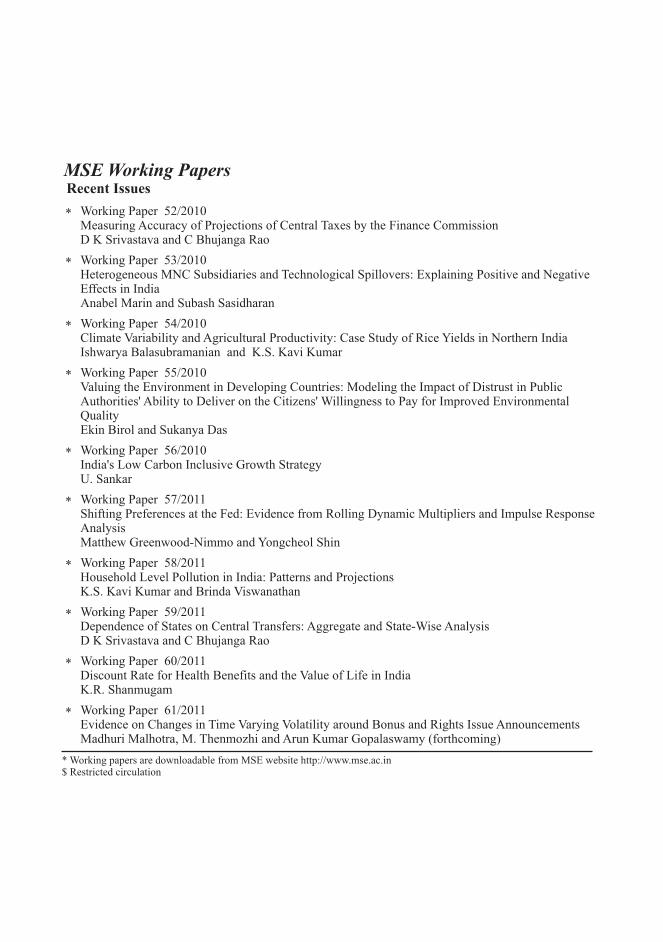

Recent Bouts of Inflation in India: Policy Paralysis? Bouts of Inflation in India: Policy Paralysis?...

30

-

Upload

phungkhanh -

Category

Documents

-

view

215 -

download

0

Transcript of Recent Bouts of Inflation in India: Policy Paralysis? Bouts of Inflation in India: Policy Paralysis?...

Recent Bouts of Inflation in India: Policy Paralysis?

T.N. Srinivasan Samuel C. Park, Jr. Professor of Economics &

Professor of International Affairs (Emeritus), Yale University, Connecticut, United States &

Yong Pung How Chair Professor, Lee Kuan Yew School of Public Policy

National University of Singapore, Singapore.

MADRAS SCHOOL OF ECONOMICS

Gandhi Mandapam Road Chennai 600 025

India

December 2011

ii

MONOGRAPH 13/2011

December 2011

MADRAS SCHOOL OF ECONOMICS

Gandhi Mandapam Road

Chiennai 600 025 India

Phone: 2230 0304/ 2230 0307/2235 2157

Fax : 2235 4847 /2235 2155

Email : [email protected]

Website: www.mse.ac.in

iii

This is a revised as of 31 December 2011 and expanded version of the paper presented as the “Third Shri. R. Venkataraman Endowment Lecture” at Madras School of Economics, on December 12, 2011.

1

INTRODUCTION

It is a great privilege and an honour for me to be invited to deliver the third Shri R.

Venkataraman Endowment Lecture. I thank Dr. D. K. Srivastava, Director and Professor

U. Sankar of the Madras School of Economics (MSE) for the invitation. I have fond

memories of the founder of MSE, the inimitable Raja Chelliah. He left a legacy to the

nation of two outstanding institutions, the National Institute of Public Finance and Policy

at New Delhi in the North and the MSE at the dynamic capital, Chennai, of the fast

growing state of Tamil Nadu in the South. Chelliah aptly captured a well known

description, probably from Vishnu Purana, among many of boundaries of Bharata Varsha

as “Aasetu Himavat Paryantam” from South to North or “Himavat Setu Paryantam” from

North to South in his institution building.

President Venkataraman (hereafter RV as he was widely known) was an

economist and a lawyer. He served the nation with great distinction in many capacities,

as a Member of Parliament and Tamil Nadu State legislature, as a trade union leader,

Minister of Industries and Labour in Tamil Nadu and Union Minister of Finance in the

Indira Gandhi Cabinet after the 1980 election. His achievements were many and well

known. In his second lecture of this series in March this year, Vijay Kelkar spoke of his

critical role as President during the turbulent times of 1987-1992 when the nation

experienced political instability with three Prime Ministers during December 1989 and

June 1991, a severe macro-economic and balance of payments crisis in 1991 that

brought the nation near default on its external debt, downgrading of its credit rating, and

above all the humiliation of having to pledge the nation’s gold stock abroad for short

term credit. The period also saw the initiation of hesitant and piecemeal economic reform

and liberalization in the mid 1980s and systemic and broad ranging reforms in 1991. In

many ways, RV’s last two years as President saw a transition of the Indian economy from

a stagnant insular inward oriented one to a dynamic globally integrated one in trade in

goods services as well as finance. Let me join in Kelkar in saluting RV for having played a

crucial role of support during this critical period as well as his manifold achievements.

My topic today is the recent bouts of inflation. India now has the dubious

distinction of having by for the highest rate of inflation of 7.5 percent among the world’s

largest economies in 2010. Naturally I turned to RV’s thoughts in speeches presenting

the budgets of 1980-81 and 1981-82 as Finance Minister, since he then faced the spectre

of rising inflation and international economic environments similar, though not identical,

to what we face today. Of course then, the monetary policy of the Reserve Bank of India

2

(RBI) was totally subservient to the dictates of the Ministry of Finance and the non-public

sector commercial banks were far less relevant for credit disbursement and selective

credit controls were ubiquitous. Above all the shift away from the capital-intensive heavy-

industry oriented industrialization and import substitution as the development strategy

and restricting domestic and import competition, all implemented by the infamous

Licence-Permit-Raj was yet to happen. One of the ostensible justifications for the

nationalization of commercial of banks in 1969 was a form of the current mantra of

“financial inclusion”. Allowing for these differences, RV’s clear understanding of the policy

tasks, both monetary and fiscal is not only remarkable but also continued to be relevant

now.

In his speech on the 1980-81 (final) budget, RV noted the serious deficiencies in

the performance of the infrastructural sectors of coal, railways and particularly in power

with planned and unplanned outages and a low capacity utilization of 45 percent of

thermal capacity. These along with a drought in 1979-80 led to significant drop in

aggregate supply and an inflation of 20 percent. He went on to say, “In the light of the

problems currently facing the economy the tasks to be accomplished are clear enough.

As there is a great deal of inflationary potential in the economy, the prime objective of

our policy will be to achieve price stability. This will have to be done through an increase

in aggregate supply and a moderation of aggregate demand. Therefore, we intend to

continue our efforts to improve the working of the infrastructure and to augment

available facilities with investment wherever necessary … With regard to demand

management, we shall have to pursue a policy of linking bank credit expansion to

productive and priority purposes and checks the diversion of funds to speculative ends.

We will also have to pursue an interest rate policy which will help in the abatement of

inflationary pressures without hurting productive activity … Since there is a great deal of

liquidity in the system, there is an obvious need to minimize the growth of money supply

by keeping the budget deficit at a much lower level than in 1979-80. This will require a

fiscal policy which will reduce wasteful and unnecessary expenditure, invest resources in

increasing the economy’s production potential and maximize the revenue potential of the

existing tax system”(Government of India, 1980). Three decades after RV’s speech it is

sad that the issues of poor infrastructure performance, high fiscal deficits and incipient

inflationary pressures are still with us. I will argue later on that his implicit recognition of

the need for coordination of fiscal and monetary policy tasks no longer seem to exist. On

the contrary the two seem to be pulling in opposite directions.

3

In presenting the next year’s budget in 1981-82 RV noted the improvement in

the inflationary situation and understandably took credit for it. But he was by no means

complacent. He said “I must caution however that although inflation has abated, it has

not been overcome. The economy remains subject to continuing cost push pressures,

including especially the transmission of international inflation through rising prices of oil

and other essential imports … It is essential to evolve a strategy for coping with cost-

push inflation effectively by tackling – the problem at its roots. This is not only a matter

of demand management. It also requires an all out effort to increase efficiency and

achieve higher productivity” (Government of India, 1981). With the easing of the crisis

situation of the previous year he argued, “The emphasis in 1981-82 must therefore shift

from crisis management to growth … But it must do so in the full knowledge that the

threat of inflation has not been fully overcome. The fiscal deficit should therefore be kept

within tolerable limits (ibid) I will come back later on to the growth slow down since the

last quarter of 2009-10. It possibly reflects increases in repo rates by RBI alone with no

apparent action by fiscal authorities.

Interestingly he highlighted a problem that also persists even now but that is not

often discussed, namely, the stagnation of the share of financial savings of the largest

saver accounting for 70 percent of domestic savings of the economy, namely, the

household sector, at around 11 percent of GDP or about a third of the total gross

domestic savings rate of around 34 percent of GDP in 2010. He put it in slightly different

terms, “Along with fiscal discipline we must also take steps to encourage the flow of

private savings into the financial system … This flow of resources into the financial

system is threatened in two ways and we must tackle both. First of all, it is threatened by

the pernicious growth of the black economy. A second impediment to financial savings is

the existence of high rates of inflation”. Again black money stashed away in secret

accounts abroad and inflation is with us now.

I will note later on that our current Finance Minister Pranab Mukherjee in his

recent suo motu statement in the Parliament on November 27, 2011 on inflation and a

durable solution for it, in essence, re-emphasized RV’s diagnoses of the malady of

inflation as well as preventive and curative cures for it.

We all owe a deep debt of gratitude for the clarity and foresightedness of RV’s

vision for our diverse economy, its plural society, and its democratic polity and for his

quiet but firm guidance during a very turbulent period.

4

MEASUREMENT OF INFLATION1

Containing Inflation, defined somewhat loosely as a sustained increase in overall prices

over an extended period of time is a concern of policy makers including central banks of

most countries of the world including India. In this lecture, I will explore several aspects

of inflation in India, particularly the analytics of the inflation process; trends in price

changes since 2004-05 till November 2011. Monetary policy tools are the primary, though

not the only, policy instruments for dealing with inflation. Central Banks are charged in

many countries with maintaining price stability as one of the macroeconomic objectives

of monetary policy in combination with other objectives, such as sustaining full

employment or ensuring that the aggregate economy operates at or close to its potential.

Implicit in these objectives is to contain the adverse consequences of sustained inflation,

unemployment, and unutilized potential of the economy on consumer welfare. RBI’s

ultimate objective is sustained growth with financial stability. It must be recognised that

from Dadabhai Naoroji in 1899, and the report of the National Planning Committee of

1938 chaired by Jawaharlal Nehru, the Bombay Plan of businessmen in 1943 and the

Peoples Plan of Indian federation of labour in 1944, eradication of poverty measured by

the population living below the poverty lines defined by each, has been the single

overarching and intrinsic objective of the nation with rapid and well distributed growth as

the primary instrument for achieving it. The mantra of “inclusive growth” chanted ad

nauseum by national and international agencies was better understood by these

visionaries.

In almost all countries of the world, the consumer price index (CPI) is used for

measuring inflation. On the other hand, broadly speaking, prices received by producers at

the farm or factory gate influence their incentives for production and hiring. As such, a

Producer Price Index (PPI) is also used in policy discussion in many countries in

conjunction with an aggregate CPI.

Neither an aggregate CPI (until very recently) nor a PPI are compiled and

published in India. Inflation is measured in India by the rate of increase in any period

(week, month or year) over its value in the corresponding period of the year before of

the Wholesale Price Index (WPI). This year-on-year or y-o-y rate of increase is called

1 I have drawn extensively on my unpublished paper, Srinivasan (2011a), in this lecture.

5

Headline Inflation. In addition, policy makers and particularly the media document the

trend in one particular component of WPI, namely, the index of Wholesale Prices of Food

Articles. To call it, “Food Inflation” is misleading since doing so does not distinguish

between a rise in price of food articles at the same rate as the rise in overall prices and

at a rate different from it. The former implies no change in the prices of food articles

relative to the basket of all commodities.

The inappropriateness of using WPI for measuring inflation has long been

recognized by policy makers including former RBI Governor Y. Venugopal Reddy and the

current Governor Subbarao. Yet according to the latter, the RBI has opted for WPI over

Consumer Price Index (CPI) for a number of reasons, one of which being that until

February 2010 an All India CPI for consumers was not available. Another reason of WPI’s

alleged clarity in communicating RBI’s policy stance. Neither reason is particularly

convincing. Moreover the Indian WPI, is neither a producer, nor even strictly speaking, a

Wholesale Price Index, since it uses retail price quotations for some and wholesale prices

for other commodities. It does not include services. Unlike the almost universal practice

of publishing seasonally adjusted prices indices, no such series of WPI or CPIs are

published in India. Although each of the four available CPIs covers a different subgroup

of the population, they all include services. It is also the case that trends in the four CPIs

in WPI often differ. Still, there is no reason for not using them altogether. After all with

the economic knowledge and statistical power in RBI and in Ministry of Finance, some

sensible statistical adjustments could have been made to take into account their

deficiencies and so adjusted aggregate CPI could have been used. In any case, it is to be

hoped that once enough data with the new CPI accumulate, the RBI will switch to its use

for monetary policy formulation.

I have discussed the deficiencies of WPI and possible reforms elsewhere

(Srinivasan, 2008a and 2008b). I proposed that in addition to the new CPI, a new

appropriately defined producer price index (PPI) _ as well as a cost of living index (COLI)

should be compiled and published. The inflation rate, rather than a COLI currently plays a

role in determining adjustments in dearness allowance of employees of the organized

sector including the Government and Government aided institutions. Further in India

there are no systematic procedures for incorporation of new goods and quality

improvements in old goods in the price indices. Although such procedures exist in US,

they have been found by the Boskin Commission to be inadequate and may have

resulted in the overstatement of CPI inflation. Introduction of systematic procedures for

reflecting quality improvements and the availability of new goods in price indices in India

6

is urgent, given the strong theoretical presumption and empirical evidence that with

trade liberalization and greater competition, the pace and quality of improvements and

widening range of goods available in the market has been accelerating. Since these

changes took place over a period of time and their full impact may take even more time

to be realized there is a strong presumption that the Inflation rates in India are

overstating their true values although the extent of overstatement cannot be ascertained

without a careful empirical study.

TRENDS IN INFLATION: HEADLINE INFLATION

The trends in the monthly Year on Year rates of change in WPI for all commodities from

April 2005 to November 2011 and weekly price trends for some important items till

December 17, 2011 are available. Obviously one could define other rates in a similar

fashion---for example, the annualized percentage rate of change of the current week’s

index over its value in the previous week is a very short-term week on previous weak

inflation rate. It is easy to see that these rates, being all based on the same data

necessarily imply purely arithmetical inter-relations among each other. Also except for

inflation measured cumulatively from the base year, others are affected by the so called

“base effect”.

The weekly inflation rates are likely to be more volatile than monthly and annual

rates. The trends in monthly rates suggest that in the 80 month period from April 2005 to

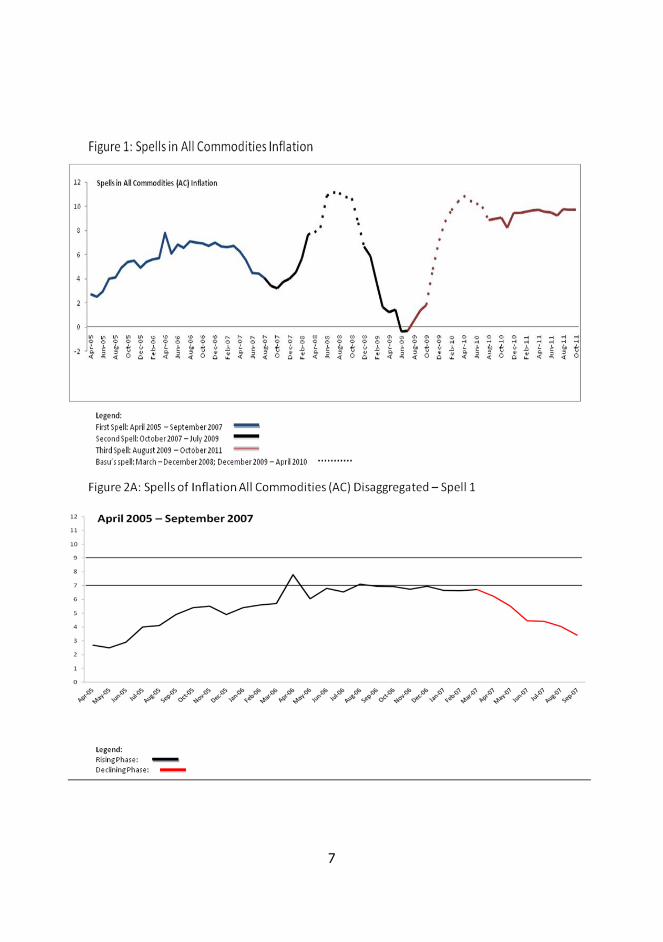

November 2011, the most recent spell of sustained inflation for all commodities seem to

have begun in August 2009. In 24 months from December 2009, monthly rates of

inflation exceeded 7 percent, and in 19 of them, 9 percent. In fact, this spell itself was

preceded by another of 30 months from April 2005 to September 2007. Taking the two

spells together in the 80 months between April 2005 and November 2011 inflation rates

were 7 percent or higher in as many as 45 months.

The spells until October 2011 are shown in a temporal sequence in different

colours in Figure 1, and each component of this sequence of spells is charted in Figures

2A, 2B, and 2C, respectively. The rising and declining phases of each spell are also

illustrated. Clearly the seeming persistence of inflation near 7 percent or higher a year

over such a long period calls for an analysis in depth of its determinants that goes

beyond ad hoc explanations.

7

8

9

TRENDS IN INFLATION: FOOD INFLATION

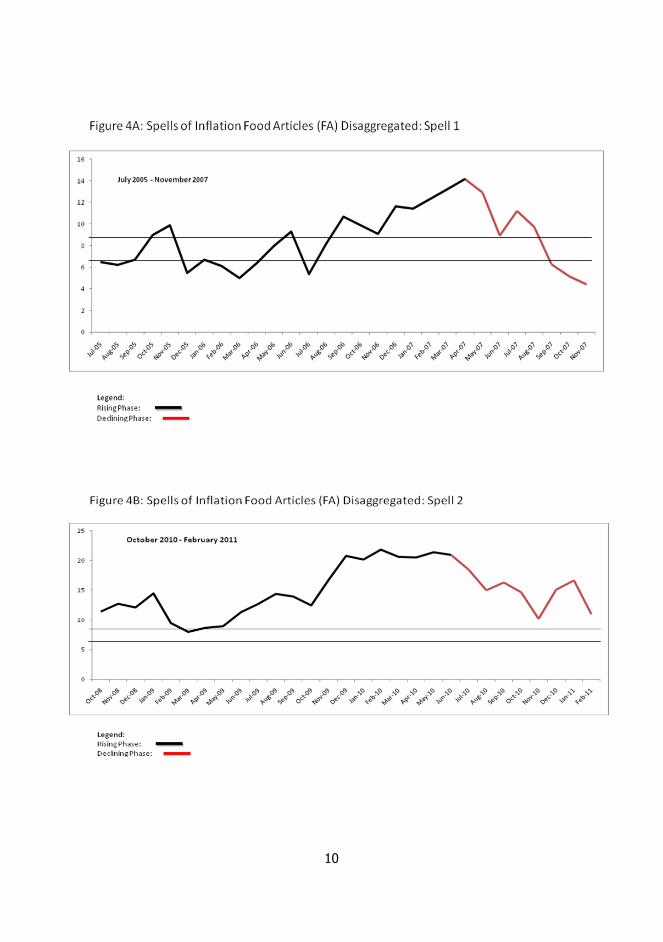

The time pattern of changes in the price of food articles is not the same as that of all

commodities. In the period of 80 months since April 2005 in 55 months, nominal food

prices rose faster than the nominal value of the bundle of all commodities. However, 53

of the 55 observations were in just 2 long spells, with 26 of them in the 29 month period

from July 2005 to November 2007, and another 27 in the 29 month period from October

2008 to February 2011. The two spells until October 2011 in inflation of Food Articles

Prices are shown in temporal sequence in Figure 3 in different colours. Each component

of this sequence of spells is charted in Figures 4A and 4B respectively. The rising and

declining phases of each spell are also illustrated.

10

11

Clearly the relative price of food articles has been rising for most of the period of

80 months since April 2005. In 35 months, inflation in all commodities was 7 percent or

higher and in 24 of them higher than 9 percent. Inflation in food articles however was at

or higher than 7 percent in as many as 55 months and above 9 percent in 44 of them.

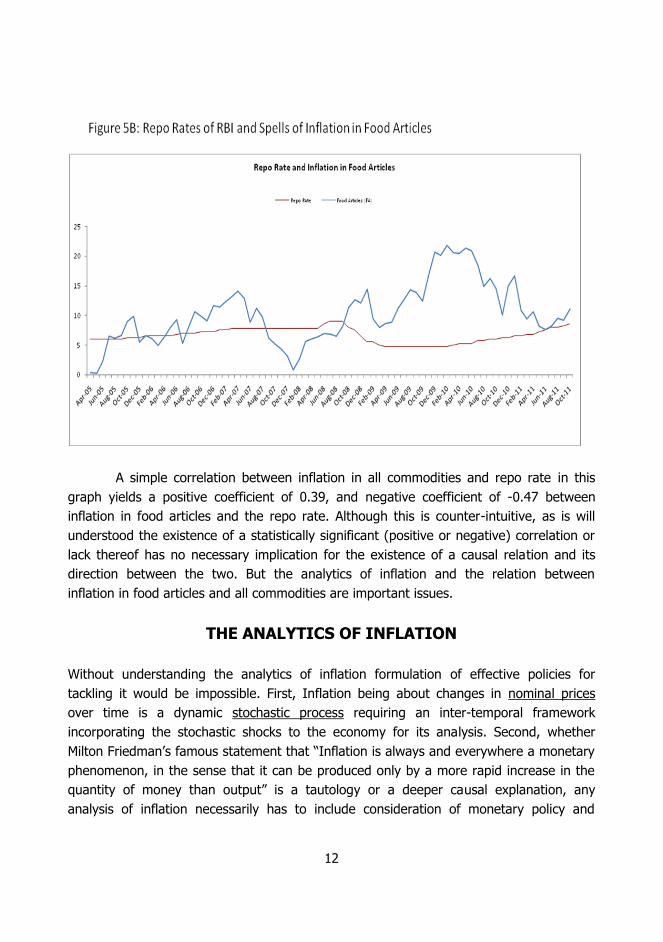

REPO RATES AND INFLATION

RBI’s policy rate is currently the repo rate. The changes in it are meant to influence its

interim target of the average of short term rates and eventually the ultimate target of

inflation rate. Figures 5A and 5B highlight the repo rates of the RBI during the spells of

inflation in all commodities and food articles, respectively. The rising (declining) phase of

inflation in all three spells in all commodities, loosely speaking, correspond with increases

(decreases) in the repo rate, though an association between a rise (fall) in the repo rate

and a subsequent decline (rise) in inflation rate cannot be clearly seen. However a similar

pattern is not seen in inflation in food articles. The rising phase of the second spell of

inflation in food articles corresponds with a reduction in the repo rate.

12

A simple correlation between inflation in all commodities and repo rate in this

graph yields a positive coefficient of 0.39, and negative coefficient of -0.47 between

inflation in food articles and the repo rate. Although this is counter-intuitive, as is will

understood the existence of a statistically significant (positive or negative) correlation or

lack thereof has no necessary implication for the existence of a causal relation and its

direction between the two. But the analytics of inflation and the relation between

inflation in food articles and all commodities are important issues.

THE ANALYTICS OF INFLATION

Without understanding the analytics of inflation formulation of effective policies for

tackling it would be impossible. First, Inflation being about changes in nominal prices

over time is a dynamic stochastic process requiring an inter-temporal framework

incorporating the stochastic shocks to the economy for its analysis. Second, whether

Milton Friedman’s famous statement that “Inflation is always and everywhere a monetary

phenomenon, in the sense that it can be produced only by a more rapid increase in the

quantity of money than output” is a tautology or a deeper causal explanation, any

analysis of inflation necessarily has to include consideration of monetary policy and

13

financial sector behavior. Third, since the public policy as well as private concerns about

inflation largely arise from its effects on the real sector, for analyzing them an integrated

framework of the real and monetary sectors is essential. The real consequences are on

consumer welfare, aggregate and sectoral outputs and growth, real investment,

employment and so on. Clearly in a largely competitive market based private sector

economy such as ours, decisions about what to produce, to consume, to export, import,

investment in real and financial assets and their economy wide or aggregate

consequences depend on the prices faced by those making the decisions at a point in

time and overtime. Since some investment and in part production decisions will have

their impact only in the future in the near and longer term, and the future prices are

unknown and uncertain at the time current decisions are made, as Keynes argued long

ago expectations of decision makers about future prices matter. Thus how expectations

are formed is a crucial issue. Anchoring price expectations is an important policy

objective. Fixing the exchange rate of the currency with that of a country known to have

stable domestic prices is an anchoring policy that some countries adopt. India is not one

of them. Thus in India success in anchoring depends crucially on whether policy makers

have built a reputation for success in stabilizing prices. But then success itself depends

on the public having well anchored expectations. Further private decisions are also

influenced by public policies both macroeconomic and microeconomic and any anticipated

changes in them. In particular, distortions created by Government interventions in

markets could also distort private decisions depending on whether interventions are

meant to correct market failure or otherwise.

Any satisfactory framework to be integrated framework has to incorporate real

and financial sectors and variables in a behaviorally sound way. Ad hoc frameworks of

integration are likely to be unsatisfactory in one or more ways.

The recent global financial crisis of 2008 and the fact of its spread from the

bursting of a real asset price (i.e. house price) bubble in the United States (U.S.) to the

entire financial sector in the U.S. and then to the rest of the world was not foreseen by

most analysts including academic economists. It also brought into sharp focus the

inadequacies of macroeconomic and financial models. This has spawned a still growing

literature on what is wrong with macroeconomics and macroeconomists.

14

ANALYTICAL DISCUSSIONS OF INDIAN INFLATION

A recent seminar on September 21, 2011 on inflation was organized by the National

Institute of Public Finance and Policy (NIPFP) in New Delhi. The staff of Planning

Commission, Department of Economic affairs (DEA), Reserve Bank of India (RBI) and

academic experts of the International Monitory fund (IMF), World Bank, Asian

Development Bank and others participated. Apparently at the seminar Kaushik Basu,

Chief Economic Adviser in the Department of Economic Affairs (DEA) in his remarks

agreed with the comment of Govinda Rao, Director of NIPFP and a member of the Prime

Minister’s Economic Advisory Council in his introduction that “the country’s economic

managers have not been able to fully grasp the processes underlying the persistence of

high inflation.” Such a conclusion by a senior policy maker and a policy adviser is deeply

disturbing.

Basu has also published in 2011 two avowedly analytical papers in the Economic

and Political Weekly, one entitled “Understanding Inflation and Controlling it” (Basu,

2011a) and the other entitled “India’s Foodgrain Policy, An Economic Theory Perspective”

(Basu, 2011b) Although they have some useful but largely well known insights,

unfortunately both devote too much space to largely peripheral theoretical curiosa and

digressions that do not contribute to a deeper understanding of the analytics of inflation,

let alone on policies for addressing it.

Basu (2011a) notes that “India’s highest inflation occurred in September 1974

when it reached 33.3%. Arguably our worst inflationary period was from November 1973

to December 1974 when inflation never dropped below 20% and above 30% for four

consecutive months starting June 1974” (p.51). In Basu (2011b) he notes that “From

October 2009 to March 2010 the year-on-year food-price inflation announced every week

hovered around 20%” (p.37). It is well known that there was an episode of steep rise in

food prices and inflation globally during 1973-1974, an episode that has not been

repeated in the same fashion since. Basu does not ask whether and why the current

episode is different from the earlier one. With regard to the divergence between the price

index of food articles and the WPI since 2000, he is breathtakingly casual about the

causal connection between the two. He simply asserts that in an earlier era “overall

inflation was powerfully driven by the agricultural sector. Overtime, the share of

agriculture in the total GDP has fallen and the growing strength of the economy

15

(whatever he means by it), means food prices alone are no longer in the driver’s seat the

way they were for the first several decades after independence” (Basu, 2011a, p53).

Whether or not his assertion is valid, he should at least have examined the

trends in relative price of food articles and the micro-economic factors in their

determination. As noted earlier, the time pattern of the inflation rates in the two indices

differed. As noted earlier in 55 of the 80 months since April 2005 the index of food

articles rose faster than that of WPI and most probably earlier as well. It is hard to argue

however that the falling trend over decades in the share of agriculture in GDP was the

major contributory factor in the divergence between WPI for all commodities and that for

food articles.

Although Basu (2011b), rightly calls for more attention to be paid to macro-

demand management through fiscal and monetary policies for controlling overall

inflation, his paper, including the section on interest rates and liquidity, has little or

nothing to say on macroeconomic theories. His reference to Brazil having successfully

lowered liquidity by counter-intuitively lowering interest rates is interesting but its

relevance to the Indian context is not evident. His digression on capital controls and

discussion on the possible impact on inflation of policies that benefit the poor such as the

National Rural Employment Guarantee Act do not answer the basic question about the

determinants of a sustained month-after-month rise in food prices during 2009-2010.

Basu’s paper on the Economic Theory of Foodgrain Management taken as a whole is

extremely disappointing as a contribution to India’s food-grain policy which is beyond the

use buffer stocks for price stabilization and in particular to containing food inflation.

Basu, given his well deserved reputation as an excellent economic theorist should have

explained the analytics of the role of India’s fiscal policy in addressing inflation.

Deepak Mohanty, Executive Director of RBI in his very recent speeches

(Mohanty, 2011a, 2011b, and 2011c) addresses the role of monetary policy and RBI in

addressing inflation. With inflation still unabated despite as many as 13 hikes in the

policy rate (repo rate) by the RBI since March 2010 questions arise whether the

transmission mechanisms between changes in repo rate and its ultimate objective of

inflation rate might have changed and the lag been between a change in repo rate and

its impact and on inflation rate might have lengthened. Moreover were the signals (on a

weekly basis) on inflation rates and on a quarterly basis on growth rate that everybody

including RBI receive used in a forward looking manner by the RBI in deciding on

whether and to what extent change (in either direction) its policy rate and if yes, how

16

were they used? Mohanty’s speeches do not provide any clue on these critical questions.

Mohanty mentions RBI’s objective of achieving a specific threshold level inflation rate as

a means for anchoring of inflationary expectations. Since RBI does not follow inflation

targeting in its monetary policy, nor does it use a fixed exchange rate of the Rupee with

a low inflation country as an anchor, it is unclear how it uses the findings from its own

periodic survey of inflationary expectations in an analytical way. The very recent

statement of the RBI that it reserves the right to intervene if necessary to address the

depreciation of the Rupee seems to contradict its policy until now of letting the market

forces determine the Rupee’s exchange rate and intervening only to mitigate the volatility

in exchange rate movements.

At a recent Confederation of Indian Industry (CII) event in Kolkata on December

9, 2011, Governor Subbarao (2011) acknowledged that the concern that RBI’s hikes of

repo rates 13 times since March 2010 have had no impact on inflation rates is legitimate

but added “ Had the RBI not acted the inflation rate now would have been 12 percent or

13 percent and not 9.7 percent at the moment” (The Hindu, December 9, 2011). This is a

merely self serving assertion since he did not offer a shred of analytical evidence in its

support. One could equally well argue that had the RBI acted by raising rates earlier and

higher once the evidence that mini hikes were not working, probably inflation at the

moment would have been much lower than 9.7 percent

Time does not permit a discussion of the paper of Mihir Rakshit (2011) that

questions the macroeconomic framework of monetary and fiscal policy making in India

and wants to be replaced by a structuralist one that in his view is consistent with Indian

reality. He also questions the monetarist thinking behind the repo rate rises of RBI in

trying to combat inflation. While analytically interesting, Rakshit unfortunately does not

provide enough empirical support for his alternative framework.

This is not the occasion for delving into the more econometrically oriented papers

and to my own admittedly simple and even simplistic, econometric exercises. My

summary assessment is that they are neither conclusive nor informative and have no

distinct take-away message. For example, on the crucial question of whether food

inflation is the driving force behind overall inflation, some studies find no convincing

empirical evidence in favour while others do. The fundamental problem with the studies

is that they are based on ad hoc specifications without any link to economic theory.

17

However the thesis of food inflation as the driving force of general inflation will

soon be put to test. The weekly inflation rate in food articles has been declining recently

from 12.21 percent in the week ended October 22, 2011 to 0.42 percent in the week

ended in December 17, 2011. In part, this is to be expected. With a good Khariff Crop

following a good monsoon and the beginning of market arrival of the Khariff harvest

(primary) rice, price of rice declined. Wheat prices have been declining even longer

perhaps following Russia’s lifting of the ban on wheat exports. It is too soon to tell

whether the recent decline of food inflation is temporary or will be sustained. If it is, it

will be interesting to see whether inflation rate in all commodities which was at 9.11

percent in November 2011 will begin to decline at the end of this fiscal year as the

Government has been forecasting.

I will conclude by summarizing and drawing policy implications from my analysis.

Let me begin with two recent developments that have implications for economic policy in

general and for addressing inflation. The first is the already mentioned good news about

recent decline in food inflation. Second is the bad news about the decline in real GDP

growth in the second quarter of this fiscal year to an annual rate of 6.9 percent in the

first quarter’s 7.7 percent. Basu has attributed this in part, perhaps euphemistically to

“delays in decision making” rather than appropriately to policy paralysis. Montek

Ahluwalia pointed out to an investment slowdown as the cause, but the data do not bear

him out. But both did not refer to the most disturbing aspect namely that the decline

started from 9.4 percent growth in the fourth quarter of 2009-10 and continued in every

quarter since then. Even the 9.4 percent growth itself is more a reflection of the recovery

from the effects of the global financial crisis. In fact the slowdown in growth had started

in the last quarter of 2007-08 before the financial crisis hit and had its impact on India. I

have argued elsewhere (Srinivasan, 2011b) that the structural problems, particularly of

infrastructural constraints had made a return after the crisis to the average growth rate

exceeding 9 percent achieved during the three years 2005-2008 very unlikely.

The recent decline could also be a reflection of shift from the unnecessary

stimulatory policy stance earlier of RBI around March 2009 and the consequent net

tightening of credit by 475 basis points through successive increases in repo rates since

December 2009. Conventionally and plausibly a reduction in growth and moderation of

inflation are associated with the rise in the interest rates. Also the shares of interest

sensitive components of the industrial composition GDP and of aggregate expenditure are

not large.

18

RV warned three decades ago, that in raising interest rates policy makers have to

keep this trade-off in mind and adopt simultaneously other policies, particularly fiscal

policies to cushion the possible adverse impacts on growth. In any case Montek Ahluwalia

ended a recent interview with Karan Thapar of CNN-IBI with the frank admission that “I

regret to say that I have to admit that” in response to Thapar’s remark “If inflation hasn’t

begun coming down by February, then the Government really does not know what it is

doing.”(CNN-IBN Live (2011)

Ahluwalia’s reasoning behind the likelihood of the current forecast of a decline of

inflation by February 2012 being credible as compared to unrealized past forecasts is not

persuasive. To say the full effects are yet to be felt is itself not credible. Why did the RBI

not raise the repo rate in bigger steps as the signals from its earlier rises in repo rates

were not felt even after the expected lag? I have already pointed out that the statement

at the CII event by Governor Subbaaro defending of RBI’s actual hikes was self-serving

without any analytical evidence. Of course, India cannot control international prices. The

possibility of their going up as well as down has to be allowed for in making forward

looking policy. Did the international prices go up more than had been allowed for in the

Government’s March 2010 forecast? The signals about the possibility of further rise in

prices were there soon after March 2010 and policy could have responded. That there is

a margin of error around any forecast is obvious. For this reason, a prudent forecaster

would make a point rather than in interval forecast that took forecast errors into account,

is inappropriate. Moreover the observed trend in one direction (upward) only in prices

suggests policy paralysis and failure and not just forecast errors.

WHERE DO WE GO FROM HERE

It is to be fervently hoped that the recent decline in weekly inflation in Food Articles

would be followed by a long-awaited sustained decline in monthly rates of overall

inflation. But apart from hopes and prayers, policy review, rethinking and actions are

called for. Let me list some without being comprehensive and exhaustive. First, a

rethinking of the framework for analysis of inflation away from paradigms largely

borrowed from developed countries and towards one that is appropriate for the Indian

context is needed. In particular, the fact of financial intermediation in India apparently

excludes significant shares of savings and investment in GDP needs to be taken into

account to assess the macroeconomic effects of the type of global financial crisis of 2008

in future. Second, the relevance to India of the foreign paradigm that monetary and the

fiscal authorities pursue different objectives has to be examined without confounding it

19

with distinct issues of independence of RBI from the fiscal authorities to set instruments

under its control independently. The latter is consistent with both having the same

objective for the economy with the two credibly coordinating their choices with each

other. The evidence from RBI studies that there appears to be little coordination in India

between them is disturbing in this context. Third, the RBI should certainly be able to

transmit credibly and effectively its policy stance by explaining reasons in a forward

looking manner for changes in its policy rate when it makes them. But the reasons must

go beyond just for influencing short term interest rates money markets in the desired

direction but more importantly for influencing one of RBI’s ultimate objectives, namely

sustaining growth with price stability.

RBI has not explained why its successive increases in policy rates 13 times since

March 2010 have had little apparent effect on inflation. While the Annual and Quarterly

reviews of the RBI of Macroeconomic Developments and Outlook are certainly valuable,

they do not meet the need for explaining reasons for policy action or non-action as major

shocks domestic and external hit the economy. To take just one example, RBI to the best

of my knowledge has not laid out its analysis of the Euro crisis and its assessment of

proposals for its resolution from an Indian perspective.

Fourth, and most important, the urgency of completing the 1991 reform agenda

ought not to be underestimated. For example, fiscal consolidation, reform of the tax

code, introduction of a goods and services tax, rethinking of market interventions, explicit

subsidies, tax expenditures, agriculture credit, energy and infrastructure investments and

policies, and also going beyond them by identifying new reforms (for example, of labour

laws and state level regulations) remain to be completed or even begun in many cases. It

should be understood first, that the lags in beneficial effect of these reforms to emerge

would vary with the reform and the lags could be long in some cases and second, any

delay in undertaking this task would avoidably keep people poor longer and prolong the

inflationary trends.

Fifth, the Government and Indian society in general seem to be ambivalent about

a commitment to liberalizing foreign trade and investment. On the one hand Prime

Minister Manmohan Singh in his speeches at the G-20 summits supported a commitment

to conclude the Doha round of Multilateral Trade Negotiation with a balanced outcome.

On the other, the Commerce Minister Anand Sharma who is India’s negotiator on Doha

wants to go back India’s position in December 2008 when India and US together

contributed to the stalling of Doha Round.

20

Recently Singh and Sharma publicly committed themselves to the decision of the

central cabinet to allow 51 percent share of Foreign Direct Investment in India’s retail

trade sector. Its implementation Under strong opposition, despite empirical evidence

that the entry of large domestic enterprises into retailing has been beneficial to farmers

and has not hurt small retailers, from Sate Governments and from political parties

including from members of the own ruling coalition has led to the suspension of its

implementation until a political consensus emerges. Since retail trade is under the

jurisdiction of states, the emergence of a consensus seems implausible.

Sixth, fiscal consolidation to reduce consolidated fiscal deficits of the centre and

states and the overall Government debt to GDP ratio to sustainable levels to support

rapid and sustainable growth under price stability seems a long way off. This is primarily

because the Government does not seem to have the requisite political support to reduce

explicit subsidies, revenue foregone from tax exemptions and to complete fiscal reform.

Clearly as compared to a desirable situation in which monetary and fiscal efforts are

coordinated to maintain price stability, without support from fiscal effort, the social cost

of monetary authorities alone trying to achieve the goal using its own tools would be

high, assuming they succeed. But their success is by no means certain.

The global fallout from the festering Euro Zone sovereign debt crisis has already

slowed the growth rate of India’s exports. As happened in 2009, most likely it would

again lead to a decline in exports in the near future, though it is hard to forecast the size

of the decline. For well known reasons, any decline in exports has its major impact on

growth of industrial production as is already happening, since a large share of India’s

exports is in manufactured products. In the aftermath of global financial crisis of 2008

external export credit flows and flows of Foreign Institutional Investment (FII) declined

and there are already evidence of this happening now.. The recent depreciation of the

Rupee could be a reflection of rationally anticipated decline in exports and FII and a rise

in current account deficit. Already with an anticipated decline in its manufactured output

China has already reversed its tightening of credit introduced for controlling inflation. I

would not be surprised if RBI goes beyond leaving the repo rates unchanged as it has

done also reverses and lowers them soon and the Government once again engages in a

stimulation effort as both in 2009. But one cannot be sure since the Indian policy

tradition is one of being re-active than pro-active!

21

Let me conclude with drawing your attention to the depth and foresight of RV’s

analysis of inflation and anti-inflationary policies by noting that the current Finance

Minister Pranab Mukherjee in his suo motu statement in Parliament on November 23,

2011 said in effect the same things as RV had said in his speech presenting the 1982 -83

budget. After listing the fiscal and monetary policy actions already taken Mukherjee went

on to describe what more needs to be done to check inflation, “a durable solution to

inflation in an economy with rising income levels lay in improving agricultural

productivity, strengthen food supply chains and augmenting capacities in manufacturing

sector in pace with the growth in demand. It requires a facilitative policy environment,

increased public investments so that these measures can be actively pursued”. These

tasks are almost the same as those in RV’s policy agenda three decades ago.

22

REFERENCES

Bannerjee, B.M., G.D. Parikh, and V.M. Tarkunde. (1944). People’s Plan for Economic

Development of India. Bombay: Indian Federation of Labour.

Basu, Kaushik (2011a), “Understanding Inflation and Controlling it”, Economic and

Political Weekly, Vol.46, No.41, Oct 8-14, 2011. 50-64.

Basu, Kaushik (2011b), “India’s Foodgrain Policy: An Economic Theory Perspective”,

Economic and Political Weekly, Vol.46, No.5, Jan 29, 2011, 37-48.

Business Line (2011). ”inflation Would Have Been Higher If Not for Monetary Tightening:

RBI Chief” www.thehindubusinessline.com/today’s-paper/tp-money-

banking/rticle2702363.ece.

CNN-IBN Live (2011). “High Inflation Blow to Govt’s Credibility: Montek

Ahluwalia”,http://ibnlive.in.com/news/high-inflation-bloe-togovts-credibility-

ahluwalia/203946-3.html

Government of India (1980), “Speech of Shri R. Venkataraman, Minister of Finance,

Introducing the Budget for the Year 1980-81 (Final)”, June 18, 1980.

Government of India (1981), “Speech of Shri R. Venkataraman, Minister of Finance,

Introducing the Budget for the Year 1981-82”, February 28, 1981.

IIAPR (1988). Report of the National Planning Committee, 1938. New Delhi, Indian

Institute of Applied Political Research.

Mohanty, D. (2011a). “How does the Reserve Bank of India Conduct its Monetary Policy?”

Speech by Deepak Mohanty, Executive Director, Reserve Bank of India, delivered

at the Indian Institute of Management (IIM), Lucknow on August 12, 2011.

Mohanty, D. (2011b). “Changing Inflation Dynamics in India” Speech by Deepak

Mohanty, Executive Director, Reserve Bank of India, delivered at the Motilal Nehru

National Institute of Technology (MNNIT), Allahabad on August 13, 2011.

23

Mohanty, D. (2011c). “Monetary Policy Response to Recent Inflation in India” - Speech

by Deepak Mohanty, Executive Director, Reserve Bank of India, delivered at the

Indian Institute of Technology (IIT), Guwahati on 3rd September, 2011.

Naoroji, D. (1899). Poverty and Un-British Rule in India, New York, Swan and

Sonnenschein. This is the published version of the 1872 Note of Naoroji as a

member to the Select Committee on Indian Finance of the British House of

Commons.

Rakshit, Mihir (2011). “Inflation and Relative prices in 2006-10: Some Analytical and

Policy Issues”. Economic and Political Weekly, Vol 46, No 16, April 16, 2011. 41-

54.

Srinivasan, T.N. (2008a). “Price Indices and Inflation Rates”, Economic and Political

Weekly, June 28, 2008, 217-223.

Srinivasan, T.N. (2008b), “Some Aspects of Price Indices, Inflation Rates and the Services

Sector in National Income Statistics” in N.Jayram and R.S. Deshpande (Eds.). In

Footprints of Development and Change: Essays in memory of Professor V.K.R.V.

Rao. New Delhi, Academic Foundation, 2008, 437-474.

Srinivasan T.N. (2011a). “Trends in Wholesale Prices in India” unpublished draft.

Srinivasan T.N. (2011b) “Growth Sustainability and India’s Economic Reform, New Delhi,

Oxford University Press.

Thakurdas,P., J.Tata, G.Birla, A. Dalal, S. Shriram, K. Lalbhai, A.Shroff and J. Mathai

(1944), A Plan of Economic Development of India, London, Penguin Books.