Recent Tax developments in hidden profit distribution - … · Recent tax developments in hidden...

23

25 April 2017 Louis Thomas Frederic Scholtus KPMG Luxembourg Hermann Schomakers Recent tax developments in hidden profit distributions

Transcript of Recent Tax developments in hidden profit distribution - … · Recent tax developments in hidden...

25 April 2017 Louis Thomas

Frederic ScholtusKPMG Luxembourg Hermann Schomakers

Recent tax developmentsin hidden profit distributions

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

Speakers

Louis ThomasPartner, TaxKPMG Luxembourg S.C.T. +352 22 51 51 5527E. [email protected]

Frederic ScholtusAssociate Partner, TaxKPMG Luxembourg S.C.T. +352 22 51 51 5333E. [email protected]

Hermann SchomakersSenior Manager, TaxKPMG Luxembourg S.C.T. +352 22 51 51 5606E. [email protected]

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

AGENDA:1. Income taxation

a. Corporate taxb. Individual tax

2. Recent case law

3. Tax reporting

4. Tax evasion and tax fraud

5. Practical guidance

a.k.a. “distribution cachée de bénéfices” or “verdeckte Gewinnausschüttung”Recent tax developments in hidden profit distributions

Income taxation of hidden profit distributions

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 5

Company(Luxembourg)

Corporate taxation

Shareholder(Luxembourg)

DIVIDENDWithholding taxmax. 15% WHT

To be addedto taxable income

Corporate taxation 20.33% CIT+surcharge

and 6.75%-12.60% MBT

Taxable incomemax. 45.78%

personal income tax• Interest• Rent• Salary• Indemnities• Fees• Royalties• Sales price ...

HIDDEN PROFIT DISTRIBUTION

• Renting out companyassets for free

• Debt assumption withoutcompensation

• Guarantee free of charge• Sale below market rate• …

Decreaseof net equity(Vermögens-minderung)

Averted increaseof net equity(verhinderte

Vermögensmehrung)

Advantage for shareholder

Motivated by shareholding relationship(not at arm’s length)

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 6

Company(Luxembourg)

Corporate taxation

Shareholder

• Family member• Business partner• Indirect shareholder• Ex-shareholder• Founder• Ultimate parent• Sister company• …

HIDDEN PROFIT DISTRIBUTION

Interestedperson

Withholding tax

To be added to taxable income

Taxable income

?05101517.65 %

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 7

Company(Luxembourg)

Individual tax implications – Luxembourg resident

Use of boat for free (which

renting value would be

estimated to EUR 200,000)

Luxembourg resident

Hidden profit

distribution

Dividends 200,000 EUR

Exemption -50%* - 100,000 EUR

Real expenses - 20,000 EUR

Abatement (couples filing jointly) - 3,000 EUR

Net income from investment income =77,000 EUR

Imputation withholding tax (15%) - 30,000 EUR

Tax at 45.78% (2017): 35,250 EUR

+ Dependence contributions (1.4%) + 1,078 EUR

* If Luxembourg company fully taxable

Possible risk of requalification into directors’ fees : Directors’ fees paid by a company in Luxembourg are subject to a 20% withholding tax calculated on the gross amount (or 25% of the deemed net amount)

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 8

Company(Luxembourg)

Individual tax implications – Luxembourg non-resident

Use of boat for free (which

renting value would be

estimated to EUR 200,000)

EU resident (outside Lux)

Hidden profit

distribution

Tax credit method (based on OECD-MC):

The income is taxable both in theState of source and in the State ofresidence.

The tax paid in the State of source iscredited against the tax due in theState of residence on the taxableincome concerned.

The credit is generally limited to theamount of tax due in the State ofresidence on the taxable incomeconcerned

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 9

UBO register - Update• Implementation :

• 4th Anti-Money Laundering Directive (AMLD) was adopted by the European Parliament

• The introduction of the UBO register in every Member State before June 26, 2017

• Definition of Ultimate Beneficial Owner (UBO):

• Basically a UBO is a private individual who, directly or indirectly, has more than 25% control over the legal entity by way of shares, voting rights, profit participating rights, or rights to appoint/dismiss directors

• Also applies to certain trusts

• UBO update in Luxembourg:

• Luxembourg Ministers Council has adopted on 31 March 2017 a legislative proposal on the introduction of a UBO registration

• Next step: sending of the bill to the Chamber of Representatives for further action and approval.

• UBO update for Belgium, Germany, the Netherlands and United Kingdom

Overview of recentcase law

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 11

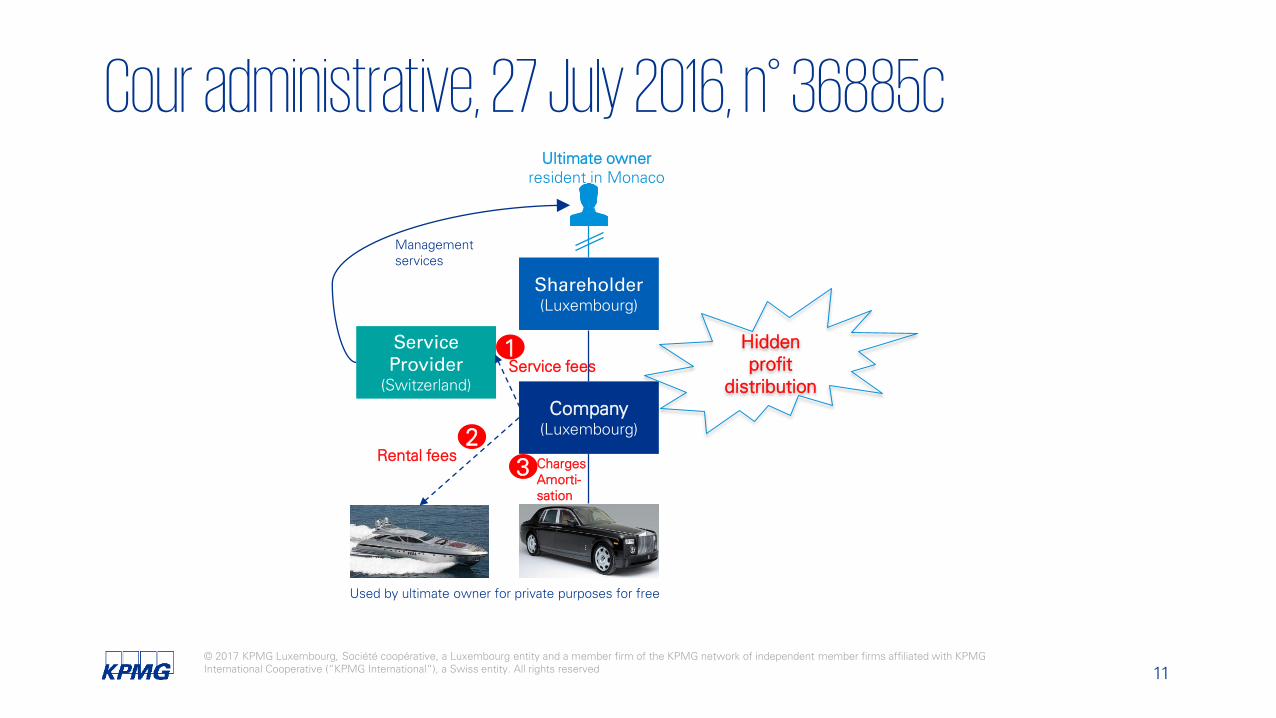

Shareholder(Luxembourg)

Company(Luxembourg)

Ultimate ownerresident in Monaco

ServiceProvider

(Switzerland)

ChargesAmorti-sation

_Rental fees

Service fees

23

1

Cour administrative, 27 July 2016, n° 36885c

Management services

Used by ultimate owner for private purposes for free

Hiddenprofit

distribution

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 12

Cour administrative, 5 July 2016, n° 36888c

Shareholder(Luxembourg)

Grand hotel SpA(Italy)

Company(Luxembourg)

Interest-free loan

5* hotel(Italy)

Hiddenprofit

distribution

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 13

Company(Luxembourg)

Sister(Luxembourg)

Tribunal administratif, 16 Dec 2015, n° 35535 (final)

Suppliers

Trade creditors

Payment of trade creditors

Hiddenprofit

distribution

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 14

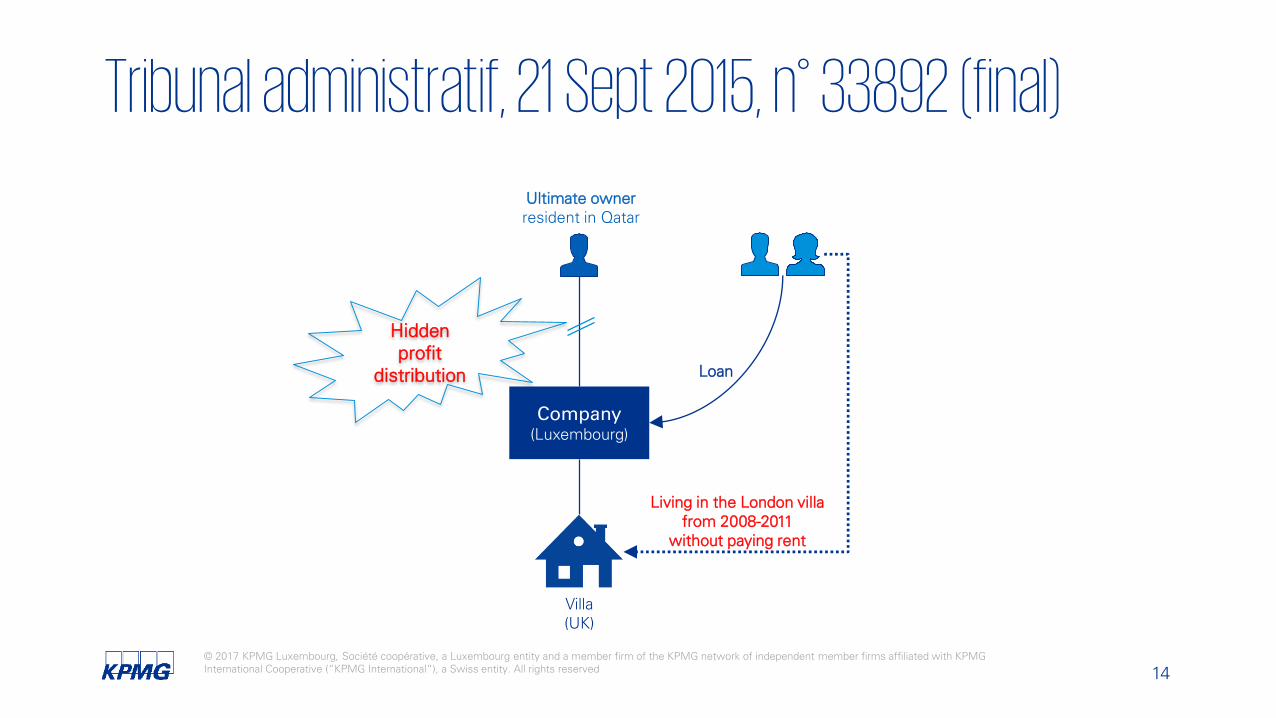

Company(Luxembourg)

Tribunal administratif, 21 Sept 2015, n° 33892 (final)

Loan

Ultimate ownerresident in Qatar

Living in the London villa from 2008-2011

without paying rent

Hiddenprofit

distribution

Villa(UK)

Tax reporting of hidden profit distributions

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 16

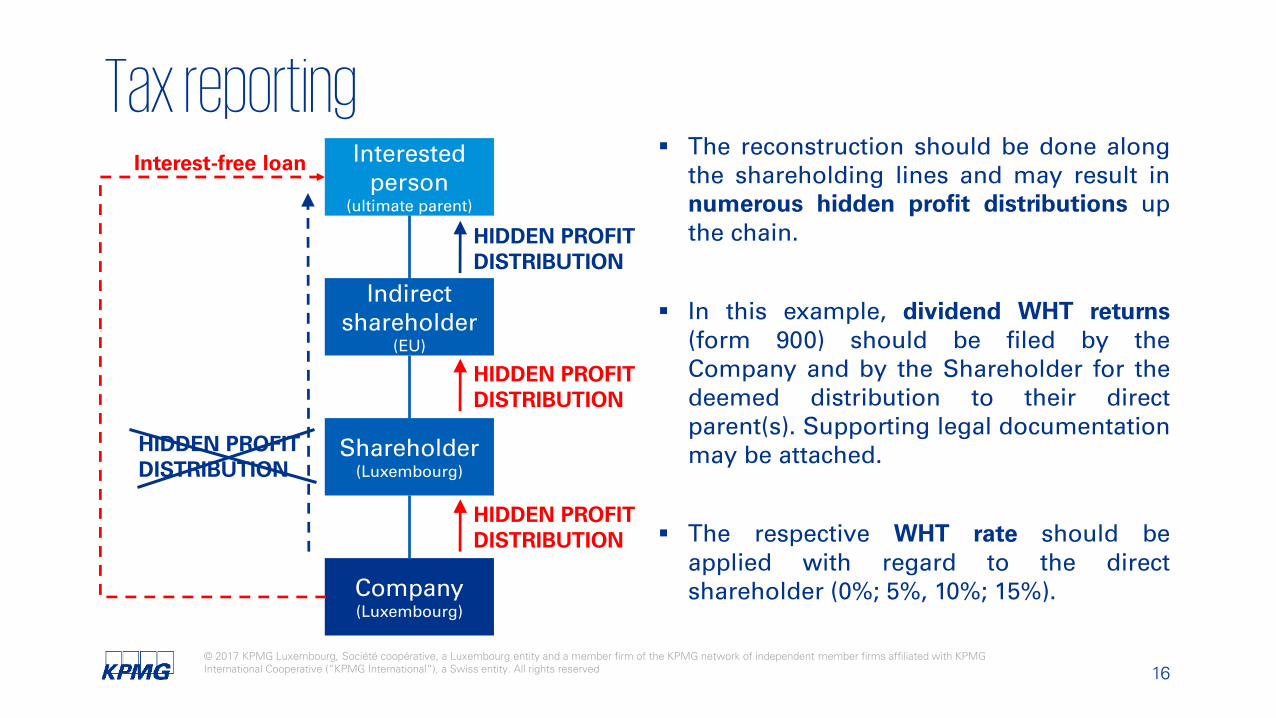

Company(Luxembourg)

Tax reporting

Shareholder(Luxembourg)

HIDDEN PROFIT DISTRIBUTION

Interestedperson

(ultimate parent)

The reconstruction should be done alongthe shareholding lines and may result innumerous hidden profit distributions upthe chain.

In this example, dividend WHT returns(form 900) should be filed by theCompany and by the Shareholder for thedeemed distribution to their directparent(s). Supporting legal documentationmay be attached.

The respective WHT rate should beapplied with regard to the directshareholder (0%; 5%, 10%; 15%).

Indirectshareholder

(EU)

HIDDEN PROFIT DISTRIBUTION

HIDDEN PROFIT DISTRIBUTION

Interest-free loan

HIDDEN PROFIT DISTRIBUTION

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved 17

Company(Luxembourg)

Tax reporting

Shareholder(Luxembourg)

HIDDEN PROFIT DISTRIBUTION

Interestedperson

(ultimate parent)

Interest-free loan ”Fiktionstheorie” abandoned by

Luxembourg jurisprudence (Couradministrative, 27 July 2016, n° 36855C).

Annual accounts should not be modified(e.g. no need to book interest income).

In the corporate tax return of theCompany, a profit adjustment should bedone for the hidden profit distribution asan off-balance sheet correction in lineR0060 of tax form 500.

Indirectshareholder

(EU)

HIDDEN PROFIT DISTRIBUTION

HIDDEN PROFIT DISTRIBUTION

Deemedinterest

Tax evasion andtax fraud: New regimesince 1 January 2017

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

TAX EVASIONFraude fiscale simple

AGGRAVATED TAX EVASIONFraude fiscale aggravée

TAX FRAUDEscroquerie fiscale

obtain undue tax advantage (e.g. unjustified tax credit) cause reduction of tax revenues (e.g. not declaring items of income, deducting fictitious expenses)

for the benefit of another person or for one´s own end by fraud through intentional behavior (act or omission)

Evaded taxes exceed 25% of annual tax/reimbursement and not less than EUR 10,000; or

exceed EUR 200,000

Significant in relative terms compared with annual tax or reimbursement due; or

Signficant in absolute terms

Systematic use of fraudulent acts aimed at (i) concealing relevant facts to the tax authorities or (ii) persuading them of incorrect facts

Administrative offence Criminal act (= primary offence for anti-money-laundering purposes)

Fine between 10% and 50% of evaded taxes

Imprisonment: 1 month – 3 years Penalty: EUR 25,000 to 6 times the

evaded taxes

Imprisonment: 1 month – 5 years Penalty: EUR 25,000 to 10 times the

evaded taxes Forfeiture of certain civil rights

Tax offence Tax crimes

19

Practical guidance

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved

1. Identify all relevant factsand circumstances

2. Analyse potentialconsequences

3. Communicate with client, advisors, stakeholders…

4. Proactive or reactive strategy?

Hiddenprofit

distribution

BEFOREPrecaution

AFTERAction

1. Identify persons who have a close relationship with shareholders

2. Document legal arrangements with interested persons and shareholders (also from a transfer pricing perspective)

Practical guidance

21

Thank you

Document Classification: KPMG Confidential

The KPMG name, logo and “cutting through complexity” are registered trademarks or trademarks of KPMG International.

The information contained herein is of a general nature and is not intended to address the circumstances of any particular individual or entity. Although we endeavor to provide accurate and timely information, there can be no guarantee that such information is accurate as of the date it is received or that it will continue to be accurate in the future. No one should act on such information without appropriate professional advice after a thorough examination of the particular situation.

kpmg.lu kpmg.lu/app

© 2017 KPMG Luxembourg, Société coopérative, a Luxembourg entity and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. All rights reserved.

![Wide Format Printers: A Hidden Profit Pool [Global Channel Partners Summit]](https://static.fdocuments.us/doc/165x107/5554ce69b4c9051b6e8b4805/wide-format-printers-a-hidden-profit-pool-global-channel-partners-summit.jpg)