Recent developments of Estonia’s social protection...

53

Recent developments of Estonia’s social protection system Avo Trumm Department of Sociology and Social Policy University of Tartu

Transcript of Recent developments of Estonia’s social protection...

Recent developments of Estonia’s social protection system

Avo Trumm Department of Sociology and Social Policy University of Tartu

2

Introduction This paper is a part of the project „EU-8 Social Policy Reviews” initiated and financed by the World Bank and coordinated by the Maastricht Graduate School of Governance. The project aims at describing and explaining the changes in national social policies of the eight new post-socialist member countries of the European Union, occurred in the conditions of unprecedented social transformations. The review is focused on three main issues: 1) presenting an overview of aggregate trends in social protection expenditures including social insurance and assistance as well as labour market policies, 2) revealing main reform directions in social protection areas, and 3) analysing welfare outcomes, including labour market incentives and participation, welfare dependency and poverty effects, and dimensions of social exclusion, and the linkages with social policy choices and economic reforms. The paper is organised around the set of analytical tables including the main input, output and outcome variables of social protection systems elaborated by the co-ordinating team. The data applied in the report are mainly obtained form the European System of Integrated Social Protection Statistics (ESSPROS), which have been methodologically harmonised in accordance to Eurostat standards. In addition, the data from the Statistical Office of Estonia, Social Insurance Board of Estonia and the Ministry of Social Affairs of Estonia are used. While preparing the paper the author has held consultations with the specialists from the Ministry of Social Affairs, Statistical Office of Estonia, Social Insurance Board of Estonia, and PRAXIS Centre for Policy Studies. In particular, advice and comments of Lauri Leppik, Andres Võrk, Ivo Ratas, Ülla Mäe, Katrin Pedastsaar, Jüri Kõre and Anne Karu have been considerable.

Background information The social protection system of Estonia has gone through rapid changes, due to new emerging social problems, ideological and political changes and economic constraints. The transition societies have taken historically unknown developmental tracks towards the ‘mainstream’ of the European Union without adequate socio-political means that could be applied for solving problems in this unique situation. The current welfare mix of Estonia is a result of several interrelated changes, occurred in policy environment, economic structures, living and social conditions of population, demographic pressures as well as in general mindset of people.

Policy environment Policy environment in Estonia has impacts from several sources: legacy of the past, prevailing right-wing governance, lessons learned from the Nordic welfare traditions, political guidelines from the European Union, as well as advice and guidelines of supranational agencies. The legacy of the ‘state-socialist welfare traditions’ has let a remarkable imprint on the current social policy system. The social protection system under the socialist regime was funded mainly by contributions from employers to the state budget. There was a

3

comprehensive social protection based on full employment, and additional targeted services at the enterprise level. The former state-socialist systems provided old-age pensions, relatively generous child support, subsidised housing and basic goods. There was a limited emphasis on cash transfers and a greater emphasis on services such as health and education. Some elements form the previous system (e.g. prevalence on employers’ contributions in social policy funding, relatively developed system of child and family benefits) are characteristic for the Estonia’s social protection system as well. Prevailing right-wing governance and strong belief into free-market economic policy is a factor, which can be useful for explaining and justifying of current principles of Estonian social policy. The establishment of “free-market economy” has been a strong (and only) priority of the ruling right-wing government coalition pushing social policy issues aside. Siim Kallas, the Prime Minister of Estonia, said in 1996: “Economic policy gives the parameters, and other policy fields must adapt themselves to these. At first, a certain level of economic potential must be created in order to solve social problems, thus we cannot hurry to distribute possible benefits. Instead, investments are today’s main priority”. Therefore, the understanding that the obligation of the state is to ensure equal opportunities for everybody to develop their individual capacities and at the same time realisation of those opportunities provided by the state is a responsibility of individuals by themselves. Proportional tax-system, removal of subsidies, and considerable decline of universal schemes and introduction of means-tested ones are the main outcomes of the implementation of a new-liberal ideology as a result. Lessons learned from the Nordic welfare traditions are evident in the several legislative acts regulating the field of social policy. In the Estonian case, the social protection system combines the elements of liberal and social-democratic welfare regimes from the very beginning. The legislative framework of social policy includes concepts taken from the Nordic welfare model (equal rights, universalism, central role of the state, etc). The Social Welfare Act (1995) including copies of paragraphs from welfare laws of Denmark, Sweden and Finland demonstrates the influence of Nordic welfare model. Learning from Nordic welfare traditions can be revealed also in the case of Social Benefits for Disabled Persons Act (2001). However, on could see the impact of Nordic welfare model only in legislative acts, not in certain regulations or policy outcomes. EU policy guidelines (European Social Model, OMC, etc) form a set of principles designing the today’s Estonian social policy system the most. As said by the Minister of Foreign Affairs in 1998: “The social dimension is of increasing importance for Estonia. We are intensifying our efforts in areas such as employment, work conditions and vocational training in order to ensure equal opportunities for all members of society. Acceding to the amended European Social Charter is a priority for Estonia and preparations aimed at meeting this goal are currently being made”. The questions of social development have received more attention in the process of EU accession and the EU Employment Strategy and the Joint Inclusion Memorandum form a strong frame for Estonia’s social policy developments today. As an additional factor, re-shaping the policy environment for social policy in Estonia as well as in other countries of Central and Eastern Europe, an impact of supranational agencies (like International Monetary Fund, World Bank, etc) can be mentioned. The influence of these agencies on pension systems and targeted social assistance schemes has been widely discussed in social policy literature (see e.g. Deacon 1995, Ferge 1997, Kapstein & Milanovic 2001).

4

Macro-economic environment In the economic development of Estonia three clearly distinguished stages can be revealed: 1) collapse of the socialist economic system in late eighties resulting in tremendous economic decline at the beginning of nineties (approximately the years 1989-1993, 2) recovery from the economic recession and stabilisation of the situation (1994-1996), followed by 3) intensive economic growth (since 1997, except the years of so called ‘Russian crisis’ in 1998-1999) when the average annual GDP growth has been over 6% (table 1).

Table 1. Economic performance of Estonia in 1996-2005 Real GDP growth rate

(percentage change on previous year) Year GDP per capita

(PPS, EU-25=100) Estonia EU-25

1996 34.7 4.4 1.7 1997 38.1 11.1 2.7 1998 39.1 4.4 3.0 1999 38.8 0.3 3.0 2000 41.0 7.9 3.9 2001 42.2 6.5 1.9 2002 45.0 7.2 1.2 2003 48.2 6.7 1.2 2004 51.2 7.8 2.4 2005 55.8 9.8 1.6

Source: Eurostat database Economic performance of the country in the large extent determines the opportunities and constraints of the social protection – as in terms of supply as well as demand. The period of 1990-1996 reflects the situation of limited resources and high demand because of economic decline and rapidly expanded unemployment and poverty. As a reaction to the emerged situation, a system of means-tested subsistence benefits and unemployment benefits were launched, in order to provide relief to unemployment, poverty and social exclusion; because of the budget breakdown, the pensions introduced in 1991 were replaced by living allowances for elderly in 1992. The living conditions survey (1994) revealed that 60% of the households had spent more than half of their resources on food, at the same time, nearly one in three Estonians reported frequent problems buying essential food products and medicines. The disproportion between needs and resources started to diminish, allowing more flexibility and sustainability to the system at the end of nineties. The developments in the economic sphere are reflected in changes of the labour market situation. During five years, the severe economic breakdown reduced the employment rate from about 80% in 1989 to 65% in 1994. After the stabilisation of economy in mid-nineties, the decrease in employability slowed down and in 2000 at the first time since restoration of independence the number of employed increased. The similar pattern can be revealed in the case of unemployment – the permanent increase of unemployment rate peaked in 2000 at the level of 13.7%, during last five years the unemployment rate has decreased by 5% reaching the level of 8% by the year 2005 (table 2). However, the data on unemployment indicate that although the unemployment rate has been falling during the last years, the long-term unemployment has stabilised on a very high level (table 3). Venesaar et al. (2004: 142), by concluding the results of the study on long-term unemployment in Estonia, point out that in 2002 there were 35,500 long-term unemployed and 17,770 inactive working-age persons in Estonia who had stopped looking for a job (were discouraged), accounting for 5.1 per cent of the working-age population.

5

Table 2. Selected employment indicators of Estonia for the population aged 15–69 years in 1994–2005 Year Labour force participation

rate, % Employment rate, % Unemployment rate, %

Males Females Total Males Females Total Males Females Total 1994 77.8 63.0 70.0 72.1 58.0 64.6 7.3 7.9 7.6 1996 74.8 61.9 68.0 66.8 56.2 61.2 10.6 9.2 9.9 1998 73.7 61.6 67.3 65.7 56.1 60.6 10.8 8.9 9.9 1999 72.6 60.8 66.4 62.8 54.2 58.2 13.5 10.9 12.3 2000 72.9 61.3 66.8 62.3 53.5 57.6 14.6 12.7 13.7 2001 72.2 61.4 66.5 62.8 53.8 58.1 13.0 12.3 12.7 2002 71.3 60.6 65.7 63.5 54.7 58.8 10.9 9.8 10.4 2003 71.7 61.7 66.4 64.3 55.5 59.7 10.3 9.9 10.1 2004 70.9 62.0 66.2 63.4 56.5 59.7 10.5 8.9 9.7 2005 70.0 62.8 66.2 63.9 58.3 60.9 8.8 7.1 8.0

Source: Estonian Labour Force Survey data (Statistical Office of Estonia)

Table 3. Unemployed persons by duration of unemployment in Estonia in 1994–2005 Less than 6 months 6–11 months 12 months or more Total Year Thousands % Thousands % Thousands % Thousands %

1994 21.5 38.8 11.9 21.5 22.0 39.7 55.5 100.0 1995 27.4 40.3 19.1 28.0 21.6 31.7 68.1 100.0 1996 20.2 29.5 10.4 15.1 37.8 55.3 68.4 100.0 1997 21.7 33.0 14.0 21.2 30.1 45.8 65.8 100.0 1998 22.9 34.7 12.1 18.3 31.1 47.1 66.1 100.0 1999 27.6 34.3 16.0 19.8 36.9 45.9 80.5 100.0 2000 35.7 39.7 13.4 14.9 40.8 45.4 89.9 100.0 2001 29.9 36.1 13.0 15.6 40.1 48.3 83.1 100.0 2002 21.3 31.7 10.4 15.4 35.5 52.9 67.2 100.0 2003 25.6 38.7 10.2 15.4 30.4 45.9 66.2 100.0 2004 21.2 33.3 9.2 14.5 33.2 52.2 63.6 100.0 2005 18.6 35.6 5.7 10.9 27.9 53.5 52.2 100.0

Source: Estonian Labour Force Survey data (Statistical Office of Estonia) Developments on the labour market have had considerable impact on social policy developments. Ever since 1997, Estonia has pursued an active labour market policy. It was considered that benefit and training systems should ensure that they actively support employability, and provide clear incentives for the unemployed to seek and take up work or training opportunities. In order to support the entrepreneurship culture, an entrepreneurship subsidy – a measure to start one’s own business – was introduced in 1998. The ongoing reforms are mostly related to labour quality and supply improvement in order to reduce corporate costs on training and retraining and sustain a free labour market. The number of unemployed entitled to active employment measures has increased from 11,400 unemployed persons to 19,300 in 2001. The relative proportion of job seekers, participating in active measures was 10.7 per cent and 14.1 per cent respectively (Joint Inclusion Report of Estonia: 59). Full implementation of the unemployment insurance scheme from January 2003, which has increased the expenditure on the social protection of the unemployed to approximately 0.7 per cent of GDP, was a principal change in the social protection of the unemployed.

Demographic development The demographic development of Estonia can be described by decreasing and aging population; The population of Estonia has been steadily decreasing from 1991 because of

6

both components of the population change – natural increase and net migration have been negative (Leppik & Kruuda 2003: 8). The absolute number of population in 1991 – 1,566 million – has declined to 1,351 million residents in 2005, which makes about 1% of absolute population decline per year. The population of Estonia is ageing. The median age has increased from 34.1 years in 1989 to 37.9 years in 2000. The percentage of people over 65 has increased from 11.4% in 1989 to 16.2% in 2005. The age dependency rate (proportion of inhabitants aged 15-64 compared to those aged 65 and older) in 1989 was 5.80, the same figure for 2004 was 4.19 (table 4). Table 4. Selected demographic indicators for Estonia in 1989-2004

1989 1994 1999 2004 Total population (thousands) 1565.6 1477.0 1379.2 1351.1 Proportion of population 0-15 20.7 20.2 18.0 15.0 Proportion of population 65+ 11.4 12.9 14.7 16.2 Age dependency rate 5.80 5.09 4.51 4.19 Total fertility rate 2.21 1.42 1.32 1.47 Crude mortality rate 11.82 15.19 13.41 13.11 Life expectancy form birth (total) - men - women

70.31 65.55 74.68

66.46 60.52 72.76

70.27 64.64 75.77

72.02 66.25 77.78

Source: Statistical Office of Estonia These demographic pressures have significantly influenced the development of social policy in Estonia. Leppik & Kruuda (2003: 13) reveal that declining birth rates have reduced somewhat the financial burden on the scheme of family benefits, from another side; increasing life expectancy has posed challenges for the pension and health insurance systems.

Changes in value orientation of the population The transforming socio-economic situation has psychological outcomes as well. Political and economic liberalisation suppressing personal responsibilities and opportunities approached the general value orientation to individual pragmatism and re-oriented the individual locus of control from outer (learned helplessness) to the inner (self-help mentality) focus. Such a fundamental re-orientation of personal values has created preconditions for legitimatisation of neo-liberal social policy ideology. The analysis of political attitudes of supporters of different parties in Estonia has revealed quite similar political orientation in all groups of voters. In comparative context, the political attitudes have much stronger right-wing orientation than in any Eastern European country. Such an orientation could be co-effect of several psycho-social factors – desire to distance from the Soviet past, individualistic general value orientation, wish to maintain the status of least communistic (and the most “Western”) country in Eastern Europe, etc. By the estimations of political scientists, it seems obvious that the political situation in Estonia will remain stable in the near future. The turn to the left is impossible, because Estonia does not have enough supporters of left-wing ideas. At the current situation, the turn more to the right, seems not realistic also.

Overview of the social protection system of Estonia The following paragraphs give necessary insight into the social protection system of Estonia. The overview is mainly based on two sources: 1) Estonia Country study, written by Leppik & Kruuda in January 2003, which is a separate contribution for the Study on the Social Protection Systems in the 13 Applicant Countries, financed by the European Commission

7

(Employment and Social Affairs DG); 2) materials prepared by the Ministry of Social Affairs, presented on the webpage of the Ministry (www.sm.ee).

The structure of social protection

The social protection system of Estonia consists of social security and social welfare. The social security comprises of seven schemes: 1) health insurance, 2) unemployment insurance, 3) pension insurance, 4) state unemployment allowances, 5) state family benefits, 6) social benefits for disabled people, and 7) state funeral benefits. Social assistance cash benefits (subsistence benefit) and social services are provided under the system of social welfare, which is separate from the system of social security (figure 1).

Figure 1. The social protection system of Estonia More detail overview about different social security schemes in 2002, compiled by the Ministry of Social Affairs, is presented in APPENDIX 1.

Administration of social protection In accordance with the State Government Act, the field of social protection is within the competence of the Ministry of Social Affairs. Within the area of administration of the Ministry, two governmental agencies – the Social Insurance Board and the Labour Market Board and two legal bodies – the Health Insurance Fund and the Unemployment Insurance Fund – are responsible for the administration of different branches of social protection. The Social Insurance Board administers the schemes of pension insurance, family benefits, social benefits for disabled persons and funeral grants. The Board maintains a State Pension Insurance Registry, which includes data of all insured persons and the social taxes paid on their behalf, as well as data on beneficiaries. The Labour market Board administers the scheme of state unemployment allowances. The Board maintains also a Registry of Unemployment Persons and Labour Market Services. The Estonian Unemployment Insurance Fund is in charge of the scheme of unemployment insurance. The health insurance scheme is run by the Health Insurance Fund.

Financing social protection The schemes of pension insurance and health insurance are financed primarily from a special earmarked tax – social tax. According to the Social Tax Act, social tax is defined as a financial

SOCIAL PROTECTION

Social security

Social welfare

Social insurance: - Health insurance - Pension insurance - Unemployment i

State social benefits: - Family benefits - Social benefits for disabled - Unemployment benefit

Welfare benefits: - Subsistence benefit

Welfare services: -Housing services -Services for disabled

8

obligation, laid on the taxpayer to obtain necessary revenues for state pension and health insurance. The rate of social tax is 33% of the tax base, of which 20 percentage points is allocated for pension insurance and 13 percentage points for the health insurance. However, the financing of state pension insurance is not exclusively confined to social tax. National pensions as well as different kind of pension supplements and administrative costs are financed from general state revenues. Nevertheless, the earmarked nature of social tax entails that revenues from social tax are kept strictly separate from other state revenues. While for the health insurance system social tax is the only source of revenues, the state still covers from general revenues certain health care costs outside the health insurance system (e.g. medical assistance for uninsured persons, the costs of ambulance service, preventive and public health programmes, etc). The second pension pillar, introduced to supplement the state pension insurance, is financed partly from additional contributions of employees, partly from reallocation of a share of the current pension insurance part of social tax. The additional funded pension system (third pillar) is voluntary and contributions are made by the employees themselves. The voluntary contributions to the third pillar are exempt from the income tax in the extent of 15% of the taxpayer income in a given taxation period. The scheme of unemployment insurance is financed from compulsory unemployment insurance contributions paid by employees and employers. Family benefits, state unemployment allowances, social benefits for disabled persons, funeral grants, social assistance subsistence benefits and state-provided social services are finances from the general state taxes. Social services are financed mainly by local municipalities from local revenues. The main financing sources of local municipalities are: 1) 56% of the personal income tax paid by the individuals living within its territory, 2) subsidies from the state budget, and 3) local taxes.

9

Social protection expenditures

The calculation of social protection expenditure is based on ESSPROS methodology. By the definition of ESSPROS, social protection is the aggregate of measures taken by the state, local governments or the private sector in order to facilitate the subsistence of a person or a household in case of partial or total loss of income when certain predefined risks occur. Social protection expenditure includes monetary benefits in cash and non-monetary benefits in the form of services or goods.

The level of a state’s social protection in general is characterised by the relative importance given to social protection in the Gross Domestic Product (GDP). In the EU-25 countries, social expenditures in 2003 amounted to on average 28.0% of GDP, ranging from 13.4% (Estonia and Latvia) to 33.5% in the case of Sweden. The lowest percentage of social expenditures from GDP in Estonia determines in the large extent the opportunities of the population of Estonia to benefit from the social protection system. Because of the considerable low GDP per capita (48.2% from EU-25 average in 2003), the total social expenditure per one individual is among the lowest in Europe as well (figure 2).

DKAT

FRDEBE

NLUKFIIT

EU-25

LTLV

EE

ELSIPT

ES

IECYMT

SKCZHU

PL

12

14

16

18

20

22

24

26

28

30

1000 2000 3000 4000 5000 6000 7000 8000

Social expenditures per capita (PPS, 2002)

Per c

ent o

f soc

ial e

xpen

ditu

res

from

GD

P (2

002)

Figure 2. The social expenditures in the European Union in 2002 (Eurostat data)

Following the change of percentage of social expenditure from GDP within the period of 1998-2003, somewhat declining trend becomes evident. The share of the social expenditures has dropped from 15.2% in 1998 to 13.2% in 2003 (being the highest in 1999 because of the considerable increase of old-age pensions by the government before the Parliament elections (figure 3).

10

15,2

16,5

14,1

13,413,0 13,2

10,00

11,00

12,00

13,00

14,00

15,00

16,00

17,00

1998 1999 2000 2001 2002 2003

% o

f GDP

600

650

700

750

800

850

900

950

1000

1050

1100

Tota

l exp

endi

ture

(mill

EUR

O)

% of GDP Total expenditure

Figure 3. Social expenditures in Estonia in 1998-2003 (ESSPROS, Ministry of Social Affairs of Estonia)

The figure illustrates also the dynamics of total social expenditure – despite of the declined percentage of social expenditures from GDP, the total spending has increased from 676 million euros in 1998 to 1068 million euros in 2003. Such a ‘controversy’ demonstrates the effect of positive economic growth for the social protection system when the decline of the percentage of social expenditures from GDP may not mean reduction of the welfare state (especially in comparative perspective).

Structure of social expenditures

The current chapter analyses the structure of social expenditures according to the functions and financing types of schemes determined by ESSPROS. Estonia has joined to ESSPROS in 2002, and the database covers only the years 2000-2003. The harmonisation of national social protection system with the ESSPROS methodology is still in process, thereby the presented data may not be fully comparable with the other countries of the European Union.

Structure of social expenditures by function

Estonia, similarly to the most EU countries, spends the highest share of her social protection resources on old-pensions and sickness/ health care and their combined share is about ¾ of total spending on benefits (figure 4).

11

0,6

0,8

1,6

1,8

9,3

10

31,8

44

2

4,6

1,5

6,6

8

8

28,3

41,1

0 5 10 15 20 25 30 35 40 45 50

housing

survivors

assistance/ exclusion

unemployment

disability

family benefits

sickness/ healthcare

old age pensions

as per cent of total benefits

EU-25Estonia

Figure 4. The structure of social expenditures by function: Estonia and EU in comparison, 2003 (ESSPROS data) The share of benefits for health, old age, families and disability from the total benefits in Estonia is higher compared to EU average, while benefits for the unemployed, survivors and social exclusion constitute lower percentage compared to the EU average. The most significant difference of the Estonian social protection expenditure is a much lower proportion spent on unemployment benefits (1.8% in Estonia compared to the EU average -6.6%), especially considering that the unemployment rate in Estonia (10.1% in 2003) is above the EU average. Relatively little resources on unemployment are spent also in Italy and Lithuania (both 1.8%), United Kingdom (2.7%), and Hungary (2.8%). However, the percentages of spending on unemployment of Estonia in 1998 (0.7%) or in 2002 (1.1%) (see table 5) are definitely the lowest in the all European Union. The per capita expenditures on unemployment in Estonia constituted 18 PPS in 2001. The same figure for the EU-25 average was 350 PPS (calculation based on Abramovici 2005). The little expenditure for unemployment benefits could be partially explained by the political declaration of the government coalition (formulated already at the beginning of nineties) according to what “low unemployment benefits preserve work motivation while high benefits create welfare dependency”1. Table 5. Overview social protection expenditures as percentage of GDP and total expenditures on social protection in 1998-20032 1998 1999 2000 2001 2002 2003

%

GDP

% total SP

% GDP

% total SP

% GDP

% total SP

% GDP

% total SP

% GDP

% total SP

% GDP

% total SP

1 The current state unemployment benefit (400 EEK/ about 25 euros) forms less than 10% of average net wage.

2 Note: the data for 1998-1999 and 2000-2003 are not fully comparable. The data for 2000-2003 are harmonized according to the methodology of ESPROSS.

12

old age pensions 5,9 38,8 6,9 41,2 6,1 43,4 5,7 42,5 5,7 43,6 5,8 44,0 survivors 0,3 1,9 0,3 2,0 0,2 1,7 0,2 1,2 0,1 0,8 disability 1,2** 7,9** 1,0 7,8 0,9 6,6 1,1 8,2 1,2 8,9 1,2 9,3 unemployment 0,1 0,7 0,2 1,3 0,2 1,3 0,2 1,4 0,1 1,1 0,2 1,8 family benefits 1,7 11,2 1,8 14,2 1,7 11,9 1,5 11,5 1,5 11,4 1,3 10,0 sickness/ healthcare 5,4 35,5 5,4 30,8 4,5 32,1 4,3 31,9 4,0 31,1 4,2 31,8 housing 0,1 0,7 0,1 0,6 0,1 0,6 0,1 0,6 social assistance/ exclusion 0,9* 5,9* 0,5* 2,8* 0,3 2,0 0,3 2,3 0,3 2,0 0,2 1,6

* Total of housing and social exclusion ** Total of survivors’ and disability pensions

Source: ESSPROS, Ministry of Social Affairs of Estonia From another hand, the percentage of benefits delivered to families and children (more than 10%) is comparable to the Nordic welfare standard (Denmark 13.2%, Finland 11.5%, Sweden 9.5%) and are much higher than the respective figures in Southern-European countries (Spain 3%, Italy 4,1%, etc). However, the monetary ‘value’ of family benefits in Estonia (150 PPS per capita) is close rather to the South-European standard (102 PPS in Spain, 220 PPS in Greece, 226 PPS in Italy, etc) than to the Nordic welfare model (1054 PPS in Denmark, 747 PPS in Finland, etc). The structure of social expenditures in 1998-2003 has been relatively stable in Estonia. The share of pension expenditures has slightly increased, because of regular increase of pensions from year to year. Some increase can be revealed also in the case of disability benefits, which is caused by the introduction of new (and more generous) disability benefits according to the Social Benefits for Disabled Persons Act, launched in 2001. Family and survivors’ benefits show declining share in the total structure of benefits.

Structure of social expenditures by financing structure

Entitlement to social benefits varies between European countries. Some countries (e.g. Germany, Spain and France) follow a “Bismarckian” tradition where social insurance is central to the social protection system, while in some other countries (like Sweden and United Kingdom) the non-contributory benefits (a “Beveridgian” system) prevail.

Estonia inherited her benefit systems from the Soviet Union, where the pension system had several Bismarckian features (e.g., entitlements were based on work and benefits were linked to the former wage). The Bismarckian traditions are characteristic also for the current social protection system of Estonia. The contributory benefits (including pension, health and unemployment insurance) form together about 80% from all benefits, which is the highest percentage among all countries of the European Union (e.g. the percentage of contributory benefits from all benefits in 2003 were in Czech Republic 76.4%, Latvia 71.1%, Slovakia 69.1%, etc).

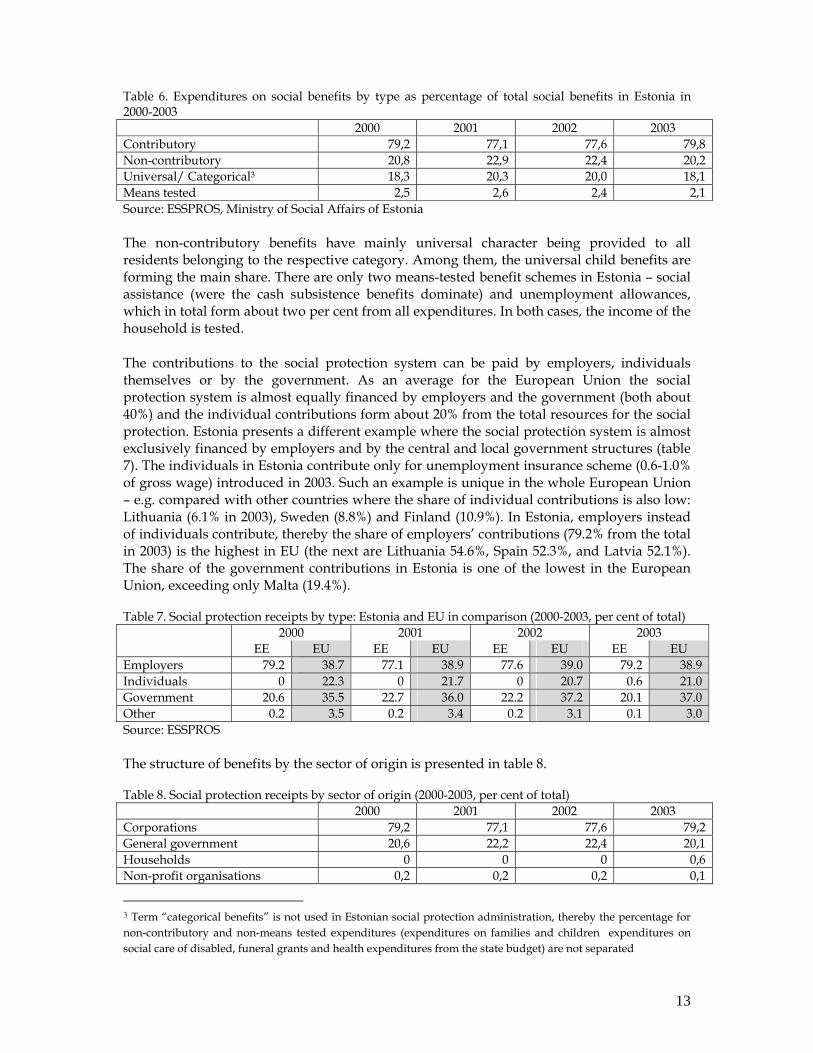

The non-contributory benefits in Estonia are benefits for disabled, families and children, unemployment allowances, funeral benefits, as well as benefits for social assistance, constituting about 20% from all social expenditures (table 6).

13

Table 6. Expenditures on social benefits by type as percentage of total social benefits in Estonia in 2000-2003 2000 2001 2002 2003 Contributory 79,2 77,1 77,6 79,8 Non-contributory 20,8 22,9 22,4 20,2 Universal/ Categorical3 18,3 20,3 20,0 18,1 Means tested 2,5 2,6 2,4 2,1 Source: ESSPROS, Ministry of Social Affairs of Estonia

The non-contributory benefits have mainly universal character being provided to all residents belonging to the respective category. Among them, the universal child benefits are forming the main share. There are only two means-tested benefit schemes in Estonia – social assistance (were the cash subsistence benefits dominate) and unemployment allowances, which in total form about two per cent from all expenditures. In both cases, the income of the household is tested.

The contributions to the social protection system can be paid by employers, individuals themselves or by the government. As an average for the European Union the social protection system is almost equally financed by employers and the government (both about 40%) and the individual contributions form about 20% from the total resources for the social protection. Estonia presents a different example where the social protection system is almost exclusively financed by employers and by the central and local government structures (table 7). The individuals in Estonia contribute only for unemployment insurance scheme (0.6-1.0% of gross wage) introduced in 2003. Such an example is unique in the whole European Union – e.g. compared with other countries where the share of individual contributions is also low: Lithuania (6.1% in 2003), Sweden (8.8%) and Finland (10.9%). In Estonia, employers instead of individuals contribute, thereby the share of employers’ contributions (79.2% from the total in 2003) is the highest in EU (the next are Lithuania 54.6%, Spain 52.3%, and Latvia 52.1%). The share of the government contributions in Estonia is one of the lowest in the European Union, exceeding only Malta (19.4%).

Table 7. Social protection receipts by type: Estonia and EU in comparison (2000-2003, per cent of total) 2000 2001 2002 2003

EE EU EE EU EE EU EE EU Employers 79.2 38.7 77.1 38.9 77.6 39.0 79.2 38.9 Individuals 0 22.3 0 21.7 0 20.7 0.6 21.0 Government 20.6 35.5 22.7 36.0 22.2 37.2 20.1 37.0 Other 0.2 3.5 0.2 3.4 0.2 3.1 0.1 3.0 Source: ESSPROS

The structure of benefits by the sector of origin is presented in table 8.

Table 8. Social protection receipts by sector of origin (2000-2003, per cent of total) 2000 2001 2002 2003 Corporations 79,2 77,1 77,6 79,2 General government 20,6 22,2 22,4 20,1 Households 0 0 0 0,6 Non-profit organisations 0,2 0,2 0,2 0,1

3 Term “categorical benefits” is not used in Estonian social protection administration, thereby the percentage for non-contributory and non-means tested expenditures (expenditures on families and children expenditures on social care of disabled, funeral grants and health expenditures from the state budget) are not separated

14

Source: ESSPROS

Tax credits Estonia introduced flat tax rate in 1994. Under this tax system all three types of income – earned income, business income and capital gains – are taxed at the same flat tax rate, irrespective of how much persons earns. From 1994 until 2004, the tax rate was 26%. As of January 2005, the tax rate is 24% and it will be gradually reduced to 20% by 2009. From January 1, 2006, the tax rate is 23%. The amount of basic tax-exempt income (personal allowance) will be annually revised and established by the Government. In 2005, the amount of personal allowance was 20400 EEK per year (about 1300 euros); in 2004, the personal allowance (1400 EEK per month or 16800 EEK per year) formed about 19% of average gross wage (45% of disposable household income per capita). Parents with children under 17 years have an additional personal allowance (in amount of basic tax exempt income) per third and every following child (from January 1, 2006 it has been extended to second and every following child. Additional tax exemptions concern certain state pensions and pensions from compulsory pension schemes in amount of 36000 EEK (2298 euros) per year (www.fin.ee). In Estonian tax system, there are only few deductions available for individuals. Most important deductions that can be made from taxable income are mortgage interest, educational expenses, gifts, donations, and payments to certain voluntary pension schemes. The amount of deductions is limited to a smaller of following two conditions: 50000 EEK (3192 euros) per year or maximum of 50% of a taxable income. The summary overview about tax credits in the Estonian taxation system is presented in the table 9. Table 9. Overview of tax credits in Estonia in 2003 Type of credit: Basis Level (absolute) Level (% of hsh. income) Basic tax exempt income 12000 EEK (765 euros) per

year 36% of average disposable household income per capita

Additional exemption per third and every following child

12000 EEK (765 euros) per year

36% of average disposable household income per capita

Additional exemption from state pension income

36000 EEK (2298 euros) per year.

164% of average old-age pension, 108% of average disposable household income per capita

Tax deductions from: • mortgage interests • educational expenses • gifts and donations • payments to voluntary

pension schemes

50000 EEK (3192 euros) per year

Up to 50% of taxable income

Source: Ministry of Finance of Estonia (www.fin.ee) The basic tax exemptions from labour and pension income contribute for the welfare of all subjects of taxation. Additional deductions depending on number of children in the household have a positive effect on income of families with (many) children and in that way reduce of vulnerability of families with children. Special deduction from mortgage interest, educational expenses, payments to voluntary pension schemes, etc support rather the groups of medium and high levels of income than the low-income groups.

15

Conditionality of benefits

The social protection system of Estonia is not that ‘selective’ or ‘targeted’ in terms on conditionality. Most of the benefits are provided without any restriction to the corresponding category of individuals and the system is rather universalistic. All benefits are exclusively provided for permanent residents of Estonia or for those persons ‚equalised’ with residents. The insurance-based benefits by definition require specific contribution (e.g. 15 years of ‘pensionable service’ for old-age, survivors’ and disability pensions). Entitlement for benefits from the health insurance system requires social tax paid by employer, by state or individual himself.

Child and family benefits are universal and are provided to all children below 16 years old. If the child is engaged in full-time studies, the payment is extended up to the age of 19. The universality of family benefits has been politically discussed from time to time. The discussion concerns replacement of universal benefits by the means-tested and therefore strictly targeted family programs. Despite of considerable support to this idea by politicians, the idea has not been developed further because of strong negative public opinion.

The means test is applied only for subsistence benefits and for unemployment benefit schemes. The means-test is applied only for household income (not for assets or property) and the household is defined as a group living on the same address and using commonly the resources of the household, there is no direct caring responsibilities for parents and/ or children. However, the family solidarity issue remains problematic in juridical terms – Social Welfare Act refers mainly to the individual responsibility, while the Family Law Act stresses the mutual responsibility of parents and children. This legislative controversy has led to situation were separately living students were not entitled to subsistence benefit because they were considered as dependants from their parents.

The activation measures (recipient should seek a work and participate in activation/ rehabilitation programmes) are applied only in case of unemployment benefit. Introduction of active labour market policy has been one of the main priorities of the Estonian social policy and the activation measures will play more significant role in the future.

There are some ‘ideological’ and value-loaded’ factors which somewhat restrict implementation of activation policy measures. The ruling right-wing government support the concept of “negative freedom” – nobody can force an individual into anything; an individual is free not to do something. By this reason, the requirement of participation in workfare programs or other similar activities could be seen as a restriction of basic human rights. However, the new concept of social welfare (2004) has introduced a case management system in social assistance. The social work professionals in cooperation with the client are formulating the individual rehabilitation plan, which also includes activation measures.

The details of conditionality for different benefit schemes are provided in table 10.

Table 10. Conditionality of selected type of benefits age Contribution history residence Means

tested Yes/no

Type of means testing

Level of means testing

Maximum family solidarity

Unemploy-ment

16-63 Have worked at least for 180 days during

Residents of

yes Dis-posable

18,1% 5 (household living on the

16

last 12 months and has registered as unemployed4

Estonia income same address)

Pension (first pillar)

63+(a) 15 years of pensionable service obtained in Estonia

Residents of Estonia

no

Children’s benefits

0-16(19)

no Residents of Estonia

no

Social assistance

16+ no Residents of Estonia

yes Dis-posable income

18% + expenditures on housing

5 (household living on the same address)

a) The age limit established by law is applicable for men since 2001, while for women it will start applying from 2016. The retirement age for women increases gradually. The retirement age for women in 2002 and 2003 was 58 years 6 months.

Administration costs

There is no formal statistics available concerning the administration costs within the particular schemes. According to the ESSPROS data the overall administration costs constituted about 1.5% from the total social expenditure in 2003 (0.2% of GDP) and the percentage has been relatively stable. However, the available statistics does not give clear evidence about real expenditures included under the heading of ‘administration costs’.

The main costs for maintaining the social protection (e.g. salaries for people working for the system – civil servants, social workers, providers of services, etc) are financed from the central and local budgets and are not considered as social expenditures. It is obvious that the expenditures for maintaining the system are increasing in Estonia. The system of social protection is still developing – especially in the field of social services, where the number of available services as well as the number of service providers increases from the year to year. One factor potentially leading to the increase of administration costs is related to the implementation of individual case management system in social assistance. For example, , the right to spend up to 5% from the total budget for subsistence benefits for administration costs was given to social workers in the local municipalities by the Ministry of Social Affairs since January 2006.

Coverage

There are no clear definitions about coverage of different social protection schemes, nor harmonised data available for Estonia. In the frames of the current project, the coverage of different schemes is defined as the percentage of beneficiaries (benefit recipients) from the total population. This definition is not that informative – in the case of old age, survivors’ and disability pensions as well as universal family benefits (which are practically entitled to every individual belonging to the respective category) the figures given in the table 11 indicate rather the changing proportion of elderly, children, disabled, etc in the whole population than the take-up ratio.

4 Registered as unemployed can be persons who are: aged between 16 and pension age; not engaged in work or other equivalent activity; ready to take up job and searching for job.

17

The proportion of old-age pension recipients is increasing from year to year – in 1998, 20.9% of the total population has been entitled to old-age pension, the same figure for 2003 was 22.9. The ageing population of Estonia can easily explain this change. However, Leppik and Kruuda (2003: 55) point out that all economically active persons are covered with the first pillar through the payment of social tax, all residents are guaranteed a national pension (the share of the recipients of old-age national pensions from the total number of old-age pensioners in 2003 was about 1%, the national pension forms about 20-25% from the average old-age pension). Accordingly, coverage and take-up ratios of the state pension system are nearly 100%.

There are two types of survivors’ pensions – survivors’ pension (insurance based) and national pension based on survivorship. Insurance-based survivors’ pension is provided to all dependant family members of a deceased insured person, provided the insured person had by the date of death a pensionable service necessary granting him/ her work-incapacity pension or old-age pension. In case the breadwinner did not satisfy the qualification period, survivors have the right to a national pension based on survivorship, provided the breadwinner resided in Estonia at least one year prior to death. Similarly, to the old-age pension, the survivors’ pensions cover nearly all persons without breadwinner. The proportion of survivors in total population form about 1%.

Table 11. Percentage of beneficiaries of different social protection schemes in Estonia in 1998-2003, (yearly averages as percentage of total population) 1998 1999 2000 2001 2002 2003 Old age pensions (a) 20,9 21,3 21,1 22,5 22,7 22,9 Survivors’ pensions (a) 1,1 1,1 1,1 1,1 1,0 0,6 Disability pensions (a) 4,3 4,5 4,9 3,2 3,5 3,8 Unemployment (b) 1,3 1,9 1,9 2,1 1,7 1,4 Family benefits (c) 24,5 23,9 22,8 22,8 22,2 21,7 Covered by health insurance (d) n.a. 95,6 93,4 93,9 94,7 94,2 Housing (e) n.a. 0,1 0,1 0,1 0,2 0,2 Social assistance (f) 7,8 7,7 7,2 6,5 5,7 4,6

(a) Data about pension recipients are obtained from the Social Insurance Board of Estonia (b) ‘Unemployment’ includes only recipients of unemployment benefit (not unemployment insurance), (c) includes only recipients of the universal regular (monthly) child benefits, excluding birth grants, parental leave allowance, child care benefit, school year start benefit, etc (data from the Ministry of Social Affairs), (d) Data from Estonian Health Insurance Fund (e) Indicates the percentage of persons entitled to social housing (f) Indicates the percentage of subsistence benefit recipients (means-tested social assistance benefit).

Disability pensions in Estonia are organised and administered in the same way as old-age pensions and survivors’, consisting of disability pension scheme for insured persons and national pensions based on incapacity to work. The system covers almost all disabled persons. The number of disability pension recipients in 1998 formed 4.3% from the total population; in 2003, the corresponding figure was 3.8%.

The system of family benefits in Estonia includes eleven different types of benefits: 1) child allowance, 2) child care fee, 3) single parent’s allowance, 4) conscript’s child allowance, 5) foster care allowance, 6) birth grant, 7) adaptation grant, 8) school grant, 9) start-in-independent-life allowance, 10) supplementary benefit for three or more children or with

18

triples, and 11) parental benefit (introduced in 2004) (see APPENDIX 1 for details). The current report refers only to child allowance. Child allowance (as all other family benefits) is universally provided to all families with children in respective age, residing in Estonia. Thereby the actual coverage is nearly 100%. The share of children at age up to 16 (19) in total population in 1998 was 24.5% (at the same time the percentage of persons 0-15 years old was about 20%). Because of declined birth rate, the percentage of child benefit recipients has declined to the level of 21.7% in 2003.

Regarding health insurance, individuals are insured firstly based on payment of social tax. However, as a number of large population categories (pensioners, children, etc) are equalised with the insured, the coverage is nearly universal, reaching 94% of population. The main non-covered population categories are non-registered (and mainly long-term) unemployed and socially excluded persons (e.g. discouraged persons, homeless, etc). Emergency social and medical assistance is available to all persons legally staying in Estonia.

The state unemployment allowance is the last resort benefit alongside with the social assistance benefit, which substitutes the unemployment insurance benefit for the person who does not satisfy the conditions for entitlement to the insurance benefit. The allowance is designed to provide assistance in the case of insufficient economic resources; the award is subject to means testing which takes into account income of the person. The allowance is paid only if the person’s income is below the rate of the allowance. The allowance is granted up to 270 days at to a person who is registered as unemployed in the employment office of the place of residence and reports to the employment office at least once within 30 days; has been employed or engaged in an activity equal to work for at least 180 days during 12 months prior to registration as unemployed; his income is below the rate of the state unemployment allowance. Table 11 indicates that the percentage of persons receiving state unemployment benefit from the total population is less than 1.5%. The percentage of beneficiaries from the labour force in 2003 was three per cent and from the total number of unemployed about 30% (table 12). Table 12. Percentage of beneficiaries of unemployment benefits in Estonia in 1998-2003

1998 1999 2000 2001 2002 2003 % of active population 2,6 4,1 4,0 4,4 3,6 3,0

% of unemployed 26,6 33,0 29,6 34,8 35,0 29,7 Source: Labour Market Board of Estonia (www.tta.ee)

Registered unemployment has compared to labour force survey data always been considerably lower by two reasons: 1) not all people who have lost their jobs register as unemployed in employment offices, 2) not all jobless qualify as unemployed (long-term unemployed and discouraged persons). The percentage of registered unemployed from all number of unemployed is not stable. Nevertheless, the latest figure from the year 2004 – 22.8% may give some confirmation about decreasing coverage rate of unemployment benefits. The explanation is twofold: 1) introduction of unemployment insurance scheme reduces the need for last-resort unemployment benefit, 2) the share on long-term unemployment from the total unemployment is in increase, and therefore more people will be not qualified as unemployed and consequently are excluded from the right to receive the unemployment benefit.

The subsistence benefit is a state support to needy persons paid by a local municipality government. The benefit is paid to households/ individuals residing in Estonia, whose

19

income after payment of fixed housing expenses (corresponding to the standard living space) are below the subsistence level established by the Parliament. Subsistence benefit is granted for one month at time. Each month a new means test is carried out. From 2002, the local governments have a right to refuse to pay the subsistence benefit to working age persons who do not work or study and who have repeatedly refused offers of suitable work or to take part in relevant social rehabilitation programmes organised by the municipality.

The percentage of subsistence benefit recipients is declining since 1997: in 1998, it formed 7.8% from the total population, the respective figure for 2003 was 4.6% and in 2004 – 3.2%. The decrease in subsistence benefit coverage can be explained by the increased living standards (less people have income lower than the benefit threshold - 500 EEK after payment of fixed housing expenses, which has not changed since 1997). The number of recipients has also decreased because introduction of the political recommendation about replacement of cash assistance benefit with necessary social services.

To sum up, the Estonian social protection system can be characterised by universal (or nearly universal) coverage.

Duration and replacement rates of social benefits

The social protection systems differ from each other not only by financing principle or universal or marginal coverage, but also by general generosity of the system. Some welfare states provide benefits for a longer period and with higher replacements rates (e.g. the North-European countries, contrasting to the poor benefits with limited duration in others (like in case of Anglo-American model).

The overview about the duration of some particular benefits schemes in Estonia is given in the table 13.

Table 13. Maximum duration of benefit in months Number of months Unemployment • State unemployment benefit is paid for 9 months (270 working days). In

certain cases the period may be extended (e.g. if less than 180 days remain until the pension age, if less than 70 days remain until the date of confinement or if the person is raising three or more children up to 18 years old).

• The unemployment insurance was introduced in 2002. The insurance benefit period depends on the length of the insurance (contribution) period and varies from 6-12 months. Insured for less than 5 years receive insurance benefit for 180 calendar days (6 months); 5-10 years – 270 days (9 months) and over 10 years – 360 days (12 months)

Children • The universal flat-rate state child allowance is paid monthly until the child reaches the age of 16. If the child is engaged in full-time studies, the payment is extended up to the age of 19. Total number of months is 16*12-19*12=192-228 months

• The system of parental benefit (parental wage) was introduced in January 1, 2004 for compensating for income not received by stay-at-home parents in the first year of the child’s life (12 months).

Social assistance

Subsistence benefit is granted for one month at a time. Granting for the next month requires new application and means test.

20

Aidukaite (2004: 72) in her comparative study of social policies in the Baltic countries concludes that the duration for unemployment benefit is quite short in the Baltic countries compared to other European countries. Kangas (1999: 27), comparing different welfare states reveals that in all transitional economies the duration of unemployment insurance lags behind the international mean.

The duration of child allowances in Estonia is comparable with “European-standards”: in most EU countries, the allowance is entitled to children at the age up to 15-16, which is often prolonged until the end of full-time studies (at the age of 18-20).

Subsistence benefits in Estonia are granted for only one month at a time. Granting for the next month requires new application and means test. The number of consequent application is not limited. The data from 2003 reveal that the percentage of welfare recipients granted in every month of the calendar years (i.e. twelve times per year) from total number of recipients was 18.3%. The studies carried out among the long-term unemployed and the poor have shown that some respondents have received permanently (without any break) the subsistence benefit during more than ten last years.

The depth (or replacement rate) of benefits can be calculated in different ways, proceeding from different thresholds/ standards. The most common replacement rates are calculated as a percentage of benefits from guaranteed minimum income level or benefit-average net wage ratio. Table 14 presents some replacement rates - as percentage of a) minimum wage, b) estimated subsistence minimum5, c) average net wage, and d) median equivalent disposable income of households. The table indicates the lowest and highest percentage within the period and gives approximate assessment about average level during 1998-2003.

The general level of generosity of the social protection system of Estonia is low. The highest replacement rates can be revealed in case of old-age pension (the average old-pension forms about 40% from the average net wage, which has been set as a minimum target in EU pension policy), the lowest in case of child allowance (3-5% of average net wage) (figure 5).

Table 14. Depth of selected social benefits (benefits as percentage of) (latest year available and fill new table for every year in the period 1998 – 2003 when major changes occurred).

% minimum wage % of calculated subsistence minimum)

% of average net wage

% of median disposable income

Unemployment low high average

18,5 (2003) 32,0 (1999) ~25

28,3 (2003) 34,1 (1999) ~30

7,7 (2003) 11,7 (1999) ~10

18,1 (2003) 22,9 (2000) ~20

5 The calculated subsistence minimum is the lowest set of essential means of subsistence that enables the capacity for work to be maintained. The calculated subsistence minimum per person a month (30 days) includes the minimum food basket and the costs of essential industrial goods and services. In calculating the minimum food basket, the suggestions of nutritionists were considered and a sample food basket created, the components of which must ensure the essential „average” human energy need of 2400 kcal and accord to average prices. For calculating the subsistence benefit for industrial goods and services, the average costs from a household budget survey were applied, corrected with various coefficients calculated by the experts. The method for calculating subsistence minimum is agreed within the trilateral negotiations between the representatives of the government, the employers and the employees. The calculated subsistence minimum is somewhat lower than the absolute poverty line.

21

Pensions (1st p) Low High Average

91,9 (2003) 123,6 (1999) ~105

105,9 (1998) 140,7 (2003) ~125

38,0 (2003) 36,6 (2001) 45,2 (1999) ~40

81,0 (1998) 89,8 (2003) ~88

Child benefits low High average

6,9 (2003) 13,6 (1998) ~10

10,6 (2003) 12,7 (1998) ~11

4,7 (1998) 2,9 (2003) ~3,5

9,7 (1998) 6,8 (2003) ~8

Social assistance Low High Average

45,6 (2003) 44,1 (2000) 49,8 (2001) ~46

42,7 (1998) 69,7 (2003) ~55

15,8 (1998) 18,9 (2003) ~17

32,7 (1998) 44,5 (2003) ~41

Old-age pension covers about 40% from average net wage, about 90 per cent of household equivalent net income, and about 125% of calculated subsistence minimum. Such rates are rather low in European context, but at least guarantee the independent economic coping socio-economic environment of Estonia. The permanent (but still modest) increase of pension payments is ensured via indexation. The index is an arithmetic average of the annual increase of the consumer price index and the increase of social tax revenues. The indexation entails that the increase of pensions will keep pace with inflation. The average pension in 1998 was 1247 EEK (80 euros) per month; in 2005 it has reached to the level of 2302 EEK (147 euros), and that increase considerably exceeds the inflation rate (23% during the period of 1998-2005). The pension-average wage ratio is rather stable (figure 5), the pension-minimum wage ratio is declining because of higher increase of minimum wage compared with pensions, the highest value in 1999 is related to the rapid increase of pensions before the elections of 1999.

Unemployment benefit covers less than 10% of average net wage, what is the lowest replacement rate in EU-25. The ‘absolute value’ of that flat-rate benefit is 400 EEK (about 25 euros) per month, which has not been changed since 1997. Because that reason, all replacement rates for unemployment benefit demonstrate declining trend. The benefit forms about ¼ of minimum wage and nearly 30% of calculated subsistence minimum. The benefit is insufficient for independent coping, consequently more than 50% of unemployed have an income less than poverty line and they have to apply for subsistence benefits in addition (see also figure 6).

39,1

4,7

9,4

15,8

39,9

3,9

10,4

16,1

36,9

3,1

8,4

17,8

38,0

2,9

7,7

18,9

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

old age pension child benefit unemployment social assistance

per c

ent o

f ave

rage

net

wag

e

1998 2000 2002 2003

22

Figure 5. Replacement rates of selected social benefits (benefit/ average net wage *100%)

Universal child allowance has the lowest replacement rate among all social benefits in Estonia constituting about 10% of minimum wage or subsistence benefit. The allowance for the first child in the family (150 EEK/ 10 euros per month) has not been changed since 1997 and the effect of the benefit on the total income of the household is disappearing – forming about three per cent of the average net wage. The child benefits were introduced for partial compensation of the costs related to childrearing. The recent study focusing in calculation of the cost of the children revealed that the costs related to one child constituted about 2600 EEK (165 euros) per month, which means that child allowance compensates about six per cent of childrearing costs. The benefit was increased to 300 EEK per month in 2004. The benefit for second and subsequent children is equal to 300 EEK per month.

The subsistence benefits in Estonia are related to the housing costs (rent). The entitlement criterion is a disposable income after payment of fixed housing expenses (corresponding to the standard living space). The amount of the benefit is calculated as a difference between the subsistence level and the disposable income of the household. Because of the rapid increase of housing costs in Estonia the average subsistence benefit has increased from the year to year (in 1998- 502 EEK, in 2003 – 984 EEK). As a result, the replacement rates of subsistence benefits have increased reaching to the level of 70% of subsistence minimum.

9,4 8,8 7,8 6,9 6,3 5,7

9,4 11,7 10,4 9,2 8,4 7,7

15,816,5

16,1 18,417,8 18,9

0,0

5,0

10,0

15,0

20,0

25,0

30,0

35,0

40,0

1998 1999 2000 2001 2002 2003

per c

ent o

f ave

rage

net

wag

e

benefit for 2 children unemployment social assistance

Figure 6. ‘Cumulative’ replacement rate of child, unemployment and subsistence benefit in case of family with one unemployment member and two children.

Some individuals/ households are simultaneously entitled to several benefits. Some patterns of different combinations of benefit entitlement are presented in tables 6a, 6b, 6c and 6d of APPENDIX 2. The most probable combination of benefits in Estonian socio-political environment includes child benefits, unemployment benefits and means-tested social assistance. Figure 6 presents a typical example of the household including two children and one unemployed household member, entitled to the subsistence benefit because of insufficient income level. The figure indicates that the cumulative replacement rate in such a situation is about 30-35% of average wage (or 90% of minimum wage). If one of the children is under three years old, then the family is additionally entitled to childcare allowance,

23

which increases the replacement rate by additional four-five per cent. The replacement rate may additionally increase because of single parenthood, disability or some other reason. Thereby the statement of authors of the study about influence of social benefits on work incentives and supply of labour (see Kuddo et al 2002) - despite of the fact that the rates of social benefits in Estonia are very low, in various cases it is more beneficial to live on benefits than start working for a minimum wage or a wage slightly above the minimum wage – sounds rather realistic. The authors propose to make eligibility criteria for unemployment and subsistence benefits stricter by placing a stronger emphasis on the elements that would encourage people to search for work, such as, participation in employment programmes. In 2003, about 20% of registered unemployed were entitled to activation programmes (see table 4b in APPENDIX 2) and the share is hopefully increasing in the forthcoming years.

Outcomes of social protection The outcomes and efficiency of the social protection system can be estimated by its impact on poverty and income inequality. Relative poverty level in particular country is more or less closely related to the extent and character of the welfare state (figure 7). The higher is the level of universality and generosity of the social protection system; the lower is the proportion of population living in poverty.

IE

IT

UK

FR

BELU

DKDENL

PT ELES

SE

ATFI

EELT

CY LVMT PL

SKHU

CZ

SI

EU-15EU-25

7

9

11

13

15

17

19

21

10 15 20 25 30 35

social protection expenditure 2000 (% of GDP)

at r

isk

of p

over

ty r

ate

2001

Table 7. At-risk-of-poverty-rate and percentage of social protection expenditure from GDP in the European Union (Eurostat data)

Estonia has one of the highest levels of income inequality in the European Union (figure 8), where the wealthiest quintile as an average has an income six time exceeding the average income of the poorest 20% of the population. The income inequality level in Estonia has slightly declined in recent years – the Gini coefficient in 1998 was 0.38, the same figure for 2003 was 0.36.

24

6,5

6,1

5,75,5 5,5

4,9 4,9 4,84,5 4,5 4,5 4,4 4,4 4,4

4 43,8 3,8

3,6 3,5 3,5 3,4 3,4 3,4 3,43,2

3

2,5

3

3,5

4

4,5

5

5,5

6

6,5

7

PT

EE EL

ES LV UK LT IT IE MT

PL

CY

EU

-15

EU

-25

BE FR LU NL

DE AT FI SE CZ

HU

SK SI

DK

S80/

S20

ratio

(200

2)

Figure 8. Income inequality in the European Union in 2002 (S80/ S20 ratio, Eurostat data)

The high level of income inequality in Estonia can be interpreted in two ways. From one hand, high income inequality per se is one of the main determinants of tasks of the social policy (i.e. high inequality challenges the system for more intensive vertical redistribution of resources. From another hand, the current level of inequality indicates particular inefficiency of the system concerning redistribution of resources and provision of equal opportunities.

Poverty patterns and trends High level of income inequality entails high risk of poverty for the society. The at-risk-of-poverty-rate (defined according to Eurostat methodology as 60% of median equivalent disposable income) in Estonia in 1998 was 19.4%. The poverty rate has been relatively stable during the period of 1998-2003 (figure 9). However, the latest data report that the at-risk-of-poverty rate has decreased and formed 14.2% in 2004, probably because of decreased unemployment rate and increase in general living standard.

7 7,2 6,4 6,7 6,9 6,5

19,4

16,718,3 18,2 17,9 18,3

0

5

10

15

20

25

1998 1999 2000 2001 2002 2003

at-ri

sk o

f pov

erty

rate

40% median 50% median 60% median

25

Figure 9. At-risk-of-poverty-rates in Estonia in 1998-2003 (40-60% thresholds, Statistical Office of Estonia)

The recent analysis of poverty in Estonia (Trumm 2005) has revealed a rather traditional structure of poverty: single parents, young and retired living alone and households with many children carry the highest risk of poverty. Among them, young people living alone are at the highest risk of poverty. The situation where about 40 per cent of single young people are living in poverty refers to the malfunctioning of the labour and social policies. The best situation is that of childless couples in working- or retirement-age, and the case of retired couples, the poverty rate is only about a third of that in the population as a whole. A comparison of the poverty trends of single person households at different ages shows that the poverty among youth and working-age singles is increasing, while among retired people a slight decrease is evident. The situation can be explained by the permanent slight increase of pensions. The labour market perspectives for the youth have not improved significantly, because of the increase of the duration of the studies (about 60 per cent of secondary school graduates continue their studies in the high schools) young people enter into the labour market at a later age. At the same time, the level of allowances for students (scholarship, social assistance, etc.) is below the poverty threshold. Families with children are traditionally vulnerable to poverty. At the highest risk are the households with three or more children. The share of households with at least three children who live in direct poverty6, is on average three times higher than for households with no children and the addition of one child to the household increases the poverty risk of a household by 1.51 times (departure of the child reduces poverty 0.6 times) (Käärik et al, 2001). However, the poverty rate for households with three and more children has decreased relatively more compared to households with one or two child (children) and the differences between the poverty rates of the households with different number of children tend to decline. Such a development could be partially explained by changes in child benefit systems. The benefit for the first child (150 EEK per month) has not been changed since 1997, while the benefit for a second and subsequent child has been increased twice during the period of 1996–2002. The amounts of the benefits compared to the average income of the household are relatively small, but may be relevant for those in the lowest income group. Additionally, introduction of supplementary childcare benefits for families with small (3–8 years old) or three and more children in 2000 might have reduced the poverty risk of households with higher number of children. The risk of poverty is unequally distributed through the life. The traditional age-specific poverty risks are childhood, the period of family formation and retirement. The poverty rates are lowest in the case of single young adults and at the period of children leaving the family of origin (empty nest). The data from 2002 do not confirm the traditional ‘W-shape’ age-specific poverty model (see table 8 in APPENDIX 2). The poverty rates for different age groups are quite similar – about 20 per cent.

6 Direct poverty – a level of material resources which fails to meet the basic needs of the subject (primarily the need for food and a place to live). According to international standards, the upper limit of direct poverty is set at a level of 80 per cent of absolute poverty (in 1998 1064 EEK) (Kutsar and Trumm 1999: 10).

26

Social status of the individual is one of the most important determinants of income as well as poverty. In every society, the risk of poverty is the lowest among the population participating in the labour market and the highest among the unemployed. However, the correlation between the unemployment and poverty rate depends on the socio-economic circumstances of a particular country. The strongest interrelation between unemployment and (new) poverty can be revealed in the Baltic countries and Poland, where the social cost of transition has been the highest. The opposite is the case of Ireland, Portugal and UK, where the high rates of poverty occur in the conditions of low unemployment. The traditional character of poverty is, to a lesser extent, evident also for Southern Europe (Italy, Spain, and Greece). The biggest group of the countries represent relatively cohesive societies, with balanced economic and social development. Such a typology corresponds to the traditional classification of the welfare regimes in Europe by Esping-Andersen (1996). In Estonia, the difference between the poverty rates for employed and unemployed is bigger than in most of the EU countries’ average. The poverty rate for unemployed has not been changed and about half of all unemployed persons continue to live in poverty. The only conclusion that can be made is that the social and labour policy measures (i.e. unemployment benefit and respective services as well as social assistance) are manifestly inadequate for ensuring at least the subsistence minimum for a person who has failed in the labour market.

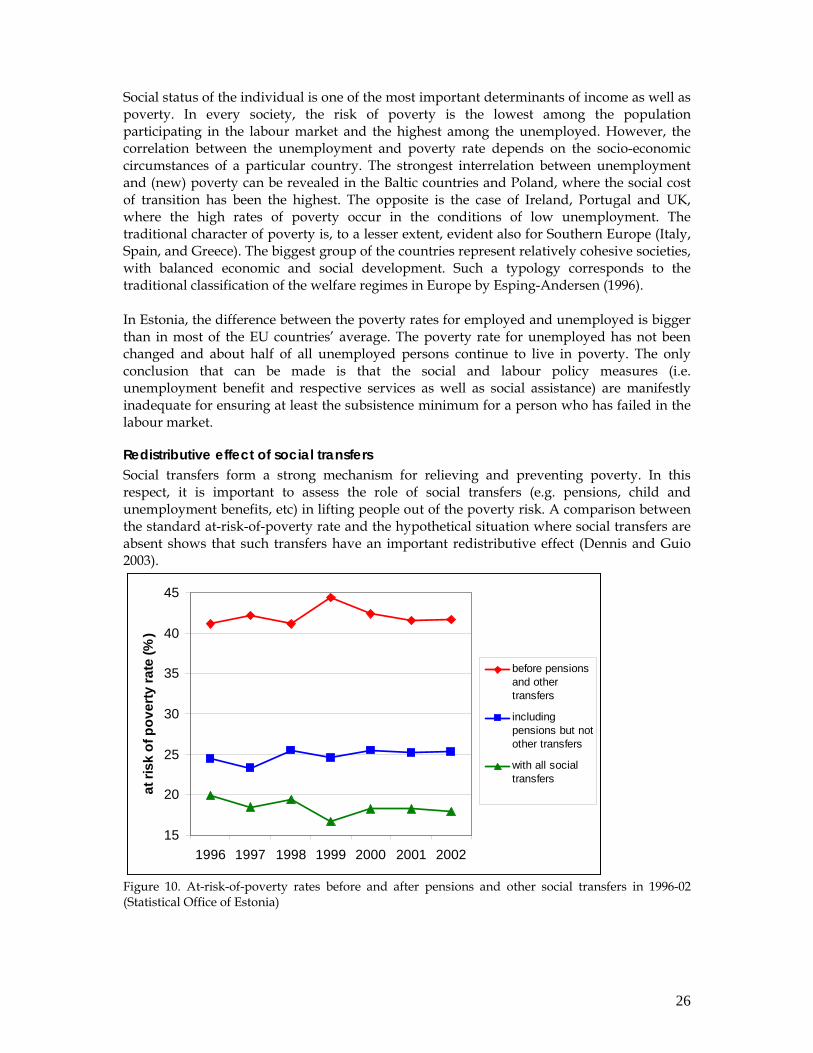

Redistributive effect of social transfers Social transfers form a strong mechanism for relieving and preventing poverty. In this respect, it is important to assess the role of social transfers (e.g. pensions, child and unemployment benefits, etc) in lifting people out of the poverty risk. A comparison between the standard at-risk-of-poverty rate and the hypothetical situation where social transfers are absent shows that such transfers have an important redistributive effect (Dennis and Guio 2003).

15

20

25

30

35

40

45

1996 1997 1998 1999 2000 2001 2002

at ri

sk o

f pov

erty

rate

(%)

before pensionsand othertransfers

includingpensions but notother transfers

with all socialtransfers

Figure 10. At-risk-of-poverty rates before and after pensions and other social transfers in 1996-02 (Statistical Office of Estonia)

27

The role of social transfers in poverty reduction is obviously important. In the absence of all social transfers, the poverty risk would be over 40 per cent in Estonia, instead of 18 per cent after all social transfer in reality (figure 10, see also table 10 in APPENDIX 2). It means that more than one fifth of the Estonian population are lifted out from poverty by the social transfers. However, here the pension payments carry the main burden in the prevention of poverty. If the pension was taken as a primary source of income for senior citizens rather than social transfers, the poverty rate without other social transfers would be about 25 per cent, which means that child and family benefits, unemployment payments, social assistance and other transfers have relatively little effect on disposable income of households (figure 11, table 7b in APPENDIX 2). Table 7a shows that the social transfers form about ¼ of the total income of the poor, the share of social transfers among the poorest income decile is more than 50%.

Figure 11. Percentage of social benefits from the disposable household income by income deciles in 2003 (Statistical Office of Estonia) Besides pensioners, the unemployed and the inactive are the social groups who benefit the most from social transfers. In the households where the head of the household is unemployed, the poverty rate falls by 21 per cent. At the same time, the poverty reduction effect of transfers is 46 per cent (table 15).

Table 15. At risk of poverty before and after social transfers in 2002 by social status of the head of the household (percentage). Social status Poverty risk before

transfers Poverty risk after transfers

Lifted out of poverty

Employed 18.8 8.0 10.8 Self-employed 27.5 12.8 14.7 Unemployed 78.1 56.7 21.4 Retired 95.6 10.3 85.3 Inactive 88.2 42.2 46.0 Source: Statistical Office of Estonia

0

10

20

30

40

50

60

rich IX VIII VII VI V IV III II poor

pensions unemployment benefits sickness/healthcare social assistance

28

Most of the social transfers are targeted to the particular social groups (children, disabled, unemployed, etc.). As a result, some groups benefit more from social transfers and are thereby more protected from the risks of poverty. Age is a main factor determining the groups of ‘winners’ and ‘non-winners’ in income redistribution. Comparing the poverty rates before pensions and social transfers with real poverty rates (after transfers) it can be demonstrated that pensioners benefit the most from income redistribution. The poverty rate before transfers – 85.4 per cent - drops to the level of 8.1 per cent after transfers (i.e. less than a tenth). The effect of transfers is the least in the case of young people – about 15 per cent (the poverty rate before transfers is 34.4% and after transfers 17.4).

Social exclusion Social exclusion is relatively new term and field of policy action for Estonia. The first introduction of the term in Estonia was probably the article by Dagmar Kutsar (1997). The article based on data from the survey of living conditions in the Baltic countries revealed that people in the Baltic countries have experienced serious losses in their welfare, determined by societal as well as individual factors. The need as become evident for re-integration and cohesion of the parts of the population who, because of their numerous deficits in welfare resources, have acquired a high risk of becoming socially excluded from mainstream society (Kutsar 1997: 103). The analysis based on data from the European Commission’s Eurobarometer Survey carried out in 2002, reports about high level of perceived social exclusion in Estonia – 18% of the population, which is 1.5 times higher than the average for EU-25 (figure 12).

57 7

9 910 10 10

11 1112 12 12

13 13 1314 14 14

15 1517

1819

20

27

0

5

10

15

20

25

30

SI DK NL ES LU AT IE SE GE PL CY EL EU MT HU BE UK FI IT FR PT LT EE CZ LV SKperc

eive

d le

vel o

f soc

ial e

xclu

sion

(%)

Figure 12. Percentage of perceived social exclusion in the European Union in 2002 (Böhnke 2004) The study indicates that on EU average level the subjective feelings of social exclusion vary only slightly among different socio-economic groups such as younger and older people or men and women. Traditional inequalities such as income, education, employment status or occupational class influence feelings of exclusion to a higher degree than the new inequalities related to social-demographic factors (Böhnke 2004: 20). The degree of polarisation of

29

perceived social exclusion in Estonia is much higher compared to EU-25 average (table 16) and the socio-demographic factors are significant determinants of social exclusion (e.g. the people over 55 years have reported about perceived social exclusion three times often compared to those 15-24 years old, which is the biggest age-specific difference in the European Union). The feeling of exclusion in Estonia varies between contrasting income and employment categories.

Table 16. Ratios of per cent feeling excluded in contrast social categories Men vs

women Old vs young

Low vs high educated

Non-skilled vs

professional class

Unemployed vs employed

Lowest vs highest income quintile