Recruitment and Selection Practices at Credit Union … and Selection Practices at Credit Union...

52

Recruitment and Selection Practices at Credit Union Boards William A. Brown Assistant Professor & Affiliated Faculty School of Community Resources & Development Center for Nonprofit Leadership & Management Arizona State University

Transcript of Recruitment and Selection Practices at Credit Union … and Selection Practices at Credit Union...

Recruitment and Select ion Pract ices at Credit Union Boards

William A. Brown Assistant Professor & Affiliated Faculty

School of Community Resources & Development Center for Nonprofit Leadership & Management

Arizona State University

Copyright © 2005 by Filene Research Institute. ISBN 1-880572-91-5 All rights reserved. Printed in U.S.A.

i

The Filene Research Institute is a non-profit organization dedicated to scientific and thoughtful analysis about issues affecting the future of consumer finance and credit unions. It supports research efforts that will ultimately enhance the well-being of consumers and will assist credit unions in adapting to rapidly changing economic, legal, and social environments.

Deeply imbedded in the credit union tradition is an ongoing search for better ways to understand and serve credit union members and the general public. Credit unions, like other democratic institutions, make great progress when they welcome and carefully consider high-quality research, new perspectives, and innovative, sometimes controversial, proposals. Open inquiry, the free flow of ideas, and debate are essential parts of the true democratic process. In this spirit, the Filene Research Institute grants researchers considerable latitude in their studies of high-priority consumer finance issues and encourages them to candidly communicate their findings and recommendations.

The name of the institute honors Edward A. Filene, the “father of the U.S. credit union movement.” He was an innovative leader who relied on insightful research and analysis when encouraging credit union development.

Filene Research Institute

Progress is the constant replacing of the best there is with something still better!

— Edward A. Filene

ii

iii

Acknowledgements Very special thanks go to Sue Brayman whose extensive experience with credit unions and credit union boards provided valuable input for this project. Additional thanks go to Vicki Joyal and Kristina Grebener at CUNA and Affiliates, for their assistance and hard work on this project.

iv

v

Table of Contents

Executive Summar y and Commentar y . . . . . . . . . . . . . . 1

About the Author . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

CHAPTER 1: Introduction . . . . . . . . . . . . . . . . . . . . . 7

CHAPTER 2: Board Member Recruitment & Selection . . 9

CHAPTER 3: Conclusions & Implications on Recruitment and Selection Practices . . . . . . . . . . . . . . 19

CHAPTER 4: Facts About Credit Union Boards in the Sample . . . . . . . . . . . . . . . . . . . . . . 21

APPENDIX Credit Union Board Governance Sur vey . . . . 25

Filene Research Institute Administrative Board/ Research Council . . . . . . . . . . . . . . . . . . . . . . . . . . . . 31

Filene Research Institute Publications . . . . . . . . . . . . 35

vi

1

Executive Summar y and Commentar yby George A . Hofheimer,

Director of Research

The nature of boards of directors is a frequent topic of discussion in the credit union industry. Many consider boards of directors a distinguishing and value-adding element of credit unions. This view is generally supported by those who regard credit unions as distinct from other financial institutions. The board, this group contends, represents members by volunteering their time, expertise and passion to ensure the credit union remains relevant and service-oriented. Others believe boards of directors are the “Achilles Heel” of credit unions. The board, this group contends, is a collection of individuals who often get in the way of management’s ability to effectively compete. Somewhere between these two extremes is a middle view reflecting a credit union’s particular competitive situation, outlook and skill-set.

The Filene Research Institute is curious about credit union boards for a number of reasons. First, credit union boards are distinct from other financial institution boards because they are comprised largely of volunteers who represent the membership. Second, as confirmed in this research, the make-up of credit union boards often fails to reflect the changing demographics of credit union membership. Third, the divergence of opinions on the value of credit union boards is extremely volatile in the credit union world and should be researched to understand such differing opinions. Fourth, current events in the business world have cast an extremely bright spotlight on the quality of governance.

In a previous Filene Research Institute report1, Professor Julie Siciliano of the Florida Institute of Technology asked the question: what activities enhance credit union board satisfaction? Siciliano discovered the following board activities (in rank order of importance) highly correlate with board satisfaction:

1. Closely monitoring the financial soundness of the credit union

2. Developing strategic action plans to achieve goals

3. Assessing appropriate skills/characteristics of board members

4. Performing the annual CEO evaluation

5. Monitoring implementation of strategic plans

This report delves into one of the areas listed above: assessing appropriate skills/characteristics of board members. Specifically, the purpose of this report is to determine how credit unions recruit and

1 “Enhancing Board Satisfaction at Credit Unions,” Filene Research Institute, 2004

2

select board members. To achieve this goal William Brown, a researcher and professor from Arizona State University, collected surveys from 672 executives and 379 board members representing 713 credit unions from across the United States. The credit unions participating in the survey are representative of all asset sizes, types and locations. So rest assured the research findings are characteristic of the credit union industry.

What Brown discovered in the survey results paints a fairly unenthusiastic view of how credit unions recruit and select board members. Brown asked credit union CEOs and board directors a series of questions which represent common business practices in board recruitment and selection. First, let’s examine how credit unions recruit new board members. The most prevalent recruitment practices include:

• Networking and word of mouth

• Relying on existing volunteer network

• Using a nominating committee often dominated by existing board members

The commonality of these practices is that they are internally focused on the skills and knowledge of the current board of directors. Other recommended (or best practice) recruitment tools are not widely used by credit unions. Survey results reported:

• Limited use of job descriptions for board members

• Limited use of skill profiles to select members

• Few strategies in place to ensure a diversity of new board members

Therefore, the natural conclusion is that the board recruitment function yields candidates who are a lot like the current board of directors, or just the existing board members.

After a slate of candidates is recruited, members are required to select the board through an election process on a single vote per member basis. Again, the survey results cast a downbeat picture of the board selection processes in place at credit unions:

• Most board position elections are uncontested

• 92% of smaller credit unions (assets $25 million or less) hold board elections only at annual meetings

3

• 46% of larger credit unions (assets $500 million or more) hold elections only at annual meetings

A picture of board recruitment and selection outcomes, now comes into focus. First, you have an internally-focused manner by which you attract potential board members. The result is that a majority of credit union board elections are uncontested. For those elections that are contested, the selection process is generally held at sparsely attended annual meetings. We should not be surprised to learn that the make-up of boards is fairly uniform with the demographic make up of board members being white (89%), male (75%), and over 50 years old (75%). Additionally, this study suggests today’s board demographic profile will continue until different practices are instituted since only 15% of survey respondents reported using term limits in their credit unions.

The use of these recruiting and selection practices may indicate that credit unions are satisfied with the performance of their boards of directors, and, therefore, do not need more effective processes. The survey results cast doubt about the wisdom of this line of thinking:

• The majority of CEOs feel there should be a limit on the number of consecutive terms a director may serve

• 30% of executives feel there is insufficient turnover on their board

Furthermore, and most alarming, is the apparent situation in which credit unions seem obliged to retain poor performing board members. According to a majority of CEOs and a substantial minority of board members:

• The board tends to re-nominate any incumbent who wants to serve another term, even if the director has not contributed much during the previous term

• Board members who provide insufficient time and effort are generally retained as board members

4

What are we to make of these findings? Recommendations to consider as credit unions move forward in their thinking on how to improve recruitment and selection processes include:

• Consider adopting a more comprehensive recruitment system

• Develop a profile of board member competencies

• Consider limiting the total number of terms board members can serve consecutively (i.e., term limits)

• Expand the election system to allow for more open participation by members (i.e., Internet or mail voting)

• Engage board members and executives in conversations about best practices in recruiting, selecting, and rotating members on and off the board

The goal of this research study is to determine how credit unions recruit and select board members. You will learn a lot of information about your colleague’s practices in the pages that follow. As you read this publication ask yourself “how can my credit union become better at recruiting and selecting board members?”

The Filene Research Institute firmly believes credit union directors are distinct from other financial institution directors and have the potential to add an enormous amount of value to their institutions. Through research projects such as this we can start the conversation about how overall credit union governance can grow and improve.

5

William A. Brown is an Assistant Professor in the School of Community Resources and Development and Graduate Coordinator for Certificate in Nonprofit Leadership & Management offered through the Center for Nonprofit Leadership and Management at Arizona State University. He teaches graduate courses in Program Evaluation, and Volunteer and Human Resources in Nonprofit Organizations, along with undergraduate courses in the American Humanics program – Introduction to Nonprofits and Fund Raising. He received a Bachelor of Science degree in Education from Northeastern University with a concentration in Human Services. He earned his Masters and Ph.D. from Claremont Graduate University, in Organizational Psychology. He has worked with numerous nonprofit organizations in the direct provision of services, consulting, and board governance. His research has focused on nonprofit governance and organizational effectiveness. Recent research investigated the extent to which boards include different constituents in governance processes and the impact of board performance on organizational effectiveness. He has published a number of articles on non-profit governance in scholarly journals including Nonprofit and Voluntary Sector Quarterly and Nonprofit Management & Leadership.

About the Author

6

7

CHAPTER 1: Introduction

The board of directors plays a key role in the success of a credit union. The board selects the CEO, manages the relationship with the CEO, and has ultimate authority over the credit union. Therefore the manner in which the board is developed can make a substantial difference in the performance of the credit union. Board development has several dimensions. The very first dimension is how the directors themselves come to sit on the board. The purpose of the study reported here is to provide information on actual credit union practices determining who will be directors. In addition, the research reports opinions of CEO’s and board chairs on how well these practices work. These results provide a way for all credit unions to evaluate their practices compared to a representative sample of all credit unions.

METHOD

We surveyed the CEO and board chair at a representative sample 1,600 credit unions in a variety of size categories. At least one individual from 713 credit unions, or 43%, responded. Table 1 shows these responses by asset size. For 338 of the 713 responding credit unions, both the CEO and the board chair replied. At the other 375 credit unions, either the CEO or the board chair responded. Altogether, 672, or 40%, of CEO’s responded, and 370, or 23% of board chairs responded. Some questions were factual, to be answered in the same way by both the CEO and the board chair. Other questions asked for opinions, and on these the CEO and board chair could differ. In reporting the results below, meaningful differences between opinions given by CEO’s and board chairs, or differences by asset size, we provide additional information by category where appropriate.

Table 1: Asset-size categories of credit union’s responding

# of CU’s Percent

$25 million or less 150 21%

$25 - 75 million 139 20%

$75 - 200 million 156 21%

$200 - 500 million 140 20%

$500 million or more 128 18%

Total 713 100%

8

99

CHAPTER 2: Board Member Recruitment & Selection

RECRUITMENT

Recruitment entails the range of activities designed to secure a broad number of qualified candidates for the board. Respondents were asked to indicate the extent to which they engaged in a number of common business practices related to recruiting and finding new board members. Table 2 shows that many of these practices are not commonly used by credit union boards. For instance, about 35% of respondents use competency or skills profiles to some or a great extent to help select potential board members, but 43% do not use this practice at all. The limited use of these practices, however, does not dampen the perception that in general that credit unions find good candidates for their boards. Board members are consistently more optimistic about the use of these practices compared to executives.

In general, larger credit unions (i.e., assets over $200 million) are more likely to carry-out common practices compared to smaller credit unions. The one exception is that smaller credit unions (assets $25 million or less) are more likely to report having the CEO more actively engaged in the board recruitment process.

Table 2: Recruitment practices

1 2 3 4 5

Mean (SD)

Not at all

some extent

great extent

Job descriptions exist for board member positions2.55

(1.48)37.8% 13.5% 19.0% 15.0% 14.7%

Competency/skill profiles developed/used to nominate new members2.14

(1.22)42.7% 21.4% 20.1% 11.1% 4.8%

CEO plays a role in board member recruitment2.66

(1.29)26.0% 18.3% 29.1% 16.8% 9.6%

Strategies are in place to insure diversity of new board members2.32

(1.15)32.4% 22.9% 28.4% 13.1% 3.2%

Nomination committee works year round identifying a wide variety of potential candidates

1.98 (1.05)

42.3% 29.8% 17.8% 8.3% 1.8%

Finds good candidates for the board3.47

(1.10)4.5% 15.2% 28.3% 32.1% 19.8%

Number of candidates typically exceeds number of seats filled2.14

(1.28)43.2% 24.1% 15.9% 9.0% 7.8%

N = 1051

In addition to the predetermined options listed in the survey, respondents were given the opportunity to specify other common practices used to recruit and attract board members. Over 900 suggestions were offered, the most common of which are presented in Table 3. Over half the

10

respondents indicated that they rely on informal networks. Network relationships were presented as the “only way” to get good candidates by some respondents, and as not entirely satisfactory to secure board members (i.e., “personal recruitment has proven ineffective”) by others.

The next most common strategy identified was to rely on existing committee members or associate board members as potential new members. In most instances respondents perceived this practice to be effective.

Table 3: Other recruitment practices

Number of comments

Percent of Total

Networking with personal contacts, business associates, or credit union members

448 54%

Rely on existing committees (i.e., Supervisory) or using associate/assistant non-voting board member

204 25%

Publicize board openings in newsletters, websites, or through flyers and postings within the credit union

108 13%

Nominating committee is instrumental in securing good board members

35 4%

Determine needs of the board (i.e., skills, knowledge, or representation) and then candidates are sought to fulfill those needs

30 4%

Total Number of Comments 825 100%

ROLE OF NOMINATION COMMITTEE IN SELEC TION

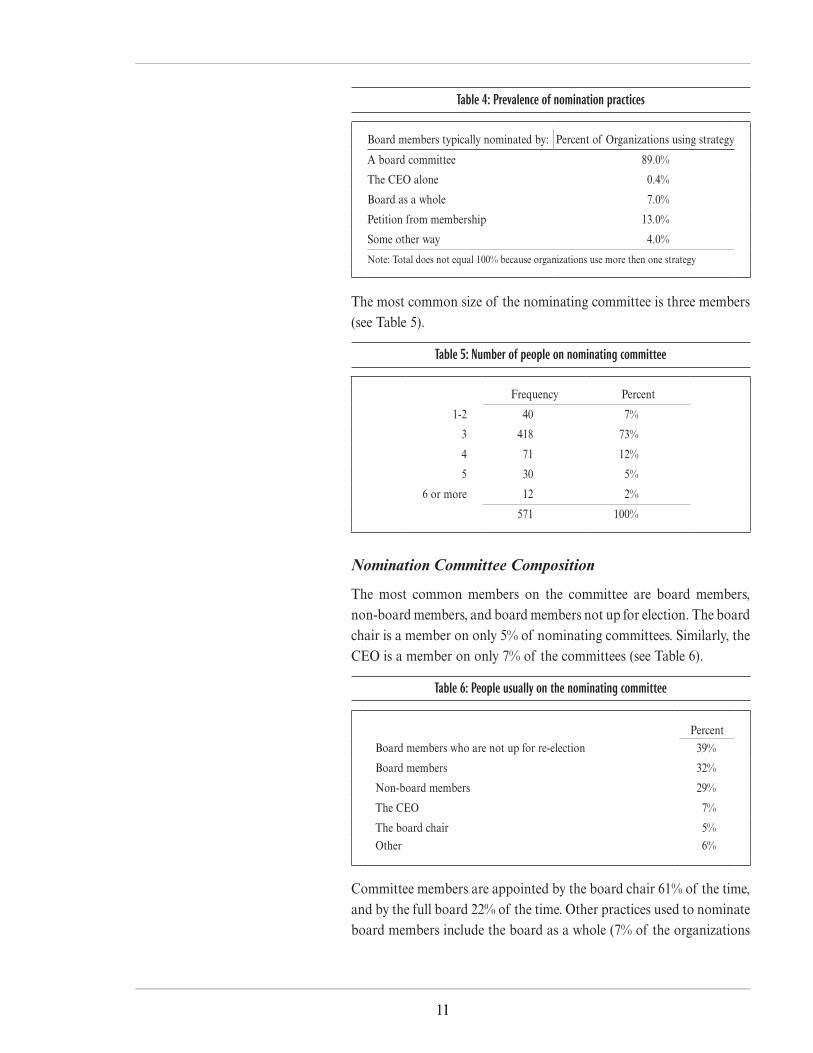

Nearly 90% of the credit unions indicated that new board members are typically nominated by a committee of the board (Table 4). Credit union asset size is associated with the tendency to use a nominating committee – 75% of smaller credit unions have nominating committees compared to 95% of larger organizations.

1111

Table 4: Prevalence of nomination practices

Board members typically nominated by: Percent of Organizations using strategy

A board committee 89.0%

The CEO alone 0.4%

Board as a whole 7.0%

Petition from membership 13.0%

Some other way 4.0%

Note: Total does not equal 100% because organizations use more then one strategy

The most common size of the nominating committee is three members (see Table 5).

Table 5: Number of people on nominating committee

Frequency Percent

1-2 40 7%

3 418 73%

4 71 12%

5 30 5%

6 or more 12 2%

571 100%

Nomination Committee Composition

The most common members on the committee are board members, non-board members, and board members not up for election. The board chair is a member on only 5% of nominating committees. Similarly, the CEO is a member on only 7% of the committees (see Table 6).

Table 6: People usually on the nominating committee

Percent

Board members who are not up for re-election 39%

Board members 32%

Non-board members 29%

The CEO 7%

The board chair 5%

Other 6%

Committee members are appointed by the board chair 61% of the time, and by the full board 22% of the time. Other practices used to nominate board members include the board as a whole (7% of the organizations

1212

uses this practice), or a petition of the membership, used by 13% of credit unions (See Table 4).

Table 7: Who appoints the nominating committee?

Frequency Percent

Board chair 386 61%

Full board 139 22%

Executive committee of the board 10 2%

Other 17 3%

Did not Specify 83 13%

Note: Percentages may not add to 100% because of rounding.

Nominating Committee Performance

The study asked two questions about the effectiveness of the nominating committee, and about nominating practices overall. Perceptions of board members and executives were often dissimilar, so both sets of responses are presented. Respondents were asked to indicate their agreement to the following statement. “The nominating committee at our credit union always re-nominates any incumbent who would like to serve another term.” Eighty-six percent of executives and 77% of board chairs agreed or strongly agreed to the statement. Size does not appear to have a significant impact on how this situation is handled.

Table 8: Nominating committee always nominates any incumbent wanting to serve

Strongly Disagree Disagree

Neither Agree nor Disagree Agree

Strongly Agree Mean SD

CEO 1% 6% 6% 29% 57% 4.33 0.95

Board Chair 2% 10% 10% 40% 37% 3.99 1.04

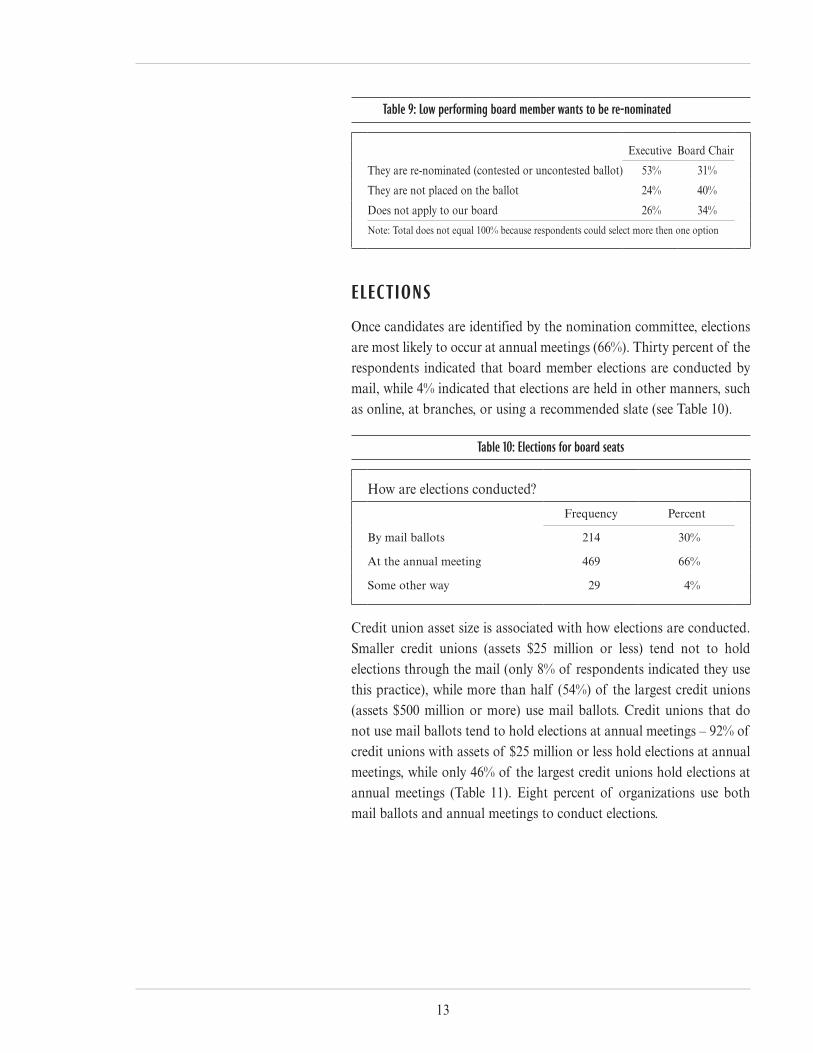

A second question asked respondents to select from several options to explain what happens when “an incumbent wants to be re-nominated for another term, but he or she has not contributed much during his or her current term.” Only 24% of CEOs indicated that the individual is “not placed on the ballot,” compared with 40% of board chairs responding that the individual is “ultimately not placed on the ballot” (See Table 9).

13

Table 9: Low performing board member wants to be re-nominated

Executive Board Chair

They are re-nominated (contested or uncontested ballot) 53% 31%

They are not placed on the ballot 24% 40%

Does not apply to our board 26% 34%

Note: Total does not equal 100% because respondents could select more then one option

ELEC TIONS

Once candidates are identified by the nomination committee, elections are most likely to occur at annual meetings (66%). Thirty percent of the respondents indicated that board member elections are conducted by mail, while 4% indicated that elections are held in other manners, such as online, at branches, or using a recommended slate (see Table 10).

Table 10: Elections for board seats

How are elections conducted?

Frequency Percent

By mail ballots 214 30%

At the annual meeting 469 66%

Some other way 29 4%

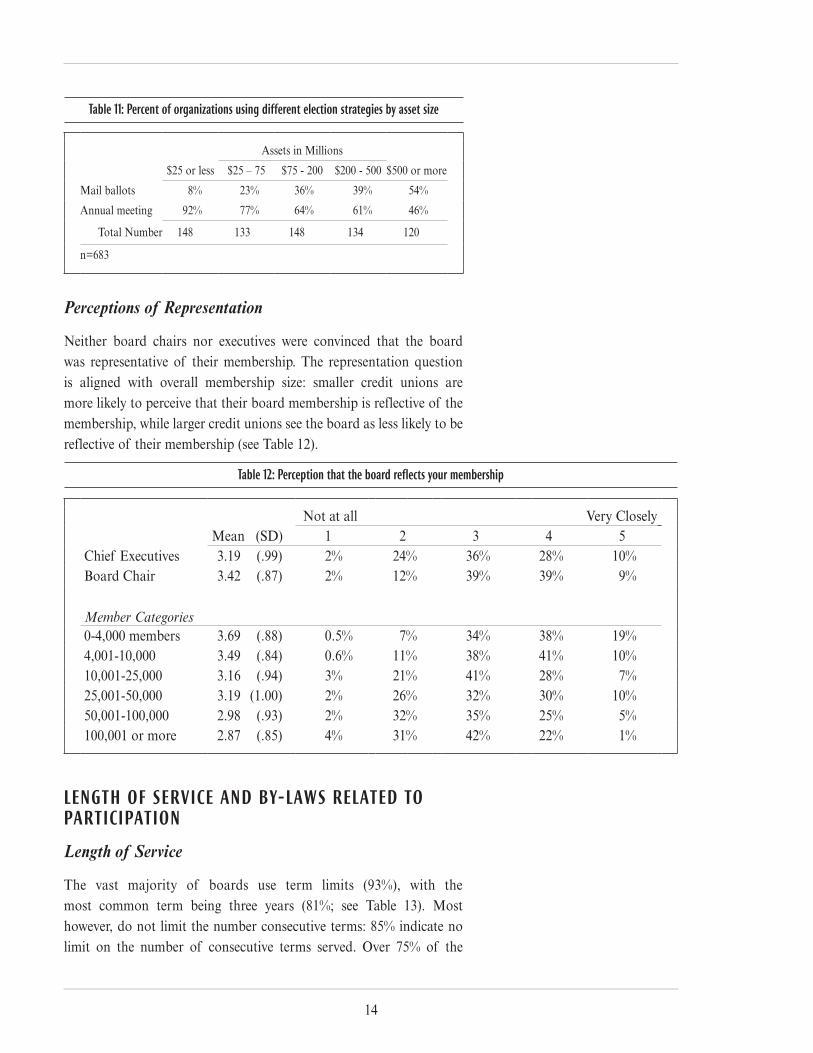

Credit union asset size is associated with how elections are conducted. Smaller credit unions (assets $25 million or less) tend not to hold elections through the mail (only 8% of respondents indicated they use this practice), while more than half (54%) of the largest credit unions (assets $500 million or more) use mail ballots. Credit unions that do not use mail ballots tend to hold elections at annual meetings – 92% of credit unions with assets of $25 million or less hold elections at annual meetings, while only 46% of the largest credit unions hold elections at annual meetings (Table 11). Eight percent of organizations use both mail ballots and annual meetings to conduct elections.

14

Table 11: Percent of organizations using different election strategies by asset size

Assets in Millions

$25 or less $25 – 75 $75 - 200 $200 - 500 $500 or more

Mail ballots 8% 23% 36% 39% 54%

Annual meeting 92% 77% 64% 61% 46%

Total Number 148 133 148 134 120

n=683

Perceptions of Representation

Neither board chairs nor executives were convinced that the board was representative of their membership. The representation question is aligned with overall membership size: smaller credit unions are more likely to perceive that their board membership is reflective of the membership, while larger credit unions see the board as less likely to be reflective of their membership (see Table 12).

Table 12: Perception that the board reflects your membership

Not at all Very Closely Mean (SD) 1 2 3 4 5

Chief Executives 3.19 (.99) 2% 24% 36% 28% 10%Board Chair 3.42 (.87) 2% 12% 39% 39% 9%

Member Categories 0-4,000 members 3.69 (.88) 0.5% 7% 34% 38% 19%4,001-10,000 3.49 (.84) 0.6% 11% 38% 41% 10%10,001-25,000 3.16 (.94) 3% 21% 41% 28% 7%25,001-50,000 3.19 (1.00) 2% 26% 32% 30% 10%50,001-100,000 2.98 (.93) 2% 32% 35% 25% 5%100,001 or more 2.87 (.85) 4% 31% 42% 22% 1%

LENGTH OF SERVICE AND BY-LAWS RELATED TO PARTICIPATION

Length of Service

The vast majority of boards use term limits (93%), with the most common term being three years (81%; see Table 13). Most however, do not limit the number consecutive terms: 85% indicate no limit on the number of consecutive terms served. Over 75% of the

15

respondents felt it took 1-2 years of board service before a member became fully effective.

Table 13: Terms for board members

Frequency Percent

1-2 years 79 11%

3 years 568 81%

No specified length 49 7%

Other 7 1%

Total 703 100%

Note: 10 did not specify

Respondents were asked to indicate the total length of continuous service in order to ensure effective board performance. Forty-three percent of executives and nearly 62% of board chairs replied that service on the board should be unlimited or limited only by age. However, 55% of the executives felt there should be at least some limit on consecutive terms served while just 34% of board chairs felt that way (See Table 14).

Table 14: Length of continuous service to ensure effective performance

CEO Board

n=672 n=379

1-3 years 5% 5%

4-6 years 20% 12%

7-10 years 29% 17%

Unlimited 30% 49%

Age limit only 13% 13%

Other 3% 4%

Less then 2% of the credit unions reported having a mandatory retirement age for board members. Of those that do not have a retirement age, 36% of the executives and 24% of the board members felt they should.

Fewer than 20% of credit unions have an emeritus program for board members. In those that do, the programs are perceived as being only moderately effective at creating openings on the board. Board members perceived the program to be slightly more effective, but 41% felt they were neither effective nor ineffective. Nearly 30% of the executives felt emeritus programs were ineffective or very ineffective.

16

With respect to board turnover, 30% of CEOs felt that there was insufficient turnover on the board, compared to 17% of board chairs. Only a handful of respondents perceived that board turnover was too high (2-3%). The remaining respondents felt board turnover was “about right.” Over 65% of the boards had experienced some turnover in the last two years. Differences between smaller and larger organizations on this issue were minimal.

Table 15: Perceptions of board member turnover

Chief Executive Board Chair

Frequency Percent Frequency Percent

Not enough 198 30% 62 17%

About right 435 67% 300 81%

Too much 21 3% 9 2%

Total 654 100% 371 100%

Note: 18 executives and 8 board chairs did not specify

CEO ON THE BOARD

About one-third of the organizations indicated that the CEO is allowed by charter to serve on the board. However, only about 18% of executives actually serve as a member of the board. Neither asset size nor location (state) is associated with this policy.

BOARD COMPENSATION

Eleven percent of the respondents indicated that their charter allows for board members to be compensated. These credit unions are located in 28 different states. However, only 36 credit unions (about 5% of the participants) actually provide compensation to board members.

Thirty-three respondents provided information about how much they compensate board members. The practice ranges from as little as $150 to as much as $15,000 in average annual compensation for board members. Size is predictive of offering board compensation: about 10% of organizations with assets over $500 million offered board member compensation (average annual compensation $7,275), but selected credit unions in all budget categories indicated offering some compensation. For instance, 3% of credit unions with assets of $25 million or less offer board member compensation, but average annual compensation is just $623 (See Table 16).

17

Table 16: Average annual compensation by asset size

Asset categories Mean N Std. Deviation

$25 million or less $ 623.33 3 162.58

$25 - $75 million $1,493.33 3 801.33

$75 - $200 million $1,763.75 8 1575.05

$200 - $500 million $2,307.14 7 2255.81

$500 million or more $7,275.00 12 4804.75

Total $3,754.85 33 4119.40

18

19

CHAPTER 3 Conclusions & Implications on Recruitment and Selection Practices

Credit union boards rely heavily on networking and word of mouth to locate prospective board members. Some respondents described the process as rigorous and comprehensive, while others recognized that it was limited to a few individuals asking friends and work colleagues to serve, and that such a practice may be ineffective. Other recommended board recruitment practices are not widely used in credit unions.

There does not appear to be a system to effectively remove or rotate members off the board. Fifty-five percent of executives felt that there should be some limit on years of consecutive service, and one-third of board chairs agreed. Assessment of individual board member’s performance would be an effective but difficult strategy, while implementation of term limits might be a more practical solution. About 20% of boards use emeritus programs, but most find them ineffective as a way to open up board seats. This conclusion is reinforced by the fact that over half of executives openly acknowledged that low performing board members are routinely re-nominated.

The process of open elections appears to be artificially limited when elections are open only to those attending annual meetings. Only 30% of credit unions in the study use mail ballots, which would provide for a more open process to elect the board. Almost half of the large credit unions (assets over $500 million) provide no other mechanism than attendance at annual meetings to vote on board membership.

Executives and board chairs hold differing perceptions about board practices and the need to limit board service. This report provides an opportunity to discuss current practices and concerns related to representation and potential stagnation on the board.

20

21

CHAPTER 4: Facts about Credit Union Boards in the Sample

Chapter 3 offered conclusions and implications about credit union board practices and recruitment. This chapter provides additional facts about the credit union boards in our sample.

BOARD CHARAC TERISTICS

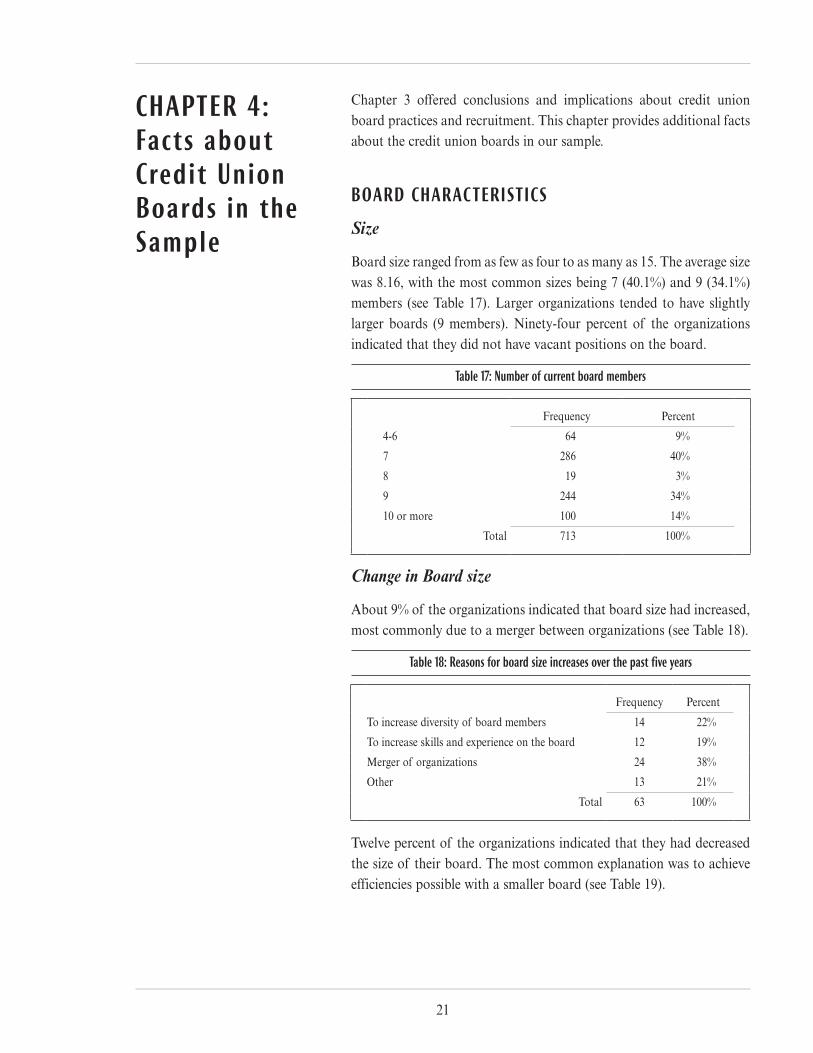

Size

Board size ranged from as few as four to as many as 15. The average size was 8.16, with the most common sizes being 7 (40.1%) and 9 (34.1%) members (see Table 17). Larger organizations tended to have slightly larger boards (9 members). Ninety-four percent of the organizations indicated that they did not have vacant positions on the board.

Table 17: Number of current board members

Frequency Percent

4-6 64 9%

7 286 40%

8 19 3%

9 244 34%

10 or more 100 14%

Total 713 100%

Change in Board size

About 9% of the organizations indicated that board size had increased, most commonly due to a merger between organizations (see Table 18).

Table 18: Reasons for board size increases over the past five years

Frequency Percent

To increase diversity of board members 14 22%

To increase skills and experience on the board 12 19%

Merger of organizations 24 38%

Other 13 21%

Total 63 100%

Twelve percent of the organizations indicated that they had decreased the size of their board. The most common explanation was to achieve efficiencies possible with a smaller board (see Table 19).

22

Table 19: Reasons for board size reduction during the past five years

Frequency Percent

To reduce costs associated with a larger board 6 7%

Merger of organizations 8 9%

To achieve efficiency of a smaller board 54 63%

Other 18 21%

Total 86 100%

BOARD MEMBER CHARAC TERISTICS

Age

Board members tend to be older than membership averages, with just 25% of board members under 50. One-third of board members are in their 50s and another 30% are in their 60s (see Table 20). Smaller organizations (assets $ 25 million or less) tend to have slightly younger boards, with 32% of board members under 50; while larger organizations (assets $500 million or more) tend to have more members who are over 50 (81%).

Table 20: Percent of board members by age category

Percent

Under 40 6%

40-49 19%

50-59 33%

60-69 29%

70 or more 13%

Total 100%

Gender

Men outnumber women on boards by about three to one. This is true almost irrespective of size, but smaller credit unions (assets $25 million or less) have slightly more women on the board, about 30%; while larger organizations (assets over $500 million) indicate that about 25% of their board members are women.

Race

The vast majority of board members are white (89%). This tends to be true irrespective of asset size or membership type (Table 21).

23

Table 21: Percent of board members by race

Percent 2003 Census

White Non-Hispanic 89% 76%

African-American 6% 12%

Hispanic 3% 14%*

Asian/Pacific Islander 1.5% 4%

Other (i.e., Native American, multi racial) 0.5% 7%

*Note: Census data provides only Hispanic or Latino of any race; consequently those individuals are first classified into a racial category and then may specify if they are Hispanic or Latino.

24

25

BOARD INFORMATION

1. How large is your credit union’s board?Number of current board members: ______ Number of vacant positions: ______

2. In the past 5 years, has the size of your credit union’s board changed?

▫ Yes, the number of members increased

If the size of the board increased, what are the reasons why? (Check all that apply.)

▫ To increase diversity ▫ To increase skills and experience on the board

▫ Merger of organizations ▫ Other (specify): ____________________________

▫ Yes, the number of members decreased

If the size of the board decreased, what are the reasons why? (Check all that apply.)

▫ To reduce costs ▫ To achieve efficiency of a smaller board

▫ Merger of organizations ▫ Other (specify): ____________________________▫ No

3. How long are terms for board members?

▫ 1 year ▫ 3 years ▫ Our terms have no specified length

▫ 2 years ▫ 4 years ▫ Other (specify): ________________

4. What is the maximum number of consecutive terms a board member may serve?

▫ 1 term ▫ 3 terms ▫ Not applicable

▫ 2 terms ▫ No limit ▫ Other (specify): ________________

5. Do board members receive compensation (excluding expense reimbursement) for serving on the board?

▫ Yes If yes, what is the average annual compensation a board member receives? $ ____________

▫ No If no, does your charter allow board members to be paid? ▫ Yes ▫ No

▫ Don’t Know

6. Is the credit union’s CEO a member of the board?

▫ Yes

▫ No If no, does your charter allow the CEO to be a board member? ▫ Yes ▫ No

APPENDIX : Credit Union Board Governance Sur vey

2626

7. Please indicate the number of board members that fall into each of the following age categories (estimates are fine):

______ Under 30 ______ 40-49 ______ 60-69 ______ 80 or older

______ 30-39 ______ 50-59 ______ 70-79

8. Please indicate the number of board members that fall into each of the following racial/ethnic groups (estimates are fine):

______ White Non-Hispanic ______ African-American ______ Other

______ Hispanic ______ Asian/Pacific Islander

9. Please indicate the number of board members that are male and the number that are female.:

______ Male ______ Female

10. How well do you feel the board reflects the composition of your credit union’s membership? (Circle only one.)

Not at all Very Closely

1 2 3 4 5

11. Which of the following best describes your credit union’s field of membership?

▫ Community credit union ▫ Single sponsor with substantial addition from SEG’s

▫ Predominantly single sponsor ▫ Other (specify): _____________________________

BOARD DEVELOPMENT PRAC TICES

12. How are new board members typically nominated? (Check all that apply.)

▫ By a committee of the board (i.e., a nominating committee)

a. If your credit union has a nominating committee, how many people are on it? ____b. Which of the following people are usually on the nominating committee?

(Check all that apply.)

▫ The CEO alone ▫ The board chair ▫ Non-board members

▫ The CEO ▫ Board members not up for re-election

▫ Board members ▫ Other (specify): __________________________▫ The board as a whole

▫ By a petition from the membership

c. Who appoints the nominating committee?▫ The board chair ▫ The executive committee of the board

▫ The full board ▫ Other (specify): __________________________

▫ Other (specify): _____________________________

13. How are elections for board seats conducted? (Check all that apply.)

▫ Mail ballots

▫ At the annual meeting

▫ Other (specify): _____________________________

14. Is proxy voting used for board seat elections? ▫ Yes ▫ No ▫ Not applicable

27

15. Please indicate the extent to which each of the following statements reflect practices used in your credit union.

The extent to which the credit union…Not at

allTo some

extent

To a great extent

Provides a comprehensive orientation for new board members 1 2 3 4 5

Has an effective process for preparing new board members for their role 1 2 3 4 5

Usually finds enough good candidates for the board 1 2 3 4 5

Typically has more than one candidate for each board position 1 2 3 4 5

Has a board development plan 1 2 3 4 5

Evaluates individual board member’s performance 1 2 3 4 5

Removes/replaces low performing members 1 2 3 4 5

Evaluates the performance of the board overall 1 2 3 4 5

The extent to which board members…Not at

allTo some

extent

To a great extent

Generally have the needed experience and background to be effective 1 2 3 4 5

Are engaged in the training they need to perform their role effectively 1 2 3 4 5

Commit sufficient time to perform their responsibilities 1 2 3 4 5

Have the appropriate skills to understand the complexities of credit unions 1 2 3 4 5

All contribute to making the board function effectively 1 2 3 4 5

Come to meetings well prepared 1 2 3 4 5

Understand and contribute constructively to the issues being discussed 1 2 3 4 5

The extent to which…Not at

allTo some

extent

To a great extent

Job descriptions exist for board member positions 1 2 3 4 5

Competency/skill profiles are developed and used to help nominate new board members 1 2 3 4 5

The CEO plays a role in board member recruitment 1 2 3 4 5

The nomination committee works throughout the year to identify a wide variety of potential candidates 1 2 3 4 5

Strategies are in place to insure a diversity of new board members 1 2 3 4 5

The number of candidates for board seats typically exceeds the number of seats to be filled 1 2 3 4 5

28

16. Please indicate the extent to which the following performance issues have been a concern about one or more board members in the past three years.

Has it been a concern that one or more board members…Not at all

To some extent

To a great extent

Not applicable

Provides insufficient time and effort 1 2 3 4 5 0

Has difficulty working with others 1 2 3 4 5 0

Interferes with management issues 1 2 3 4 5 0

Has insufficient knowledge and understanding 1 2 3 4 5 0

Has physical or cognitive limitations 1 2 3 4 5 0

17. Which of the following statements describes how the board would most likely deal with an incumbent that has not contributed much during his/her current term but wants to re-nominated for another term? (Check all that apply.)

The non-contributing board member…

▫ Is re-nominated and no one else is placed on the ballot to contest the position

▫ Is re-nominated along with one or more other candidates so the position is contested

▫ Is encouraged by someone on the board or CEO to not run for the position, so that they are ultimately not placed on the ballot

▫ Is encouraged by a staff member to not run for the position, so that they are ultimately not placed on the ballot

▫ Ultimately negotiates to be placed on the ballot

▫ None of these apply to our board

18. Please indicate the extent to which you agree with the statement: “The nominating committee at our credit union always re-nominates any incumbent who would like to serve another term.”

▫ Strongly agree ▫ Neither agree nor disagree ▫ Strongly disagree

▫ Agree ▫ Disagree ▫ Don’t know or not applicable

19. How would you describe board turnover in the past five years?

▫ Not enough ▫ About right ▫ Too much

20. Approximately, how long has it been since a board member left the board?

▫ Less than a year ▫ 3-4 years ▫ 8 years or more

▫ 1-2 years ▫ 5-7 years

21. In your opinion, the length of time a board member needs to serve on the board before he or she becomes fully effective is usually about:

▫ 6 months or fewer ▫ 2 years ▫ 4 years or more

▫ 1 year ▫ 3 years

22. In your opinion, in order to ensure effective board member performance the total length of continuous service by a board member should be about:

▫ 1-3 years ▫ 7-10 years ▫ Unlimited except by an appropriate age limit

▫ 4-6 years ▫ Unlimited ▫ Other (specify): ______________________

29

Do you have an emeritus program for prior board members?

▫ Yes If yes, how effective has this program been in helping to open up positions on the board?

▫ No ▫ Very effective ▫ Neither effective nor ineffective ▫ Very ineffective

▫ Somewhat effective ▫ Somewhat ineffective ▫ Don’t know

23. Do you have a mandatory retirement age policy for board members?

▫ Yes (specify age): _______

▫ No If no, do you think your credit union’s board should have a mandatory retirement age policy?

▫ Yes ▫ No

24. What are some of the most effective ways your organization uses to get good board members?

25. What are some of the most effective ways your organization uses to prepare and retain high performing board members?

26. What are some of the most effective ways your organization uses to remove unproductive board members?

27. Please consider the following description of board development practices and then indicate the extent to which your credit union is reflected in these ideas:

Our credit union board is made up of individuals who can contribute critically needed skills, experience, wisdom and time to the organization. Because no one person can provide all of those qualities and because the needs of an organization continually change, our board has a well-conceived plan to identify and recruit the most appropriate people to serve on the board. Once selected, new members are oriented to the organization and existing board members receive training on pertinent topics. Our board also regularly rotates people off the board to ensure that it can be infused with new ideas without making the board so large that it becomes unwieldy.

The description above…

▫ Does not describe my credit union’s board at all ▫ Mostly describes my credit union’s board

▫ Slightly describes my credit union’s board ▫ Completely describes my credit union’s board

▫ Somewhat describes my credit union’s board

30

28. Please rate the effectiveness of your credit union’s board of directors in each of the following areas:

Not at all

Neither Effective nor ineffective

Very Effective

Providing financial oversight 1 2 3 4 5

Serving member interests and needs 1 2 3 4 5

Setting mission, policies, and long-range strategy 1 2 3 4 5

Marketing and promoting the organization 1 2 3 4 5

Evaluating and selecting (if necessary) the senior executive 1 2 3 4 5

Ensuring consistency and high quality leadership on the board 1 2 3 4 5

29. Overall, how satisfied are you with the performance of your credit union’s board?

▫ Very satisfied ▫ Neither satisfied nor dissatisfied ▫ Very dissatisfied

▫ Somewhat satisfied ▫ Somewhat dissatisfied ▫ Don’t know

30. For each of the following areas please rate your credit union’s performance over the past 12 months compared to that of similar credit unions:

Much worse than

elsewhereSame as

elsewhere

Much better than

elsewhere

Financial management/performance 1 2 3 4 5

Member service and range of services offered 1 2 3 4 5

Member relations 1 2 3 4 5

RESPONDENT INFORMATION

31. What is your position with this credit union?

▫ Board chair ▫ Board member (not the chair)

▫ CEO ▫ Other (specify): ______________________

32. How long have you been in your current position at the credit union? _________ years

33. How long have you been affiliated with this credit union? ___________ years

34. The results of the study will be emailed to participants. If you would like a copy please provide the following contact information:Name: ________________________ Email address: ________________________ Phone: ____________________

31

Filene Research Institute Administrative Board

Research Council

CHAIRMAN Thomas R. Dorety, President/CEO Suncoast Schools Federal Credit Union

VICE CHAIRMAN Lawrence D. Knoll, President/CEO Midwest Financial Credit Union

VICE PRESIDENT/TREASURER Daniel A. Mica, President/CEO CUNA & Affiliates

SECRETARY Paul Mercer Chairman, American Association of Credit Union Leagues President, Ohio Credit Union League

DIRECTOR Jeff H. Post, President/CEO CUNA Mutual Group

DIRECTOR Patsy Van Ouwerkerk, President/CEO Travis Credit Union

PRESIDENT EMERITUS Richard M. Heins, Director Emeritus CUNA Mutual Group

Martin M. Breland, President/CEO Tower Federal Credit Union

David Brock, President/CEO Community Educators’ Credit Union

Bruce Brumfield, President/CEO Founders Federal Credit Union

Michael J. Connery, President/CEO United Nations Federal Credit Union

32

Sharon Custer, President BMI Federal Credit Union

Charles F. Emmer, President/CEO Ent Federal Credit Union

W. Craig Esrael, President/CEO First South Credit Union

Kathy Garner, President/CEO Northwest Corporate Credit Union

Charles Grossklaus, President/CEO Royal Credit Union

Robert H. Harvey, President/CEO Seattle Metropolitan Credit Union

Hubert H. Hoosman, President/CEO Vantage Credit Union

Andrew Hunter, President/CEO Patelco Credit Union

Gary W. Irvin, President/CEO Forum Credit Union

Olan O. Jones, President/CEO Eastman Credit Union

Kirk Kordeleski, President/CEO Bethpage Federal Credit Union

Mike L’Ecuyer, President/CEO Telephone Credit Union of New Hampshire

Harriet B. May, President/CEO Government Employees Credit Union of El Paso

David Mooney, President/CEO Alliant Credit Union

Marcus B. Schaefer, President/CEO Truliant Federal Credit Union

Robb Scott, President/CEO Deer Valley Credit Union

33

Jack Sheets, President/CEO Elkhart County Farm Bureau Credit Union

Bob Siravo, President/CEO WesCorp

Patricia E. Smith, President/CEO Oregon Telco Community Credit Union

A. Lee Williams, President/CEO Aviation Associates Credit Union

Ex-Officio: Fred B. Johnson, President Credit Union Executives Society

FILENE RESEARCH INSTITUTE Robert F. Hoel, Ph.D. Executive Director

George A. Hofheimer Director of Research

34

35

Aldag, Ramon J. and Antonioni, David, University of Wisconsin-Madison. Mission Values and Leadership Styles In Credit Unions, 2000.

Amburgey, Terry L., University of Kentucky and Dacin, M. Tina, Texas A&M University. Evolutionary Development of Credit Unions, 1993.

Barrick, Murray R., University of Iowa. Human Resource Testing: What Credit Unions Should Know, 2002.

Barrick, Murray R., University of Iowa. Predicting Employee Turnover and Performance: Pre-Employment Tests and Questions that Work, 2003.

Barron, David N. and West, Elizabeth, University of Oxford; and Hannan, Michael T., Stanford University. Competition, Deregulation, and the Fortunes of Credit Unions, 1995.

Brown, William A., Arizona State University. Recruitment and Selection Practices at Credit Union Boards, 2005.

Burger, Albert E. and Dacin, Tina, University of Wisconsin-Madison. Field of Membership: An Evolving Concept, 1991.

Burger, Albert E., University of Wisconsin-Madison; Fried, Harold O., Union College; Lovell, C. A. Knox, University of Georgia. Technology Strategies of Best Practice Credit Unions: Today, the Near Future, and the Far Future, 1997.

Burger, Albert E., University of Wisconsin-Madison and Kelly, Jr., William A., CUNA Research & Development. Building High Loan/Share Ratios: Challenges and Strategies, 1993.

Burger, Albert E., University of Wisconsin-Madison and Lypny, Gregory M., Concordia University, Montreal, Canada. Taxation of Credit Unions, 1991.

Burger, Albert E. and Zellmer, Mary, University of Wisconsin-Madison. Strategic Opportunities in Serving Low to Moderate Income Individuals, 1995.

Burger, Albert E., Zellmer, Mary and Robinson, David, University of Wisconsin-Madison. The Digital Revolution: Delivering Financial Services in the Future, 1997.

Filene Research Institute Publications

36

Caskey, John P., Swarthmore College. The Economics of Payday Lending, 2002.

Caskey, John P., Swarthmore College. Lower Income Americans, Higher Cost Financial Services, 1997.

Caskey, John P., Swarthmore College; Humphrey, David B., Florida State University; Kem, Reade, research assistant. Credit Unions and Asset Accumulation by Lower-Income Households, 1999.

Caskey, John P., Swarthmore College and Brayman, Susan J., assistant. Check Cashing and Savings Programs for Low-Income Households: An Action Plan for Credit Unions, 2001.

Colloquium at Stanford University. Consolidation of the Financial Services Industry: Implications for Credit Unions, 1999.

Colloquium at the University of California-Berkeley. Financial Incentives to Motivate Credit Union Managers and Staff, 2001.

Colloquium at the University of California–Berkeley. Three Innovative Searches for Better Incentive Programs, 2001.

Colloquium at the University of California–San Diego. Serving New Americans: A Strategic Opportunity for Credit Unions, 2003.

Colloquium at the University of Virginia. Attracting and Retaining High-Quality Employees: New Strategies for Credit Unions, 2001.

Colloquium at the University of Virginia. Fresh Approaches to Bankruptcy and Financial Distress – Volume I: Why Don’t More People Declare Bankruptcy?, 2000.

Colloquium at the University of Virginia. Fresh Approaches to Bankruptcy and Financial Distress – Volume II: Working With Members in Financial Distress, 2000.

Colloquium at the University of Virginia. Managing Credit Union Capital: Subordinated Debt, Uninsured Deposits, and Other Secondary Sources, 2004.

Colloquium at the University of Wisconsin–Madison. Financial Stress and Workplace Performance: Developing Employer-Credit Union Partnerships, 2002.

37

Colloquium sponsored by the Filene Research Institute and the Center for Credit Union Research – Madison, Wisconsin. Outsourcing and Sharing Credit Union Management , 2003.

Colloquium sponsored by the Filene Research Institute and the Center for Credit Union Research – Madison, Wisconsin. Strategy Errors Made by Even the Smartest CEOs: How to Avoid Them in Credit Unions, 2005.

Compeau, Larry D., Clarkson University. Successful Turnarounds from Bad Credit to Good: What We Can Learn from the Borrower’s Experience, 2001.

Dacin, Peter A., Texas A&M University. Marketing Credit Union Services: The Role of Perceived Value, 1995.

Donkersgoed, William L. and Hautaluoma, Jacob E., Colorado State University; and Pipal, Janet E. Consensus Building Strategies for Productive CEO-Board Relationships, 1998.

Doyle, Joanne M., James Madison University; Kelly, William A. Jr., University of Wisconsin-Madison. Predicting and Managing a Credit Union’s Expense Ratio, 2004.

Feinberg, Robert M., American University. The Effects of Credit Unions on Bank Rates in Local Consumer Lending Markets, 2001.

Feinberg, Robert M., American University. The Effect of Credit Unions on Market Rates for Unsecured Consumer Loans, 1999.

Feinberg, Robert M., American University and Kelly, Jr., William A., University Wisconsin–Madison. Less-Restricted Fields of Member-ship for Credit Unions: Public Policy Implications, 2003.

Feinberg, Robert M., American University; and Rahman, Ataur, American University. Key Influences on Loan Pricing at Credit Unions and Banks, 2004.

Filene Research Institute and The Center for Credit Union Innovation, LLC, in cooperation with the National Credit Union Foundation. 15 Steps to an Effective SEG Program, 2003.

Filene Research Institute. Attracting and Retaining Young Adult Members, 2003

38

Fried, Harold O., Union College; Hoel, Robert F., Filene Research Institute; Kelly, Jr., William A., University of Wisconsin-Madison. Member Satisfaction Levels: National Norms for Comparing Local Survey Results, 1998.

Fried, Harold O., Union College; Hoel, Robert F., Filene Research Institute; Kelly, Jr., William A., University of Wisconsin-Madison. Member Satisfaction Levels: National Norms for Comparing Local Survey Results Second Edition, 2002.

Fried, Harold O., Union College and Lovell, C. A. Knox, University of Georgia. Credit Union Service-Oriented Peer Groups, 1994.

Fried, Harold O., Union College and Lovell, C. A. Knox, University of North Carolina. Evaluating the Performance of Credit Unions, 1992.

Fried, Harold O., Union College; Lovell, C. A. Knox, University of Georgia and University of New South Wales; Yaisawarng, Suthathip, Union College. How Credit Union Mergers Affect Service to Members, 1999.

Fried, Harold O., Union College and Overstreet, Jr., George A., University of Virginia, editors; Frank Berrish, Thomas Sargent, and James Ware, contributors. Information Technology and Management Structure: A Case Study of First Technology Credit Union, 1998.

Fried, Harold O., Union College and Overstreet, Jr., George A., University of Virginia, editors; Richard Grenci, Peter Keen, R. Ryan Nelson, and Nancy Pierce, contributors. Information Technology and Management Structure II: Insights for Credit Unions, 1999.

Grube, Jean A. and Aldag, Ramon J., University of Wisconsin-Madison. How Organizational Values Affect Credit Union Performance, 1996.

Hannan, Michael T., Stanford University; and West, Elizabeth and Barron, David N., McGill University. Dynamics of Populations of Credit Unions, 1994.

Hautaluoma, Jacob E., Donkersgoed, William J. and Morgan, Kimberly J., Colorado State University. Board-CEO Relationships: Successes, Failures, and Remedies, 1996.

Hautaluoma, Jacob E., Jobe, Lloyd, Donkersgoed, Bill, Suri, Taaj and Cropanzano, Russell, Colorado State University. Credit Union Boards and Credit Union Effectiveness, 1993.

39

Hoel, Robert F., Filene Research Institute and Kelly, Jr., William A., University of Wisconsin-Madison. Why Many Small Credit Unions Are Thriving, 1999.

Humphrey, David B., Florida State University. Prospective Changes in Payment Systems: Implications for Credit Unions, 1997.

Jackson, III, William E., University of North Carolina–Chapel Hill. The Future of Credit Unions: Public Policy Issues, 2003.

Jackson, III, William E., University of North Carolina-Chapel Hill. Pricing Movements and For-Profit Behavior: A Comparison of Banks and Credit Unions, 2005

Johnson, Ramon E., University of Utah. Field of Membership and Performance: Evidence from the State of Utah, 1995.

Joseph, Matt L. Changes in the Automotive Distribution System: Challenges and Opportunities for Credit Unions, 2001.

Kane, Edward J., Boston College. Deposit Insurance Reform: A Plan for the Credit Union Movement, 1992.

Kane, Edward J., Boston College; and Hickman, James C. and Burger, Albert E., University of Wisconsin-Madison. Implementing a Private-Federal Deposit Insurance Partnership, 1993.

Karofsky, Judith F., Center for Credit Union Research, University of Wisconsin-Madison School of Business. Shopping Strategies for Financial Consumers: a Study of Three Markets, 2000.

Kelly, Jr., William A., University of Wisconsin-Madison. Financial Strength: A Comparison of State and Federal Credit Unions, 1998.

Kelly, Jr., William A. and Karofsky, Judith F., University of Wisconsin-Madison. Federal Credit Unions Without Federal Share Insurance: Implications for the Future, 1999.

Kelly, Jr., William A. and Karofsky, Judith F., University of Wisconsin-Madison; HARK Management, Inc.; Krueckeberg, Harry F., Colorado State University (retired). Monetary Incentives for Credit Union Staffs, 1998.

Lambrinos, James, Union College and Kelly, Jr., William A., University of Wisconsin-Madison. The Effects of Member Income Levels on Credit Union Financial Performance, 1996.

40

Lee, Jinkook, Ohio State University and Kelly, Jr., William A., University of Wisconsin-Madison. Building Savings-Per-Member at Credit Unions, 2004.

Lee, Jinkook, University of Georgia and Kelly, Jr., William A., University of Wisconsin-Madison. Financial Product Use over Household Life Cycles: A Guide for Credit Unions, 2002.

Lee, Jinkook, Ohio State University and Kelly, Jr., William A., University of Wisconsin-Madison. Gifts That Connect the Generations: A Role for Credit Unions, 2004.

Lee, Jinkook, University of Georgia and Kelly, Jr., William A., University of Wisconsin-Madison. The Human Touch in the Information Age: What Do Members Want?, 2001.

Lee, Jinkook, Ohio State University and Kelly, Jr., William A., University of Wisconsin-Madison. Inheritances: Who Expects to Leave Money to Heirs?, 2004.

Lee, Jinkook, University of Georgia and Kelly, Jr., William A., University of Wisconsin-Madison. Life Cycle Marketing for Credit Unions: Mid Age Households, 2002.

Lee, Jinkook, University of Georgia and Kelly, Jr., William A., University of Wisconsin-Madison. Life Cycle Marketing for Credit Unions: Senior Households, 2002.

Lee, Jinkook, University of Georgia and Kelly, Jr., William A., University of Wisconsin-Madison. Life Cycle Marketing for Credit Unions: Young Households, 2001.

Lee, Jinkook, Ohio State University and Kelly, Jr., William A., University of Wisconsin-Madison. Marketing Checking Accounts to Members: A Guide for Credit Unions, 2003.

Lee, Jinkook, Ohio State University and Kelly, Jr., William A., University of Wisconsin-Madison. Professional Financial Advice for Consumers: Implications for Credit Unions, 2003.

Lee, Jinkook, Ohio State University and Kelly, Jr., William A., University of Wisconsin-Madison. Uninsured Accounts: An Assessment of Member Interest, 2003.

41

Lee, Jinkook, University of Georgia and Kelly, Jr., William A., University of Wisconsin-Madison. Where Are Households’ Financial Assets?, 2001.

Lee, Jinkook, University of Georgia and Kelly, Jr., William A., University of Wisconsin-Madison. Who Uses Credit Unions? Second Edition, 2001.

Lee, Jinkook, Ohio State University and Kelly, Jr., William A., University of Wisconsin-Madison. Who Uses Credit Unions? Third Edition, 2004.

Lee, Jinkook, University of Tennessee and Kelly, Jr., William A., University of Wisconsin-Madison. Who Uses Credit Unions?, 1999.

Lemmon, Nicolette, LEMMON-AID Marketing Services; Gourley, David, Arizona State University; Ward, James, Arizona State University. Member Acceptance of Electronic Access Systems: Innovators versus Laggards, 1999.

Lepisto, Lawrence R., Central Michigan University. Consumer Relationships with Financial Institutions, 1993.

Lepisto, Lawrence R., Central Michigan University. Psychological and Demographic Factors Affecting Relationships with Financial Institutions, 1994.

Matsumura, Ella Mae and Dickson, Peter, University of Wisconsin-Madison; and Kelly, Jr., William A., University of Wisconsin-Madison, Member Segmentation and Profitability: Current Practice and Future Possibilities, 1999.

Meyer, Mark C. The Implementation of Check-Cashing Services: A Growth Opportunity for Credit Unions, 2004.

Overstreet, Jr., George A., University of Virginia and Rubin, Geoffrey M., Princeton University. The Applicability of Credit Scoring in Credit Unions, 1996.

Overstreet, Jr., George A. and Rubin, Geoffrey M., University of Virginia. Blurred Vision: Challenges in Credit Union Research and Modeling, 1991.

42

Proceedings from the Second Annual Credit Union Colloquium co-sponsored by Filene Research Institute, Center for Credit Union Research, and the Center for Financial Services Studies. Discrimination in Lending: What Are the Issues?, 1995.

Reynolds, Bruce L., University of Virginia. Household Credit in China: Recent Experience and Lessons from Other Countries, 2005.

Sayles, William W., The Center for Credit Union Innovation, LLC. Serving Members Around the Globe, 2001.

Sayles, William W., The Center for Credit Union Innovation, LLC. Small Business: The New Frontier, 2002.

Sayles, William W., The Center for Credit Union Innovation, LLC. Small Credit Union Data Processors: Survey Results, 2002.

Siciliano, Julie, Florida Institute of Technology. Enhancing Board Satisfaction at Credit Unions, 2004.

Smith, David M., Pepperdine University and Woodbury, Stephen A., Michigan State University. Differences in Bank and Credit Union Capital Needs, 2001.

Sollenberger, Harold M., Michigan State University and Schneckenburger, Kurt, Olson Research Associates, Inc. Applying Risk-Based Capital Ratios to Credit Unions, 1994.

Sullivan, A. Charlene, Purdue University and Worden, D. Drecnik, Olivet Nazarene University. Personal Bankruptcy: Causes and Consequences, 1992.

Udell, Jon G., University of Wisconsin-Madison and Kelly, Jr., William A., University of Wisconsin-Madison. Asset Growth at Credit Unions: Growth in Membership vs. Assets per Member, 2004.

Udell, Jon G., University of Wisconsin-Madison. Management Practices and Growth at Mid-sized Credit Unions (Assets of $50-200 Million), 2003.

Warfield, Terry D., University of Wisconsin-Madison and Henning, Steven L., University of Colorado-Boulder. Financial Reporting by Credit Unions in the United States, 1994.

43

Whitener, Ellen M., University of Virginia. The Effects of Human Resource Practices on Credit Union Employees and Performance, 1998.

Whitener, Ellen M., University of Virginia and Brodt, Susan E., Duke University. Forging Employee Morale, Trust and Performance, 2000.

Wilcox, James A., Haas School of Business, University of California, Berkeley. Capital Instruments for Credit Unions: Precedents, Issuance and Implementation, 2003.

Wilcox, James A., Haas School of Business, University of California, Berkeley. Failures and Insurance Losses of Federally-Insured Credit Unions: 1971-2004, 2005.

Wilcox, James A., Haas School of Business, University of California, Berkeley. Subordinated Debt for Credit Unions, 2002.

Woodbury, Stephen A. and Smith, David M., Michigan State University; and Kelly, Jr., William A., University of Wisconsin-Madison. An Analysis of Public Policy on Credit Union Select Employee Groups, 1997.

Woodbury, Stephen A., Michigan State University; Smith, David M., Pepperdine University; Kelly, Jr., William A., University of Wisconsin-Madison. A State and Regional Analysis: Effects of Public Policy on Credit Union Select Employee Groups, 1997.

44