Recent International Tax Developments in the Middle East · Recent International Tax Developments...

29

Recent International Tax Developments in the Middle East 18 th International Tax Conference - Dec 6-8, 2012, Mumbai Thomas Hanzély www.bbd-e.com

-

Upload

hoangkhanh -

Category

Documents

-

view

216 -

download

0

Transcript of Recent International Tax Developments in the Middle East · Recent International Tax Developments...

Recent International TaxDevelopments in the Middle East

18th International Tax Conference - Dec 6-8, 2012, Mumbai

Thomas Hanzély

www.bbd-e.com

Introduction

Taxes in the Middle East - an overview

Presentation will focus on the GCC (inparticular Bahrain, Qatar and the UAE)

Will taxes remain low in the Middle East andwhat impact could the recent political turmoilin the region have on tax policies?

The role of the GCC - will we see a politicaland economic union?

www.bbd-e.com

Overview of Taxes

Corporate Income Tax

VAT - the next tax to come in the GCC? Anyharmonization of indirect taxes foreseeable inthe GCC in the near future?

Personal Income Tax

Withholding Tax regimes applied by most ofthe MENA countries

www.bbd-e.com

Tax rate changes

55 :A

45%

20%

I Old

I New

Saudi Kuwait Oman Qatar Egypt

Arabia

Iraq Libya

Source: Ernst & Young, Tax Treaties - Recent Applications in the Middle East, 2010

www.bbd-e.com

Treaty NetworkBBD ENTERPRISES

Rapidly growing Double Tax Treaty network- Availability of treaty benefits

- Dispute resolution not tested in many jurisdictions

- Aggressive approach in various matters (e.g.Permanent Establishments, Withholding Taxes)

- Non-Discrimination article

- Subject-to-Tax provisions

UN Model vs OECD Model

www.bbd-e.com

Ease of Doing Business

The international view of the investment climate in theGCC:- Ease of Doing Business report (World Bank, 2012) places Saudi

Arabia overall 12th, the UAE 33rd, Qatar 36th, Bahrain 38th- Index of Economic Freedom (Heritage Foundation in

cooperation with the WSJ 2012) places Bahrain 12th, Qatar25th, UAE 35th

Communication with authorities- Interpretation of tax rules- Language

Bankruptcy laws / credit rating systemStill a safe haven for business?

www.bbd-e.com

Economic Substance in the GCC

ES is an emerging trend

ES can be implemented in the region - i.e.place of effective management and controlcan be in GCC countries

There are plenty of non-tax reason toestablish a company in the GCC

www.bbd-e.com

COUNTRY PROFILES

www.bbd-e.com

BAHRAIN

www.bbd-e.com

Bahrain - Tax Profile

Only GCC country without any (statutory) tax- No corporate income tax (CIT), no capital gains tax

(CGT), no withholding tax (WHT), no personal incometax (PIT) and no VAT

- Except a 46% corporate income tax levied on oil andgas companies

Treaty network (28 in force, 6 pending)- a.o. Austria, China, France, Ireland, Luxembourg,

Netherlands, Singapore

- Pending treaties with Belgium, South Korea, UK

www.bbd-e.com

Bahrain - at a Glance IBBD ENTERPRISES

Historical financial and trading hub in the ME

Not considered a tax haven

100% foreign ownership allowed

Business friendly environment

Good infrastructure

Reasonable Costs

Political situation?

www.bbd-e.com

Bahrain - at a Glance IIBBD ENTERPRISES

Free Trade Agreement with the U.S. (2006)Bahrain International Investment Park (BMP)

0% Corporate Tax with a 10 year guarantee- Duty free access to the markets of the Gulf Cooperation Council

(Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the UnitedArab Emirates)

- 100% Foreign Ownership- Availability of serviced industrial land at extremely competitive

rates- Renewable 50 year leases- No recruitment restrictions for the first 5 years

Dedicated assistance of a professional management team

www.bbd-e.com

QATAR

www.bbd-e.com

Qatar - Tax Profile

New Tax Code effective since 1 January 2011

CIT and CGT 10% (flat rate); petroleumcompanies are taxed at not less than 35% oras determined in the production sharingagreement (PSA)

No PIT

No VAT

www.bbd-e.com

Qatar - at a Glance

One of the fastest growing economies worldwide

In general, restricted foreign ownership (49/51)

100% foreign ownership only in exceptional cases

Qatar Financial Centre (QFC) - separate/parallelfrom Qatari legal system based on common lawprinciples

Qatarization lawsCosts

Treaty Network (42 in force, 11 pending)

www.bbd-e.com

The Qatar Financial Center (QFC)

Established in 2005Onshore center for banks, insurance andinvestment sectors together with supportingfirms100% foreign ownership allowedNoWHTEncourages also the incorporation of SPVs andHolding CompaniesAccess to Double Tax TreatiesMeeting all OECD standards

www.bbd-e.com

BBD ENTERPRISES

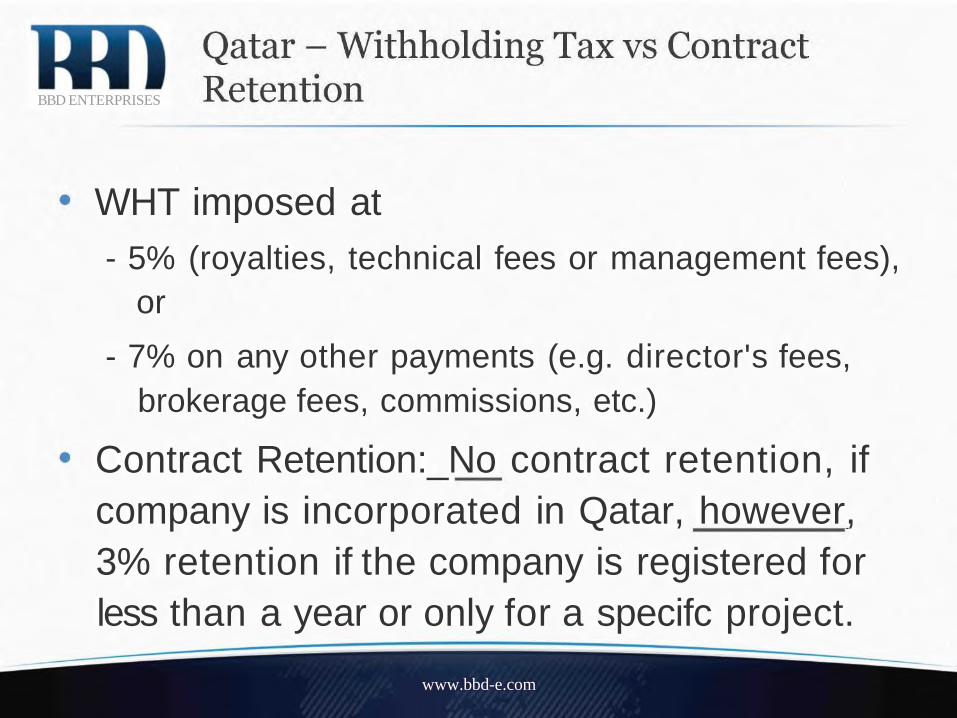

WHT imposed at- 5% (royalties, technical fees or management fees),

or

- 7% on any other payments (e.g. director's fees,brokerage fees, commissions, etc.)

Contract Retention:_No contract retention, ifcompany is incorporated in Qatar, however,3% retention if the company is registered forless than a year or only for a specifc project.

www.bbd-e.com

BBD ENTERPRISES

UNITED ARAB EMIRATES

www.bbd-e.com

UAE - Tax ProfileBBD ENTERPRISES

Statutory CIT exists, but not enforced, currently0% CIT

Petroleum companies taxed at rates between50-55% or based on individual agreementsBranches of foreign banks are also taxed

No PIT, no CGT, no VAT

Treaty Network (45 treaties in force, 12 pending)- Many OECD countries, India, China, Singapore,

Mauritius

www.bbd-e.com

UAE - Free Zones

Free Zones- 100% foreign ownership only in free zones - new

company laws on the agenda

- guaranteed tax holiday

- no restrictions on hiring foreign professionals

- State of the art infrastructure

- Professional local authorities / procedures put inplace

More than 30 Free Zones in the Emirates

www.bbd-e.com

UAE - Free Zones & Economic SubstanceBBD ENTERPRISES

Dubai International Financial Center (DIFC) JebelAli Free Zone (JAFZA) most well known- Most Free Zones allow for the implementation of

economic substance

Anti-avoidance provisions in tax treaties- limitation of benefits

- subject-to-tax / liable-to-tax (unclear whether UAEresidents are liable to tax in the context of the treaty)

- Conclusion: bonafide business at least required inorder to benefit from tax treaties

www.bbd-e.com

UAE - Recent DevelopmentsBBD ENTERPRISES

Ras Al-Khaimah (RAK) - new offshorejurisdiction- Is the UAE (still) promoting offshore structures?

Since 1 January 2011 offshore companies maynot acquire real estate in the UAE anymore- A result of the fight against money laundering and

a move towards greater transparency

- Only entities registered with the Jebel AN FreeZone are eligible to register real estate

www.bbd-e.com

GENERAL ISSUES

www.bbd-e.com

General Legal Issues I

"Anti-Fronting Laws" - what to do?- How are minority shareholders protected under

local laws?

- How can additional protection be incorporated?

Bilateral Investment Treaties (BIT)

"Revival" of the Organisation of IslamicCooperation (OIC) Investment Treaty

www.bbd-e.com

General Legal Issues II

Legal Systems / Dispute Resolution- civil law (based on Egyptian law)

- common law (e.g. DIFC and other free zones)

- Shariah law (GCC countries have a dual system)

- Arbitration

- Enforceability of DIFC court judgments in the UAE(ie, outside the DIFC) and the GCC

Laws in the GCC are very protective of localnationals and local economic interests

www.bbd-e.com

Greater Arab Free Trade Agreement(GAFTA)

Pan-Arab free trade greement (1997)14 signatory statesFull liberalization of goods with full exemption ofcustoms duties and chargesKey benefits: reduction of usual 15/20% importduty imposed by many MENA countriesTo benefit from the GAFTA, the importedproducts must be enhanced in one of thesignatory states - the UAE is often used as agateway to other GAFTA countries, since it haslow import duties (5%)

www.bbd-e.com

Indian Double Tax Treaties with GCCBBD ENTERPRISES

Kuwait (in force, 2007)

Oman (1997)

Qatar(2000)

Saudi Arabia (2006)

UAE (1997, amended in 2007)

www.bbd-e.com

CONCLUSION

www.bbd-e.com

THANK YOUADDRESSBBD Enterprises WLLLevel 22, West TowerBahrain Financial HarbourKing Faisal HighwayManama, Kingdom of Bahrain

PHONE+973 17502909 (Office)

Sunday to Thursday, 8:30AM to 5:30PMStandard time zone: UTC/GMT +3 hours

+973 17502910

www.bbd-e.com