Relationships Between Produce Supply Firms and...

10

Relationships Between Produce Supply Firms and Retailers in the New Food Supply Chain Jill J. McCluskey and A. Desmond O’Rourke Increasedconsolidationin the retail fwd industry,retail discount stores’expansioninto fbodjand the use of informationteclmologyhave createda new breedof retail groceryestablishmentsthat are rapidly capturinga growing shareof the retail fmd business.In orderto studythe relationshipsbetweenproduce suppliersand buyers and to offer strategiesfor smalland mdlum-sized produce supplyfins, executives representinga Pacific Northwestsampleof produce supplyfirms and major retail chains were interviewed. The resultspresented and evaluatedin this paper are based on informationobtainedfrom these interviews, currentbusiness practices,and evolvingrelationshipsbetweenlarge retail buyersand small and medium- sized suppliersof fresh produceand frozenfruits and vegetables. Introduction The increased level of mergers and acquisi- tions among retail grocery store chains, retail dis- count stores’ expansion into fo@ and the use of information technology have created a new breed of retail grocery establishment with a rapidiy growing share of the retail food business. Produc- er% packers, and processors are concerned about their ability to adapt to the changing needs of large vohnne buyers. Many small end me&ru- sized agricuhural suppliers fear that they will gradually be excluded horn doing business with high-volume buyers as retail operators reduce the number of suppliers, seek formal alliances (often linked by electronic data interchange systems), and demand more quality assurances and process controls. One potential concern is that the gap in market power, which is apparently widening between buying entities and food suppliers, has shifted bargaining power to buyers. Many sup- pliers pref= to do business with only one large- volume buyer, such as Wal-Mart. The buyer can potentially dictate the relationship terms. Since there are many suppliers, one supplier is easily replaceable; however, it may be more Theauthorsare assistantprofwsorandprofessoremeritus, respectively, Department of Agricultural Economies, Wash- ingtonStateUniversity. Theauthorswishto thank,without implicatingTomSehotzko, JimYoude,SarahDmffeLand BrucePrenguberfor theircontribution to this projxt and PaulBarkleyfor his helpfi.dcomments.‘I& projectwas fimded under the U.S. Department of Agricukure- AgricukurdMarketingService(USDA-AMS) FederalState MarketImprovement ProgramCooperativeAgreement #12- 2543-0259between the USDA-AMS, WashingtonStateUni- versity,andGlobalwise, Inc. difiicult for a supplier to find another buyer of comparable size. In additiom the large buyer may require the supplier to make au investment in a specific electronic data interchange (EDI) system and to gain knowledge of system operations. For example, Wal-Mart expects its vendors to pur- chase and use Retail L* a proprietary software package that requires special training and constant updates by Wal-Mart (McEvoy, 1999.) This in- vestment brings up asset-specificity issues, which have been extensively analyzed in transaction cost economics. Asset specificity is defined as the in- vestment in assets that are specialized to the ex- change between a specific buyer and seller (Perry, 1989). A large difference can exist between the value of the asset in this use and the value in its next best use. In theory, the potential for oppor- tunistic behavior with asset specificity requires more complex aud lengthy contracts and makes vertical integration desirable. Our study provides some support for this theory-based hypothesis. We found that the larger the retail organization%the greater the use of con- tracts and the longer the contract period. The iio- zen produce market as a whole had primarily been a spot mark~ but at the time of the survey, more and more of’the market was being covered with contracts. (In the tlesh produce marketj contracts were being used more than they had been in the P% -but it Wm a primarily a spot market.) h adihtionj we found thatj although most contracts were not complex in relative terms, retail buyers wanted product characteristics to be more strictly defined than they had been in the past. Retailers may ako have been exercising mar- ket power by demanding lower prices under one guise or another. Some retailers required bids on large-volume orders. Other retailers expected

-

Upload

truongdang -

Category

Documents

-

view

215 -

download

0

Transcript of Relationships Between Produce Supply Firms and...

Relationships Between Produce Supply Firmsand Retailers in the New Food Supply Chain

Jill J. McCluskey and A. Desmond O’Rourke

Increasedconsolidationin the retail fwd industry,retaildiscount stores’expansioninto fbodjand the useof informationteclmologyhave createda newbreedof retailgroceryestablishmentsthat are rapidlycapturinga growingshareof the retail fmd business.In orderto studythe relationshipsbetweenproducesuppliersand buyersand to offerstrategiesfor smalland mdlum-sized producesupplyfins, executivesrepresentinga PacificNorthwestsampleof producesupplyfirmsand majorretailchainswere interviewed.Theresultspresentedandevaluatedin this paperare basedon informationobtainedfromthese interviews,currentbusinesspractices,and evolvingrelationshipsbetweenlarge retail buyersand smalland medium-sizedsuppliersof freshproduceand frozenfruitsand vegetables.

Introduction

The increased level of mergers and acquisi-tions among retail grocery store chains, retail dis-count stores’ expansion into fo@ and the use ofinformation technology have created a new breedof retail grocery establishment with a rapidiygrowing share of the retail food business. Produc-er% packers, and processors are concerned abouttheir ability to adapt to the changing needs oflarge vohnne buyers. Many small end me&ru-sized agricuhural suppliers fear that they willgradually be excluded horn doing business withhigh-volume buyers as retail operators reduce thenumber of suppliers, seek formal alliances (oftenlinked by electronic data interchange systems),and demand more quality assurances and processcontrols.

One potential concern is that the gap inmarket power, which is apparently wideningbetween buying entities and food suppliers, hasshifted bargaining power to buyers. Many sup-pliers pref= to do business with only one large-volume buyer, such as Wal-Mart. The buyer canpotentially dictate the relationship terms. Sincethere are many suppliers, one supplier iseasily replaceable; however, it may be more

Theauthorsare assistantprofwsorand professoremeritus,respectively,Departmentof AgriculturalEconomies,Wash-ingtonStateUniversity.Theauthorswishto thank,withoutimplicatingTom Sehotzko,Jim Youde,SarahDmffeLandBrucePrenguberfor their contributionto this projxt andPaul Barkleyfor his helpfi.dcomments.‘I& projectwasfimded under the U.S. Department of Agricukure-AgricukurdMarketingService(USDA-AMS)FederalStateMarketImprovementProgramCooperativeAgreement#12-2543-0259betweentheUSDA-AMS,WashingtonStateUni-versity,andGlobalwise,Inc.

difiicult for a supplier to find another buyer ofcomparable size. In additiom the large buyer mayrequire the supplier to make au investment in aspecific electronic data interchange (EDI) systemand to gain knowledge of system operations. Forexample, Wal-Mart expects its vendors to pur-chase and use Retail L* a proprietary softwarepackage that requires special training and constantupdates by Wal-Mart (McEvoy, 1999.) This in-vestment brings up asset-specificity issues, whichhave been extensively analyzed in transaction costeconomics. Asset specificity is defined as the in-vestment in assets that are specialized to the ex-change between a specific buyer and seller (Perry,1989). A large difference can exist between thevalue of the asset in this use and the value in itsnext best use. In theory, the potential for oppor-tunistic behavior with asset specificity requiresmore complex aud lengthy contracts and makesvertical integration desirable.

Our study provides some support for thistheory-based hypothesis. We found that the largerthe retail organization%the greater the use of con-tracts and the longer the contract period. The iio-zen produce market as a whole had primarily beena spot mark~ but at the time of the survey, moreand more of’ the market was being covered withcontracts. (In the tlesh produce marketj contractswere being used more than they had been in theP% -but it Wm a primarily a spot market.) hadihtionj we found thatj although most contractswere not complex in relative terms, retail buyerswanted product characteristics to be more strictlydefined than they had been in the past.

Retailers may ako have been exercising mar-ket power by demanding lower prices under oneguise or another. Some retailers required bidson large-volume orders. Other retailers expected

12 November 2000 Journal of Food Distribution Research

prompt payment discount% even when they didnot meet time deadlines for payment. Buyers de-manded more in terms of product specification.

There has been considerable debate as to howsmall and medium-sized suppliers will tie in thenew and changing food supply distribution network.Relatively large cmupauies have greater capital andhurnm resources with which to respond to the&anging stmcture and idormation technology.Smaller companies, even if growing tend to havelimited levels of both types of resourees.

In order to evaluate the viability and relation-ships between small and medium-sized producesupply firms and retailers, personal interviewswere conducted with small and medium-sizedfresh produce packer% frozen hit and vegetableprocesso~ and executives ftom major retailchains. Our research goals were: (1) to assess thecurrent relationships between large purchasingcompanies and a sample of small and medium-sized suppliers; (2) to project how the terms ofthose relationships are changing as large pur-chasing companies attempt to strengthen theircompetitive positiomy and (3) to determine whatsmall and medium-sized suppliers need to do toremain viable against such large purchasing com-panies in the retail grocery industry. In this paper,changes in the fd supply chain will be dis-cussed; findings flom the interviews will be pre-sente@ and the implications of these findings willbe explored.

The Changing Retail Food Environment

Mergers and acquisitions have been plentifidin the past several years. As a result the largechains are getting larger. From the early 1980sthrough 1998, the percent of total sales capturedby the top four supermarket chains increased from18 percent to 22 percent (Kinsey, 1998). Severalexamples directly involved grocay chains in thePacific Northwest. In November 1997, FredMeyer-a PortIan4 Oregon-based chain-ac-quired Quality Food Centers and Ralph’s @OCOry

Company in separate transactions worth about $2bdlion. It ako purchased Smith’s Food and DragCenters for $1.96 billion (Moriwaki, 1997). InMay 1998, Royal Ahold acquired Giant Fo@ Inc.for $2.6 billio~ and in October 1998, Safkwayacquired the Dominick’s supermarket chain for$1.85 billion (Canedy, 1998). In August 1998,when Albertson’s acquired American Stores

Company for $8.3 billio% it briefly became thenation’s largest cha@ with $36 billion in revenueand 2,500 stores in 37 states (Canedy, 1998).However, K.roger took over that title when it ac-quired Fred Meyer in May 1999 (AP, 1999). AsKoger moved westwart Safeway-which hadacquired California-based Vons--added Randall’sin Houston and Carr Gottstein Foods in AIaska(Zwieback 1999).

Internal growth and expansion has been asignificant factor in the retail grocery industry inrecent history. Wal-Mart entered the retail gro-cery industry a decade ago and has been ex-panding rapidly. According to SEC filings, as ofJanuary 31, 2000, the company reported having1,797 Wal-Mart stores, 710 Supercenter% and463 Sam’s Club stores in the United States, aswell as 1,008 outlets in nine other countries.Wal-Mart sells food through its supercenters andclub stores and has begun to expand its newestformat of smaller “neighborhood” grocery stores.Wal-Mart became the third largest food retailerin the United States with sales of about $32 bil-lion in 1998 (F’oodInstitute Report, 1999). Manyanalysts believe that WaLMart is currently thelargest fwd retailer in the United States. Its maincompetitor in the club store segmenz Costco-anIssaquah, Washington-based discount warehousechain-is reported to be on the verge of expand-ing its own grocery segment. Consolidation isalso taking place at the wholesale level. Super-valu acquired Richfoods Holdings. CertifiedGrocers of California merged with United Gro-cers of Portlant and Ahold acquired U.S. FoodServices, Inc.

The big are getting bigger; the smail arenot keeping up; and the resulting shifl in marketpower will result in major changes for foodsuppliers. Furthermore, as retailers expan~ willthey be willing or able to buy from any suppli-ers except those that are relatively large? Thisquestion illustrates the importance of additionalresearch.

The Role of Technology and Innovation

Wat-Mart has been a catalyst for manychanges in retail distribution. In 40 years, it hasgrown Born a small discount store in rural Arkan-sas into the world’s largest retailer, with estimatedglobal sales of $165 billion for the year endingJanuary 31, 2000. Wal-Mart built much of its suc-

McChJSk%?y,J J andA. ~. O ‘Rourh . . . Produce Supply Firms and Retailers in the Nm Food Supp@ Chain 13

cess on the use of information technology in thecontrol of costs m every part of its syste~ thusallowing it to sell at everyday low prices (EDLP)that drew in an ever-expanding pool of customers.

Wal-Mart expanded its presence in food re-tailing iu the 1990s for two reasons. F- it sawopporhmities to gain market share from traditionalfood supermarkets with its EDLP concept. Sec-ond in its supercenter and club formats, fbodcould be used to build traffic since consumerstend to shop more hquently for food than fordurable goods (McEvoy, 1999). Wal-Martbrought its purchasing might logistics expertise,and category management skills to the food re-tailing business.

In mid-1992, @aditional players in the fdsupply chain formed a working group to evaluateinefficiencies and to develop strategies for im-proving the system to counter the competition cre-ated by nontraditional fmd retailers like Wal-Mart.A new initiative, efficient consumer response(ECR), oame out of this working group (KurtSahnon Associat~ Inc., 1993). The main tenet ofECR is an accurate flow of information deliveredon a timely basis (Park and Mcm 1998).This concept encourages retailers to hold onlyenough inventmy to meet immediate consumerneeds. For example if consumers bought an itemonce a weelGinventory should be about one week’ssupply, not many weeks as had previously been thecase (King and Phurnpiw 1996).

The ECR initiative led to mauy innovations.It encouraged the adoption of information tech-nology for the identification of inefficiencies.Some applications of this technology encouragedcategory management and activity-based costin~enabling both supplier and retailer to identifi op-portunities for lowering costs and enhancing valueto wnsumers. Vertical alliances in the distributionsystem became more oommon.

Category management enabled retailers toassess the sales, cost% and profitability of eachstock-keeping unit (SKU) in a category. In addi-tiom retailers used information obtained fromcategory management to make intelligent deci-sions about the addition or subtraction of SKUS,promotion choices, quality maintenance, andmethods for reducing shrink. Some major retailersentrust the management of a catego~ to a majorsupplier. For example, Wal-Mart allows Chiqui@Dole, and Del Monte to be the category managersfor bananas in various WaM4art distribution cen-

ters (Turcsilq 1999). The Washington AppleCommission provides category managementservices to 40 retail chains with more than 3,000stores. Catego~ management in produce is ex-pauding rapidly as the volume of brande~ pack-aged produce and the number of product lookupcodes increase. The Wal-Mart tiormation systemand the original platform for ECR were based onproprieW’y EDI systems. These systems can beeasily justified by large buyers but could be pro-hibitively expensive for small-volume suppliers.For example, shared EDI between Wal-Mart andProcter and Gamble made economic sense. How-ever, the linkage of a small supplier with a numb-er of different proprietary EIX systems would beinfeasible.

The Produce Supply Industry

The structure of the produce supply industryis also changing. Until recently, the productionof produce could be described as fragmented andcomprised of many (mostly small) producers inmany growing regions with little verticalcoordination. In recent years, the production ofmajor produce commodities has becomeconcentrated in fewer but larger firms (WilsoUl%ompso~ and Coolq 1997). In the Washingtonapple industry, for example, the number ofwarehouses deoreased dramatically in the past 10years, and the percentage of the state’s total cropserviced by the largest warehouses increased(Lutz, 1998). In 1999, the top 20 shippers ofWashington apples supplied almost 60 percent ofthe state’s total apple stales (Warner, 2000).Given that the number of small and medium-sized firms is declinin~ important items ofresearch include: the role of these firms in thenew food supply chain and the sort ofrelationships that firms establish with retailbuyers. Small and medium-volume producesuppliers are concerned about finding newstrategies for survival in the new fwd supplychain, Their concern was a major motivation forthiS study.

Interviews

In order to evaluate the changing rehition$hipsbetween produce suppliers and retailer% we con-ducted extensive personal interviews with smalland medium-sized suppliers based in the U.S. Pa-

14 November 2000 Journal of Food Distribution Research

cific Northwest and with executives ftom majorretail chains. We interviewed top-level executivesfrom 19 produce supply firms and from four majorretail food chains. Although our sample of suppli-ers is relatively small and confined to the PacificNorthwe~ there are wide diflbmnces in their prod-ucts, customer% internal organizatio~ and pre-fmed distribution systems. The large retail chainsincluded in this project were limited to those withoutlets in the western United States to increase thelikelihood that they would have business relation-ships with the suppliers in this study. The majorretailers varied in store format and in businessgoals. The sample size for retailers was small rela-tive to the number of chains but significant in termsof market share. For disclosure reasons, we cannotpresent market share numbers, but we can state thatthe retailers in our sample are among the leadingfirms in the industry.

Suppliers were segmented into two catego-ries: (1) fi-esh hit or vegetables and (2) frozenfruit or vegetables. Suppliers who met thesecriteria were included in the study at the rec-ommendation of experts familiar with PacificNorthwest agriculture. Fresh suppliers includedonly handlers of vegetables, potatoes, and treefruits. Frozen suppliers were limited to vegeta-bles, berries, and processed vegetable and fi-uitproducts. Nine fresh suppliers participated inthe interview process. Of those nine, one re-ported annual sales less than $10 million whilethe remainder reported sales between $10 mil-lion and $50 million. Three of the fresh proces-sors focused on potato and onion industry sales;four sold tree fruit and three handled vegeta-bles. The 10 frozen product suppliers were splitevenly between companies with brands andcompanies that dealt exclusively with privatelabels. Four reported annual sales of less than$100 million; five had armual sales between$100 million and $500 million; and one re-ported annual sales of just over $500 million.These firms produce a variety of frozen fruitand vegetable products.

Each set of questiomaires included questionsabout the impacts of consolidation and technologyfrom different perspeetives. Qaestions pertainedto supplier capabilitie~ order volume and fre-quency; special packaging and organic capabili-ties; relationship technology, such as stock re-plenishment, and electronic data interchange; andbusiness terms.

Supplier Iuterview Results

The consolidation and growth in the retailindustry affected suppliers in a variety of ways. Interms of account numbers, the consolidation trenddid not appear to impact some suppliers at all.Although many of the interviewed processors andhandlers said that the number of companies towhich they sold had declined, others indicated thattheir numbers had increased or had at least re-mained steady. Of the nine fresh produce firmsinterviewed, three suppliers indicated that thenumber of buyers to whom they provided servicehad remained steady or increased; six replied thatthe number had decreased. Several respondentsstated that, despite declining account numbers, theaverage volume of accounts increased. This trendwas not so apparent with the frozen product sup-pliers. Less than one-half of the interviewed fko-zen product firms said that the number of compa-nies to which they provided service had de-creased. Four others replied that the numbers hadremained constant and two stated that they hadexperienced an increase in account numbers. Fivefrozen product firms said that the number in-creased during the past five years.

Small and Medium Supplier Capabilities

All fresh produce firms claimed the ability tofill orders in one day or less, although this was nottypically required by customers. Frozen foodcompanies needed more time for filling ordersthan the flesh produce suppliers did. Four firmsneeded between one and four days; several statedthat it could be done fmter, but buyers were dis-couraged from such requests by monetary penal-ties. Four firms needed one week, and the re-maining two firms required between one and twoweeks. Firms with brands tended to have the abil-ity to respond more quickly than their counter-parts who provided private-label produets.

Most frozen product firms had the ability todeliver or arrange delivery to buyers’ specifiedlocations at an appointed time. They also providedassistance in arranging transportation for theirbuyers upon request. All firms offimxi less-than-tmckload volumes, although several offered fidltruckload discounts or required the buyer to dealwith transportation or pay premiums for smallamounts. Most firms allowed buyers to set theirown schedules as to frequeney of delivery since

McCluskey, J J andA. D. O ‘Rode . . . Produce Supply Firms and Retailers in the New Food Supply Chain 15

they were the ones paying for @ansporWion. Sev-eral firms limited the frequency of delivery ac-cording to the size of the account. Logistics andmode of transportation limited frequency of deliv-ery. Although several firms had the capability toship anywhere in the United Stat= most firmsserved mainly companies in the West and Mid-west, Some firms could also skip internationally.

Fresh produce firms had the ability to meetspecial packaging requirements for their accounts;however, the extent to which they were able to doso varied greatly. Five firms could vary size; fivecould create boxe@ bagg@ or banded packs; fivecould vary labeling and one of the vegetablefirms created special product mixes and cuts. Thefrozen suppliers also had the ability to providespecial packaging. Variations on size% includingbundled produet~ could generally be provided byall of the firms. Other firms could provide diff@r-ent produet mixes and recipes, sty~es of package,promotional pallet% and universal product codes(uPcs).

The ability to supply organic productsvaried greatly among respondents. While allbut one fresh produce firm received requestsfor organic produce, only three seriously in-cluded organics in their product mix. Threeadditional fresh produce firms explored or-ganics but found them either prohibitivelycostly or not readily available. All of the sup-pliers expected to be able to meet requests inthe future if the organic supply were to in-crease. Three firms did not handle organics atthe time of the survey but were developing theability to do so on a small scale.

Six fkozen product iirrns processed organicproducts. Only one firm said that they did notreceive any requests for organic products. Threeadditional fms were not processing any organ-ics at the time of the survey, although each isnow considering a change in that policy. Six ofthe 11 interviewed executives foresaw continuedgrowth in the organic market; however, two ofthe companies that processed organic products atthe time of the survey were considering with-drawing from this market and another was notsure the organic segment had the growth poten-tial to remain profitable. These respondents sawthe organic segment as a niche market only. Oneother executive commented that organic productsreceived such high premiums on the fresh market

that fi-ozen organic production was not ade-quately supplied.

Electronic Data Interchange StockReplenishment Programs andAccount Trends

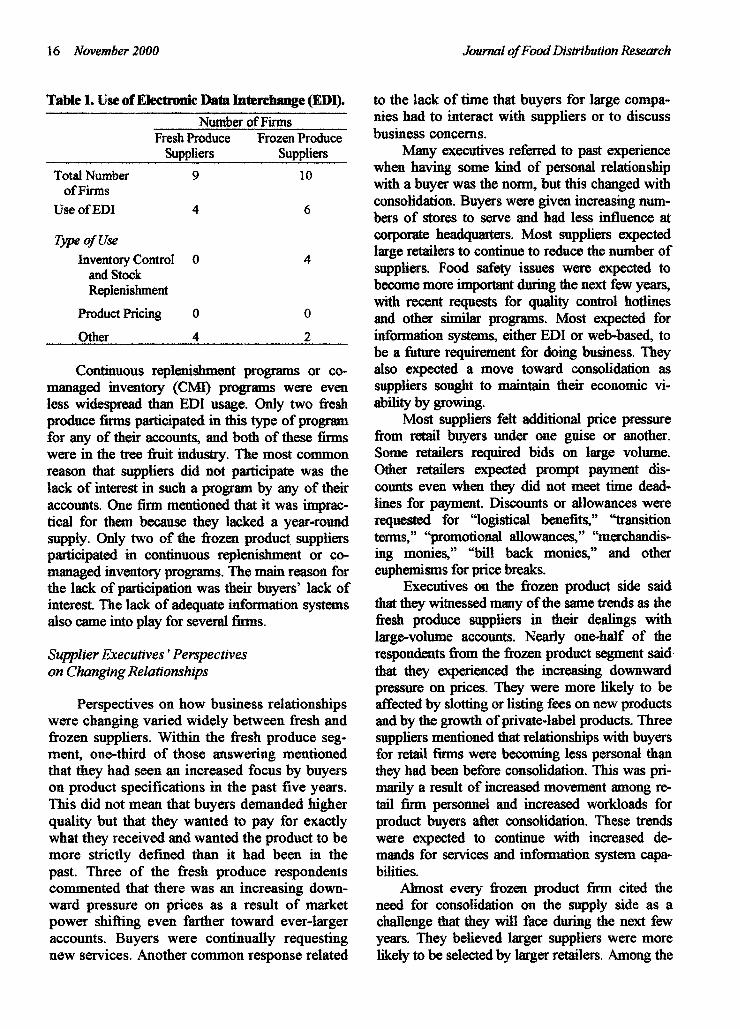

Electronic Data Interchange (EJX) was be-ing utilized within the fkesh produce industry,but it was not filly integrated into the businesspractices of any one firm (see Table 1). Althoughfour of the nine interviewed fms used EDI insome way, none used it for inventory control,stock replenishment programs, or pricing, Twofirms used their EDI systems for invoicing andanother firm used EDI only for automatic depos-its. The systems seemed to lack the true inter-change concept. The number of buyers withwhom fresh produce suppliers interfaced via EDIwas very low, but the accounts tended to havelarge volumes. Several of the firms that did notuse an EDI system claimed that working soft-ware was not yet available. The lack of a stan-dard EDI software system that would be used byall the major retailers has potentially damagedsmall and medkun-volume suppliers. A standardsystem would create a positive network external-ity and enable a supplier to use the same EDIsoftware to interact with more than one retailer.This would eliminate some of the bargainingpower that the retailers gain when suppliers in-vest in gaining expertise in a particular EDIsofkire system and/or the purchase of specificsoftware.

EDI usage among fkozen product supplierswas both Wore common and more advanced (seeTable 1), However, these firms were aiso, on av-erage, 10 times larger than the fresh produce sup-pliers who were interviewwl. Six firms had fimc-tiOd S@eJllS, and four OfthOSefirms used themfor inventory control and stock replenishment.None of the questioned firms used EDI for anyform of product pricing, but one firm used it toreceive confhmation of receipt of inbound productby forward warehouses. Several of the firms thatdid not use a true EDI system at the time of thesurvey were in the proms of acquiring one. Sev-eral of the firms that already had a system in placeadmitted that their systems were not yet fully op-erational. Of the frozen product EDI users, EDIwas being used with anywhere from 2 percent to90 percent of their customers.

16 Novernber2000 Jourrud of Food Di*”bution Research

Table 1. Use of Electronic Data Interchange (EIM).

Numberof FirmsFreshProduce FrozenProduce

SuppIiers suppliers

TotalNumber 9 10of Firms

Use of EDI 4 6

TW of Use

InventoryControl O 4and StockRepkmishment

ProductPricing O 0

Other 4 2

Continuous replenishment programs or co-managed inventory (CMI) programs were evenless widespread than EDI usage. Only two fleshproduce &ms participated in this type of programfor any of their acoounts, and both of these firmswere in the tree fit industry. The most commonreason that suppliers did not participate was thelack of interest in such a program by any of theiraccounts. One firm mentioned that it was imprac-tical for them because they lacked a year-roundsupply. Only two of the frozen product suppliersparticipated in eontiuuous replenishment or co-managed inventory programs. The main reason forthe lack of participation was their buyers’ lack ofinterest. The lack of adequate information systemsalso came into play for several firms.

Supplier Executives’ Perspectiveson Changing Relationships

Perspectives on how business relationshipswere changing varied widely between fresh andfrozen suppliers. Within the tlesh produce seg-ment, one-third of those answering mentionedthat they had seen an increased focus by buyerson product specifications in the past five years.This did not mean that buyers demanded higherquality but that they wanted to pay for exactlywhat they received and wanted the product to bemore strictly defined than it had been in thepast. Three of the fresh produce respondentscommented that there was an increasing down-ward pressure on prices as a result of marketpower shifting even farther toward ever-largeraccounts. Buyers were continually requestingnew services. Another common response related

to the lack of time that buyers for large compa-nies had to interact with suppliers or to discussbusiness concerns.

Mauy executives referred to past experiencewhen having some kind of personal relationshipwith a buyer was the nom but this changed withconsolidation. Buyers were given increasing num-bers of stores to serve and had less influence atcorporate headquarters. Most suppliers expectedlarge retailers to continue to reduce the number ofsuppliers. Food @&y issues were expected tobeeome more important during the next few year%with recent requests for quality control hotlinesand other similar programs. Most expected forinformation systems, either EDI or web-based tobe a fhture requirement for doing business. Theyalso expected a move toward consolidation assuppliers sought to maintain their economic vi-abiity by growing.

Most suppliers felt additional price pressurefrom retail buyers under one guise or another.Some retailers required bids on Iarge volume.Other retailers expeeted prompt payment dis-counts even when they did not meet time dead-lines for payment, Discounts or allowances wererequested for “logistical benefits,” %msitionterms~’ “promotional allowances,” “merchandis-ing monies,” “bill back moniesfl and othereuphemisms for price breaks.

Executives on the frozen product side saidthat they witnessed many of the same trends as thefresh produce suppliers in thek dealings withlarge-volume accounts. Nearly one-half of therespondents from the frozen product segment saidthat they experienced the increasing downwardpressure on prices. They were more likely to beaffected by slotting or listing fbes on new produetsand by the growth of private-label products. Threesuppliers mentioned that relationships with buyersfor retail firms were becoming less personal thanthey had been before consolidation. This was pri-marily a result of increased movement among re-tail firm personnel and increased workloads forproduct buyers after consolidation. These trendswere expected to continue with increased de-mands for services and information system capa-bilities.

Almost every frozen product firm cited theneed for consolidation on the supply side as achallenge that they will face during the next fewyears. They believed larger suppIiers were morelikely to be selected by larger retailers. Among the

MX%&ey, J J andA. 11.0 ‘Rourke . . . Produce Supp@Firms and Re@ilers in the Nw Food Supply Chain 17

strategies being considered were expansionthrough internal growth or merger and buildingalliances with related firms in other regions. Someconcentration has already occurred in the produceind~. As Epperson and Estes (1999) pointedout the U.S. produce industry has moved to amore integrated structure with joint partnershipsand St@OgiC flhYMf3S.

Results of Retailer Interviews

Supplier Preferences

Two of the retailers prefiied to maintain amix of small and medium-sized firms among theirfit and vegetable suppliers. The desirability ofVdOI COE@itiOQ flexibility, and the @ty tO

mwt consumer demands were reasons given for themix prei%rence.One firm had no vendor size pref-erence, as long as the supplier was flexible andcould meet retailer and consumer needs and ex-pectations. The fourth respondent stated ~ as alarge retailer, his firm preferred to deal with larger,more .staMe suppliers. All respondents stated thatproduct quality aud value were foremost criteria inchoosing and maintaining vendors. Some retailerslimited the percent of an individual supplier’s vol-ume that they would purchase to minimim “domi-nant customef’ issues.

Multi-product-line mppliers were preferredby three of the four retailers to reduce logisticaland transportation costs. One respondent believedthat each item should stand on its own merits andon consumer demand regardless of size or type ofsupplier. Two retailers prefamd to deal with localsuppliers in their fit and vegetable procurementmixe% the other two indicated no preference be-tween local and national suppliers.

Ordertng, Delivery, and Stock Replenishment

Most orders were placed with suppliers sevento 14 days before delivery was required. Someorders for processed products were placed as longas two months before delivery. Longer lead timesexisted for imported items than for domesticproducts. Most fit and vegetable items were de-livered to retailer distribution centers, with a verylimited amount of direct-store delivery allowed orrequired. None of the retailers had store-levelstock replenishment programs for f!keshor proc-essed fruits and vegetables nor did they anticipate

the implementation of such programs in the fore-seeable tie.

Although delivery of fbll truckloads of prod-ucts to distribution centers was generally pre-fm~ the balance between volume, price, andcost of service was most important. Two retailersentertained proposals from suppliers and chose thebest combination of price, delivery, and promo-tional support, Delivery frequency requirementsdepended upon the product with adequate leadtimes being most important. One or two deliveriesper week to distribution centers were common.Some retailers had penalty schedules fm late de-liveries with exceptions for unusual circum-stances, such as weather delays. Other retailersrequired late suppliers to deliver directly to stores;they would drop a vendor for chronically late de-liveries.

Only a few specialty items were purchasedthrough independent wholesalers. Brokers wereless important as a source of hit and vegetableproducts than they had been in the past for two ofthe respondents. The others indicated no change inthe importance of brokers during the past threeyears, but the number of brokers had declined sig-nificantly.

Supplier Selection, Purchase Agreements,and Payment Terms

All surveyed retailers purchased their hitand vegetable products from prequalified sup-pliers on approved vendor lists, Suppliers werechosen from the lists to til specMc purchase or-ders. Bids or proposals were invited from ap-proved vendors. For the majority of retailersmost price-competitive bids were negotiatedfrom among the suppliers willing to meet prod-uct and packaging specifications; one or morevendors were selected to meet the retailer’s totalvolume requirements.

Considerable variation existed among inter-viewed retailers in the use of contracts and spottransactions in their hit and vegetable pur-chases. Spot purchases were more prevalent forfresh fruits and vegetables than for frozen andcanned products. The larger the retail organiza-tio~ the greater its use of contracts and thelonger the contract period for processed fruitsand vegetables.

Retailer payment terms offered to vendors forfruit and vegetable purchases were net 21-30

18 November 2000 .lournalof FdDistribution Research

days, with a 2-percent discount for paymentwithin 10 days. One retailer tied payment dis-counts to the use of electronic fund transfer ar-rangements with vendors.

Slotting Fees and Promotional Support

New suppliers to all but one surveyed retailerwere required to pay slotting fees for seller-brand@ processed tit and vegetable items.These fms ranged fiorn $1,000 to $8,000 per item(nornudly an SKU) per store unit. The larger re-tailers generally charged the highest amounts paitem. Private-1abel iterns and fresh produce gener-ally were exempt from slotting fees; however,some retailers were considering a broadw appli-cation of slotting fees in the fbture, with suppliersof brauded fresh produce items as likely candi-dates.

AU retailers encouraged suppliers to conductor support in-store demonstrations and productsampling, especially for new items. All respon-dents also worked with indushy groups to pro-mote fresh fruits and vegetables through point-of-sale materials and product stickers. Some retailersalso worked with these industry groups on coop-erative media advertising campaigns.

EDI Stock Replenishment Programsand Other Management Tools

All respondents planned to use EDI more ex-tensively in the future, but only one of four retailersplanned to experiment with an automatic restock-ing progr~ at the ditibution center leve~ forshelf-stable items. None of the retailers envisioneda filly integrat~ electronically link~ store-levelstock repknishment system with their fresh orprocessed fit and vegetable suppliers.

Retailers were asked about their plans toutilize other EDI-related management tools orconcepts in the foreseeable fiture. One companyplanned to move ahead with a more extensiveECR system by developing finther electronic linkswith suppliers throughout the supply chain. Theother respondents did not have plans to developiidly integrated electronic links with vendors.Two retailers pkumed to increase their focus oncategory management, and two respondentsplanned to fhrther develop activity-based costing,working with suppliers to identifi and eliminateunnecessary costs in the procurement process.

Market Strategies

Both suppliers and retailers agreed that logis-tical efficiency was a must. They were realigningtheir warehouses and distribution centers to re-duce inventory and to speed up responsiveness.Deadlines for delivery times and penalties for latedeliveries were universal. Intenned.kies, such asbrokers and wholesal~ were being bypassedmore frequently, however, the seamless supplychain envisaged under ECR was still, at best, awork in progress and was ovemated as a source ofincreased food system efficiency. Stock replen-ishment was still not widespread. EDI was usedonly by some retailers and suppliers, and wasmostly used far below its Ml potential, although ittended to be used more for larger accounts. In-compatible technology was blamed for much ofthe delay, but there was also considerable am-bivalence about the fhture role of EDI as moreand more fkms moved to web-based cmmmmica-tion systems. However, most suppliers and retail-ers expected to move ahead with EDI, EC~ cate-gory management and activity-based costing on aselective basis.

Both retailers and suppliers recognized theimportance of joint efforts in advertising pro-moting, merchandising, and food product demon-strations. Suppliers accepted the fact that they, ortheir promotional agencies would need to providefimds for such efforts as part of the normal proc-ess of doing business.

Fresh produce handlers and processors saidthat Pacific Northwest produce firms had a num-ber of advantages to oflbr in dealing with chang-ing situations. Most provided the year-round sup-ply and consistently high-quality produce that re-tailers wanted. These firms saw themselves asflexible and service-oriented. Among the chal-lenges for small and medium-volume supplierswere buyers’ high expectations (which were ofhmperceived as unrealistic by suppliers), capital de-mands, capacity, cost contro~ and niche develop-ment for value-differentiated produce.

Suppliers of frozen products felt that theycould offer large buyer flexibility, an expandedproduct line, financial stabiSity, and customerservice. Several of the firms had brands, whichthey believed to offer retailers increased catego~sales and consistently strong margins. Some sup-pliers had niche products that they thought wouldkeep buyers loyal.

McCluskey, J J andA. D. O ‘Rourke . . . Produce Supply Firms and Retailers in the New Food Supply Chain 19

The retailers also saw advantages- htcltid-ing flexibility, ability to react quickly, local orregional presence, competition for larger suppli-ers, service orientation lower overhead costs, andsupply reliability-in buying from small and me-dium-sized vendors. However, the retailers alsonoted several challenges that small and medium-sized companies would face and would need toovercome in order to remain viable fit andvegetable suppliers. These challenges includedcompetition with larger competitors on the basisof price per unit and product quality; limitedcapital for upgrading facilities and technology;payment of slotting on products for which retail-ers require it development and maintenance oftechnical expertise to meet food safety require-ments; difficulty in creating consumer demandand awareness for their branded products throughmedia advertising; and supply of a large enoughmix of items to meet retailer needs, especially as apart of promotional campaigns.

Small suppliers will have difficulty inmatching the prices of larger suppliers, in ac-quiring the capital needed to upgrade their facili-ties and technology, in meeting new demands ofthe systenq such as those relating to food safety,and in competing in branded advertising. Whilemost buyers and suppliers expected to moveahead with EDI and other initiatives, there wasno consensus as to how widely within the systemor how rapidly any supply-chain managementconcepts would be implemented. Suppliers needto be prepared to understand these initiatives andto impIement tha if required by key customers.Small and medium-sized suppliers should pushcollectively for a standardization of EDI soilwaresystems.

As noted by Ricks, Woods, and Stern (1999),many analysts call for grower-shipper firms toform marketing and distribution alliances in or-der to survive; however, they argued that coordi-nation over many small fms was generally dif-ficult to achieve. Given the retailer attitude re-vealed by our survey, smaller produce supplyfirms may be under strong pressure to find waysto overeome these difficulties and to form alli-ances in order to stay competitive in the newfood Supply chain.

Conclusions

Whether retailers are local, regional, or na-tional, they need reliable suppliers, quality prod-ucts, marketing assistance, timely and accurateinformatio~ and efficient logistics in order to at-tract and retain customers. Suppliers and retailerswho work together effectively to ensure consumersatisfaction will emerge as winners, even as thesupply chain evolves. Opportunities exist forsmall and medium-sized fruit and vegetable sup-pliers to sell products to large food retail custom-ers operating in the Pacific Northwest andthroughout the United States. Indeed major retail-ers want to keep suppliers of all sizes on their ap-proved vendor lists; however, retail chain re-quirements of vendors (including listing fees, foodsafety testing, and use of sophisticated EDI sys-tems) will make it more difficult for small, under-capitalized iirms to compete and survive in a moreconcentrated and sophisticated fmd marketingsystem.

The growing market power of buying entitiesand the shill of bargaining power to the buyers isa major concern to smaller produce supply firms.The retail chains can potentially dictate the termsof all the transactions. To meet the more de-manding requirements of their retail customersand to counter the growing market power of themajor retailers, smaller tit and vegetable suppli-ers will need to (1) better understand how foodsystem demands are changing; (2) push for stan-dardization of EDI software across retailers; (3)consolidate into larger units; and/or (4) form alli-ances with other producers, packers, and proces-sors to achieve critical mass as cost-competitivesuppliers.

References

AP (AssociatedPress).1999.“FTCApprovesKroger’sAc-quisitionofFredMeyer.”Seattle Times. 27May.

Canedy,Dana.1998.%roger to Buy Fred Meyer, CreatingCountry’s Biggest Gnxer.” New York Times on theWeb (Business/Finaacial Desk). 20 October.

Epperson, J.E. and E.A. Estes. 1999. “Frnit and VegetableSupply-Chain Management, innovations, and Comp-etitiveness: Cooperative Regional Research Projeet S-222.” Journal of Food Dism”bution Research.30(3) :3s-43.

20 Noventber2000 Jinwnal ojFoodDistribution Research

Food Institute Report. 1999. Fairlawn, NJ:AmarieanInstituteofFoodDistribution.p. 8.1 February.

Kiag,RobertP. andPaulF. [email protected].“ReengineeringtheFoodSupplyCharnTheECRInitiativein theGro-ceryindustry.”American Journal of Agricultural Eco-nomics. 78(5): 1181–1186.

Kinsey, Jean. 1998. “Concentration of Ownership in FoodRetailing A Review of the Evidence About ConsumerImpact.” Working Paper 98-04, The Retail Food In-dustry Center, UniversityofMinnesota.

Kurt SalmonAssociates,Inc. 1993.“EfficientConsumerResponse,EnhancingConsumerValuein the GroceryIndustry.”GroceryManufacturersof America.

L@ Steve.1998.“Megatrendsand the WashingtonAppleIndustry.”1998hUUd Meeting Proceedings, Wash-ington State Horticultural Association.

MCEVOY,Bruce. 1999. “Wal-Mart’s Superccnter Points toFood Retail Future.” Eurofmit A4agm”ne.March:28-30.

Moriwalci,Lee. 1997.“FredMeyerto Buy QFC.” SeattleTimes. 7 November.

ParkJ.L. and E.W. McLaughlin. 1998.“New Developments inGrueerY Manufacturer and Distributor Mad!@ing Pro-grams: A Survey of U.S. Whoksakrs and Ret&m.”Journal of F& Distribution Research. 29(3):15-23.

Perry, M.K. 1989. “Vertical Integration: Determinants andEffkds; in Handbook of Zndustriai Organization, VOLume I, R Schmalenseeand RD. Willig,eds.NorthHollandAmsterdam.

Ricks, Donald, Timothy Woods, and James Stern. 1999.“Supply Chain Management Improving Vertieal Coor-dination in Fruit Industries.” Journalof Food Distribu-tion Research. 30(3)44-53.

Turcsik, Richard. 1999. “Ripening Nicely.” Supplement toProgressive Grocer. Septembec14-18.

Warner. Geraldine. 2000. “The New Dynamics of Buyingand Selliig.” The Good Fruit Grower. 15 May:27-28.

WilsoLPaulN., GaryD. l%omps~ andRobertaL. Cook.1997.“MotherNature,BusinessStrategy,and FreshProduce.”Choices.FirstQuarteK18-21,24-25.

Zwieba& Elliot. 1999.“ConsolidationContinuesDespiteFTCRoadblocks.”Supermarket News. 27 Dsc:1O-12.