Renewable Energy Market Outlook 1-2. Ali...Market Outlook The 5th Northeast Asia Energy Security...

27

Renewable Energy Market Outlook The 5th Northeast Asia Energy Security Forum Ali Izadi December 12, 2017

Transcript of Renewable Energy Market Outlook 1-2. Ali...Market Outlook The 5th Northeast Asia Energy Security...

Renewable Energy Market OutlookThe 5th Northeast Asia Energy Security Forum

Ali Izadi

December 12, 2017

1 December 12, 2017

Analysis to help you understand the future of energy

Solar Wind Power and

Utilities

Electric

Vehicles

Energy Smart

Technologies

Gas Carbon

Markets &

Climate

Frontier

Power

Mobility and

Autonomous

Driving

Emerging

Technologies

Storage

Europe, Middle East

& AfricaAsia PacificAmericas

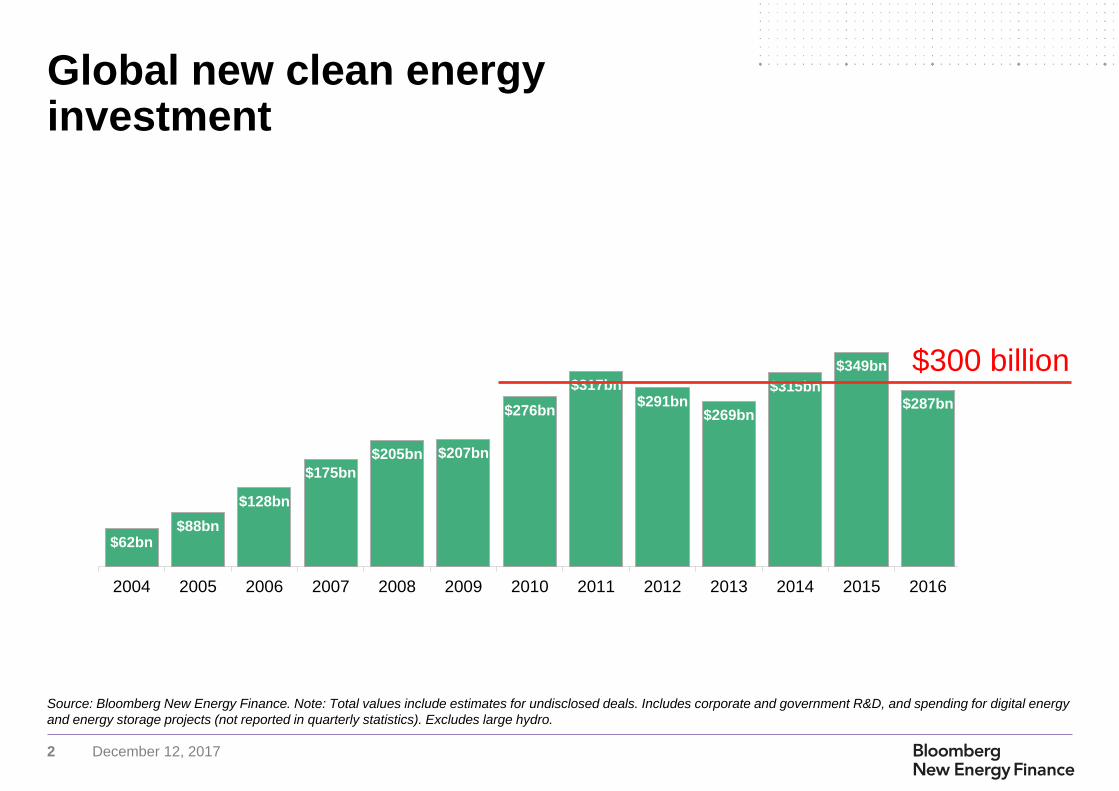

2 December 12, 2017

$62bn$88bn

$128bn

$175bn

$205bn $207bn

$276bn

$317bn$291bn

$269bn

$315bn

$349bn

$287bn

$258bn(estimate)

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

0.00

100.00

200.00

300.00

400.00

500.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Source: Bloomberg New Energy Finance. Note: Total values include estimates for undisclosed deals. Includes corporate and government R&D, and spending for digital energy

and energy storage projects (not reported in quarterly statistics). Excludes large hydro.

Global new clean energy investment

$300 billion

3 December 12, 2017

$62bn$88bn

$128bn

$175bn

$205bn $207bn

$276bn

$317bn$291bn

$269bn

$315bn

$349bn

$287bn

$258bn(estimate)

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

0.00

100.00

200.00

300.00

400.00

500.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

0.00

100.00

200.00

300.00

400.00

500.00

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

20GW

88GW

Source: Bloomberg New Energy Finance. Note:Total values include estimates for undisclosed deals. Includes corporate and government R&D, and spending for digital energy

and energy storage projects (not reported in quarterly statistics). Excludes large hydro.

Global new clean energy investment and capacity installations

$300 billion

160GW

4 December 12, 2017

Source: Maycock, Bloomberg New Energy Finance

Solar technology is getting cheaper, faster

0.1

1

10

100

1 10 100 1,000 10,000 100,000 1,000,000

historic prices (Maycock) Chinese c-Si module prices (BNEF) Experience curve at 28%

2016 ($/W)

2003

1976

1985

2008

Cumulative capacity

2015

2017

(estimate)

5 December 12, 2017

Source: Bloomberg New Energy Finance

BNEF global benchmark capexforecast for fixed-axis utility-scale systems

$1.85

$0.48 $0.29 $0.22 $0.18 $0.15 $0.12

$3.24

$1.14$0.86

$0.70 $0.59 $0.51 $0.45

2010 2016 2020 2025 2030 2035 2040

$/W (DC - 2016 real)

Module Inverter Balance of plant EPC Other System cost

6 December 12, 2017

Source: Bloomberg New Energy Finance Note: Data by contract signing date

Turbine price by delivery date

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1980 1984 1988 1992 1996 2000 2004 2008 2012 2016 2020

Global (ex. China) Germany (ExTool) Denmark (Extool) US (LBL) China (BNEF) Vestas global

million Euro/MW

7 December 12, 2017

Source: Bloomberg New Energy Finance Notes: Line shows central case, error bars

reflect the range between low speed and high speed sites

Source: Bloomberg New Energy Finance Note: Note: Averages are capacity-

weighted. We calculate the capacity factor with our proprietary Wind Farm Capacity

Factor Tool using real project data and wind resource data provided by 3TIER and

Vaisala. We assume P90 value in the capacity factor tool.

Onshore wind capacity factor Capacity factor forecast for the U.S

Onshore wind is getting cheaper as capacity factors rise

0%

10%

20%

30%

40%

50%

60%

19801984198819921996200020042008201220162020

Germany Denmark UK Spain US Canada

299MW

0%

10%

20%

30%

40%

50%

60%

70%

2017 2020 2025 2030 2035 2040

8 December 12, 2017

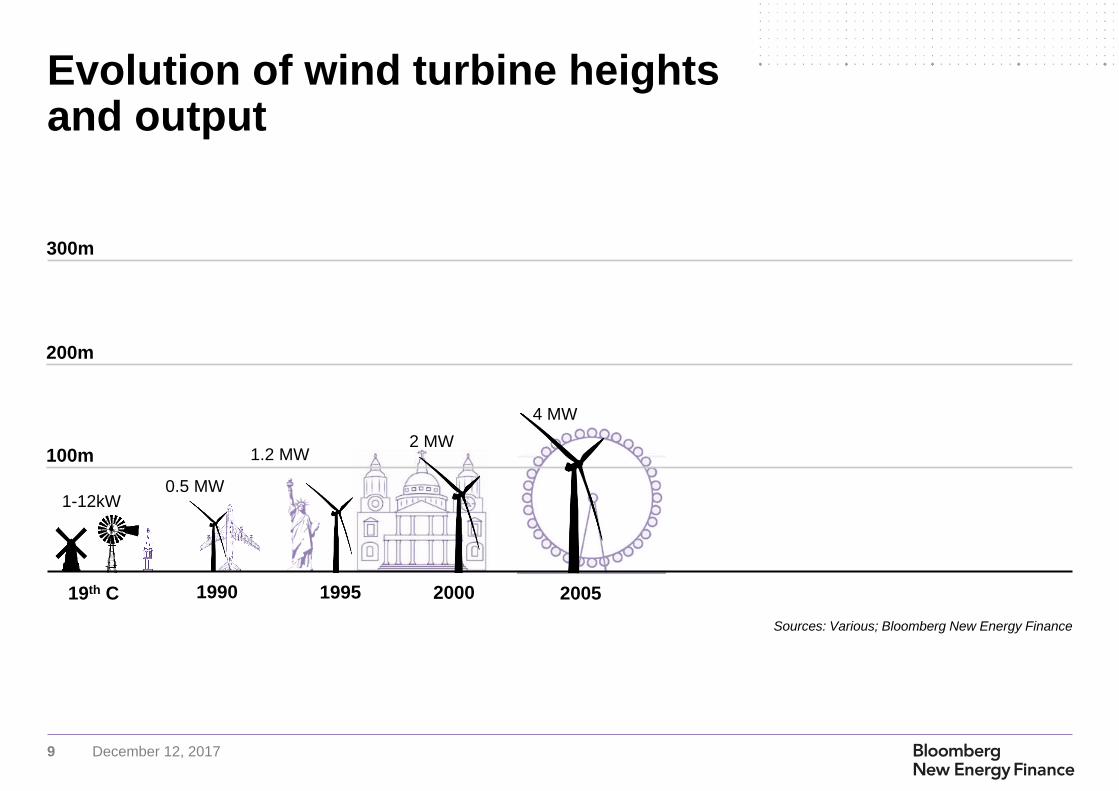

Evolution of wind turbine heights and output

20001995199019th C

300m

200m

100m

1-12kW0.5 MW

1.2 MW2 MW

Sources: Various; Bloomberg New Energy Finance

9 December 12, 2017

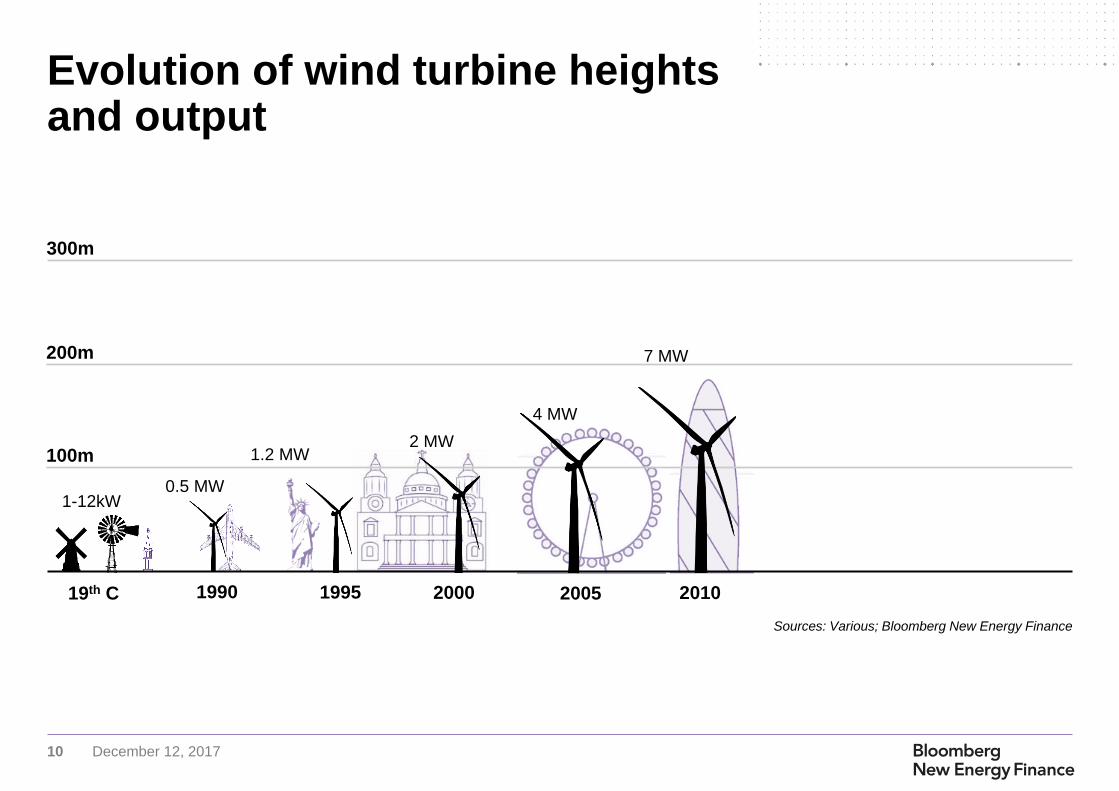

Evolution of wind turbine heights and output

2000 20051995199019th C

300m

200m

100m

1-12kW0.5 MW

1.2 MW2 MW

4 MW

Sources: Various; Bloomberg New Energy Finance

10 December 12, 2017

Evolution of wind turbine heights and output

2000 2005 20101995199019th C

300m

200m

100m

1-12kW0.5 MW

1.2 MW2 MW

4 MW

7 MW

Sources: Various; Bloomberg New Energy Finance

11 December 12, 2017

Evolution of wind turbine heights and output

20152000 2005 20101995199019th C

300m

200m

100m

1-12kW0.5 MW

1.2 MW2 MW

4 MW

7 MW 9 MW

Sources: Various; Bloomberg New Energy Finance

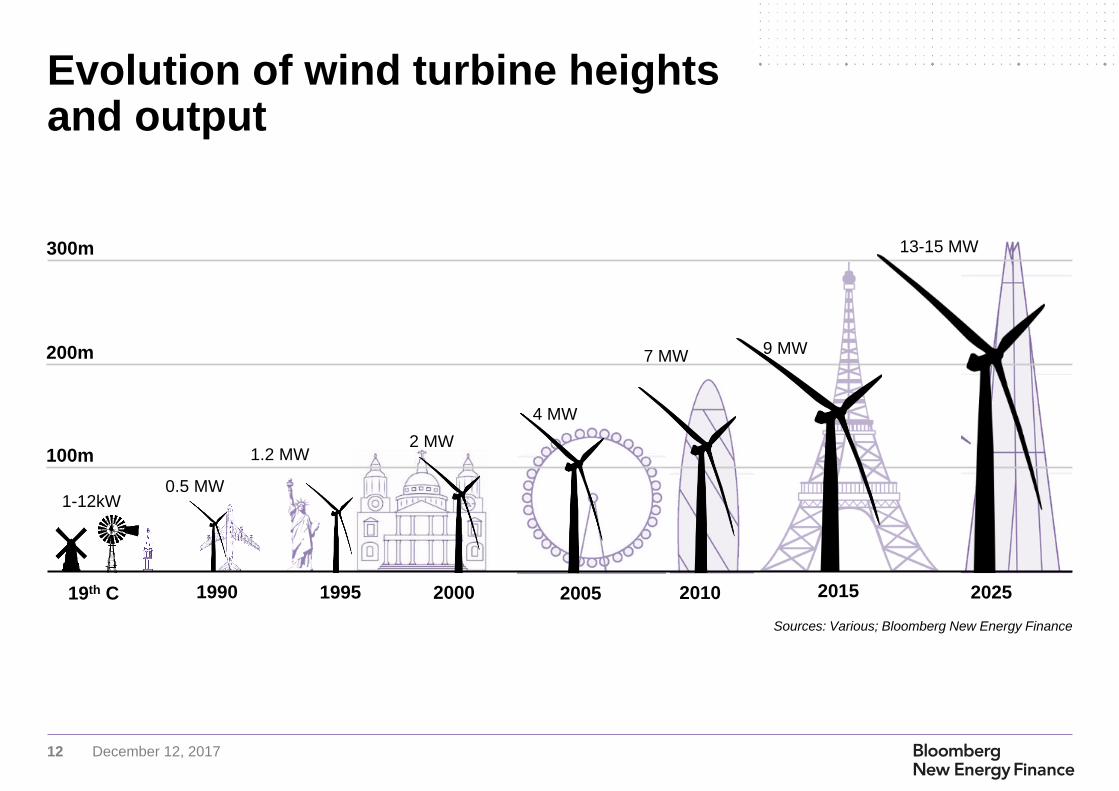

12 December 12, 2017

Evolution of wind turbine heights and output

202520152000 2005 20101995199019th C

300m

200m

100m

1-12kW0.5 MW

1.2 MW2 MW

4 MW

7 MW 9 MW

13-15 MW

Sources: Various; Bloomberg New Energy Finance

13 December 12, 2017

Source: Bloomberg New Energy Finance Note: Projects by commissioning date. Full dots show the project level LCOEs have been estimated using winning tariffs, tariff

duration, indexation (if applicable) and a power price assumption for the merchant tail.

Offshore wind has surprised us

Completed auction

Anholt

Horns Rev III

Danish near-shore

Krieger's Flak

Borssele I & II

Borssele III & IV

Zuid I & II

Zuid III & IV

Noord

CfD-R1-East Anglia 1

CfD-R1-Neart na Goithe

CfD-Round 2

CfD-Round 3

Gode Wind 3

BRW II, OWP West

He Dreiht

0

50

100

150

200

250

2012 2014 2016 2018 2020 2022 2024 2026 2028

Netherlands

Denmark

U.K.

Planned auction

BNEF central view

Germany

Historical BNEF central LCOE BNEF LCOE range (H2 2016)

$/MWh (2016 $)

14 December 12, 2017

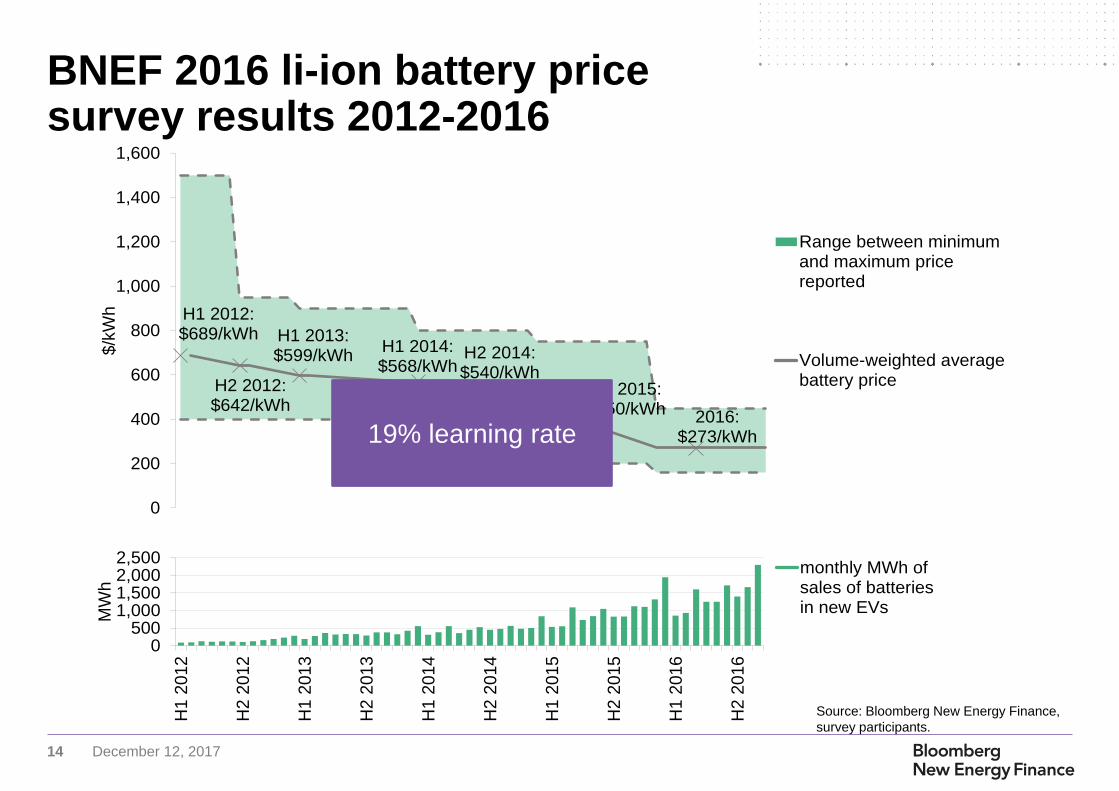

Source: Bloomberg New Energy Finance,

survey participants.

BNEF 2016 li-ion battery price survey results 2012-2016

H1 2012: $689/kWh

H2 2012: $642/kWh

H1 2013:$599/kWh

H1 2014: $568/kWh

H2 2014:$540/kWh

H2 2015:$350/kWh 2016:

$273/kWh

0

200

400

600

800

1,000

1,200

1,400

1,600

$/k

Wh

0500

1,0001,5002,0002,500

H1 2

012

H2 2

012

H1 2

013

H2 2

013

H1 2

014

H2 2

014

H1 2

015

H2 2

015

H1 2

016

H2 2

016

MW

h

689642599

Range between minimumand maximum pricereported

Volume-weighted averagebattery price

0500

1,0001,500

H1…H2…H1…H2…H1…H2…H1…

monthly MWh ofsales of batteriesin new EVs

19% learning rate

15 December 12, 2017

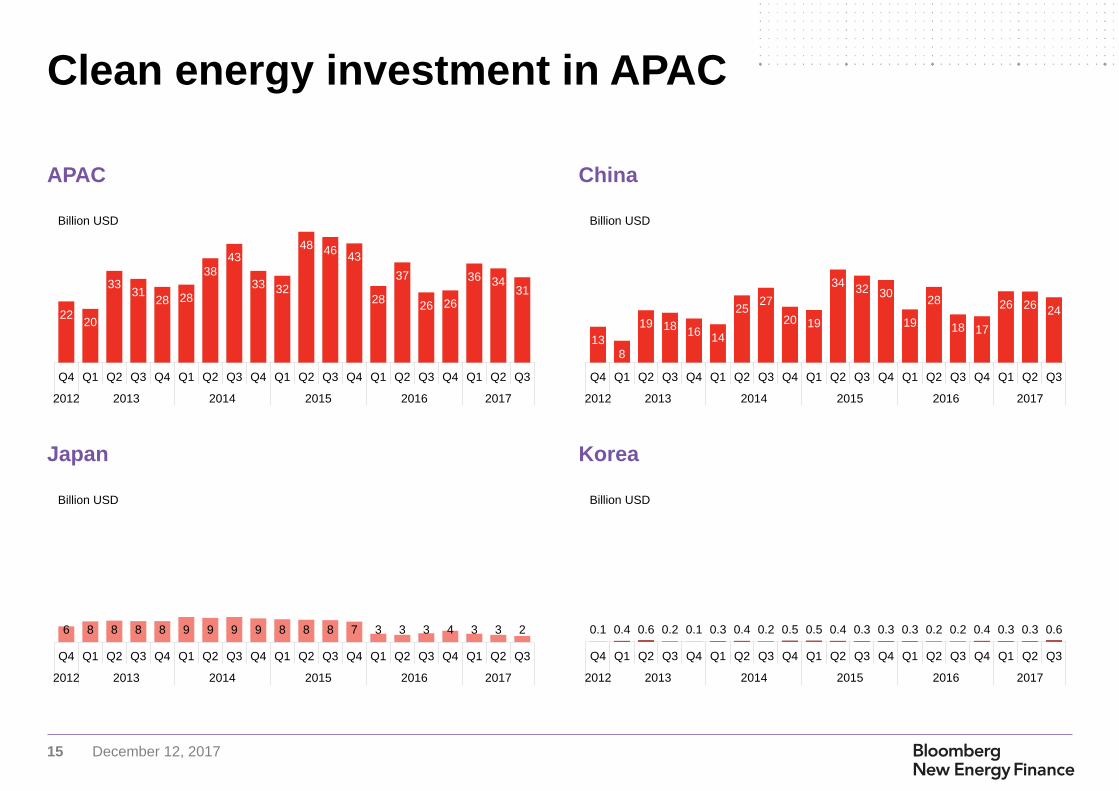

APAC China

Japan Korea

Clean energy investment in APAC

2220

3331

28 28

38

43

33 32

48 4643

28

37

26 26

36 3431

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2012 2013 2014 2015 2016 2017

Billion USD

13

8

19 1816

14

2527

20 19

3432 30

19

28

18 17

26 2624

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2012 2013 2014 2015 2016 2017

Billion USD

6 8 8 8 8 9 9 9 9 8 8 8 7 3 3 3 4 3 3 2

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2012 2013 2014 2015 2016 2017

Billion USD

0.1 0.4 0.6 0.2 0.1 0.3 0.4 0.2 0.5 0.5 0.4 0.3 0.3 0.3 0.2 0.2 0.4 0.3 0.3 0.6

Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3

2012 2013 2014 2015 2016 2017

Billion USD

16 December 12, 2017

Source: Bloomberg New Energy Finance

Renewable energy (excluding large hydro) proportion of power generation, 2006-16

Lowest

Mid

Highest

No data

13%

30%

Spain

3%12%

Australia

6%

18%

Brazil

5% 6%

Canada

6%10%

China

9%

29%

Germany2%

25%

UK

4% 6%

India12%

25%

Italy

7%12%

Japan

3%9%

US

1% 3%

South Africa

17 December 12, 2017

Climatescope coverage, 2017

26Latin American

& Caribbean

nations

19Sub-Saharan

Africa

nations

10Asian countries,

including 25

states/provinces in

India & China

3 MENA nations

OECD Since 2012 Since 2014 Since 2016 Since 2017 Non-OECD not in Climatescope

13countries in Central Asia

and Eastern Europe

Climatescope 2017

18 December 12, 2017

Ranking and Parameters

0

0.5

1

1.5

2

2.5

3

Chin

aB

razil

Jord

an

Me

xic

oIn

dia

So

uth

Afr

ica

Chile

Ke

nya

Uru

gua

yV

ietn

am

Se

ne

ga

lIn

do

nesia

Pa

kis

tan

Hon

du

ras

Tu

rke

yR

wa

nda

Uga

nd

aC

osta

Ric

aE

gypt

Arg

en

tina

Mo

ng

olia

Sri

La

nka

Nig

eri

aN

ep

al

Pe

ruC

olo

mbia

Ba

rba

do

sG

ua

tem

ala

Ta

nzan

iaE

thio

pia

Ba

ng

lade

sh

Gh

ana

Pa

na

ma

Russia

Sie

rra

Leo

ne

Leb

an

on

Nic

ara

gu

aE

l S

alv

ad

or

Lib

eria

Ukra

ine

Ge

org

iaB

oliv

iaE

cua

dor

Cam

ero

on

Bo

tsw

an

aJam

aic

aZ

am

bia

Cote

d'Iv

oir

eD

om

inic

an R

ep

ub

licB

eliz

eM

old

ova

Haiti

Zim

bab

we

Ka

za

kh

sta

nM

ozam

biq

ue

Arm

en

iaA

zerb

aija

nB

ela

rus

Kyrg

yzsta

nM

ya

nm

ar

Ma

law

iB

aha

mas

Ta

jikis

tan

Trin

idad

& T

ob

ago

Con

go

(D

em

. R

ep.)

Gu

yan

aU

zbe

kis

tan

Ve

ne

zue

laS

urin

am

eP

ara

gu

ay

Tu

rkm

en

ista

n

Enabling Framework Financing & Investment Value Chains Greenhouse-Gas Management

Source: Bloomberg New Energy Finance, Climatescope 2017

Climatescope 2017

19 December 12, 2017

2016 2040

Global electricity generation mix

Coal37%

Gas23%

Oil4%

Nuclear10%

Hydro17%

Onshore wind4%

Utility-scale PV1%

Small-scale PV1%

24,155TWh

Coal22%

Gas16%

Nuclear9%

Hydro15%

Onshore wind15%

Utility-scale PV

12%

Small-scale PV5%

38,079TWh

Source: Bloomberg New Energy Finance

New Energy Outlook 2017

20 December 12, 2017

Source: Bloomberg New Energy Finance

Global electricity generation by fuel type

Fossil fuel

Nuclear

Solar & Wind

Other Renewables

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2012 2016 2020 2025 2030 2035 2040

(TWh)

New Energy Outlook 2017

21 December 12, 2017

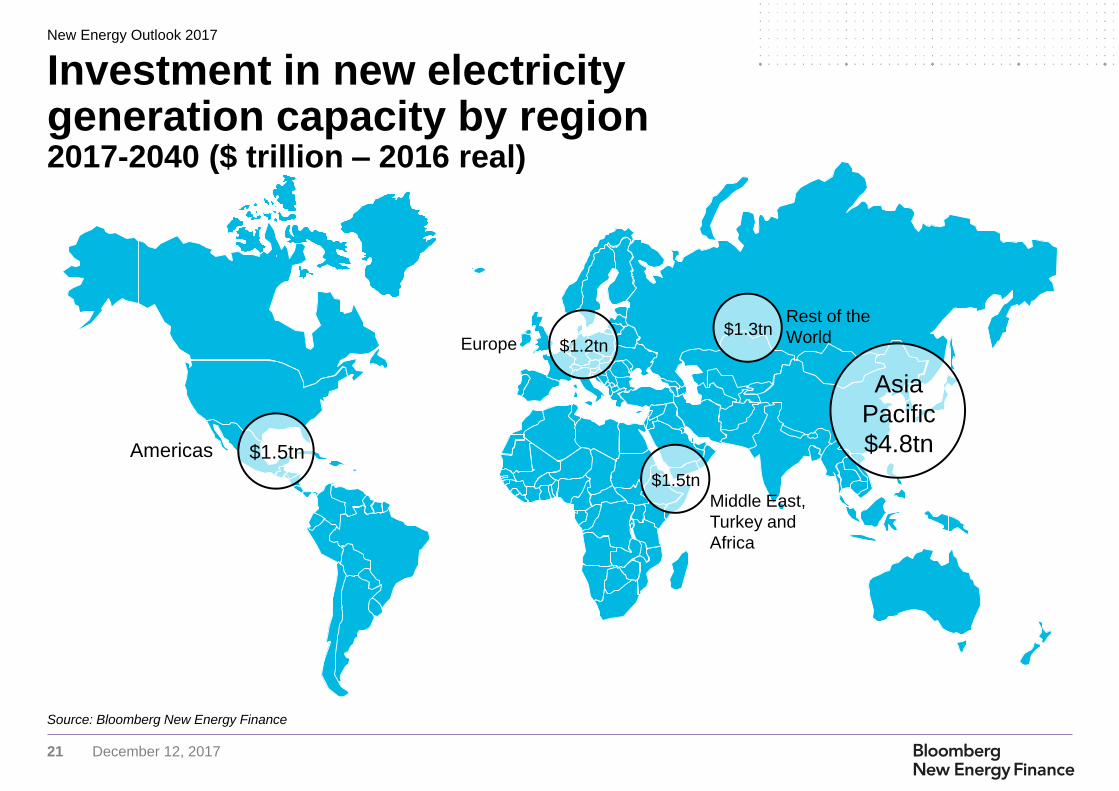

Source: Bloomberg New Energy Finance

Investment in new electricity generation capacity by region2017-2040 ($ trillion – 2016 real)

Source: Bloomberg New Energy Finance

Asia

Pacific

$4.8tn$1.5tnAmericas

$1.2tnEurope

$1.5tn

Middle East,

Turkey and

Africa

$1.3tnRest of the

World

New Energy Outlook 2017

22 December 12, 2017

Source: Bloomberg New Energy Finance

Global investment by region, 2017-2040 APAC investment by region, 2017-2040

APAC: 47% of investmentChina & India: 83% of investment in APAC

$2,823

$1,157

$431

$195

$142

$79

China

India

SE Asia

Japan

SouthKorea

Australia

($ billion - 2016 real)

Coal Gas Nuclear Hydro

Wind Solar Other

$4,828

$1,454

$1,454

$1,264

$1,185

APAC

AMER

META

RoW

Europe

($ billion - 2016 real)

Coal Gas Nuclear Hydro

Wind Solar Other

New Energy Outlook 2017

23 December 12, 2017

Source: Bloomberg New Energy Finance

Country All renewables Country PV and wind

Italy 96% Mexico 73%

Brazil 96% Iberia 63%

Iberia 86% Germany 61%

Chile 86% Italy 59%

Mexico 82% Chile 55%

Canada 79% Australia 55%

Germany 74% UK 50%

France 65% France 46%

UK 63% Brazil 43%

Australia 62% India 41%

China 55% China 39%

India 49% Thailand 39%

Thailand 49% SSA 34%

Turkey 48% South Korea 32%

Philippines 47% United States 31%

Japan 42% Japan 30%

United States 38% Philippines 30%

Malaysia 37% Turkey 28%

South Korea 34% MENA 27%

Indonesia 31% Canada 24%

Renewable penetration ranking by 2040

New Energy Outlook 2017

24 December 12, 2017

Source: Bloomberg New Energy Finance

Power sector emissions peak in 2026 but remain far from 2 trajectory

NEO2017

NDC trajectory

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2016 2020 2025 2030 2035 2040

(MtCO2)

NEO2017

NEO2017 - 2deg trajectory

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

2012 2016 2020 2025 2030 2035 2040

(MtCO2)

Global power sector CO2 emissions trends and

Paris Agreement targets (NDC)

Global power sector CO2 emissions trends and

the 2 degree pathway

New Energy Outlook 2017

25 December 12, 2017

This publication is the copyright of Bloomberg New Energy Finance. No portion of this document may be photocopied,

reproduced, scanned into an electronic system or transmitted, forwarded or distributed in any way without prior consent of

Bloomberg New Energy Finance.

The information contained in this publication is derived from carefully selected sources we believe are reasonable. We do not

guarantee its accuracy or completeness and nothing in this document shall be construed to be a representation of such a

guarantee. Any opinions expressed reflect the current judgment of the author of the relevant article or features, and does not

necessarily reflect the opinion of Bloomberg New Energy Finance, Bloomberg Finance L.P., Bloomberg L.P. or any of their

affiliates ("Bloomberg"). The opinions presented are subject to change without notice. Bloomberg accepts no responsibility

for any liability arising from use of this document or its contents. Nothing herein shall constitute or be construed as an

offering of financial instruments, or as investment advice or recommendations by Bloomberg of an investment strategy or

whether or not to "buy," "sell" or "hold" an investment.

Copyright and disclaimer

Coverage.

Renewable Energy

Power & Utilities

Gas

Carbon Markets & Climate Negotiations

Energy Smart Technologies

Storage

Electric Vehicles

Mobility and Autonomous Driving

Frontier Power

Emerging Technologies

Bloomberg New Energy Finance is a

research firm that helps energy

professionals generate opportunities. With a

team of experts spread across six

continents, BNEF provides independent

analysis and insight, enabling decision-

makers to navigate change in an evolving

energy economy.

BNEF research and analysis is accessible

via web and mobile platforms, as well as on

the Bloomberg Terminal.

about.bnef.com

@BloombergNEF

Ali Izadi