Report on Mining - Uranium - Special Issue #1 - 2011

18

-

Upload

fusion-publishing-media-inc -

Category

Documents

-

view

218 -

download

0

description

Report on Mining - Uranium - Special Issue #1 - 2011

Transcript of Report on Mining - Uranium - Special Issue #1 - 2011

URANIUMSPECIAL EDITION

UraniumCover.indd 1 04/03/2011 6:27:58 AM

Fractional Membership Jet Card

877.703.2348 • flightoptions.com

REDEFINING MID-SIZE AIRCRAFT. Fly faster and farther in a cabin size that overpowers the competition. If that isn’t enough, we’ve perfected the aircraft by adding elliptical winglets and onboard Wi-Fi. Step up to a larger class with enhanced features while flying at lower operating costs. Don’t settle for less – expect more.

With over 13 years of proven innovation, you will receive the best in safety, service and value. As the second largest fractional provider in the industry, the difference is clear. Contact us today to experience our Perfect Ten.

Over 1,300 customers • Over 100 aircraft • Over 1.5 million hours flownOnly fractional provider to achieve ARG/US Platinum Safety Rating five consecutive times

SIZE MATTERS.NETJETS CITATION EXCEL • COST $2,647 per hr • SPEED 480 mph • CABIN SIZE 461 cu ft • RANGE 2,004 sm

FLIGHT OPTIONS CITATION X • COST $2,444 per hr • SPEED 575 mph • CABIN SIZE 593 cu ft • RANGE 3,638 sm

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 3

Volume 14 | Number 2 | Special Edition #1, 2011Vancouver, British Columbia www.ReportOnMining.com

Planning for Profits - Report on Mining edition is published four times a year by Fusion Publishing Inc. All rights reserved. Any reproduction or duplication without prior written consent of Fusion Publishing Inc. is strictly prohibited. Published by Fusion Publishing Inc.

Canadian OfficeFusion Publishing Inc.#317 – 1489 Marine Dr.West Vancouver, BCCanada V7T 1B81.888.925.0313 (Toll Free)

USA OfficeFusion Publishing Inc.145 Tyee Dr.Pt. Roberts, WA USA 98281-9602 1.888.925.0313 (Toll Free)

PublisherTerry Tremaine

Associate Publisher & Editor Connie Ekelund

Production ManagerChristie Smith

Contributing EditorsRobert Setter

Account Managers1.888.925.0313 Terry Tremaine Ext: 1002Maureen O’Brien Ext: 2001Marie Richards Ext: 3002

Publication Mail Agreement #41124091

Circulation & DistributionCanada PostDistacor Inc.NewsstandDigital

Non-deliverables please return to:Fusion Publishing Inc.Report On Mining Magazine#317 - 1489 Marine DriveWest Vancouver, BC Canada V7T 1B8

Subscriptions:1 year $14.95 in Canada (+$8.00 in USA) 2 years $28.00 in Canada (+$16.00 in USA)1.888.925.0313 [email protected]

Free Digital Subscriptionwww.ReportOnMining.com

The information in Planning for Profits - Report on Mining has been carefully compiled from sources believed to be reliable, but its accuracy is not guaranteed.

www.ReportOnMining.com

Century Mining Corporation: starting in Canada, expanding in Peru.

It was not so long ago that CEOs of uranium companies were feeling particularly unappreciated or even unwanted. Now the marketplace has entirely changed with some suggesting uranium is the new ‘gold.’

It has become apparent that the demand for uranium is going to outstrip supply in the relative near term. The price continues to rise while the shares in juniors exploring for uranium are particularly volatile.

The latest rallying call is ‘there’s uranium in them there hills.’Investors take note: there is opportunity here.

South America4 Fission Energy Corp.

8 Macusani Yellowcake Discovering Peru’s Uranium Potential

10 Uranium: An Overview by Robert Setter North America12 Energy Fuels Meeting the Growing Demand for Uranium

14 Nemaska Exploration Lithium and the Dawn of New Energy Storage

16 MEG Pipeline Activity Index

4 Planning for Profits | Report on Mining | Uranium www.ReportOnMining.com

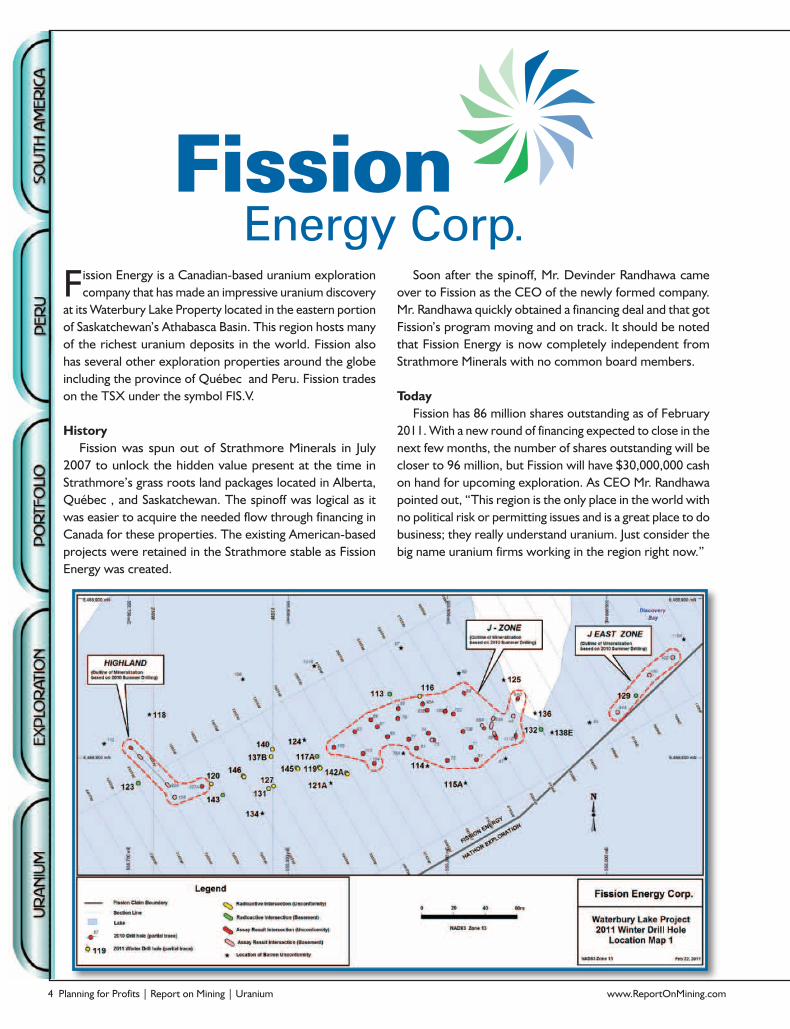

Fission Energy is a Canadian-based uranium exploration company that has made an impressive uranium discovery

at its Waterbury Lake Property located in the eastern portion of Saskatchewan’s Athabasca Basin. This region hosts many of the richest uranium deposits in the world. Fission also has several other exploration properties around the globe including the province of Québec and Peru. Fission trades on the TSX under the symbol FIS.V.

HistoryFission was spun out of Strathmore Minerals in July

2007 to unlock the hidden value present at the time in Strathmore’s grass roots land packages located in Alberta, Québec , and Saskatchewan. The spinoff was logical as it was easier to acquire the needed flow through financing in Canada for these properties. The existing American-based projects were retained in the Strathmore stable as Fission Energy was created.

Soon after the spinoff, Mr. Devinder Randhawa came over to Fission as the CEO of the newly formed company. Mr. Randhawa quickly obtained a financing deal and that got Fission’s program moving and on track. It should be noted that Fission Energy is now completely independent from Strathmore Minerals with no common board members.

TodayFission has 86 million shares outstanding as of February

2011. With a new round of financing expected to close in the next few months, the number of shares outstanding will be closer to 96 million, but Fission will have $30,000,000 cash on hand for upcoming exploration. As CEO Mr. Randhawa pointed out, “This region is the only place in the world with no political risk or permitting issues and is a great place to do business; they really understand uranium. Just consider the big name uranium firms working in the region right now.”

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 5

Fission has 13 other properties in its stable. These holdings are the hidden value in Fission. The 43-101 inferred resource at the Dieter Lake property in Québec outlines a resource of 24.4 million pounds U308 at a grade of .057%. In Peru at Macusani, Fission holds rights to nine mineral concessions encompassing 51 square kilometres as well as surface rights with known uranium mineralization present. While the current focus is on Waterbury Lake, Mr. Randhawa hinted they may spin out some of these other properties to unlock their value much like the history of Fission Strathmore.

ResultsThe J-Zone discovery was big news in 2010. As Chief

Operating Officer Mr. McElroy stated, “Most explorers are happy with 0.3% to 0.5% uranium grades. Consider that our results showed an average grade of >2.5% with assays as high as 57.61% as per hole WAT10-091.” Much of the mineralization exists at 200 metres depth at the unconformity. The team relies on geophysics to get into the right areas. According to Mr. McElroy, the area has many significant corridors and the Waterbury Lake property encompasses an area greater than 40,000 hectares.

In 2010, they drilled 27 holes in the J-Zone in an area 120 metres by 50 metres across with high grade mineralization results. Fission recently increased the east-west mineralized strike length of the J-Zone from ~120 metres to ~203 metres or by 69% since drilling resumed in January. As well, they have expanded the J-Zone uranium discovery at its eastern and western margin.

In addition to identifying more unconformity related mineralization at the newly named PKB Zone (in the Discovery Bay Corridor 338 metres to the west of the currently defined J-Zone), mineralization is trending to the west and remains open along strike and in all directions.

UpcomingThe 2011 drilling program will pick up where it left

off in the J-Zone with three rigs going. Three stepouts hit holes with robust mineralization so drilling continues along the 2.5 kilometre Discovery Bay corridor. Mr. McElroy indicated that the J-Zone west to Highland may connect and further drilling between J-Zone to PKB is required to see how mineralization might be related.

The end of the winter drilling program will be dictated by the weather and usually ends when the ice breaks up, typically by April. As Mr. McElroy explained it, “They have to hit hard and fast in the winter even though there is a summer program. Nearly 70% of our exploration efforts are in the winter as we can move around much easier when everything is frozen. The transportation costs are that much lower when using tractors as opposed to helicopters.”

Fission is fortunate in that they have all weather roads to the exploration grounds resulting in ease of accessibility. Last year, they brought in a large barge which allowed them to drill through the lake into the ground below during the summer months. Although they have not gotten an estimate of the resource at this time, it is expected that the winter drilling results will be available by early summer and anticipate a 43-101 report estimate by the fall of this year. There is agreement between Fission and its partners to spend $30 million over the next three years on Waterbury.

Aerial shot showing J-Zones and Roughrider; Drilling WTA10-107A from the barge.

Helicopter, Summer 2010

6 Planning for Profits | Report on Mining | Uranium www.ReportOnMining.com

Named top 50Mr. Randhawa stated, “We were very pleased

to be named in the top 50 but considering there were five categories and that we were number four in the mining exploration section, well, that says a lot about the entire organization.” Mr. Randhawa attributes this recognition to a few factors such as the strong results reported at Waterbury Lake and the resulting buzz. As well, the company has been working diligently to get the story out and has been well covered by the analysts. Mr. Randhawa went on to say, “Being named in the top 50 is just the icing on the cake.”

Share PriceA major factor affecting share price has been the discovery

and drill results which saw the share price move from $0.17 to $1.25 last year. After the price retreated somewhat, it again moved sharply and doubled from December, 2010 to February, 2011 due to the continued drilling success this winter. Management suggested that the recent share price was also in part driven by the rising price of spot uranium from the low $40s per pound to the more recent levels just over $70 per pound. As was noted, such a move in the underlying commodity tends to inflate the share price of all exposed companies.

Another factor affecting share price is the buyback provision that Fission can exercise with its 50% partner in the project. For a onetime $6,000,000 cash payment, Fission Energy can obtain an additional 10% ownership from partner Korea Waterbury Uranium Limited Partnership (the KEPCO Consortium). Mr. McElroy suggested this would be a positive step for Fission to take and it was management’s intention to do so; probably by April of this year. When this takes place, Fission would control 60% of the Westbury Lake project leaving KEPCO with 40%.

ManagementDevinder Randhawa is Chairman and CEO of Fission

Energy. He founded Strathmore Minerals in 1996 then had a significant role in spinning Fission out of Strathmore in 2007. Mr. Randhawa was also the founder and president of RD Capital, a private venture capital and finance company. He also founded Royal County Minerals which was taken over by Canadian Gold Hunter in 2003.

Ross McElroy is President and Chief Operating Officer. He is a professional geologist with more than two decades of related experience having managed a range of exploration projects at various stages of development including majors as well as junior mining companies. His track record includes BHP Billiton, Cogema Canada (now AREVA) and Cameco. Mr. McElroy was also a key part of the team that discovered the MacArthur River uranium deposit.

Example of High Grade Mineralization, 51 wt% U308; Waterbury Lake Property; Eastern Athabasca Region; Uranium Supply and Demand.

Discovery Bay drilling activity.

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 7

Uranium and the Global SettingHistorically, the uranium price has been set weekly,

although there is a new broker’s average measure published daily. Back in 2007, the uranium price went as high as $140 per pound, likely due to spec buying in the market. Normally, the short and longer term delivery prices move together but at that time, a significant divergence between short and long occurred and was in hindsight an early indicator that a correction in uranium prices was likely. Today, we do not see this type of divergence which indicates a supply demand balance and an overall firmer market.

Over the long term, the demand side of the uranium market appears to be solid as demand in China and in Asia continues to grow. Nearly all Asian countries have nuclear programs and the Chinese are adding 25% demand per year going forward. Fission is well positioned to continue to increase its asset value with the $30 million exploration program and may even be a takeover target in the not too distant future.

The Company’s website at www.fission-energy.com and public filings at www.sedar.com provide additional detailed information on its properties and other related documentation with respect to its management and operations.

Fission Energy Corp.#700-1620 Dickson Ave.Kelowna BC CanadaV1Y 9Y2Phone: 1.877.868.8140Email: [email protected]: FIS Year Hi/Low: $1.48/$.39

Mr. Jody Dahrouge, a professional geologist with 18 plus years domestic and international experience, is on the team as a Director. He has managed a range of projects from grass roots exploration to mine development and production. Since 2004, Mr. Dahrouge has been instrumental in the acquisition and management of Fission’s exploration properties.

Also a Director, Mr. George Sanders is a mining entrepreneur with 30 plus years of exploration, development and mining finance experience. He spent over 15 years as a minerals specialist with Canaccord Capital and has worked for Wescan Goldfields and Shore Gold. He is President of Goldcliff Resources and a Director of Bitterroot Resources, Silvercrest Mines and an important contributor to the Fission team.

Mr. Frank Estergaard is a professional Chartered Accountant and Director with Fission. After retiring as a Partner with KPMG in 2001, Mr. Estergaard served as a Director and Chairman of the audit committee for QHR Technologies and CFO for Metalex Ventures among others.

Ice Road across MnMahon Lake to camp drill sites.

8 Planning for Profits | Report on Mining | Uranium www.ReportOnMining.com

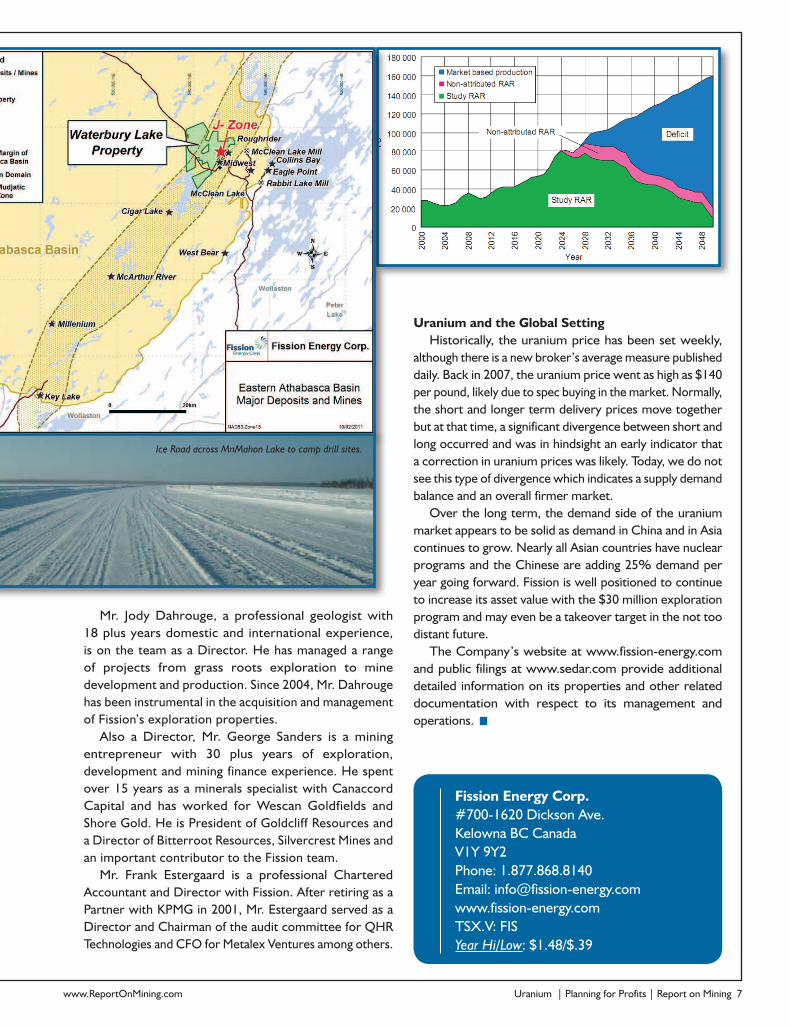

Macusani Yellowcake Inc. is a Canadian uranium exploration company with over 24,000 hectares (240

km2) of mineral properties in south-eastern Peru. The Company is exploring a major new uranium district on the Macusani Plateau and has recently delineated resources across all categories (measured, indicated and inferred) totalling over 27 million pounds of low grade, near surface U3O8 at its Colibri and Corachapi concessions. While the preliminary economic assessment for Colibri demonstrates good economics at current uranium prices, it is the initial drill results indicating multiple high grade deposits on the nearby Kihitian property that is spurring much interest in the Company as of late.

Table 1 - Resource summary for target concessions on the Macusani Plateau, Peru

Discovering Peru’s Uranium PotentialHigh Grade Uranium Potential at Kihitian

In early 2010 the Company sampled 297 metres of underground adits originally developed by the Peruvian Nuclear Energy Institute (IPEN) in the 1980s. A total of 146 channel samples were collected along the adits with results ranging from trace to a high of 11.24% U3O8 (224 lbs U3O8 per ton).

Radiometric map and drill hole locations for Kihitian concession.

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 9

Macusani Yellowcake Inc.Peter Hooper141 Adelaid St. West, 12th FlrToronto, ON Canada M5H 3L5Phone: [email protected]: YEL; QG1-FrankfurtYear Hi/Low: $1.55/0.64

There are currently two drills turning at Kihitian as part of a 20 hole program; assay results will be forthcoming over the next several months. Initial drilling results released late last year and early this year have confirmed the potential for high grades at Kihitian. Results from the initial five boreholes include intercepted areas with grades of 1% uranium (first quartile worldwide). The first 20 holes are being drilled at 100 metre and 200 metre stepouts from the sampled adits across a lateral extent of approximately 200 metres.

Above: Macusani Yellowcake properties map indicating target concessions on the east side of the Macusani Plateau, Puno District, Peru. Right: Radiometric surface readings being taken at Kihitian.

Assuming metallurgy is similar to the lower grades already defined at Colibri and Corachapi (>90% of the uranium is recoverable using conventional heap leach-IX technology), it won’t take many pounds of high-grade Kihitian uranium to have a meaningful impact on overall project economics.

Mining in PeruThe mining sector in Peru has attracted over U.S. $18

billion in investments over the past 15 years; as a whole the industry generates more than 128,000 direct and 400,000 indirect jobs and accounts for over 60% of the country’s total exports. As of last year Peru ranked globally for several important commodities including: #1 for silver, #1 for tin, #2 for copper, #2 for zinc, #4 for lead, and #6 for gold.

In addition to a stable government and good regulatory framework, Peru also offers much of the core infrastructure required to move Macusani Yellowcake’s projects into full production including ample power (lines currently run over the Company’s properties), excellent roads (including the Twin Oceans Highway that goes through the town of Macusani), and a good availability of sulphuric acid (Peru is a net exporter).

For more information about the Company visit: www.maycel.com.

Top: Macusani Plateau, Puno District, SE Peru; bottom: Geiger counter being used on core samples.

10 Planning for Profits | Report on Mining |Uranium www.ReportOnMining.com

The determination of the uranium spot price is not the same as other metals, such as gold or silver, where price is broadcast from numerous sources, tick by tick

virtually 24 hours per day as the markets open and close around the globe. Uranium price is determined by private sources that monitor developments in the uranium market place. They interpret and analyze the most recent transactions between suppliers and sellers and in thin trading will at times factor in the bid/ask and lot size in determining the current price. Occasionally, the two recognized price publishers differ by a few dollars per pound or more. These sources are, for the most part, equally recognized by industry, government, exchanges, and producers. The longest running provider, the Ux U3O8 Price® indicator, has been publishing prices since the early 1990s and provides a daily and weekly price. The daily pricing is a fairly recent addition to the overall price determination mix.

Has uranium run its course or is it just getting ready to resume its upward climb to 100 plus dollars per pound? From 2003 through 2007 uranium price gains were dramatic but proved to be unsustainable. As prices soared, eventually nearing $140 per pound, analysts began to question the size of the move based solely on the long term uranium demand story. In our techno-wired world it is not unusual for markets and equities to run ahead of themselves as rising prices lead to more buying which in turn leads to higher prices. When this momentum continues over a long enough period of time, prices eventually climb to levels that are disconnected from the existing fundamentals. Industry insiders and uranium market observers tend to agree that the price of $140 per pound was reached due to the presence of speculation buying.

One indicator of this was the divergence between the short and longer term delivery pricing, especially in 2007. Another noteworthy factor was the formation of the Uranium Participation Corporation that began purchasing millions of pounds of U308 around 2005. This buying was not directly market demand driven, yet served to support the price rise along the way. The Participation Corporation was established to provide a vehicle for investors to play purely on the uranium price as compared to buying miners and the inherent accompanying up and downside variables.

Uranium: An Overview

In today’s market, short and long term prices are not divergent, suggesting current market conditions are in balance and reflective of more typical market conditions than what existed in 2007. Industry observers have suggested China is likely responsible for the recent price upswing from spot $40.75 in May 2010 to the current price in the $65 to $70 range, (as of March 2011). Very recently, in the last few weeks of February and into early March, prices have softened by about $5 per pound but appear to be solidifying with buyers present at the lower prices.

On the supply front, there is a great deal of pressure to open up uranium mining in Australia. Recent exploration efforts in Queensland have shown there is an estimated uranium resource of around $20 billion waiting to be mined. Strangely, in that jurisdiction, mining is not legal, however exploration is. This does imply that at some point, mineral extraction will be approved not withstanding domestic political considerations. As a group, Australia, Canada and Kazakhstan produce nearly two thirds of the current world supply of uranium. Considering the high entry costs, the 5-10 years of lead time to get permits, environmental assessments and a mine operating, in the medium term, the assets “down under” will likely remain down under and unavailable for consumption.

Uranium was discovered in the 18th century and is found all over the earth in minute amounts. Prior to WWII German physicists showed that uranium could yield energy by being split, leading to its primary use today as fuel for nuclear reactors in the creation of electricity. With the super powers mothballing their nuclear programs, some supply has come from the thousands of decommissioned war heads. According to the World Nuclear Association, highly-enriched uranium from weapons stockpiles is displacing some 10,600 tonnes of U3O8 production from mines each year, and meets about 13% of world reactor requirements. The contracts in place to dispose of stockpiled U308 did not greatly affect the supply demand equation.

by Robert Setter

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 11

In terms of future demand, the growing middle class in China and India will consume more of everything, including power. In an attempt to keep up to ever increasing needs, more power plants will be built and are being planned with China planning 50 new reactors by 2020. According to the World Nuclear Association, Chinese demand will reach 44 million pounds per year with only 5 million pounds internal production in the same time period. There are 442 reactors currently running globally with 63 more under construction and another 478 planned or proposed leading to an estimated 5% annual growth rate in demand for U308 through 2020 for a market that is already in deficit.

Inset and below: Reactors; at right, McMaster Nuclear Reactor.

12 Planning for Profits | Report on Mining | Uranium www.ReportOnMining.com

The uranium spot price is on the rise again, but unlike previous years this run in uranium prices may be

spurred by sustainable demand, not just supply disruptions. With two fully permitted conventional uranium mines, a suite of properties and uranium resources and an approved uranium mill license in hand, Energy Fuels (TSX:EFR) is poised to lead new uranium production in the United States.

What Are the Experts Saying?David Talbot, Mining Analyst at Dundee Securities

recently published in the Street Wise Energy Report (01/25/2011), “Yes, I am bullish on the spot price of uranium. I think it’s all about demand this time. I believe that in the past, investors were essentially focused on supply disruptions as the driver for uranium prices. This time around, I think the demand fundamentals are strong and people are paying attention to that.” He continued, “In 2007 spot trading was only about 20 M lb., or only 8% of the total volume of uranium trades. This time around I think it’s a little different. The spot market is much, much bigger—about 50 million pounds, which represents about one-third of the entire market.”

Meeting the Growing Demand for Uranium

Recent Supply ChallengesIn addition to the sustained demand for uranium, supply

challenges will likely continue to affect the spot price for uranium. Energy Resources of Australia recently announced that due to significantly higher than average rainfall at its Ranger Mine, the company is suspending plant processing operations at Ranger for a period of 12 weeks. The Ranger mine represents roughly 5% of global uranium mine production. This action will undoubtedly create short-term supply challenges.

Energy Fuels — Right Place at the Right TimeEnergy Fuels (TSX:EFR) has leveraged its property portfolio

with an experienced management team to re-open its U.S. uranium mines and develop the first new uranium mill to be built in the U.S. in 30 years. Energy Fuels’ properties and proposed new mill are located in the highly prolific historically producing area of Colorado and Utah known as the Uravan Mineral Belt. This area was once one of the largest producing areas in the United States and boasts the highest grade of uranium available in the U.S., outside of the Arizona Strip. Between 1948 and 1990 approximately 250 million pounds of U3O8 was produced from Colorado and Utah. Production ceased due to falling commodity price rather than resource depletion.

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 13

Energy Fuels Inc.Gary Steele2 Toronto Street, Suite 500Toronto, ON, Canada M5C 2B6Phone: 1.303.974.2140Email: [email protected]: EFRYear Hi/Low: $1.59/$0.13

Today, Energy Fuels estimates that there is over 40 years of mill feed (at 500 tons per day) in the area, a portion of which is owned by Energy Fuels, while the

rest is scattered amongst smaller operators and private companies. Energy Fuels currently has two fully permitted uranium mines, the Energy Queen Mine and the Whirlwind Mine, and at least one other property that can be readily permitted and put into production. Both mines are on care and maintenance at the moment while the Company determines its course of action following approval from the State of Colorado for the construction of a new uranium mill in the area. The mill, when built, will use state of the art technology

and employ up to 80 skilled workers from the region, which has been economically depressed for several years. Locals are very supportive of the project which represents numerous jobs and robust support-business opportunities that will be derived from mining activity in the area.

With an eye to consolidation, Energy Fuels is also contemplating acquisitions, mergers, ore purchases, and toll-milling agreements with some of the past producers in the region. The Company is actively talking to local mine owners about various options to secure long-term supply for the new mill. In addition, Energy Fuels is actively engaging prospective strategic partners to negotiate long-term uranium supply contracts.

“With the strengthening uranium spot price, the timing of our mill permit couldn’t be better for Energy Fuels. We have long believed in the potential of the area and we have acted early to establish our regional leadership position, allowing us to truly be in the right place and at the right time,” said Steve Antony, President and CEO of Energy Fuels.

For more information on Energy Fuels please visit our website at www.energyfuels.com.

14 Planning for Profits | Report on Mining | Uranium www.ReportOnMining.com

With the resurgence of electric vehicles and the advent of hybrid electric vehicles, the demand for lithium

batteries is growing, creating a new market for spodumene concentrate and lithium carbonate. Nemaska Exploration (NMX:TSX-V) boasts one of the largest and richest hard rock pegmatite lithium projects in the world. The Company recently completed a Preliminary Economic Assessment on its Whabouchi Project, initiated a feasibility study, and signed a strategic Chinese investor.

The Growing Lithium Market Lithium-ion batteries are rechargeable batteries that

have all but replaced nickel cadmium batteries in virtually every portable device and are now used in new hybrid and electric vehicles that are being developed and commercially sold today.

Experts from signumBox, a Chilean-based provider of market intelligence research within the natural resource sector, predicts the demand for lithium batteries in electric vehicles alone will top 100,000 metric tonnes a year by 2025 from its current level of about 5,000 metric tonnes.

Lithium carbonate which is used in lithium batteries can come from two sources, salar (brine deposits) or pegmatite hard rock deposits. Adam Marchionni, B.Sc., MBA, Research Analyst, Mining at Industrial Alliance, recently wrote, “While the salar/pegmatite debate continues, the emerging consensus is that salar projects will dominate the bulk of the lithium carbonate market but that certain pegmatite projects with favourable geological and metallurgical characteristics will be economically exploitable even at a discount to the current price of lithium carbonate/spodumene concentrate. Moreover, based on an analysis of comparable pegmatite projects, it appears that Whabouchi has comparably favourable in-pit resources, grade, strip ratio and metallurgy.”(Industrial Alliance Resource stock watch list, December 22, 2010.)

Lithium and the Dawn of New

Energy Storage

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 15

Nemaska Exploration Inc450, Gare du Palais Street, Box 10Québec , QC, CanadaG1K 3X2Phone: 1.418.704.6038Email: [email protected] www.nemaskaexploration.comTSX.V: NMXYear Hi/Low: $0.68/$0.26

Lithium is also used in other applications including ceramics, glass, metallurgy, polymers, etc. and this market remains strong. This market typically requires a spodumene concentrate which is then transformed into the various lithium products. signumBOX currently estimates that until 2015 total lithium’s demand (excluding the use of batteries in the automotive industry) will grow around 5% per year, but in the medium term the demand should start growing at a steady state rate (which means annual rates of around 3.5% — 4.0% per year).

Nemaska’s Role in the Growing Lithium MarketNemaska Exploration (NMX:TSX-V) is a mineral

exploration company with properties located in a prolific polymetallic greenstone belt formation in the James Bay region of Québec. In just two short years, Nemaska has worked diligently to bring historical lithium showing to a world class deposit, with a positive Preliminary Economic Assessment and a feasibility study due out by fall 2011. The Company is currently undertaking a drill program to move more of the resource into the measure and indicated categories as defined by NI43-101 standards. This is a necessary step in moving the project into the feasibility stage and ultimately production.

Nemaska has also commissioned SGS Minerals Services Lakefield laboratory to produce both a spodumene concentrate and a lithium carbonate. In both cases, using off-the-shelf technology and processes, the ore from Whabouchi exceeded industry requirements of 6.25% for spodumene concentrate and 99.96% for the lithium carbonate.

As lithium is an industrial mineral, marketing the product is as important as producing it, and therefore Nemaska has been actively pursuing strategic partners to assist it in delivering product to end users. The Company recently inked a deal with an important Chinese group that is involved in the transformation and production of lithium products, for an initial private placement of 7,370,468 common shares or 10% of the Company’s outstanding shares. The closing of this transaction is expected on or about March 4, 2011.

Guy Bourassa, President and CEO of Nemaska Exploration commented on the new strategic relationship, “This is an important milestone in the evolution of Nemaska and a great validation of the strong potential of our lithium assets. We are delighted to welcome our Chinese partner who has deep expertise in lithium products and we look forward to building upon this initial relationship as we move our projects towards the commercial production of spodumene concentrate. The Chinese market is a major consumer and producer of lithium products including vehicle batteries for hybrid and electric vehicles. Our new investor views their investment in Nemaska as part of a broad strategy to not only diversify their supply for raw materials but also to have an ownership position in a high-quality resource capable of producing battery-grade lithium carbonate.”

For more information on Nemaska Exploration please visit their website at www.nemaskaexploration.com.

16 Planning for Profits | Report on Mining |Uranium www.ReportOnMining.com

Metals Economics Group Strategic Report:

Uranium Supply Pipeline, 2010Uranium miners respond to supply deficit by increasing mine production

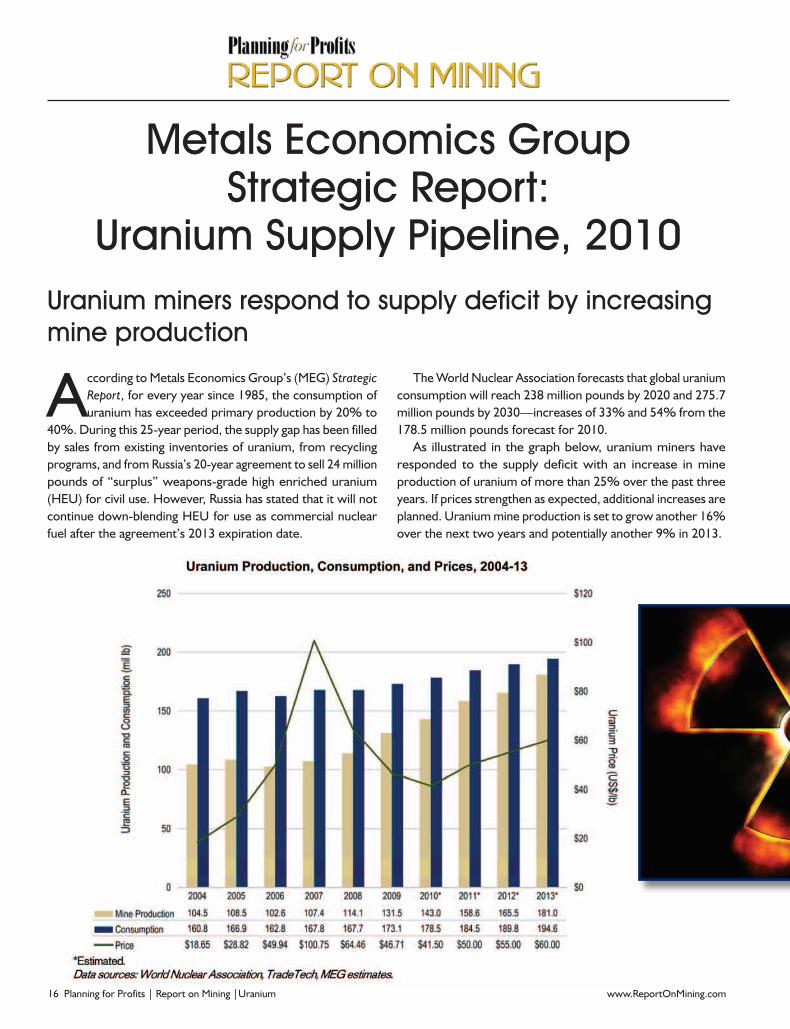

According to Metals Economics Group’s (MEG) Strategic Report, for every year since 1985, the consumption of uranium has exceeded primary production by 20% to

40%. During this 25-year period, the supply gap has been filled by sales from existing inventories of uranium, from recycling programs, and from Russia’s 20-year agreement to sell 24 million pounds of “surplus” weapons-grade high enriched uranium (HEU) for civil use. However, Russia has stated that it will not continue down-blending HEU for use as commercial nuclear fuel after the agreement’s 2013 expiration date.

The World Nuclear Association forecasts that global uranium consumption will reach 238 million pounds by 2020 and 275.7 million pounds by 2030—increases of 33% and 54% from the 178.5 million pounds forecast for 2010.

As illustrated in the graph below, uranium miners have responded to the supply deficit with an increase in mine production of uranium of more than 25% over the past three years. If prices strengthen as expected, additional increases are planned. Uranium mine production is set to grow another 16% over the next two years and potentially another 9% in 2013.

www.ReportOnMining.com Uranium | Planning for Profits | Report on Mining 17

Based on current trends of increasing consumption and lower inventory sales, as secondary resources are gradually drawn down prices should move higher, encouraging primary production to gain an increasing share of the total uranium supply. The increased production will occur through ramp-up of several new Kazakhstan mines and development of new projects in Canada, Niger, Namibia, and elsewhere.

For more details on Metals Economic Group services and for subscription information visit the MEG website at www.metalseconomics.com; phone (902) 429-2880; fax (902) 429-6593; email [email protected].

About Metals Economics Group (www.metalseconomics.com)Metals Economics Group (MEG) is the most trusted source of global mining information and analysis. We draw on three decades of comprehensive information and analysis, with an unsurpassed level of experience and historical data. To help our clients reach better decisions more quickly, we supply raw data and sophisticated analysis based on unbiased research and reporting. From worldwide exploration, development, and production to strategic planning and acquisitions activity—our databases and studies help you make confident decisions and, ultimately, improve results.

MEGContact: Nadine Tanner, Director, Marketing, Metals Economics Group, Suite 300, 1718 Argyle St., Halifax, Nova Scotia, Canada B3J 3N6. T: +1 902.429.2880; F: +1 902.429.6593; [email protected].

Radioactive; Uranium ore; Uranium billet.

Rustico (rus.ti.co) “simplicity and charm typical of the countryside, rural setting with a relaxed welcome-home attitude, romantic, artisan, handcrafted quality.” Swirl and savor our boutique winery portfolio from old-fashioned tumblers while sharing the ambience of an antique-filled olden-days’ tasting saloon. Try Farmer’s Daughter Dry Gewürztraminer, Isabella’s Poke Pinot Gris, Doc’s Buggy Pinot Noir, Mother Lode Merlot or Last Chance, a five-varietal big red and if still cellared, share our certified gold edition Threesome, a CabFranc / CabSauv / Merlot blend or maybe Bonanza the old-vine Zinfandel people are talking about.

Experience Rustico’s heritage, hand-hewn, sod-roof silver mine bunkhouse and collection of vintage ranch wagons while toasting the ranching, mining and agricultural history of Oliver and Osoyoos in the South Okanagan. Bring along your country picnic to the chuck-wagon and we’ll provide dishes and cutlery. Then enjoy the misted coolness of our shady old pergola and corral overlooking hundreds of vineyard acres across the valley to Lake Osoyoos. Rustico Farm & Cellars on the southwest corner of the acclaimed Golden Mile where old-vines thrive in the country’s premier text-book terroir . . . and folks say we’re Canada’s most romantic winery!

rusticowinery.com • 250.498.3276Golden Mile Oliver, BC