Recent Trends in M&A in Asia - American Bar...

35

Recent Trends in M&A in Asia ABA Section of International Law 2016 Fall Meeting – Tokyo Mitsuru Claire Chino (ITOCHU Corporation) Tao Guo (JunHe LLP) Ng Eng Leng (Dentons Rodyk & Davidson LLP) Kaye Naoko Yoshino (Paul, Weiss, Rifkind, Wharton & Garrison LLP)

Transcript of Recent Trends in M&A in Asia - American Bar...

Recent Trends in M&A in Asia

ABA Section of International Law

2016 Fall Meeting – Tokyo

Mitsuru Claire Chino (ITOCHU Corporation)

Tao Guo (JunHe LLP)

Ng Eng Leng (Dentons Rodyk & Davidson LLP)

Kaye Naoko Yoshino (Paul, Weiss, Rifkind, Wharton & Garrison LLP)

Summary of the Committee’s session in Tokyo – Recent trends in M&A in Asia

Recent trends in Asian M&A - this subject was very topical to discuss in Tokyo which is one of the significant M&A centers of Asia. The beginning of the session was chaired by Mr. Takashi Toichi of Anderson Mori & Tomotsune, Tokyo. Mr. Toichi explained that the session would be discussed from three perspectives; Asia to US/Europe, US/Europe to Asia, and Asia to Asia. During the session, recent trends in each market were explained by Mr. Eng Leng NG from Dentons Rodyk & Davidson, Singapore, by using a PowerPoint presentation depicting very recent figures. He explained, among others, about the increasing Asian investments in ASEAN countries, by Japanese and Chinese investors, and some of the key industries where these investments were made. Mr. Tao Guo from JuneHe, Beijing, explained about the increase of Chinese investors and supported his statement with statistics and relevant background. He discussed about applicable Chinese regulations for outbound investments by Chinese investors. He also spoke about challenges that investors from Western countries are facing regarding Chinese antitrust law and obtaining other regulatory approvals, and also about how Chinese companies seek investment into Japanese and ASEAN countries. Ms. Kaye N. Yoshino from Paul Weiss, Tokyo, explained about Chinese companies facing increased regulatory scrutiny abroad and uncertainties surrounding CFIUS creating a disadvantage for Chinese investors because of which, they are required to offer higher price, higher termination fee and escrow, etc. in order to enter foreign markets. She also mentioned that Chinese companies prefer to carry out acquisitions in Europe than in the US because of the real and perceived difficulties with CFIUS. In addition, she shares her experience about difficulties Asian companies are facing regarding investments in India, from tax exposure and negotiation perspectives.

Ms. Mitsuru Claire Chino, Executive Officer and General Counsel of Itochu Corporation, Tokyo, shared her experience as in-house counsel of a leading Japanese trading house. She empathized the importance of due diligence, especially integrity due diligence in supply chain management etc., and about the increasing trend of many jurisdictions to require pre-merger notification filings in an extra-territorial manner. She also spoke on the increased importance of due diligence on anticorruption based on the OECD and JFBA guideline, and also from corporate governance perspectives. To summarize the event: panelists had lively discussed regarding the increase of Chinese and other Asian country investors investing heavily in US/Europe and the arising legal issues relating thereto, including CFIUS. They even discussed the legal and cultural barriers investors from US/Europe and even some Asian countries were facing with respect to the recent trends emerging in M&As in Asia.

Takashi Toichi (Anderson Mori & Tomotsune)

Asia to US/Europe

3

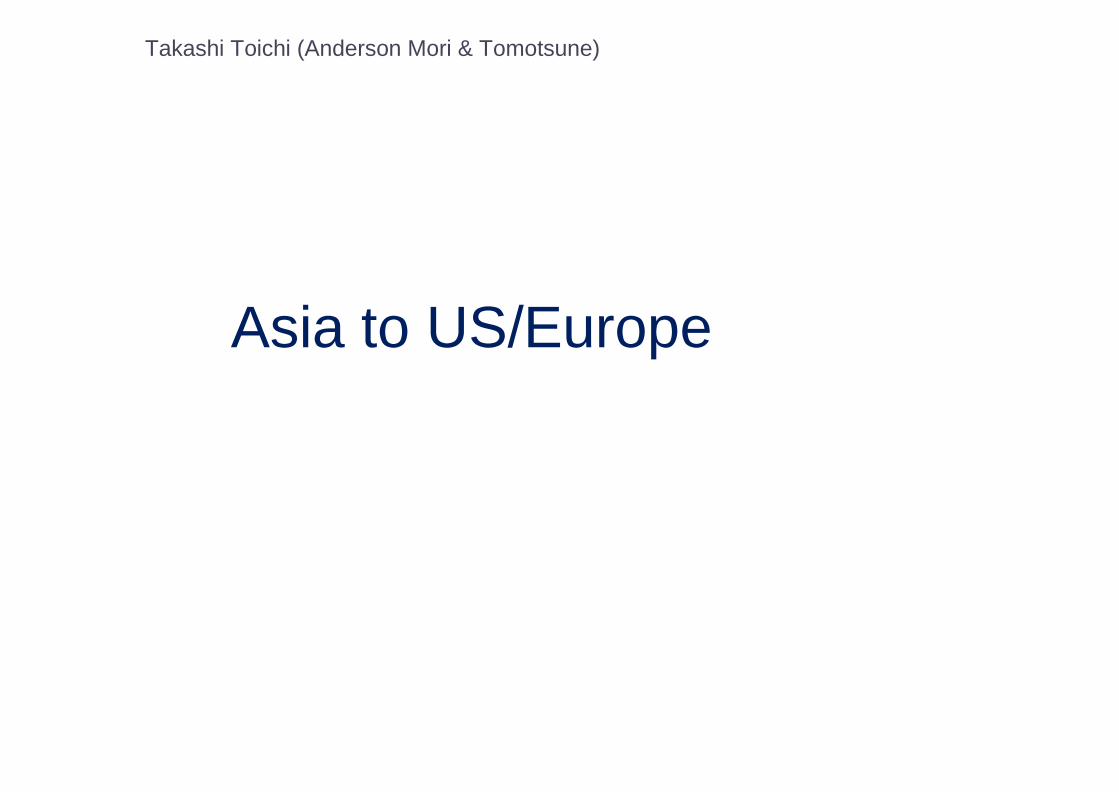

Asian outbound to US and Europe by deal count

450

400

350

300

250

200

Europe

US

150

100

50

0

2013 2014 2015 H1 2016

165

395

313

276

251 244

204

148

Dea

l co

un

t

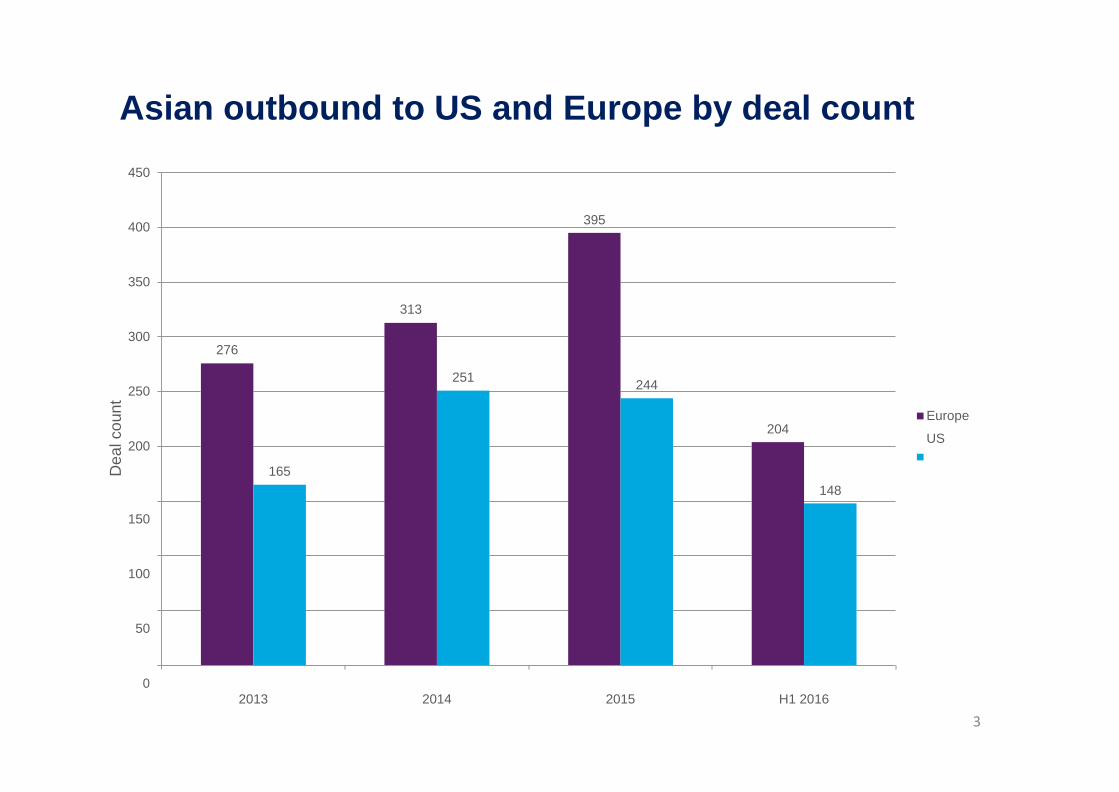

Asian outbound to US and Europe

M&A – industry of target for the full analyzed period

4

Utilities, 2% Insurance, 1% Telecommunications, 1%

Retailing, 3%

Diversified Financials, 3%

Media, 3%

Energy, 3%

Diversified Fin; 4%

Materials, 6%

Info Tech, 18%

Real Estate, 17%

Info Tech Real Estate

Industrials Consumer

Healthcare Materials

Automotive Energy

Healthcare, 7%

Consumer, 15%

Industrials, 16%

Media

Diversified Financials

Retailing

Utilities Insurance

Telecommunications

Based on total deal count

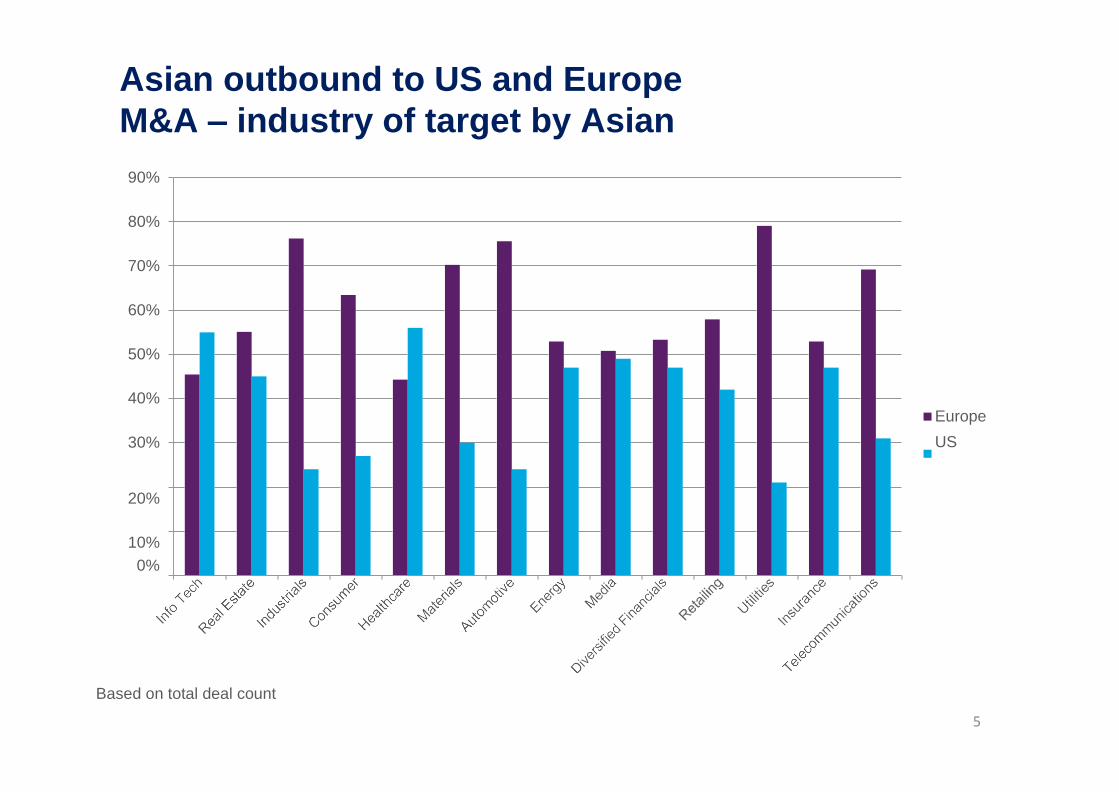

Asian outbound to US and Europe

M&A – industry of target by Asian buyer

Based on total deal count

5

90%

80%

70%

60%

50%

40%

30%

Europe

US

20%

10%

0%

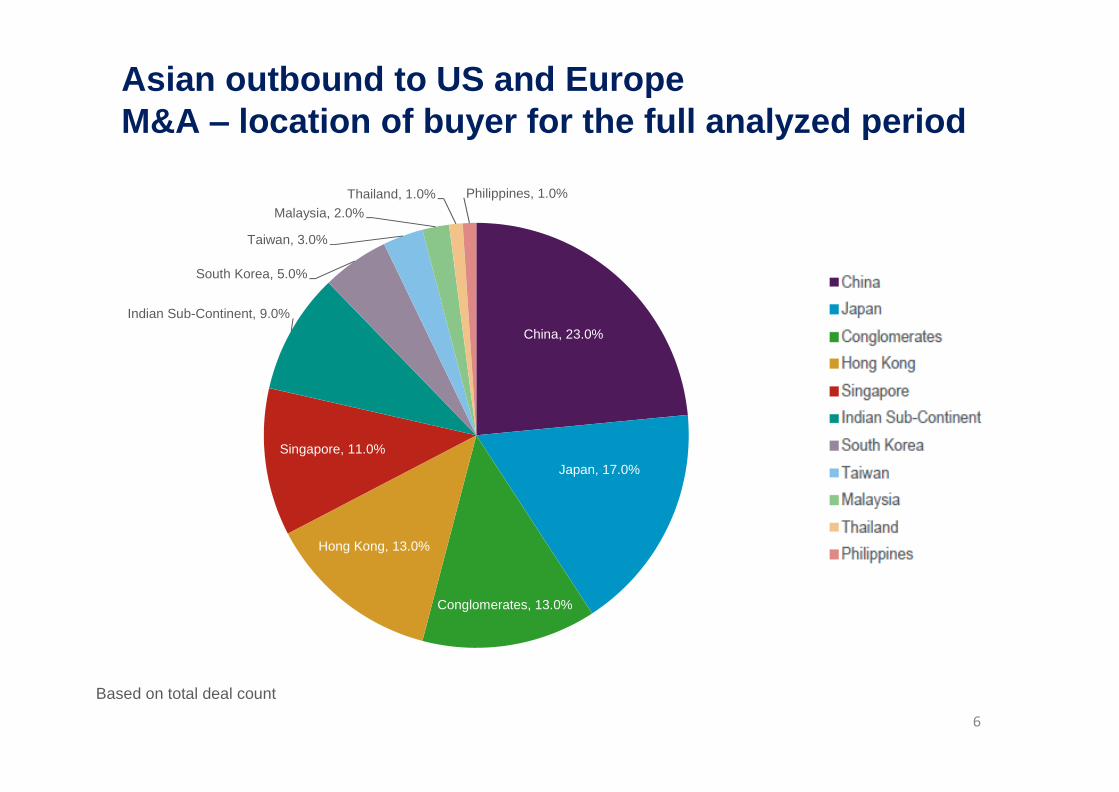

Asian outbound to US and Europe

M&A – location of buyer for the full analyzed period

Based on total deal count

6

Thailand, 1.0% Philippines, 1.0%

Malaysia, 2.0%

Taiwan, 3.0%

South Korea, 5.0%

Indian Sub-Continent, 9.0%

Singapore, 11.0%

Hong Kong, 13.0%

China, 23.0%

Japan, 17.0%

Conglomerates, 13.0%

China Japan

Conglomerates

Hong Kong

Singapore

Indian Sub-Continent

South Korea

Taiwan Malaysia

Thailand Philippines

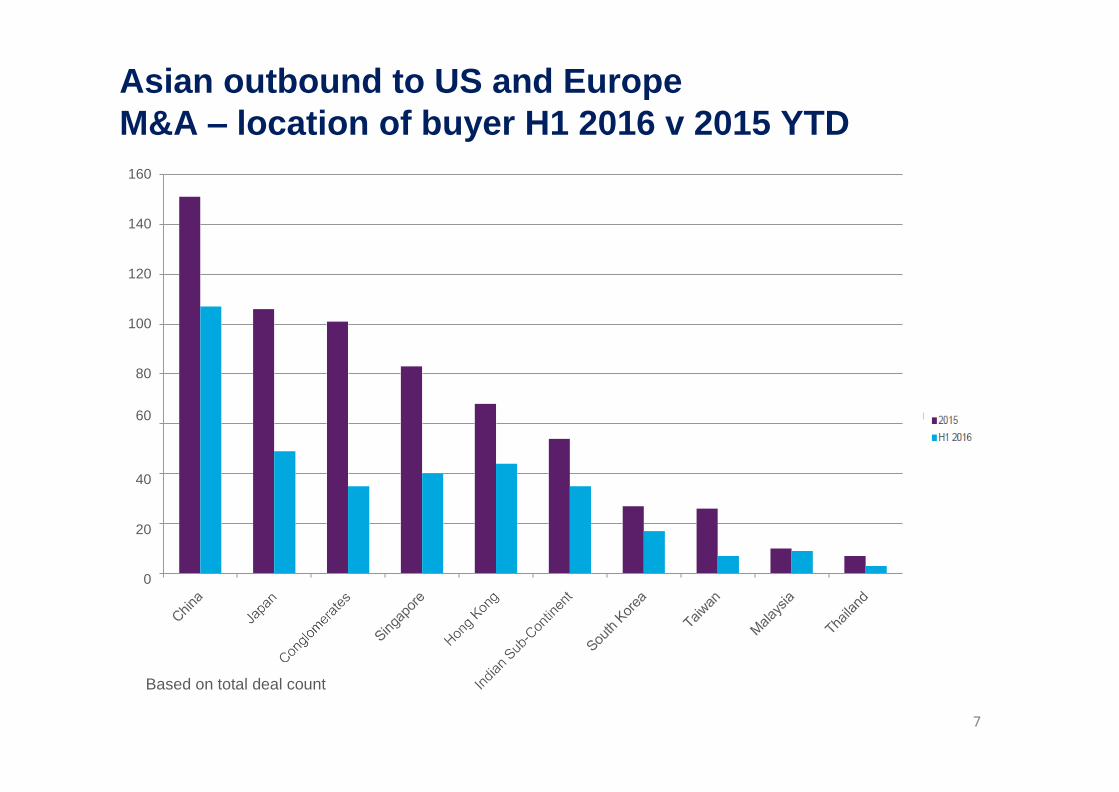

Asian outbound to US and Europe

M&A – location of buyer H1 2016 v 2015 YTD

7

160

140

120

100

80

60

40

20

0

Based on total deal count

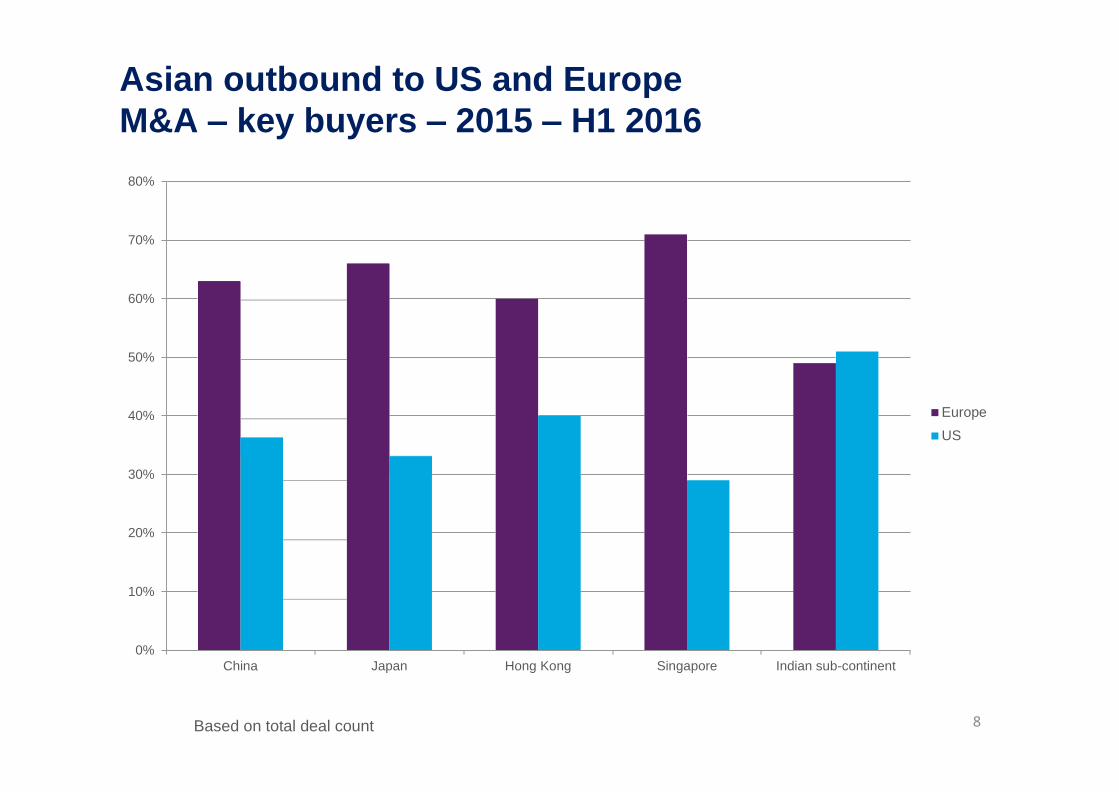

Asian outbound to US and Europe

8 Based on total deal count

M&A – key buyers – 2015 – H1 2016

80%

70%

60%

50%

40% Europe

US

30%

20%

10%

0%

China Japan Hong Kong Singapore Indian sub-continent

9

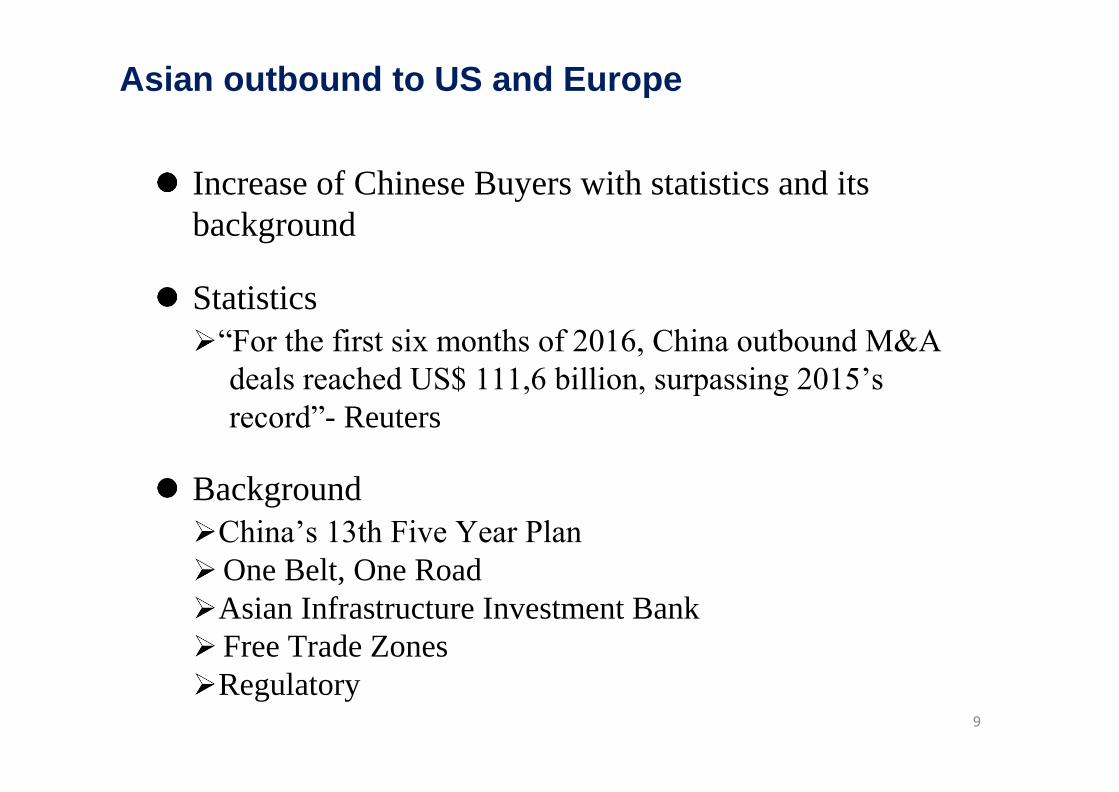

Asian outbound to US and Europe

Increase of Chinese Buyers with statistics and its

background

Statistics

“For the first six months of 2016, China outbound M&A

deals reached US$ 111,6 billion, surpassing 2015’s

record”- Reuters

Background

China’s 13th Five Year Plan

One Belt, One Road

Asian Infrastructure Investment Bank

Free Trade Zones

Regulatory

10

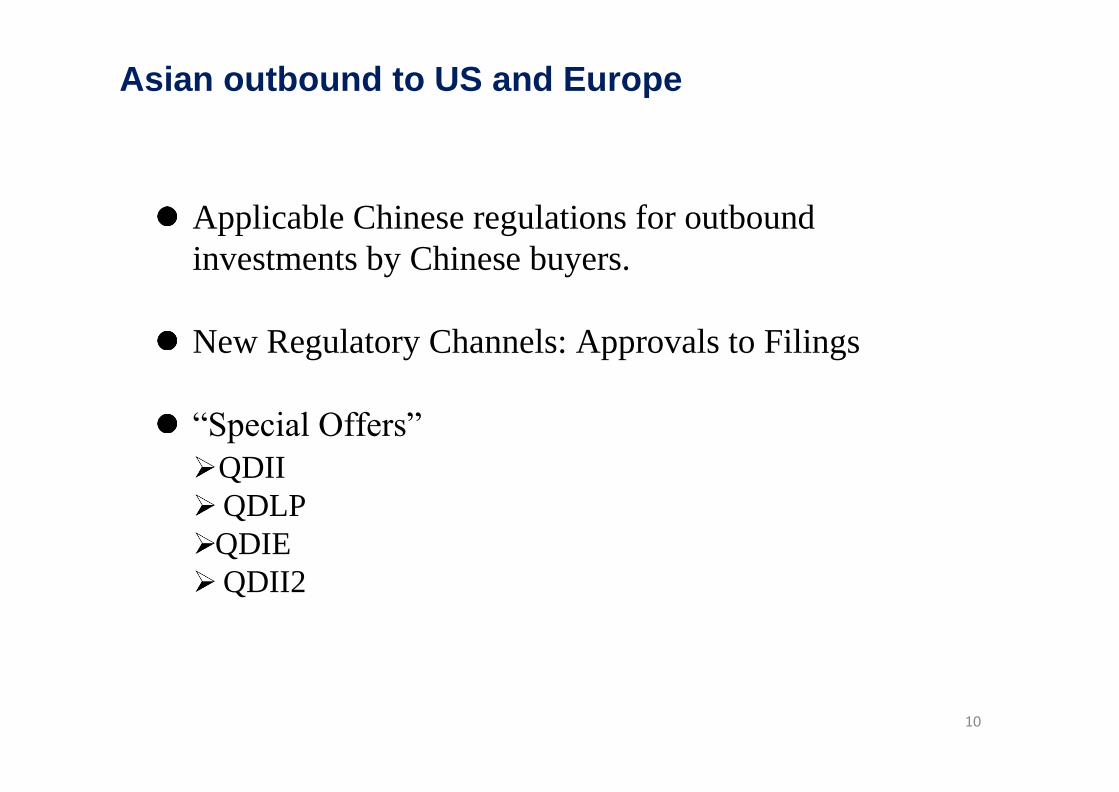

Asian outbound to US and Europe

Applicable Chinese regulations for outbound

investments by Chinese buyers.

New Regulatory Channels: Approvals to Filings

“Special Offers”

QDII

QDLP

QDIE

QDII2

Asian outbound to US and Europe

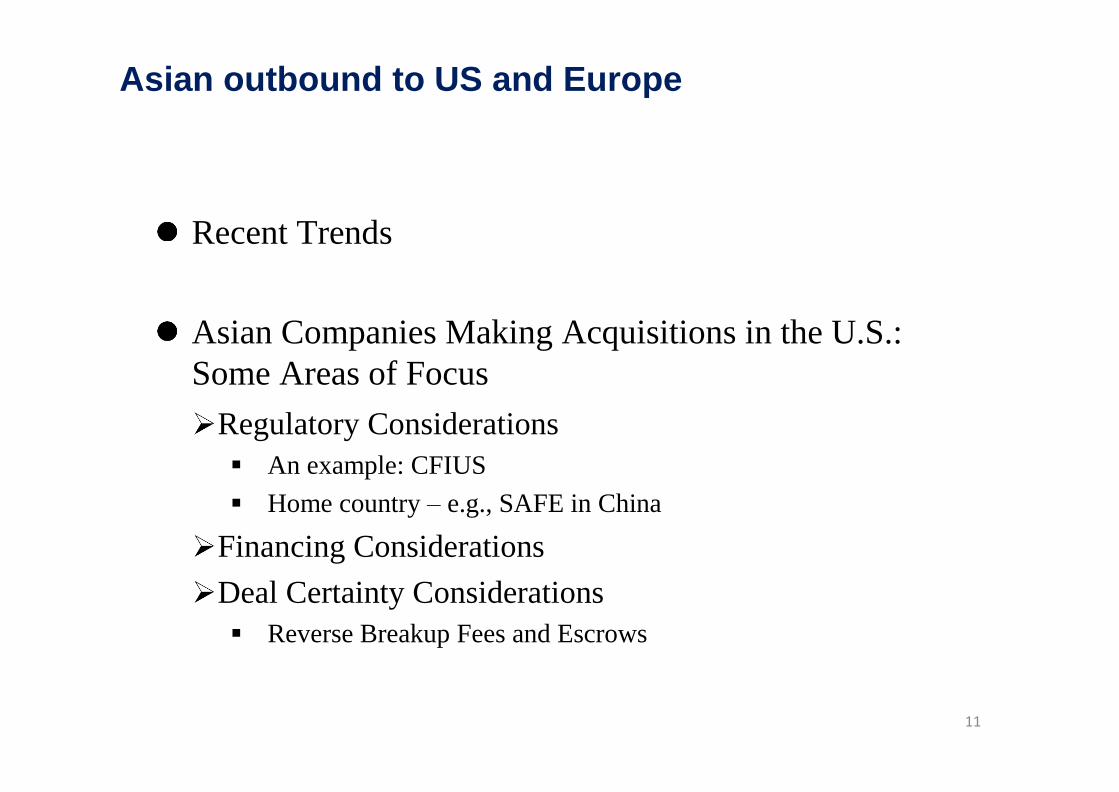

11

Recent Trends

Asian Companies Making Acquisitions in the U.S.:

Some Areas of Focus

Regulatory Considerations

An example: CFIUS

Home country – e.g., SAFE in China

Financing Considerations

Deal Certainty Considerations

Reverse Breakup Fees and Escrows

Asian outbound to US and Europe

12

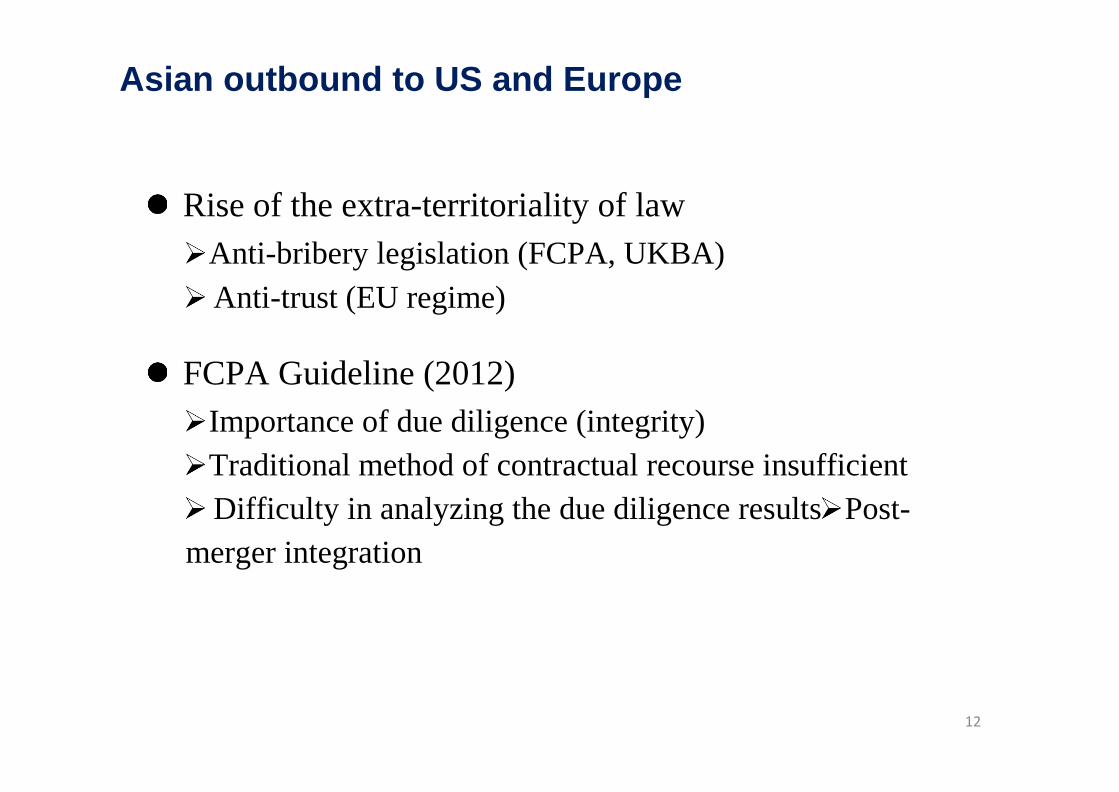

Rise of the extra-territoriality of law

Anti-bribery legislation (FCPA, UKBA)

Anti-trust (EU regime)

FCPA Guideline (2012)

Importance of due diligence (integrity)

Traditional method of contractual recourse insufficient

Difficulty in analyzing the due diligence results Post-

merger integration

US/Europe to Asia

14

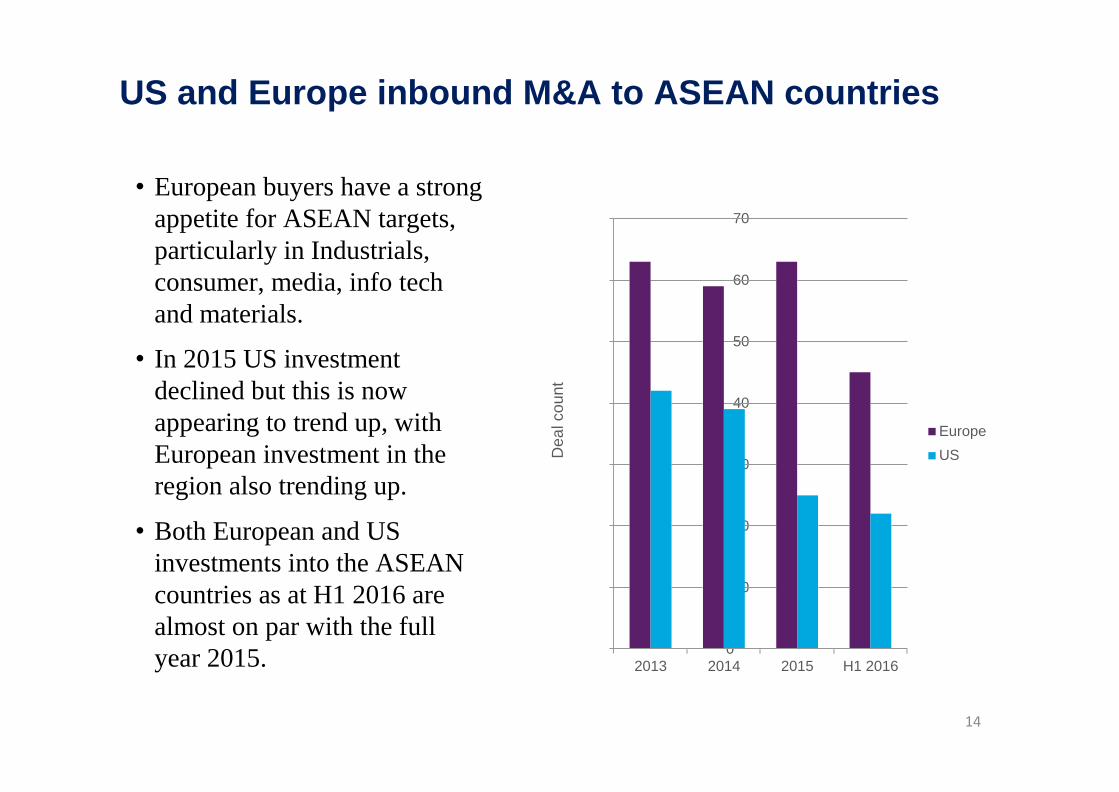

US and Europe inbound M&A to ASEAN countries

• European buyers have a strong

appetite for ASEAN targets,

particularly in Industrials,

consumer, media, info tech

and materials.

• In 2015 US investment

declined but this is now

appearing to trend up, with

European investment in the

region also trending up.

• Both European and US

investments into the ASEAN

countries as at H1 2016 are

almost on par with the full

year 2015.

70

60

50

40

30

20

10

0

2013 2014 2015 H1 2016

Europe

US Dea

l co

un

t

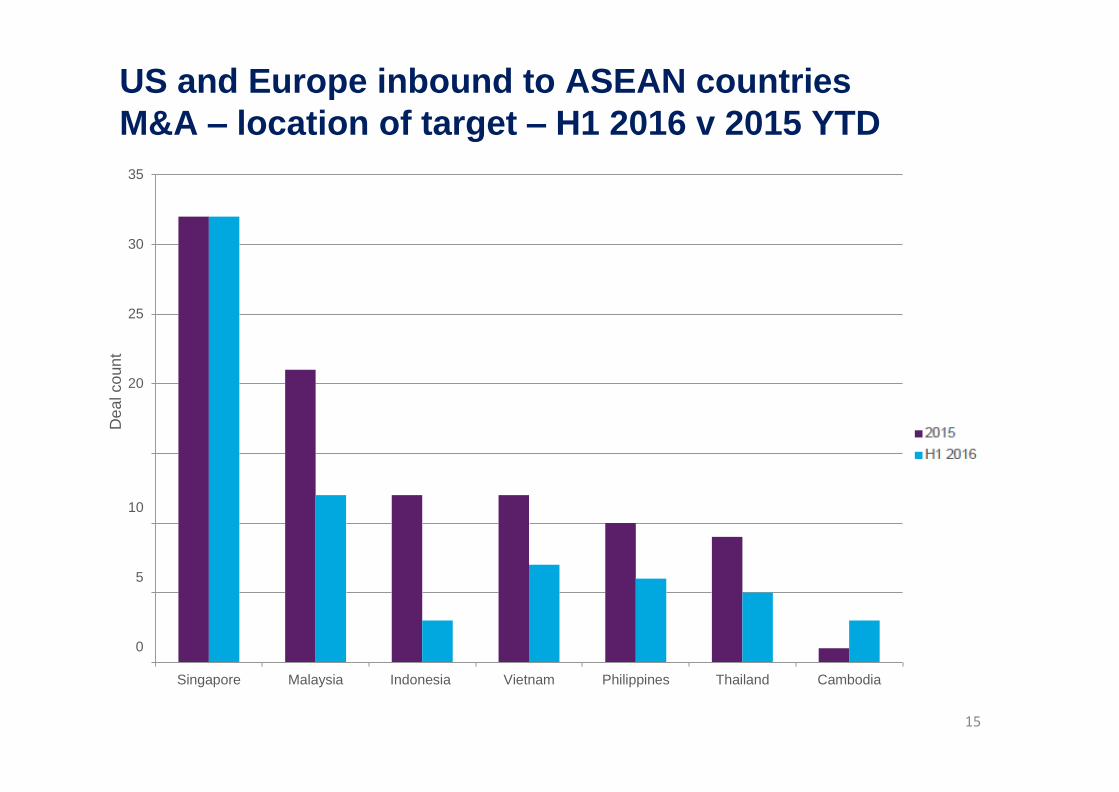

US and Europe inbound to ASEAN countries

M&A – location of target – H1 2016 v 2015 YTD

15

35

30

25

20

2015

H1 2016 15

10

5

0

Singapore Malaysia Indonesia Vietnam Philippines Thailand Cambodia

Dea

l co

un

t

US and Europe inbound to ASEAN countries

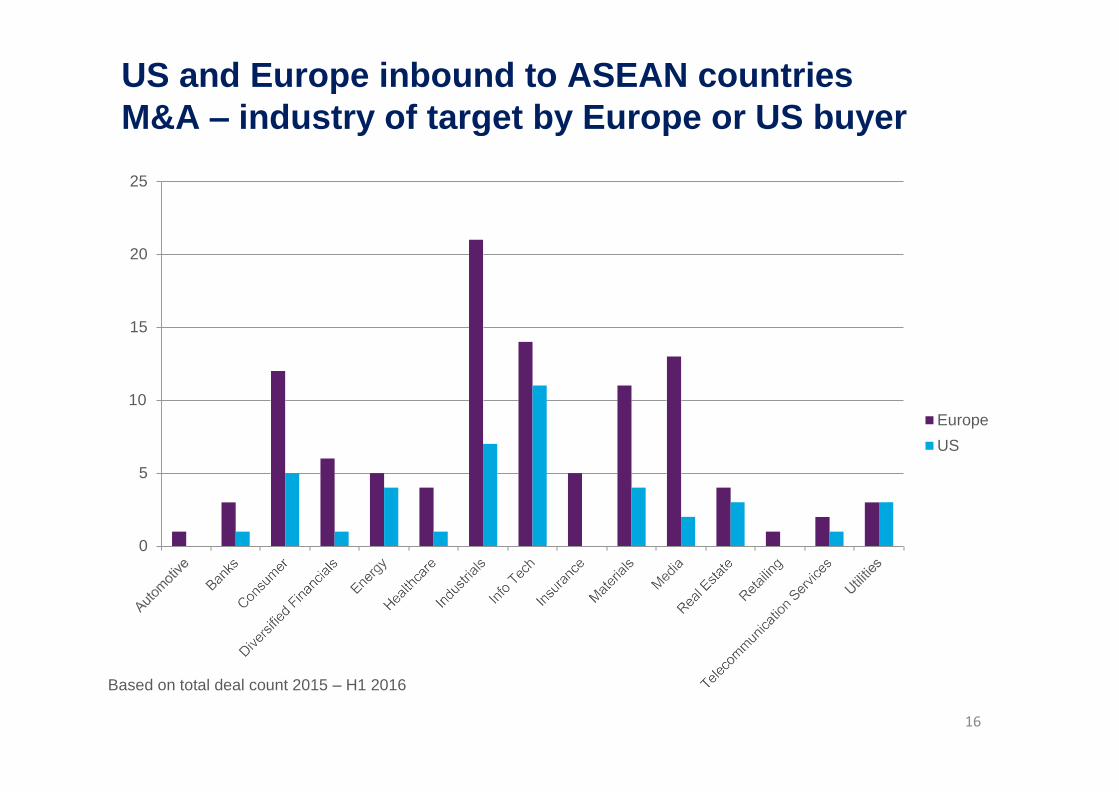

M&A – industry of target by Europe or US buyer

16

25

20

15

10

Europe

US

5

0

Based on total deal count 2015 – H1 2016

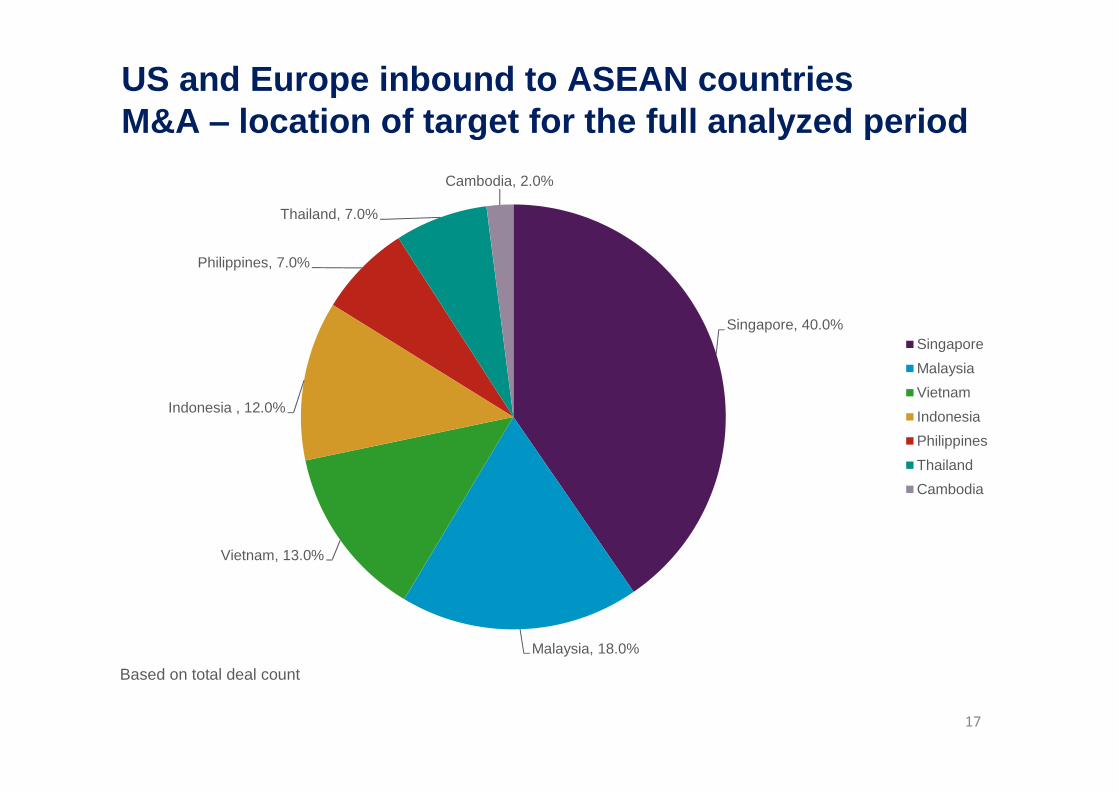

US and Europe inbound to ASEAN countries

M&A – location of target for the full analyzed period

17

Cambodia, 2.0%

Thailand, 7.0%

Philippines, 7.0%

Indonesia , 12.0%

Singapore, 40.0%

Singapore

Malaysia

Vietnam

Indonesia

Philippines

Thailand

Cambodia

Vietnam, 13.0%

Malaysia, 18.0%

Based on total deal count

US and Europe inbound to China

18

Statistics

Challenges

Chinese anti-trust law

Basic Requirements

Case Study: Uber/Didi

Regulatory Approvals

Approvals to Filings

New Foreign Investment Law

US and Europe inbound to China

19

Increased importance of pre-merger notification in the

PRC

Issue of transactions outside the PRC

Issues surrounding bidding projects

Issues surrounding parties in joint control

US and Europe inbound to other Asian countries

20

Recent Trends

U.S. Companies Making Investments in Japan: Some

Observations

Cross-Border Transactions by Companies in Regulated

Industries

Within Asia

22

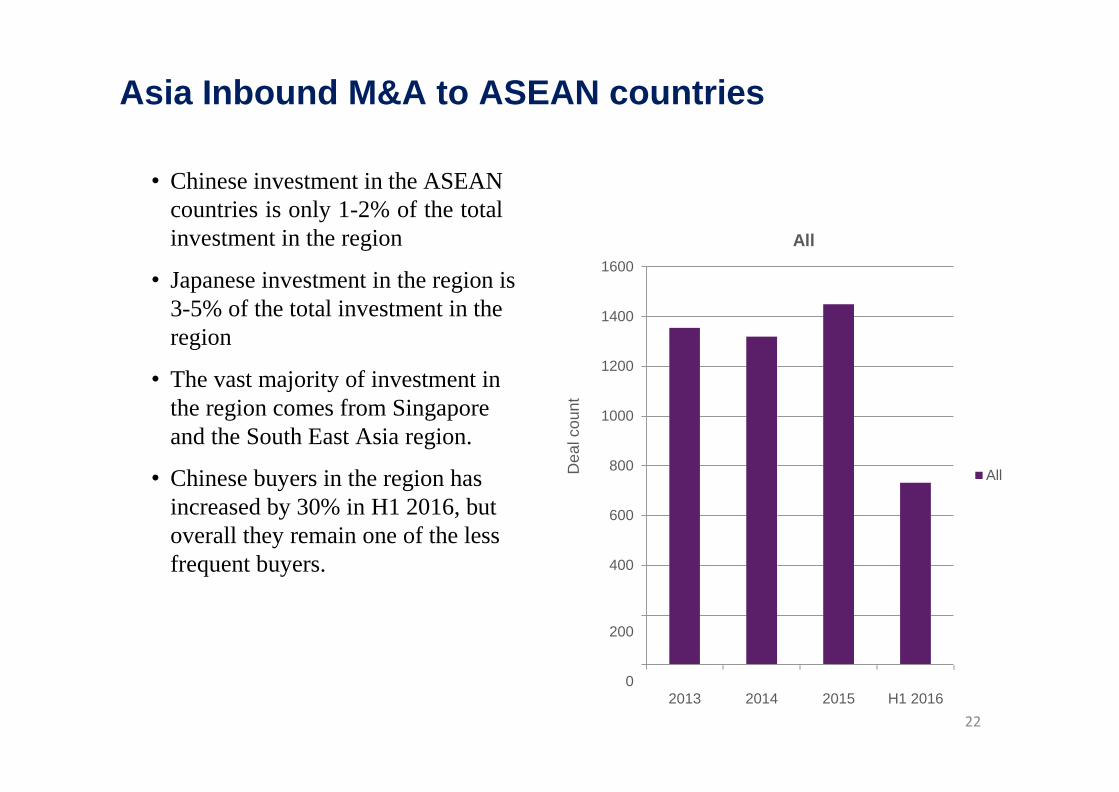

Asia Inbound M&A to ASEAN countries

• Chinese investment in the ASEAN

countries is only 1-2% of the total

investment in the region

• Japanese investment in the region is

3-5% of the total investment in the

region

• The vast majority of investment in

the region comes from Singapore

and the South East Asia region.

• Chinese buyers in the region has

increased by 30% in H1 2016, but

overall they remain one of the less

frequent buyers.

1600

1400

1200

1000

800

600

400

All

All

200

0

2013 2014 2015 H1 2016

Dea

l co

un

t

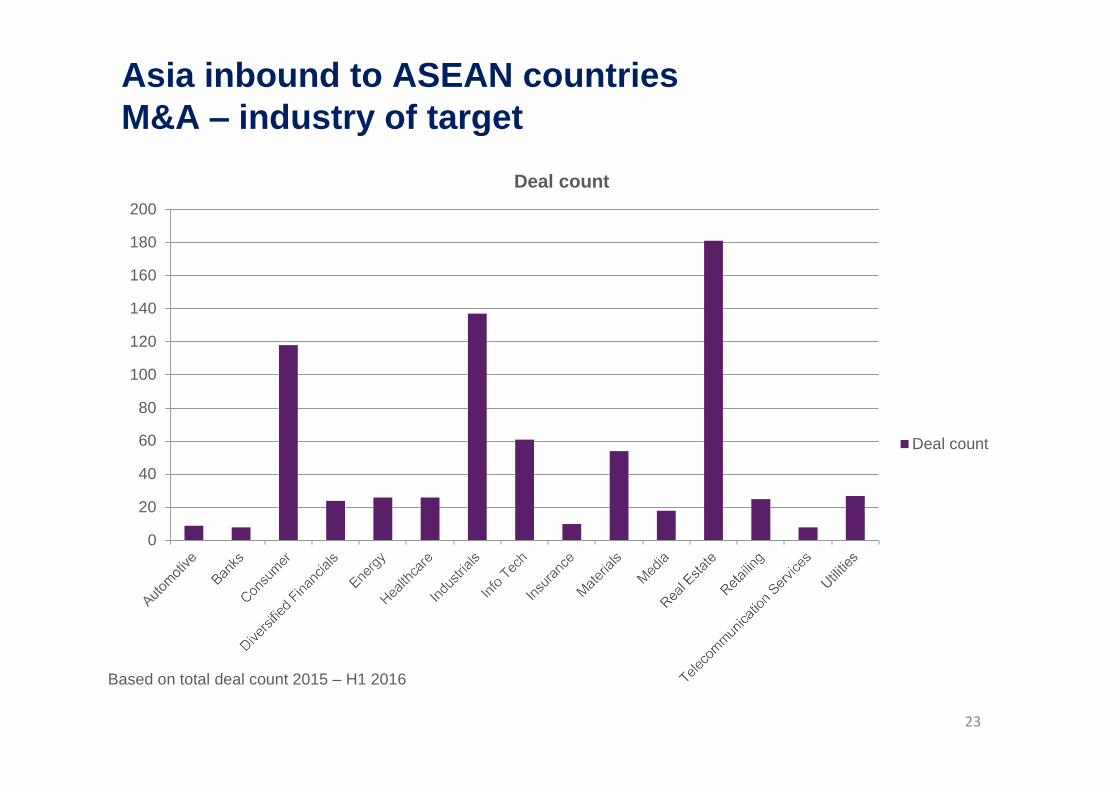

Asia inbound to ASEAN countries

M&A – industry of target

23

Deal count

200

180

160

140

120

100

80

60 Deal count

40

20

0

Based on total deal count 2015 – H1 2016

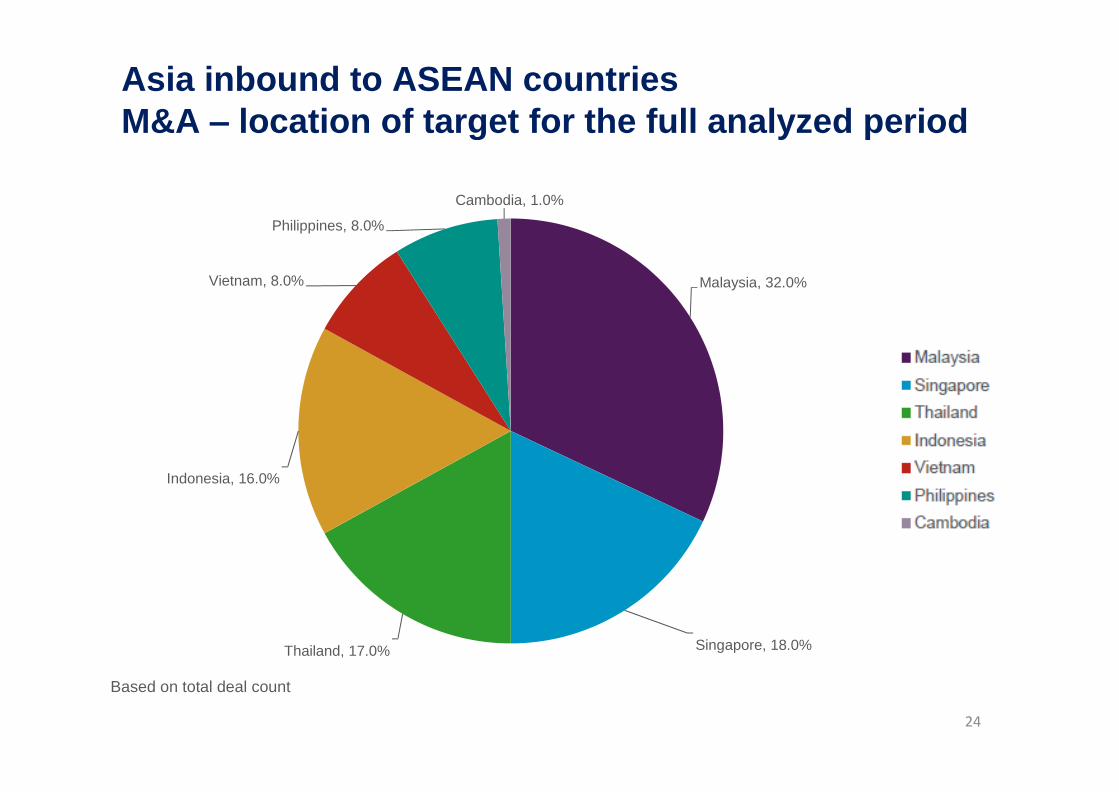

Asia inbound to ASEAN countries

M&A – location of target for the full analyzed period

24

Cambodia, 1.0%

Philippines, 8.0%

Vietnam, 8.0% Malaysia, 32.0%

Indonesia, 16.0%

Malaysia

Singapore

Thailand

Indonesia

Vietnam

Philippines

Cambodia

Thailand, 17.0% Singapore, 18.0%

Based on total deal count

25

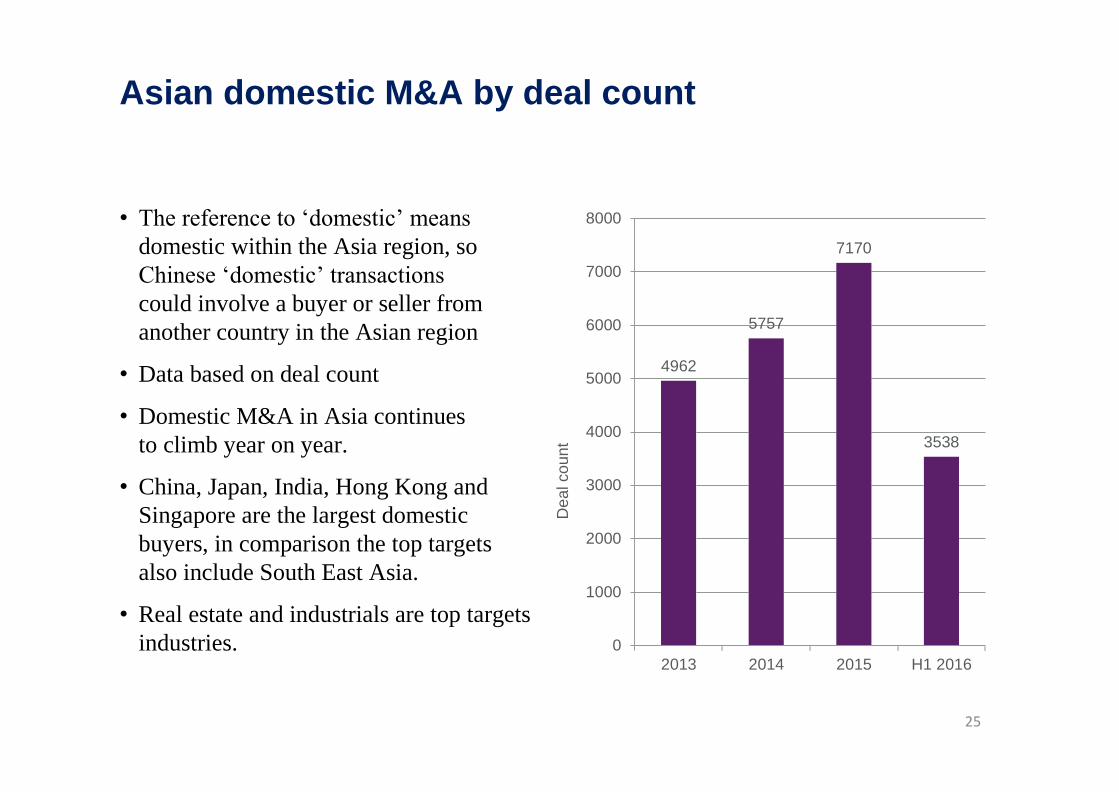

Asian domestic M&A by deal count

• The reference to ‘domestic’ means

domestic within the Asia region, so

Chinese ‘domestic’ transactions

could involve a buyer or seller from

another country in the Asian region

• Data based on deal count

• Domestic M&A in Asia continues

to climb year on year.

• China, Japan, India, Hong Kong and

Singapore are the largest domestic

buyers, in comparison the top targets

also include South East Asia.

• Real estate and industrials are top targets

industries.

8000

7000

6000

5000

4000

3000

2000

1000

0

2013 2014 2015 H1 2016

Dea

l co

un

t

7170

5757

4962

3538

26

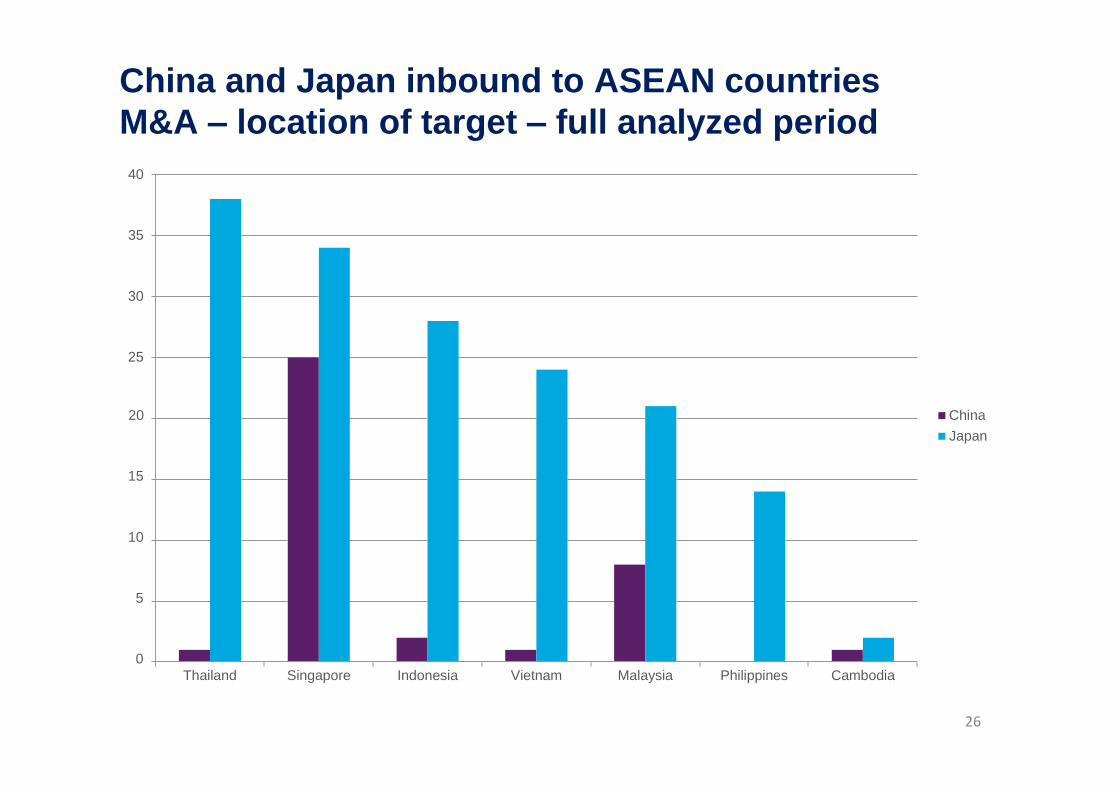

China and Japan inbound to ASEAN countries

M&A – location of target – full analyzed period

40

35

30

25

20 China

Japan

15

10

5

0

Thailand Singapore Indonesia Vietnam Malaysia Philippines Cambodia

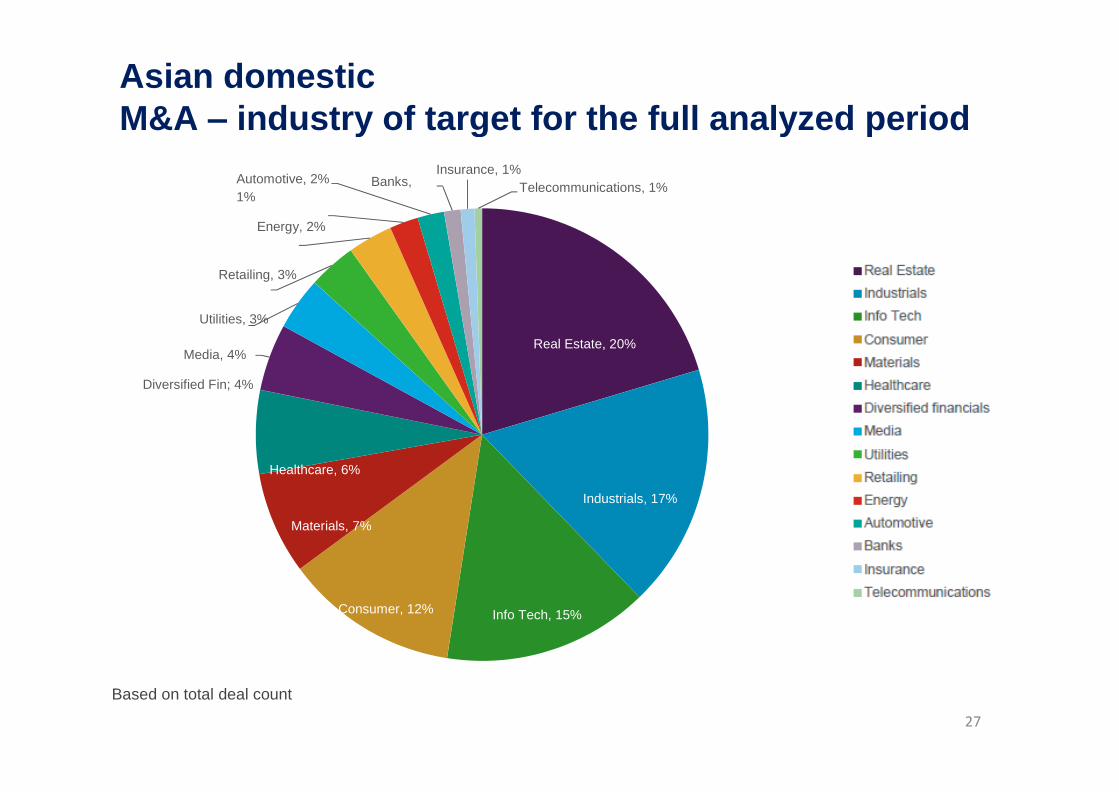

Asian domestic

M&A – industry of target for the full analyzed period

27

Automotive, 2% Banks, 1%

Energy, 2%

Insurance, 1%

Telecommunications, 1%

Retailing, 3%

Utilities, 3%

Media, 4%

Diversified Fin; 4%

Healthcare, 6%

Materials, 7%

Consumer, 12%

Real Estate, 20%

Industrials, 17%

Info Tech, 15%

Real Estate

Industrials Info Tech

Consumer Materials

Healthcare

Diversified financials

Media

Utilities Retailing

Energy Automotive

Banks Insurance

Telecommunications

Based on total deal count

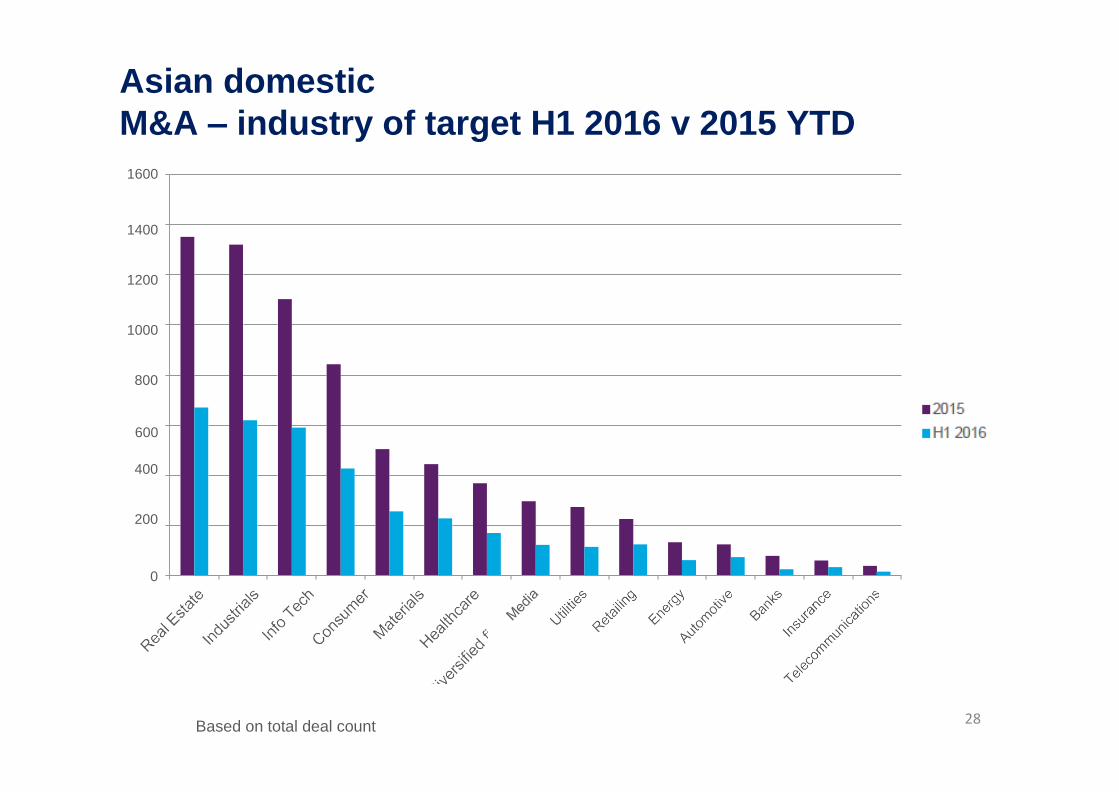

Asian domestic

M&A – industry of target H1 2016 v 2015 YTD

1600

1400

1200

1000

800

600

400

200

0

Based on total deal count 28

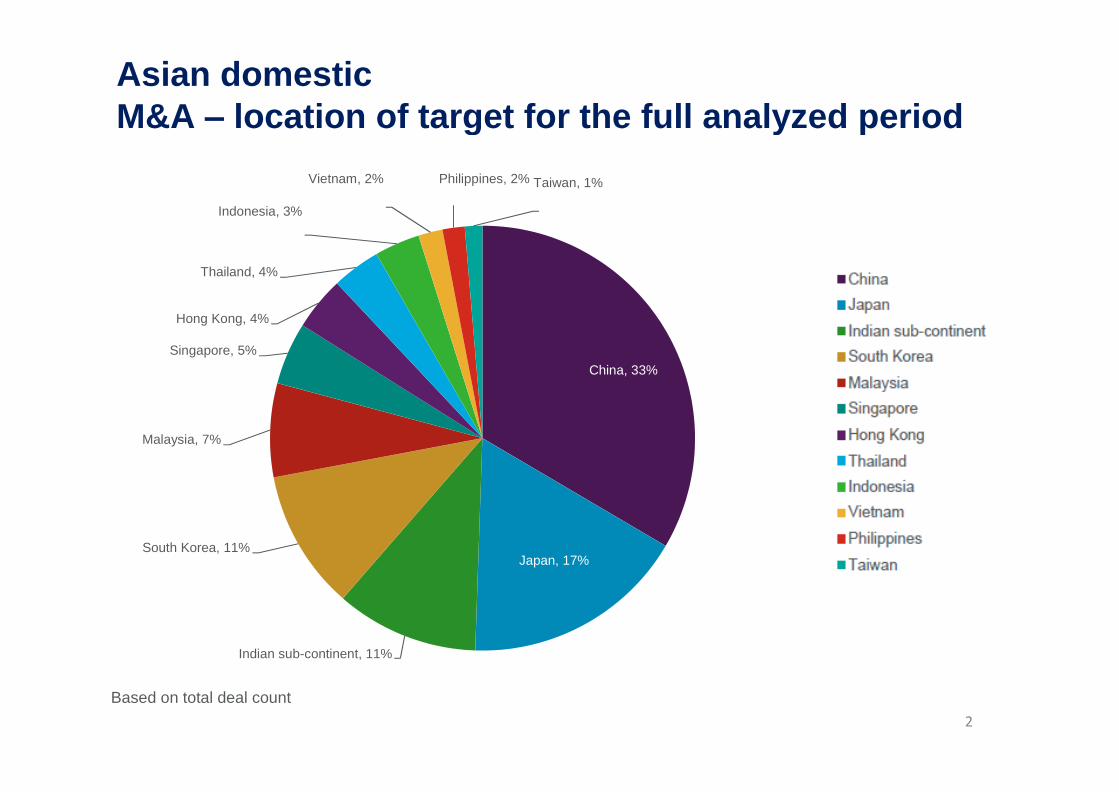

Asian domestic

M&A – location of target for the full analyzed period

2 9

Indonesia, 3%

Vietnam, 2% Philippines, 2% Taiwan, 1%

Thailand, 4%

Hong Kong, 4%

Singapore, 5%

Malaysia, 7%

South Korea, 11%

Japan, 17%

China, 33%

China Japan

Indian sub-continent

South Korea

Malaysia

Singapore Hong

Kong Thailand

Indonesia Vietnam

Philippines Taiwan

Indian sub-continent, 11%

Based on total deal count

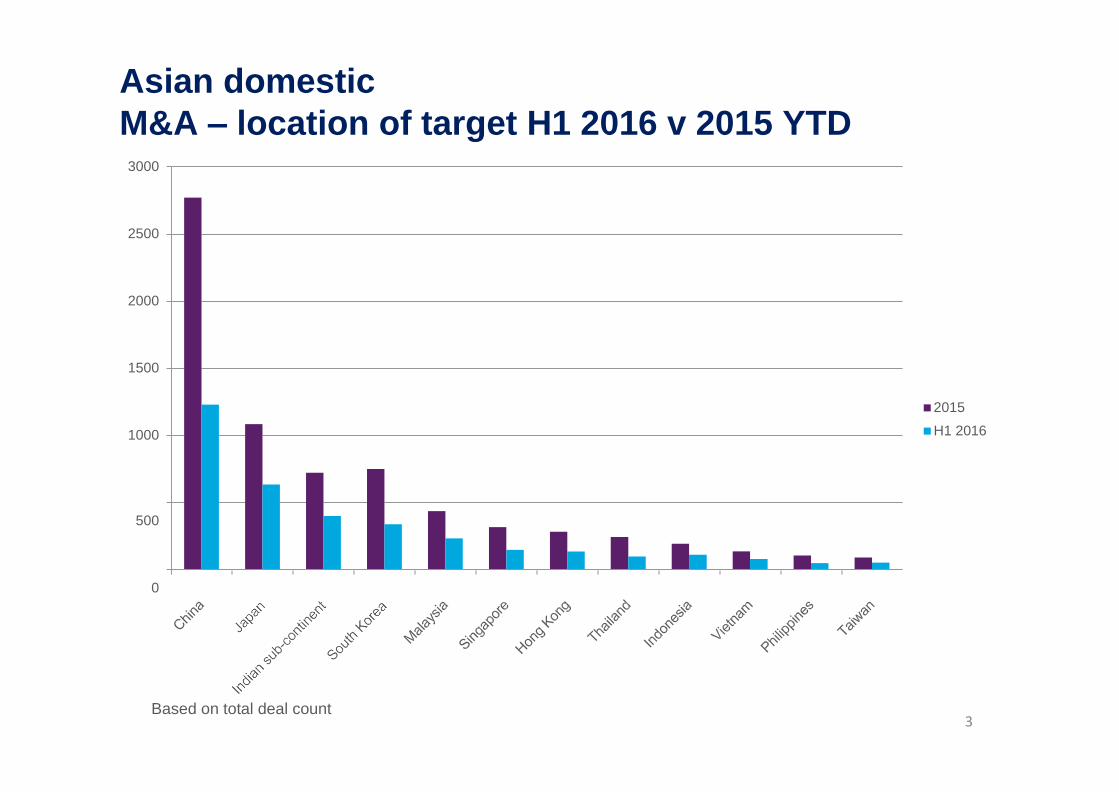

Asian domestic

M&A – location of target H1 2016 v 2015 YTD

3 0

3000

2500

2000

1500

1000

2015

H1 2016

500

0

Based on total deal count

Asian domestic

31

Japanese Anti-Bribery Law

OECD criticism of Japanese Anti-Bribery Law

Movement towards personal jurisdiction

Treatment of facilitation payment

Revision of Guideline to Prevent Bribery of Foreign

Public Officials (2015)

JFBA guideline on anti-bribery (2016)

Matter of group corporate governance (2014)

Asian domestic

32

Investments by Chinese companies in Japanese and

ASEAN countries.

Current Status

More on “One Belt, One Road”

Asian domestic

33

Recent Trends

Japanese Companies Investing in the Asia: Some

Observations

Use of Representation and Warranty Insurance

Importance of Anti-Corruption Due Diligence

Thank you

![The Muscular System - American Bar Associationapps.americanbar.org/abastore/products/books/abstracts/1620521... · The Muscular System No muscle uses its power in pushing[,] ... stiffening](https://static.fdocuments.us/doc/165x107/5b42f5527f8b9a4f5d8b848f/the-muscular-system-american-bar-the-muscular-system-no-muscle-uses-its-power.jpg)