Real Estate Country Facts · Real Estate Country Facts November 2007 / Page 3 ing in the tradable...

11

NOVEMBER 2007 BANK AUSTRIA CREDITANSTALT REAL ESTATE RESEARCH • UNICREDIT GROUP NEW EUROPE RESEARCH NETWORK Bulgaria EU Speculations Boost Commercial Real Estate Market Real Estate Country Facts

Transcript of Real Estate Country Facts · Real Estate Country Facts November 2007 / Page 3 ing in the tradable...

NOVEMBER 2007

BANK AUSTRIA CREDITANSTALT REAL ESTATE RESEARCH • UNICREDIT GROUP NEW EUROPE RESEARCH NETWORK

Bulgaria EU Speculations Boost Commercial Real Estate Market

Real Estate Country Facts

Real Estate Country Facts

November 2007 / Page 1

Imprint and Disclosure

Imprint

Publisher and media owner: Bank Austria Creditanstalt AG, Vordere Zollamtsstraße 13, A-1030 Vienna; Am Hof 2, A-1010 Vienna, Austria.

http://www.ba-ca.com Editor: BA-CA Real Estate Consulting & Investment, Karla Schestauber, Tel. +43 (0)50505-54784 and CEE Research, Bernhard Sinhuber, Tel +43(0)50505-41964

Layout: horvath grafik design Dated: 2 November, 2007 Sources:

This publication is based on our own research and research conducted by Immobilien Rating GmbH (IRG) as well as analyses of reports from various international and national sources, press reports and statistical data which we consider reliable.

Disclaimer:

Despite diligent research and the use of reliable sources, Bank Austria Creditanstalt AG assumes no responsibility or liability regarding the completeness and accuracy of the information herein. This publication is not a proposal or request for proposal and shall not be construed as such.

Real Estate Country Facts

November 2007 / Page 2

Bulgaria - exploiting benefits of EU

accession

Macroeconomic fundamentals are strongly un-

derpinned by successful structural transforma-

tion and EU accession in 2007

Most macroeconomic and financial sector indicators

exhibit values, which are fairly in line with those perceived

to be equilibrium ones for a converging economy. Recent

data showed that the speed of GDP growth has acceler-

ated. At the same time a substantial degree of fiscal tight-

ening has allowed public sector indebtedness to fall to risk-

free levels, while also driving fiscal reserves to above 14%

of projected GDP in 2007. Positively for the health of exter-

nal finances, FDI is estimated to pick up further this year,

reaching at least 15% of GDP. The risk of a large scale

capital misallocation is small since most of the investments

are channelled through the banking sector, which is con-

trolled by foreign banks with proven expertise in risk man-

agement. Above all, EU accession provides a host of posi-

tive stimuli for the economy including unconstrained access

to the single EU market, which represent an enormous

boost for competition and trade and therefore for growth

and prosperity.

While fundamentals of the Bulgarian economy remain

strong most recent data signal an aggravation of the exist-

ing macroeconomic imbalances. Inflation has reached

levels unseen since 1998, partly reflecting one-off external

shocks, but also excessive growth in labor costs as pres-

sure for higher incomes in the public sector spills over into

the rest of the economy.

The current account (CA) gap continued to expand, al-

though the extent of the deterioration is unclear as prob-

lems with the quality of foreign trade data collected through

the INTRASTAT system still persist. Difficult structural

reforms were put aside fuelling long-term concerns for the

competitiveness of the economy in the context of the fixed

exchange rate regime.

Economic growth accelerated to a real 6.6% yoy

in Q2 2007 and 6.4% in H1 2007

The growth pattern also experienced some improve-

ment, although, generally it remains overreliant on exter-

nally funded investments and robust consumption appetite

in the household sector. Compared with the previous quar-

ter, the negative contribution of net exports decreased

significantly, mostly in response to a gradual export recov-

ery. Despite the excessive increase in retail credit and

wages, individual consumption lost further momentum to

5.7% yoy in Q2 2007. Investments continued to expand at

an impressive rate compensating for the flagging spending

appetite in the households sector, thereby boosting me-

dium- to long-term economic growth prospects. Gross fixed

capital formation (GFCF) including changes in inventories,

reached 35% of GDP for Q2 2007, still somewhat weaker

when compared with the all-time record posted in the pre-

vious quarter, when investments edged up to 40% of GDP.

The structure of expenditure for the acquisition of tan-

gible fixed assets also improved. In H1 2007 capital spend-

Macroeconomic data and forecasts

2005 2006 2007f 2008f 2009f

Nominal GDP (EUR bn) 21.9 25.1 28.5 31.8 35.0

Per capita GDP (EUR) 2,835 3,268 3,732 4,178 4,623

Real GDP yoy (%) 6.2 6.1 6.2 6.2 6.0

Inflation (CPI) yoy, avg (%) 5.0 7.3 8.1 5.6 4.2

Unemployment rate, avg (%) 10.7 9.1 7.3 6.5 6.0

Exchange rate EUR / BGN, eop/avg 1.96 1.96 1.96 1.96 1.96

Current account / GDP (%) -12.0 -15.8 -17.6 -16.8 -15.0

FDI / GDP (%) 14.2 16.4 15.0 13.0 9.5

Consolidated gov. balance / GDP (%) 2.3 3.6 3.0 2.0 2.0

Public debt/ GDP (%) (ESA 95) 31.3 24.7 19.8 18.6 18.4

Sources: Bulgarian Central Bank, Statistical Office, UniCredit Group New Europe Research Network

Real Estate Country Facts

November 2007 / Page 3

ing in the tradable goods sectors increased by 55% on an

annual basis, raising their relative share on total invest-

ments to 40%, from 37% a year ago.

On the supply side, an anticipated drop in the agricul-

ture sector (-5.3% yoy), was more than balanced by indus-

try and services growing by a real 10.5% and 9.5% respec-

tively.

GDP growth (yoy, in % 2001 - 2006)

-10

-5

0

5

10

15

2001 2002 2003 2004 2005 2006

Private Consumption Public Consumption

Fixed Investment Net exports

GDP real growth

Source: Statistical Office Bulgaria

In the forthcoming years, growth prospects remain very

favorable. A gradual recovery in exports and solid growth

momentum behind investments, also backed by the start of

EU-funded projects, will keep GDP growth around 6.2% in

real terms in 2007 and in 2008. Nevertheless, renewed

volatility in the international markets remains the key down-

side risk for our baseline GDP growth scenario. The poten-

tial worsening of global financial conditions and the deep-

ening of risk aversion could have a detrimental impact on

FDI and the cost of external borrowing, thereby reducing

investments and GDP growth, and making it more difficult

for the country to finance its large CA shortfall.

Healthy fiscal performance made a 3% cut in so-

cial-insurance contribution rate possible in Octo-

ber and bolstered plans for introduction of a 10%

flat tax on personal incomes next year

With year-to-date revenues in July totalling 62% of

those planned for 2007 as a whole, and expenditures

amounting to only 52% of the plan, the state budget is in a

very favorable position to meet its year-end target of BGN

1.4 billion, equivalent to 2.5% of projected GDP. The com-

bination of a very conservative revenue planning, strong

economic growth and cutbacks in the size of the grey sec-

tor, enabled revenues in the consolidated fiscal program for

the first seven months of the year to outperform the target

by 17.1%. Thus, at the end of July the budget is running a

surplus of BGN 2.4 billion which corresponds to 4.2% of

GDP for the whole year.

Against these backdrops, the government unveiled

plans for another 10% increase in state-funded pensions on

top of the commitment to cut back the social insurance

contribution rate by 3%, effective from 1 October, 2007.

Fiscal plans for the next year include a reduction in

taxation on labour via the introduction of a 10% flat tax on

personal incomes, changing proportions at which social

insurance contributions are divided between employers and

employees and an indexation of pensions by a rate equal to

the sum of 50% of the inflation rate and 50% of the rate of

increase in the contributions actually collected in the first

pillar of the pension system. Excise on cigarettes will be

raised by half of what remains in order to complete the

harmonization process, with the last remaining step sched-

uled for 2009.

Fiscal plans for the coming year should bring no risks

to macroeconomic stability. On the contrary, the cutback in

the taxation on labour will have a broadly based favorable

impact on the economy and therefore deserves praise. It

will help to reduce the widely spread grey sector and will

boost the collection of social insurance contributions, a task

which has proved to be particularly elusive so far. Lower

taxation on high-income earners will bring an increase in

their disposable income and consequently will positively

affect saving rates.

The reduction of personal income tax was also wel-

comed by the representatives of employers organisations,

which in turn agreed to raise the wage ceilings used to

calculate due social insurance contributions in the private

sector. Thus, the income base to be used to calculate con-

tribution payments will increase by between 25% and 35%,

with rates being highest in sectors such as construction and

tourism, where the problem of underreporting of incomes

for tax evasion purposes has been particularly acute.

On the negative side, the government’s plans to re-

structure the ailing health care and education sectors re-

main controversial, which gives the impression that there is

still a lack of enough political will to forge ahead with the

process.

Risks for price stability shift upward in H2 2007

From 4.3% in May, twelve-month inflation broke

through the 10.0% mark in just three months to reach

13.1% in September, its highest level in almost nine years.

The unprecedented spike in consumer prices was attribut-

able, above all, to soaring food prices. Eurostat data for

June showed substantial increases in food and beverage

Real Estate Country Facts

November 2007 / Page 4

prices across all EU member countries, with new Member

States being hit particularly badly. Year-on-year price dy-

namics were highest in Bulgaria (14.7%), followed at a

narrow margin by Latvia (12.2%) and Hungary (10.1%).

Clearly, the spike in food costs witnessed in Bulgaria in

the last three months was part of a one-off supply shock of

global proportions. However, there are several country-

specific factors, some of them structural, which are also

exercising upside pressure on local prices. Slow progress

in the enlargement of arable land is restricting capital

spending and competition in the agriculture sector. Follow-

ing EU entry some local foodstuff manufacturers increased

the share of their output channelled to other EU countries

to benefit from the existing price differentials. Unfavorable

climate conditions adversely affected agriculture output,

while imports from non EU-neighbors became more expen-

sive, following the adoption of the Common External Tariff.

Consumer price inflation (yoy %)

-2

0

2

4

6

8

10

12

14

Dec 99 Dec 00 Dec 01 Dec 02 Dec 03 Dec 04 Dec 05 Dec 06

%

Source: Statistical Office Bulgaria

Lack of structural reforms aimed at boosting competi-

tion in agriculture, electricity, gas and water, railway trans-

port and postal services, makes it easy for the producers to

transfers all cost related pressure to end-customers. The

situation looks very similar also in the ailing health care and

education sectors, which are also among the sources of

inflationary pressure in the economy. Elevated pay pres-

sure (average wages increased by 17% in Q1 2007 and

18% in Q2 2007) and the robust expansion of money and

credit aggregates were also too high to have had no impact

on price stability.

Nevertheless, inflationary pressure should moderate

somewhat towards the end of the current year. However,

causes for unabated price pressure remain broadly based

and often structural in nature, which highlights the funda-

mental case for persistently high inflation in the forthcoming

periods.

We forecast average CPI (measured according to the

national methodology) to slow down gradually to 5.6% in

2008 and further to 4.2% in 2009. Anchoring inflationary

expectations will be challenging. It will require a sustained

restrictive fiscal and monetary policy, while reinvigorating

restructuring efforts aimed at expanding the role of the free

market and competition in the sectors, where reforms have

lost momentum in the last couple of years.

External imbalances widened amidst persisting

problems with quality of foreign trade data col-

lected through the INTRASTAT system

In January-July, the year-to-date CA gap expanded by

74% yoy, reaching 10.5% of projected full-year GDP. The

deterioration was entirely attributable to the widening of the

foreign trade shortfall, which increased by 31% in compari-

son with the same period last year. Merchandise exports

posted annual growth of 8.6%, which, however, was out-

paced by an even stronger increase in imports of 18.8%.

On the positive side, the year-to-date net services bal-

ance recorded a 40% increase, which was attributable

above all to the 18% growth in sales receipts from interna-

tional tourism. Accordingly, the coverage net services pro-

vides to the merchandise trade gap remained little changed

at around 20%. Net incomes reported a marginal deteriora-

tion, since the improved compensation of employees fell

short of balancing the combined effect of raising profit repa-

triation and higher debt servicing costs. Net current trans-

fers were almost flat, when compared with the last year, as

rising remittances from emigrants counterbalanced the

contribution payments in favour of the EU common budget.

On the financing side, net FDI edged up by 12% yoy

reaching 9.4% of projected full-year GDP, while BNB re-

serves increased almost in the same proportions as a year

ago (+ EUR 933 million), fuelling money supply and credit

aggregates.

Real Estate Country Facts

November 2007 / Page 5

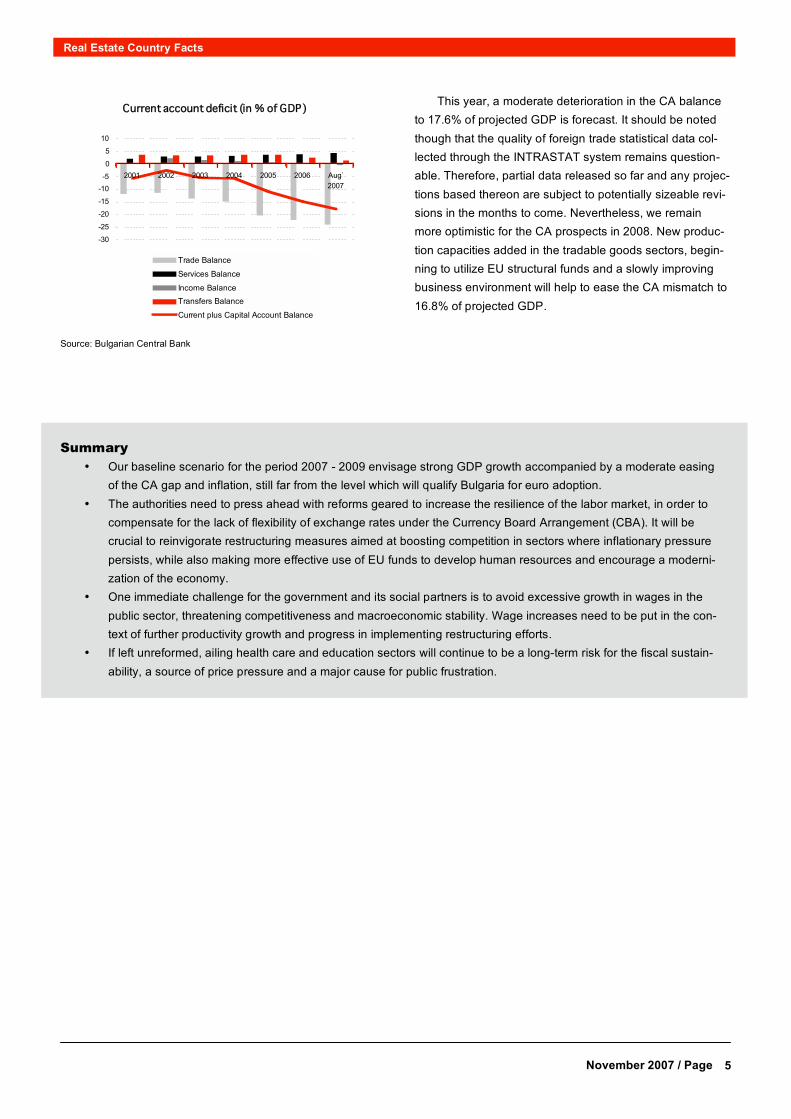

Current account deficit (in % of GDP)

-30

-25

-20

-15

-10

-5

0

5

10

2001 2002 2003 2004 2005 2006 Aug`

2007

Trade Balance

Services Balance

Income Balance

Transfers Balance

Current plus Capital Account Balance

Source: Bulgarian Central Bank

This year, a moderate deterioration in the CA balance

to 17.6% of projected GDP is forecast. It should be noted

though that the quality of foreign trade statistical data col-

lected through the INTRASTAT system remains question-

able. Therefore, partial data released so far and any projec-

tions based thereon are subject to potentially sizeable revi-

sions in the months to come. Nevertheless, we remain

more optimistic for the CA prospects in 2008. New produc-

tion capacities added in the tradable goods sectors, begin-

ning to utilize EU structural funds and a slowly improving

business environment will help to ease the CA mismatch to

16.8% of projected GDP.

Summary

• Our baseline scenario for the period 2007 - 2009 envisage strong GDP growth accompanied by a moderate easing

of the CA gap and inflation, still far from the level which will qualify Bulgaria for euro adoption.

• The authorities need to press ahead with reforms geared to increase the resilience of the labor market, in order to

compensate for the lack of flexibility of exchange rates under the Currency Board Arrangement (CBA). It will be

crucial to reinvigorate restructuring measures aimed at boosting competition in sectors where inflationary pressure

persists, while also making more effective use of EU funds to develop human resources and encourage a moderni-

zation of the economy.

• One immediate challenge for the government and its social partners is to avoid excessive growth in wages in the

public sector, threatening competitiveness and macroeconomic stability. Wage increases need to be put in the con-

text of further productivity growth and progress in implementing restructuring efforts.

• If left unreformed, ailing health care and education sectors will continue to be a long-term risk for the fiscal sustain-

ability, a source of price pressure and a major cause for public frustration.

Real Estate Country Facts

November 2007 / Page 6

EU speculations boost real estate market Bulgaria's economy is benefiting strongly from EU ac-

cession. The net inflow of direct investment soared in the run-up to accession and in 2006 reached a good EUR 4 billion or 16.4% of GDP. Around one third of FDI to Bulgaria found its way into the real estate sector. If the funds that flowed into construction are included the figure rises to 45%. This year direct foreign investment seems to be stay-ing high. In the first six months 2007, FDI into Bulgaria totalled more than EUR 2 billion, with almost 50% of this targeting the real estate and construction business. This dynamic development has resulted in a tangible shortage of skilled construction workers and powerful surges in con-struction costs.

In the latest "Doing Business 2008" report of the World Bank, which is an important indicator of the investment climate in a country, Bulgaria managed to move up to posi-tion 46, slightly ahead of Romania.

Doing Business 2008

Country Ranking

Singapore 1

Estonia 17

Georgia 18

Latvia 22

Austria 25

Lithuania 26

Slovakia 32

Hungary 45

Bulgaria 46

Romania 48

Source: World Bank

Having a healthy investment climate is crucial to the

sustainability of economic growth. Yet in spite of the im-provements achieved, inadequate legal and administration conditions in particular still continue to be problematic. Major reform efforts are still required after EU accession as well.

Against this background, the market for commercial real estate is booming; yield compression is strong, though in this respect the country does somewhat lag behind Ro-mania, the other new EU member.

Key figures 2006

Bulgaria Romania

Area of country in 1,000 km2 110.9 238.4

Population in million 7.7 21.6 Gross domestic product

in EUR billion 25.1 97.2

GDP per capita in EUR 3,270 4,500

Top yields (midyear 2007)

Office in % 7.5 6.5

Retail in % 8.5 7.5

Logistics in % 9.0 8.0 Source: UniCredit Group New Europe Research Network, IRG, BA-CA Real Estate

When reflecting on future yield development one should not forget the higher risk represented by Bulgaria and Romania in comparison to the "more mature" econo-mies of the EU. The crisis on the US sub prime mortgage market has led to a worldwide dip in risk appetite, with fundamentals coming increasingly to the fore again. There-fore, in addition to market risk, the quality of construction of buildings especially is becoming a hot topic. So far, invest-ment demand is still high outstripping supply. Forward purchases of new developments in Sofia or in other large Bulgarian towns and cities remain common. Nevertheless, the behavior of investors is likely to undergo gradual change. One can assume that short-term investment strategies will become less popular as the potential for yield compression declines.

One of the most significant deals so far was the sale of Business Park Sofia in the south of the city for a reported EUR 180 million and an alleged yield of around 7.0% to a US investment fund.

Source: Colliers, IRG, BA-CA Real Estate

Office prime yields

0

1

2

3

4

5

6

7

8

9

10

Kiev

Moscow

Istanbul

Sofia

Bucharest

Warsaw

Praha

Budapest

%

Real Estate Country Facts

November 2007 / Page 7

Supply of office space is rising steadily

By mid-2007 the supply of office space in Sofia had in-

creased to 600,000 m2. DTZ estimates approximately

160,000 m2 of this can be classed as modern offices.

Classes B and C are primarily found in the city centre of

Sofia, while class A is offered principally in the newly de-

veloped office complexes along the main roads heading

into the city.

The rents for class A office space range from EUR 12

to 23 m2/month, whereby the best prices are obtained for

modern offices in central locations. Under strong demand

the vacancy rates have been relatively stable, averaging

out at 5% in the first six months of 2007, with the recorded

figures being lower in central locations.

The next few years will see some new office space

make its way onto the market. According to Colliers there is

some 450,000 m2 of space already under construction. The

majority should be completed between 2008 and 2011.

Source: Colliers, BA-CA Real Estate 1) Data for 2006

Most of the new developments are found along and

around the main roads leading into the city as well as

around the southern part of the ring-road. Large, multi-

purpose projects also containing office space are being

built as well, especially in the area around the airport. De-

velopment in the central business district (CBD) on the

other hand is hampered by the difficult traffic conditions and

the lack of suitable space for new developments.

There is also a whole range of office building projects

underway in the other large towns and cities of Plovdiv,

Varna and Burgas. The rents are on average about 30%

below what one can expect to achieve in Sofia.

The demand for modern office space is driven primarily

by international companies who are already present on the

market and want to expand or relocate their offices. Also

smaller Bulgarian firms who still often use converted

apartments as their offices are likely to move gradually into

more modern premises in the future. These developments

will contribute to an adjustment of the office market.

Yields have fallen sharply in recent years. While top

yields in Sofia two years ago still reached 10%, they cur-

rently amount to below 7%. Although there is still some

potential for further decreases, quality aspects of real es-

tate portfolios should become increasingly important.

Source: Colliers, BA-CA Real Estate

Shopping centre boom

Robust growth in salaries and a strong labour market

are fuelling the development of the retail trade in Bulgaria.

Although the gross domestic product (GDP) has risen pow-

erfully in recent years, the country still has a lot of ground to

make up as far as purchasing power is concerned. Per

capita GDP rose by EUR 433 in 2006 to EUR 3,270. In

Austria, by comparison, the corresponding figure amounts

to EUR 30,960.

Source: UniCredit Group New Europe Research Network

With a declining population the demographic structure

of Bulgaria is not too healthy. Nonetheless, Sofia in particu-

lar is managing to buck the trend. On account of migration

from rural areas the city is growing. Bottlenecks in infra-

Office space per capita

midyear 2007

0,00

0,20

0,40

0,60

0,80

1,00

1,20

1,40

1,60

1,80

2,00

Praha

War

saw

Bratis

lava

Bud

apes

t

Tallin

n

Mos

cow

Zagr

ebSof

ia

Buc

hare

st 1

)

Belgr

ade

Viln

ius

Kiev

Riga

Ista

nbul

sqm

Office space/capita Office space plus space under construction /capita

GDP per capita

0

2000

4000

6000

8000

10000

12000

Cze

ch R

epub

lic

Hun

gary

Slova

kia

Polan

d

Rus

sia

Rom

ania

Turke

y

Bulga

ria

Ukr

aine

in EUR

Spitzenrenditen im Bürobereich

Sofia

0

2

4

6

8

10

12

14

16

18

2002 2003 2004 2005 2006 1.Hj.2007

in %

Real Estate Country Facts

November 2007 / Page 8

structure rear their heads on a daily basis. Although there

are ambitious development plans for roads (e.g. upgrading

of the ring-road) and public transport (e.g. extension of the

underground system), subsequent action is slow.

The traditional shopping street in Sofia is the Vitosha

Blvd. Rents there fetch between EUR 40 and 150

m2/month. Many shoppers are also to be found on Graf

Ignatiev St., Rakovski St., Patriath Evtimii Blvd., Solunska

St. and Alabin St. Vacancy rates are very low. High street

development is hindered due to the limited building oppor-

tunities coupled with the transport and parking problems.

By contrast, the shopping center (SC) sector is making

dynamic progress. In 2006 the first three shopping centres

were opened in Sofia. The "Mall of Sofia" with its approxi-

mately 35,000 m2 of retail and entertainment space, the

"City Center Sofia" with its roughly 20,000 m2 and the "Sky

City Center" with around 15,000 m2 of space. These new

malls conform to international standards without exception,

accommodating global brands in the areas of both retail

and gastronomy.

There are other large and ambitious SC projects being

built or currently being planned. The new Carrefour Mall will

have lettable space in excess of 60,000 m2. The "Bulgaria

Mall" will be completed on Bulgaria Blvd by the end of 2009

with approximately 50,000 m2 in retail space and an office

tower. In summer 2007 the construction of the "Serdika

Center" began, which in addition to having about 50,000 m2

in retail space will also accommodate offices over a further

35,000 m2. A similar project, the "Olympian Mall" is being

built on Europa Blvd, which will offer roughly 45,000 m2 in

retail space and offices.

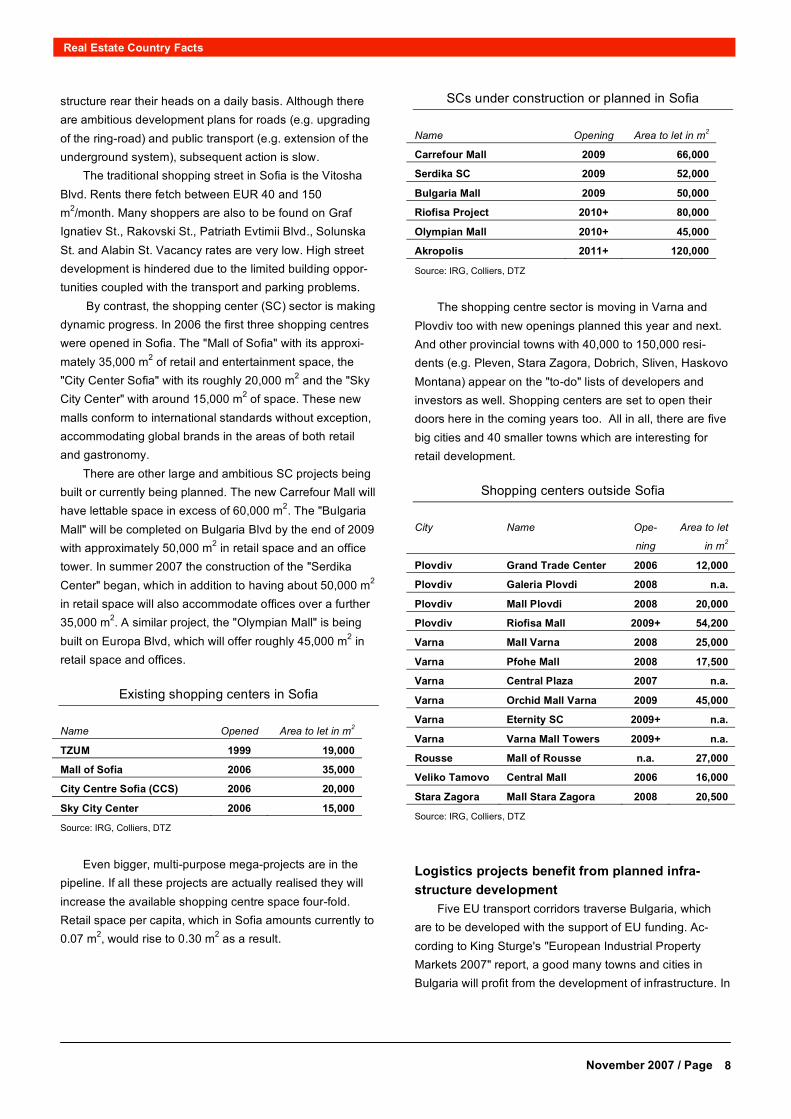

Existing shopping centers in Sofia

Name Opened Area to let in m2

TZUM 1999 19,000

Mall of Sofia 2006 35,000

City Centre Sofia (CCS) 2006 20,000

Sky City Center 2006 15,000

Source: IRG, Colliers, DTZ

Even bigger, multi-purpose mega-projects are in the

pipeline. If all these projects are actually realised they will

increase the available shopping centre space four-fold.

Retail space per capita, which in Sofia amounts currently to

0.07 m2, would rise to 0.30 m

2 as a result.

SCs under construction or planned in Sofia

Name Opening Area to let in m2

Carrefour Mall 2009 66,000

Serdika SC 2009 52,000

Bulgaria Mall 2009 50,000

Riofisa Project 2010+ 80,000

Olympian Mall 2010+ 45,000

Akropolis 2011+ 120,000

Source: IRG, Colliers, DTZ

The shopping centre sector is moving in Varna and

Plovdiv too with new openings planned this year and next.

And other provincial towns with 40,000 to 150,000 resi-

dents (e.g. Pleven, Stara Zagora, Dobrich, Sliven, Haskovo

Montana) appear on the "to-do" lists of developers and

investors as well. Shopping centers are set to open their

doors here in the coming years too. All in all, there are five

big cities and 40 smaller towns which are interesting for

retail development.

Shopping centers outside Sofia

City Name Ope-

ning

Area to let

in m2

Plovdiv Grand Trade Center 2006 12,000

Plovdiv Galeria Plovdi 2008 n.a.

Plovdiv Mall Plovdi 2008 20,000

Plovdiv Riofisa Mall 2009+ 54,200

Varna Mall Varna 2008 25,000

Varna Pfohe Mall 2008 17,500

Varna Central Plaza 2007 n.a.

Varna Orchid Mall Varna 2009 45,000

Varna Eternity SC 2009+ n.a.

Varna Varna Mall Towers 2009+ n.a.

Rousse Mall of Rousse n.a. 27,000

Veliko Tamovo Central Mall 2006 16,000

Stara Zagora Mall Stara Zagora 2008 20,500

Source: IRG, Colliers, DTZ

Logistics projects benefit from planned infra-

structure development

Five EU transport corridors traverse Bulgaria, which

are to be developed with the support of EU funding. Ac-

cording to King Sturge's "European Industrial Property

Markets 2007" report, a good many towns and cities in

Bulgaria will profit from the development of infrastructure. In

Real Estate Country Facts

November 2007 / Page 9

terms of expected growth in transport and traffic volume the

cities are ranked in the following order: Varna, Plovdiv,

Pleven, Burgas, Sofia and Vidin.

However, the inadequate legal and administrative con-

ditions that prevail in Bulgaria still could hinder investments.

Administrative bottlenecks in particular could lead to only

parts of the planned EU funding for infrastructure develop-

ment being made available.

The international airports in Sofia and Varna have al-

ready been modernised and expanded. The strong growth

in tourism has prompted no-frills airlines like Sky Europe for

example to fly regularly to Bulgaria. The key ports on the

Black Sea, Varna and Bourgas, are to be modernised and

developed. Although the ports on the Danube such as

Rousse and Lom are part of the EU transport corridor de-

velopment programme, there have yet to be any noticeable

investments.

The stock of logistics objects in Sofia is estimated by

Colliers at 1.2 million m2. Rents for old adapted premises

range from EUR 1.5 to 4/m2/month.

Modern logistic space

achieves between EUR 3.5 to 5.0/m2/month. One of the key

projects in Sofia is the Sofia Airport Center (SAC) with

space of 165,000 m2. Here, a class A business park is

being built. Locations along the Sofia ring-road would also

be suitable for logistics projects, were it not for the high

property prices that hinder development.

In addition to Sofia, the cities of Varna and Plovdiv

have also proved to be attractive locations for logistics

projects. Speculative areas are increasingly being offered

in industrial zones.

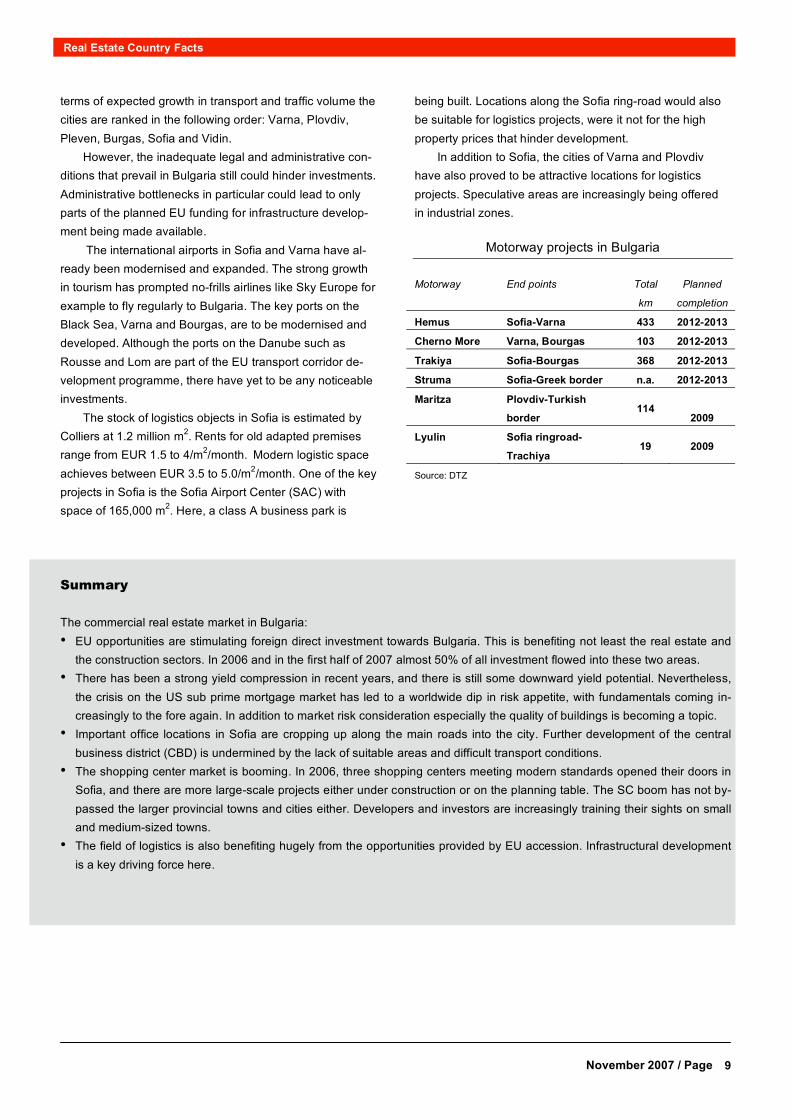

Motorway projects in Bulgaria

Motorway End points Total

km

Planned

completion

Hemus Sofia-Varna 433 2012-2013

Cherno More Varna, Bourgas 103 2012-2013

Trakiya Sofia-Bourgas 368 2012-2013

Struma Sofia-Greek border n.a. 2012-2013

Maritza Plovdiv-Turkish

border 114

2009

Lyulin Sofia ringroad-

Trachiya 19 2009

Source: DTZ

Summary

The commercial real estate market in Bulgaria:

• EU opportunities are stimulating foreign direct investment towards Bulgaria. This is benefiting not least the real estate and

the construction sectors. In 2006 and in the first half of 2007 almost 50% of all investment flowed into these two areas.

• There has been a strong yield compression in recent years, and there is still some downward yield potential. Nevertheless,

the crisis on the US sub prime mortgage market has led to a worldwide dip in risk appetite, with fundamentals coming in-

creasingly to the fore again. In addition to market risk consideration especially the quality of buildings is becoming a topic.

• Important office locations in Sofia are cropping up along the main roads into the city. Further development of the central

business district (CBD) is undermined by the lack of suitable areas and difficult transport conditions.

• The shopping center market is booming. In 2006, three shopping centers meeting modern standards opened their doors in

Sofia, and there are more large-scale projects either under construction or on the planning table. The SC boom has not by-

passed the larger provincial towns and cities either. Developers and investors are increasingly training their sights on small

and medium-sized towns.

• The field of logistics is also benefiting hugely from the opportunities provided by EU accession. Infrastructural development

is a key driving force here.

Real Estate Country Facts

November 2007 / Page 10

Contacts:

Bank Austria Creditanstalt AG

International Real Estate Finance

Vordere Zollamtstraße 13

A-1030 Vienna, Austria

Teresa Dreo

Tel: + 43 (0) 50505-55333

E-mail: [email protected]

Anton Höller

Tel: + 43 (0) 50505-55980

E-mail: anton.hö[email protected]

Real Estate Research

Karla Schestauber

Tel: + 43 (0) 50505-54784

E-mail: [email protected]

UniCredit New Europe Research Network

CEE Economic Research

Via Tortona, 33 – 20144 Mailand

Fabio Mucci

Tel: + 39 (0)2 4762-4055

E-Mail: [email protected]

UniCredit Bulbank

Real Estate Finance

7, Sveta Nedelq.Sq.

BG-1000 Sofia

Martin Gikov

Tel: + 359 2 9269 427

E-mail: [email protected]

Planning and Control Division, Economic Research Unit

1, Ivan Vazov Street

BG-1000 Sofia

Kristofor Pavlov

Tel: + 35 929 269390

E-mail: [email protected]

Katerina Topalova

Tel: + 35 929 269390

E-mail: [email protected]