Regional Cooperation in Promoting and Sustaining CDM Initiatives Ashok Sarkar, Ph.D. Regional and...

24

Regional Cooperation in Promoting and Sustaining CDM Initiatives Ashok Sarkar, Ph.D. Regional and Sustainable Development Department Asian Development Bank (ADB), Manila, Philippines * CD4CDM Workshop Asian Institute of Technology, Bangkok, Thailand 21 October 2005 * The views presented herein are the author’s own made in his personal capacity and do not necessarily represent that of the ADB

-

Upload

baldwin-carr -

Category

Documents

-

view

220 -

download

1

Transcript of Regional Cooperation in Promoting and Sustaining CDM Initiatives Ashok Sarkar, Ph.D. Regional and...

Regional Cooperation in Promoting and Sustaining CDM

Initiatives

Ashok Sarkar, Ph.D.Regional and Sustainable Development DepartmentAsian Development Bank (ADB), Manila, Philippines*

CD4CDM WorkshopAsian Institute of Technology, Bangkok, Thailand

21 October 2005

*The views presented herein are the author’s own made in his personal capacity and do not necessarily represent that of the ADB

R.FED & UKRAINE

0%W&E EUROPE -8%

CANADA - 6%

US - 7%

AUSTRALIA +8%

JAPAN -6%

N. ZEALAND 0%

Global Kyoto Global Kyoto CommitmentCommitment

• 38 countries faced reduction/limitation commitments - overall reduction of 5.2% from 1990 emission levels

• Commitments respond to a GHG reduction of 30%-40% below business as usual forecasts over period 2008 - 2012

• 2nd Commitment Period (2013-2017)• 3rd Commitment Period (2018-2022)

Annex 1 targetsAnnex 1 targets

• Who’s missing their targets?

9

Kyoto gaps

-6000 -5000 -4000 -3000 -2000 -1000 0 1000 2000 3000 4000

MtCO2e

Russia

CEECs

Ukraine

Canada

OOECD

Japan

EU15

Net sellers

Net buyers

How Big a Market Will It How Big a Market Will It Be?Be?

– 2 x 109 tons traded at @ $5-20 = $10-40 billion

– Global market may exceed $100 billion per year by 2020 as estimated by the Financial Times

– The Economist (October, 1999): $1 trillion global trading market if clear rules are established

Annual Volumes Traded Annual Volumes Traded (MtCO2e) to 2012 (MtCO2e) to 2012

VintagesVintages

Source: State and Trends of the Carbon Market 2005, World Bank & Point Carbon Market Outlook July 2005

1838

18 16 25

78115

134.5

020406080

100120140160

1998 1999 2000 2001 2002 2003 2004 2005Jan -July

Estimated Market Value Estimated Market Value (US$M)(US$M)

0200400600800

100012001400160018002000

1998 1999 2000 2001 2002 2003 2004 2005Jan -July

Source: State and Trends of the Carbon Market 2005, World Bank & Point Carbon Market Outlook July 2005

Who is Buying?Who is Buying?Australia

3%Japan21%

Other EU32%

Netherlands16%

NZ7%

Canada5%

USA4%

UK12%

Jan 03 – Dec 04 Jan 04 – Apr 05

Source: World Bank 2005

Japan29%

Other EU30%

Netherlands22%

Canada6%

UK6%

Australia1%

USA3%

NZ3%

Who is Selling?Who is Selling?Rest of Latin

America22%

OECD14%

India31%

Africa0%

Rest of Asia14%

Brazil13%

Transition Economies

6%

Jan 03 – Dec 04 Jan 04 – Apr 05

Source: World Bank 2005

Rest of Latin America

23%

OECD10%

India26%

Africa3%

Rest of Asia17%

Brazil12%

Transition Economies

9%

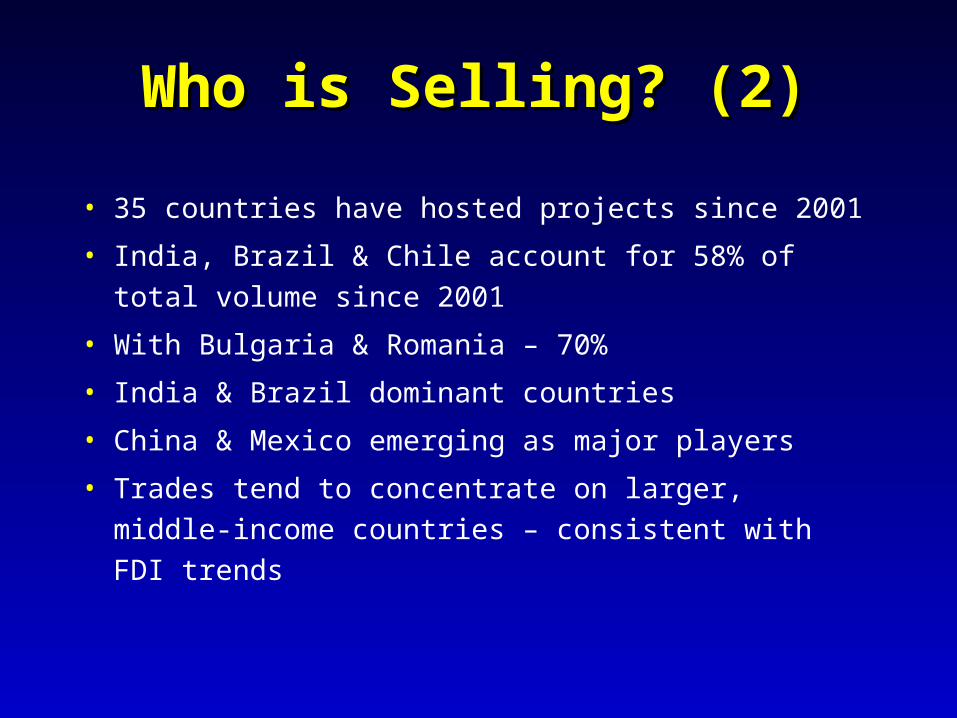

Who is Selling? (2)Who is Selling? (2)

• 35 countries have hosted projects since 2001

• India, Brazil & Chile account for 58% of total volume since 2001

• With Bulgaria & Romania – 70%

• India & Brazil dominant countries

• China & Mexico emerging as major players

• Trades tend to concentrate on larger, middle-income countries – consistent with FDI trends

Technology BreakdownTechnology Breakdown

LULUCF4%

HFC23%

N2O3%

Other8%

LFG16%

Hydro9%

Wind8%

Biomass14%

Animal Waste12%

Energy Efficiency

3%

Source: World Bank 2005Jan 03 – Dec 04 Jan 04 – Apr 05

LULUCF4%

HFC25%

N2O4%

Other7%

LFG10%

Hydro12%

Wind7%

Biomass11%

Animal Waste18%

Energy Efficiency

2%

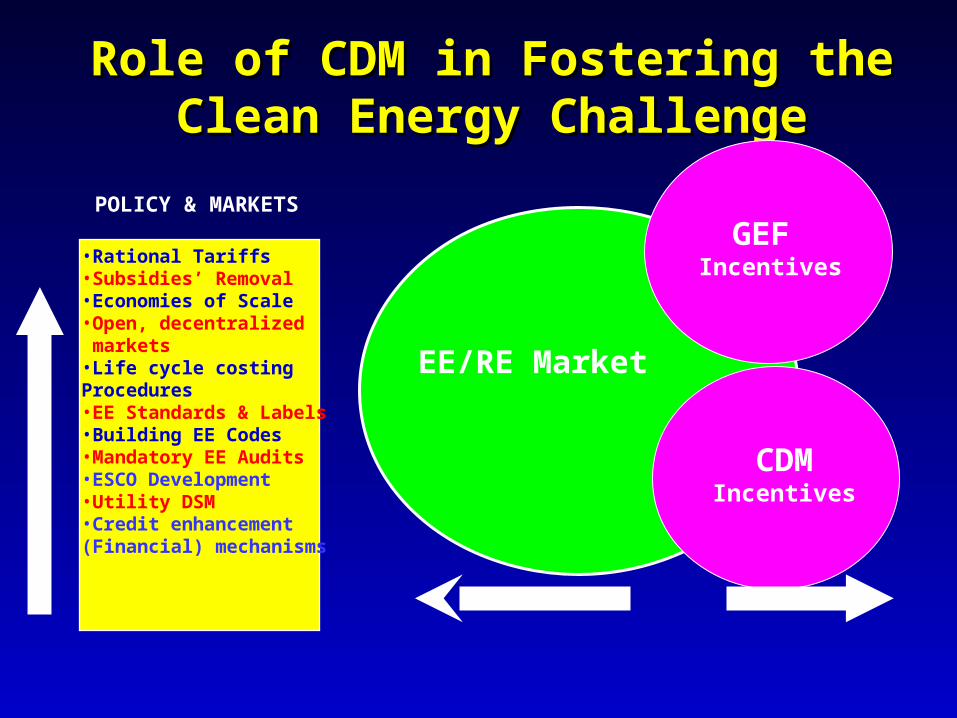

Role of CDM in Fostering the Role of CDM in Fostering the Clean Energy ChallengeClean Energy Challenge

CDM Incentives

EE/RE Market

•Rational Tariffs•Subsidies’ Removal•Economies of Scale•Open, decentralized markets•Life cycle costing Procedures•EE Standards & Labels•Building EE Codes•Mandatory EE Audits•ESCO Development•Utility DSM•Credit enhancement (Financial) mechanisms

POLICY & MARKETS GEF

Incentives

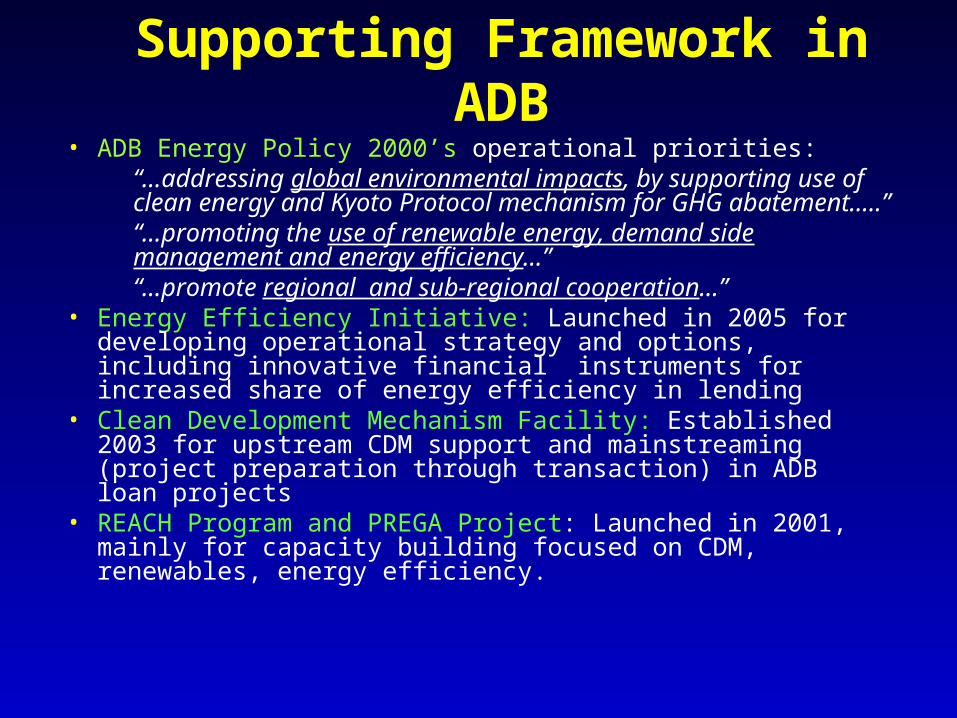

Supporting Framework in ADB

• ADB Energy Policy 2000’s operational priorities:“…addressing global environmental impacts, by supporting use of clean energy and Kyoto Protocol mechanism for GHG abatement…..”“…promoting the use of renewable energy, demand side management and energy efficiency…”“…promote regional and sub-regional cooperation…”

• Energy Efficiency Initiative: Launched in 2005 for developing operational strategy and options, including innovative financial instruments for increased share of energy efficiency in lending

• Clean Development Mechanism Facility: Established 2003 for upstream CDM support and mainstreaming (project preparation through transaction) in ADB loan projects

• REACH Program and PREGA Project: Launched in 2001, mainly for capacity building focused on CDM, renewables, energy efficiency.

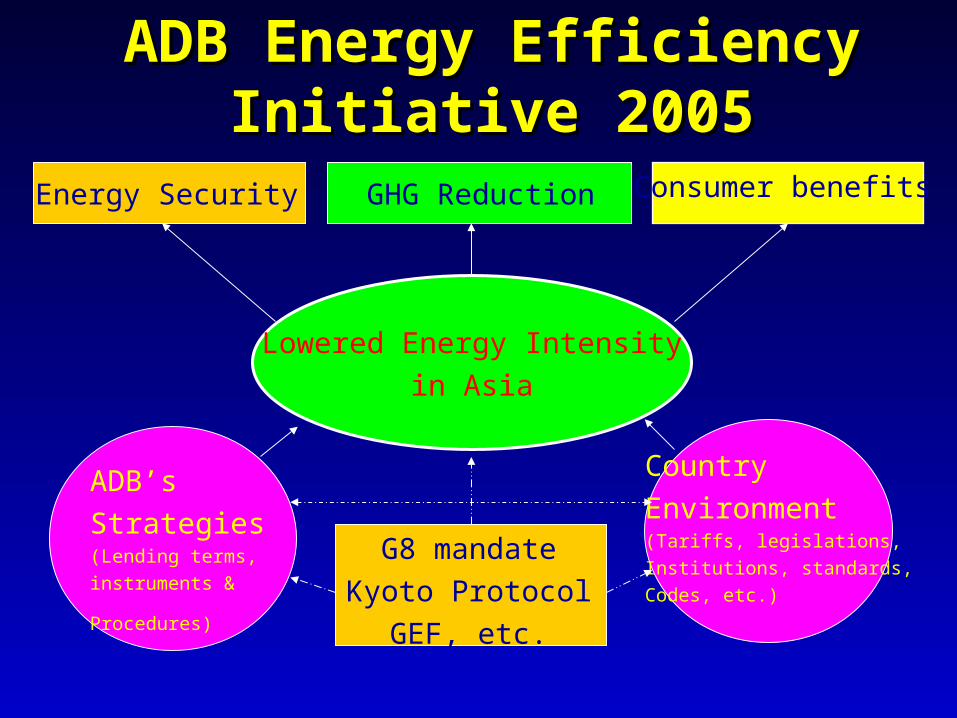

ADB Energy Efficiency ADB Energy Efficiency Initiative 2005Initiative 2005

Lowered Energy Intensityin Asia

Energy Security GHG Reduction Consumer benefits

ADB’sStrategies(Lending terms, instruments &

Procedures)

CountryEnvironment(Tariffs, legislations,Institutions, standards,Codes, etc.)

G8 mandateKyoto Protocol

GEF, etc.

ADB CDM FacilityADB CDM Facility• Set up in 2003• Honest “broker” role• Screening projects for CDM potential • Identification of potential buyers • Development of new baseline and monitoring

methodologies (if required) • Preparation of Project Design Document (PDD) • Stakeholder Consultation • Seek a Letter of Host Country Approval • Arranging validation• Negotiation of Emission Reduction Purchase Agreement

(ERPA) • Registration with CDM Executive Board • Arranging verification• Capacity Building

Renewable Energy, Energy Efficiency and Climate Change Program

(http://www.adb.org/reach)

– Netherlands Cooperation Fund for Promotion of Renewable Energy and Energy Efficiency ($6.0 million)• PREGA (TA 5972-REG) -$4.5 million

– Canadian Cooperation Fund for Climate Change (Can $5 million)

– Danish Cooperation Fund for Renewable Energy and Energy Efficiency in Rural Areas (DKK 30 million)

– Finnish TA Grant Fund (for renewable energy) (~Euro 1.8 million)

Promotion of Renewable Energy, Promotion of Renewable Energy, Energy Efficiency and Greenhouse Energy Efficiency and Greenhouse

Gas Abatement (PREGA)Gas Abatement (PREGA)

• RETA 5972 ($4.5 million) through Dutch Coop Fund

• Activities (2002-2004)- Phase 1• a. Capacity building on REGA project

preparation• b. Identification of REGA opportunities • c. Technical, financial, economic,

environmental/ GHG evaluation of projects • d. Review of barriers and policy assessment• e. Dissemination of lessons learned and

demonstration through pilot projects

• Phase 2 (2005) – additional focus on bankable projects, CDM preparation and REGA mainstreaming in financial sector

• Phase 3 (2006) – focus on fund

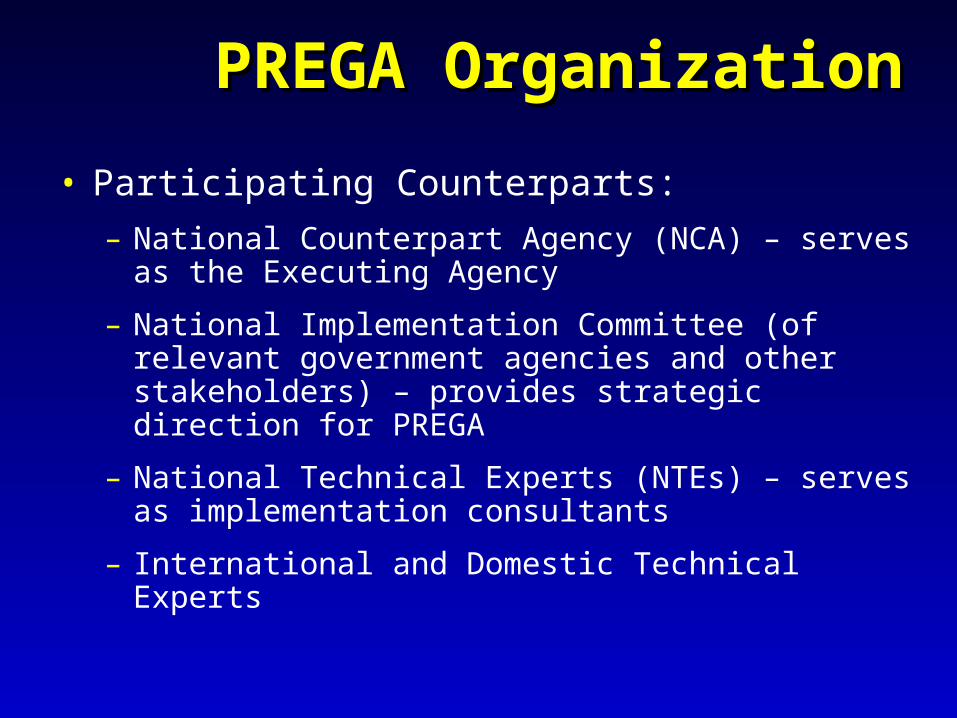

PREGA OrganizationPREGA Organization

• Participating Counterparts:

– National Counterpart Agency (NCA) – serves as the Executing Agency

– National Implementation Committee (of relevant government agencies and other stakeholders) – provides strategic direction for PREGA

– National Technical Experts (NTEs) – serves as implementation consultants

– International and Domestic Technical Experts

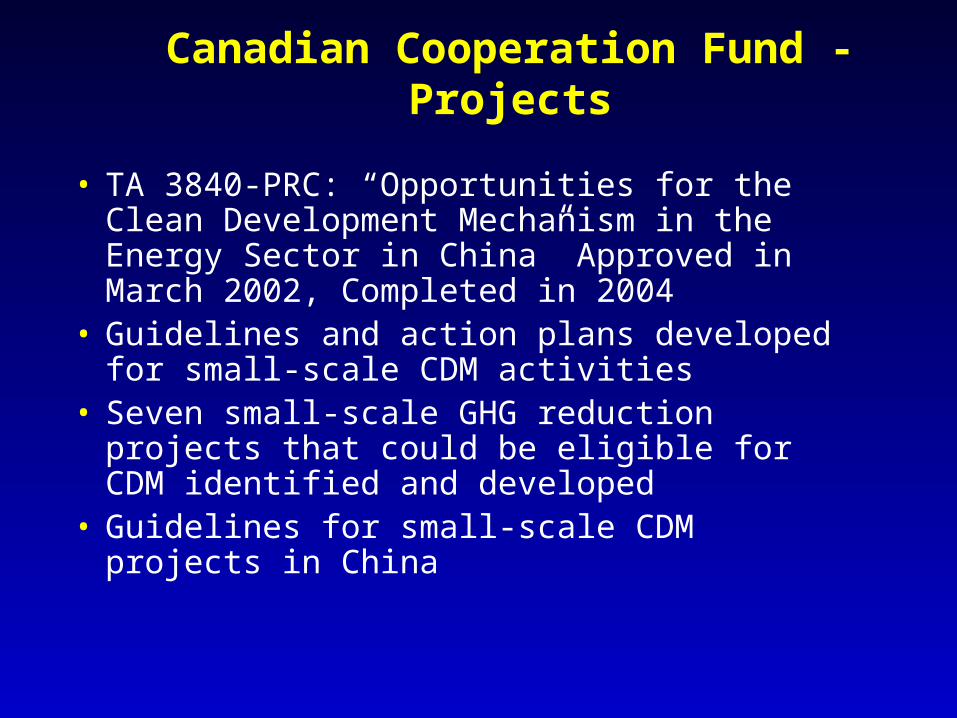

Canadian Cooperation Fund - Projects

• TA 3840-PRC: “Opportunities for the Clean Development Mechanism in the Energy Sector in China” Approved in March 2002, Completed in 2004

• Guidelines and action plans developed for small-scale CDM activities

• Seven small-scale GHG reduction projects that could be eligible for CDM identified and developed

• Guidelines for small-scale CDM projects in China

Canadian Cooperation Fund - Projects (2)

• TA-6064-REG: Climate Change Adaptation for the Pacific (ClimaP): Integrating Adaptation Measures into the Programs and Project Cycles- Approved November 2002

• TA 4137-INO: Carbon Sequestration in Indonesia- Assist Government in piloting a carbon sequestration project – Approved July 2003.

• TA 4496-IND: Capacity Building for CDM in India – approved December 2004

• TA 4333-INO: Gas Generation from Waste in Palm Oil Industry in Indonesia- approved May 2004

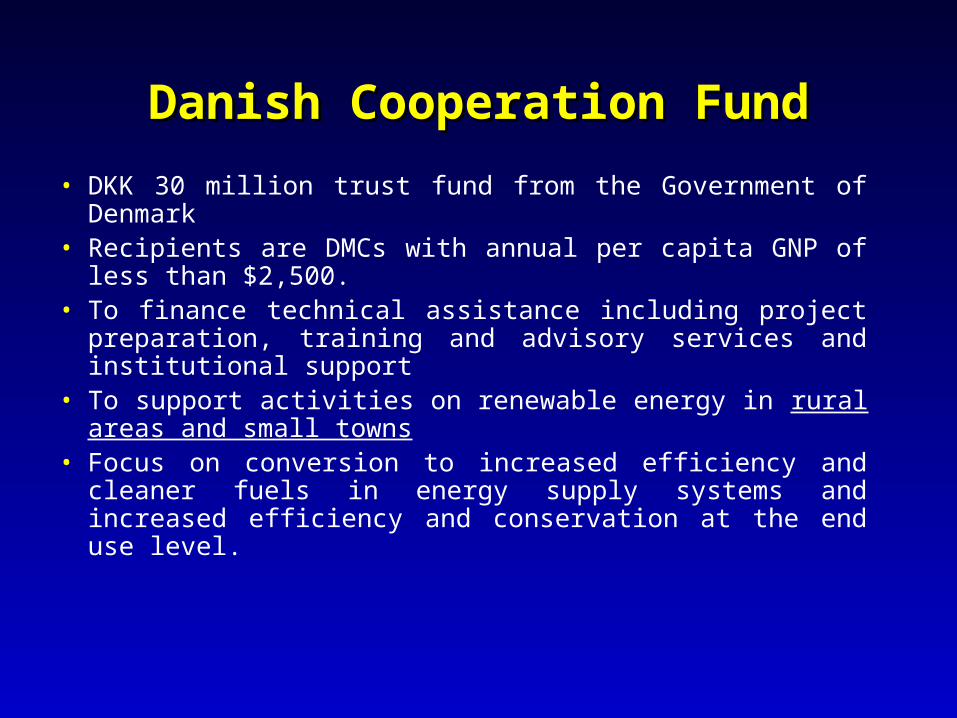

Danish Cooperation FundDanish Cooperation Fund

• DKK 30 million trust fund from the Government of Denmark

• Recipients are DMCs with annual per capita GNP of less than $2,500.

• To finance technical assistance including project preparation, training and advisory services and institutional support

• To support activities on renewable energy in rural areas and small towns

• Focus on conversion to increased efficiency and cleaner fuels in energy supply systems and increased efficiency and conservation at the end use level.

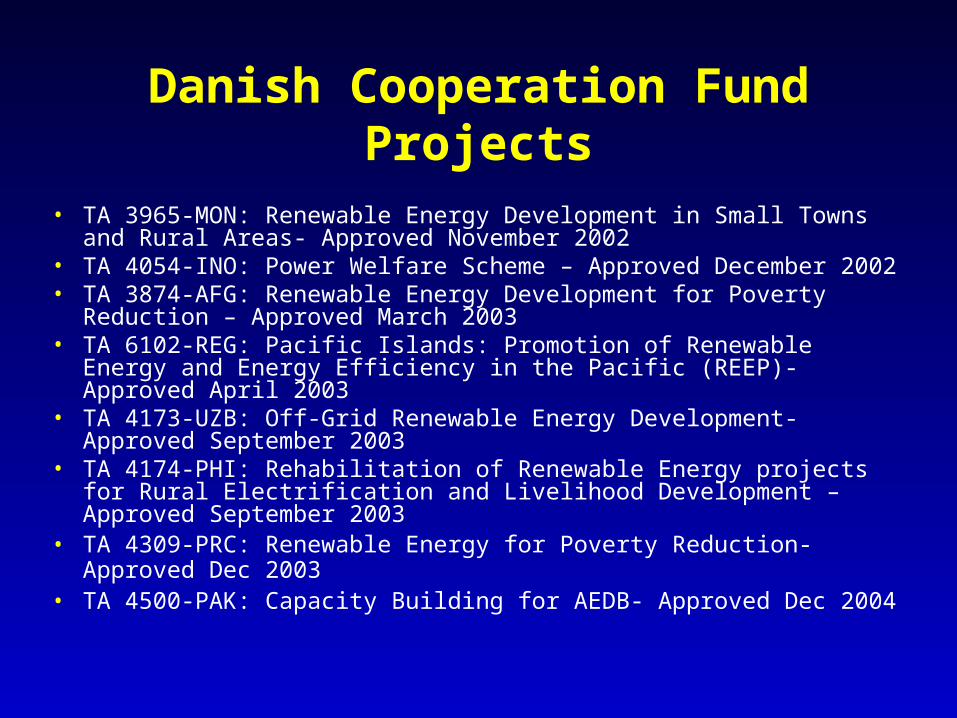

Danish Cooperation Fund Projects

• TA 3965-MON: Renewable Energy Development in Small Towns and Rural Areas- Approved November 2002

• TA 4054-INO: Power Welfare Scheme – Approved December 2002

• TA 3874-AFG: Renewable Energy Development for Poverty Reduction – Approved March 2003

• TA 6102-REG: Pacific Islands: Promotion of Renewable Energy and Energy Efficiency in the Pacific (REEP)- Approved April 2003

• TA 4173-UZB: Off-Grid Renewable Energy Development- Approved September 2003

• TA 4174-PHI: Rehabilitation of Renewable Energy projects for Rural Electrification and Livelihood Development – Approved September 2003

• TA 4309-PRC: Renewable Energy for Poverty Reduction- Approved Dec 2003

• TA 4500-PAK: Capacity Building for AEDB- Approved Dec 2004

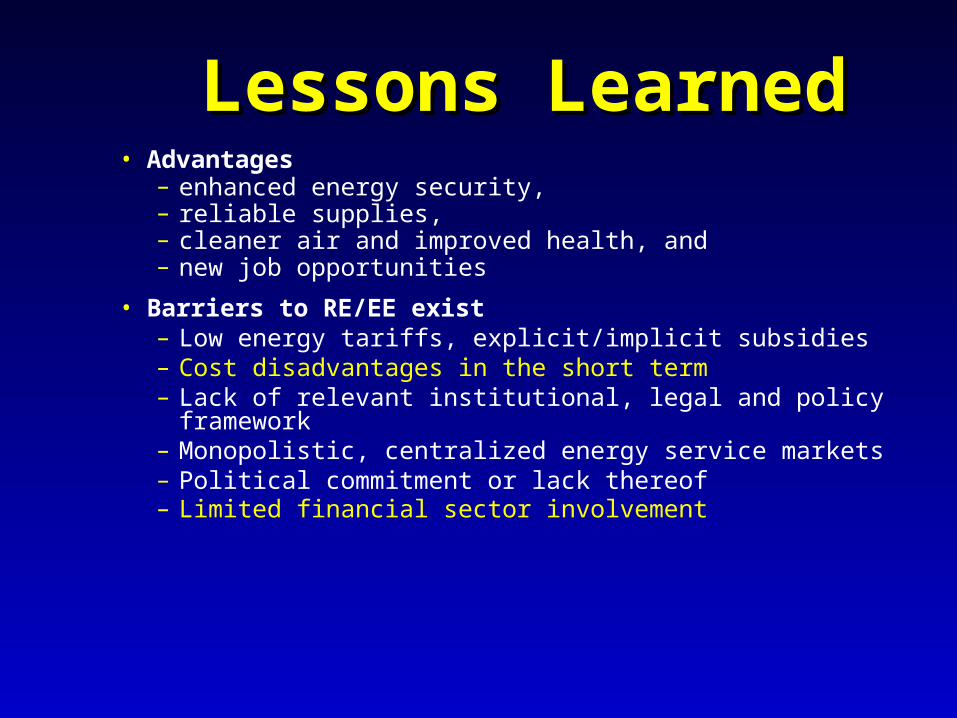

Lessons Lessons LearnedLearned

• Advantages– enhanced energy security, – reliable supplies, – cleaner air and improved health, and – new job opportunities

• Barriers to RE/EE exist – Low energy tariffs, explicit/implicit subsidies– Cost disadvantages in the short term – Lack of relevant institutional, legal and policy

framework– Monopolistic, centralized energy service markets– Political commitment or lack thereof– Limited financial sector involvement

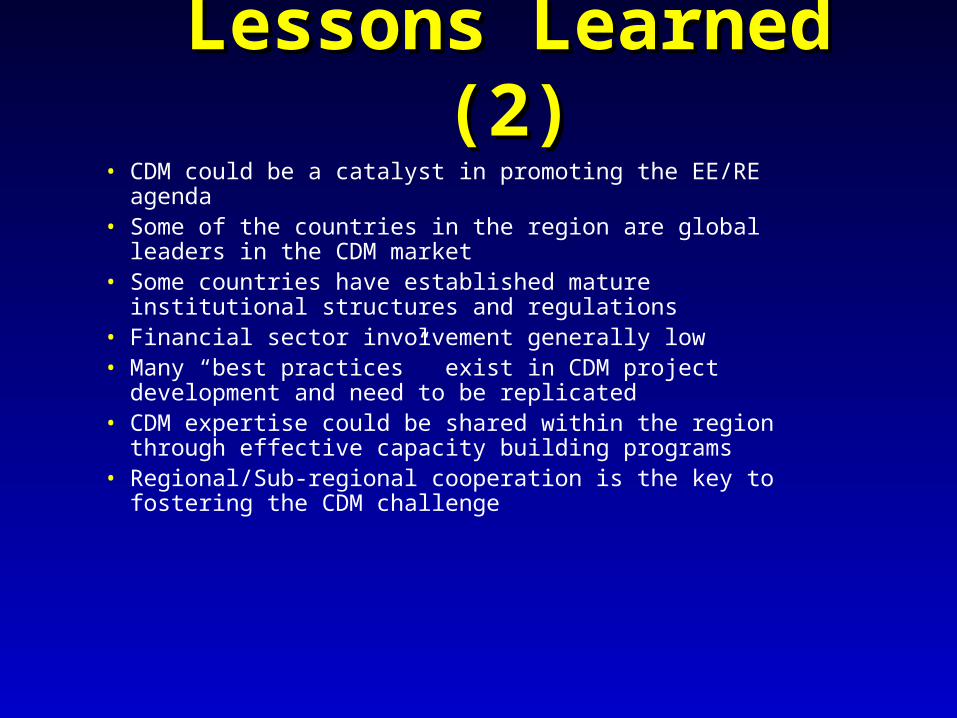

Lessons Learned Lessons Learned (2)(2)

• CDM could be a catalyst in promoting the EE/RE agenda• Some of the countries in the region are global leaders in

the CDM market• Some countries have established mature institutional

structures and regulations • Financial sector involvement generally low• Many “best practices” exist in CDM project

development and need to be replicated• CDM expertise could be shared within the region

through effective capacity building programs• Regional/Sub-regional cooperation is the key to

fostering the CDM challenge

Thank YouThank You

Ashok SarkarRegional and Sustainable Development Department

Asian Development BankP.O. Box 789, 0980 Manila, Philippines.

Tel: (63-2) 632-6624Fax: (63-2) 636-2198

E-mails: [email protected], [email protected]

Websites: http://www.adb.org/cdmf, http://www.adb.org/reach