclosures in offer documents by insurance companies. The areas of disclosures as

identified taking into account the practices followed in other jurisdictions and

suggestions/ comments of the merchant bankers and IRDA were discussed in the SEBI

Committee on Disclosures and Accounting Standards (SCODA) in its meeting held on

August 24, 2009.

1.3. SCODA during its deliberations suggested that the suitability/sufficiency of the existing

provisions of SEBI (ICDR) Regulations to insurance companies may be examined.

2. Constitution of the Sub-group:

2.1.In order to examine the extant regulatory requirements vis a vis the disclosure

requirements for insurance companies, SCODA decided to constitute a sub-group

comprising following members:

Sl Name Designation Organization

1. Ms. Dipti Neelakantan MD & Group COO JM Financials Ltd

2. Shri Prithvi Haldea CMD Prime Database Ltd

3. *Shri R K Sharma Deputy Director Insurance Regulatory and

Development Authority

Page | 4

Sl Name Designation Organization

(IRDA)

4. Dr. S. Subramanian Head, IBD Enam Securities Ltd

5. Shri Shrawan Jalan Director Ernst & Young

6. *Shri Sunil Kadam General Manager Securities and Exchange

Board of India (SEBI)

* Shri R K Sharma, Deputy Director, IRDA and Shri Sunil Kadam, General Manager, SEBI

replaced Ms Mamta Suri, Joint Director, IRDA and Shri Parag Basu, General Manager, SEBI,

respectively due to internal changes in their respective organizations.

2.2 The group places on record its appreciation for the valuable contribution made by Ms

Lakha Nair, Enam securities Ltd, Shri Sanjay Purao, Deputy General Manager, SEBI

and Shri E Balasubramanian, Assistant General Manager, SEBI in preparation of this

report.

3. Scope of the Sub-group:

The following scope of work was identified by the sub-group:

i. Provisions of SEBI (ICDR) Regulations vis a vis insurance companies

ii. Disclosures by insurance companies

iii. Continuous disclosure requirements for insurance companies

4. Recommendations of Sub-group

4.1. Amendment to SEBI(ICDR) Regulations

The provisions of SEBI (ICDR) Regulations have been examined primarily with regard

to its suitability and sufficiency with respect to disclosures by insurance companies. The

provisions of SEBI (ICDR) were discussed. The sub-group agreed that the provisions of

SEBI (ICDR) Regulations shall be applicable to insurance companies. The sub-group

after deliberations gave their comments on certain provision of the SEBI (ICDR)

Regulations along with the recommendations.

The recommendations of the sub-group are as follows:

Page | 5

a) Monitoring Agency: Regulation 16(1) of SEBI (ICDR) Regulations provides that if

the issue size exceeds Rs. 500 crore, the use of issue proceeds has to be monitored

by a public financial institution or a scheduled commercial bank. The Regulation

also states that the said provision is not applicable in case of issues made by a bank

or a financial institution. Sub-group noted that the said dispensation was given as

banks generally raise funds to meet the capital adequacy norms set out and

monitored by RBI, the sectoral regulator. Sub-group further noted that in case of

insurance companies too, the funds would be raised primarily to maintain/enhance

solvency requirement, as stipulated by IRDA. Further, IRDA stipulates periodic

reporting of solvency ratios and has also specified investment regulations for

investing the funds raised for meeting the solvency margin. In view of the above,

the sub-group recommends that insurance companies may be exempted from the

provision of Regulation 16 of SEBI (ICDR) Regulations in line with exemption

given to banks and financial institutions.

b) Disclaimer clause: In the case of banks, section XI (K) of part A of Schedule

VII of SEBI (ICDR) Regulations provide for disclosure of a disclaimer clause

of RBI. Similarly, a disclaimer clause of IRDA may be provided for in the offer

documents of insurance companies.

4.2.Disclosures by Insurance Companies:

4.2.1. Industry- specific Risk Factors for Insurance Companies:

The insurance industry is different from other industries and has risks which are

unique to it. In order to get an understanding of risks specific to the insurance

industry, offer documents of certain insurance companies which came out with

issue of capital in other jurisdictions were studied. Based on the risk factors

disclosed in such offer documents, following are the minimum broad industry

specific risk areas that needs to be disclosed:

i. Claims arising out of catastrophic losses (natural and man-made), which

could materially and adversely impact the profitability or cash flow of the

insurance companies.

Page | 6

ii. Concentrated surrenders which may materially affect cash flows, results of

operations and financial condition.

iii. Differences in future actual claims resulting from the assumptions used in

pricing and establishing reserves for insurance and annuity products which

may materially affect earnings.

iv. Risk with reference to concentration by region/type of policies of the

insurance company.

v. The assumptions based on which the embedded value is calculated and

disclosed may vary significantly from time to time / among industry players.

vi. Deviations in mortality/morbidity rates from those predicted in determining

reserve amounts.

vii. Deviations in persistency/lapse rates from those predicted in determining

reserve amounts

viii. Inability to attract and retain productive agents in a growing competitive

business environment.

ix. Fluctuations in reserves due to guaranteed benefits

x. Inability to obtain reinsurance on a timely basis or at all, which results in

bearing increased risks or reduce the level of our underwriting

commitments.

xi. Default by one or more of our reinsurers which could materially affect the

financial condition and results of operations.

xii. Regulatory restrictions on investments by insurance companies

xiii. Exposure to recovery related risks including for foreclosure of the

mortgages

xiv. Inability to accurately predict benefits, claims and other costs or to manage

such costs through loss limitation methods, which could have a material

adverse effect on the operations and financial condition

The sub-group recommends that the aforementioned list may act as guidance for

companies while disclosing the risk factors in the offer documents. The sub-group

also compiled detailed risk factors for insurance companies which are placed at

Annexure I.

Page | 7

The sub-group recommends that:

a. The detailed risk factors as identified by sub-group may be placed on the

website of IRDA which may act as guidance to insurance companies

coming out with IPO.

b. SEBI may prescribe the disclosure of aforementioned list of risk factors in

the offer documents of insurance companies through circular or standard

observations.

4.2.2. Disclosure on Overview of the Insurance Industry:

The SEBI (ICDR) Regulation does not prescribe the format or the contents of

industry overview which need to be disclosed in the offer documents for any

industry. However, considering the fact that no insurance company in India has

come out with an issue so far, it is felt necessary that the investors get a broad

overview of the insurance industry. In view of this, broad parameters under which

the disclosure on insurance industry overview may be made have been listed and

placed in Annexure II.

The sub-group recommends that this list may be placed in the website of IRDA,

which may act as guidance for insurance companies coming out with issues.

4.2.3. Disclosure of Financial Information:

It is observed that the components of financial statements of insurance companies

are significantly different from other companies. An insurance company prepares

two types of income accounts i.e. policy holder’s account (Revenue account) and

shareholder’s account (profit and loss account). IRDA has prescribed the formats

in which the financials of the insurance companies need to be submitted to them

on a periodic basis. On the other hand, provisions regarding disclosure of

financial information in SEBI (ICDR) Regulations are general and are applicable

to all companies. The subgroup noted that banking companies follow format of

financial statements prescribed under Banking Regulation Act, 1949 and similarly

insurance companies may follow formats specified by IRDA.

Page | 8

Sub-group recommended that the financial disclosure for insurance companies

may be as per the format specified by IRDA.

4.2.4. Specific Disclosures which are followed in other Jurisdictions:

The sub-group carried out an analysis of the specific disclosures which are

followed in other jurisdictions. A detailed comparative chart along with the

comments of the IRDA on each disclosure item in case of life insurance

companies is attached as Annexure III. It is observed that the extant disclosure

norms prescribed by IRDA are by and large at par with the international practice

in vogue in various jurisdictions.

Sub-group recommends that following additional disclosures applicable in other

jurisdictions shall be included in the offer documents of life insurance companies

i. Gross premium- along with Geographic segmentation

ii. Cross selling

iii. Distribution network

iv. Persistency

v. Operating expense ratio

vi. Investment yield

vii. Embedded value Report comprising of:

New Business Value

Value of in force business

Embedded value

viii. Investment of above 5% of total Funds in each sector through equity &

bonds

ix. Reinsurance

x. Interest rate sensitivity

xi. Liability for future policy benefits and policy holders account balances.

xii. NBAP

xiii. Manner of arriving at unrealized gain/losses –under IFRS or Indian

equivalent

Page | 9

As regards the disclosure on NBAP (New Business Achieved Profit) IRDA has

reservations on mandating the said disclosure for insurance companies due to lack

of uniformity/standardization of approach adopted for calculation, as of now.

Considering the nascent stage of the insurance industry in India and lack of

understanding of this business by investors in general, the sub-group felt that

there is a need for an expert opinion on both the Embedded Value (EV) and

New Business Value (NBV) which together reflect the fair value of the

business of an insurance company. Accordingly, sub-group recommends that

report of an independent actuary on the EV and NBV of the insurance

company should be made a part of the offer document. The contents and

format of the EV/NBV reports and criteria for actuaries who are authorized

to prepare such report may be prescribed by IRDA.

The sub-group recommends that SEBI may mandate the disclosure of

aforementioned list of disclosure items in the offer documents of insurance

companies through circular or standard observations.

4.2.5. Glossary of terms used in the Insurance Industry:

In order to familiarize the investors with terms used in insurance industry and to

standardize the definition and understanding of such terms, the sub-group felt that

a “Glossary of the terms used in Insurance industry” may be prepared. IRDA

provided a “Glossary of the terms used in Insurance industry” which is placed in

Annexure IV. This glossary of terms may act as guidance for insurance

companies coming out with issues.

The sub group recommends that the glossary may be placed on the website of

IRDA.

4.2.6. Continuous Disclosure Requirements for Insurance Companies:

The continuous disclosure requirements i.e the disclosure/reporting requirements

of companies after its shares are listed at the stock exchanges are prescribed

through the listing agreement. The provisions of the listing agreement have been

examined in light of continuous disclosure requirements of the insurance

Page | 10

companies. It may be noted that clause 41 of the listing agreement prescribes the

format in which the listed companies are required to disclose the financial

information on a quarterly basis to the stock exchanges. Further, a separate

format of financial and a format of limited review report has been provided for

banks under the clause 41 of the listing agreement. On the same lines, a separate

format of financial information and a format of limited review report were

recommended for the insurance companies.

SCODA suggested the sub-group to re-work on the formats specified in Clause 41

of the Listing Agreement and retain only critical portions, as the same needs to be

published in the newspapers. Further, SCODA suggested that the sub-group

should classify those disclosures which need to be filed with the exchanges and

those which need to be published.

5. Other issues raised by IRDA:

5.1. Advertisements regarding public issues: IRDA requires that all advertisements

issued by insurance companies be filed with IRDA for vetting at least 30 days before

publishing the same.

Sub-group noted that issue advertisements are typically made post the filing of the red

herring prospectus which leaves a very short time between the date of filing of RHP and

issue opening date. Sub-group recommended that the issue advertisements made by

insurance companies being statutory advertisements, may be as per the provisions of

SEBI (ICDR) Regulations only.

5.2. Objects of issue: The IRDA representative suggested that insurance companies

should be allowed to raise money only for the following objects:

a. To augment the solvency requirement

b. For general corporate purposes

c. For any other purpose which has a specific approval of IRDA

The sub-group noted that SEBI (ICDR) Regulations does not have any specific

restriction on nature of objects for which a company can raise money from the

public. Hence, the sub-group recommends that SEBI (ICDR) Regulations need not

Page | 11

be amended in this regard. However, IRDA may, if it considers necessary issue

guidelines to the insurance companies in this regard.

5.3. Issuance of partly-paid shares: The IRDA representative stated that partly-paid

shares should not be allowed as it may inflate the capital.

Sub-group noted that the Companies Act, 1956 permits issuance of partly paid up

shares by companies. Hence, placing such restriction through subordinate legislation

may not be appropriate and may not also be legally tenable. Therefore sub-group

recommended that restrictions, if considered necessary, can be put by IRDA under its

regulatory powers.

5.4. Definition of Promoters: IRDA stated that as per the existing provisions, all the

shareholders of insurance companies are treated as promoters and employees who

have been issued shares under ESOP scheme are excluded. Further, any transfer of

shares of more than one percent by the pre-IPO shareholders requires prior approval

of IRDA. Therefore, IRDA suggested that the definition of ‘Promoter’ under SEBI

(ICDR) Regulations may be amended as follows:

“Promoters mean the shareholders of the company at the date of fi ling of the

application for IPO with IRDA/ SEBI. However, employees / officers who have

been issued shares under ESOP scheme should be excluded“

The sub-group recommends that the existing definition of promoters as per the

SEBI (ICDR) Regulations should be applicable to the insurance companies as well

and that IRDA may issue separate guidelines to insurance companies in relation to

pre-IPO transfer of shares, if so considered necessary. However, disclosure

regarding any such restriction shall be made in the offer document.

5.5. Relaxation from eligibility criteria: The IRDA representative was of the view that

insurance companies may find it difficult to comply with the eligibility requirement

(i.e. profitability criteria), since gestation period of life insurance business is

comparatively longer and it takes around 6 to 7 years for a life insurer to achieve

break even. IRDA representative enquired whether such companies can still raise

capital through fixed price issue.

Page | 12

The sub-group felt that there is no need to provide specific relaxation from the

eligibility conditions to insurance companies since the companies which do not

comply with the profitability criteria can still raise the capital through book

building process.

5.6. Key Management Personnel : The IRDA representative suggested the inclusion of

the following officers in an insurance company in the definition of key

management personnel : Chief Executive, Chief Marketing Officer, Appointed

Actuary, Chief Investment Officer, Chief of Internal Audit and Chief Finance

Officer.

In this context, sub-group noted that the key management personnel generally

means and includes only employees in management. The sub-group suggested that

the provisions of extant SEBI (ICDR) Regulations may apply as it is and that

IRDA, if it so considers necessary, may issue guidelines to the insurance

companies specifying the inclusion of additional persons as key management

personnel.

5.7. Disclosure with regard to uniform financial denomination: The IRDA Accounting

Regulations require that figures in all financial statements should be in

“thousands”. It was brought to the notice of IRDA representative that SEBI

(ICDR) Regulations do not specify any particular denomination in which the

financial information shall be disclosed. The clause VIII (G) of Part A of Schedule

VIII of SEBI (ICDR) Regulations requires the issuer to use one standard financial

unit in the offer document.

The sub-group noted that insurance companies can easily comply with the

requirement of IRDA on denomination without any conflict with the provisions of

SEBI (ICDR) Regulations and hence suggested no change.

*****

Page | 13

Annexure I: INDUSTRY SPECIFIC RISK FACTORS FOR INSURANCE SECTOR (LIFE and NON-

LIFE)

General

No insurance company is yet listed in the Indian capital market. Insurance sector has a unique operation and

it presents various types of unique risks. Investors should read the section on “Insurance Industry” to

acquaint themselves with the key features of this sector. In addition, investors should consider the risks

associated with the industry in which the Company operates as well as those relating specifically to it.

Interest Rate Risk

Changes in interest rates may materially and adversely affect our profitability. The profitability of some of the

products and investment returns of insurance companies are highly sensitive to interest rate fluctuations, and

changes in interest rates could adversely affect our investment returns and results of operations. In periods of rising

interest rates, while the increased investment yield will increase the returns on newly added assets in our investment

portfolios, surrenders and withdrawals of existing insurance policies may also increase as policyholders seek to buy

products with perceived higher returns. These surrenders and withdrawals may result in cash payments requiring the

sale of invested assets at a time when the prices of those assets are adversely affected by the increase in market

interest rates, potentially resulting in realized investment losses. These cash payments to policyholders would result

in a decrease in total invested assets and a potential decrease in net income. Moreover, a rise in interest rates would

adversely affect our shareholders’ equity in the immediate fiscal year due to a decrease in the fair value of our fixed

income investments. Conversely, a decline in interest rates could result in reduced investment returns on our newly

added assets and have an adverse impact on our profitability. During periods of declining interest rates, our average

investment yield will decline as our maturing investments, as well as bonds that are redeemed or prepaid to take

advantage of the lower interest rate environment, are replaced with new investments carrying lower yields, which

would adversely affect our profitability. In addition, the liabilities associated with our life insurance policies tend to

have a longer duration than our investment assets, which may result in the re-investment returns of our maturing

investments being lower than the average guaranteed pricing rate for our insurance policies in a declining interest

rate environment.

Maturity Risk

Due to the limited availability of long-term fixed income securities in the Indian capital market and the legal

and regulatory restrictions on the types of investments we may make, we are unable to match closely the

duration of our assets and liabilities, which increases our exposure to interest rate risk. Restrictions under the

IRDA regulations on the asset classes in which we may invest, as well as the limited availability in the Indian

market of long duration investment assets capable of matching the duration of our liabilities, can result in the

duration of our assets being shorter than that of our liabilities, in particular, our liabilities in life insurance

operations. If we are unable to match closely the duration of our assets and liabilities, we will continue to be

exposed to risks related to interest rate changes, which would materially and adversely affect our results of

operations and financial condition.

Liquidity Risk

Differences in future actual claims results from the assumptions used in pricing and establishing reserves for

our insurance and annuity products may materially and adversely affect our earnings. Our earnings depend

significantly upon the extent to which our actual claims results are consistent with the assumptions used in setting

the prices for our products and establishing the liabilities in our financial statements for our obligations for future

policy benefits and claims. Our assumptions include those for investment returns, mortality, morbidity, expenses and

persistency, as well as macro-economic factors such as inflation. To the extent that trends in actual claims results are

less favorable than our underlying assumptions used in establishing these liabilities, and these trends are expected to

continue in the future, we could be required to increase our liabilities. Any such increase could have a material

adverse effect on our profitability and, if significant, our financial condition. Any material impairment in our

solvency level could change our customers' or our business associates' perception of our financial health, which in

turn could adversely affect our sales, earnings and operations.

Page | 14

Concentrated surrenders may materially and adversely affect our cash flows, results of operations and

financial condition. Under normal circumstances, it is generally possible for insurance companies to estimate the

overall amount of surrenders in a given period. However, the occurrence of emergency events that have significant

impact, such as sharp declines in customer income due to a severe deterioration in economic conditions, radical

changes in relevant government policies, loss of customer confidence in the insurance industry due to the weakening

of the financial strength of one or more insurance companies, or the severe weakening of our financial strength, may

trigger massive surrenders of insurance policies. If this were to occur, we would have to dispose of our investment

assets, possibly at unfavorable prices, in order to make the significant amount of surrender payments. This could

materially and adversely affect our cash flows, results of operations and financial condition.

Investments Risk

We may incur significant losses on our investments, which may cause our investment income to decrease, and

could have a material adverse effect on our financial condition and results of operations. We primarily invest

in fixed income products such as term deposits, government bonds, subordinated bonds issued by financial

institutions, corporate bonds and equity. Our investment returns, and thus our profitability, may be adversely

affected from time to time by conditions affecting our specific investments and, more generally, by market

fluctuations as well as general economic, market and political conditions. In particular, our ability to make a profit

on our insurance products depends in part on the returns on investments supporting our obligations under these

products, and the value of specific investments may fluctuate substantially. Future movements in market interest

rates, unfavorable conditions in the Indian capital market or other factors may cause our investment income to

decrease significantly, and could have a material adverse effect on our financial condition and results of operations.

Catastrophic Losses Risk

Catastrophic losses could materially reduce our profitability or cash flow. Our insurance operations expose us

to claims arising out of catastrophes. Earthquakes, typhoons, floods, wind, fires, explosions, industrial accidents,

epidemics, terrorist attacks, and other events may cause catastrophes, and the occurrence and severity of

catastrophes are inherently unpredictable. It is possible that both the frequency and severity of natural disasters may

increase in the future. We establish reserves only after an assessment of potential losses relating to catastrophes that

have taken place. However, we cannot assure you that such reserves will be sufficient to pay for all related claims.

Although we carry some reinsurance to reduce our catastrophe loss exposures, due to limitations in the underwriting

capacity and terms and conditions of the reinsurance market as well as difficulties in assessing our exposures to

catastrophes, this reinsurance may not be sufficient to protect us adequately against losses. As a result, one or more

catastrophic events could materially reduce our profits and cash flows and harm our financial condition.

Reinsurance Risk

If we are not able to obtain reinsurance on a timely basis or at all, we may be required to bear increased risks

or reduce the level of our underwriting commitments. Our ability to obtain reinsurance on a timely basis and at a

reasonable cost is subject to a number of factors, including prevailing market conditions that are beyond our control.

The availability and cost of reinsurance may affect the volume of our business as well as our profitability. In

particular, we may be unable to maintain our current reinsurance coverage or to obtain other reinsurance coverage in

adequate amounts and at favorable rates. If we are unable to renew our expiring coverage or to obtain new

reinsurance coverage, either our net risk exposure would increase or, if we are unwilling to bear an increase in net

risk exposures, our overall underwriting capacity and the amount of risk we are able to underwrite would decrease.

To the extent we are not able to obtain reinsurance on a timely basis and at a reasonable cost, or at all, our business,

financial condition and results of operations would be materially and adversely affected.

A default by one or more of our reinsurers could materially and adversely affect our financial condition and

results of operations. Like other major insurance companies in the world, we transfer some of the risk we assume

under the insurance policies we underwrite to reinsurance companies in exchange for a portion of the premiums we

receive in connection with the underwriting of these policies. Although reinsurance makes the reinsurer liable to us

for the risk transferred, it does not discharge our liability to our policyholders. As a result, we are exposed to credit

risk with respect to reinsurers in all lines of our insurance business. In particular, a default by one or more of our

reinsurers under our existing reinsurance arrangements would increase our financial losses arising out of a risk we

have insured, which would reduce our profitability and may adversely affect our liquidity position. In the event of a

Page | 15

catastrophic loss that affects a significant number of Indian insurers, the reinsurers may not b able to pay us on a

timely basis, or at all.

Embedded Value Risk

The embedded value information we present in this prospectus is based on several assumptions and may vary

significantly as those assumptions are changed. In order to provide investors with an additional tool to understand

our economic value and business results, we have disclosed information regarding our embedded value, as discussed

in the section entitled, "Embedded Value". These measures are based on a discounted cash flow valuation

determined using commonly applied actuarial methodologies. Standards with respect to the calculation of embedded

value are still evolving, however, and there is no single adopted standard for the form, determination or presentation

of the embedded value of an insurance company. Moreover, because of the technical complexity involved in

embedded value calculations and the fact that embedded value estimates vary materially as key assumptions are

changed, you should read the discussion under the section entitled "Embedded Value". You should use special care

when interpreting embedded value results and should not place undue reliance on them.

Regulatory Risks

Regulations may restrict our ability to operate. The insurance industry is subject to extensive regulation by

IRDA. IRDA has broad administrative powers to regulate many aspects of the insurance business, which include

premium rates, marketing practices, advertising, policy forms and capital adequacy. IRDA is concerned primarily

with the protection of policyholders rather than shareholders. Insurance laws and regulations impose restrictions on

the amount and type of investments, prescribe solvency standards that must be met and maintained and require the

maintenance of reserves. Premium rate regulation is common across all of our lines of business and may make it

difficult for us to increase premiums to adequately reflect the cost of providing insurance coverage to our

policyholders. In our underwriting, we rely heavily upon information gathered from third parties such as credit

report agencies and other data aggregators. The use of this information is also highly regulated and any changes to

the current regulatory structure could materially affect how we underwrite and price premiums.

Our business is highly regulated and we may be materially and adversely affected by future regulatory

changes. Our life insurance and general insurance businesses are regulated primarily by IRDA and we are subject

to laws regulating all aspects of our insurance business. In addition, our securities business is regulated by SEBI.

Compliance with applicable laws, rules and regulations may restrict our business activities. Furthermore, these laws,

rules and regulations may change from time to time and we cannot assure you that future legislative or regulatory

changes, including deregulation, would not have a material adverse effect on our business, financial condition and

results of operations. We cannot predict at this time the effect of potential regulatory changes on our business and

profitability. Moreover, failure to comply with any of the numerous laws, rules and regulations to which we are

subject could result in fines, suspension or, in extreme cases, business license revocation, which could materially

and adversely affect us. In particular, future laws, rules and regulations, or the interpretation of existing or future

laws, rules and regulations, may have a material adverse affect on our business, financial condition and results of

operations.

The Indian insurance regulatory regime is undergoing significant change as it moves toward a more transparent

regulatory process. Some of these changes may result in additional costs or restrictions on our activities. In

particular, some of the changes may require us to take additional steps to comply with new rules and regulations on

a timely basis. We cannot assure you that we will be able to achieve full compliance with any such new rules and

regulations within any prescribed timeframe, and any such compliance may result in our incurring increased

compliance and other costs. Moreover, because the terms of our products are subject to regulations, changes in

regulations may affect our profitability on the policies and contracts we issue.

Regulatory investigations and the resulting sanctions or penalties may adversely affect our reputation,

business, results of operations and financial condition. We may also be subject to regulatory actions from time to

time. A substantial legal liability or a significant regulatory action could have an adverse effect on us or cause us

reputational harm, which in turn could harm our business prospects. We are subject to periodic examinations by

IRDA, which may impose sanctions, fines and other penalties on us. If IRDA, in connection with their future audits

or examinations, requires us to take corrective measures or impose administrative penalties on us or if as a result we

Page | 16

become the target of negative publicity, our corporate image and reputation and the credibility of our management

may be materially and adversely affected.

New accounting pronouncements may significantly affect our financial statements for the current and future

years, and may materially and adversely affect our reported net profits and shareholders’ equity, among

other things.

Solvency Risks

Our ability to comply with minimum solvency requirements stipulated by IRDA is affected by a number of

factors, and our compliance may force us to raise additional capital, which could be dilutive to you, or could

reduce our growth. We are required by IRDA regulations to maintain our solvency at a level in excess of minimum

solvency levels. Our minimum solvency is affected primarily by the policy reserves we are required to maintain

which, in turn, are affected by the volume of insurance policies we sell and by regulations on the determination of

statutory reserves. Our solvency is also affected by a number of other factors, including the profit margin of our

products, returns on our investments, underwriting and acquisition costs, and policyholder and shareholder

dividends. If we continue to grow rapidly in the future, or if the required solvency level is increased in the future, we

may need to raise additional capital to meet our solvency requirement, which would be dilutive to you. If we are not

able to raise additional capital, we may be forced to reduce the growth of our business.

Insurance Risk

Impact of Lapse Rates, Expense Level, mortality / Morbidity Rates

Legal Risk

We may suffer losses from unfavorable outcomes from litigation and other legal proceedings. Legal actions are

inherent in our businesses and operations. We are subject to litigation and other legal proceedings as part of the

claims process, the outcomes of which are uncertain. We maintain reserves for these legal proceedings as part of our

reserves. We also maintain separate reserves for legal proceedings that are not related to the claims process. In the

event of an unfavorable outcome in one or more legal matters, our ultimate liability may be in excess of amounts we

have currently reserved for and such additional amounts may be material to our results of operations and financial

condition.

As industry practices and legal, judicial, social and other conditions change, unexpected and unintended issues

related to claims and coverage may emerge. These issues may adversely affect our financial condition and results of

operations by either extending coverage beyond our underwriting intent or by increasing the number and size of

claims. In some instances, these changes may not become apparent until some time after we have issued insurance

contracts that are affected by the changes.

Risk Management Risk

Our risk management and internal reporting systems, policies and procedures may leave us exposed to

unidentified or unanticipated risks, which could materially and adversely affect our businesses or result in

losses. Our policies and procedures to identify, monitor and manage risks may not be fully effective. Many of our

methods of managing risk and exposures are based upon our use of observed historical market behavior or statistics

based on historical models. As a result, these methods may not predict future exposures, which could be

significantly greater than what the historical measures indicate. Other risk management methods depend upon the

evaluation of information regarding markets, customers or other matters that is publicly available or otherwise

accessible to us, which may not always be accurate, complete, up-to-date or properly evaluated. In addition, a

significant portion of business information needs to be centralized from our many branch offices. Management of

operational, legal and regulatory risks requires, among other things, policies and procedures to record properly and

verify a large number of transactions and events, and these policies and procedures may not be fully effective.

Failure or the ineffectiveness of these systems could materially and adversely affect our business or result in losses.

Page | 17

We are likely to offer a broader and more diverse range of insurance and investment products in the future as the

insurance market in India continues to develop. At the same time, we anticipate that the relaxing of regulatory

restraints will result in our being able to invest in a significantly broader range of asset classes. The combination of

these factors will require us to continue to enhance our risk management capabilities and is likely to increase the

importance of our risk management policies and procedures to our results of operations and financial condition. If

we fail to adapt our risk management policies and procedures to our changing business, our business, results of

operations and financial condition could be materially and adversely affected. Catastrophes could materially reduce

our earnings and cash flow.

We may experience failures in our information technology system, which could materially and adversely

affect our business, results of operations and financial condition. We depend heavily on our information

technology system to record and process our operational and financial data and to provide reliable services. We may

be subject to severe failures in our information technology system arising from natural disasters or failures of public

infrastructure, our information technology infrastructure or our applications software systems that are wholly or

partially beyond our control. Although we back up our business data daily and have an emergency disaster recovery

center located at a site different from our production data center, any material disruption to the operation of our

information technology system could have a material adverse effect on our business. Our failure to address these

problems could result in our inability to perform, or prolonged delays in performing, critical business operational

functions, the loss of key business data, or our failure to comply with regulatory requirements, which could

materially and adversely affect our business operations, customer service and risk management, among others. This

could in turn materially and adversely affect our business, results of operations and financial condition

Competition Risk

Competition in the Indian insurance industry is increasing and our business and prospects will be harmed if

we are not able to compete effectively as well as have a material adverse effect on our financial condition and

results of operations by, among other things: reducing our market share in our principal lines of business;

decreasing our margins and spreads; reducing the growth of our customer base; increasing our policy

acquisition costs; increasing our operating expenses, such as sales and marketing expenses; and increased

turnover of management and sales personnel. Some of our competitors may have advantages over us in one or

more areas, such as financial strength, management capabilities, resources, operating experience, market share,

distribution channels and capabilities in pricing, underwriting and claims settlement. In addition, we face potential

competition from commercial banks, some of which invest in, or form alliances with, existing insurance companies

to offer insurance products and services that compete against those offered by us. These commercial banks may also

establish subsidiaries of their own to engage in insurance business directly. Such potential competitors may further

increase the competitive pressures we experience.

Competition from foreign-invested life insurance companies is likely to increase in the future, as restrictions

on their operations in India are relaxed. Moreover, foreign-invested life insurance companies may have

access to greater financial, technological or other resources than we do.

We are likely to face increasing competition from companies offering products that compete with our own. In

addition to competition from insurance companies, we face competition from other companies that may offer

products that compete with our own, including real estate companies, mutual fund companies and other financial

services providers.

Market Growth Risk

The rate of growth of the Indian insurance market may not be as high or as sustainable as we anticipate.

The rate of growth of the Indian insurance market may not be as high or as sustainable as we anticipate. This may be

the case even though we expect the insurance market in India to expand and the penetration rate to rise with the

growth of the Indian economy and household wealth, continued social welfare reform, demographic changes and the

opening of the Indian insurance market to foreign participants. The impact on the Indian insurance industry of

certain trends and events, such as the pace of economic growth in India and the ongoing reform of the social welfare

system is unpredictable and consequently, the growth and development of the Indian insurance market is subject to a

number of uncertainties that are beyond our control.

Page | 18

An economic slowdown in the country, such as the one experienced following the recent global financial crisis,

may reduce the demand for our products and services and have a material adverse effect on our results of

operations, financial condition and profitability. In an economic downturn characterized by higher

unemployment, lower family income, lower corporate earnings, lower business investment and lower consumer

spending, the demand for our insurance products and services could be adversely affected. In addition, we may

experience an elevated incidence of claims and lapses or surrenders of policies. Our policyholders may also choose

to defer paying insurance premiums or stop paying insurance premiums altogether.If the Indian economy continues

to experience a slower growth or a significant downturn, our results of operations and financial condition would be

materially and adversely affected.

Agents’ Risk

All of our insurance agents are required to obtain a qualification certificate from IRDA; any changes in the

regulatory policies with regard to the agents may materially and adversely affect our business. Moreover, our

growth is dependent on our ability to attract and retain productive agents. A substantial portion of our business

is conducted through agents. Competition for agents from insurance companies and other business institutions may

force us to increase the compensation of our agents and sales representatives, which would increase operating costs

and reduce our profitability.

If we are unable to develop other distribution channels for our products, our growth may be materially and

adversely affected. Banks and post offices are rapidly emerging as some of the fastest growing distribution

channels in India. We do not have exclusive arrangements with any of the banks and post offices through which we

sell insurance and annuity products, and thus our sales may be materially and adversely affected if one or more

banks or post offices choose to favor our competitors' products over our own.

Agent misconduct is difficult to detect and deter and could harm our reputation or lead to regulatory sanctions or

litigation costs. Agent misconduct could result in violations of law by us, regulatory sanctions, litigation or serious

reputational or financial harm. Misconduct could include engaging in misrepresentation or fraudulent activities

when marketing or selling insurance policies or annuity contracts to customers; hiding unauthorized or unsuccessful

activities, resulting in unknown and unmanaged risks or losses; or otherwise not complying with laws or our control

policies or procedures. We cannot always deter agent misconduct, and the precautions we take to prevent and detect

these activities may not be effective in all cases. We cannot assure you that agent misconduct will not lead to a

material adverse effect on our business, results of operations or financial condition.

Other Risks

– We depend on select actuarial personnel and could be materially and adversely affected by the loss of their

services.

– A perceived reduction in our financial strength could increase policy surrenders and withdrawals and

damage our relationship with our creditors, our counterparties and the distributors of our products.

– Prospective investors should acquaint themselves with the Financial Statements, drawn specifically for the

insurance companies.

– Contingent liabilities could adversely affect the financial condition and results of operations of the

insurance company.

– Investment in the relatives/associates of the Promoters/ Directors of the Insurance Company can be

detrimental to the interests of our company.

– Risk with reference to concentration by region/type of policies of the Insurance Company

– Insurance Companies are subject to restrictions on payments of dividends

– We will incur increased costs as a result of being a listed company.

The insurance industry is cyclical, which may impact our results. The insurance industry is cyclical. Although

no two cycles are the same, insurance industry cycles have typically lasted for periods ranging from two to six years.

The segments of the insurance markets in which we operate tend not to be correlated to each other, with each

segment having its own cyclicality. Periods of intense price competition due to excessive underwriting capacity,

periods when shortages of underwriting capacity permit more favorable rate levels, consequent fluctuations in

underwriting results and the occurrence of other losses characterize the conditions in these markets. Historically,

Page | 19

insurers have experienced significant fluctuations in operating results due to volatile and sometimes unpredictable

developments, many of which are beyond the direct control of the insurer, including competition, frequency of

occurrence or severity of catastrophic events, levels of capacity, general economic conditions and other factors. This

may cause a decline in revenue at times in the cycle if we choose not to reduce our product prices in order to

maintain our market position, because of the adverse effect on profitability of such a price reduction. We can be

expected therefore to experience the effects of such cyclicality and changes in customer expectations of appropriate

premium levels, the frequency or severity of claims or other loss events or other factors affecting the insurance

industry that generally could have a material adverse effect on our results of operations and financial condition.

The insurance and related businesses in which we operate may be subject to periodic negative publicity,

which may negatively impact our financial results. The nature of the market for the insurance and related

products and services we provide is that we interface with and distribute our products and services ultimately to

individual consumers. There may be a perception that these purchasers may be unsophisticated and in need of

consumer protection. Accordingly, from time to time, consumer advocate groups or the media may focus attention

on our products and services, thereby subjecting our industries to periodic negative publicity. We may also be

negatively impacted if another company in one of our industries engages in practices resulting in increased public

attention to our businesses. Negative publicity may result in increased regulation and legislative scrutiny of industry

practices as well as increased litigation, which may further increase our costs of doing business and adversely affect

our profitability by impeding our ability to market our products and services, requiring us to change our products or

services or increasing the regulatory burdens under which we operate.

The impact of investigations of possible anti-competitive practices by the company cannot be predicted and

may have a material adverse impact on our results of operations, financial condition and financial strength

ratings.

We may be exposed to environmental liability from our commercial mortgage loan and real estate

investments. As a commercial mortgage lender, we customarily conduct environmental assessments prior to making

commercial mortgage loans secured by real estate and before taking title through foreclosure to real estate

collateralizing delinquent commercial mortgage loans held by us. Based on our environmental assessments, we

believe that any compliance costs associated with environmental laws and regulations or any remediation of affected

properties would not have a material adverse effect on our results of operations or financial condition. However, we

cannot provide assurance that material compliance costs will not be incurred by us.

The effects of emerging claims and coverage issues on our business are uncertain. As industry practices and

legal, judicial, social and other conditions change, unexpected and unintended issues related to claims and coverage

may emerge. These issues may adversely affect our business by either extending coverage beyond our underwriting

intent or by increasing the number or size of claims. In some instances, these changes may not become apparent

until some time after we have issued insurance or reinsurance contracts that are affected by the changes. As a result,

the full extent of liability under our insurance and reinsurance contracts may not be known for many years after a

contract is issued. Recent example of emerging claims and coverage issues include:

larger settlements and jury awards in cases involving professionals and corporate directors and officers

covered by professional liability and directors and officers liability insurance and

a growing trend of plaintiffs targeting property and casualty insurers in class action litigation related to

claims handling, insurance sales practices and other practices related to the conduct of our business.

We may be unable to accurately predict benefits, claims and other costs or to manage such costs through our

loss limitation methods, which could have a material adverse effect on our results of operations and financial

condition. Our profitability depends in large part on accurately predicting benefits, claims and other costs, including

medical and dental costs, and predictions regarding the frequency and magnitude of claims on our disability and

property coverage. It also depends on our ability to manage future benefit and other costs through product design,

underwriting criteria, utilization review or claims management and, in health and dental insurance, negotiation of

favorable provider contracts. Utilization review is a review process designed to control and limit medical expenses,

which includes, among other things, requiring certification for admission to a health care facility and cost-effective

ways of handling patients with catastrophic illnesses. Claims management entails the use of a variety of means to

mitigate the extent of losses incurred by insureds and the corresponding benefit cost, which includes efforts to

improve the quality of medical care provided to insureds and to assist them with vocational services. The aging of

Page | 20

the population and other demographic characteristics and advances in medical technology continue to contribute to

rising health care costs. Our ability to predict and manage costs and claims, as well as our business, results of

operations and financial condition may be adversely affected by:

changes in health and dental care practices;

inflation;

new technologies;

the cost of prescription drugs;

clusters of high cost cases;

changes in the regulatory environment;

economic factors;

the occurrence of catastrophes; and

numerous other factors affecting the cost of health and dental care and the frequency and severity of

claims in all our business segments.

The judicial and regulatory environments, changes in the composition of the kinds of work available in the

economy, market conditions and numerous other factors may also materially adversely affect our ability to manage

claim costs. As a result of one or more of these factors or other factors, claims could substantially exceed our

expectations, which could have a material adverse effect on our results of operations and financial condition.

As industry practices and legal, judicial, social and other environmental conditions change, unexpected and

unintended issues relating to claims and coverage may emerge. These issues could materially adversely affect our

results of operations and financial condition by either extending coverage beyond our underwriting intent or by

increasing the number or size of claims or both. We may be limited in our ability to respond to such changes, by

insurance regulations, existing contract terms, contract filing requirements, market conditions or other factors.

Page | 21

Annexure II: Overview of Insurance Industry

1. Introduction

2. Background- A brief history about Insurance Industry

2.1. Pre-Nationalization

2.2. Nationalization of the Sector

2.3. Insurance Reforms

2.4. Interim Insurance Regulatory Authority

2.5. Insurance Regulatory and Development Authority

2.6. Approach to Reforms

3. Global Insurance Environment- A brief on global and domestic scenario covering Insurance Penetration,

Density, growth of Industry etc

3.1. Global Insurance Environment

3.2. Domestic Market Overview

4. Industry Outlook

4.1. Life Insurance -Total Premium Underwritten

4.1.1. Market Share (% share)

4.1.2. Growth of Business

4.2. Non Life insurer Market Share (% share)

4.2.1. Market Share (% share)

4.2.2. Growth of Business

5. Analysis of Trends

5.1. Life Insurance

5.1.1. Enlarged Coverage

5.1.2. Introduction of New Products

5.2. General Insurance

5.2.1. Tariff and non-tariff Products

5.2.2. Enlarged Coverage

5.2.3. Introduction of New Products

5.2.4. Reinsurance Supported Products

5.3. Health Insurance

5.3.1. Enlarged Coverage

5.3.2. Introduction of New Products

Page | 22

5.4. Reinsurance Business

6. Investment of Funds by the Insurance Industry

6.1. Investment Pattern

7. FDI in Insurance Sector

8. Intermediaries

8.1. Commission Structure

8.1.1. Life Insurance Industry

8.1.2. Non Life Insurers

9. Changes in Insurance Legislation

9.1. Changes in Insurance Legislation

9.2. Regulatory Issues and Changes

9.3. Consumer Related Changes

9.4. Removal of Redundant Clauses

9.5. Enhancement of Enforcement Powers and Levy of Penalties

10. Corporate Governance Guidelines for Insurance Companies

11. Conclusion

Page | 23

Annexure III: Comparison table on disclosures made in offer documents of life insurance companies in other jurisdictions

Particular Cathy FHC,

Taiwan

China Life Ping AN Sony Financial Delta Lloyd Groep IRDA's Observations

1 Business Description

1.a Gross Premium By business line

(life V/s Non-life)

and by product line

By product

profitability (group

life vs. individual life/ Participating

vs. traditional non-

participating/ Singe premium vs regular

premium)

By business life (life

vs non-life), By

region (Coastal vs. others), by product

(Life % of regular

premium/ % of renewal premium /

Bancassurnace vs.

group life vs. individual life, non-

life, auto vs. non-

auto

By business line

(life, non-life &

banking) By product (individual life vs.

individual annuity

vs. group life, group annuity)

By business line (life vs.

non-life) By region

(Netherlands, Belgium) By product (Individual/ group,

savings/ pension, traditional

/ linked)

Covering various business lines

(including the renewal premiums in

case of life companies). Also

disclosre on buisness underwritten on

geography wise basis

1.b Cross selling Between Insurance and banking

Not Available Between life and non-life

Between life, non-life and bank

Between life, non-life and bank and fund management

Between insurance & banking (details

of referrals and bancassurance to be

provided)

1.c Distribution network Agents Branch/ Agents/

Bancassurance

Branch/agents/.

Bancassurance

Life planner sales

employees and

independent agents

Different channels utilized Agents, corporate agents,

bancassurance, brokers and Referrals.

The same will be specified by IRDA as

an additional disclosure.

1.d Persistency 13-month

persistency

Not Available 13-month and 25-

month persistency

12-months

persistency

Not available Applicable only for life insurance

business. Already covered in the re-

statement of the financial statement.

However, if require, the same may be

repeated here giving 13months, 25th

month, 37months, 49th months and

61th months persistency ratio

2 Income Statement

Page | 24

Particular Cathy FHC,

Taiwan

China Life Ping AN Sony Financial Delta Lloyd Groep IRDA's Observations

2.a Renewals Not available Not available Mentioned Mentioned Mentioned (in MCEV) Would be covered under the Revenue

Statement - specific for life companies.

2.b Agent productivity Not available Briefly discussed Annualized FYP per agent, new life

policies per agent

per month

Mentions only the number of sales

employees and

agents

Mentions number of agents Annualized FYP per agent; new life

policies per agent per month. - case of

life companies

2.c Margin per product

line

By different

business line

Not available By different product

(bancassurance vs

group life vs individual)

By different product

lines and different

business divisions

By different business

divisions Not in vogue in India at present.

However, segment wise disclosure have

already been specified for revenue a/c.

In case of non-life companies,

disclosure would be underwriting

experience segment wise.

2.d Operating expense

ratio

ratio given for life

insurance

Only expenses

disclosed in P&L

Expenses disclosed

in detail

Only expenses

disclosed in P&L

Mentioned only for general

insurance divisions, for life

insurance expenses in P&L

Already covered in management

expense ratio

3 Balance Sheet

3.a Investment Yield for overall investment

Yield for each class of investment

Yield for each class of investment

Yield for each class of investments

Yield for each class of investments

Already covered in the financial

statement and the continuous

disclosures- – to be disclosed for the

shareholders’ funds; traditional

portfolio and on the ULIPs in case of

life com.

3.b Investment portfolio Loans/ overseas

investment/ short

term security/ bonds etc.

Deposit/fixed

maturity/ equity/

loan

Deposit/fixed

income/ equity/loan

Deposit /fixed

income/equity/loan

Deposit/fixed

income/equity/loan/bonds Already covered in the financial

statements to be restated

3.c cost of liability Not available Not available Provides interest

rates directly to

illustrate negative spreads

Provides interest

rates directly to

illustrate negative spreads

Interest amount by type of

liability provided In the Indian context, the only form of

capital presently permitted is Equity. As

such, there is presently only the

notional cost of capital involved. For

the present, disclosures in this context

may not be required.

4 Capital and EV (including assumptions)

Page | 25

Particular Cathy FHC,

Taiwan

China Life Ping AN Sony Financial Delta Lloyd Groep IRDA's Observations

4.a Value of new Business

Not available with sensitivity analysis

With sensitivity analysis

with sensitivity analysis

with sensitivity analysis not required to be disclosed as there is

no uniformity in the approach to be

followed for computation of Value of

New Business.

4.b NBAP Not available Not available New business value

/ first year premium

(No assumptions

mentioned)

disclosure of NBAP

and NBAP %

(Assumptions

mentioned)

disclosure of NBAP and

NBAP % (Assumptions

mentioned)

-do-

4.c Embedded Value Assumptions are

mentioned very

briefly

Assumptions are

mentioned very

briefly

Assumptions are

mentioned very

briefly

Assumptions are

mentioned in detail

Assumptions are mentioned

in detail The same needs to be disclosed.

Institute of Actuaries of India is already

in process of finalisation of the

guidelines on Embedded Value.

4.d Capitalization Mentioned Mentioned Mentioned Mentioned Mentioned Already covered as a part of financial

statement.

4.e Solvency margin statutory disclosure statutory disclosure statutory disclosure statutory disclosure Regulatory and IFRS basis Covered in the ratios prescribed by the

Authority.

5 Risk Management

5.a Market risk Described the risk

and explained the

way it is managed

Described the risk

and explained the

way it is managed

Described the risk

and explained the

way it is managed

Described the risk

and explained the

way it is managed

Described the risk and

explained the way it is

managed

Covered

5.b Operational risk Not available Not available Explained the risk

and the measures

taken to manage it

Described the risk

and explained the

way it is managed

Described the risk and

explained the way it is

managed

Covered

5.c Credit risk Described the risk and explained the

way it is managed

Described the risk and explained the

way it is managed

Described the risk and explained the

way it is managed

Described the risk and explained the

way it is managed

Described the risk and explained the way it is

managed

Covered

5.d Liquidity risk Described the risk and explained the

way it is managed

Described the risk and explained the

way it is managed

Described the risk and explained the

way it is managed

Described the risk and explained the

way it is managed

Described the risk and explained the way it is

managed

Covered

5.e Assets Liability

Management

Described the risk

and explained the way it is managed

Described the risk

and explained the way it is managed

Described the risk

and explained the way it is managed

Described the risk

and explained the way it is managed

Described the risk and

explained the way it is managed

Covered

6 Investment

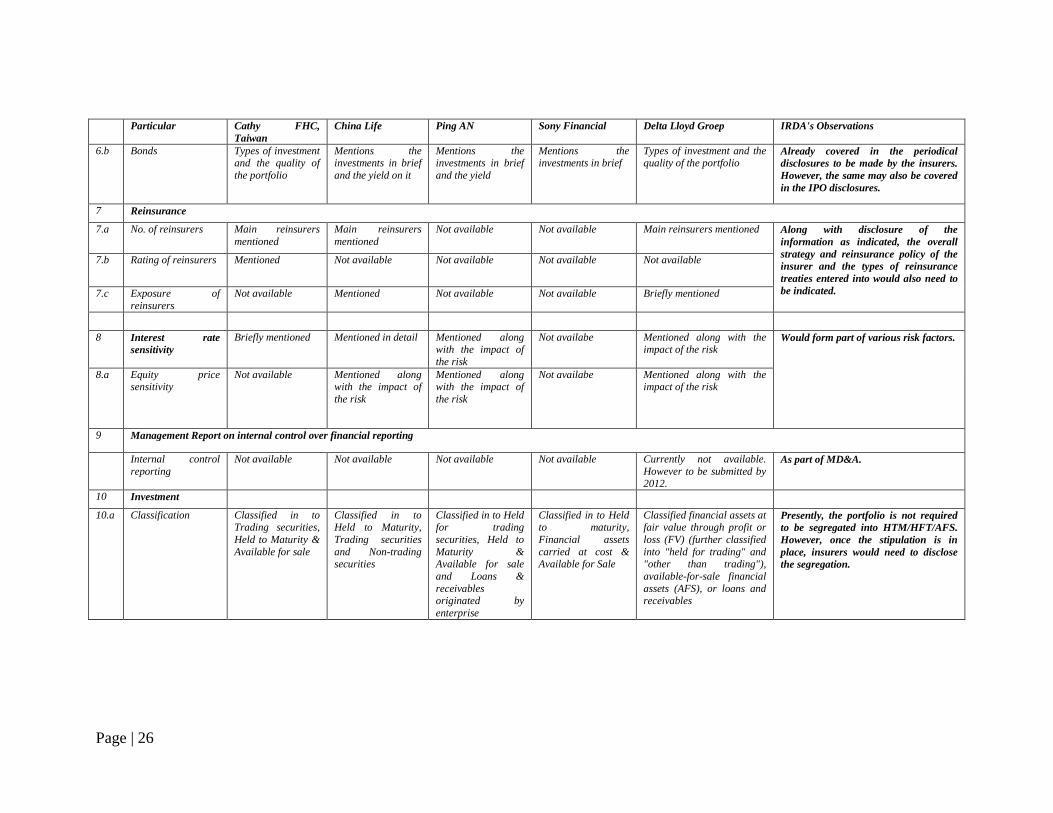

6.a Equity Types of investment and the quality of

the portfolio

Mentions the investments in brief

and the yield

Mentions the investments in brief

and the yield

Mentions the investments, yield

and the industry

wise bifurcation n brief and the yield

Types of investment and the quality of the portfolio

At present covered only in the financial

statement. It is suggested that the

investments, yield and the industry wise

bifurcation in brief may also be

captured.

Page | 26

Particular Cathy FHC,

Taiwan

China Life Ping AN Sony Financial Delta Lloyd Groep IRDA's Observations

6.b Bonds Types of investment and the quality of

the portfolio

Mentions the investments in brief

and the yield on it

Mentions the investments in brief

and the yield

Mentions the investments in brief

Types of investment and the quality of the portfolio

Already covered in the periodical

disclosures to be made by the insurers.

However, the same may also be covered

in the IPO disclosures.

7 Reinsurance

7.a No. of reinsurers Main reinsurers

mentioned

Main reinsurers

mentioned

Not available Not available Main reinsurers mentioned Along with disclosure of the

information as indicated, the overall

strategy and reinsurance policy of the

insurer and the types of reinsurance

treaties entered into would also need to

be indicated.

7.b Rating of reinsurers Mentioned Not available Not available Not available Not available

7.c Exposure of

reinsurers

Not available Mentioned Not available Not available Briefly mentioned

8 Interest rate

sensitivity

Briefly mentioned Mentioned in detail Mentioned along with the impact of

the risk

Not availabe Mentioned along with the impact of the risk

Would form part of various risk factors.

8.a Equity price sensitivity

Not available Mentioned along with the impact of

the risk

Mentioned along with the impact of

the risk

Not availabe Mentioned along with the impact of the risk

9 Management Report on internal control over financial reporting

Internal control

reporting

Not available Not available Not available Not available Currently not available.

However to be submitted by 2012.

As part of MD&A.

10 Investment

10.a Classification Classified in to Trading securities,

Held to Maturity &

Available for sale

Classified in to Held to Maturity,

Trading securities

and Non-trading securities

Classified in to Held for trading

securities, Held to

Maturity & Available for sale

and Loans &

receivables originated by

enterprise

Classified in to Held to maturity,

Financial assets

carried at cost & Available for Sale

Classified financial assets at fair value through profit or

loss (FV) (further classified

into "held for trading" and "other than trading"),

available-for-sale financial

assets (AFS), or loans and receivables

Presently, the portfolio is not required

to be segregated into HTM/HFT/AFS.

However, once the stipulation is in

place, insurers would need to disclose

the segregation.

Page | 27

Particular Cathy FHC,

Taiwan

China Life Ping AN Sony Financial Delta Lloyd Groep IRDA's Observations

10.b Valuation Trading securities and Available for

sale are marked to

market and Held to Maturity are stated

at amortized cost

Held to maturity securities are

reported at

amortized cost and Trading and Non-

trading securities

are reported at fair

value

Held to maturity and Available for

sale reported at fair

value and Trading securities and Loans

& receivables at

cost

Held to maturity are reported at

amortized cost, Held

for trading securities and available for

sale are stated at

fair value with

unrealized gains or

losses charged to

income

FV and AFS are carried at fair value. Changes in the

fair value of "held for

trading" and "other than trading" investments are

charged to income.

Changes in the fair value of

AFS (except for impairment

losses and relevant foreign

exchanges gains and losses) are recorded in a specific

investment valuation reserve

within equity, mortgages and loan assets are reported

at amortized cost.

As per the present dispensation, listed

equity is valued at market price. Debt

instruments are valued at amortized

cost. The same is already being covered

in Significant accounting policies.

10.c Unrealized gains/ losses

Unrealised gains/ losses on Trading

securities are taken

to current earnings, on Available for

sale are taken to a

separate component of

shareholder's

equity and premiums &

discounts on Held

to Maturity are amortized over the

period of

investment

Unrealised gains/ losses on Held to

Maturity and

Trading securities are reported in

profit and loss

account whereas as that on Non trading

are routed through

investment revaluation reserve

Unrealised gains/ losses on Held for

trading are included

in consolidated results, for

Available for Sale,

they are recognised as a separate

component of equity

Unrealised gains or losses on securities

held for trading

charged to income

Fair Value movement on Held for trading and other

than held for trading are

included in the results, gross fair value gains/ losses

shown in Equity account

Manner of arriving at the unrealized

gains to be indicated.

11 Others

11.a Deferred acquisition

cost

Amortized Amortized Amortized Not available Amortized In the Indian context, the acquisition

costs are not permitted to be deferred.

Thus, no disclosures required.

Page | 28

Particular Cathy FHC,

Taiwan

China Life Ping AN Sony Financial Delta Lloyd Groep IRDA's Observations

11.b Liability for Future policy benefits and

Policyholder

Account Balances

Not available Calculated through the use of

assumptions for

investment returns, mortality,

morbidity, expenses

and persistency, as

well as certain

macro-economic

factors such as inflation

Briefly mentioned Briefly mentioned Briefly mentioned Calculated based on various actuarial

assumptions – in case of life insurers.

In case of non life insurance

companies, disclosure with respect to

reserving -loss triangles/claims

development would also be required to

be made.

11.c Risk Based Capital Calculated as per

the regulatory guidelines

prescribed by ROC

Calculated as per

the regulatory guidelines

prescribed by CIRC

Calculated as per

the regulatory guidelines

prescribed by CIRC

Solvency margin

ratio is mentioned along with the

calculations

Solvency margin ratio is

mentioned for all divisions These prescriptions are presently not

applicable to insurance companies in

India.

11.d Monitoring

Mechanism

CIRC CIRC CIRC FSA Not mentioned Already decided that no monitoring

agency is required.

29

Annexure IV: Glossary of terms used in Insurance Industry

(A) LIFE INSURANCE

Glossary- Life

Annuity

A periodic payment made for an agreed period of time (usually up to the death of the

recipient) in return for a cash sum. The cash sum can be paid as one amount or as a

series of premiums. If the annuity commences immediately after the payment of the

sum it is termed an immediate annuity. If it commences at some future date it is termed

a deferred annuity.

Annual premium equivalent

(APE)

An industry measure of new business. The total of new annualised regular premiums

plus 10% of single premiums written during the applicable period.

Assumptions Variables applied to data used to project expected outcomes.

Acquisition costs

Expenses related to the procurement and processing of new business written including

a share of overheads.

Board The board of Directors of the Company.

Bonus Surplus funds that a life insurance company allocates to its policyholders

Certainty Equivalent The approach adopted in calculating the value of in-force under the MCEV basis,

where all cash flows are projected and discounted at risk-free rates

Conventional with-profit or

CWP

Traditional policies which participate in the profits of the company-participating

policies

Cost income ratio

The ratio of total costs to total income for the year expressed as a percentage. These

are measures by reference to which the development, performance or position of the

business can be measured effectively. It indicates how much of total income is being