REGIONAL COUNCIL (2019-2022) Newsletter Feb 2019... · 2019-05-08 · SOP. c) Size of your...

17

NORTHERN INDIA REGIONAL COUNCIL OF THE INSTITUTE OF CHARTERED ACCOUNTANTS OF INDIA e-Newsletter VOL. IV No. 1 February 2019 REGIONAL COUNCIL (2019-2022)

Transcript of REGIONAL COUNCIL (2019-2022) Newsletter Feb 2019... · 2019-05-08 · SOP. c) Size of your...

NORTHERN INDIA REGIONAL COUNCILOF

THE INSTITUTE OF CHARTEREDACCOUNTANTS OF INDIA

e-Newsletter

VOL. IV No. 1

February 2019

REGIONALCOUNCIL(2019-2022)

From the Desk of the Chairman...

Dear Professional Colleagues

Greetings for the day!

A beginning, it is said, is only the start of a journey

to another beginning. As I begin my new role as

the 67th Chairman of the Northern India Regional

Council of The Institute of Chartered Accountants

of India in the 70th year of its magnificent

presence and gratitude, I wish that the profession

too makes a new ‘commencement’—a new

beginning with improved energy to scale new

heights of excellence and integrity in varied ways.

A voyage of a thousand miles originates with a solo

step. Let’s take that first step together and re-

dedicate ourselves to our chosen profession.

With vanity, together with wisdom of

accountability, I pen my first communication as

Chairman. Before I proceed, let me extend my

heartfelt thanks to all the professional members,

my colleagues in the Regional Council and also

other stakeholders for reposing their faith in me to

lead the forward march of our profession.

It takes a proud privilege for me to mention that

our very own CA. Prafulla P. Chhajed has taken

over the pedals as President, ICAI, and CA. Atul

Kumar Gupta has been selected as Vice-President,

ICAI. We look forward to work together for the

greater glory of our alma mater. I also wish to

congratulate with my heart CA. Charanjot Singh

Nanda, CA.Hans Raj Chugh, CA. Pramod Jain,

[email protected] ; [email protected]

ChairmanVice ChairpersonMemberMemberMemberMemberMemberMember

Editor : CA. Harish Kumar Choudhary Jain

Editorial BoardCA. Harish Kumar Choudhary JainCA. Shweta PathakCA. Pankaj GuptaCA. Vijay Kumar GuptaCA. Rajender AroraCA. Nitin KanwarCA. Sumit GargCA. Avinash Gupta

Regional Council Members

CA. Harish Kumar Choudhary Jain CA. Shweta PathakCA. Pankaj GuptaCA. Vijay Kumar GuptaCA. Rajender AroraCA. Sumit Garg CA. Shashank AgrawalCA. Avinash GuptaCA. Nitin Kanwar CA. Ajay SinghalCA. Gaurav GargCA. Rachit Bhandari CA. Rattan Singh Yadav

ChairmanVice-ChairpersonSecretaryTreasurerNICASA ChairmanNICASA MemberNICASA MemberExecutive MemberExecutive MemberMemberMemberMemberMember

9891457129981105761999997815009871174091989111212095600646459582101001981075199998103871639811181118989999493498153005899810692723

Central Council Members (Northern Region)

CA. Prafulla Premsukh ChhajedCA. Atul Kumar GuptaCA. Hans Raj ChughCA. Pramod JainCA. Charanjot Singh NandaCA. Rajesh Sharma CA. Sanjeev Kumar Singhal

Hon’ble President, ICAIHon’ble Vice-President, ICAICentral Council MemberCentral Council MemberCentral Council MemberCentral Council MemberCentral Council Member

9821090612981010361198112079249811073867921270035398102773949811565606

DISCLAIMER: The NIRC of ICAI is not in any way responsible for the result of any action taken on the basis of the advertisement published in the e-Newsletter. The members, however, may bear in mind the provision of the Code of Ethics while responding to the advertisements.

The views and opinions expressed or implied in Northern Indian Chartered Accountants e-Newsletter are those of the authors or contributors and do not necessarily reflect those of NIRC. Unsolicited articles and transparencies are sent in at the owner’s risk and the publisher accepts no liability for loss or damage Material in this publication may not be reproduced whether in part or in whole, without the consent on NIRC.

I congratulate my team of office bearers

comprising CA. Shweta Pathak, Vice-Chairperson,

CA. Pankaj Gupta, Secretary, CA. Vijay Kumar

Gupta, Treasurer and CA. Rajender Arora, NICASA

Chairman. I also congratulate CA. Sumit Garg and

CA. Shashank Agrawal as a NICASA Member. I am

sure that experience and insights of my dear

friends in the Regional Council CA. Nitin Kanwar,

CA. Avinash Gupta, CA. Ajay Singhal, CA. Gaurav

Garg, CA. Rachit Bhandari and CA. Rattan Singh

Yadav will help me in achieving our goals.

It is indeed a great honour to serve as the

Chairman of the NIRC of ICAI. But when I look

back at the distinguished history of the NIRC of the

Institute and its past Chairman’s who have served

it with such distinction and peculiarity, I also feel

humbled. I am confident that with your able

support I shall live up to the expectations.

This reminds me of the inspiring words on

leadership by John Adams, “If your actions inspire

others to dream more, learn more, do more,

become more....you are a leader. ”Over the years,

we have built a very strong foundation and

infrastructure for our Region with a network of

dynamic Branches for members and students,

which in turn are well supported by the various

Study Circles. The Branches and Study Circles

have a new team of office bearers and I am proud

to say that the new leaders of the Branches and

Study Circles have already begun their quest for

excellence in achieving the best for their

respective members and students. As I lead this

Northern Region, I assure every member and

student that they will be provided with the best

platform for professional and academic

development with the continuous support of my

respected Central and Region Council Members,

Branch leaders and Study Circle governing

CA. Rajesh Sharma, CA. Sanjeev Kumar Singhal

for being elected as a member of the 24th Central

Council of The Institute of Chartered Accountants

of India.

members.

Our activities and events for the members and

students are continuously being conducted in a

systematic and coordinated manner to ensure

maximum benefit to all. Going forward, I wish to

focus on ensuring that a concrete and robust

platform is created for the support and

development of young members both

professionally and in soft skills as they shall be

representing ICAI for a long time, and also pass

their knowledge to the next generation. I will

ensure that our excellent infrastructure shall be

optimally utilised to carry out necessary activities

for all.

I also wish to host events that are specifically

designed to enrich our women members and

students. GMCS and Career Counselling shall also

be areas of particular focus during the year.

I would like to end by quoting words of Hon'ble

Past President of India have Dr. A.P.J. Abdul

Kalam, where he reposed faith and confidence in

us and stated that we, as Partners in Nation

Building, should serve the society and the Nation

with Excellence, Independence and Integrity- our

finest professional virtues. I am sure that I will

receive the support of all the respected members

and my dear students during the year as we aspire

to achieve the best.

My new responsibility is both an opportunity and a

challenge. But I hope that I will continue to enjoy

your love and affection and I have no doubt that

we can reach our collective goals together.

The NIRC will continue its journey to support

members as well as students of Northern Region.

With best wishes,

thDate: 18 March, 2019

Place: New Delhi

CA. Harish Kumar Choudhary Jain

Chairman

February, 2019 NIRC NEWSLETTER

4

It is an honour and privilege for me to write as

Secretary in the monthly newsletter of Northern

India Regional Council (NIRC) of our esteemed

Institute, The Institute of Chartered Accountants of

India (ICAI).

At the out set, I would like to thank all the members

from the bottom of my heart for the love, blessings

and support that they have showered on me due to

which I have been elected as member of the Twenty

Third Regional Council of the Institute. I am also

thankful to my dear colleagues in the Central Council

and Regional C council for reposing faith in me and

giving me an opportunity to serve the profession by

electing me as Secretary of the Regional Council.

Friends, we cannot forget the contribution made by

the members who have served the Regional Council

in the past and I would like to thank each one of them

because of which the regional council has reached to

this stage. As someone has rightly said that there is

always room for improvement, in which I firmly

believe, and applying the same in the regional

council also we will work towards the further

development and progress of the profession. We also

have branches and study circles which are an integral

part of our region and will ensure that we work

together to improve on various matters relating to

the Members, Students, Society and Profession at

large. Efforts will be made for the betterment of each

of the member in the wide spread region through

these branches & study circles.

This time members in the northern region have

elected ten new faces in the regional council and

have also re-elected three members who served as

members in the previous council. With taking the

maximum from the experience and guidance of re-

elected members and channelizing energies &

expertise of the newly elected members, I hope that

region will achieve new heights. The guidance and

support is also required from each one of you to face

the challenges and taking the profession and nation

to new heights.

I also take the inspiration from the following words

said by our beloved father of the nation Mahatma

Gandhi ji

“The best way to find yourself is to lose yourself in the

service of others.”

Friends, it being the start of my journey as Secretary

and as a member of Regional Council, I look forward

to your valuable suggestions that we can implement

together within the guidelines framed under the ICAI

regulations for betterment of the profession.

At last I can assure you all that, under the guidance

and support of our worthy President, Vice President,

Chairman and my other respected colleagues in

Central Council and regional Regional Councils, I will

give the best to enhance the image of our region and

ICAI.

I wish you all a very happy, healthy and prosperous

life.

Warm regards,

CA. Pankaj Gupta Secretary

Respected Members

Greetings !

From the Desk of the Secretary

thDate: 18 March, 2019

Place: New Delhi

5

CA. Ravinder Singh Pawar

IND AS 27: Separate Financial Statements

February, 2019 NIRC NEWSLETTER

6

February, 2019 NIRC NEWSLETTER

7

CA. NEHA JAWA

HOW TO DRAFT A STANDARD OPERATING PROCEDURE

PART 1: FORMATTING YOUR SOP1. Choose your format• Simple Steps Format: It is to the point only. It is based on simple sentence and listed in bullets. It looks more like a to-do list than a report. • Hierarchical Steps Format: It is usually for long procedures, involving a few decisions to make, clarification and terminology. This is usually a list of main steps all with substeps in a very particular order.• Flowchart Format: If the procedure is more like a map with an almost infinite number of possible outcomes, a flowchart is the best option for you. This is the format you should opt when results are not always predictable.

2. Consider your audienceThere are 3 main factors to be considered before writing a SOP

a) Prior knowledge of your audience: Are they familiar with your organization and its procedure? Do they know the terminology? Your language needs to match the knowledge of reader. b) Language abilities of audience: Is there any chance people who don’t speak your language will be reading your SOP? If this is an issue, then it’s better to include lots of pictures and diagrams in your SOP.c) Size of your audience: If multiple people are reading your SOP at once then you should write your SOP more like a conversation in a Play.

3. Keep your SOP purpose in mind: Check out if there is any particular reason that this SOP is useful? Once you are aware of the purpose of writing then it would become easier what to emphasis upon. The following are the possible reasons for the formation of SOP:• To ensure compliance Standards are met.• To maximize production requirements.• To ensure the procedure has no adverse impact on environment.• To ensure safety• To ensure everything goes according to schedule.• To prevent failures in manufacturing• To be used as training document

PART – 2: WRITING YOUR SOP1. Cover the necessary material: In general, technical SOP will consist of four main elements apart from procedure itselfa) Title Page: It includes name of process and the name of department to which SOP applies. b) Table of contents: It is to summarize the name of contents in the document.c) Quality Assurance/Quality Control: Make sure to insert proper

material through which user could check whether he is following the things properly.d) Reference: Be sure to list all cited or significant references. Also, if your SOP is related with any other SOP be sure to attach the necessary information.

2. Cover the necessary items For the procedure :a) Scope and applicability: It is important to clearly define the scope, otherwise it could overlap with other procedural documents.b) Methodology and procedures: What is the right way of carrying out the process should be clearly mentioned.c) Clarification of Terminology: All the abbreviations, acronyms and phrases should be clearly depicted.d) Health and Safety Warnings: Where the concern has section related with health and safety then it should be properly mentioned in its column.e) Equipment and supplies: A complete list of required equipments must be mentioned, like what to use, when to use and how to use.f) Cautions and interferences: In case of any mishap, what should be done, whom should be called for must be properly disclosed.

3. Make your writing concise and easy to read

4. Breakup large chunks of text with diagrams and flowcharts

5. Use a consistence style: If this is a document to be used solely for demonstrating to the industry then a technical and trite language would be good for the entire document. However, if workers are going to use this as a reference (as and when required), then the language should be clear and actionable.

6. Try to access potential problems in the whole process: Once you are done with whole writing, try to access where could be potential errors while implementing the same. To access what you have drafted, try it by testing on those employees who are going to use it on day to day basis. Make sure they are able to give feedback on the procedures presented so that you can make alterations to the process.Once you are done with the whole process from start to finish and all the stakeholders have signed off on the document, implement the Standard Operating Procedure for the necessary process and file the document appropriately.

February, 2019 NIRC NEWSLETTER

8

CA. Sameer Jain

BANK BRANCH AUDIT

1. Deposit :- Term / Saving / Current / FCNR/ NRE / NRNR / Verify

transactions during the year relating to:a. New Accounts opened;b. Accounts closed;c. Dormant Accounts;d. Interest calculations;e. Test check account statements for unusual / large / overdraft

transaction;f. Overdue Term deposits & banks policy for its renewal;g. Accrual of interest;h. RBI Norms for Non-resident deposits & its operations - with due

importance to opening and operation of accounts like NRE,

NRNR,FCNR,RFC, etc.;i. Interest on various types of deposits Ascertain reasons for frequent

reversal of interest and the authorization for the same, RBI Norms for non-

resident deposits & its operations- with due importance to opening and

operation of accounts like NRE, NRNR, FCNR, RFC, etc, Examine interest

trends as compared to average annual deposits (monthly average figures),

In case of deposits frozen by Revenue / Regulatory / Government etc,

procedure given in Master Circular on Interest Rates on Rupee Deposits

held in Domestic, Ordinary Non-Resident (NRO) and Non- Resident

(External) (NRE) Accounts should be followed for Interest credit and Verify

that interest on term deposit matured and remaining unpaid will attract

saving bank account rate of interest .j. Tax Deducted at Source :- Verify that TDS returns have been uplinked as

per schedule laid down in the Income - tax Act, 1961. Also ensure if the From

15-G and Form 15-H are filed with the Income-tax department within the

specified time schedule and refer CBDT circular no. 3/2010 dated

02.03.2010 on Tax Deduction at Source on interest accrual in Core-Branch

Banking Solutions (CBS) software.k. Large deposits placed at the end of the year (probable window

dressing).l. Examine unusual trend in account opening or account closing, dormant

accounts that have suddenly been reactivated by heavy cash withdrawals or

deposits, overdrawing, etc.m. Examine interest trends as compared to average annual deposits

(monthly average figures).n. Review the Master Circular on Maintenance of Deposit Accounts issued

by RBI dated March 1, 2004 attached hereto.

2. Advance :-I. Preliminary information before audit of Advances:a. Obtain the Head Office delegation of power and duties & limit fixed for

Branch and its executives.b. Study the various reports issued by the concurrent auditors, RBI

Inspection reports, RO inspectors. Gain understanding of various audit

points and material discrepancies and irregularities reported and

compliances of the same. Review monitoring reports sent by the branch to

the controlling authorities in respect of irregular advances.c. Obtain the detailed list of advances to identify major borrowers, period

since when granted, nature to advances and clients, major defaulters,

lending under various schemes, possibility of window dressing in the

account, up gradation as well as down gradation of accounts. Compare the

list with previous audit to find out major recoveries II. Verification of Advances : -a. Review monitoring reports (irregularity reports) sent by the branch to

the controlling authorities in respect of irregular advances.b. Review appraisal system, Files of large as well as critical borrowers,

sanctions, disbursement, renewals,c. Documentation, systems, securities, etc.d. Review on test check basis operations in the Advances Accounts.e. Compliance of sanction terms and conditions in the case of new

advances.f. Whether the borrower is regular in submission of stock statements,

book debt statements, insurance policies, balance sheets, half yearly

results, etc. and whether penal interest is charged in case of default/ delay

in submission of such data.g. Charge of interest and recovery for each quarter or as applicable to be

verified.h. Review the monitoring system, i.e. monitoring end use of funds,

analytical system prevalent for the advances, cash flow monitoring, branch

follow-up, consortium meetings, inspection reports, stock audit reports,

market intelligence, etc.a. Check classification of advances, incomes, recognition and provisioning

as per RBI Norms/ Circulars.b. Examine interest trends as compared to average annual advances

(monthly average figures).c. Scrutinize the final advances statements with regard to assets

classification, security value, documentation, drawing power, out

standings, provisions, etc.d. Check whether Non-Fund based (Letter of Credits/ Bank Guarantees)

exposure of the borrowers is within the sanctioned limits.e. Compare projected financial figures given at the time of project

appraisal with actual figures from audited financial statements for relevant

period and ascertain reasons for large variance.f. Take into account the assessment of RBI if the regional office of RBI has

forwarded a list of individual advances to the bank, where the variance in

the provisioning requirements between the RBI and the bank is above

certain cut off levels (refer para 5.1.2 of the master circular)g. Restructured Advances :• Verify whether branch has complied with Master Circular No. DBOD. No.

BP.BC.21 /21.04.048/2010-11 dated July 1, 2010 on Restructured of

advance.• Consider the following important points covered in Circular:I. Restructured account could be under ‘Standard’, ‘ Sub-standard’ and

February, 2019 NIRC NEWSLETTER

9

‘Doubtful’ categories. Banks cannot reschedule / restructure / re-negotiate

borrower accounts with retrospective effect.ii. Date of approval of the restructured package by the competent

authority would be relevant to decide the asset classification status of the

account after restructuring rescheduling/ renegotiation.iii. Prior approval should be obtained in case of BIFR and CDR cases under

restructuring.iv. An existing ‘Standard asset’ will not be downgraded to Sub-standard

category upon restructuring and if during the specified period, the asset

classification of Sub-standard / Doubtful accounts will not deteriorate upon

restructuring, if satisfactory performance is demonstrated during the

specified period.v. Asset Classification will not be downgraded if satisfactory performance

observed during the specified period, subject to:• Dues being fully secured• Unit becomes viable in 7 years (10 years for infrastructure cases)• Loan is repayable in 10 years (15 years for Infrastructure cases)• Promoter sacrificed and additional funding of at least 15% of Bank

Sacrifice• Obtaining personal Guarantee of promoters

vi. Verify the Financial viability and reasonable certainty of certainty of

repayment of each account restructured.vii. Verify that advance covered under restructuring should be from other

than capital market exposure, personal/ consumer loan.viii. Verify whether borrowers indulging in frauds and malfeasance are not

taken for restructuring. As per circular they remain ineligible for

restructuring.ix. Prudential norms on Unsecured Advances (RBI Circular

DBOD.No.BP.BC.96 /08.12.014/2009-10 dated April 23,2010)• Intangible Securities like rights, licenses, authorization etc. charged to

the bank as collateral security should not be reckoned as tangible security

and to be recorded as unsecured.• Banks should also disclose the total amount of advances for which

intangible securities such as charge over the rights, licenses, authority, etc.

has been taken as also the estimated value of such intangible collateral. The

disclosure may be made under a separate head in “Notes to Accounts”. This

would differentiate such loans from other entirely unsecured loans.• I n t e r m o f p a r a g r a p h 2 ( a ) o f c i r c u l a r

DBOD.No.BP.BC.125/21.04.048/2008-09 dated April 17,2009 on

‘Prudential Norms on Unsecured Advances’, rights, licenses, authorizations,

etc. charged to banks as collateral in respect of projects (including

infrastructure projects) should not be reckoned as tangible security. In

partial modification to the above it has been decided that banks may treat

annuities under build -operate-transfer (BOT) model in respect of

road/highway projects and toll collection rights, where there are provisions

to compensate the project sponsor if a certain level of traffic is not achieved,

as tangible securities subject to the condition that banks’ right to receive

annuities rights is legally enforceable and irrevocable.

III. Provisioning Norms;i. Normal Provision: Bank will hold provision against restructured

advances as per the existing provisioning norms. Provision should be

difference between the fair value of loan before and after restructuring.• Fair value before restructuring: Present value of cash flows (Principal

and interest at the existing rate charged on the advance before

restructuring) discounted at a rate equal to bank’s BPLR plus appropriate

term premium and credit risk premium for the borrower category on the

date of restructuring”• WCTL fair value should be computed as per actual cash flow • In case any security is taken in lieu of the diminution in the fair value of

the advance, it should be valued at Re. 1 till maturity of the security. ii. Option in notionally computation of Diminution in fair value: Due to lack

of expertise/ appropriate infrastructure RBI has given option to provide

diminution at five percent of the total exposure, in respect of all

restructured accounts where the total dues to bank(s) are less than Rs. 1

crore till the financial year ending March 2011. The position would be

reviewed thereafter.• Income Recognition in case additional finance is provided:• Incase of standard asset: May be treated as ‘standard asset’, up to a

period of one year after the first interest/ principal payment.• In case where pre-restructuring facilities were classified as ‘sub-

standard’ and ‘doubtful: On cash basis only.

o Conversion of principal into debt/ equity and conversion of unpaid

interest into ‘Funded Interest Term Loan’ (FITL),

• Master circular on Agricultural Debt Waiver and Debt Relief Scheme,

2008- Prudential Norms on Income Recognition, Asset Classification,

Provisioning, and Capital Adequacy should be followed in case of

agricultural advances as per debt waiver scheme.• As per RBI Circular No. DBOD.No. BP.BC.46/21.04.048/2009-10 dated

September 24,2009• On an account turning NPA, banks should reverse the interest already

charged and not collected by debiting Profit and Loss account, and stop

further application of interest. However, banks may continue to record such

accrued interest in a Memorandum account in their books, as is the practice

currently followed by some banks.• For the purpose of computing Gross Advance, interest recorded in the

Memorandum account should not be taken into account.

3. Profit & Loss Account: Income/ Expenditure: Verify:a. Short debit of interest / commission on advances;b. Excess credit of interest on deposits;c. In case the discrepancies are existing in large number of cases, the

auditor should consider the impact of the same on the accounts;d. Determine whether the discrepancies noticed are intentional or by

error;e. Check whether the recurrence of such discrepancies are general or in

respect of some specific clients;f. Proper authority in income / expenditure especially for the last month

of the financial year.h. Divergent Trends:i. Divergent trends in income / expenditure of the current year may be

analyzed with the figures of the.j. Previous year.1. Monthly average figures, composition of the income/ expenditure, etc.

4. Balance Sheet:-1. Cash & Bank Balances:a. Physically verify the Cash Balance as on March 31, 2005 or reconcile the

cash balance from the date of verification to March 31,2005.b. Confirm and reconcile the Balance with banks as on March 31,2005.2. Investments:a. Physically verify the Investments held by the branch on behalf of Head

Office and issue certificate of physical verification of investments to bank’s

February, 2019 NIRC NEWSLETTER

10

February, 2019 NIRC NEWSLETTER

Investments Department.b. Check receipt of interest and its subsequent credit to be given to Head

Office.3. Advances Provisioning:As per RBI norms, unrealized interest on NPA accounts should be reversed

and not charged to ‘Advance Accounts”. Reversal of unrealized interest of

previous years in case of NPA accounts is required to be checked.Partial Recovery in respect of NPA account should be generally

appropriated against principal amount in respect of doubtful assets.

5. Fixed Assets:Check Inter-branch transfer memos relating to Fixed Assets and whether

they have been correctly classified in the accounts and depreciation

accounting thereof.5. Inter Branch Reconciliation (IBR):A. Understand the IBR system and accordingly prepare an audit plan to

review the IBR transactions. The large volume of Inter Branch Transactions

and the large number of un reconciled entries in the banking system makes

the area fraud-prone.b. Check up head office inward communication to branch to ascertain date

upto which statements relating to inter branch reconciliation have been

sent.6. Contingent Liabilities.a. Contingent liabilities, being an important “off balance sheet” item, seek

reasonable assurance that all contingent liabilities are identified and

properly disclosed. E.G. Increase in rent of premises by landlord disputed by

bank.b. Obtain a letter of representation.7. Check and report:1. Reversal of any large / old / unexplained entries, which had remained

outstanding in IBR.2 Items of revenue nature, cash-in-transit (for example, cash meant for

deposit into currency chest) which remains pending for more than a

reasonable period.3. Double responses to the entries in the Accounts.4. Test Check accuracy and correctness of “Daily statements”which are

prepare by the branch and sent to IOR department.The auditor should duly consider the extent of non-reconciliation in forming

his opinion on the financial statements.5. Where the amount involved are material, the auditor should suitable

q u a l i f y h i s a u d i t re p o r t , F u r t h e r, v i d e i t s c i rc u l a r n o .

DBOD.No.BP.BC.73/21.04.018/2002-03 dated February 26,2003, the

Reserve Bank (RBI) advised the banks to maintain category-wise (head-

wise) accounts for various types of transaction put through inter branch

accounts so that the netting can be donor category-wise. Further,RBI

advised banks to make 100 percent provision (category-wise) for net debit

position in their inter-branch accounts arising out of the unreconciled

entries, both debit and credit, outstanding for more than six months (Refer

to the master circular).a. Suspense Accounts, Sundry Deposits, etcb. Suspense accounts are adjustment accounts in which certain debit

transaction are temporarily posted whose authorization is pending for

approval. Sundry Deposit accounts are adjustment accounts in which

certain credit transactions are temporarily posted whose authorization is

pending for approval. As and when the transactions are duly authorized by

the concerned officials they are posted to be respective accounts and the

Suspense account / Sundry Deposit account is credited respectively.c. Ask for and analyses their year-wise break-up.

D. Check the nature of entries parked in such Accounts.e. Check any movement in such old balances and whether the same is

genuine and has properly authorized by the competent authority.f. Check for any revenue items lying in such accounts and whether proper

treatment has been given for the same.

6. Auditors Report & Memorandum of Changes.a. The Auditors Report should be a self contained document and should

contain no reference of any point.b. made in any other report including the LFAR;c. Include Audit Qualifications in the Auditors Report and not in the LFAR;D. Quantify the Audit Qualifications for a better appreciation of the point

made to the reader;e. For suggesting any charges in the financial statements of the branch,

quantify the same in the Memorandum of Changes (MOC) and make it a

subject matter of qualification and annex it to the Auditors Report.

7. Long From Audit Report (LFAR).A RBI has revised the LFAR w.e.f.F.Y.2002-2003 and it has now been made

more comprehensive.b. Study the LFAR Questionnaire thoroughly;c. Plan the LFAR work along with the statutory audit right from day one;d. The LFAR questionnaire is a useful tool for planning the statutory audit

of a branch;e. Complete & submit the Auditors Audit Report as well as the LFAR

simultaneously;f. Be specific while replying the LFAR;g. Give instances of shortcomings/ weaknesses existing in the respective

areas of the branch functioning in the LFAR;h. The LFAR should be sufficiently detailed and quantified so that they can

be expeditiously consolidated by the bank.

8. General.a. Send a Letter of your Requirements to the Branch before commencing

the audit [Draft Letter enclosed herewith].b. Obtain the latest status of cases involving fraud, vigilance and matters

investigation having effect on the accounts and its reporting requirement.

Review the Master circular on FRAUDS - CLASSIFICATION AND REPORTING

issued by RBI dated 19 September 2003 enclosed herewith.c. Obtain a Management Representation Letter (MRL) [Draft MRL

enclosed herewith].

9. Credit Facility (Basis for treating a Credit Facility as NPA)a. Term Loans:- Interest or installment remains overdue for a period of

more than 90 days from end of the quarter w.e.f. March 31,2004

Agricultural Advances: In respect of advances granted for agricultural

purposes where interest and / or installment of principal remains overdue

for a period of more than two harvest seasons but for a period not

exceeding two half years, the advance should be treated as NPA.b. Cash Credits & Overdraftsc. The account remains continuously “out order” for a period of more than

90 days i.e. Outstanding balance remains continuously in excess of the

sanctioned limit/ drawing power or there are no credits continuously for a

period of 90 days as on the date of Balance Sheet or credits are not enough

to cover the interest during the same period.d. The bills purchased / discounted remains overdue for a period of more

than 90 days.

11

February, 2019 NIRC NEWSLETTER

REQUEST FOR PROPOSAL

NIRC of ICAI requires 2000 – 3000 sq. ft covered area/Floor/Building on hiring basis atvarious part of North, East, South, West part in Delhi for its various classes/ Programmes/ Library/ Conferences/ Reading Room etc.

Kindly send your proposal with details at NIRC office, ICAI Bhawan, 5 th -Floor, AnnexeBuilding, Indraprastha Marg, New Delhi-110002.

E-Mail – [email protected]

12

February, 2019 NIRC NEWSLETTER

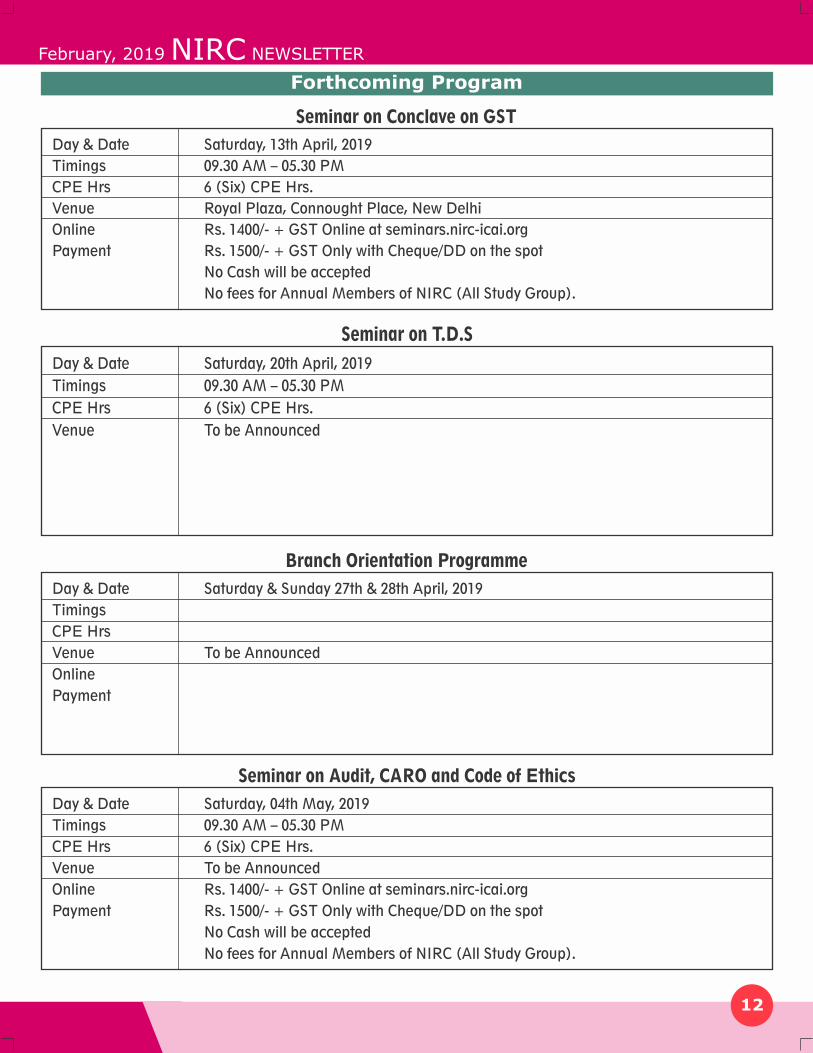

Forthcoming Program

Seminar on T.D.S

Day & Date

Timings

CPE Hrs

Venue

Saturday, 20th April, 2019

09.30 AM – 05.30 PM

6 (Six) CPE Hrs.

To be Announced

Branch Orientation Programme

Day & Date

Timings

CPE Hrs

Venue

Online

Payment

Saturday & Sunday 27th & 28th April, 2019

To be Announced

Seminar on Conclave on GST

Day & Date

Timings

CPE Hrs

Venue

Online

Payment

Saturday, 13th April, 2019

09.30 AM – 05.30 PM

6 (Six) CPE Hrs.

Royal Plaza, Connought Place, New Delhi

Rs. 1400/- + GST Online at seminars.nirc-icai.org

Rs. 1500/- + GST Only with Cheque/DD on the spot

No Cash will be accepted

No fees for Annual Members of NIRC (All Study Group).

Seminar on Audit, CARO and Code of Ethics

Day & Date

Timings

CPE Hrs

Venue

Online

Payment

Saturday, 04th May, 2019

09.30 AM – 05.30 PM

6 (Six) CPE Hrs.

To be Announced

Rs. 1400/- + GST Online at seminars.nirc-icai.org

Rs. 1500/- + GST Only with Cheque/DD on the spot

No Cash will be accepted

No fees for Annual Members of NIRC (All Study Group).

13

February, 2019 NIRC NEWSLETTER

Forthcoming Program

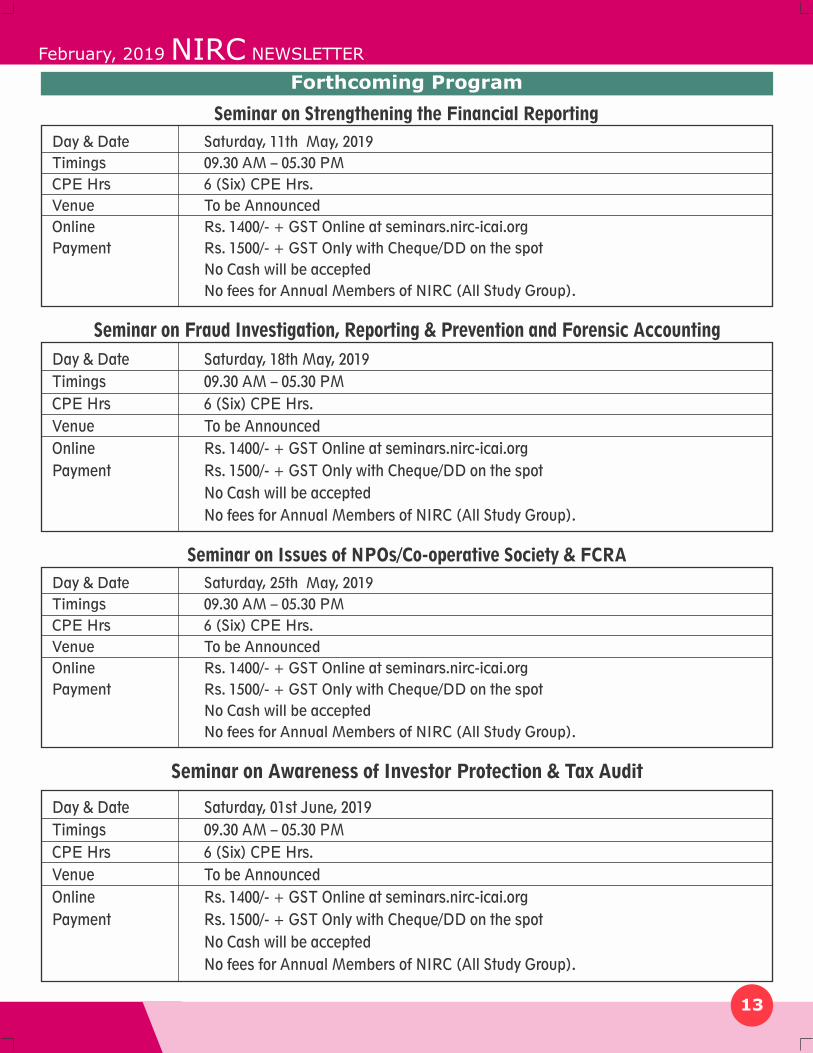

Seminar on Strengthening the Financial Reporting

Day & Date

Timings

CPE Hrs

Venue

Online

Payment

Saturday, 11th May, 2019

09.30 AM – 05.30 PM

6 (Six) CPE Hrs.

To be Announced

Rs. 1400/- + GST Online at seminars.nirc-icai.org

Rs. 1500/- + GST Only with Cheque/DD on the spot

No Cash will be accepted

No fees for Annual Members of NIRC (All Study Group).

Seminar on Issues of NPOs/Co-operative Society & FCRA

Day & Date

Timings

CPE Hrs

Venue

Online

Payment

Saturday, 25th May, 2019

09.30 AM – 05.30 PM

6 (Six) CPE Hrs.

To be Announced

Rs. 1400/- + GST Online at seminars.nirc-icai.org

Rs. 1500/- + GST Only with Cheque/DD on the spot

No Cash will be accepted

No fees for Annual Members of NIRC (All Study Group).

Seminar on Fraud Investigation, Reporting & Prevention and Forensic Accounting

Day & Date

Timings

CPE Hrs

Venue

Online

Payment

Saturday, 18th May, 2019

09.30 AM – 05.30 PM

6 (Six) CPE Hrs.

To be Announced

Rs. 1400/- + GST Online at seminars.nirc-icai.org

Rs. 1500/- + GST Only with Cheque/DD on the spot

No Cash will be accepted

No fees for Annual Members of NIRC (All Study Group).

Seminar on Awareness of Investor Protection & Tax Audit

Day & Date

Timings

CPE Hrs

Venue

Online

Payment

Saturday, 01st June, 2019

09.30 AM – 05.30 PM

6 (Six) CPE Hrs.

To be Announced

Rs. 1400/- + GST Online at seminars.nirc-icai.org

Rs. 1500/- + GST Only with Cheque/DD on the spot

No Cash will be accepted

No fees for Annual Members of NIRC (All Study Group).

14

GLIMPSESFebruary, 2019 NIRC NEWSLETTER

A View at the CA. Womens Conference “ASTITVA – Recreating from within” organized by NIRC of ICAI held on 9th February 2019.

Two Days Regional Conference of NIRC of ICAI held at Hotel Le Meridien, Delhi on 2nd & 3rd February 2019

15

GLIMPSESFebruary, 2019 NIRC NEWSLETTER

A View at the Election of NIRC Office Bearers held on 27th February 2019.

A View at the NIRC Annual Award Function of NIRC of ICAI held on 26th February 2019.

16

February, 2019 NIRC NEWSLETTER

Central Council Members from Northern Region

CA. Sanjeev Singhal CA. Pramod Jain

CA. Atul Kumar Gupta(Hon’ble Vice-President, ICAI)

CA. Rajesh Sharma CA. Hans Raj Chugh CA. Charanjot Singh Nanda

CA. Prafulla Premsukh Chhajed(Hon’ble President, ICAI)

February, 2019

NIRC e-Newsletter

17

CA. Vijay Kumar Gupta (Treasurer)

CA. Rattan Singh Yadav(Member)

CA. Nitin Kanwar (Executive Member)

CA. Ajay Singhal

(Member)

CA. Sumit Garg (NICASA Member)

CA. Pankaj Gupta (Secretary)

CA. Avinash Gupta

(Executive Member)

CA. Rajender Arora (NICASA Chairman)

CA. Shashank Agrawal

(NICASA Member)

CA. Rachit Bhandari

(Member)CA. Gaurav Garg

(Member)

CA. Jain Harish Kumar Choudhary(Chairman)

CA. Shweta Pathak(Vice-Chairperson)

NIRC of ICAI 2019-2020Regional Council Members