re eor rer - Aljazira Capital · Please read Disclaimer on the back Insurance Sector Report Sector...

11

Please read Disclaimer on the back Insurance Sector Report Sector report | KSA | Q3-2017 November 2017 Saudi Insurance Sector- Quarterly Q3-2017 November 2017

-

Upload

nguyenkien -

Category

Documents

-

view

214 -

download

0

Transcript of re eor rer - Aljazira Capital · Please read Disclaimer on the back Insurance Sector Report Sector...

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

Saudi Insurance Sector- QuarterlyQ3-2017

November 2017

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

Company Name Codes

The Company for Cooperative Insurance Tawuniya

Salama Cooperative Insurance Co. Salama

UCA Cooperative Assurance Co. UCA

Al-Rajhi Company for Cooperative Insurance Al Rajihi Takaful

Al Alamiya for Cooperative Insurance Co. Al Alamiya

Allied Cooperative Insurance Group ACIG

Bupa Arabia for Cooperative Insurance Co. Bupa Arabia

Arabian Shield Cooperative Insurance Co. Arabian Shield

Buruj Cooperative Insurance Co. Buruj

Al Sagr Cooperative Insurance Co. Sagr Insurance

Malath Cooperative Insurance Co. Malath Insurance

Solidarity Saudi Takaful Co. Solidarity

Trade Union Cooperative Insurance Co. Trade Union

Sanad Cooperative Insurance Company Sanad

Walaa Cooperative Insurance Co. Walaa

Allianz Saudi Fransi Cooperative Insurance Co. Allianz SF

Al-Ahlia Insurance Co. Al Ahlia

The Mediterranean and Gulf Insurance and Reinsurance Co. MEDGULF

Saudi Indian Company for Cooperative Insurance Wafa Insurance

SABB Takaful Co. SABB Takaful

Saudi Arabian Cooperative Insurance Company SAICO

Gulf Union Cooperative Insurance Co. Gulf Union

Saudi Re for Cooperative Reinsurance Co. Saudi Re

Arabia Insurance Cooperative Company AICC

ALAHLI TAKAFUL COMPANY ATC

AXA Cooperative Insurance Co. AXA-Cooperative

Weqaya Takaful insurance and reinsurance Company Weqaya Takaful

CHUBB Arabia Cooperative Insurance Co. Chubb Arabia

Gulf General Cooperative Insurance Co. Gulf General

Wataniya Insurance Co. Wataniya

Amana Cooperative Insurance Co. Amana Insurance

Saudi Enaya Cooperative Insurance Co. Enaya

Alinma Tokio Marine Co. Alinma Tokio

MetLife AIG ANB Cooperative Insurance Co. MetLife

Aljazira Takaful Taawuni Co. Jazira Takaful

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

GWP-Sector WIse

Health

Motor

Property/ Fire

Others

55%27%

4%4%

10%

Energy

Bupa

Arab

ia

Enay

a

Al R

ajih

iTa

kafu

l

Sala

ma

Mal

ath

Insu

ranc

e

ATC

UCA

Aman

aIn

sura

nce

Alin

ma

Toki

o M

Gul

fG

ener

al

0%10%20%30%40%50%60%70%80%90%

100%

Health

Motor

Protection and Saving

Others

60%

34%

2% 2%

Accident and Liability

Bupa Arabia Tawuniya

Al Rajihi Takaful MEDGULF

Others

30.5%

17.2%

9.0%6.2%

4.5%

32.6%

AXA-Cooperative

Al R

ajih

i Tak

aful

Taw

uniy

a

Saud

i Re

Mal

ath

UCA

Bupa

Ara

bia

Trad

e Un

ion 3.7%

2.66%2.07%

0.8% 0.6%

-5.7%

-2.1%-0.9% -0.6% -0.5%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

2.0%

4.0%

6.0%

Met

Life

AIG

Ala

rabi

AICC

Arab

ian

Shie

ld

Q1

- 201

7

Q2

- 201

7

Q3

- 201

7

Q2

- 201

2

Q3

- 201

2

Q4

- 201

2

Q1

- 201

3

Q2

- 201

3

Q3

- 201

3

Q4

- 201

3

Q1

- 201

4

Q2

- 201

4

Q3

- 201

4

Q4

- 201

4

Q1

- 201

5

Q2

- 201

5

Q3

- 201

5

Q4

- 201

5

Q1

- 201

6

Q2

- 201

6

Q3

- 201

6

Q4

- 201

6 70%72%74%76%78%80%82%84%86%88%90%

0

2,000

4,000

6,000

8,000

10,000

12,000

Premium Ceded - LHS Retention Ratio - RHS

NPE-Sector Wise

Top 5 and Bottom 5- Retention Ratio Top 5 Gainers and Losers- GWP market Share

Premium Ceded-Industry

Net Premium Earned

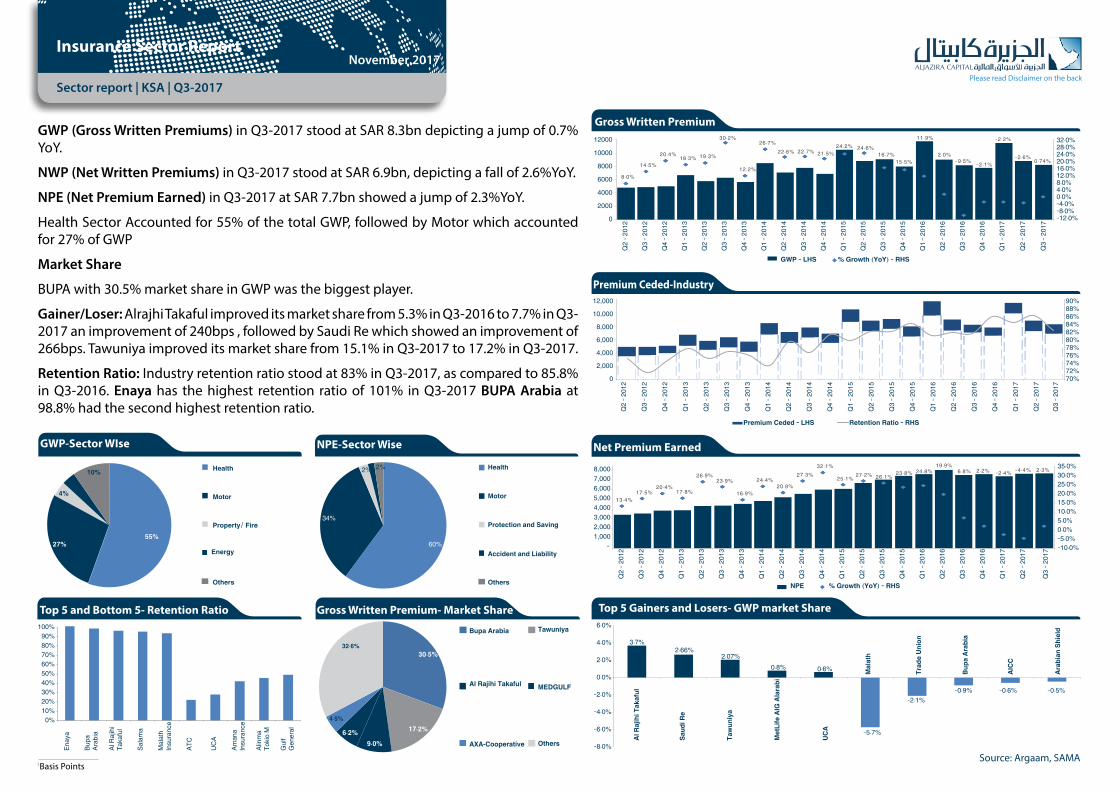

Gross Written PremiumGWP (Gross Written Premiums) in Q3-2017 stood at SAR 8.3bn depicting a jump of 0.7% YoY.

NWP (Net Written Premiums) in Q3-2017 stood at SAR 6.9bn, depicting a fall of 2.6%YoY.

NPE (Net Premium Earned) in Q3-2017 at SAR 7.7bn showed a jump of 2.3%YoY.

Health Sector Accounted for 55% of the total GWP, followed by Motor which accounted for 27% of GWP

Market Share

BUPA with 30.5% market share in GWP was the biggest player.

Gainer/Loser: Alrajhi Takaful improved its market share from 5.3% in Q3-2016 to 7.7% in Q3-2017 an improvement of 240bps , followed by Saudi Re which showed an improvement of 266bps. Tawuniya improved its market share from 15.1% in Q3-2017 to 17.2% in Q3-2017.

Retention Ratio: Industry retention ratio stood at 83% in Q3-2017, as compared to 85.8% in Q3-2016. Enaya has the highest retention ratio of 101% in Q3-2017 BUPA Arabia at 98.8% had the second highest retention ratio.

Q1

- 201

7

Q2

- 201

7

Q3

- 201

7

Q2

- 201

2

Q3

- 201

2

Q4

- 201

2

Q1

- 201

3

Q2

- 201

3

Q3

- 201

3

Q4

- 201

3

Q1

- 201

4

Q2

- 201

4

Q3

- 201

4

Q4

- 201

4

Q1

- 201

5

Q2

- 201

5

Q3

- 201

5

Q4

- 201

5

Q1

- 201

6

Q2

- 201

6

Q3

- 201

6

Q4

- 201

6-1,000 2,000 3,000 4,000 5,000 6,000 7,000 8,000

NPE % Growth (YoY) - RHS

-10.0%-5.0%0.0%5.0%10.0%15.0%20.0%25.0%30.0%35.0%

13.4%17.5%

20.4%17.8%

26.9%23.9%

16.9%

24.4%20.9%

27.3%32.1%

25.1% 27.2% 26.1%23.8% 24.8%

19.9%6.8% 2.2% -2.4% -4.4% 2.3%

-8.0%-12.0%

-4.0%0.0%4.0%8.0%12.0%16.0%20.0%24.0%28.0%32.0%

0

2000

4000

6000

8000

10000

12000

GWP - LHS % Growth (YoY) - RHS

Q1

- 201

7

Q2

- 201

7

Q3

- 201

7

Q2

- 201

2

Q3

- 201

2

Q4

- 201

2

Q1

- 201

3

Q2

- 201

3

Q3

- 201

3

Q4

- 201

3

Q1

- 201

4

Q2

- 201

4

Q3

- 201

4

Q4

- 201

4

Q1

- 201

5

Q2

- 201

5

Q3

- 201

5

Q4

- 201

5

Q1

- 201

6

Q2

- 201

6

Q3

- 201

6

Q4

- 201

6

8.0%

14.5%

20.4%18.3% 19.3%

30.2%

12.2%

26.7%22.6% 22.7% 21.5%

24.2% 24.6%16.7%

15.5%

11.9%

2.0%-9.5% -2.1%

-2.2%

-2.6%0.74%

Gross Written Premium- Market Share

Source: Argaam, SAMA1Basis Points

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

Bupa Arabia Tawuniya

MEDGULF Al Rajihi Takaful

Others

Malath AXA

25%25%

25%10%

8%

3%3%

Q3 - 2016 Q3 - 2017

Mal

ath

Insu

ranc

e

MED

GUL

F

Al R

ajih

i Tak

aful

Met

Life

AXA

Bupa

Ara

bia

Waf

a In

sura

nce

Taw

uniya

Allia

nz S

F

ACIG

Sala

ma

Trad

e Un

ion

Al A

hlia

Alin

ma

Toki

o M

SAIC

O

Wal

aa

Arab

ian

Shie

ld

Saud

i Re

AIC

C

Wat

aniya

Gul

f Uni

on

Enay

a

Gul

f Gen

eral

Aman

a In

sura

nce

Buru

j

Sagr

Insu

ranc

e

UCA

Chu

bb A

rabi

a

Al A

lam

iya

Solid

arity

ATC

SABB

Tak

aful

Jazir

a Ta

kafu

l0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

Mal

ath

Insu

ranc

e

Met

Life

AIG

Ala

rabi

Al R

ajih

i Tak

aful

Bupa

Ara

bia

Coo

pera

tive

Waf

a In

sura

nce

Alin

ma

Toki

o M

Wal

aa In

sura

nce

Arab

ian

Shie

ld

Sagr

Insu

ranc

e

Gul

f Gen

eral

Chu

bb A

rabi

a

Aman

a In

sura

nce

SABB

Tak

aful

Jazir

a Ta

kafu

l

Others

Health

Motor

Protection and Saving

Others

64%

32%

2% 2%

Engineering

Q3 - 2016 Q3 - 2017

80%

140%160%

100%120%

0%

60%

20%40%

180%

MED

GUL

F

Aman

a In

sura

nce

Alin

ma

Tokio

M

Wat

aniya

Met

Life

AIG

Ala

rabi

Enay

a

Mal

ath

Insu

ranc

e

Gul

f Uni

on

SABB

Tak

aful

Waf

a In

sura

nce

SAIC

O

Allia

nz S

F

AXA

Saud

i Re

Sagr

Insu

ranc

e

ACIG

AICC

Al A

hlia

Al R

ajih

i Tak

aful

Sala

ma

Tawu

niya

Bupa

Ara

bia

Al A

lam

iya

Trad

e Un

ion

Gul

f Gen

eral

Arab

ian

Shie

ld

Buru

j

Chub

b Ar

abia

Wal

aa In

sura

nce

Solid

arity

UCA

ATC

Jazir

a Ta

kafu

l

Q1

- 201

7

Q2

- 201

7

Q2

- 201

2

Q3

- 201

2

Q3

- 201

7

Q4

- 201

2

Q1

- 201

3

Q2

- 201

3

Q3

- 201

3

Q4

- 201

3

Q1

- 201

4

Q2

- 201

4

Q3

- 201

4

Q4

- 201

4

Q1

- 201

5

Q2

- 201

5

Q3

- 201

5

Q4

- 201

5

Q1

- 201

6

Q2

- 201

6

Q3

- 201

6

Q4

- 201

6

Net Claims Paid - LHS % Growth (YoY) - RHS

-

1,000

2,000

3,000

4,000

5,000

6,000

7,000

24% 24%32% 29%

38% 40%

66%

25%17% 17%

-7%

24% 23% 21%29%

17% 19%

7%-2% 0.2%

-13.2%

3.4%

-20%-10%0%10%20%30%40%50%60%70%

IN M

N S

AR Q3 - 2016 Q3 - 2017

0200400600800

10001200140016001800

Bupa

Ara

bia

Taw

uniya

MED

GUL

F

Al R

ajih

i Tak

aful

Mal

ath

Insu

ranc

e

AXA

Waf

a In

sura

nce

Allia

nz S

F

Trad

e Un

ion

SAIC

O

Wal

aa In

sura

nce

Sala

ma

Arab

ian

Shie

ld

Saud

i Re

ACIG

UCA

AIC

C

Buru

j

Wat

aniya

Gul

f Uni

on

Met

Life

AIG

Ala

rabi

Sagr

Insu

ranc

e

Gul

f Gen

eral

ATC

Alin

ma

Toki

o M

Chu

bb A

rabi

a

Solid

arity

Al A

hlia

Enay

a

Al A

lam

iya

Aman

a In

sura

nce

SABB

Tak

aful

Jazir

a Ta

kafu

l

Gross Claims Paid - LHS % Growth (YoY) - RHS

Q3

- 201

7

Q1

- 201

7

Q2

- 201

7

Q2

- 201

2

Q3

- 201

2

Q4

- 201

2

Q1

- 201

3

Q2

- 201

3

Q3

- 201

3

Q4

- 201

3

Q1

- 201

4

Q2

- 201

4

Q3

- 201

4

Q4

- 201

4

Q1

- 201

5

Q2

- 201

5

Q3

- 201

5

Q4

- 201

5

Q1

- 201

6

Q2

- 201

6

Q3

- 201

6

Q4

- 201

6

9%

24% 22%

30%

27% 19%25%

17%24%

31%

18%

23%

24%

9%

28%

13%9% 7%

-3%

7%

-10%-5%0%5%

10%15%20%25%30%35%

-

1,500

3,000

4,500

6,000

7,500

-1%-7%

Claims Market Share-Company wise Claims Market Share-sector wise

Loss Ratio Combined Ratio

Net Claims Paid

Gross Claims PaidGCP (Gross Claims Paid) in Q3-2017 stood at SAR 6.1bn depicting a jump of 7.0% YoY.

NCP (Net Claim Paid) in Q3-2017 stood at SAR 5.7bn, depicting a rise of 3.4%YoY.

Market Share

BUPA Arabia with 25.3% market share in GCP paid the highest claims of SAR 1.33bn, followed by Tawuniya at 24.9% market share in claims.

Aljazira Takaful paid the lowest claims of SAR 2.02mn.

Health sector accounted for the highest share in claims at 64% , followed by Motor sector at 32%.

Malath insurance had the highest loss ratio of 99.0% in Q3-2017,followed by MedGulf at 88.1% in Q3-2017.

Aljazira Takaful had the lowest loss ratio of 10.3%.

UCA had the highest combined ratio of 153%, whereas Amana insurance had the lowest combined ratio of 23.4%.

Claims Paid-Company wise

Source: Argaam, SAMA, AlJazira Capital

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

0.0%

0.5%

1.0%

1.5%

2.0%

2.5%

3.0%

3.5%

4.0%

Solidarity Jazira Takaful

Amana Buruj Walaa Chubb Arabia

Arabian Shield

ATC Wataniya Sagr

0%

20%

40%

Buru

j

Al R

ajih

i Tak

aful

Arab

ian

Shie

ld

Sala

ma

Wal

aa In

sura

nce

Mal

ath

Alin

ma

Toki

o M

Enay

a

Met

Life

AIG

MED

GUL

F

-80%

-60%

-40%

-20%

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

Jazira Takaful

Solidarity Amana Buruj Chubb Arabia

Sagr Arabian Shield

GulfGeneral

ATC SaudiRe

0.0%

5.0%

10.0%

-15.0%

-10.0%

-5.0% Buru

j

Solid

arity

Arab

ian

Shie

ld

Wal

aa In

sura

nce

Sala

ma

Mal

ath

Insu

ranc

e

Alin

ma

Tokio

M

Met

Life

AIG

Enay

a

MED

GUL

F

In M

n SA

R

Al R

ajih

i Tak

aful

Taw

uniya

Bupa

Ara

bia

Saud

i Re

MED

GUL

F

AXA

Trad

e Un

ion

Aman

a

Jazir

a Ta

kafu

l

SABB

Tak

aful

Alin

ma

Tokio

M

Al A

hlia

Solid

arity

Allia

nz S

F

Al A

lam

iya

ATC

Met

Life

AIG

Buru

j

SAIC

O

UCA

Wat

aniya

ACIG

Sala

ma

Enay

a

AIC

C

Arab

ian

Shie

ld

Chu

bb A

rabi

a

Gul

f Uni

on

Sagr

Insu

ranc

e

Waf

a In

sura

nce

Mal

ath

Gul

f Gen

eral

Wal

aa 0

5101520253035404550

In M

n SA

R

Bupa

Ara

bia

Tawu

niya

MED

GUL

F

Al R

ajih

i Tak

aful

Wal

aa In

sura

nce

Buru

j

Sala

ma

Arab

ian

Shie

ld

Solid

arity

Trad

e Un

ion

Aman

a In

sura

nce

SAIC

O

Mal

ath

Insu

ranc

e

AXA

ATC

Jazir

a Ta

kafu

l

Allia

nz S

F

Wat

aniya

Chub

b Ar

abia

Sagr

Insu

ranc

e

Al A

lam

iya

Gul

f Gen

eral

ACIG

AICC

Al A

hlia

Gul

f Uni

on

SABB

Tak

aful

Enay

a

Saud

i Re

UCA

Alin

ma

Tokio

M

Waf

a In

sura

nce

Met

Life

AIG

Ala

rabi

-100

-50

0

50

100

150

200

In M

n SA

R

Bupa

Ara

bia

Taw

uniy

a

Al R

ajih

i Tak

aful

MED

GU

LF

Wal

aa In

sura

nce

Buru

j

Arab

ian

Shie

ld

Sala

ma

Solid

arity

SAIC

O

Trad

e U

nion

Aman

a In

sura

nce

Mal

ath

Insu

ranc

e

AXA

Coo

pera

tive

ATC

Wat

aniy

a

Chu

bb A

rabi

a

Al A

lam

iya

Sagr

Insu

ranc

e

Allia

nz S

F

Jazi

ra T

akaf

ul

Gul

f Gen

eral

ACIG

AIC

C

Al A

hlia

Gul

f Uni

on

SABB

Tak

aful

Enay

a

UC

A

Waf

a In

sura

nce

Alin

ma

Toki

o M

-50

0

50

100

150

200

250

In M

N S

AR

Q1

- 201

7

Q2

- 201

7

Q3

- 201

2

Q3

- 201

7

Q4

- 201

2

Q1

- 201

3

Q2

- 201

3

Q3

- 201

3

Q4

- 201

3

Q1

- 201

4

Q2

- 201

4

Q3

- 201

4

Q4

- 201

4

Q1

- 201

5

Q2

- 201

5

Q3

- 201

5

Q4

- 201

5

Q1

- 201

6

Q2

- 201

6

Q3

- 201

6

Q4

- 201

6

17.3% YoY235.5% QoQ

340 179 (49) (117)

3 (1,159) (41)

199 405 233 (31)

240 491 122 285 432 803 620 319 197.9 664.1

(1,300)

(900)

(500)

(100)

300

700

1,100 -

Operating Margins-Highest 10 Net Margins-Highest 10

ROE-Top 5 /Bottom 5 ROA-Top 5/ Bottom 5 Investment Income

Net Income-Company wise

Net IncomeNet income for the sector stood at SAR 664.1mn in Q3-2017, as compared to SAR 802.1mn in Q3-2016, depicting a fall of 17.2%. On a QoQ basis net income showed a 235.5% increase. Net income before Zakat stood at SAR 756.7mn, depicting a fall of 15.4%, whereas a 144.2% jump on QoQ basis

BUPA with net income of SAR 198.2mn, showed a fall of 18.3%YoY.

BUPA showed the highest surplus, from its insurance operations , at SAR 229.4mn, depicting a fall of 21.0%YoY and a QoQ jump of 57.8%.

AlRajhi takaful showed the highest investment income of SAR 47.8mn in the sector, registering growth of 62.7%YoY and 9.9%QoQ.

Solidarity showed the highest Operating margins at 3.8%, whereas Jazira takaful showed the highest net margin at 35.7%, respectively.

Buruj posted the highest ROE of 35.8%

Buruj also posted the highest ROA of 11.0%.

Surplus From Insurance Operations

Source: Argaam

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

Insurance Sector (LHS) Bupa (RHS)

90

100

110

120

130

140

6,500.00

6,700.00

6,900.00

7,100.00

7,300.00

7,500.00

7,700.00

Dec 2016 Mar 2017 Jun 2017 Sep 2017

TASI (LHS) Insurance Sector (RHS)

4,300.00

4,500.00

4,700.00

4,900.00

5,100.00

5,300.00

5,500.00

6,500.00

6,700.00

6,900.00

7,100.00

7,300.00

7,500.00

7,700.00

Dec 2016 Mar 2017 Jun 2017 Sep 2017

Insurance Sector (LHS) Medgulf (RHS)

10

20

30

40

50

60

70

80

6,500.00

6,700.00

6,900.00

7,100.00

7,300.00

7,500.00

7,700.00

Dec 2016 Mar 2017 Jun 2017 Sep 2017

Insurance Sector (LHS) Alrajhi takaful (RHS)

30

35

40

45

50

55

60

65

6,500.00

6,700.00

6,900.00

7,100.00

7,300.00

7,500.00

7,700.00

Dec 2016 Mar 2017 Jun 2017 Sep 2017

Insurance Sector (LHS) Tawuniya (RHS)

80

85

90

95

100

105

6,500.00

6,700.00

6,900.00

7,100.00

7,300.00

7,500.00

7,700.00

Dec 2016 Mar 2017 Jun 2017 Sep 2017

Insurance Sector (LHS) WALAA (RHS)

15

20

25

30

35

6,500.00

6,700.00

6,900.00

7,100.00

7,300.00

7,500.00

7,700.00

Dec 2016 Mar 2017 Jun 2017 Sep 2017

In M

n SA

R

-

2,000

4,000

6,000

8,000

10,000

12,000

Tawuniya Bupa Arabia AlRajhi Takaful MEDGULF WALAA

0.00.20.40.60.81.01.21.41.61.82.0

Saudi Re SagrInsurance

SAICO U C A Trade Union Gulf General Gulf Union Al-Ahlia AXACooperative

Solidarity

9.1%

4.8%4.3%

2.0% 1.7%

0.0%1.0%2.0%3.0%4.0%5.0%6.0%7.0%8.0%9.0%

10.0%

Sagr Insurance Arabian Shield Tawuniya Jazira Takaful Buruj

0.0

2.0

4.0

6.0

8.0

10.0

12.0

Buruj ArabianShield

Gulf Union Solidarity SAICO Trade Union U C A WALAA Salama Saudi Re

BUPA-1 Yr Performance

Tadawul Insurance Index- 1 Yr Performance

Alrajhi Takaful-1 Yr Performance

Tawuniya-1 Yr Performance

Medgulf-1 Yr Performance Walaa-1 Yr Performance Top 5 Companies-Market Cap

Lowest PB

Highest Dividend Yield

Lowest PEUnited Cooperative Assurance had the lowest PE of 8.3x, followed by Buruj with a PE of 8.5x.

Saudi Re for Cooperative Reinsurance Co has the lowest PB of 0.8x, followed by Sagr insurance with a PB of 1.4x

Only 5 companies gave out dividends, SAGR insurance had the highest dividend yield of 9.1% followed by Arabian Sheild with a dividend yield of 4.8%

Source: Tadawul, Bloomberg, prices as of 13 of June 2017

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

APPENDIX 1

GWP YoY %Increase

QoQ %Increase NWP YoY

%IncreaseQoQ

%Increase NPE YoY %Increase QoQ %Increase

Q3-2016 Q2-2017 Q3-2017 Q3-2016 Q2-2017 Q3-2017 Q3-2016 Q2-2017 Q3-2017

MetLife AIG Alarabi 36 88 103 185.4% 17.1% 26 63 89 241.7% 41.2% 42 55 69 66.1% 25.5%

Jazira Takaful 29 32 28 -5.9% -13.2% 15 13 13 -10.2% 1.0% 7 9 7 -2.9% -18.9%

Tawuniya 1,241 2,104 1,421 14.5% -32.5% 1,077 1,764 1,161 7.7% -34.2% 1,759 1,832 1,883 7.0% 2.8%

Malath Insurance 531 144 62 -88.3% -56.8% 466 127 55 -88.2% -56.6% 351 227 220 -37.3% -3.2%

MEDGULF 511 869 513 0.4% -40.9% 420 702 426 1.3% -39.4% 714 586 565 -20.9% -3.7%

Allianz SF 180 227 147 -18.0% -35.2% 115 134 102 -11.0% NM* 130 166 160 23.3% NM*

Salama 132 202 159 20.4% -21.3% 125 194 148 18.9% -23.7% 113 168 181 60.3% 7.9%

Walaa Insurance 268 218 284 5.9% 30.7% 193 173 174 -9.6% 0.7% 161 200 196 21.7% -2.2%

Arabian Shield 153 165 115 -24.5% -30.2% 101 114 79 -22.0% -30.6% 102 122 106 3.3% -13.5%

SABB Takaful 49 45 51 2.8% 11.6% 36 34 39 6.9% 14.3% 32 34 33 3.0% -4.3%

SAICO 160 149 157 -2.1% 5.5% 108 105 142 31.6% 36.0% 124 130 142 14.6% 9.1%

Wafa Insurance 93 119 100 7.1% -16.1% 78 73 62 -20.8% -15.5% 126 101 98 -22.4% -3.3%

Gulf Union 46 79 32 -29.4% -58.9% 26 52 17 -35.2% -67.2% 23 56 54 130.2% -4.1%

ATC 115 58 120 4.1% 106.1% 29 10 24 -17.8% 132.3% 21 21 16 -24.3% -24.3%

Al Ahlia 43 46 53 23.0% 14.7% 38 43 48 25.0% 12.1% 43 37 37 -15.5% -1.4%

ACIG 136 102 113 -17.4% 10.3% 115 88 98 -14.2% 12.0% 110 87 82 -24.9% -5.6%

AICC 110 69 59 -46.5% -14.5% 96 46 38 -60.8% -19.0% 70 73 54 -23.8% -26.4%

Trade Union 274 289 103 -62.5% -64.4% 231 245 77 -66.8% -68.7% 193 189 176 -9.0% -6.9%

Solidarity 55 21 37 -33.3% 79.5% 48 18 30 -37.9% 70.7% 52 43 40 -23.7% -8.0%

Wataniya 148 83 152 2.4% 83.6% 89 42 88 -1.5% 106.5% 65 74 73 11.9% -1.7%

Amana Insurance 11 16 9 -18.4% -44.6% 4 6 7 72.0% 16.0% 58 14 11 -81.6% -24.1%

AXA-Cooperative 387 220 369 -4.6% 67.9% 346 195 334 -3.5% 71.4% 265 323 300 13.5% -6.9%

Gulf General 37 46 26 -29.9% -44.5% 17 23 11 -35.5% -54.1% 34 29 23 -31.8% -19.5%

Buruj 109 144 95 -12.8% -34.4% 92 133 81 -12.3% -39.3% 100 117 131 30.7% 11.6%

Al Alamiya 64 48 57 -11.0% 18.8% 27 26 21 -20.8% -16.1% 50 46 39 -22.5% -14.4%

Saudi Re 82 121 303 267.0% 150.2% 75 89 89 18.9% 0.9% 119 143 150 26.0% 5.0%

UCA 64 251 116 82.5% -53.7% 25 61 39 51.3% -36.7% 146 52 37 -75.0% -30.0%

Bupa Arabia 2,579 1,848 2,523 -2.2% 36.5% 2,567 1,832 2,497 -2.7% 36.3% 1,939 1,909 1,937 -0.1% 1.4%

Sagr Insurance 13 93 61 380.0% -34.6% (9) 68 56 -744.3% -18.0% 95 42 58 -39.1% 36.6%

Chubb Arabia 42 48 42 0.6% -13.4% 17 28 14 -16.8% -49.0% 29 27 26 -11.1% -2.7%

Enaya 21 66 59 178.0% -10.3% 13 65 60 365.4% -8.6% 14 34 52 270.2% 55.5%

Al Rajhi Takaful 434 680 742 71.2% 9.2% 410 649 711 73.2% 9.6% 407 686 719 76.5% 4.8%

Alinma Tokio M 47 103 51 7.8% -50.9% 17 25 27 58.8% 8.7% 33 32 35 4.0% 9.1%

Total 8,201 8,794 8,261 0.7% -6.1% 7,035 7,240 6,856 -2.5% -5.3% 7,529 7,665 7,706 2.4% 0.5%Source: Argaam, *NM: Not meaningfull

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

APPENDIX 2Gross Claims Paid YoY %Increase QoQ %Increase Net Claims Paid YoY %Increase QoQ %Increase

Q3-2016 Q2-2017 Q3-2017 Q3-2016 Q2-2017 Q3-2017

Tawuniya 1,237 1,519 1,512 22.2% -0.5% 1,306 1,230 1,484 13.6% 20.6%

Salama 62 112 113 81.6% 1.0% 80 83 128 60.0% 54.1%

UCA 187 64 60 -67.9% -5.6% 124 98 15 -87.8% -84.6%

Al Rajhi Takaful 287 559 462 60.8% -17.4% 303 329 592 95.1% 79.9%

Al Alamiya 28 23 18 -34.6% -21.6% 25 25 12 -51.9% -52.2%

ACIG 75 73 60 -19.6% -17.6% 81 79 57 -29.7% -28.0%

Bupa Arabia 1,333 1,647 1,536 15.2% -6.8% 1,511 1,399 1,475 -2.4% 5.5%

Arabian Shield 43 90 69 58.8% -23.3% 66 66 61 -6.8% -7.1%

Buruj 42 61 59 42.1% -3.8% 56 65 78 39.1% 20.6%

Sagr Insurance 59 42 26 -56.2% -39.0% 69 41 35 -48.8% -14.6%

Malath Insurance 436 264 198 -54.6% -25.0% 400 472 168 -58.1% -64.5%

Solidarity 36 26 24 -33.6% -7.2% 25 18 6 -77.3% -69.0%

Trade Union 142 143 141 -0.8% -1.3% 176 153 116 -34.0% -24.1%

Walaa Insurance 67 125 101 49.2% -19.5% 79 83 100 25.9% 20.0%

Allianz SF 89 147 160 79.7% 8.9% 100 102 124 23.8% 22.1%

Al Ahlia 31 24 23 -27.3% -5.5% 36 27 22 -38.9% -18.9%

MEDGULF 666 633 632 -5.1% -0.0% 657 539 459 -30.2% -14.9%

Wafa Insurance 104 149 96 -7.8% -35.4% 102 94 74 -27.6% -21.5%

SABB Takaful 5 15 8 57.3% -45.9% 4 5 3 -18.6% -41.1%

SAICO 93 135 110 18.6% -19.0% 80 76 95 19.3% 26.1%

Gulf Union 20 47 50 157.5% 7.9% 11 12 31 170.0% 154.0%

Saudi Re 48 82 57 19.8% -30.3% 569 77 114 -79.9% 48.7%

AICC 73 63 47 -35.4% -25.5% 56 37 27 -52.6% -28.2%

ATC 11 35 18 65.2% -48.7% 4 5 (0) -108.3% -107.1%

AXA-Cooperative 206 211 203 -1.5% -4.1% 219 217 238 8.4% 9.7%

Chubb Arabia 28 29 31 11.3% 7.3% 10 14 10 8.3% -27.8%

Gulf General 39 35 39 -1.6% 9.1% 20 16 10 -48.3% -38.0%

Wataniya 75 57 80 6.7% 39.8% 46 42 49 7.1% 15.8%

Amana Insurance 48 22 12 -76.0% -47.6% 63 33 (8) -112.4% -123.5%

Enaya 13 23 31 128.7% 31.9% 8 6 31 286.5% 387.9%

Alinma Tokio M 45 30 30 -34.2% -1.3% 23 23 18 -23.1% -23.7%

MetLife AIG Alarabi 37 46 59 59.1% 27.3% 33 36 66 97.3% 85.3%

Jazira Takaful 1 2 2 128.1% 26.9% 1 2 2 157.4% 16.8%

Total 5,667 6,533 6,064 7.0% -7.2% 6,344 5,505 5,692 -10.3% 3.4%Source: Argaam, *NM: Not meaningfull

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

APPENDIX 3Net income Before Zakat YoY %Increase QoQ %Increase Net Income YoY %Increase QoQ %Increase

Q3-2016 Q2-2017 Q3-2017 Q3-2016 Q2-2017 Q3-2017

MetLife AIG Alarabi (4.2) (3.2) (10.4) 146.0% 219.7% (4.2) (3.8) (10.9) 158.9% 188.4%

Jazira Takaful 6.4 8.9 6.8 6.9% -23.0% 6.0 8.1 6.5 9.2% -19.8%

Tawuniya 283.2 248.8 159.7 -43.6% -35.8% 259.6 231.0 141.5 -45.5% -38.7%

Malath Insurance 1.3 5.0 11.1 730.9% 120.4% 0.0 3.5 9.6 NM* 171.5%

MEDGULF 60.0 (417.3) 60.1 0.1% -114.4% 51.8 (440.0) 56.6 9.2% -112.9%

Allianz SF 6.3 7.8 8.0 26.4% 2.3% 4.9 6.0 6.4 30.2% 6.0%

Salama 8.7 16.2 22.0 152.1% 36.3% 7.5 14.9 20.8 177.5% 39.4%

Walaa Insurance 40.0 35.6 44.4 11.0% 24.7% 38.0 32.3 41.1 8.3% 27.2%

Arabian Shield 18.7 22.3 23.1 23.6% 3.5% 16.1 19.2 20.0 24.7% 4.4%

SABB Takaful 2.7 1.8 2.1 -24.8% 15.5% 1.3 0.6 0.7 -47.0% 19.6%

SAICO 17.4 11.5 16.4 -5.6% 42.4% 15.5 9.8 14.4 -6.9% 46.6%

Wafa Insurance 8.7 2.9 (3.6) -141.3% -222.5% 8.4 1.1 (5.2) -162.3% -590.6%

Gulf Union (0.2) 5.8 2.0 -954.9% -65.3% (0.9) 4.0 0.9 -207.5% -76.7%

ATC 7.1 11.1 8.7 22.5% -21.5% 5.8 9.4 8.7 49.9% -7.8%

Al Ahlia (8.6) 4.1 3.2 -136.6% -22.6% (9.3) 3.4 2.0 -121.6% -41.6%

ACIG 4.7 6.6 3.9 -16.4% -40.5% 3.8 6.1 3.0 -22.5% -51.6%

AICC (1.7) 3.6 3.9 -328.4% 6.0% (1.7) 1.6 2.5 -248.2% 60.5%

Trade Union 27.2 25.1 16.7 -38.6% -33.6% 25.7 22.6 16.7 -35.0% -26.2%

Solidarity 14.1 12.9 19.6 39.1% 51.7% 13.4 13.1 17.8 33.1% 36.0%

Wataniya 8.0 7.7 8.2 1.9% 6.7% 7.4 6.9 5.8 -21.6% -15.2%

Amana Insurance 7.9 (1.8) 14.6 85.3% -916.1% 7.6 (2.3) 15.1 98.2% -757.6%

AXA-Cooperative 11.2 14.8 12.6 12.5% -15.1% 7.5 10.8 8.8 16.8% -18.4%

Gulf General 7.0 11.3 4.6 -33.4% -59.0% 6.7 9.8 3.4 -48.8% -65.1%

Buruj 8.6 27.8 24.0 180.5% -13.7% 7.0 25.1 21.4 203.6% -15.0%

Al Alamiya 12.2 7.1 8.8 -27.8% 23.9% 10.0 6.4 4.8 -51.6% -24.3%

Saudi Re 2.7 13.4 (0.3) -110.0% -102.0% (0.7) 9.4 (3.6) 436.8% -138.6%

UCA 26.1 27.4 (2.2) -108.3% -107.9% 23.1 25.9 (3.7) -115.9% -114.1%

Bupa Arabia 260.4 145.8 217.0 -16.7% 48.8% 244.5 127.0 198.2 -18.9% 56.1%

Sagr Insurance 26.7 6.9 7.5 -71.7% 8.8% 21.8 2.3 5.1 -76.5% 123.5%

Chubb Arabia 9.5 9.8 7.8 -17.6% -20.3% 7.6 8.1 5.8 -23.9% -28.7%

Enaya (6.3) (3.5) 0.7 -111.6% -120.9% (6.5) (4.1) 0.1 -102.0% -103.1%

Al Rajihi Takaful 29.6 41.1 58.7 98.5% 42.9% 26.5 38.1 54.0 103.8% 41.6%

Alinma Tokio M (1.1) (7.5) (3.2) 193.4% -56.7% (2.2) (8.5) (4.3) 94.6% -49.7%

Total 894.2 309.8 756.7 -15.4% 144.2% 802.1 197.9 664.1 -17.2% 235.5%Source: Argaam, *NM: Not meaningfull

Please read Disclaimer on the back

Insurance Sector Report

Sector report | KSA | Q3-2017

November 2017

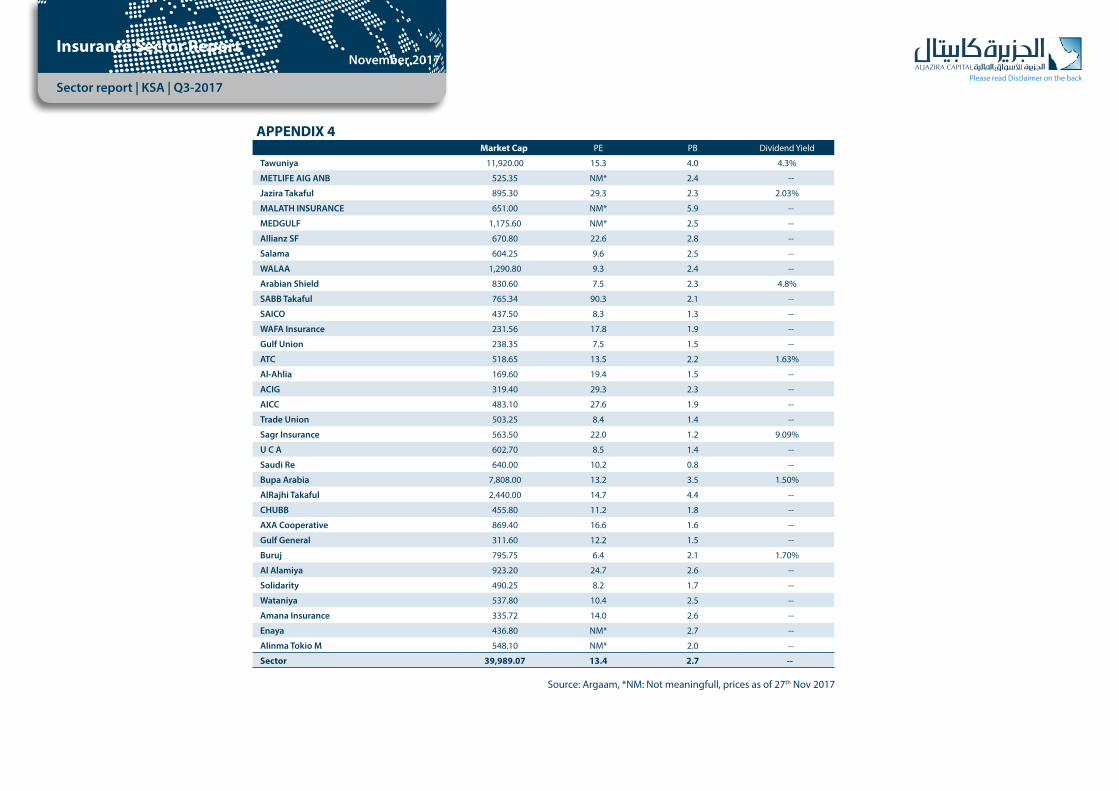

APPENDIX 4Market Cap PE PB Dividend Yield

Tawuniya 11,920.00 15.3 4.0 4.3%

METLIFE AIG ANB 525.35 NM* 2.4 --

Jazira Takaful 895.30 29.3 2.3 2.03%

MALATH INSURANCE 651.00 NM* 5.9 --

MEDGULF 1,175.60 NM* 2.5 --

Allianz SF 670.80 22.6 2.8 --

Salama 604.25 9.6 2.5 --

WALAA 1,290.80 9.3 2.4 --

Arabian Shield 830.60 7.5 2.3 4.8%

SABB Takaful 765.34 90.3 2.1 --

SAICO 437.50 8.3 1.3 --

WAFA Insurance 231.56 17.8 1.9 --

Gulf Union 238.35 7.5 1.5 --

ATC 518.65 13.5 2.2 1.63%

Al-Ahlia 169.60 19.4 1.5 --

ACIG 319.40 29.3 2.3 --

AICC 483.10 27.6 1.9 --

Trade Union 503.25 8.4 1.4 --

Sagr Insurance 563.50 22.0 1.2 9.09%

U C A 602.70 8.5 1.4 --

Saudi Re 640.00 10.2 0.8 --

Bupa Arabia 7,808.00 13.2 3.5 1.50%

AlRajhi Takaful 2,440.00 14.7 4.4 --

CHUBB 455.80 11.2 1.8 --

AXA Cooperative 869.40 16.6 1.6 --

Gulf General 311.60 12.2 1.5 --

Buruj 795.75 6.4 2.1 1.70%

Al Alamiya 923.20 24.7 2.6 --

Solidarity 490.25 8.2 1.7 --

Wataniya 537.80 10.4 2.5 --

Amana Insurance 335.72 14.0 2.6 --

Enaya 436.80 NM* 2.7 --

Alinma Tokio M 548.10 NM* 2.0 --

Sector 39,989.07 13.4 2.7 --

Source: Argaam, *NM: Not meaningfull, prices as of 27th Nov 2017

Asset Management | Brokerage | Corporate Finance | Custody | Advisory

Head Office: King Fahad Road, P.O. Box: 20438, Riyadh 11455, Saudi Arabia، Tel: 011 2256000 - Fax: 011 2256068

RESE

ARC

H

DIV

ISIO

NRE

SEAR

CH

DIVI

SION

RATI

NG

TERM

INO

LOG

YBR

OKE

RAG

E A

ND

IN

VEST

MEN

T CE

NTE

RS

DIV

ISIO

N

Disclaimer

AlJazira Capital, the investment arm of Bank AlJazira, is a Shariaa Compliant Saudi Closed Joint Stock company and operating under the regulatory supervision of the Capital Market Authority. AlJazira Capital is licensed to conduct securities business in all securities business as authorized by CMA, including dealing, managing, arranging, advisory, and custody. AlJazira Capital is the continuation of a long success story in the Saudi Tadawul market, having occupied the market leadership position for several years. With an objective to maintain its market leadership position, AlJazira Capital is expanding its brokerage capabilities to offer further value-added services, brokerage across MENA and International markets, as well as offering a full suite of securities business.

1. Overweight: This rating implies that the stock is currently trading at a discount to its 12 months price target. Stocks rated “Overweight” will typically provide an upside potential of over 10% from the current price levels over next twelve months.

2. Underweight: This rating implies that the stock is currently trading at a premium to its 12 months price target. Stocks rated “Underweight” would typically decline by over 10% from the current price levels over next twelve months.

3. Neutral: The rating implies that the stock is trading in the proximate range of its 12 months price target. Stocks rated “Neutral” is expected to stagnate within +/- 10% range from the current price levels over next twelve months.

4. Suspension of rating or rating on hold (SR/RH): This basically implies suspension of a rating pending further analysis of a material change in the fundamentals of the company.

The purpose of producing this report is to present a general view on the company/economic sector/economic subject under research, and not to recommend a buy/sell/hold for any security or any other assets. Based on that, this report does not take into consideration the specific financial position of every investor and/or his/her risk appetite in relation to investing in the security or any other assets, and hence, may not be suitable for all clients depending on their financial position and their ability and willingness to undertake risks. It is advised that every potential investor seek professional advice from several sources concerning investment decision and should study the impact of such decisions on his/her financial/legal/tax position and other concerns before getting into such investments or liquidate them partially or fully. The market of stocks, bonds, macroeconomic or microeconomic variables are of a volatile nature and could witness sudden changes without any prior warning, therefore, the investor in securities or other assets might face some unexpected risks and fluctuations. All the information, views and expectations and fair values or target prices contained in this report have been compiled or arrived at by Aljazira Capital from sources believed to be reliable, but Aljazira Capital has not independently verified the contents obtained from these sources and such information may be condensed or incomplete. Accordingly, no representation or warranty, express or implied, is made as to, and no reliance should be placed on the fairness, accuracy, completeness or correctness of the information and opinions contained in this report. Aljazira Capital shall not be liable for any loss as that may arise from the use of this report or its contents or otherwise arising in connection therewith. The past performance of any investment is not an indicator of future performance. Any financial projections, fair value estimates or price targets and statements regarding future prospects contained in this document may not be realized. The value of the security or any other assets or the return from them might increase or decrease. Any change in currency rates may have a positive or negative impact on the value/return on the stock or securities mentioned in the report. The investor might get an amount less than the amount invested in some cases. Some stocks or securities maybe, by nature, of low volume/trades or may become like that unexpectedly in special circumstances and this might increase the risk on the investor. Some fees might be levied on some investments in securities. This report has been written by professional employees in Aljazira Capital, and they undertake that neither them, nor their wives or children hold positions directly in any listed shares or securities contained in this report during the time of publication of this report, however, The authors and/or their wives/children of this document may own securities in funds open to the public that invest in the securities mentioned in this document as part of a diversified portfolio over which they have no discretion. This report has been produced independently and separately by the Research Division at Aljazira Capital and no party (in-house or outside) who might have interest whether direct or indirect have seen the contents of this report before its publishing, except for those whom corporate positions allow them to do so, and/or third-party persons/institutions who signed a non-disclosure agreement with Aljazira Capital. Funds managed by Aljazira Capital and its subsidiaries for third parties may own the securities that are the subject of this document. Aljazira Capital or its subsidiaries may own securities in one or more of the aforementioned companies, and/or indirectly through funds managed by third parties. The Investment Banking division of Aljazira Capital maybe in the process of soliciting or executing fee earning mandates for companies that is either the subject of this document or is mentioned in this document. One or more of Aljazira Capital board members or executive managers could be also a board member or member of the executive management at the company or companies mentioned in this report, or their associated companies. No part of this report may be reproduced whether inside or outside the Kingdom of Saudi Arabia without the written permission of Aljazira Capital. Persons who receive this report should make themselves aware, of and adhere to, any such restrictions. By accepting this report, the recipient agrees to be bound by the foregoing limitations.

Head of Research

Talha Nazar +966 11 [email protected]

AnalystSultan Al Kadi+966 11 [email protected]

Analyst

Jassim Al-Jubran +966 11 [email protected]

Analyst

Waleed Al-Jubayr+966 11 [email protected]

Analyst

Muhanad Al-Odan+966 11 [email protected]

General Manager – Brokerage Services

& sales

Alaa Al-Yousef+966 11 [email protected]

AGM-Head of international and institutional

brokerage

Luay Jawad Al-Motawa +966 11 [email protected]

AGM- Head of Western and Southern Region

Investment Centers

Mansour Hamad Al-Shuaibi +966 12 [email protected]

AGM-Head of Sales And Investment Centers

Central Region

Sultan Ibrahim AL-Mutawa +966 11 [email protected]

AGM-Head of Qassim & Eastern Province

Abdullah Al-Rahit +966 16 3617547 [email protected]

Aljazira Capital is a Saudi Investment Company licensed by the Capital Market Authority (CMA), license No. 07076-37

![BGD001B Retro Digital 100M-WR (Black & Pink) 12 EOR - Mist ... · Mist Digital 100M-WR [Nude & Rosegold] 222 EOR - - BG002A Diva Bronze 190 EOR - BG002B Diva Silver 133 EOR - BG003C](https://static.fdocuments.us/doc/165x107/5e7cf3eec367ea52344b7489/bgd001b-retro-digital-100m-wr-black-pink-12-eor-mist-mist-digital.jpg)