REGISTRATION,UPDATES AND CANCELLATION · PDF filedeed of absolute sale, deed of conditional...

48

THRESHOLD AMOUNTS RR 3-2012 1

-

Upload

truongtuyen -

Category

Documents

-

view

220 -

download

1

Transcript of REGISTRATION,UPDATES AND CANCELLATION · PDF filedeed of absolute sale, deed of conditional...

THRESHOLD AMOUNTS

RR 3-2012 1

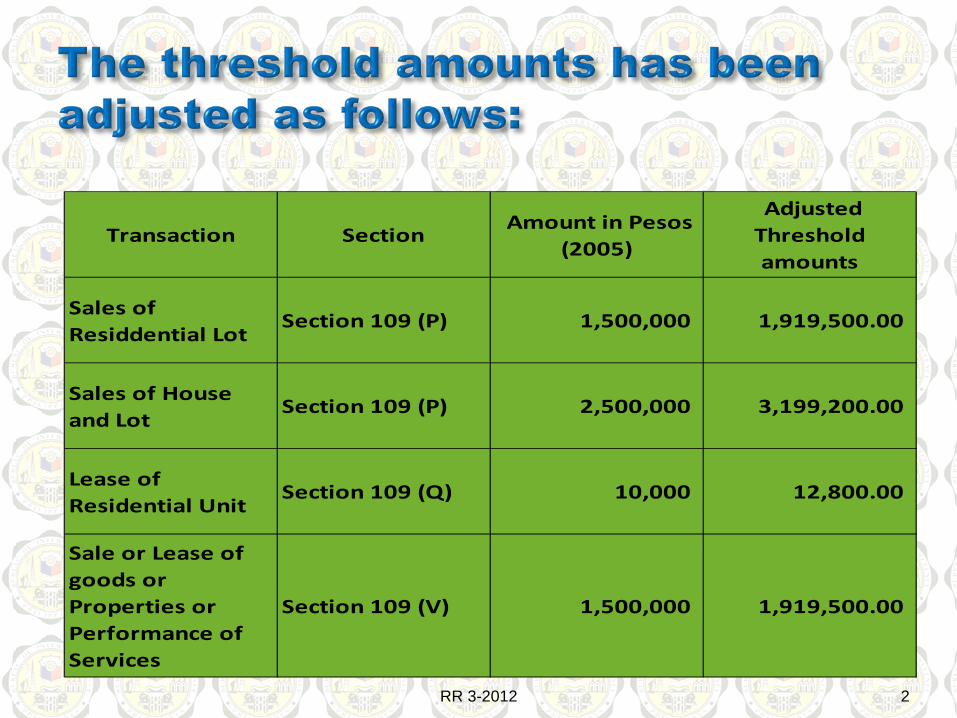

Transaction Section Amount in Pesos (2005)

Adjusted Threshold amounts

Sales of Residdential Lot

Section 109 (P) 1,500,000 1,919,500.00

Sales of House and Lot

Section 109 (P) 2,500,000 3,199,200.00

Lease of Residential Unit

Section 109 (Q) 10,000 12,800.00

Sale or Lease of goods or Properties or Performance of Services

Section 109 (V) 1,500,000 1,919,500.00

RR 3-2012 2

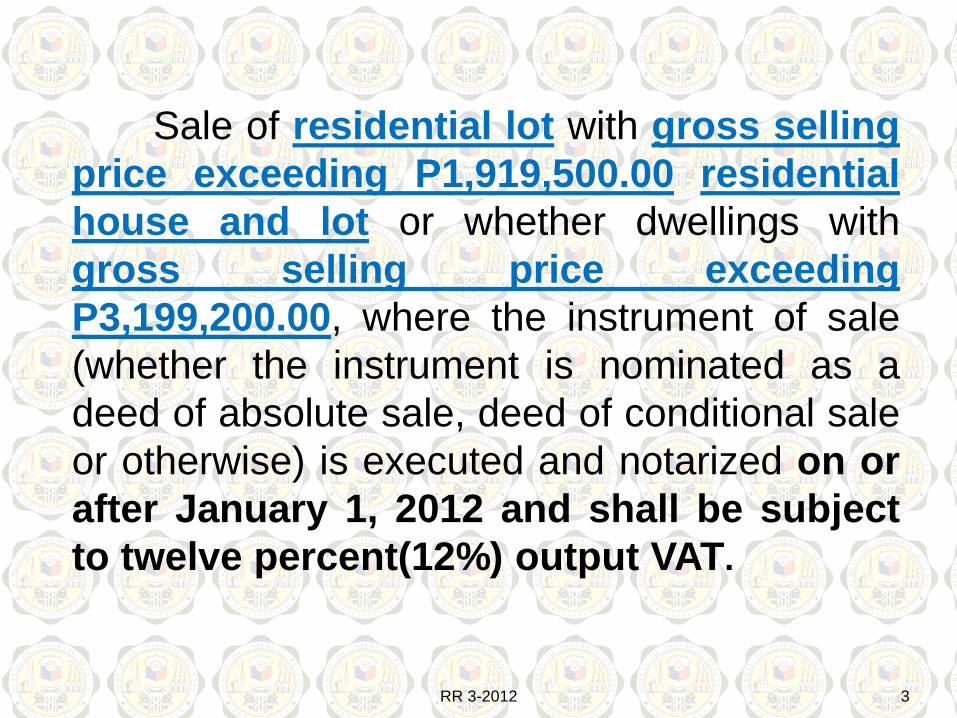

Sale of residential lot with gross sellingprice exceeding P1,919,500.00 residentialhouse and lot or whether dwellings withgross selling price exceedingP3,199,200.00, where the instrument of sale(whether the instrument is nominated as adeed of absolute sale, deed of conditional saleor otherwise) is executed and notarized on orafter January 1, 2012 and shall be subjectto twelve percent(12%) output VAT.

RR 3-2012 3

VAT treatment on Sale of Adjacent Residential Lots, House and Lots or

Other Residential Dwellings.

RR 13-2012 4

It has come to the attention of the Bureauof Internal Revenue that sale to one buyer ofadjacent residential lots, house & lots or otherresidential dwellings like condominium unitswhich are actually being combined andutilized as one residential unit areintentionally being documented as separateunits in order to avoid payment of valueadded tax (VAT) by keeping them below theVAT threshold amount.

RR 13-2012 5

Sale, Transfer or disposal within a 12-monthperiod of two or more adjacent residential lots, houseand lots or other residential dwellings in favor of onebuyer from the same seller, for the purpose of utilizing thelots, house and lots or other residential dwellings as one residentialarea wherein the aggregate value of the adjacent properties exceedsP1,919,500.00, for residential lots and P3,199,200.00 for residentialhouse and lots or other residential dwellings. Adjacent residential lots,house and lots or other residential dwellings although covered by separatetitles and/or separate tax declarations, when sold or disposed to one and thesame buyer, whether covered by one or separate Deed/s of Conveyance.Shall be presumed as a sale of one residential lot, house and lot orresidential dwelling.

This however, does not include the sale ofparking lot which may or not be included in the sale of condominiumunits. The sale of parking lots in a condominium is a separate and distincttransaction and is not covered by rules on threshold amount not being aresidential lot, house & lot & lot or a residential dwelling, thus, should besubject to VAT regardless of amount of selling price.”

RR 13-2012 6

Imposition of DocumentaryStamp Tax on inter-office memocovering ADVANCES GRANTEDby an affiliated corporation

RMC 48-2011 7

Refers to a contract in writingwhere one of the parties delivers toanother money or other consumablething, upon the condition that thesame amount of the same kind andquality shall be paid. The term shallinclude credit facilities, which maybe evidenced by credit memo,advice or drawings.

RMC 48-2011 8

In cases where no formal loanagreements or promissory noteshave been executed to cover creditfacilities, the documentary stamp taxshall be based on the amount ofdrawings or availment of the facilities,which may be evidenced bycredit/debit memo, advice or drawingsby any form of check or withdrawalslip.

RMC 48-2011 9

Applying the aforesaid provisions to thecase at bench, we find that theinstructional letter as well as thejournal and cash vouchersevidencing the advances FDCextended to its affiliates in 1996 and 1997qualified as loan agreementsupon which documentary stamp tax may beimposed. (En Banc Supreme Court Decision in thecase CIR vs. Filinvest Development Corp. G.R. Nos.163653 and 167689 dated July 19, 2011

10

Binding effect of rulings issued prior to Tax Reform Act of 1997

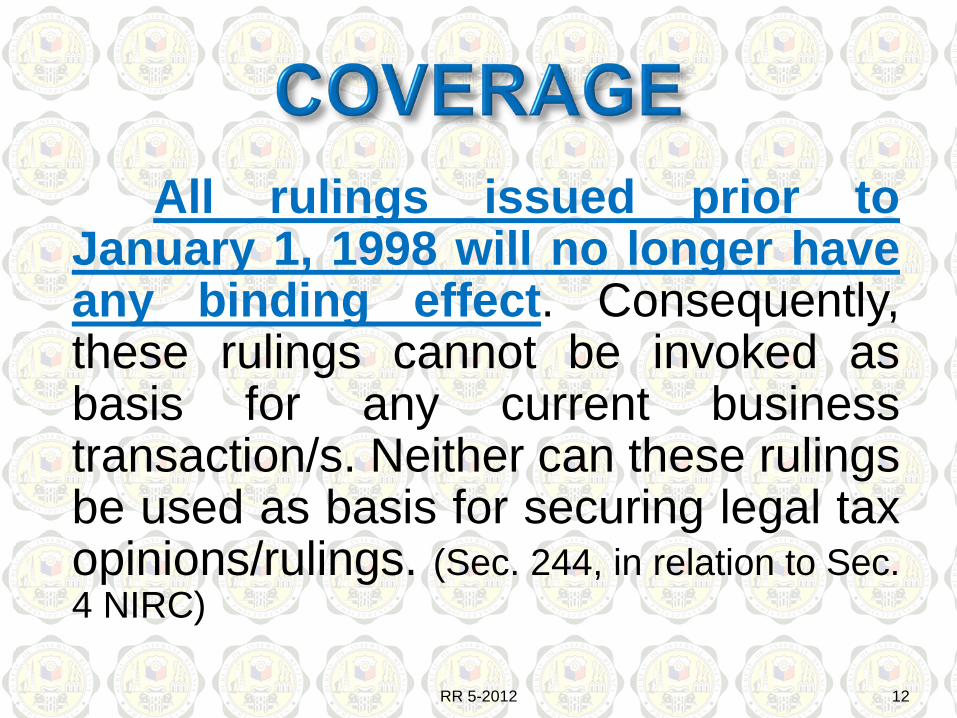

RR 5-2012 11

All rulings issued prior toJanuary 1, 1998 will no longer haveany binding effect. Consequently,these rulings cannot be invoked asbasis for any current businesstransaction/s. Neither can these rulingsbe used as basis for securing legal taxopinions/rulings. (Sec. 244, in relation to Sec.4 NIRC)

RR 5-2012 12

All laws decrees, executiveorders, rules and regulations orparts thereof which are contrary toor inconsistent with this Code areherby repealed, amended ormodified accordingly. (Sec.291- NIRCR.A. 8424 or Tax Reform Act of 1997)

RR 5-2012 13

Clarification on Revenue Regulation No.5-2012

RMC 22-201214

All BIR Rulings issued prior to January 1, 1998 are not be usedas precedent by any taxpayer as a basis to secure rulings forthemselves for current business transaction/s or in support of theirposition against any assessments.

All BIR Rulings issued prior to Jan.1,1998 are not to be used byany BIR action lawyer in issuing new rulings for request forrulings involving current business transaction/s.

However, BIR Rulings issued prior to Jan. 1,1998 remains to be valid but only:

a. To the taxpayer who was issued the ruling;and

a. Covering the specific transaction/s which is the subject of the same ruling

BIR Ruling issued prior to Jan.1, 1998, shall remain valid asmentioned above, unless expressly notified of its revocationor unless the legal basis in law for such issuance has alreadybeen repealed/amended in the current Tax Code.

RMC 22-2012 15

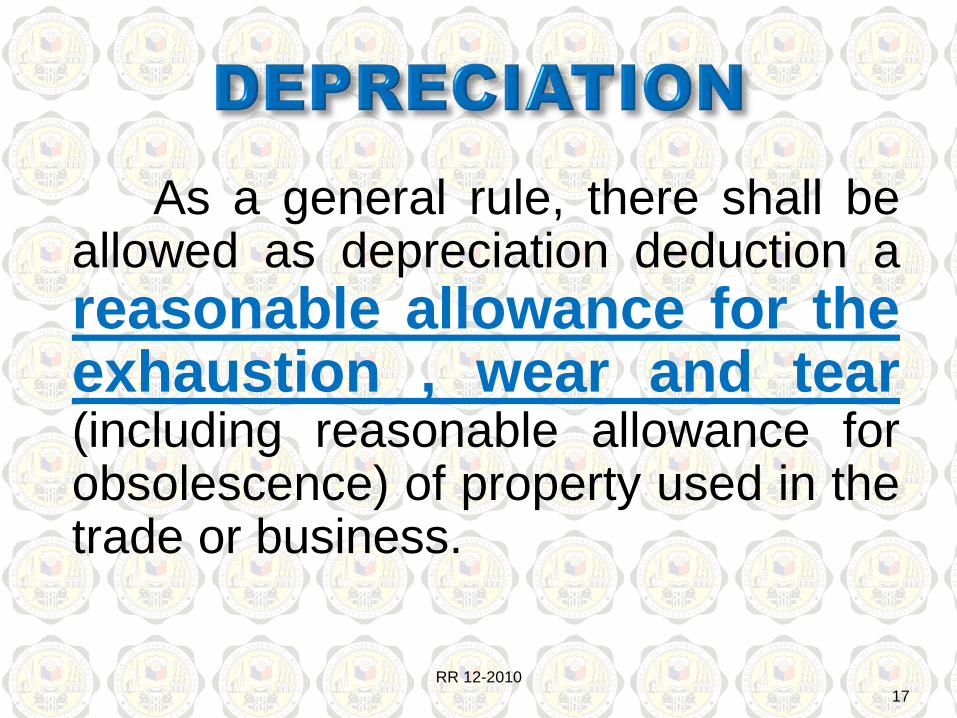

Deductibility of DepreciationExpenses as it Relates toPurchase of Vehicles and otherExpenses Related Thereto, andInput Taxes Allowed Therefor.

RR 12-2010 16

As a general rule, there shall beallowed as depreciation deduction areasonable allowance for theexhaustion , wear and tear(including reasonable allowance forobsolescence) of property used in thetrade or business.

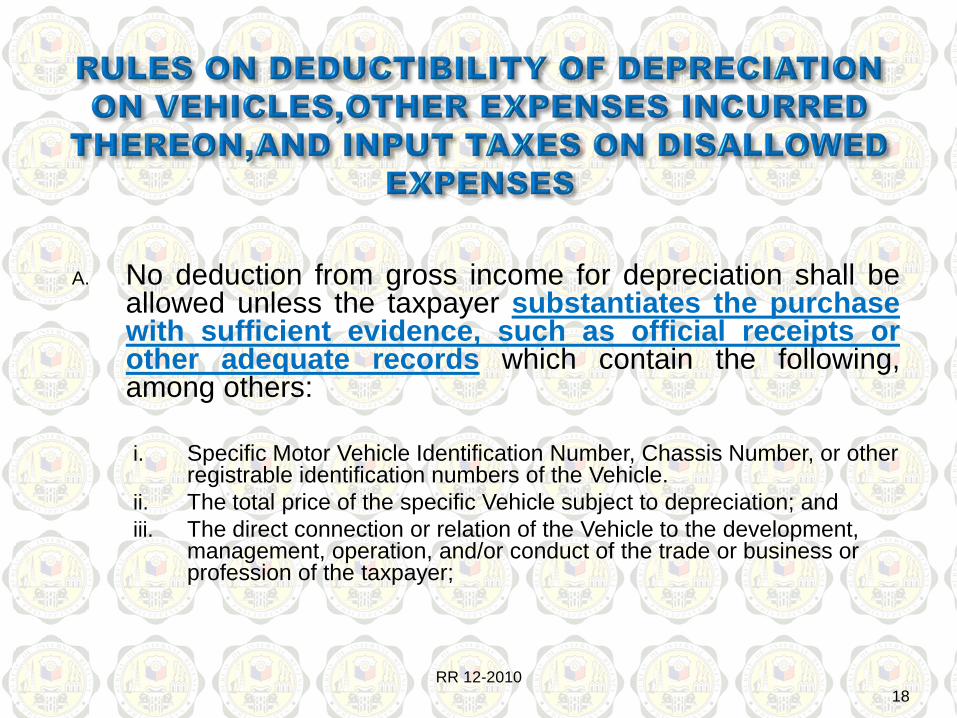

RR 12-201017

A. No deduction from gross income for depreciation shall beallowed unless the taxpayer substantiates the purchasewith sufficient evidence, such as official receipts orother adequate records which contain the following,among others:

i. Specific Motor Vehicle Identification Number, Chassis Number, or other registrable identification numbers of the Vehicle.

ii. The total price of the specific Vehicle subject to depreciation; andiii. The direct connection or relation of the Vehicle to the development,

management, operation, and/or conduct of the trade or business or profession of the taxpayer;

RR 12-201018

B. Only one Vehicle for landtransport is allowed for the useof an official or employee, thevalue of which should notexceed Two Million FourHundred Thousand Pesos(Php2,400,000.00);

RR 12-201019

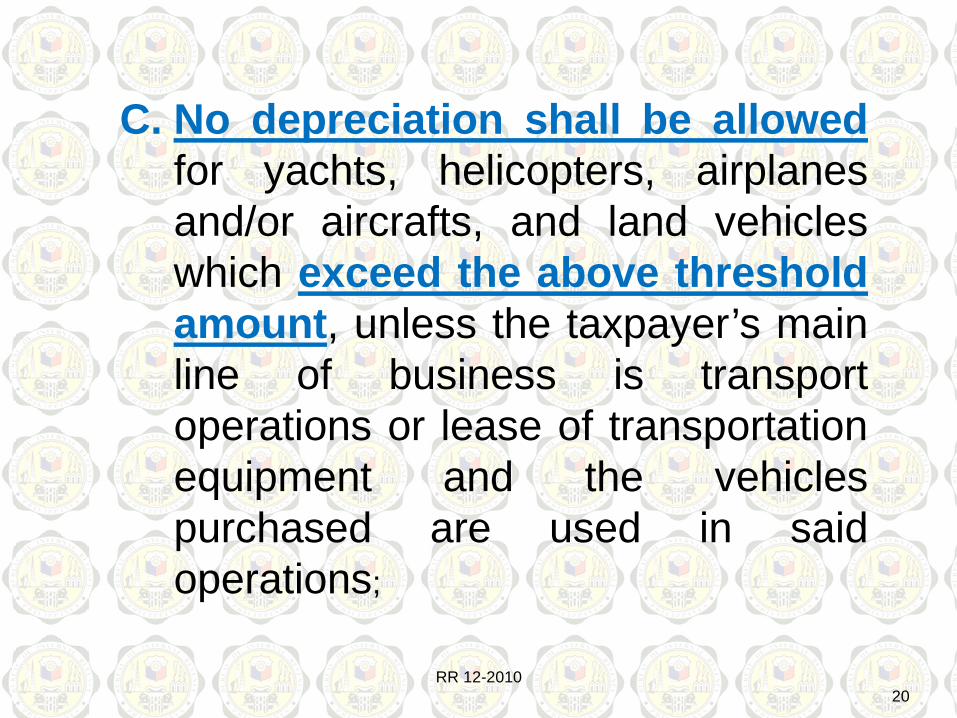

C. No depreciation shall be allowedfor yachts, helicopters, airplanesand/or aircrafts, and land vehicleswhich exceed the above thresholdamount, unless the taxpayer’s mainline of business is transportoperations or lease of transportationequipment and the vehiclespurchased are used in saidoperations;

RR 12-201020

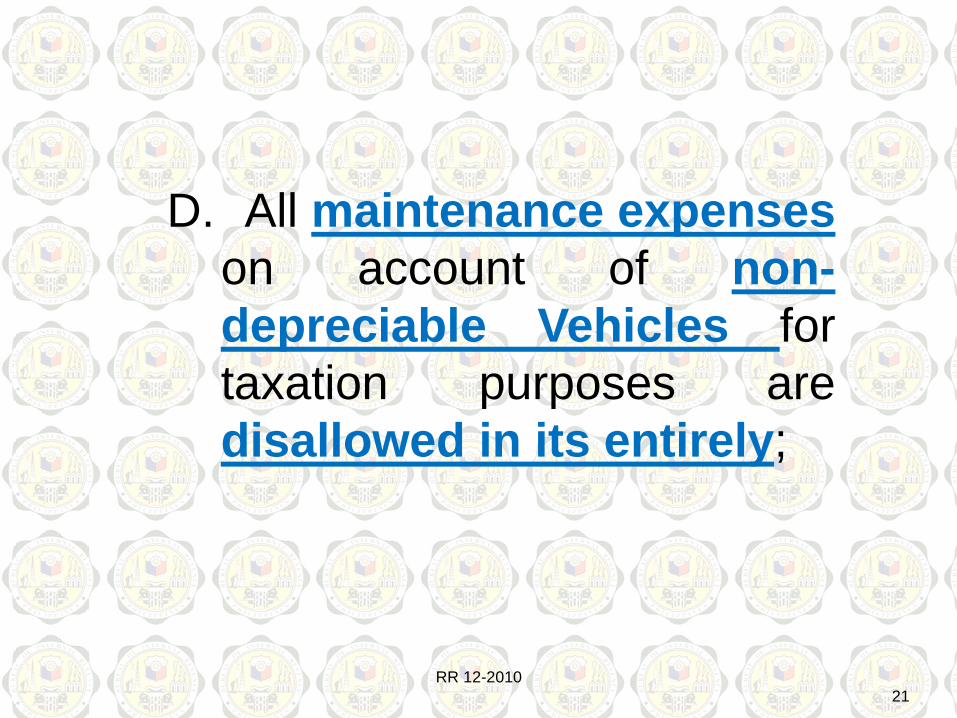

D. All maintenance expenseson account of non-depreciable Vehicles fortaxation purposes aredisallowed in its entirely;

RR 12-201021

E.The input taxes on thepurchase of non-depreciable Vehicles andall input taxes onmaintenance expensesincurred thereon are likewisedisallowed for taxationpurposes.

RR 12-201022

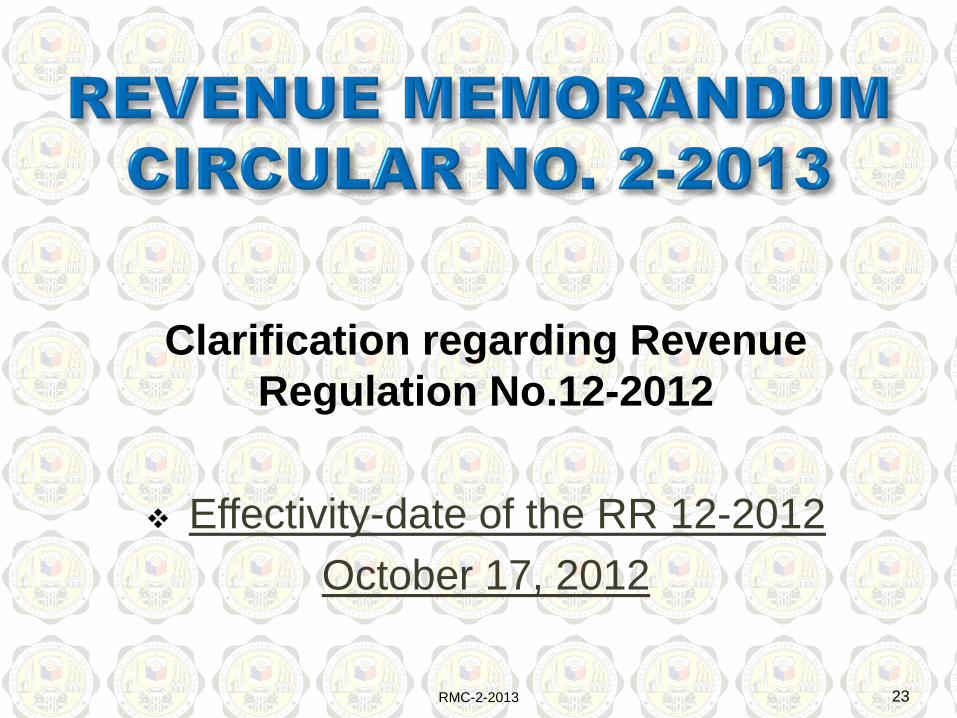

Clarification regarding Revenue Regulation No.12-2012

Effectivity-date of the RR 12-2012 October 17, 2012

RMC-2-2013 23

Does the RR apply to land vehicles purchased priorto its effectivity where the purchased amountexceed the threshold of P2,400,000.00? No. The RR applies prospectively,

thus, it applies to land vehiclespurchased upon its effectivity.

In case the Vehicles (defined in the RR aspassenger vehicles of all type, whether by land,water, or air) which are not allowed depreciationexpense, or the non-depreciable Vehicles, will besold at a loss, will the loss to be incurred from suchsale deductible from gross income? Any loss the will be incurred as a

result of the sale shall NOT be allowedas a deduction.

RMC 2-2013 24

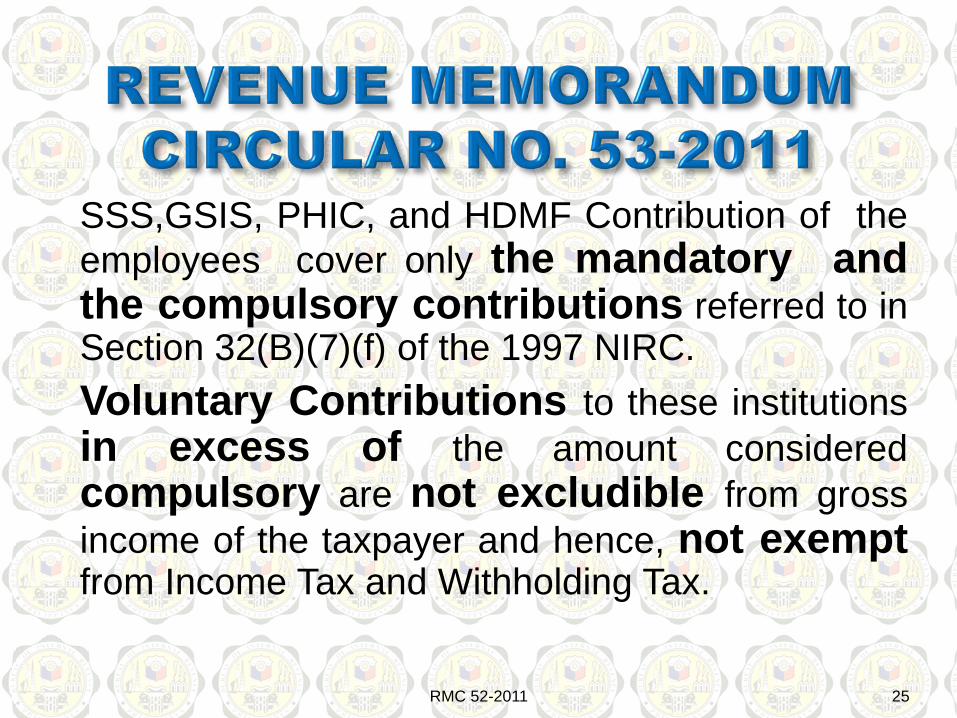

SSS,GSIS, PHIC, and HDMF Contribution of theemployees cover only the mandatory andthe compulsory contributions referred to inSection 32(B)(7)(f) of the 1997 NIRC.Voluntary Contributions to these institutionsin excess of the amount consideredcompulsory are not excludible from grossincome of the taxpayer and hence, not exemptfrom Income Tax and Withholding Tax.

RMC 52-2011 25

Requiring the Mandatory Submission of Quarterly

Summary List of Sales and Purchases (SLSP) by All

VAT Registered Taxpayer.

RR 1-2012 26

“Every payor required to deduct andwithhold taxes under these regulations shallfurnish in triplicate, each payee, whetherindividual or corporate, with a withholding taxstatement, using the prescribed form,(BIRForm No. 2307),showing the income paymentsmade and the amount of taxes withheldtherefrom, for every month of the quarter, withintwenty (20) days following the close of taxablequarter employed by the payee in filing his/itsquarterly income tax return”.

RMC 85-2012 27

The payor should always retain a copy of dulyissued BIR Form No.2307. Failure to furnish the sameshall be a ground for mandatory audit of payor’sincome tax liabilities (including withholding tax)uponverified compliant of the payee.

For final withholding taxes, the statementshould be given to the payee on or beforeJanuary 31 of the succeeding year.

Upon request of the payee, however, the payormust furnish such certificate simultaneously with theincome payment. Section 2.58(B) RR 2-98

RMC 85-2012 28

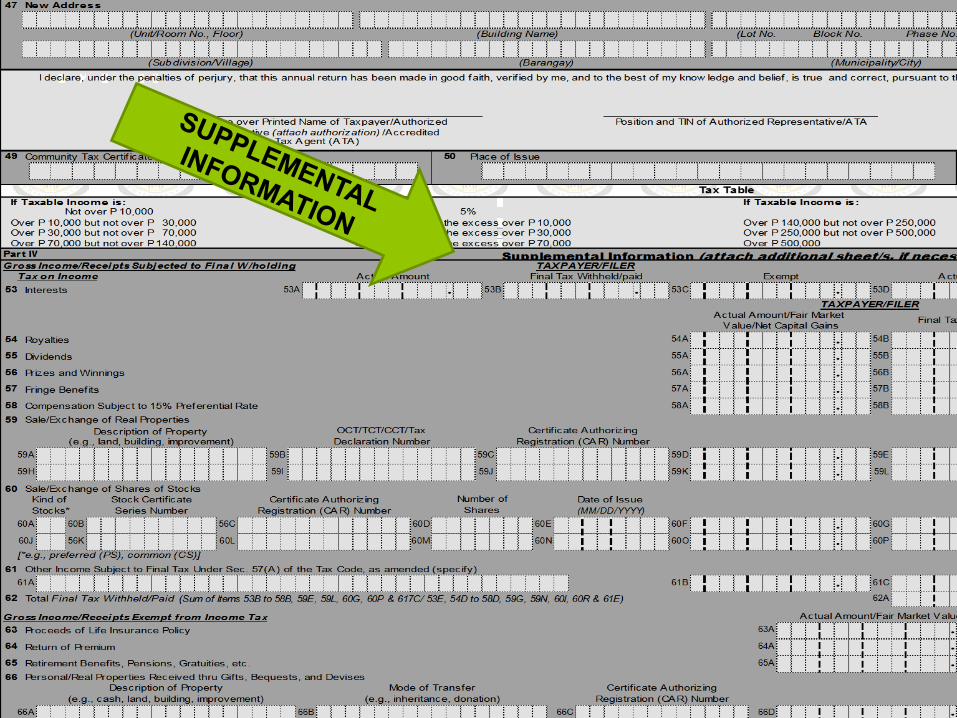

Making the disclosure ofSupplemental Information under BIR FormNos. 1700 and 1701 optional on the part of thetaxpayer for income tax filing covering and startingwith the calendar year 2012.

Starting with the calendar year 2013,the disclosures required under SupplementalInformation portion of the said forms will bemandatory.

RMC 21-2013 29

30

Deleting Section 2.6.1 ofRevenue Regulation 13-2001 which provides thatpenalties and/or interest imposed on the taxpayermay be abated or cancelled on the groundof one date late filing andremittance due to failure to beat thebank cut-off time.

RR 4-2012 31

All Accredited Agent Banks(AABs) are hereby reminded toaccept tax payments on April 6, 2013and April 13, 2013 and extendbanking hours up to 5:00 P.M. forthe period April 1 to 15, 2013 forpurposes of accepting tax payments.

BANK BULLETIN 2013-03 32

RMO 25-2012 33

To ensure strict compliance by taxpayerswith internal revenue laws and regulations, inrelation to requisites of deductibility or certainexpenses and payment of correct income tax,annual income tax returns(ITRs)filed for thecurrent year shall be subject to pre-audit by theRevenue District Offices.

RMO 25-2012 34

Shall cover the pre-audit of all theannual ITRs filed by individualtaxpayers engaged in business or in thepractice of their profession and corporatetaxpayers that are registered in theRevenue District Offices

RMO 25-201235

RMO 25-201236

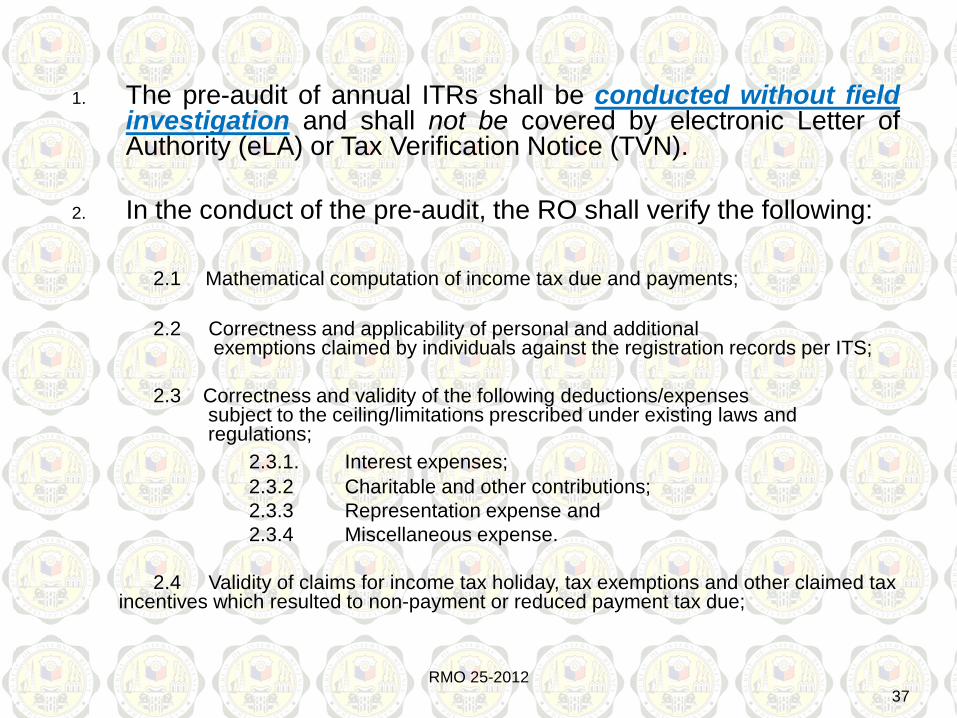

1. The pre-audit of annual ITRs shall be conducted without fieldinvestigation and shall not be covered by electronic Letter ofAuthority (eLA) or Tax Verification Notice (TVN).

2. In the conduct of the pre-audit, the RO shall verify the following:

2.1 Mathematical computation of income tax due and payments;

2.2 Correctness and applicability of personal and additionalexemptions claimed by individuals against the registration records per ITS;

2.3 Correctness and validity of the following deductions/expensessubject to the ceiling/limitations prescribed under existing laws andregulations;

2.3.1. Interest expenses;2.3.2 Charitable and other contributions;2.3.3 Representation expense and2.3.4 Miscellaneous expense.

2.4 Validity of claims for income tax holiday, tax exemptions and other claimed tax incentives which resulted to non-payment or reduced payment tax due;

RMO 25-201237

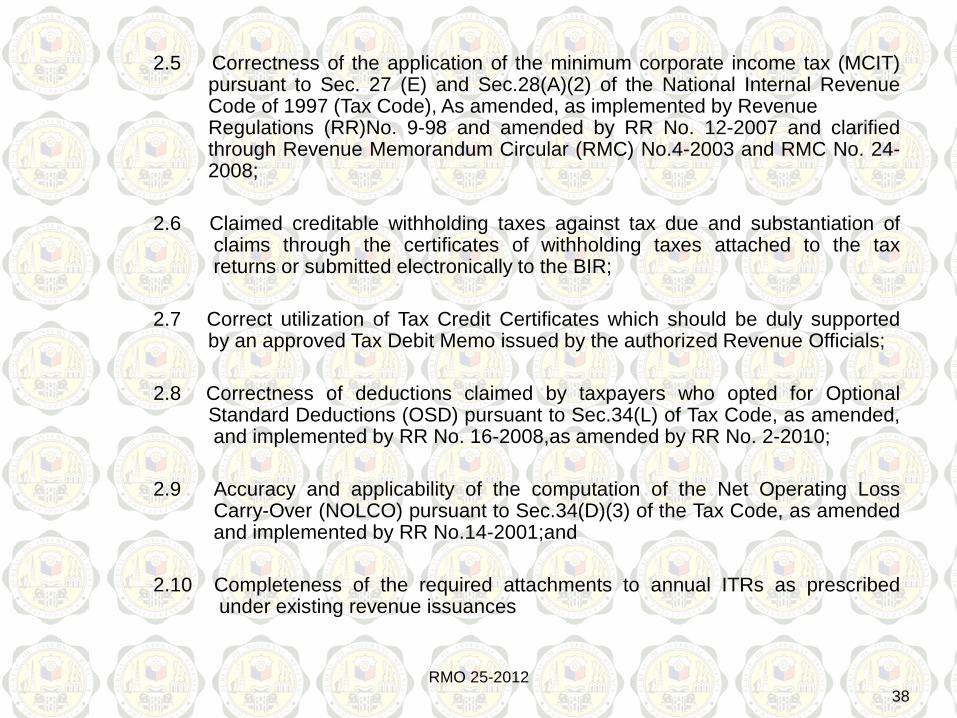

2.5 Correctness of the application of the minimum corporate income tax (MCIT)pursuant to Sec. 27 (E) and Sec.28(A)(2) of the National Internal RevenueCode of 1997 (Tax Code), As amended, as implemented by RevenueRegulations (RR)No. 9-98 and amended by RR No. 12-2007 and clarifiedthrough Revenue Memorandum Circular (RMC) No.4-2003 and RMC No. 24-2008;

2.6 Claimed creditable withholding taxes against tax due and substantiation ofclaims through the certificates of withholding taxes attached to the taxreturns or submitted electronically to the BIR;

2.7 Correct utilization of Tax Credit Certificates which should be duly supportedby an approved Tax Debit Memo issued by the authorized Revenue Officials;

2.8 Correctness of deductions claimed by taxpayers who opted for OptionalStandard Deductions (OSD) pursuant to Sec.34(L) of Tax Code, as amended,and implemented by RR No. 16-2008,as amended by RR No. 2-2010;

2.9 Accuracy and applicability of the computation of the Net Operating LossCarry-Over (NOLCO) pursuant to Sec.34(D)(3) of the Tax Code, as amendedand implemented by RR No.14-2001;and

2.10 Completeness of the required attachments to annual ITRs as prescribedunder existing revenue issuances

RMO 25-201238

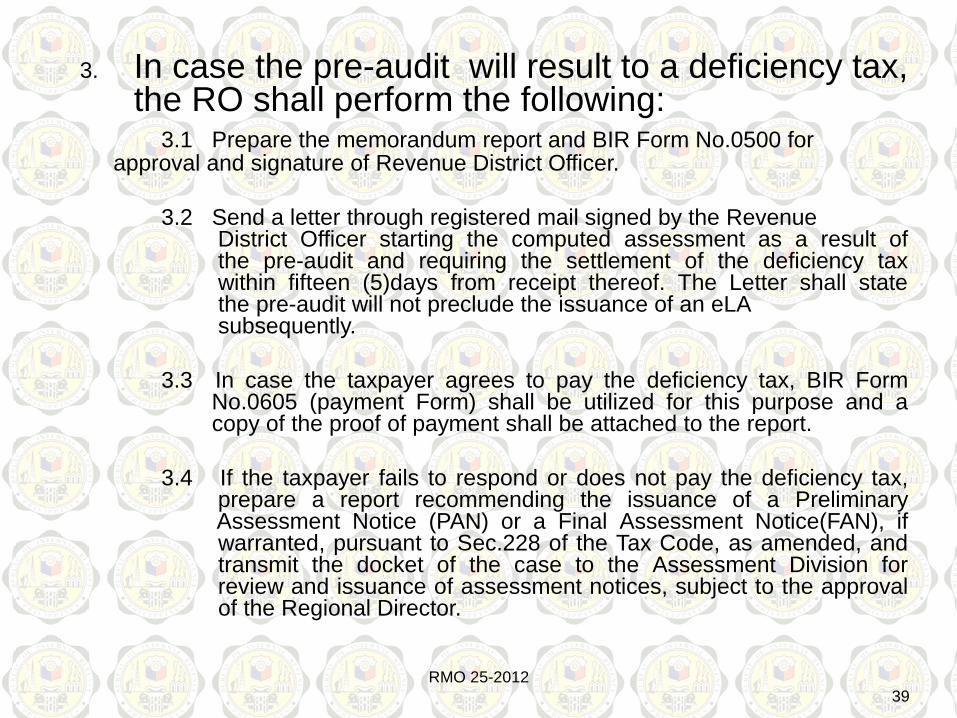

3. In case the pre-audit will result to a deficiency tax,the RO shall perform the following:

3.1 Prepare the memorandum report and BIR Form No.0500 forapproval and signature of Revenue District Officer.

3.2 Send a letter through registered mail signed by the RevenueDistrict Officer starting the computed assessment as a result ofthe pre-audit and requiring the settlement of the deficiency taxwithin fifteen (5)days from receipt thereof. The Letter shall statethe pre-audit will not preclude the issuance of an eLAsubsequently.

3.3 In case the taxpayer agrees to pay the deficiency tax, BIR FormNo.0605 (payment Form) shall be utilized for this purpose and acopy of the proof of payment shall be attached to the report.

3.4 If the taxpayer fails to respond or does not pay the deficiency tax,prepare a report recommending the issuance of a PreliminaryAssessment Notice (PAN) or a Final Assessment Notice(FAN), ifwarranted, pursuant to Sec.228 of the Tax Code, as amended, andtransmit the docket of the case to the Assessment Division forreview and issuance of assessment notices, subject to the approvalof the Regional Director.

RMO 25-201239

4. If in the course of the pre-audit of the taxreturn, it has been established by the RO thata thorough audit/investigation isnecessary, the RO assigned mayrecommend to the Regional Director, throughhis Revenue District Officer, theaudit/investigation of all internal revenue taxliabilities of the concerned taxpayer.

RMO 25-201240

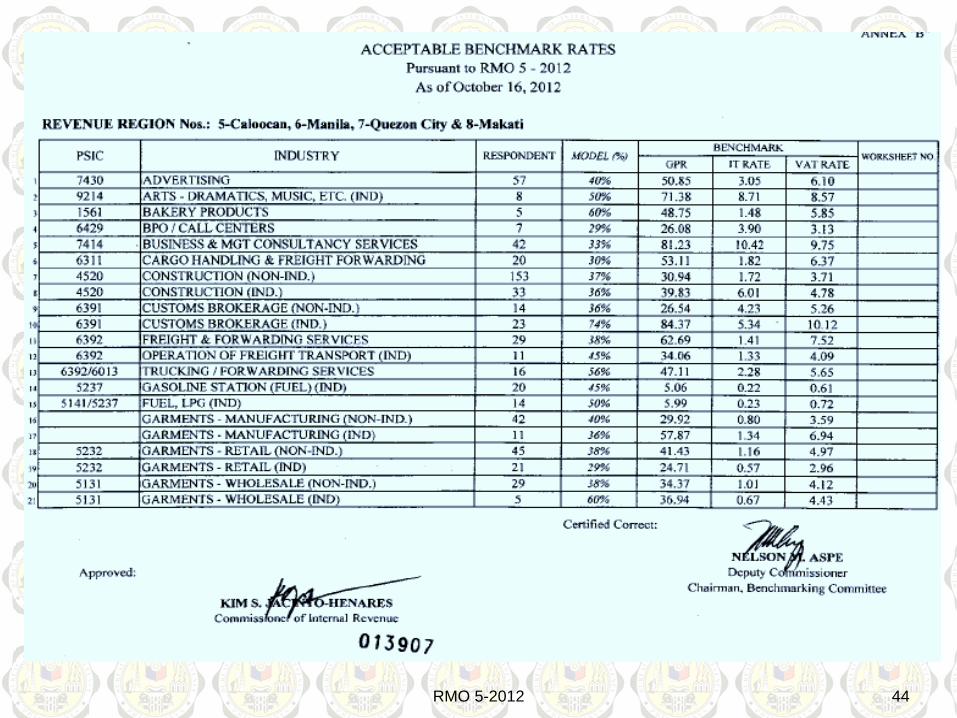

Performance Benchmarking Method BENCHMARK

Is a point of reference for measurement or a setof standard to be used to measure theperformance/compliance of taxpayers in a particularindustryBENCHMARKING OF TAXPAYERS

Refers to the process of setting a standard todetermine the performance level of taxpayers in agiven line of industry or sector. In this case, the ratiosof Net VAT Due and Income Tax Due in relation to grosssales/receipts. vis-à-vis profit margin rate is to be used forthe purpose of setting the industry standard fortaxpayers’ compliance

RMO 5-2012 41

TAX GAPIs defined as the aggregate amount of

true tax liability imposed by law for a given taxyear that is not paid voluntarily and timely. Itrepresents the difference between the actualrevenue collected and the amount that wouldbe collected if there were 100percentcompliance.GROSS COMPLIANCE RATIO

Is defined as the actual VAT collection inratio or as percentage to total potential VATcollection.

RMO 5-2012 42

EFFECTIVE VAT RATIO (EVR)Means the profit margin rate of an industry,

as benchmarked, multiplied by the VAT rate fixedby law.TAXPAYER PROFILING

Is a method of gathering data orinformation to determine the general view ofwhat is actually occurring within a system. Itcovers extensive analysis of taxpayer datawithin a given line of industry to diagnosecompliance bottlenecks.

RMO 5-2012 43

RMO 5-2012 44

In the absence of an annual audit program, theCommissioner has the authority to make assessmentspursuant to Section6(A) of the Tax Code, as amended,to wit:SEC.6. Power of the Commissioner to MakeAssessments and Prescribe Additional Requirementsfor Tax Administration and Enforcement.-

(A) Examination of Returns and Determination of Tax Due.-After a return has been filed as required under theprovisions of this Code, the Commissioner or his dulyauthorized representative may authorize the examinationof any taxpayer and the assessment of the correct amountof tax: Provided, however; That failure to file a return shallnot prevent the Commissioner from authorizing theexamination of any taxpayer.

RMC 6-2013 45

The BIR, in accordance with RevenueRegulation 11-2006, as amended, can refuse totransact official business with taxagents/practitioners who are not accreditedbefore it.

Therefore, all taxpayers are enjoined toensure that the tax agents/practitioners whomthey will engage are accredited with the BIR.

RMC 6-2013 46

RMC 29-2012 47

48