Recent Changes in Company Law By Mahavir Lunawat.

26

Recent Changes in Company Law By Mahavir Lunawat

-

Upload

bernice-karen-booker -

Category

Documents

-

view

218 -

download

0

Transcript of Recent Changes in Company Law By Mahavir Lunawat.

Recent Changes in Company Law

By Mahavir Lunawat

Outline

• History – Sequence of Milestone Events

• Developments since 2005 till date – Amendments– Significant Judicial Pronouncements – Proposed Law

Sequence of Milestone Events• Scams in US• US Sarbanes Oxley Act, 2002• SEC Rules under SoX• Naresh Chandra Committee on Corporate Governance• Companies Amendment Bill, 2003• Concept Paper on Company Law• White Paper on Modern Company Law, UK• Company Law Reform Bill, UK• J J Irani Committee• Concept Paper on LLP Law

Amendments

SEBI Law• Implementation of revised Clause 49

– Independent Directors– Subsidiary Monitoring– Shareholders’ Prior approval for compensation / stock options to

NEDs– Audit Committee – Eligibility Criteria, mandatory review etc.– Statutory Compliance Review– Risk Management Procedure– Code of Conduct for Directors & Senior Management– CEO and CFO Certification– Non-Mandatory : Term of Independent Director, Whistle

Blower Policy etc.

SEBI Law• SEBI (DIP) Guidelines, 2000 - Book Building Norms

– Enhancing allocation category for RIIs

In case of book built issues with mandatory allocation of 60% to QIBs under Rule 19(2)(b), the respective figures shall be 30% for RIIs and 10% for NIIs.

– Redefining “Retail Individual Investors” : RIIs can apply for shares up to a maximum amount of Rs.1,00,000/- as against the extant limit of Rs.50,000/-

– Reducing the bidding period : The bidding period has been reduced from current 5 – 10 days (including holidays) to 3 -7 working days

– Timing of disclosure of Price Band / Floor Price in case of listed companies : Listed issuers making a follow-on public issue may disclose the price band /floor price atleast one day before bid opening

[SEBI/CFD/DIL/DIP/15/20, dated March 29, 2005]

Category From To

RIIs 25 35

Non Institutional Investors (NIIs) 25 15

QIBs 50 50

SEBI Law

• SEBI (DIP) Guidelines, 2000 - Book Building Norms

– Changes re. QIB allotment • Out of the existing 50% portion available for QIBs,

5% will be specifically available for Mutual Funds registered with SEBI. However, the Mutual Funds will also be eligible for allotment in the remaining 45% portion

• QIBs will bring at least 10% margin (calculated on application money) while submitting the bids

• The allotment of shares to QIBs will be on proportionate basis

SEBI Law

• SEBI Press Release (no. 108/2005 dated August 26, 2005) on Minimum Public Shareholding – All listed companies to maintain atleast 25%

shareholding with public for continuous listing. However, companies permitted to make an IPO of atleast 10% to public under Rule 19(2)(b) to maintain min. 10% only

– Listed companies, not complying with the min. public holding requirement to be given a period of 2 years for compliance

– Government companies, infrastructure companies and companies registered with BIFR to be exempted

SEBI Law

• Review of Demat Charges – Effective 9-1-2006, no charges will be levied by a

depository on a DP and by a DP on a Beneficiary Owner (BO) when a BO transfers his account to another branch of the same DP or to another DP of the same depository or another depository. [MRD/DoP/Dep/Cir-22/05 dated 9-11-2005]

– SEBI vide Circular MRD/DoP/SE/Dep/Cir-4/2005 dated January 28, 2005, had already waived the following charges effective February 1, 2005 –

• charge towards opening of a BO Account except for applicable statutory charges

• charge for credit of securities into BO Account • custody charge

SEBI Law

• Guidelines for Execution of Block Deals on the Stock Exchanges [Circular MRD/DoP/SE/Cir-19/05 dated 2-9-2005]– A trade, with a min. quantity of 5,00,000 shares or value of Rs.5 crore,

through a single transaction, will constitute a “block deal” – Block deals will be executed on a separate trading window - for a limited

period of 35 minutes a day from 9.55 am to 10.30 am – Orders may be placed at a price not exceeding +/- 1% from the ruling

market price or previous day's closing price as applicable – Block deals will need to be settled in delivery and will not be squared off

or reversed – Stock exchanges will make public the information on block deals such as

the scrip, client, quantity of shares bought/sold, traded price etc. on the same day, after the market hours.

• Block delas will be in addition to the disclosure of ‘bulk deals’. In terms of SEBI Circular SEBI/MRD/SE/Cir -7/2004 dt. 14-01-2004, a“bulk” deal constitutes of “all transactions in a scrip (on an exchange) where total quantity of shares bought/sold (in one or more transactions) is more than 0.5% of the no. of equity shares of the company.

SEBI Law• SEBI Press Release dated Dec 30, 2005

(Note : These are policy announcements based on decisions of the Board and do not reflect change in the existing legal framework until the relevant amendments are effected through issue of circulars.)

– Public issue refunds through Electronic Clearing Scheme (ECS) – Introduction of optional grading of IPOs by credit rating agencies – Rationalizing disclosure requirements for further public offers and

rights issues – Common platform for electronic filing and dissemination of corporate

information – Amendment to Takeover Regulations – Amendment to SEBI (Delisting of Securities) Guidelines– Unique Identification Number (UIN) : To resume fresh registrations

for obtaining UIN under MAPIN Regulations

SEBI Law

• Amendment to Takeover Regulations– Restrictions on market purchases, preferential

allotments as in the Takeover Regulations to be removed.

– Outgoing shareholder (promoter) can sell entire stake to incoming acquirer in case of takeover.

– Shareholders holding more than 55% would be able to make further acquisitions subject to making open offer

SEBI Law

• Clarifications on the revised Clause 49 of the Listing Agreement (Effected vide SEBI Circular SEBI/CFD/DIL/CG/1/2006/13 dt. January 13, 2006) – Max time gap between two Board meetings has

been increased from 3 months to 4 months – Sitting fees paid to non-executive directors as

authorized by the Companies Act, 1956 would not require shareholders’ approval

– Certification of internal controls and internal control systems by CEO/ CFO would be for the purpose for financial reporting

Euro Issue - 2005 First Amendment

• Dated Aug. 31, 2005• Eligibility of issuer [New Paragraphs 3(1)(A) and 3(1)(B)]

1. An Indian company, which is not eligible to raise funds from the Indian Capital Market will not be eligible to issue ADRs/GDRs/FCCBs under the Scheme.

2. An Indian company which has been restrained from accessing the securities market by SEBI will not be eligible to issue ADRs/GDRs/FCCBs under the Scheme.

3. An unlisted Indian company issuing GDRs/ADRs/FCCBs will be required to simultaneously list its shares on one or more of the recognized Stock Exchanges in India

Euro Issue - 2005 First Amendment

• Eligibility of subscriber : Paragraph 3(1)(C), inserted by the amended Scheme, provides that – the erstwhile OCBs which are not eligible to

invest in India through the portfolio route and – entities prohibited to buy, sell or deal in

securities by SEBI

will not be eligible to subscribe to Euro Issues.

Euro Issue - 2005 First Amendment• Pricing

– The amendments to Paragraph 5 of the Scheme provides that ADRs / GDRs issued by listed companies should be made at a price not less than the higher of the following two averages :

1. The average of the weekly high and low of the closing prices of the related shares quoted on the stock exchange during the 6 months preceding the relevant date;

2. The average of the weekly high and low of the closing prices of the related shares quoted on a stock exchange during the two weeks preceding the relevant date.

The “relevant date” means the date 30 days prior to the date on which the shareholders’ meeting is held, under section 81(IA) of the Companies Act.

– Conversion price of the FCCBs will also be in accordance with the above provisions.

– The pricing of ADRs/GDRs as well as the conversion price of FCCBs of unlisted companies should be in accordance with the RBI Regulations notified under the FEMA, which talks of CCI Valuation Guidelines.

Euro Issue - 2005 Second Amendment• The applicability of the amended Scheme has been relaxed by the

Ministry for those companies which have already taken effective steps and thereby incurred costs before August 31, 2005, provided these companies complete their issues latest by December 31, 2005.

• “Effective steps,” for the above purpose, will mean the following :– That the company has completed due diligence and filed offering

circular in the overseas exchange(s); or– That approval of overseas exchange(s) has been obtained; or– That the payment of listing fees is made; or– That the approval of the Reserve Bank of India, where applicable, for

meeting issue related expenses has been obtained.• Private placements of issues, where no offering circular was placed

before the overseas exchange(s), would not qualify for “effective steps” .

Euro Issue – 2005 Third Amendment• Dated November 17, 2005

• The companies going in for an offering in the domestic market and a simultaneous or immediate follow on offering (within 30 days of domestic issue) through ADR/GDR issues wherein GDRs/ADRs are priced at or above the domestic price, would be exempt from the requirement of the revised pricing guidelines. Such companies will have to take SEBI’s approval for such issue, which will specify the percentage to be offered in the domestic and ADR/GDR markets.

• It is also clarified that in terms of the First Amendment, 2005, unlisted companies, which have already issued GDRs/FCCBs and are to list in the domestic market, would be required to do so by March 31, 2006.

• All other conditions of the First Amendment dated August 31, 2005 would continue to be applicable.

Significant Judicial Pronouncements

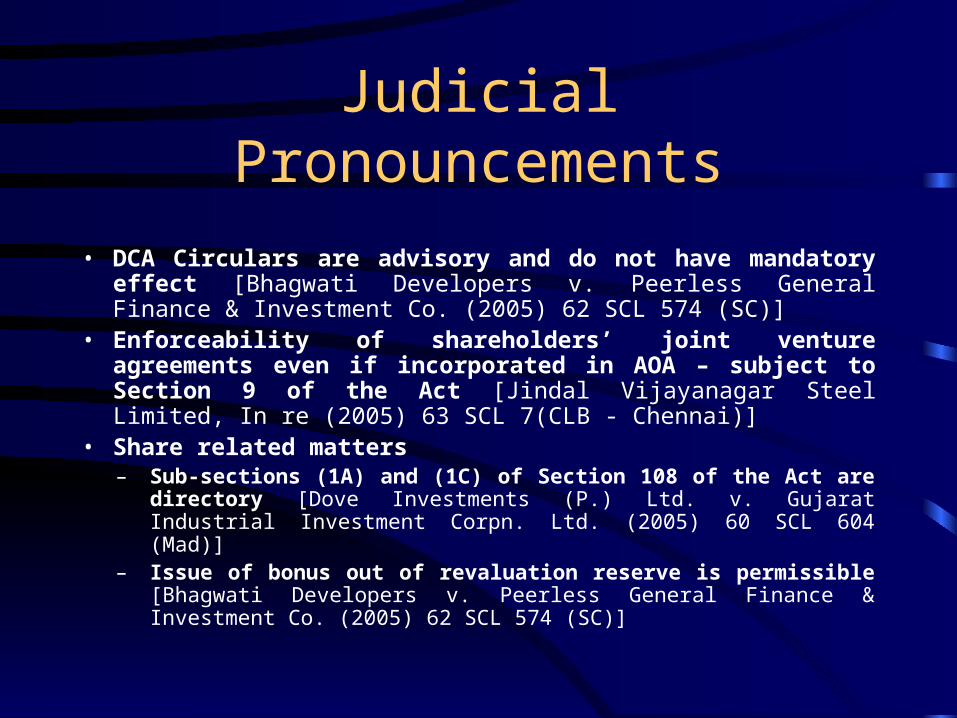

Judicial Pronouncements

• DCA Circulars are advisory and do not have mandatory effect [Bhagwati Developers v. Peerless General Finance & Investment Co. (2005) 62 SCL 574 (SC)]

• Enforceability of shareholders’ joint venture agreements even if incorporated in AOA – subject to Section 9 of the Act [Jindal Vijayanagar Steel Limited, In re (2005) 63 SCL 7 (CLB - Chennai)]

• Share related matters – Sub-sections (1A) and (1C) of Section 108 of the Act are directory

[Dove Investments (P.) Ltd. v. Gujarat Industrial Investment Corpn. Ltd. (2005) 60 SCL 604 (Mad)]

– Issue of bonus out of revaluation reserve is permissible [Bhagwati Developers v. Peerless General Finance & Investment Co. (2005) 62 SCL 574 (SC)]

Judicial Pronouncements

• Corporate Directors not liable merely because of being directors– For dishonour of cheque for insufficiency, etc.,

of funds in account – NI Act [S.M.S. Pharmaceuticals Ltd. v. Neeta Bhalla 63 SCL 93 (SC); S.V. Mazumdar v. Gujarat State Fertilizers Co. Ltd. (2005) 62 SCL 116 (SC); CDR. Shekhar Singh v. N.K. Wahi (2005) 57 SCL 9 (Del)]

– For payment of wages under the Payment of Wages Act [P.C. Agarwala v. Payment of Wages Inspector, MP (2005) 63 SCL 109 (SC)]

Judicial Pronouncements

• Auditors’ duties re. report about disqualification of a director under Section 274(1)(g) [Pawan Jain v. Hindusthan Club Ltd. (2005) 62 SCL 610 (Cal)]

• A corporation or company can be prosecuted for any offence punishable under law [Standard Chartered Bank v. Directorate of Enforcement (SC) 2005]

• Meetings - POA is a valid proxy [Gharda Chemicals Ltd. v. Jer Rutton Kavasmaneck (2005) 63 SCL 222 (Bom)]

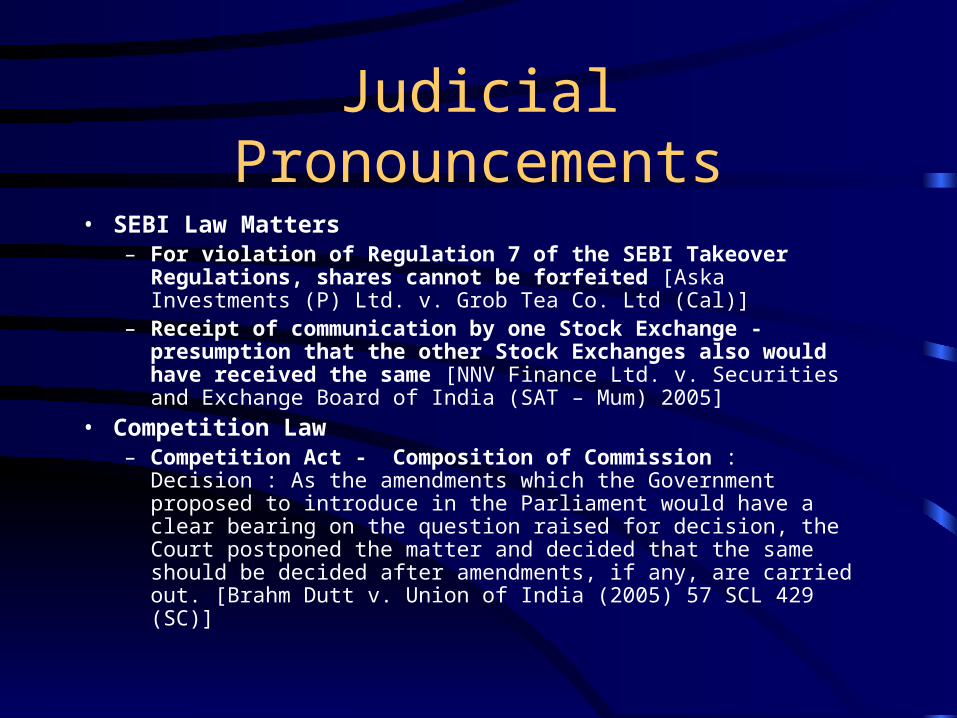

Judicial Pronouncements

• SEBI Law Matters– For violation of Regulation 7 of the SEBI Takeover

Regulations, shares cannot be forfeited [Aska Investments (P) Ltd. v. Grob Tea Co. Ltd (Cal)]

– Receipt of communication by one Stock Exchange - presumption that the other Stock Exchanges also would have received the same [NNV Finance Ltd. v. Securities and Exchange Board of India (SAT – Mum) 2005]

• Competition Law– Competition Act - Composition of Commission :

Decision : As the amendments which the Government proposed to introduce in the Parliament would have a clear bearing on the question raised for decision, the Court postponed the matter and decided that the same should be decided after amendments, if any, are carried out. [Brahm Dutt v. Union of India (2005) 57 SCL 429 (SC)]

Proposed Law

Committee Reports / Concept Papers

• Concept Rules on New Company Law• J J Irani Committee on Company Law• M H Kania Committee on SEBI Act• O P Vaish Committee on Streamlining

Prosecution Mechanism under Company Law• Concept Paper on LLP Law• Other Committees like Capoor

Committee on MAPIN, Lahiri Committee on FII investments etc.

Thank You !

![Bhagwan Mahavir Swami[1]](https://static.fdocuments.us/doc/165x107/552244c04a79595d5e8b4812/bhagwan-mahavir-swami1.jpg)