Rep and Warranty Breaches in M&A Transactions and Warranty Breaches in M&A Transactions: Common...

24

Rep and Warranty Breaches in M&A Transactions: Common Claims and Navigating the Road to Recovery February 10, 2015 Presenters: Michael T. Wolf, Aon plc John Tuhey, ITW Craig C. Martin, Jenner & Block LLP Jason D. Osborn, Jenner & Block LLP

Transcript of Rep and Warranty Breaches in M&A Transactions and Warranty Breaches in M&A Transactions: Common...

Rep and Warranty Breaches in M&A

Transactions:

Common Claims and Navigating the Road to Recovery

February 10, 2015

Presenters:

Michael T. Wolf, Aon plc

John Tuhey, ITW

Craig C. Martin, Jenner & Block LLP

Jason D. Osborn, Jenner & Block LLP

2

The material contained herein is the work product of Jenner & Block LLP and should not be

construed to represent the opinions of the panel members or their individual employers.

Nothing contained in this packet is to be considered as rendering legal advice for specific

contracts or cases and readers are responsible for obtaining such advice from their own legal

counsel. This packet is intended for educational and informational purposes only.

© 2015 Jenner & Block LLP. All rights reserved.

3

Overview

• Tension between Getting the Deal Done and Positioning for Post-Closing Litigation

• Using Representations and Warranties to Allocate Risk

• Trouble Spots: Which representations lead to claims?

• Structural Impediments to Recovery

• Contractual Impediments to Recovery

• Common Law Impediments to Recovery

• Trends in R&W Insurance Payouts

4

Tension: Perfect Timing v. Perfect Documents

• Goal: Get the deal done within the valuation requirements and risk profile of the

participants

• Mandate: Get the Deal Done!

– Timing drivers:

• Competitive Auctions (particularly when comments are due in advance of a bid)

• Execution Risk

• Favorable Announcement Timing

• Need to realize on synergies quickly

• Risk Management

– Probability/Materiality Weighting: How likely is this to become an issue? How

material would it be if it did become an issue in terms of dollars spent and time to

resolve?

– Tail Risk: Even if unlikely, would the results be catastrophic (e.g., material

environmental liability, underfunded pension or multiemployer plan liability, litigation

with a key customer or sole supplier)?

5

Setting the Stage: Allocating Risk with

Representations and Warranties

• For purposes of our discussion today, we are assuming a transaction between

sophisticated parties involving the sale of a private company

• Although representations and warranties are also used to elicit disclosure,

allocate transaction execution risk between signing and closing and establish

conditions for closing, we are focused on allocation of risk for losses arising

post-closing

• We’ll assume that the breach doesn’t constitute or involve fraud

6

Trouble Spots: Which Reps are likely to be

the subject of a Claim?• How often are claims made?

– According to J.P. Morgan 2014 M&A Escrow Study, 23% of all deals with an

indemnification escrow had at least 1 claim (although this includes specific

indemnity claims)

– AIG Warranties and Indemnities Insurance Claims Review 2000-2013

identifies claims for breaches of reps & warranties in 28% of all deals in

North America

– Shareholder Representative Services 2013 SRS M&A Post-Closing Claims

Study found non-purchase price adjustment claims (including reps and

warranties, but also including fraud and specific indemnities) in 44% of deals

• According to J.P. Morgan and SRS, the closer the escrow is to expiring, the

more likely a claim is to be received

7

Trouble Spots: Claims Made by Rep

28%

19%16%

14%

23%

J.P Morgan Study

Taxes

Litigation

FinancialStatementsEmployment

Other

26%

14%

11%12%

37%

SRS Study

Taxes

UndisclosedLiabilitiesFinancialStatementsIP

Other

14%

17%

18%

10%

41%

AIG Study

Taxes

Litigation &ComplianceFinancialStatementsUndisclosedLiabilitiesOther

8

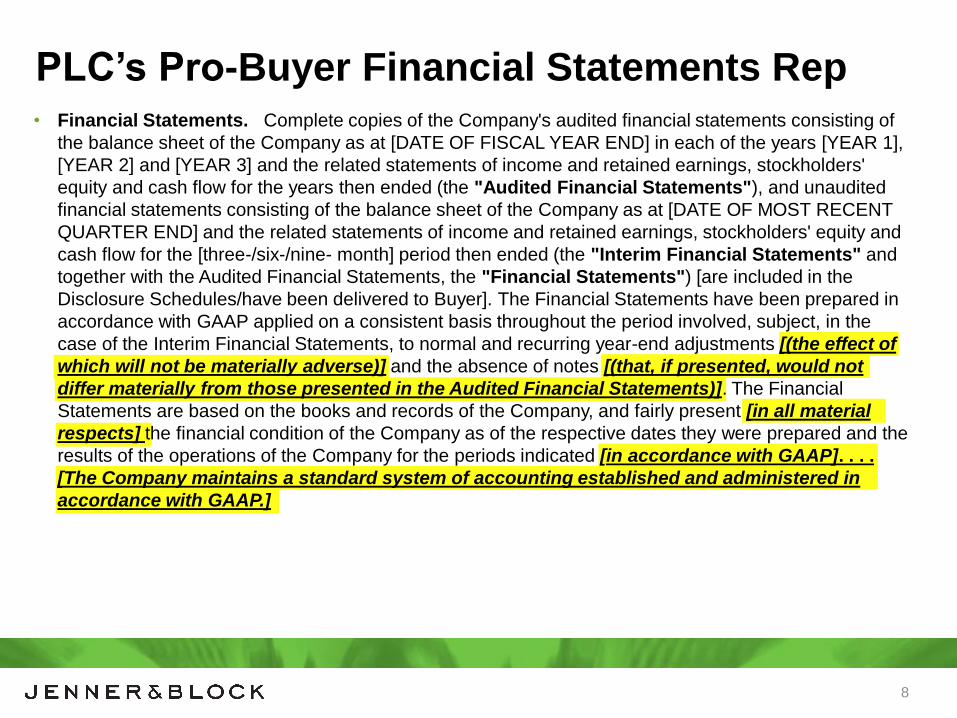

• Financial Statements. Complete copies of the Company's audited financial statements consisting of

the balance sheet of the Company as at [DATE OF FISCAL YEAR END] in each of the years [YEAR 1],

[YEAR 2] and [YEAR 3] and the related statements of income and retained earnings, stockholders'

equity and cash flow for the years then ended (the "Audited Financial Statements"), and unaudited

financial statements consisting of the balance sheet of the Company as at [DATE OF MOST RECENT

QUARTER END] and the related statements of income and retained earnings, stockholders' equity and

cash flow for the [three-/six-/nine- month] period then ended (the "Interim Financial Statements" and

together with the Audited Financial Statements, the "Financial Statements") [are included in the

Disclosure Schedules/have been delivered to Buyer]. The Financial Statements have been prepared in

accordance with GAAP applied on a consistent basis throughout the period involved, subject, in the

case of the Interim Financial Statements, to normal and recurring year-end adjustments [(the effect of

which will not be materially adverse)] and the absence of notes [(that, if presented, would not

differ materially from those presented in the Audited Financial Statements)]. The Financial

Statements are based on the books and records of the Company, and fairly present [in all material

respects] the financial condition of the Company as of the respective dates they were prepared and the

results of the operations of the Company for the periods indicated [in accordance with GAAP]. . . .

[The Company maintains a standard system of accounting established and administered in

accordance with GAAP.]

PLC’s Pro-Buyer Financial Statements Rep

9

PLC’s Pro-Buyer Undisclosed Liabilities Rep

• Undisclosed Liabilities. The Company has no liabilities, obligations or

commitments of any nature whatsoever, asserted or unasserted, known or

unknown, absolute or contingent, accrued or unaccrued, matured or unmatured

or otherwise ("Liabilities"), except (a) those which are adequately reflected or

reserved against in the Balance Sheet as of the Balance Sheet Date, and (b)

those which have been incurred in the ordinary course of business consistent

with past practice since the Balance Sheet Date and which are not, individually

or in the aggregate, material in amount.

• Sellers’ attempt to limit “Liabilities” by:

– Defining “Liabilities” to those required to be disclosed on a balance sheet prepared in accordance

with GAAP

• What about notes to the financial statements?

– Using a knowledge qualifier

– Using a dollar threshold to limit risk – basically a “super” deductible

– Excluding liabilities addressed by other representations and warranties

10

PLC’s Pro-Buyer Legal Proceedings Rep

• Legal Proceedings. Except as set forth in Section [X] of the Disclosure Schedules, there

are no Actions pending or, to Seller's Knowledge, threatened (a) against or by the

Company affecting any of its properties or assets (or by or against Seller or any Affiliate

thereof and relating to the Company); or (b) against or by the Company, Seller or any

Affiliate of Seller that challenges or seeks to prevent, enjoin or otherwise delay the

transactions contemplated by this Agreement. [No event has occurred or

circumstances exist that may give rise to, or serve as a basis for, any such Action.]

• "Action" means any claim, action, cause of action, demand, lawsuit, arbitration,

[inquiry, audit,] notice of violation, proceeding, litigation, citation, summons, subpoena

or [investigation] of any nature, civil, criminal, administrative, regulatory or otherwise,

whether at law or in equity.

• "Knowledge of Seller or Seller's Knowledge" or any other similar knowledge

qualification, means the actual [or constructive] knowledge of any director or officer of

Seller or the Company[, after due inquiry].

11

Case Study: Winshall v. Viacom Int’l

• Merger Agreement between Viacom International, Inc. and Harmonix Music Systems, Inc.

• Harmonix’s IP infringement R&Ws:

– No activity, business operation, or Current Game of Harmonix violates 3rd party IP

– Harmonix has adequate rights in software used in Current Games or games in development to permit the

company’s current use of such software

• Indemnity provision allowed Viacom to recover for breaches of representations &

warranties from two sources of funds:

– Portion of purchase price (~7%) held in escrow for 18 months after closing

– Upon exhaustion of escrow funds, deductions against earn-out payments that would otherwise be owed to

Harmonix’s selling shareholders based on two years of post-closing financial performance

• After closing, four IP infringement claims were asserted against Harmonix in relation to its

successful Rock Band video game franchise

• Viacom sought indemnification from escrow

12

Case Study: Winshall v. Viacom Int’l

• Delaware’s Chancery Court and Supreme Court agreed that Viacom was not entitled to

indemnification for costs of defending & settling the 3rd party IP claims

• Timing is everything: the IP reps were not breached

– IP reps & warranties were written in the present tense; covered infringement existing at the time of closing

– The alleged infringement related to the public release of the Rock Band game, but the “current use” of the IP in

question at the time of closing was merely for internal development & testing

– Court stated that it would not make sense for selling shareholders to indemnify the buyer for actions occurring

long after control over the business changed hands

• No Breach of R&W No Indemnity

– One word makes all the difference: the indemnity covered actual breaches of the reps & warranties—not costs

related to any and all alleged breaches

– Case might have come out differently if the indemnity provision required the sellers to “indemnify, defend, and

hold harmless…,” as many M&A transaction agreements do

• Court ordered release of escrow funds to the selling shareholders

• Winshall v. Viacom Int’l, Inc., C.A. No. 39, 2013 (Del. Oct 7, 2013)

13

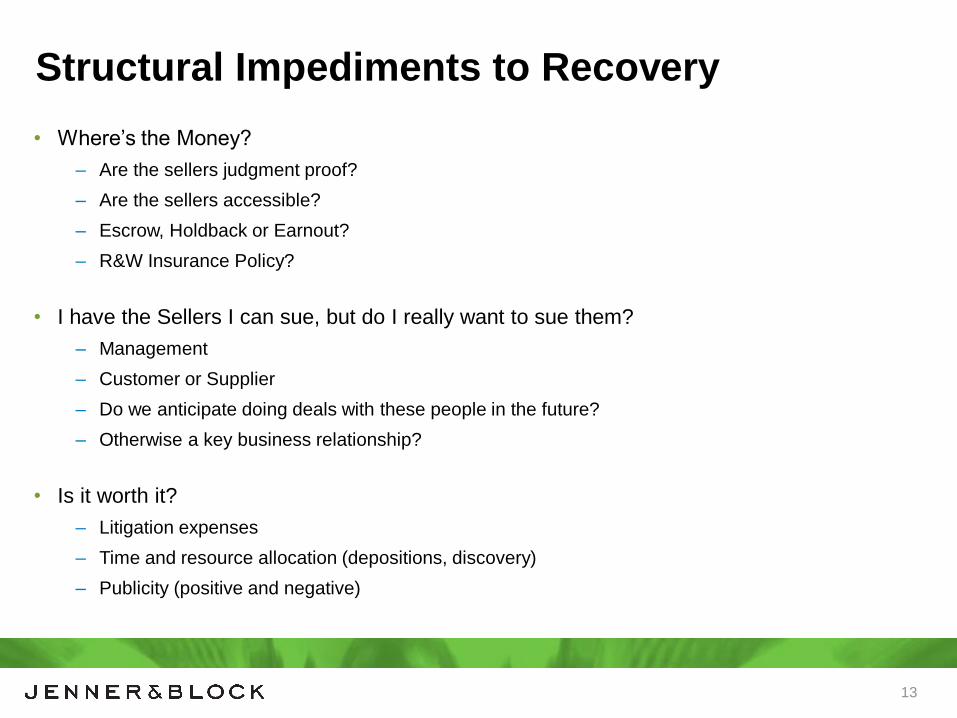

Structural Impediments to Recovery

• Where’s the Money?

– Are the sellers judgment proof?

– Are the sellers accessible?

– Escrow, Holdback or Earnout?

– R&W Insurance Policy?

• I have the Sellers I can sue, but do I really want to sue them?

– Management

– Customer or Supplier

– Do we anticipate doing deals with these people in the future?

– Otherwise a key business relationship?

• Is it worth it?

– Litigation expenses

– Time and resource allocation (depositions, discovery)

– Publicity (positive and negative)

14

Contractual Impediments to Recovery: Survival Periods

• Specified R&Ws only survive the closing for a limited period of time

• Generally intended to shorten the deadline for breach and indemnity

claims, but courts may not interpret them consistently:

– Depends on state law; Delaware is more likely to strictly enforce a survival clause than

California.

– Depends on precise wording. Does the survival provision require the non-breaching

party to file suit by the deadline or merely to give the other party notice of the claim?

• Varying time horizons for survival of representations:

– Short: Past performance and current condition of business (e.g., financial statements,

insurance)

– Long / Indefinite: “Fundamental” reps (e.g., good standing, capitalization)

15

Contractual Impediments to Recovery: Caps/Baskets

• Caps: limits on recovery

• Baskets: hurdles to recovery

– Tipping (first-dollar) basket?

– Deductible basket?

– Mini-basket?

• Dollar amounts usually based on a percentage of purchase price

• May not apply to breaches of fundamental reps

• Materiality or knowledge qualifiers make it harder to fill the basket or reach the

cap, but may be mitigated, in the case of materiality by a “materiality scrape”

• Materiality scrape has 2 flavors: (i) scrape for determining breach and damages

and (ii) scrape for purposes of determining damages only

16

Contractual Impediments to Recovery: Limits on Damages

Not just a laundry list: these words have important meanings.

17

Contractual Impediments to Recovery: Limits on

Damages (PLC formulation)

• In no event shall any Indemnifying Party be liable to any

Indemnified Party for any punitive, incidental,

consequential, special or indirect damages, including loss

of future revenue or income, loss of business reputation or

opportunity relating to the breach or alleged breach of this

Agreement, or diminution of value or any damages based

on any type of multiple [(other than indemnification for

amounts paid or payable to third parties in respect of

any third-party claim for which indemnification

hereunder is otherwise required)].

18

Contractual Impediments to Recovery: Limits on Damages

• Direct damages: naturally and necessarily flow from the breach

– E.g., market price for improving or replacing assets not delivered in the condition promised

• Incidental damages: costs related to rejection of goods being sold

– Not a major issue in M&A transactions

• Consequential damages

– Everything else!

– Losses that result from a breach because of the particular circumstances of the non-breaching party; e.g., inability

to perform on 3rd party contracts because of the breach

– Like all contract damages, must be reasonably foreseeable—not remote

• Lost profits

– Often misunderstood as a subset of consequential damages, but can be direct too

• Recent trend of pushing back on broad boilerplate:

– 2008 article piqued interest in true meaning of damages waivers (Glenn D. West & Sara G. Duran)

– Buyers do not have to accept a complete waiver of consequential damages as a foregone conclusion

19

Contractual Impediments to Recovery: Exclusive Remedies

• Indemnification as the exclusive remedy for breaches of representations & warranties

• ABA Study: > 90% of M&A purchase agreements contain this provision

• May limit buyer’s rights in numerous, and sometimes unexpected, ways:

– Calculation of damages

– Time limits on bringing claims

– Dispute resolution procedures

– Availability of equitable remedies, except as specified

• In some jurisdictions, do not preclude alternative remedies for securities law claims or

certain tort claims (e.g., claims based on intentional misconduct or gross negligence)

• Usually some exclusions (e.g., purchase price adjustments, equitable remedies for

specifically negotiated restrictive covenants)

20

Contractual Impediments to Recovery: Anti-Sandbagging

• Buyer knew of a breach, but it was not listed as an exception to the representation on the

disclosure schedules. Can the buyer seek indemnification?

• Contentious issue:

– Buyers want to enforce the allocation of risk they negotiated

– Sellers fear intentional exploitation of oversights in the due diligence and scheduling processes

• ABA study: 41% of M&A deals have a pro-sandbagging clause; 5% anti-sandbagging

• What about the “silent majority”?

– State law fills in the blanks with default rules

• Delaware: Pro-sandbagging

• New York: Depends on the expectations of the parties

• Illinois: Pro-sandbagging

• California: Anti-sandbagging

• Sandbagging generally an exception under R&W insurance policies, but can be limited to

things known at signing

21

Common Law Impediments to Recovery: Statute of Limitations

• Deadline for filing a particular type of claim

• SOL for breach of contract varies by state:

– Delaware: 3 years

– New York: 6 years

– Illinois: 10 years

– California: 4 years

• Clock generally starts ticking when the breach occurs, and for M&A reps, that is

usually at the time of closing

• Equitable: may get an extension if delay was caused by other party’s

wrongdoing

• Procedural, not substantive: not always captured by a generic choice-of-law

provision

22

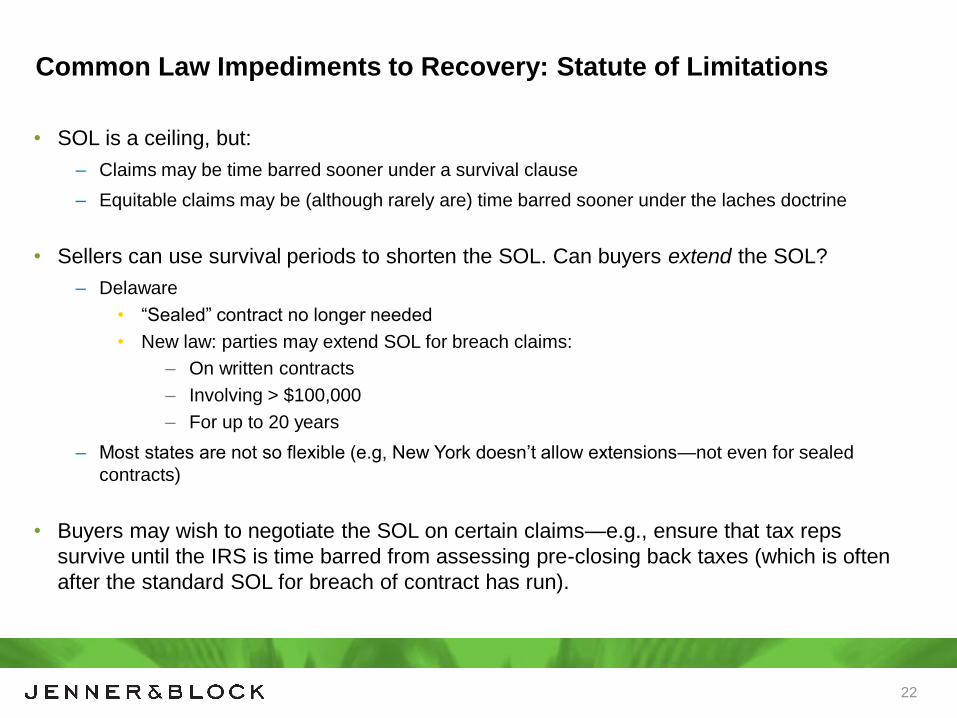

Common Law Impediments to Recovery: Statute of Limitations

• SOL is a ceiling, but:

– Claims may be time barred sooner under a survival clause

– Equitable claims may be (although rarely are) time barred sooner under the laches doctrine

• Sellers can use survival periods to shorten the SOL. Can buyers extend the SOL?

– Delaware

• “Sealed” contract no longer needed

• New law: parties may extend SOL for breach claims:

– On written contracts

– Involving > $100,000

– For up to 20 years

– Most states are not so flexible (e.g, New York doesn’t allow extensions—not even for sealed

contracts)

• Buyers may wish to negotiate the SOL on certain claims—e.g., ensure that tax reps

survive until the IRS is time barred from assessing pre-closing back taxes (which is often

after the standard SOL for breach of contract has run).

23

Trends in R&W Insurance Recovery

• 500+ policies written in 2014

• Improved pricing, coverage and product usage– R&W insurance now priced between +/- 3 to 4% of limit purchased (one-time payment at closing)

– Usually a due diligence fee of $20,000 to $40,000

– Coverage can extend beyond “market” representation, warranty and indemnity terms

• Data on claims history is largely anecdotal– AIG presentation provides several examples of approved “Claim Scenarios”, such as:

• Paying out for breaches of financial statement and accounts receivable representations under a seller-side

insurance policy after seller failed to disclose $1 million of outstanding gift certificates.

• Paying out for breaches of financial statement, good title, no material adverse change, and other

representations under a buyer-side insurance policy while the parties arbitrated their dispute.

– Litigation involving R&W coverage

• Ageas (UK) Ltd. v. Kwik-Fit (UK) Ltd:

– England’s High Court of Justice considered a dispute about proper method of calculating damages for

seller’s breach of accounting representations.

– Before the case went to trial, insurer admitted responsibility for any damages in excess of £5 million (a

deductible basket amount specified in the Share Purchase Agreement and R&W policy).

• Good incentives to pay claims: R&W insurers are repeat players. – Companies and law firms involved in future deals will only consider using their policies if they have a good

reputation for promptly approving valid claims.

24

Questions?