What’s Hot: Some Recent Policy Developments Affecting Public Health

Recent developments affecting the supply-demand-balance

of acidspar: The buyers view

Dr. Oliver Rhode

LANXESS Deutschland GmbH

Fluorspar Conference November 2011 2

Agenda

1

2

Introduction

Recent developments affecting the demand

Recent developments affecting the supply 3

FSA and other alternatives 4

Summary & Outlook 5

Fluorspar Conference November 2011 3

LANXESS facts and figures

Fluorspar Conference November 2011 4

LANXESS facts and figures

Fluorspar Conference November 2011 5

LANXESS produces hydrofluoric acid in Leverkusen, Germany

Berlin

Frankfurt

Munich

Leverkusen

Fluorspar Conference November 2011 6

Standard specification for acidspar

- Min. 97% CaF2.

- Max. 1% silica (SiO2).

- Max. 1% carbonate (CaCO3).

- Max. 10ppm arsenic.

- Max. 300ppm phosphorus.

- Max. 0.10% sulfur as sulfide or free sulfur.

- Restrictions on iron, lead and other metals.

- Restrictions on organics.

- Particle size: maximum 10% +150 microns,

60% -45 microns.

- Max. 10% water content as filter cake.

Fluorspar Conference November 2011 7

The balance of supply and demand of acidspar is determined by various factors

Supply-Demand-

Balance

Factors affecting the supply

New projects (green-field, brown-field, met-spar upgrading).

Capacity expansion of existing producers.

Export-policy of China.

Factors affecting the demand

Development of the downstream markets (fluorocarbons, fluoro-polymers, AlF3).

Development of HF-market.

Alternatives to replace acidspar or downstream products.

Fluorspar Conference November 2011 8

The domestic market in China is the trigger for the global supply-demand-balance

China has become the largest fluorochemical

production and consumption area.

Although the role of China has changed, it still

dominates the acidspar market.

As long as the domestic demand is strong,

there is no incentive for any producer to

switch to higher grade export material.

Several non-Chinese producers of acidspar

adopt the pricing scheme of Chinese acidspar

exports.

Supply-Demand-

Balance

Fluorspar Conference November 2011 9

Agenda

1

2

Introduction

Recent developments affecting the demand

Recent developments affecting the supply 3

FSA and other alternatives 4

Summary & Outlook 5

Fluorspar Conference November 2011 10

The average annual growth rate for acidspar is estimated at 1,5% per year

Non-Feedstock

Fluorocarbons

Aluminum

Fluoride

Feedstock

Fluorocarbons

Products Demand

• Refrigerants

• Foaming agents

• Aerosols

• steady • 35%

• PTFE

• PVDF

• PEEK

• FPE

• AAGR 2,5% • 15%

• AlF3 • AAGR 2% • 25%

• Uranium enrichment

• Stainless steel pickling

• Gasoline alkylation

• Electronics

• Glass etching

• AAGR 2% • 25%

Others

approx. % of

HF consumption*

Source: Roskill, SRI, own estimates *based on 2.1 mt HF produced in 2010

Fluorspar Conference November 2011 11

Fluorine-based replacements for existing fluorocarbons affects acidspar demand

Environmental pressures are opposing the

application of some fluorochemical products.

Fluorine-based replacements for these

fluorocarbons affects the future acidspar

demand.

Replacement candidates are hydrofluoro-

olefins of the HFO-1234-type for use in

automotive air-conditioning systems and

aerosol applications.

Fluorspar Conference November 2011 12

Production development of fluorocarbons and fluoropolymers in China

0

100

200

300

400

500

600

2002 2005 2008 2010

HCFC-22

HFC-134a

PTFE(HCFC-22)

other fluoro-polymers

kt

Source: CCR, SRI, own estimates

Fluorspar Conference November 2011 13

China’s fluorochemical industry needs technological innovation

– China's fluorochemical industry has largest capacity in the world.

– Industry has developed by relying on resource advantage and simple

production technologies.

– Capacity of high-value-added fluorochemicals is very limited.

– Positioning at the low end of the industrial chain with no differentiation of

products.

– Research of high-end fluorochemical products is weak.

– Chinese government has issued policies to support the development

towards a high-tech industry.

Source: CCR

Fluorspar Conference November 2011 14

China encourages the production of high-value fluorocarbons and fluoropolymers

Acidspar HF Fluorocarbons Fluoropolymers

Current Situation

restricting exports extreme overcapacity overcapacity (primary products)

overcapacity (primary products)

Future Situation

further restrictions (?) moderate overcapacity balanced capacity (shift to advanced products)

Apparent China Strategy

Safeguard domestic availability of (low cost) raw material

Emphasize use in domestic downstream production, reduction of overcapacity

Develop more capacity for domestic & export demand, focus on “high-end” fluorocarbons

Production Chain

Develop more capacity for domestic & export demand, focus on “high-end” fluoropolymers

balanced capacity (shift to advanced products)

Vertical integration

Fluorspar Conference November 2011 15

Total production volume approx. 830 kt

Global production volume of aluminum fluoride in 2010

59%

16%

19%

6%

China

NAFTA

WE

ROW

Source: AIT, own estimates

Fluorspar Conference November 2011 16

Total installed production capacity approx. 2.6 mt

Average plant utilization rate estimated at 80% = 2.1 mt HF produced

Global production capacities for hydrofluoric acid in 2010

54%

15%

11%

11%

9%

China

NAFTA

WE

ROW

CIS

Source: CCR, Roskill, SRI, own estimates

Fluorspar Conference November 2011 17

Recent developments in the production of hydrofluoric acid in China 1/2

– HF production capacity has expanded rapidly.

– Today more than 50 HF producers.

– 2010: HF output approx. 940 kt, up 12% from 2009.

– Average plant utilization rate was 67%.

– Exports of HF accounted for 160 kt, up 48% from 2009.

– Largest export destination was Japan (46% of total HF exports),

followed by Taiwan (19%) and Korea (14%).

– HF producers mainly distributed in the southeast; they are now

beginning to move towards Inner Mongolia.

Fluorspar Conference November 2011 18

Recent developments in the production of hydrofluoric acid in China 2/2

– Consumption will continue to grow at 6% to 7% annually and will reach 1.08

mt in 2015.

– Average plant utilization rate of will remain at 60% to 70%.

– February 2011 - "Access Conditions for Hydrogen Fluoride Industry":

– total HF capacity of any new producer should be at least 50 kt/a, and

– capacity of any new HF plant should be not less than 20 kt/a.

– April 2011 - "Guiding Catalogue for Restructuring of Fluorine Chemical

Industry“:

– construction of new HF plants should be restricted, and

– HF plants with a capacity of less than 5 kt/a should be eliminated.

Fluorspar Conference November 2011 19

Agenda

1

2

Introduction

Recent developments affecting the demand

Recent developments affecting the supply 3

FSA and other alternatives 4

Summary & Outlook 5

Fluorspar Conference November 2011 20

Production capacity of acidspar by country in 2010 according to standard specification

Spain 140 kt

South Africa 300 kt

Namibia 120 kt

Kenya 100 kt

Morocco 100 kt

Mongolia 140 kt

China 2.300 kt

CIS 220 kt

Mexico 500 kt

Germany 30 kt

Mexico 120 kt

Bulgaria 30 kt Mongolia 50 kt

China 500 kt

Source: Roskill, own estimates

out of

specification

within specification,

but captive

within specification,

not captive

3.260 kt

290 kt

1.100 kt

Fluorspar Conference November 2011 21

Historic developments in the production of acidspar in China

– Early 1990s: China has become a major source of supply.

– Production elsewhere declined.

– Domestic demand has grown at an AAGR of 20% since 2000, compared to

less than 1% in Europe or North America.

– Since 2004: Chinese government introduced a number of policies which

reduced exports of acidspar.

– Lower export from China was not balanced by other producers.

Fluorspar Conference November 2011 22

Recent developments in the production of acidspar in China

– April 2010 - "Notification on the 2010 Mining Quotas for Fluorite”:

– national total mining quota for fluorite ore is 11 mt in 2010.

– May 2010 - "Production Quotas of Fluorite for Every Province in 2010”

– national production quota for acidspar is 2.44 mt.

– The actual output of acidspar exceeded the quota.

– June 2010: fluorite resource tax increased from 3 RMB/t to 20 RMB/t.

– Reduction of the 2011 national total fluorite mining quota by 500 kt.

Fluorspar Conference November 2011 23

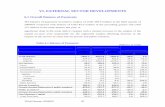

361386

215

575

483

564

422

252280

301

193

173

0

100

200

300

400

500

600

700

2006 2007 2008 2009 2010 2011

150

200

250

300

350

400

450

500

Chinese annual exports of acidspar and average FOB-price

Volume

[kt] FOB-Price

[USD/t]

Jan.-Sep. Source: CCR

Fluorspar Conference November 2011 24

Where can we source new acidspar supplies in the future?

Additional potential volume of acidspar of more than 1 mt

Fluorspar Conference November 2011 25

Agenda

1

2

Introduction

Recent developments affecting the demand

Recent developments affecting the supply 3

FSA and other alternatives 4

Summary & Outlook 5

Fluorspar Conference November 2011 26

Will flurosilicic acid contribute to the supply-demand-balance of acidspar?

– Main fluorine resources are fluorite, phosphate rock, apatite, cryolite,

sellaite, sodium fluoride and bastnaesite.

– Fluorite supplies around 92% of global fluorine demand.

– Phosphate rock contains up to 3.5% fluorine, and it accounts for more

than 90% of the world's fluorine reserves.

– One ton of wet-process phosphoric acid (WPA) can yield approximately

50 - 60kg flurosilicic acid (FSA).

– A potential 3.5 mt of equivalent acidspar would be available as by-product

FSA.

Fluorspar Conference November 2011 27

Will flurosilicic acid contribute to the supply-demand-balance of acidspar?

– High capital and processing costs have militated against FSA as acidspar

replacement.

– First HF plant using FSA opened in China in April 2008.

– Approx. 300 kt of acidspar equivalent, in the form of FSA, is used in AlF3

manufacture.

– Around 150 - 200 kt of FSA are used in water fluoridation.

– Remainder is generally neutralised, discharged, ponded or pumped to sea.

Fluorspar Conference November 2011 28

Neither FSA nor another raw material will replace acidspar in the next couple of years

– Increased utilisation of FSA is unlikely to progress significantly.

– China promotes the further development of HF-production from FSA.

– A few thousand tons per year of synthetic acidspar is recovered - primarily

from uranium enrichment, but also from gasoline alkylation and stainless

steel pickling.

– Aluminum smelting dross, borax, calcium chloride, iron oxides, manganese

ore, silica sand, and titanium dioxide have been used as substitutes for

acidspar fluxes.

– Neither FSA nor another raw material will replace acidspar in he next

couple of years.

Fluorspar Conference November 2011 29

Agenda

1

2

Introduction

Recent developments affecting the demand

Recent developments affecting the supply 3

FSA and other alternatives 4

Summary & Outlook 5

Fluorspar Conference November 2011 30

Uncertainty and turbulence in the markets

- Health of economies in Europe,

- United States debt,

- China dilemma: low inflation rate vs.

GDP growth.

The further development of the global

economy depends on these topics, and

consequently the development of the

fluorochemical industry.

Fluorspar Conference November 2011 31

Will demand for acidspar outstrip supply in the next five years?

After the worldwide recession, acidspar

markets recovered in 2010, and continued to

grow in 2011.

Supply was tight in the middle of 2011, now

the situation changed, acidspar is readily

available.

Supply and demand are in balance – there is

no structural deficit of acidspar.

No significant acidspar supply-demand-gap is

expected in the next couple of years.

Supply-Demand-

Balance

Fluorspar Conference November 2011 32

Non-Chinese

“Yes“

Chinese

“No“

Do you believe China will become a net importer of acidspar in the next five years?

Results of a recent non-representative

survey

We asked Chinese and non-Chinese

market participants:

“Do you believe China will become a net

importer of acidspar in the next five years?”

All Chinese answered “No”.

In contrast, the non-Chinese believe “Yes”.

Thank You

for Your Attention