Regulatory Revitalizati on of Indonesia’s … Energy Asia 2010/2_5...Development status &...

18

1 Regulatory Revitalizati on of Indonesia’s Geothermal Program Mike Crosetti 3 November 2010

Transcript of Regulatory Revitalizati on of Indonesia’s … Energy Asia 2010/2_5...Development status &...

1

Regulatory Revitalizati on of Indonesia’s Geothermal Program

Mike Crosetti

3 November 2010

Agenda

• Prevailing framework & Government targets

• Assessment of geothermal resources, costs and regulatory processes

• Policy options to address impediments

2

• Draws on analysis & findings of the on‐going Geothermal Pricing & Policy Study

• Conducted for Indonesia Ministry of Energy & Mineral Resources (MEMR)

• Financed by World Bank/GEF• Views presented here are not necessarily those of the

World Bank or the MEMR

The Government has set ambitious targets for geothermal

• “It is my intention that Indonesia

become the largest user of

geothermal energy [in the world]”. –

President SBY, World Geothermal

Congress 2010

• Current installed capacity is 1,191 MW

• Permen 15/2010 targets 3,967

additional MW of geothermal by end

of 2014– 1,751 MW from existing geothermal

working areas (GWA)

– 2,116 MW from new geothermal working

areas

• Both new and legacy GWA additions

are required to meet targets

3

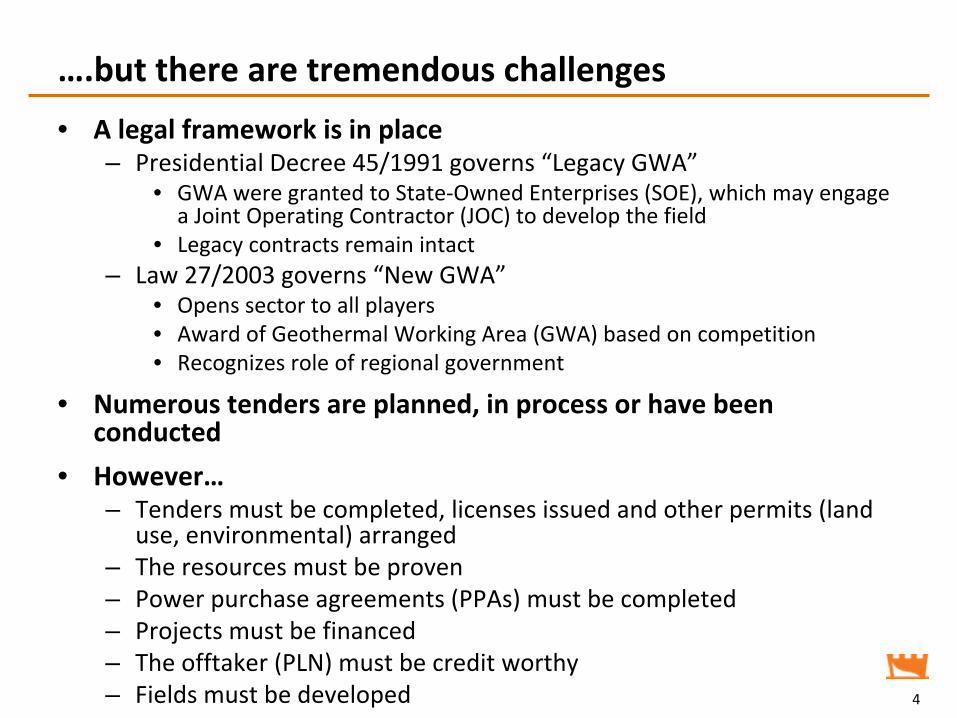

….but there are tremendous challenges

• A legal framework is in place– Presidential Decree 45/1991 governs “Legacy GWA”

• GWA were granted to State‐Owned Enterprises (SOE), which may engage

a Joint Operating Contractor (JOC) to develop the field

• Legacy contracts remain intact– Law 27/2003 governs “New GWA”

• Opens sector to all players• Award of Geothermal Working Area (GWA) based on competition• Recognizes role of regional government

• Numerous tenders are planned, in process or have been

conducted

• However…– Tenders must be completed, licenses issued and other permits (land

use, environmental) arranged

– The resources must be proven– Power purchase agreements (PPAs) must be completed– Projects must be financed– The offtaker (PLN) must be credit worthy– Fields must be developed 4

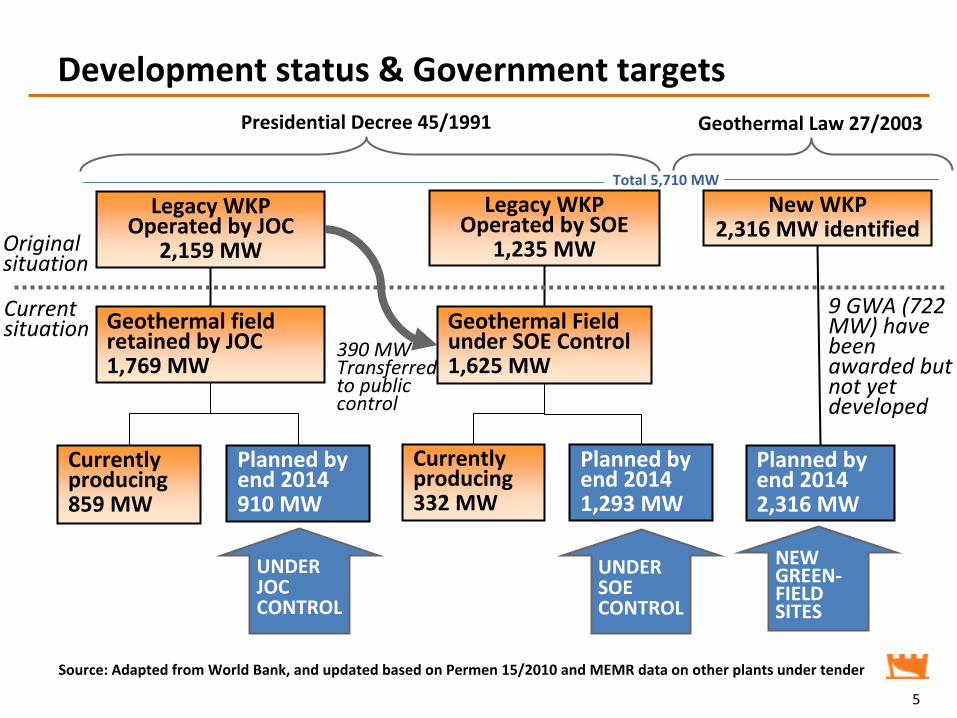

Development status & Government targets

Legacy WKP

Operated by JOC

2,159 MW

Geothermal field

retained by JOC1,769 MW

Currently

producing859 MW

Legacy WKP

Operated by SOE

1,235 MW

New WKP2,316 MW identified

Geothermal Field

under SOE Control1,625 MW

Presidential Decree 45/1991 Geothermal Law 27/2003

Total 5,710 MW

Currently

producing332 MW

Planned by

end 20142,316 MW

UNDER JOC CONTROL

UNDER SOECONTROL

NEW

GREEN‐

FIELD

SITES

Source: Adapted from World Bank, and updated based on Permen 15/2010 and MEMR data on other plants under tender

Original

situation

Current

situation

390 MW

Transferred

to public

control

9 GWA (722

MW) have

been

awarded but

not yet

developed

Planned by

end 2014910 MW

Planned by

end 20141,293 MW

5

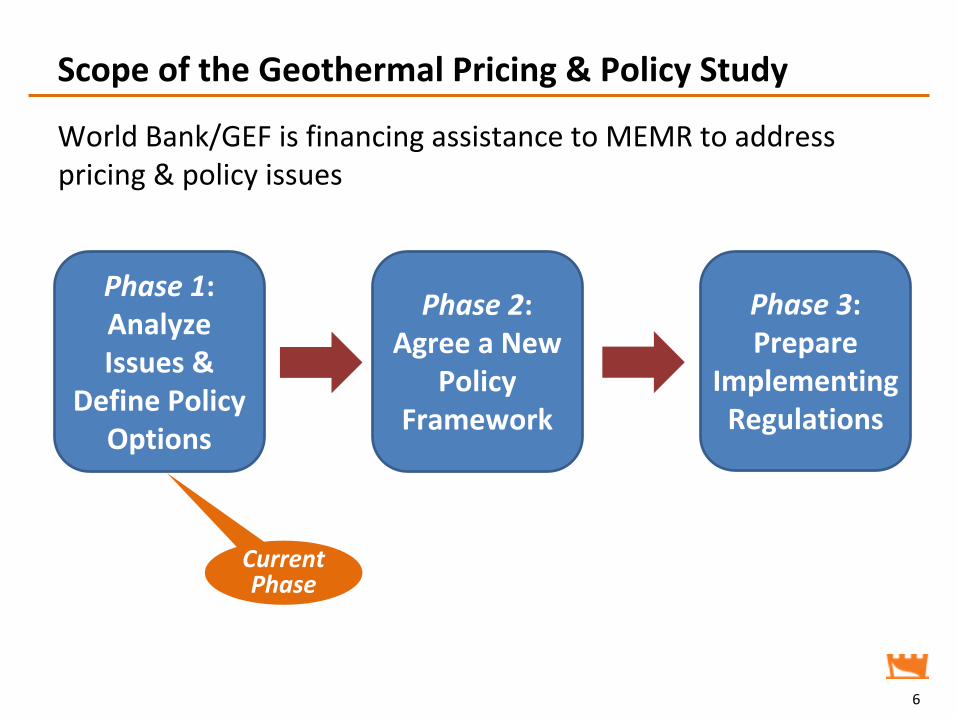

Scope of the Geothermal Pricing & Policy Study

World Bank/GEF is financing assistance to MEMR to address

pricing & policy issues

6

Phase 1:Analyze

Issues &

Define Policy

Options

Phase 2:Agree a New

Policy

Framework

Phase 3:Prepare

Implementing

Regulations

Current

Phase

Principal Activities of Phase 1• Confirm the resources

– “Due diligence”

on Government targets and other estimates– Field‐by‐field review of all available data– Probabilistic approach using “volume method”

• Assess production costs– Financial levelized cost of energy (LCOE) on probabilistic basis– Geothermal and competing conventional technology– Segmentation as a basis for policy formulation

• Identify impediments to development– Stakeholder consultations– Review of laws and regulations

• Define policy, regulatory & pricing options– Risk allocation & mitigation– Compensation– Pricing– Tender process– Targets targets depend on the policies to be adopted

7

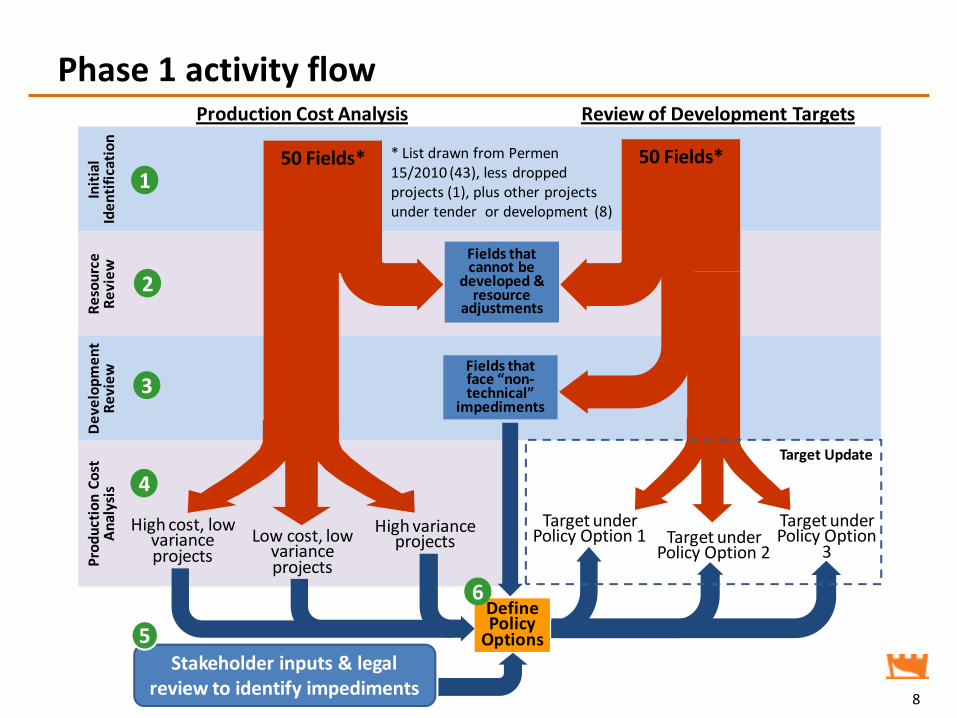

Phase 1 activity flow

8

Production Cost Analysis Review of Development TargetsInitial

Iden

tification

Resource

Review

Develop

men

t Re

view

Prod

uction

Cost

Analysis

50 Fields* 50 Fields*

Fields that cannot be

developed & resource

adjustments

Fields that face “non‐technical”

impediments

* List drawn from Permen15/2010 (43), less dropped projects (1), plus other projects under tender or development (8)

High cost, low variance projects

Low cost, low variance projects

Target under Policy Option 1 Target under

Policy Option 2High variance

projectsTarget under Policy Option

3

Define Policy Options

Target Update

1

4

3

2

6

Stakeholder inputs & legal review to identify impediments

5

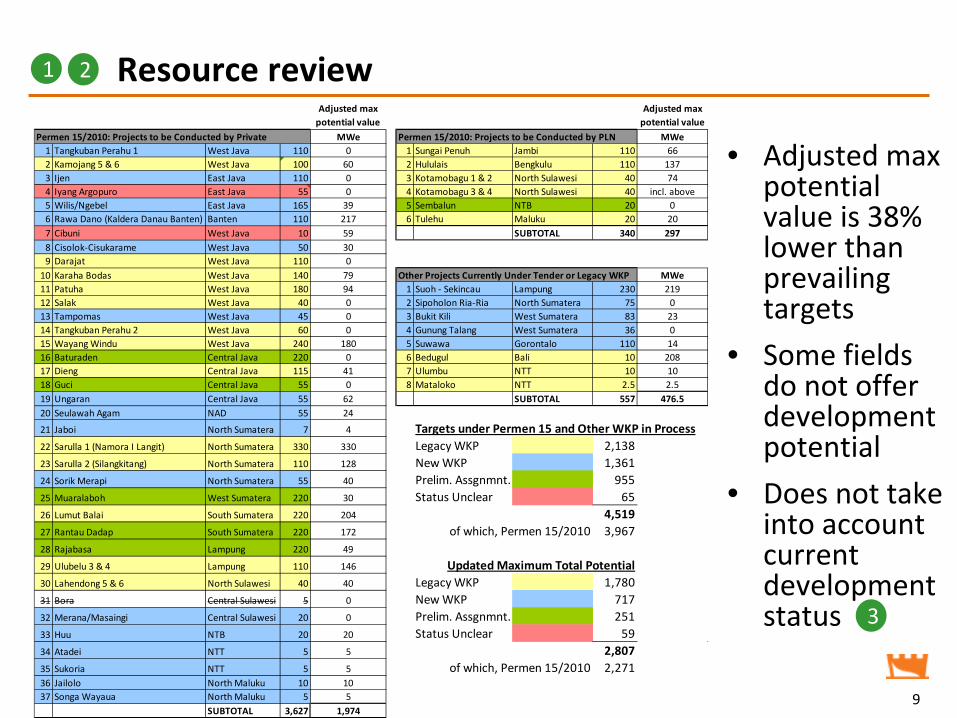

Resource review

• Adjusted max

potential

value is 38%

lower than

prevailing

targets

• Some fields

do not offer

development

potential

• Does not take

into account

current

development

status

9

2

3

1

Adjusted max potential value

Adjusted max potential value

Permen 15/2010: Projects to be Conducted by Private MWe Permen 15/2010: Projects to be Conducted by PLN MWe1 Tangkuban Perahu 1 West Java 110 0 1 Sungai Penuh Jambi 110 662 Kamojang 5 & 6 West Java 100 60 2 Hululais Bengkulu 110 1373 Ijen East Java 110 0 3 Kotamobagu 1 & 2 North Sulawesi 40 744 Iyang Argopuro East Java 55 0 4 Kotamobagu 3 & 4 North Sulawesi 40 incl. above5 Wilis/Ngebel East Java 165 39 5 Sembalun NTB 20 06 Rawa Dano (Kaldera Danau Banten) Banten 110 217 6 Tulehu Maluku 20 207 Cibuni West Java 10 59 SUBTOTAL 340 2978 Cisolok‐Cisukarame West Java 50 309 Darajat West Java 110 010 Karaha Bodas West Java 140 79 Other Projects Currently Under Tender or Legacy WKP MWe11 Patuha West Java 180 94 1 Suoh ‐ Sekincau Lampung 230 21912 Salak West Java 40 0 2 Sipoholon Ria‐Ria North Sumatera 75 013 Tampomas West Java 45 0 3 Bukit Kili West Sumatera 83 2314 Tangkuban Perahu 2 West Java 60 0 4 Gunung Talang West Sumatera 36 015 Wayang Windu West Java 240 180 5 Suwawa Gorontalo 110 1416 Baturaden Central Java 220 0 6 Bedugul Bali 10 20817 Dieng Central Java 115 41 7 Ulumbu NTT 10 1018 Guci Central Java 55 0 8 Mataloko NTT 2.5 2.519 Ungaran Central Java 55 62 SUBTOTAL 557 476.520 Seulawah Agam NAD 55 24

21 Jaboi North Sumatera 7 4 Targets under Permen 15 and Other WKP in Process22 Sarulla 1 (Namora I Langit) North Sumatera 330 330 Legacy WKP 2,13823 Sarulla 2 (Silangkitang) North Sumatera 110 128 New WKP 1,36124 Sorik Merapi North Sumatera 55 40 Prelim. Assgnmnt. 95525 Muaralaboh West Sumatera 220 30 Status Unclear 6526 Lumut Balai South Sumatera 220 204 4,51927 Rantau Dadap South Sumatera 220 172 of which, Permen 15/2010 3,96728 Rajabasa Lampung 220 49

29 Ulubelu 3 & 4 Lampung 110 146 Updated Maximum Total Potential30 Lahendong 5 & 6 North Sulawesi 40 40 Legacy WKP 1,78031 Bora Central Sulawesi 5 0 New WKP 71732 Merana/Masaingi Central Sulawesi 20 0 Prelim. Assgnmnt. 25133 Huu NTB 20 20 Status Unclear 5934 Atadei NTT 5 5 2,80735 Sukoria NTT 5 5 of which, Permen 15/2010 2,27136 Jailolo North Maluku 10 1037 Songa Wayaua North Maluku 5 5

SUBTOTAL 3,627 1,974

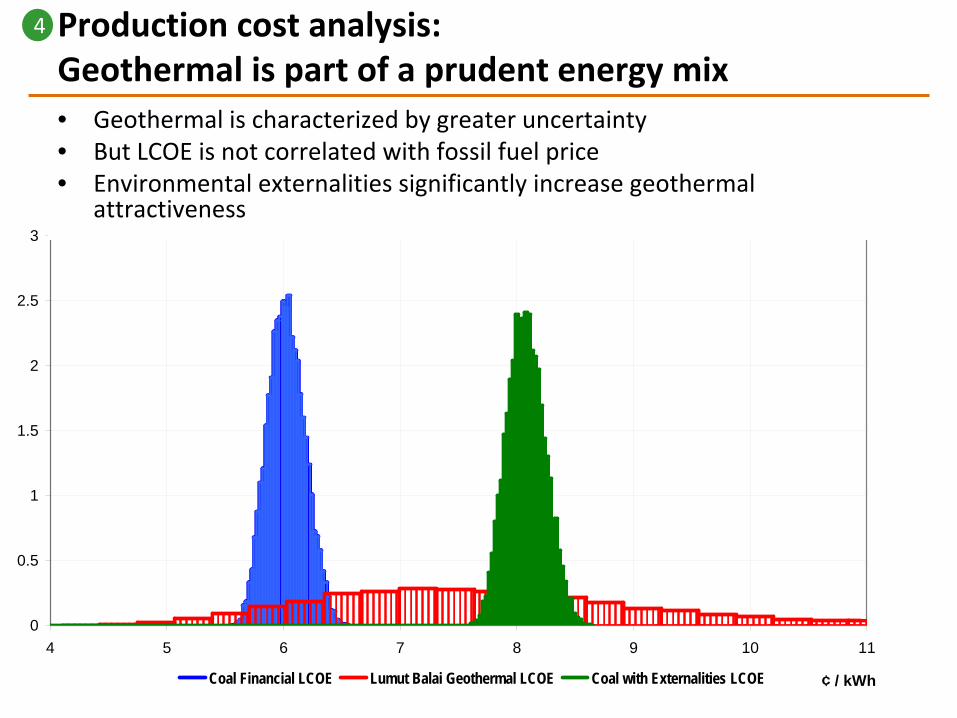

Production cost analysis: Geothermal is part of a prudent energy mix

10

Sumatera Incremental Generation Cost

0

0.5

1

1.5

2

2.5

3

4 5 6 7 8 9 10 11

¢ / kWhCoal Financial LCOE Lumut Balai Geothermal LCOE Coal with Externalities LCOE

• Geothermal is characterized by greater uncertainty• But LCOE is not correlated with fossil fuel price• Environmental externalities significantly increase geothermal

attractiveness

4

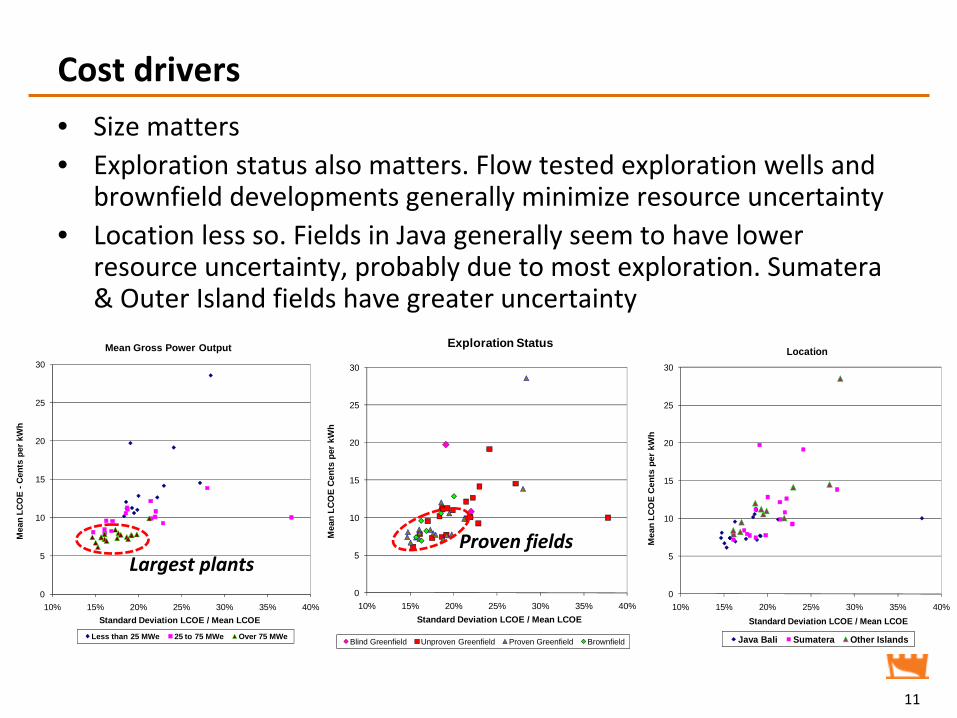

Cost drivers

• Size matters• Exploration status also matters. Flow tested exploration wells and

brownfield developments generally minimize resource uncertainty• Location less so. Fields in Java generally seem to have lower

resource uncertainty, probably due to most exploration. Sumatera

& Outer Island fields have greater uncertainty

11

0

5

10

15

20

25

30

10% 15% 20% 25% 30% 35% 40%

Mea

n LC

OE

-Cen

ts p

er k

Wh

Standard Deviation LCOE / Mean LCOE

Mean Gross Power Output

Less than 25 MWe 25 to 75 MWe Over 75 MWe

0

5

10

15

20

25

30

10% 15% 20% 25% 30% 35% 40%

Mea

n LC

OE

Cen

ts p

er k

Wh

Standard Deviation LCOE / Mean LCOE

Location

Java Bali Sumatera Other Islands

0

5

10

15

20

25

30

10% 15% 20% 25% 30% 35% 40%

Mea

n LC

OE

Cen

ts p

er k

Wh

Standard Deviation LCOE / Mean LCOE

Exploration Status

Blind Greenfield Unproven Greenfield Proven Greenfield Brownfield

Largest plantsProven fields

12Permen ESDM 32/2009

Perm

en ESD

M

11/200

8

Permen ESDM 10/2005Permen ESDM 26/2008

Permen ESDM 11/2009

Perm

en ESD

M 2/200

9

MEMR assigns

preliminary

survey

Firm conducts

preliminary

survey

MEMR

designates GWA

Firm applies for

preliminary

survey

Inputs from

Geological

Agency

Government

Authority

tenders GWA &

awards on price

Power plant

construction

Firm conducts

exploration

Field

exploitation

Firm conducts

feasibility

study

Firm

negotiates

PPA with

PLN

Commercial

operation

Firm applies for

generation license

MEMR

approves

price

5

8

32

1

7

4

6

11

10

9

12

13

Key issues for processing new WKP under Law 27/2003

14

1.

Standards for readiness to tender should be strengthened2.

Limited provision for stakeholder input (“market sounding”)

into project design3.

Lack of rigorous prequalification criteria and use of lowest

price award criteria allows unqualified bidders and winners4.

Lack of pre‐feasibility study precludes government

guarantee, as required by PPP regulations5.

Bid documents do not clarify risk allocation or include draft

PPA. 6.

Capability of tender committee uncertain. 7.

No involvement or commitment from offtaker (PLN). (PP

59/2007 precludes PLN participation on tender committee)8.

Tenders based on preliminary survey awards are not

attracting multiple bidders9.

Project financing may run into bank legal lending limits

10.

Firms will not typically invest in exploratory drilling

prior to PPA. 11.

Relationship between tender price and PLN

negotiation unclear.12.

PLN has disincentive to accept geothermal price

above cost of supply (Perpres drafted to address this)13.

One‐by‐one price negotiations are time consuming14.

Prevailing price cap precludes some economically

justified development

5

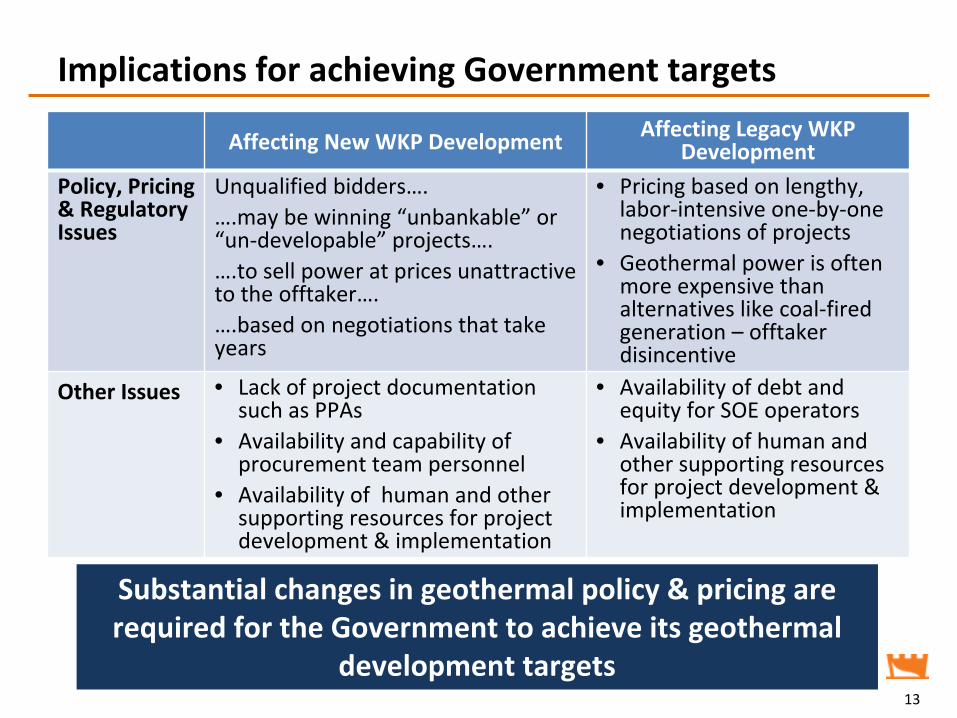

Implications for achieving Government targets

Affecting New WKP Development Affecting Legacy WKP

Development

Policy, Pricing

& Regulatory

Issues

Unqualified bidders….….may be winning “unbankable”

or

“un‐developable”

projects….….to sell power at prices unattractive

to the offtaker….….based on negotiations that take

years

• Pricing based on lengthy,

labor‐intensive one‐by‐one

negotiations of projects

• Geothermal power is often

more expensive than

alternatives like coal‐fired

generation –

offtaker

disincentive

Other Issues • Lack of project documentation

such as PPAs

• Availability and capability of

procurement team personnel

• Availability of human and other

supporting resources for project

development & implementation

• Availability of debt and

equity for SOE operators

• Availability of human and

other supporting resources

for project development &

implementation

13

Substantial changes in geothermal policy & pricing are

required for the Government to achieve its geothermal

development targets

Key Pricing & Policy Issues

• The nature of geothermal power– uncertain– diverse– one size does not fit all

• The need for a compensation mechanism– There is an economic justification for geothermal power

– But prevailing financial cost of geothermal is higher than conventional

alternatives

– Developers need reasonable returns– The offtaker (PLN) does not print money

– Incremental cost must be paid for by some combination of electricity

consumers, Government (taxpayers) and sales of CERs

• Policy & pricing must be explicitly consider risk allocation

• Processes & standards should reflect international practice

14

6

Resource segmentation as an input to policy making• Plants may be characterized by both expected LCOE as well as

uncertainty in LCOE estimates

• Plant size and exploration status can be used for segmentation

15

0

5

10

15

20

25

30

10% 15% 20% 25% 30% 35% 40%

Mea

n LC

OE

US

Cen

ts p

er k

Wh

Std Dev LCOE / Mean LCOE

WKP > 55 MW & Proven WKP<55 MW Other Islands & Proven WKP<55 MW on JB & Proven

WKP<55 MW on Sumatra & Proven Blind or Unproven Greenfields

Large Plant Feed

in tariff for

proven GWA?

GWA requiring

further

exploration?

Small Plant Feed

in tariff for

proven GWA?

Example of how incremental costs could be funded

16

THESE MECHANISMS

ARE NOT MUTUALLY

EXCLUSIVE

Key assumptions:

Total geothermal

installed5000 MW target

CDM Revenue

contribution $10/tCO2 , 0.8 per

kWh emission factor

Mandatory pass‐

through contribution5% rate increase

premium, base of 147 TWh

Green electricity

scheme contribution10% participation rate

of all rate payers, paying full cost of geothermal (147 TWh)

(Rp.467)

(Rp.723) (Rp.78)

(Rp.93)

(Rp.47) (Rp.38)

Source: World Bank

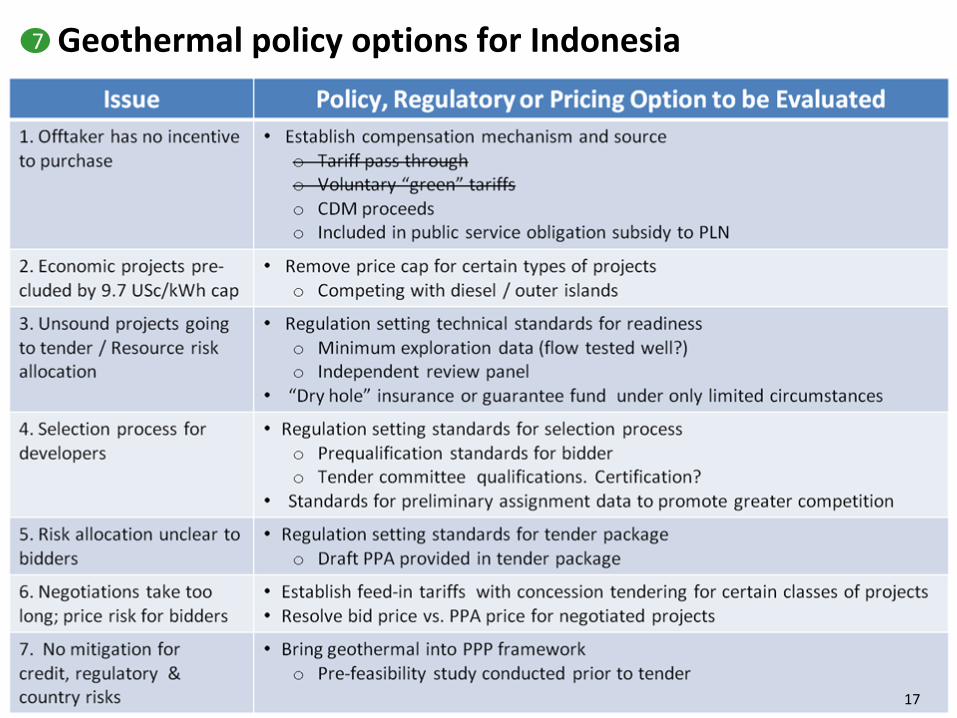

Geothermal policy options for Indonesia

17

7

THANK YOU !

18