REFILOE GLADYS BENEDICT - UJ IR

161

AN INVESTIGATION OF THE ACCOUNTING RECORDS MAINTAINED BY BLACK BUSINESSES IN QWAQWA By REFILOE GLADYS BENEDICT FULL DISSERTATION Submitted in fulfilment of the requirements for the degree MASTERS COMMERCII in ACCOUNTING in the FACULTY OF ECONOMIC AND FINANCIAL SCIENCES at the UNIVERSITY OF JOHANNESBURG SUPERVISOR: PROFESSOR D COETSEE MAY 2012

Transcript of REFILOE GLADYS BENEDICT - UJ IR

AN INVESTIGATION OF THE ACCOUNTING RECORDS

MAINTAINED BY BLACK BUSINESSES IN QWAQWA

By

REFILOE GLADYS BENEDICT

FULL DISSERTATION

Submitted in fulfilment of the requirements for the degree

MASTERS COMMERCII

in

ACCOUNTING

in the

FACULTY OF ECONOMIC AND FINANCIAL SCIENCES

at the

UNIVERSITY OF JOHANNESBURG

SUPERVISOR: PROFESSOR D COETSEE

MAY 2012

ii

DECLARATION

I hereby declare that this dissertation, submitted to the University of Johannesburg (UJ) for the

degree of Master of Commercial in Accounting has not been previously submitted by me for any

degree at any University elsewhere. I confirm that this study is a product of my own work in

design and execution and that all the material contained in it has been duly acknowledged.

Name……………………

Signed……………………

Date……………………..

iii

DEDICATION

To God be the glory for all the great things He has done.

This dissertation is dedicated to my wonderful husband,

Olumide Henrie;

and my beautiful children

Korede Lehlohonolo, Ibunkun Rorisang and Opefoluwa Bokang

may our lives as a family be filled with affection,

happiness and the love of God…Amen

iv

ACKNOWLEDGEMENTS

I thank the almighty God for keeping me alive till today and seeing me through my endeavours.

I will always be indebted to you and love you all the days of my life. With much respect and

appreciation, I thank my supervisor Professor D. Coetsee. You were very thorough in the

scrutiny my work and constructive in your recommendations and amendments. Thank you for

your inspiration.

To my wonderful families: the Makobanes and the Benedicts. I don’t know how to start

expressing my gratitude to you. For your love, guidance, discipline, support and, most especially,

your prayers, I thank you. May God preserve your lives and keep you. Also, thank you to my

siblings. I love you all. I thank my entire extended family.

Warm regards to all my respondents, without whose cooperation this study would not have been

possible. Thank you for taking time to answer the questions. I am keeping my promise and the

responses are strictly for research purposes.

To my research assistants, friends and helpers, Shibe (Angie), Pusheletso (Pushi), Ronel and her

Husband, Gissele (Gisy), Thembekile (Thembi) and others, I do not underestimate your

contributions. I recognise, respect and thank you. To my colleagues at work, I thank you for your

immense contributions and understating.

I acknowledge the contribution of the Research Development Office of the University of

Johannesburg, for supporting and funding this research, together with the National Research

Fund (NRF). Special thanks and recognition to the Head of our Department, Mr. Dirkie van Der

Watt, for his understanding and quick responses to enquiries. I respect you. Keep up the good

work!

Last but not the least, I thank the University of Johannesburg. “You’re the best”. I acknowledge

the support and constant empathy from the administrative and library staff. To all whose names I

did not mention, also thanks – I acknowledge every one of you from my heart.

v

ABSTRACT

Towards addressing the detrimental economic effects past dispensations had on the marginalized

majority, different Government initiatives and other interventions have been put in place to

encourage the participation of Blacks in the economy of South Africa. These development

initiatives seek to address poverty and unemployment levels, some focussing on growing small,

medium, and micro enterprises (SMMEs). Growth and sustainability of such businesses can only

be achieved through the maintenance of appropriate financial information, on which economic

decisions are based, but such information can only be generated or processed if relevant and

adequate accounting data, through accounting recordkeeping, are maintained.

The study examines whether this is also applicable to micro or survivalist businesses, and was

carried out to investigate the accounting records maintained by small Black-owned businesses in

QwaQwa. In the literature study it became vital to elucidate the uniqueness of micro and

survivalist businesses as they are often generalised under the rather broad umbrella of the term

‘SMMEs’. The literature further indicates that there is no prescribed regulation or framework

specifically for accounting recordkeeping in micro and survivalist businesses.

The dissertation analyses responses to questionnaires administered to a purposively selected

sample of 88 small Black-owned businesses in QwaQwa, and interpreting 44 respondents

interviewed. The interviews became necessary due to insufficient responses to the section in the

questionnaires addressing the third research objective. Hence, both a quantitative and a

qualitative research design were eventually used. Data collection took place at respondents’

business premises. Responses to the questionnaires were analysed using Statistical Package for

the Social Sciences (SPSS), which was used to generate descriptive statistics. The researcher

documented the interview proceedings in written format. Common responses from interviews

were clustered in themes then interpreted.

Results show that small Black-business owners maintain some basic form of accounting records

such as sales records, payment records and stock records, however, since they operate mainly on

the cash basis, debtors’ and creditors’ records were seldom maintained. These findings are

vi

consistent with previous studies into the kind of accounting records maintained by small

businesses. Small Black-business owners also perceived maintaining accounting records to be

important in determining the profitability and future sustainability of their businesses.

These owners, however, demonstrated limited understanding of accounting concepts and

principles or how these applied to their business. They identified a need for some form of

interventions to improve their knowledge of accounting recordkeeping and risk management. A

further need identified was the availability of funds to finance their businesses. Therefore,

financial help together with training and development are needed to better their businesses. This

may go a long way in improving growth and stability, as well as reducing the poverty and

unemployment rate in the country.

In order for micro and survivalist business owners to realise some of the benefits of maintaining

relevant accounting records, it is recommended that the owners are trained on how to keep basic

accounting records that are useful and easy to convert into accounting information, and that may

add value to their businesses and ensure the monitoring of profitability and sustainable growth.

vii

TABLE OF CONTENTS

PAGE

LIST OF TABLES xv

LIST OF FIGURES xvii

LIST OF ACRONYMS xix

CHAPTER 1: BACKGROUND, OBJECTIVES AND SCOPE OF DISSERTATION 1

1.1 Introduction 1

1.2 Small businesses in South Africa 1

1.3 Motivation for study 2

1.4 Statement of the problem 3

1.5 Research question 4

1.6 Research objectives 4

1.7 Research structure 6

1.8 Methodology 7

1.9 Significance of the dissertation 7

1.10 Delimitation of the dissertation 8

1.11 Outline and structure of the chapters 8

1.12 Conclusion 11

CHAPTER 2: LITERATURE REVIEW 12

2.1 Introduction 12

2.2 Black involvement in the economy 14

viii

2.3 Empowerment and black economic empowerment 15

2.3.1 Legislation 16

2.3.2 Broad-Based Black Economic Empowerment 17

2.3.3 Empowerment initiatives and shortcomings 18

2.3.4 Conclusion 20

2.4 Description, classification and nature of small businesses 21

2.4.1 Definition and classification of small businesses 21

2.4.2 Formal and informal businesses 24

2.4.3 Importance of small businesses 26

2.5 Financial management for small business 30

2.6 Financial reporting 32

2.6.1 Applicability of financial statements to big and small businesses 36

2.6.2 Differential reporting 36

2.6.3 Conclusion 41

2.7 Financial accounting records and bookkeeping 42

2.7.1 Nature of accounting records 42

2.7.2 Importance of records and bookkeeping 43

2.7.3 Financial accounting records that should be kept by small businesses 44

2.7.3.1 Cash records and bank account 46

2.7.3.2 Sales/revenue records 47

2.7.3.3 Debtors records 48

2.7.3.4 Purchases records 48

2.7.3.5 Creditors records 49

ix

2.7.3.6 Wages and salaries 49

2.7.4 Conclusion 49

2.8 Need for training in accounting 50

2.9 Conclusion 51

CHAPTER 3: RESEARCH METHODOLOGY 53

3.1 Introduction 53

3.2 Research objective 53

3.3 Research methodology 54

3.4 Research design 55

3.4.1 The research instruments 55

3.4.1.1 The questionnaire 56

3.4.1.2 The interviews 57

3.4.2 Data analysis and interpretation 58

3.4.3 Scientific Validity 58

3.5 Method of sampling 60

3.5.1 Sampling and source of data 60

3.5.2 Recruitment, participation and ethical issues 62

3.6 Conclusion 62

CHAPTER 4: PRESENTATION AND DISCUSSION OF QUSTIONNNAIRES 64

4.1 Introduction 64

4.2 The questionnaire 64

x

4.3 Section A: General Information 65

4.3.1 Gender of respondents 65

4.3.2 Age of Respondents 67

4.3.3 Qualification 68

4.3.4 Conclusion 69

4.4 Section B: Nature of business 69

4.4.1 Existence of the business 69

4.4.2 Type of ownership 71

4.4.3 Type of industry 72

4.4.4 Means of starting business 73

4.4.5 Conclusion 74

4.5 Section C: Accounting records 75

4.5.1 Banking facilities 75

4.5.1.1 Customer payment 75

4.5.1.2 Banking facilities 76

4.5.1.3 Type of bank account 77

4.5.1.4 Internet banking 78

4.5.1.5 Telephone banking 79

4.5.1.6 Bank card 80

4.5.2 Conclusion on banking 81

4.5.3 Accounting records 82

4.5.3.1 Recording revenue 82

4.5.3.2 Recording of expenses 83

xi

4.5.3.3 Debtors and creditors records 85

4.5.3.4 Cash book 87

4.5.3.5 Frequency of preparation of financial statements 88

4.5.3.6 Financial statements 89

4.5.3.6.1 Statement of financial position (Balance sheet) 90

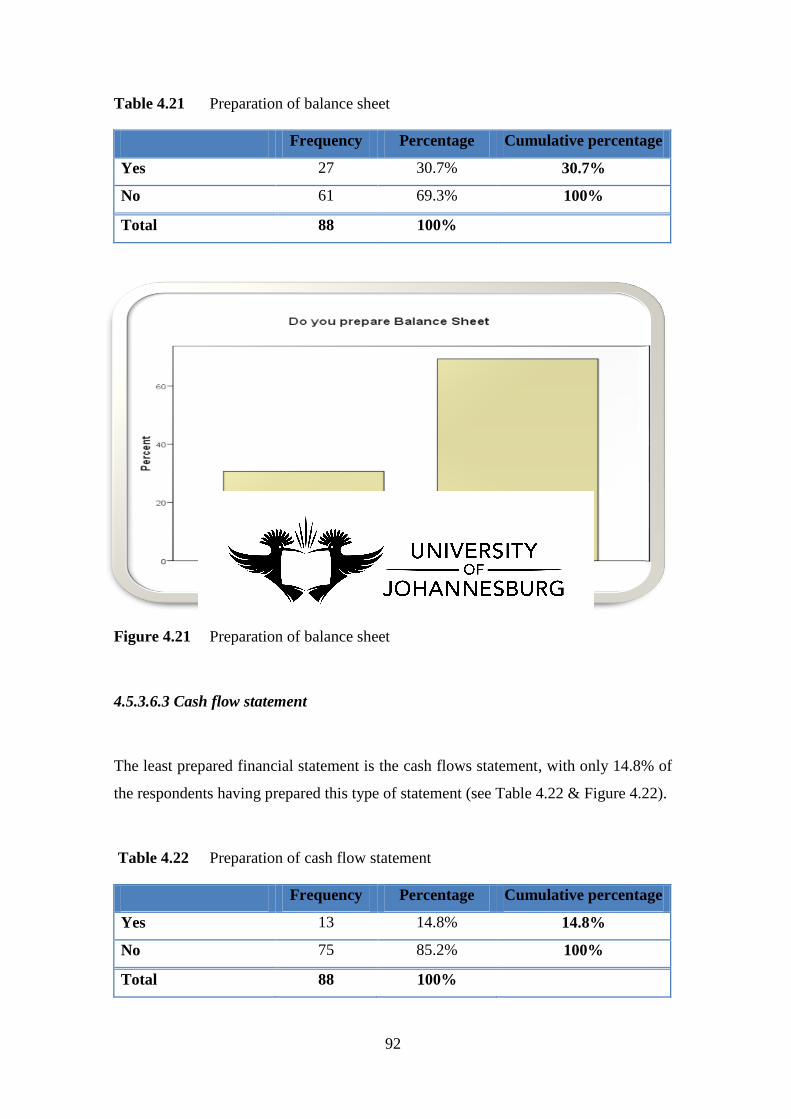

4.5.3.6.2 Cash flow statement 91

4.5.4 Conclusion 92

4.6 Section D: Finance 93

4.6.1 Purpose of financial statement 94

4.6.2 Funding of business 95

4.6.3 Start-up funding of business 96

4.6.4 Conclusion 97

4.7 Section E and F 98

4.8 Conclusion 98

CHAPTER 5: PRESENTATION AND DISCUSSION OF INTERVIEWS 100

5.1 Introduction 100

5.2 Research method and presentation 101

5.3 Presentations and discussions based on interviews 102

5.3.1 Type of accounting records 102

5.3.2 Perception regarding accounting records 103

5.3.2.1 Question 103

5.3.2.2 Descriptive presentation of results 103

5.3.2.3 Interpretation: Perception regarding accounting records 105

xii

5.3.3 Perception regarding management of financial risks 106

5.3.3.1 Question 106

5.3.3.2 Descriptive presentation of results 106

5.3.3.3 Interpretation: Perception regarding management of financial risks 108

5.3.4 Perception regarding the respondents’ knowledge 108

5.3.4.1 Question 108

5.3.4.2 Descriptive presentation of results 109

5.3.4.3 Interpretation: Perception regarding respondents’ knowledge 110

5.3.5 Perception regarding the respondents’ knowledge 111

5.3.5.1 Question 111

5.3.5.2 Descriptive presentation of results 111

5.3.5.3 Interpretation: Perception regarding respondents needs 113

5.4 Conclusion 113

CHAPTER 6: RECOMMENDATIONS AND CONCLUSION 115

6.1 Introduction 115

6.2 The literature review 116

6.3 Questionnaires 117

6.4 Interviews 117

6.5 Conclusion 118

6.6 Recommendations 120

6.6.1 Accounting training 120

6.6.2 University engagement with informal micro and survivalist businesses 120

xiii

6.6.3 A simple, relevant and comparable guideline for micro businesses 120

6.6.4 Database for informal businesses 121

6.7 Further Research 121

REFERENCE LIST 123

APPENDICES 135

Appendix 1 Questionnaire 135

xiv

LIST OF TABLES

Table 1.1 Research structure 6

Table 2.1 Categories of SMMEs (National Small Business Act, 2004) 23

Table 2.2 Government Development Institution for Small Business

(Agupusi, 2007:6) 29

Table 2.3 Financial reporting standards and application to categories 37

Table 3.1 Objectives 2 and 3 of the dissertation and the instruments used 56

Table 4.1 Sections of the Questionnaire 65

Table 4.3 Ages of Respondents 67

Table 4.4 Highest Qualification 68

Table 4.5 Existence of the business 70

Table 4.6 Type of ownership 71

Table 4.7 Type of industry 72

Table 4.8 Means of starting business 74

Table 4.9 Customer payment 75

Table 4.10 Banking facilities 77

Table 4.11 Use of internet banking facilities 78

Table 4.12 Use of telephone banking 80

Table 4.13 Use of credit card facilities 81

Table 4.14 Recording of revenue 82

Table 4.15 Recording of expenses 84

Table 4.16 Records of debtors 85

xv

Table 4.17 Recording of creditors 86

Table 4.18 Maintaining cash book 87

Table 4.19 Frequency of preparing financial statement 88

Table 4.20 Preparation of income statement 89

Table 4.21 Preparation of balance sheet 91

Table 4.22 Preparation of cash flow statement 91

Table 5.1 Importance of maintaining accounting records 104

Table 5.2 Financial risk management 107

Table 5.3 Knowledge of maintaining accounting records 110

Table 5.4 Training needs 112

xvi

LIST OF FIGURES

Figure 1.1 Focus of the study 6

Figure 2.1 First and Second Economies (DTI, 2004) 25

Figure 2.2 Links between Accounting Records and Financial Statements

(based on elements of financial statements) 33

Figure 2.3 Barriers of applicability is IFRS for SMEs 40

Table 3.2 Features of Qualitative & Quantitative Research (Neil, 2007) 59

Figure 4.2 Genders of Respondents 66

Figure 4.3 Ages of Respondents 67

Figure 4.4 Highest Qualification 68

Figure 4.5 Existence of the business 70

Figure 4.6 Type of ownership 72

Figure 4.7 Type of industry 73

Figure 4.8 Means of starting business 74

Figure 4.9 Customer payment 76

Figure 4.10 Banking facilities 78

Figure 4.11 Use of internet banking facilities 79

Figure 4.12 Use of telephone banking 80

Figure 4.13 Use of credit card facilities 81

Figure 4.14 Recording of revenue 83

Figure 4.15 Recording of expenses 84

Figure 4.16 Records of debtors 85

Figure 4.17 Recording of creditors 86

xvii

Figure 4.18 Maintaining cash book 87

Figure 4.19 Frequency of preparing financial statement 88

Figure 4.21 Preparation of balance sheet 91

Figure 4.22 Preparation of cash flow statement 92

Figure 5.1 Importance of maintaining accounting records 104

Figure 5.2 Financial risk management 107

Figure 5.3 Knowledge of maintaining accounting records 110

Figure 5.4 Training needs 112

Figure 6.1 Empirical situation of the focus of dissertation 119

xviii

LIST OF ACRONYMS

ANC African National Congress

ASGI-SA Accelerated and Shared Growth Initiative

BBBEE Broad-Based Black Economic Empowerment

BEE Black Economic Empowerment

CIPC Companies and Intellectual Property Commission

DTI Department of Trade and Industry

ETU Education and Training Unit

FDC Free State Development Corporation

FRS Financial Reporting Standards

GAAP Generally Accepted Accounting Practice

GEP Gauteng Enterprise Propeller

GNP Gross National Product

IASB International Accounting Standard Board

ICT Information and Communication Technologies

IDC Industrial Development Commission

IFRS International Financial Reporting Standards

NEF National Empowerment Fund

PFMA Public Finance Management Act

RSA Republic of South Africa

SAMAF South African Micro Fund Apex Fund

SARS South African Revenue Services

xix

SEDA Small Enterprises Development Agency

SMEs Small Medium Enterprises

SMMEs Small Medium Micro Enterprises

SPSS Statistical Package for the Social Sciences

UK United Kingdom

USA United States of America

VAT Value Added Tax

1

CHAPTER 1

BACKGROUND, OBJECTIVES AND SCOPE OF DISSERTATION

1.1 INTRODUCTION

This dissertation is an investigation of the financial accounting records maintained by small

Black-owned businesses in the rural area of QwaQwa in the Free State Province of South

Africa, hereafter referred to as QwaQwa. This chapter presents the background to the

dissertation, the rationale behind it, and the research problem. It further highlights the

research questions and objectives which will later serve as a guide in developing the research

data collection instruments, namely the questionnaire and structured interviews. Finally, it

demarcates the field of study and outlines the structure of the dissertation.

1.2 SMALL BUSINESSES IN SOUTH AFRICA

De Farias, Nataraajan and Kovacs (2009:1) pointed out that small business, including those

that are solely owned, family owned and sometimes partnerships, are becoming an area of

focus in the economic development of most countries. In South Africa, coupled with

legislation on redistribution of wealth, affirmative action and post-apartheid governance,

small businesses (especially those of previously disadvantaged groups) are being given

considerable attention (Edigheji, 2004: 11). Many studies (Cahan & Van Staden, 2009;

Rwigema & Venter, 2005; Brink, Cant & Lighthelm, 2003), which have generated different

findings, have been conducted on small businesses in South Africa. Access to capital or start-

up funds is just one of the many persistent problems that small Black-owned businesses face

(Allee & Yohn, 2009; Drew, 2007a). To overcome this challenge, many have participated in

augmented loan programmes (Beech, 1997:1), some of which are administered by private

institutions, banks and government institutions.

2

Identified problems, which are relevant to the current study, include lack of managerial

competences (Van Auken, 2001:242), and a lack of knowledge and use of financial

information (Allee & Yohn, 2009:2). These authors claim that these factors may result in the

taking of wrong economic decisions that affect the business adversely.

In QwaQwa, the geographical focus of this dissertation, one of the major institutions, apart

from the commercial banks, that provide Black entrepreneurs with finance is the Free State

Development Corporation (FDC). This was established during preliminary investigations.

Nevertheless, it may be the case that access to finance fails to solve all the problems faced by

small businesses. The use and knowledge of financial information is important, and the

researcher believes that a small business owner can have financial information only if some

form of accounting record is maintained. Hence, this serves as the main motivation for the

research. This opinion is backed by Rajaram and O’Neill (2009:100), who argue that these

business owners need to have “the knowledge and accounting skills” to confidently ascertain

the “fundamental question” of whether or not their businesses are making a profit.

1.3 MOTIVATION FOR THE STUDY

The importance of accounting records as a basis for financial information (Rajaram &

O’Neill, 2009:100), as well as the researcher’s previous interaction with some business

owners in QwaQwa, provide the basic motivations for this study. The researcher’s attention

was drawn to this topic because of the role of small businesses in the sustainable

empowerment and eradication of poverty amongst Black people in the rural area of QwaQwa.

The area is also convenient and cost-effective for the researcher to gather information

because it was the researcher’s place of permanent residence. It is important to also state that

the researcher took part in a community service initiative that entailed helping and teaching

small businesses in QwaQwa how to keep accounting records of their businesses. This

initiative also exposed the researcher to the need of investigating what financial accounting

records are being maintained by these Black-owned small businesses. The study into these

matters is intended to locate needs for better practices or training.

3

It is the researcher’s opinion that investigating the accounting records of these businesses and

understanding their owners’ perceptions on the importance of accounting information may be

helpful in recommending interventions that may contribute towards their sustainability and

long-term success. In this way, the researcher therefore hopes that this dissertation may be

able to assist, in creating more awareness among entrepreneurs of the importance of keeping

accounting records for small businesses.

Preliminary investigations also identified a need for better management of small businesses.

Although business plans and marketing research may have been prepared and presented, it

seems that the majority of these small Black business owners lack the accounting skills to

record, control, report and manage their finances and business transactions (FDC, 2006). The

study therefore also aims to fill a knowledge gap, as although there is a wealth of existing

knowledge about small businesses and their importance to the economy, little research has

been conducted on micro businesses or the type of accounting records that they keep. As will

be seen in the literature review, studies already conducted on the accounting recordkeeping of

small businesses have received little attention compared to those on financial statements of

formal businesses, e.g., companies and registered small businesses.

1.4 STATEMENT OF THE PROBLEM

The problem in this dissertation is twofold: to investigate and evaluate the financial

accounting records maintained by small Black-owned businesses in QwaQwa, and to gather

their perceptions on the importance of maintaining financial accounting records.

A preliminary study, through non-scheduled interviews with FDC and small Black-owned

businesses in QwaQwa, coupled with observations of the industrial areas and commercial

venues, showed that small Black businesses in the rural area were facing many difficulties in

remaining profitable and sustainable. Possible reasons for this were considered to be lack of

proper financial information at their disposal and absence of accounting records.

4

1.5 RESEARCH QUESTIONS

Having stated the research problem and explained the background and motivation of this

study, it is important to clarify the research questions (Badenhorst, 2010:26). The following

three research questions were posed in this dissertation:

1. What financial accounting records should be maintained by small businesses?

2. What financial accounting records do small Black-owned businesses in the rural area of

QwaQwa maintain?

3. How important do small Black-owned businesses in QwaQwa perceive the maintaining

of financial accounting records to be?

1.6 RESEARCH OBJECTIVES

Bak (2004:16) suggested that research objectives may either be academic (primarily to fill

knowledge gaps) or strategic (non-academic audiences). The objectives here are both primary

and strategic as they fill the knowledge gap about small Black-owned businesses in QwaQwa,

and the findings may also be useful for policymakers. The three research questions that were

earlier identified resulted in the following research objectives:

1. To explain, through the use of relevant literature, the nature of the financial

accounting records that should be maintained by small businesses.

2. To investigate what financial accounting records are being maintained by small

Black-owned businesses in QwaQwa.

3. To understand how small Black-owned businesses in QwaQwa perceive the

importance of maintaining financial accounting records.

5

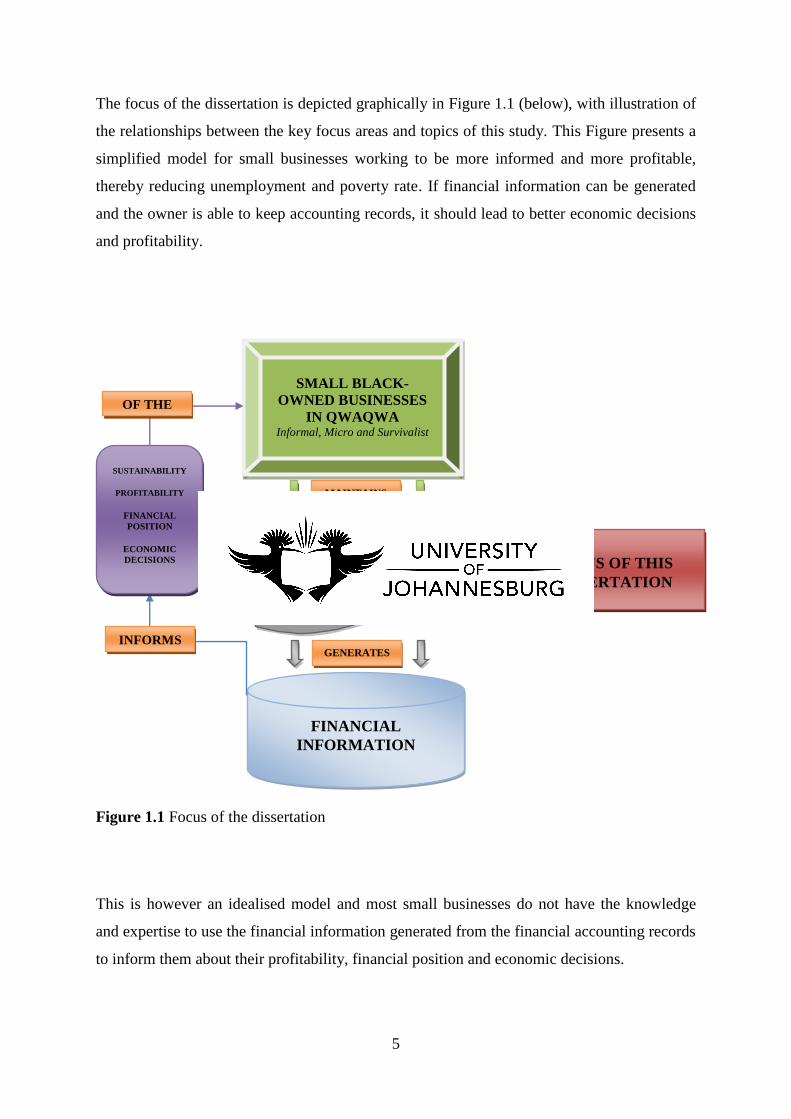

The focus of the dissertation is depicted graphically in Figure 1.1 (below), with illustration of

the relationships between the key focus areas and topics of this study. This Figure presents a

simplified model for small businesses working to be more informed and more profitable,

thereby reducing unemployment and poverty rate. If financial information can be generated

and the owner is able to keep accounting records, it should lead to better economic decisions

and profitability.

Figure 1.1 Focus of the dissertation

This is however an idealised model and most small businesses do not have the knowledge

and expertise to use the financial information generated from the financial accounting records

to inform them about their profitability, financial position and economic decisions.

SMALL BLACK-

OWNED BUSINESSES

IN QWAQWA Informal, Micro and Survivalist

FINANCIAL

ACCOUNTING

RECORDS

FINANCIAL

INFORMATION

FOCUS OF THIS

DISSERTATION

MAINTAINS

GENERATES

INFORMS

SUSTAINABILITY

PROFITABILITY

FINANCIAL

POSITION

ECONOMIC

DECISIONS

OF THE

6

1.7 RESEARCH STRUCTURE

A logical research process is followed in this dissertation, which may serve as a tool for easy

understanding and cross-referencing. The problem statement has been broken down into three

research questions, then research objectives formulated in such a manner that, if they are

achieved, they will provide answers to the research questions. The research objectives are

achieved at different stages of this dissertation. The first objective, to explain the use of

financial accounting records in small businesses, is the subject of Chapter 2, the literature

review. The second, to investigate the accounting records of the population, is researched

through the use of a questionnaire as the research instrument in Chapter 4. The last research

objective, to identify the perceptions of the respondents about the importance of maintenance

accounting records, is researched through the use of structured interviews in Chapter 5. Table

1.1 (below) lays out the structure of this dissertation:

Table 1.1: The structure of this dissertation by objective and chapter

Objective Research Question Chapter Linkage Data Collection

Objective 1

To explain, through the

use of relevant literature

and past researches, the

nature of the financial

accounting records that

should be maintained by

small businesses

Research Question 1:

What financial

accounting records

should be maintained by

small businesses?

Chapter 2:

Literature Review

Secondary Data:

Literature Review

Objective 2

To investigate what

financial accounting

records are being

maintained by small

Black-owned businesses

in the rural area of

QwaQwa

Research Question 2:

What financial

accounting records do

small Black-owned

businesses in the rural

area of QwaQwa

maintain?

Chapter 4:

Presentation and

Discussion of

Questionnaire

Primary Data:

Questionnaire

7

Objective 3

To understand how

small Black-owned

businesses in the rural

area of QwaQwa

perceives the importance

of maintaining financial

accounting records

Research Question 3:

How important do small

Black-owned businesses

in QwaQwa perceive the

maintaining of financial

accounting records to

be?

Chapter 5:

Presentation and

Discussion of Interviews

Primary Data:

Interviews

The initial plan was to obtain all the data through the questionnaire, however, it was

discovered that some sections (E & F) of the questionnaires, which required open-ended

responses, were not appropriately completed by the respondents and so could not be

subjected to meaningful interpretation. Hence, it became necessary to introduce the interview

method of obtaining information from the respondents. Through structured interviews, it was

possible to gather information needed to answer the third question pertaining to the perceived

importance of maintaining financial accounting records.

1.8 METHODOLOGY

For the purpose of this study, data was collected through a questionnaire and interviews. The

questionnaire items were informed by the literature review and collected data analysed in the

form of descriptive statistics and interpretative analyses. A more comprehensive explanation

of the research design and methodology is in Chapter 3.

1.9 SIGNIFICANCE OF THE DISSERTATION

It is anticipated that the findings in this dissertation could provide more insight into the types

of financial accounting records maintained by small Black-owned businesses. The researcher

also believes and wishes that the findings of the dissertation will improve the understanding

of financial accounting records that are maintained in small businesses in QwaQwa. This

understanding may lead to interventions which may foster more profitability and sound

economic decision-making by small Black-owned businesses. These may be possible if these

8

business owners become more aware of the usefulness of the financial information that may

be generated from accounting records and its impact on profitability and the continued

existence of their businesses.

1.10 DELIMITATIONS OF THE DISSERTATION

An academic dissertation at this level is usually limited to a narrow scope, for which reason

the research focused on selected businesses of the broad sector of the Black-owned

businesses in QwaQwa. It should also be noted that only such businesses were visited and, as

such, the results of this dissertation may not be generalized and consequently applied to all

the small Black-owned businesses throughout South Africa. For the purpose of this

dissertation, the term “Black” only refers to Africans, excluding Indians and Coloureds.

Even though references may be made to small, medium, and micro enterprises (SMMEs), for

the purpose of this dissertation the term ‘small businesses’ refers to survivalist enterprises

and micro businesses (more clarification on this is provided in Chapter 2). Such businesses

are of an informal nature, and carry on business mainly for survival, generally defined as

providing income below the poverty line (DTI, 2005). According to Van der Nest (2004:36),

the government has identified the importance of separating the small and medium entities

from the micro and survivalist ones.

1.11 OUTLINE AND STRUCTURE OF THE CHAPTERS

The outline of the dissertation is as follows:

Chapter One – Introduction:

Chapter One of the dissertation contains the introductory background to the dissertation and

the statement of the research problem. The need for the dissertation and its significance are

9

clearly stated, with a comprehensive explanation of the rationale, aims and objectives, as well

as demarcation of the topic.

Chapter Two - Literature Review:

Chapter Two provides a review of related literature on the subject, from different authors and

researchers who have carried out similar and relevant studies. This chapter is divided into

sections and subsections that address: the description, nature, classification and importance of

small businesses; the development of small businesses in South Africa; the role of economic

empowerment; financial management for small businesses; differential reporting; the nature

and importance of financial accounting records; and the financial accounting records

applicable to small businesses. The literature review forms a significant part of this

dissertation as it serves as a source of information for the data instruments. All references are

duly acknowledged in the reference list. This chapter focuses on the first research objective:

to explain, through the use of relevant literature and research, the nature of the financial

accounting records that should be maintained by small businesses.

Chapter Three - Research Design:

Chapter Three focuses on the research design used in tackling the last two research

objectives, and describes the methodology used in this research, namely the sampling

methods, the population, the data collection methods and the research instruments used in the

data analysis process.

Chapter Four - Presentation and Discussion of Questionnaire:

Since the questionnaire is mainly quantitative in nature, the results presented in Chapter Four

are mainly as percentages and figures. This was further explained through discussions that

supported the analyses of the findings of the questionnaires. The questionnaire emanated

from the statement of the research problem as well as the ensuing research questions.

Specifically, the second research objective of investigating: to investigate what financial

10

accounting records are being maintained by small Black-owned businesses in QwaQwa was

addressed in this chapter.

Chapter Five - Presentation and Discussion of Interviews:

As stated above, some interviews were conducted to elicit more qualitative information from

respondents. The questions posed were replicas of the ones not satisfactorily answered in the

questionnaire. The discussion in Chapter Five details the outcome of the conducted

interviews. As with the questionnaire, the interview schedule was guided towards addressing

the applicable research objective as well as the research question (i.e., Objective No.3 and

Question No.3).

The five questions posed in the interviews were:

1. Which type of financial records do you keep?

2. What is your perception of the importance of maintaining efficient accounting records?

3. Explain how you manage your financial risks?

4. Do you have the knowledge to maintain efficient accounting records and to manage

your financial risks?

5. What are your needs (if any) to be able to control and manage your business

effectively?

Particularly, the focus of the interviews relates to research objective three, namely: to

understand how small Black-owned businesses in QwaQwa perceive the importance of

maintaining financial accounting records.

11

Chapter Six - Conclusions and Recommendations:

Chapter Six draws a broad conclusion to the whole document. Some recommendations were

made and directed towards the small black-owned businesses. The chapter also indicates

possible further research that may follow from this particular dissertation.

1.12 CONCLUSION

This chapter has served as an introduction to the research report. The background and the

statement of the research problem were discussed extensively, with explanation of the

rationale, objectives and the importance of the dissertation. In so doing, the statement of the

problem and the purpose of the dissertation were also explained. The dissertation investigates

the financial accounting records that are maintained by small Black-owned businesses

(mainly micro and survivalist) in QwaQwa. To address the research problem, three research

questions were posed.

Using a structured table, this chapter also explained how the three research objectives were to

be achieved and how they relate to each respective chapter. The findings in this dissertation

should add to the body of knowledge on matters relating to Black-owned businesses and may

inform policymakers’ intervention initiatives. The main focus of the study was illustrated in

Figure 1.1, on accounting records maintained by small businesses that are survivalist and

informal. In the next chapter, literature and research that have already been carried out on

related research topics are reviewed.

12

CHAPTER 2

LITERATURE REVIEW

2.1 INTRODUCTION

This chapter reviews literature on the definition, nature, importance of and accounting

recordkeeping of small businesses. Despite some aspects of this chapter making reference to

Small, Medium, and Micro Enterprises (SMMEs), which include survivalist, micro, very

small, small, and medium enterprises, the focus is on survivalist and micro businesses, as

stated in the delimitation section of the previous chapter.

This chapter provides an overview of the literature on small businesses in South Africa and

their financial accounting records, having served as a background to the questionnaire and

interviews used in the collection of data. There is therefore a link between this chapter and

the items in the data collection instrument, broken down into specific aspects of the research

problem that move from the more general, Black involvement, to the specific, accounting

records of small businesses.

As indicated in Chapter 1.6, this chapter addresses the first objective of this dissertation,

which is to explain, through the use of relevant literature, the nature of financial accounting

records that should be maintained by small businesses. The literature review, therefore,

should be able to answer the first research question:

What financial accounting records should be maintained by small businesses?

13

2. Black involvement in the economy

The structures that represent the major subheadings of the chapter are:

1. Introduction

3. Empowerment and BEE

4. Description, classification and nature of small business

5. Financial management for small business

Conceptual Framework

6. Financial reporting

9. Conclusion

7. Financial accounting records and bookkeeping

8. Need for training in accounting

14

2.2 BLACK INVOLVEMENT IN THE ECONOMY

This section of the literature review provides a brief history of South Africa as it pertains to

past legislation and the effects on the participation of Blacks in the economic activities of the

country.

The National Treasury of the Republic of South Africa (RSA) assembled an international

team of economists from the Harvard Centre for International Development to analyse the

country’s economy and its growth prospects, as a drive towards the objectives of the

Accelerated and Shared Growth Initiative (ASGI-SA) (Haussmann, 2008:1). This was

important because South Africa, newly emerging from apartheid, needed to change. The past

dispensations left a legacy of poverty, inequality in wealth distribution and skewed access to

educational and employment opportunities (DTI, 2005:23), with a particularly adverse impact

on the involvement of the Blacks in the economy of the country. This, in the light of the new

democracy, required drastic interventions that would be corrective but which proved an

important test for the new government.

The aforementioned team of economists, according to Haussmann (2008:3), agree that the

new legislature in South Africa, after the successful democratic elections of 1994, has been

able to replace a system that denied basic economic and political rights to the majority with

an atmosphere that is conducive for trade openness, macroeconomic stability, and

redistribution of wealth and property rights. Lundahl and Petersson (2009:8) share similar

sentiments when they purport that the ultimate aim of the post-apartheid development

strategy is to abolish or reduce the extent of poverty and to close the large income gaps

between the different population groups.

Hausmann (2008:5), analysing the reports of ASGI-SA, pointed out that unemployed South

Africans are predominantly Black, female, young and poorly educated. He also indicated that

over 85% of those with a university degree are working and fewer than 35% of those without

a Matric (Grade 12) have jobs. These figures reaffirm the impact of past dispensations and

illustrate the high unemployment rate. As argued by Lundahl and Petersson (2009:2), South

15

Africa has had two main economic problems: i) increasing the growth rate, and ii) improving

the distribution of income and wealth. The majority of active citizens are without

employment, with Haussmann (2008:6) reporting a 40% unemployment rate among those

between the ages of 35 and 50, and over 75% of those between 20 and 25 years old. Some

factors resulting in the low employment rate in South Africa, according to Haussmann

(2008:8), may be as a result of the decline in the mining and agricultural sectors, which had

been the highest employer of unskilled labour or people with low education qualifications. To

tackle these figures, intervention in support of more self-employment and self-creation of

jobs was seen as vital, and as a thrust towards achieving these mandates the government had

to introduce different aggressive strategies, such as the following examples provided by

Cahan and van Staden (2009:4).

The Employment Equity Act legalized affirmative action policies and indicates that

employment on all levels must reflect the make-up of the population. Also, the

introduction of the policy of Black Economic Empowerment (BEE) which, for

example, requires businesses to have a proportion of black ownership or to do major

projects in partnership with black-owned business.

Blacks in South Africa had been systemically excluded from participating in economic

activities, such as having their own businesses (Haussmann, 2008; Lundahl & Peterson,

2009), but after 1994 the new government started putting different initiatives in place, geared

to eradicating the legacies of marginalisation and poverty.

2.3 EMPOWERMENT AND BLACK ECONOMIC EMPOWERMENT

Some government interventions directed at redressing the effects of previous legislation are

discussed in this section, examining their initial objectives, their implementation and their

shortcomings. In response to the above-mentioned racial inequalities, particularly in terms of

economic participation, it is important to highlight some recursive interventions undertaken

by the new government.

16

2.3.1 Legislation

Under the apartheid regime, South Africa experienced wide marginalisation of Black people

from the economic activities of the nation. Esser and Dekker (2008) write that one of the

major consequences of their deliberate exclusion from meaningful participation in the

economy culminated in limited access to proper education, skill development and

employment opportunities; hence, they lacked significant property and asset ownership. The

systemic exclusion of non-Whites, prior to 1994, also had a detrimental effect on the

Coloureds and Indians, and especially the Africans (Blacks), who generally remained very

poor and were not given opportunities to use their talents, for instance in starting their own

businesses and so improving their standard of living (Esser & Dekker, 2008).

After 1994, the shortcomings of the past dispensations had to be addressed and corrective

measures in the form of empowerment and upliftment of Blacks became inevitable.

According to a study by Kovacevic (2007:4), the legislation that followed the abolition of

apartheid, enacted between 1994 and 2001, was the world’s most rigorous form of

affirmative action. The Broad-Based Black Economic Empowerment (BBBEE) Act of 2003

strove for the “effective participation of black people in the economy [in order to achieve the]

economic unity of the nation” (RSA, 2003a). Its purpose was:

To establish a legislation framework for promotion of black economic empowerment;

to empower the Minister to issue codes of good practice and to publish

transformation charters; to establish the Black Economic Empowerment Advisory

Council; and to provide for matters connected therewith. (RSA, 2003a)

Ngwenya (2007:25), in his research report, identified some of the interventions, in the form

of government Acts, which were put in place for the purpose of redress:

National Small Business Act of 1996

Competition Act No. 89 of 1998

17

Employment Equity Act, No. 55 of 1998

National Empowerment Fund Act No. 105 of 1998

Preferential Procurement Policy Framework Act no. 5 of 2000

Skills Development Acts

Broad-Based Black Economic Empowerment Act 53 of 2003.

2.3.2 Broad-Based Black Economic Empowerment

The Broad-Based Black Economic Empowerment (BBBEE) Act of 2003 specifically states

that the South Africa’s policy of black economic empowerment is not simply a moral

initiative to redress the wrongs of the past. Black Economic Empowerment (BEE) in the

BBBEE Act is a pragmatic growth strategy that aims to realise the country’s full economic

potential, with Broad-Based Economic Empowerment defined in the BBBEE Act (RSA,

2003a) as follows:

broad-based black economic empowerment means the economic empowerment of all

black people including women, workers, youth, people with disabilities and people

living in rural areas through diverse but integrated socio-economic strategies that

include, but are not limited to-

(a) increasing the number of black people that manage, own and control

enterprises and productive assets;

(b) facilitating ownership and management of enterprises and productive assets

by communities, workers, cooperatives and other collective enterprises;

(c) human resource and skill development; …

For Van der Nest (2004:11), BEE can also be seen as a way of deepening the economy and

stimulating growth in the country by releasing the economic potential of the black population,

with the BEE initiative and the recently modified version, the BBBEE Act, acting as

incentives for the black population to start their own businesses. This allows them, for

18

instance, to solicit tenders from the government entities and to get sub-contracts in other

larger projects.

BBBEE, which is based on redistribution according to race rather than the wealth or income

(Kovacevic 2007:4), can be achieved:

when businesses fulfil rigorous race quotas in a quest for a (demographically

representative) staff. Redistribution legislation has made it more difficult for skilled

white workers to find employment domestically resulting in an outflow of skill.

Between 1994 and 2001, the percentage of enterprises that perceived the emigration

of skilled manpower as (significant) rose from 2 percent to 33 percent. This disturbing

skills shortage in many sectors of the economy is accompanied by slow economic

growth rates that barely keep pace with population growth.

Through earmarked objectives that endeavour to promote economic transformation and

empowerment of Blacks as active participants in the economy (RSA, 2003a), they were

given opportunities to start, improve and grow their businesses, so that they could sustain

themselves and not depend on government grants, for which not everybody qualifies.

2.3.3 Empowerment initiatives and shortcomings

The introduction to the BBEEE Act emphasised the importance of rectifying the past

imbalance (RSA, 2003a). Dixon, Durrheim, Tredoux, Tropp, Clack and Eaton (2010:401-

405) recommend, among other things, wealth redistribution and the participation of Blacks in

economic activities as practical measures of addressing some of the effects of the past

legislation of South Africa. This is also important because a new democracy and the mere

removal of the apartheid legacy will not be sufficient to correct imbalances of the past. A

corrective intervention will be necessary for redress. According to Ngwenya (2007:8):

19

This Act is part of a plethora of legislation enacted to give effect to citizens’ right to

equality as enshrined in the Constitution of the Republic; specifically to promote the

right to equality in the workplace through the elimination of unfair discrimination by

requiring employers to implement employment equity in the workplace to achieve

workforce diversity that reflects the demographics of the nation and improves the

efficiency and productivity of the national workforce.

For those not formally in the workplace, the government has helped communities to take the

initiative and be more independent, apart from a few who did not know about the BBBEE

Act or legislation, especially those in rural areas who could not take advantage of projects

confined largely to urban areas (Ngwenya, 2007:8).

Kovacevic (2007:4) has pointed out the perpetuation of small black elite by the current

system without helping the masses who are mostly in dire need as part of the shortcomings of

the BEE policies and as a crisis that requires urgent attention. She added (2007:4) that

although BEE professes to promote the meaningful participation of black people in the

economy, its implementation is actually negated by increased political cronyism that benefits

only a select few.

In 2003, Kovacevic (2007:4) indicated that, for example, 60% of empowerment deals

amounting to 25.3 billion rand went to the companies of only two black businessmen, hence

presenting a situation where a few wealthy Blacks are being enriched at the expense of a

majority living in poverty with lack of economic participation. He therefore concluded that in

these cases of government employment, where racial preferences commonly outweigh skill-

based qualifications, Black employees certainly benefit, but the masses of poor Black citizens

who rely on basic government services, such as health care and water, face exorbitant costs.

The above mentioned are major limitations to the implementation of empowerment and

upliftment initiatives aimed at Black entrepreneurs. Consequently, to some extent, the

majority are instead relying on the benefits the government is providing rather than

20

developing themselves in the fight against poverty. The result is that not everyone will

benefit (Kovacevic, 2007:44).

On one hand, these discussions suggest that the ANC-led government has tried to encourage

the employment of Black previously disadvantaged people in all levels of business, and has

also tried to encourage Black entrepreneurialism and business ownership. On the other hand,

at a macro level, the ANC’s labour policies appear to be having a limited effect as

unemployment remains very high (Haussmann, 2008:18). Instead of focusing on BEE,

Haussmann recommends that the government can achieve empowerment through job

creation, training and supplier development for people currently on the lower levels of

income distribution.

These developments over the years have highlighted the importance of boosting small

businesses at the grassroots level, as a strategy towards poverty eradication, wealth re-

distribution and sustainable empowerment.

2.3.4 Conclusion

Entrepreneurs in the rural areas have also engaged in business activities for different reasons,

for instance to eradicate poverty, create jobs and survive. Despite the interventions it seems

that job creation and poverty alleviation rates have been slow, and that a more sustainable

intervention is needed, namely the establishment and fostering of small businesses. This is

because, despite the success of some of the intervention initiatives, to a great extent the

economic and income divides still exist in the country. As previously stated, this dissertation

focuses on these smaller entrepreneurs and particularly on their accounting records.

Something more practical and ‘hands-on’ is needed so that everybody can participate in the

economic activities of the country. Prior to focusing on the type of accounting records that

are suitable for small businesses, the next section therefore discusses the description,

classification and importance of small businesses.

21

2.4 DESCRIPTION, CLASSIFICATION AND NATURE OF SMALL BUSINESSES

As Vosloo (1994:3) states, differences exist in the various interpretations of the concept

“small business” that is encountered within the same country. According to Bullock and

Hertz (1982:2), the need for a standardized international definition is not always realised or

accepted. In attempts to reduce poverty and unemployment, anyone who is willing and able

to start a small business may do so, which explains why there are informal businesses, such

as sole traders and partnerships, which cater for the bulk of micro and survivalist businesses.

2.4.1 Definition and classification of small businesses

In an effort to provide guidance on the issues surrounding the definition of small businesses,

the Department of Trade and Industry (DTI, 2005:1) have provided a definition of small

business in South Africa as follows:

Small business is a separate and distinct business entity, including co-operative

enterprises and non-governmental organisations, managed by one or more which,

including its branches or subsidiaries, if any, is predominantly carried on in any

sector or subsector of the economy, and which can be classified as micro-, very small,

a small or a medium enterprise.

Ntsika (1999:2) states that this above-stated definition could be considered as official and

applied generally where suitable. He also observed that it categorises small businesses into

four types: micro, very small, small and medium enterprises. To assist in the qualitative

classification, his view is that small businesses are enterprises that are more established and

likely to operate from business or industrial premises are registered for tax and meet other

formal registration requirement. The quantifiable aspects, on the other hand, are annual

turnover, the number of employees in service, the total assets of the business and the activity

level of the business.

22

Van der Nest, (2004:45), however, classified small businesses in South Africa as small and

medium enterprises (SME’s), or small, medium and micro enterprises (SMME’s), with the

micro being those that carry on business normally for survivalist purposes. The

Government’s White Paper on the promotion of small business acknowledges important

differences and needs between survivalist and micro enterprise on the one hand, and small

and medium enterprises on the other. This implies that what is viewed as important and vital

to a survivalist or micro business owner may not necessarily be of much importance to a

medium or small business owner. Van der Nest (2004: 52) also defines SMMEs as any

business activity/enterprise engaged in industry or agri-business/services, whether single

proprietorship, cooperative, partnership, or corporation.

Burns (1989:2) characterised a small business as an independent economic unit that is

motivated by profit-making, and highlighted some attributes of such an independent

economic unit as having: independent ownership, independent management, a simple

organisational structure and a relatively small influence on the market. Its owners are

associated with the entrepreneurs, the providers of capital, the managers, the decision makers

and those who share in the profit. The view here is that small businesses are mostly owner-

managed and less complicated. This is applicable to micro and survivalist businesses in rural

areas.

Other classifications of small businesses were established to serve as qualitative and

quantitative frameworks for profiling and rendering possible financial assistances to small

businesses. Business Partners (1999), a Small Business Development Corporation, has laid

down quantitative and qualitative criteria for small businesses in South Africa. The

quantitative criteria are total assets of less than R1,5 million, annual turnover of less than R5

million and fewer than 100 employees, while the qualitative criteria are independent

decision-making; simplified organisational structure and legal liability of the owner(s). This

shows that the classification of small businesses is complicated and may overlap.

The National Small Business Act (RSA, 2004) grouped SMMEs into 5 categories, as

summarised by the Education and Training Unit (ETU, 2010) in Table 2.1 (below).

23

Table 2.1 Categories of SMMEs (National Small Business Act of 2004) (RSA, 2004)

Category of SMME Description

Survivalist

enterprises Operates in the informal sector of the economy

Mainly undertaken by unemployed persons

Income generated below the poverty line, providing minimum

means to keep the unemployed and their families alive

Not much training

Opportunities for growing the business very small

Micro enterprises Between one to five employees, usually the owner and family

Informal – no license or formal business premises

Turnover below the VAT registration level of R300 000 per year

Basic business skills and training

Potential to make the transition to a viable formal small business

Very small

enterprise Part of the formal economy, use technology

Less than 10 paid employees

Includes self-employed artisans (electricians, plumbers) and

professionals

Small enterprise Less than 100 employees

More established than very small enterprises, formal and

registered, fixed business premises

Owner-managed, but more complex management structure

Medium enterprise Up to 200 employees

Still mainly owner managed, but decentralised management

structure with division of labour

Operates from fixed premises with all formal requirements

The National Small Business Act (RSA, 2004) suggests that the categories under the ambit of

the term SMMEs may be grouped as informal and formal businesses. While survivalist and

micro businesses are mostly informal, the small and medium businesses are normally formal.

2.4.2 Formal and informal business

Jäckle and Li (2006:558), in a study on the formality of micro enterprises in Peru, posits that

entrepreneurs wanting to start up business need to decide either to go into the formal or

24

informal sector, depending on, among other things, the size of the business, the age of the

entrepreneurs, and the location of the business. They (2006:567) added that any informal

business that plans to grow must consider switching to the formal sector. On the other hand,

Esselaar, Stork, Ndiwalana and Deen-Swarray (2007:87-89) have suggested that informal

businesses that utilise information and communication technologies (ICT) are very profitable

and successful, based on a study of 280 small businesses in eight African countries.1 Blurtit

(2011) states that the formal business sector of a country is made up of all recognised sources

of income on which income taxes may be paid.

In South Africa, informal businesses, unlike the formal, are the economic sector of the

country that is not governed by any form of legislation and not included in the calculation of

the Gross National Product (GNP) (ETU, 2010). Hence, the term ‘formal’, from the view of

the researcher, implies that the business is registered with a regulatory body, such as

Companies and Intellectual Property Commission (CIPC) (formally CIPRO) and perhaps

registered for taxation with the South African Revenue Service (SARS). Informal business is

normally sole or family traders and could include partnerships, while the formal businesses

may be close corporations and private companies. The ETU (2010) stated that formal small

businesses (mainly of White and some Indian ownership) are predominantly situated in urban

areas, while the informal businesses (mainly of African and Coloured ownership) are situated

in townships, informal settlements and rural areas.

The ETU (2010) suggested that by far the largest sector is the survivalist sector, which

implies that most people are active in the informal sector where they have little institutional

support as a result of not being registered with any governing or regulatory bodies.

These suggestions are further explained in Figure 2.1 (below), which shows the difference

between the first and second economies.

1 However, the small businesses on which this dissertation focuses do not utilize ICT.

25

Figure 2.1 First and Second Economies (DTI, 2005)

The first economy, represented by the upper part of the triangle, is mainly registered with

some agencies and is recognised by commercial banks, which may provide them with loan

facilities. The second economy is represented by the larger, base section of the triangle. As

they constitute the economically active poor and the very poor masses, they fit the description

of the micro and survivalist businesses, respectively.

Former president, Thabo Mbeki, coined the term ‘the second economy’ to describe the

informal sector (Devey, Skinner and Valodia, 2006) and to point to the structural barriers to

participation in the formal economy faced by many South Africans. Devey et al. (2006) see

the second economy as structurally disconnected from the mainstream one, whilst Kirsten

(2006:2) also argues that the second economy is the space within which those who are

marginalized will operate, that is the Black majority. Table 2.1 and Figure 2.1 show that

survivalist and micro enterprises are operating in the informal sector of the economy, and that

they normally generate income below the poverty line, providing minimum means to keep

their families alive (survival).

26

Devey et al., (2006:9) have confirmed the popularity of informal employment, as opposed to

the formal sector, by indicating that it is common not only to developing countries but also to

many other parts of the world. In terms of government support, Devey et al. (citing ETU,

2010), believe that “most [of] government [‘s] small business initiatives have been of little

benefit to the informal sector”. In this regard, Rogerson (cited in Devey et al., 2006:14)

opined that the DTI funding allocations for SMMEs have inevitably favoured and been

biased heavily towards support for established small and medium enterprises (often white

owned), rather than emerging micro-enterprises and the informal economy. Notwithstanding,

the importance of small businesses to the economy has always been recognized.

In an effort to describe the neglect of micro businesses, Devins, Gold, Johnson and Holden

(2005:540) have identified a lack of policy interventions that connect with the needs of the

micro businesses. For them, this marginalisation might have resulted from the assumption

that micro businesses are embraced by the term ‘small business’ or ‘SME’ (Devins et al.,

2005:547). It was therefore important for the researcher to explain the uniqueness of micro

and survivalist businesses as opposed to the common generalisation of the term SMMEs as

often referred to in literature.

2.4.3 Importance of small businesses

The importance of small businesses was enunciated by Mutezo (2005:35), noting that the

small and micro enterprises in South Africa employ 54 percent of the economically active

population and contribute close to 35 percent of Gross Domestic Product. Research carried

out by the Bridges Organisation (2000:2) indicates that small business development is

increasingly being recognised as important and must be tailored to a country’s circumstances.

Drew (2007b:1), together with van der Nest (2004), state that small business support offers

interventions aimed at eradicating poverty and ensuring growth. He specifically states further

that:

Small businesses are the backbone of any nation. If properly nurtured, many of these

firms have the potential to turn big fishes in the business world. But, the paradox is

that the failure ratio is also high in case of small businesses. Many businesses start

27

but fail to capitalise due to a number of reasons, lack of financial resources being one

of the most prominent reason (Drew, 2007b:1).

The Business Partners and Council (1999:14 as quoted by van der Nest, 2004) also state that:

Small businesses are an important source of competition, and challenges to larger

companies might prompt them to more innovative marketing and or supply. Small

businesses promote healthier participation in, and contribution to, the diffusion of

economic activity thereby eradicating the past unjust marginalisation.

There have been two main reasons for people being able to start their own business (Reijonen

and Komppula, 2007:670), namely the freedom it brings and a desire for financial

independence. However, van Gelderen, Thurik and Patel (2011) also found that the majority

of aspirants are held back by two factors, the employee mentality and the lack of guidance on

how to implement business ideas. The concepts of enterprise and entrepreneurship, as

opinioned by Van der Nest (2004:46), embrace much that would be considered as expressions

of small business activity, and such words as ‘enterprise’, ‘entrepreneurship’ and ‘small

business’ often appear interchangeable, although there are many small businesses that do not

demonstrate much enterprise. However, he states that a small business is important for a

variety of reasons, including diversity, social stability, and the competitiveness it provides

with other businesses. Ntsika (1999:16) agrees that the small business sector can play a major

role in creating jobs and wealth in any economy.

Consequently, the small business sector has drawn much attention from policymakers

because small businesses are valuable sources of innovation and creativity and are usually not

price-competitive, but compete through service and technology. Small businesses are

important partners to larger enterprises, whose initiatives they often reinforce and supplement

rather than replace (Business Partners and Council 1999:14).

Business Partners and Council (1999:14, in van der Nest, 2004), consider the most important

roles of small businesses in the South African economy as fourfold. Firstly, developing

28

economies have a strong demand for basic consumer goods, of which the small business

sector is a natural supplier. However, these small businesses ensure continuity of products

and services in rural areas that are often out of reach of larger enterprises or in markets that

larger companies do not endeavour to enter. Secondly, small businesses, compared with other

mainstream businesses, are by far the most cost effective and efficient job creators in the free

enterprise economy.

Hence, small businesses help the government to reduce the unemployment rate, which is

particularly high in South Africa. Thirdly, small businesses are important in the eradication of

the wealth and income disparity among the racial groups. This is possible through the free

enterprise characteristics of SMMEs. Small businesses contribute to the achievement of self-

sufficiency and human self-confidence. Fourthly, small businesses are viewed as a vehicle of

transition from the small scale to the large scale, because the informal business sector of the

country’s economy, represented mainly by the micro and survivalist businesses, should be

encouraged in a manner that serves as a logical starting point for the Black entrepreneur.

Even though the level of formalisation in terms of management and ownership structure are

key distinguishing characteristics between smaller companies and medium-sized enterprises

(Van Broembsen, 2003:2), “all levels of entrepreneurs are found in businesses of all sizes”

(Rajaram & O’Neill, 2009:100). Hence, entrepreneurs of informal small businesses, rather

than more structured ones, are characterised by the reality that they, “due to limited start-up

resources, use the small business as port of entry into the business world” (Vosloo,

1994:159).

Due to acknowledgement of the importance of small businesses to the economy, the

government has established many institutions to promote small businesses. Agupusi (2007:6-

8), as shown in Table 2.2 (below), summarised some of these and the activities that they

render towards achieving that goal:

29

Table 2.2 Government Development Institution for Small Business (Agupusi, 2007:6)

Institutions Activities

Small Enterprise

Development

Agency (SEDA)

SEDA offers a range of business development services. It provided

financial services through integrated support agencies across the

nation with more than 284 Enterprise Information Centres in the

municipalities across the nation.

Khula Enterprise Khula Enterprise facilitates access to finance for small businesses. It

has various financial products and works with major commercial

banks and private organisations such as Business Partners. Khula’s

operations involve loans and credit guarantees through commercial

banks. It also offers a mentorship programme.

National

Empowerment

Fund (NEF)

NEF provides various start-ups for small businesses and rural and

community transformation. Its financial capacity ranges from R250

000 to R10 000 000. NEF focuses specifically on disadvantaged

individuals.

Industrial

Development

Commission (IDC)

IDC generates its funds independently of the government. It provides

various sector-focused financing products ranging from R1 000 000,

with specific focus on SMEs and empowerment.

South African

Micro Fund Apex

Fund (SAMAF)

SAMAF is modelled on the Grameen Bank in Bangladesh. It provides

loans of up to R10 000 to micro and survivalist enterprises in poor

areas. Its main focus is on poverty alleviation.

Gauteng

Enterprise

Propeller (GEP)

GEP is a Gauteng Provincial Government (GPG) agency established

under the auspices of the Department for Economic Development to

provide non-financial and financial support and to co-ordinate

stakeholders for the benefit of SMMEs in Gauteng Province.

Based on the discussions in this section, it is evident that the small businesses investigated in

this dissertation are informal in nature and are either classified as micro or survivalist. It may

mean that they have no access to established government interventions. It nevertheless

remains that some of the matters applicable to formal businesses are also applicable to

informal ones.

30

Stokes and Wilson (2010:225) have emphasized the importance of financial management to

owner-managed-small (survivalist and micro businesses are mainly owner-managed)

businesses by summarising four major factors that contribute to the failure of small

businesses: 1.) availability of finance, 2.) management capacity of owners, 3.) marketing

problems and 4.) difficulty in complying with new laws and regulations, such as income tax

laws. Although all four factors are important, the focus of this dissertation is on the financial

aspects, therefore reviewing literature on financial management of small businesses is more

relevant.

2.5 FINANCIAL MANAGEMENT FOR SMALL BUSINESS

According to Reijonen and Komppula (2007:15), small business success is about more than

just a great idea, prime office location or qualified employees. Small business owners must

continually improve their knowledge and skills and understand why they are in business.

Businesses have many functions, of which financial management is core, because it is the one

that sources the required funds (cash or loans) and makes the most efficient use of those

funds on projects (investments or trades) that will ensure the final bottom line of maximising

profits (Nieuwenhuizen, 2010; Stokes and Wilson, 2010). Financial management of small

businesses entails bookkeeping, planning, accounting and other accounting and actuarial

activities (Brazma, 2007c:3), e.g., evaluating, managing and advising on financial risks

(Haynes, 2010). Concerning the importance of financial management to small businesses,

Nieuwenhuizen (2010:319) has stated that:

Financial management is responsible for acquiring the necessary financial resources

to ensure the most advantageous result for the small business over both the short and

long term. The term ‘financial management’ also covers the responsibility for making

sure the business makes the best use of its financial resources.

Nieuwenhuizen (2010:318) also cautioned that financial management, although different

from other managerial and business functions and activities, should not be viewed in isolation

from other business activities, because these also have financial implications.

31

Bowes (2007:2) has stated that nurturing a small business is a cumbersome task and that the

most common reason for failure is lack of control over its financial matters. He therefore

emphasised the importance of time management, as activities, such as the day-to-day

bookkeeping tasks, on their own can be time-consuming (Bowes, 2007). This is applicable to

even micro and survivalist business. In South Africa, according to Van der Nest (2004:46),

small businesses face a wider range of problems and are less able to address the problems on

their own than are small businesses in other countries. She further identified some constraints

they face, relating to the:

legal and regulatory environment confronting SMEs, the access to markets; finance

and business premises (at affordable rentals); the acquisition of skills and managerial

expertise; access to appropriate technology; the quality of the business infrastructure

in poverty areas... (Van der Nest, 2004:46).

Ciobanu (2006:1) advises that before starting a small business, the entrepreneur needs to

conduct as much research as possible, and talk to other people who have started a small

business and are willing to give some guidance. The importance of finances cannot be over-

emphasized as it is difficult to carry on a trade without first injecting some capital into it.

Hence, financial help is essential to aspiring business-minded individuals who want to start

their own business (Riley, 2007:2). According to Drew (2007), sustained financial support is

important for the business plan, start up and continuous development of small businesses, and

that one of the major functions of the financial manager is to source funds. The small

business loan may also be very important (Drew, 2007:1).

Despite the importance of proper financial record keeping and financial management in a

small business, it may be a task that is beyond the expertise of many small business owners,

leading Brazma (2007a:2) to conclude that keeping a tab on various financial transactions

throughout the year is a tough act for a small business. Kelly (2006:11) confirms that small

businesses are the most difficult of all types of business to run. Emphasising the importance

of efficient financial accounting records, Brazma (2007d: 2) stated that both big and small

business enterprises need an expert to handle the financial affairs of the entity, and suggested

32