Report No. 373-PAK Pakistan Appraisal of Multan Fertilizer Expansion ... · PDF fileReport No....

185

Report No. 373-PAK FILE Copy Pakistan Appraisal of MultanFertilizer Expansion Project April 3, 1974 Industrial ProjectsDepartment Not for Public Use Document of the International Bank for Reconstruction and Development International DevelopmentAssociation This report was prepared for official use only by the BankGroup. It may not be published, quoted or cited without Bank Group authorization. The BankGroup does not accept responsibility for the accuracyor completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of Report No. 373-PAK Pakistan Appraisal of Multan Fertilizer Expansion ... · PDF fileReport No....

Report No. 373-PAK FILE CopyPakistanAppraisal ofMultan Fertilizer Expansion ProjectApril 3, 1974

Industrial Projects Department

Not for Public Use

Document of the International Bank for Reconstruction and DevelopmentInternational Development Association

This report was prepared for official use only by the Bank Group. It may not be published,quoted or cited without Bank Group authorization. The Bank Group does not accept responsibilityfor the accuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS WEIGHTS AND NWASURES

Except where otherwise indicated All units are metric., except gasall figures are quoted in Pakistan volume which is in cubic feet.Rupees (PRs).

PRs 1.0 US$0.10 1 Metric Ton (t) = 1,000 Kilograms (Kg)PRs 9.90 US$1.00 1 Metric Ton (t) = 2,204.6 PoundsPRs 1 million US$101,010 1 Kilometer (km) = 0.62 miles

1 Hectare = 2.47 acres1 Cubic Meter = 35.3 cubic feet

PRINCIPAL ABBREVIATIONS AND ACR0NY1S USED

ANL Ammonium Nitrate Limestone (26-0-0, i.e. 26% Nitrogen)CAN Calcium Amonium Nitrate (26-o-o, i.e. 26% Nitrogen)DAP Diammonium Phosphate (18-46-0, i.e. 18% Nitrogen, 46% P205)K20 (abbrev. K) Potassium Oxide, the Indicator of Potassium Content of

FertilizerMAP Mono-Ammonium Phosphate (11-55-0, i.e. 11% Nitrogen,

<5% P2o5)N Nitrogen, the Indicator of Nitrogen Content of FertilizerNP Nitrophosphate (23-23-0)P2O5 (abbrev.P) Phosphorus Pentoxide, the Indicator of Phosphorus Content

of FertilizerTSP Triple Super Phosphate (0-46-0, i.e. 46% P205)

KWH Kilowatt HourMCF Thousand Standard Cubic FeetPPm Parts per Milliontpd Metric Tons per Daytpy Metric Tons per Year

ADB Asian Development BankA.^OC Abu Dhabi National Oil CorporationDH Dawood Hercules Chemicals LimitedGOP, Government Islamic Republic of Pakistan, The GuarantorIFC International Finance CorporationNFC National Fertilizer CorporationNGFF Natural Gas Fertilizer CorporationPASC Punjab Agricultural Supplies CorporationPFL Pakarab Fertilizers Limited, The BorrowerSNGPL Sui Northern Gas Pipelines LimitedWPIDC West Pakistan Industrial Development Corporation

FISCAL YEAR

July 1 - June 30 for NGFFJanuary 1 - December 31 for PFL

PAKISTAN

MULTAN FERTILIZER EXPANSION PROJECT

TABLE OF CONTENTS

Page No.

SUMMARY AND CONCLUSIONS ........................ i - i

I. INTRODUCTION ................. 1............

A. General ..................... 1B. Bank Group Involvement in the Pakistan

Fertilizer Sector .. ......

II. THE COMPANY .............................. 2

A. Background and Ownership ..... ............... 2B. Existing Facilities ...... ................... 3C. Organization and Management ..... ............ 3D. Financial History of Existing Facilities .... 4E. Transfer of Existing Operations to PFL ...... 4

III. FERTILIZER MARKET AND MARKETING ............ ... 5

A. Past Fertilizer Growth in Pakistan .... ...... 5B. Fertilizer Forecast for Pakistan .......... 6C. Fertilizer Forecast for the Project's

Principal Marketing Area ................ . 6D. Competition ................................... 7E. Credit Availability and Other Constraints ... 8F. Transportation .... .......................... 9G. Fertilizer Distribution ..... ................ 9H. Prices . . . . . . . . . . . ...................... . . 9

IV. THE PROJECT ... 1..............1

A. Objectives, Scope and ProjectDescription ......... 11

B. Raw Materials and Utilities ............... .. 11C. Basis for Location and Product Mix .......... 12D. Ecology and Safety Considerations ........... 12

This report has been prepared by Messrs. Perram, Pratt and Shen of theIndustrial Projects Department.

TABLE OF CONTENTS (Cont'd)

Page No.

E. Labor Force and Training .................... 13P. Project Implementation, Procurement and

Construction ............................. 13

V. CAPITAL COST AND FINANCING PLAN .................. 14

A. Project Cost ......... 4. .......... ............ 14B. Working Capital .............................. 16C. Financing Plan ....... ..... .................. 16D. Allocation and Disbursement ... .............. 17

VI. FINANCIAL ANALYSIS OF THE PROJECT ......... ....... 19

A. Basis of Analysis ............... ... ....... . 19B. Operating Costs and Revenues ............... . 19C. Financial Indicators .... .................... 21D. Profitability and Financial Return ........ . 21E. Financial Position, Debt Service Coverage

and Financial Covenants ................ .. 22F. Major Risks .............. ................... 24

VII. ECONOMIC ANALYSIS ................... ... 24

A. International Fertilizer Prices ............. 24B. Economic Rate of Return .... n................. 25C. Foreign Exchange Savings .................... 25D. Other Economic Benefits ....... .............. 26

VIII. AGREEMENTS REACHED WITH THE GUARANTOR, NATIONALFERTILIZER CORPORATION AND THE BORROWER .......... 26

TABLE OF CONTENTS (Cont'd)

ANNEXES

1-1 Glossary of Technical Terms1-2 Alternative Project Scope Studies1-3 Dawood Hercules Results1-4 Fauji Foundation Urea Project

2-1 Sponsors and Management2-2 Financial Statements - Existing Plants

3-1 Agricultural Sector in Pakistan3-2 Fertilizer Industry in Pakistan3-3 Fertilizer Distribution, Credit, Prices and Transportation

4-1 Project Description4-2 Production Flow Chart4-3 Production Processes4-4 Plant Layout4-5 Raw Materials4-6 Environmental Protection and Safety4-7 Project Schedule

5-1 Capital Cost Estimate5-2 Working Capital Requirements5-3 Projected Disbursement of Bank Loan

6-1 Production Costs6-2 Financial Forecasts6-3 Financial Return and Sensitivity Tests6-4 Break-Even Chart

7-1 Economic Return and Sensitivity Tests7-4 Foreign Exchange Savings

MAP

Present and Proposed Fertilizer Plants in Pakistan (IBRD 10818)

PAKISTAN

MULTAN FERTILIZER EXPANSION PROJECT

SUMMARY AND CONCLUSIONS

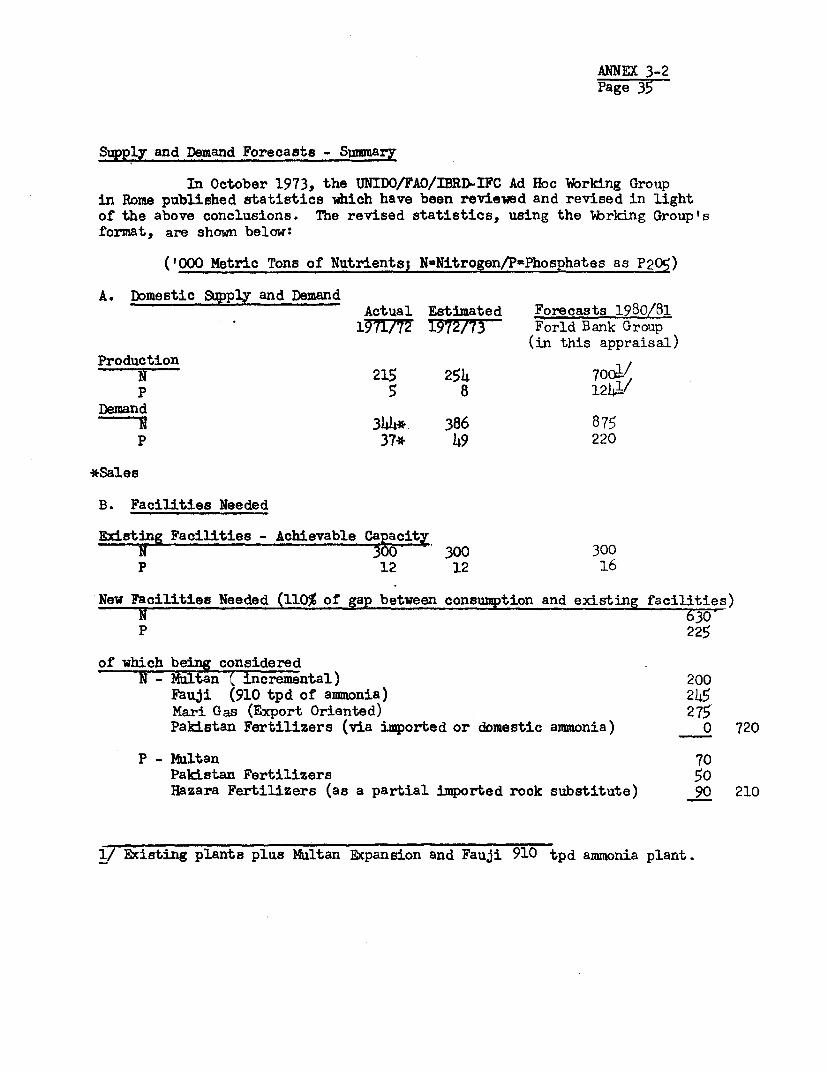

i. This report appraises the proposed expansion of the Government-owned Natural Gas Fertilizer Factory (NGFF) operated by the National FertilizerCorporation (NFC) at Multan in the Province of the Punjab. NGFF has producedurea and ammonium nitrate limestone since 1962 from natural gas from the Suigas field. To cater to the growing fertilizer requirements of the country,NFC will buiild a large new ammonia plant with a daily capacity of 910 tons-- thereby allowing it to shut down the existing small and obsolete ammoniaunits. The ammonia will feed the existing fertilizer plants as well as newfertilizer units which are to produce high water soluble nitrophosphate (1,020tons/day) and calcium ammonium nitrate (1,500 tons/day). A new company,Pakarab Fertilizer Ltd. (PFL) to be owned 70% by NFC and 30% by the Abu DhabiNational Oil Corporation (ADNOC), has been formed and will be the Borrower.The expansion, which will also be based on Sui gas and which will increasePakistan's annual fertilizer production by about 200,000 tons of nitrogen(N) and 70,000 tons of phosphate in terms of P20 , is expected to cost PRs928 million (US$94 million). Engineering work started in February 1974 andthe project is to be completed by the end of 1976.

ii. The Bank's only direct financing of industry in Pakistan to datehas consisted of a US$32 million loan in 1968 (together with an IFC investmentof US$2.9 million) for the Dawood Hercules Chemicals (DH) ammonia/ureafertilizer project, also located in the Punjab near Lahore. Constructionwas completed on schedule in July 1971 and was achieved with only a minorcost overrun, primarily due to increases in customs duties. DH has rapidlyattained and been able to sustain over 100% rated capacity production. Inappraising the DH project, the Bank pointed out the critical importance ofbalancing nitrogen with phosphatic fertilizers. The Multan project will helpto achieve this aim. No additional fertilizer plants have be en built inPakistan recently but other projects are now being planned, one of which -an ammonia/urea plant sponsored by the Pauji Foundation of Pakistan - IFC hasbeen asked to assist.

iii. Fertilizer consumption has increased rapidly in Pakistan since theearly 1960's. Sales of nitrogenous fertilizers went up from 41,000 nutrienttons in 1962/63 to about 400,000 tons in 1972/73, somewhat above the projec-tions made in the DH appraisal report. The rapid growth in fertilizer con-sumption has been due largely to the greater awareness of the benefits offertilizers among the farmers and to the Government's effort to increase itsavailability. With regard to future use of fertilizers, it is estimated thatby about 1980 demand will reach some 875,000 nutrient tons for nitrogenousand 220,000 nutrient tons for phosphatic fertilizers. Pakistan's productionincluding the expanded Multan plant and the Fauji project, is expected toamount to about 700,000 nutrient tons of N and 80,000 nutrient tons of P 0The project therefore is particularly urgent. Since nitrophosphate fertilizers

- ii -

arec -r-elatively new to the farmers in Pakistan, the Government has agreed toimport such fertilizers for promotional purposes prior to the completion ofthe project.

iv. The Gcvernment of Pakistan has asked IBRD and the Asian DevelopmentBank (ADB) for loans of US$35 and 27 million equivalent respectively; theUS$40 million balance of the US$102 million financing required will be coveredb,7 equity from NFC and ADNOC and local loans. The proposed Bank loan willf3nviace the cost of equipment and spares for the amonia plant and utilities,r-he f_i> fer related engineerirg and the technical advisor. The loan will befor 15 years, including four years of grace, with an effective interest rateto PFL of 9-1/2% per annum, including a guarantee fee accruing to the Govern-ment. The Bank loan will meet about 40% of the cost of the project or about50% of its foreign exchange needs. The balance of the foreign exchange expen-ditures will be covered by the ADB loan to be used primarily for the nitricacid and nitrophosphate plants, and by a portion of the equity, which is alsoto finance local expenditures. No cash generation from the existing planthas been assumed in the financing plan. Although not many local suppliersare expected to qualify for the type of equipment to be financed by the Bank,they will be allowed a preference of 15% or the customs duties for a non-exemptimporter whichever is lower.

v. The objectives of the project are: (1) to provide an economic-sizedplant (based on modern proven technology new to Pakistan) to help meet thecountry's phosphate needs, now met mostly by limited imports; (2) to avoidforeign exchange expenditures for imported sulfur by using nitric acid madefrom Pakistan natural gas instead of sulfuric acid; and (3) to supply nitrogento reduce the dependence on expensive, often hard to obtain, imports. Theproject is not designed to meet all of Pakistan's nitrogen and phosphateneeds as other urea plants and an additional phosphate plant are planned tocomplement the expanded Multan production at appropriate future intervals.

vi. The project is designed to assist Pakistan to utilize more fullyat an economic cost its agricultural potential particularly in the Punjab, itsmost fertile agricultural area. Pakistan's agronomic potential for fertilizerusage would be greater than assumed in this report were it not for constraintssuch as credit, water, seeds, pesticides, and shortage of foreign exchangefor imports. As in the past, insufficient production in the short run willcontinue to be the most serious handicap to more rapid increases in Pakistan'sagricultural output.

vii. The project has been developed with the assistance of a competentPakistani firm of chemical consultants. The project's Managing Director andGeneral Manager (Project) have been appointed. The Bank has emphasized theimportance of forging a strong and effective team to carry out the projectand has stressed the need for an experienced industrial management to thisend. PFL has appointed a qualified firm with nitrophosphate experience as"owner's representative"i or technical advisor to assist the project's manage-ment during construction and uatil all units can be run on a sustained basis

- iii -

of at least 90% of capacity without further outside assistance. The exist-ing plant currently employs a total of 1,700 workers including 42 technicaland 20 non-technical supervisors. Due to a substantial excess of labor atthe plant at present, no additional workers will be required for the expandedplant.

viii. The project's capitalization, based on about 64/36 debt/equityfinancing provides a sound basis. As the loans are repaid and reservesbuilt up out of earnings, the company's financial position will furtherimprove and further expansion should be possible. A satisfactory return onthe equity is sought by the Government as well as the shareholders to attractadditional capital to the fertilizer industry. To ensure PFL's financialviability, the Bank obtained agreement that the Government will not set: ferti-lizer prices at a level which would prevent PFL from reaching the earningstarget set by its shareholders, i.e., a 15% return on equity. Projectedcash generation for long-term debt service coverage is adequate. The finan-cial return, using an increased gas cost to take into account the returnrequired by the gas supply company (Sui Northern Gas Pipelines Ltd.), isestimated to be 23% before tax and 17% after tax. Even under adverse condi-tions, the financial return is not expected to drop below 10%.

ix. The project's estimated economic return is 34%, reflecting thecompetitive advantage of local production from indigenous gas compared tolong-term import prices (assumed in the report to be about 50% of currenthigh world market prices). Based on foreseeable adverse factors such asincreased gas, phosphate rock and bag costs not fully offset by higherprices, and a maximum production of 80% of capacity, the economic returnwould still be above 20%. Annual net foreign exchange savings ascribed tothe project at 90% capacity are estimated to be US$50 million.

x. Based on agreements reached as summarized at the end of the report,the project is suitable for a Bank loan of US$35 million equivalent.

I. INTRODUCTION

A. General

1.01 The Government of Pakistan has requested a Bank loan of US$35million equivalent for a project which is expected to cost US$94 millionequivalent and which is to increase more than five-fold the capacity of therather small and partly outdated Multan nitrogenous fertilizer unit of theGovernment-owned National Fertilizer Corporation (NFC). The Asian Develop-ment Bank (ADB) has agreed to lend US$27 million for the project and thebalance will be financed with equity and rupee loans on terms satisfactoryto the Bank. The proposed Bank loan would be made to Pakarab FertilizersLimited (PFL), a newly formed company owned by NFC (70%) and the Abu DhabiNational Oil Corporation (ADNOC) (30%) and would be guaranteed by Pakistanand NFC. The project, based on indigenous natural gas and imported phosphaterock would increase capacity by 306,000 tons per year (tpy) of nitrophosphate 1/(NP) and 450,000 tpy of calcium ammonium nitrate (CAN) 2/ and provide 57,000tpy of ammonia for the existing plant. Upon completion of the project theMultan fertilizer unit would have a total capacity of about 240,000 tpy ofnitrogen (N) and 70,000 tpy of phosphate (P205). Detailed engineeringcommenced in February 1974 and commercial production is scheduled to startby January 1977.

1.02 Multan, located in the center of the Punjab province, Pakistan'sprime agricultural area (IBRD MaplO818), is one of three NFC fertilizer units.The plant began production in 1962 and has never operated at full capacitydue to technical difficulties in the ammonia section. However, despitethese difficulties and the sub-economic size of most plant units, the factoryhas shown a profit in most years by virtue of subsidies paid by the provincialand central governments.

1.03 The project was first reviewed by the Bank in mid-1972 and alter-native projects (Annex 1-2) were evaluated by local consultants (ChemicalConsultants Pakistan, Ltd.) in early 1973 at the Bank's request. The proj-ect of the scope and size now proposed resulted from these comparativestudies.

1.04 The appraisal was carried out in Pakistan in September/October 1973by Messrs. Perram (Chief), Pratt and Shen of the Industrial Project Departmentconcurrently with an ADB appraisal mission.

B. Bank Group Involvement in the Pakistan Fertilizer Sector

1.05 The proposed loan would be the Bank's second for a fertilizer projectin Pakistan; the first loan of US$32 million equivalent together with an IFCequity investment of US$2.9 million was made in July 1968 to Dawood Hercules

1/ A Glossary of Technical Terms is contained in Annex 1-1.

2/ Equivalent to 187,000 tpy of N and 70,000 tpy of P as P 02 5

-2-

5he :llS6 11 (D) for their 620/1,100 tpd ammonia/urea plant (Report AA-4a datedJune 2C 8.6`). D. began production in July 1971 virtually on schedule andwithin the original foreign exchange budget. The plant reached rated capacityin record time and has been operating above capacity on a sustained basis.Local ca?itai costs were higher than estimated due primarily to increases incustom duties. Currency revaluations also increased the amount of the dollarequivaient of 4he Bank loan disbursemenlts to over US$35 million equivalentres:lting in a total cost of US$84.6 million versus the original US$78.2million estimate. Annex 1-3 describes the DH results to date.

1.06 At the time of the DH loan the Bank was considering a second similarfertilizer project to meet Pakistan's growing nitrogen needs. Due to avariety of factors including failure of the local and foreign partners toreach sntisfactory agreements between themselves and the Government, theGovrernment sanction expired. Since then no major fertilizer project hasboen implemented in Pakistan except DH. IFC is now considering anotherammonia/urea project sponsored by Pakistan's Fauji Foundation and the Bankmay also be asked to participate in the financing (Annex 1-4).

II. THE COMPANY

A. Background and Ownership

2.01 The project will be carried out by PFL, which has an authorizedcapital of PRs 1,000 million (US$101 million). The 70% owner, NFC, is agovernment agency whose primary purpose is to operate and promote fertilizerproduction in the public sector. It succeeded the West Pakistan IndustrialDevelopment Corporation (WPIDC) vhich grew into a large complex organization,having until recently operational responsibility for most of the 59 projectsit Promoted; it is now gradually divesting itself of these operational respon-sibilities in line with a reorganization announced in August 1973 and intendsincreasingly to play the role of a development corporation. WPIDC has notreceived any financing from the Bank. During construction of the project,NFC will exercise control over PFL through its majority on the PPL Board butit is anticipated that once PFL is operational the relationship will becomethat of a holding company to one of its investments. NFC has agreed to guar-antee the proposed Bank loan and not to dispose of any of its shares in PPLwithout Bank approval. In March 1973, ADNOC, the Abu Dhabi Government'snational oil corporation, agreed to acquire 30% of the equity of the new ferti-lizer company. ADNOC's interest in investing in a fertilizer plant in Pakistanis in accordance with an agreed plan of mutual cooperation between Pakistanand Abu Dhabi in certain ventures, including joint investments in industry,particularly oil refineries. ADNOC's role as a minority shareholder is clearlyone of an investor; the promotion, financing, organization and implementationof the project is being left to NFC. Annex 2-1 describes the sponsors, theinitial Board, the senior officers and L a organization chart.

-3-

B. Existing Facilities

2.02 These comprise two 100 tpd ammonia plants plus downstream unitsfor making 180 tpd crystalline urea, 200 tpd nitric acid (100% basis) and300 tpd ammonium nitrate-limestone (ANL-26% N). Offsites include boilers,water treatment and cooling, storage buildings, offices and a housing colony.The ammonia plants have never averaged more than about 80% of their capacityon a sustained basis and require excessive maintenance. Conversely, thedownstream units have worked well and can achieve 120% of design capacity,given sufficient ammonia. Consequently, as is described in more detail inconnection with the discussion of the project in Chapter IV, it is intendedto shut down the ammonia plants. PFL will keep the downstream units in opera-tion to produce, after some modification, prilled urea (46% N) and CAN (26%N). Economically produced ammonia from the project and the virtual elimina-tion of depreciation and financial charges on the existing plants is expect-ed to result in economic operation, even though the capacities are small andthe units are old.

C. Organization and Management

2.03 NFC has the right to appoint 8 and ADNOC 4 directors. PFL'sinitial Board was designated in November 1973. The full Board is beingconstituted. NFC has elected its Chairman Mr. Baber Ali as PFL's Chairmanand appointed a Managing Director who will have day to day responsibilityfor the Company's operations. The Chairman is well known to the Bank Groupand is considered to be an outstanding industrial executive with a successfulrecord in private industry. The Managing Director, Mr. Amman Ullah Loan, isthe former Technical Manager of Stii Northern Gas Pipelines, Limited. He isan engineer, well-known to Bank staff. He will coordinate the work of theTechnical Advisor, the engineering firms and the local Chemical Consultants.While he has no experience as an industrial executive, he has been associatedwith Bank financed projects and has demonstrated the drive and initiativeneeded for this new assignment. Furthermore, NFC's Chairman has been givenfreedom to offer salaries to attract experienced industrial executives, andas necessary, he will seek additional senior management with industrial experi-ence. The selected project manager, Mr. Zahur Ahmad Khan, has been with NFCand its predecessors for about 20 years and has the technical knowledge andability to direct work at the site. He also has general familiarity with theexisting facilities.

2.04 The existing plant will be operated by the present experiencedGeneral Manager, Mr. Hafizullah, under the Managing Director's control. Afterthe project is completed and operation of the old and new plants integrated,reassignments are anticipated.

D. Financial History of Existing Facilities

2.05 Detailed historical and forecast financial statements for theexisting Multan facilities without the project are contained in Annex 2-2.As the project will replace the existing ammonia units and provide the oldurea and ANL units with new ammonia, the financial history of Multan bearslittle relation to the project or PFL. Also, fertilizer price changes inPakistan in August 1973 and the up-grading of the urea product by prillinghave considerably changed the financial outlook of the existing unit.

2.06 Capacity of the existing plants is about 70,000 tpy of N based onthe 200 tpd ammonia units. However, the production since 1969 in terms ofN has been as follows:

Multan Production of Nitrogen('000 tons of N)

Year Ended June 30 1969 1970 1971 1972 1973

Urea 21 21 15 12 6

ANL 17 22 22 20 16

38 43 37 32 22

Results for 1973 were adversely affected by strikes and compressor failures.Production forecasts for the next three years show 42,000 tpy of N splitevenly between urea and ANL. This can be achieved but will depend primarilyon the sustained operation of the old ammonia units.

2.07 Financially the Multan operation has shown a total net profit ofonly PRs 14 million over the five years, 1969-73, after a subsidy 1/ of PRs 120million from the provincial and central governments. Cash generation (includingthe subsidy) over the period was PRa 100 million. With higher fertilizer prices,(para. 3.13) NFC requires less subsidy and Multan is expected to show improvedfinancial results during project implementation. However, the financing planfor the project does not take into account any cash generation that may becontributed by the existing plant. Of the original PRs 237 million investmentmade during the early 1960's (about US$50 million at the then current exchangerate), the Multan unit had by June 30, 1973 transferred PRs 207 million toWPIDC in lieu of debt repayments in addition to 7% interest on the investment(less transfers).

E. Transfer of Existing Operations to PFL

2.08 NFC intends to retain ownership of the existing operation untilthe project is completed to utilize the depreciation, tax and subsidy con-cessions granted to the unit. Upon project completion, NFC will transfer

1/ The subsidy was based on a margin of 6% between operating cost andrevenue including the subsidy.

the existing Multan fertilizer business to PFL at which time these conces-sions will expire. Pending such transfer NFC has agreed to limit its annualcapital expenditures relating to the Multan business to US$1 million equivalent.

III. FERTILIZER MARKET AND MARKETING

3.01 Past and projected consumption and production of fertilizer inPakistan, with special reference to the Province and District where theproject will be located, are detailed in Annex 3-1. An international con-sumption pattern is also given for comparison (Annex 3-2).

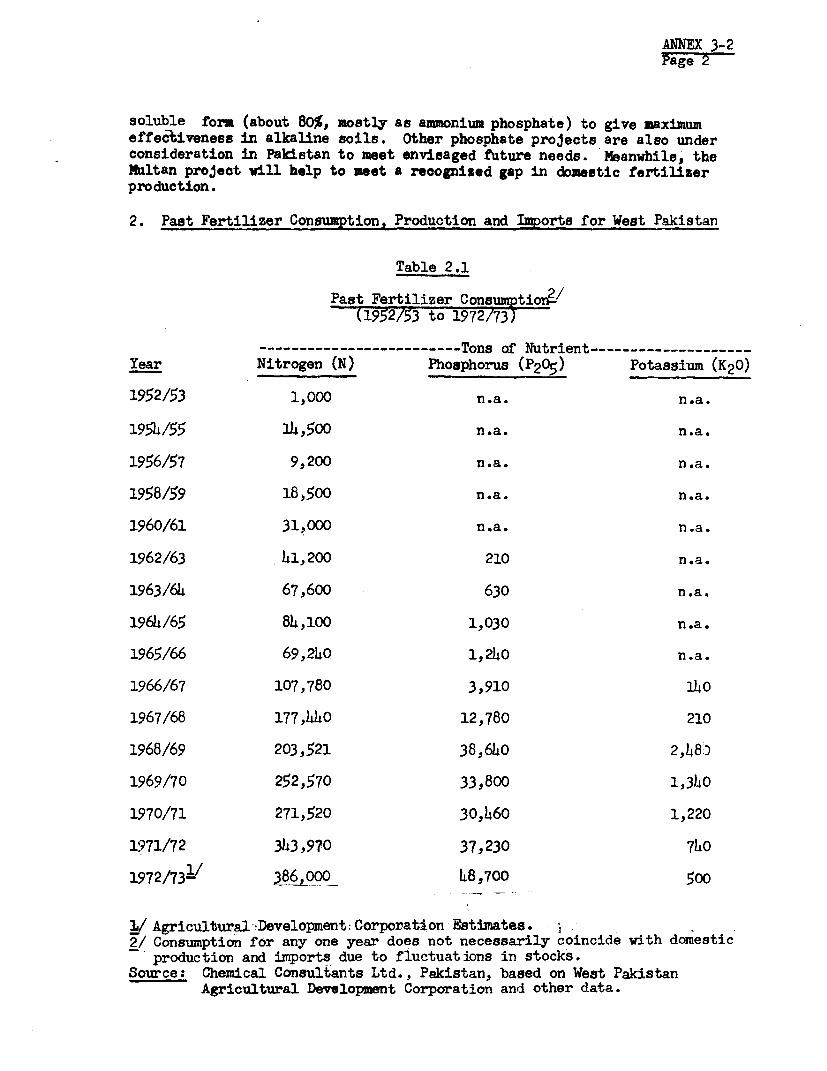

A. Past Fertilizer Growth in Pakistan

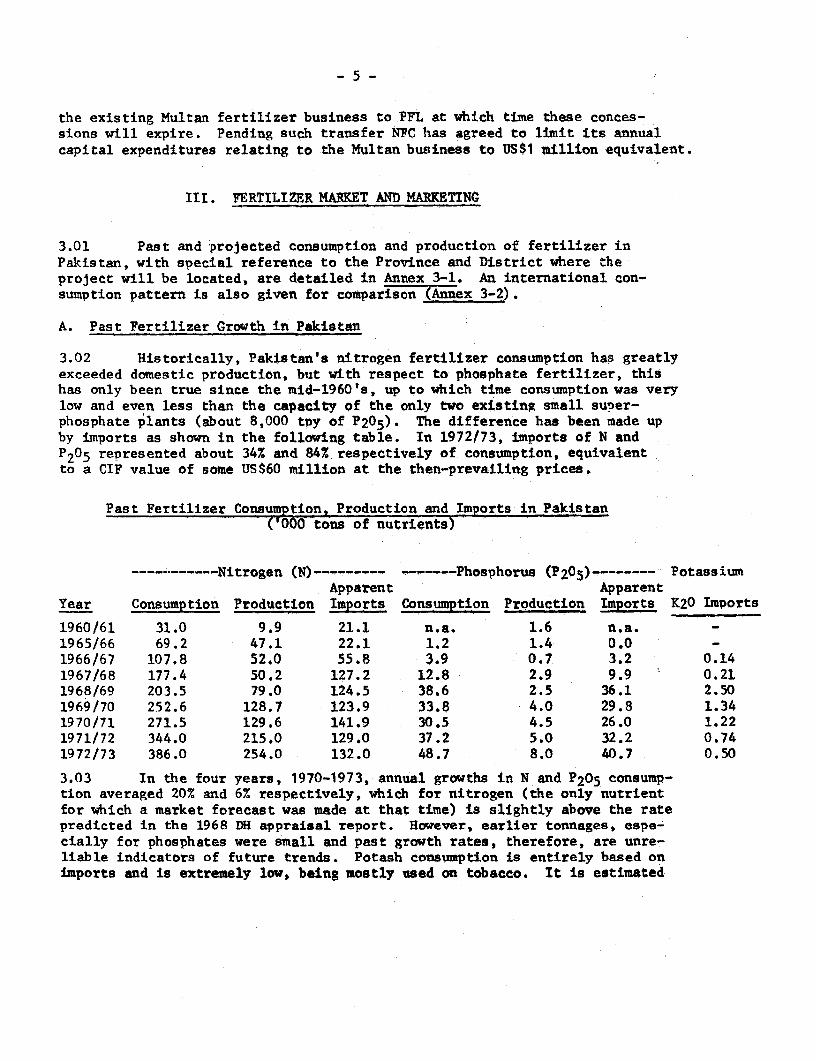

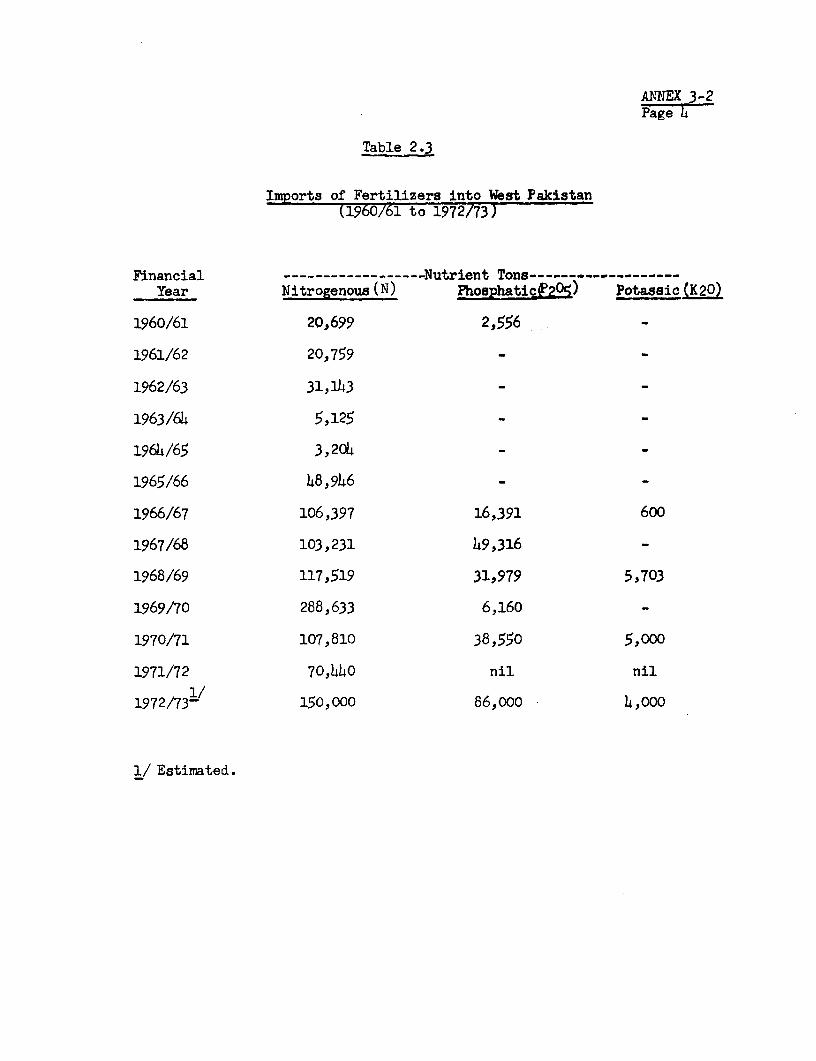

3.02 Historically, Pakistan's nitrogen fertilizer consumption has greatlyexceeded domestic production, but with respect to phosphate fertilizer, thishas only been true since the mid-1960's, up to which time consumption was verylow and even less than the capacity of the only two existing small super-phosphate plants (about 8,000 tpy of P205). The difference has been made upby imports as shown in the following table. In 1972/73, imports of N andP205 represented about 34% and 84% respectively of consumption, equivalentto a CIF value of some US$60 million at the then-prevailing prices.

Past Fertilizer Consumption, Production and Imports in Pakistan('000 tons of nutrients)

…---------Nitrogen (N) --- ------- Phosphorus (P205)-------- PotassiumApparent Apparent

Year Consumption Production Imports Consumption Production Imports K20 Imports

1960/61 31.0 9.9 21.1 n.a. 1.6 n.a.1965/66 69.2 47.1 22.1 1.2 1.4 0.0 -1966/67 107.8 52.0 55.8 3.9 0.7 3.2 0.141967/68 177.4 50.2 127.2 12.8 2.9 9.9 0.211968/69 203.5 79.0 124.5 38.6 2.5 36.1 2.501969/70 252.6 128.7 123.9 33.8 4.0 29.8 1.341970/71 271.5 129.6 141.9 30.5 4.5 26.0 1.221971/72 344.0 215.0 129.0 37.2 5.0 32.2 0.741972/73 386.0 254.0 132.0 48.7 8.0 40.7 0.50

3.03 In the four years, 1970-1973, annual growths in N and P205 consump-tion averaged 20% and 6% respectively, which for nitrogen (the only nutrientfor which a market forecast was made at that time) is slightly above the ratepredicted in the 1968 DH appraisal report. However, earlier tonnages, espe-cially for phosphates were small and past growth rates, therefore, are unre-liable indicators of future trends. Potash consusption is entirely based onimports and is extremely low, being mostly used on tobacco. It is estimated

-6-

that acttual fertilizer consumption would have grown faster, were it not forscme of the constraints described in Section E below; these have been, inparticular, lack of the foreign exchange to import fertilizer, and more re-cently the scarcity of fertilizer on world markets, coupled with unprecedentedprice increases.

B. Fertilizer Forecast for Pakistan

3.04 Demand estimates prepared by experienced agronomists in Pakistanand based 'on likely crop patterns as well as production forecasts, takinginto account existing and probable additional fertilizer capacity (Multanand Fauji) are summarized below. These are detailed in Annex 3-2 andrepresent average annual growth rates of 11% for N and 21% for P205.

…----Nitrogen (N)----- ----Phosphorus (P 20 5 ) - Potash (K20)Apparent Apparent

Year Demand Production Imports Demand Production Imports Imports

1973/74 430 281 149 60 9 51 101974/75 475: 290 185 73 10 63 151975/76 530 292 238 90 10 80 201976/77 590 346 244 108 40 68 251977/78 650 551 99 130 72 58 301978/79 720 678 42. 155 104 51 351979/80 790 697 93 185 112 73 401980/81 875 697 178 220 124 96 45

It can be seen that even after the Multan and Fauji projects will have comeon stream (expe'ted for 1977 and 1978 respectively), Pakistan would stillhave to import fertilizer to meet predicted demand for both N and P2 05 . Theabove forecasts are about in the middle of various demand predictions, sothat maximum fertilizer use in 1980/81 could be some 15% and 20% above therespective N and P2 05 forecasts used here. Furthermore, Pakistan's fertilizerapplication rates are still among the lowest in the world and on a per capitabasis are below those of India. Finally, Pakistan has still a very high N/P2 05application ratio of about 9/1 as compared to a world average of 1.6/1. Evenaccounting for varying soil conditions, there is therefore much room forPakistan to increase its usage of phosphate fertilizer. Furthermore, promptadditional use of phosphates (and potassium later) is essential, otherwisemuch of the extra nitrogen added and the benefits of planting high-yieldingvarieties of wheat, rice and other crops will be wasted. This matter wasemphasized during negotiations.

C. Fertilizer Forecast For the Project's Principal Marketing Area

3.05 As indicated in Annex 3-1, the Punjab (the major market area of theproject) reprev-ents some 65% of the country's cropped acreage and producesoYter 70% of it. !.a_or crops. This province, together with the North Westi! :^ier Province (NWFP), an adjoining small potential market area for thep.L, 4accounted for 75% of Pakistan's N and P2 05 consumption during the last

-7 -

three years. Based on agronomic forecasts, this proportionate demand isexpected to continue, thus giving the following projected demand and pro-duction pattern for these two provinces.

Projected Fertilizer Demand and Production in the Punjaband North West Frontier Provinces

('000 tons of nutrients)

…------ Nitrogen (N)-------- -- Phosphorus (P205)-------Surplus Surplus

Year Demand Production (Deficit) Demand Production (Deficit)

1973/74 322 281 (41) 45 9 (36)1974/75 356 290 (66) 55 10 (45)1975/76 398 292 (106) 67 10 (57)1976/77 443 346 (97) 81 40 (41)1977/78 490 551 61 97 72 (25)1978/79 540 678 138 117 75 (42)1979/80 593 697 104 139 79 (60)1980/81 658 697 39 165 79 (86)

D. Competition

3.06 The above production projections for nitrogen conservatively assumethat the Fauji Foundation will proceed with the larger of two project alterna-tives (530,000 tpy of urea or 240,000 tpy of N) and that all its output wouldbe available in the Punjab and the NWFP. While the Fauji plant would bebuilt in the Punjab, its proposed location is, however, only some 40 km fromthe Punjab/Sind border and most of its natural market therefore would be inthe Sind. On the other hand, the Multan plant lies in the Multan Districtand thus in the heart of the main marketing area which consumes 64% of N salesin the entire Punjab Province, and is some 330 km distant from the envisagedFauji plant. Therefore, even if the larger Fauji plant were to be built andeven if some excess of nitrogen fertilizer appears in the Punjab during thelate 1970's (as indicated by the above table), no really significant competi-tion is foreseen.

3.07 Regarding P205 competition, the only other phosphate plant thathas been sanctioned to date is a monoammonium phosphate (MAP) plant atKarachi, based on imported phosphoric acid. In addition phosphate rock hasbeen discovered in the NWFP and consideration of a fertilizer plant near thedeposits is under study. As phosphate fertilizer is likely to continue tobe in short supply throughout the forecast period, and the Karachi projectwould be about 800 km distant from Multan, competition would be insignificant,especially as the MAP is expected to find ready sales in the Sind. Projecteddomestic N and P205 production and demand in the project's marketing area arecompared in tabular and graphic form in Annex 3-3.

- 8 -

E. Credit Availability and Other Constraints

3.08 Many large and medium sized farms can pay cash or obtain short-term loans for fertilizers and other needs, such as from the AgriculturalBank at about 8% interest, but millions of subsistence cultivators have hadno access to credit on favorable terms. The Government planned to make PRs775 million credit available to the poorer farmers in 1973/74, via commercialbanks, agricultural supply corporations, cooperatives and the AgriculturalDevelopment Bank. Also, the newly-formed Punjab Agricultural Su;rplies Corpo-ration (PASC) intends not only to bring fertilizer and other inputs to thepoorer rural areas but also to provide credit to purchase them. It is intendedthat some of these loans would be interest-free and be secured by future crops.Nevertheless, as the potential for increasing agricultural output is largestwith the great number of small farms and increased fertilizer for such smallfarms has been assumed in the projections, the Government has agreed to makeavailable to the Bank by December 31, 1974 a detailed description of an agri-cultural credit program to be prepared and implemented by the Governmentthroughout Pakistan, and has agreed to afford to the Bank reasonable oppor-tunity to comment thereon. Such credit facilities will become increasinglyimportant as fertilizer consumption in Pakistan is expected to continuerising during the remainder of this decade.

3.09 Other major actual and potential constraints include increasinginternational fertilizer prices and decreasing fertilizer availability, limitedwater supplies, fixed crop prices and poor farmer education. Most farms aretotally dependent on irrigation or uncertain rainfall and during the earlymonths of 1970 and 1971, river and well levels were the lowest in 100 years.However, completion of the Tarbela Dam in 1974 will help to provide more regu-lar irrigation. Lack of sufficient fertilizer due to foreign exchange restric-tions and limited domestic production has curtailed use and appreciation ofthe benefits fertilizers provide. Greater availability from the expandedMultan plant will help to remedy this situation. Crop prices have a greatinfluence on fertilizer use and the Government has tended to delay priceincreases because of political repercussions; however, grain prices wereraised recently and the cost benefit ratio of fertilizer to crops shouldremain attractive even after further fertilizer price increases. Regardingfarmer education, producers in both the public and private sectors undertakefertilizer campaigns and demonstrations, but much additional work needs tobe done, especially in promoting greater use of phosphates. The Governmenthas agreed that it will make available to the Bank by December 31, 1974 astudy of improvements needed in fertilizer promotion and marketing to becarried out by the Government and afford to the Bank opportunity to commentthereon. The Government has also agreed to import nitrophosphate or similarphosphatic fertilizer into Multan's marketing area (equivalent to about 50,000,100,000 and 150,000 tpy of nitrophosphate in the years ending June 1974, 1975and 1976 respectively) during project implementation to prepare the farmersfor increased availability of phosphate once the project is completed and atthe same time, obtain a better N/P ratio sooner.

-9-

F. Transportation

3.10 Recent experience of Dawood Hercules and at Multan shows road trans-port to be speedier and cheaper, if distances from plant to distribution cen-ters are under 250 to 300 km. As typical distances between Multan and themajor warehouses are 130 to 160 km, it is estimated that about two-thirds ofthe project's output will be moved by road and one-third by rail. Multan hasa big truck depot and truckers are anxious to obtain extra loads. Regardingrail transport, Multan is about 60 km south and 100 km north of two of thelargest make-up yards in the country, hence no difficulty is anticipated inobtaining empty wagons and rapid turnarounds. Discussions with the railwayauthorities revealed no anticipated difficulties either in moving heavyequipment, phosphate rock and "seeding" fertilizer supplies from Karachi toMultan, or hauling finished fertilizer to railhead towns in the quantitiesrequired. Furthermore, agricultural materials are second in priority onlyto military needs.

G. Fertilizer Distribution

3.11 From 1967 to October 1973, fertilizers were distributed and soldeither by producers or by a group of Principal Agents, who had representativesin the mandi (market) towns throughout the country. In October 1973, thePunjab Provincial Government re-entered fertilizer marketing and issued adecree taking over full distribution and sales from all private and publicsector plants (except Esso which has an agreement with the Central Govern-ment to undertake its own sales of which only 15% are sold in the Punjab).Dawood Hercules obtained a concession to distribute half of its urea outputas it wishes; the remainder being handled by the Punjab Agricultural SupplyCorporation (PASC). However, the Multan plant has been instructed to sellall its current and future production through PASC.

3.12 This restricted marketing may place the Multan project at a seriousdisadvantage compared to other producers because PASC is inexperienced in thisfield. Also, absence of competition in marketing Multan's products because ofsole distribution and selling rights could reduce the educational and sal?sefforts needed to increase fertilizer use - especially by farmers with littleor no experience of proper fertilizer application. Therefore, the Governmenthas agreed that it will enable PFL to utilize or establish an efficient distri-bution network to market the project's production; the performance of thenetwork to be subject to periodic Bank review. While it is intended thatPASC should undertake this marketing, the representatives of the Governmentrecognized during negotiations that the network could be either the publicor private sector or a combination.

H. Prices

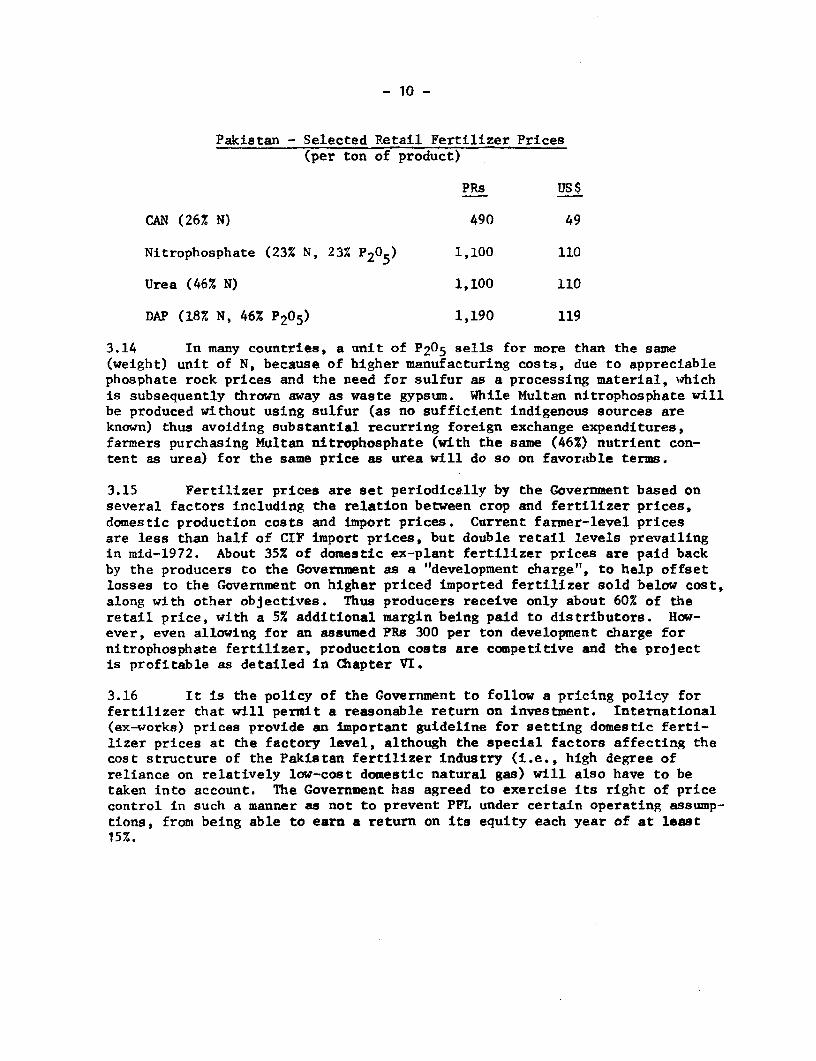

3.13 At full capacity utilization, the expanded Multan plant will producethe following types and quantities of fertilizer (in tpy): CAN 450,000;nitrophosphate 306,000; urea 72,600 and some 50,000 tons of ammonium nitratelimestone (ANL). Gazetted retail prices at farmer level after the latestincreases in August 1973 are:

- 10 -

Pakistan - Selected Retail Fertilizer Prices(per ton of product)

PRs US$

CAN (26% N) 490 49

Nitrophosphate (23% N, 23% P205) 1,100 110

Urea (46% N) 1,100 110

DAP (18% N, 46% P205) 1,190 119

3.14 In many countries, a unit of P205 sells for more than the same(weight) unit of N, because of higher manufacturing costs, due to appreciablephosphate rock prices and the need for sulfur as a processing material, wqhichis subsequently thrown away as waste gypsum. While Multan nitrophosphate willbe produced without using sulfur (as no sufficient indigenous sources areknown) thus avoiding substantial recurring foreign exchange expenditures,farmers purchasing Multan nitrophosphate (with the same (46%) nutrient con-tent as urea) for the same price as urea will do so on favoratble terms.

3.15 Fertilizer prices are set periodically by the Government based onseveral factors including the relation between crop and fertilizer prices,domestic production costs and import prices. Current farmer-level pricesare less than half of CIF import prices, but double retail levels prevailingin mid-1972. About 35% of domestic ex-plant fertilizer prices are paid backby the producers to the Government as a "development charge", to help offsetlosses to the Government on higher priced imported fertilizer sold below cost,along with other objectives. Thus producers receive only about 60% of theretail price, with a 5% additional margin being paid to distributors. How-ever, even allowing for an assumed PRs 300 per ton development charge fornitrophosphate fertilizer, production costs are competitive and the projectis profitable as detailed in Chapter VI.

3.16 It is the policy of the Government to follow a pricing policy forfertilizer that will permit a reasonable return on investment. International(ex-works) prices provide an important guideline for setting domestic ferti-lizer prices at the factory level, although the special factors affecting thecost structure of the Pakistan fertilizer industry (i.e., high degree ofreliance on relatively low-cost domestic natural gas) will also have to betaken into account. The Government has agreed to exercise its right of pricecontrol in such a manner as not to prevent PFL under certain operating assump-tions, from being able to earn a return on its equity each year of at least15%.

- t1 -

IV. THE PROJECT

A. Objectives, Scope and Project Description

4.01 The project is to produce simultaneously nitrogen and phosphatefertilizers to help mitigate current shortages of both nutrients in Pakistan,using domestic resources to the maximum extent possible. The existing in-efficient ammonia units will be shut down and replaced by one large, modern,910 tpd plant that will feed a new 1,020 tpd prilled nitrophosphate (NP) unit;a new 1,500 tpd prilled CAN unit; plus the existing urea and ANL units thatare in course of being modified to produce 220 tpd prilled urea and 200 to300 tpd granular CAN. Based on the new ammonia plant achieving 90% of an-nual capacity, Multan would produce about 275,000 tpy of NP (22.5% N and22.5% P205); 30,000 additional tpy of urea (46% N); and 425,000 tpy of extraCAN (26% N) equivalent to an additional 187,000 tpy of N and 63,000 of P205.At the same time existing facilities, offsites and labor will be used tothe optimum extent.

4.02 Nitrophosphates are not new or distinctive fertilizer compounds butmixtures of traditional fertilizer materials - ammonium phosphate and amoniumnitrate made by dissolving phosphate rock in nitric acid produced from ammonia.A product having a phosphate water-solubility of at least 80% will ensureagronomic results fully comparable with those based on phosphates such astriple superphosphate (TSP) or diammonium phosphate (DAP) made by dissolvingphosphate rock in sulphuric acid (Annex 3-3). These alternatives, as well asthe production of urea were studied and compared, as were plants of differentsizes. The products and processes chosen, as well as the plant sizes selectedrepresent the optimum combination for this specific project at the expectedlevel of fertilizer use and nutrient combination in Multan's marketing area.

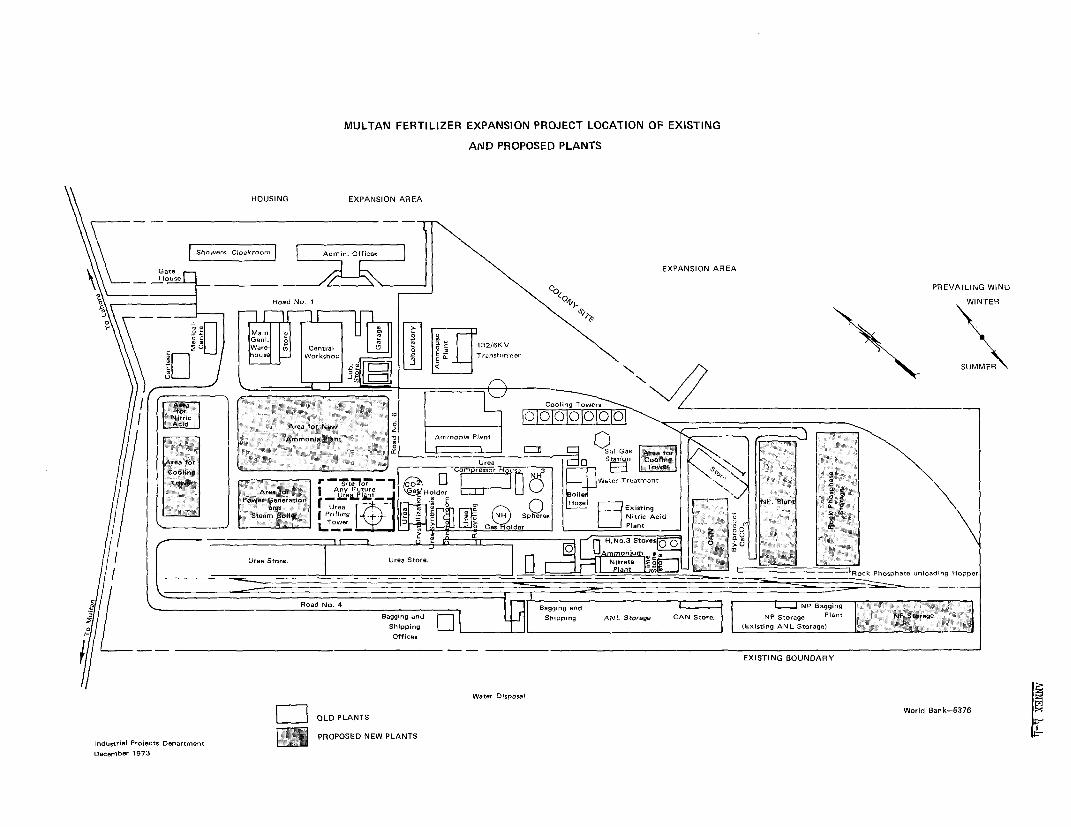

4.03 The project is detailed in Annex 4-1 and the flow chart for theexisting and new facilities is shown in Annex 4-2. Ammonia will be producedfrom steam-reformed natural gas in a single train, and latest proven tech-nology based on steam turbine-driven centrifugal compressors will be used.The,selected engineering firm for design and construction of the ammonia plantand offsites is Kellogg International Corporation Ltd. (U.K.) who will alsobe responsible for general coordination and supervision of the entire project.The selected engineering firm for design and construction of the nitric acid,NP and CAN plants is Uhde GmbH (FRG). The ammonia plant will use the Kelloggprocess, the nitric acid and CAN units will use Uhde technology and the NP plantwill be based on Dutch States Mines process design. The various productionprocesses are described in Annex 4-3. The new facilities will be built withinthe existing plant boundaries as shown in the layout in Annex 4-4.

B. Raw Materials and Utilities

4.04 The availability and supply of the principal raw materials are de-scribed in more detail in Annex 4-5; these will be natural gas to be suppliedby Sui Northern Gas Pipelines Ltd. (SNGPL) from their Sui field some 300 kmdistant and phosphate rock from Jordan or elsewhere. Gas reserves are amplebut existing needs of the Multan plant will have to be supplemented by con-structing additional loops. The Government has agreed to finance on terms

- 12 -

and conditions satisfactory to the Bank, the cost of the additional invest-ments required for the gas supply (amounting to 1.56 million cubic meters,or 55 million cubic feet per day at full production including 10% contingency).In addition, it is a condition of effectiveness of the Loan that Sui Northernshall have agreed to supply to PFL such amount of gas on a long-term basisas from June 30, 1976. Phosphate rock has been purchased by WPIDC from Jordanfor many years and this can be extended to meet the needs of Multan (about220,000 tpy). In view of rapidly increasing world demand for phosphate rock,it is a condition of effectiveness of the Loan that satisfactory arrangementsfor the supply of phosphate rock to PFL shall have been made.

4.05 Major utilities are power, natural gas for steam generation andwater. The plant will produce its own power via steam raised in waste-heatrecovery units and gas-fired boilers. Water for processing and coolingpurposes will come from nearby deep wells.

4.06 Adequate supplies of bags are essential and, in addition to poly-ethylene-lined cotton bags now used, alternatives such as woven polyprophylenebags are being studied as well as bag-recycling. The Government has agreedto make arrangements satisfactory to the Bank for the supply to PFL of thenecessary quantity of fertilizer bags for the operation of the Multan plantand to make available to the Bank for review by June 30, 1975 a program forthe production of such bags.

C. Basis for Location and Product Mix

4.07 As reviewed in Annex 3-2 Multan is in the heart of the major agri-cultural area of the Punjab and is therefore ideally located in terms ofmarketing and distribution as well as nearness to its major feedstock -natural gas. The existing plant is well connected by road and rail to therest of the Province and the country. It has ample room for expansion andhas its own housing colony, plus plentiful additional labor resources inMultan city. Management, supervisors and operators are well experienced inmost of the fertilizer technology applied in the project. Expanding Multanis therefore logical. The product mix suits the fertilizer applicationpattern for many crops, namely, a 1:1 N to P2 05 ratio for basal (seed bed)application as nitrophosphate, followed by a subsequent top dressing of anall nitrogen fertilizer such as CAN or urea.

D. Ecology and Safety Considerations

4.08 These are reviewed in detail in Annex 4-6. Appreciable volumes ofharmless water vapor and carbon dioxide will be vented to the atmosphere.Fluorine vapors resulting from impurities in phosphate rock will be recoveredbefore venting exhaust gases to the atmosphere, and rendered harmless byappropriate chemical treatment. Nitrogen oxide vapors from the old and new

- 13 -

nitric acid plants will be reduced to acceptable levels. Dusts will beminimized in the interests of economy as well as ecology, and it was agreedthat the entire plant will meet gaseous and liquid pollution levels nowrequired in populated areas of Europe or USA, to be monitored by the Govern-ment. Safety and fire precautions will also meet standards acceptable over-seas.

E. Labor Force and Training

4.09 About 1,700 people are currently employed in the Multan plant whichis more than double present actual needs. This labor surplus will be ampleto operate the additional process units and meet expanded handling, baggingand other requirements, thus helping to reduce present plant overstaffing.Key supervisory and technical personnel (who are already experienced inammonia, nitric acid and CAN production) will be given training in largeammonia, NP and CAN plants overseas, in accordance with a plan to be preparedby the Technical Advisor. Some PFL staff will spend time on design and pro-curement in the offices of the plant contractors (Kellogg and Uhde).

F. Project_Implementation, Procurement and Construction

4.10 As mentioned, Kellogg has been selected to design and constructthe ammonia plant, offsites and tie-ins of existing and new facilities andUhde to design and construct the nitric acid, NP and CAN units. Both werechosen after international competition. Procurement of equipment and mate-rials will be undertaken in London and DDrtmund by PFL together with Kelloggand Uhde specialists. The design and construction of civil works (which arebeing financed by the Government) will be performed by qualified domesticfirms under the supervision of Kellogg. Financing of Kellogg's services willbe assisted by the proposed Bank loan, while the nitric acid, NP and CANplants' engineering will be financed by ADB. With the exception of pro-prietary equipment (estimated to cost US$1 million equivalent) and criticalitems affecting the process guarantees and/or the project completion schedule(estimated to cost US$4 million equivalent), all orders over an estimatedUS$25,000 to be financed by the proposed Bank loan will be procured by inter-national competitive bidding under the Bank's guidelines. Suppliers forcritical items will be recommended by Kellogg based on their experience,delivery times and competitive prices. Qualified Pakistani bidders will begiven a preference of 15% or the customs duties for non-exempt importers,whichever is lower. To expedite the project and avoid retroactive financing,preliminary engineering costs and down payments on long delivery items willbe financed from equity. On this basis design work commenced in early 1974and the construction is to be completed by the end of 1976. The anticipatedschedule is depicted in Annex 4-7; this schedule is tight but achievable,provided equipment delivery times are not significantly prolonged on accountof the sharp increase in the construction of fertilizer plants in the world.

- 14 -

4.11 To coordinate the project and assist PFL during design, procurementand construction, a Technical Advisor team from Stamicarbon (Netherlands)with experience in large-scale production of ammonia and nitrogen fertilizerincluding nitrophosphate has been engaged. This team can be retained afterplant start-up for a period satisfactory to the Bank to help assure thatproduction can quickly reach and be sustained at a high level of capacity.Close liaison between the Technical Advisor and PFL's local consultants(Chemical Consultants Ltd.) will be maintained throughout.

4.12 To ensure that delays and extra costs will not arise due to im-port procedures, the Bank has obtained assurances that import licenses willbe issued promptly according to an agreed Critical Path Schedule. It wasalso stated by the representatives of the Government during negotiations thatwith certain minor exceptions, imported equipment, materials and other itemsneeded for the project will be free of import duties, as assumed in thecapital cost estimates.

4.13 Sui Northern Gas Pipelines Limited (SNGPL) will be responsible forconstruction of the expansion of the capacity of the Multan line, by June 30,1976, in time for testing the gas line and the fertilizer facilities. TheBank in its supervision of its loans to SNGPL is following the pipelineproject. As PFL's Managing Director designate is SNGPL's former TechnicalManager the necessary close coordination between PFL and SNGPL should beassured.

4.14 The Government representatives also agreed that a proposed heavywater plant to be based on PnL's ammonia plant facilities will not interferewith PFL's operations and that PFL will be compensated for any additionalcapital or opcrating costs as a consequence of the heavy water plant.

V. CAPITAL COST AND FINANCING PLAN

A. Project Cost

5.01 The project is estimated to require total financing amounting toPRs 1,007 million (US$101.7 million) with the local currency portion accountingfor about 23%. Ay July 1, 1976 the fixed assets of the existing plant will betransferred from NFC to PFL at PRs 46.7 million (US$4.7 million). The de-tails of capital cost estimate are given in Annex 5-1 and its summary isgiven in the table below:

- 15

Project Cost - Summary

PRs (millions) US$ Equivalent (millions)Local Foreign Local ForeignCurrency Exchange Total Currency Exchange Total %

Engineering, Erectionand Procurement 105 101 206 10.5 10.2 20.7 22

Equipment, Freightand Spares, C&F - 477 477 - 48.1 48.1 51

Local Goods and Services 17 - 17 1.7 - 1.7 2

Furniture, Fixtures andVehicles 2 - 2 0.2 - 0.2 -

Training, Start-up andConsultancy 11 12 23 1.1 1.2 2.3 2

Sub-total: 134 589 723 13.5 59.5 73.0 78

Contingencies:

-Physical 5 59 64 0.5 6.0 6.5 7-Price 5 48 53 0.5 4.8 5.3 6

Sub-Total 10 107 117 1.0 10.8 11.8 13

Total Fixed Assets 144 696 840 14.5 70.3 84.8 91

Working Capital 70 18 88 7.1 1.8 8.9 9

Total Project Cost 214 714 928 21.6 72.1 93.7 100

Interest During Construction 19 60 79 2.0 6.0 8.0

Total Financing Required 233 774 1,007 23.6 78.1 101.7

Purchase of Existing Assets 47 - 47 4.7 - 4.7

Total Capitalization 280 774 1,054 28.3 78.1 106.4

5.02 The foreign exchange estimates are based on fixed engineering fees,indicative equipment costs prepared by the winning engineering firms in February1974 and civil construction costs in Pakistan in March 1974. Foreseeable es-calation through March 1974 and contingencies of 10% are already included in

- 16 -

these costs, i.e., outside the contingencies separately shown. It has beenassumed that all equipment will be imported although a small percentage maybe fabricated in Pakistan at competitive costs.' Thus, there may be somesavings in foreign exchange compared to the above estimates.

5.03 A 10% contingency allowance has been made on the fixed engineer-ing bids and on the indicative equipment cost items. In addition, a 10%allowance for price escalation has been made on all equipment costs. Con-sidering the advanced stage of the project and assuming equipment ordersare placed over the next 9 months, the escalation provisions appear reason-able. They have been revised following negotiations in the light of worldwidedevelopments since the original estimates were prepared in mid-1973. Localcosts are based on new contracts being negotiated by construction firms.To this has lbeen added 7-1/2% for contingencies, and at this time, theseestimates appear reasonable. Although not part of the project's capitalcosts, the additional gas line loops are expected to cost PRs 107 million.

B. Working Capital

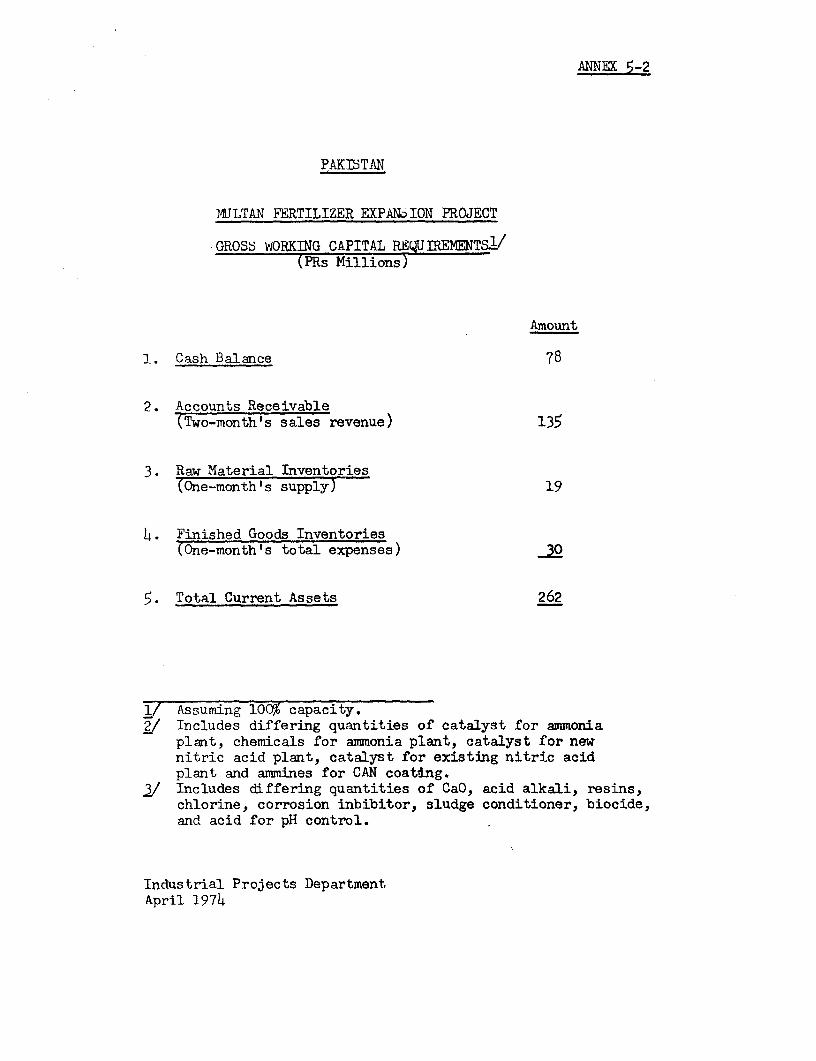

5.04 Using conservative assumptions (Annex 5-2) for the level of receiv-ables, inventories and cash, the Bank has estimated maximum current assetsduring the first operating year (1977) to be about PRa 200 million, of whichsome 70% could be financed by normal working capital credits. The balancewould be provided in equity. Thus, we have used PRs 88 million as a con-servative amount to be included in the financing requirements for the initialworking capital. Of this, PRs 18 million is assumed to be required in foreignexchange for imported raw materials, primarily phosphate rock.

C. Financing Plan

5.05 The proposed financing plan is based on a concept of about 64% debtand 36% equity. Of the equity, about 30% is to be provided by ADNOC. Thebalance of the equity is to come from the Government through NPC, in localcurrency and - to the extent necessary to meet the project's needs - inforeign exchange (about US$5 million equivalanet). The ADB signed theirUS$27 million equivalent loan in January 1974, and ADNOC paid its initialequity subscription also in January 1974. The Government has agreed tofinance any local currency or foreign exchange overrun on the project, assurethat PFL has a maximum debt/equity ratio of 65/35 at project completion date, 1/and cover all costs of the related gas pipeline within the time required bythe project. In addition assurances have been obtained that (i) the Govern-ment will provide sufficient funds to NFC to allow it to subscribe in cashfor its portion of PFL's share capital and in the time as required by theproject; and (ii) share capital can be used for foreign exchange expendituresby the conversion of rupees, as necessary.

1/ Project completion is defined as one continuous month of productionat 80% capacity.

- 17 -

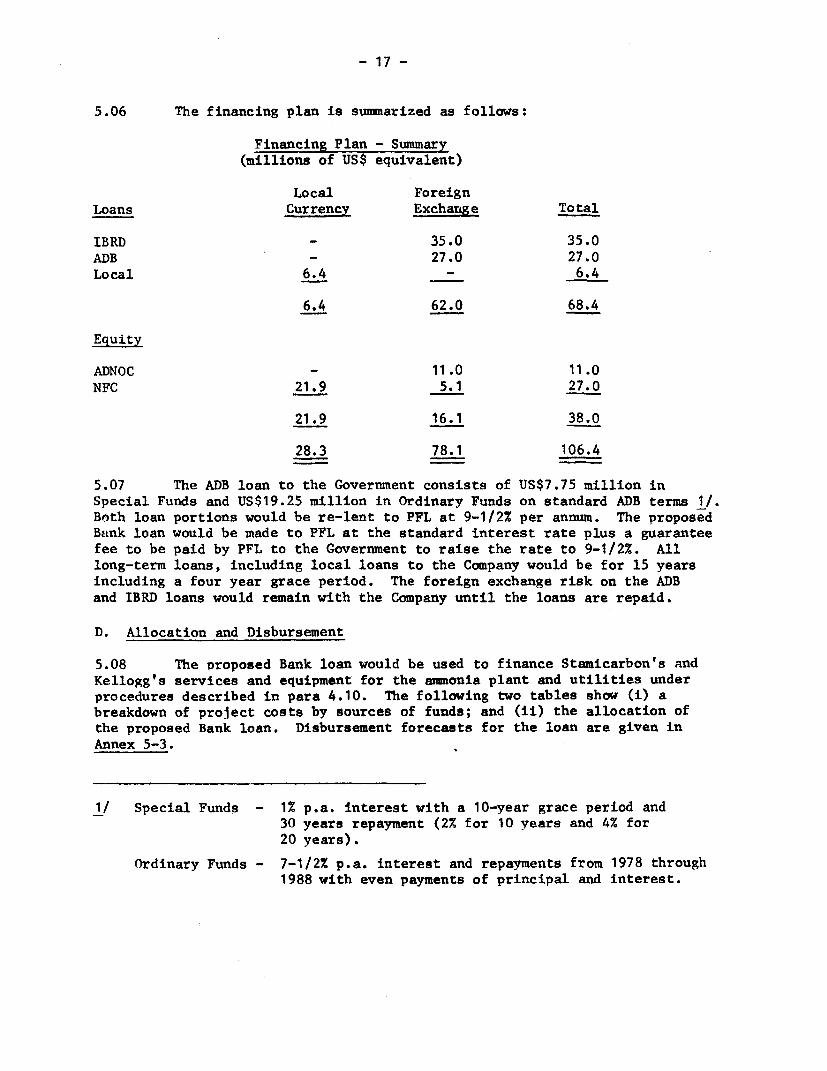

5.06 The financing plan is summarized as follows:

Financing Plan - Summary(millions of US$ equivalent)

Local ForeignLoans Currency Exchange Total

IBRD 35.0 35.0ADB - 27.0 27.0

Local 6.4 - 6.4

6.4 62.0 68.4

Equity

ADNOC - 11.0 11.0NFC 21.9 5.1 27.0

21.9 16.1 38.0

28.3 78.1 106.4

5.07 The ADB loan to the Government consists of US$7.75 million inSpecial Funds and US$19.25 million in Ordinary Funds on standard ADB terms 1/.

Both loan portions would be re-lent to PFL at 9-1/2X per annum. The proposed

Bank loan would be made to PFL at the standard interest rate plus a guarantee

fee to be paid by PFL to the Government to raise the rate to 9-1/2x. All

long-term loans, including local loans to the Company would be for 15 years

including a four year grace period. The foreign exchange risk on the ADB

and IBRD loans would remain with the Company until the loans are repaid.

D. Allocation and Disbursement

5.08 The proposed Bank loan would be used to finance Stamicarbon's and

Kellogg's services and equipment for the ammonia plant and utilities underprocedures described in para 4.10. The following two tables show (i) abreakdown of project costs by sources of funds; and (ii) the allocation ofthe proposed Bank loan. Disbursement forecasts for the loan are given in

Annex 5-3.

1/ Special Funds - 1Z p.a. interest with a 10-year grace period and30 years repayment (2% for 10 years and 4% for

20 years).

Ordinary Funds - 7-1/2% p.a. interest and repayments from 1978 through1988 with even payments of principal and interest.

- 18 -

Project Costs by Sources of Funds(PRs million)

Local Foreign Exchange -- GrandCurrency ADB IBRD Equity Total Total

Equipment and Services - 226 292 59 Ll 577 577Civil Works &

Local Erection 104 - - - - 104Training, Consultancy,Start Up andMiscellaneous 30 - 7 5 12 42

Contingencies 10 41 48 18 107 117Working Capital 70 - - 18 18 88Interest duringConstruction 19 - - 60 60 79

Purchase of ExistingAssets 47 - 47

Total 280 267 347 160 774 1,054

/1 Downpayment and initial engineering fees until ADB and IBRD loans areavailable, plus financing for part of utilities.

Allocation of Bank Loan

(million of US$ Equivalent)

IBRD

Engineering & Erection 2.0

Equipment & Spare PartsAmmonia Plant 20.0Utilities 7.5

Sub-total 27.5

Technical Advisory Services 0.7

Unallocated 4.8

Total 35.0

- 19 -

VI. FINANCIAL ANALYSIS OF THE PROJECT

A. Basis of Analysis

6.01 As mentioned, the project will produce ammonia for the existingnitric acid, urea and ANL plants as well as the new nitric acid, 11? and CANplants. In calculating the economic and financial returns, the entireproduction from the old and new plants are taken as benefits and the existingfacilities are taken at their depreciated value as of June 30, 1976.

6.02 Project expenditures by source are estimated as follows:

Multan - Project Expenditures by Source(PRa million)

Calendar Year 1973 1974 1975 1976 Total

Foreign Loans

IBRD - 25 252 70 347ADB - 52 200 15 267

= 77 452 85 614

Foreign Equity (ADNOC) - 46 61 3 110

Local Equity (NFC)and Loans 15 25 66 224 330

Total 15 148 579 312 1 054

Some of the guarantee payments on equipment will only be made in 1977 butthese are relatively small and have therefore no substantial effect on thefinancial and economic analyses.

B. Operating Costs and Revenues

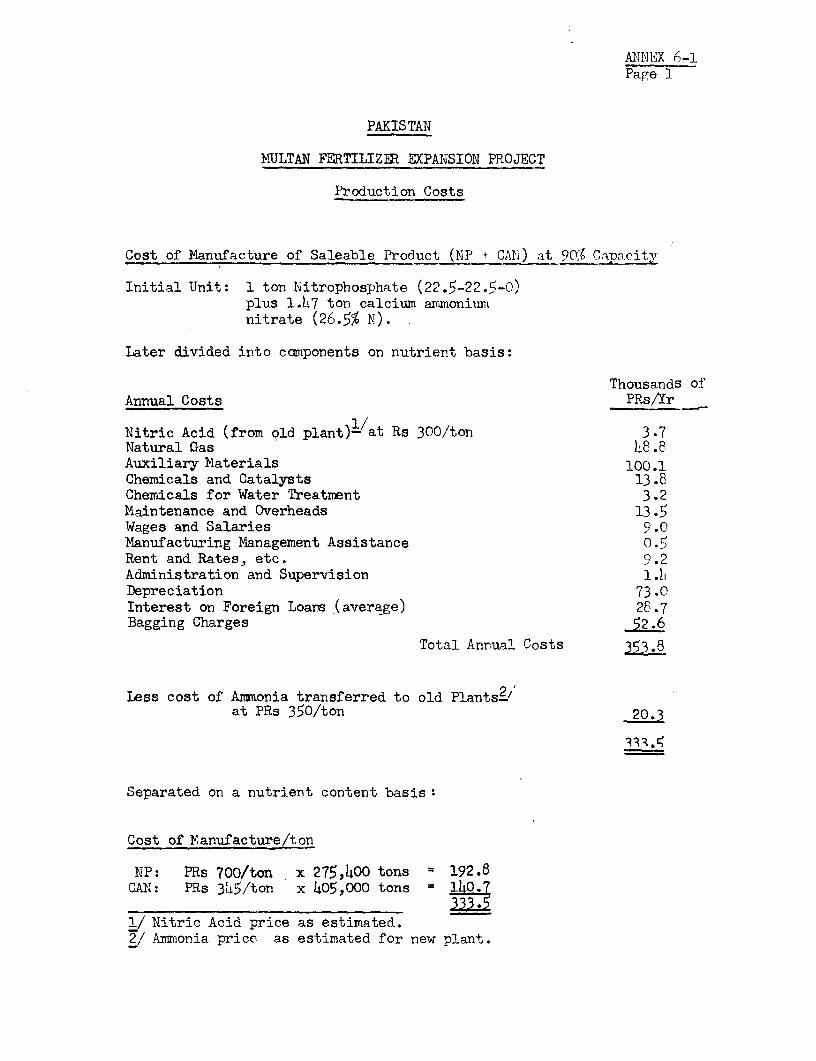

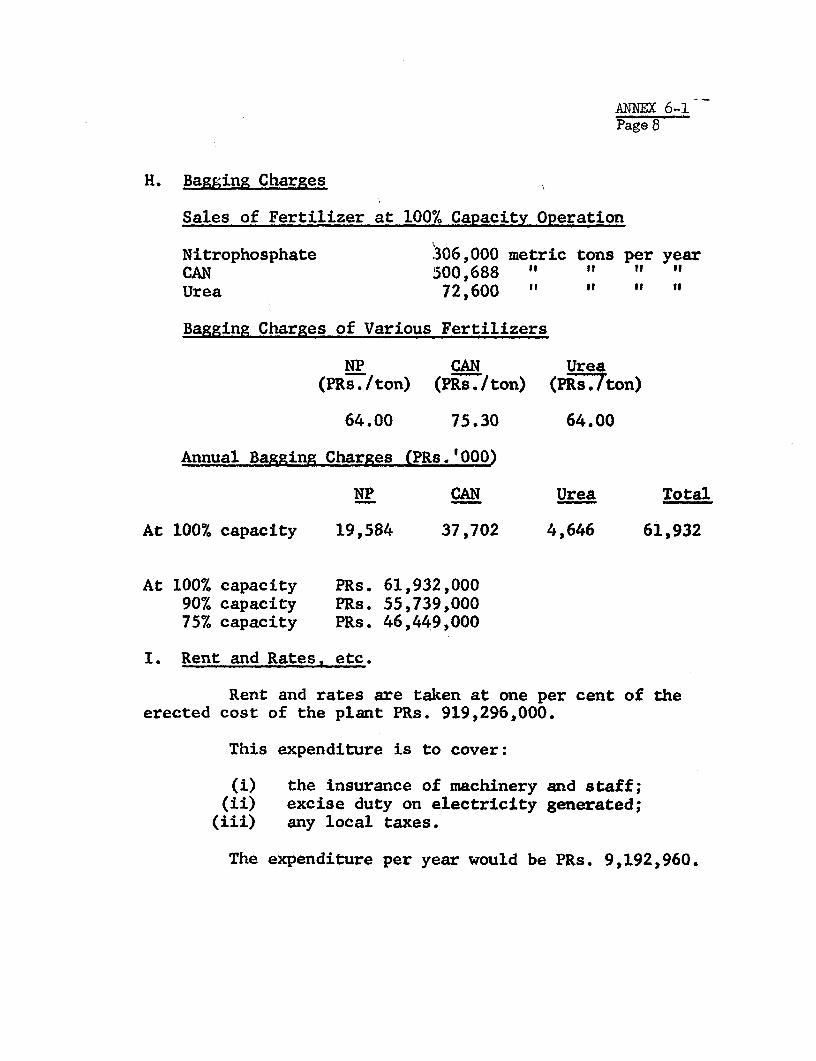

6.03 Detailed operating costs for each of the major products of theexpanded plant are shown in Annex 6-1 and are summarized below:

- 20 -

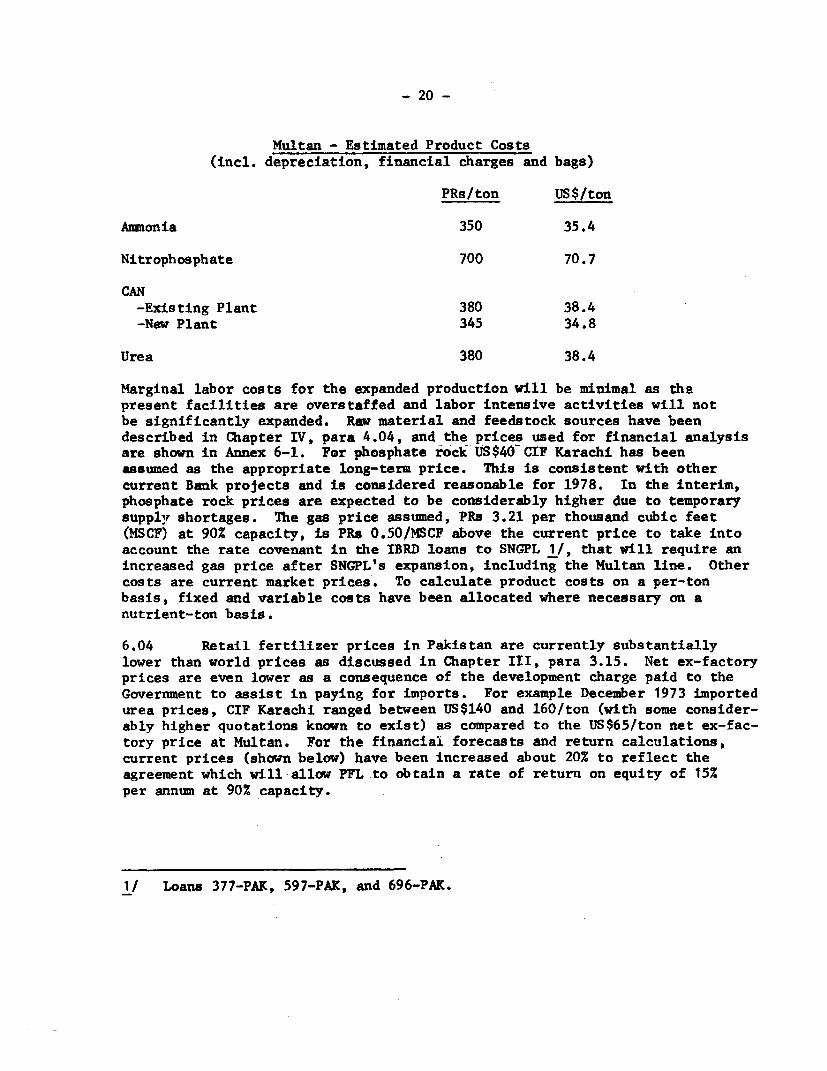

Multan - Estimated Product Costs(incl. depreciation, financial charges and bags)

PRs/ton US$/ton

Ammonia 350 35.4

Nitrophosphate 700 70.7

CAN-Existing Plant 380 38.4-New Plant 345 34.8

Urea 380 38.4

Marginal labor costs for the expanded production will be minimal as thepresent facilities are overstaffed and labor intensive activities will notbe significantly expanded. Raw material and feedstock sources have beendescribed in Chapter IV, para 4.04, and the prices used for financial analysisare shown in Annex 6-1. For phosphate rock US$40--CIF Karachi has beenassumed as the appropriate long-term price. This is consistent with othercurrent Bank projects and is considered reasonable for 1978. In the interim,phosphate rock prices are expected to be considerably higher due to temporarysupply shortages. The gas price assumed, PRa 3.21 per thousand cubic feet(MSCF) at 90% capacity, is PRs 0.50/MSCP above the current price to take intoaccount the rate covenant in the IBRD loans to SNGPL 1/, that will require anincreased gas price after SNGPL's expansion, including the Multan line. Othercosts are current market prices. To calculate product costs on a per-tonbasis, fixed and variable costs have been allocated where necessary on anutrient-ton basis.

6.04 Retail fertilizer prices in Pakistan are currently substantiallylower than world prices as discussed in Chapter III, para 3.15. Net ex-factoryprices are even lower as a consequence of the development charge paid to theGovernment to assist in paying for imports. For example December 1973 importedurea prices, CIF Karachi ranged between US$140 and 160/ton (with some consider-ably higher quotations known to exist) as compared to the US$65/ton net ex-fac-tory price at Multan. For the financial forecasts and return calculations,current prices (shown below) have been increased about 20% to reflect theagreement which will allow PFL to obtain a rate of return on equity of 15%per annum at 90% capacity.

1/ Loans 377-PAK, 597-PAK, and 696-PAK.

- 21 -

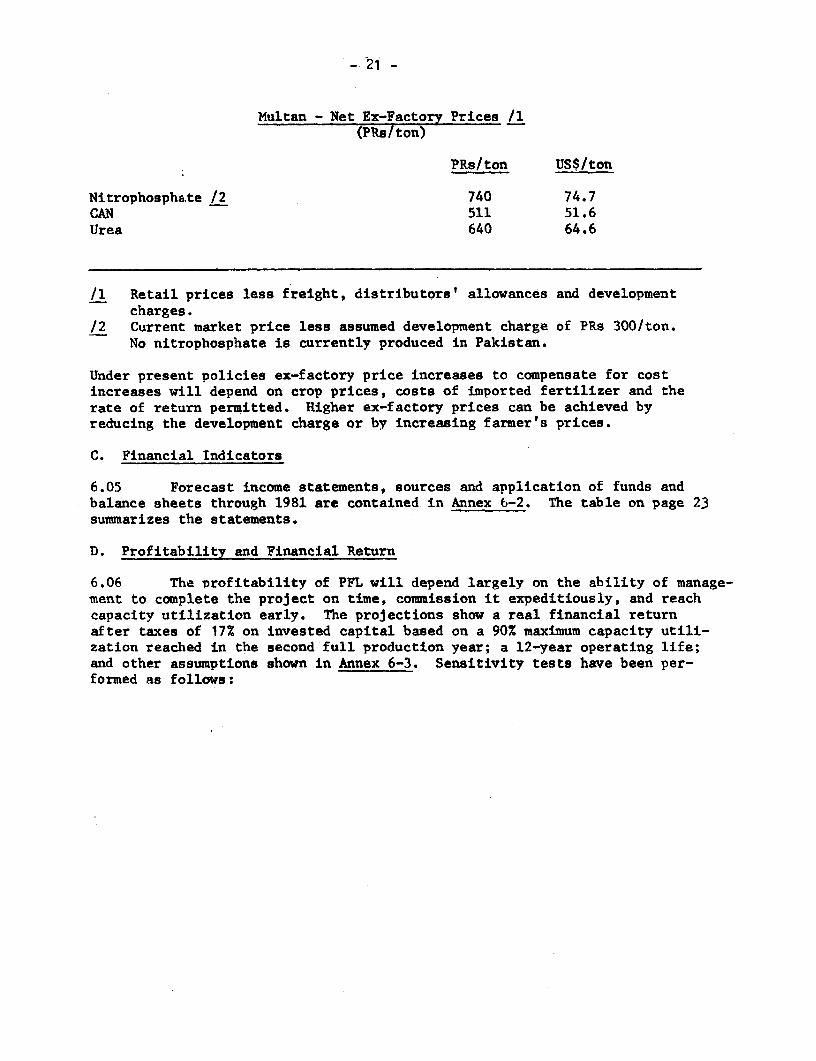

Multan - Net Ex-Factory Prices /1(PRa/ton)

PRs/ton US$/ton

Nitrophosphate /2 740 74.7CAN 511 51.6Urea 640 64.6

/1 Retail prices less freight, distributors' allowances and developmentcharges.

/2 Current market price less assumed development charge of PRs 300/ton.No nitrophosphate is currently produced in Pakistan.

Under present policies ex-factory price increases to compensate for costincreases will depend on crop prices, costs of imported fertilizer and therate of return permitted. Higher ex-factory prices can be achieved byreducing the development charge or by increasing farmer's prices.

C. Financial Indicators

6.05 Forecast income statements, sources and application of funds andbalance sheets through 1981 are contained in Annex 6-2. The table on page 23summarizes the statements.

D. Profitability and Financial Return

6.06 The profitability of PFL will depend largely on the ability of manage-ment to complete the project on time, commission it expeditiously, and reachcapacity utilization early. The projections show a real financial returnafter taxes of 17% on invested capital based on a 90% maximum capacity utili-zation reached in the second full production year; a 12-year operating life;and other assumptions shown in Annex 6-3. Sensitivity tests have been per-formed as follows:

- 2 2-

Financial Return and Sensitivity Tests

-Base Case - After Taxes 17Before Taxes 23

-2C% Increase in Project Cost and12 months delay in construction 13

-20% Decrease in Revenues 6

-Gas Costs Increased 100% 13

-Phosphate Rock Costs Increased 20% 16

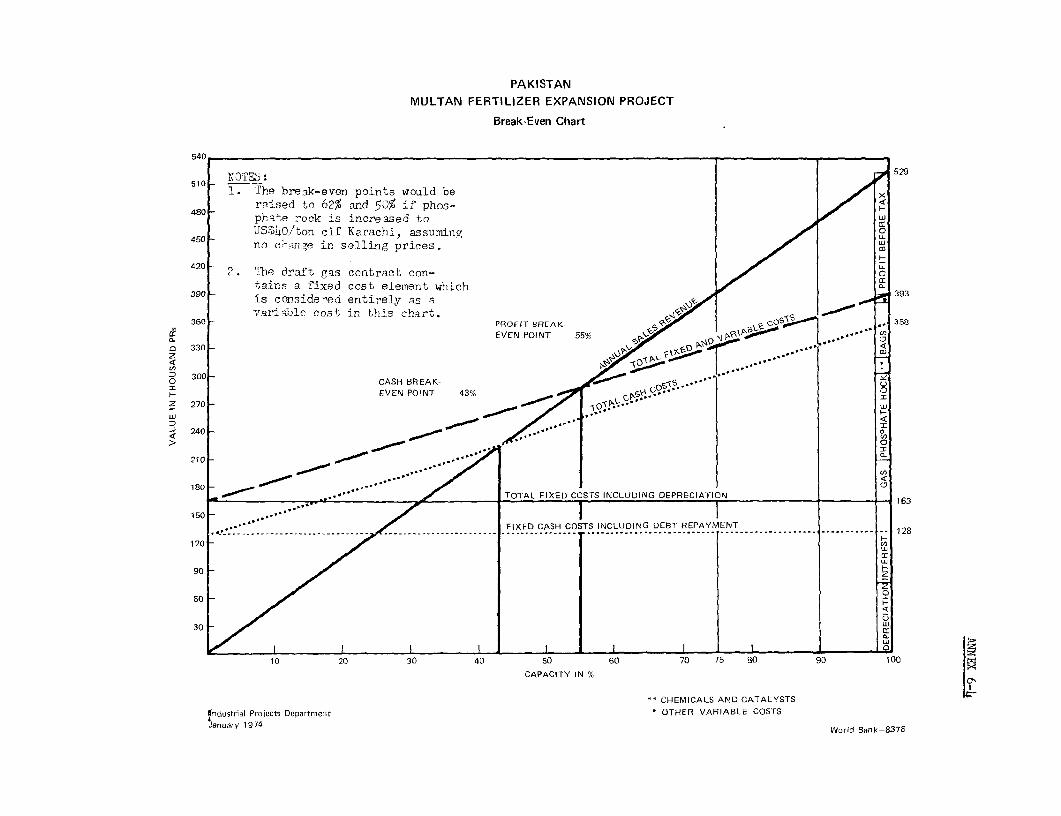

From an equity point of view, the discounted return would be over 25%. Atcurrent sales prices the profit breakeven point is estimated to be 62% andthe cash breakeven point 50% (Annex 6-4). The above returns reflect therelatively low additional investment requirements on account of the largelyexisting infrastructure and the favorable feedstock price, measured by today'sworld standards of traded hydrocarbon resources.

E. Financial Position, Debt Service Coverage and Financial Covenants

6.07 With 15% dividend payments assumed to start in 1979, projectionsshow a current ratio of 1.4:1 or better for all years and a long-term debt/equity ratio of less than 60/40 after 1977. These ratios are sound and con-sidered achievable. Debt service would be covered 1.8 times from 1978 on-ward, the first year full loan repayment is due.

6.08 To ensure the financial viability of PFL, the following agreementshave been obtained: (a) the Government will take all necessary action tomaintain a current ratio of at least 1.5:1 as at Project Completion Date andthereafter of 1.2:1 and to assure that as at Project Completion Date the debtequity ratio of PFL shall be no more than 65:35; (b) further long-term bor-rowing and investments in fixed assets without prior approval of the Bank belimited to no more than US$3 million equivalent per year: (c) for purposes ofincurring debt the debt service coverage to be maintained at not less than1.5 times; and (d) limitation of dividends or other cash outlays, includingdebt pre-payments, to prior earnings and subject to the maintenance of a cur-rent ratio of not less than 1.5:1 after declaration or repayment. In addition,PFL will implement a satisfactory cost control, accounting and management infor-mation system, which, inter alia, will provide information suitable for support-ing requests to the Government for fertilizer price increases to offset highercosts as they arise.

- 23 -

SUMMARY FORECAST FINANCIAL STATEMENTS(PRs Millions)

Year Ending December 31 1976 1977 1978 1979 1980 1981Capacity Production Start-up 75% 290 20% 90% 90%

Income StatementRevenue_/ - 468 562 575 585 590Cost of Sales - 291 328 328 328 328Other Charges2/ - 73 71 66 60 55Gross Profit before T;xes - 104 165 191 197 207Taxes and Workers' Participation

Fund 64 103 119 123 130Net Profit - 40 62 72 74 77Net Profit as % of:Sales - 9 11 12 13 13Share C pital - 11 16 19 20 20Equity3. - 11 15 15 15 15

Sources & Application of FundsCash Generation & Interest - 180 204 200 207 205Debt Service Requirement - 67 112 109 110 107Debt Service Coverage - 2.7 1.8 1.8 1.9 1.9Dividend Payment - 15% - - - 56 56 56

Balance SheetCurrent Assets 87 236 236 236 236 236Current Liabilities 20 157 171 145 148 150Working Capital 67 79 65 91 88 86Current Ratio 4.3 1.5 1.4 1.6 1.6 1.6Net Fixed Assets 967 894 821 748 673 602Long-Term Debt (LTD) 658 615 570 522 470 415Share C3pital 376 376 376 376 376 376Equity4/ 376 416 478 494 512 533Total LTD and Equity 1,034 1,031 1,048 1,016 982 948

LTD/Equity Ratio 64:36 60:40 54:46 52:48 48:52 44:56

1/ Gross revenue less freight, distributbr's allowance and development charge.2/ Interest and management assistance.i/ Beginning of year.j/ Assuming 15% dividend beginning in 1979.

- 24 -

F. Major Risks

6.09 The major potential financial risks foreseen are: delays in com-pleting the project due to a world wide increase in plant construction andequipment demand; difficulties in reaching adequate capacity utilization; costescalations due to the boom in the fertilizer equipment maiufacturing industry,inflation and further currency realignments; delays in the delivery of gas;untested management arrangements; introduction of a relatively new product;distribution uncertainties; and a potential shortage of bags. These riskshave been reduced to acceptable levels by the use of proven processes andexperienced contractors, detailed cost estimates with appropriate contin-gencies; Bank supervision of the gas transmission company; use of a technicaladvisor and competent local consultants and studies of the distributionsystem and alternative bagging materials and a promotion program during con-struction based on imported nitrophosphate.

VII. ECONOMIC ANALYSIS

A. International Fertilizer Prices

7.01 In view of shortages of fertilizer, increased investment costs,high freight rates, rising prices for raw materials and the general effectof currency realignments, fertilizer prices have reached historic highs. 1/However, it is estimated by the Bank that lhrge new plants, with naturalgas such as in the Persian Gulf, will be able to sell their production onthe world market and earn an attractive return, in 1978 at US$110/ton forurea and US$150/ton for DAP (bulk FOB Persian Gulf) the two main sourcesof N and P in international trade. Exporting countries, which do not havethe advantages of low-cost feedstocks might set prices US$10-20 higher.Historic low3 for urea were about US$55 in the mid-1960's and prices are overUS$200 today. Whether countries with surplbses will actually sell at theindicated prices in the late 1970's and early 1980's will depend on marketforces. Supply is not expected to catch up with demand for at least three orfour years.

1/ In the last half of the 1960's, investments in new plants by traditionaland new producers, especially petroleum companies, as well as improvedtechnology led to large stocks, despite rising consumption in developedand developing countries (respectively 15X and 8X annually). As pricesand profits declined, the oil companies rapidly lost interest and plantswere closed down or contracted out; others were delayed and failed toreach expected capacities. With the market growing rapidly, the inven-tories disappeared and today's tight stapply situation resulted.

- 25 -

B. Economic Rate of Return

7.02 To calculate a realistic economic rate of return under currentuncertainties is difficult. Using US$130/ton for urea and US$170/ton 1/forDAP, both CIF Karachi in bulk form, plus US$15/ton for bags and freightfrom Karachi to warehouses in the Punjab would give ex-factory prices ofUS$145/ton for urea, Us$140 for NP and US$88 for CAN; these prices havebeen used for the economic return calculation of this project.

7.03 The cost of gas for the economic return has been taken at US$1.40per 1,000 cubic feet equivalent to US$54/ton or US$8 per barrel for fuel oil.This is necessarily an arbitrary assumption based on the Bank's review of theopportunity cost of gas for gas based fertilizer projects (Annex 7-1 page 3).Market prices, as in the financial return have been used for other rawmaterials. It was established that the gas to be used did not have a near-term alternative domestic use such as replacing oil imports 2/ and thatexporting gas (which is not contemplated) would require transportation andtransformation costs which would partially offset increased prices if exportsof liquified gas were used for the opportunity cost of gas.

7.04 Using the above assumptions and fund flows as detailed in Annex 7-1the project shows an economic return of 34% at 90% capacity utilization onthe basis of a 12-year operating life. The economic return is twice thefinancial return due to the elimination of high income taxes (60.5%) and theuse of forecast international fertilizer pr4ees which are more than twicethe current ex-factory prices in Pakistan. The economic return is sensitiveto selling prices, and gas and phosphate rock costs. However, the assumedprices have been calculated on a basis consistent with assumed costs andtherefore if input costs are raised, it is likely that international priceswill remain at levels which would provide good returns to the least costproducers. Sensitivity tests have been performed assuming a 12-month delayin start-up, maximum production of 80% and a 10% overrun on capital costs.Under the most adverse foreseeable combination of factors, the economicreturn is not expected to fall below 20%.

C. Foreign Exchange Savings

7.05 The estimated annual net foreign exchange savings attributable tothe project at 90% capacity is US$50 million and the foreign exchange invest-ment of about US$78 million can be recovered in less than two years (Annex 7-2).

1/ This is consistent with a price of US$40/ton CIF for rock phosphate usedas an economic cost.

2/ As indicated in Annex 4-5 latest estimates of Sui reserves are 8.9 trillioncubic feet out of which 4.9 trillion are committed. The project willdemand only about 4.3% of the uncommitted reserves over a 12-year operatinglife.

- 26 -

D. Other Economic Benefits

7.06 The unmeasured economic benefits of management and technical train-ing, and assured supplies of fertilizer, make this project particularly at-tractive. It is of high priority in the context of the Government's policyto attain self-sufficiency in food and to increase agricultural output andexports, and it puts to profitable use a valuable national asset, natural gas,which is presently under-utilized.

VIII. AGREEMENTS REACHED WITH THE GUARANTOR,NATIONAL FERTILIZER CORPORATION AND THE BORROWER

8.01 Agreements have been reached on the following major points:

The Guarantor (Pakistan)

(1) To provide funds to NFC for its equity subscriptionto PFL, to provide PFL further funds as needed to meet theMarch 1974 budget estimates and to charge a fee for itsguarantee on the Bank loan to raise the interest rate to9-1/2% per annum (paras 5.05-5.07).

(2) To provide additional funds as necessary in foreign exchangeand local currency to complete the project on terms and con-ditions satisfactory to the Bank (para 5.05).

(3) To assure that PFL will have a current ratio of at least1.5:1 at project completion date and of 1.2:1 thereafter andthat PFL will have a debt equity ratio as at project completiondate of not more than 65:35 (paras 5.05 and 6.08).

(4) To promptly issue import licenses as required by an agreedcrltical path schedule (para 4.12).

(5) To enable PFL to utilize an efficient and competitive dis-tribution network (para 3.12).

(6) To assure that prices will not be set at levels which wouldprevent PFL's shareholders from being able to achieve areasonable return on their investment (para 3.16).

(7) To use its best endeavors to import finished phosphate fertilizerfor promotional purposes through the construction period (para 3.09).

(8) To finance the expansion of the gas line capacity necessary forthe project (para 5.03 and 5.05).

- 27 -

(9) To make available for review by the Bank studies and programsto be prepared by December 31, 1974 and implemented by the Gov-erment relating to the provision of agricultural credit andthe improvement of fertilizer marketing and distribution(para 3.08 and 3.09).

(10) To assure the supply of the necessary quantity of fertilizerbags and to make available by June 30, 1975 for the Bank'sreview, a program for the production of such bags (para. 4.06).

(11) To ensure that the construction and operation of the heavywater unit will not interfere with the operations of PFLand to compensate PFL against any additional capital oroperating costs resulting therefrom (para 4.14).

National Fertilizer Corporation (;FC)

(1) To guarantee the Loan (para 2.01).

(2) To transfer its existing Multan fertilizer business toPFL by not later than June 30, 1976, and, in the meantime,to vest the management of the existing Multan plant in PFL(para 2.08).

(3) To limit its capital expenditures relating to the Multanfertilizer business prior to the transfer thereof to US$1million equivalent per year (para 2.01).

The Borrower (PFL)

(1) To employ a Managing Director and a General Manager (Project)with powers and responsibilities agreed by the Bank (para 2.05).

(2) To contract with a technical advisor and local engineeringconsultants acceptable to the Bank on terms and conditionssatisfactory to it (para 4.11).

(3) To observe the financial covenants regarding return on equity,debt and dividend limitations, current ratios and further capi-tal expenditures (para 3.16 and 6.08).

(4) To establish an adequate accounting, cost control and managementinformation system with the assistance of experienced consultants(para 6.08).

(5) To install and utilize pollution controls at Multan to meetenvironmental protection standards agreed with the Bank. Theoperation of these controls will be monitored by the Govern-ment (para 4.08).

- 2g --

8.02 In addition the making of satisfactory arrangements for the supplyof phosphate rock and natural gas for the project is a condition of effec-tiveness of the Loan (para 4.04).

8.03 Based on the above agreements, the project is suitable for a Bankloan of US$35 million equivalent for 15 years including a 4 year grace period.

Industrial Projects DepartmentApril 3, 1974

ANNEX 1-1

PAKIST _ Page 1

MULTAN FERTILIZER EXPANSION PROJECT

GLOSSARY OF TECHNICAL TERMS

1. Following is a description of the technical terms used in thisreport: