ReAssure Ltd · Form 2 Statement of solvency - long-term insurance business Name of insurer...

245

ReAssure Ltd Annual PRA Insurance Returns for the year ended 31 December 2015 IPRU(INS) Appendices 9.1, 9.2, 9.3, 9.4, 9.4A, 9.5, 9.6

Transcript of ReAssure Ltd · Form 2 Statement of solvency - long-term insurance business Name of insurer...

ReAssure Ltd

Annual PRA Insurance Returns for the year ended

31 December 2015

IPRU(INS) Appendices 9.1, 9.2, 9.3, 9.4, 9.4A, 9.5, 9.6

Contents

Balance Sheet and Profit and Loss Account

Form 1 Statement of solvency - general insurance business 1

Form 2 Statement of solvency - long-term insurance business 2

Form 3 Components of capital resources 3

Form 11 Calculation of general insurance capital requirement - premiums

amount and brought forward amount

6

Form 12 Calculation of general insurance capital requirement - claims

amount and result

8

Form 13 Analysis of admissible assets 10

Form 14 Long term insurance business liabilities and margins 25

Form 15 Liabilities (other than long term insurance business) 29

Form 16 Profit and loss account (non-technical account) 30

Form 18 With-profits insurance capital component for the fund 31

Form 19 Realistic balance sheet 33

General Insurance Business: Revenue Account and Additional Information

Form 20A Summary of business carried on 37

Form 20 Technical account (excluding equalisation provisions) 40

Form 21 Accident year accounting: Analysis of premiums 43

Form 22 Accident year accounting: Analysis of claims, expenses and

technical provisions

46

Form 23 Accident year accounting: Analysis of net claims and premiums 49

Form 31 Accident year accounting: Analysis of gross claims and premiums

by risk category for direct insurance and facultative reinsurance

52

Long Term Insurance Business: Revenue Account and Additional Information

Form 40 Revenue account 53

Form 41 Analysis of premiums 57

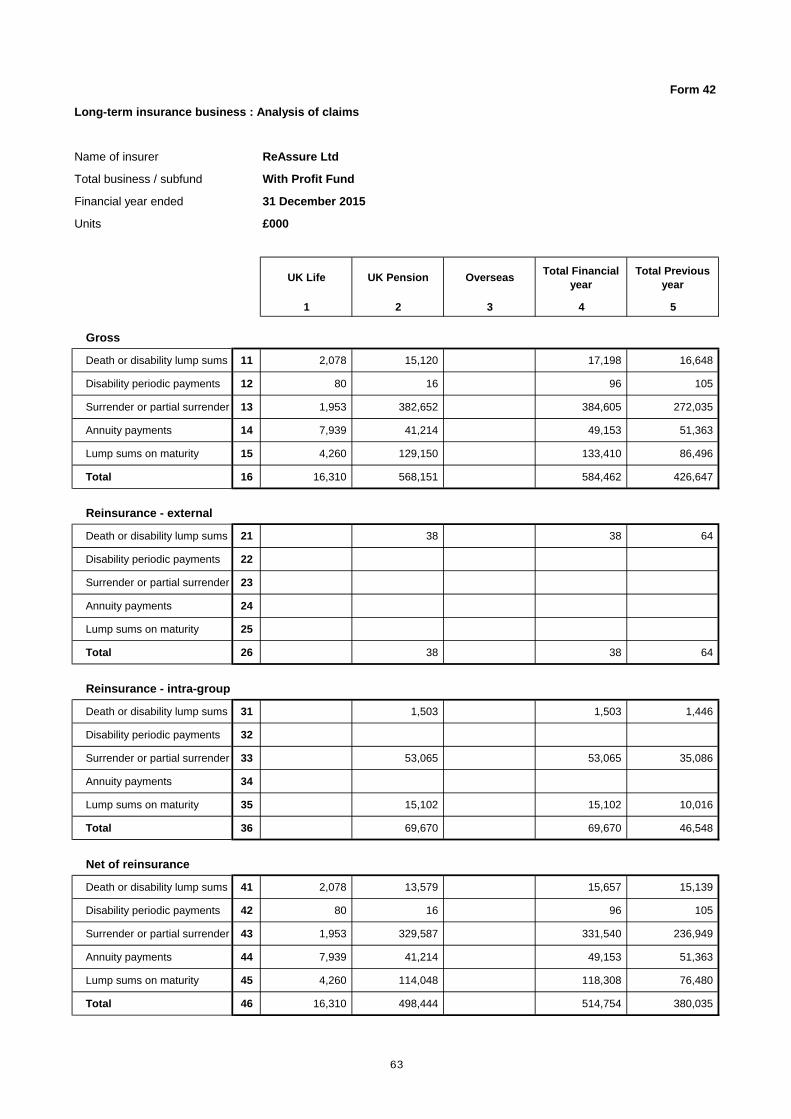

Form 42 Analysis of claims 61

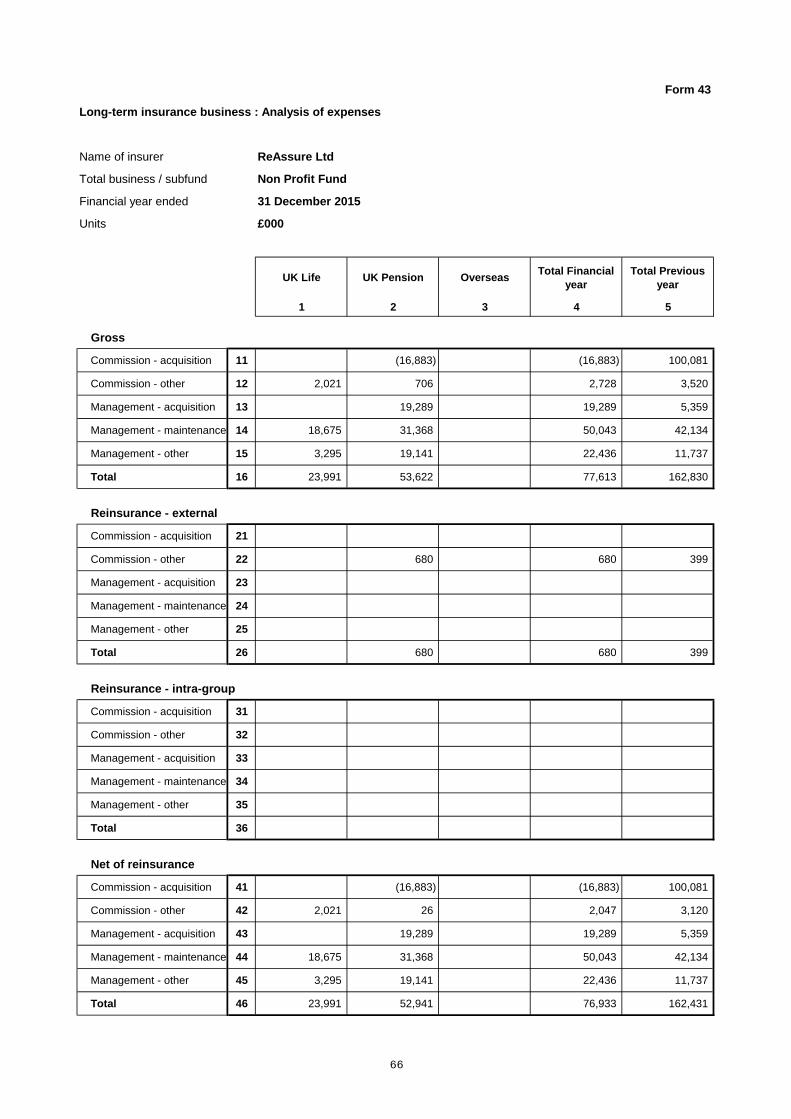

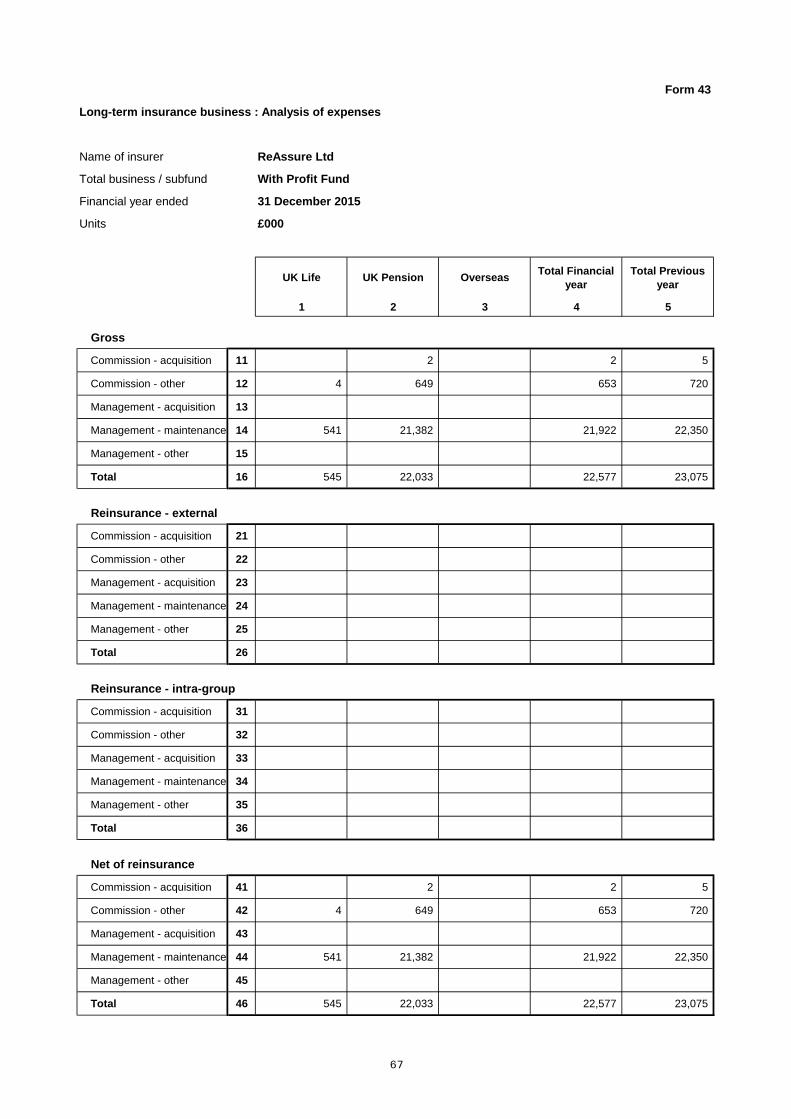

Form 43 Analysis of expenses 65

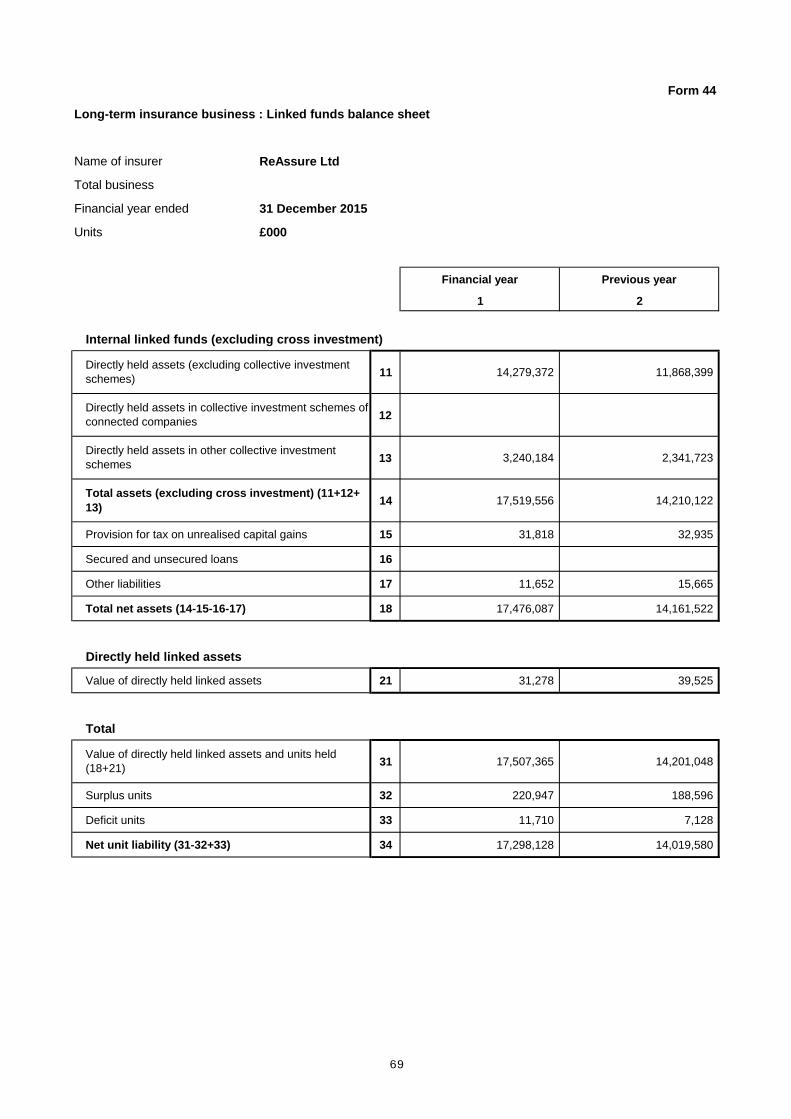

Form 44 Linked funds balance sheet 69

Form 45 Revenue account for internal linked funds 70

Form 46 Summary of new business 71

Form 47 Analysis of new business 72

Form 48 Assets not held to match linked liabilities 75

Form 49 Fixed and variable interest assets 79

Form 50 Summary of mathematical reserves 83

Form 51 Valuation summary of non-linked contracts (other than

accumulating with-profits contracts)

87

Form 52 Valuation summary of accumulating with-profits contracts 104

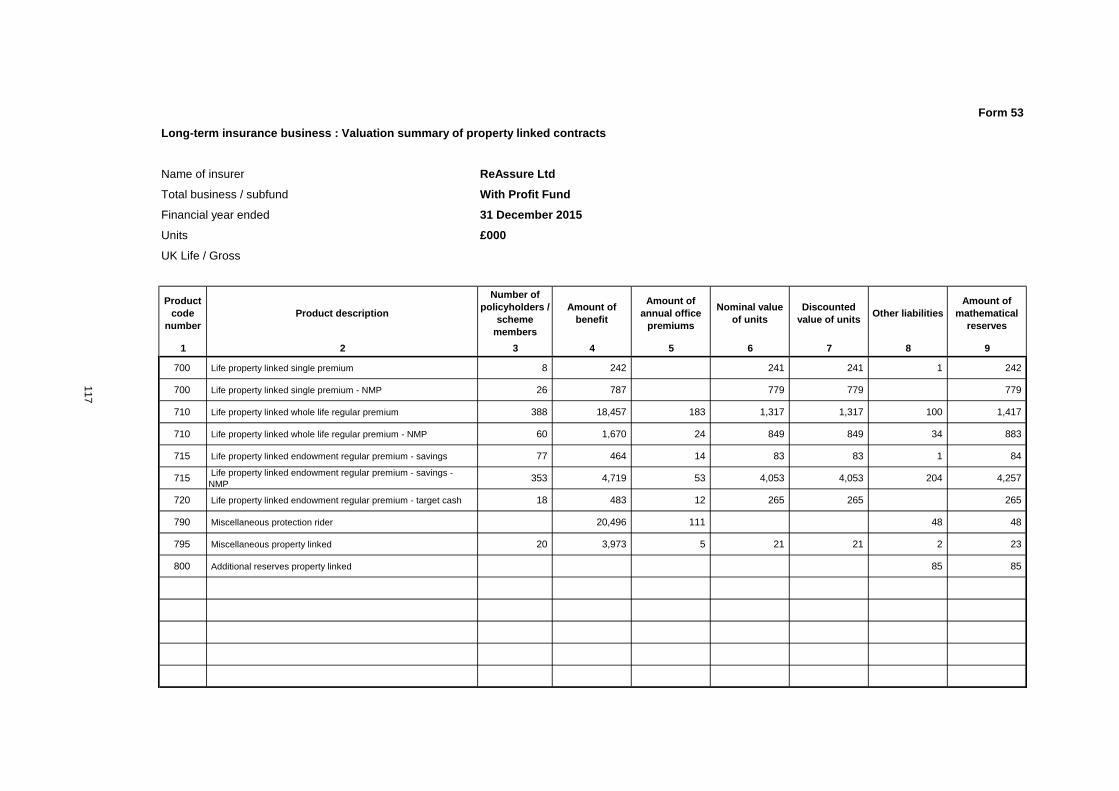

Form 53 Valuation summary of property linked contracts 110

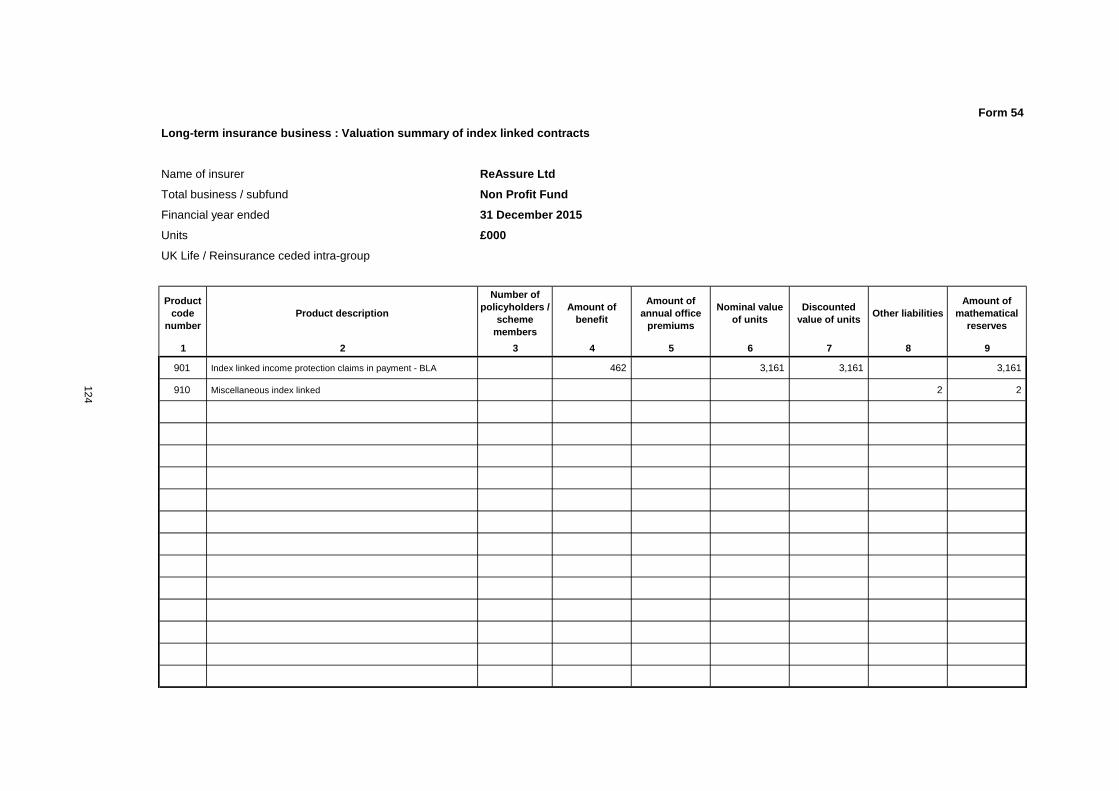

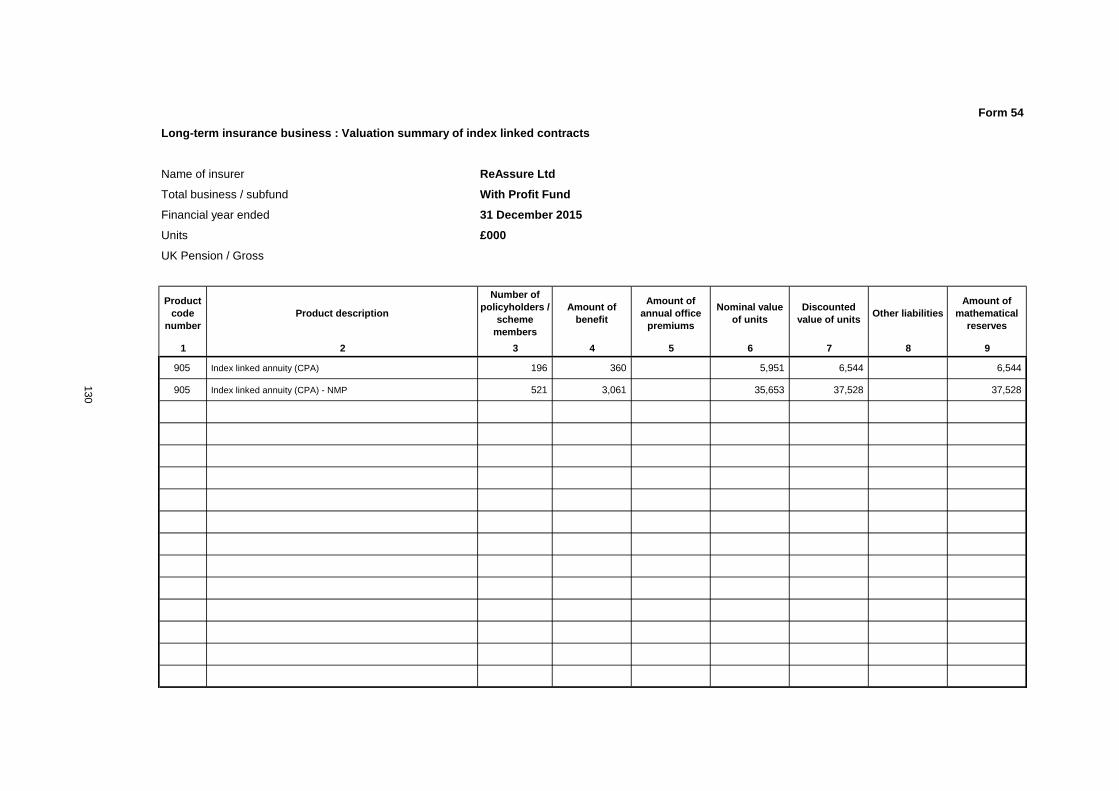

Form 54 Valuation summary of index linked contracts 122

Form 55 Unit prices for internal linked funds 131

Form 56 Index linked business 133

Form 57 Analysis of valuation interest rate 134

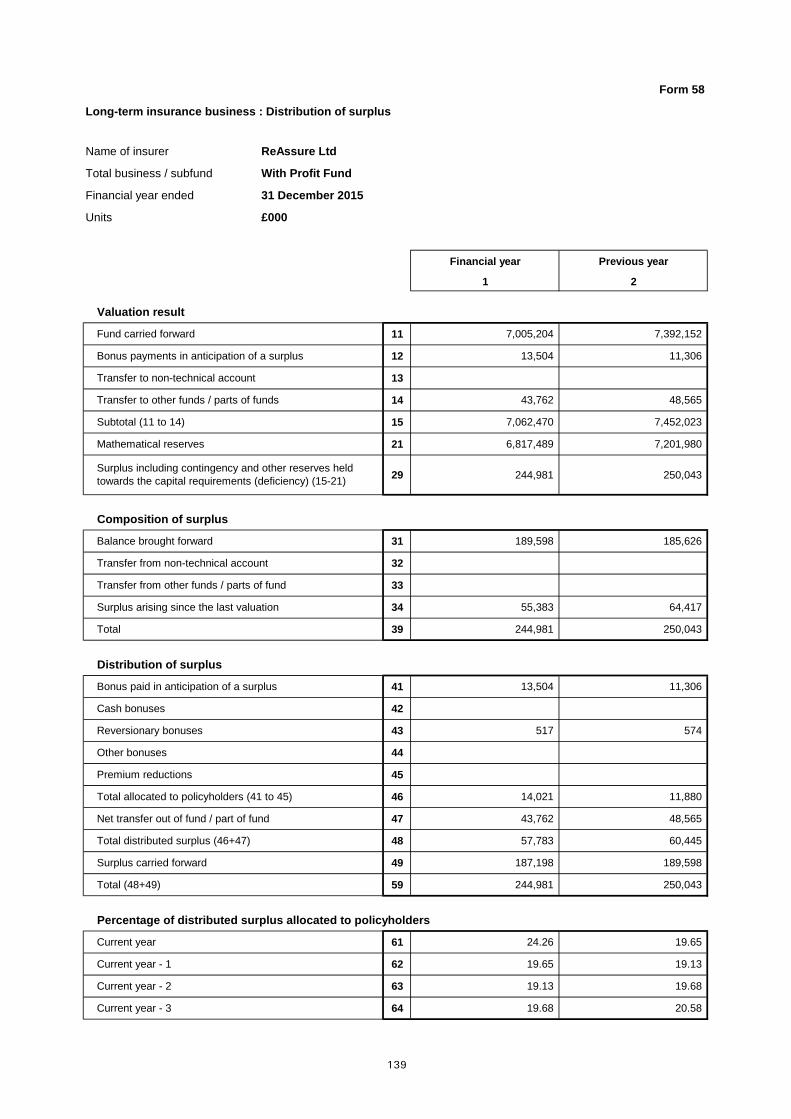

Form 58 Distribution of surplus 137

Form 59A/B With-profits payouts on maturity / surrender 141

Form 60 Long-term insurance capital requirement 145

Supplementary notes to the return 147

Additional information on reinsurance business 156

Additional information on derivative contracts 157

Additional information on controllers 158

Abstract of the Valuation Report 159

Abstract of the Realistic Report 215

Directors' Certificate 238

Auditor's Report 240

Form 1

Statement of solvency - general insurance business

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Solo solvency calculation Company GL/

registration UK/ day month year Units

number CM

R1 754167 GL 31 12 2015 £000

As at end of As at end of

this financial the previous

year year

1 2

Capital resources

Capital resources arising outside the long-term insurance fund 11 460,558 740,504

12 457,901 737,602

13 2,657 2,902

Guarantee fund

Guarantee fund requirement 21 2,657 2,902

22

Minimum capital requirement (MCR)

General insurance capital requirement 31 272 272

Base capital resources requirement 33 2,657 2,902

Individual minimum capital requirement 34 2,657 2,902

Capital requirements of regulated related undertakings 35

Minimum capital requirement (34+35) 36 2,657 2,902

Excess (deficiency) of available capital resources to cover 50% of MCR 37 1,329 1,451

Excess (deficiency) of available capital resources to cover 75% of MCR 38 664 725

Capital resources requirement (CRR)

Capital resources requirement 41 2,657 2,902

42

Contingent liabilities

51

Capital resources allocated towards long-term insurance business arising

outside the long-term insurance fund

Capital resources available to cover general insurance business capital

resources requirement (11-12)

Excess (deficiency) of available capital resources to cover guarantee fund

requirement

Excess (deficiency) of available capital resources to cover general

insurance business CRR (13-41)

Quantifiable contingent liabilities in respect of other than long-term

insurance business as shown in a supplementary note to Form 15

1

Form 2

Statement of solvency - long-term insurance business

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Solo solvency calculation Company GL/

registration UK/ day month year Units

number CM

R2 754167 GL 31 12 2015 £000

As at end of As at end of

this financial the previous

year year

1 2

Capital resources

Capital resources arising within the long-term insurance fund 11 1,590,991 1,330,813

12 457,901 737,602

13 2,048,892 2,068,415

Guarantee fund

Guarantee fund requirement 21 141,026 141,743

22 1,907,866 1,926,671

Minimum capital requirement (MCR)

Long-term insurance capital requirement 31 423,076 425,229

Resilience capital requirement 32

Base capital resources requirement 33 2,657 2,902

Individual minimum capital requirement 34 423,076 425,229

Capital requirements of regulated related undertakings 35

Minimum capital requirement (34+35) 36 423,076 425,229

Excess (deficiency) of available capital resources to cover 50% of MCR 37 1,837,354 1,855,799

Excess (deficiency) of available capital resources to cover 75% of MCR 38 1,731,585 1,749,492

Enhanced capital requirement

With-profits insurance capital component 39 750,957 775,803

Enhanced capital requirement 40 1,174,033 1,201,032

Capital resources requirement (CRR)

Capital resources requirement (greater of 36 and 40) 41 1,174,033 1,201,032

42 874,859 867,382

Contingent liabilities

51

Capital resources allocated towards long-term insurance business arising

outside the long-term insurance fund

Capital resources available to cover long-term insurance business capital

resources requirement (11+12)

Excess (deficiency) of available capital resources to cover guarantee fund

requirement

Excess (deficiency) of available capital resources to cover long-term

insurance business CRR (13-41)

Quantifiable contingent liabilities in respect of long-term insurance business

as shown in a supplementary note to Form 14

2

Form 3

(Sheet 1)

Components of capital resources

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Company GL/

registration UK/ Units number CM

R3 GL 31 12 2015 £000

General Long-term Total as at Total as at

insurance insurance the end of the end of

business business this financial the previous

year year

1 2 3 4

Core tier one capital

Permanent share capital 11 288,868 288,868 288,868

Profit and loss account and other reserves 12 2,657 1,017,356 1,020,013 880,296

13 134,075 134,075 134,075

Positive valuation differences 14 751,068 751,068 880,303

15 11,864 11,864 11,687

16

Core tier one capital (sum of 11 to 16) 19 2,657 2,203,231 2,205,888 2,195,229

Tier one waivers

21

Implicit Items 22

Tier one waivers in related undertakings 23

24

Other tier one capital

25

26

27

28

31 2,657 2,203,231 2,205,888 2,195,229

32

33

34

35

36

37

39 2,657 2,203,231 2,205,888 2,195,229

day month year

754167

Share premium account

Fund for future appropriations

Core tier one capital in related undertakings

Unpaid share capital / unpaid initial funds and calls for

supplementary contributions

Total tier one waivers as restricted (21+22+23)

Perpetual non-cumulative preference shares as restricted

Perpetual non-cumulative preference shares in related

undertakings

Innovative tier one capital as restricted

Innovative tier one capital in related undertakings

Deductions from tier one (32 to 36)

Total tier one capital after deductions (31-37)

Total tier one capital before deductions

(19+24+25+26+27+28)

Investments in own shares

Intangible assets

Amounts deducted from technical provisions for discounting

Other negative valuation differences

Deductions in related undertakings

3

Form 3

(Sheet 2)

Components of capital resources

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Company GL/

registration UK/ Units number CM

R3 GL 31 12 2015 £000

General Long-term Total as at Total as at

insurance insurance the end of the end of

business business this financial the previous

year year

1 2 3 4

Tier two capital

41

42

43

44

45

46

Upper tier two capital in related undertakings 47

Upper tier two capital (44 to 47) 49

Fixed term preference shares 51

Other tier two instruments 52 100,000

Lower tier two capital in related undertakings 53

Lower tier two capital (51+52+53) 59 100,000

61 100,000

Excess tier two capital 62

63

69 100,000

day month year

754167

Implicit items, (tier two waivers and amounts excluded from

line 22)

Perpetual non-cumulative preference shares excluded from

line 25

Innovative tier one capital excluded from line 27

Tier two waivers, innovative tier one capital and perpetual

non-cumulative preference shares treated as tier two capital

(41 to 43)

Perpetual cumulative preference shares

Perpetual subordinated debt and securities

Total tier two capital before restrictions (49+59)

Further excess lower tier two capital

Total tier two capital after restrictions, before

deductions (61-62-63)

4

Form 3

(Sheet 3)

Components of capital resources

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Company GL/

registration UK/ Units number CM

R3 GL 31 12 2015 £000

General Long-term Total as at Total as at

insurance insurance the end of the end of

business business this financial the previous

year year

1 2 3 4

Total capital resources

71

72 2,657 2,203,231 2,205,888 2,295,229

73 154,339 154,339 223,913

74

75

76

77

79 2,657 2,048,892 2,051,549 2,071,316

Available capital resources for GENPRU/INSPRU tests

81 2,657 2,048,892 2,051,549 2,071,316

82 2,657 2,048,892 2,051,549 2,071,316

83 2,657 2,048,892 2,051,549 2,071,316

Financial engineering adjustments

91

92

93

94

95

96

day month year

754167

Positive adjustments for regulated non-insurance related

undertakings

Total capital resources before deductions

(39+69+71)

Inadmissible assets other than intangibles and own shares

Assets in excess of market risk and counterparty limits

Deductions for related ancillary services undertakings

Deductions for regulated non-insurance related undertakings

Deductions of ineligible surplus capital

Total capital resources after deductions

(72-73-74-75-76-77)

Available capital resources for guarantee fund requirement

Any other charges on future profits

Sum of financial engineering adjustments

(91+92-93+94+95)

Available capital resources for 50% MCR requirement

Available capital resources for 75% MCR requirement

Implicit items

Financial reinsurance - ceded

Financial reinsurance - accepted

Outstanding contingent loans

5

Form 11

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

General insurance business

Company GL/

registration UK/ day month year Unitsnumber CM

R11 754167 GL 31 12 2015 £000

This financial year Previous year1 2

11 48

12

13 48

14

15

16 48

21 58

22

23 58

24

25

26 58

30 58

31 58

32 10

33

34 10

41 2,162 2,824

42

43 499 499

44

45 2,215 2,278

46 446 1,045

47

48 446 1,045

49 1.00 1.00

50 10

51 499 499

52

53 272 272

54 272 272

Calculation of general insurance capital requirement - premiums amount and brought forward amount

Gross premiums written

Premiums taxes and levies (included in line 11)

Premiums written net of taxes and levies (11-12)

Premiums for classes 11, 12 or 13 (included in line 13)

Premiums for "actuarial health insurance" (included in line 13)

Sub-total A (13 + 1/2 14 - 2/3 15)

Gross premiums earned

Premium taxes and levies (included in line 21)

Premiums earned net of taxes and levies (21-22)

Premiums for classes 11, 12 or 13 (included in line 23)

Premiums for "actuarial health insurance" (included in line 23)

Sub-total H (23 + 1/2 24 - 2/3 25)

Sub-total I (higher of sub-total A and sub-total H)

Adjusted sub-total I if financial year is not a 12 month period to produce

an annual figure

Division of gross adjusted premiums

amount sub-total I

(or adjusted sub-total I if

appropriate)

x 0.18

Excess (if any) over 61.3M EURO x

0.02

Sub-total J (32-33)

Claims paid in period of 3 financial years

Claims outstanding carried

forward at the end of the 3

year period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Claims outstanding brought

forward at the beginning of

the 3 year period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Provision for claims outstanding (before discounting and gross of reinsurance) if

both 51.1 and 51.2 are zero, otherwise zero

Brought forward amount (See instruction 4)

Greater of lines 50 and 53

Sub-total C (41+42+43-44-45)

Amounts recoverable from reinsurers in respect of claims included

in Sub-total C

Sub-total D (46-47)

Reinsurance Ratio

(Sub-total D /sub-total C or, if more, 0.50 or, if less, 1.00)

Premiums amount (Sub-total J x reinsurance ratio)

Provision for claims outstanding (before discounting and net of

reinsurance

6

Form 11

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Long term insurance business

Company GL/

registration UK/ day month year Unitsnumber CM

R11 754167 GL 31 12 2015 £000

This financial year Previous year1 2

11 48,165 51,685

12

13 48,165 51,685

14

15 35,155 36,987

16 24,728 27,028

21 48,165 51,685

22

23 48,165 51,685

24

25 35,155 36,987

26 24,728 27,028

30 24,728 27,028

31

32 4,451 4,865

33

34 4,451 4,865

41 138,364 124,481

42

43 87,654 95,031

44

45 94,761 90,754

46 131,257 128,757

47 16,879 18,730

48 114,378 110,027

49 0.87 0.85

50 3,879 4,157

51 85,293 90,330

52

53 4,970 5,096

54 4,970 5,096

Calculation of general insurance capital requirement - premiums amount and brought forward amount

Gross premiums written

Premiums taxes and levies (included in line 11)

Premiums written net of taxes and levies (11-12)

Premiums for classes 11, 12 or 13 (included in line 13)

Premiums for "actuarial health insurance" (included in line 13)

Sub-total A (13 + 1/2 14 - 2/3 15)

Gross premiums earned

Premium taxes and levies (included in line 21)

Premiums earned net of taxes and levies (21-22)

Premiums for classes 11, 12 or 13 (included in line 23)

Premiums for "actuarial health insurance" (included in line 23)

Sub-total H (23 + 1/2 24 - 2/3 25)

Sub-total I (higher of sub-total A and sub-total H)

Adjusted sub-total I if financial year is not a 12 month period to produce

an annual figure

Division of gross adjusted premiums

amount sub-total I

(or adjusted sub-total I if

appropriate)

x 0.18

Excess (if any) over 61.3M EURO x

0.02

Sub-total J (32-33)

Claims paid in period of 3 financial years

Claims outstanding carried

forward at the end of the 3

year period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Claims outstanding brought

forward at the beginning of

the 3 year period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Provision for claims outstanding (before discounting and gross of reinsurance) if

both 51.1 and 51.2 are zero, otherwise zero

Brought forward amount (See instruction 4)

Greater of lines 50 and 53

Sub-total C (41+42+43-44-45)

Amounts recoverable from reinsurers in respect of claims included

in Sub-total C

Sub-total D (46-47)

Reinsurance Ratio

(Sub-total D /sub-total C or, if more, 0.50 or, if less, 1.00)

Premiums amount (Sub-total J x reinsurance ratio)

Provision for claims outstanding (before discounting and net of

reinsurance

7

Form 12

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

General insurance businessCompany GL/

registration UK/ day month year Units

number CM

R12 754167 GL 31 12 2015 £000

This financial year Previous year1 2

11 36 36

21 2,162 2,824

22

23 499 499

24

25 2,215 2,278

26 446 1,045

27

28

29 446 1,045

31 149 348

32 39 91

33

39 39 91

41 39 91

42 272 272

43 272 272

Calculation of general insurance capital requirement - claims amount and result

Reference period (No. of months) See INSPRU 1.1.63R

Claims paid in reference period

Claims outstanding carried

forward at the end of the

reference period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Claims outstanding brought

forward at the beginning of

the reference period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Claims incurred in reference period (21+22+23-24-25)

Claims incurred for classes 11, 12 or 13 (included in 26)

Claims incurred for "actuarial health insurance" (included in 26)

Claims amount Sub-total G x reinsurance ratio (11.49)

Higher of premiums amount and brought forward amount (11.54)

General insurance capital requirement (higher of lines 41 and 42)

Sub-total E (26 +1/2 27 - 2/3 28)

Sub-total F - Conversion of sub-total E to annual figure (multiply by

12 and divide by number of months in the reference period)

Division of sub-total F

(gross adjusted claims

amount)

x 0.26

Excess (if any) over 42.9M EURO x 0.03

Sub-total G (32-33)

8

Form 12

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Long term insurance businessCompany GL/

registration UK/ day month year Units

number CM

R12 754167 GL 31 12 2015 £000

This financial year Previous year1 2

11 36 36

21 138,364 124,481

22

23 87,654 95,031

24

25 94,761 90,754

26 131,257 128,757

27

28 92,002 86,524

29 69,922 71,075

31 23,307 23,692

32 6,060 6,160

33

39 6,060 6,160

41 5,281 5,264

42 4,970 5,096

43 5,281 5,264

Calculation of general insurance capital requirement - claims amount and result

Reference period (No. of months) See INSPRU 1.1.63R

Claims paid in reference period

Claims outstanding carried

forward at the end of the

reference period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Claims outstanding brought

forward at the beginning of

the reference period

For insurance business accounted for

on an underwriting year basis

For insurance business accounted for

on an accident year basis

Claims incurred in reference period (21+22+23-24-25)

Claims incurred for classes 11, 12 or 13 (included in 26)

Claims incurred for "actuarial health insurance" (included in 26)

Claims amount Sub-total G x reinsurance ratio (11.49)

Higher of premiums amount and brought forward amount (11.54)

General insurance capital requirement (higher of lines 41 and 42)

Sub-total E (26 +1/2 27 - 2/3 28)

Sub-total F - Conversion of sub-total E to annual figure (multiply by

12 and divide by number of months in the reference period)

Division of sub-total F

(gross adjusted claims

amount)

x 0.26

Excess (if any) over 42.9M EURO x 0.03

Sub-total G (32-33)

9

Form 13

(Sheet 1)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Total other than long term insurance business assets

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 1

As at end of this

financial year

As at end of the

previous year

1 2

Land and buildings 11 3,000 3,000

21

22

23

24

25 103 103

26

27

28

29

30

Other financial investments

Equity shares 41

Other shares and other variable yield participations 42

Holdings in collective investment schemes 43

Rights under derivative contracts 44 (28)

45 435,302 408,861

46

47

48

Participation in investment pools 49

Loans secured by mortgages 50

51

52

Other loans 53

54 3,996 316,827

55

Other financial investments 56

Deposits with ceding undertakings 57

58

59

Investments in group undertakings and participating interests

UK insurance dependantsShares

Debts and loans

Other insurance dependantsShares

Debts and loans

Non-insurance dependantsShares

Debts and loans

Other group undertakingsShares

Debts and loans

More than one month withdrawal

Participating interestsShares

Debts and loans

Fixed interest securitiesApproved

Other

Assets held to match linked liabilitiesIndex linked

Property linked

Variable interest securitiesApproved

Other

Loans to public or local authorities and nationalised industries or

undertakings

Loans secured by policies of insurance issued by the company

Bank and approved credit & financial

institution deposits

One month or less withdrawal

10

Form 13

(Sheet 2)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Total other than long term insurance business assets

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 1

As at end of this

financial year

As at end of the

previous year

1 2

60

61

62

63

71

72

73

74

75

76

77

78 11,947 5,256

79

80

81 3,009 2,019

82

83

84 4,198 5,869

85

86

87

89 461,554 741,906

Reinsurers' share of technical provisions

Provision for unearned premiums

Claims outstanding

Provision for unexpired risks

Other

Debtors and salvage

Direct insurance businessPolicyholders

Intermediaries

Salvage and subrogation recoveries

ReinsuranceAccepted

Ceded

Dependantsdue in 12 months or less

due in more than 12 months

Otherdue in 12 months or less

due in more than 12 months

Deferred acquisition costs (general business only)

Other prepayments and accrued income

Deductions from the aggregate value of assets

Grand total of admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (11 to 86 less 87)

Other assets

Tangible assets

Deposits not subject to time restriction on withdrawal with approved

institutions

Cash in hand

Other assets (particulars to be specified by way of supplementary note)

Accrued interest and rent

11

Form 13

(Sheet 3)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Total other than long term insurance business assets

Company GL/ Category

registration UK/ day month year Units ofnumber CM assets

R13 754167 GL 31 12 2015 £000 1

As at end of this

financial year

As at end of the

previous year

1 2

91 461,554 741,906

92

93

94

95

96

97

98 (1,401)

99

100

101

102 461,554 740,505

103

Reconciliation to asset values determined in accordance

with the insurance accounts rules or international

accounting standards as applicable to the firm for the

purpose of its external financial reporting

Total admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (as per line 89 above)

Admissible assets in excess of market and counterparty limits

Inadmissible assets directly held

Capital resources requirement deduction of regulated related

undertakings

Ineligible surplus capital and restricted assets in regulated related

insurance undertakings

Total assets determined in accordance with the insurance accounts

rules or international accounting standards as applicable to the firm

for the purpose of its external financial reporting (91 to 101)

Amounts included in line 89 attributable to debts due from related

insurers, other than those under contracts of insurance or reinsurance

Inadmissible assets of regulated related undertakings

Book value of related ancillary services undertakings

Other differences in the valuation of assets (other than for assets

not valued above)

Deferred acquisition costs excluded from line 89

Reinsurers' share of technical provisions excluded from line 89

Other asset adjustments (may be negative)

12

Form 13

(Sheet 1)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

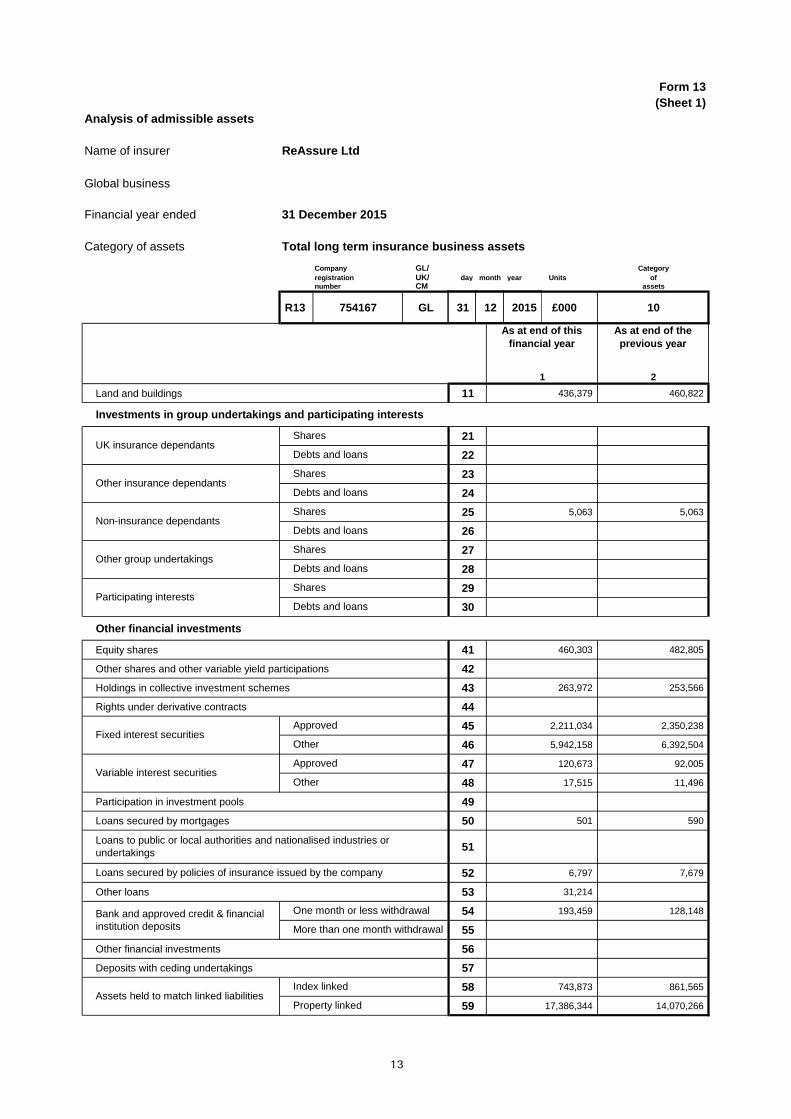

Category of assets Total long term insurance business assets

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 10

As at end of this

financial year

As at end of the

previous year

1 2

Land and buildings 11 436,379 460,822

21

22

23

24

25 5,063 5,063

26

27

28

29

30

Other financial investments

Equity shares 41 460,303 482,805

Other shares and other variable yield participations 42

Holdings in collective investment schemes 43 263,972 253,566

Rights under derivative contracts 44

45 2,211,034 2,350,238

46 5,942,158 6,392,504

47 120,673 92,005

48 17,515 11,496

Participation in investment pools 49

Loans secured by mortgages 50 501 590

51

52 6,797 7,679

Other loans 53 31,214

54 193,459 128,148

55

Other financial investments 56

Deposits with ceding undertakings 57

58 743,873 861,565

59 17,386,344 14,070,266

Investments in group undertakings and participating interests

UK insurance dependantsShares

Debts and loans

Other insurance dependantsShares

Debts and loans

Non-insurance dependantsShares

Debts and loans

Other group undertakingsShares

Debts and loans

More than one month withdrawal

Participating interestsShares

Debts and loans

Fixed interest securitiesApproved

Other

Assets held to match linked liabilitiesIndex linked

Property linked

Variable interest securitiesApproved

Other

Loans to public or local authorities and nationalised industries or

undertakings

Loans secured by policies of insurance issued by the company

Bank and approved credit & financial

institution deposits

One month or less withdrawal

13

Form 13

(Sheet 2)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Total long term insurance business assets

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 10

As at end of this

financial year

As at end of the

previous year

1 2

60

61

62

63

71

72

73

74

75 6,646 12,554

76

77

78 186,790 72,977

79

80

81 101,468 98,821

82

83

84 148,816 149,245

85

86 991 2,469

87

89 28,263,996 25,452,813

Reinsurers' share of technical provisions

Provision for unearned premiums

Claims outstanding

Provision for unexpired risks

Other

Debtors and salvage

Direct insurance businessPolicyholders

Intermediaries

Salvage and subrogation recoveries

ReinsuranceAccepted

Ceded

Dependantsdue in 12 months or less

due in more than 12 months

Otherdue in 12 months or less

due in more than 12 months

Deferred acquisition costs (general business only)

Other prepayments and accrued income

Deductions from the aggregate value of assets

Grand total of admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (11 to 86 less 87)

Other assets

Tangible assets

Deposits not subject to time restriction on withdrawal with approved

institutions

Cash in hand

Other assets (particulars to be specified by way of supplementary note)

Accrued interest and rent

14

Form 13

(Sheet 3)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Total long term insurance business assets

Company GL/ Category

registration UK/ day month year Units ofnumber CM assets

R13 754167 GL 31 12 2015 £000 10

As at end of this

financial year

As at end of the

previous year

1 2

91 28,263,995 25,452,813

92

93 47,270 111,229

94

95

96

97

98 (224) (224)

99 112,684

100 767,287 583,025

101 17,905 99,436

102 29,096,234 26,358,962

103 15,671 9,862

Reconciliation to asset values determined in accordance

with the insurance accounts rules or international

accounting standards as applicable to the firm for the

purpose of its external financial reporting

Total admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (as per line 89 above)

Admissible assets in excess of market and counterparty limits

Inadmissible assets directly held

Capital resources requirement deduction of regulated related

undertakings

Ineligible surplus capital and restricted assets in regulated related

insurance undertakings

Total assets determined in accordance with the insurance accounts

rules or international accounting standards as applicable to the firm

for the purpose of its external financial reporting (91 to 101)

Amounts included in line 89 attributable to debts due from related

insurers, other than those under contracts of insurance or reinsurance

Inadmissible assets of regulated related undertakings

Book value of related ancillary services undertakings

Other differences in the valuation of assets (other than for assets

not valued above)

Deferred acquisition costs excluded from line 89

Reinsurers' share of technical provisions excluded from line 89

Other asset adjustments (may be negative)

15

Form 13

(Sheet 1)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets With Profit Fund

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 21

As at end of this

financial year

As at end of the

previous year

1 2

Land and buildings 11 57,322 58,136

21

22

23

24

25

26

27

28

29

30

Other financial investments

Equity shares 41 53,631 57,876

Other shares and other variable yield participations 42

Holdings in collective investment schemes 43 58,265 65,350

Rights under derivative contracts 44

45 651,217 269,923

46 231,650 635,893

47 9,110

48 6,467

Participation in investment pools 49

Loans secured by mortgages 50

51

52 40 259

Other loans 53

54 11,943 309

55

Other financial investments 56

Deposits with ceding undertakings 57

58 130,205 150,256

59 5,881,004 6,190,846

Investments in group undertakings and participating interests

UK insurance dependantsShares

Debts and loans

Other insurance dependantsShares

Debts and loans

Non-insurance dependantsShares

Debts and loans

Other group undertakingsShares

Debts and loans

More than one month withdrawal

Participating interestsShares

Debts and loans

Fixed interest securitiesApproved

Other

Assets held to match linked liabilitiesIndex linked

Property linked

Variable interest securitiesApproved

Other

Loans to public or local authorities and nationalised industries or

undertakings

Loans secured by policies of insurance issued by the company

Bank and approved credit & financial

institution deposits

One month or less withdrawal

16

Form 13

(Sheet 2)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets With Profit Fund

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 21

As at end of this

financial year

As at end of the

previous year

1 2

60

61

62

63

71

72

73

74

75

76

77

78 1,608 5,734

79

80

81 1,688 2,939

82

83

84 11,331 14,000

85

86 113 96

87

89 7,105,593 7,451,619

Reinsurers' share of technical provisions

Provision for unearned premiums

Claims outstanding

Provision for unexpired risks

Other

Debtors and salvage

Direct insurance businessPolicyholders

Intermediaries

Salvage and subrogation recoveries

ReinsuranceAccepted

Ceded

Dependantsdue in 12 months or less

due in more than 12 months

Otherdue in 12 months or less

due in more than 12 months

Deferred acquisition costs (general business only)

Other prepayments and accrued income

Deductions from the aggregate value of assets

Grand total of admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (11 to 86 less 87)

Other assets

Tangible assets

Deposits not subject to time restriction on withdrawal with approved

institutions

Cash in hand

Other assets (particulars to be specified by way of supplementary note)

Accrued interest and rent

17

Form 13

(Sheet 3)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets With Profit Fund

Company GL/ Category

registration UK/ day month year Units ofnumber CM assets

R13 754167 GL 31 12 2015 £000 21

As at end of this

financial year

As at end of the

previous year

1 2

91 7,105,593 7,451,619

92

93

94

95

96

97

98

99

100

101

102 7,105,593 7,451,619

103

Reconciliation to asset values determined in accordance

with the insurance accounts rules or international

accounting standards as applicable to the firm for the

purpose of its external financial reporting

Total admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (as per line 89 above)

Admissible assets in excess of market and counterparty limits

Inadmissible assets directly held

Capital resources requirement deduction of regulated related

undertakings

Ineligible surplus capital and restricted assets in regulated related

insurance undertakings

Total assets determined in accordance with the insurance accounts

rules or international accounting standards as applicable to the firm

for the purpose of its external financial reporting (91 to 101)

Amounts included in line 89 attributable to debts due from related

insurers, other than those under contracts of insurance or reinsurance

Inadmissible assets of regulated related undertakings

Book value of related ancillary services undertakings

Other differences in the valuation of assets (other than for assets

not valued above)

Deferred acquisition costs excluded from line 89

Reinsurers' share of technical provisions excluded from line 89

Other asset adjustments (may be negative)

18

Form 13

(Sheet 1)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

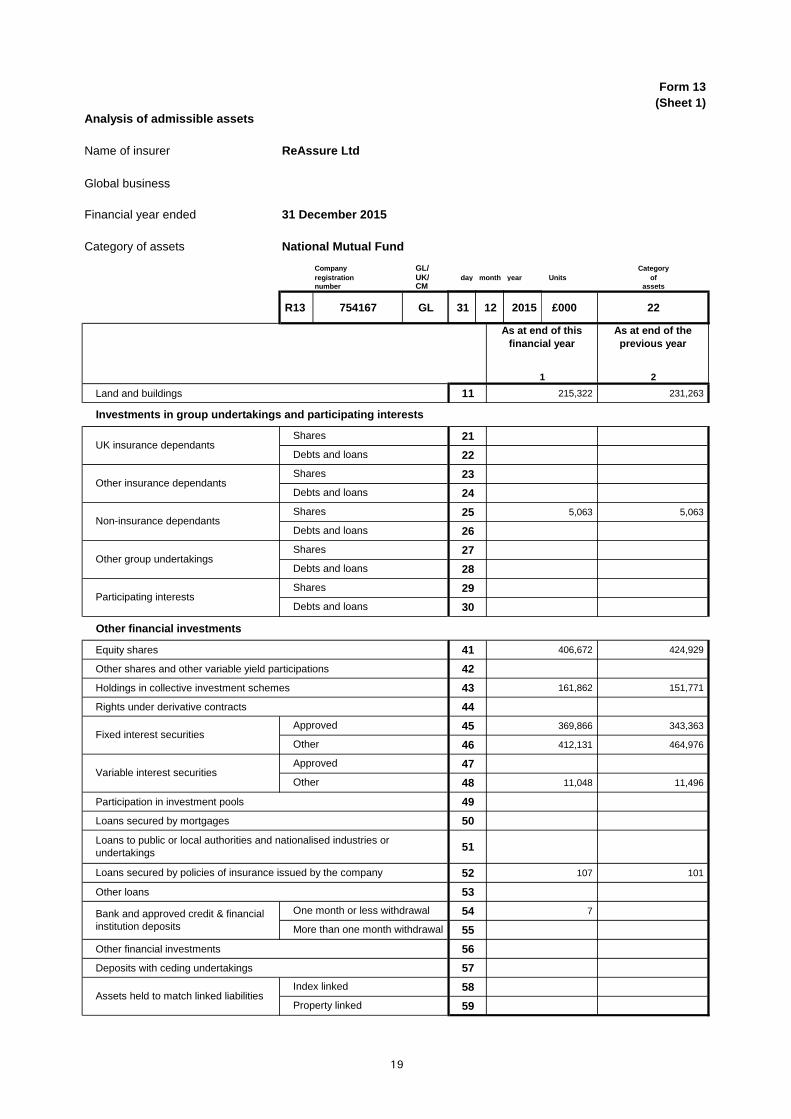

Category of assets National Mutual Fund

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 22

As at end of this

financial year

As at end of the

previous year

1 2

Land and buildings 11 215,322 231,263

21

22

23

24

25 5,063 5,063

26

27

28

29

30

Other financial investments

Equity shares 41 406,672 424,929

Other shares and other variable yield participations 42

Holdings in collective investment schemes 43 161,862 151,771

Rights under derivative contracts 44

45 369,866 343,363

46 412,131 464,976

47

48 11,048 11,496

Participation in investment pools 49

Loans secured by mortgages 50

51

52 107 101

Other loans 53

54 7

55

Other financial investments 56

Deposits with ceding undertakings 57

58

59

Investments in group undertakings and participating interests

UK insurance dependantsShares

Debts and loans

Other insurance dependantsShares

Debts and loans

Non-insurance dependantsShares

Debts and loans

Other group undertakingsShares

Debts and loans

More than one month withdrawal

Participating interestsShares

Debts and loans

Fixed interest securitiesApproved

Other

Assets held to match linked liabilitiesIndex linked

Property linked

Variable interest securitiesApproved

Other

Loans to public or local authorities and nationalised industries or

undertakings

Loans secured by policies of insurance issued by the company

Bank and approved credit & financial

institution deposits

One month or less withdrawal

19

Form 13

(Sheet 2)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets National Mutual Fund

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 22

As at end of this

financial year

As at end of the

previous year

1 2

60

61

62

63

71

72

73

74

75

76

77

78 380 510

79

80

81 2,665 4,400

82

83

84 12,697 9,952

85

86 850 754

87

89 1,598,669 1,648,578

Reinsurers' share of technical provisions

Provision for unearned premiums

Claims outstanding

Provision for unexpired risks

Other

Debtors and salvage

Direct insurance businessPolicyholders

Intermediaries

Salvage and subrogation recoveries

ReinsuranceAccepted

Ceded

Dependantsdue in 12 months or less

due in more than 12 months

Otherdue in 12 months or less

due in more than 12 months

Deferred acquisition costs (general business only)

Other prepayments and accrued income

Deductions from the aggregate value of assets

Grand total of admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (11 to 86 less 87)

Other assets

Tangible assets

Deposits not subject to time restriction on withdrawal with approved

institutions

Cash in hand

Other assets (particulars to be specified by way of supplementary note)

Accrued interest and rent

20

Form 13

(Sheet 3)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets National Mutual Fund

Company GL/ Category

registration UK/ day month year Units ofnumber CM assets

R13 754167 GL 31 12 2015 £000 22

As at end of this

financial year

As at end of the

previous year

1 2

91 1,598,669 1,648,578

92

93

94

95

96

97

98 (224) (224)

99

100

101

102 1,598,445 1,648,354

103

Reconciliation to asset values determined in accordance

with the insurance accounts rules or international

accounting standards as applicable to the firm for the

purpose of its external financial reporting

Total admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (as per line 89 above)

Admissible assets in excess of market and counterparty limits

Inadmissible assets directly held

Capital resources requirement deduction of regulated related

undertakings

Ineligible surplus capital and restricted assets in regulated related

insurance undertakings

Total assets determined in accordance with the insurance accounts

rules or international accounting standards as applicable to the firm

for the purpose of its external financial reporting (91 to 101)

Amounts included in line 89 attributable to debts due from related

insurers, other than those under contracts of insurance or reinsurance

Inadmissible assets of regulated related undertakings

Book value of related ancillary services undertakings

Other differences in the valuation of assets (other than for assets

not valued above)

Deferred acquisition costs excluded from line 89

Reinsurers' share of technical provisions excluded from line 89

Other asset adjustments (may be negative)

21

Form 13

(Sheet 1)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Non Profit Fund

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 31

As at end of this

financial year

As at end of the

previous year

1 2

Land and buildings 11 163,735 171,424

21

22

23

24

25

26

27

28

29

30

Other financial investments

Equity shares 41

Other shares and other variable yield participations 42

Holdings in collective investment schemes 43 43,845 36,445

Rights under derivative contracts 44

45 1,189,952 1,736,951

46 5,298,377 5,291,634

47 111,563 92,005

48

Participation in investment pools 49

Loans secured by mortgages 50 501 590

51

52 6,651 7,319

Other loans 53 31,214

54 181,509 127,839

55

Other financial investments 56

Deposits with ceding undertakings 57

58 613,668 711,309

59 11,505,340 7,879,420

Investments in group undertakings and participating interests

UK insurance dependantsShares

Debts and loans

Other insurance dependantsShares

Debts and loans

Non-insurance dependantsShares

Debts and loans

Other group undertakingsShares

Debts and loans

More than one month withdrawal

Participating interestsShares

Debts and loans

Fixed interest securitiesApproved

Other

Assets held to match linked liabilitiesIndex linked

Property linked

Variable interest securitiesApproved

Other

Loans to public or local authorities and nationalised industries or

undertakings

Loans secured by policies of insurance issued by the company

Bank and approved credit & financial

institution deposits

One month or less withdrawal

22

Form 13

(Sheet 2)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Non Profit Fund

Company GL/ Category

registration UK/ day month year Units of

number CM assets

R13 754167 GL 31 12 2015 £000 31

As at end of this

financial year

As at end of the

previous year

1 2

60

61

62

63

71

72

73

74

75 6,646 12,554

76

77

78 184,801 66,733

79

80

81 97,115 91,481

82

83

84 124,788 125,293

85

86 28 1,618

87

89 19,559,733 16,352,616

Reinsurers' share of technical provisions

Provision for unearned premiums

Claims outstanding

Provision for unexpired risks

Other

Debtors and salvage

Direct insurance businessPolicyholders

Intermediaries

Salvage and subrogation recoveries

ReinsuranceAccepted

Ceded

Dependantsdue in 12 months or less

due in more than 12 months

Otherdue in 12 months or less

due in more than 12 months

Deferred acquisition costs (general business only)

Other prepayments and accrued income

Deductions from the aggregate value of assets

Grand total of admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (11 to 86 less 87)

Other assets

Tangible assets

Deposits not subject to time restriction on withdrawal with approved

institutions

Cash in hand

Other assets (particulars to be specified by way of supplementary note)

Accrued interest and rent

23

Form 13

(Sheet 3)

Analysis of admissible assets

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Category of assets Non Profit Fund

Company GL/ Category

registration UK/ day month year Units ofnumber CM assets

R13 754167 GL 31 12 2015 £000 31

As at end of this

financial year

As at end of the

previous year

1 2

91 19,559,733 16,352,616

92

93 47,270 111,229

94

95

96

97

98

99 112,684

100 767,287 583,025

101 17,905 99,436

102 20,392,196 17,258,989

103 15,671 9,862

Reconciliation to asset values determined in accordance

with the insurance accounts rules or international

accounting standards as applicable to the firm for the

purpose of its external financial reporting

Total admissible assets after deduction of admissible assets

in excess of market risk and counterparty limits (as per line 89 above)

Admissible assets in excess of market and counterparty limits

Inadmissible assets directly held

Capital resources requirement deduction of regulated related

undertakings

Ineligible surplus capital and restricted assets in regulated related

insurance undertakings

Total assets determined in accordance with the insurance accounts

rules or international accounting standards as applicable to the firm

for the purpose of its external financial reporting (91 to 101)

Amounts included in line 89 attributable to debts due from related

insurers, other than those under contracts of insurance or reinsurance

Inadmissible assets of regulated related undertakings

Book value of related ancillary services undertakings

Other differences in the valuation of assets (other than for assets

not valued above)

Deferred acquisition costs excluded from line 89

Reinsurers' share of technical provisions excluded from line 89

Other asset adjustments (may be negative)

24

Form 14

Long term insurance business liabilities and margins

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Total business/Sub fund Summary

Units £000 As at end of As at end of

this financial the previous

year year

1 2

Mathematical reserves, after distribution of surplus 11 25,947,779 23,499,182

12

Balance of surplus/(valuation deficit) 13 1,143,219 883,041

Long term insurance business fund carried forward (11 to 13) 14 27,090,998 24,382,223

Gross 15 153,212 145,666

Reinsurers' share 16 710 5,631

Net (15-16) 17 152,502 140,035

Taxation 21

Other risks and charges 22 9,049 62

Deposits received from reinsurers 23 141,392 157,914

Direct insurance business 31 19,482 23,024

Reinsurance accepted 32 1,152 5,781

Reinsurance ceded 33 24,174 38,428

Secured 34

Unsecured 35

Amounts owed to credit institutions 36

Taxation 37 57,509 50,705

Other 38 319,965 206,869

Accruals and deferred income 39

41

Total other insurance and non-insurance liabilities (17 to 41) 49 725,225 622,818

Excess of the value of net admissible assets 51 447,772 447,772

Total liabilities and margins 59 28,263,995 25,452,813

61 28,290 28,494

62 17,298,128 14,019,575

71 26,673,004 24,122,000

Increase to liabilities - DAC related 72

Reinsurers' share of technical provisions 73 663,028 583,025

Other adjustments to liabilities (may be negative) 74 765,940 980,917

Capital and reserves and fund for future appropriations 75 994,263 673,020

76 29,096,234 26,358,962

Provision for "reasonably foreseeable adverse variations"

Amounts included in line 59 attributable to liabilities to related companies,

other than those under contracts of insurance or reinsurance

Amounts included in line 59 attributable to liabilities in respect of property

linked benefits

Total liabilities (11+12+49)

Total liabilities under insurance accounts rules or international accounting

standards as applicable to the firm for the purpose of its external financial

reporting (71 to 75)

Cash bonuses which had not been paid to policyholders prior

to end of the financial year

Claims outstanding

Provisions

Creditors

Debenture loans

Creditors

25

Form 14

Long term insurance business liabilities and margins

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Total business/Sub fund Non Profit Fund

Units £000 As at end of As at end of

this financial the previous

year year

1 2

Mathematical reserves, after distribution of surplus 11 18,372,680 15,470,138

12

Balance of surplus/(valuation deficit) 13 622,546 332,344

Long term insurance business fund carried forward (11 to 13) 14 18,995,226 15,802,482

Gross 15 113,542 105,699

Reinsurers' share 16 710 5,631

Net (15-16) 17 112,832 100,068

Taxation 21

Other risks and charges 22 9,049 62

Deposits received from reinsurers 23 141,392 157,914

Direct insurance business 31 19,482 23,024

Reinsurance accepted 32 1,152 5,781

Reinsurance ceded 33 24,174 38,428

Secured 34

Unsecured 35

Amounts owed to credit institutions 36

Taxation 37 42,898 25,491

Other 38 213,529 199,366

Accruals and deferred income 39

41

Total other insurance and non-insurance liabilities (17 to 41) 49 564,507 550,134

Excess of the value of net admissible assets 51

Total liabilities and margins 59 19,559,733 16,352,616

61 28,290 28,494

62 11,417,126 7,828,729

71 18,937,187 16,020,272

Increase to liabilities - DAC related 72

Reinsurers' share of technical provisions 73

Other adjustments to liabilities (may be negative) 74

Capital and reserves and fund for future appropriations 75

76

Provision for "reasonably foreseeable adverse variations"

Amounts included in line 59 attributable to liabilities to related companies,

other than those under contracts of insurance or reinsurance

Amounts included in line 59 attributable to liabilities in respect of property

linked benefits

Total liabilities (11+12+49)

Total liabilities under insurance accounts rules or international accounting

standards as applicable to the firm for the purpose of its external financial

reporting (71 to 75)

Cash bonuses which had not been paid to policyholders prior

to end of the financial year

Claims outstanding

Provisions

Creditors

Debenture loans

Creditors

26

Form 14

Long term insurance business liabilities and margins

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

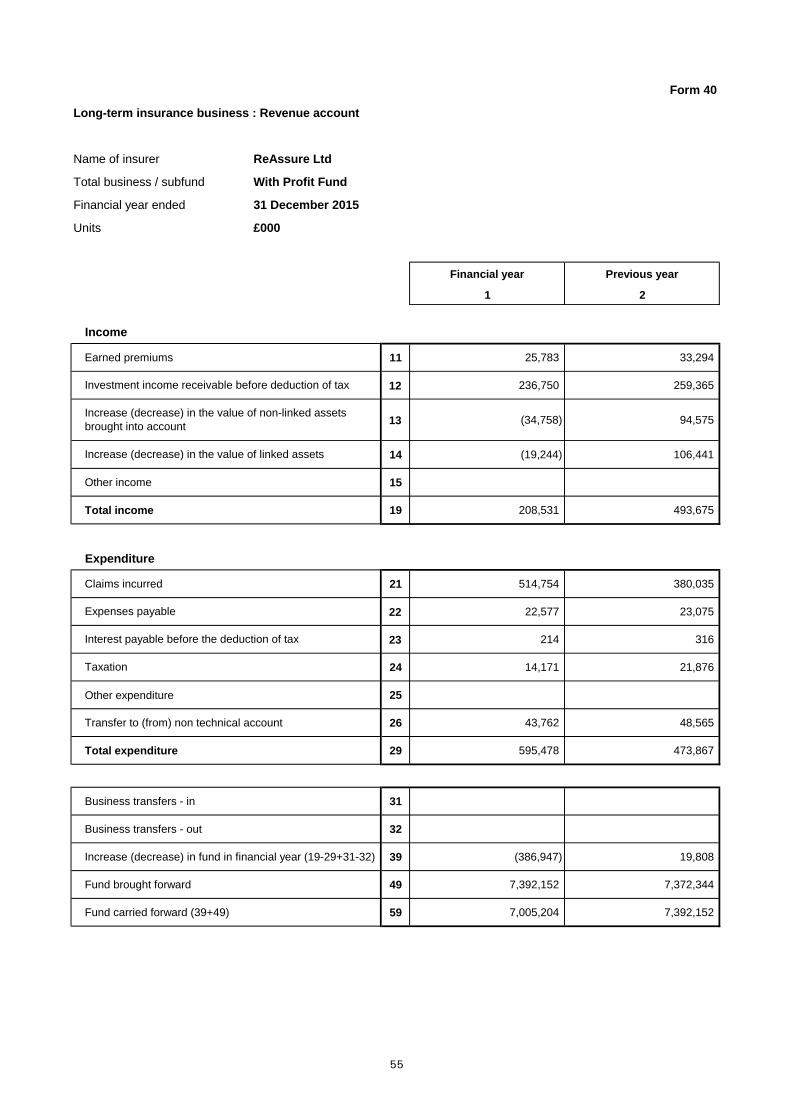

Total business/Sub fund With Profit Fund

Units £000 As at end of As at end of

this financial the previous

year year

1 2

Mathematical reserves, after distribution of surplus 11 6,818,006 7,202,554

12

Balance of surplus/(valuation deficit) 13 187,198 189,598

Long term insurance business fund carried forward (11 to 13) 14 7,005,204 7,392,152

Gross 15 33,293 33,218

Reinsurers' share 16

Net (15-16) 17 33,293 33,218

Taxation 21

Other risks and charges 22

Deposits received from reinsurers 23

Direct insurance business 31

Reinsurance accepted 32

Reinsurance ceded 33

Secured 34

Unsecured 35

Amounts owed to credit institutions 36

Taxation 37 14,220 22,929

Other 38 52,875 3,318

Accruals and deferred income 39

41

Total other insurance and non-insurance liabilities (17 to 41) 49 100,388 59,465

Excess of the value of net admissible assets 51 1 1

Total liabilities and margins 59 7,105,593 7,451,619

61

62 5,881,002 6,190,846

71 6,918,394 7,262,019

Increase to liabilities - DAC related 72

Reinsurers' share of technical provisions 73

Other adjustments to liabilities (may be negative) 74

Capital and reserves and fund for future appropriations 75

76

Provision for "reasonably foreseeable adverse variations"

Amounts included in line 59 attributable to liabilities to related companies,

other than those under contracts of insurance or reinsurance

Amounts included in line 59 attributable to liabilities in respect of property

linked benefits

Total liabilities (11+12+49)

Total liabilities under insurance accounts rules or international accounting

standards as applicable to the firm for the purpose of its external financial

reporting (71 to 75)

Cash bonuses which had not been paid to policyholders prior

to end of the financial year

Claims outstanding

Provisions

Creditors

Debenture loans

Creditors

27

Form 14

Long term insurance business liabilities and margins

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Total business/Sub fund National Mutual Fund

Units £000 As at end of As at end of

this financial the previous

year year

1 2

Mathematical reserves, after distribution of surplus 11 757,093 826,491

12

Balance of surplus/(valuation deficit) 13 333,475 361,099

Long term insurance business fund carried forward (11 to 13) 14 1,090,568 1,187,590

Gross 15 6,377 6,749

Reinsurers' share 16

Net (15-16) 17 6,377 6,749

Taxation 21

Other risks and charges 22

Deposits received from reinsurers 23

Direct insurance business 31

Reinsurance accepted 32

Reinsurance ceded 33

Secured 34

Unsecured 35

Amounts owed to credit institutions 36

Taxation 37 391 2,285

Other 38 53,561 4,185

Accruals and deferred income 39

41

Total other insurance and non-insurance liabilities (17 to 41) 49 60,330 13,218

Excess of the value of net admissible assets 51 447,771 447,771

Total liabilities and margins 59 1,598,670 1,648,578

61

62

71 817,423 839,709

Increase to liabilities - DAC related 72

Reinsurers' share of technical provisions 73

Other adjustments to liabilities (may be negative) 74

Capital and reserves and fund for future appropriations 75

76

Provision for "reasonably foreseeable adverse variations"

Amounts included in line 59 attributable to liabilities to related companies,

other than those under contracts of insurance or reinsurance

Amounts included in line 59 attributable to liabilities in respect of property

linked benefits

Total liabilities (11+12+49)

Total liabilities under insurance accounts rules or international accounting

standards as applicable to the firm for the purpose of its external financial

reporting (71 to 75)

Cash bonuses which had not been paid to policyholders prior

to end of the financial year

Claims outstanding

Provisions

Creditors

Debenture loans

Creditors

28

Form 15

Liabilities (other than long term insurance business)

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Company GL/

registration UK/ day month year Units

number CM

R15 754167 GL 31 12 2015 £000

As at end of As at end of

this financial the previous

year year

1 2

Technical provisions (gross amount)

Provisions for unearned premiums 11

Claims outstanding 12 499 499

Provision for unexpired risks 13

Credit business 14

Other than credit business 15

Other technical provisions 16

Total gross technical provisions (11 to 16) 19 499 499

Provisions and creditors

Taxation 21

Other risks and charges 22

Deposits received from reinsurers 31

Direct insurance business 41

Reinsurance accepted 42

Reinsurance ceded 43

Secured 44

Unsecured 45

Amounts owed to credit institutions 46

Taxation 47

Foreseeable dividend 48

Other 49 498 904

Accruals and deferred income 51

Total (19 to 51) 59 996 1,403

Provision for "reasonably foreseeable adverse variations" 61

Cumulative preference share capital 62

Subordinated loan capital 63

Total (59 to 63) 69 996 1,403

71

Amounts deducted from technical provisions for discounting 82

Other adjustments (may be negative) 83 (1,401)

Capital and reserves 84 460,558 740,504

85 461,555 740,506

Total liabilities under insurance accounts rules or international accounting

standards as applicable to the firm for the purpose of its external financial

reporting (69-82+83+84)

Equalisation provisions

Provisions

Creditors

Debenture

loans

Creditors

Amounts included in line 69 attributable to liabilities to related insurers,

other than those under contracts of insurance or reinsurance

29

Form 16

Profit and loss account (non-technical account)

Name of insurer ReAssure Ltd

Global business

Financial year ended 31 December 2015

Company GL/

registration UK/ day month year Units

number CM

R16 754167 GL 31 12 2015 £000

This financial Previous

year year

1 2

From Form 20 11 51

Equalisation provisions 12

13 240,000

14 14,992 1,924

Investment income 15 42 4,707

16 2,228 1,455

17 7,115 7,968

Investment charges 18 3,776 2,356

19 11,317 3,470

20

21 (614)

29 (4,946) 233,729

Tax on profit or loss on ordinary activities 31 (2,201)

Profit or loss on ordinary activities after tax (29-31) 39 (4,946) 235,930

41

Tax on extraordinary profit or loss 42

Other taxes not shown under the preceding items 43

Profit or loss for the financial year (39+41-(42+43)) 49 (4,946) 235,930

Dividends (paid or foreseeable) 51 275,000 395,000

Profit or loss retained for the financial year (49-51) 59 (279,946) (159,070)

Transfer (to)/from the

general insurance business

technical account

Transfer from the long term insurance business

revenue account

Income

Value re-adjustments on

investments

Gains on the realisation of

investments

Investment management

charges, including interest

Value re-adjustments on

investments

Loss on the realisation of

investments

Allocated investment return transferred to the general

insurance business technical account

Other income and charges (particulars to be specified

by way of supplementary note)

Profit or loss on ordinary activities before tax

(11+12+13+14+15+16-17-18-19-20+21)

Extraordinary profit or loss (particulars to be specified

by way of supplementary note)

30

Form 18

With-profits insurance capital component for the fund

Name of insurer ReAssure Ltd

With-profits fund With Profit Fund

Financial year ended 31 December 2015

Units £000

As at end of As at end of

this financial year the previous year

1 2

Regulatory excess capital

11 7,105,593 7,451,620

12

13 6,534,345 6,902,140

14 615 864

15

19 570,633 548,616

21 283,661 300,415

22 100,388 59,465

29 384,049 359,880

31 11,396 12,069

32

39 395,445 371,949

Regulatory excess capital (19-39) 49 175,189 176,667

Realistic excess capital

51

Excess assets allocated to with-profits insurance business

61 175,189 176,667

62

63

64 349,524 492,360

65

66

Regulatory value

of assets

Long-term admissible assets of the fund

Implicit items allocated to the fund

Mathematical reserves in respect of the fund's

non-profit insurance contracts

Long-term admissible assets of the fund

covering the LTICR of the fund's non-profit

insurance contracts

Long-term admissible assets of the fund

covering the RCR of the fund's non-profit

insurance contracts

Total (11+12-(13+14+15))

Regulatory value

of liabilities

Mathematical reserves (after distribution of

surplus) in respect of the fund's with-profits

insurance contracts

Regulatory current liabilities of the fund

Total (21+22)

Long-term insurance capital requirement in respect of the fund's

with-profits insurance contracts

Resilience capital requirement in respect of the fund's

with-profits insurance contracts

Present value of other future internal transfers not

already taken into account

With-profits insurance capital component for fund (if 62 exceeds

63, greater of 61+62-63-64-65 and zero, else greater of 61-64-65

and zero)

Sum of regulatory value of liabilities, LTICR and RCR

(29+31+32)

Realistic excess capital

Excess (deficiency) of assets allocated to with-profits insurance

business in fund (49-51)

Face amount of capital instruments attributed to the fund and

included in capital resources (unstressed)

Realistic amount of capital instruments attributed to the fund and

included in capital resources (stressed)

Present value of future shareholder transfers arising

from distribution of surplus

31

Form 18

With-profits insurance capital component for the fund

Name of insurer ReAssure Ltd

With-profits fund National Mutual Fund

Financial year ended 31 December 2015

Units £000

As at end of As at end of

this financial year the previous year

1 2

Regulatory excess capital

11 1,598,669 1,648,578

12

13 52,999 52,430

14 2,135 2,114

15

19 1,543,535 1,594,034

21 704,094 774,060

22 60,330 13,218

29 764,424 787,278

31 28,154 30,953

32

39 792,578 818,231

Regulatory excess capital (19-39) 49 750,957 775,803

Realistic excess capital

51

Excess assets allocated to with-profits insurance business

61 750,957 775,803

62

63

64

65

66 750,957 775,803

Regulatory value

of assets

Long-term admissible assets of the fund

Implicit items allocated to the fund

Mathematical reserves in respect of the fund's

non-profit insurance contracts

Long-term admissible assets of the fund

covering the LTICR of the fund's non-profit

insurance contracts

Long-term admissible assets of the fund

covering the RCR of the fund's non-profit

insurance contracts

Total (11+12-(13+14+15))

Regulatory value

of liabilities

Mathematical reserves (after distribution of

surplus) in respect of the fund's with-profits

insurance contracts

Regulatory current liabilities of the fund

Total (21+22)

Long-term insurance capital requirement in respect of the fund's

with-profits insurance contracts

Resilience capital requirement in respect of the fund's

with-profits insurance contracts

Present value of other future internal transfers not

already taken into account

With-profits insurance capital component for fund (if 62 exceeds

63, greater of 61+62-63-64-65 and zero, else greater of 61-64-65

and zero)

Sum of regulatory value of liabilities, LTICR and RCR

(29+31+32)

Realistic excess capital

Excess (deficiency) of assets allocated to with-profits insurance

business in fund (49-51)

Face amount of capital instruments attributed to the fund and

included in capital resources (unstressed)

Realistic amount of capital instruments attributed to the fund and

included in capital resources (stressed)

Present value of future shareholder transfers arising

from distribution of surplus

32

Form 19

Realistic balance sheet (Sheet 1)

Name of insurer ReAssure Ltd

With-profits fund With Profit Fund

Financial year ended 31 December 2015

Units £000

As at end of As at end of

this financial year the previous year

1 2

Realistic value of assets available to the fund

11 570,633 548,616

12

13

21

22 399,727 427,494

23

24

25

26 970,360 976,110

27

29 970,360 976,110

Realistic value of liabilities of fund

31 243,377 259,870

32 129,416 119,752

33

34 57,308 52,502

35

36 7,122 7,182

41 13,662 24,118

42

43 29,440 31,579

44

45 399,112 426,630

46

47 4,780 9,376

49 626,596 656,775

Realistic current liabilities of the fund 51 100,388 59,465

59 970,361 976,110

With-profits benefit reserve

Regulatory value of assets

Implicit items allocated to the fund

Value of shares in subsidiaries held in fund (regulatory)

Excess admissible assets

Present value of future profits (or losses) on non-profit insurance contracts

written in the fund

Value of derivatives and quasi-derivatives not already reflected in lines

11 to 22

Planned deductions for other costs deemed chargeable

to with-profits benefits reserve

Future costs of contractual guarantees (other than

financial options)

Future costs of non-contractual commitments

Future costs of financial options

Future costs of smoothing (possibly negative)

Value of shares in subsidiaries held in fund (realistic)

Prepayments made from the fund

Realistic value of assets of fund (11+21+22+23+24+25-(12+13))

Support arrangement assets

Assets available to the fund (26+27)

Financing costs

Any other liabilities related to regulatory duty to treat

customers fairly

Other long-term insurance liabilities

Total (32+34+41+42+43+44+45+46+47-(33+35+36))

Realistic value of liabilities of fund (31+49+51)

Future policy

related liabilities

Past miscellaneous surplus attributed to with-profits

benefits reserve

Past miscellaneous deficit attributed to with-profits

benefits reserve

Planned enhancements to with-profits benefits

reservePlanned deductions for the costs of guarantees,

options and smoothing from with-profits benefits

reserve

33

Form 19

(Sheet 2)

Realistic balance sheet

Name of insurer ReAssure Ltd

With-profits fund With Profit Fund

Financial year ended 31 December 2015

Units £000

As at end of As at end of

this financial year the previous year

1 2

Realistic excess capital and additional capital available

62 970,361 976,110

63

64 970,361 976,110

65

66

67

68

69

Other assets potentially available if required to cover the fund's risk capital margin

81 699,670 690,717

82

Working capital for fund (29-59)

Working capital ratio for fund (68/29)

Additional amount potentially available for inclusion in line 62

Additional amount potentially available for inclusion in line 63

Value of relevant assets before applying the most adverse scenario

other than the present value of future profits arising from business

outside with-profits funds

Amount of present value of future profits (or losses) on long-term

insurance contracts written outside the fund included in the value

of relevant assets before applying most adverse scenario

Value of relevant assets before applying the most adverse scenario

(62+63)

Risk capital margin for fund (62-59)

Realistic excess capital for fund (26-(59+65))

Realistic excess available capital for fund (29-(59+65))

34

Form 19

Realistic balance sheet (Sheet 1)

Name of insurer ReAssure Ltd

With-profits fund National Mutual Fund

Financial year ended 31 December 2015

Units £000

As at end of As at end of

this financial year the previous year

1 2

Realistic value of assets available to the fund

11 1,543,535 1,594,034

12

13

21

22 2,135 2,114

23

24

25

26 1,545,670 1,596,148

27

29 1,545,670 1,596,148

Realistic value of liabilities of fund

31 976,153 1,047,619

32 238,918 246,779

33

34 149,695 149,759

35

36

41 8,268 10,664

42

43 112,306 128,109

44

45

46

47

49 509,187 535,311

Realistic current liabilities of the fund 51 60,330 13,218

59 1,545,670 1,596,148

With-profits benefit reserve

Regulatory value of assets

Implicit items allocated to the fund

Value of shares in subsidiaries held in fund (regulatory)

Excess admissible assets

Present value of future profits (or losses) on non-profit insurance contracts

written in the fund

Value of derivatives and quasi-derivatives not already reflected in lines

11 to 22

Planned deductions for other costs deemed chargeable

to with-profits benefits reserve

Future costs of contractual guarantees (other than

financial options)

Future costs of non-contractual commitments

Future costs of financial options

Future costs of smoothing (possibly negative)

Value of shares in subsidiaries held in fund (realistic)

Prepayments made from the fund

Realistic value of assets of fund (11+21+22+23+24+25-(12+13))

Support arrangement assets

Assets available to the fund (26+27)

Financing costs

Any other liabilities related to regulatory duty to treat

customers fairly

Other long-term insurance liabilities

Total (32+34+41+42+43+44+45+46+47-(33+35+36))

Realistic value of liabilities of fund (31+49+51)

Future policy

related liabilities

Past miscellaneous surplus attributed to with-profits

benefits reserve

Past miscellaneous deficit attributed to with-profits

benefits reserve

Planned enhancements to with-profits benefits

reservePlanned deductions for the costs of guarantees,

options and smoothing from with-profits benefits

reserve

35

Form 19

(Sheet 2)

Realistic balance sheet

Name of insurer ReAssure Ltd

With-profits fund National Mutual Fund

Financial year ended 31 December 2015

Units £000

As at end of As at end of

this financial year the previous year

1 2

Realistic excess capital and additional capital available

62 1,545,670 1,596,148

63

64 1,545,670 1,596,148

65

66

67

68

69

Other assets potentially available if required to cover the fund's risk capital margin

81 699,670 690,717

82

Working capital for fund (29-59)

Working capital ratio for fund (68/29)

Additional amount potentially available for inclusion in line 62

Additional amount potentially available for inclusion in line 63

Value of relevant assets before applying the most adverse scenario

other than the present value of future profits arising from business

outside with-profits funds