Recent Canadian Developments - Canadian Tax Foundation PPTS/4 - Recent Canadian... · 2017 IFA...

61

Tuesday April 25 &Wednesday April 26 MetroToronto Convention Centre Recent Canadian Developments Moderator: Michael Kandev, Davies Ward Phillips & Vineberg LLP, Montreal Presenters: Kim Maguire, Borden Ladner Gervais LLP, Vancouver Carrie Smit, Goodmans LLP, Toronto Christopher Steeves, Fasken Martineau DuMoulin LLP, Toronto Julie Vezina, PricewaterhouseCoopers LLP, Montreal YIN Rapporteur: Audrey Dubois, KPMG LLP, Montreal

Transcript of Recent Canadian Developments - Canadian Tax Foundation PPTS/4 - Recent Canadian... · 2017 IFA...

Tuesday April 25 & Wednesday April 26 Metro Toronto Convention Centre

Recent CanadianDevelopments

Moderator: Michael Kandev, Davies Ward Phillips & Vineberg LLP, Montreal

Presenters:Kim Maguire, Borden Ladner Gervais LLP, VancouverCarrie Smit, Goodmans LLP, TorontoChristopher Steeves, Fasken Martineau DuMoulin LLP, TorontoJulie Vezina, PricewaterhouseCoopers LLP, Montreal

YIN Rapporteur: Audrey Dubois, KPMG LLP, Montreal

LegislativeDevelopments

2017 IFA International Tax Conference

Recent Canadian Developments

K. Maguire

● Extension of base erosion rules to foreign branches ofCanadian life insurers

● Current rules apply to include in FAPI income frominsurance of Canadian risks of a controlled foreignaffiliate

● New rules in 138 and 95(2)

3

Budget 2017 - Life Insurance Branches

2017 IFA International Tax Conference

Recent Canadian Developments

K. Maguire

● Applicationo ≥10% gross premium income earned by foreign branch is

premium income in respect of Canadian risks

o Deem insurance of Canadian risks to be part of Canadiantaxpayer’s business and policies to be policies in Canada

● Anti-avoidance ruleso Insurance swaps or ceding of Canadian risks

o Foreign branch insured foreign risks and purpose test

● Apply to taxations years of Canadian taxpayersbeginning on or after March 22, 2017

4

Budget 2017 - Life Insurance Branches

2017 IFA International Tax Conference

Recent Canadian Developments

K. Maguire

● Applies on division of a foreign corporation

● Current: deems “original” foreign corporation to confera benefit on shareholder

● Amendment: If shares received by shareholders on apro rata basis…o pro rata distribution equal to FMV of shares 90(2)

dividend or 90(3) capital reduction

o No gain/loss to foreign corporation b/c share distribution

o Cost of new shares = FMV under 52(2)

o Deemed FMV proceeds and cost to foreign corporations

● Application: divisions occurring after October 23, 2012

5

Foreign Division – 15(1.4)(e)

2017 IFA International Tax Conference

Recent Canadian Developments

K. Maguire

● Structure of new ruleso 91(1.1) sets out requisite conditions for 91(1.2)

application

o 91(1.2) operative rule for taxpayer and “connected”corporations and partnerships

o 91(1.3) meaning of “connected”

o 91(1.4) and (5) circumstances in which taxpayers mayelect for 91(1.2) to apply

o Related amendments in Reg. 5907(8) and (8.1)

● In force July 12, 2013

6

Stub Period FAPI

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● Ss. 212.3(1) is amended to expand the application provision.

● Previously applied to a investment by a corporation resident inCanada (CRIC) in a non-resident corporation if:o the non-resident corporation is (or becomes as part of series) an FA of

CRIC; and

o CRIC is (or becomes as part of series) controlled by a non-residentcorporation.

FAD Amendments

NRParent

CRIC

FA

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● Now rules apply to an investment by a CRIC in a non-resident corporation if:o the non-resident corporation is (or becomes as part of

series) an FA of CRIC or an FA of a corporation that doesnot deal at arm’s length with CRIC (the “OCC”) (para.212.3(1)(a)); and

o CRIC or OCC is (or becomes as part of series) controlledby a non-resident corporation (para. 212.3(1)(b)).

FAD Amendments

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

Canco 1

NRParent

Canco 2

FAInvestment

FAD Amendments

● Mischief:

● Canco 2 is the CRIC making the investment, Canco 1 is the OCC.

● Does amendment to para. 212.3(1)(a) address this? Why needamendment to para. 212.3(1)(b)?

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● OCC is defined “a corporation that does not deal atarm’s length with the CRIC (in this subsection referredto as the “other Canadian corporation”)”

o Must an OCC be a Canadian resident corporation?Explanatory notes suggest yes.

o Does this include para. 251(5)(b) rights? Question offact?

FAD Amendments

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

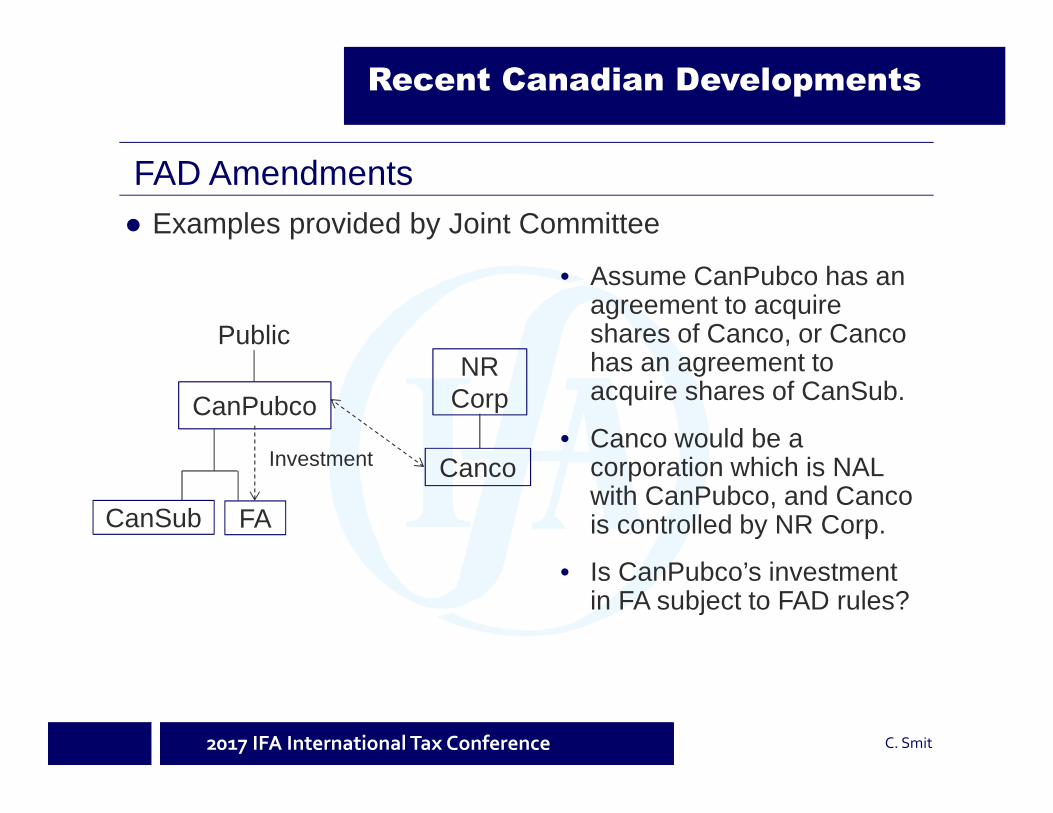

● Examples provided by Joint Committee

• Assume CanPubco has anagreement to acquireshares of Canco, or Cancohas an agreement toacquire shares of CanSub.

• Canco would be acorporation which is NALwith CanPubco, and Cancois controlled by NR Corp.

• Is CanPubco’s investmentin FA subject to FAD rules?

FAD Amendments

Public

CanPubco

NRCorp

Canco

CanSub FA

Investment

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

• CanSub is a corporationwhich is NAL with Canco,and is controlled byUSco.

• Is Canco’s investment inFA subject to FAD rules?

FAD Amendments

Brother US Brother Canada

USco Canco

Investment

CanSub FA

• Issues arise due to amendment to para. 212.3(1)(b).

• Should OCC in para 212.3(1)(b) be an OCC in which thesubject corporation is an FA?

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

• Assume CanHoldco isfactually NAL withCanPubco.

• Do the FAD rules apply toCanPubco’s investment inFA?

• Changes FAD test from anon-resident de jurecontrol test to a de factocontrol test.

FAD Amendments

NR Corp

CanHoldcoPublic

60%40%

CanPubco

Investment

FA

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

Canco 1(CRIC)

NRCorp

Canco 2(OCC)

FAInvestment

Mr. X

FAD Amendments

● Consequence is deemed dividend paid by the CRIC to the non-resident parent

● Non-resident parent may not own any shares of CRIC:o Treaty rate

o PUC reduction

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● Joint Committee suggested eliminating amendmentsand replacing with a deeming rule:o “For the purposes of this section, if at any time a non-

resident corporation is a foreign affiliate of a particularcorporation resident in Canada, the non-residentcorporation shall at that time be deemed to be a foreignaffiliate of every corporation resident in Canada that is atthat time related to the particular corporation (otherwisethan because of a right referred to in paragraph251(5)(b))”.

● Similar to ss.17(13) and para. 95(2)(n).

FAD Amendments

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● December 23, 2016 comfort letter issued byFinance.

● Will recommend an amendment to paragraph95(2)(b) to provide a rule similar to clause95(2)(a)(ii)(D).

Para 95(2)(b) Comfort Letter

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

Para 95(2)(b) Comfort Letter

• Foreign Manager providesmanagement services toOpco and Foreign Holdcopays for those services.

• Service fee is deductible incomputing ForeignHoldco’s FAPI – causesFAPL.

• Service fee is FAPI toForeign Manager underpara 95(2)(b).

• If Service fee were paid byForeign Opco, would notbe FAPI.

Canco

ForeignManager

(FA 1)

ForeignOpco(FA 3)

ForeignHoldco(FA 2)

Service Fee

OtherShareholders

ActiveBusiness

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● Comfort letter recommends that subclause95(2)(b)(i)(B)(I) not apply in respect of income of an FA(FA 1) from providing services, if conditions analogousto those in clause 95(2)(a)(ii)(D) are met:o income is derived by FA 1 from amounts paid by another

FA (FA 2) in consideration for services;

o amount paid is for expenditures incurred by FA 2 for thepurpose of gaining or producing income from property;

o property is shares of another FA (FA 3) which are excludedproperty; and

o Canadian taxpayer has a QI in FA 1, FA 2 and FA 3.

● Any FAPL of FA 2 would be eliminated.

Para 95(2)(b) Comfort Letter

JudicialDevelopments

2017 IFA International Tax Conference

Recent Canadian Developments

K. Maguire

● 2017 FCA 39

● Factso 2005/6: Quebec company received dividends from

Barbados and Cyprus subsidiaries

o 2010/11: Rectification orders from Barbados and Cypruscourts declaring payments were loans not dividends

o Informed CRA after orders obtained

● Issue: Whether CRA is bound to treat payments asloans?

20

Canadian Forest Navigation Co. Ltd. v The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

K. Maguire

● Tax Courto Barbadian and Cypriot court orders did not bind CRA

because not “homologated” by a Quebec court

● Federal Court of Appealo Lack of homologation irrelevant

o Barbadian and Cypriot court orders are proof thatcorporate resolutions have been rectified

o BUT “what remains to be determined is the foreignorders’ effect vis-à-vis the Minister … depend on theevidence adduced by the parties… weight ascribed to theforeign orders as facts… determinations for the TaxCourt”

21

Canadian Forest Navigation Co. Ltd. v The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

K. Maguire

● Tax is an accessory systemo See e.g. Lagueux & Frères 74 DTC 6569 (FCTD) and

Perron 60 DTC 554 (TAB)

● Form matters?

● No mention of Fairmont

22

Canadian Forest Navigation Co. Ltd. v The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● Upcoming TCC case.

● Is Alta Energy Luxembourg S.a.r.l. (Luxco) entitled totreaty benefits on the sale of shares which are TCP?

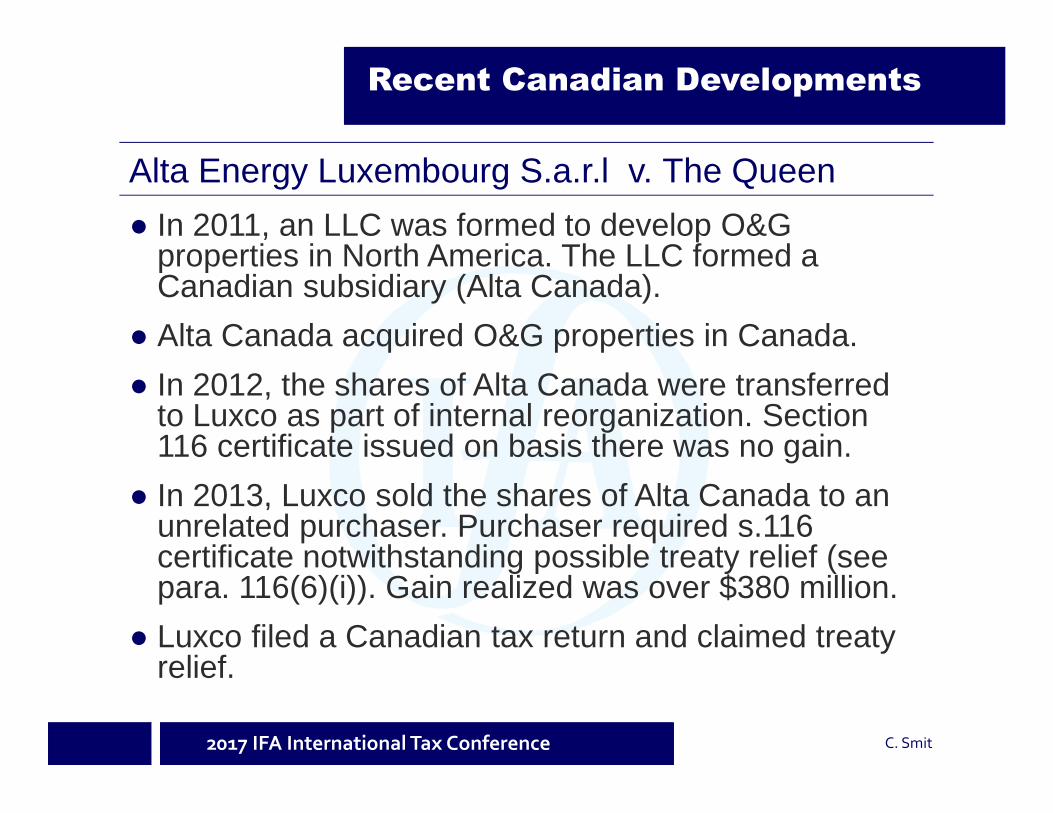

Alta Energy Luxembourg S.a.r.l v. The Queen

Luxco

AltaCanada

Sale

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● In 2011, an LLC was formed to develop O&Gproperties in North America. The LLC formed aCanadian subsidiary (Alta Canada).

● Alta Canada acquired O&G properties in Canada.

● In 2012, the shares of Alta Canada were transferredto Luxco as part of internal reorganization. Section116 certificate issued on basis there was no gain.

● In 2013, Luxco sold the shares of Alta Canada to anunrelated purchaser. Purchaser required s.116certificate notwithstanding possible treaty relief (seepara. 116(6)(i)). Gain realized was over $380 million.

● Luxco filed a Canadian tax return and claimed treatyrelief.

Alta Energy Luxembourg S.a.r.l v. The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● Lux Treaty

oArticle 13(4) taxes gain from sale of shares if valueof shares is derived principally from immovableproperty situated in Canada.

o immovable property does not include property “inwhich the business of the company was carried on”.

Alta Energy Luxembourg S.a.r.l v. The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● CRA claims that Alta Canada’s O&G propertieswere not properties in which its business wascarried on:

oNo employees

oManagement services contracted to a US LLC

oMinimal drilling activity

Alta Energy Luxembourg S.a.r.l v. The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● CRA’s Reply asserts that Alta Canada did not “exploitits assets on a regular, continuous and substantialbasis”, and its minimal activities were only “windowdressing”.

● Prior CRA positions apply exception to mines, timberproperties, motels, manufacturing plants, etc.:o “Generally, mineral and timber rights that are beneficially

owned by a company and which are actively exploited bythe company in the conduct of its business would beconsidered property … in which the business of thecompany was carried on.” (CRA T.I. 9703965)

Alta Energy Luxembourg S.a.r.l v. The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● CRA also asserts that Luxco was not a resident ofLuxembourg for purposes of the Lux Treaty.

● Under Lux Treaty, a resident is any person who, underthe laws of Luxembourg, is liable to tax therein byreason of domicile, residence, place of management,etc.

● No substance requirement.

Alta Energy Luxembourg S.a.r.l v. The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

C. Smit

● CRA also asserts GAAR:o transfer to Luxco was undertaken to avoid Canadian tax

o misuse of provisions of Act and Lux Treaty.

● FCA decision in R. v. MIL (Investments) S.A.:o did not find object and purpose underlying Article 13 of

Lux Treaty in order to justify departure from plain words

o rejected double non-taxation argument.

Alta Energy Luxembourg S.a.r.l v. The Queen

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

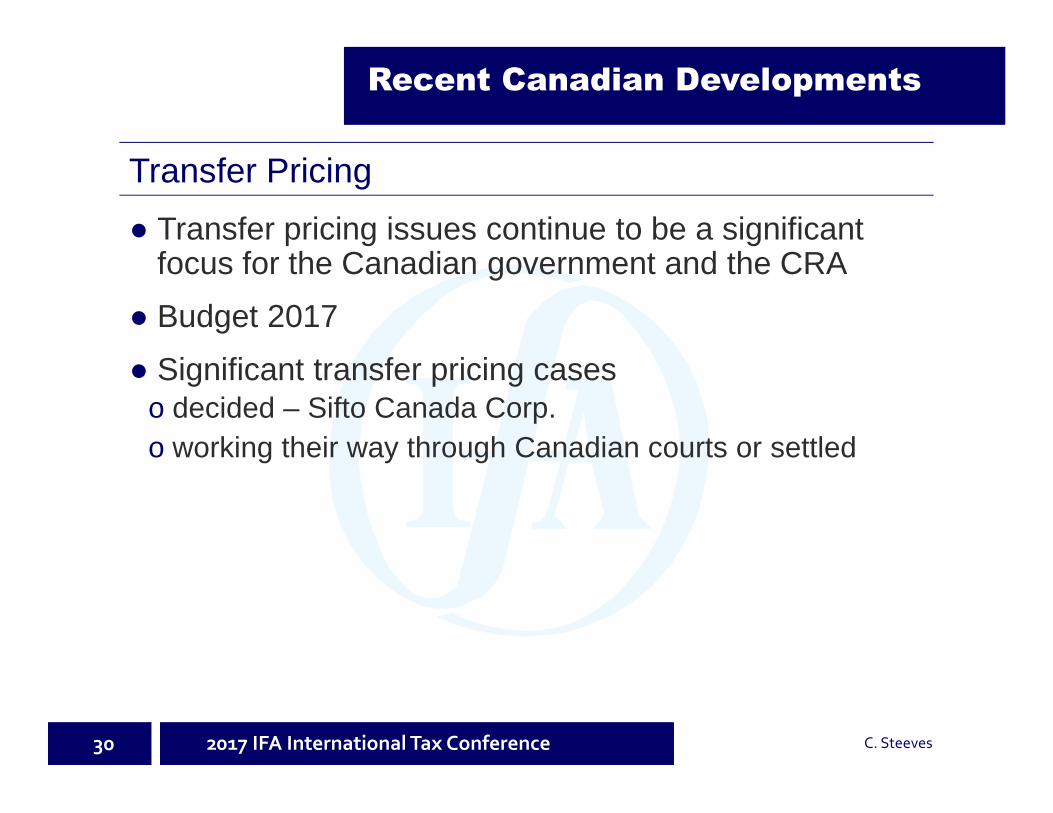

● Transfer pricing issues continue to be a significantfocus for the Canadian government and the CRA

● Budget 2017

● Significant transfer pricing caseso decided – Sifto Canada Corp.

o working their way through Canadian courts or settled

30

Transfer Pricing

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Budget 2017 refers to how newly required country-by-country reports for multinational enterprises will“enable [tax authorities] to better assess high-levelavoidance risks such as the potential for mispricing oftransactions between entities of the group in differentjurisdictions”

● Budget 2017 also states that CRA is now applying therevised international guidance on transfer pricingarising from the OECD BEPS project as theserevisions provide an “improved interpretation” of thearm’s length principle found in Canada’s tax laws

31

Transfer Pricing – Budget 2017

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

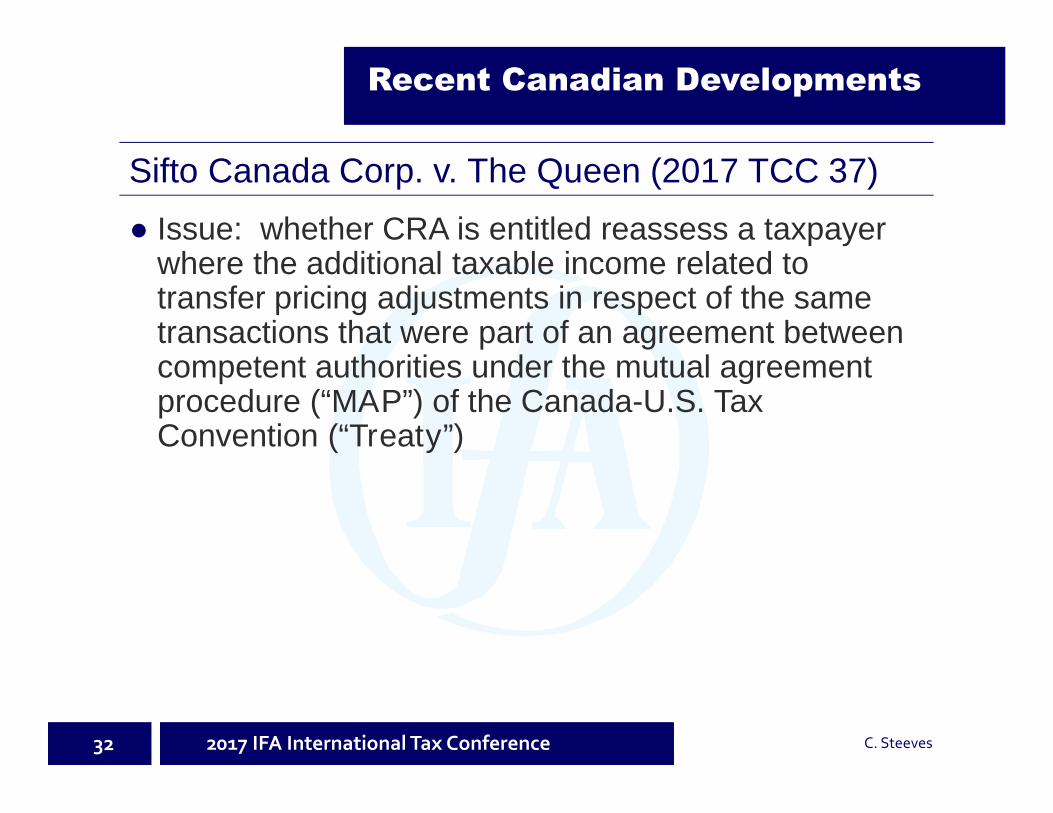

● Issue: whether CRA is entitled reassess a taxpayerwhere the additional taxable income related totransfer pricing adjustments in respect of the sametransactions that were part of an agreement betweencompetent authorities under the mutual agreementprocedure (“MAP”) of the Canada-U.S. TaxConvention (“Treaty”)

32

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● In 2007, Sifto Canada made a voluntary disclosurereporting additional income for taxation years from2002 to 2006 (approx. $13 million in the aggregate)

● Taxpayer’s new transfer pricing methodology resultedin increased profits relating to the sale of rock salt bySifto Canada to a related U.S. corporation (“NASC”)

● CRA accepted and the voluntary disclosure and inApril, 2008, CRA issued reassessments for the 2002to 2006 years (“Reassessments”) reflecting theadditional income reported by Sifto Canada as part ofthe voluntary disclosure

33

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Without a corresponding reduction in the income ofNASC for U.S. tax purposes, the Reassessmentswould result in double taxation

● Sifto Canada requested assistance from theCanadian competent authority (“CCA”) for relief fromdouble taxation under Articles IX (Related Persons)and XXVI (MAP) of the Treaty

● CCA and the U.S. competent authority (“USCA”)correspondence and discussions about the SiftoCanada request began in August, 2008

34

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

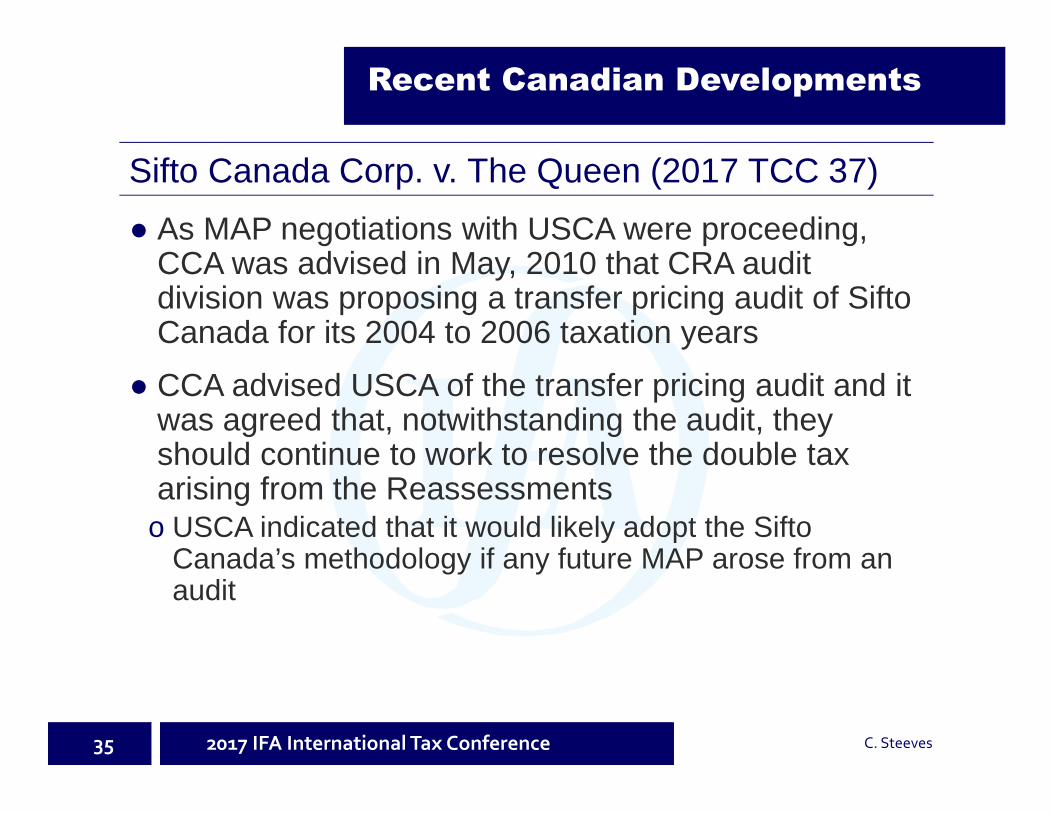

● As MAP negotiations with USCA were proceeding,CCA was advised in May, 2010 that CRA auditdivision was proposing a transfer pricing audit of SiftoCanada for its 2004 to 2006 taxation years

● CCA advised USCA of the transfer pricing audit and itwas agreed that, notwithstanding the audit, theyshould continue to work to resolve the double taxarising from the Reassessmentso USCA indicated that it would likely adopt the Sifto

Canada’s methodology if any future MAP arose from anaudit

35

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● In December, 2010, CCA and USCA reached anagreement for the avoidance of double taxation inconnection with Sifto Canada transfer pricingadjustments from the Reassessments for the 2003 to2006 yearso reduced the income of NASC for U.S. tax purposes, and

o allowed NASC to pay Sifto Canada US$11 million free ofU.S. withholding tax

● Sifto Canada was advised of the MAP agreement andaccepted its terms which were in accordance with thetransfer pricing adjustments in its voluntary disclosure

36

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● On August 1, 2012, CRA reassessed Sifto Canada inrespect of its 2004 to 2006 taxation yearso Additional income of $135 million was the result of

transfer pricing adjustments by CRA in respect of the saleof rock salt to NASC

● Sifto Canada objected to and appealed these newreassessments to the Tax Courto argued that the completed competent authority

proceedings resulted in a binding agreement with CRAthat fixed the transfer price for the sale of salt to NASC

● Crown argued that there was no agreement with SiftoCanada and, even if there was, the CRA was obligedunder the ITA to reassess, once it was in possessionof facts revealed by the audit

37

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Did the Sifto Canada’s acceptance of the MAPagreements constitute a settlement agreementbetween Sifto Canada and CRA?

● Owen J.: to be considered a settlement agreementthe following requirements must be met (Apotex Inc.v. Allergan, Inc. – 2016 FCA 155):o Mutual intention to create legal relations

o Mutual consideration

o Certainty of terms

● Tax Court concluded that these requirements weremet in the circumstances; therefore, the MAPagreement constituted settlement agreements

38

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Is the CRA required to reassess Sifto Canadanotwithstanding the settlement agreements?

● Crown argued the CRA has a statutory duty to assessthe amount taxable on the facts as it has determined(Galway – [1974] 1 F.C. 600, FCA)

● Owen J. states that decisions in Galway and CIBCWorld Markets (2012 FCA 3) allow the CRA to enterinto a binding settlement agreement unless it is“indefensible on the facts and the law”

39

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● In this case, the transfer prices adopted by Sifto Canadaand accepted by the USCA were at the low end of thecomparable range determined using the TNMM

● CCA and USCA agreed the transfer prices were inaccordance with the arm’s length principle under Article IXof the Treaty

● Tax Court stated that it was reasonable to assume that theIRS would not have agreed to Sifto Canada’s transferpricing methodology if it was indefensibleo Supported further by the fact that the IRS indicated that it would

have insisted on using Sifto Canada’s transfer prices even if anew MAP was initiated

● Tax Court concluded that the MAP agreements werebinding on the CRA as settlement agreements with SiftoCanada

40

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Owen J. indicated that even if his conclusion is wrong, theMAP agreements were still binding by virtue of Article XXVIof the Treaty

● “By reassessing [Sifto Canada] to increase the incomeattributed to Canada from the relevant transactions, theMinister has breached Canada’s obligations under the[Treaty] by failing to give continuing effect to the MAPagreements…”

● Subsection 3(2) of the Canada-United States TaxConvention Act, 1984 gives the Treaty paramountcy in theevent the Treaty’s provisions are inconsistent with the ITA

● CRA’s power under the ITA to reassess the taxation yearscovered by the MAP agreements is inconsistent with thepower of the CCA and USCA to resolve cases by mutualagreement under Article XXVI – accordingly, the Treatyprovisions are paramount

41

Sifto Canada Corp. v. The Queen (2017 TCC 37)

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Cameco Corporationo sale of uranium to Swiss subsidiary

o CRA reassessed 2003 to 2015 taxation years

o 3 taxation years are currently before the Tax Court

● CRA arguments (from pleadings):o sham

o paras. 247(2)(b) and (d) - re-characterize transactions

o paras. 247(2)(a) and (c) – transfer pricing adjustments

● At stake for all years:o ~$7.4B additional income

o ~$2.2B in taxes plus interest (and possibly penalties)

42

Upcoming Transfer Pricing Cases

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Silver Wheaton Corp.o Streaming transactions involving subsidiaries (Cayman

Island and Luxembourg) and arm’s length foreign miningcompanies

o Service fees charged by taxpayer to its subsidiarieso 2005 – 2010 years are before the Tax Court

● CRA arguments (from pleadings):o paras. 247(2)(b) and (d) - re-characterize transactionso paras. 247(2)(a) and (c) – transfer pricing adjustments

● At stake for all years:o ~$715.3 million additional incomeo ~$280.4 million in taxes, interest and penalties

43

Upcoming Transfer Pricing Cases

2017 IFA International Tax Conference

Recent Canadian Developments

C. Steeves

● Burlington Resources Finance Companyo taxpayer issued $3B bonds guaranteed by U.S. parento bond proceeds loaned to Canadian operating subsidiarieso guarantee fees paid by NSULC to U.S. parento 2002 – 2005 years are before the Tax Court

● CRA arguments (from pleadings):o guarantee fees and certain costs of bond issuance are

non-deductible under paras. 18(1)(a), 20(1)(e.1)o paras. 247(2)(a) and (c) – transfer pricing adjustmentso paras. 247(2)(b) and (d) - re-characterize transactions

● At stake for all years:o ~$90 million additional income plus potential transfer

pricing penalties

44

Upcoming Transfer Pricing Cases

2017 IFA International Tax Conference

Recent Canadian Developments

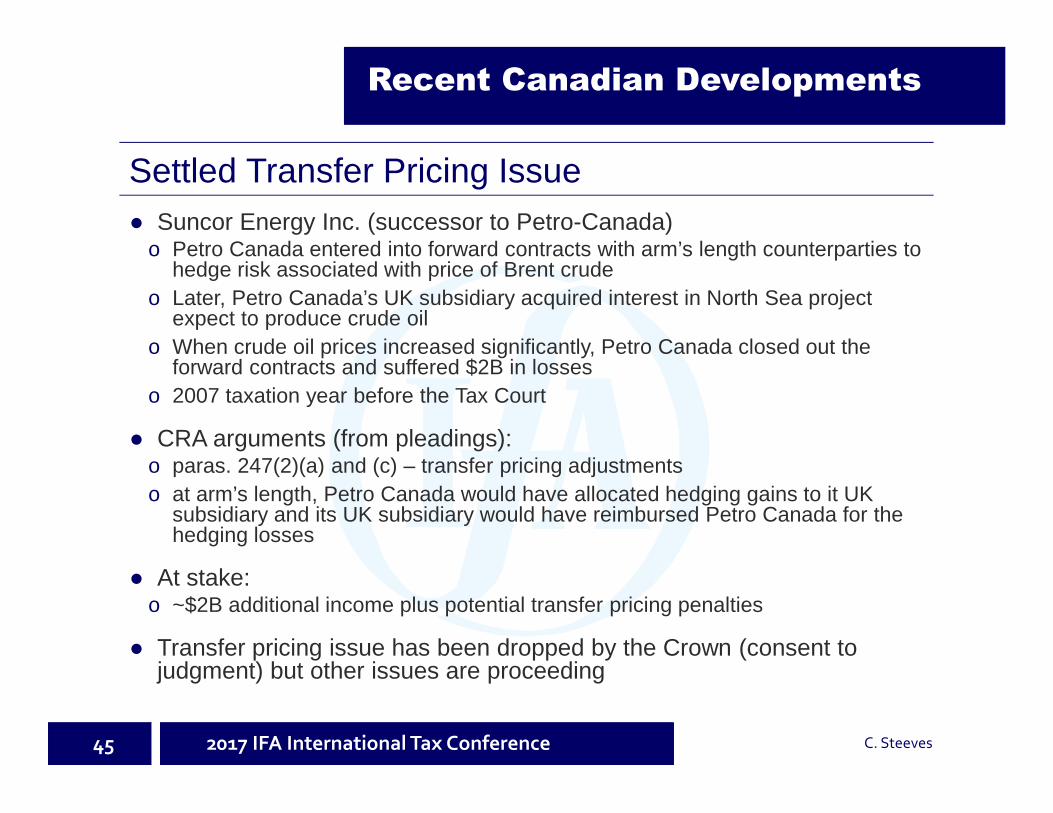

C. Steeves

● Suncor Energy Inc. (successor to Petro-Canada)o Petro Canada entered into forward contracts with arm’s length counterparties to

hedge risk associated with price of Brent crude

o Later, Petro Canada’s UK subsidiary acquired interest in North Sea projectexpect to produce crude oil

o When crude oil prices increased significantly, Petro Canada closed out theforward contracts and suffered $2B in losses

o 2007 taxation year before the Tax Court

● CRA arguments (from pleadings):o paras. 247(2)(a) and (c) – transfer pricing adjustments

o at arm’s length, Petro Canada would have allocated hedging gains to it UKsubsidiary and its UK subsidiary would have reimbursed Petro Canada for thehedging losses

● At stake:o ~$2B additional income plus potential transfer pricing penalties

● Transfer pricing issue has been dropped by the Crown (consent tojudgment) but other issues are proceeding

45

Settled Transfer Pricing Issue

AdministrativeDevelopments

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina2

2014-054559 Upstream loan and debt forgiveness

Upstreamloan (UL)

Upstream loan! @ #Sale of FA shares Loan forgiven

Thirdparty

FA

Canco

FA

CancoThirdparty

FA

Canco

UL ULforgiven

Is the upstream loan considered to have been repaid?Do the upstream loan rules and debt forgiveness rules both apply?

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina3

2014-054559 Upstream loan and debt forgiveness (cont’d)

Upstream loan rules• Upstream loan rules apply (90(6), 90(9), 90(12))• No repayment for the purpose of 90(8) and 90(14)• Inclusion/deduction mechanism may continue indefinitely

Debt forgiveness rules• No “forgiven amount” for the purpose of the debt forgiveness

rules• The loan is considered an “excluded obligation”• Situation remains unchanged whether or not a 90(9) deduction

is available/claimed

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina49

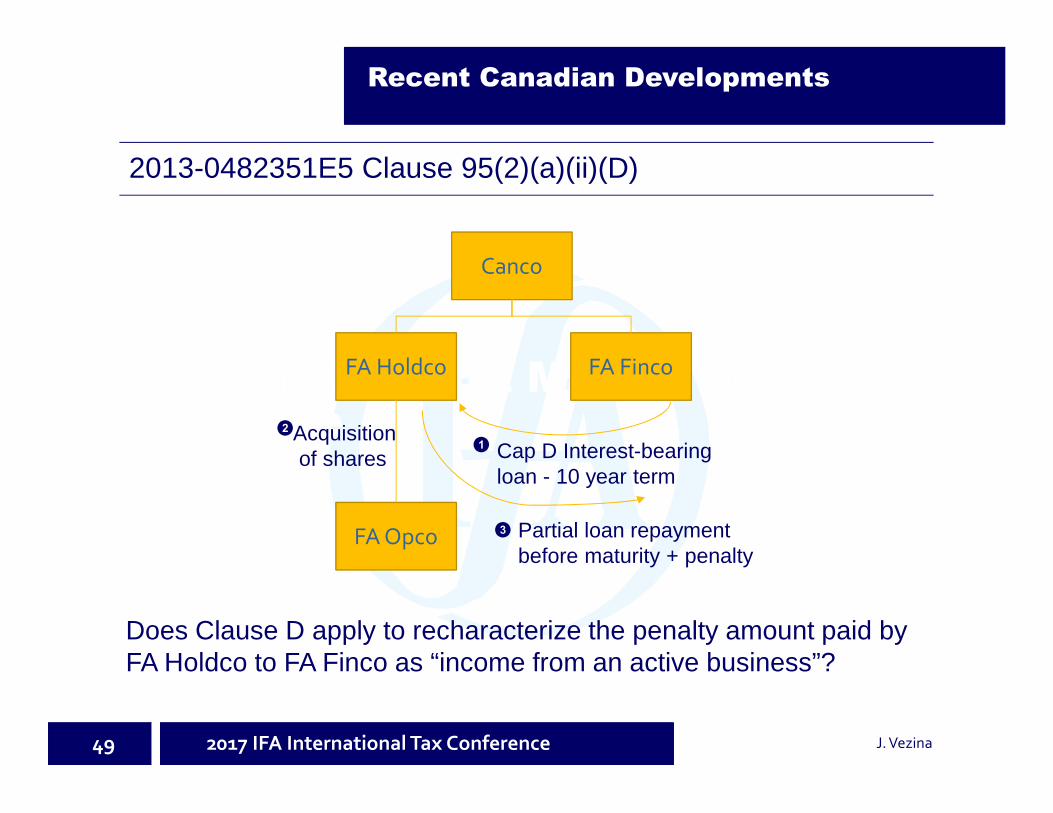

2013-0482351E5 Clause 95(2)(a)(ii)(D)

Canco

FA Holdco

Partial loan repaymentbefore maturity + penalty

@

#

!

FA Finco

FA Opco

Cap D Interest-bearingloan - 10 year term

Acquisitionof shares

Does Clause D apply to recharacterize the penalty amount paid byFA Holdco to FA Finco as “income from an active business”?

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina

Requirement Is requirement met?

1. Penalty received by FA Finco must bederived from amount paid/payable byFA Holdco

Yes. Penalty is considered payable as soonas FA Holdco becomes legally obligated topay penalty.

2. Penalty received must be paid/payableunder a legal obligation to pay intereston borrowed money

Yes, if penalty amount is paid. Par. 18(9.1)is then triggered and the amount of thepenalty is deemed to have been paid andreceived as interest on the loan.

3. Penalty received is an amountpaid/payable by FA Holdco “in respectof any particular period in the year”

* Important given requirement that FA Holdco hold the shares of FAOpco throughout that period, and that the FA Opco shares be EPthroughout that same period

Yes. Since the penalty payment occurs at aparticular time (unlike interest which isaccruing on a daily basis over a period oftime), the relevant period during which FAHoldco must meet Cap D requirements isthe time at which the penalty ispaid/received.

4. The borrowed money is used for thepurpose of earning income fromproperty that is shares of a FA

Yes. As long as FA Holdco holds the sharesof FA Opco (source of income) at the timethe penalty is received by FA Finco.

2013-0482351E5 Clause 95(2)(a)(ii)(D) (cont’d)

5

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina6

2017-068229 - Profit transfer agreements (PTA)

Canco

FA-P

FA-Sub

Canada

Germany

PTApayment

CRA position announced at theMay 2016 IFA Conference

• General Approach - PTA paymentsare “income from property” thatcould be recharacterized as incomefrom an active business under95(2)(a) to the extent that FA-Subhad earnings from an activebusiness

• IFA 2016 Q.6 – CRA answeredaffirmatively and suggested to limitthe application of the GeneralApproach to pre-2017 PTApayments (“IFA position”)

1 class ofshares

Could PTA payments be deemed to bea dividend under 90(2) to avoid anypotential FAPI at FA-P level?

2017 IFA International Tax Conference

Recent Canadian Developments

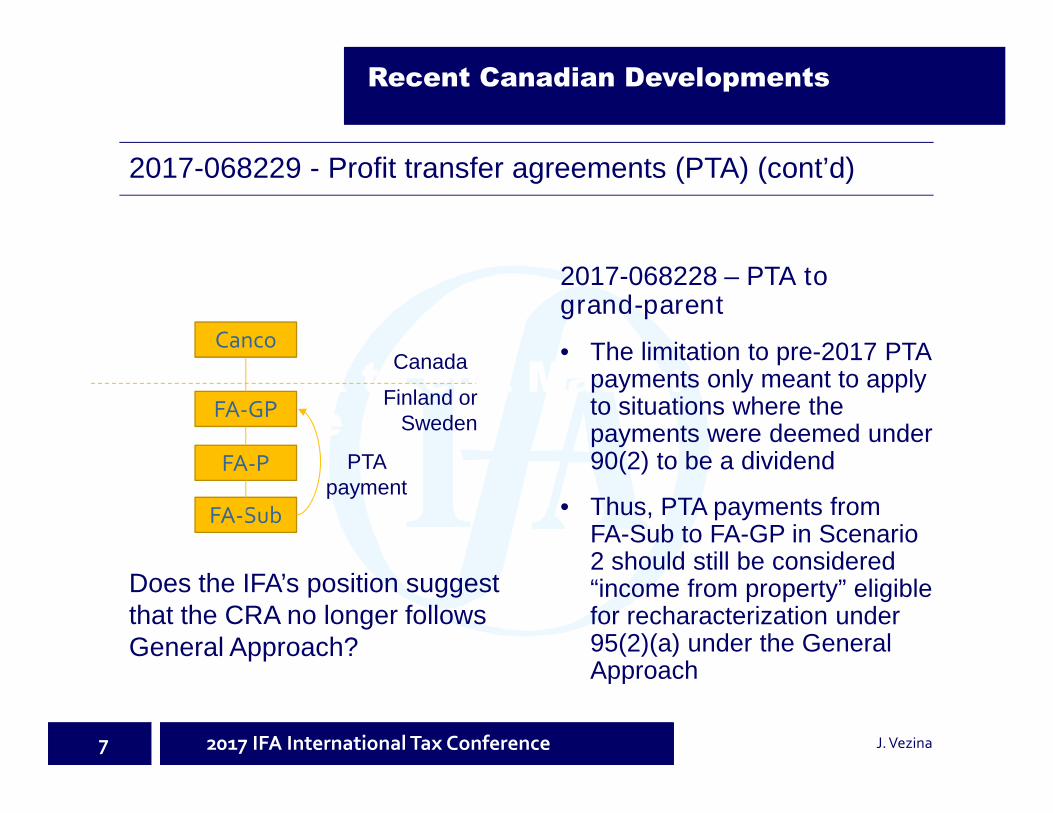

J. Vezina

2017-068228 – PTA togrand-parent

• The limitation to pre-2017 PTApayments only meant to applyto situations where thepayments were deemed under90(2) to be a dividend

• Thus, PTA payments fromFA-Sub to FA-GP in Scenario2 should still be considered“income from property” eligiblefor recharacterization under95(2)(a) under the GeneralApproach

7

2017-068229 - Profit transfer agreements (PTA) (cont’d)

Canco

FA-GP

FA-P

FA-Sub

Canada

Finland orSweden

PTApayment

Does the IFA’s position suggestthat the CRA no longer followsGeneral Approach?

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina8

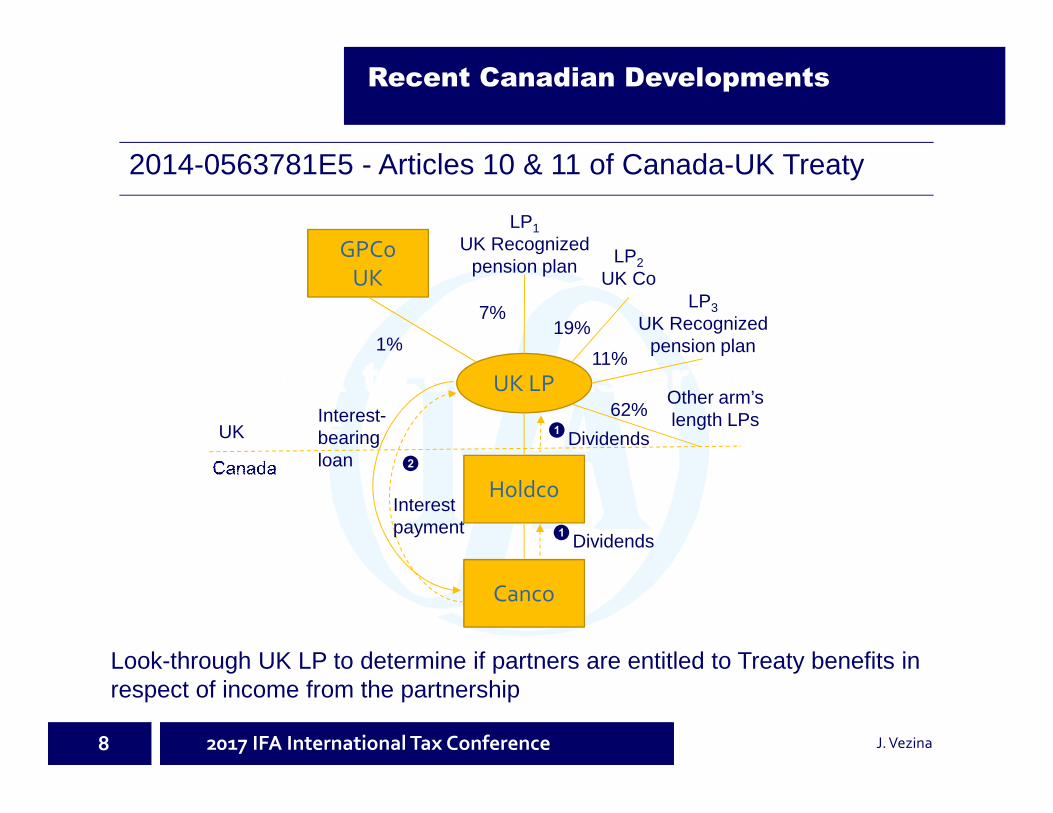

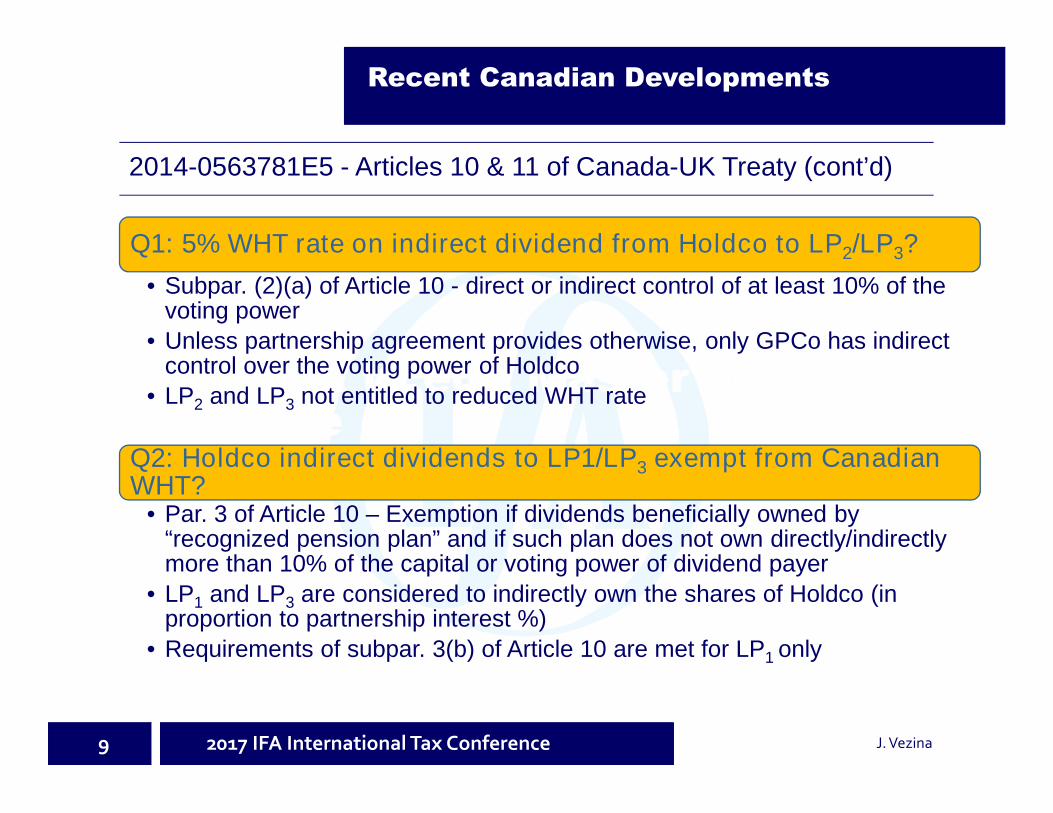

2014-0563781E5 - Articles 10 & 11 of Canada-UK Treaty

GPCoUK

Holdco

LP1

UK Recognizedpension plan

Canco

UK LP

LP2

UK CoLP3

UK Recognizedpension plan

Other arm’slength LPs

1%

7%19%

62%

11%

Dividends

UK

Look-through UK LP to determine if partners are entitled to Treaty benefits inrespect of income from the partnership

Interest-bearingloan

Interestpayment !

@

Dividends!

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina

Q1: 5% WHT rate on indirect dividend from Holdco to LP2/LP3?

• Subpar. (2)(a) of Article 10 - direct or indirect control of at least 10% of thevoting power

• Unless partnership agreement provides otherwise, only GPCo has indirectcontrol over the voting power of Holdco

• LP2 and LP3 not entitled to reduced WHT rate

Q2: Holdco indirect dividends to LP1/LP3 exempt from CanadianWHT?

• Par. 3 of Article 10 – Exemption if dividends beneficially owned by“recognized pension plan” and if such plan does not own directly/indirectlymore than 10% of the capital or voting power of dividend payer

• LP1 and LP3 are considered to indirectly own the shares of Holdco (inproportion to partnership interest %)

• Requirements of subpar. 3(b) of Article 10 are met for LP1 only

9

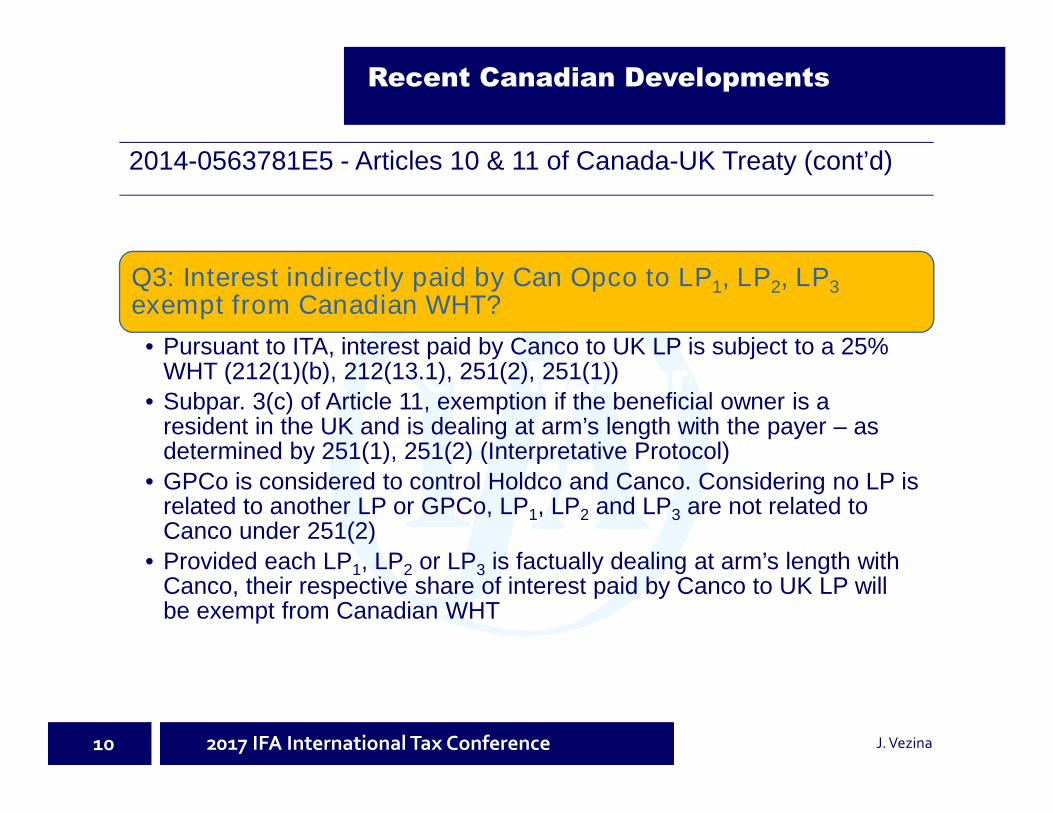

2014-0563781E5 - Articles 10 & 11 of Canada-UK Treaty (cont’d)

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina

Q3: Interest indirectly paid by Can Opco to LP1, LP2, LP3exempt from Canadian WHT?

• Pursuant to ITA, interest paid by Canco to UK LP is subject to a 25%WHT (212(1)(b), 212(13.1), 251(2), 251(1))

• Subpar. 3(c) of Article 11, exemption if the beneficial owner is aresident in the UK and is dealing at arm’s length with the payer – asdetermined by 251(1), 251(2) (Interpretative Protocol)

• GPCo is considered to control Holdco and Canco. Considering no LP isrelated to another LP or GPCo, LP1, LP2 and LP3 are not related toCanco under 251(2)

• Provided each LP1, LP2 or LP3 is factually dealing at arm’s length withCanco, their respective share of interest paid by Canco to UK LP willbe exempt from Canadian WHT

10

2014-0563781E5 - Articles 10 & 11 of Canada-UK Treaty (cont’d)

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina

Subsection 247(2) adjustment

● Year X is statute-barred from reassessment under Part 1pursuant to 152(4)

● 247(2) contemplates an adjustment to any amount forany taxation year of Canco (notjust the transaction year)

– Minister can make anadjustment to the property’sACB without triggering anassessment under Part I inYear X

– Minister can assess a highercapital gain in Year X+7

11

2016-0631631I7 - Transfer pricing capital adjustment

Forco

Canco

Purchase of capitalproperty - Year X$10M

!

Sale of capitalproperty - Year X + 7(arm’s length buyer)$15M

@

CRA conducts audit of Year X + 7ACB of capital property = $1MCapital gain = $14M (15 -1)

#

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina

Subsection 247(3) penalty

● The penalty applies for Year X, the year of acquisitionunder textual, contextualand purposive approach

● No time limit restricting the Minister’s ability to assess apenalty under 247(3)(versus assessment underPart I)

● Interest will accrue from the day the initial notice of thepenalty is sent (161(11)(c)).

12

2016-0631631I7 - Transfer pricing capital adjustment (cont’d)

Forco

Canco

Purchase of capitalproperty - Year X$10M

!

Sale of capital property- Year X + 7(arm’s length buyer)$15M

@

CRA conducts audit of Year X + 7ACB of capital property = $1MCapital gain = $14M (15 -1)

#

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina

● “Income from a business other than an active business” & capital gains aredistinct FAPI components (variables A& B)

● Capital gains rule is more specific –capital gains must be tested forinclusion under variable B (not withinscope of variable A). If intangibleproperty is an excluded property, noFAPI should arise

● If gain on disposition had been qualified as business income (ratherthan capital gain) incidental to a“business other than an activebusiness” carried on by FA, it could beincluded in FAPI under variable A as“income from a business other than anactive business”

14

2016-0658241T7 - Application of 95(2)(a.1) to a capital gain

CanParent

Canco

Unrelated party

@

!LLCAcquisitionof intangibleproperty

Sale of intangibleproperty torelated party

Can par. 95(2)(a.1) apply to thedisposition of an intangible propertywhich generates a capital gain?

2017 IFA International Tax Conference

Recent Canadian Developments

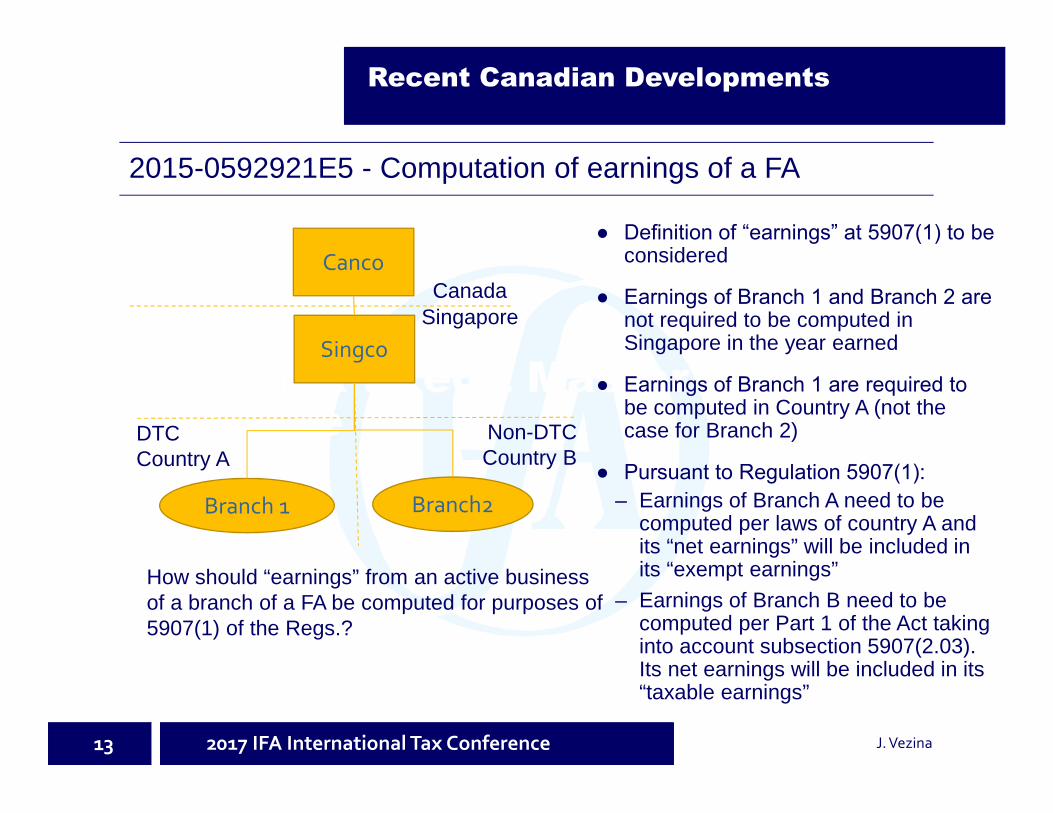

J. Vezina

● Definition of “earnings” at 5907(1) to be considered

● Earnings of Branch 1 and Branch 2 are not required to be computed inSingapore in the year earned

● Earnings of Branch 1 are required to be computed in Country A (not thecase for Branch 2)

● Pursuant to Regulation 5907(1):

– Earnings of Branch A need to becomputed per laws of country A andits “net earnings” will be included inits “exempt earnings”

– Earnings of Branch B need to becomputed per Part 1 of the Act takinginto account subsection 5907(2.03).Its net earnings will be included in its“taxable earnings”

13

2015-0592921E5 - Computation of earnings of a FA

Canco

Branch2Branch 1

Singco

SingaporeCanada

DTCCountry A

Non-DTCCountry B

How should “earnings” from an active businessof a branch of a FA be computed for purposes of5907(1) of the Regs.?

2017 IFA International Tax Conference

Recent Canadian Developments

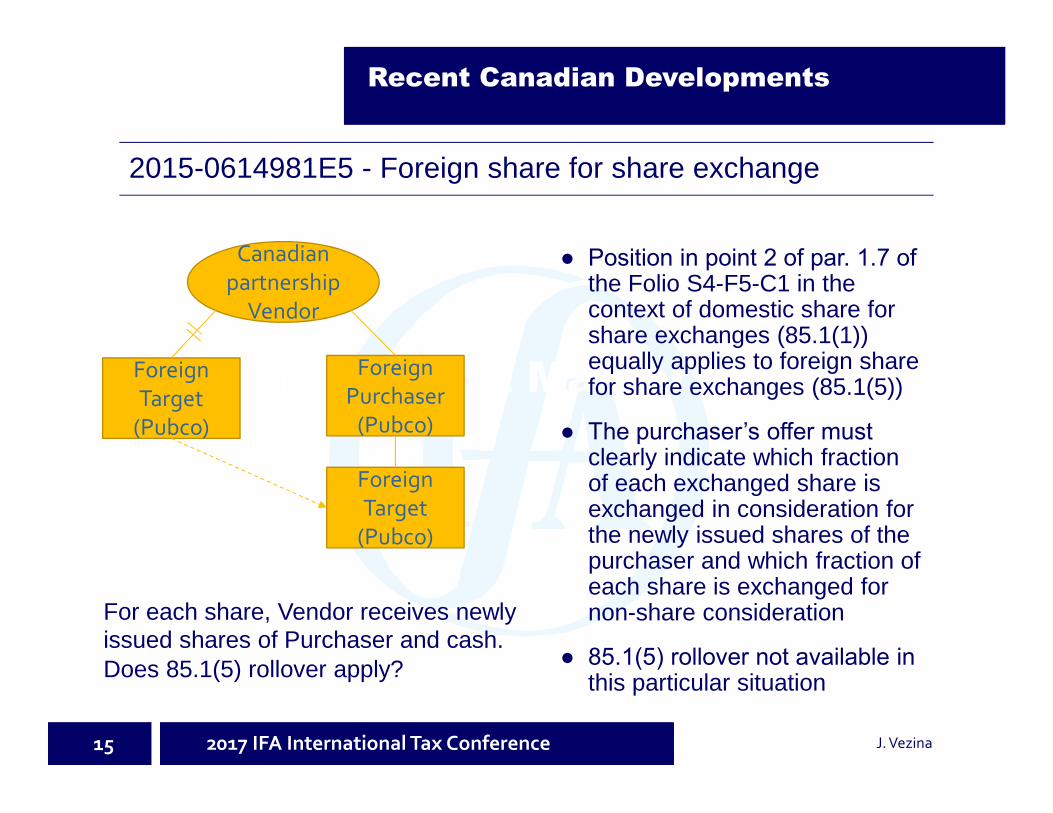

J. Vezina

● Position in point 2 of par. 1.7 of the Folio S4-F5-C1 in thecontext of domestic share forshare exchanges (85.1(1))equally applies to foreign sharefor share exchanges (85.1(5))

● The purchaser’s offer must clearly indicate which fractionof each exchanged share isexchanged in consideration forthe newly issued shares of thepurchaser and which fraction ofeach share is exchanged fornon-share consideration

● 85.1(5) rollover not available in this particular situation

15

2015-0614981E5 - Foreign share for share exchange

Canadianpartnership

Vendor

ForeignTarget

(Pubco)

For each share, Vendor receives newlyissued shares of Purchaser and cash.Does 85.1(5) rollover apply?

ForeignPurchaser

(Pubco)

ForeignTarget

(Pubco)

2017 IFA International Tax Conference

Recent Canadian Developments

J. Vezina

● Question raised - Whether shares in a corporation that is resident in Canada (or interest in a trust) are considered “to derive their valueprincipally from real property situated in Canada” for purposes ofXIII(3)(b) of the Treaty?

● In the domestic and treaty context, this expression allows one to look through a particular property (share of a corporation or interest of atrust) to the real property owned by such corporation or trust

● The value of a share of a corporation (or interest in a trust) derived from real property is determined at the relevant time. No look-back rulecontained in Article XIII(3) (point-in time test versus 5-year look-backrule in definition of taxable Canadian property)

● If, at the time of disposition, the corporation or the trust only hold cash proceeds from the disposition of real property previously held by thecorporation or trust, the shares or interest would not be considered toderive their value principally from real property situated in Canada forpurposes of XIII(3)(b) of the Treaty.

61

2016-0658431E5 – Article XIII of Canada-U.S. Convention